may 29, 2011 emerging indian pharma multinationals ... · pdf fileemerging indian pharma...

TRANSCRIPT

1

May 29, 2011

_______________________________________________________________________________

Emerging Indian pharma multinationals: latecomer

catch-up strategies in a globalised high tech industry ___________________________________________________________________

Gert Bruche

Berlin School of Economics and Law

Badensche Str. 52, 10825 Berlin, Germany

E-mail: [email protected]

Abstract:

Leading Indian pharmaceutical companies (IPCs) are frequently taken as prime examples

of the new ‘emerging multinationals’ from developing countries. Business researchers

have studied their catch-up and internationalisation strategies from a resource-based

perspective, often in reference to the specific institutional changes in the Indian economy.

While these studies identify significant advances in IPCs' capabilities and

internationalisation, the global competitive position they have achieved and the reach of

this position remain elusive. By taking a ‘global industry perspective’ the paper argues that

IPCs are still no serious competitive challenge to Big Pharma and have to largely rely on

more subordinate collaborative strategies. More generally, the findings from this

explorative case study suggest that certain global structural characteristics of various

industries may be important variables in the explanation of the trajectories and dynamics of

emerging multinationals’ international catch-up processes.

Keywords: emerging multinationals; pharmaceutical industry; Indian multinational firms;

Big Pharma, India, catch-up strategies, leapfrogging, internationalisation strategies, Triad

multinationals.

Reference to this paper should be made as follows: Bruche, G. ‘Emerging Indian pharma

multinationals: latecomer strategies in a globalised high tech industry, European J. of

International Management. Forthcoming May 2012

Biographical note: Gert Bruche is a Professor of International Management at the Berlin

School of Economics and Law (BSEL), Germany, where he has also held the positions of

Dean and Vice-President. Before joining the BSEL he gained substantial practitioner

experience in leading international management positions in the pharmaceutical industry in

Asia and Europe and worked in a research position at the WZB – Social Science Research

Center Berlin. He has also served with the United Nations Development Programme in

Turkey, as a strategy consultant to multinational companies, and as Director of an

executive training programmes at Nanyang Business School in Singapore. His current

research interests focus on Chinese and Indian multinationals’ strategies, on innovation

offshoring to Asia, and on global value chains and knowledge networks.

2

1 Introduction

The study of the internationalisation of firms and multinational companies (MNCs) in

international business and in strategic management research has historically been based on the

observation of ‘conventional’ MNCs from the Triad (i.e. the U.S., EU and Japan). Only in the last

decade has increasing attention been paid to the phenomenon of a growing number of ‘latecomer

multinationals’, ‘third-world multinationals’ or ‘emerging multinationals’ (EMNCs) from

developing and newly industrialised countries. One line of thinking has been that these companies

have found ways of overcoming their ‘late mover disadvantage’ to acquire resources and

capabilities at an accelerated rate and ‘leapfrog’ into full-fledged MNCs in a comparatively short

time. A related proposition has been that EMNCs internationalise less often to exploit an existing

competitive advantage, but to build this advantage in the first place so that the latter follows

internationalisation rather than preceding it (Amighini, Sanfilippo, and Rabelotti, 2009; Athreye

and Kapur, 2009; Guillén and Garcia-Canal, 2009; Mathews, 2002; Mathews, 2006; Yadong

and Tung, 2007). Another claim has been that leading EMNCs become ‘challengers’ of the Triad-

MNCs with significant implications for the international competitiveness and industrial

knowledge base of Triad countries (e.g. Sirkin, Hemerling, and Bhattacharya, 2008).

While the studies refer to firms from a diverse range of developing countries, Indian EMNCs from

industries such as automotive, steel, IT services and pharmaceuticals feature high in the more

recent debates: the ‘BCG challenger 100’ list for instance contains 20 Indian EMNCs, second only

to China with 41 (ibid, p.277). Among the Indian firms pharmaceutical companies such as

Ranbaxy or Dr. Reddy’s have been referred to as prominent cases and success stories and a

number of academic studies, mainly conducted by researchers from India or of Indian origin, have

contributed to the discussion (see below). While the academic research and debates about a catch-

up scenario of Indian pharmaceutical companies (IPCs) have mainly relied on classic theories

about the internationalisation of firms (Dunning, 1998), resource-based and dynamic capabilities

theory (e.g. Teece and Pisano, 1997), the institution-based view of strategy (Peng and Wang,

2008), and innovation and learning theories (e.g. Cohen and Levinthal, 1990), it is a central

contention of this article that the research to date has neglected and does not explain the ‘reach’ or

‘levels of achievement’ of the catch-up process. Hence, even though the debate has generated

valuable insights into the internationalisation and capability building processes of IPCs, their

strategic positioning, catch-up opportunities and strategic alternatives in the context of a global

market dominated by large Triad-based MNCs (‘Big Pharma’) are not yet properly understood.

3

The following case study seeks to contribute to closing this gap by providing a ‘revelatory’

account of the catch-up and internationalisation phenomenon based on external industry

benchmarks. It is hoped that this account does not only help to understand the strategic challenges

and potential pathways of IPCs in their internationalisation process, but demonstrates the more

general need - at least for the study of EMNCs in high tech industries with multiple global entry

barriers - , to better understand how to assess the ‘distance of the leap’ in their ‘leapfrogging’, as

well as the challenge they present for conventional Triad MNCs. Extending the prevailing

resource-based approaches by a complementary global industry perspective may also be seen as a

kind of ‘triangulation’ as suggested by researchers who see in-depth case studies as a starting point

for theory building (Eisenhardt and Graebner, 2007; Yin, 1994). The study is based on an analysis

of a large variety of archival data, search in relevant data bases and websites as well as review of

annual reports. It also draws on various discussions with pharmaceutical managers during an

extended research stay of the author in India as well as on his industry expertise.1

The remainder of this article is organized as follows. The first section provides a brief description

of the major changes and current state of the Indian as well as the global pharmaceutical industry.

The second section reviews the academic IB literature on IPCs in the context of the debate on

emerging multinationals. In the third section we confront and augment these findings with an

account and complementary assessment from a global pharmaceutical industry perspective. In the

final chapter we draw conclusions and elaborate on the possible research implications of EMNC

catch-up processes.

1 Seminal changes in the Indian and global pharmaceutical industry

1.1 Transformation of the Indian institutional context

The current state and strategic challenges of the Indian pharmaceutical industry and its leading

companies ought to be understood in the context of the concurrent changes in the ‘rules of the

game’ (North, 1990) of the Indian and the global pharmaceutical industry. The two major path-

breaking changes in India are the Patent Act of 1970 and the Patent (Amendment) Act of 2005.

The latter was introduced in the wake of India’s New Economic Policy of 1991 and the

subsequent WTO accession in 1995 which included the signature of the TRIPS-agreement; the

agreement provided for a transition period from 1995 until 2005 for the final enactment of the new

patent legislation (Chaudhuri, 2005; Mueller, 2006). Abolishing the old British inspired product

patent system and deliberately introducing a weaker process patent system in 1970 stimulated an

4

upsurge in reverse engineering and copying of foreign patented drugs. Supported by

complementary public investments into higher education, public research institutes and state-

owned pharmaceutical firms, these changes provided the basis for the rise of India’s

pharmaceutical industry to become one of the world’s major volume players (Chaudhuri, 2005;

Greene, 2007; Manil, 2006).

Over several decades IPCs developed a core competence in chemical and pharmaceutical process

reengineering and production and learnt how to cope with India’s fragmented, heavily regulated

and ultra-low price domestic market. The limited exports and outward FDI of the period until the

mid-1990s were mainly directed towards the unregulated markets of other developing countries.

Moreover, as Big Pharma left India and sold their Indian operations during this period, major IPCs

acquired some state-of-the-art factories, laboratories, products, and trained staff which supported

their quest for world class quality levels. Although IPCs became ‘locked-in’ in an imitative path,

the policies served India well in making a broad range of essential medicines available at very low

affordable prices.

The enactment of the Patent (Amendment) Act of 2005 ended 36 years of the protection of India’s

home market and its pharmaceutical companies. The new act provides for the registration of

product patents and – despite some concerns over its interpretation and implementation – has

proved to be game-changing (Chaudhuri, 2005; Mueller, 2006; Mueller, 2008). As the decision to

introduce product patents in line with the TRIPS framework was already taken in 1995, Big

Pharma as well as Indian companies had a transition period of ten years to prepare for the new

institutional context. Big Pharma's renewed interest is evident in the rapid upsurge of patent filings

by leading MNCs, and an increase in inward FDI as well as in numerous collaborative deals (CG,

2010; Evalueserve, 2008, and box 2 below). While relying on their core competences in low cost

reengineering and production, the leading IPCs embarked upon various new strategic initiatives

aimed at technological upgrading, started to enter the regulated pharmaceutical markets of the

U.S. and Europe, and expanded their collaborative deals with Big Pharma.

1.2 Shifts in the global pharmaceutical industry

For the last four or five decades the pharmaceutical industry (of the Triad) has consistently been

one of the most profitable industrial sectors (Ghemawat, 2010, p.18). Global pharmaceutical

industry growth rates have come down from double-digit figures up to the 1990s to (high) single

digits in the new millennium. In 2009 the global pharmaceutical world market for prescription

5

drugs stood at a total sales value of US$ 808 billion, more than double its size compared to the

start of the decade. The Triad countries represented 82 per cent of this market (North America 40,

Europe 31, Japan 11 per cent) and the emerging and developing countries 18 per cent (India 1-2

per cent) (IMS, 2010). While the Triad still dominates the current market, a number of big

emerging markets represent the major growth opportunity of the future (Hill and Chui, 2010).

Big Pharma pursues an innovation-based business model relying on very high R&D spending (in

the order of 15-20% of sales) and supporting a risky and lengthy drug discovery and drug

development process lasting from 10 to 15 years (for a good explanation of this process see

Pisano, 1996; see also figure 2 below). In a positive scenario, the process yields a high-priced

patent protected drug, in the best case a ‘blockbuster’ (i.e. a drug with sales of more than US$ 1

billion ), which is launched (ideally) in parallel in all key markets, involving a major push in

marketing and sales. Due to increasingly stringent regulatory requirements and falling R&D

productivity (i.e. the chances for ‘easy targets’ are being steadily exhausted), the R&D cost and

risky capital outlays for manufacturing have increased dramatically while research productivity

has been declining (Accenture, 2007; CMR, 2010; Pisano, 1996). A second important challenge

for Big Pharma emerged in the 1980s with the rise of biologicals, or large molecule drugs, based

on advances in biotechnology and genetic engineering. Eventually this led to new methods of

‘rational drug design’ requiring companies to master a new more complex set of capabilities

involving deep biological and disease know-how (Bhandari et al., 1999; Gassmann and

Reepmeyer, 2005; Pisano, 1996).

The business model of Big Pharma has also come under pressure from another side. While it was

initially prohibitively costly and time-consuming for imitator companies in the Triad to introduce

copycat drugs after patent expiry, this situation changed fundamentally after the 1984 Watchman-

Hax Act was passed first in the U.S., and then with some delay in Europe as well. The new act

provided for filing of ‘Abbreviated New Drug Applications’ (ANDAs) even before patent expiry

without performing extensive clinical trials, just by proving that the imitator drug was

‘bioequivalent’ to the patented originator drug. The new legislation resulted in the emergence of a

generics segment with companies pursuing a ‘production-based’ business model relying on

imitating drugs that have come off patent.

The rapid rise of the generics segment in the Triad markets in the 1990s and after the millennium

and the deteriorating R&D productivity and rising cost pressures stimulated two principal coping

6

strategies by Big Pharma. On the one hand, successive waves of horizontal M&As have led to an

on-going consolidation into very large groups with the aim of getting access to promising

development pipelines, building a worldwide footprint in drug discovery, development, regulatory

resources and sales forces, and seeking market dominance in certain disease categories (Knol,

2010; KPMG, 2009). The second major coping strategy which increased in importance after the

turn of the millennium aims at cost savings through outsourcing pharmaceutical production via

contract manufacturing deals and a shift of contract research and development to qualified low-

cost locations such as India or China.

1.3 Transformational growth of the Indian pharmaceutical industry

The Indian pharmaceutical industry underwent rapid growth after the turn of the millennium, with

total sales reaching US$ 19 billion in 2008, ranked 3rd

worldwide by volume of production (10 per

cent of global volumes) and 14th

by value (1.5 per cent), indicating the much lower cost and

pricing of drugs in India compared to Triad markets) (GOI, 2009). Along with IT services,

automotive components and other sectors the Indian pharmaceutical industry proved to be one of

the rapidly internationalising sectors in the Indian economy after the reforms of the early 1990s

(Cygnus, 2006; Greene, 2007). Pharmaceutical exports grew at double-digit annual growth rates

and IPCs became major suppliers to various parts of the world with the U.S., Germany, Russia,

UK and China as the main destinations (ibid). A large part of the export growth was based on bulk

supply agreements of Active Pharmaceutical Ingredients (APIs) to Big Pharma and major generics

companies. The parallel expansion in exporting finished drugs required building and expanding a

growing base of ‘FDA-approved’ high quality production plants of which India now has the

highest number outside of the U.S. (PwC, 2010, p.12). The domestic Indian pharmaceutical

market itself has grown with rates of 10-15% in the second half of the decade achieving around

US$ 10 million in 2009 (No. 14 on a global scale and No. 2 in emerging Asia). It is projected to

‘outgrow’ the Triad markets and double to US$ 20-24 billion by 2015 (McKinsey, 2007).

The ‘organized’ sector of India’s pharmaceutical industry comprises some 250 firms accounting

for around 70 per cent of products in the market and located on top of a fragmented base of an

estimated 10,000-15,000 smaller producers. The top 10 firms represent some 40 per cent of total

(Greene, 2007; KPMG, 2006) global sales and around 30 per cent of domestic sales, with a trend

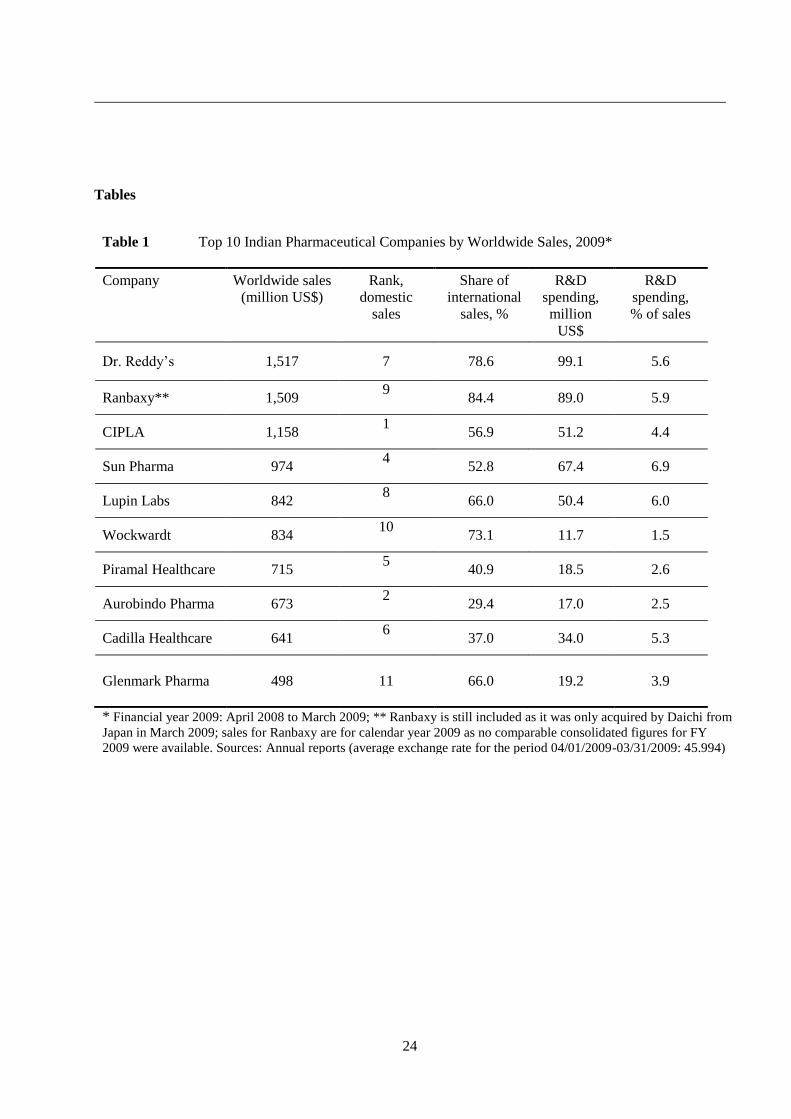

towards consolidation. As can be seen from table 1 three firms had crossed the US$ one billion

- Insert Table 1 approximately here --

7

threshold by 2009, seven of the firms had international sales in excess of 50 per cent of total

revenues and R&D spending is hovering around two to seven per cent of sales. Only one Triad-

based MNC, GlaxoSmithKline, had a significant position in the domestic pharmaceutical market

(No. 3 position by market share).

2 Academic research on emerging Indian pharma multinationals

2.1 Internationalisation, capability accumulation and trend to innovativeness

After this overview of the long-term contextual and internal changes in the Indian and global

pharmaceutical markets, we now turn to the pertinent International Business research on IPCs in

the context of the debate about EMNCs. Even in earlier debates on EMNCs, Indian

pharmaceutical companies featured among the more prominent examples. Bartlett and Goshal

(2000) for instance profile Ranbaxy as one of their leading cases of ‘late movers going global’,

starting to rapidly move up the pharmaceutical value curve from bulk and intermediate production

and generics to innovative drugs (ibid, 135). They attribute this ‘success story’ to strong visionary

leadership from the top (ibid, 142). Khanna and Palepu (2006) mention Ranbaxy in their article on

‘Emerging Giants’ and Accenture (2008) refers to the same company in a report on the ‘Rise of

the Emerging Country Multinationals’. The Boston Consulting Group’s list of 100 leading

EMNCs cites three Indian pharmaceutical firms (Cipla, Dr. Reddy’s, Ranbaxy) as ‘global

challengers’ (Sirkin, Hemerling, and Bhattacharya, 2008, p.277).

Based on their findings from interviews in six major IPCs, Kale and Little (2007) suggest that

these firms have successfully moved through the ‘cumulative capability creating model’ shown for

Korean and Taiwanese firms from other industries (Kim, 1997; Kim and Nelson, 2000). From

‘reverse engineering R&D’ via ‘duplicative imitation’, ‘creative imitation’ and ‘collaborative

R&D’, the firms are said to have built ‘a solid base for the development of competence in

advanced innovative R&D’ (Kale and Little, 2007, p.608). Pradhan (2008) bases his observations

on the mainstream theory of the internationalisation of the firm. He characterises the cross-border

acquisitions of five IPCs as strategic asset-seeking initiatives to ‘overcome the most important

innovation limit of inadequate product development capability’ (ibid, p.5), noting that this mode

of outward FDI has increased rapidly since about 2000 after a preceding phase of greenfield FDI

in the 1990s (ibid, p.6). Another study by researchers from Duke and Harvard University on the

globalisation of the pharmaceutical R&D value chain claims that ‘several firms in India and China

8

are performing advanced research and development and are moving into the highest segments of

the pharmaceutical value chain’ (Wadhwa et al., 2008, p.2).

Chittoor et al. (2008) and Chittoor et al. (2009) study the transformation of IPCs in response to the

institutional changes in the Indian economy after 1991 based on data sets of 118 and 206 Indian

pharmaceutical firms for the period 1996-2005. The earlier study finds a significant increase in the

firms’ internationalisation which the authors take as confirmation of Mathews’ (2006) and others’

proposition that this is a case of accessing new resources ‘with capability development and

competitive advantage following, rather than leading their internationalisation’ (Chittoor et al.,

2008, p.263). They also suggest that Indian pharmaceutical firms follow an ‘indigenous growth

model’ relying on the ‘entrepreneurial leadership and managerial capital of Indian entrepreneurs

and managers’ (ibid, p.263). According to the authors, by having developed significant ‘absorptive

capacity’ in the pre-liberalization era IPCs can effectively import critical resources and embark

upon foreign acquisitions which provide them with ‘the resources and capabilities needed to

compete with well entrenched MNCs in both domestic and global markets’ (ibid, 265). The

second study provides ‘preliminary support for the idea that Indian firms may have developed

‘innovation capabilities’ by participating in international resource and product markets’ although

the indicators to support this proposition reflect a rather modest measurement threshold (Chittoor

et al., 2009, p.199).

Athreye and Godley (2009) try to understand the attempts of Indian pharmaceutical firms’

‘technological leapfrogging’ by comparing them with the rapid acquisition of new capabilities by

U.S. pharmaceutical firms in the context of the 1940s antibiotics revolution. The ‘firm specific

advantages’ of U.S. pharmaceutical firms were mainly acquired through various kinds of

international linkages (rather than being built domestically first, and then exploited

internationally). The fast entries of leading Indian firms into developed countries’ markets after

2000 mainly through acquisitions are perceived as asset-seeking moves in support of the

companies’ globalisation strategies in generics and of new biotechnology-based discovery

capabilities (ibid, p.313). As a general conclusion, the authors take the successful early use of a

variety of internationalisation strategies by U.S.firms as ‘suggesting that there may be

considerable merit in the more aggressive internationalisation strategies adopted by Indian

generics producers today’ (ibid, p.319). The character of the ‘leapfrogging’ itself, i.e. accelerating

a path or skipping normal stages of a path, remains somewhat elusive ( on technological

‘leapfrogging’ in the Korean context, see for example the study of Lee and Lim, 2001).

9

2.2 Inter-company variations and emerging global players

While the contributions mentioned so far try to generalize across major IPCs, some of the authors

above have also investigated the differences in competitive and internationalisation strategies at

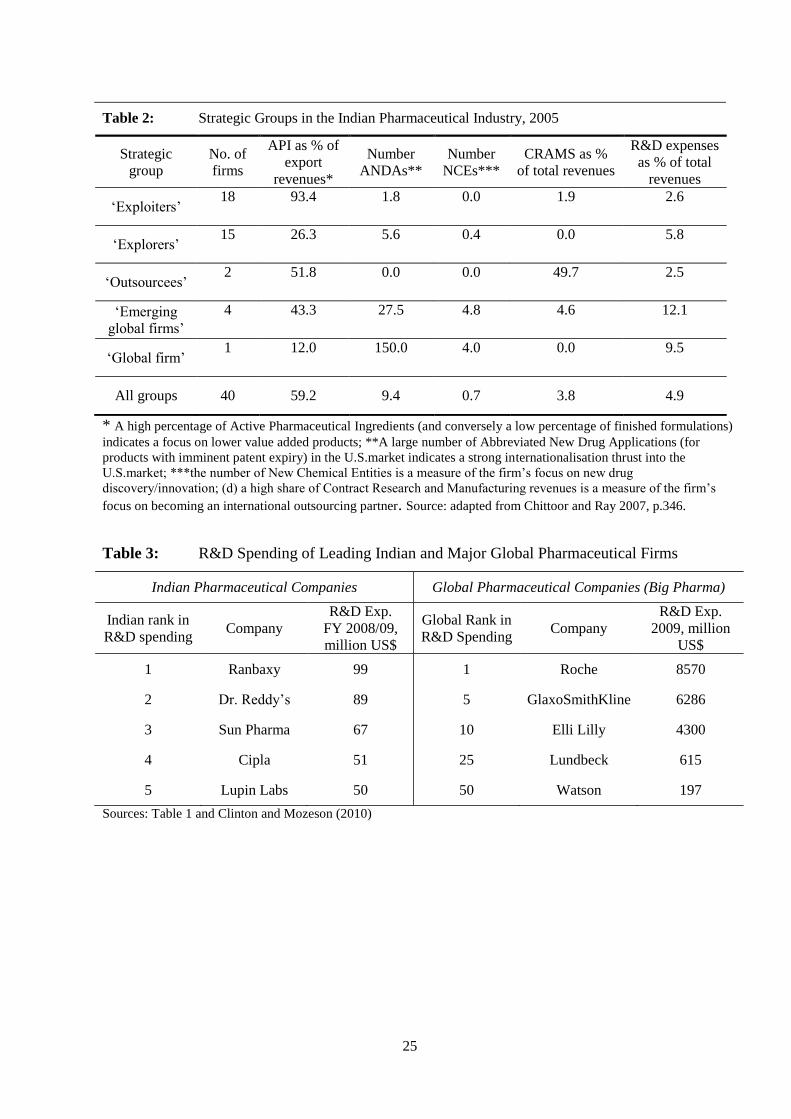

strategic group or individual firm level. Chittoor and Ray (2007) base their analysis on data from

40 major pharmaceutical firms and identify five strategic groups (see table 2). In their

internationalisation strategy the comparatively large numbers of ‘exploiters’ leverage

- insert table 2 approximately here –

their core competences in chemical synthesis and process optimisation coupled with a low cost

manufacturing location. Another larger group termed ‘explorers’ show some signs of acquiring

new capabilities over and above their traditional strengths by moving into the U.S.market and

increasing their R&D spending. ‘Outsourcees’ are companies emphasising the integration into the

value chain of Big Pharma in a strongly collaborative mode. Only four Indian companies are

found to be in the ‘emerging’ global firms’ group (case example Dr. Reddy’s) or are actually

considered global firms (only one firm and case example: Ranbaxy). In analysing firms from the

last two groups the authors conclude that despite their constraints ‘developing economies can

throw up a few TMNCs that are globally competitive and are capable of posing stiff competition

to the established MNCs from developed economies […] Armed with superior dynamic

capabilities these TMNCs […] may catch up with the established MNCs sooner or later’ (ibid,

p.353).

Athreye, Kale, and Ramani (2009) intend to evaluate the ‘dynamic capability building strategies’

of four leading Indian pharmaceutical firms (Ranbaxy, Dr. Reddy’s, Wockhardt and Piramal).

While it seems to be difficult to generalize across these firms’ behaviour, they identify three broad

trends: all firms have expanded into the international generics market with an emphasis on the

U.S. and Europe; they have developed new forms of collaboration with Triad MNCs, and they

have started to acquire skills for new drug discovery. The authors conclude that the co-evolution

of strategies and dynamic capability building varies significantly as a function of past firm-

specific trajectories such as technology bases and managerial vision. While ‘safe integrated

capability building’ (Ranbaxy), ‘safe niche capability building’ (Piramal) and ‘risky capacity

building’ (Dr. Reddy’s) are different avenues pursued by the firms, they come to the more

10

cautious conclusion that they do not (yet) see signs of an evolutionary trajectory of dynamic

capabilities emerging with the potential of lasting competitive advantage (ibid, pp.757-758).

Drawing on insights from Big Pharma's reaction to the biotech revolution in the 1990s, Kale's

most recent contribution (2010) investigates differences in R&D-oriented learning strategies of

IPCs based on the path dependent nature of learning processes. Relying on in-depth interviews

with top R&D personnel from six leading IPCs (Dr. Reddy’s, Ranbaxy, NPIL, Glenmark,

Wockhardt, Lupin), he concludes that reverse-engineering-experienced scientists, lack of cross-

disciplinary knowledge integration, a short-term mindset and too much focus on in-house R&D

coupled with a lack of collaboration between industry and academia are some of the ‘core

rigidities’ which IPCs have to overcome. In confronting these challenges, the six firms differ

considerably in their learning and capability building approaches; DRL and Ranbaxy are the most

advanced, also due to their early moves into innovation; the other firms are extremely focussed on

their R&D efforts (Glenmark, Wockhardt, Lupin) or focus mainly on contract research (Piramal).

Although the last mentioned contributions strike a more careful note, all the articles which rely on

resource-based, knowledge and learning-based or institutional perspectives converge in varying

degrees towards the idea of the ‘catch-up’ of leading IPCs. According to these authors, resource

accumulation and internationalisation will result, on the one hand, in the positioning of IPCs

among a small number of leading global players in the generics space, and, on the other hand, – a

point more often emphasised – it will eventually also include successful entry into the innovation-

based segment of the global pharmaceutical market. In the following section we review these

assumptions and findings and demonstrate that they must be complemented by an industry-based

view of the economics and key success factors of the global pharmaceutical market if one wants to

assess the ‘reach’ and perspectives of the catch-up process.

3 Indian pharmaceutical companies in a global industry-based perspective

3.1 Path-changing towards an innovation-based business model

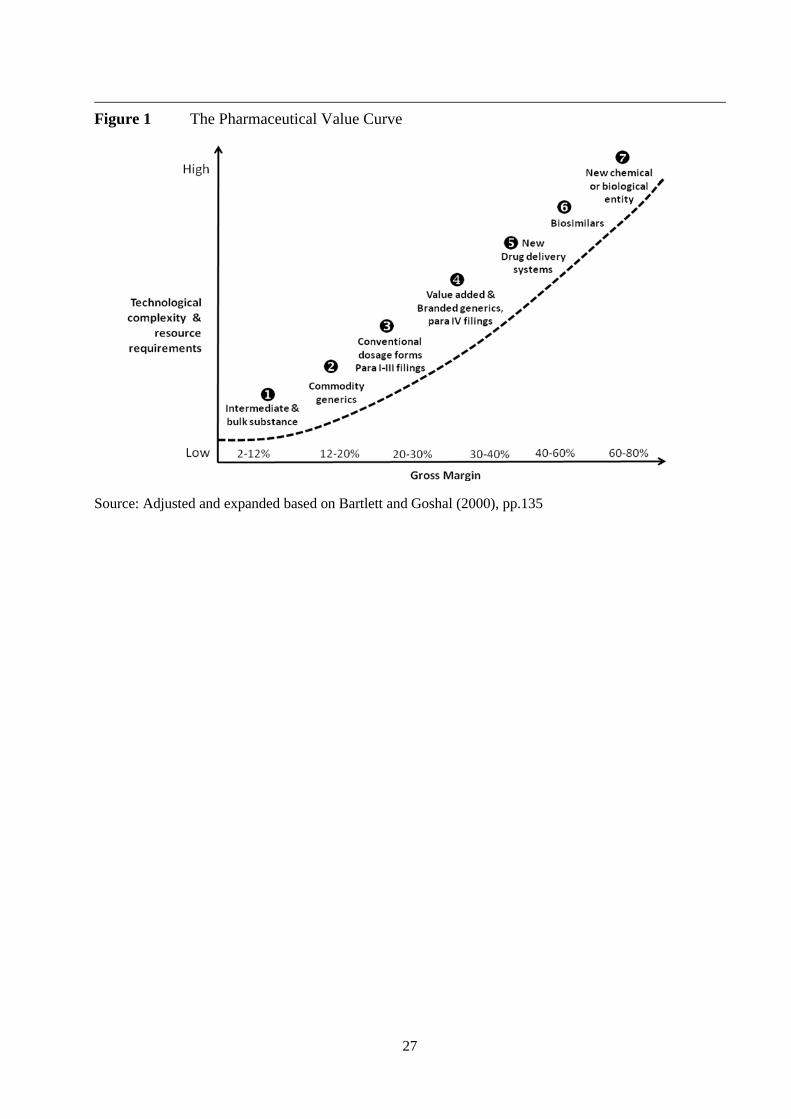

Most of the leading IPCs pursue ‘bundles of strategic initiatives’ which can be related to different

stages along a pharmaceutical value curve. As illustrated in figure 1, the profitability of a

pharmaceutical company’s operations generally depends on the degree of uniqueness or product

differentiation which reflects an ever higher level of technological capability and innovation. In

advanced stages of the value chain companies create higher value and, at the same time, capture

11

an increasing share of the value created, which can principally be explained by the relative rarity

of resources and growing barriers to imitation. While IPCs had their traditional stronghold in

--insert Figure 1 approximately here --

supplying bulk and final drugs in stages one to three of the curve, some of them have aggressively

tried to move up the curve. Dr. Reddy’s is the most striking example for this upward move since,

in parallel to its activities in stages one to three of the value curve, it has been working very

actively on stages four to seven (see also box on Dr. Reddy’s below). Dr. Reddy’s, Ranbaxy,

Cipla, Sun Pharma or Lupin, and other leading IPCs listed in table 1 as well as a number of

medium sized firms have pursued strategies to incrementally move up the value chain through a

range of different activities: the aggressive challenging of patents before patent expiry, the

independent development of improved formulations, the development of new drug delivery

systems for known substances, or the more active branding of generic drugs.

The attempt to build a capability in ‘biosimilars’2 is another avenue pursued by many of leading

IPCs as well as a number of smaller companies. Establishing ‘comparability’ to the original

innovator (biopharmaceutical) drug is much more complex than in small molecule drugs since

imitators do not have access to the originator’s original molecular clone and the effects of the

drugs may be sensitive to manufacturing changes. The regulatory requirements in Europe and the

U.S. are therefore more demanding and open to further changes. While a number of IPCs (e.g.

Biocon, Intas, Reliance Life Sciences, Wockhardt, Dr. Reddy’s) have launched biosimilars under

the less stringent Indian conditions or in other emerging markets, the first successful entries into

European and U.S.markets are expected in 2011 (KPMG, 2006, p.11; PWC 2010, p.19). If IPCs

can develop a significant capability in biosimilars and can pass the demanding hurdles of

European and U.S. regulatory agencies, this would give a strong stimulus to their

internationalisation strategies and the entry into a higher margin business (with higher risks and

returns).

While all these initiatives can be considered as incremental path-changing moves into higher

margin activities, successful entry into the global market for research-based pharmaceuticals (by

introducing proprietary new chemical or biological entities, see no. 7 in the value curve, figure 1)

would be truly path-breaking. The business model of innovative Big Pharma requires entirely

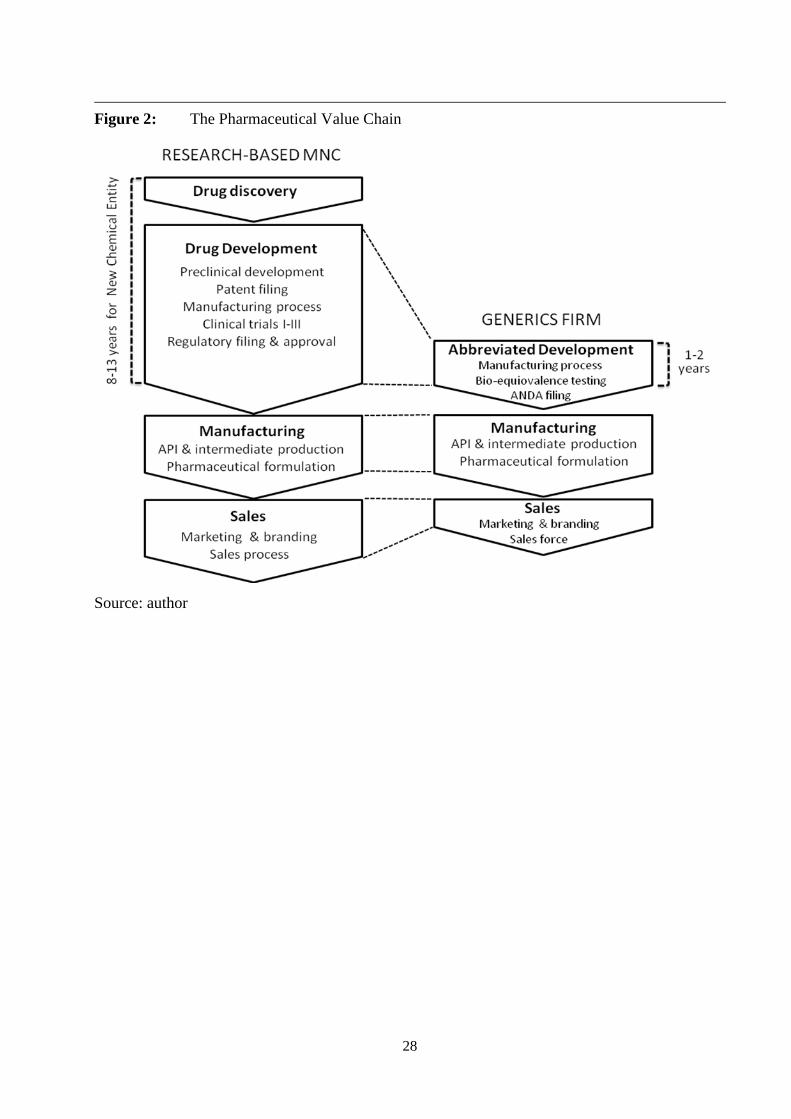

different threshold resources and capabilities. As can be seen from figure 2, the

12

-- insert figure 2 approximatel here -

initial entry by a number of IPCs into ‘drug discovery’ in a single or several disease areas only

concerns a first stage in an integrated full-scale R&D capability (this initial stage includes

activities such as biological pathway targeting and identification, compound generation and

screening, lead identification and optimisation, and the final validation of a drug candidate for

development). The development and commercial launch of a drug candidate which survives the

long ‘stage-gate process’ requires several important complementary resources: a geographically

dispersed network of qualified development centres, deep worldwide knowledge resources on

regulatory, treatment and reimbursement systems, and established relationships with key opinion

leaders as well as broad customer relationships in major lead markets. Big Pharma companies

have built all these resources, capabilities and organizational competencies over decades of

learning and resource accumulation.

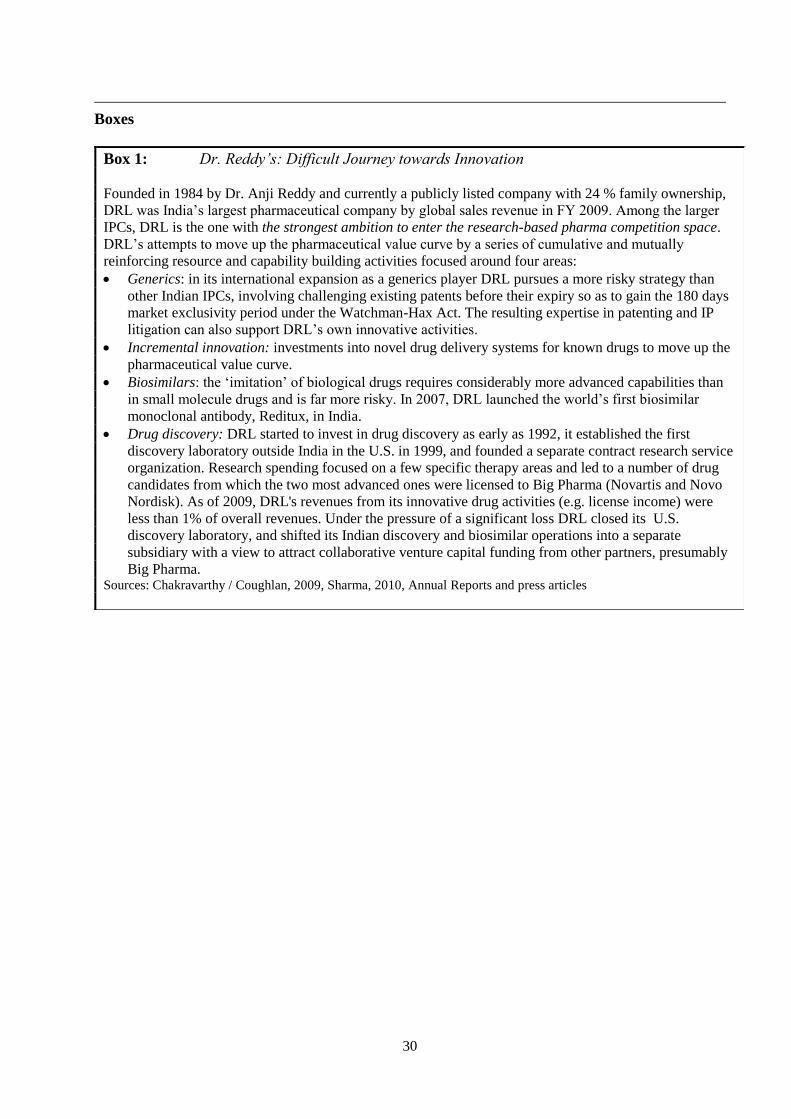

Among the leading IPCs, Dr. Reddy’s is the most committed and advanced firm in the attempt to

build an independent drug discovery capability; the company’s top management explicitly stated

aim is to become a fully integrated pharmaceutical company (Chakravarthy and Coughlan, 2009).

Dr. Reddy’s experiences and challenges testify to the difficulties and hurdles encountered in

entering the research-based segment (see box 1 below). Other active companies are for example

Wockhardt (Ten New Chemical Entities – NCEs - in the pipeline), Biocon, Piramal, Glenmark or

Sun Pharma. Following Dr. Reddy’s lead, most major IPCs have spun off their drug discovery and

innovative R&D activities into separate units, often in order to attract additional outside

investment (see also PWC 2010, pp.15-18). Aside from these conventional drug discovery

activities by larger IPCs, India is also home to a small biotechnology industry with a few highly

specialised players like Serum Institute of India, Biocon and Panacea Biotech which, aside from

discovery activities, are also building capabilities in the development and manufacturing of

biosimilars (ibid, p.18).

Apart from availability of threshold resources, the major ‘mobility barrier’, i.e. entry barrier, into

the group of research-based pharma companies is the paramount need for global scale. With R&D

costs extremely high and still growing, a very large principally global customer base is required to

provide the source of adequate R&D funding. DiMasi and Grabowski (2007) estimate that the full

cost of bringing a NCE or new biological entity to market – i.e. from drug discovery through to

13

development – have risen from US$ 138 million in 1975 to US$ 1.3 billion in 2006; this includes

all the failures as well as the opportunity cost of capital. The largest share of these costs -

estimated at some 54% by EFPIA (2010) – are incurred during the development phase. Compared

to ‘stand-alone’ drug development, there are also considerable scope economies which Big

Pharma exploits through broader drug portfolios in the discovery, development, regulatory,

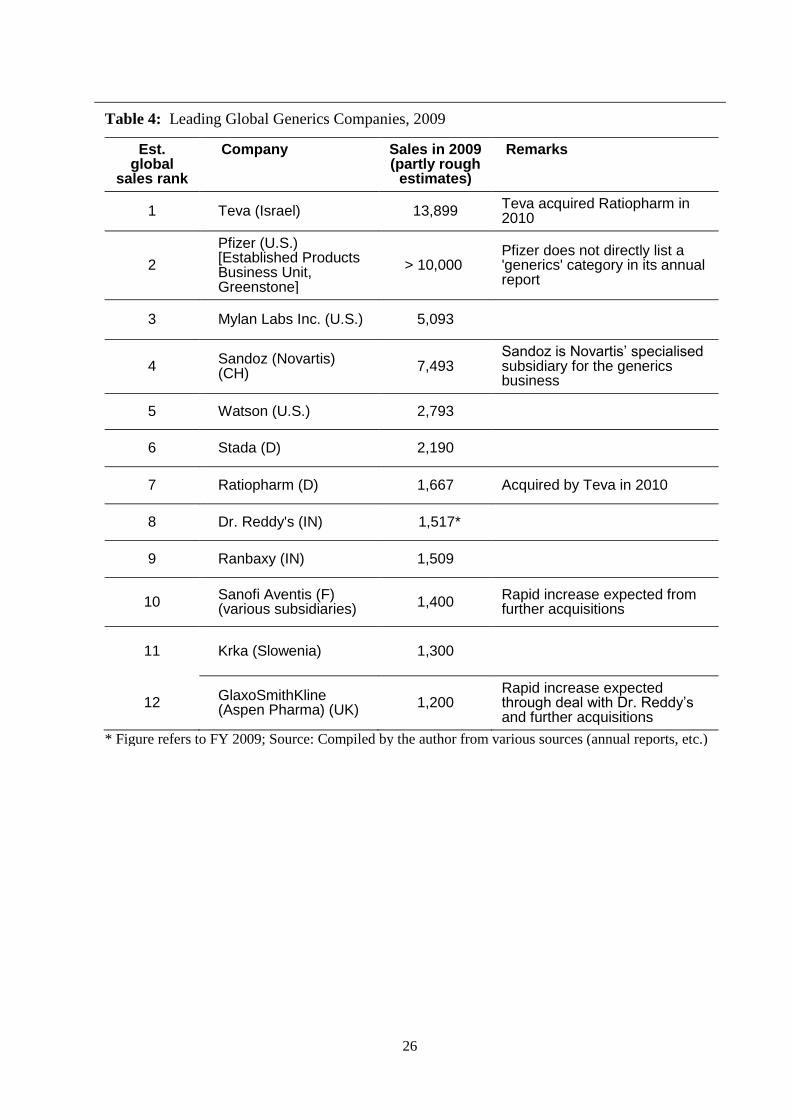

production and sales functions. If we compare the R&D spending of the five leading Indian

-- insert Table 3 approxiamtely here –

firms with the spending of selected firms in the worldwide Top 50 pharmaceutical companies,

even Ranbaxy’s near US$ 100 million R&D spending is negligible compared to the Big Pharma

companies in the top 10 range, and even way below number 50 on a worldwide basis; furthermore,

a considerable share of the R&D spending by IPCs is on process research to support the launch of

new copycat products in their generics business. Moreover, through successive mega-merger

waves, recent examples being Pfizer’s 2009 acquisition of Wyeth for US$ 68 billion and Merck’s

purchase of Schering-Plough for US$ 41 billion, the pharmaceutical innovation race is

increasingly turning into global oligopolistic competition.

Taken together, the findings of a global industry-based perspective lead to the conclusion - in

contrast to the more upbeat tenor of some of the academic research mentioned above - that

(independent) drug discovery investments by such firms as Ranbaxy, DRL, Wockhardt, Sun

Pharma or Lupin Labs and the related capability building processes in this space are still far away

from entering the strategic group of integrated global research-based pharmaceutical companies

(Big Pharma). In order to fund their ‘drug discovery activities and access complementary

-- Insert box 1 approximately here --

knowledge and development resources, IPCs therefore have to rely on ‘outlicensing deals’ or other

collaborative agreements with Big Pharma. In such deals, they will usually be the ‘junior partner’

and only appropriate a lower proportion of the value created if successful (on value appropriation

in licensing deals see for instance Levin et al., 1987, Rothaermel, 2001). Even if serendipity led to

the independent discovery of a successful drug candidate with major global sales potential, it is

still an open question whether the lucky IPC can appropriate the major value portion from such an

innovation and ‘ride to full global integration on its back’ .

14

3.2 Collaborating as Partners in Big Pharma’s Global Value Chains

Three trends in the global pharmaceutical market have a major effect on Indian IPCs: first, as

mentioned before, rising R&D costs and increasing pressure from generics competition continued

to drive Big Pharma to outsource non-core and particularly costly and time-consuming activities in

their value chain. Second, Big Pharma is increasingly moving into generics itself rather than

leaving this market opportunity only to pure generics firms. Third, Big Pharma also needs an

answer to the opportunities presented by the rapid growth of emerging markets in Asia, Latin

America and Africa which are often dominated by generics (on the rise of emerging pharma

markets, see Hill and Chui, 2009). The emerging paradigm shift of Big Pharma’s business model

towards a more modular value creation system as well as a more diversified approach entails three

significant collaborative growth opportunities for IPCs: supplying Big Pharma or generics

companies with APIs (in bulk form); supplying finished unbranded or branded generic drugs; and

providing contract research services (discovery, preclinical services and clinical trial services).

Collaborative strategies – in a sense comparable to the contract manufacturing and design services

strategies of Asian firms in the electronics sector – have become one of the major growth

opportunities for IPCs (Motilal Oswal, 2010). Although the worldwide market for Contract

Manufacturing Services in pharmaceuticals is still dominated by North American and European

companies, Indian (and Chinese) firms are rapidly increasing their respective shares (ibid). The

numerous consultant reports and reports of the increasing numbers of deals between IPCs and Big

Pharma especially after 2008 present the engagement in Contract Research and Contract

Manufacturing Services (CRAMS) as a major low-risk strategic opportunity for large, but also for

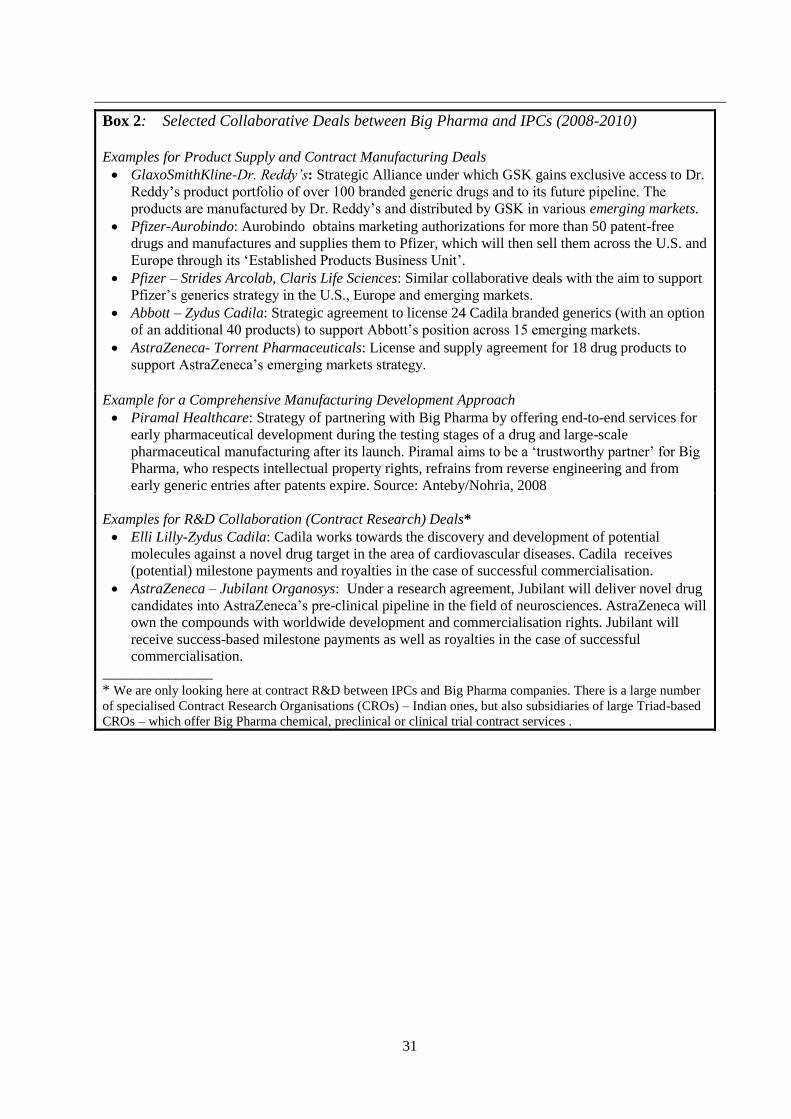

medium-sized IPCs (ibid; Bang, 2009; and see box 2). The growth opportunities are also driven by

the upcoming surge in products coming off patent (see below) and by the U.S. healthcare reform.

The Indian Government support for the Indian CRAMS export business includes establishing

Special Economic Zones comparable to the policies adopted for IT and IT enabled services. It

should however also be noted that Big Pharma invests heavily into their own captive R&D centres

in India and China which may slow down growth in the outsourcing of research services to

external (Indian) providers (on R&D offshoring to India and China see BCG, 2006; Bhalla et al.,

2006; Bruche, 2009).

3.3 Becoming Global Generics Players

15

While the collaborative approach - especially in contract manufacturing and licensing of branded

generics to Big Pharma - is mainly based on existing or incrementally improved domestic

-- insert Box 2 approximately here –

capabilities and location advantages, the internationalisation of leading IPCs is most closely

related to their attempt to establish leading positions in the U.S. and European generics markets.

Compared to the research-based competition segment of the global pharmaceutical market, entry

barriers into the U.S. and European generics markets are much lower. With the supply side of the

market still rather fragmented and smaller size targets with modest valuations still available,

entries via cross-border acquisition have been feasible. Moreover, the successful introduction of

new generics ‘only’ requires an ANDA filing and the availability of certified low cost production

sites. Under these conditions, major IPCs have been relatively well positioned for successful entry

: they have the largest number of FDA approved factories outside the U.S., world-class process

capabilities and a significant low cost talent base, and can exploit decades of experience and

learning in ‘frugal operating’.

Through a series of smaller acquisitions, the most prominent IPCs have built ‘bridgeheads’ in the

U.S. and European markets from which they pursue expanded market entry and market

penetration. From 2000 until mid-2008 for instance, Pradhan reports a total of 105 acquisition

deals with a total value of US$ 2.9 billion of which more than 80 per cent involved takeover

targets from developed countries (Pradhan 2008, 9). The acquisitions provide initial direct access

to the generics drugs markets while simultaneously integrating new resources (such as for instance

new products, specialised managerial, technological and marketing skills, local sales

organizations, regulatory know how and relationships as well as additional formulation plants). As

many of the acquisition targets were ailing companies before their takeover, their Indian acquirers

had to start turnaround programmes. This usually involved trying to provide additional value for

the acquired company by integrating it into the supply chain of (Indian) low cost production sites

and expanding its presence in the local generics market by increasing the number of ANDA filings

(for an analysis of the very different approaches of three leading Indian pharmaceutical companies

see Budhwar et al. 2009). Between 2007 and July 2010, more than one third of ANDA approvals

granted by the FDA in the U.S. were filed by such Indian companies as DRL, Wockhardt,

Aurobindo or Sun Pharma which often rely on their newly acquired U.S. subsidiaries (FDA,

2010).

16

If we look at how far Indian companies have managed to climb the ranks of global generics

companies, one must take into account that the market is in a state of considerable flux and the

available data is far less reliable than for the pharmaceutical market as a whole. In a ranking of

global generics companies by sales, a revenue data estimate for 2009 puts the two major Indian

contenders as eighth and ninth (see table 4).

--Insert table 4 approximately here –

The global generics market is undergoing major changes producing opportunities as well as threats

for IPCs. There is a huge growth opportunity, since between 2010 and 2014 alone a global sales

volume of US$ 142 billion of patented drugs will come off patent, two thirds of this in the U.S.,

peaking in 2011 and 2012 (IMS, 2010); depending on the extent of price erosion, this offers an

additional market opportunity for generics firms amounting to almost US$ 50-100 billion. This

growth opportunity is further fuelled by the increasing cost containment activities of governments

as well as the reform of the U.S. healthcare system. Another important opportunity for generics is

the fast ascent of some big emerging markets with a high reliance on generics. In 2009, China,

India itself, Brazil, Russia, Mexico, Turkey and South Korea represented around 50 per cent of the

growth of the global pharmaceutical market , while representing only around 11 per cent of global

sales (Hill and Chui, 2010).

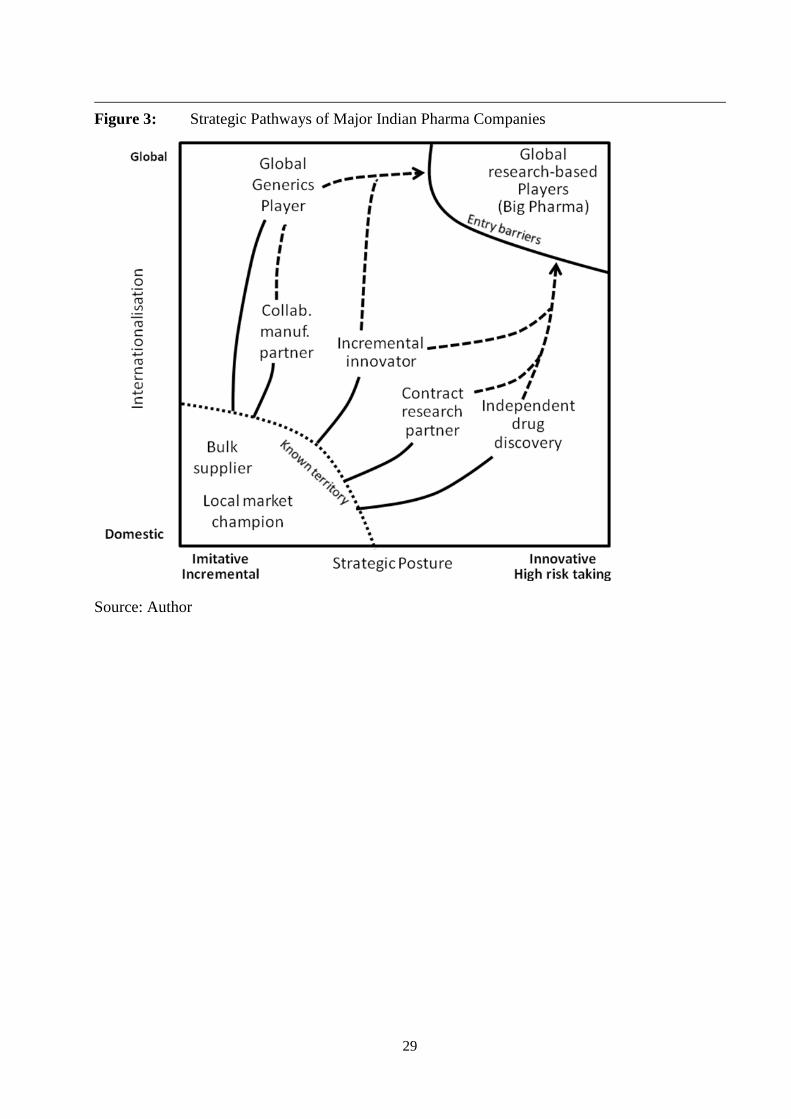

4. Conclusions and perspectives

A review of recent studies in the tradition of resource-based theory and International Business

research points to significant advances in capability building in leading IPCs, often going hand in

hand with strategic moves on asset-seeking internationalisation. The companies exploit their

historical advantage in low cost process engineering and location advantages while at the same

time exploring various new avenues to advance on the pharmaceutical value curve. Authors agree

that a number of companies have shown the potential to become important players in the

international arena. Most authors perceive a number of IPCs as on a capability-creating strategic

path from an imitative stance to an innovation-based business model and take the entry of a

significant number of IPCs into ‘drug discovery’ as the most immediate sign that IPCs are

evolving into research-based players. Some authors see the development of some IPCs in a

‘leapfrogging’ or ‘catch-up’ scenario which lead them to challenge Big Pharma. Some studies

17

relate the speed of these moves with particular traits of Indian managers (e.g. Cappelli et al., 2010)

or with a ‘reverse brain drain’ of Indian engineers and scientists trained in the USA (Kale, 2009).

One drawback of these findings, primarily based on resource-based and institutional perspectives,

is that they do not include global ‘benchmarks’ or reference points to evaluate the ‘reach’ or

achievement level of the catch-up and internationalisation process. This paper has demonstrated

how extending these perspectives with an ‘outside-in’ global industry perspective can help close

this gap and provide insights as to the relative ‘reach’ and current position of leading IPCs as a

result of their fast resource accumulation and learning processes. The findings can be summarized

in identifying a number of ‘strategic pathways’ or ‘trajectories’ of leading IPCs which are

principally located in the strategic space of increasing internationalisation and innovativeness/risk

(see figure 3).

-- Insert figure 3 approximately here --

The most direct attempt by leading IPCs to create the resources and capabilities for an innovation-

based path is the establishment of drug discovery units. These have already produced a limited

number of candidates to enter the development phase. As drug discovery is a high risk process and

global development, registration and commercialisation requires substantial complementary

resources, it is highly uncertain whether this pathway will lead to fully integrated companies

which can ‘catch-up’ with Big Pharma in the medium term. The collaborative integration of drug

discovery units as contract research partners and their spin-off into separate companies which

may then access venture capital help to ‘de-risk’ the parent company and may be a viable business

model. They will however not be conducive to the near term evolution into integrated player

status.

Leading IPCs have also ventured into incremental innovations in selected areas, and with the

move into biosimilars into a more complex imitation space. This strategic pathway helps in

creating valuable resources and complementary capabilities in support of a later move towards a

fully integrated research-based company. They will, however, also help to buttress the other two

major strategic paths based on the IPCs traditional and location-dependent advantage. The

collaborative manufacturing partnering strategy path fits very well with the existing resource-

based competitive advantage of IPCs. By offering their copycat products and their low cost

18

manufacturing capacities to Big Pharma (often to the generics subunits of Big Pharma), they

pursue a classic resource leverage strategy reinforcing a sustainable competitive advantage.

The major rationale for the internationalisation of leading IPCs and for most of their foreign

acquisitions has been their strategy to become global generics players. This strategic path also

relies on traditional capabilities and location advantages, but necessitated the acquisition of new

resources and capabilities such as patent know-how, regulatory capabilities, and sales capacities in

the regulated pharmaceutical markets of the U.S. and Europe. So far only a few IPCs have

achieved or are in the process of achieving global player status. They may be able to profit from

the enormous growth opportunities of the major wave of patent expiries in the coming years, and

may also exploit their existing positions in unregulated emerging markets. On the other hand,

rivalry is increasing rapidly (mainly through the entry of Big Pharma into the generics space) and

take-overs of larger generics companies entail significant risk, as illustrated by Dr. Reddy’s recent

loss from its German Betafarm takeover (Sharma, 2010).

While it can be concluded that the global generics player pathway as well as the collaborative

strategy both fit well with environmental opportunities and the particular resources and

capabilities of leading IPCs – and can mutually reinforce each other – there is another ‘risk’ for

the Indian pharmaceutical industry and its leading players which is outside the key success factors

in product markets. Leading IPCs are often family owned companies (in business groups or as

stand-alones) which look for rapid growth and short- to medium term profit pay back. While there

were some earlier IPC takeovers by Big Pharma (such as Fresenius' acquisition of Dabur Pharma

in 2008) the most important event in this changing scenario has been the 2009 acquisition of

Ranbaxy, India’s ‘crown jewel’ among IPCs, , by Daiichi Sankyo (Yee, 2008; Sharma, 2009).

Although in this article Ranbaxy has still been treated as an IPC, it is in fact now the subsidiary of

a Japanese MNC. Leading positions in Ranbaxy have been staffed with Japanese managers and

Ranbaxy’s drug discovery activities are being terminated (BS, 2010). Another major move has

been the takeover of Piramal’s domestic Indian operations in 2010 by Abott Labs which reduces

another one of the top 10 IPCs to a smaller player (India Knowledge@Wharton, 2010, Fontanella-

Khan and Jack, 2010, Jayakumar and Barman, 2010). GlaxoSmithKline (and other Big Pharma

companies) are said to have an interest in Dr. Reddy’s and a number of other IPCs. Given these

dynamics, the only certainty seems to be that India will remain and advance as a globally

important manufacturing and contract research base. Whether Indian-owned pharmaceutical

companies will play a leading role in the global generics market (or in the long term even in the

19

innovation-based market segment) and become ‘adult EMNCs’ (Ramamurti, 2008) will not only

depend on the adequate resource and capability building strategies suggested in the academic

research reviewed above. It will, on the one hand, require surmounting the significant industry-

specific entry and mobility barriers; on the other hand, it will also depend on developments in the

‘market for corporate control’ which are influenced by the readiness of Indian owner families to

pursue a patient long-run strategy in which they may have to sacrifice short-term gains in favour

of long-term rewards.

For a select group of EMNCs in one particular high tech industry, this paper has exemplified the

influence of global structural industry characteristics on the distance or speed of their ‘leap’ in

‘leapfrogging’ and has found significant barriers which prevent a fast catch-up with ‘conventional’

MNEs. On the other hand, there are well-known examples of a fast catch-up process by EMNCs in

some other high tech or knowledge-based industries like for instance in telecom equipment

(Huawei and ZTE from China) or in IT Services (Tata Consulting Services and others from India).

It may therefore be useful to distinguish ‘fortress industries’ and ‘leapfrogging industries as the

two extreme points of a continuum. The former would tend to be industries where conventional

MNEs have entrenched positions based on industry typical barriers like accumulated knowledge,

reputational or intellectual assets, or complex global entry barriers like for instance in the global

pharmaceutical, auto, packaged software, or certain branded consumer goods industries. On the

other hand, the chances for leapfrogging by EMNCs may be higher in the emergent stages of an

industry life cycle like for instance in the wind, photovoltaic or IT outsourcing services industries,

or in mature and commoditized industries such as (standard) PCs or base steel. Further exploratory

case studies on EMNCs in selected industries are needed to discern the role of structural industry

characteristics from other influences like locational or company-specific antecedents or

Government support. Such studies along with resource-based and institutional approaches would

help to frame the ‘EMNC phenomenon’ in a larger historical perspective and evaluate some the

formidable barriers that the majority of EMNCs may have to overcome on their way to full

‘adulthood’.

20

References

Accenture (2007) ‘The Pursuit of High Performance through Research and Development – Understanding

Pharmaceutical Research and Development Cost Drivers’. Obtained through: http://www.accenture.com

[accessed 28/07/2010].

Accenture (2008) ‘Multipolar World 2: The Rise of the Emerging Country Multinational’. Obtained

through: http://www.accenture.com [accessed 1/8/2010]

Amighini, A., Sanfilippo, M. and Rabelotti, R. (2009) ‘The Rise of Multinationals from Developing

Countries. WP Series - N. 04/09. Università del Piemonte Orientale, Vercelli, Italy.

Anteby, M. and Nohria, N. (2008) ‘Michael Fernandes at Nicholas Piramal’. Harvard Business School

Case 9-408-001, Harvard Business School Publishing.

Athreye, S. and Godley, A. (2009) ‘Internationalization and Technological Leapfrogging in the

Pharmaceutical Industry’, Industrial and Corporate Change, Vol. 18, No. 2, pp.295-323.

Athreye, S., Kale, D. and Ramani, S.V. (2009): Experimentation with Strategy and Evolution of Dynamic

Capability in the Indian Pharmaceutical Sector, Industrial and Corporate Change, Vol. 18, No. 4, pp.729-

759.

Athreye, S.and Kapur, S. (2009) ‘Introduction: The internationalization of Chinese and Indian Firms -

Trends, Motivations and Strategy’, Industrial and Corporate Change, Vol. 18, No. 2, pp.209-221.

Bang, N. (2009) ‘A Shot in the Arm: Indian Pharmaceutical Sector has a Bright Future. 29th December.

Obtained through: http://www.stockmarketsreview.com [accessed 28/07/2010].

Bartlett, C. A. and Goshal, S. (2000) ‘Going Global - Lessons from Late Movers’, Harvard Business

Review, Vol. 78, No. 2, pp.131-141.

BCG (2006) ‘Harnessing the Power of India - Rising to the Productivity Challenge in Biopharma R&D’.

The Boston Consulting Group. Obtained through: http://www.bcg.com [accessed 2/8/2010].

Bhalla, V. et al. (2006) ‘Looking Eastward - Tapping India and China to Reinvigorate the Global

Biopharmaceutical Industry’. The Boston Consulting Group. Obtained through: http://www.bcg.com

[accessed 2/8/2010].

Bhandari, M. et al. (1999) ‘A Genetic Revolution in Health Care’. The McKinsey Quarterly, No. 4, pp. 59-

67.

Bruche, G. (2009) ‘The Emergence of China and India as New Competitors in MNCs Innovation

Networks’. Competition & Change, Vol. 13, No. 3, pp.267-288.

BS (2009) ‘Making Ranbaxy ‘Singh’ Again’. Business Standard, June 1, New Delhi, India.

BS (2010) ‘Ranbaxy to Shift Focus from New Drug Research to Generics’. Business Standard, May 16,

New Delhi, India.

Budhwar, P. S. et al. (2009) ‘The Role of HR in Cross-Border Mergers and Acquisitions: The Case of

Indian Pharmaceutical Firms’. The Multinational Business Review, Vol. 17, No. 2, pp. 89-110.

Cappelli. P. et al. (2010) The India Way: How India’s Top Business Leaders Are Revolutionizing

Management, Boston, MA.: Harvard Business Press.

CG (2010) Controller General of Patents Designs and Trademarks: Revised List of Pharmaceutical Product

Patents Granted During 2005-06 to 200-10, released 29 July. Obtained through:

http://www.patentoffice.nic.in [accessed 30/07/2010].

Chakravarthy, B. and Coughlan, S. (2009) ‘Dr. Reddy’s Laboratories: Realizing an Ambitious Vision’.

IMD case study IMD-3-2117, Lausanne, Switzerland.

Chaudhuri, S. (2005) The WTO and India's Pharmaceutical Industry: Patent Protection, TRIPS, and

Developing Countries, Oxford: Oxford University Press.

21

Chittoor, R. and Ray, S. (2007) ‘Internationalization Paths of Indian Pharmaceutical Firms - A Strategic

Group Analysis’. Journal of International Management, Vol. 13, pp.338-355.

Chittoor, R. et al. (2008) ‘Strategic Responses to Institutional Changes: 'Indigenous Growth' Model of the

Indian Pharmaceutical Industry’. Journal of International Management, Vol. 14, pp.252-269.

Chittoor, R. et al. (2009): Third-World Copycats to Emerging Multinationals: Institutional Changes and

Organizational Transformation in the Indian Pharmaceutical Industry. Organization Science, Vol. 20, No.

1, pp.187-205.

Clinton, P. and Mozeson, M. (2010) ‘Pharm Exec 50’. Pharmaceutical Executive, May, pp.69-80.

CMR (2010) (Center for Medicines Research) CMR International 2010 Pharmaceutical R&D Factbook,

Thomson Reuters - CRM International.

Cohen, W. M. and Levinthal, D.A. (1990) ‘Absorptive Capacity: a New Perspective on Learning and

Innovation’. Administrative Science Quarterly, Vol. 35, No. 1, pp.128-152.

Congressional Budget Office (2006): Research and Development in the Pharmaceutical Industry. Congress

of the United States, Washington, D.C., U.S.

Cygnus (2006). ‘White Paper on Indian Pharma Industry - Quest for Global Leadership’. Conference Paper

for Assocham Conference on 14 November 2006, Cygnus Business Consulting & Research, New Delhi,

India.

DiMasi, J. A. and Grabowski, H.G. (2007) ‘The Cost of Biopharmaceutical R&D: Is Biotech Different?’

Managerial and Decision Economics, Vol. 28, pp.469-479.

Dunning, J. H. (1998) ‘Location and Multinational Enterprise: A Neglected Factor?’ Journal of

International Business Studies, Vol. 29, No.1, pp.45-66.

EFPIA (2010) (European Federation of Pharmaceutical Industries and Associations) The Pharmaceutical

Industry in Figures. 2010 Edition, Brussels, Belgium.

Eisenhardt, K. M. and Graebner, M.E. (2007) ‘Theory Building from Cases: Opportunities and

Challenges’. Academy of Management Journal, Vol. 50, No.1, pp.25-32.

Evalueserve (2008) Patenting Landscape in India. Whitepaper No. 16, Evalueserve, Bangalore, India.

FDA (2010) Drugs@FDA – Original Abbreviated New Drug Application (ANDA) Approvals (by month).

Obtained through: http://www.accessdata.fda.gov [accessed 25/08/2010].

Fontanella-Khan, J. and Jack. A. (2010) Abott Buys India Drugs Unit for $3.7 bn., Financial Times, May

21, London, U.K.

Gassmann, O. and Reepmeyer, G. (2005) Organizing Pharmaceutical Innovation: From Science-based

Knowledge Creators to Drug-oriented Knowledge Brokers. Creativity & Innovation Management, Vol. 14

(3), pp.233-245.

Ghemawat, P. (2010) Strategy and the Business Landscape, Upper Saddle River, N.J.: Pearson.

GOI (2009) Annual Report. New Delhi: Government of India, Department of Pharmaceuticals.

Greene, W. (2007) The Emergence of India's Pharmaceutical Industry and Implications for the U.S.

Generic Drug Market. Office of Economics Working Paper No. 2007-05-A, Washington, D.C.: U.S.

International Trade Commission.

Guillén, M. F. and Garcia-Canal, E. (2009) ‘The American Model of the Multinational Firm and the 'New'

Multinationals from Emerging Economies’. Academy of Management Perspectives, Vol. 23, No. 2, pp.23-

35.

Hill, R. and Chui, M. (2009) ‘The Pharmerging Future’. Pharmaceutical Executive, July, pp.44-52.

IMS (2010) IMS Forecasts Global Pharmaceutical Market Growth of 5-8% Annually through 2014;

Maintains Expectations of 4-6% Growth in 2010. Press Release of 20 April. Obtained through:

www.imshealth.com [accessed 20/06/2010].

22

India Knowledge@Wharton (2010) A ‘Bigger Foothold’: What Does the Abott-Piramal Deal Mean for

Indian Pharma? Obtained through: http://knowledge.wharton.upenn.edu [accessed 10/06/2010].

Jayakumar, P.B. and Barman, A. (2010) ‘Making Money was not the Reason for this Sale’. May 22,

Business Standard, New Delhi, India.

Kale, D. (2009) ‘International Migration, Knowledge Diffusion and Innovation Capacities in the Indian

Pharmaceutical Industry’. New Technology, Work and Employment, Vol. 24, No. 3, pp.260-276

Kale, D. (2010) ‘The Distinctive Patterns of Dynamic Learning and Inter-Firm Differences in the Indian

Pharmaceutical Industry’. British Journal of Management, Vol. 21, pp.223-238.

Kale, D. and Little, S. (2007) ‘From Imitation to Innovation: The Evolution of R&D Capabilities and

Learning Processes in the Indian Pharmaceutical Industry’. Technology Analysis & Strategic Management,

Vol. 19, No. 5, pp.589-609.

Khanna, T. and Palepu, K. (2006) ‘Emerging Giants - Building World Class Companies in Developing

Countries’. Harvard Business Review, Vol. 84, No. 10, pp.60-70.

Kim, L. (1997), From Imitation to Innovation: The Dynamics of Korea's Technological Learning. Boston,

MA.: Harvard Business Press.

Kim, L. and Nelson, R.R. (2000) ‘Introduction: Technology, and Industrialisation in Newly Industrialising

Countries’. In: Kim, L. and Nelson, R.R. (eds.), Technology, Learning and Innovation: Experiences of

Newly Industrialising Economies (pp.1-10), Cambridge: Cambridge University Press.

Knol (2010) M&A Review: Pharmaceutical & Biotechnology Industry. Obtained through: http://knol.google.com [accessed 27/07/2010].

KPMG (2006) ‘The Indian Pharmaceutical Industry - Collaboration for Growth’. KPMG International.

KPMG (2009) ‘Global M&A: Outlook for Pharmaceuticals’. KPMG International.

Lamont, J and Whipp, L. (2009) ‘Industry ‘Odd Couple’ Hits Bump in the Road’. Financial Times, May 26, London, U.K..

Lee, K. and Lim, C. S. (2001) Technological Regimes, Catching-up and Leapfrogging: Findings from the

Korean Industries, Research Policy, Vol.30, No. 3, pp.459-483.

Levin, R. C. and Klevorick, A.K., et al. (1987) ‘Appropriating the Returns from Industrial Research and

Development’. Brookings Papers on Economic Activity No. 3.

Manil, S. (2006) ‘Sectoral System of Innovation of Indian Pharmaceutical Industry’. Working Paper No.

382, Trivandrum: Centre for Development Studies, India.

Mathews, J. A. (2002) Dragon Multinationals - A New Model for Global Growth. Oxford: Oxford

University Press.

Mathews, J. A. (2006) ‘Dragon Multinationals: New Players in 21st Century Globalization’. Asia Pacific

Journal of Management, Vol. 23, No. 1, pp.5-27.

McKinsey (2007) ‘India Pharma 2015 – Unlocking the Potential of the Indian Pharmaceutical Market’. McKinsey&Company.

Motilal Oswal Securities Ltd. (2010) ‘CRAMS – In Calmer Waters’. Mumbai, India.

Mueller, Janice M (2006) ‘The Tiger Awakens: The Tumultuous Transformation of India’s Patent System and the Rise of Indian Pharmaceutical Innovation’. Working Paper 43, University of Pittsburgh School of Law Working Paper Series, Pittsburgh, U.S.

Mueller, J. M. (2008) ‘Biotechnology Patenting in India: Will Bio-Generics Lead a ‘Sunrise Industry’ to

Bio-Innovation?’ Working Paper No. 2008-2, Legal Studies Research Paper Series, University of

Pittsburgh, School of Law, U.S.

North, D. (1990) Institutions, Institutional Change and Economic Performance. Cambridge: Cambridge

University Press.

23

Peng, M. W., Wang, D.Y. and Yi, J. (2008) ‘An Institution-based View of International Business Strategy:

a Focus on Emerging Economies’. Journal of International Business Studies, Vol. 39, pp.920-936.

Pisano, G. P. (1996) The Development Factory: Unlocking the Potential of Process Innovation. Boston,

Mass.: Harvard Business School.

PWC (2010) ‘Global Pharma Looks to India: Prospects for Growth’. PriceWaterhouseCoopers.

Pradhan, J. P. (2008) ‘Overcoming Innovation Limits through Outward FDI: The Overseas Acquisition

Strategy of Indian Pharmaceutical Firms’. Working Paper, Institute for Studies in Industrial Development,

New Delhi, India

Ramamurti, R. (2008) ‘What have we Learned about EMNEs’. In: Ramamurti, R. and Singh, J. (eds.),

Emerging Multinationals from Emerging Markets (Chapter 13), Cambridge: Cambridge University Press.

Reddy, K A. (2008) ‘Daiichi-Ranbaxy: A Transformational Deal’, The Economic Times, 16 June, Mumbai, India.

Rothaermel, F. T. (2001) ‘Incumbent's Advantage Through Exploiting Complementary Assets Via

Interfirm Cooperation’, Strategic Management Journal, Vol. 22, pp.687-699.

Sharma, Kumar E. (2009) ‘Indian Pharma’s Search for the Magic Pill’, Business Today, November 29, Mumbai, India.

Sharma, Kumar E. (2010) ‘Beyond Betafarm’, Business Today, March 21, Mumbai, India.

Sirkin, H. L. , Hemerling, J.W. and Bhattacharya, A.K. (2008) Globality - Competing with Everyone from

Everywhere for Everything. New York: Boston Consulting Group/Business Plus.

Teece, D. J. , Pisano, G., and Shuen, A. (1997) ‘Dynamic Capabilities and Strategic Management’.

Strategic Management Journal, Vol. 18, pp.509-533.

Wadhwa, V. et al. (2008) ‘The Globalization of Innovation: Pharmaceuticals - Can China and India Cure

the Global Pharmaceutical Market?’ Ewing Marion Kauffman Foundation.

Yadong, L., Tung, R.L. (2007) ‘International Expansion of Emerging Market Enterprises: A Springboard

Perspective’. Journal of International Business Studies, Vol. 38, pp.481-484.

Yee, A. (2008) ‘Big Pharma Meets Generics as Sons Hand Over ‘Crown Jewel’’. Financial Times, June 16,

London, UK.

Yin, R.K. (1994) Case Study Research: Design and Methods (2nd

ed.), Newbury Park, CA: Sage.

Notes

1 The data and material for the paper were collected in spring 2010 during a four month stay of the author at

Symbiosis Institute of International Business in Pune. In his previous career the author has worked in senior

management positions with a large pharmaceutical multinational, including five years as the company’s general

manager for China. 2 In Europe the term ‘biosimilars’ is used while in the U.S. the term ‘follow-on biologics’ is the official term for

generic biopharmaceuticals

24

Tables

Table 1 Top 10 Indian Pharmaceutical Companies by Worldwide Sales, 2009*

Company Worldwide sales

(million US$)

Rank,

domestic

sales

Share of

international

sales, %

R&D

spending,

million

US$

R&D

spending,

% of sales

Dr. Reddy’s 1,517 7 78.6 99.1 5.6

Ranbaxy** 1,509 9

84.4 89.0 5.9

CIPLA 1,158 1

56.9 51.2 4.4

Sun Pharma 974 4

52.8 67.4 6.9

Lupin Labs 842 8

66.0 50.4 6.0

Wockwardt 834 10

73.1 11.7 1.5

Piramal Healthcare 715 5

40.9 18.5 2.6

Aurobindo Pharma 673 2

29.4 17.0 2.5

Cadilla Healthcare 641 6

37.0 34.0 5.3

Glenmark Pharma 498

11

66.0 19.2 3.9

* Financial year 2009: April 2008 to March 2009; ** Ranbaxy is still included as it was only acquired by Daichi from

Japan in March 2009; sales for Ranbaxy are for calendar year 2009 as no comparable consolidated figures for FY

2009 were available. Sources: Annual reports (average exchange rate for the period 04/01/2009-03/31/2009: 45.994)

25

Table 2: Strategic Groups in the Indian Pharmaceutical Industry, 2005

Strategic

group

No. of

firms

API as % of

export

revenues*

Number

ANDAs**

Number

NCEs***

CRAMS as %

of total revenues

R&D expenses

as % of total

revenues

‘Exploiters’ 18 93.4 1.8 0.0 1.9 2.6

‘Explorers’ 15 26.3 5.6 0.4 0.0 5.8

‘Outsourcees’ 2 51.8 0.0 0.0 49.7 2.5

‘Emerging

global firms’

4 43.3 27.5 4.8 4.6 12.1

‘Global firm’ 1 12.0 150.0 4.0 0.0 9.5

All groups 40 59.2 9.4 0.7 3.8 4.9

* A high percentage of Active Pharmaceutical Ingredients (and conversely a low percentage of finished formulations)

indicates a focus on lower value added products; **A large number of Abbreviated New Drug Applications (for

products with imminent patent expiry) in the U.S.market indicates a strong internationalisation thrust into the

U.S.market; ***the number of New Chemical Entities is a measure of the firm’s focus on new drug

discovery/innovation; (d) a high share of Contract Research and Manufacturing revenues is a measure of the firm’s

focus on becoming an international outsourcing partner. Source: adapted from Chittoor and Ray 2007, p.346.

Table 3: R&D Spending of Leading Indian and Major Global Pharmaceutical Firms

Indian Pharmaceutical Companies Global Pharmaceutical Companies (Big Pharma)

Indian rank in

R&D spending Company

R&D Exp.

FY 2008/09,

million US$

Global Rank in

R&D Spending Company

R&D Exp.

2009, million

US$

1 Ranbaxy 99 1 Roche 8570

2 Dr. Reddy’s 89 5 GlaxoSmithKline 6286

3 Sun Pharma 67 10 Elli Lilly 4300

4 Cipla 51 25 Lundbeck 615

5 Lupin Labs 50 50 Watson 197

Sources: Table 1 and Clinton and Mozeson (2010)

26

Table 4: Leading Global Generics Companies, 2009

Est. global

sales rank

Company Sales in 2009 (partly rough

estimates)

Remarks

1 Teva (Israel) 13,899 Teva acquired Ratiopharm in 2010

2

Pfizer (U.S.) [Established Products Business Unit, Greenstone]

> 10,000 Pfizer does not directly list a 'generics' category in its annual report

3 Mylan Labs Inc. (U.S.) 5,093

4 Sandoz (Novartis) (CH)

7,493 Sandoz is Novartis’ specialised subsidiary for the generics business

5 Watson (U.S.) 2,793

6 Stada (D) 2,190

7 Ratiopharm (D) 1,667 Acquired by Teva in 2010

8 Dr. Reddy's (IN) 1,517*

9 Ranbaxy (IN) 1,509

10 Sanofi Aventis (F) (various subsidiaries)

1,400 Rapid increase expected from further acquisitions

11 Krka (Slowenia) 1,300

12 GlaxoSmithKline (Aspen Pharma) (UK)

1,200 Rapid increase expected through deal with Dr. Reddy’s and further acquisitions

* Figure refers to FY 2009; Source: Compiled by the author from various sources (annual reports, etc.)

27

Figure 1 The Pharmaceutical Value Curve

Source: Adjusted and expanded based on Bartlett and Goshal (2000), pp.135

28

Figure 2: The Pharmaceutical Value Chain

Source: author

29

Figure 3: Strategic Pathways of Major Indian Pharma Companies

Source: Author

30

Boxes

Box 1: Dr. Reddy’s: Difficult Journey towards Innovation

Founded in 1984 by Dr. Anji Reddy and currently a publicly listed company with 24 % family ownership,

DRL was India’s largest pharmaceutical company by global sales revenue in FY 2009. Among the larger

IPCs, DRL is the one with the strongest ambition to enter the research-based pharma competition space.

DRL’s attempts to move up the pharmaceutical value curve by a series of cumulative and mutually

reinforcing resource and capability building activities focused around four areas:

Generics: in its international expansion as a generics player DRL pursues a more risky strategy than

other Indian IPCs, involving challenging existing patents before their expiry so as to gain the 180 days

market exclusivity period under the Watchman-Hax Act. The resulting expertise in patenting and IP

litigation can also support DRL’s own innovative activities.

Incremental innovation: investments into novel drug delivery systems for known drugs to move up the

pharmaceutical value curve.

Biosimilars: the ‘imitation’ of biological drugs requires considerably more advanced capabilities than

in small molecule drugs and is far more risky. In 2007, DRL launched the world’s first biosimilar

monoclonal antibody, Reditux, in India.

Drug discovery: DRL started to invest in drug discovery as early as 1992, it established the first

discovery laboratory outside India in the U.S. in 1999, and founded a separate contract research service

organization. Research spending focused on a few specific therapy areas and led to a number of drug

candidates from which the two most advanced ones were licensed to Big Pharma (Novartis and Novo

Nordisk). As of 2009, DRL's revenues from its innovative drug activities (e.g. license income) were

less than 1% of overall revenues. Under the pressure of a significant loss DRL closed its U.S.

discovery laboratory, and shifted its Indian discovery and biosimilar operations into a separate

subsidiary with a view to attract collaborative venture capital funding from other partners, presumably

Big Pharma. Sources: Chakravarthy / Coughlan, 2009, Sharma, 2010, Annual Reports and press articles

31

Box 2: Selected Collaborative Deals between Big Pharma and IPCs (2008-2010)

Examples for Product Supply and Contract Manufacturing Deals

GlaxoSmithKline-Dr. Reddy’s: Strategic Alliance under which GSK gains exclusive access to Dr.

Reddy’s product portfolio of over 100 branded generic drugs and to its future pipeline. The

products are manufactured by Dr. Reddy’s and distributed by GSK in various emerging markets.

Pfizer-Aurobindo: Aurobindo obtains marketing authorizations for more than 50 patent-free

drugs and manufactures and supplies them to Pfizer, which will then sell them across the U.S. and

Europe through its ‘Established Products Business Unit’.

Pfizer – Strides Arcolab, Claris Life Sciences: Similar collaborative deals with the aim to support

Pfizer’s generics strategy in the U.S., Europe and emerging markets.

Abbott – Zydus Cadila: Strategic agreement to license 24 Cadila branded generics (with an option

of an additional 40 products) to support Abbott’s position across 15 emerging markets.

AstraZeneca- Torrent Pharmaceuticals: License and supply agreement for 18 drug products to

support AstraZeneca’s emerging markets strategy.

Example for a Comprehensive Manufacturing Development Approach

Piramal Healthcare: Strategy of partnering with Big Pharma by offering end-to-end services for

early pharmaceutical development during the testing stages of a drug and large-scale

pharmaceutical manufacturing after its launch. Piramal aims to be a ‘trustworthy partner’ for Big

Pharma, who respects intellectual property rights, refrains from reverse engineering and from

early generic entries after patents expire. Source: Anteby/Nohria, 2008

Examples for R&D Collaboration (Contract Research) Deals*

Elli Lilly-Zydus Cadila: Cadila works towards the discovery and development of potential

molecules against a novel drug target in the area of cardiovascular diseases. Cadila receives

(potential) milestone payments and royalties in the case of successful commercialisation.

AstraZeneca – Jubilant Organosys: Under a research agreement, Jubilant will deliver novel drug

candidates into AstraZeneca’s pre-clinical pipeline in the field of neurosciences. AstraZeneca will

own the compounds with worldwide development and commercialisation rights. Jubilant will

receive success-based milestone payments as well as royalties in the case of successful

commercialisation.

_______________

* We are only looking here at contract R&D between IPCs and Big Pharma companies. There is a large number

of specialised Contract Research Organisations (CROs) – Indian ones, but also subsidiaries of large Triad-based

CROs – which offer Big Pharma chemical, preclinical or clinical trial contract services .