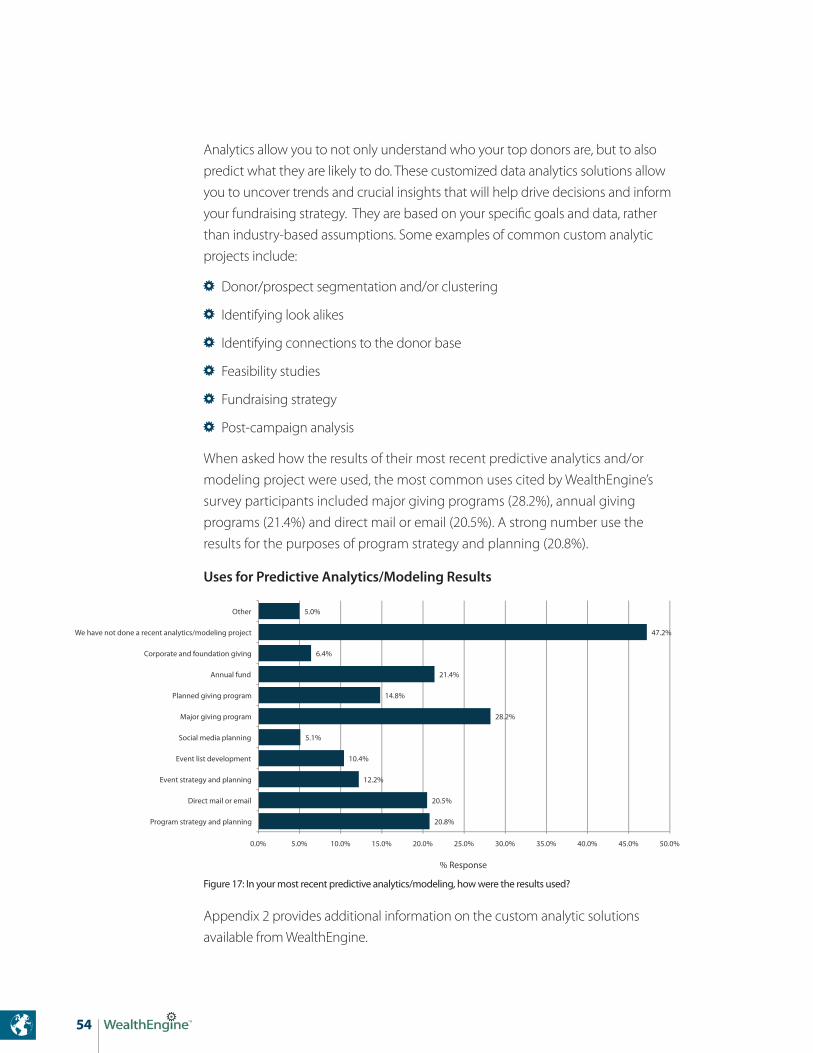

measuring fundraising return on investment and the …€¦ · measuring fundraising return on...

TRANSCRIPT

Principles of Fundraising Strategy for

Nonprofit Organizations

2013

White Paper

Measuring Fundraising Return on Investment and the Impact of Wealth Intelligence

About This PaperEvaluating Return on Investment (ROI) provides great advantage for moving a nonprofit organization’s fundraising office, management and the board forward in aligning the business of fundraising with their overall philanthropic mission. WealthEngine has written its second edition of Measuring Fundraising Return on Investment, to explore the various factors to consider when measuring the ROI of fundraising, including the ROI when systematically deploying wealth intelligence.

Since our first edition in 2010, there has been a shift in attitudes towards measuring and evaluating ROI, as donations by Americans to nonprofit groups mirror the slow recovery of the larger economy and organizations realize that investing in fundraising is likely to improve returns. In this paper, we include the findings from a WealthEngine survey on measuring ROI and business analytics, along with case studies, perspectives from industry leaders, and in-depth content on the non-financial measurements of return.

WealthEngine Publications Team: Special Thanks to:

©2013 WealthEngineTM, Inc. All Rights Reserved.

Reproduction and distribution of this publication in any form without prior written permission is forbidden. The information

contained herein has been obtained from sources believed to be reliable. This document is informational in nature and we do not

guarantee any of the information either expressed or implied. Readers are encouraged to consult with their appropriate legal,

accounting and professional counsel before implementing any suggested actions. WealthEngine has no liability for errors, omissions

or inadequacies in the information contained herein or for interpretations thereof and shall not be held liable for any claims or

losses that may rise from the implementation of the best practices in this report. This document includes ideas for enhancing

WealthEngine’s products. These ideas are subject to change at any time.

Tony Glowacki, President and Chief Executive Officer

Shane Bair, Creative Director

Sally Boucher, Director of Research, WealthEngine Institute

Lili Mehta, Senior Consultant, Marketing & Special Projects

Kimberly O’Donnell, Chief Marketing Officer

Wendy Tanner, Marketing Communications Specialist

Norman Olshansky, Fundraising Consultant and President of NFP Consulting Resources

Rick Dunham, President & CEO of Dunham+Company

Carrie Collins, Vice President of Institutional Advancement at University of the Sciences, Philadelphia PA

Mark Koenig, Senior Director for Advancement Services at Oregon State University Foundation

David Ferguson, Executive Director at Maryland Republican Party (Maryland GOP)

Measuring Fundraising Return on Investment 1Measuring Fundraising Return on Investment 1

ContentsOverview 2The Fundraising Landscape 6Measuring Return on Investment 14

Calculating Net Revenues 17Other Important Measurements of Success 18Measuring Success 20The Cost-Benefit Analysis 22

Assessing Development Expenses: The Development Office 26Organization Structure and Costs 27Development Staff Expenses 28Other Direct Expenses 29Wearing Multiple Hats 30

Investing in Fundraising 32Controlling Costs and Maximizing Contributions: Striking a Balance 36

The Challenges of Accounting for Overhead Expenses 38The Impact of Donor Cultivation 39Special Considerations for Planned Giving 41

The Tie to the Marketing Office 42The Impact of Social Media 45Measuring ROI of Social Efforts 47

The Impact of Wealth Intelligence on Fundraising Return on Investment 48Uses of Wealth Intelligence for Successful Fundraising and Beyond 51Investing in Wealth Intelligence 52The Role of Predictive Analytics 53Measuring the Return of Your Wealth Intelligence Investment 55

Other Factors Affecting Return on Investment Metrics 58Factors to Consider when Evaluating Your ROI and CRD 61

Conclusion and Next Steps 62Case Studies 66Appendix 1: Worksheets 80Appendix 2: WealthEngine Custom Analytics 88Appendix 3: ROI Measurements: Results from the WealthEngine 2013 Surveys 90

White Paper For Nonprofit Organizations

2

Overview

Measuring Fundraising Return on Investment 3

Understanding Return on Investment (ROI) is critical to a nonprofit organization’s long term strategic planning – regardless of their size, age, mission or the constituents they serve. With today’s tight economy, nonprofits face increased pressure to improve every facet of their fundraising operation in terms of productivity, efficiency and value, and organizations must be cognizant of the relationship between their investment in fundraising and the return on that investment.

Having a command of ROI-related metrics helps to inform decision-making and foster a strategic approach to development planning, budgeting, staffing and other key operational areas. For example, tracking, measuring and reporting the results of various fundraising programs and activities is critical for internal staff, organizational leadership and external stakeholders, such as donors and community members. This includes cost-related metrics such as ROI and Cost to Raise a Dollar (CRD), as well as key performance metrics across prospecting, new donors, renewals and repeat donors. In addition to measuring the results of individual fundraising activi-ties, and then comparing the effectiveness and ROI of each activity against other activities, it is important to analyze the success of each fundraising activity against its initial goals by doing a cost-benefit analysis. Looking at this data over a number of years allows the nonprofit organization to establish its own benchmarks, uncover trends, and determine if they are progressing in the right direction.

Wealth intelligence is an important component within the fundraising operations for organizations of all sizes and types. By combining the use of wealth, lifestyle and biographical research data with advanced analytics, wealth intelligence provides the foundation for targeted and successful identification, cultivation, solicitation, and stewardship strategies. When performed effectively and supported by a develop-ment and marketing office that implements targeted fundraising programs, wealth intelligence can have a significant impact on fundraising ROI. It enables organiza-tions to save time and money by identifying and focusing on their best prospects, and to raise more money in the long run.

4

Measuring ROI can help nonprofits justify their investments in staffing, research and wealth intelligence. And perhaps even more importantly, it can help maximize the efficiency of these efforts by providing the benchmark for understanding the overall cost of raising money for their organization.

As development offices, board members, donors and volunteers all look to have greater transparency into the costs and outcomes of fundraising, ROI metrics provide an important indication of the overall effectiveness of the organization’s fundraising efforts. ROI, CRD and other performance measures allow them to determine what mix of fundraising investments, done at this stage in their fund-raising strategy, gives the organization the best return over time. This information is especially important to board members, CFOs and others who have a say in how the fundraising budget is set. It also allows the nonprofit to potentially increase their wealth intelligence and analytics budget by providing the proof positive that wealth intelligence is an investment that yields positive results.

At the end of the day, it’s about striking a balance between efficiency and effect-iveness. ROI metrics may vary depending on the organization’s efforts towards achieving maximum net revenues, or effectiveness, versus maximum efficiency, or keeping fundraising expenses as low as possible.

This white paper will explore various factors to consider when measuring the ROI of fundraising for the nonprofit organization, including the ROI when systematically deploying wealth intelligence. As part of the discussion of ROI, and the benefits and costs of wealth intelligence in increasing returns while lowering the cost of a dollar raised, we present several WealthEngine client case studies. These real-world examples demonstrate the use of wealth intelligence and custom analytics and its ROI in the context of various fundraising campaigns.

“In today’s tough economy, there is a trend towards building fundraising strategies in a highly disciplined and cost-conscious manner, and as a result, fundraising is becoming more of a science. While there is still an art to it, the science is playing a bigger role.”

- Norman Olshansky Fundraising Consultant and President of NFP Consulting Resources

Measuring Fundraising Return on Investment 5

White Paper For Nonprofit Organizations

6

The Fundraising Landscape

Measuring Fundraising Return on Investment 7

The Fundraising LandscapeThe nonprofit sector represents a significant part of the overall U.S. economy, growing steadily over the past decade and increasing in size by 25%, from 1,259,764 million nonprofits in 2001 to 1,574,674 million nonprofits in 2011, according to the Urban Institute. Indeed, the growth rate of the nonprofit sector has surpassed the rate of both the business and government sectors. Nonprofit organizations represent a significant portion of the U.S. workforce (5.4% of the gross domestic product (GDP) and 9% of all wages/salaries paid1). The nonprofit sector contributed $779 billion to the U.S. economy in 2010, and public charities, the largest component of the nonprofit sector, reported more than $1.51 trillion in revenue, $1.45 trillion in expenses, and $2.71 trillion in assets.

Charitable organizations have four primary sources of revenue:

T Private payments, such as education tuition, fees for medical care or fees for other goods and services

T Private charitable contributions – including those from individuals (outright and deferred, such as planned gifts), corporations, foundations and bequests

T Government grants and payments

T Income from investments

The percentage of revenue from each source varies widely across various sectors, with education, healthcare (including hospitals) and human services related charities relying more heavily on private payments. Healthcare and human services related charities generally receive higher percentages of their revenue from government grants, while educational institutions have greater investment income – driven largely by the higher education endowments.

2012 Contributions by Source

Individuals

Corporations

Foundations

Bequests72%

15%

6%

7%

Figure 1: 2012 Contributions by Source (by percentage of the total). Total 2012 conributions: $316.23 billion.

1 The Nonprofit Sector in Brief: Public Charities, Giving and Volunteering, The Urban Institute, 2012

8

In 2012, private charitable contributions in the U.S., which include giving to public charities and religious congregations, totaled $316.23 billion. The single largest influence on this increase was from an $8.67 billion increase in gifts made by individuals, over 20112.

In terms of charitable contributions, individual giving far exceeds foundation giving. According to Giving USA 2013, and illustrated in Figure 1, individual giving represents nearly three quarters of charitable giving in the United States3. Individuals donated $228.9 billion in 2012, a 3.9% increase from $220.3 billion in 2011. If you include bequests, which are also contributions from individuals, that total rises to 79%. While some organizations depend largely on government grants, and others get much of their funding from corporate sponsorships or foundation grants, the vast majority of nonprofit organizations depend on individual giving to fulfill their missions. As discussed in this paper, many industry experts have voiced the opinion that if individual giving could be increased by only a few percentage points, the impact would be tremendous.

The report shows that donations by Americans to nonprofit groups are mirroring the slow recovery of the larger economy. However, their findings indicated that if charitable giving continues to grow at its recent rates, it will take about another six or seven years to return to pre-recession levels. Overall donations are still down about 8% from their 2007 peak of $344.5 billion.

In a study published in April 2013 by the Nonprofit Research Collaborative (NRC)4, 58% of organizations saw fundraising receipts increase in 2012. This is up from 53% in 2011 and 43% in 2010. And, 63%, met their fundraising goal in 2012. This is up from 59% in 2011 and 52% in 2010.

This survey was completed by over 1,200 respondents from large and small organizations (by budget size) and organizations from every sub-sector, from Arts, Culture & Humanities to Religion, and included organizations in the U.S. and Canada. The survey questions ranged from changes in charitable receipt amounts in 2012 compared with 2011 to expectations for 2013.

2 2013 Giving USA Highlights: An Overview of Giving in 2012. The Giving Institute. 3 2013 Giving USA Highlights: An Overview of Giving in 2012. The Giving Institute. 4 Nonprofit Fundraising Study: Covering Charitable Receipts at U.S. and Canadian Nonprofit Organizations in 2012, Nonprofit Research Collaborative, April 2013. (http://www.urban.org/UploadedPDF/412836-nonprofit-research- collaborative.pdf )

Measuring Fundraising Return on Investment 9

Change in Charitable Receipts

42%

Decreased over the prior year

About the same

Increased over the prior year 58%

16%

26%

Figure 2: Percentage of responding organizations reporting change in charitable receipts, 2012 compared with 2011

Many of today’s donors are concerned about the sluggish economy, federal furloughs and sequesters and the fiscal cliff. With potential cuts to federal spending, and looming changes to the tax code, donors are more careful of their spending. Meanwhile, changing technology and fundraising practices provide new challenges and opportunities to reaching supporters and cultivating donors. A 2012 Dunham+Company State of Philanthropy Study showed that while Americans feel the economy is improving, donors anticipate that their giving in 2013 will revert to recession-like levels, with 27% of adults—the same percentage as 2009 and 2010 and more than double the percentage in 2012—saying they will give less in the coming year. In essence, when the economy appears unstable or uncertain, charitable giving is at risk5.

Industry leaders have long held the stance that those organizations that invest in fundraising are likely to see the benefit. In fact, some fundraising veterans claim that we’d see far greater impact by investing in individual giving than by directly supporting programs. Individual giving far exceeds foundation giving, as demonstrated above. While presenting at a Council on Foundations conference, Dan Pallota, activist and fundraiser, asserted that stronger fundraising would generate more than enough new dollars from individual donors to off-set whatever foundation dollars weren’t spent directly on programs6. The sentiment

5 Dunham and Company Annual State of Philanthropy Study, January 2013. (http://dunhamandcompany.com/down loads/DC_StateOfPhilanthropyStudy_PresentationDeck20130123.pdf ) 6 Doughty, Roger. The Multiplier Effect: Invest in Fundraising, Philanthropy411 blog, April 11, 2011. (http://philanthro py411.wordpress.com/2011/04/11/multiplier/)

10

is that philanthropy’s more important job is to figure out how to have the greatest impact with those resources available, and how to use those resources to fuel further growth of the organization. The greater the growth, the greater the funds raised, and thus the greater impact that can be made in serving the mission.

Those who continue to invest in fundraising and growing individual gifts are better positioned than those who maintain status quo. And important to investing in fundraising programs – including major gifts, planned giving and annual giving – is understanding the overall revenue and expense associated with the program or activity. This allows you to calculate your fundraising return on investment (ROI) and cost to raise a dollar (CRD). When you can demonstrate the impact that contributions have on your organization – and the fact that every dollar is making a difference – donors are more likely to donate again and again. ROI becomes a valuable tool for nonprofits to demonstrate the value of their organization.

As Norman Olshansky, Fundraising Consultant and President of NFP Consulting Resources explained in an exclusive interview with WealthEngine, “We need to move away from measuring outputs and begin to look at measuring outcomes. Outcomes are inherently harder to measure. You have to look at evidence-based practices.” This is critical to building a philanthropy-focused organization.

“When talking to your stakeholders, if you need to have a story to tell, tell about your accomplishments. Talk about both your points of pride and your challenges. Major donors give not just to solve your problems, but to be part of your success.”

- Norman Olshansky Fundraising Consultant and President of NFP Consulting Resources

Measuring Fundraising Return on Investment 11

A Fresh Perspective: Changing the Way We Think About Changing the World7

Dan Pallota, author, speaker and founder and Chief Humanity Officer of Advertising for Humanity as well as founder and President of the Charity Defense Council, has led the movement dedicated to transforming the way the donating public thinks about charity and change. In his acclaimed 2013 TED talk, he talks about the need to change the way we think about changing the world. The precept is that social problems are massive, yet social organizations are tiny in scale, and we have a belief system that keeps them tiny. He argues that the rules for the nonprofit sector and the rules for the rest of the world should not be different.

By following some of the same rules that the commercial world goes by, nonprofits – and their causes – will be better off. But the main thing getting in the way of nonprofits doing this is the discrimination nonprofits face:

T Donors are obsessed with low overhead, so it makes organizations obsessed with overhead as well. What is needed is an understanding that development work costs money; you need to have proper support structures (administrative, financial, logistical, security, procurement, etc.) in order to function properly and effectively. This obsession with low overhead makes NGOs cut down on the essentials, which ultimately results in staff burnout, ineffective implementation, and other negative consequences.

T There is a misconception that doing good cannot be synonymous with doing well financially. Nonprofit CEO’s are paid dramatically lower than their counter-parts in commercial organizations, when in reality the impact they can have on society (and the economy) may be just as great or even greater.

T Commercial organizations are rarely, if ever, scrutinized for spending on adver-tising and marketing. Nonprofits, on the other hand, are often criticized if they overspend in this area. Donors don’t like the idea of an organization spending on advertising because it is thought of as overhead, even if it is effective.

T Charitable giving is stuck at 2% of GDP since the 1970’s, and in 40 years has not been able to wrestle market share away from the for-profit sector. Unless there is some change to shake things up, this is likely not going to change soon. But today, it’s nearly impossible for charitable giving to take on more market share because it is not allowed to market.

7 Pallotta, Dan. The way we think about charity is dead wrong, TED, March 2013. (http://www.ted.com/talks/dan_pal lotta_the_way_we_think_about_charity_is_dead_wrong.html)

12

T There is reluctance to taking risks on new revenue ideas. Why? Because if it doesn’t produce results, your character falls into question. There is a fear of failure among nonprofits, and a fear of ruining their reputations. This fear is killing their ability to innovate. And without innovation, the nonprofit cannot grow and cannot solve the problems that their mission seeks to address.

T There is also a different set of expectations for nonprofits. One example Pallotta cites is Amazon. It took Amazon 6 years to become profitable, because they had to invest in scaling their business. If a nonprofit took six years to start supporting their constituents because they were focusing on scaling their business, it wouldn’t be considered acceptable.

T Nonprofits cannot use their profit to attract risk capital. The for-profit sector has a lock on the capital markets, and as a result nonprofits are starved for growth, risk and idea capital. They cannot use money to lure talent, task risks, advertise, or fund their growth.

Percentage Allocated Towards Fundraising vs Cause

Cause

Fundraising

Figure 3: Percentage that is allocated towards fundraising is minor compared to what goes towards the cause

There is a misconception that overhead is not part of the cause, when in fact it is. This thinking forces charities to forgo what they need in order to grow, because they feel pressured to keep overhead low. As a result, the percentage that is allocated towards fundraising is minor compared to what goes towards the cause.

Measuring Fundraising Return on Investment 13

In the end, it’s about making the pie bigger. In his ‘Bake Sale’ example, Pallotta sites how a bake sale fundraiser with 5% overhead is considered “morally superior” to the professional fundraiser with 40% overhead. But if you increase the investment in the organization – in staffing, fundraising, customer service, operations, etc., the overall revenue is much higher despite the fact that the percentage of overhead is greater.

Investment in Organization vs Overall Revenue

5%

$71.00

40%

$71,000,000.00

Bake Sale Enterprise

Figure 4: Investment in the organization vs overall revenue

Therefore, you need to invest more in fundraising because fundraising has or does the one thing you need in order to invest in the mission.

According to Pallota is that if we could move charitable giving from 2% to 3% of GPD by investing in that growth, that would give us an extra $150 billion a year in contributions just for health and human services organizations alone – three times the dollar amount they raise today.

In the end, donors, constituents and other stakeholders shouldn’t care about the rate of overhead, they should care about the scale of the organization’s dreams, because this is how the underlying human and social problems will get solved!

White Paper For Nonprofit Organizations

14

Measuring Return on Investment

Measuring Fundraising Return on Investment 15

Measuring Return on InvestmentIn a 2013 survey by WealthEngine to assess the state of fundraising effectiveness and business analytics, 79.3% of respondents said that measuring ROI is either somewhat or very important for their organization.

Importance of Measuring Fundraising Return on Investment by Organization

4% 8%

31%

48%

9%

Not at all important

Somewhat unimportant

Somewhat important

Very important

Don’t Know/Not Sure

Figure 5: How important is measuring fundraising Return on Investment (ROI) for your organization?

WealthEngine’s survey included over 1,126 respondents over a range of organization types and sizes, with the primary types being Education (31%), Social & Human Services (18%), Healthcare/Hospitals (14%) and Art / Culture / Museum (11%). Of all respondents, 40% have a budget of $600,000 to $5,000,000.

Survey Participants by Organization Type

2.8% 8.3%

2.1% 3.9%

31.1% 3.5%

0.6% 9.4%

4.1% 1.5%

4.2% 15.6%

1.4% 0.5% 0.6% 0.5%

9.9%

Advocacy Arts - Culture

Arts - Museums Community Organization

Education Environment

Fraternal Organization Healthcare

Hospital International and Foreign A airs

Religious Organization Social/Human Services

Grant-making Organization Consulting and/or Business Services

Political Organization Professional Services

Other

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0%

Figure 6: Survey Participants by Organization Type

What’s New in FindWealth 8

T Advanced Search Functionality

T Enhanced Ratings & Scores

T Valuable Alert Features

T Intuitive & Easy to Use

T Fast, Accurate Results

16

Survey Participants by Contribution Size

19% 4%

40%

20%

17%

Under $600k

$600K to under $5MM

$5MM to under $25MM

$25MM and over

Don't know/Not sure

Figure 7: What is your organization’s level of annual contributions from all sources?

So how does the fundraising office begin to determine which information is relevant when tracking and reporting on their ROI? It begins with understanding the ROI of your staff and frontline fundraisers, and includes the ROI of programmatic activities. There are two key cost-related metrics to assess return on investment (ROI). The most common, ROI, is the net revenues generated from fundraising, divided by the total investment in fundraising, or fundraising expense. Another metric is Cost to Raise a Dollar (CRD), which is the inverse of ROI and a figure that many nonprofits believe is equally important. In looking at these figures, organizations can better understand the value of their fundraising activities and determine how the costs to carry out one activity compare to the costs to carry out another activity.

Return on Investment (ROI) =

Cost to Raise a Dollar (CRD) = $+-Expense of Investment

Net Revenue

Net Revenue

Expense of Investment

Who Wants to Know About ROI?

WealthEngine research shows that calculating and under-standing ROI is important not only for the develop-ment office, but is a topic of increasing interest among organization executives (CEO, CFO), the board and/or trust-ees, donors and volunteers. Transparency is critical to the cost side of the equation while return serves as a per-formance measuring stick.

Measuring ROI is important, and it is a long term process. It is the foundation for maximizing the efficiency and effectiveness of your fundraising operations.

Measuring Fundraising Return on Investment 17

Groups/Individuals Interested in Measuring Return on Investment%

Res

pons

e

68.0%

59.6%

68.3%

54.0%

25.9%

10.3% 4.9% 5.2%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Board and/o

r Tru

stees

Development

execu

tives

Organiza

tion Execs

execu

tives (

CEO, CFO,

etc.)

Development Sta�

Donors

Volunteers

None

Other

Figure 8: Which groups/individuals are interested in measuring Return on Investment?

Calculating Net RevenuesNet Revenue is simply the sum of cash gifts and commitments, minus the amount spent on fundraising. For gift commitments and the various types of deferred gifts, organizations may use different methodologies to account for gift expectancies. One useful example is the Guidelines for Counting Charitable Gifts developed by the Partnership for Philanthropic Planning (formerly NCPG). These guidelines recommend that organizations set three separate and complementary goals, and report on their fundraising results separately, for (1) gifts received during the campaign period, (2) irrevocable deferred gifts and (3) revocable gifts. It offers a paradigm for structuring and measuring results of both annual and multi-year campaigns, and for counting and reporting gifts within those campaigns.

Utilizing these guidelines and measuring ROI separately for the three different types of gifts enables organizations to differentiate between new commitments and commitments from previous campaigns that have changed in character. This puts organizations in a position to show how different development activities can affect the financial state (both present and future) of the institution without appearing to count the same gift twice. This is especially important in the case of deferred gifts, where it may be years before a gift commitment is fully realized.

18

Other Important Measurements of SuccessTracking, measuring and reporting the results of various fundraising programs and activities is critical for internal staff, organizational leadership and external stakeholders, such as donors and community members. It allows internal teams to determine what is working, what needs adjusting, and to determine how changes in strategy or direction can impact the efforts of other internal and external stakeholders. This makes it easier to make course corrections in a timely manner so that the organization can maximize its fundraising success.

WealthEngine outlines this step in detail in our 2012 publication, Growing Individual Gifts, which provides important insight on data understanding, analysis, forecasting and strategy development for fundraisers. As explained in the workbook, having these metrics is important not only for fundraising leadership, but for staff as well. Staff should have easy access to all data that pertains to their areas of responsibility.

In WealthEngine’s 2013 survey, we asked participants which metrics they use to determine fundraising return. The responses varied, with the top four metrics, other than CRD and ROI, being:

T Measure the increase/decrease in number of gifts (51%)

T Measure the number of new and recaptured donors (47.7%)

T Measure the increase/decrease in average size of gifts (45.4%)

T Measure the number of gifts renewed or maintained (44.7%)

33.8%

48.4%

20.3%

16.3%

23.0%

8.2%

51.0%

45.4%

47.7%

44.7%

32.4%

18.8%

8.4%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Calculate the Return on Investment

Calculate the Cost to Raise a Dollar

Measure the number of prospects per major gift secured

Measure the number of contacts per prospect to secure a gift

Measure the increase/decrease in size of prospect pool

Measure the increase/decrease in average cultivation time

Measure the increase/decrease in number of gifts

Measure the increase/decrease in average size of gifts

Measure the number of new and recaptured donors

Measure the number of gifts renewed or maintained

Measure the number of gifts upgraded or downgraded

None

Other

% Response

ROI M

easu

rem

ents

How Do You Measure Success and Return on Investment?

Figure 9: How do you measure success and return on investment?

Measuring Fundraising Return on Investment 19

Major DonorAny donor who gives a gift at your major gift level or above, typically the top 1% to 5% of gift levels to your organization

New Donor*

A donor who gives in the current year but has never given previously

Lapsed DonorA donor who has given in a prior year, but not in the current year

Recaptured DonorA previously lapsed donor who gives again in the current year

New Donor RenewalAny new or recaptured donor who gave in the last year, but not the previous year, who gives again in the current year

Repeat Donor RenewalAny donor who gives in the current year and has also given at least in the two previous years

Upgrade DonorAny donor who gives more in the current year than in the previous year

Regrade DonorAny donor who gives the same amount in the current year as in the previous year

Downgrade DonorAny donor who gives less in the current year than in the previous year

MetricA measurement used to gauge some quantifiable component of an organization’s performance

BenchmarkA point of reference for assessing perfor-mance that could be based on industry standards, the performance of peer organizations or your organization’s historical performance

Useful Definitions:

* These definitions are consistent with definitions used in the AFP/Urban Institute research study: 2011 Fundraising Effectiveness Survey Report (FEP).

20

Measuring SuccessThe key performance metrics that the fundraising office should track, measure and report on are provided in Table 1. It is important to track these metrics for each key fundraising activity or program, and assess by:

T Comparing the effectiveness and ROI of each activity against the initial goals

T Comparing the effectiveness and ROI of each activity against other activities

T Comparing the effectiveness and ROI of each activity over a three or even five-year timeframe to determine year over year changes and trends.

These measurements allow fundraising management and leadership to identify areas of maximum impact, inform the fundraising strategy, forecast revenue and expenses, and better focus their fundraising efforts on those that yield maximum return.

All of these metrics, taken individually and combined, can help the organization better understand what is working, and what needs adjusting, and to determine how changes in strategy or direction can impact overall results. This makes it easier to make course corrections in a timely manner so that the organization can maximize its fundraising success.

As Olshansky states, “There is a cost to start and a cost to sustain. An initial invest-ment may not pay off for a few years. It’s important to look at trends over a number of years (3-5) and determine if you are progressing in the right direction.”

Measuring ROI and CRD enable the nonprofit to determine what mix of fundraising investments, done at this stage in their fund-raising strategy, gives the organization the best return over time.

Measuring Fundraising Return on Investment 21

Fundraising Key Performance Metrics

Prospecting Year 1 Year 2 Year 3

Number of Prospects Under Management*

Increase/decrease in Size of Prospect Pool

Average Time (months)

Discovery to Cultivation (Months)

Cultivation to Solicitation (Months)

Solicitation to Stewardship (Months)

New and Recaptured Donors Year 1 Year 2 Year 3

Number of New and Recaptured Donors

Number of Prospects Solicited

Dollars Raised from New and Recaptured Donors

Average Gift Size from New and Recaptured Donors

New Donor Renewals (renewing after first gift) Year 1 Year 2 Year 3

Number of New Donor Renewals

Percent of New Donor Renewals

Number of First Time Donors Solicited

Dollars Raised from First Time Donors

Average Gift Size from First Time Donors

Repeat Donors Year 1 Year 2 Year 3

Number of Repeat Donors

Percent of Repeat Donors

Number of Repeat Donors Solicited

Dollars Raised from Repeat Donors

Average Gift Size from Repeat Donors

Upgraded/Regraded/Downgraded Donors Year 1 Year 2 Year 3

Number of Donors Upgrading Gifts

Percent of Donors Upgrading Gifts

Dollars Raised from Upgraded Donors

Average Gift Size from Upgraded Donors

Number of Donors Maintaining Gifts (Regraded)

Percent of Donors Maintaining Gifts (Regraded)

Number of Donors Downgrading Gifts

Percent of Donors Downgrading Gifts

Table 1: Fundraising Key Performance Metrics

* Additional tracking and analysis of prospects under management within each stage of the fundraising lifecycle should be done, as further explained in the Growing Individual Gifts workbook.

22

The Cost-Benefit AnalysisIn addition to measuring the results of individual fundraising activities and then comparing the effectiveness and ROI of each activity against other activities, it is important to analyze the success of each fundraising activity against its initial goals by doing a Cost-Benefit Analysis. For each activity, a quantifiable goal should be established during the planning stage, when the organization is forecasting its fundraising potential and creating a development plan to achieve that potential. For each goal, it is important to measure the costs of implementing the strategies used to achieve the goal, the benefit or payoff from implementation, and the return on investment for each. An example of such a Cost-Benefit analysis, using data provided in the examples used in the Growing Individual Gifts workbook is provided in Table 2.

Sample Cost-Benefit Analysis

Goals Strategies Cost Benefit Return on Investment ROI

Goal: Maximize Individual Giving

Increase number of major gifts closed by 18% from 51 to 60 and Increase major gift average gift size by 20%

•Purchase data and analytics to determine best prospects to cultivate ($25K)

• Invest in training for major gift staff and volunteers ($20K)

•Begin implementing prospect management and major gift metrics ($10K add’l salary)

$55,000 $182,584 232%

Grow event participation by 15%

• Invite high potential prospects •Leverage board relationships disclosed in

data purchase•Promote event via social media

$1,000 $3,577 257%

Prepare report for board with recom-mendations for Planned Giving Program for September meeting

•Research, interview and prepare report of findings and recommendations for board

N/A N/A N/A

Increase renewal rate among first-time donors by 5% to 15%

• Invest in welcome communications with first-time donors

•Segment donors for most cost-effective approach

$4,000 $12,830 221%

Measuring Fundraising Return on Investment 23

Sample Cost-Benefit Analysis (Continued)

Goals Strategies Cost Benefit Return on Investment ROI

Goal: Increase Donor Loyalty

Increase annual fund upgrades by 5%

•Segment population for customized approaches

•Apply consistent, customized formulas to drive upgraded donations

$500 $10,389 1977%

Increase volunteer participation in fundraising by 10%

•Develop individualized communications plan for volunteers

• Institute volunteer recognition event

$1,000 $2,492 149%

Grow social media communities by 30%

• Institute email campaigns to add community members

•Create and post interesting content and conversations

N/A N/A N/A

Goal: Improve Fundraising Efficiency

Reduce costs by 20% •Purchase email overlay for donors and prospects for whom we don’t already have email addresses

• Institute regular email communications for all viable donors and prospects

•Segment constituents to exclude mailings to least likely to respond

$1,250 Est. Savings: $ -6,200

$4,605 268%

Table 2: Fundraising Operations and Program Expenses

Appendix 1 provides additional sample worksheets for measuring fundraising return on investment, as well as worksheets for measuring the return from wealth intelligence. These include:

T Appendix 1.1: Fundraising ROI: Development Audit Worksheet

T Appendix 1.2: Tracking and ROI of Gift Activity, and the Impact of Wealth Intelligence

T Appendix 1.3: Tracking and ROI of Fundraising, and the Impact of Wealth Intelligence

T Appendix 1.4: ROI for Fundraising Operations

T Appendix 1.5: ROI of Frontline Fundraisers

24

The sample worksheets for tracking fundraising results, including tracking of cultivation efforts, are useful to evaluate the success of an organization’s research and screening efforts and determine how the investment in wealth intelligence and prospect research has impacted the organization’s fundraising programs. The example provided in Appendix 1.3 for Major Gifts can be used as a template for evaluating the results of any type of giving campaign. Depending on the components of your fundraising program, you may want to measure your results in planned giving, annual fund leadership solicitations and other fundraising activities.

The template for calculating ROI for Fundraising Operations includes the expenses and revenues for the overall fundraising effort as well as specifically for major gifts, annual giving, planned giving and corporate and foundation gifts.

The sample worksheets in Appendix 1.5 for tracking the ROI for the frontline fundraising team have been provided by Carrie Collins, Vice President of Institutional Advancement at University of Sciences in Philadelphia. These worksheets can help you capture key performance-related metrics for gift officers as well as the associated costs of staffing and employment. By determining the ROI of the frontline fundraising team – through examining the ratio of dollars raised against the cost of employment – senior management can demonstrate to their executives and board members that frontline fundraisers are closing gifts in amounts larger than it costs to employ them, lending credence to the adage that you have to spend money to make money.

Measuring Fundraising Return on Investment 25

White Paper For Nonprofit Organizations

26

Assessing Development Expenses: The Development Office

Measuring Fundraising Return on Investment 27

Organization Structure and CostsTo accurately assess the expenses or costs associated with fundraising, it is important to measure these aspects of fundraising: staff and human resource costs, overhead costs and direct expenses.

In the first edition of WealthEngine’s ROI white paper, we noted that the size of a nonprofit’s development organization – and the cost required to operate it – depends on a number of factors, including the size of the overall organization, the scope of its fundraising initiatives and its overall budget. “We think of non-profits as education, healthcare, large charities and advocacy organizations, but it’s a lot more than that. We cannot forget about the associations, the government organizations. And size is important too – the metrics that a large organization can expect, who has the benefit of economies of scale, are dramatically different than what a small organization may experience,” explains Olshansky.

Nonprofit organizations should take into account several realities of fundraising when setting fundraising targets and staffing to meet them. North Carolina State University has developed Relationship Management Best Practices that offer a more formalized, structured system for major gift prospect portfolio management to ensure their fundraising activity is aligned with fundraising goals. These guidelines include:

T Major gift officers (MGO’s) identify, qualify, cultivate, and solicit major gifts of $25,000 and higher by matching donors’ philanthropic interests with needs of the university

T MGO’s average 18-24 asks of $25,000 and up per year

T MGO’s carry a major gift prospect portfolio of 120-150 major gift prospects in active solicitation cycle (those not in perpetual stewardship)

T MGO’s maintain 20-30 top prospects who will move through the solicitation cycle in 12-18 months

T MGO’s maintain 20-30 emerging prospects whose proposal is not yet in negotiation and cultivate them to become top prospects within12-18 months.8

Industry benchmarks show that organizations typically receive 75-85% of their “ask” and, contrary to the standard 80/20 rule, roughly 90% of campaign gifts come from 10% of donors.

8 NC State University, Relationship Management Best Practice, February 2009. (http://www.ncsu.edu/advancement- services/prospectmgmt/2-4-09%20NC%20States%20Relationship%20Management%20Best%20Practi.pdf )

28

When planning staffing for fundraising campaigns, most nonprofit organizations take into account the number of prospects a development officer can reasonably manage. Most consultants and industry veterans recommend a prospect portfolio of between 75 and 150 prospects per major gift officer – depending on the ask amount, geography, other job responsibilities and the major gift officer’s (MGO) skill and experience level.

As prospects make gifts or choose not to, the MGO’s portfolio must be resup-plied from a pool of new prospects, a responsibility typically managed through the prospect research function. Prospect researchers evaluate the overall pool of prospective donors and pass those that meet appropriate criteria to the MGOs for cultivation. A ratio of 4-5 MGO’s per prospect researcher is considered by many to be appropriate. However, depending on the organization’s fundraising goals, the research tools available to the research staff and level of screening efficiency, higher or lower ratios may be workable.

Development Staff ExpensesHuman resource costs such as salaries, benefits and travel expenses, are generally the largest portion of the fundraising or development budget. The Association of Fundraising Professionals (AFP) publishes an annual comprehensive salary survey, which is intended to capture overall salary and benefits data, including health/medical, retirement and general perquisites or “perks” for U.S. and Canadian non-profits. Their 2012 findings show that the mean (average) salary for all respondents is $75,595. The median (middle value) salary is $66,000. The top 25 percent of respondent fundraisers earn more than $90,000, and the bottom 25 percent earns $50,000 or less9. These figures demonstrate a 6% increase in the mean and a 4% increase in the median salary since 2009, which is consistent with the 5.8% increase in U.S. cost of living between 2009 and 201210.

Factors that influence salary levels include, but are not limited to, years of experience, education, CFRE-certification and location. Fundraisers working in national and international organizations reported average salaries higher than those affiliated with local or state/regional entities. There were also strong positive correlations between average compensation and the size of an organization’s staff, its budget, and the amount of funds raised11.

When calculating the cost of employment, it is important to include the gross salary, plus fringe benefits. Carrie Collins of University of the Sciences suggests a

Determining the appropriate staffing level ultimately depends on a number of factors, including:

T The nonprofit organiza-tion’s overall fundraising goal

T The amount desired from each type of fundraising effort or program

T The desired number of donors at each giving level

T The timeline to achieve the goal

9 2012 AFP Compensation and Benefits Report, Association of Fundraising Professionals, 2012.10 Social Security Administration, History of Cost of Living Adjustments. (http://www.ssa.gov/cola/automatic-cola.htm)11 2012 AFP Compensation and Benefits Report, Association of Fundraising Professionals, 2012.

Measuring Fundraising Return on Investment 29

guideline of 33% for fringe benefits, plus an additional $15,000 per person in travel and hospitality expenses. As Collins points out “Not including these figures in your calculations, you are underestimating how much money your institution is spending to ensure that your frontline fundraisers are, in fact, on the front lines.”

Other Direct ExpensesIn addition to the staffing component, organizations also incur a variety of direct expenses to support their development efforts. These can include accounting and budgeting software, donor management systems and other fundraising software, including research and analytical tools and prospect screening. It is important to account for and accurately attribute these expenses, as well as other direct expenses incurred for proposal generation, special events, direct mail and other campaign-related costs. In many cases, reasonable approximations and/or percentage allocations will suffice. Table 3 provides a summary of some of the typical categories of expenses incurred by development departments. This information can be generated to calculate return on investment, as well as cost per dollar raised, for individual fundraising programs as well as for the overall fundraising function.

Fundraising Operations and Program Expenses

Expenses Overall Major Gifts Annual Fund

Corp & Foundation

Planned Giving

Salary & Benefits

Fundraiser Salary & Benefits

Prospect Researcher Salary & Benefits

Administrative Overhead

Subtotal Salary & Benefits

Direct Expenses

Travel

Meals

Events

Telephone

Printing & Mailing

Office Supplies

Technology – Hardware, Software

Equipment

Maintenance

Dues & Membership

Donor Recognition

Professional Development

30

Fundraising Operations and Program Expenses (Continued)

Expenses Overall Major Gifts Annual Fund

Corp & Foundation

Planned Giving

Research Subscriptions

Wealth Intelligence & Data Analytics

Subtotal Direct Expenses

Total Expenses

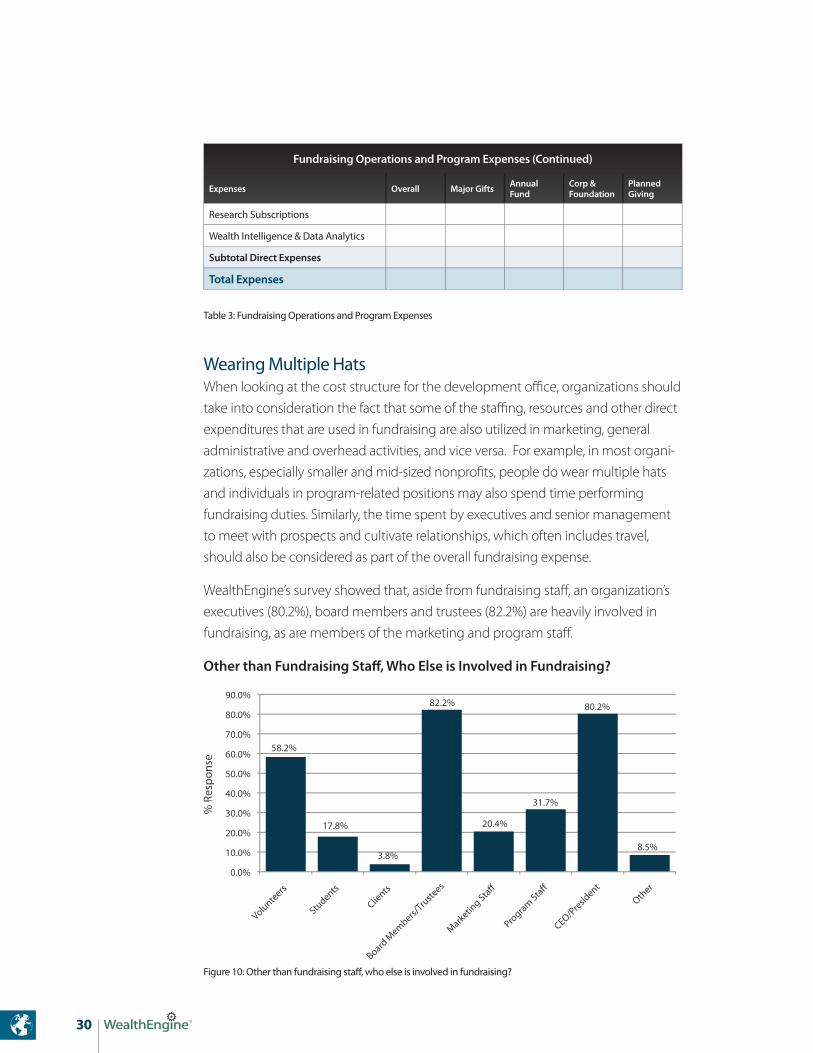

Table 3: Fundraising Operations and Program Expenses

Wearing Multiple HatsWhen looking at the cost structure for the development office, organizations should take into consideration the fact that some of the staffing, resources and other direct expenditures that are used in fundraising are also utilized in marketing, general administrative and overhead activities, and vice versa. For example, in most organi-zations, especially smaller and mid-sized nonprofits, people do wear multiple hats and individuals in program-related positions may also spend time performing fundraising duties. Similarly, the time spent by executives and senior management to meet with prospects and cultivate relationships, which often includes travel, should also be considered as part of the overall fundraising expense.

WealthEngine’s survey showed that, aside from fundraising staff, an organization’s executives (80.2%), board members and trustees (82.2%) are heavily involved in fundraising, as are members of the marketing and program staff.

Other than Fundraising Staff, Who Else is Involved in Fundraising?

% R

espo

nse

% R

espo

nse

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Volunteers

Students

Clients

Board M

embers/Tru

stees

Marketin

g Sta

Program Sta

CEO/Presid

ent

Other

17.8%

58.2%

3.8%

82.2%

20.4%

31.7%

80.2%

8.5%

Figure 10: Other than fundraising staff, who else is involved in fundraising?

Measuring Fundraising Return on Investment 31

Carrie Collins, JDVice President of Institutional Advancement, University of the Sciences, Philadelphia PA

As development professionals, it is important to demonstrate – to the board, to the executive team, to the finance office - that frontline fundraisers are taking advantage of the data they have available to them (the science) to perfect the art of cultivating and soliciting donors. By showing how frontline fundraisers are closing gifts in amounts larger than it costs to employ them, we lend credence to the adage that you have to spend money to make money.

In her experience, she has found the following metrics to be the most relevant in determining a gift officer’s success, and the key benchmarks that she has found applicable to major gift officers at an institution of higher education:

T Number of personal visits: 120 to 150 visits with major prospects

T Percentage of unique visits: calculated as the number of prospects visited/number of visits made, with a goal of 50-75% unique visit prospecting

T Proposals submitted: apply a tiered approach based upon the level of prospects to which the gift officer is assigned, such as:• $25,000 to $100,000: 10 to 15• $100,000 or greater: 4 to 7

T Number of gifts closed: using the following as a general guideline• $25,000 to $100,000: 7 to 20• $100,000 or greater: 2 to 3

T Amount of gifts closed: includes all monies that were donated as a direct result of the gift officer’s efforts, including those that are less than the proposal threshold for which he or she receives credit

T Assists/shared credit: recognize teamwork among gift officers, which makes them far less likely to hoard or poach prospects

T Multiple of total compensation: dollars raised divided by the cost of employment

While most organizations have a formal, annual performance review process, it is important to conduct these assessments more frequently – ideally on a quarterly basis. This allows you to assess performance, make adjustments in staffing or strategy, and document lackluster performance to create a record for future employment decisions.

Collins recommends that organizations prepare a document of expectations for each fundraiser, with the metrics clearly stated, and have the individual agree and sign off on them. When performance evaluations are conducted, you can include these expectations in the evaluation.

White Paper For Nonprofit Organizations

32

Investing in Fundraising

Measuring Fundraising Return on Investment 33

Investing in FundraisingAs organizations can vary in the structure and size of their fundraising infrastructure and fundraising strategy, separate investment decisions and separate ROI tracking should be made for the various types of activities related to fundraising. For exam-ple, activities and campaigns related to acquiring new donors can differ from those related to donor retention and renewal. The key activities related to fundraising typically fall into one of these five areas:

T Capacity-building, which includes operating expenses related to assessing an organization’s capacity to raise money, strategic planning, board recruitment and development, marketing, setting up donor management systems and fundraising systems.

T New donor acquisition efforts, such as direct mail, where nonprofits identify and target donors that make small-to-medium size gifts.

T Individual donor renewal, or fund raising activity that produces net contribu-tions from the second, third, etc. gifts from prior individual donors. Donor renewal focuses on retention and upgrading of prior donors. It includes major gifts, annual gifts, special gifts, capital gifts and gifts for endowment.

T Individual planned giving, in which donors are asked to make deferred, non-cash or life-income gifts.

T Grantseeking from institutional sources such as corporations and foundations.

Furthermore, different fundraising techniques have different costs per dollar raised associated. For example, if you are raising a large percentage of major gifts, then your average cost per dollar raised may be lower than an organization that is focused on raising money through its annual fund. The cost of fundraising can also vary depending on variables such as: the age of the organization, the size of the budget, the popularity of the cause, the skills of the development staff, the strength of the organization’s leadership – and many more.

Historical research done by James Greenfield, a well-respected leader in fundraising and the retired Senior Vice President of Resource Development at Hoag Memorial Hospital Presbyterian in Newport Beach, California, showed average costs to raise a dollar at anywhere from $.05 to $1.00 per dollar raised, depending on the fund-raising activity or method, with a national average of $.20 per dollar raised12. Each method of fundraising should be measured against the results it achieved, and most importantly it should be measured against prior years’ performance using the same

12 Taken from Supporting Advancement.com FAQ, What is the average cost per dollar raised? (http://www.supporting advancement.com/faq/cost_per_dollar_raised.htm)

34

method. This assessment should be done for at least three cumulative years in order to get a complete and accurate picture13.

Reasonable Cost Guidelines for Solicitation Activities

Solicitation Activity Reasonable Cost Guidelines

Direct Mail (acquisition) $1.25 to $1.50 per $1.00 raised

Direct Mail (renewal) $0.20 to $0.25 per $1.00 raised

Membership Associations $0.20 to $0.30 per $1.00 raised

Activities, Benefits and Special Events $0.50 per $1.00 raised (gross revenue and direct costs)*

Donor Clubs and Support Group Organizations $0.20 to $0.30 per $1.00 raised

Volunteer-led Personal Solicitation $0.10 to $0.20 per $1.00 raised

Corporations $0.20 per $1.00 raised

Foundations $0.20 per $1.00 raised

Special Projects $0.10 to $0.20 per $1.00 raised

Capital Campaigns $0.10 to $0.20 per $1.00 raised

Planned Giving $0.20 to $0.30 per $1.00 raised

Table 4: Reasonable Cost Guidelines for Solicitation Activities14

*To calculate bottom-line total costs and net proceeds from a benefit event, calculate and add the indirect and overhead support expenses to direct costs incurred and subtract from gross revenue.

Source: Greenfield, James. “Accountability and Budgeting, Assessing Costs, Results and Outcomes.” In Hank Rosso, Achieving Excellence in Fundraising, New York: Wiley, 2003. Originally published by James M. Greenfield, ed. Fund-Raising Cost Effectiveness: A Self Assessment Workbook, 1996, p.281.

National Averages for Fundraising Costs and Return on Investment

Method Cost Return on Investment

Direct Mail to General Lists (non donors) 115% -15%

Special Events 50% 50%

Planned Giving 25% 75%

Direct Mail to Prior Donors 20% 80%

Foundations/Corporations 20% 80%

Major Gifts 5-10% 90-95%

National Average, all methods 20% 80%

Table 5: National Averages for Fundraising Costs and Return on Investment

Source: Greenfield, James. Fund-Raising: Evaluating and Managing the Fund Development Process.

13 Greenfield, James. “Accountability and Budgeting, Assessing Costs, Results and Outcomes.” In Hank Rosso, Achieving Excellence in Fundraising, New York: Wiley, 2003. 14 Greenfield, James. “Accountability and Budgeting, Assessing Costs, Results and Outcomes.” In Hank Rosso, Achieving Excellence in Fundraising, New York: Wiley, 2003. Originally published by James M. Greenfield, ed. Fund-Raising Cost Effectiveness: A Self Assessment Workbook, 1996, p.281.

Measuring Fundraising Return on Investment 35

Table 5 indicates that you would need to spend $1.15 in order to raise $1.00 through direct mailings to general lists. To solicit major gifts, you would spend 5 to 10 cents to raise $1.00. In practice, however, there is such wide range in costs and many variables to be considered, that it is hard to place a target or benchmark on how much it should cost to raise a dollar. Depending on the circumstance, the campaign, timing and goal, an organization can (and should) spend anywhere from $0.10 to over $2.00 to raise a dollar. In addition, different organization types have different channels available to them and some are more effective than others.

The more important considerations are to assess the returns of each activity against the initial fundraising goal, and against other activities, and do this over a three or five-year timeframe to determine trends. Mal Warwick highlighted this in his Ask Mal blog entry, “How Much to Spend”:

“Some organizations are blessed with highly efficient fundraising programs that allow them either to acquire new donors at a breakeven or to derive so much revenue so quickly from new donors that the effect is much the same.

Other nonprofits are forced to wait for two or three years, or even more, to recoup their investment.

With all that said, however, it’s becoming increasingly common for nonprofit organizations to pay a net initial cost of between $5 and $50 to acquire an aver-age new donor. In such circumstances, I advise clients that – if it’s worth paying, say, $30 to enroll a new donor – it’s worth paying at least that much to reacti-vate a donor who has lapsed.”15

As Rick Dunham, President & CEO of Dunham+Company, a national fundraising consultancy with specialization working with ministries, pointed out in an interview with WealthEngine, “The press has unfairly characterized the topic of ROI and donor acquisition. Some organizations will spend $100 to get a donor, but will get $1000, which is great – a 10:1 return. Others will spend $20-25 and get $50, so a 2:1 return. But over time they can grow that value. So you have to look at it as a cumulative measure, and not on a single basis. Looking at net revenue is extremely important as well. It serves as the ballast for comparing other metrics. For example, you could spend $20,000 to raise $100,000, or you could spend $30,000 and raise $125,000. In the second scenario, the ROI is lower but the net revenue is higher.”

15 Mal Warwick Associates, How much to spend? (http://www.malwarwick.com/mals-corner/askmal/how-much-to- spend.html)

White Paper For Nonprofit Organizations

36

Controlling Costs and Maximizing Contributions: Striking a Balance

Measuring Fundraising Return on Investment 37

Controlling Costs and Maximizing Contributions: Striking a BalanceIt is important for organizations to look at their ROI as a benchmark that is specific to their unique organization and that is tied to their overall strategic plan and fundraising strategy. Development professionals, CFOs and board members can use ROI, CRD and other performance measures to determine what mix of fundraising investments, done at this stage in their fundraising strategy, gives the organization the best return over time.

Historically, there has been much pressure on organizations to minimize fundraising costs. Published in 2004, The National Overhead Cost Project16 reported that nonprofits should spend no more than 25 to 50 percent of contributions on fundraising, where the average across all industry sectors is to spend less than 35 percent of contribu-tions on fundraising17. This means that a charity was expected to spend no more than $0.35 to raise each dollar. However, the majority of charities were actually spending far less than this amount – between $0.15 and $0.24 per dollar raised. Many organiza-tions that went above the 35% benchmark were criticized by donors and the media, which incited a high degree of pressure to keep their costs in check.

More contemporary attitudes dispel the notion that lower fundraising costs are associated with a better-managed nonprofit. Current research into the economics of charitable fund raising indicates that investing in the development and fundraising function not only improves the annual rate of growth of giving, but can also help the nonprofit to improve the overall effectiveness and efficiency of their organization.

Nevertheless, the pressure is on. Nonprofits have historically had tight budgets and the economic environment has exacerbated this. As Rick Dunham points out, “There is a high sensitivity to measuring ROI and controlling expenses, in the U.S. and even more so in the U.K. There is a sensitivity to ensuring that the investment is making a return. But when organizations get into expense management and become too focused on lowering expenses, it does more harm than good. In many cases, campaigns get derailed by an over-focus on the expenses, when in fact if the organization had continued the course, they would have raised more.”

At the end of the day, it’s about striking a balance between efficiency and effectiveness. ROI will vary depending on the organization’s efforts towards achieving maximum net revenues, or effectiveness, versus maximum efficiency, or keeping fundraising expenses as low as possible.

16 The Nonprofit Fundraising and Administrative Cost Project, published in 2004, is a collaboration between the Center on Philanthropy at Indiana University and the Center on Nonprofits and Philanthropy at the Urban Institute. 17 The Pros and Cons of Financial Efficiency Standards, Nonprofit Overhead Cost Project, Brief No. 5, Center on Nonprofits and Philanthropy, Urban Institute and Center on Philanthropy, Indiana University, August 2004.

38

The Challenges of Accounting for Overhead Expenses Fundraising costs, including the cost of wealth intelligence solutions, are a key component to the organization’s operating expenses. While these overhead expenses must be reported in the nonprofit’s IRS Form 990, there are a number of issues that affect the reliability of these figures. Issues abound, from the lack of a uni-versal accounting standard for nonprofits, to the variations and changing definitions of the ways in which fundraising and administrative expenses should be accounted for, to conflicting ideas about where fundraising expenses should be charged.

In fact, a survey done by the Nonprofit Fundraising & Administrative Cost project in 2004 found that 37% of organizations with more than $50,000 in private contributions reported zero fundraising and special event costs. Of those reporting costs, more than a quarter received more than $15 for each dollar spent on fundraising. These remarkable figures show that the pressure to keep costs low is leading to questionable accuracy in how costs are tracked and reported.

Nonprofits face pressure from their funding sources (government agencies, individuals, and foundations) as well as external watchdog organizations to keep a tight rein on overhead expenses. Part of the pressure to keep costs low and efficiency percentages high also comes from grant organizations and donors, who want to know that their dollars are making a difference. The Better Business Bureau’s Wise Giving Alliance provides standards for charity accountability and produces reports on nationally soliciting charitable organizations. Included in their recommendation is a guideline that organizations spend no more than 35% of related contributions on fundraising. Related contributions include donations, legacies, and other gifts received as a result of fundraising efforts. However, while most organizations keep well within this guideline, their research found that over half of adult Americans felt that nonprofit organizations should have overhead rates of 20 percent or less; nearly four in five felt that overhead should be less than 30 percent18.

While regulators, watchdogs, and donors may have altruistic concerns when evaluating charities and encouraging them to limit their costs, this creates excessive pressure that can actually hamper the charities ability to deliver upon their mission. Professionals within the nonprofit community have the power to change donor thinking about fundraising costs, and we are beginning to see this play out.

18 Bedsworth, Gregory and Howard, Nonprofit Overhead Costs: Breaking the Vicious Cycle of Misleading Reporting, Unrealistic Expectations, and Pressure to Conform, 2008, which cites a 2001 research study by the Better Business Bureau Wise Giving Alliance (BBB Wise Giving Alliance Donor Expectations Survey, Princeton Research Associates, 2001.)

Measuring Fundraising Return on Investment 39

In traditional thinking, donors would consider issues such as:

T How much goes to the mission or cause? How high are the nonprofit’s expenses?

T Do they need my money? Will my money just be lying around in their reserve?

It is the nonprofits responsibility to facilitate the reshaping of donor thinking, by be-ing able to provide answers to the more relevant questions of:

T How efficient and effective is their fundraising? What is their cost-per-fundraised-dollar ratio?

T Is the charity run properly? How efficient and effective is their human capital? Management team?

It is these questions that allow us to focus on the key measures of efficiency and effectiveness and to truly evaluate nonprofits on their ability to deliver change and serve their cause. At the end of the day, that is the return that is most important.

The Impact of Donor CultivationROI and CRD metrics are more meaningful when looked at in conjunction with factors such as average donor cycles and cultivation time. For example, first year expenses may be higher, but as the fundraising program matures, the cost to raise a dollar tends to taper. Likewise, returns are typically higher in the early stages of a major giving campaign, and in fact most fundraising professionals have found that the greatest contributions are made during the silent phase before the campaign even reaches the public domain. It is typical for 60% or more to be raised before the campaign goes public. This underscores the need to evaluate ROI and CRD over a three, five and ten year timeframe for each individual fundraising activity and for all combined. By looking at ROI in this way, the organization can balance the issues of efficiency and effectiveness.

As Olshansky points out, “There is an old saying: you want advice, ask for money. You want money, ask for advice. The trick is to really engage your donors. Transactional fundraising is not the way to gain success or improve your ROI.”

The Association of Advancement Services Professionals (AASP) and the Association for Professional Researchers for Advancement (APRA) teamed together to create a consistent, usable set of policies and procedures for the industry so that metrics and evaluation, as well as actions and prospect management, can be consistent across staff members19. Their best practices in prospect management include the following portfolio optimization guidelines:

19 Association of Advancement Services Professionals (AASP) http://www.advserv.org/Resources/Documents/AASPA PRA_Best%20Practices_ProspectManagement_Polies%20and%20Procedures.pdf

40

T Assign a priority to each prospect: top (ask within 12-18 months), emerging (move to Top within 12-18 months), discovery, stewardship, perpetual steward-ship (probably not going to give much more, but continue contacting them)

T Based on having approximately 120-150 major gift prospects (20-30 in Top, 20-30 in emerging)• 25% in Qualification• 25% in Cultivation • 30% in Pre-solicitation or Solicitation• 20% in Identification (before a gift) or Stewardship (after a gift)

T 80-150 major gift prospects to be cultivated over the next 2-5 years , leading to 30-45 asks per year, which should yield 10-15 gifts each year

Cultivation is the longest stage in the continuum, and can last up to a year. Traditionally, it’s also the most resource-intensive from a human capital perspective, as the gift officer’s responsibilities include in-person meetings, handwritten notes, personal phone calls, tours, etc. But in the long run it is a strategy that pays off. Industry metrics show that the costs of acquiring a new donor can be 6 to 7 times more than retaining an existing donor.

Studies have shown that donors who give over multiple years give much more than those who don’t. For every year you retain a donor, they become more valuable. And because your cost to cultivate doesn’t rise as quickly as does their support, you are generating greater net revenue to fuel your organization. For example, a study presented in 2010 by The Center on Philanthropy at Indiana University20 showed that persistent (3-yr) donors give more on average than repeat (2-yr), or occasional donors (1-yr). This study is based on a sample of 5,728 households who answered giving questions in 2001, 2003, and 2005.

Persistent (3-yr) Repeat (2-yr) Occasional (1-yr)

Mean Median Mean Median Mean Median

Total $2,659 $1,260 $1,022 $400 $406 $150

Religion $1,627 $500 $592 $50 $216 $0

Secular $1,033 $380 $430 $127 $190 $51

Table 6: Persistent, Repeat & Occasional Donors. Based on COPPS data.

Source: Based on COPPS data.

20 The Center on Philanthropy at Indiana University, http://www.cic.edu/News-and-Publications/Multimedia-Library/CIC ConferencePresentations/2011%20Presidents%20Institute/philanthropic-giving.pdf.

Measuring Fundraising Return on Investment 41

Special Considerations for Planned GivingROI metrics for planned giving should be considered separately from other gift types. The related costs for planned gifts can occur many years before the income is received. In fact, the average time from inception to maturity for a planned gift is 7-10 years. Therefore, looking at its ROI in the context of the year in which the gift is initially committed gives an incomplete measurement.

Furthermore, charitable organizations have different guidelines in accounting for planned gifts, determining the charitable tax deduction for planned gifts, and counting planned gifts for capital campaign reporting. For example, IRS charitable deduction calculations were not created for the purpose of counting planned gifts and, while valid for tax purposes, do not offer a way of counting planned gifts that recognizes the total campaign and development effort21. In many cases, these various yet accepted methods for accounting, counting, and determining the charitable deduction do not effectively capture the value of planned gifts.

The Partnership for Philanthropic Planning (formerly NCPG) offers Guidelines for Counting Charitable Gifts as well as Valuation Standards for Charitable Planned Gifts to help nonprofits understand the value of a planned gift in terms of its present purchasing power. Utilizing these standards to measure the value of a planned gift – and calculating ROI accordingly – enables the organization to better understand the costs and benefits of planned gift fundraising and determine the overall effective-ness of their investment in planned giving.

The good news is that donors can be more generous with non-cash gifts because of additional tax benefits. The typical capital gift target is 20 times a donor’s largest annual fund gift, while the typical planned giving target is 200 times a donor’s largest annual fund gift22. So while understanding the costs and returns of planned gift fundraising may prove challenging, the benefits are proven.

“Donor cultivation, and ultimately donor retention, is a careful dance between the short-term funding needs of the organization and the long-term impact of keeping a donor year after year.”23

- Rick Dunham President & CEO, Dunham+Company

21 Partnership for Philanthropic Planning, National Committee on Planned Giving, Guidelines for Counting Charitable Gifts, 2nd Edition, 2008. ( http://www.pppnet.org/pdf/NCPG-counting-guidelines-(rev-2008).pdf) 22 http://www.plannedgiving.com/answers/marketing 23 Dunham+Company, http://dunhamandcompany.com/rickblog/fundamental-3-donor-cultivation-and-retention/

White Paper For Nonprofit Organizations

42

The Tie to the Marketing Office

Measuring Fundraising Return on Investment 43

The Tie to the Marketing OfficeWhile there are massive differences between fundraising, marketing and commu-nications, fundraising and marketing professionals need to work closely together to achieve fundraising goals. The fundraising and development process is designed to convince prospective donors to contribute to the nonprofit organization, while the marketing process serves to promote the delivery of services that benefit their constituents. In practice, fundraising provides the opportunity for donors to support their community and/or the nonprofit’s constituency. Marketing advances the efforts to carry out the organization’s mission through advertising, promotion, publicizing its programs and services to its users and the general community, and recruiting volunteers and sponsors.

In essence, development focuses on the donor, and marketing focuses on the constituent. That said, there are great opportunities for the two groups to generate synergies. Their priorities need not be in conflict with each other, and the marketing director and the development director should regularly coordinate, interact, encourage and support their mutual goals, efforts and achievements.

For example, the marketing communications that are used to support fundraising activities also serve to build awareness for the organization as a whole and its cause. This in turn helps to build a pipeline for potential donors and facilitates the “ask.” Second, it is the brand identity and messaging that marketing creates that helps the organization speak with a single voice and deliver a clear message that resonates with current and prospective donors.

WealthEngine’s research in the marketplace shows that one of the closest points of interaction between the two groups is in the area of communications and social media, and data and analytics. Marketing helps fundraising with commu-nications, while fundraising aids marketing with acquiring and maintaining data, and preparing or recommending list segmentations. The majority of fundraising professionals who participated in our survey feel that the relationship between the two departments is somewhat or very collaborative.

One of the most promising aspects of social media is its impact on ROI. Nonprofits of every kind are finding that social media is making word of mouth marketing and advertising exponentially more effective.

44

How Marketing Department Assists with Fundraising

Figure 11: Please specify how your marketing department assists with fundraising

How Development Team Assists with Marketing

Figure 12: Please specify how your development team assists with marketing

% Response % Response

52.1%

49.0%

62.4%

43.6%

39.0%

34.7%

15.2%

6.4%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Preparing or recommending list segmentations

Acquiring data

Maintaining database

Conducting prospect and market level research

Monitoring and contributing to social media communities

Data analytics

Does not assist

Other

% Response % Response

11.2%

26.6%

57.4%

28.7%

22.8%

16.8%

45.9%

7.6%

8.6%

7.4%

6.8%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Does not assist

We do not have a separate marketing department

Issuing communications and press releases