medium-term renewable energy market report 2014 · · 2015-10-272013 to 2020 strong momentum for...

TRANSCRIPT

© OECD/IEA 2014

2050 GW by 2050?An IEA Perspective

Dr. Paolo Frankl,

Head, Renewable Energy Division

International Energy Agency

WORLD HYDROPOWER CONGRESS, 19-21 May 2015, BEIJING

© OECD/IEA 2015

Power: a share reversal is needed to limit temperature increase to 2°C

Today: Fossils: 68%

Renewables: 20%

Global electricity generation by technology

2011 6DS 2DS hi-Ren

By 2050 Renewables: 65 to 80%

Fossils: 20% (and with CCS)

Sou

rce:

En

erg

yTe

chn

olo

gy

Per

spec

tive

s 2

01

4

© OECD/IEA 2015

Different optimal power mixes in different regions by 2050

Sou

rce:

En

erg

yTe

chn

olo

gy

Per

spec

tive

s 2

01

4

© OECD/IEA 2015

Vision for IEA Hydropower Roadmap

Hydropower generation will double by 2050 and reach 2 000 GW and 7 000 TWh, mostly from

large plants in emerging/developing economies© OECD/IEA 2012

China

India

AseanOther Asia Pacific

Africa M. East

OECD Europe

RussiaTransition eco.

Canada

Other LAM+Mex

Brazil

USA

Asia Pacific

Africa

Europe & Eurasia

Central & South America

North America

Middle East

16%

19%

17%

Share on total electricity generation

© OECD/IEA 2015

Renewable electricity projected to scale up by 45% from 2013 to 2020

Strong momentum for renewable electricity

Global renewable electricity production, historical and projected

0%

5%

10%

15%

20%

25%

30%

5001 0001 5002 0002 5003 0003 5004 0004 5005 0005 5006 0006 5007 0007 500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

TWh

Hydropower Bioenergy Onshore wind

Offshore wind Solar PV Geothermal

STE/CSP Ocean % total generation (right axis)

Historical data and estimates Forecast

Natural gas 2013

Nuclear 2013

© OECD/IEA 2015

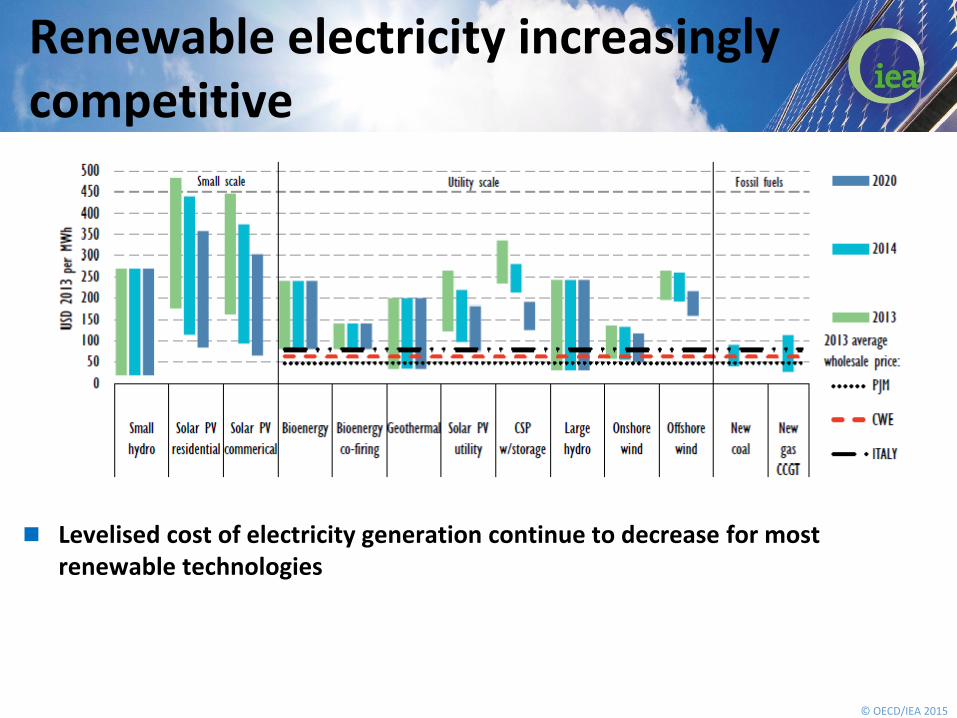

Renewable electricity increasingly competitive

Levelised cost of electricity generation continue to decrease for most renewable technologies

© OECD/IEA 2015

Growth in hydropower led by non-OECD countries

Hydropower capacity* expected to grow 225 GW by 2020 (+2.6% annual growth), lead by non-OECD countries (+203 GW)

China accounts for almost half of growth (+105 GW) driven by target (420 GW by 2020).

Non-OECD Americas and Asia should also contribute substantially by adding ~35-37 GW each by 2020

Hydropower generation* expected to reach 4670 TWh; China, alone accounts for 27%

Generation largely influenced by how China decides to use the pumped storage capacity planned to be installed by 2020.

*Includes pumped storage

Hydropower electricity generation (TWh)Hydropower capacity additions (GW)

© OECD/IEA 2015

Hydropower capacity additions declining

Annual solar PV and wind power capacity additions will increase – and more so in the enhanced case

Annual hydropower capacity additions decrease in the next five years

?

© OECD/IEA 2015

3) Increase flexibility of other power system

components

Grids Generation

Storage Demand Side

1) Foster System-friendly

RE

Increasing variable RE will require greater system flexibility

2) Better market design & operation

© OECD/IEA 2015

Drivers and Barriers for reaching 2TW

Affordability, security

Proven, reliable, local

Fostering social and economic development

Multipurpose water management

Irrigation, freshwater

Flood protection

Power generation

Navigation, recreation

Support for wind & PV

Arbitrage and services

Sustainability challenges

Safety, resettlement

Water quality, wildlife

Civil works, GHGs

Financing challenges

Large capital intensive projects, long lead times

YoY return variations

Long tenures

Flexibility under-valued

Power market design, the policy challenge