mclean county unit school district no. 5 normal, illinois

TRANSCRIPT

MCLEAN COUNTY UNIT SCHOOLDISTRICT NO. 5Normal, Illinois

FINANCIAL STATEMENTS ANDSUPPLEMENTAL INFORMATION

June 30, 2010

i

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5

TABLE OF CONTENTS

PAGE

INDEPENDENT AUDITOR’S REPORT...................................................... 1

BASIC FINANCIAL STATEMENTSGovernment-Wide Financial Statements:

Statement of Net Assets - Modified Cash Basis.............................. 3Statement of Activities - Modified Cash Basis ................................. 4

Fund Financial Statements:Statement of Assets and Liabilities Arising from

Cash Transactions - Governmental Funds................................ 5Reconciliation of the Governmental Funds Statement

of Assets and Liabilities Arising From Cash Transactionsto the Statement of Net Assets - Modified Cash Basis .............. 7

Statement of Revenue Collected, Expenditures Paid, andChanges in Fund Balances - Governmental Funds................... 8

Reconciliation of the Governmental Funds Statementof Revenue Collected, Expenditures Paid, and Changes in Fund Balances With the Statement ofActivities - Modified Cash Basis ................................................ 10

Proprietary Funds - Internal Service Funds - Statement ofAssets and Liabilities Arising From Cash Transactions ............. 11

Proprietary Funds - Internal Service Funds - Statement ofRevenue Received, Expenses Disbursed andChanges in Net Assets.............................................................. 12

Statement of Fiduciary Net Assets - Modified Cash Basis .............. 13Fiduciary Fund - Statement of Changes in Fiduciary Net Assets -

Modified Cash Basis ................................................................. 14

Notes to Basic Financial Statements ................................................ 15

Required Supplementary Information - Unaudited:Schedule of Funding Progress - Illinois Municipal

Retirement and Other Post Employment Benefits ..................... 42Statement of Revenue Collected, Expenditures Paid,

and Changes in Fund Balances - Budget and Actual -General Fund and Working Cash Fund..................................... 43

Notes to Required Supplementary Information ............................... 45

ii

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5

TABLE OF CONTENTS

STATEMENT PAGESUPPLEMENTAL INFORMATION

Combining and Individual Fund Financial Statements:Governmental Fund Types:

Other Governmental Funds:Combining Statement of Assets and Liabilities

Arising from Cash Transactions .......................................... 1 47Combining Statement of Revenue Collected,

Expenditures Paid, and Changes in Fund Balances............ 2 48

General Fund:Combining Statement of Assets and Liabilities Arising

From Cash Transactions........................................................... 3 49Combining Statement of Revenue Collected, Expenditures

Paid, and Changes in Fund Balance ......................................... 4 50Educational Account:

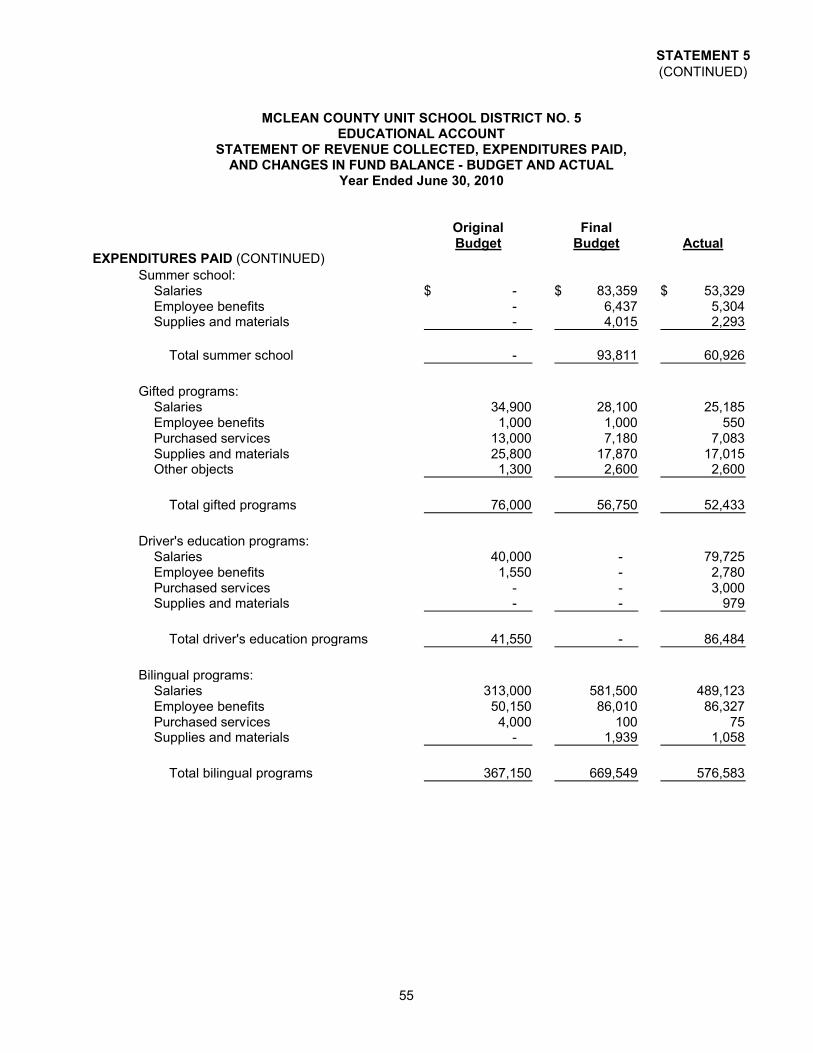

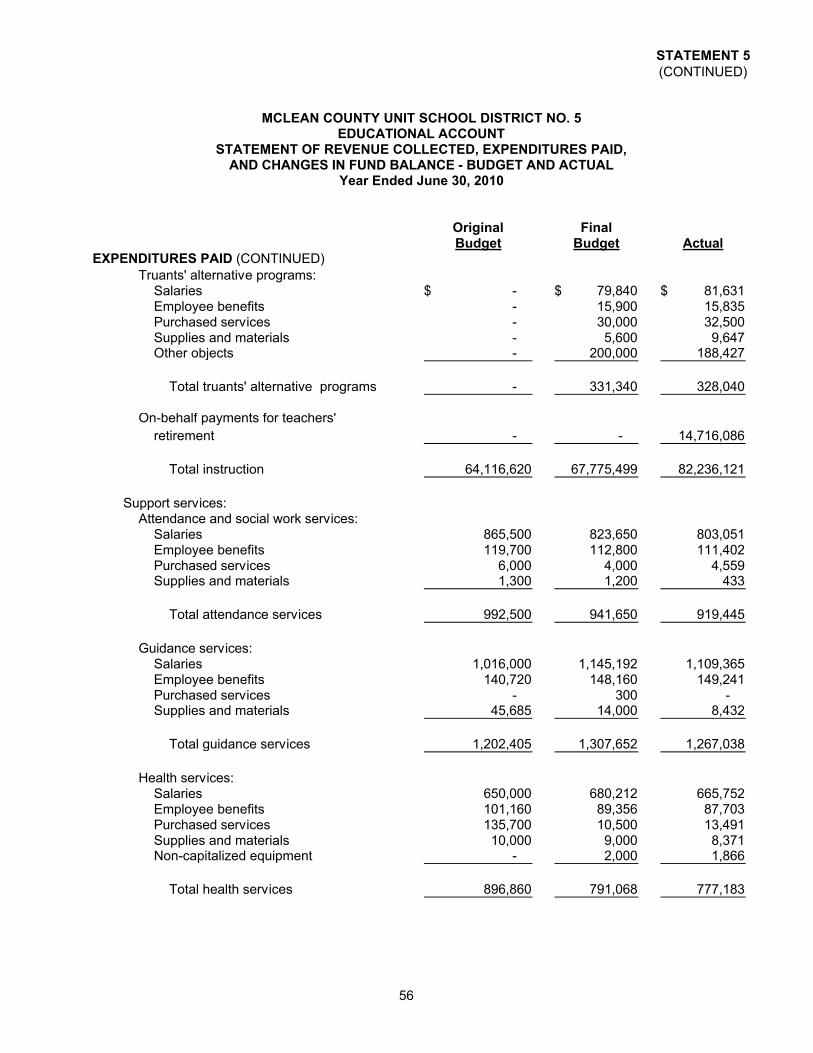

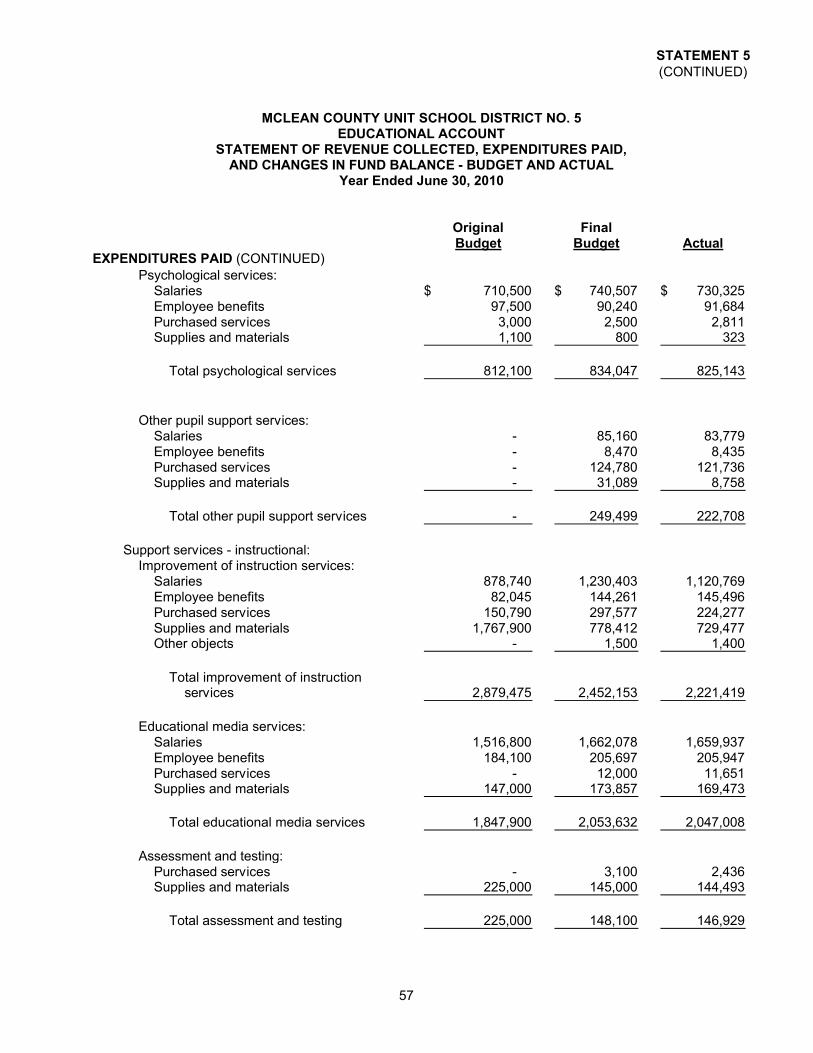

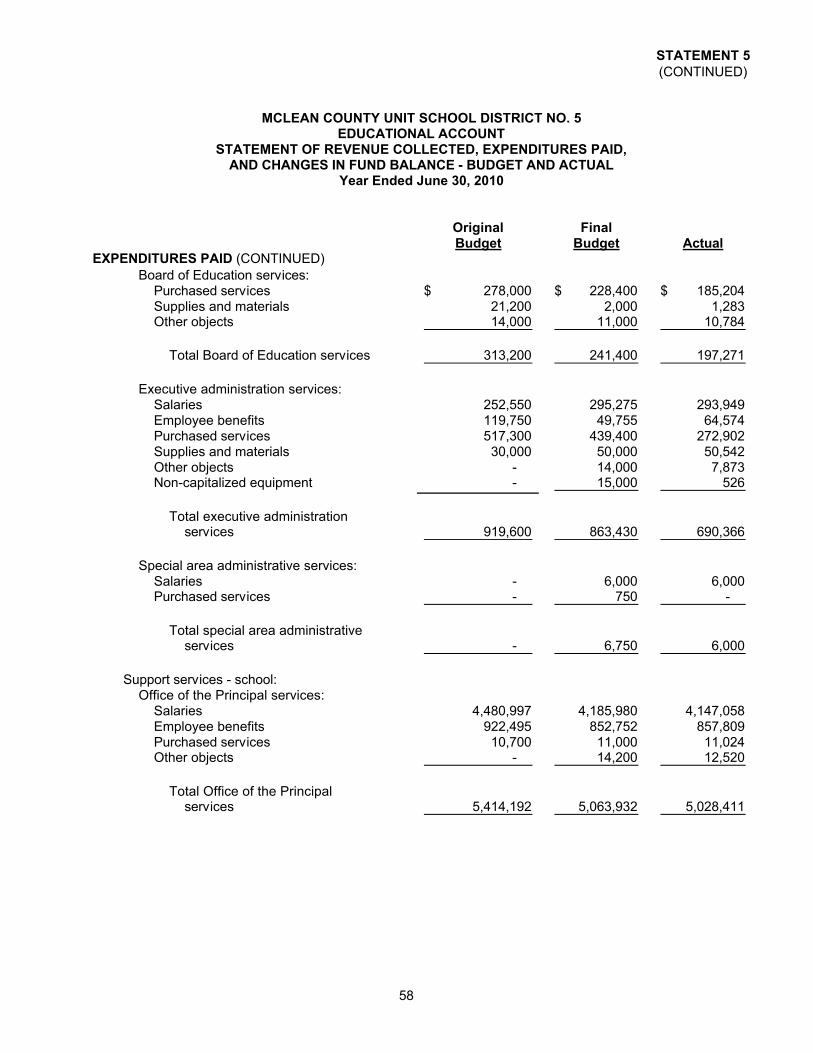

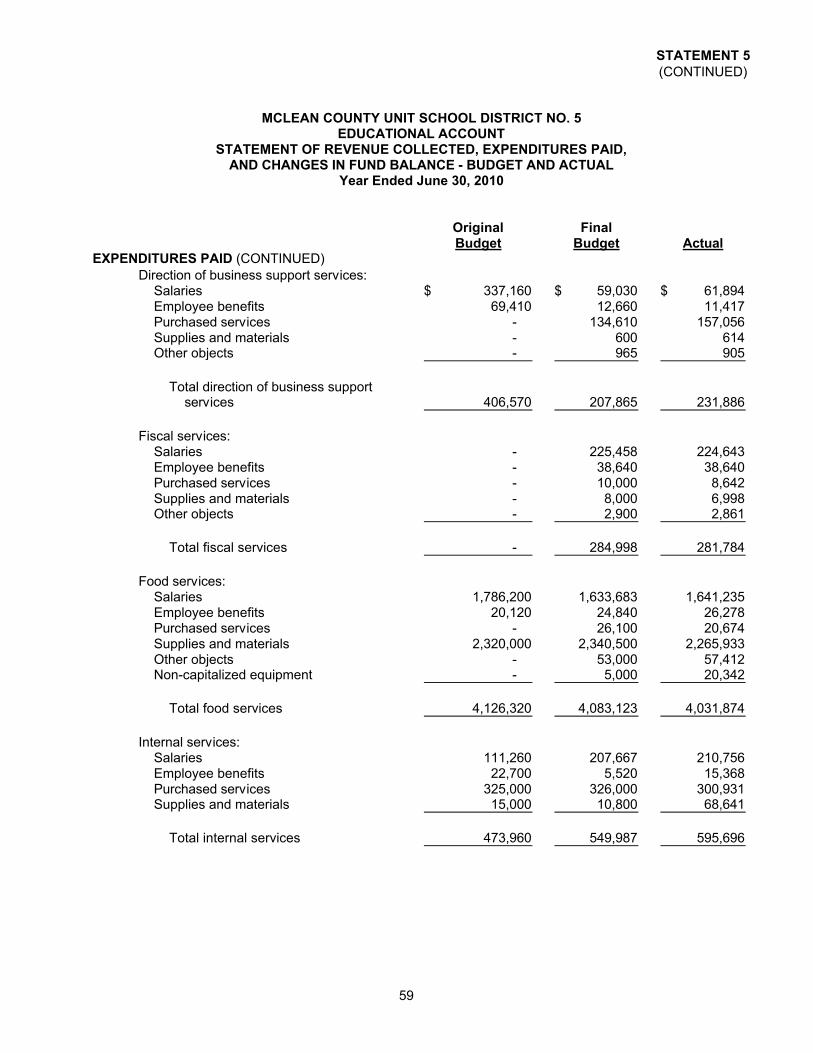

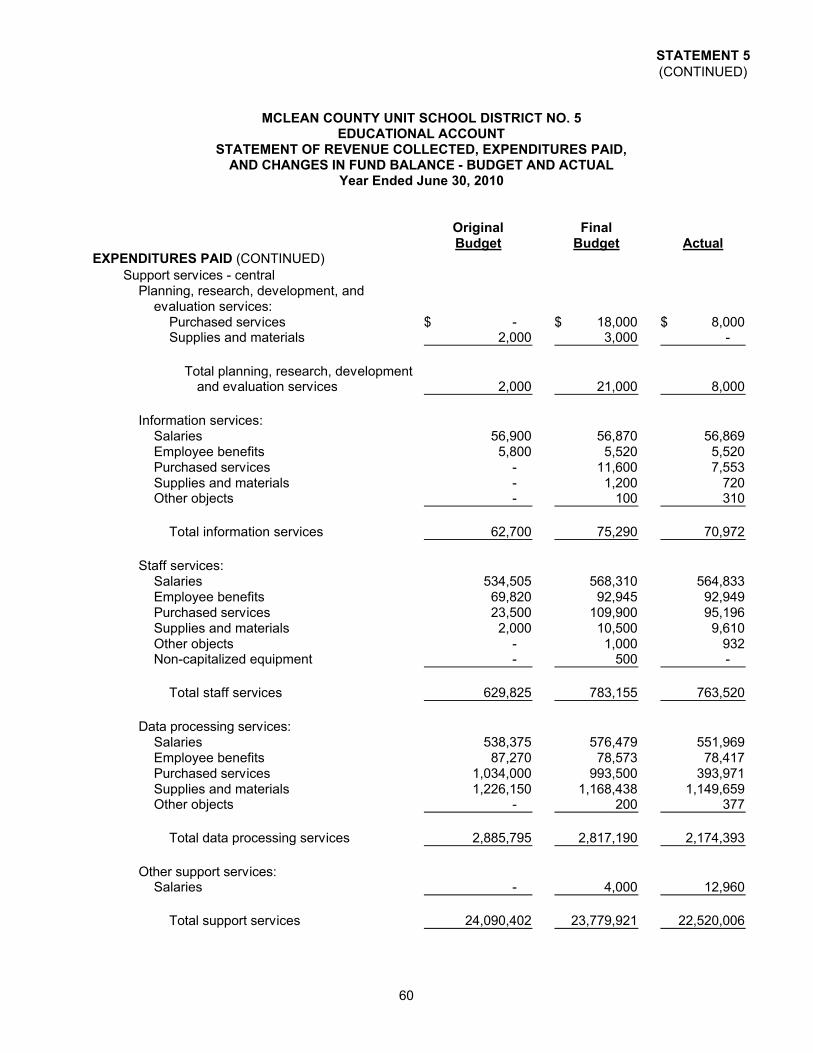

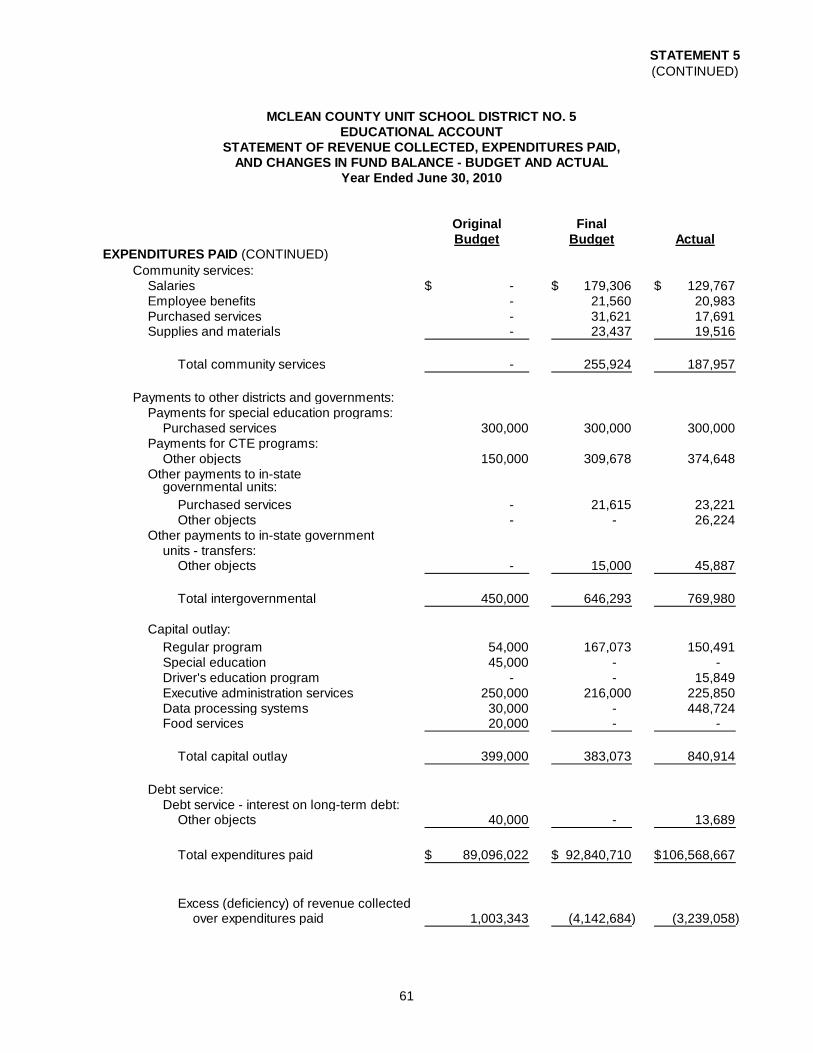

Statement of Revenue Collected, Expenditures Paid,and Changes in Fund Balance - Budget and Actual ............ 5 52

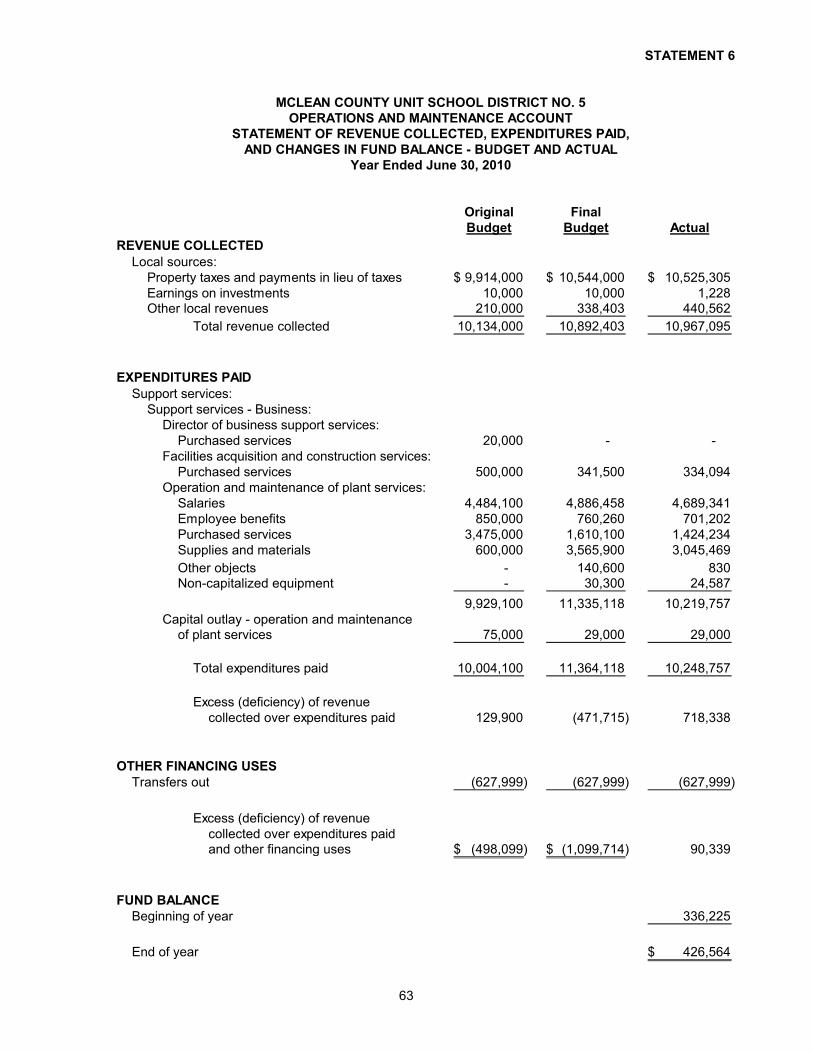

Operations and Maintenance Account:Statement of Revenue Collected, Expenditures Paid,

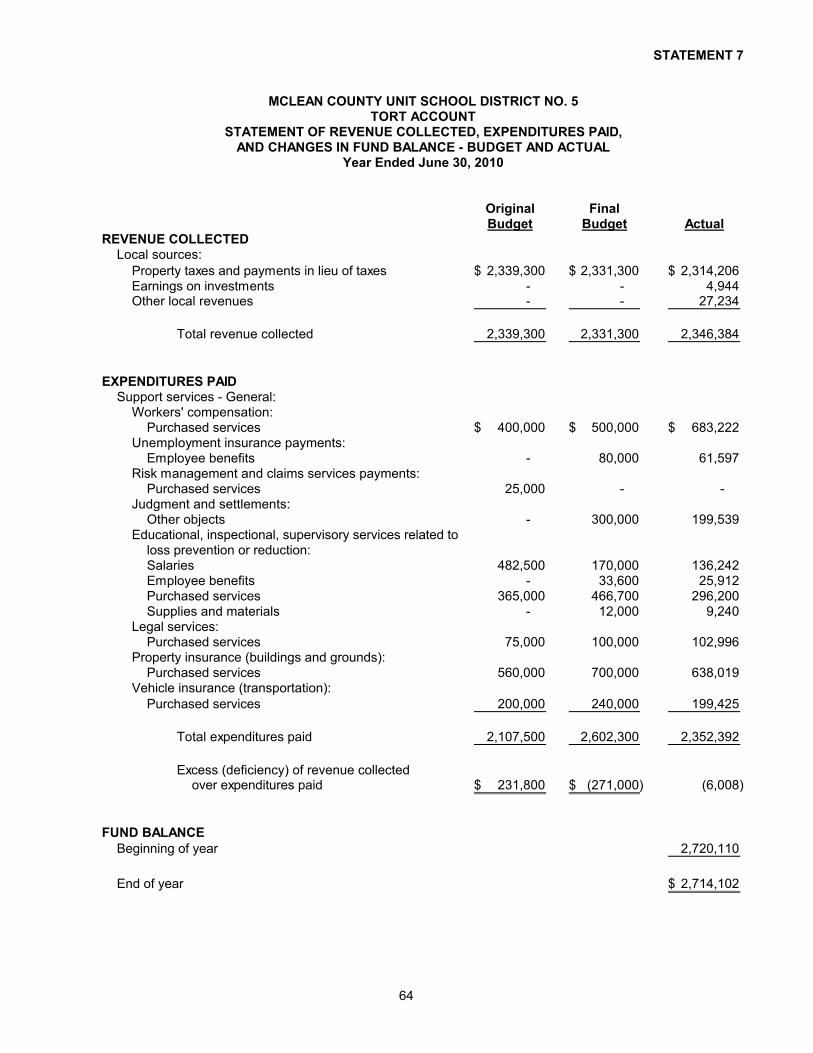

and Changes in Fund Balance - Budget and Actual ............ 6 63Tort Account:

Statement of Revenue Collected, Expenditures Paid,and Changes in Fund Balance - Budget and Actual ............ 7 64

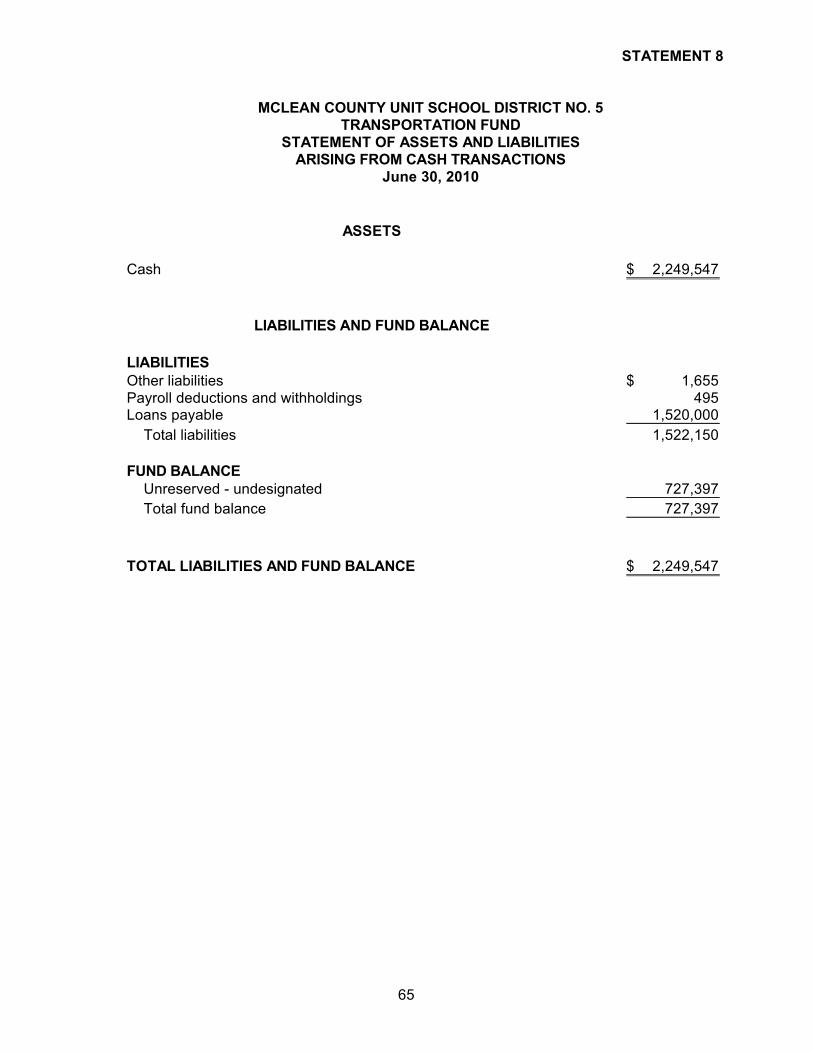

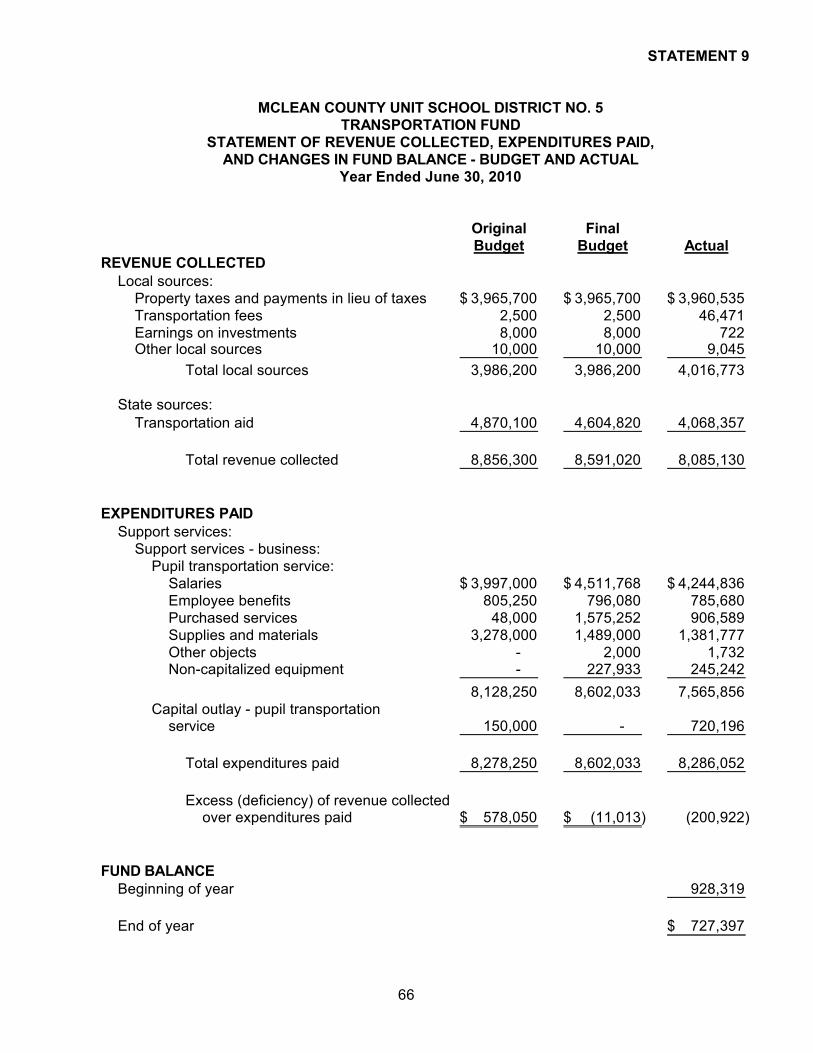

Transportation Fund:Statement of Assets and Liabilities Arising From Cash

Transactions ............................................................................. 8 65Statement of Revenue Collected, Expenditures Paid,

and Changes in Fund Balance - Budget and Actual .................. 9 66

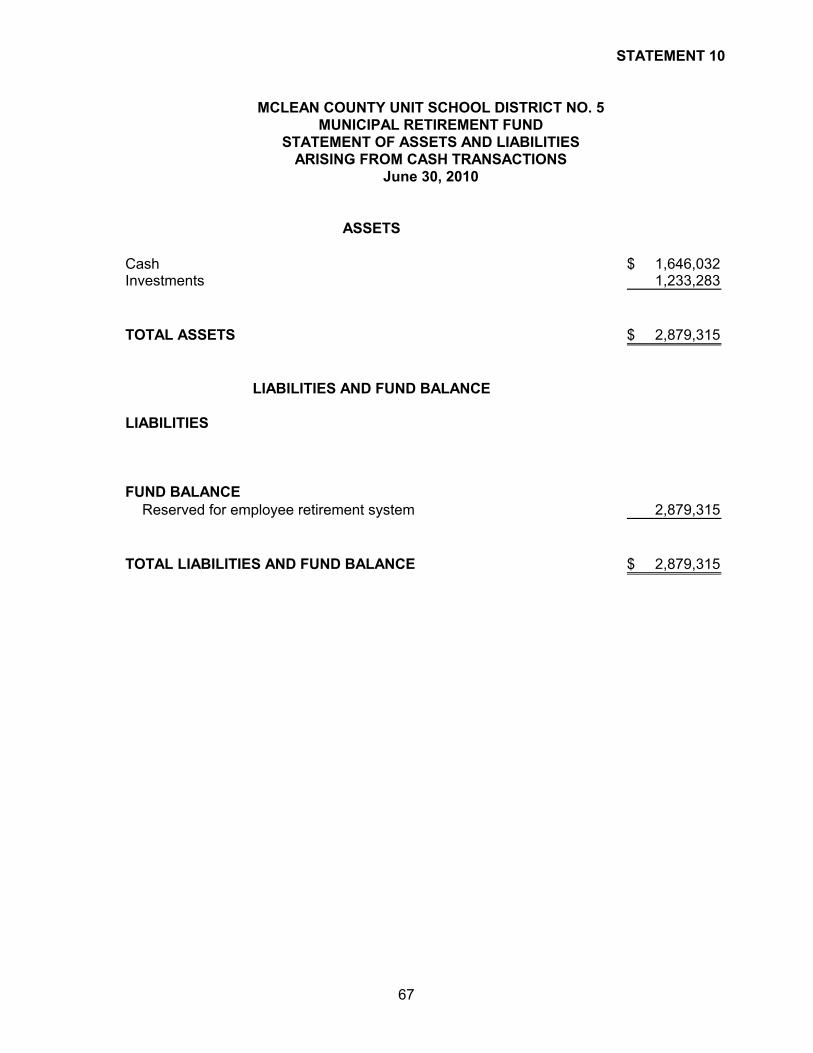

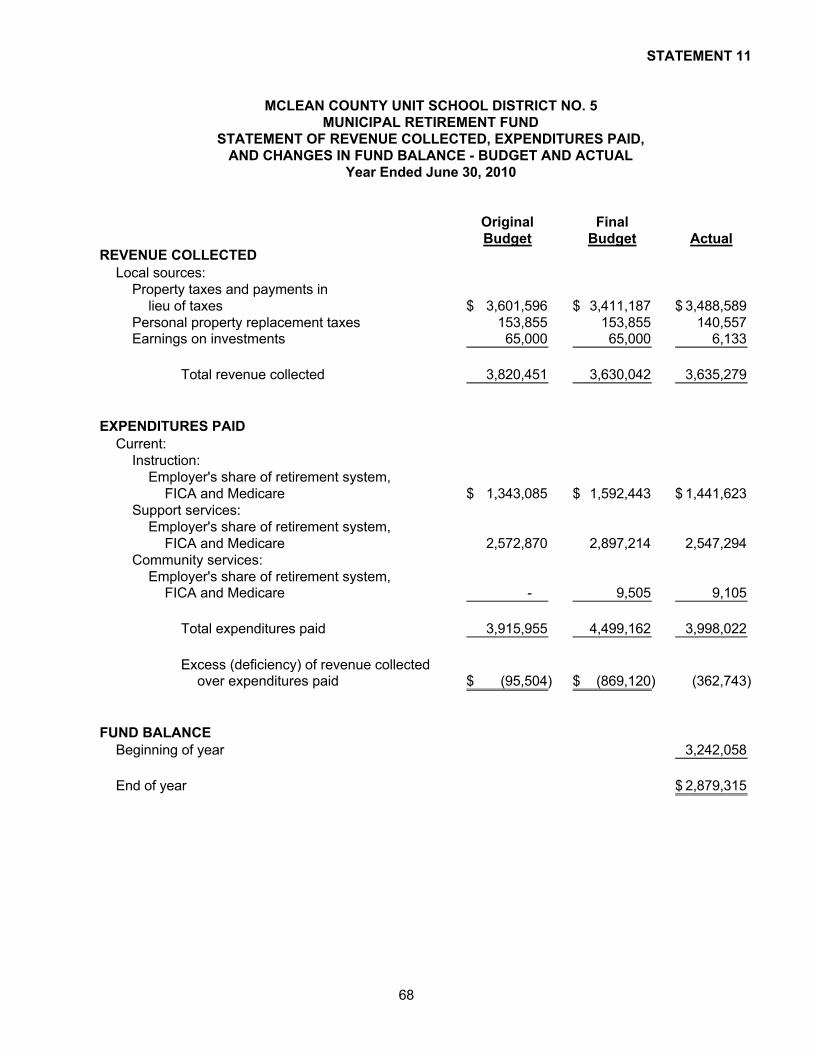

Municipal Retirement Fund:Statement of Assets and Liabilities Arising From Cash

Transactions ............................................................................. 10 67Statement of Revenue Collected, Expenditures Paid,

and Changes in Fund Balance - Budget and Actual .................. 11 68

iii

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5

TABLE OF CONTENTS

STATEMENT PAGESUPPLEMENTAL INFORMATION (CONTINUED)

Combining and Individual Fund Financial Statements (Continued):Working Cash Fund:

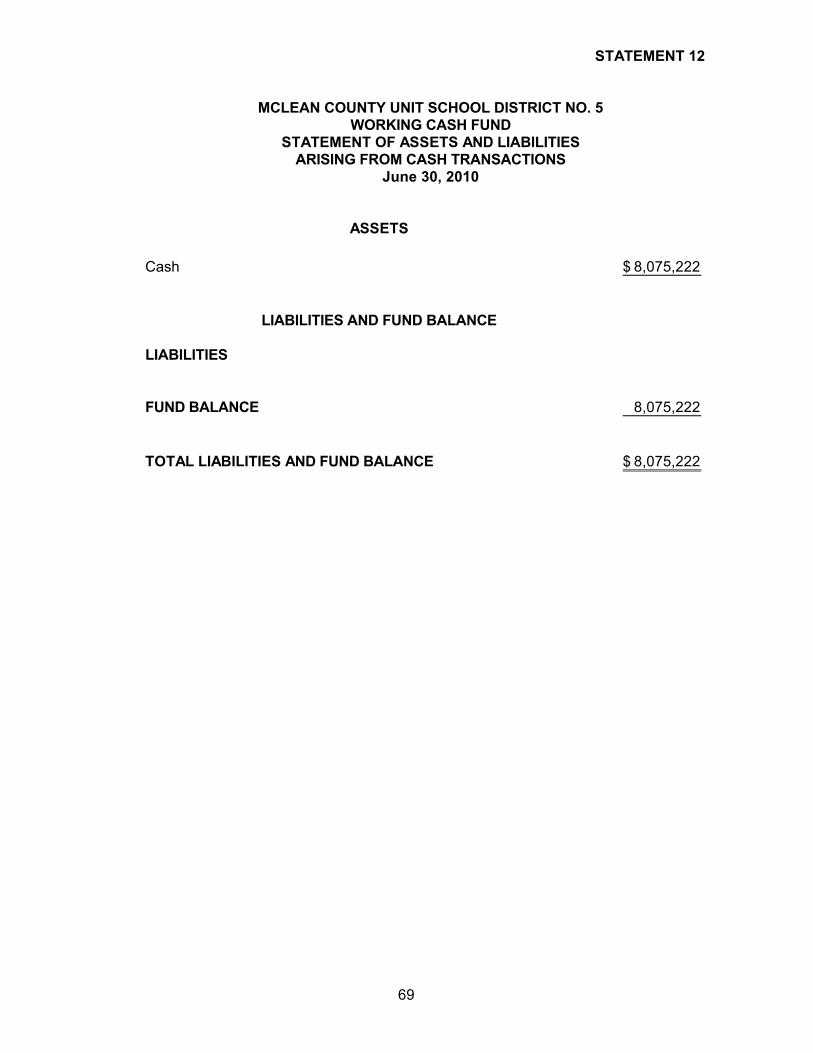

Statement of Assets and Liabilities Arising From CashTransactions ............................................................................. 12 69

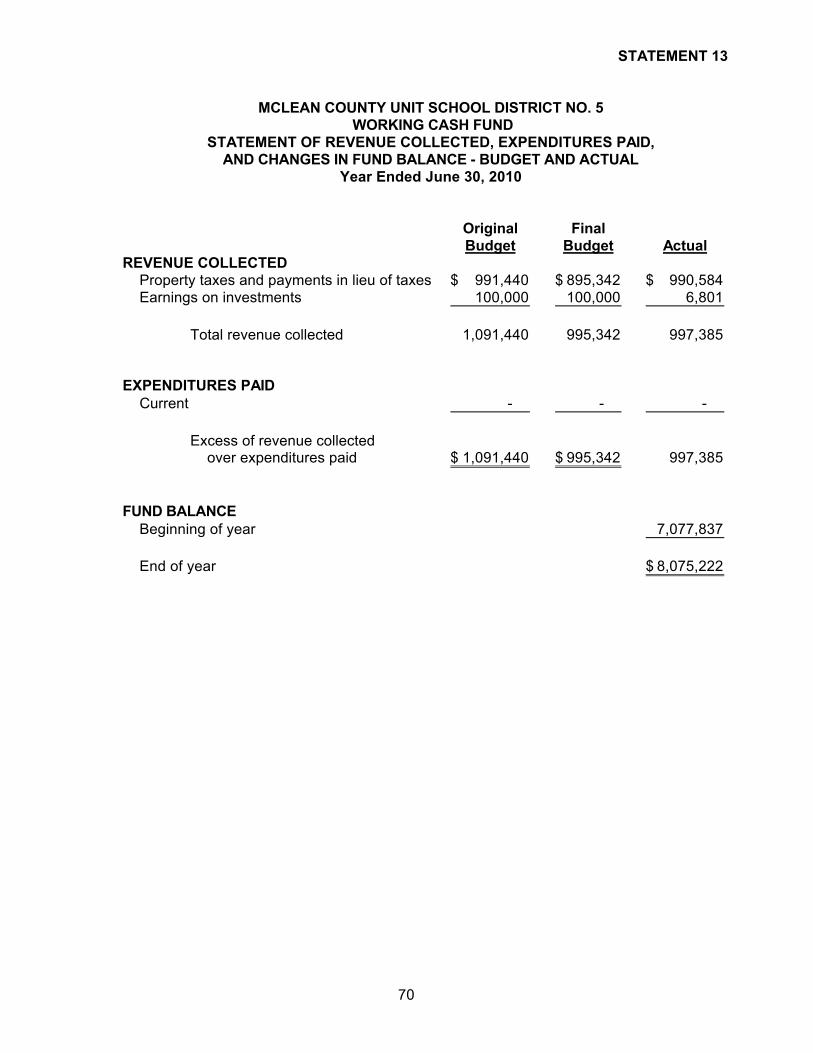

Statement of Revenue Collected, Expenditures Paid,and Changes in Fund Balance - Budget and Actual .................. 13 70

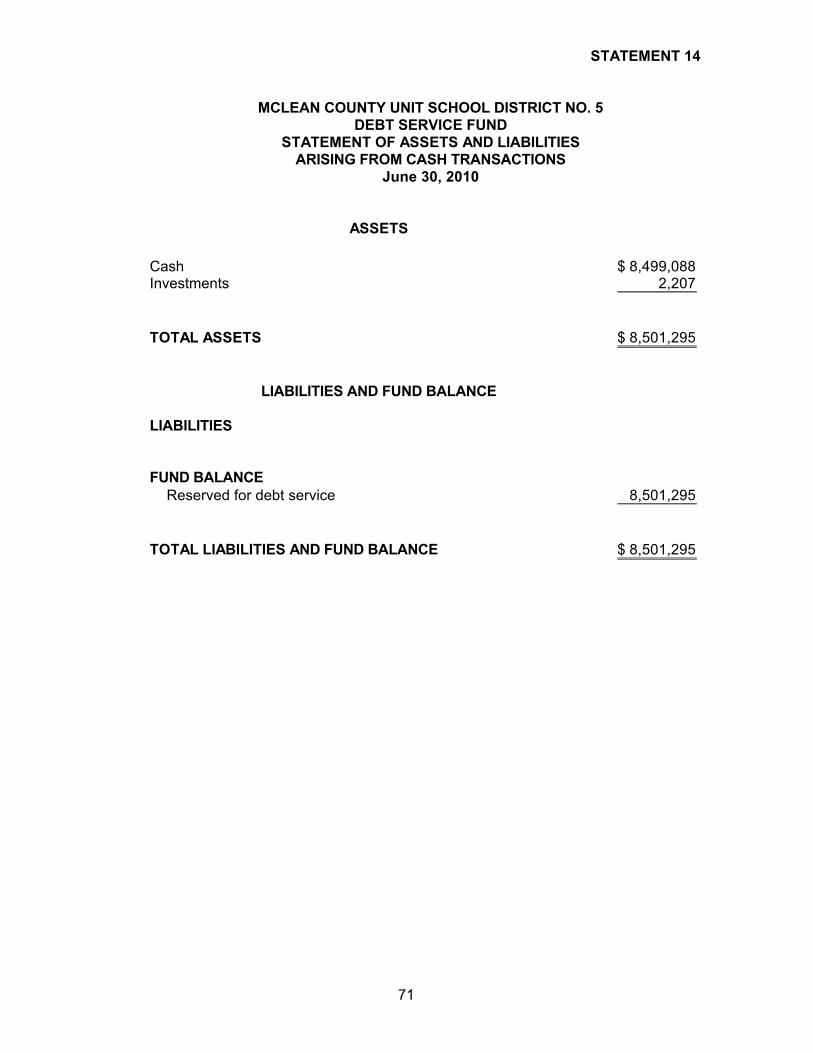

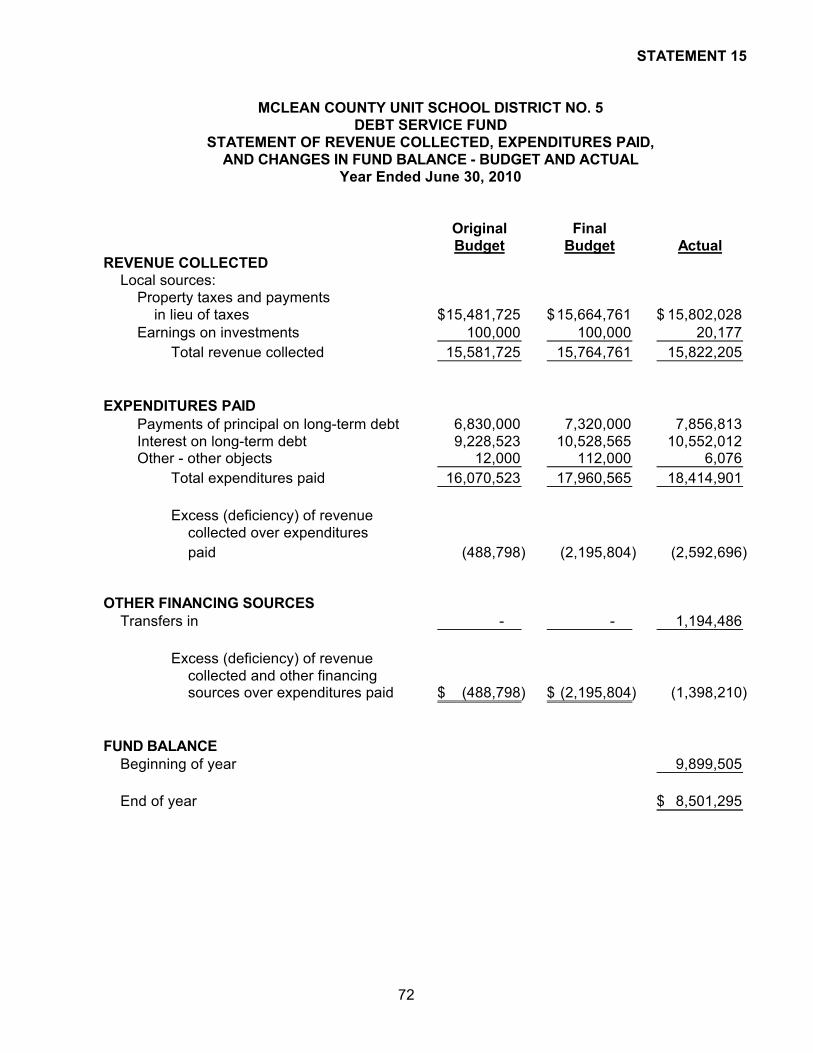

Debt Service Fund:Statement of Assets and Liabilities Arising From Cash

Transactions ............................................................................. 14 71Statement of Revenue Collected, Expenditures Paid,

and Changes in Fund Balance - Budget and Actual .................. 15 72

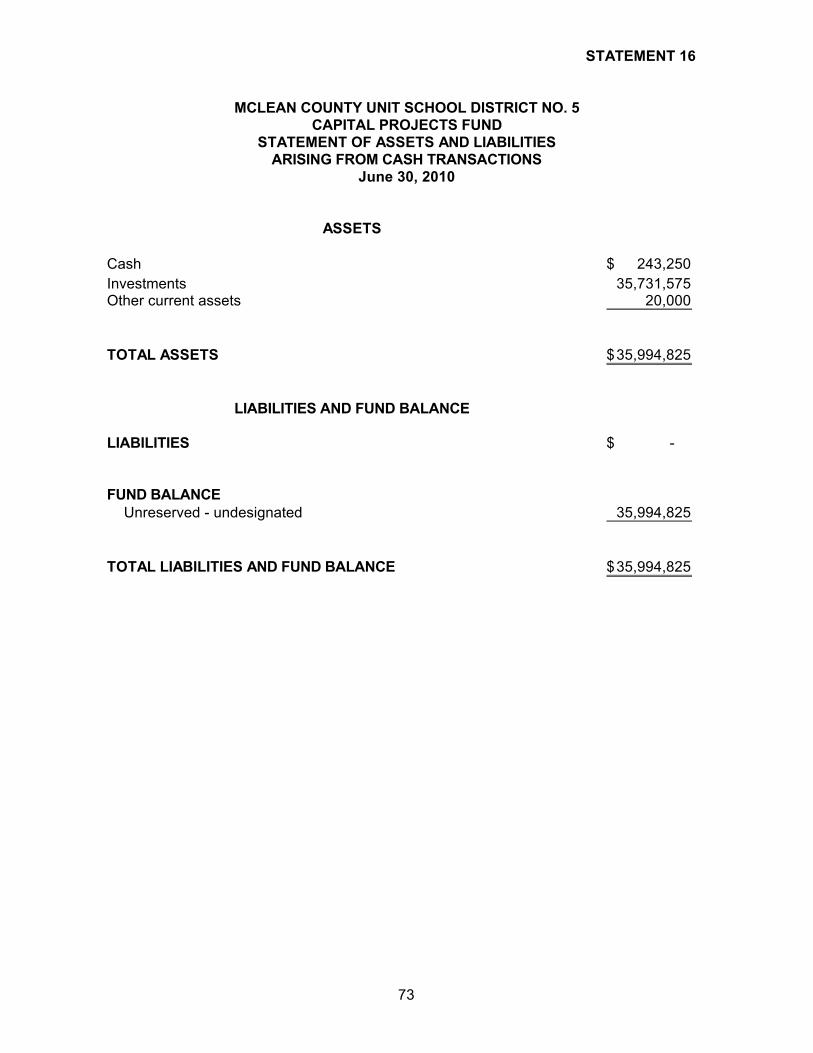

Capital Projects Fund:Statement of Assets and Liabilities Arising From Cash

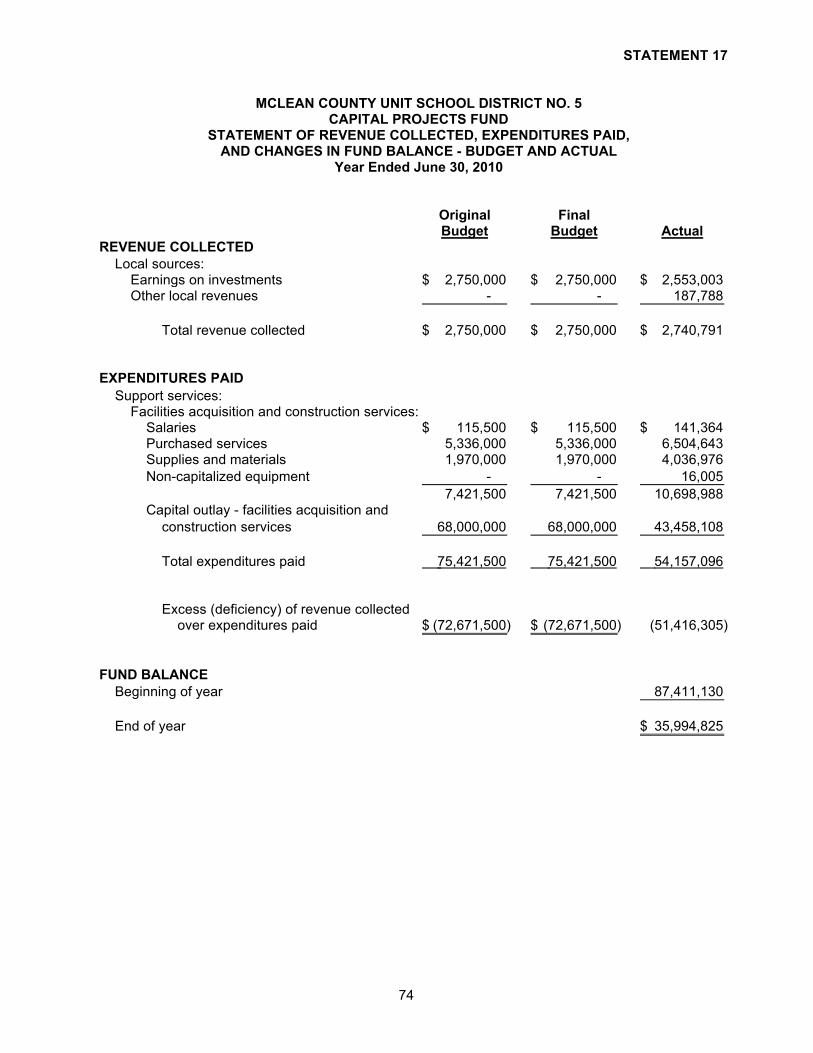

Transactions ............................................................................. 16 73Statement of Revenue Collected, Expenditures Paid,

and Changes in Fund Balance - Budget and Actual .................. 17 74

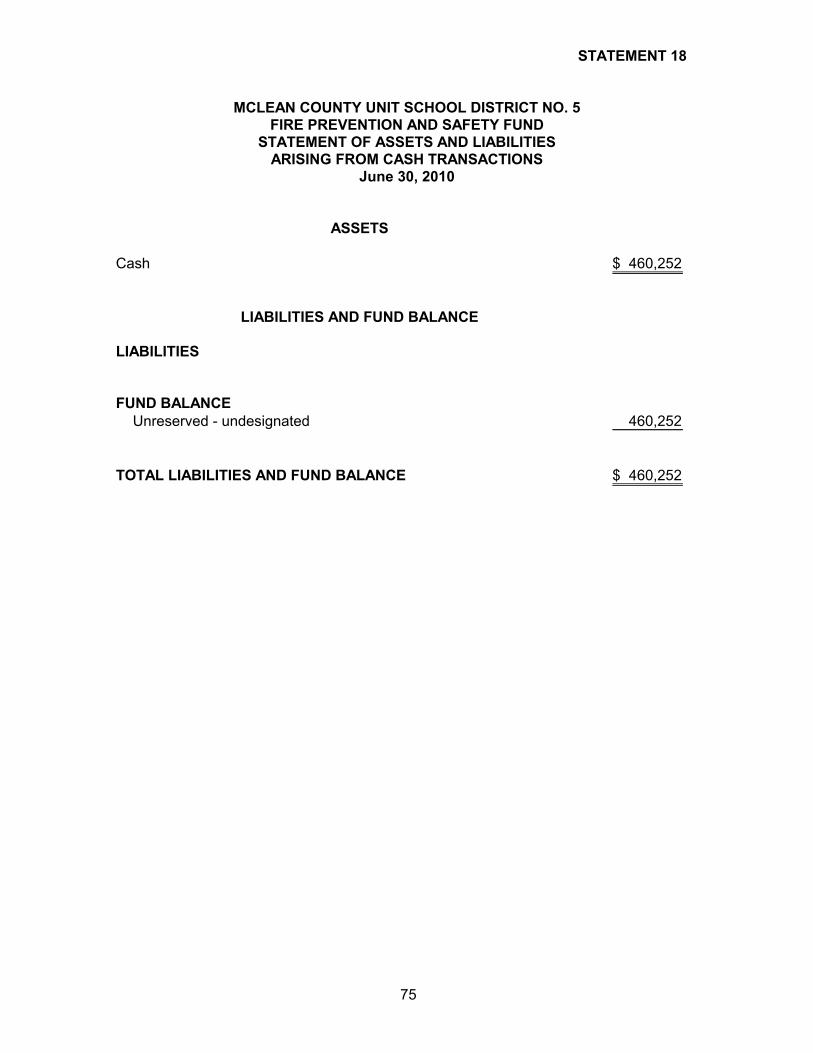

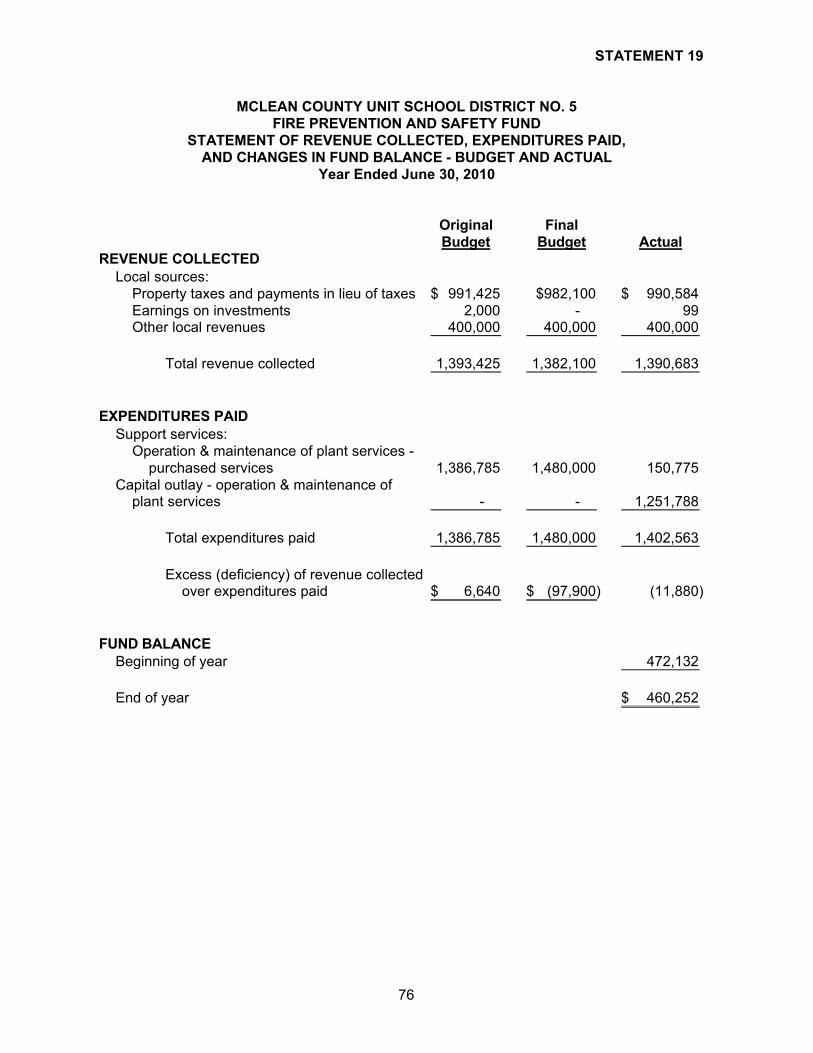

Fire Prevention and Safety Fund:Statement of Assets and Liabilities Arising From Cash

Transactions ............................................................................. 18 75Statement of Revenue Collected, Expenditures Paid,

and Changes in Fund Balance - Budget and Actual .................. 19 76

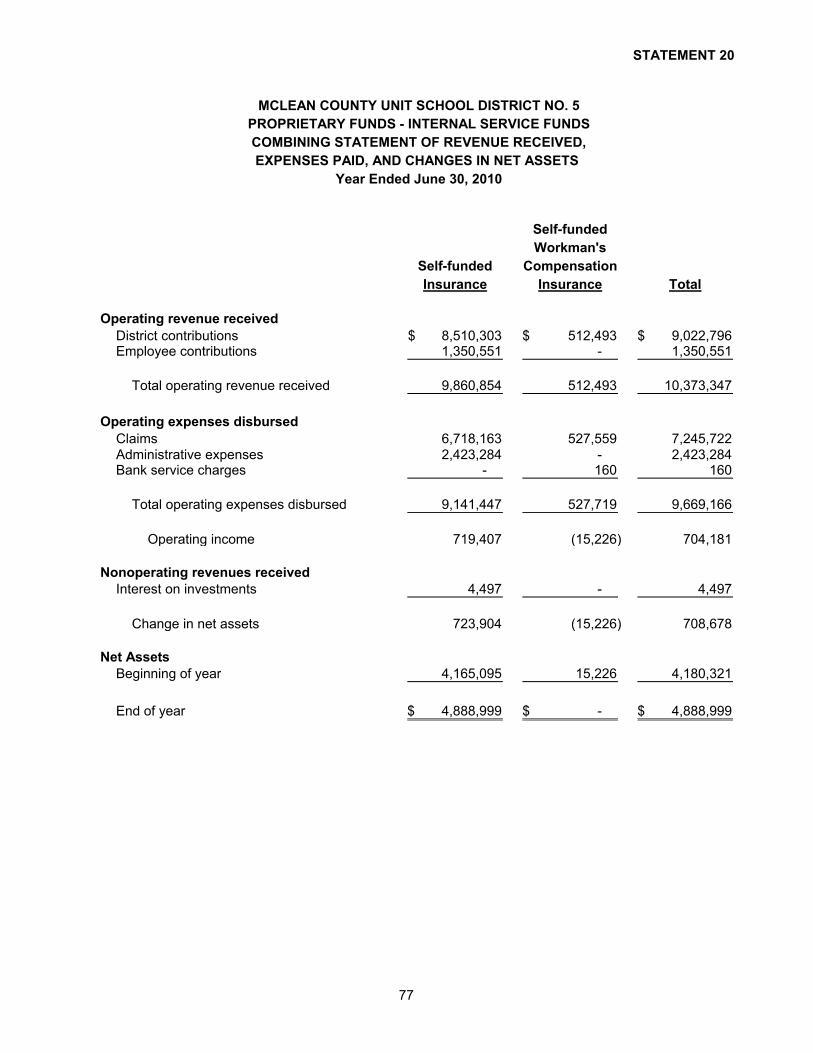

Proprietary Fund - Internal Service FundsCombining Statement of Revenue Received, Expenses Paid,

and Changes in Net Assets…………......................................... 20 77

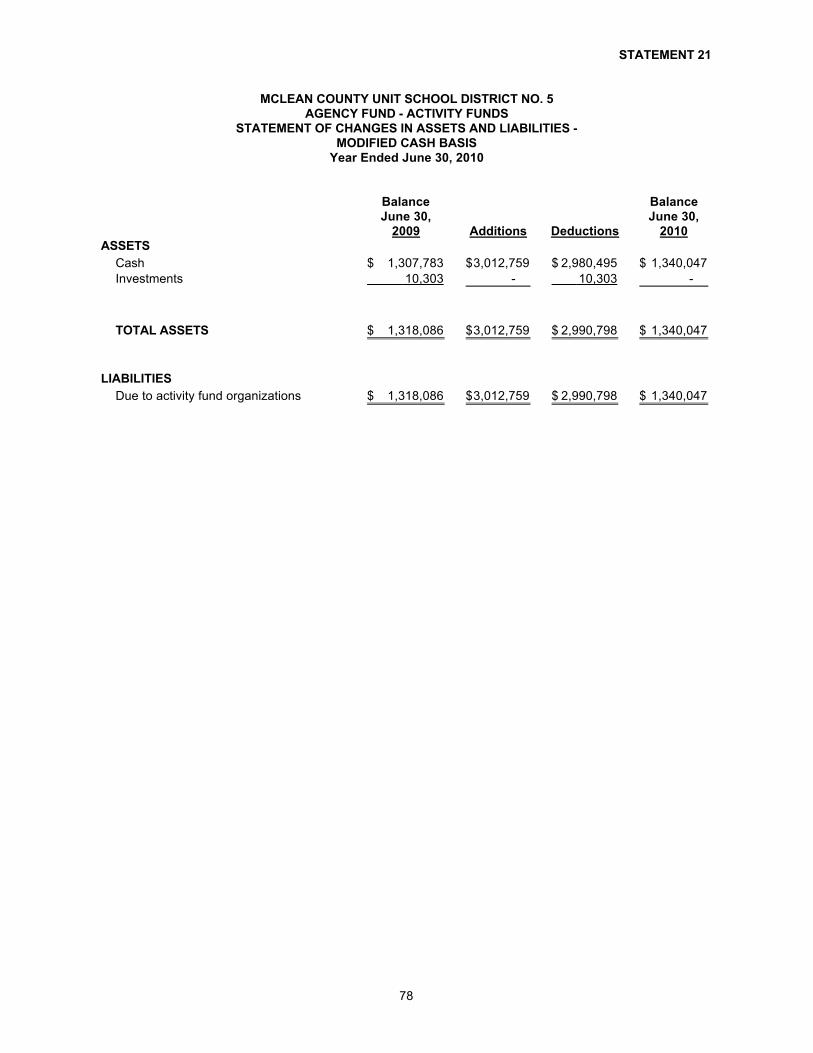

Agency Fund - Activity Funds:Statement of Changes in Assets and Liabilities - Modified

Cash Basis................................................................................ 21 78

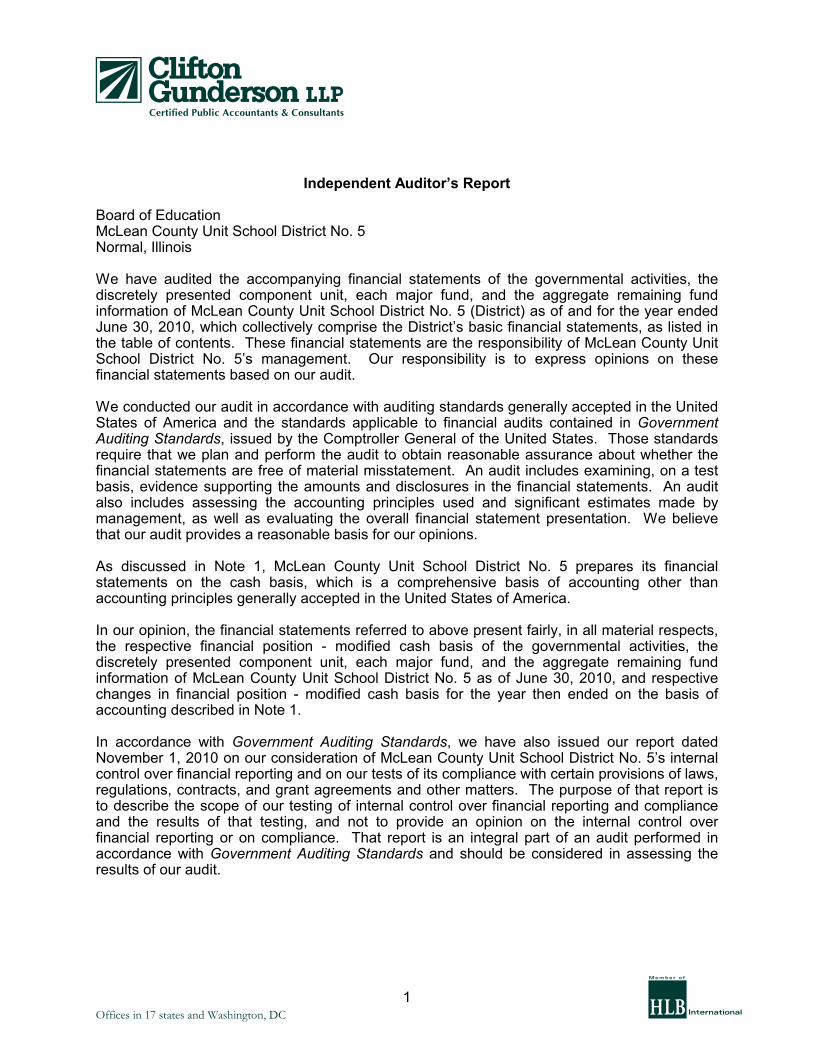

1

Independent Auditor’s Report

Board of EducationMcLean County Unit School District No. 5Normal, Illinois

We have audited the accompanying financial statements of the governmental activities, the discretely presented component unit, each major fund, and the aggregate remaining fund information of McLean County Unit School District No. 5 (District) as of and for the year ended June 30, 2010, which collectively comprise the District’s basic financial statements, as listed in the table of contents. These financial statements are the responsibility of McLean County Unit School District No. 5’s management. Our responsibility is to express opinions on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinions.

As discussed in Note 1, McLean County Unit School District No. 5 prepares its financial statements on the cash basis, which is a comprehensive basis of accounting other than accounting principles generally accepted in the United States of America.

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position - modified cash basis of the governmental activities, the discretely presented component unit, each major fund, and the aggregate remaining fund information of McLean County Unit School District No. 5 as of June 30, 2010, and respective changes in financial position - modified cash basis for the year then ended on the basis of accounting described in Note 1.

In accordance with Government Auditing Standards, we have also issued our report dated November 1, 2010 on our consideration of McLean County Unit School District No. 5’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

A1

Offices in 17 states and Washington, DC h

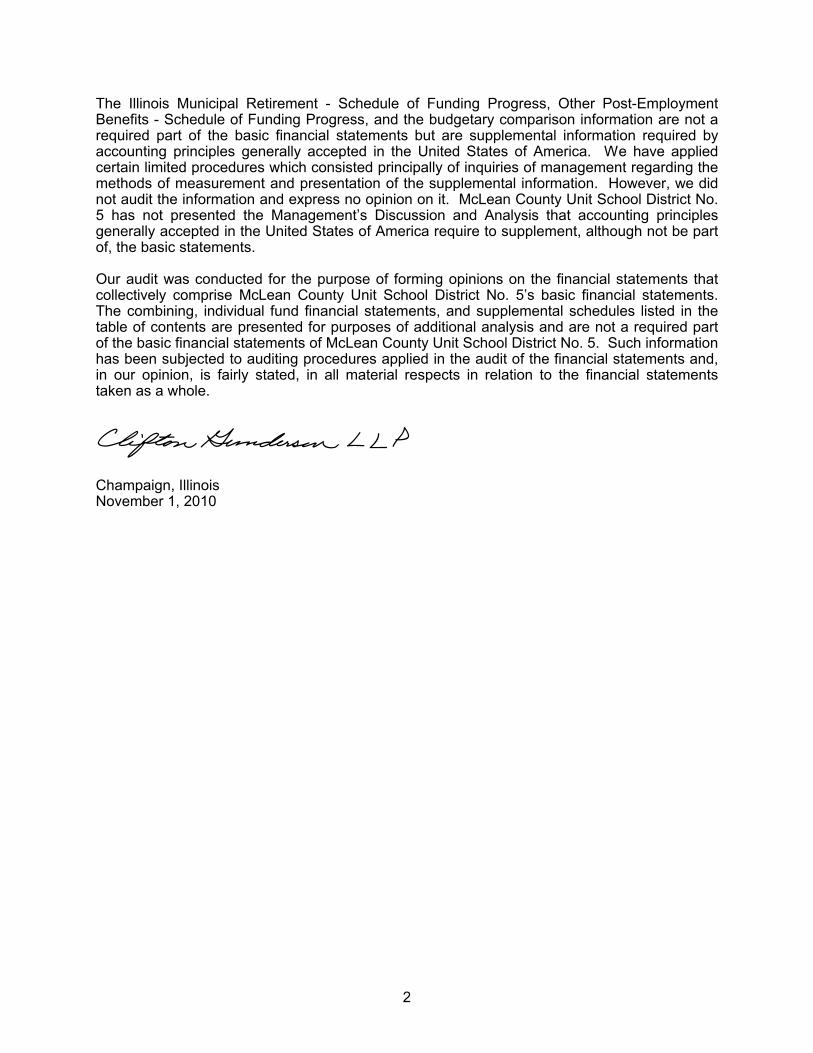

2

The Illinois Municipal Retirement - Schedule of Funding Progress, Other Post-Employment Benefits - Schedule of Funding Progress, and the budgetary comparison information are not a required part of the basic financial statements but are supplemental information required by accounting principles generally accepted in the United States of America. We have applied certain limited procedures which consisted principally of inquiries of management regarding the methods of measurement and presentation of the supplemental information. However, we did not audit the information and express no opinion on it. McLean County Unit School District No. 5 has not presented the Management’s Discussion and Analysis that accounting principles generally accepted in the United States of America require to supplement, although not be part of, the basic statements.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise McLean County Unit School District No. 5’s basic financial statements. The combining, individual fund financial statements, and supplemental schedules listed in the table of contents are presented for purposes of additional analysis and are not a required part of the basic financial statements of McLean County Unit School District No. 5. Such information has been subjected to auditing procedures applied in the audit of the financial statements and, in our opinion, is fairly stated, in all material respects in relation to the financial statements taken as a whole.

Champaign, IllinoisNovember 1, 2010

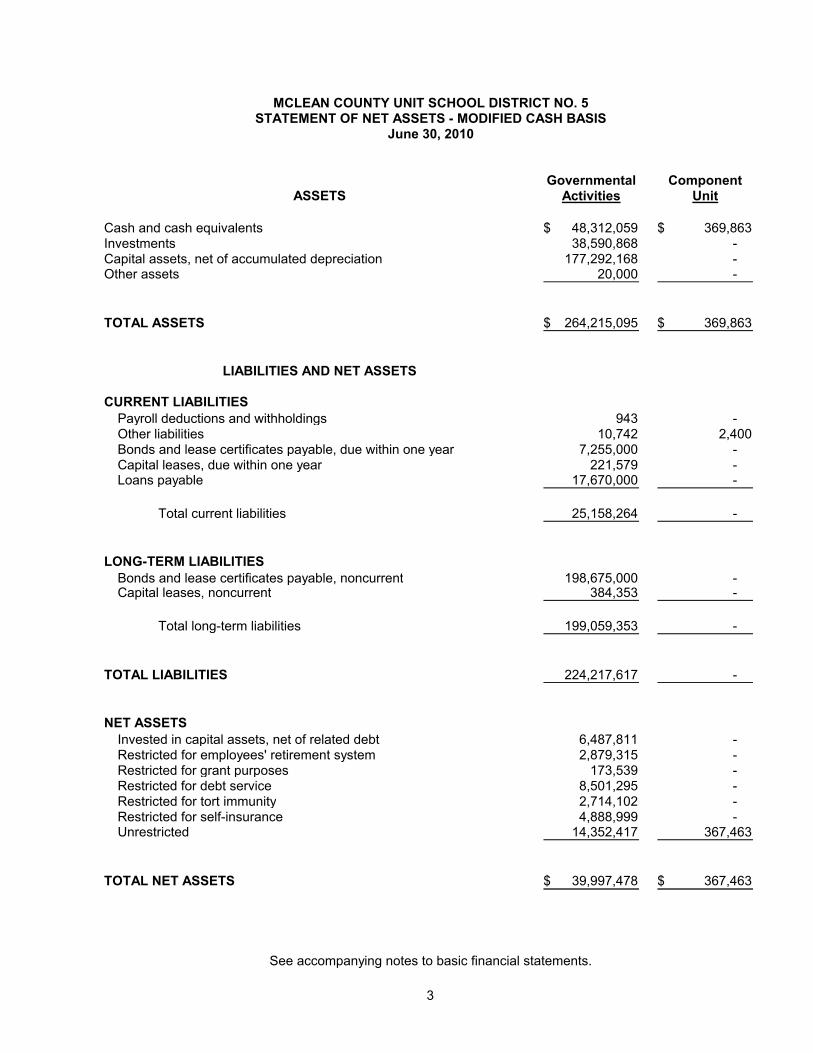

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5STATEMENT OF NET ASSETS - MODIFIED CASH BASIS

June 30, 2010

Governmental ComponentActivities Unit

Cash and cash equivalents 48,312,059$ 369,863$ Investments 38,590,868 - Capital assets, net of accumulated depreciation 177,292,168 - Other assets 20,000 -

TOTAL ASSETS 264,215,095$ 369,863$

LIABILITIES AND NET ASSETS

CURRENT LIABILITIES

Payroll deductions and withholdings 943 - Other liabilities 10,742 2,400 Bonds and lease certificates payable, due within one year 7,255,000 - Capital leases, due within one year 221,579 - Loans payable 17,670,000 -

Total current liabilities 25,158,264 -

LONG-TERM LIABILITIES

Bonds and lease certificates payable, noncurrent 198,675,000 - Capital leases, noncurrent 384,353 -

Total long-term liabilities 199,059,353 -

TOTAL LIABILITIES 224,217,617 -

NET ASSETS

Invested in capital assets, net of related debt 6,487,811 - Restricted for employees' retirement system 2,879,315 - Restricted for grant purposes 173,539 - Restricted for debt service 8,501,295 - Restricted for tort immunity 2,714,102 - Restricted for self-insurance 4,888,999 - Unrestricted 14,352,417 367,463

TOTAL NET ASSETS 39,997,478$ 367,463$

ASSETS

See accompanying notes to basic financial statements.

3

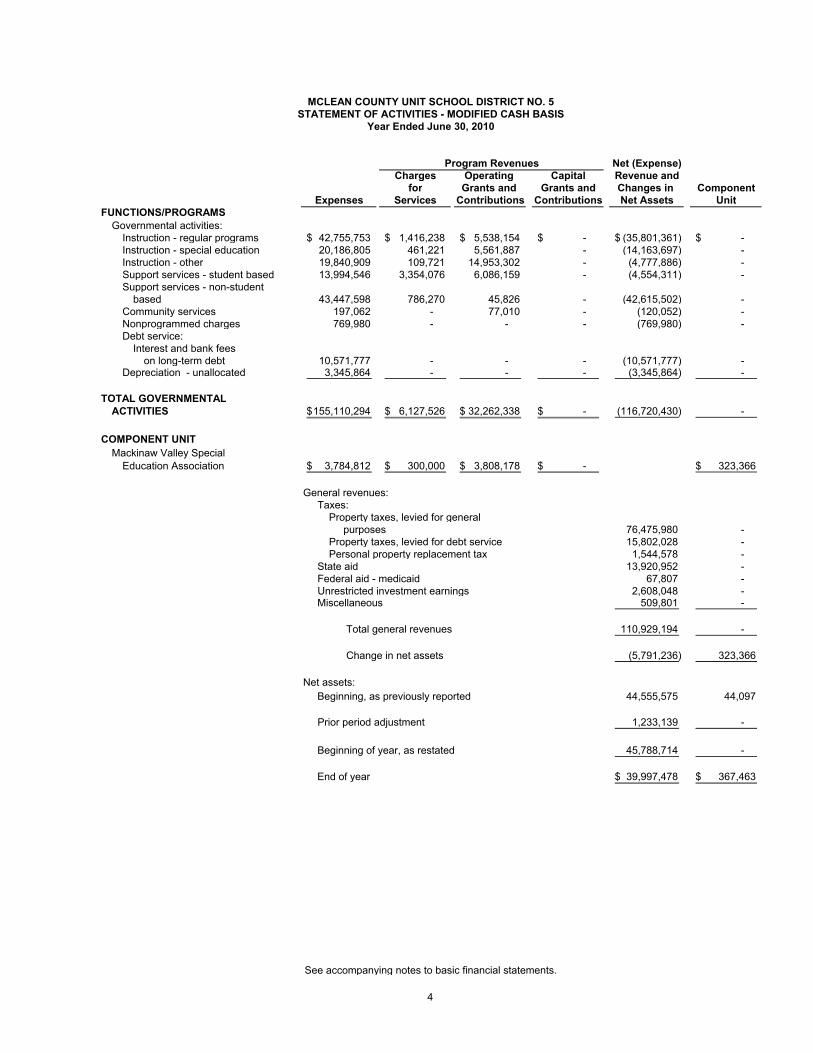

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5STATEMENT OF ACTIVITIES - MODIFIED CASH BASIS

Year Ended June 30, 2010

Net (Expense)Charges Operating Capital Revenue and

for Grants and Grants and Changes in ComponentExpenses Services Contributions Contributions Net Assets Unit

FUNCTIONS/PROGRAMS

Governmental activities:Instruction - regular programs 42,755,753$ 1,416,238$ 5,538,154$ -$ (35,801,361)$ -$ Instruction - special education 20,186,805 461,221 5,561,887 - (14,163,697) - Instruction - other 19,840,909 109,721 14,953,302 - (4,777,886) - Support services - student based 13,994,546 3,354,076 6,086,159 - (4,554,311) - Support services - non-student

based 43,447,598 786,270 45,826 - (42,615,502) - Community services 197,062 - 77,010 - (120,052) - Nonprogrammed charges 769,980 - - - (769,980) - Debt service:

Interest and bank feeson long-term debt 10,571,777 - - - (10,571,777) -

Depreciation - unallocated 3,345,864 - - - (3,345,864) -

TOTAL GOVERNMENTALACTIVITIES 155,110,294$ 6,127,526$ 32,262,338$ -$ (116,720,430) -

COMPONENT UNIT

Mackinaw Valley SpecialEducation Association 3,784,812$ 300,000$ 3,808,178$ -$ 323,366$

General revenues: Taxes: Property taxes, levied for general purposes 76,475,980 - Property taxes, levied for debt service 15,802,028 - Personal property replacement tax 1,544,578 - State aid 13,920,952 - Federal aid - medicaid 67,807 - Unrestricted investment earnings 2,608,048 - Miscellaneous 509,801 -

Total general revenues 110,929,194 -

Change in net assets (5,791,236) 323,366

Net assets:

Beginning, as previously reported 44,555,575 44,097

Prior period adjustment 1,233,139 -

Beginning of year, as restated 45,788,714 -

End of year 39,997,478$ 367,463$

See accompanying notes to basic financial statements.

Program Revenues

4

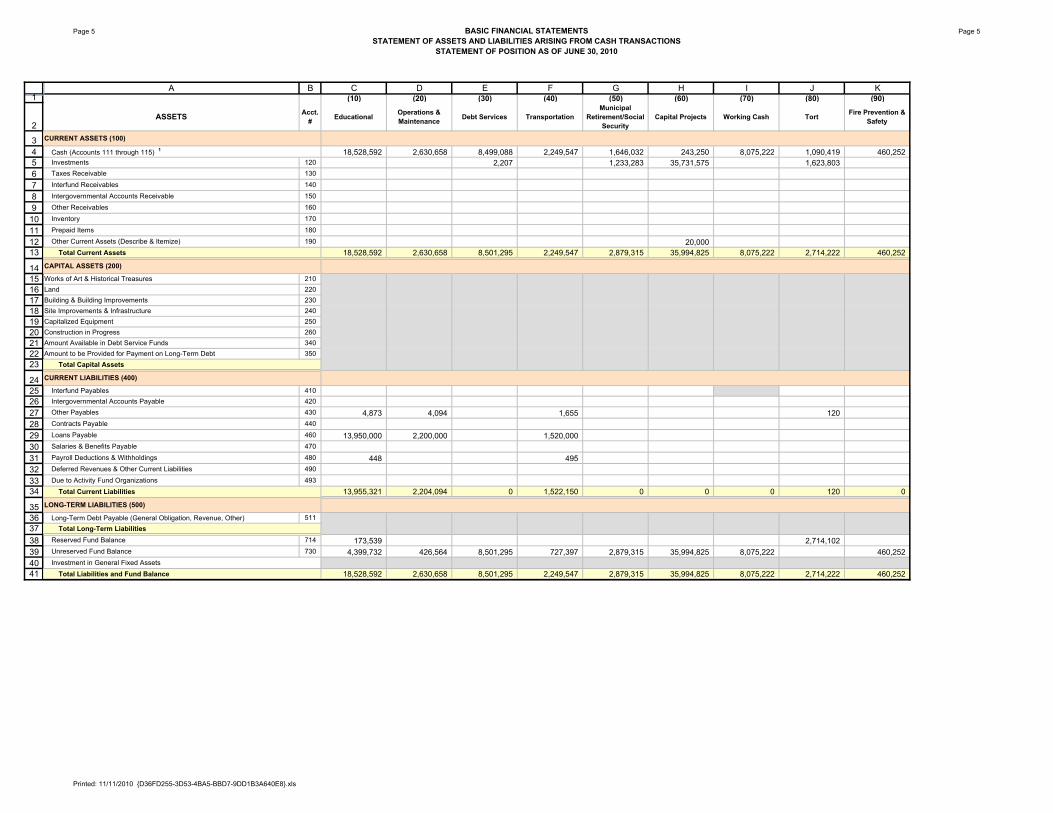

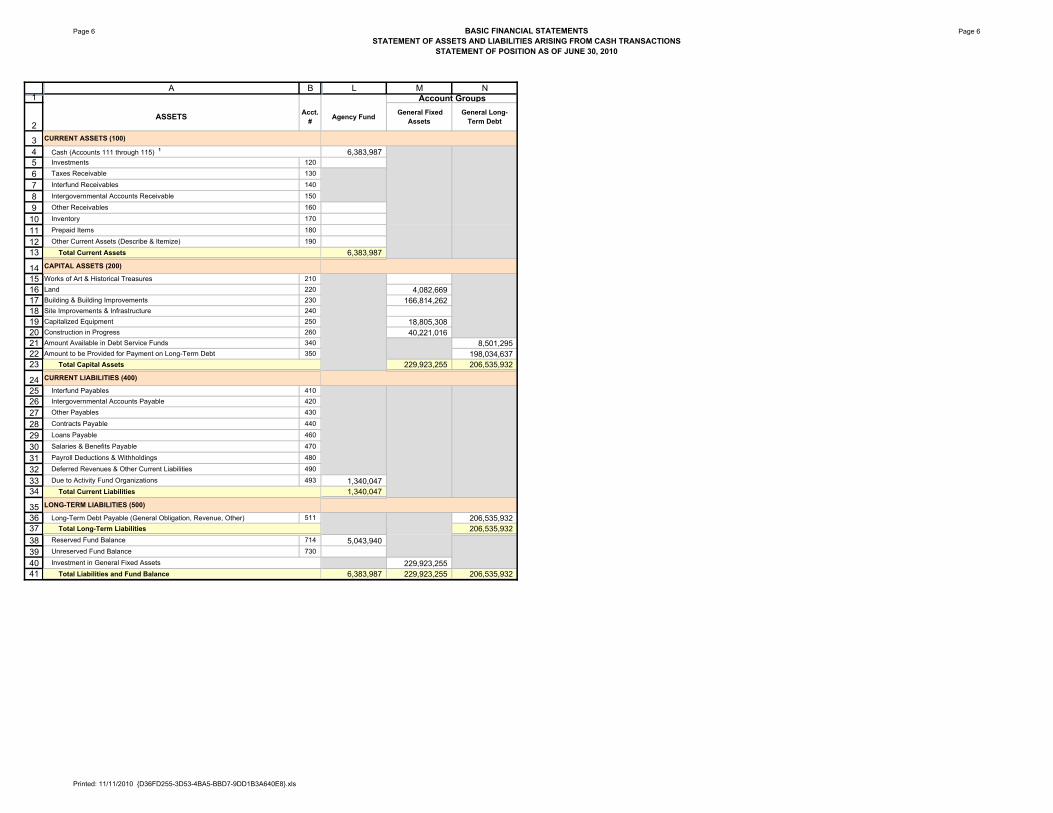

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5STATEMENT OF ASSETS AND LIABILITIES

ARISING FROM CASH TRANSACTIONSGOVERNMENTAL FUNDS

June 30, 2010

GeneralFund

Cash and cash equivalents 22,249,669$ Investments 1,623,803 Other assets -

TOTAL ASSETS 23,873,472$

LIABILITIES

Other liabilities 9,087$

Payroll deductions and withholdings 448 Loans payable 16,150,000

TOTAL LIABILITIES 16,159,535

FUND BALANCESReserved for employee retirement system - Reserved for educational fund 173,539 Reserved for debt service - Reserved for tort immunity 2,714,102 Unreserved:

Undesignated, reported in:General Fund 4,826,296 Transportation Fund - Working Cash Fund - Capital Projects Funds -

Total fund balances 7,713,937

TOTAL LIABILITIES AND FUND BALANCES 23,873,472$

ASSETS

LIABILITIES AND FUND BALANCES

5

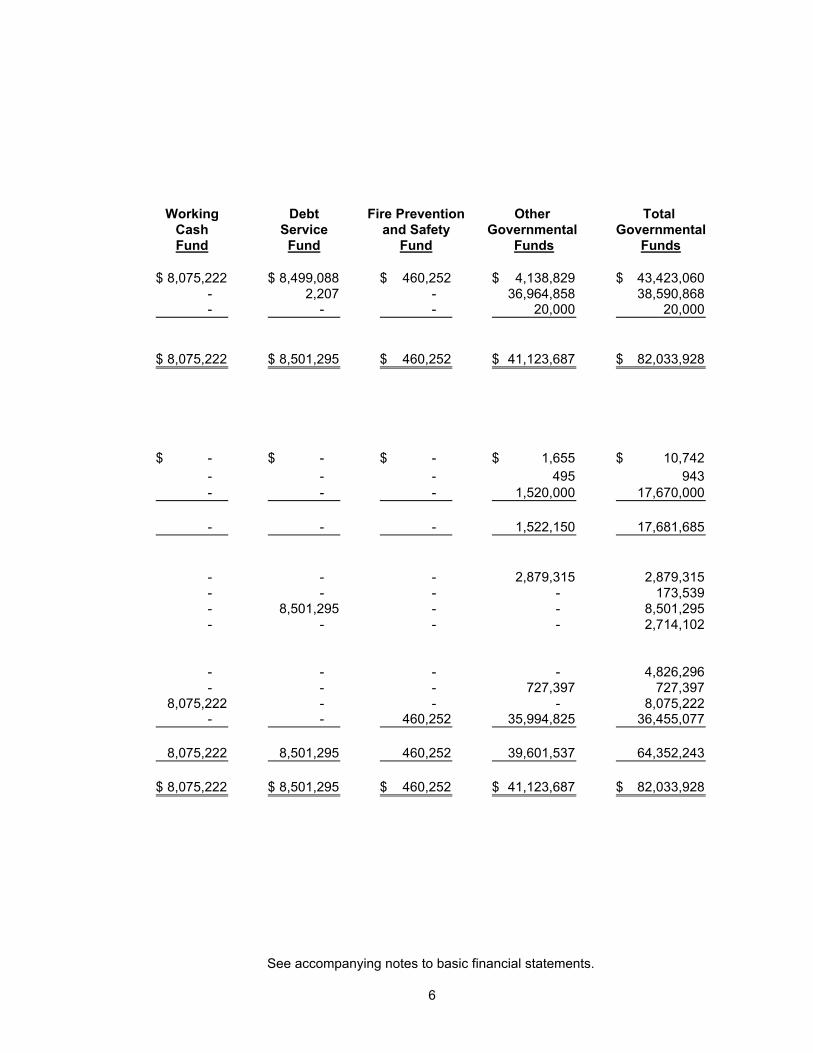

Working Debt Fire Prevention Other Total Cash Service and Safety Governmental GovernmentalFund Fund Fund Funds Funds

8,075,222$ 8,499,088$ 460,252$ 4,138,829$ 43,423,060$ - 2,207 - 36,964,858 38,590,868 - - - 20,000 20,000

8,075,222$ 8,501,295$ 460,252$ 41,123,687$ 82,033,928$

-$ -$ -$ 1,655$ 10,742$

- - - 495 943 - - - 1,520,000 17,670,000

- - - 1,522,150 17,681,685

- - - 2,879,315 2,879,315 - - - - 173,539 - 8,501,295 - - 8,501,295 - - - - 2,714,102

- - - - 4,826,296 - - - 727,397 727,397

8,075,222 - - - 8,075,222 - - 460,252 35,994,825 36,455,077

8,075,222 8,501,295 460,252 39,601,537 64,352,243

8,075,222$ 8,501,295$ 460,252$ 41,123,687$ 82,033,928$

See accompanying notes to basic financial statements.

6

THIS PAGE INTENTIONALLY LEFT BLANK

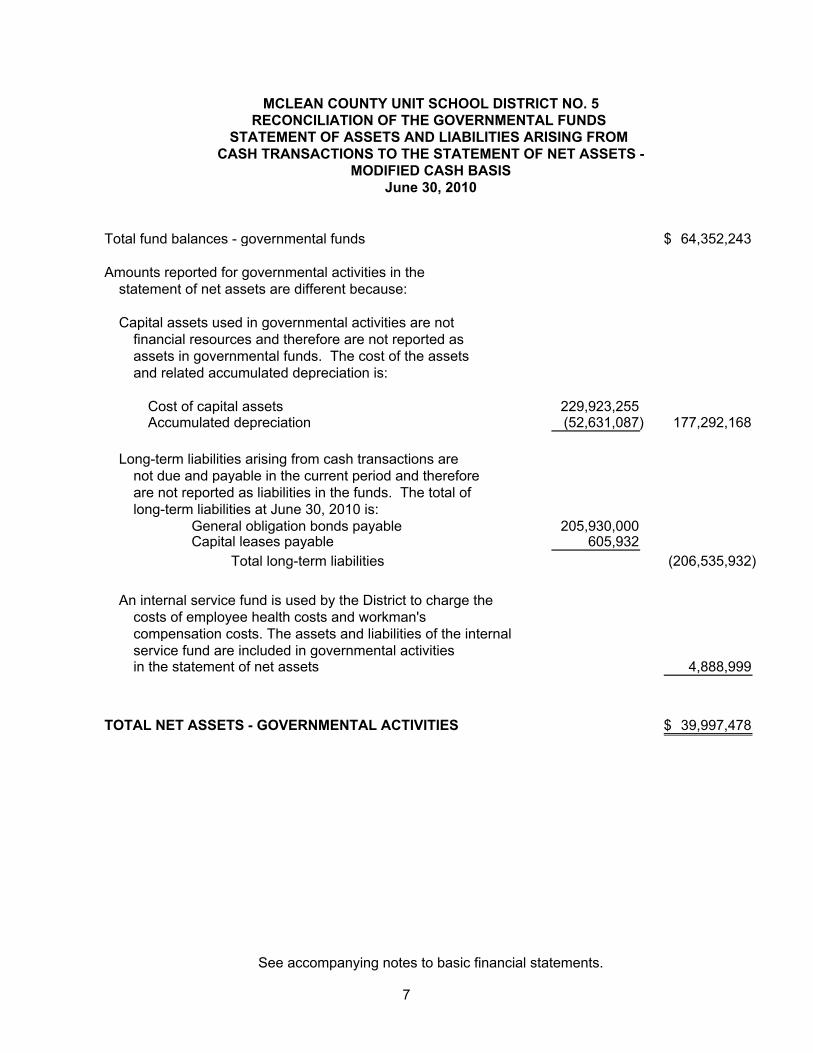

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5RECONCILIATION OF THE GOVERNMENTAL FUNDS

STATEMENT OF ASSETS AND LIABILITIES ARISING FROM CASH TRANSACTIONS TO THE STATEMENT OF NET ASSETS -

MODIFIED CASH BASISJune 30, 2010

Total fund balances - governmental funds 64,352,243$

Amounts reported for governmental activities in thestatement of net assets are different because:

Capital assets used in governmental activities are notfinancial resources and therefore are not reported asassets in governmental funds. The cost of the assetsand related accumulated depreciation is:

Cost of capital assets 229,923,255 Accumulated depreciation (52,631,087) 177,292,168

Long-term liabilities arising from cash transactions are not due and payable in the current period and therefore are not reported as liabilities in the funds. The total oflong-term liabilities at June 30, 2010 is:

General obligation bonds payable 205,930,000 Capital leases payable 605,932

Total long-term liabilities (206,535,932)

An internal service fund is used by the District to charge the costs of employee health costs and workman's compensation costs. The assets and liabilities of the internal service fund are included in governmental activitiesin the statement of net assets 4,888,999

TOTAL NET ASSETS - GOVERNMENTAL ACTIVITIES 39,997,478$

See accompanying notes to basic financial statements.

7

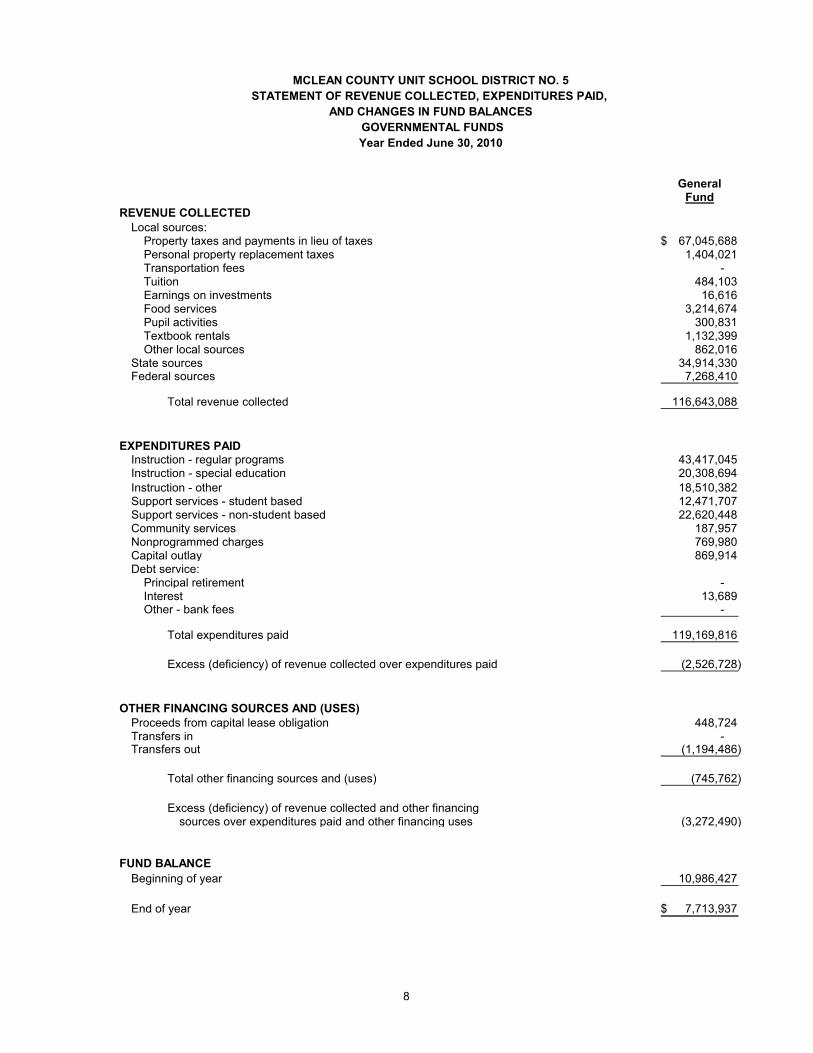

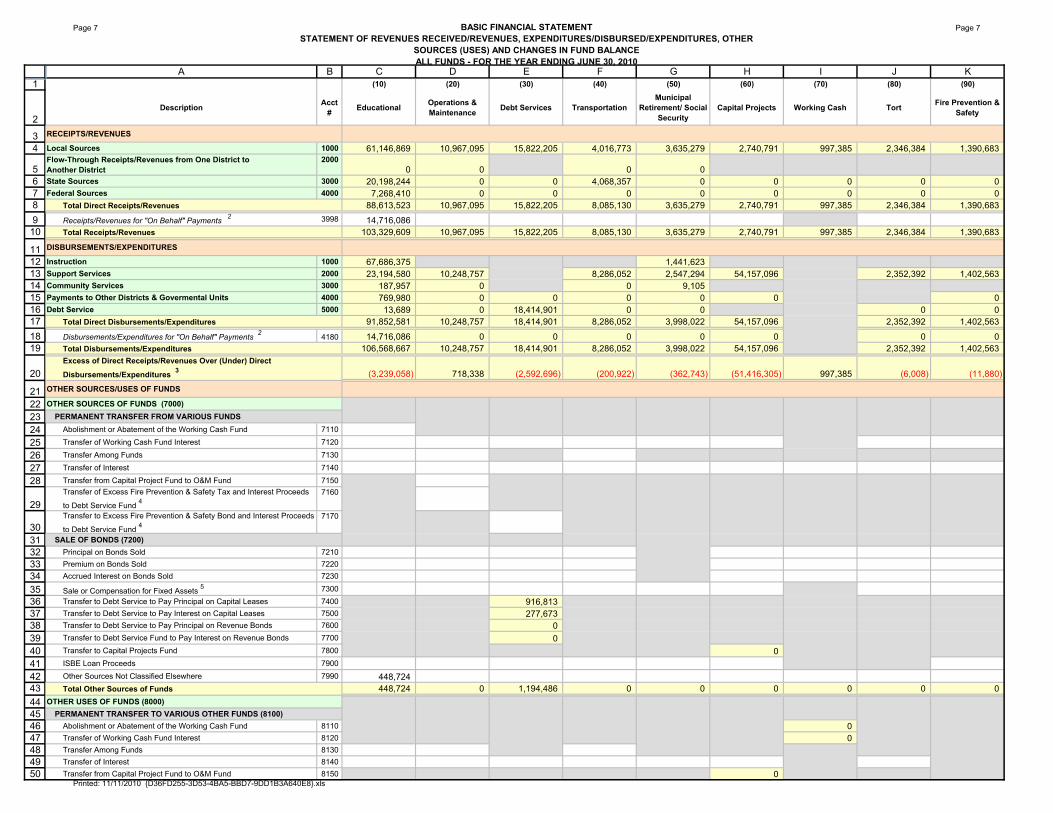

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5

STATEMENT OF REVENUE COLLECTED, EXPENDITURES PAID,

AND CHANGES IN FUND BALANCES

GOVERNMENTAL FUNDS

Year Ended June 30, 2010

GeneralFund

REVENUE COLLECTEDLocal sources:

Property taxes and payments in lieu of taxes 67,045,688$ Personal property replacement taxes 1,404,021 Transportation fees - Tuition 484,103 Earnings on investments 16,616 Food services 3,214,674 Pupil activities 300,831 Textbook rentals 1,132,399 Other local sources 862,016

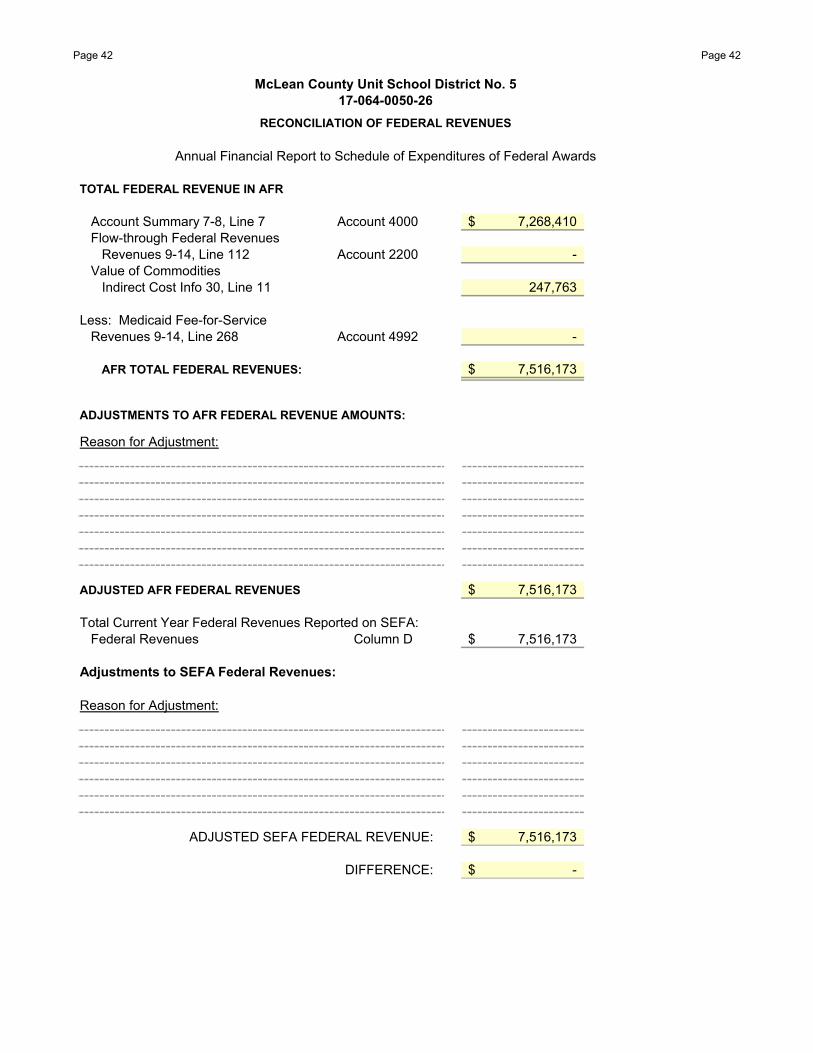

State sources 34,914,330 Federal sources 7,268,410

Total revenue collected 116,643,088

EXPENDITURES PAIDInstruction - regular programs 43,417,045 Instruction - special education 20,308,694 Instruction - other 18,510,382 Support services - student based 12,471,707 Support services - non-student based 22,620,448 Community services 187,957 Nonprogrammed charges 769,980 Capital outlay 869,914 Debt service:

Principal retirement - Interest 13,689 Other - bank fees -

Total expenditures paid 119,169,816

Excess (deficiency) of revenue collected over expenditures paid (2,526,728)

OTHER FINANCING SOURCES AND (USES)Proceeds from capital lease obligation 448,724 Transfers in - Transfers out (1,194,486)

Total other financing sources and (uses) (745,762)

Excess (deficiency) of revenue collected and other financing sources over expenditures paid and other financing uses (3,272,490)

FUND BALANCE

Beginning of year 10,986,427

End of year 7,713,937$

8

Working Debt Fire Prevention Other TotalCash Service and Safety Governmental GovernmentalFund Fund Fund Funds Funds

990,584$ 15,802,028$ 990,584$ 7,449,124$ 92,278,008$ - - - 140,557 1,544,578 - - - 46,471 46,471 - - - - 484,103

6,801 20,177 99 2,559,858 2,603,551 - - - - 3,214,674 - - - - 300,831 - - - - 1,132,399 - - 400,000 196,833 1,458,849 - - - 4,068,357 38,982,687 - - - - 7,268,410

997,385 15,822,205 1,390,683 14,461,200 149,314,561

- - - - 43,417,045 - - - - 20,308,694 - - - 1,441,623 19,952,005 - - - - 12,471,707 - - 150,775 20,812,138 43,583,361 - - - 9,105 197,062 - - - - 769,980 - - 1,251,788 44,178,304 46,300,006

- 7,856,813 - - 7,856,813 - 10,552,012 - - 10,565,701 - 6,076 - - 6,076

- 18,414,901 1,402,563 66,441,170 205,428,450

997,385 (2,592,696) (11,880) (51,979,970) (56,113,889)

- - - - 448,724 - 1,194,486 - - 1,194,486 - - - - (1,194,486)

- 1,194,486 - - 448,724

997,385 (1,398,210) (11,880) (51,979,970) (55,665,165)

7,077,837 9,899,505 472,132 91,581,507 120,017,408

8,075,222$ 8,501,295$ 460,252$ 39,601,537$ 64,352,243$

See accompanying notes to basic financial statements.

9

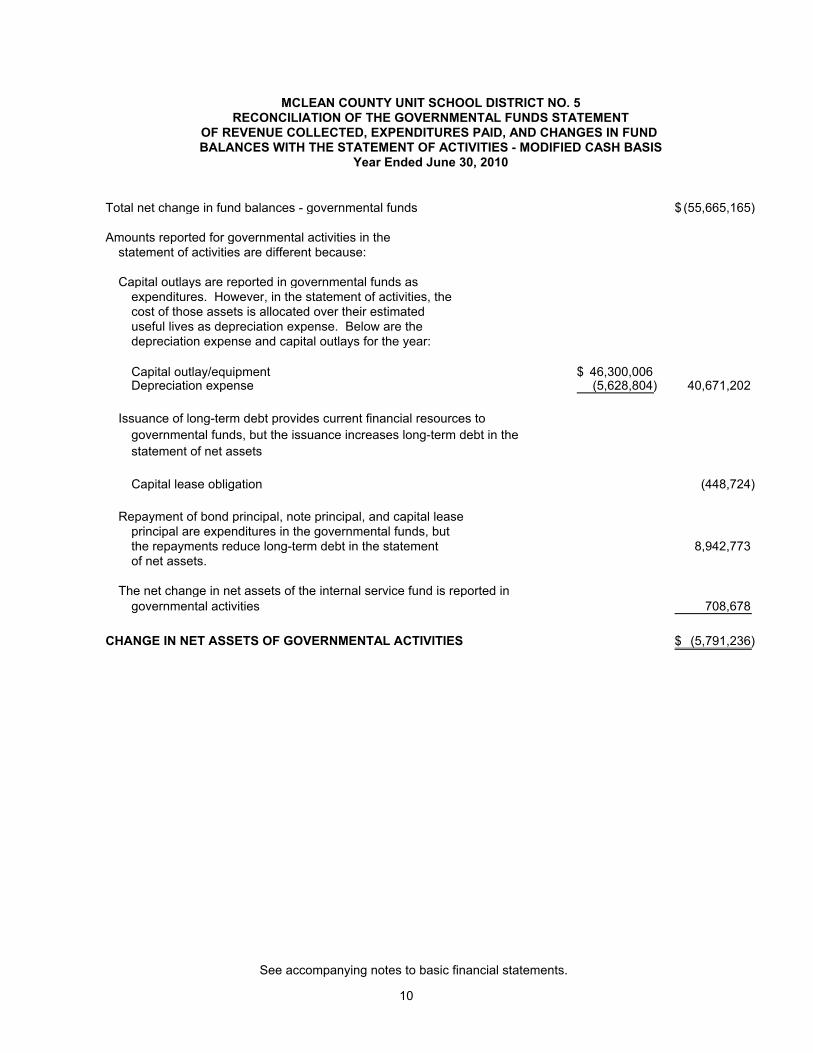

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5RECONCILIATION OF THE GOVERNMENTAL FUNDS STATEMENT

OF REVENUE COLLECTED, EXPENDITURES PAID, AND CHANGES IN FUND BALANCES WITH THE STATEMENT OF ACTIVITIES - MODIFIED CASH BASIS

Year Ended June 30, 2010

Total net change in fund balances - governmental funds (55,665,165)$

Amounts reported for governmental activities in thestatement of activities are different because:

Capital outlays are reported in governmental funds asexpenditures. However, in the statement of activities, thecost of those assets is allocated over their estimated useful lives as depreciation expense. Below are thedepreciation expense and capital outlays for the year:

Capital outlay/equipment 46,300,006$ Depreciation expense (5,628,804) 40,671,202

Issuance of long-term debt provides current financial resources to

governmental funds, but the issuance increases long-term debt in the

statement of net assets

Capital lease obligation (448,724)

Repayment of bond principal, note principal, and capital lease principal are expenditures in the governmental funds, butthe repayments reduce long-term debt in the statement 8,942,773 of net assets.

The net change in net assets of the internal service fund is reported in governmental activities 708,678

CHANGE IN NET ASSETS OF GOVERNMENTAL ACTIVITIES (5,791,236)$

See accompanying notes to basic financial statements.

10

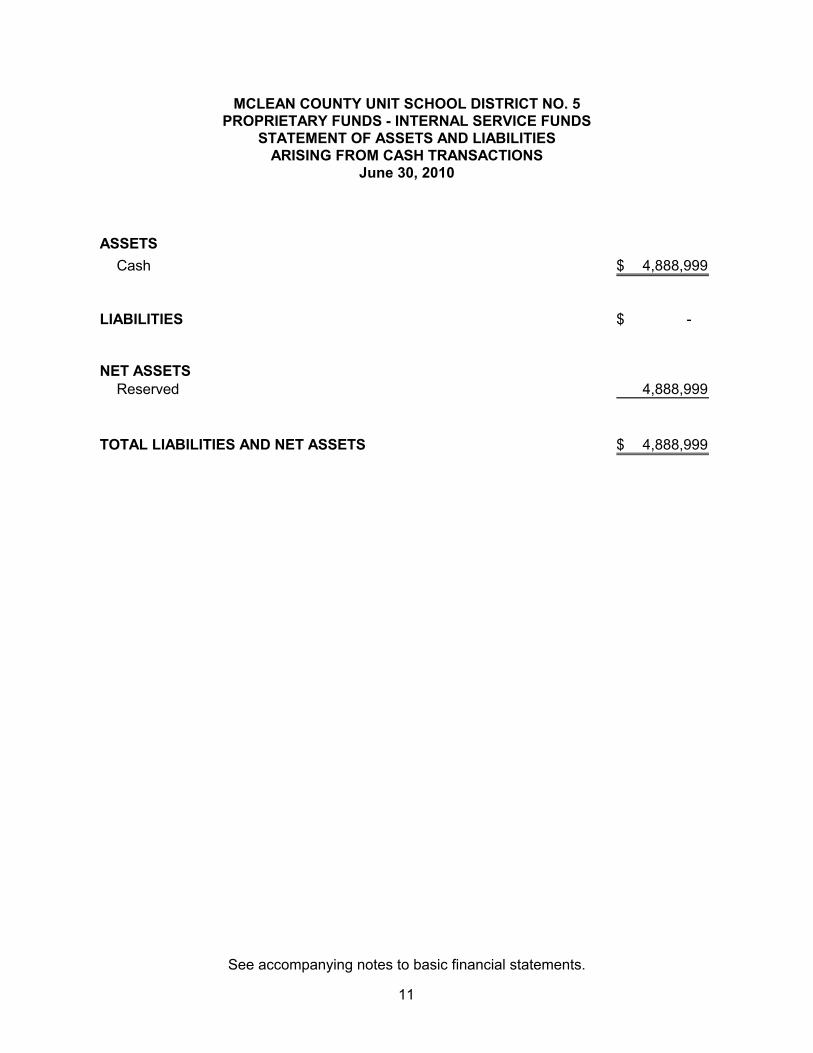

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5PROPRIETARY FUNDS - INTERNAL SERVICE FUNDS

June 30, 2010

ASSETS

Cash 4,888,999$

LIABILITIES -$

NET ASSETSReserved 4,888,999

TOTAL LIABILITIES AND NET ASSETS 4,888,999$

See accompanying notes to basic financial statements.

STATEMENT OF ASSETS AND LIABILITIESARISING FROM CASH TRANSACTIONS

11

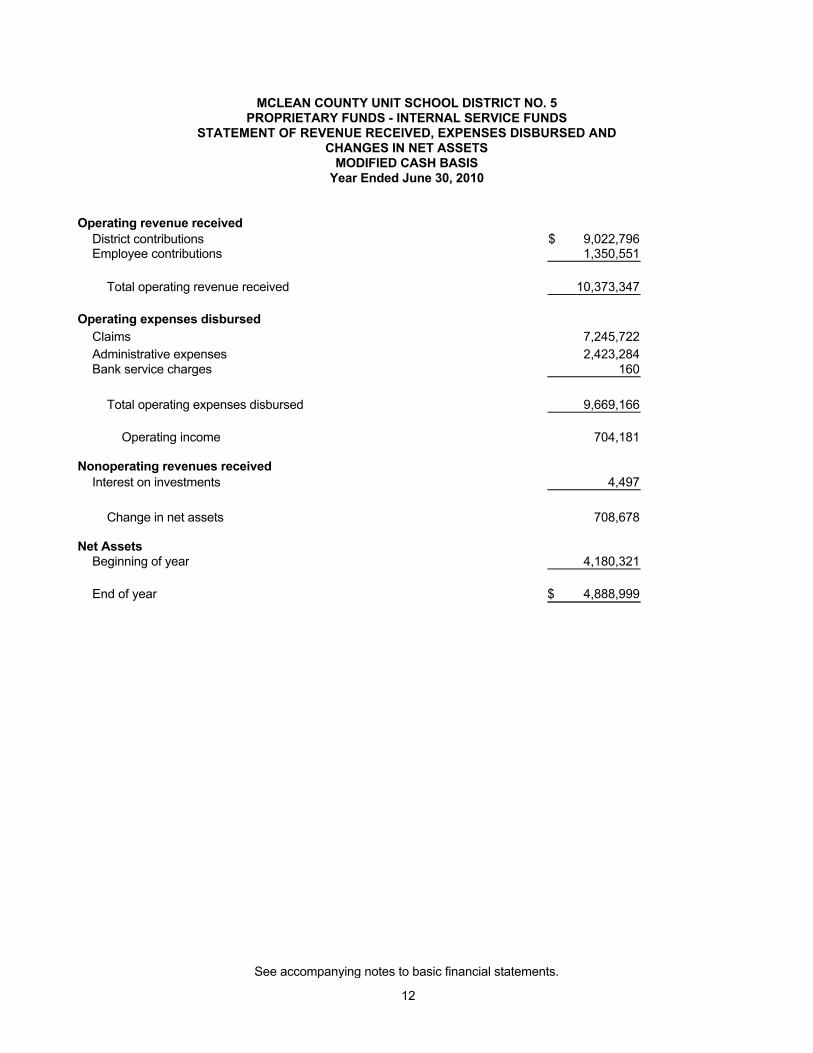

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5PROPRIETARY FUNDS - INTERNAL SERVICE FUNDS

STATEMENT OF REVENUE RECEIVED, EXPENSES DISBURSED ANDCHANGES IN NET ASSETS

MODIFIED CASH BASISYear Ended June 30, 2010

Operating revenue receivedDistrict contributions 9,022,796$ Employee contributions 1,350,551

Total operating revenue received 10,373,347

Operating expenses disbursed

Claims 7,245,722

Administrative expenses 2,423,284 Bank service charges 160

Total operating expenses disbursed 9,669,166

Operating income 704,181

Nonoperating revenues receivedInterest on investments 4,497

Change in net assets 708,678

Net AssetsBeginning of year 4,180,321

End of year 4,888,999$

See accompanying notes to basic financial statements.

12

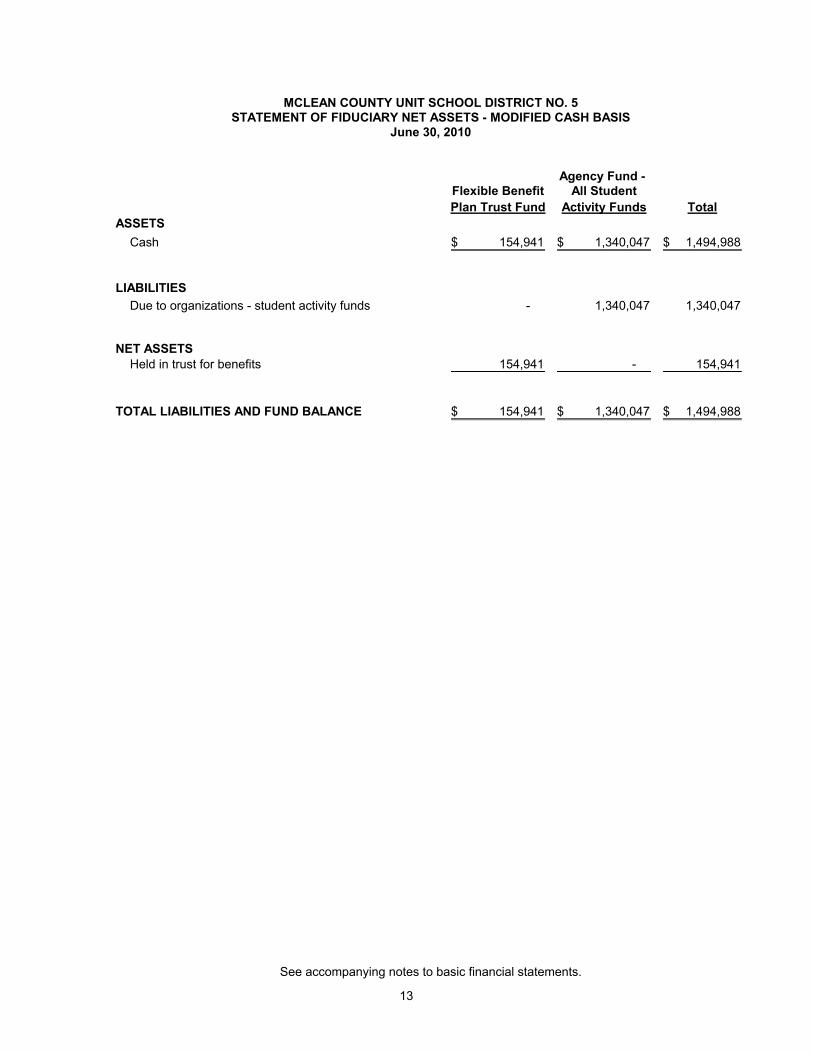

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5STATEMENT OF FIDUCIARY NET ASSETS - MODIFIED CASH BASIS

June 30, 2010

Agency Fund - Flexible Benefit All Student

Plan Trust Fund Activity Funds Total

ASSETS

Cash 154,941$ 1,340,047$ 1,494,988$

LIABILITIES

Due to organizations - student activity funds - 1,340,047 1,340,047

NET ASSETSHeld in trust for benefits 154,941 - 154,941

TOTAL LIABILITIES AND FUND BALANCE 154,941$ 1,340,047$ 1,494,988$

See accompanying notes to basic financial statements.

13

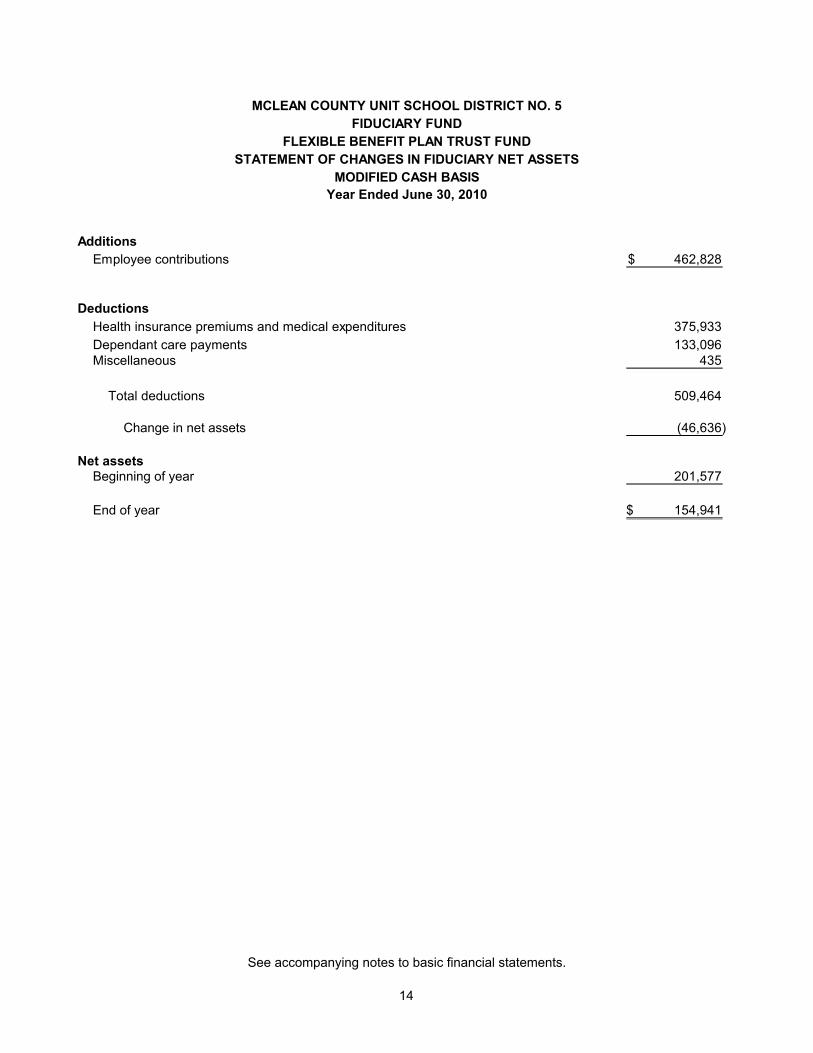

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5

FIDUCIARY FUND

FLEXIBLE BENEFIT PLAN TRUST FUND

STATEMENT OF CHANGES IN FIDUCIARY NET ASSETS

MODIFIED CASH BASIS

Year Ended June 30, 2010

Additions

Employee contributions 462,828$

Deductions

Health insurance premiums and medical expenditures 375,933

Dependant care payments 133,096 Miscellaneous 435

Total deductions 509,464

Change in net assets (46,636)

Net assetsBeginning of year 201,577

End of year 154,941$

See accompanying notes to basic financial statements.

14

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

15

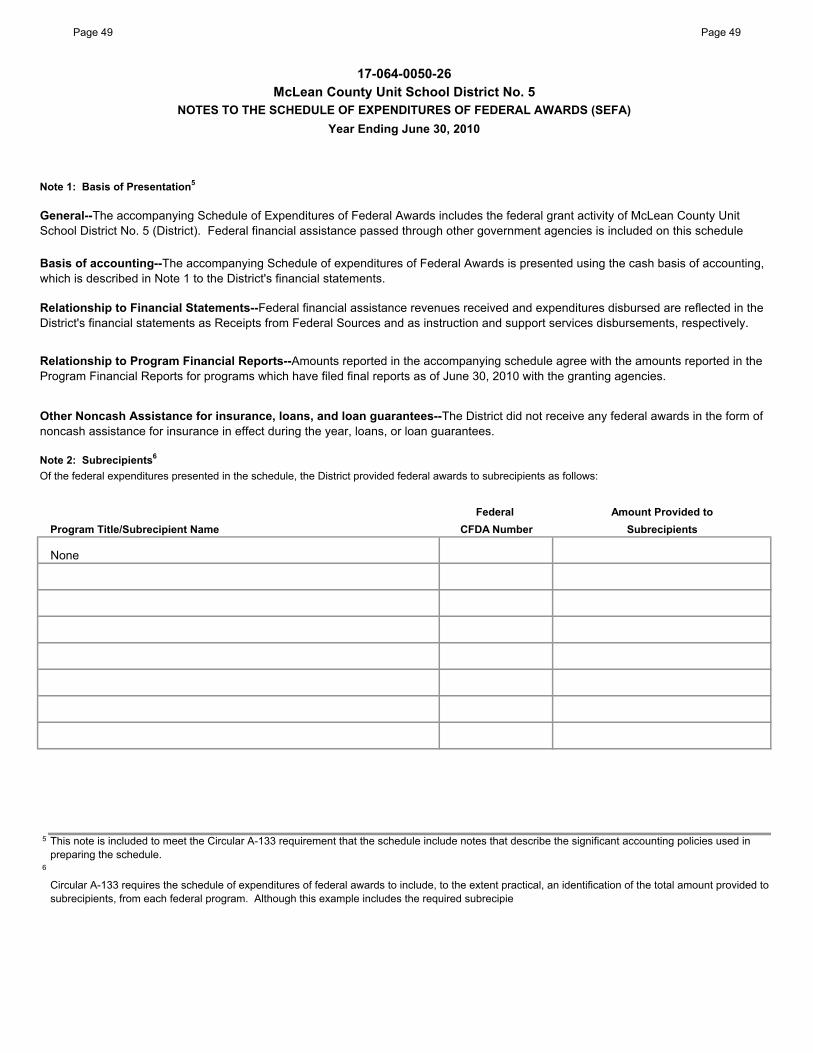

NOTE 1 - DESCRIPTION OF ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

McLean County Unit School District No. 5 (District) is a school district serving students in Normal, Illinois and the surrounding area. Revenues are substantially generated as a result of taxes assessed and allocated to the District and grants received from other state and federal governmental agencies. The District’s revenues are, therefore, primarily dependent upon the availability of funds at the state and federal level and the economy within its territorial boundaries. Industry within the territorial area is primarily retail and agricultural.

The following is a summary of the more significant accounting policies which the District applies:

(a) Financial Reporting Entity

In evaluating how to define the government, for financial reporting purposes, management has considered all potential component units. The decision to include a potential component unit in the reporting entity was made by applying the criteria set forth in the Codification of Government Accounting and Financial Reporting Standards, Section 2100. The financial reporting entity consists of (a) the primary government, McLean County Unit School District No. 5, which has a separately elected governing body, is legally separate and fiscally independent of other state and local governments, (b) organizations for which the primary government is financially accountable, and (c) other organizations for which the nature and significance of theirrelationship with the primary government are such that exclusion would cause the reporting entity’s financial statements to be misleading or incomplete.

Discretely Presented Component Unit

Mackinaw Valley Special Education Association (Association) is a component unit of the District. There is a joint agreement between the District and the Association and the District exercises significant influence over the assets, operations, and management of the Association.

The regulatory financial statements for the Association can be obtained from the District’s administrative office located at 1809 W. Hovey, Normal, IL 61761-4339.

There are no other component units of McLean County Unit School District No. 5 nor is McLean County Unit School District No. 5 dependent on any other entity.

(b) Government-Wide and Fund Financial Statements

The government-wide financial statements (i.e., the statement of net assets and the statement of activities) report information on all of the nonfiduciary activities of the District. For the most part, the effect of interfund activity has been removed from these statements.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

16

NOTE 1 - DESCRIPTION OF ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(b) Government-Wide and Fund Financial Statements (Continued)

The statement of activities demonstrates the degree to which the direct expenses of a given function or segment are offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function or segment. Program revenues include 1) charges to students, employees, and others who purchase, use, or directly benefit from goods, services, or privileges provided by a given function or segment and 2) grants and contributions that are restricted to meeting the operational or capital requirements of a particular function or segment.

Taxes and other items not properly included among program revenues are reported instead as general revenues.

Separate financial statements are provided for governmental funds and fiduciary funds, even though the latter are excluded from the government-wide financial statements. Major individual governmental funds are reported as separate columns in the fund financial statements.

(c) Measurement Focus, Basis of Accounting, and Financial Statement Presentation

The government-wide financial statements are reported using the cash basis of accounting as are the fiduciary fund financial statements. Capital assets and long-term debt are recognized on an economic resources measurement focus. Revenues are recorded when the cash is received and expenses are recorded when they are paid. Property taxes are recognized as revenues in the year for which they are levied for budgetary purposes.

Governmental fund financial statements are reported using the cash basis of accounting. Revenues are recognized when the cash is received. Expenditures are recorded when they are paid.

The District reports the following major governmental funds:

General Fund - The Educational, Operations and Maintenance and Tort Accountscomprise the general operating fund. It is used to account for all financial resources except those required to be accounted for in other funds.

The Educational Account includes the regular operations of the Educational Fund. All receipts that are not allocated by law or contractual agreement to some other fund are accounted for in this account. This account is used for regular operations, including educational costs, textbook costs, the food service department and certain other special programs, including many federal and state programs.

The Operations and Maintenance Account includes the cost of maintaining, improving, or repairing school buildings and property.

The Tort Account is used to account for resources to fund, and costs related to, tort immunity and tort judgment purposes.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

17

NOTE 1 - DESCRIPTION OF ORGANIZATION AND SUMMARY OF SIGNIFICANTACCOUNTING POLICIES (CONTINUED)

(c) Measurement Focus, Basis of Accounting, and Financial Statement Presentation(Continued)

Working Cash - The Working Cash Fund is used to account for financial resources held by the District which may be temporarily loaned to other funds.

Debt Service Fund - The Debt Service Fund is used to account for the accumulation of resources for payment of general long-term bonded debt principal, interest, and related costs.

Fire Prevention and Safety - The Fire Prevention and Safety Fund is used to account for financial resources to alter and/or reconstruct existing facilities to meet fire prevention and safety standards, to meet environmental regulations, to reduce energy consumption, and for security purposes.

Additionally, the District reports the following fund types:

Internal Service Funds - These funds are used to account for self-insured employee health plan and the workman’s compensation plan.

Fiduciary - These funds are used to account for assets held by the District in a trustee capacity or as an agent for individuals, private organizations, other governments or other funds.

The Flexible Benefit Plan Trust Fund is used to account for the plan maintained on behalf of employers.

Agency Funds - Student Activity Funds - The Student Activity Funds are custodial in nature (assets equal liabilities), do not involve the measurement of the results of operations, and are treated as Agency Funds.

(d) Budgets and Budgetary Accounting

The District follows these procedures in establishing the budgetary data reflected in the financial statements:

1. Prior to July 1, a tentative operating budget is submitted to the Board of Education for the fiscal year commencing on July 1. The tentative operating budget includes proposed expenditures and the means of financing them.

2. Public hearings are conducted at a public meeting to obtain taxpayer comments, at least 30 days prior to final action by the Board of Education.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

18

NOTE 1 - DESCRIPTION OF ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(d) Budgets and Budgetary Accounting (Continued)

3. Prior to October 1, the budget is legally adopted through passage of a resolution. Prior to the last Tuesday in December, a tax levy ordinance is filed with the County Clerk to obtain tax revenues.

4. The Board of Education is authorized to transfer up to 10 percent of the total budget between departments within any fund. Any revisions that alter the total expenditures of any fund must be amended by the same procedure as provided for the original budget. The legal level of control is the fund level.

5. All appropriations lapse at the end of each fiscal year.

(e) Common Cash Account

Separate bank accounts are not maintained for all District funds. Instead, various funds maintain their cash balances in a common checking account. Accounting records are maintained to show the portion of the common cash balance attributable to each participating fund.

(f) Deposits and Investments

According to the District’s investment policy, the District is allowed to invest in securities as authorized by the Illinois Compiled Statutes, which include obligations of the U.S. Treasury and its agencies; interest-bearing savings; certificates of deposit or time deposits; commercial paper; money market mutual funds; short term discount obligations of the Federal National Mortgage Association; dividend-bearing share accounts of a credit union; Public Treasurer’s Investment Pool; Illinois School District Liquid Asset Fund Plus and repurchase agreements.

(g) Property Taxes

Property taxes attach as an enforceable lien on property as of January 1. The District must file its tax levy ordinance by the last Tuesday in December of each year. The District’s property tax is levied each year on all taxable real property located in the District. Property taxes are payable in two installments in approximately June and September at the County Collector’s office. Sale of taxes on any uncollected amounts is prior to November 30 or shortly thereafter by the County Collector’s office. Final distribution to all taxing bodies is usually made prior to November 30 by the County Collector’s office. Taxes, as other revenues of the District, are recognized on the cash basis of accounting and are, therefore, recognized as received.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

19

NOTE 1 - DESCRIPTION OF ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(h) Land, Buildings, and Equipment

Capital assets, which include land, land improvements, buildings and improvements, and equipment, have been acquired for general governmental purposes. Assets purchased are recorded as expenditures in the individual funds and capitalized at costs in the general fixed assets account group. Donated fixed assets are valued at their estimated fair value on the date donated.

All buildings, improvements, and equipment are depreciated using the straight-line method over the following estimated useful lives:

Improvements other than building 20 yearsBuildings 50 yearsEquipment 5-10 years

(i) Long-term Obligations

In the government-wide financial statements, long-term debt and other long-term obligations are reported as liabilities in the statement of net assets.

In the fund financial statements, governmental funds recognize bond premiums and discounts, as well as bond issue costs, during the current period. Premiums received on debt issuances are reported as other financing sources while discounts on debt issuances are reported as other financing uses. Issuance costs, whether or not withheld from the actual debt proceeds received, are reported as debt service expenditures. The face amount of debt issued is reported as other financing sources at the date received. Payments on debt principal are recorded as an expenditure.

(j) Fund Equity Restrictions and Designations

Reservations of fund equity are for amounts that are not available for appropriation or are legally restricted by outside parties for use for a specific purpose.

When both restricted and unrestricted resources are available for use, it is the District’s policy to use restricted resources first, then unrestricted resources as they are needed.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

20

NOTE 1 - DESCRIPTION OF ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(k) Adoption of New Accounting Standards

As further discussed in Note 13, effective July 1, 2009, the District adopted Governmental Accounting Standards Board (GASB) Statement No. 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions. This statement requires a systematic measurement of other postemployment benefit (OPEB) expense over a period that approximates employees’ years of service. The Statement also requires the information about actuarial accrued liabilities associated with OPEB and whether and to what extent progress is being made in funding the plan.

(l) Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues, expenditures/expenses, gains, losses, and other changes in fund equity during the reporting period. Actual results could differ from those estimates.

NOTE 2 - DEPOSITS AND INVESTMENTS

Custodial Credit Risk - Deposits

Custodial credit risk for is the risk that, in the event of a bank failure, the District’s deposits may not be returned to it. The District’s investment policy requires that all amounts deposited or invested with financial institutions in excess of any insurance limit be collateralized in accordance with the Public Fund Investment Act 30 ILCS2351.

The market value of the pledged securities should equal or exceed the portion of the deposit requiring collateralization.

As of June 30, 2010, none of the District’s bank balances of $23,336,843 was exposed to custodial credit risk.

The carrying amount of these deposits, excluding petty cash of $2,430, is $22,422,428 as of June 30, 2010.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

21

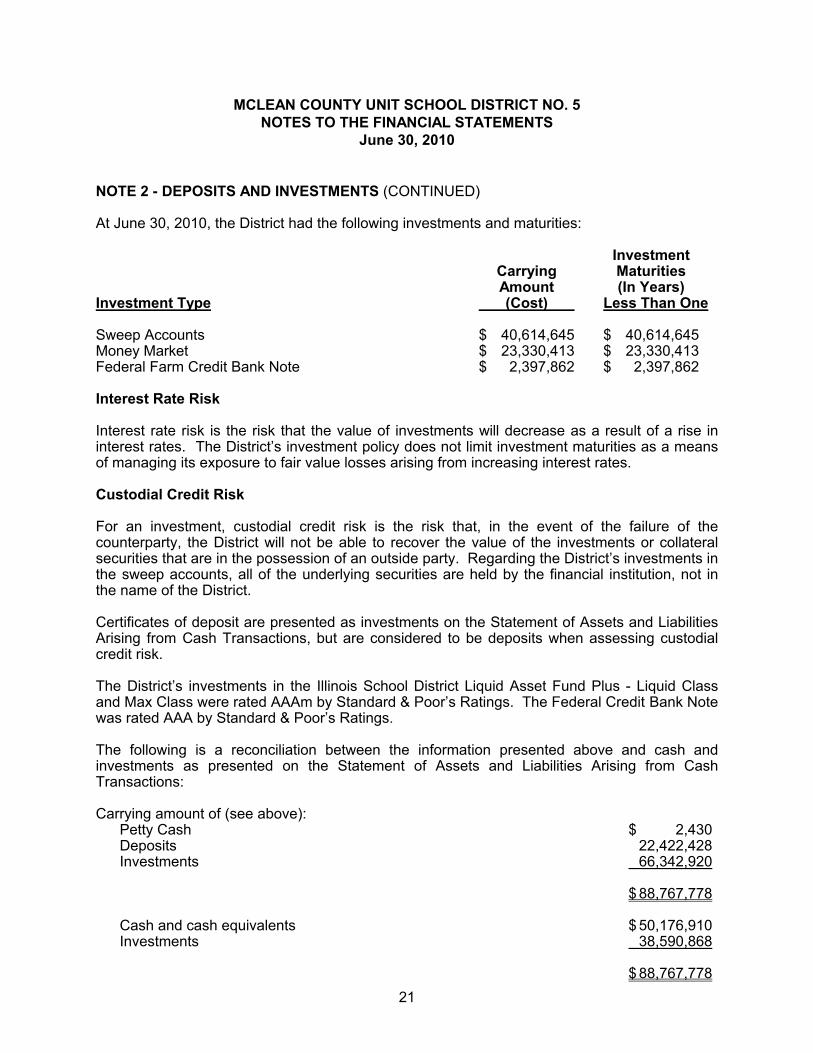

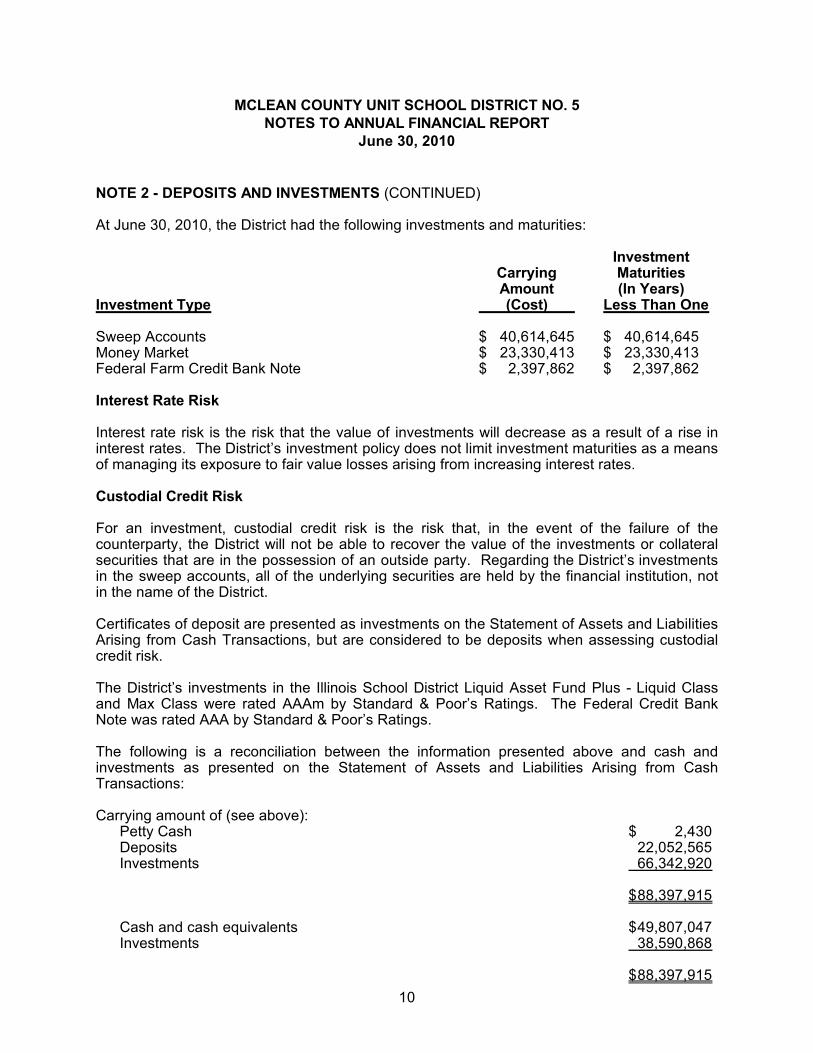

NOTE 2 - DEPOSITS AND INVESTMENTS (CONTINUED)

At June 30, 2010, the District had the following investments and maturities:

InvestmentCarrying MaturitiesAmount (In Years)

Investment Type (Cost) Less Than One

Sweep Accounts $ 40,614,645 $ 40,614,645Money Market $ 23,330,413 $ 23,330,413Federal Farm Credit Bank Note $ 2,397,862 $ 2,397,862

Interest Rate Risk

Interest rate risk is the risk that the value of investments will decrease as a result of a rise in interest rates. The District’s investment policy does not limit investment maturities as a means of managing its exposure to fair value losses arising from increasing interest rates.

Custodial Credit Risk

For an investment, custodial credit risk is the risk that, in the event of the failure of the counterparty, the District will not be able to recover the value of the investments or collateral securities that are in the possession of an outside party. Regarding the District’s investments in the sweep accounts, all of the underlying securities are held by the financial institution, not in the name of the District.

Certificates of deposit are presented as investments on the Statement of Assets and Liabilities Arising from Cash Transactions, but are considered to be deposits when assessing custodial credit risk.

The District’s investments in the Illinois School District Liquid Asset Fund Plus - Liquid Class and Max Class were rated AAAm by Standard & Poor’s Ratings. The Federal Credit Bank Note was rated AAA by Standard & Poor’s Ratings.

The following is a reconciliation between the information presented above and cash and investments as presented on the Statement of Assets and Liabilities Arising from Cash Transactions:

Carrying amount of (see above):Petty Cash $ 2,430Deposits 22,422,428Investments 66,342,920

$ 88,767,778

Cash and cash equivalents $ 50,176,910Investments 38,590,868

$ 88,767,778

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

22

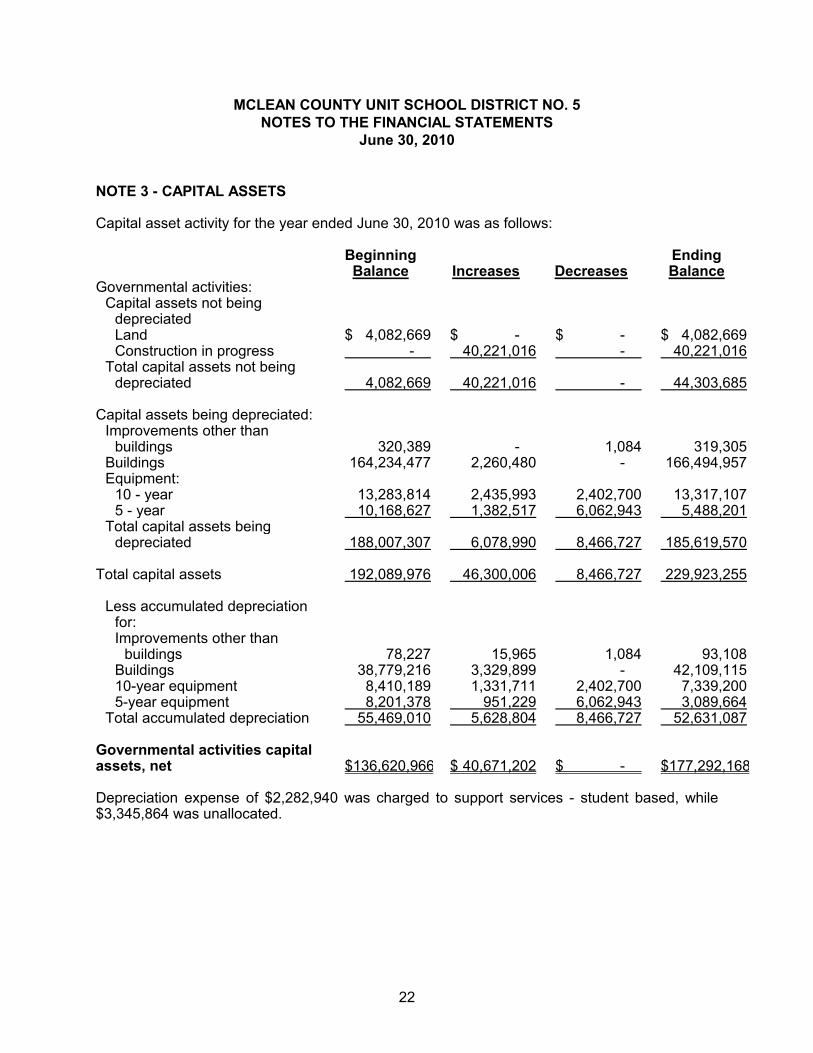

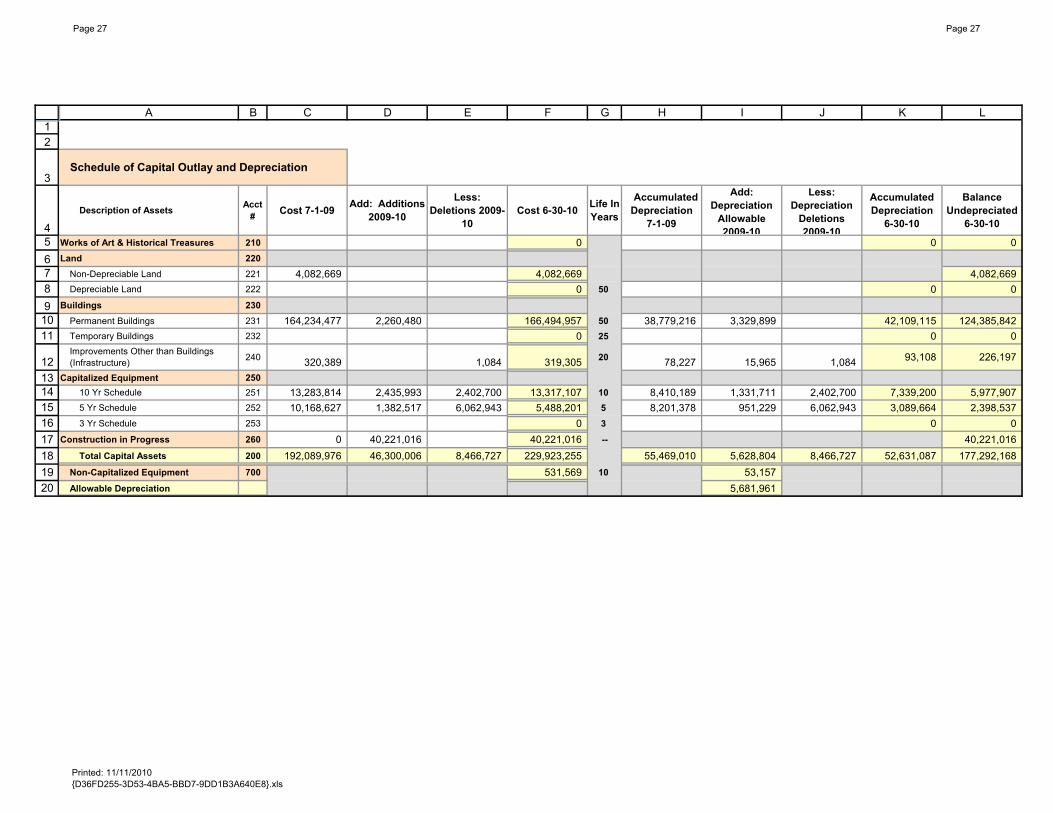

NOTE 3 - CAPITAL ASSETS

Capital asset activity for the year ended June 30, 2010 was as follows:

Beginning EndingBalance Increases Decreases Balance

Governmental activities:Capital assets not being

depreciatedLand $ 4,082,669 $ - $ - $ 4,082,669Construction in progress - 40,221,016 - 40,221,016

Total capital assets not beingdepreciated 4,082,669 40,221,016 - 44,303,685

Capital assets being depreciated:Improvements other than

buildings 320,389 - 1,084 319,305Buildings 164,234,477 2,260,480 - 166,494,957Equipment:

10 - year 13,283,814 2,435,993 2,402,700 13,317,1075 - year 10,168,627 1,382,517 6,062,943 5,488,201

Total capital assets beingdepreciated 188,007,307 6,078,990 8,466,727 185,619,570

Total capital assets 192,089,976 46,300,006 8,466,727 229,923,255

Less accumulated depreciationfor:Improvements other than

buildings 78,227 15,965 1,084 93,108Buildings 38,779,216 3,329,899 - 42,109,11510-year equipment 8,410,189 1,331,711 2,402,700 7,339,2005-year equipment 8,201,378 951,229 6,062,943 3,089,664

Total accumulated depreciation 55,469,010 5,628,804 8,466,727 52,631,087

Governmental activities capital assets, net $136,620,966 $ 40,671,202 $ - $177,292,168

Depreciation expense of $2,282,940 was charged to support services - student based, while $3,345,864 was unallocated.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

23

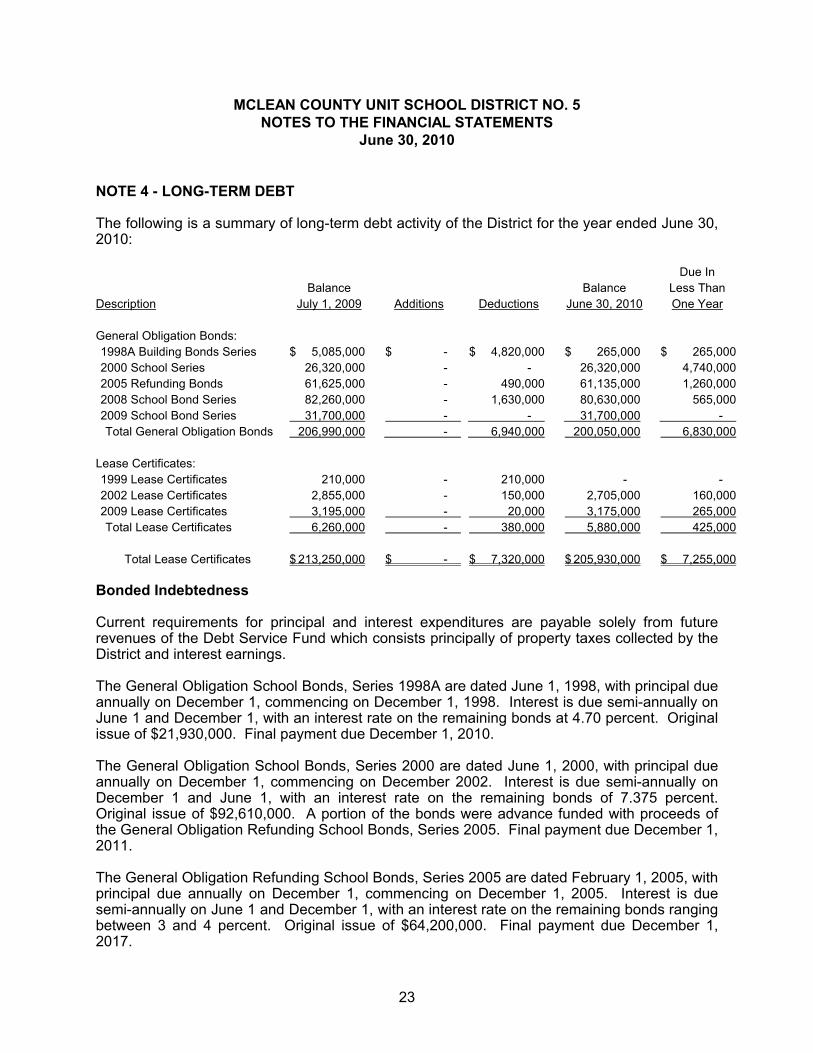

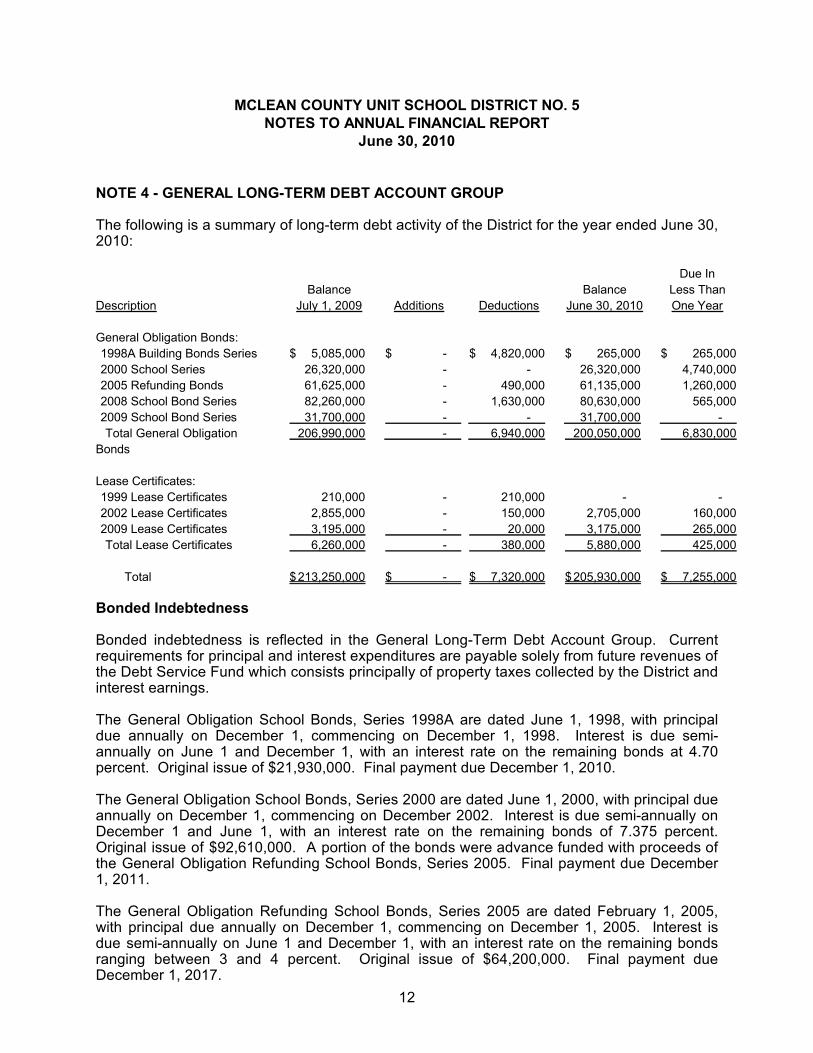

NOTE 4 - LONG-TERM DEBT

The following is a summary of long-term debt activity of the District for the year ended June 30, 2010:

Description

Balance

July 1, 2009 Additions Deductions

Balance

June 30, 2010

Due In

Less Than

One Year

General Obligation Bonds:

1998A Building Bonds Series $ 5,085,000 $ - $ 4,820,000 $ 265,000 $ 265,000

2000 School Series 26,320,000 - - 26,320,000 4,740,000

2005 Refunding Bonds 61,625,000 - 490,000 61,135,000 1,260,000

2008 School Bond Series 82,260,000 - 1,630,000 80,630,000 565,000

2009 School Bond Series 31,700,000 - - 31,700,000 -

Total General Obligation Bonds 206,990,000 - 6,940,000 200,050,000 6,830,000

Lease Certificates:

1999 Lease Certificates 210,000 - 210,000 - -

2002 Lease Certificates 2,855,000 - 150,000 2,705,000 160,000

2009 Lease Certificates 3,195,000 - 20,000 3,175,000 265,000

Total Lease Certificates 6,260,000 - 380,000 5,880,000 425,000

Total Lease Certificates $ 213,250,000 $ - $ 7,320,000 $ 205,930,000 $ 7,255,000

Bonded Indebtedness

Current requirements for principal and interest expenditures are payable solely from future revenues of the Debt Service Fund which consists principally of property taxes collected by the District and interest earnings.

The General Obligation School Bonds, Series 1998A are dated June 1, 1998, with principal due annually on December 1, commencing on December 1, 1998. Interest is due semi-annually on June 1 and December 1, with an interest rate on the remaining bonds at 4.70 percent. Original issue of $21,930,000. Final payment due December 1, 2010.

The General Obligation School Bonds, Series 2000 are dated June 1, 2000, with principal due annually on December 1, commencing on December 2002. Interest is due semi-annually on December 1 and June 1, with an interest rate on the remaining bonds of 7.375 percent. Original issue of $92,610,000. A portion of the bonds were advance funded with proceeds of the General Obligation Refunding School Bonds, Series 2005. Final payment due December 1, 2011.

The General Obligation Refunding School Bonds, Series 2005 are dated February 1, 2005, with principal due annually on December 1, commencing on December 1, 2005. Interest is due semi-annually on June 1 and December 1, with an interest rate on the remaining bonds ranging between 3 and 4 percent. Original issue of $64,200,000. Final payment due December 1, 2017.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

24

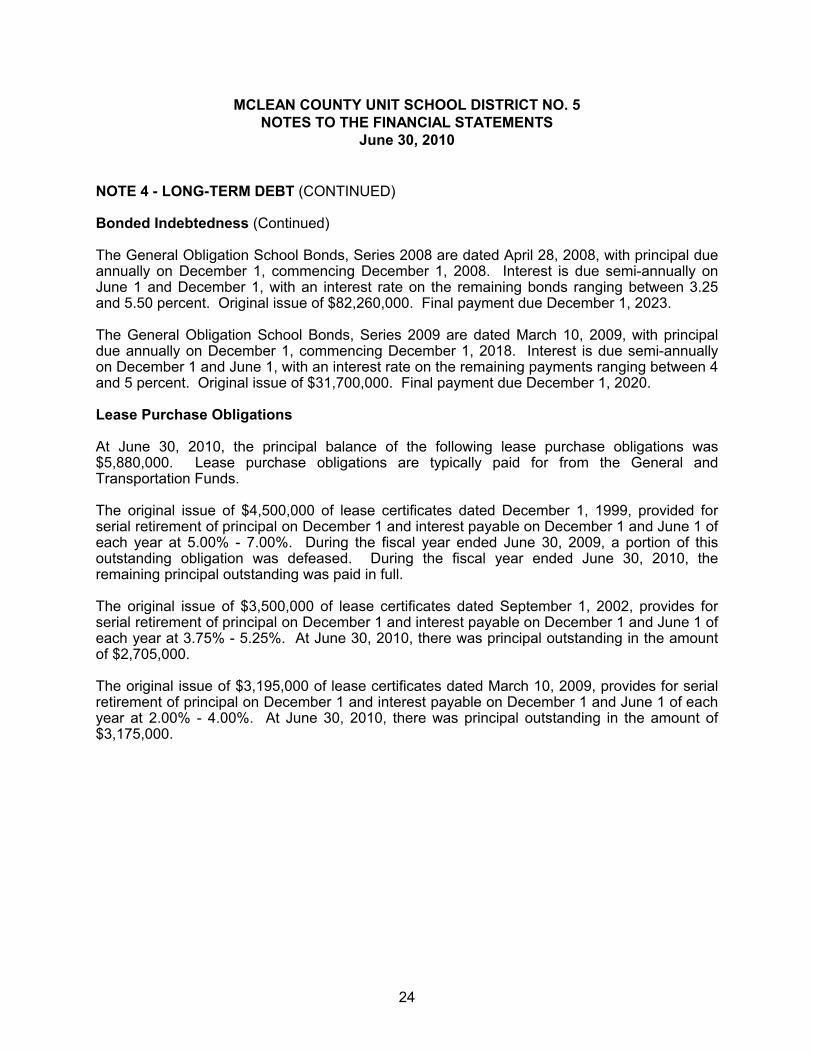

NOTE 4 - LONG-TERM DEBT (CONTINUED)

Bonded Indebtedness (Continued)

The General Obligation School Bonds, Series 2008 are dated April 28, 2008, with principal due annually on December 1, commencing December 1, 2008. Interest is due semi-annually on June 1 and December 1, with an interest rate on the remaining bonds ranging between 3.25 and 5.50 percent. Original issue of $82,260,000. Final payment due December 1, 2023.

The General Obligation School Bonds, Series 2009 are dated March 10, 2009, with principal due annually on December 1, commencing December 1, 2018. Interest is due semi-annually on December 1 and June 1, with an interest rate on the remaining payments ranging between 4 and 5 percent. Original issue of $31,700,000. Final payment due December 1, 2020.

Lease Purchase Obligations

At June 30, 2010, the principal balance of the following lease purchase obligations was $5,880,000. Lease purchase obligations are typically paid for from the General and Transportation Funds.

The original issue of $4,500,000 of lease certificates dated December 1, 1999, provided for serial retirement of principal on December 1 and interest payable on December 1 and June 1 of each year at 5.00% - 7.00%. During the fiscal year ended June 30, 2009, a portion of this outstanding obligation was defeased. During the fiscal year ended June 30, 2010, the remaining principal outstanding was paid in full.

The original issue of $3,500,000 of lease certificates dated September 1, 2002, provides for serial retirement of principal on December 1 and interest payable on December 1 and June 1 of each year at 3.75% - 5.25%. At June 30, 2010, there was principal outstanding in the amount of $2,705,000.

The original issue of $3,195,000 of lease certificates dated March 10, 2009, provides for serial retirement of principal on December 1 and interest payable on December 1 and June 1 of each year at 2.00% - 4.00%. At June 30, 2010, there was principal outstanding in the amount of $3,175,000.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

25

NOTE 4 - LONG-TERM DEBT (CONTINUED)

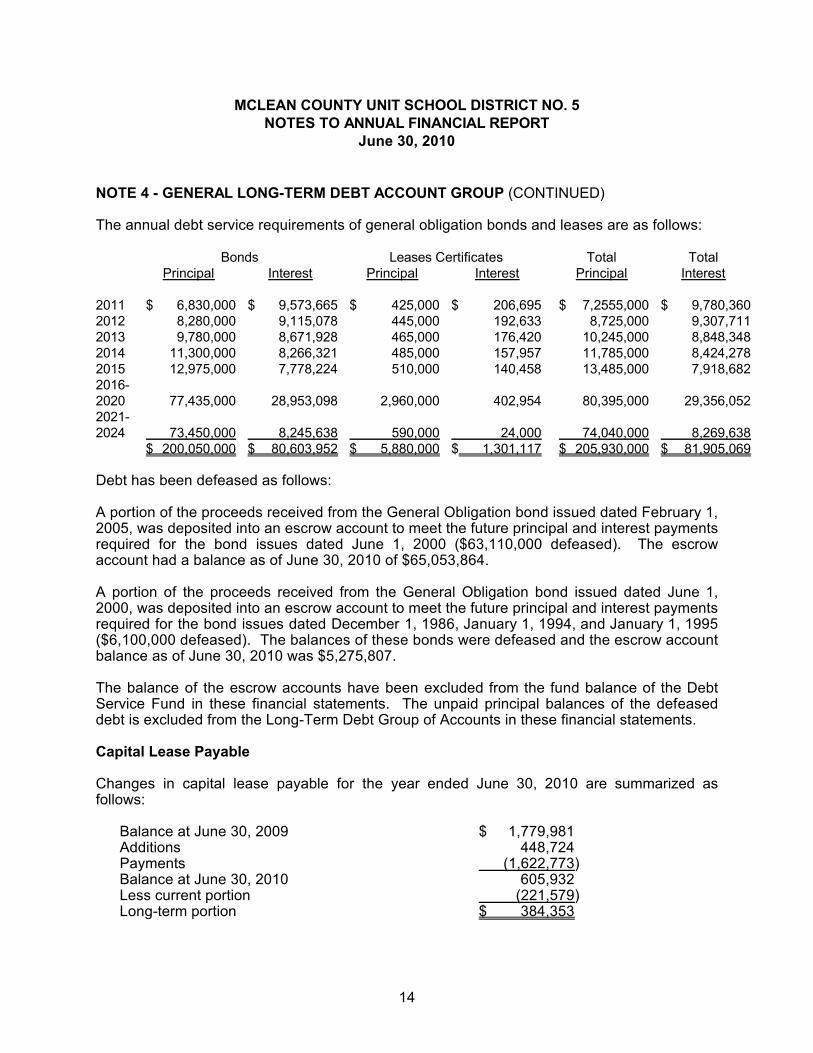

The annual debt service requirements of general obligation bonds and leases are as follows:

Bonds Leases Certificates Total TotalPrincipal Interest Principal Interest Principal Interest

2011 $ 6,830,000 $ 9,573,665 $ 425,000 $ 206,695 $ 7,255,000 $ 9,780,3602012 8,280,000 9,115,078 445,000 192,633 8,725,000 9,307,7112013 9,780,000 8,671,928 465,000 176,420 10,245,000 8,848,3482014 11,300,000 8,266,321 485,000 157,957 11,785,000 8,424,2782015 12,975,000 7,778,224 510,000 140,458 13,485,000 7,918,6822016-2020 77,435,000 28,953,098 2,960,000 402,954 80,395,000 29,356,0522021-2024 73,450,000 8,245,638 590,000 24,000 74,040,000 8,269,638

$ 200,050,000 $ 80,603,952 $ 5,880,000 $ 1,301,117 $ 205,930,000 $ 81,905,069

Prior Years’ Debt Defeasance

In prior years, the District has defeased various bond issues by creating separate irrevocable trust funds. New debt has been issued and the proceeds have been used to purchase U.S. government securities that were placed in the trust funds. The investments and fixed earnings from the investments are sufficient to fully service the refunded debt until the debt is called or matures. For financial reporting purposes, the debt has been considered defeased and therefore removed as a liability from the District’s long-term liabilities. As of June 30, 2010, the amount of defeased debt outstanding but removed from long-term liabilities is $69,210,000.

Capital Lease Payable

Changes in capital lease payable for the year ended June 30, 2010 are summarized as follows:

Balance at June 30, 2009 $ 1,779,981Additions 448,724Payments (1,622,773)Balance at June 30, 2010 605,932Less current portion (221,579)Long-term portion $ 384,353

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

26

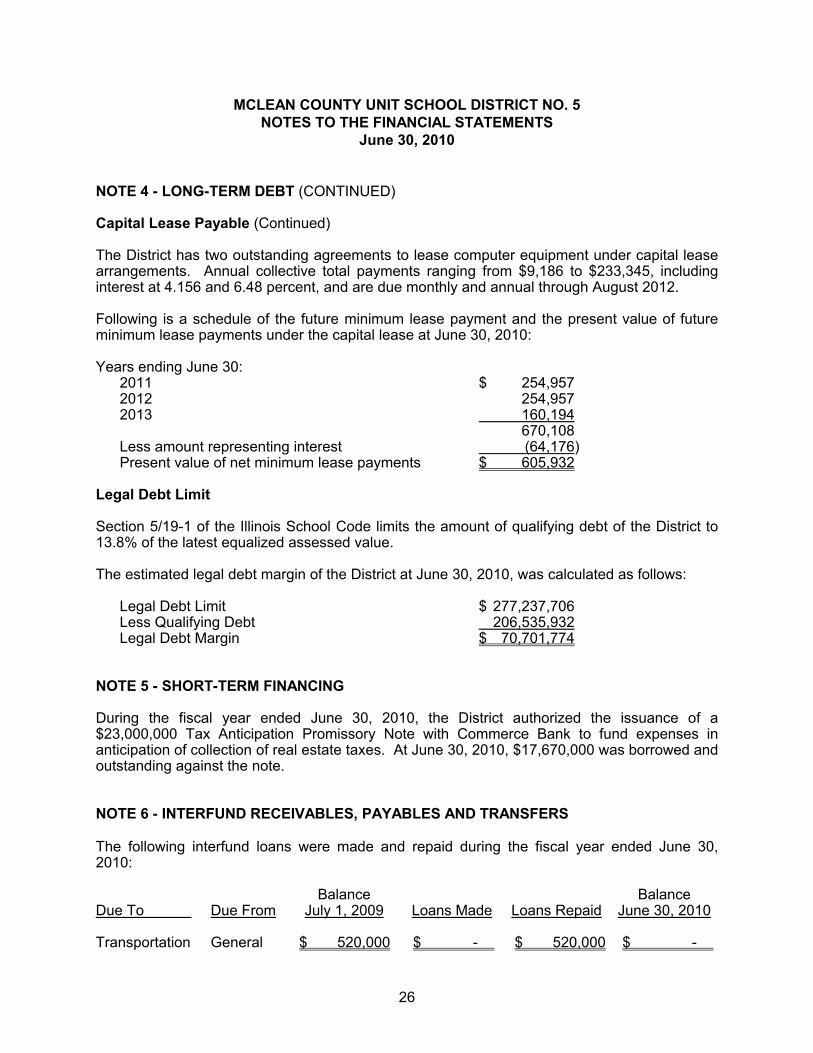

NOTE 4 - LONG-TERM DEBT (CONTINUED)

Capital Lease Payable (Continued)

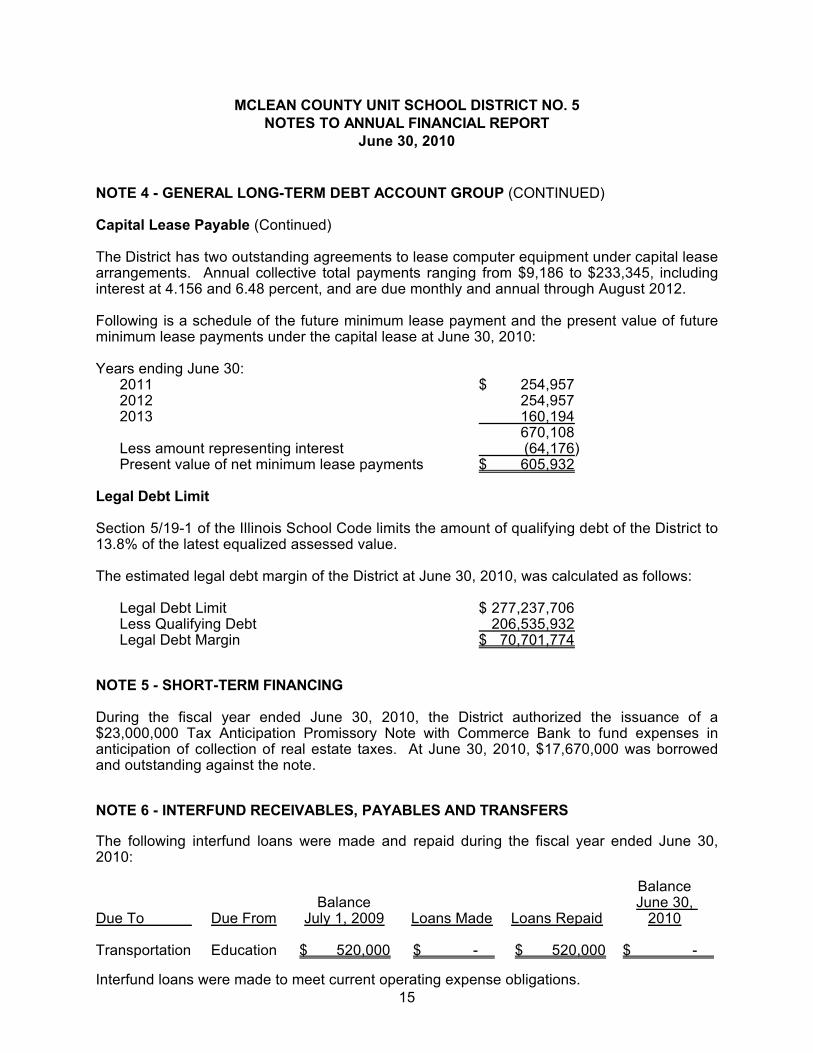

The District has two outstanding agreements to lease computer equipment under capital lease arrangements. Annual collective total payments ranging from $9,186 to $233,345, including interest at 4.156 and 6.48 percent, and are due monthly and annual through August 2012.

Following is a schedule of the future minimum lease payment and the present value of future minimum lease payments under the capital lease at June 30, 2010:

Years ending June 30:2011 $ 254,9572012 254,9572013 160,194

670,108Less amount representing interest (64,176)Present value of net minimum lease payments $ 605,932

Legal Debt Limit

Section 5/19-1 of the Illinois School Code limits the amount of qualifying debt of the District to 13.8% of the latest equalized assessed value.

The estimated legal debt margin of the District at June 30, 2010, was calculated as follows:

Legal Debt Limit $ 277,237,706Less Qualifying Debt 206,535,932Legal Debt Margin $ 70,701,774

NOTE 5 - SHORT-TERM FINANCING

During the fiscal year ended June 30, 2010, the District authorized the issuance of a $23,000,000 Tax Anticipation Promissory Note with Commerce Bank to fund expenses in anticipation of collection of real estate taxes. At June 30, 2010, $17,670,000 was borrowed and outstanding against the note.

NOTE 6 - INTERFUND RECEIVABLES, PAYABLES AND TRANSFERS

The following interfund loans were made and repaid during the fiscal year ended June 30, 2010:

Due To Due FromBalance

July 1, 2009 Loans Made Loans RepaidBalance

June 30, 2010

Transportation General $ 520,000 $ - $ 520,000 $ -

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

27

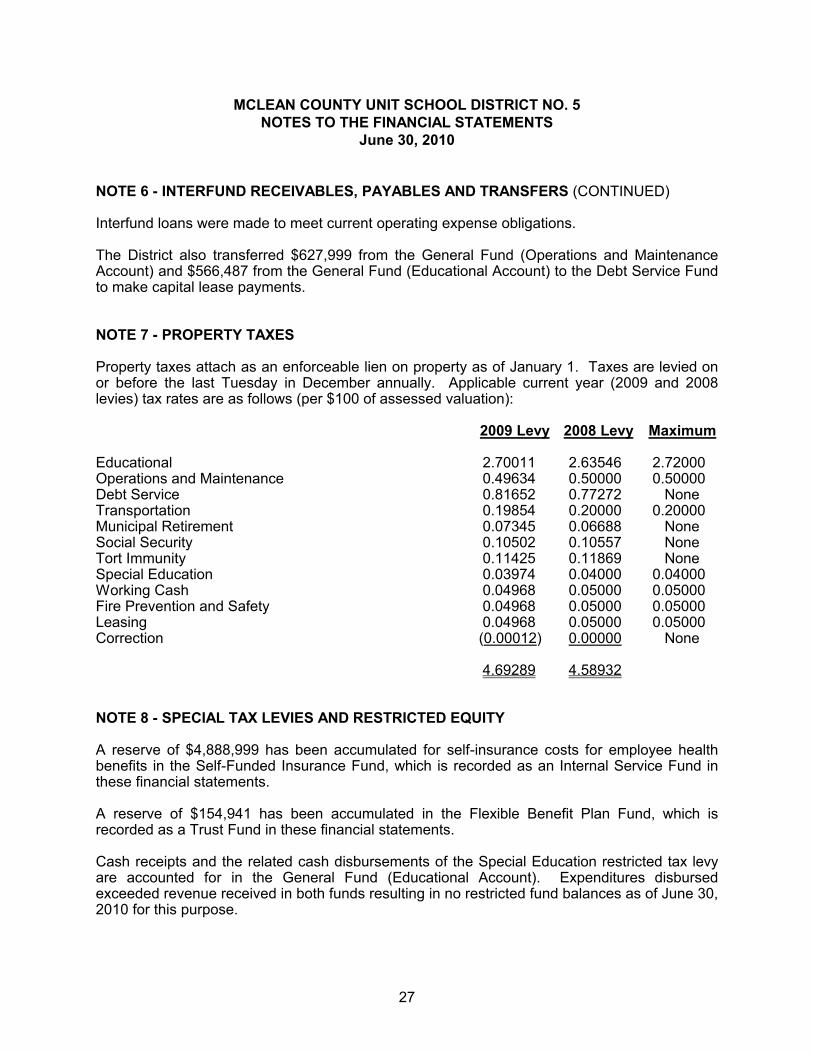

NOTE 6 - INTERFUND RECEIVABLES, PAYABLES AND TRANSFERS (CONTINUED)

Interfund loans were made to meet current operating expense obligations.

The District also transferred $627,999 from the General Fund (Operations and Maintenance Account) and $566,487 from the General Fund (Educational Account) to the Debt Service Fund to make capital lease payments.

NOTE 7 - PROPERTY TAXES

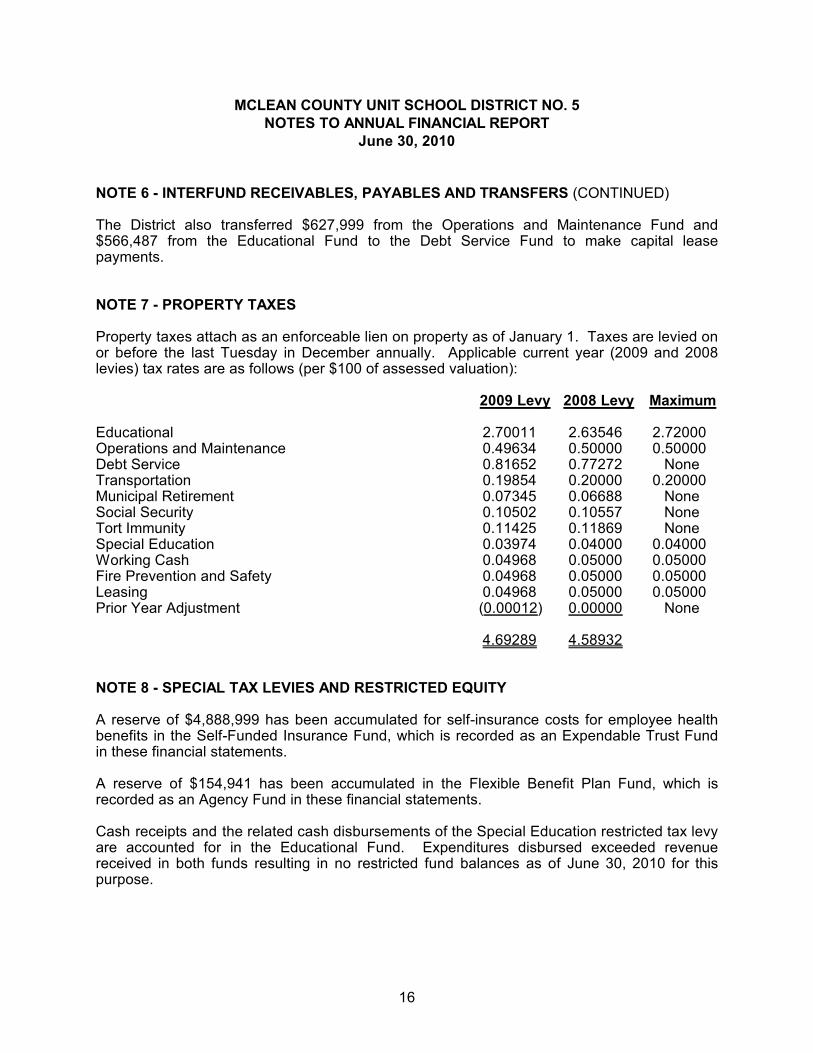

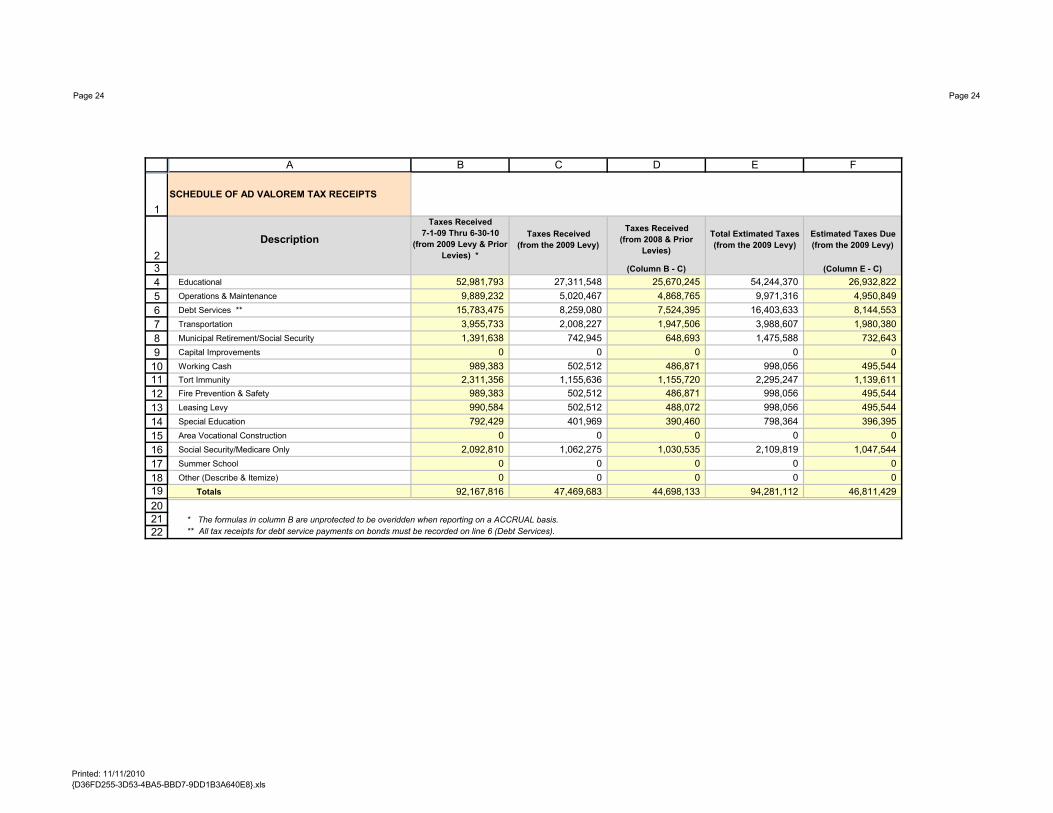

Property taxes attach as an enforceable lien on property as of January 1. Taxes are levied on or before the last Tuesday in December annually. Applicable current year (2009 and 2008levies) tax rates are as follows (per $100 of assessed valuation):

2009 Levy 2008 Levy Maximum

Educational 2.70011 2.63546 2.72000Operations and Maintenance 0.49634 0.50000 0.50000Debt Service 0.81652 0.77272 NoneTransportation 0.19854 0.20000 0.20000Municipal Retirement 0.07345 0.06688 NoneSocial Security 0.10502 0.10557 NoneTort Immunity 0.11425 0.11869 NoneSpecial Education 0.03974 0.04000 0.04000Working Cash 0.04968 0.05000 0.05000Fire Prevention and Safety 0.04968 0.05000 0.05000Leasing 0.04968 0.05000 0.05000Correction (0.00012) 0.00000 None

4.69289 4.58932

NOTE 8 - SPECIAL TAX LEVIES AND RESTRICTED EQUITY

A reserve of $4,888,999 has been accumulated for self-insurance costs for employee health benefits in the Self-Funded Insurance Fund, which is recorded as an Internal Service Fund in these financial statements.

A reserve of $154,941 has been accumulated in the Flexible Benefit Plan Fund, which is recorded as a Trust Fund in these financial statements.

Cash receipts and the related cash disbursements of the Special Education restricted tax levy are accounted for in the General Fund (Educational Account). Expenditures disbursed exceeded revenue received in both funds resulting in no restricted fund balances as of June 30, 2010 for this purpose.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

28

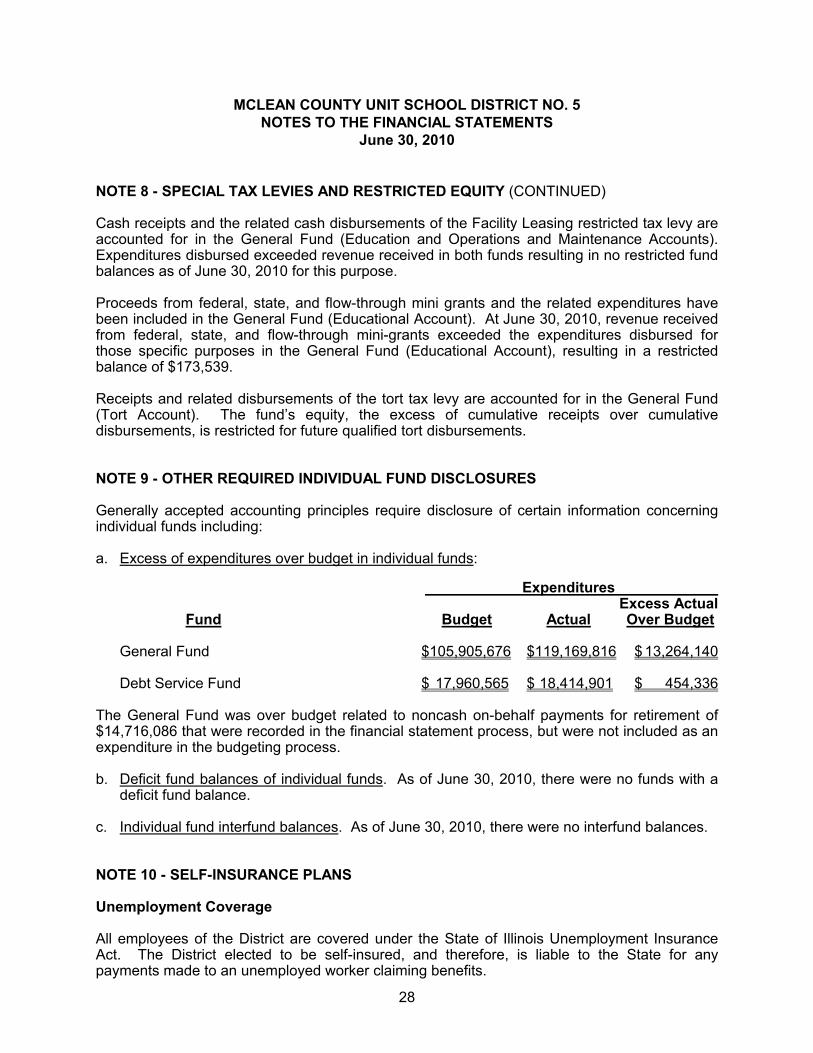

NOTE 8 - SPECIAL TAX LEVIES AND RESTRICTED EQUITY (CONTINUED)

Cash receipts and the related cash disbursements of the Facility Leasing restricted tax levy are accounted for in the General Fund (Education and Operations and Maintenance Accounts). Expenditures disbursed exceeded revenue received in both funds resulting in no restricted fund balances as of June 30, 2010 for this purpose.

Proceeds from federal, state, and flow-through mini grants and the related expenditures have been included in the General Fund (Educational Account). At June 30, 2010, revenue received from federal, state, and flow-through mini-grants exceeded the expenditures disbursed forthose specific purposes in the General Fund (Educational Account), resulting in a restricted balance of $173,539.

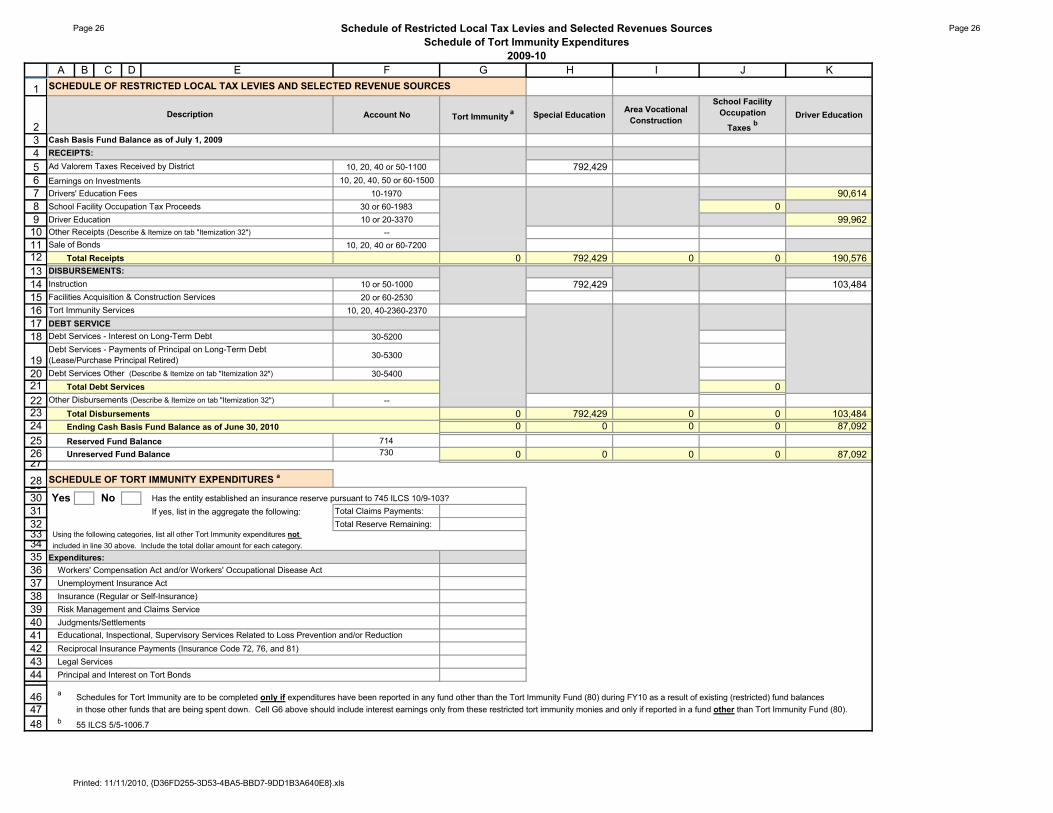

Receipts and related disbursements of the tort tax levy are accounted for in the General Fund (Tort Account). The fund’s equity, the excess of cumulative receipts over cumulative disbursements, is restricted for future qualified tort disbursements.

NOTE 9 - OTHER REQUIRED INDIVIDUAL FUND DISCLOSURES

Generally accepted accounting principles require disclosure of certain information concerning individual funds including:

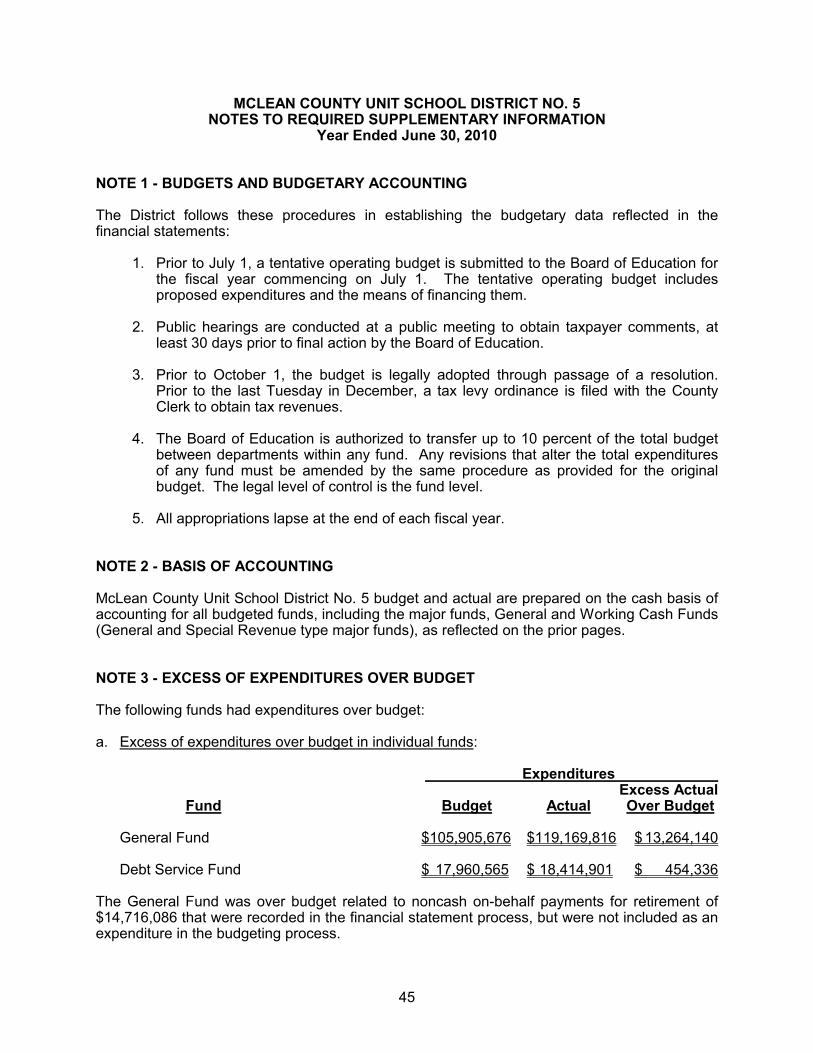

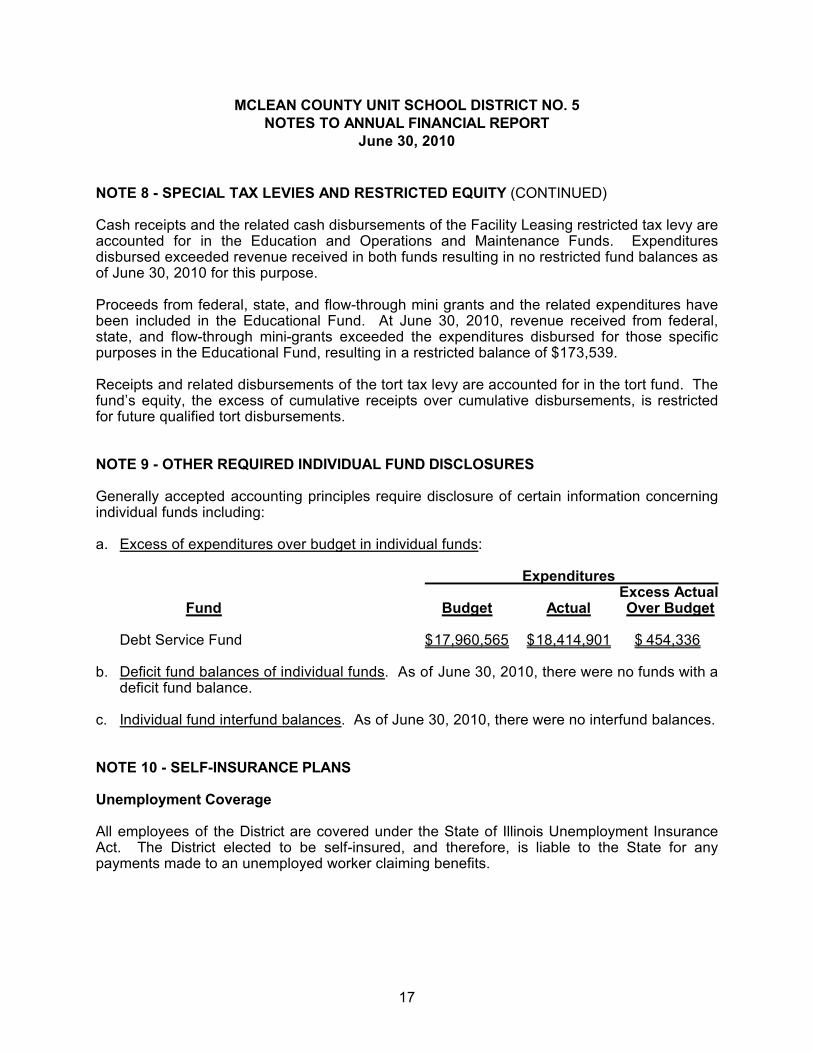

a. Excess of expenditures over budget in individual funds:

ExpendituresExcess Actual

Fund Budget Actual Over Budget

General Fund $105,905,676 $119,169,816 $ 13,264,140

Debt Service Fund $ 17,960,565 $ 18,414,901 $ 454,336

The General Fund was over budget related to noncash on-behalf payments for retirement of $14,716,086 that were recorded in the financial statement process, but were not included as an expenditure in the budgeting process.

b. Deficit fund balances of individual funds. As of June 30, 2010, there were no funds with a deficit fund balance.

c. Individual fund interfund balances. As of June 30, 2010, there were no interfund balances.

NOTE 10 - SELF-INSURANCE PLANS

Unemployment Coverage

All employees of the District are covered under the State of Illinois Unemployment Insurance Act. The District elected to be self-insured, and therefore, is liable to the State for any payments made to an unemployed worker claiming benefits.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

29

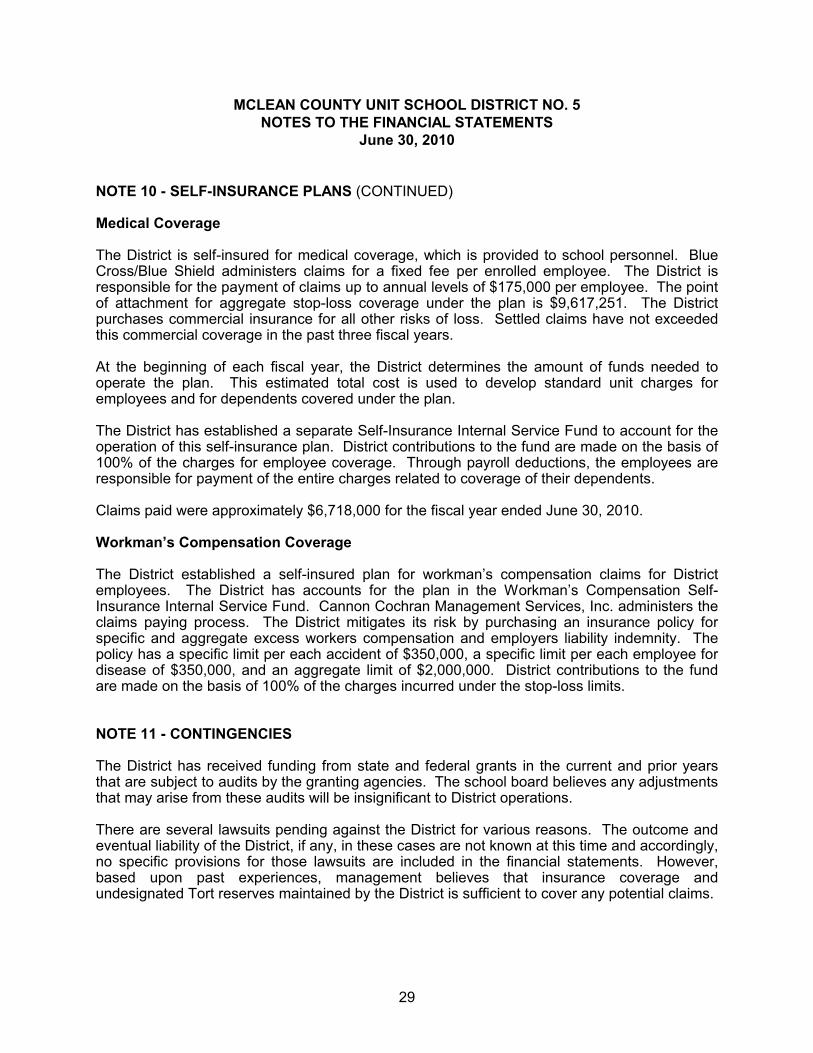

NOTE 10 - SELF-INSURANCE PLANS (CONTINUED)

Medical Coverage

The District is self-insured for medical coverage, which is provided to school personnel. Blue Cross/Blue Shield administers claims for a fixed fee per enrolled employee. The District is responsible for the payment of claims up to annual levels of $175,000 per employee. The point of attachment for aggregate stop-loss coverage under the plan is $9,617,251. The District purchases commercial insurance for all other risks of loss. Settled claims have not exceeded this commercial coverage in the past three fiscal years.

At the beginning of each fiscal year, the District determines the amount of funds needed to operate the plan. This estimated total cost is used to develop standard unit charges for employees and for dependents covered under the plan.

The District has established a separate Self-Insurance Internal Service Fund to account for the operation of this self-insurance plan. District contributions to the fund are made on the basis of 100% of the charges for employee coverage. Through payroll deductions, the employees are responsible for payment of the entire charges related to coverage of their dependents.

Claims paid were approximately $6,718,000 for the fiscal year ended June 30, 2010.

Workman’s Compensation Coverage

The District established a self-insured plan for workman’s compensation claims for District employees. The District has accounts for the plan in the Workman’s Compensation Self-Insurance Internal Service Fund. Cannon Cochran Management Services, Inc. administers the claims paying process. The District mitigates its risk by purchasing an insurance policy for specific and aggregate excess workers compensation and employers liability indemnity. The policy has a specific limit per each accident of $350,000, a specific limit per each employee for disease of $350,000, and an aggregate limit of $2,000,000. District contributions to the fund are made on the basis of 100% of the charges incurred under the stop-loss limits.

NOTE 11 - CONTINGENCIES

The District has received funding from state and federal grants in the current and prior years that are subject to audits by the granting agencies. The school board believes any adjustments that may arise from these audits will be insignificant to District operations.

There are several lawsuits pending against the District for various reasons. The outcome and eventual liability of the District, if any, in these cases are not known at this time and accordingly, no specific provisions for those lawsuits are included in the financial statements. However, based upon past experiences, management believes that insurance coverage and undesignated Tort reserves maintained by the District is sufficient to cover any potential claims.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

30

NOTE 12 - RETIREMENT COMMITMENTS

Teachers’ Retirement System of the State of Illinois

The District participates in the Teachers’ Retirement System of the State of Illinois (TRS). TRS is a cost-sharing multiple-employer defined benefit pension plan that was created by the Illinois legislature for the benefit of Illinois public school teachers employed outside the City of Chicago.

The Illinois Pension Code outlines the benefit provisions of TRS, and amendments to the plan can be made only by legislative action with the Governor’s approval. The State of Illinois maintains primary responsibility for the funding of the plan, but contributions from participating employers and members are also required. The TRS Board of Trustees is responsible for the system’s administration.

TRS members include all active non-annuitants who are employed by a TRS-covered employer to provide services for which teacher certification is required. The active member contribution rate through June 30, 2010 was 9.4 percent of creditable earnings. These contributions, which may be paid on behalf of employees by the employer, are submitted to TRS by the employer. The active member contribution rate was also 9.4 percent for the years ended June 30, 2009and 2008.

The State of Illinois makes contributions directly to TRS on behalf of the District’s TRS-covered employees.

On-behalf Contributions. The State of Illinois makes employer pension contributions on behalf of the District. For the year ended June 30, 2010, the State of Illinois contributions were based on 23.38 percent of creditable earnings not paid from federal funds, and the District recognized revenue received and expenditures paid of $14,205,702 in pension contributions that the State of Illinois paid directly to TRS. For the years ended June 30, 2009 and 2008, the State of Illinois contribution rates as percentages of creditable earnings were 17.08 ($9,475,407) and 13.11 percent ($7,012,600), respectively.

The District makes other types of employer contributions directly to TRS.

a) 2.2 Formula Contributions. Employers contribute 0.58 percent of total creditable earnings for the 2.2 formula change. This rate is specified by statute. Contributions for the year ended June 30, 2010 were $351,390. Contributions for the years ending June 30, 2009 and 2008 were $333,649 and $310,245, respectively.

b) Federal and Trust Fund Contributions. When TRS members are paid from federal andspecial trust funds administered by the District, there is a statutory requirement for the District to pay an employer contribution from those funds. Under a policy adopted by the TRS Board of Trustees that was first effective in the fiscal year ended June 30, 2006, employer contributions for employees paid from federal and trust funds will be the same as the state contribution rate to TRS.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

31

NOTE 12 - RETIREMENT COMMITMENTS (CONTINUED)

Teachers’ Retirement System of the State of Illinois (Continued)

For the year ended June 30, 2010, the employer pension contribution was 23.38 percent of salaries paid from federal and trust funds. For the years ended June 30, 2009 and 2008, the employer pension contribution was 17.08 and 13.11 percent of salaries paid from federal and special trust funds, respectively. For the year ended June 30, 2010, salaries totaling $2,945,807 were paid from federal and trust funds that required employer contributions of $688,730. For the years ended June 30, 2009 and 2008, required District contributions were $349,974 and $310,311, respectively.

c) Early Retirement Option. The District is also required to make one-time employer contributions to TRS for members retiring under the Early Retirement Option (ERO). The payments vary depending on the age and salary of the member.

Public Act 94-0004 made changes in the ERO program that were in effect for all ERO retirements in fiscal years 2008 through 2010. The Act increased member and employer contributions and eliminated the waiver of member and employer ERO contributions that had been in effect for members with 34 years of service.

Under the current ERO, the maximum employer contribution is 117.5 percent and applies when the member is age 55 at retirement.

For the year ended June 30, 2010, the District paid $113,705 to TRS for employer contributions under the ERO program. For the years ended June 30, 2009 and June 30, 2008, the District paid $61,618 and $43,177 in employer ERO contributions, respectively.

Salary Increases Over Six Percent and Excess Sick Leave

Public Act 94-0004 added two new employer contributions to TRS.

If an employer grants salary increases over 6 percent and those salaries are used to calculate a retiree’s final average salary, the employer makes a contribution to TRS. The contribution will cover the difference in actuarial cost of the benefit based on actual salary increases and the benefit based on salary increases of up to 6 percent.

For the year ended June 30, 2010, the District paid $39,151 to TRS for employer contributions due on salary increases in excess of 6 percent. For the years ended June 30, 2009, and 2008, the District paid $15,087 and $0, respectively, to TRS for employer contributions due on salary increases in excess of 6 percent.

If an employer grants sick leave days in excess of the normal annual allotment and those days are used as TRS service credit, the employer makes a contribution to TRS. The contribution is based on the number of excess sick leave days used as service credit, the highest salary used to calculate final average salary, and the TRS total normal cost rate (18.55 percent of salary during the year ended June 30, 2010).

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

32

NOTE 12 - RETIREMENT COMMITMENTS (CONTINUED)

Teachers’ Retirement System of the State of Illinois (Continued)

For the year ended June 30, 2010 the District made no payment to TRS for sick leave days granted in the excess of normal annual allotment. For the years ended June 30, 2009 and June 30, 2008, the District paid $682 and $3,097, in employer contributions granted for sick leave days, respectively.

TRS financial information, an explanation of TRS benefits, and descriptions of member, employer, and state funding requirements can be found in the TRS Comprehensive Annual Financial Report for the year ended June 30, 2009. The report for the year ended June 30, 2010 is expected to be available in late 2010.

The reports may be obtained by writing to the Teachers’ Retirement System of the State ofIllinois, P.O. Box 19253, 2815 West Washington Street, Springfield, Illinois 62794-9253. The most current report is also available on the TRS web site at trs.illinois.gov.

THIS Fund Employer Contributions

The District (employer) participates in the Teacher Health Insurance Security (THIS) Fund, a cost-sharing, multiple-employer defined benefit postemployment healthcare plan that was established by the Illinois legislature for the benefit of Illinois public school teachers employed outside the City of Chicago. The THIS Fund provides medical, prescription, and behavioral health benefits, but does not provide vision, dental, or life insurance benefits to annuitants of the Teachers’ Retirement System (TRS). Annuitants may participate in the State administered participating provider option plan or choose from several managed care options.

The State Employees Group Insurance Act of 1971 (5 ILCS 375) outlines the benefit provisions of THIS Fund, and amendments to the plan can be made only by legislative action with the Governor’s approval. The Illinois Department of Healthcare and Family Services (HFS) and the Illinois Department of Central Management Services (CMS) administer the plan with the cooperation of TRS. The director of HFS determines the rates and premiums for annuitants and dependent beneficiaries and establishes the cost-sharing parameters. Section 6.6 of the State Employees Group Insurance Act of 1971 requires all active contributors to the TRS who are not employees of the State make a contribution to THIS.

The percentage of employer required contributions in the future will be determined by the Director of Healthcare and Family Services and will not exceed 105 percent of the percentage of salary actually required to be paid in the previous fiscal year.

On Behalf Contributions to THIS Fund

The State of Illinois makes employer retiree health insurance contributions on behalf of the District. State contributions are intended to match contributions to THIS Fund from active members which were 0.84 percent of pay during the year ended June 30, 2010. State of Illinois contributions were $510,384, and the District recognized revenue and expenditures of this amount during the year.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

33

NOTE 12 - RETIREMENT COMMITMENTS (CONTINUED)

THIS Fund Employer Contributions (Continued)

On Behalf Contributions to THIS Fund (Continued)

State contributions intended to match active member contributions during the years ended June 30, 2009 and 2008 were also 0.84 percent of pay. State contributions on behalf of district employees were $466,004 and $449,320, respectively.

Employer Contributions to THIS Fund

The District also makes contributions to THIS Fund. The District THIS Fund contribution was 0.63 percent during the years ended June 30, 2010, June 30, 2009, and June 30, 2008. For the year ended June 30, 2010, the District paid $382,788 to the THIS Fund. For the years ended June 30, 2009 and June 30, 2008, the District paid $362,412 and $336,990 to the THIS Fund, respectively, which was 100 percent of the required contribution.

Further Information on THIS Fund

The publicly available financial report of the THIS Fund may be obtained by writing to the Department of Healthcare and Family Services, 201 S. Grand Avenue, Springfield, IL 62763-3838.

Illinois Municipal Retirement Fund

Plan Description

The District’s defined benefit pension plan for regular employees provides retirement and disability benefits, postretirement increases, and death benefits to plan members and beneficiaries. The District plan is affiliated with the Illinois Municipal Retirement Fund (IMRF), an agent multi-employer plan. Benefit provisions are established by statute and may only be changed by the General Assembly of the State of Illinois. IMRF issues a publicly available financial report that includes financial statements and required supplementary information. The report may be obtained on-line at www.imrf.org.

Funding Policy

As set by statute, the District’s regular plan members are required to contribute 4.50 percent of their annual covered salary. The statutes require employers to contribute the amount necessary, in addition to member contributions, to finance the retirement coverage of its own employees. The employer contribution rate for calendar year 2009 was 9.59 percent of annual covered payroll. The employer also contributes for disability benefits, death benefits, and supplemental retirement benefits, all of which are pooled at the IMRF level. Contribution rates for disability and death benefits are set by the IMRF Board of Trustees, while the supplemental retirement benefits rate is set by statute.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

34

NOTE 12 - RETIREMENT COMMITMENTS (CONTINUED)

Illinois Municipal Retirement Fund (Continued)

Annual Pension Cost

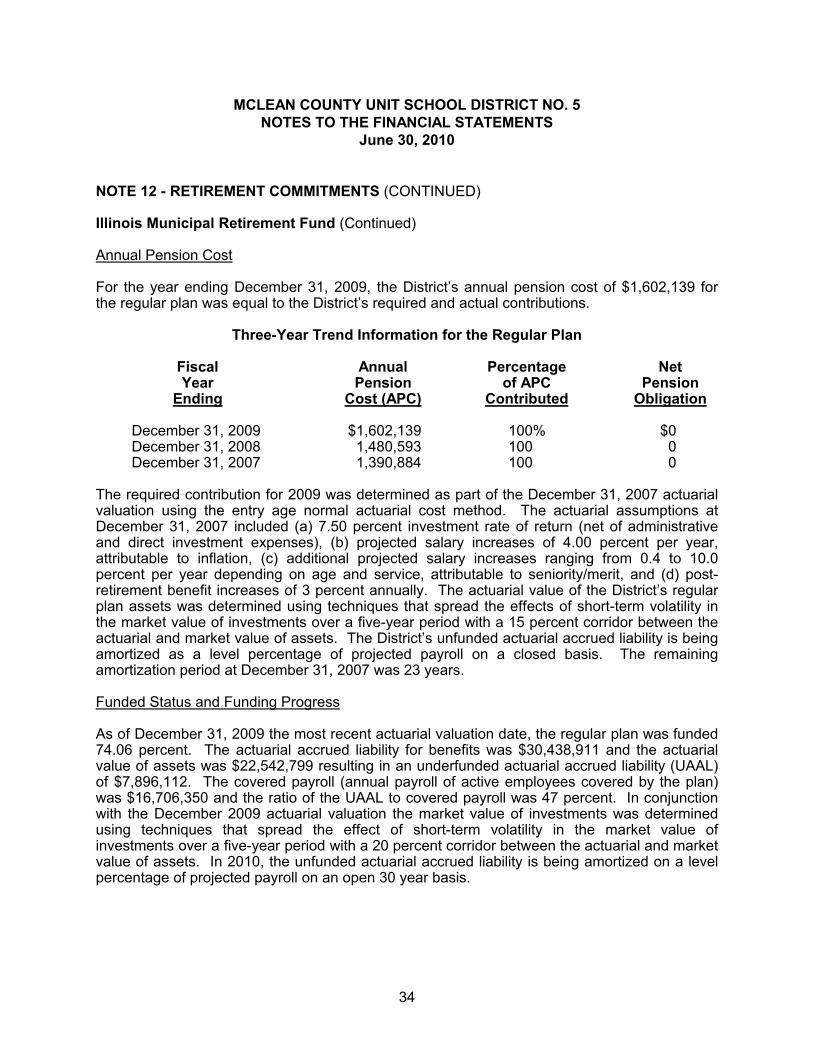

For the year ending December 31, 2009, the District’s annual pension cost of $1,602,139 for the regular plan was equal to the District’s required and actual contributions.

Three-Year Trend Information for the Regular Plan

Fiscal Annual Percentage NetYear Pension of APC Pension

Ending Cost (APC) Contributed Obligation

December 31, 2009 $1,602,139 100% $0December 31, 2008 1,480,593 100 0December 31, 2007 1,390,884 100 0

The required contribution for 2009 was determined as part of the December 31, 2007 actuarial valuation using the entry age normal actuarial cost method. The actuarial assumptions at December 31, 2007 included (a) 7.50 percent investment rate of return (net of administrative and direct investment expenses), (b) projected salary increases of 4.00 percent per year, attributable to inflation, (c) additional projected salary increases ranging from 0.4 to 10.0percent per year depending on age and service, attributable to seniority/merit, and (d) post-retirement benefit increases of 3 percent annually. The actuarial value of the District’s regular plan assets was determined using techniques that spread the effects of short-term volatility in the market value of investments over a five-year period with a 15 percent corridor between the actuarial and market value of assets. The District’s unfunded actuarial accrued liability is being amortized as a level percentage of projected payroll on a closed basis. The remaining amortization period at December 31, 2007 was 23 years.

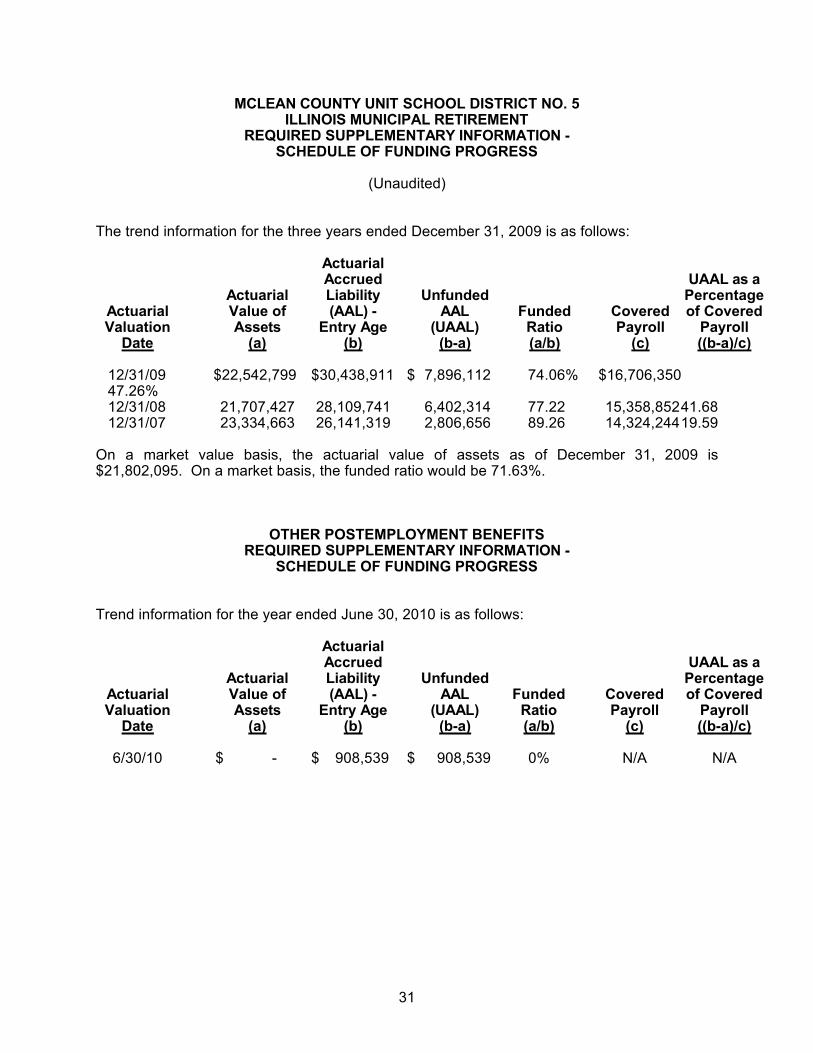

Funded Status and Funding Progress

As of December 31, 2009 the most recent actuarial valuation date, the regular plan was funded 74.06 percent. The actuarial accrued liability for benefits was $30,438,911 and the actuarial value of assets was $22,542,799 resulting in an underfunded actuarial accrued liability (UAAL) of $7,896,112. The covered payroll (annual payroll of active employees covered by the plan) was $16,706,350 and the ratio of the UAAL to covered payroll was 47 percent. In conjunction with the December 2009 actuarial valuation the market value of investments was determined using techniques that spread the effect of short-term volatility in the market value of investments over a five-year period with a 20 percent corridor between the actuarial and market value of assets. In 2010, the unfunded actuarial accrued liability is being amortized on a level percentage of projected payroll on an open 30 year basis.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

35

NOTE 12 - RETIREMENT COMMITMENTS (CONTINUED)

The schedule of funding progress, presented as Required Supplemental Information (RSI)following the notes to financial statements, presents multi-year trend information about whether the actuarial value of plan assets is increasing or decreasing over time relative to the actuarial accrued liability for benefits. The schedule of funding progress includes information from Mackinaw Valley Special Education Association, a joint agreement administered by the District.

Other Retirement Incentives

For the duration of the current employment agreement, qualifying teachers of the District who have completed ten years or more of creditable service with the school district, who have contributed to Illinois Teacher’s Retirement System for twenty years, who are at least fifty-five years of age, and whose retirement will not result in a penalty to the District, shall be eligible for the following retirement incentive:

1. If the Board is given irrevocable notice of retirement by May 1st three years prior to the year of retirement, the Board shall pay a six percent retirement incentive for eachremaining year of service.

2. If the Board is given irrevocable notice of retirement by May 1st two years prior to the year of retirement, the Board shall pay a six percent retirement incentive for each remaining year of service.

3. If the Board is given irrevocable notice of retirement by May 1st one year prior to the year of retirement, the Board shall pay a six percent retirement incentive for each remaining year of service.

As of June 30, 2010, the District was obligated for $364,802 under this retirement incentive. The current employment agreement expired on June 30, 2010.

NOTE 13 - OTHER POSTEMPLOYMENT BENEFITS

The District implemented Governmental Accounting Standards Board Statement (GASB) No. 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions, effective July 1, 2009. This statement requires the costs of postemployment benefits other than pension benefits to be recognized over a period that approximates an employee’s years of service. Implementation of this statement results in a liability of $24,912. Additional disclosures required by this statement are included below.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

36

NOTE 13 - OTHER POSTEMPLOYMENT BENEFITS (CONTINUED)

a. Plan Description

In addition to providing the pension benefits described in Note 12, the District provides postemployment health care benefits (OPEB) for retired employees through a single employer defined benefit plan (Retiree Healthcare Program). The benefits, benefit levels, employee contributions and employer contributions are governed by the District and can be amended by the District through its personnel manual and union contracts. The plan is not accounted for as a trust fund, as an irrevocable trust has not been established to account for the plan. The plan does not issue a separate report.

b. Benefits Provided

The District provides limited health care insurance coverage for its eligible retired employees in accordance with Illinois statutes, which creates an implicit subsidy of retiree health care coverage. To be eligible for benefits, an employee must qualify for retirement under one of the District’s retirement plans. Upon a retiree reaching age 65 years of age, Medicare becomes the primary insurer.

c. Membership

The District’s Retiree Healthcare Program includes two employee groups: those qualifying for Illinois Municipal Retirement and Teachers’ Retirement System of the State of Illinois, which are the same as those used for the pension plan.

At June 30, 2010, membership consisted of:

Retirees and beneficiaries currently receiving benefits 21Terminated employees entitled to benefits but not yet receiving them 0Active vested plan members 611Active nonvested plan members 686

Total 1,318

Participating employers 1

d. Funding Policy

The District is not required to and currently does not advance fund the cost of benefits that will become due and payable in the future. Active employees do not contribute to the plan until retirement.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

37

NOTE 13 - OTHER POSTEMPLOYMENT BENEFITS (CONTINUED)

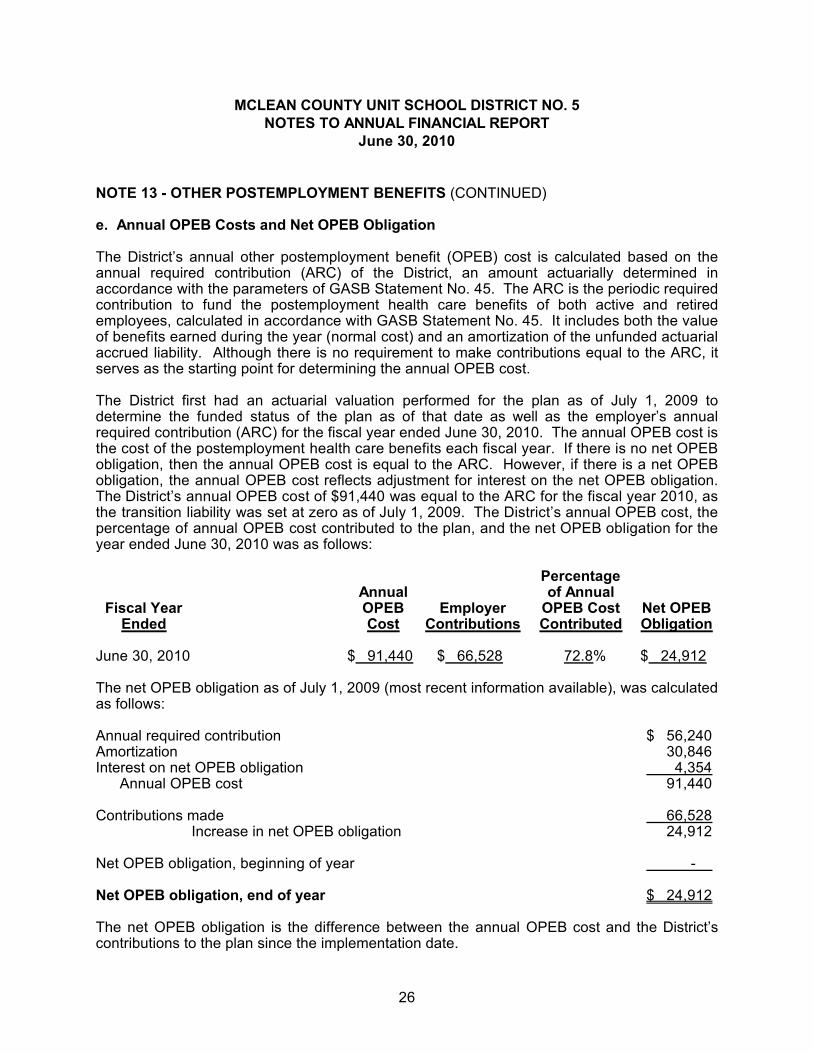

e. Annual OPEB Costs and Net OPEB Obligation

The District’s annual other postemployment benefit (OPEB) cost is calculated based on the annual required contribution (ARC) of the District, an amount actuarially determined in accordance with the parameters of GASB Statement No. 45. The ARC is the periodic required contribution to fund the postemployment health care benefits of both active and retired employees, calculated in accordance with GASB Statement No. 45. It includes both the value of benefits earned during the year (normal cost) and an amortization of the unfunded actuarial accrued liability. Although there is no requirement to make contributions equal to the ARC, it serves as the starting point for determining the annual OPEB cost.

The District first had an actuarial valuation performed for the plan as of July 1, 2009 to determine the funded status of the plan as of that date as well as the employer’s annual required contribution (ARC) for the fiscal year ended June 30, 2010. The annual OPEB cost is the cost of the postemployment health care benefits each fiscal year. If there is no net OPEB obligation, then the annual OPEB cost is equal to the ARC. However, if there is a net OPEB obligation, the annual OPEB cost reflects adjustment for interest on the net OPEB obligation. The District’s annual OPEB cost of $91,440 was equal to the ARC for the fiscal year 2010, as the transition liability was set at zero as of July 1, 2009. The District’s annual OPEB cost, the percentage of annual OPEB cost contributed to the plan, and the net OPEB obligation for the year ended June 30, 2010 was as follows:

PercentageAnnual of Annual

Fiscal Year OPEB Employer OPEB Cost Net OPEBEnded Cost Contributions Contributed Obligation

June 30, 2010 $ 91,440 $ 66,528 72.8% $ 24,912

The net OPEB obligation as of July 1, 2009 (most recent information available), was calculated as follows:

Annual required contribution $ 56,240Amortization 30,846Interest on net OPEB obligation 4,354

Annual OPEB cost 91,440

Contributions made 66,528Increase in net OPEB obligation 24,912

Net OPEB obligation, beginning of year -

Net OPEB obligation, end of year $ 24,912

The net OPEB obligation is the difference between the annual OPEB cost and the District’s contributions to the plan since the implementation date.

MCLEAN COUNTY UNIT SCHOOL DISTRICT NO. 5NOTES TO THE FINANCIAL STATEMENTS

June 30, 2010

38

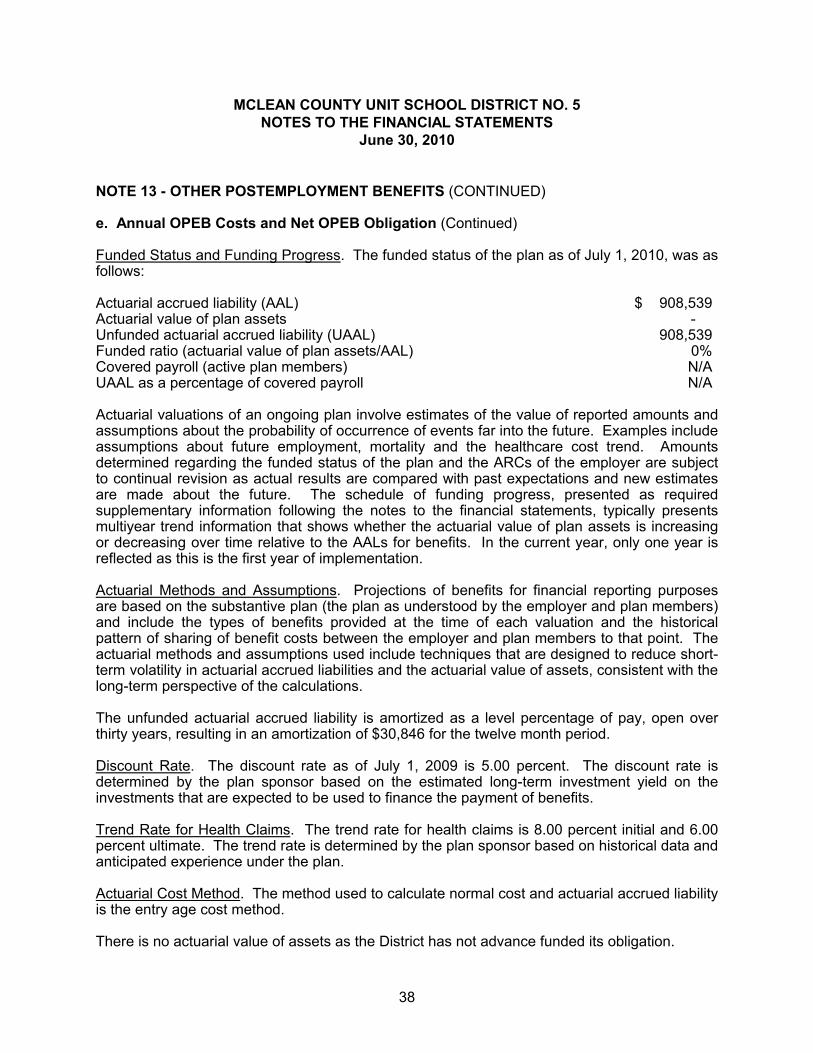

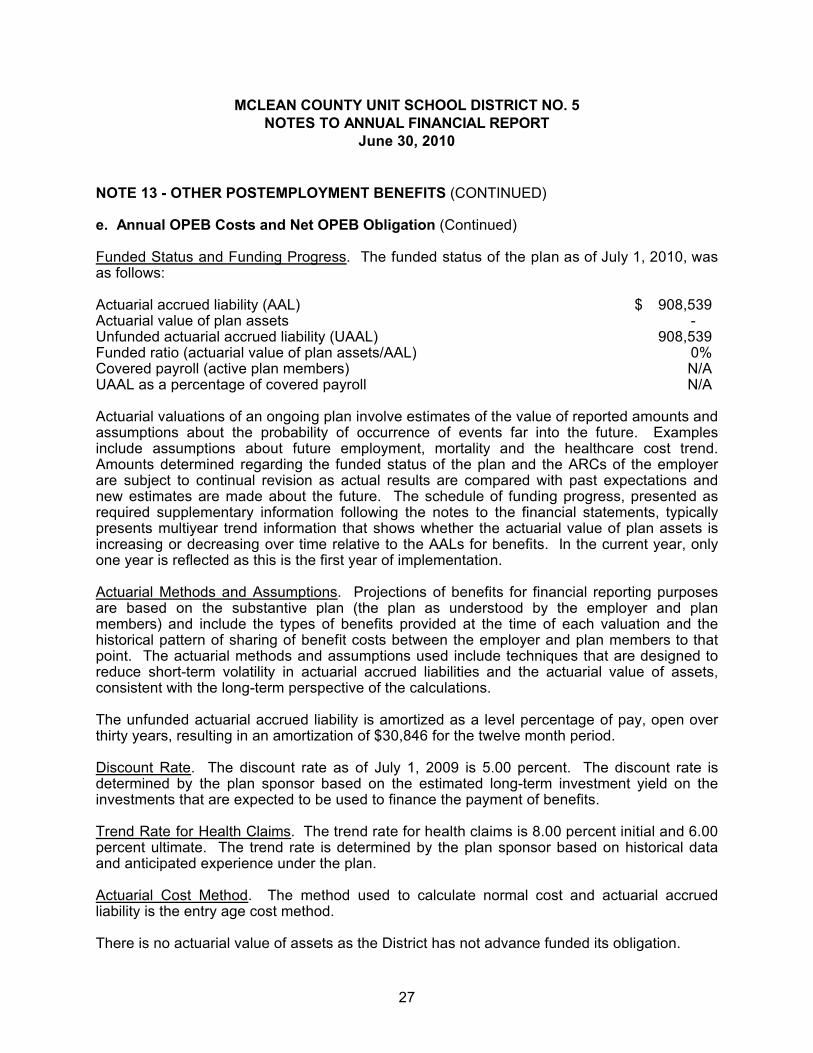

NOTE 13 - OTHER POSTEMPLOYMENT BENEFITS (CONTINUED)

e. Annual OPEB Costs and Net OPEB Obligation (Continued)

Funded Status and Funding Progress. The funded status of the plan as of July 1, 2010, was as follows: