mcgraw-hill/ irwin copyright © 2002 by the mcgraw-hill companies, inc. all rights reserved. 6-1...

TRANSCRIPT

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-11

Intercorporate Transfers of Services and Noncurrent Assets

6Electronic Presentation by

Douglas Cloud Pepperdine University

Baker / Lembke / KingBaker / Lembke / King

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

Intercorporate Transfers• A parent company and its subsidiaries often

engage in a variety of transactions among themselves.

• For example, manufacturing companies often have subsidiaries that develop raw materials or produce components to be included in the products of affiliated companies.

• These transactions between related companies are referred to as intercorporate transfers.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

• The central idea of consolidated financial statements is that they report on the activities of the consolidating affiliates as if the separate affiliates actually constitute a single company.

• Because single companies are not permitted to reflect internal transactions in their financial statements, consolidated entities also must exclude from their financial statements the effects of transactions that are contained totally within the consolidated entity.

Intercorporate Transfers

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

• Building on the basic consolidation procedures presented in earlier chapters, this chapter and the next two deal with the effects of intercorporate transfers.

• This chapter deals with intercorporate services (e.g., consulting) and sales of fixed assets, while intercorporate sales of inventory and intercorporate debt transfers are discussed in Chapters 7 and 8, respectively.

Intercorporate Transfers

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

• All aspects of intercorporate transfers must be eliminated in preparing consolidated financial statements so that the statements appear as if they were those of a single company.

• PSAK 4 mentions open account balances, security holdings, sales and purchases, and interest and dividends as examples of the intercompany balances and transactions that must be eliminated.

Intercorporate Transfers

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

• The focus in consolidation is on the single-entity concept rather than on the percentage of ownership.

• Once the conditions for consolidation are met, a company becomes part of a single economic entity and all transactions with related companies become internal transfers that must be eliminated fully, regardless of the level of ownership held.

Intercorporate Transfers

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-77Transactions of Affiliated CompaniesTransactions of Affiliated Companies

Parent Company

Parent Company

Subsidiary A

Subsidiary A

Subsidiary B

Subsidiary B

Consolidated EntityConsolidated Entity

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

• Profit of loss from selling an item to a related party normally is considered realized at the time of the sale from the selling company’s perspective, but the profit is not considered realized for consolidation purposes until confirmed, usually through resale to an unrelated party.

• This unconfirmed profit from an intercorporate transfer is referred to as unrealized intercompany profit.

Unrealized Profits and Losses

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

• From a consolidated viewpoint, the sale of an asset wholly within the consolidated entity involves only a change in the location of the asset and does not represent the culmination of the earning process.

• To culminate the earning process with respect to the consolidated entity, a sale must be made to a party external to the consolidated party.

Unrealized Profits and Losses

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-10

• The key to deciding when to report a transaction in the consolidated financial statements is to visualize the consolidated entity and determine whether a particular transaction occurs totally with the consolidated entity, in which case its effects must be excluded from the consolidated statements, or involves outsiders and thus constitutes a transaction of the consolidated entity.

Unrealized Profits and Losses

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1111Asset Transfers Involving Land

• When intercorporate transfers of noncurrent assets occur, adjustments often are needed in the preparation of consolidated financial statements for as long as the assets are held by the acquiring company.

• The simplest example of an intercorporate asset transfer is the intercorporate sale of land.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1212Intercorporate SalesIntercorporate Sales

PT AnakPT Anak

Consolidated EntityConsolidated Entity

PT IndukPT Induk

Purchase of Rp10,000,000

T1

T1–Purchase of land from outsider for Rp10,000,000.

T1–Purchase of land from outsider for Rp10,000,000.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1313Intercorporate SalesIntercorporate Sales

PT AnakPT Anak

Consolidated EntityConsolidated Entity

Sale/Purchase of Rp15,000,000

Gain of Rp5,000,000

PT IndukPT Induk

Purchase of Rp10,000,000

T1

T2–Land sale from PT Induk to PT Anak for Rp15,000,000.

T2–Land sale from PT Induk to PT Anak for Rp15,000,000.

T2

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1414Intercorporate SalesIntercorporate Sales

PT AnakPT Anak

Consolidated EntityConsolidated Entity

Sale/Purchase of Rp15,000,000

Gain of Rp5,000,000

Gain of Rp10,000,000

Sale of Rp25,000,000

PT IndukPT Induk

Purchase of Rp10,000,000

T1

T3–Land sale from PT Anak to outsider for Rp25,000,000.

T3–Land sale from PT Anak to outsider for Rp25,000,000.

T2 T3

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1515

PT IndukPT Induk PT AnakPT Anak

Consolidated EntityConsolidated Entity

Purchase of Rp10,000,000

Sale/Purchase of Rp15,000,000

Sale of Rp25,000,000

Gain of Rp5,000,000

Gain of Rp10,000,000

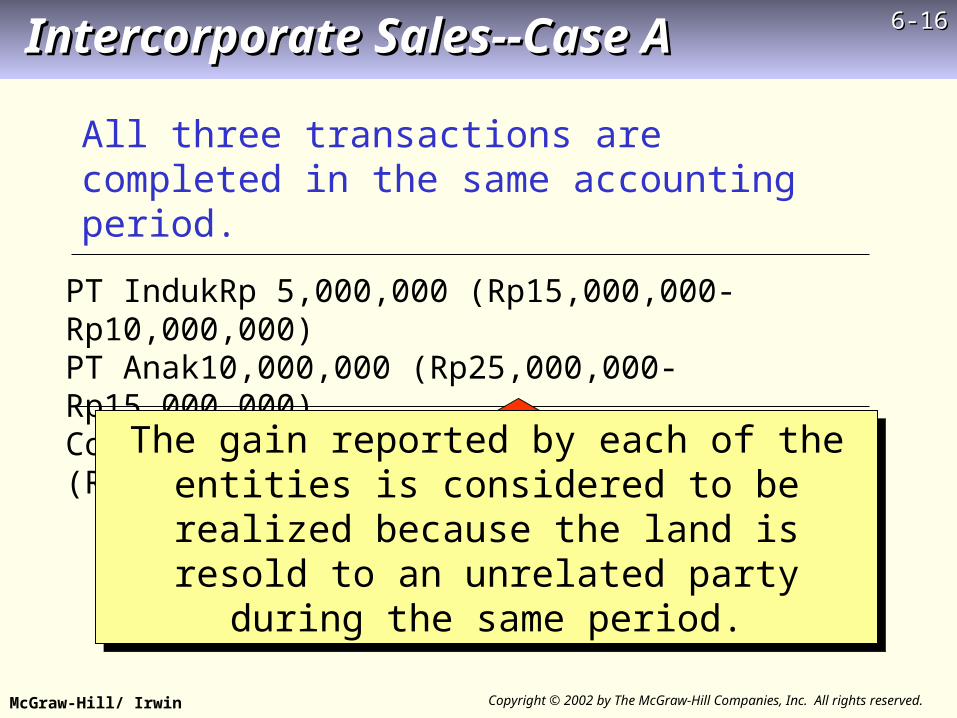

If all three transactions are completed in the same accounting period, the

parent records a gain of Rp5,000,000, thesubsidiary Rp10,000,000, and the consolidated

entity reports a gain of Rp15,000,000.

If all three transactions are completed in the same accounting period, the

parent records a gain of Rp5,000,000, thesubsidiary Rp10,000,000, and the consolidated

entity reports a gain of Rp15,000,000.

Intercorporate Sales--Case AIntercorporate Sales--Case A

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1616

All three transactions are completed in the same accounting period.

PT Induk Rp 5,000,000 (Rp15,000,000- Rp10,000,000)PT Anak 10,000,000 (Rp25,000,000- Rp15,000,000)Consolidated Entity 15,000,000 (Rp25,000 ,000- Rp10,000,000)

Gain

The gain reported by each of the entities is considered to be realized because the land is resold

to an unrelated party during the same period.

The gain reported by each of the entities is considered to be realized because the land is resold

to an unrelated party during the same period.

Intercorporate Sales--Case AIntercorporate Sales--Case A

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1717

Only transaction T1 is completed during the current period.

PT Induk Rp -0-PT Anak -0-Consolidated Entity -0-

No sale has been made by either of the affiliated companies, and no gains are reported or realized.

No sale has been made by either of the affiliated companies, and no gains are reported or realized.

Intercorporate Sales--Case BIntercorporate Sales--Case B

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1818

Only transactions T1 and T2 are completed during the current period.

PT Induk Rp5,000,000 (Rp15,000,000 - Rp10,000,000)PT Anak

-0-

Consolidated Entity

-0-

Intercorporate Sales--Case CIntercorporate Sales--Case C

GainThe gain reported by PT Induk is considered

unrealized from a consolidated point of view and is not reported in the consolidated income statement.

The gain reported by PT Induk is considered unrealized from a consolidated point of view and is not reported in the consolidated income statement.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-1919

Only transaction T3 is completed during the current period.

PT Induk Rp -0- PT Anak 10,000,000 (Rp25,000,000 - Rp15,000,000)Consolidated Entity 15,000,000 (Rp25,000,000– Rp10,000,000)

Intercorporate Sales--Case DIntercorporate Sales--Case D

Gain

PT Anak recognizes a gain equal to the difference between its selling price of Rp25,000 and cost of Rp15,000, while the consolidated entity reports a gain equal to the difference between the selling

price and the parent’s original cost.

PT Anak recognizes a gain equal to the difference between its selling price of Rp25,000 and cost of Rp15,000, while the consolidated entity reports a gain equal to the difference between the selling

price and the parent’s original cost.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2020

PT AnakPT AnakPT IndukPT Induk

Consolidated EntityConsolidated Entity

January 1, 20X1

Purchased land for Rp20,000,000

Overview of the Profit Elimination ProcessOverview of the Profit Elimination Process

PT Induk (Entry 1)PT Induk (Entry 1)PT Induk (Entry 1)PT Induk (Entry 1)

Jan. 1 Land 20,000,000 Cash 20,000,000

Record purchase of land.

Jan. 1 Land 20,000,000 Cash 20,000,000

Record purchase of land.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2121Overview of the Profit Elimination ProcessOverview of the Profit Elimination Process

PT IndukPT Induk PT AnakPT Anak

Consolidated EntityConsolidated Entity

July 1, 20X1

Intercorporate transfer of land Rp35,000,000

PT Induk (Entry 2)PT Induk (Entry 2)PT Induk (Entry 2)PT Induk (Entry 2)

July 1 Cash 35,000,000 Land 20,000,000 Gain on Sale of Land 15,000,000

Record sale of land to PT Anak.

July 1 Cash 35,000,000 Land 20,000,000 Gain on Sale of Land 15,000,000

Record sale of land to PT Anak.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2222

PT IndukPT Induk PT AnakPT Anak

Consolidated EntityConsolidated Entity

July 1, 20X1

Intercorporate transfer of land Rp35,000,000

PT Anak (Entry 3)PT Anak (Entry 3)PT Anak (Entry 3)PT Anak (Entry 3)

July 1 Land 35,000,000 Cash 35,000,000 Record purchase of land from PT Induk.

July 1 Land 35,000,000 Cash 35,000,000 Record purchase of land from PT Induk.

Overview of the Profit Elimination ProcessOverview of the Profit Elimination Process

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

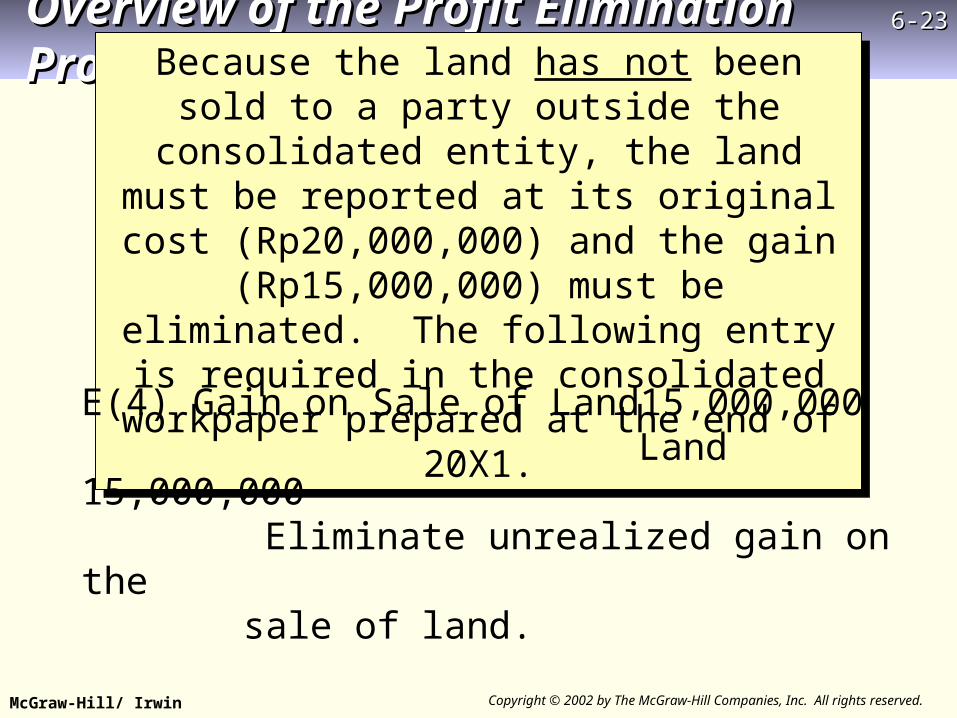

6-6-2323Overview of the Profit Elimination ProcessOverview of the Profit Elimination Process

Because the land has not been sold to a party outside the consolidated entity, the land must be reported at its original cost (Rp20,000,000) and

the gain (Rp15,000,000) must be eliminated. The following entry is required in the consolidated

workpaper prepared at the end of 20X1.

Because the land has not been sold to a party outside the consolidated entity, the land must be reported at its original cost (Rp20,000,000) and

the gain (Rp15,000,000) must be eliminated. The following entry is required in the consolidated

workpaper prepared at the end of 20X1.

E(4) Gain on Sale of Land 15,000,000 Land 15,000,000 Eliminate unrealized gain on the

sale of land.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2424Assignment of Unrealized Profit EliminationAssignment of Unrealized Profit Elimination

When a sale is from a parent to a subsidiary, referred to as a downstream sale, any gain or

loss on the transfer accrues to the stockholders of the parent company.

When the sale is from a subsidiary to its parent, an upstream sale, any gain or loss accrues to the stockholders of the subsidiary, which is

apportioned between the parent company and the noncontrolling shareholders.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2525Downstream SaleDownstream Sale

1. PT Induk purchases 80 percent of the stock of PT Anak on December 31, 20X1, at the stock’s book value of Rp240,000,000.

2. On July 1, 20X1, PT Induk sells land to PT Anak for Rp35,000,000. The land originally cost PT Induk Rp20,000,000.

3. During 20X1, PT Anak reports net income of Rp50,000,000 and declares dividends of Rp30,000,000.

4. PT Induk accounts for its investment in PT Anak using the basic equity method.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2626

Basic Equity MethodBasic Equity Method

Downstream SaleDownstream Sale

(6) Investment in PT Anak Stock 40,000,000Income from Subsidiary 40,000,000

Record equity-method income

(5) Cash 24,000,000Investment in PT Anak Stock 24,000,000

Record dividend from PT Anak.

Rp50,000,000 Rp50,000,000 x .80x .80

Rp30,000,000 Rp30,000,000 x .80x .80

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2727

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

Income from Subsidiary 40,000

Dividends Declared (60,000 (30,000)

Investment in PT Anak 256,000

An entry is needed to eliminate the changes in PT Induk’s investment account for the year, the income

from PT Anak recognized by PT Induk, and PT Induk’s share of PT Anak’ dividends.

An entry is needed to eliminate the changes in PT Induk’s investment account for the year, the income

from PT Anak recognized by PT Induk, and PT Induk’s share of PT Anak’ dividends.

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

)

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2828

Income from Subsidiary 40,000 (7) 40,000

Dividends Declared (60,000 (30,000) (7) 24,000

Investment in PT Anak 256,000 (7) 16,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is needed to eliminate the changes in PT Induk’s investment account for the year, the income

from PT Anak recognized by PT Induk, and PT Induk’s share of PT Anak’ dividends.

An entry is needed to eliminate the changes in PT Induk’s investment account for the year, the income

from PT Anak recognized by PT Induk, and PT Induk’s share of PT Anak’ dividends.

)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-2929

An entry is necessary to assign a share of PT Anak’income to the noncontrolling stockholders and eliminate

their share of PT Anak’ dividends.

An entry is necessary to assign a share of PT Anak’income to the noncontrolling stockholders and eliminate

their share of PT Anak’ dividends.

Income to Noncontrolling Interest

Dividends Declared (60,000) (30,000) (7) 24,000

Noncontrolling Interest

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3030

Income to Noncontrolling Interest (8) 10,000 (10,000)

Dividends Declared (60,000) (30,000) (7) 24,000

(8) 6,000 (60,000)Noncontrolling Interest (8) 4,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is necessary to assign a share of PT Anak’income to the noncontrolling stockholders and eliminate

their share of PT Anak’ dividends.

An entry is necessary to assign a share of PT Anak’income to the noncontrolling stockholders and eliminate

their share of PT Anak’ dividends.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3131

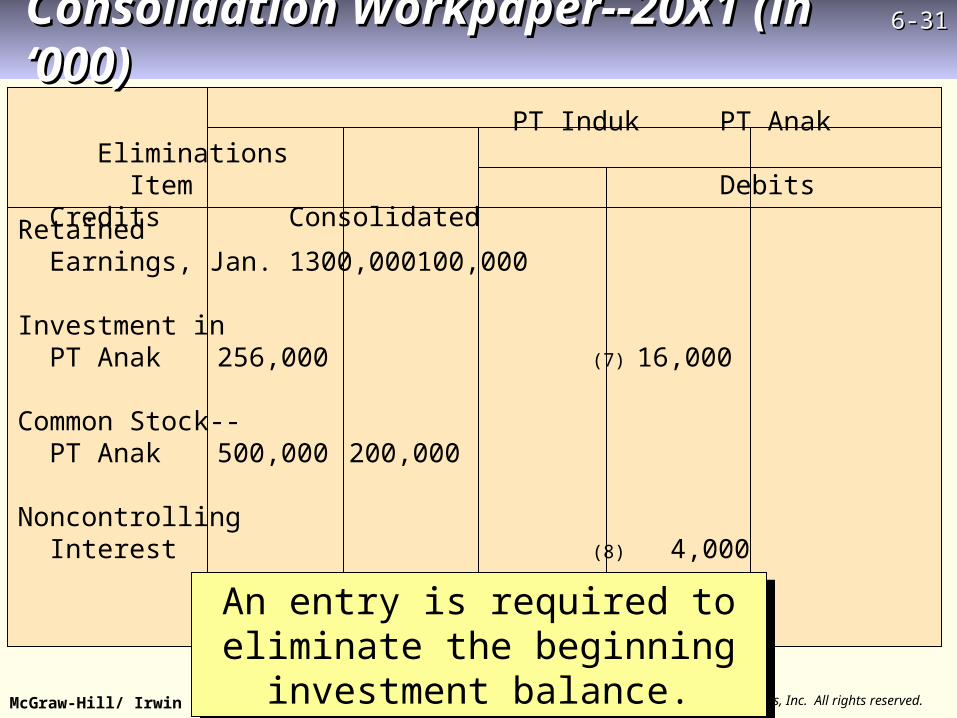

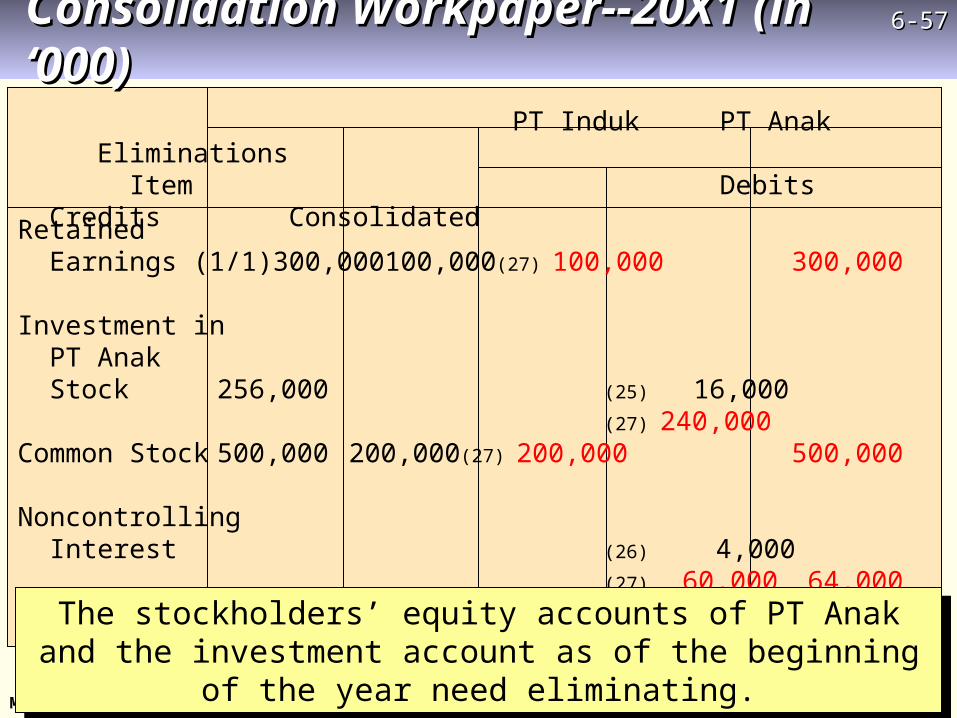

Retained Earnings, Jan. 1 300,000 100,000

Investment in PT Anak 256,000 (7) 16,000

Common Stock-- PT Anak 500,000 200,000

Noncontrolling Interest (8) 4,000

An entry is required to eliminate the beginning investment balance.

An entry is required to eliminate the beginning investment balance.

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

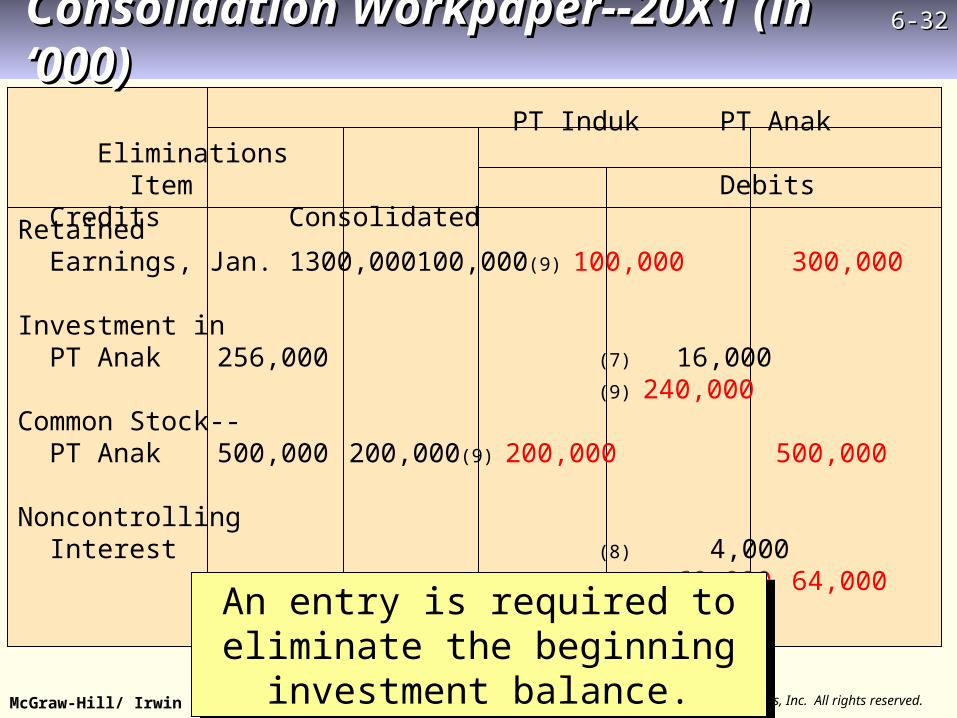

6-6-3232

Retained Earnings, Jan. 1 300,000 100,000 (9) 100,000 300,000

Investment in PT Anak 256,000 (7) 16,000

(9) 240,000Common Stock-- PT Anak 500,000 200,000 (9) 200,000 500,000

Noncontrolling Interest (8) 4,000

(9) 60,000 64,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is required to eliminate the beginning investment balance.

An entry is required to eliminate the beginning investment balance.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3333

Gain on Sale of Land 15,000 (10) 15,000 0

Land 155.000 75.000 (10) 15,000 215.000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is needed to eliminate the changes in PT Induk’s investment account for the year, the income

from PT Anak recognized by PT Induk, and PT Induk’s share of PT Anak’ dividends.

An entry is needed to eliminate the changes in PT Induk’s investment account for the year, the income

from PT Anak recognized by PT Induk, and PT Induk’s share of PT Anak’ dividends.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3434

Downstream Sales

On Subsequent year, not yet sold:

E(17) Retained Earnings 15,000,000

Land 15,000,000

Eliminate unrealized gain on the sale of land

If Sold on Subsequent year:

E(19) Retained Earnings 15,000,000

Gain on Sale of Land 15,000,000

Eliminate unrealized gain on the sale of land

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3535Upstream Sales - Basic Equity Method Entries—20X1Upstream Sales - Basic Equity Method Entries—20X1

(12) Investment in PT Anak Stock 52,000,000Income from Subsidiary 52,000,000

Record equity-method income

(11) Cash 24,000,000Investment in PT Anak 24,000,000

Record dividend from PT Anak

Rp65,000,000 Rp65,000,000 x .80x .80

Rp30,000,000 Rp30,000,000 x .80x .80

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3636

An entry is needed to eliminate the income from the subsidiary.

An entry is needed to eliminate the income from the subsidiary.

Income from Subsidiary 52,000

Dividends Declared (60,000) (30,000)

Investments in PT Anak Stock 268,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3737

An entry is needed to eliminate the income from the subsidiary.

An entry is needed to eliminate the income from the subsidiary.

Income from Subsidiary 52,000 (13) 52,000

Dividends Declared (60,000) (30,000) (13) 24,000

Investments in PT Anak Stock 268,000 (13) 28,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3838

Income to Noncontrolling Interest

Dividends Declared (60,000) (30,000) (13) 24,000

Noncontrolling Interest

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is required to assign income to the noncontrolling interest.

An entry is required to assign income to the noncontrolling interest.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-3939

An entry is required to assign income to the noncontrolling interest.

An entry is required to assign income to the noncontrolling interest.

Income to Noncontrolling Interest (14) 10,000 (10,000)

Dividends Declared (60,000) (30,000) (13) 24,000

(14) 6,000

Noncontrolling Interest (14) 4,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4040

An entry is needed to eliminate the beginning investment balance.

An entry is needed to eliminate the beginning investment balance.

Retained Earnings (1/1) 300,000 100,000

Investment in PT Anak Stock 268,000 (13) 28,000

Common Stock 500,000 200,000

Noncontrolling Interest (14) 4,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4141

An entry is needed to eliminate the beginning investment balance.

An entry is needed to eliminate the beginning investment balance.

Retained Earnings (1/1) 300,000 100,000 (15)100,000 300,000

Investment in PT Anak Stock 268,000 (13) 28,000

(15) 240,000Common Stock 500,000 200,000 (15)200,000

Noncontrolling Interest (14) 4,000

(15) 60,000 64,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

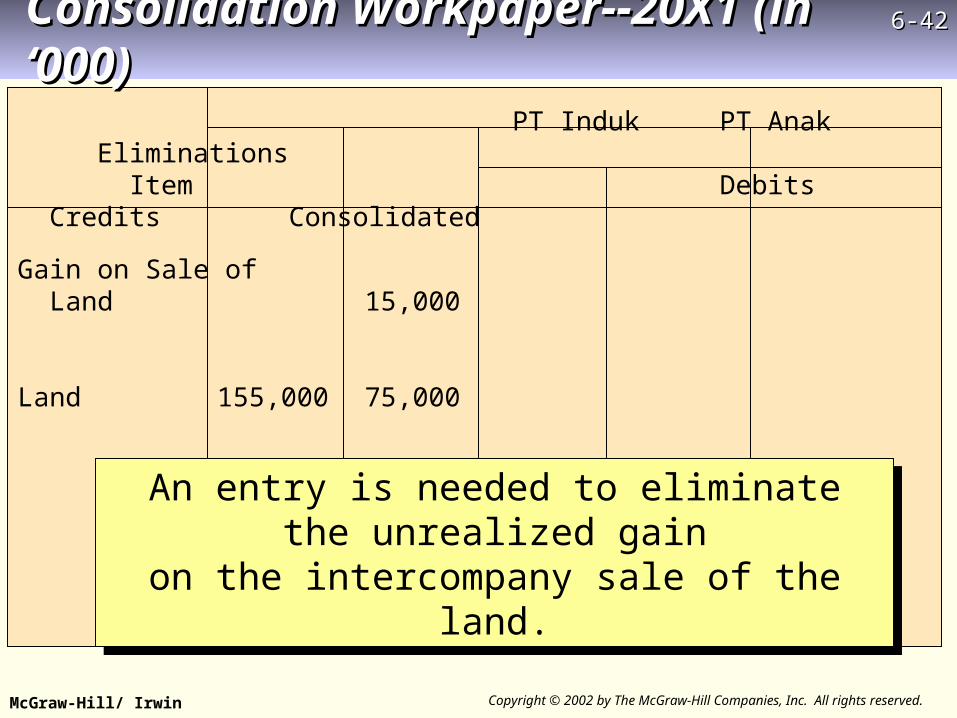

6-6-4242

An entry is needed to eliminate the unrealized gainon the intercompany sale of the land.

An entry is needed to eliminate the unrealized gainon the intercompany sale of the land.

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

Gain on Sale of Land 15,000

Land 155,000 75,000

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4343

Gain on Sale of Land 15,000 (16) 15,000

Land 155,000 75,000 (16) 15,000 215,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is needed to eliminate the unrealized gainon the intercompany sale of the land.

An entry is needed to eliminate the unrealized gainon the intercompany sale of the land.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4444Consolidated Net Income--20X1Consolidated Net Income--20X1

PT Induk’s separate income Rp155,000,000 Less: Unrealized intercompany profit on downstream land sale -15,000,000PT Induk’s separate realized income Rp140,000,000 PT Induk’s share of PT Anak’s income:

PT Anak’ net income Rp50,000,000PT Induk’s proportionate share x .80 40,000,000

Consolidated net income, 20X1 Rp180,000,000

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4545

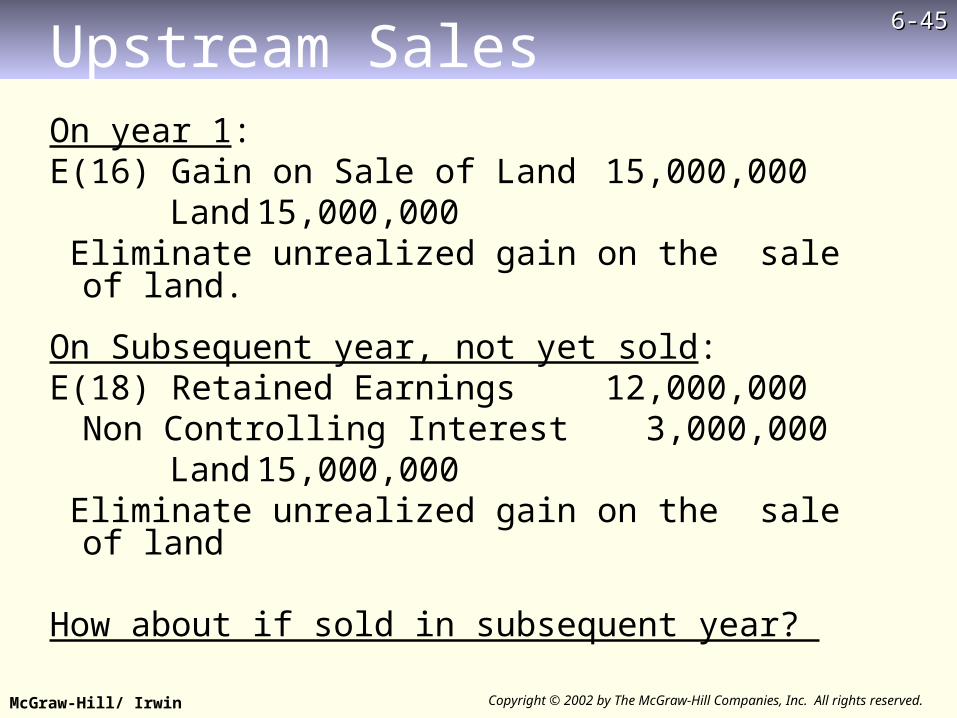

Upstream SalesOn year 1: E(16) Gain on Sale of Land 15,000,000

Land 15,000,000 Eliminate unrealized gain on the sale of land.

On Subsequent year, not yet sold: E(18) Retained Earnings 12,000,000

Non Controlling Interest 3,000,000 Land 15,000,000

Eliminate unrealized gain on the sale of land

How about if sold in subsequent year?

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4646

Transfers Involving Depreciable Assets

• Unrealized intercompany profits on a depreciable or amortizable asset are viewed as being realized gradually over the remaining economic life of the asset as it is used by the purchasing affiliate in generating revenue from unaffiliated parties.

• In effect, a portion of the unrealized gain or loss is realized each period as benefits are derived from the asset and its service potential expires.

• The amount of depreciation recognized on a company’s books each period on an asset purchased from an affiliate is based on the intercorporate transfer price.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4747

• Yet, from a consolidated viewpoint, depreciation must be based on the cost of the asset to the consolidated entity, which is the cost of the asset to the related company that originally purchased it from an outsider.

• Eliminating entries are needed in the consolidation workpaper to restate the asset, associated accumulated depreciation, and depreciation expense to the amounts that would appear in the financial statements if there had been no intercompany transfer.

• Because the intercompany sale takes place totally within the consolidated entity, the consolidated financial statements must appear as if the intercompany transfer had never occurred.

Transfers Involving Depreciable Assets

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4848Downstream Sale – Depreciable AssetsDownstream Sale – Depreciable Assets

PT IndukPT Induk

Consolidated EntityConsolidated Entity

December 31, 20W8

Purchase equipment for Rp9,000,000

PT AnakPT Anak

Equipment Estimated Useful Life: 10 yearsEquipment Estimated Useful Life: 10 yearsEquipment Estimated Useful Life: 10 yearsEquipment Estimated Useful Life: 10 years

Dec. 31 Equipment 9,000,000 Cash 9,000,000

Record purchase of equipment.

Dec. 31 Equipment 9,000,000 Cash 9,000,000

Record purchase of equipment.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-4949

Consolidated EntityConsolidated Entity

PT IndukPT Induk PT AnakPT AnakDecember 31, 20X1

Intercorporate transfer of equipment

Rp7,000,000

PT Anak (Entry 20)PT Anak (Entry 20)PT Anak (Entry 20)PT Anak (Entry 20)

Dec. 31 Equipment 7,000,000 Cash 7,000,000

Record purchase of equipment.

Dec. 31 Equipment 7,000,000 Cash 7,000,000

Record purchase of equipment.

Downstream SaleDownstream Sale

PT Induk (Entry 21)PT Induk (Entry 21)PT Induk (Entry 21)PT Induk (Entry 21)

Dec. 31 Depreciation Expense 900,000 Accumulated Depreciation 900,000

Record 20X1 depreciation expense on equipment sold.

Dec. 31 Depreciation Expense 900,000 Accumulated Depreciation 900,000

Record 20X1 depreciation expense on equipment sold.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5050Downstream SaleDownstream Sale

PT Induk records the sale of the equipment at the end of 20X1 and recognizes the gain on the sale:

PT Induk (Entry 22)PT Induk (Entry 22)PT Induk (Entry 22)PT Induk (Entry 22)

Dec. 31 Cash 7,000,000Accumulated Depreciation 2,700,000

Equipment 9,000,000 Gain on Sale of Equipment 700,000

Record sale of equipment.

Dec. 31 Cash 7,000,000Accumulated Depreciation 2,700,000

Equipment 9,000,000 Gain on Sale of Equipment 700,000

Record sale of equipment.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

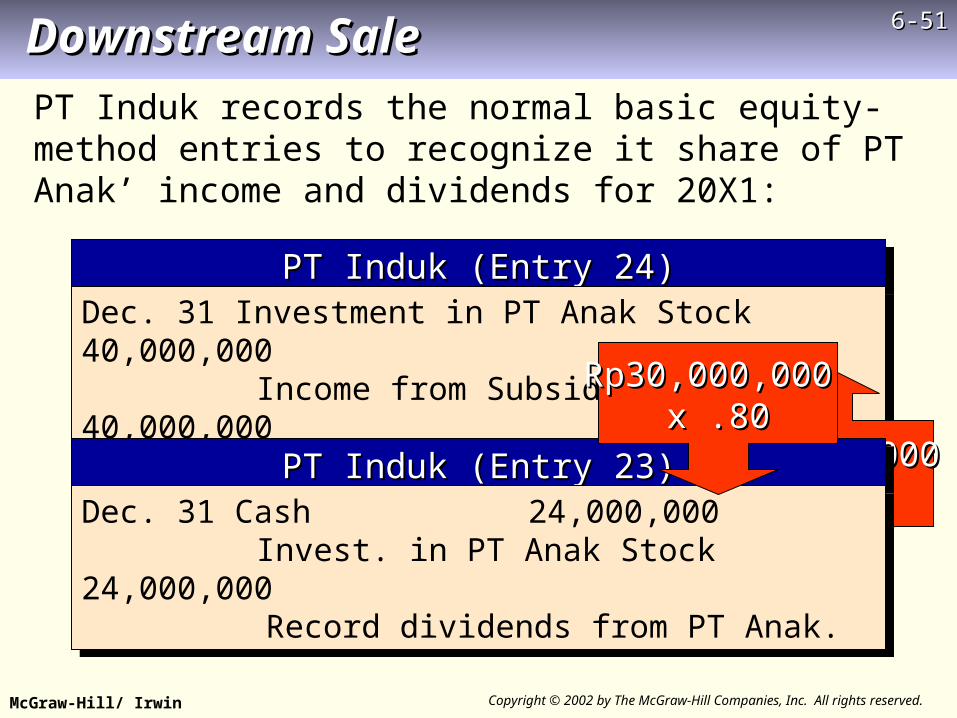

6-6-5151Downstream SaleDownstream Sale

PT Induk records the normal basic equity-method entries to recognize it share of PT Anak’ income and dividends for 20X1:

PT Induk (Entry 2PT Induk (Entry 244))PT Induk (Entry 2PT Induk (Entry 244))

Dec. 31 Investment in PT Anak Stock 40,000,000 Income from Subsidiary 40,000,000

Record equity-method income.

Dec. 31 Investment in PT Anak Stock 40,000,000 Income from Subsidiary 40,000,000

Record equity-method income.

Rp50,000,000 Rp50,000,000 x .80x .80

PT Induk (Entry 2PT Induk (Entry 233))PT Induk (Entry 2PT Induk (Entry 233))

Dec. 31 Cash 24,000,000 Invest. in PT Anak Stock 24,000,000

Record dividends from PT Anak.

Dec. 31 Cash 24,000,000 Invest. in PT Anak Stock 24,000,000

Record dividends from PT Anak.

Rp30,000,000 Rp30,000,000 x .80x .80

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5252

Income from Subsidiary 40,000

Dividends Declared (60,000 (30,000)

Investment in PT Anak 256,000

An entry is needed to eliminate the income and dividendsfrom PT Anak recognized by PT Induk and the change in

the investment account for the year.

An entry is needed to eliminate the income and dividendsfrom PT Anak recognized by PT Induk and the change in

the investment account for the year.

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5353

Income from Subsidiary 40,000 (25) 40,000

Dividends Declared (60,000 (30,000) (25) 24,000

Investment in PT Anak 256,000 (25) 16,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is needed to eliminate the income and dividendsfrom PT Anak recognized by PT Induk and the change in

the investment account for the year.

An entry is needed to eliminate the income and dividendsfrom PT Anak recognized by PT Induk and the change in

the investment account for the year.

)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5454

Income to Non- controlling Interest

Dividends Declared (60,000) (30,000) (25) 24,000

Noncontrolling Interest

An entry is required to assign incometo the noncontrolling interest.

An entry is required to assign incometo the noncontrolling interest.

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5555

Income to Non- controlling Interest (26) 10,000 (10,000)

Dividends Declared (60,000) (30,000) (25) 24,000

(26) 6,000 (60,000) Noncontrolling Interest (26) 4,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is required to assign incometo the noncontrolling interest.

An entry is required to assign incometo the noncontrolling interest.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5656

Retained Earnings (1/1) 300,000 100,000

Investment in PT Anak Stock 256,000 (25) 16,000

Common Stock 500,000 200,000

Noncontrolling Interest (26) 4,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5757

Retained Earnings (1/1) 300,000 100,000 (27) 100,000 300,000

Investment in PT Anak Stock 256,000 (25) 16,000

(27) 240,000Common Stock 500,000 200,000 (27) 200,000 500,000

Noncontrolling Interest (26) 4,000

(27) 60,000 64,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5858

The unrealized gain on downstream saleof equipment needs eliminating.

The unrealized gain on downstream saleof equipment needs eliminating.

Gain on Sale of Equipment 700

Buildings and Equipment 791,000 607,000

Accumulated Depreciation 447,300 320,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-5959

Gain on Sale of Equipment 700 (28) 700

Buildings and Equipment 791,000 607,000 (28) 2,000 1,400,000

Accumulated Depreciation 447,300 320,000 (28) 2,700 770,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

The unrealized gain on downstream saleof equipment needs eliminating.

The unrealized gain on downstream saleof equipment needs eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6060

In 20X2

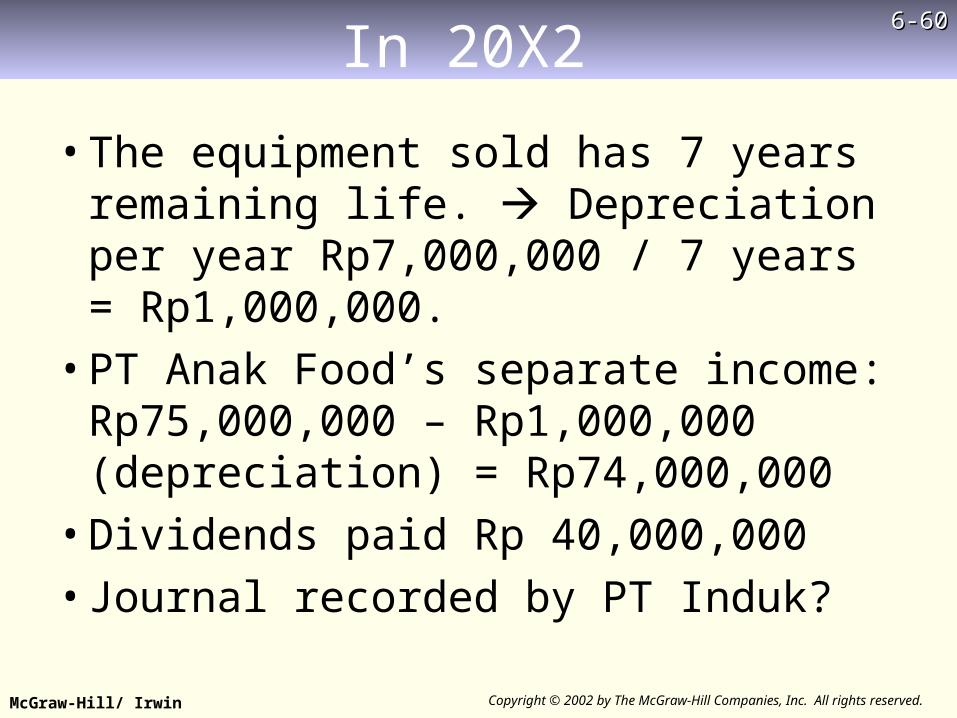

• The equipment sold has 7 years remaining life. Depreciation per year Rp7,000,000 / 7 years = Rp1,000,000.

• PT Anak Food’s separate income: Rp75,000,000 – Rp1,000,000 (depreciation) = Rp74,000,000

• Dividends paid Rp 40,000,000

• Journal recorded by PT Induk?

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6161Upstream Sales - Basic Equity Method Entries—20X1Upstream Sales - Basic Equity Method Entries—20X1

(12) Investment in PT Anak Stock 59,200,000Income from Subsidiary 59,200,000

Record equity-method income

(11) Cash 32,000,000Investment in PT Anak Stock 32,000,000

Record dividend from PT Anak.

Rp74,000,000 Rp74,000,000 x .80x .80

Rp40,000,000 Rp40,000,000 x .80x .80

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6262

An entry is needed to eliminate income form the subsidiary.

An entry is needed to eliminate income form the subsidiary.

Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

Income from Subsidiary 59,200

Dividends Declared (60,000) (40,000)

Investments in PT Anak Stock 283,200

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6363

An entry is needed to eliminate income form the subsidiary.

An entry is needed to eliminate income form the subsidiary.

Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

Income from Subsidiary 59,200 (32) 59,200

Dividends Declared (60,000) (40,000) (32) 32,000

Investments in PT Anak Stock 283,200 (32) 27,200

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6464Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

An entry is required to assign income to the noncontrolling interest.

An entry is required to assign income to the noncontrolling interest.

Income to Noncontrolling Interest

Dividends Declared (60,000) (40,000) (32) 32,000

Noncontrolling Interest

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6565Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

An entry is required to assign income to the noncontrolling interest.

An entry is required to assign income to the noncontrolling interest.

Income to Noncontrolling Interest (33) 14,800 (14,800)

Dividends Declared (60,000) (40,000) (32) 32,000

(33) 8,000 (60,000)

Noncontrolling Interest (33) 6,800

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6666Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

Retained Earnings (1/1) 420,700 120,000

Investment in PT Anak Stock 283,200 (32) 27,200

Common Stock 500,000 200,000

Noncontrolling Interest (33) 6,800

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6767Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

Retained Earnings (1/1) 420,700 120,000 (34)120,000

Investment in PT Anak Stock 283,200 (32) 27,200

(34) 256,000Common Stock 500,000 200,000 (34)200,000 500,000

Noncontrolling Interest (33) 6,800

(34) 64,000 70,800

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6868Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

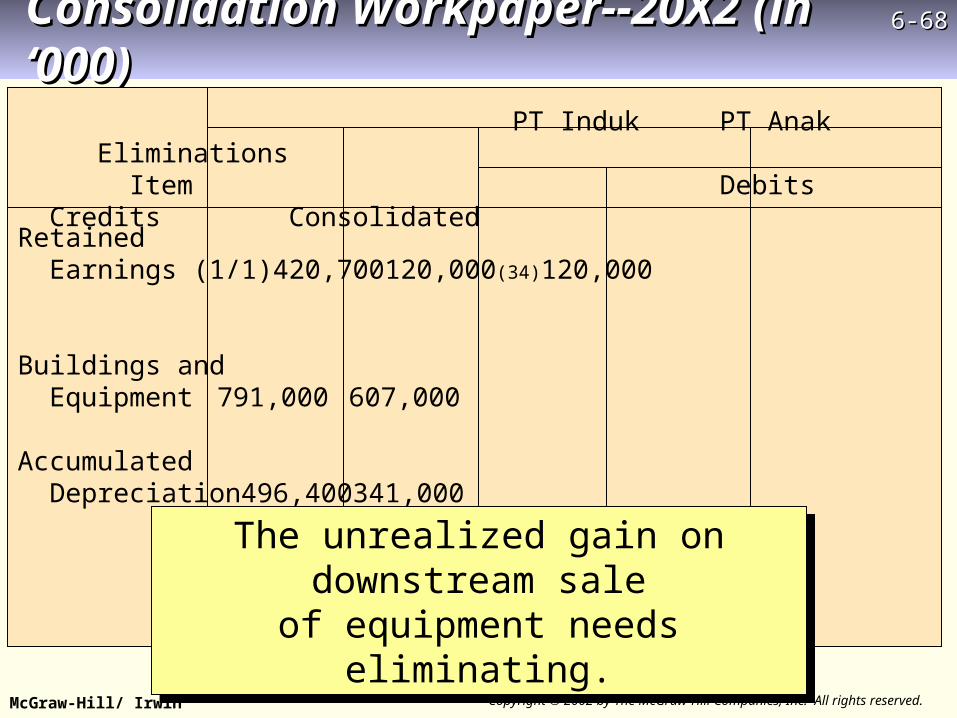

The unrealized gain on downstream saleof equipment needs eliminating.

The unrealized gain on downstream saleof equipment needs eliminating.

Retained Earnings (1/1) 420,700 120,000 (34)120,000

Buildings and Equipment 791,000 607,000

Accumulated Depreciation 496,400 341,000

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-6969Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

The unrealized gain on downstream saleof equipment needs eliminating.

The unrealized gain on downstream saleof equipment needs eliminating.

Retained Earnings (1/1) 420,700 120,000 (34)120,000

(35) 700 420,000

Buildings and Equipment 791,000 607,000 (35) 2,000

Accumulated Depreciation 496,400 341,000 (35) 2,700

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7070Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

An entry is required to adjust depreciation for realization of the intercompany gain.

An entry is required to adjust depreciation for realization of the intercompany gain.

Depreciation and Amortization 49,100 21,000

Accumulated Depreciation 496,400 341,000 (35) 2,700

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7171Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

An entry is required to adjust depreciation for realization of the intercompany gain.

An entry is required to adjust depreciation for realization of the intercompany gain.

Depreciation and Amortization 49,100 21,000 (36) 100 70,000

Accumulated Depreciation 496,400 341,000 (36) 100 (35) 2,700 840,000

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7272

Notes

Journal 35 and 36 can be united into:

Building and Equipment 2,000,000

Retained Earnings 700,000

Depreciation Expense 100,000

Accumulated Depreciation 2,600,000

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7373Consolidated Net Income--20X2Consolidated Net Income--20X2

PT Induk’s separate incomeRp160,900,000

Partial realization of intercompany gain on downstream sale of equipment

100,000PT Induk’s separate realized income

Rp161,000,000 PT Induk’s share of PT Anak’s income:

PT Anak’ net income Rp74,000,000PT Induk’s proportionate share x .80 59,200,000

Consolidated net income, 20X2Rp220,200,000

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7474Subsequent years, if not sold

Building and Equipment 2,000,000Retained Earnings 600,000

Accumulated Depreciation 2,600,000

Accumulated Depreciation 100,000Depreciation Expense 100,000

OR: Building and Equipment 2,000,000Retained Earnings 600,000

Depreciation Expense 100,000Accumulated Depreciation 2,500,000

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7575Upstream SaleUpstream SalePT Anak sold Equipment for Rp7,000,000 (which previously bought at Rp9,000,000 and had been depreciated for 2 years). PT Anak records the sale of the equipment at the end of 20X1 and recognizes the gain on the sale:

PT AnakPT AnakPT AnakPT Anak

Dec. 31 Depreciation Expense 900,000

Accumulated Depreciation 900 ,000 Record sale of equipment.

Dec. 31 Depreciation Expense 900,000

Accumulated Depreciation 900 ,000 Record sale of equipment.

PT AnakPT AnakPT AnakPT AnakDec. 31 Cash 7,000,000Accumulated Depreciation 2,700 ,000

Equipment 9,000,000 Gain on Sale of Equipment 700 ,000

Record sale of equipment.

Dec. 31 Cash 7,000,000Accumulated Depreciation 2,700 ,000

Equipment 9,000,000 Gain on Sale of Equipment 700 ,000

Record sale of equipment.

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7676Uostream SaleUostream Sale

PT Induk records the purchase of the equipment at the end of 20X1 as follows:

PT Induk (Entry PT Induk (Entry 4141))PT Induk (Entry PT Induk (Entry 4141))

Dec. 31 Equipment 7,000,000

Cash 7,000,000

Dec. 31 Equipment 7,000,000

Cash 7,000,000

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7777Upstream SaleUpstream Sale

PT Induk records the normal basic equity-method entries to recognize it share of PT Anak’ income and dividends for 20X1:

PT Induk (Entry PT Induk (Entry 4343))PT Induk (Entry PT Induk (Entry 4343))

Dec. 31 Investment in PT Anak Stock 40,560,000 Income from Subsidiary 40,560 ,000

Record equity-method income.

Dec. 31 Investment in PT Anak Stock 40,560,000 Income from Subsidiary 40,560 ,000

Record equity-method income.

Rp50,700 Rp50,700 x .80x .80

PT Induk (Entry PT Induk (Entry 4242))PT Induk (Entry PT Induk (Entry 4242))

Dec. 31 Cash 24,000,000 Invest. in PT Anak Stock 24,000,000

Record dividends from PT Anak.

Dec. 31 Cash 24,000,000 Invest. in PT Anak Stock 24,000,000

Record dividends from PT Anak.

Rp30,000,000 Rp30,000,000 x .80x .80

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7878

Income from Subsidiary 40,560

Dividends Declared (60,000 (30,000)

Investment in PT Anak 256,560

An entry is needed to eliminate the income and dividendsfrom PT Anak recognized by PT Induk and the change in

the investment account for the year.

An entry is needed to eliminate the income and dividendsfrom PT Anak recognized by PT Induk and the change in

the investment account for the year.

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-7979

Income from Subsidiary 40,560 (44) 40,560

Dividends Declared (60,000 (30,000) (44) 24,000

Investment in PT Anak 256,560 (44) 16,560

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is needed to eliminate the income and dividendsfrom PT Anak recognized by PT Induk and the change in

the investment account for the year.

An entry is needed to eliminate the income and dividendsfrom PT Anak recognized by PT Induk and the change in

the investment account for the year.

)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8080

Income to Non- controlling Interest

Dividends Declared (60,000) (30,000) (44) 24,000

Noncontrolling Interest

An entry is required to assign incometo the noncontrolling interest.

An entry is required to assign incometo the noncontrolling interest.

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8181

Income to Non- controlling Interest (45) 10,000 (10,000)

Dividends Declared (60,000) (30,000) (44) 24,000

(45) 6,000 (60,000) Noncontrolling Interest (45) 4,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

An entry is required to assign incometo the noncontrolling interest.

An entry is required to assign incometo the noncontrolling interest.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8282

Retained Earnings (1/1) 300,000 100,000

Investment in PT Anak Stock 256,000 (44) 16,560

Common Stock 500,000 200,000

Noncontrolling Interest (45) 4,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8383

Retained Earnings (1/1) 300,000 100,000 (46) 100,000 300,000

Investment in PT Anak Stock 256,560 (44) 16,560

(46) 240,000Common Stock 500,000 200,000 (46) 200,000 500,000

Noncontrolling Interest (45) 4,000

(46) 60,000 64,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8484

The unrealized gain on upstream saleof equipment needs eliminating.

The unrealized gain on upstream saleof equipment needs eliminating.

Gain on Sale of Equipment 700

Buildings and Equipment 807,000 591,000

Accumulated Depreciation 450,000 317,300

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8585

Gain on Sale of Equipment 700 (47) 700

Buildings and Equipment 807,000 591,000 (47) 2,000 1,400,000

Accumulated Depreciation 450,000 317,300 (47) 2,700 770,000

Consolidation Workpaper--20X1Consolidation Workpaper--20X1 (in ‘000) (in ‘000)

The unrealized gain on upstream saleof equipment needs eliminating.

The unrealized gain on upstream saleof equipment needs eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8686

On 20X2

• The equipment sold has 7 years remaining life. Depreciation per year Rp7,000,000 / 7 years = Rp1,000,000.

• PT Anak Food’s separate income: Rp75,900,000

• Dividends paid Rp 40,000,000

• Journal recorded by PT Induk?

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8787Upstream Sales - Basic Equity Method Entries—Upstream Sales - Basic Equity Method Entries—20X120X1

Investment in PT Anak Stock 60,720,000Income from Subsidiary 60,720,000

Record equity-method income

Cash 32,000,000Investment in PT Anak Stock 32,000,000

Record dividend from PT Anak.

Rp75,900Rp75,900,000,000 x .80x .80

Rp40,000,000 Rp40,000,000 x .80x .80

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8888

An entry is needed to eliminate income form the subsidiary.

An entry is needed to eliminate income form the subsidiary.

Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

Income from Subsidiary 60,720

Dividends Declared (60,000) (40,000)

Investments in PT Anak Stock 285,280

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-8989

An entry is needed to eliminate income form the subsidiary.

An entry is needed to eliminate income form the subsidiary.

Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

Income from Subsidiary 60,720 (48) 60,720

Dividends Declared (60,000) (40,000) (48) 32,000

Investments in PT Anak Stock 285,280 (48) 28,720

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9090Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

An entry is required to assign income to the noncontrolling interest.

An entry is required to assign income to the noncontrolling interest.

Income to Noncontrolling Interest

Dividends Declared (60,000) (40,000) (48) 32,000

Noncontrolling Interest

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9191Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

An entry is required to assign income to the noncontrolling interest.

An entry is required to assign income to the noncontrolling interest.

Income to Noncontrolling Interest (49) 15,200 (15,200)

Dividends Declared (60,000) (40,000) (48) 32,000

(49) 8,000 (60,000)

Noncontrolling Interest (49) 7,200

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9292Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

Retained Earnings (1/1) 420,560 120,700

Investment in PT Anak Stock 285,280 (48) 28,720

Common Stock 500,000 200,000

Noncontrolling Interest (49) 7,200

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9393Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

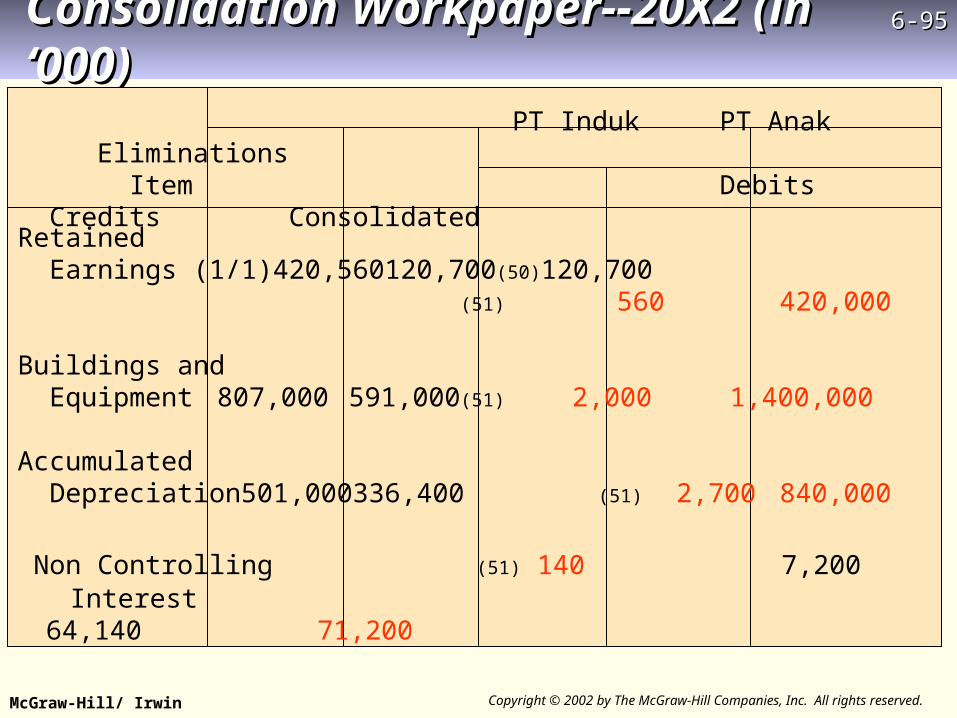

Retained Earnings (1/1) 420,560 120,700 (50)120,700

Investment in PT Anak Stock 285,280 (48) 28,720

(50) 256,560Common Stock 500,000 200,000 (50)200,000 500,000

Noncontrolling Interest (49) 7,200

(50) 64,140 71,340

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

The stockholders’ equity accounts of PT Anak and the investment account as of the beginning of the year need eliminating.

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9494Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

The unrealized gain on downstream saleof equipment needs eliminating.

The unrealized gain on downstream saleof equipment needs eliminating.

Retained Earnings (1/1) 420,560 120,700 (50)120,700

Buildings and Equipment 807,000 591,000

Accumulated Depreciation 501,000 336,400

Non Controlling 7,200Interest 64,140

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9595Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

Retained Earnings (1/1) 420,560 120,700 (50)120,700

(51) 560 420,000

Buildings and Equipment 807,000 591,000 (51) 2,000 1,400,000

Accumulated Depreciation 501,000 336,400 (51) 2,700 840,000

Non Controlling (51) 140 7,200Interest 64,140 71,200

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9696Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

An entry is required to adjust depreciation for realization of the intercompany gain.

An entry is required to adjust depreciation for realization of the intercompany gain.

Depreciation and Amortization 49,100 21,000

Accumulated Depreciation 501,000 336,400 (51) 2,700

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9797Consolidation Workpaper--20X2Consolidation Workpaper--20X2 (in ‘000) (in ‘000)

An entry is required to adjust depreciation for realization of the intercompany gain.

An entry is required to adjust depreciation for realization of the intercompany gain.

Depreciation and Amortization 49,100 21,000 (52) 100 70,000

Accumulated Depreciation 501,000 336,400 (52) 100 (51) 2,700 840,000

PT Induk PT Anak Eliminations Item Debits Credits Consolidated

McGraw-Hill/ Irwin Copyright © 2002 by The McGraw-Hill Companies, Inc. All rights reserved.

6-6-9898Chapter SixChapter Six

THE ENDTHE END