may-18 aug-18 nov-18 jan-19 initiation · centres (puskesmas, the first level referral under uhc...

TRANSCRIPT

Company Note | Alpha series Hospitals │ Indonesia │ April 15, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

INITIATION

Medikaloka Hermina The healthiest growth

■ A well-paced expansion plan could enable HEAL to reach c.40 hospitals by 2020F, driving FY18-21F revenue CAGR of 16%, EBITDA margin of 18-20%.

■ The time-tested doctor partnership business model allows for balanced UHC and private patient growth, despite the scarcity of doctors in Indonesia.

■ UHC rollout completion could spark investor interest and we think HEAL is the best Indonesia healthcare proxy. Initiate Add, DCF-based TP of Rp4,000.

Growing at a healthy pace With 32 hospitals and 3,350 beds as at end-2018, HEAL plans to add four new hospitals

p.a. in FY19-20F, to reach a total of 40 hospitals and c.4,000 beds. Its moderate growth

strategy allows for mature hospitals to support new hospitals, which in turn, would enable

the company to sustain overall EBITDA margin of 18-20% in FY19-21F, with the ratio of

mature/new hospitals at 50:50. While its revenue/EBITDA rose by CAGR of 21%/20% in

FY15-18, we project slower revenue CAGR over FY18-21F, albeit at a decent pace of

c.16%, against the current 8% average for the Indonesian healthcare sector.

A tried and true model HEAL is one of the oldest private hospital chains in Indonesia with a simple hospital

design, in our view. Its capex per hospital is relatively low, at Rp150bn, vs. SILO’s and

MIKA’s c.Rp300bn. Its patient mix has also been consistent, i.e. more broad-based and

middle class, unlike the latter two players that targeted the upper-class segment but later

were compelled to have more UHC (Universal Healthcare) exposure. This results in more

consistent financial returns. Its doctor partnership model also allows for a more stringent

capital structure, which provides stability and supports consistent dividend payout.

Well suited to serve the middle class We believe HEAL was well positioned to benefit from the UHC rollout in 2014, given that

its low-cost model and patient profile are very compatible with the healthcare regulation

changes. Additional patient volume growth from UHC referrals could be absorbed by its

portfolio that is skewed towards Type C hospitals (78.5%). Its profit margins remain

robust under the Indonesia Case Base Group (INA-CBG) reimbursement scheme as it

treats simpler cases. As the middle class comprises 67% of the population in 2018 (56%

in 2010), we think HEAL will benefit as its business model caters to this demographic.

The best healthcare proxy We think HEAL’s business model promises healthier earnings growth than peers, and is

well-positioned to benefit from changing demographics in the long term. The hospital

sector has de-rated by 44% since UHC was rolled out in 2014, shedding most of the

euphoric premium, in our view. We believe the conclusion of UHC rollout in 2019F should

provide more certainty and, hence, visibility which could reignite investors’ interest in the

sector. Initiate coverage with an Add rating and DCF-based TP of Rp4,000 (WACC 10%,

LTG 6%), implying 19x FY19F EV/EBITDA. Downside risks include regulatory changes.

#DO NOT Leave Any Unused Text, Para etc. below this Line! as it will appear in the Email

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Indonesia

ADD

Consensus ratings*: Buy 5 Hold 0 Sell 0

Current price: Rp3,320

Target price: Rp4,000

Previous target: N/A

Up/downside: 20.5%

CIMB / Consensus: -4.8%

Reuters: HEAL.JK

Bloomberg: HEAL IJ

Market cap: US$699.0m

Rp9,870,360m

Average daily turnover: US$0.10m

Rp1,427m

Current shares o/s: 2,973m

Free float: 31.5% *Source: Bloomberg

Key changes in this note

N/A.

Source: Bloomberg

Price performance 1M 3M 12M

Absolute (%) -0.9 30.7

Relative (%) -1.7 30

Major shareholders % held Yulisar Khiat 11.8

Non Widjaja Kusuma 7.3

Binsar Parasian Simorangkir 5.8

Insert

Analyst(s)

Patricia GABRIELA

T (62) 21 3006 1734 E [email protected]

Vilhelmina T (62) 21 3006 1732 E [email protected]

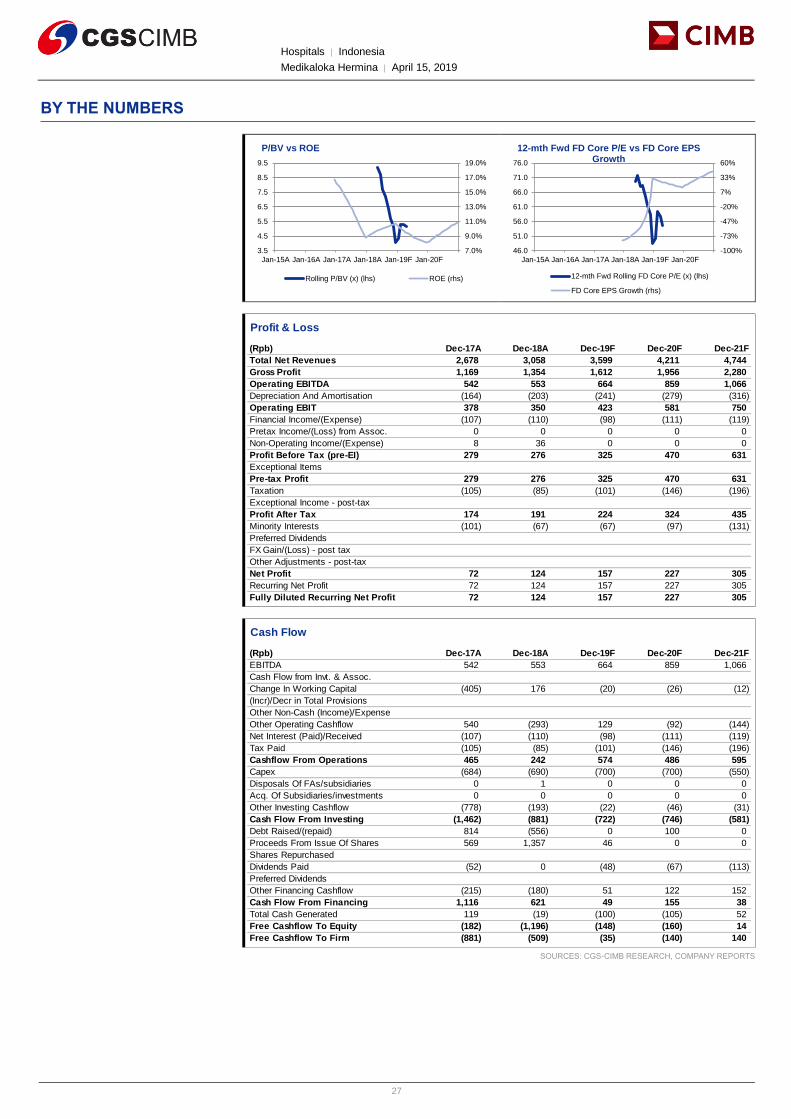

Financial Summary Dec-17A Dec-18A Dec-19F Dec-20F Dec-21F

Revenue (Rpb) 2,678 3,058 3,599 4,211 4,744

Operating EBITDA (Rpb) 542 553 664 859 1,066

Net Profit (Rpb) 72.4 124.4 156.8 226.9 304.7

Core EPS (Rp) 29.2 41.8 52.7 76.3 102.5

Core EPS Growth (71.8%) 43.1% 26.0% 44.8% 34.3%

FD Core P/E (x) 95.75 72.71 62.96 43.50 32.40

DPS (Rp) 21.15 0.00 16.06 22.60 38.16

Dividend Yield 0.64% 0.00% 0.48% 0.68% 1.15%

EV/EBITDA (x) 17.81 19.76 16.72 13.27 10.78

P/FCFE (x) NA NA NA NA 720.8

Net Gearing 97.4% 23.7% 25.5% 30.4% 25.7%

P/BV (x) 18.09 5.29 4.89 4.53 4.16

ROE 8.8% 10.7% 8.1% 10.8% 13.4%

% Change In Core EPS Estimates

CIMB/consensus EPS (x) 0.90 1.15

51.0

69.8

88.5

107.3

2,300

2,800

3,300

3,800

Price Close Relative to JCI (RHS)

10

20

30

40

May-18 Aug-18 Nov-18 Jan-19

Vo

l m

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

2

Healthy growth

BACKGROUND AND OVERVIEW

Company background

PT Medikaloka Hermina Tbk (HEAL) was first established in 1985 under the

licensed operation of a maternity hospital, Rumah Sakit Bersalin (RSB) Hermina.

Since then, the hospitals have undergone continuous expansion, adding beds

through new hospitals, development of existing hospitals, as well as acquisitions.

It now has 32 hospitals with 3,350 operational beds.

Under its expansion pipeline, four new hospitals will be built each year until

2020F, i.e. an additional 400 operational beds p.a. (from greenfield) to reach 40

hospitals in total. Although HEAL is more prominent in the women & children

subspecialty, its range of services include complex operating procedures,

laboratory services, radiology and imaging facilities, fertility treatment and public

health services, pharmacy, as well as diagnostic and emergency services.

HEAL is the largest private hospital group in the Greater Jakarta area and the

second largest private hospital on a national scale in terms of number of

hospitals and operational beds as at 2017. Its women & children services

provides one of the most comprehensive facilities compared to others in the

private segment, according to Frost & Sullivan in 2017.

Its operational scale allows it to be an early adopter of the Universal Healthcare

Coverage (UHC) programme while its business continues thriving. HEAL’s

EBITDA margin stayed at c.20% in 2016-18 with blended UHC patient

proportion increasing from 29% to 50% during the same period.

HEAL is the only listed hospital operator that adopts a doctor-partnership

business model (source: Frost & Sullivan). Under this scheme, doctors hold up

to 30% minority stake in each of the hospitals, which allows them to receive

dividends.

After adopting this model for more than 20 years, HEAL deems this approach

successful in retaining its main group of specialists (92% retention as of 2017),

recruiting qualified doctors, as well as preserving a loyal team of doctors and

medical staff who are familiar with each hospital’s operations. We believe this is

especially important in the midst of the scarcity of doctors observable across the

industry.

We expect HEAL to maintain its high retention rate, as their doctors benefit from

the operations of a large-scale hospital, sans worries about its management and

internal processes. This allows them to focus on their expertise while enjoying

the hospital’s growth.

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

3

Figure 1: HEAL’s list of hospitals and operational beds as of 2018

Note: *RS Hermina Grand Wisata recently upgraded to Type B hospital as of Jan 2019

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Hospitals in Indonesia are generally categorised into five different types – Class

A, B, C, D, and E. Different hospital types offer different facilities and are

equipped with different medical equipment. Here are the facilities provided in

each type of hospital:

- Hospital Type A: These are the top referral hospitals. They have a wide

range of specialists and subspecialists offering medical services from the

government. This is the highest form of reference available under UHC.

- Hospital Type B: Provides a wide range of specialist services, but limited

subspecialists. Type B hospitals are built in each province’s capital, to

accept referrals from regional hospitals.

- Hospital Type C: Provides limited subspecialist medical services. Type C

hospitals are built as regional hospitals to accept referral from local health

centres (Puskesmas, the first level referral under UHC referral system).

- Hospital Type D: These are hospitals in transition. They will soon convert to

Type C hospitals.

- Hospital Type E: These are special hospitals, offering only one specialised

medical service at each hospital (i.e. psychiatric, leprosy, pulmonary,

cardiology, and maternity hospitals). Most Type E hospitals are opened by

government bodies.

The UHC system currently applies the referral system for patients, making it

mandatory for patients to first visit lower ranked hospitals (Type C or D) before

they can see specialists in Type B or C hospitals.

Hospital nameCommencement of

operations (year)

Number of

operational bedsHospital type

RS Hermina Jatinegara 1985 170 B

RS Hermina Kemayoran 1995 108 B

RS Hermina Bekasi 1997 250 B

RS Hermina Depok 2000 180 B

RS Hermina Daan Mogot 2002 190 B

RS Hermina Bogor 2002 140 B

RS Hermina Grand Wisata 2009 150 *B

RS Hermina Pasteur 2004 130 C

RS Hermina Pandaran 2005 75 C

RS Hermina Tangkubanprahu 2006 85 C

RS Hermina Sukabumi 2007 95 C

RS Hermina Tangerang 2008 135 C

RS Hermina Arcamanik 2010 105 C

RS Hermina Galaxy 2010 90 C

RS Hermina Palembang 2011 150 C

RS Hermina Ciputat 2011 70 C

RS Hermina Mekarsari 2013 80 C

RS Hermina Serpong 2013 50 C

RS Hermina Banyumanik 2014 45 C

RS Hermina Solo 2014 50 C

RS Hermina Ciruas 2014 90 C

RS Hermina Yogya 2015 42 C

RS Hermina Bitung 2016 50 C

RS Hermina Makassar 2017 50 C

RS Hermina Balikpapan 2017 50 C

RS Hermina Medan 2017 50 C

RS Hermina Podomoro 2017 50 C

RS Hermina Purwokerto 2017 50 C

RS Hermina Samarinda 2018 50* C

RS Hermina Palembang 2018 50* C

RS Hermina Padang 2018 50* C

RS Hermina Lampung 2018 50* C

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

4

Management profile

Most of HEAL’s directors and commissioners are experienced doctors who have

been with the company since the start in 1985. Hence, they have hands-on

knowledge and experience with hospital operations. Most of them are also the

founding partners of the company.

Figure 2: HEAL's board of commissioners

SOURCES: COMPANY REPORTS

Name Position Background

Dr. Paulus Kusuma Gunawan,

SpOG

President

Commissioner

(2017-present)

73 years. Obsgyn Specialist and General Practitioners

from University of Indonesia.

A practicing doctor in RS Hermina Jatinegara (from

1975).

Dr. Husen Sutakaria, SpOG Vice President

Commissioner

(1982-present)

77 years. Obsgyn Specialist from University of

Padjajaran and General Practitioners from University of

Indonesia.

A practicing doctor in RS Hermina Jatinegara (from

1982).

Dr. Sudarsono, SpRM Commissioner

(2012-present)

56 years. Specialist degree for Physical Medicine and

Rehabilitation and General Practitioners from University

of Indonesia.

A practicing doctor in RS Hermina Jatinegara (from

2010).

Dr. Ir. Darwin Cyrill Noerhadi, MBA Commissioner

(2017-present)

56 years. Strategic Management Doctorate degree from

University of Indonesia, MBA in Finance & Economics

from University of Houston, Bachelor degree in Oil &

Geological Engineering from Institut Teknologi Bandung.

An Independent Commissioner for PT Austindo

Nusantara Jaya Tbk (2017-present), Independent

Commissioner for PT Mandiri Sekuritas (2012-present),

and President Director in PT Creador (2011-present).

Alexander Steven Rusli, PhD, MBA Independent

Commissioner

(2018-present)

47 years. Ph.D in Information Technology, Bachelor of

Commerce (Hons) in Information Technology and

Bachelor of Business from Curtin University of

Technology.

President Director for PT Indosat, Tbk (2012-2017),

Managing Director in PT Northstar Pacific (2009-2012),

Minister's expert staff at the Indonesian Ministry of

BUMN (2007-2009), Minister's expert staff at the

Indonesian Ministry of Information and Communication

(2001-2007), and Senior Consultant in

PricewaterhouseCoopers Consulting Asia Pacific (1997-

2001).

Dr. Heridadi Independent

Commissioner

(2018-present)

65 years. Doctorate degree from the School of Medicine

of Universitas Gajah Mada, Master in Healthcare

Planning and Management, and General Practitioners

from University of Indonesia.

Head of Alumni for FKUI 1977 (2012-present), Chairman

of Purna Warga Kesehatan TNI AD (2015-present), Vice

Chairman for Relations Section of Persatuan

Purnawirawan Angkatan Darat Relations (2012-present),

Master's Degree Professor in Universitas Pertahanan

(2012-present), and Commissioner in PT Biofarma (2014-

present).

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

5

Figure 3: HEAL's board of directors

SOURCES: COMPANY REPORTS

Private equity firms enter as shareholders and HEAL goes public

HEAL was listed on the Indonesia Stock Exchange (IDX) on 4 May 2018. It listed

351m ordinary shares at Rp3,700/share and raised Rp1.3tr.

Prior to this, in Sep 2017 the company went through financial restructuring with

the entry of private equity (PE) companies such as Creador Sdn Bhd through

preemptive rights issue, raising over Rp600bn. This diluted existing

shareholders’ stake by about 7.8%.

In addition to 351m ordinary shares issued for the public, 94.5m new shares

were issued for conversion of Mandatory Convertible Notes (MCN) to Apollo

Aurora Pte Ltd (Singapore) (Unlisted) and Andira Cordata Sdn Bhd (Unlisted)

and PT Sentul Cycling Klub (Unlisted). The current shareholder composition

shows that no single shareholder owns more than 15% of the total shares

outstanding. The shareholders include the company’s senior management. This

is again a unique model vs. other listed peers in Indonesia.

Under the listing covenant, it cannot issue additional shares or other instruments

that can be equivalently converted to shares within the next 12 months after the

IPO date.

Patient profile

In FY18, HEAL served a total of 5.6m patients, of which 5.3m were outpatients.

49% of total outpatients were UHC patients while 65% of total inpatient

admissions were UHC patients. Overall blended UHC patient proportion for

HEAL is 50% as of 2018, vs. Mitra Keluarga Karyasehat’s (MIKA IJ, Reduce, TP:

Rp1,450) 21% and Siloam International Hospital’s (SILO IJ, Hold, TP: Rp2,800)

27%. Note that blended UHC patient portion refers to total number of UHC

patients from both outpatient and inpatient combined, against total patients.

Name Position Background

Dr. Hasmoro, SpAn, MM, MHA President

Director (1991-

present)

75 years. Doctorate degree specialising in Anestensice

care and Anesthesia from University of Indonesia,

Master's degree focusing on Management from

Universitas Indonusa Esa Unggul, Master's degree for

Hospital Administration from IEU Institute of

Management, Anesthesia specialist from University of

Indonesia, General Practitioners University of

Padjajaran.

Member the Indonesian government team of doctors

(1979-2000).

Dr. Binsar Parasian Simorangkit,

SpOG

Medical and

Compliance

Director (1998-

present)

75 years. Obsgyn specialist and General Practitioners

from University of Indonesia.

Head of Hospital for RS Pusat Polri Raden Said

Sukanto (1994-1997).

Yulisar Khiar, SE, MARS Operational &

General Director

(1997-present)

60 years. Master's degree on Hospital Management

from University of Indonesia and Bachelor of Economics

from STIE PBM.

Vice General Director in RS Hermina Jatinegara (1985-

1997), Finance Manager in RS Hermina Hatinegara

(1983-1985).

Aristo Setiawidjaja, B.Sc, MBA Finance &

Strategic

Planning Director

(2019-present)

39 years. MBA from Dartmouth College, Bachelor's

degree in Chemical Engineering from University of

Wisconsin.

Senior Advisor position in Olympus Capital.

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

6

Figure 4: Shareholder structure, pre- and post-IPO as at May 2018

Note: Employee Stock Allocation (ESA) and Management and Employee Stock Option Plan (MESOP)

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Description

No of shares Nominal value (Rp) % No of shares Nominal value (Rp) %

Total Capital 10,000,000,000 1,000,000,000,000 10,000,000,000 1,000,000,000,000

Paid in Capital

Board of Commissioners:

- Husen Sutakaria 120,160,000 12,016,000,000 4.76% 104,110,500 10,411,050,000 3.40%

- Sudarsono 195,190,000 19,519,000,000 7.72% 169,118,900 16,911,890,000 5.52%

Board of Directors:

- Hasmoro 130,620,000 13,062,000,000 5.17% 113,173,300 11,317,330,000 3.70%

- Yulisar Khiat 403,830,000 40,383,000,000 15.98% 349,891,200 34,989,120,000 11.43%

- Binsar Parasian Simorangkir 199,180,000 19,918,000,000 7.88% 172,575,900 17,257,590,000 5.64%

Others:

- Non Widjaja Kusuma 250,640,000 25,064,000,000 9.92% 217,162,300 21,716,230,000 7.09%

- Soepardiman 190,570,000 19,057,000,000 7.54% 165,116,000 16,511,600,000 5.39%

- Tjiptawati Budiharta 171,820,000 17,182,000,000 6.80% 148,870,400 14,887,040,000 4.86%

- Soedibijo Toeloes 190,460,000 19,046,000,000 7.54% 165,020,700 16,502,070,000 5.39%

- Iskandar Wahidayat 125,890,000 12,589,000,000 4.98% 109,075,100 10,907,510,000 3.56%

- Raden Endjun 174,260,000 17,426,000,000 6.90% 150,984,500 15,098,450,000 4.93%

- Lydia Immanuel 197,380,000 19,738,000,000 7.81% 171,016,400 17,101,640,000 5.58%

- PT Citra Artha Niramaya 176,890,000 17,689,000,000 7.00% 79,685,800 7,968,580,000 2.60%

- Apollo Aurora (Singapore) - - 0.00% 77,167,400 7,716,740,000 2.52%

- Andira Cordata Sdn. Bhd - - 0.00% 155,095,900 15,509,590,000 5.06%

- PT Sentul Cycling Klub - - 0.00% 10,050,800 1,005,080,000 0.33%

- MHAI Master (Singapura) Pte. Ltd - - 0.00% 85,135,300 8,513,530,000 2.78%

- Brickellia Limited - - 0.00% 85,568,800 8,556,880,000 2.79%

- Masyarakat - - 0.00% 444,180,800 44,418,080,000 14.51%

- Program MESOP - - 0.00% 89,190,000 8,919,000,000 2.91%

Total Paid in Capital 2,526,890,000 252,689,000,000 100.00% 3,062,190,000 306,219,000,000 100.00%

Remaining Stocks 7,473,110,000 747,311,000,000 6,937,810,000 693,781,000,000

Before preemptive rights issue of shares, IPO, execution

of convertibles, ESA and MESOP programme, and selling

of shares by existing shareholders

After preemptive rights issue of shares, IPO, execution of

convertibles, ESA and MESOP programme, and selling of

shares by existing shareholders

Share Capital

Ordinary shares with Rp100 nominal value per stock

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

7

Figure 5: Patient volume breakdown Figure 6: Inpatient and outpatient volume

contribution from UHC

Figure 7: Revenue breakdown

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY

REPORTS SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY

REPORTS SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY

REPORTS

Similar to most hospitals, HEAL’s patient volume distribution has always been

dominated by outpatient visits, representing 95% of total patient volume but

outpatient visits contribute a relatively lower 33% of total revenue as at 2018.

Inpatient admissions, on the other hand, represent only 5% of total patient

volume but contribute 67% of total revenue. This percentage of volume and

revenue contribution from inpatient and outpatient has remained more or less

constant over the past three years. We expect the proportion to remain the same

in FY19-21F.

INDUSTRY OVERVIEW

Indonesia’s Universal Healthcare (UHC)

Indonesia officially launched the UHC programme – with Badan Penyelenggara

Jaminan Sosial (BJPS, Social Insurance Administration Body,) Health as its

running body – on 1 Jan 2014. Through this, the government expects 100% of

Indonesian citizens to have access to basic health coverage by 2019. The rollout

of UHC consists of a 5-year plan to fully cover all Indonesians and it has been

on track thus far (85% coverage as of 2M19).

Since its first year of operation, BPJS Health has been running a budget deficit.

One of the main reasons for this is the monthly premium fee that is set at an

affordable Rp23,000 for the subsidised populace (citizens entitled to Penerima

Bantuan Iuran, PBI), vs. the actuarial calculation of Rp36,000. Class III pays

Rp25,500/month though the actuarial estimate is more than double at Rp53,000.

Meanwhile, Class II forks out Rp51,000/month vs. the actuarially calculated fee

of Rp63,000. Though Class I is charged the same amount as that suggested

through actuarial calculations at Rp80,000/month.

In 2018 alone, BPJS Health incurred an Rp11tr deficit and received an Rp11tr

injection from the government to cover it. Given that escalating healthcare cost

outpaces premium fees, this deficit is unlikely to be resolved, in our view, unless

the government increases the monthly premium fee significantly and

continuously.

As part of the effort to manage ballooning cost, treatment curtailment has

become inevitable. The government has been pursuing this strategy (matching

disease coverage with available funding) in an effort to control the deficit

incurred by the programme.

Title:

Source:

Please fill in the values above to have them entered in your report

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018 2019F 2020F

Outpatient visits (%)

Inpatient admissions (%)

Inpatient admissions ('000)

Outpatient visits ('000)

Title:

Source:

Please fill in the values above to have them entered in your report

0%

20%

40%

60%

80%

100%

120%

140%

2016 2017 2018 2019F 2020F

Inpatient admissions Outpatient visits

Title:

Source:

Please fill in the values above to have them entered in your report

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018 2019F 2020F

Outpatient visits revenue (%)

Inpatient admissions revenue (%)

Inpatient admissions revenue

Outpatient visits revenue

Rp (bn)

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

8

To recap, Figure 8 summarises the UHC journey, which includes recent efforts to

lower the programme’s budget deficit. Most recently in Feb 2019, the new

ministerial decree excluded two drugs that treat metastatic colorectal cancer –

Bevacizumbab and Cetuximbab – which prompted quite a number of complaints.

A few weeks later in Mar 2019, the government announced its decision to cancel

the exclusion until further notice. Meanwhile, the government is reassessing the

drugs’ effectiveness in patient life extension.

Coordination of Benefit (COB) is another term intertwined with UHC. With the

COB facility, a patient is allowed to top-up medical benefits that were originally

eligible under UHC. The surplus cost incurred from treating the patient will be

borne by the insurance company while the cost which the patient was originally

eligible for will be paid for by BPJS Health. Although the COB mechanism has

been made available since 2014, we believe that it was only put into practice this

year. The recent 2019 ministerial decree allowing patients a maximum upgrade

of one level (for example, if UHC identified a person’s eligibility to be Class III,

the maximum upgrade is to Class II) is viewed positively by industry players, as

it finally allows insurance companies to implement better pricing and hence,

attract more prospective clients.

Nevertheless, given the political will, we expect the UHC programme to continue

to be well supported by the government.

Figure 8: UHC progress – UHC system as at Apr 2019

Note: *Formularium Nasional (ForNas) is a list of drugs covered by the BPJS Health system.

SOURCES: CGS-CIMB RESEARCH, MINISTRY OF HEALTH

It is noteworthy to us that Indonesia’s UHC programme has been very well

reviewed by the international community (source: Turkey Global Leaders Award

2018) despite the disparaging headlines locally. In addition, most Indonesians

have generally been very pleased with the programme despite the long

treatment queue (source: Kompas Dec 2018).

Effective Date Item

2014All diseases are covered under UHC with exception being: aesthetic procedures and infertility

treatment

2017 Eliminate possibility for patients to choose a specific hospital from referral system.

2018Exclusion of Pediatrician treatment for healthy babies, cataract operation procedure, and

physiotheraphy

2018Exclusion and re-inclusion of Trastuzumab (breast cancer drug) from (and to) ForNas/

Formularium Nasional*

2018Implemented supply chain financing (SCF) for claim payments through coordination with

Banks. Lower down late payment charge from initial 1%.

2018 Announced re-inclusion of pediatrician service for healthy baby, cataract operation for vision

quality worse than 6/18, and physiotheraphy for a maximum of 8x visit per month in Oct18.

2019 Applicable cost for patients Rp10-20k outpatient and 10% of INA-CBG tariff for inpatient

2019 Maximum of one level up in treatment class through co-payment

2019Exclusion and re-inclusion of Bevacizumbab and Cetuximbab (metastatic colorectal cancer

drug). Drugs are currently under assessment for its effectiveness.

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

9

Figure 9: Number of people covered by BPJS Health Figure 10: % of Indonesian population under coverage – 2019F

is the target for full coverage

SOURCES: CGS-CIMB RESEARCH, BPJS HEALTH SOURCES: CGS-CIMB RESEARCH, BPJS HEALTH

Applicable UHC monthly premium payments differ for each population group

(Figure 11), with main categories and their contributions detailed below.

a) Subsidised group: Rp23,000 monthly premium paid by government

b) Paid workers (Pekerja Penerima Upah, PPU)

b.1) PPU working in government institutions

Monthly premium of 5% of salary (maximum salary calculation at

Rp8m). 3% contribution from company and 2% contribution from worker.

b.2) PPU working in public or private companies

Monthly premium of 5% of salary (maximum salary calculation at

Rp8m). 4% contribution from company and 1% contribution from worker.

Additional members starting from the 4th child will be charged 1% of salary

monthly premium paid by worker.

c) Non-paid workers

Monthly premium paid by individual, depending on class preference.

d) Non-working group

Monthly premium paid by individual, depending on class preference.

Figure 11: Premium paid for UHC as at 2018

SOURCES: CGS-CIMB RESEARCH, MINISTY OF HEALTH

Title:

Source:

Please fill in the values above to have them entered in your report

133,423,653

156,790,287

171,939,254

187,982,949

215,860,046

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

2014 2015 2016 2017 2018

No of people

Title:

Source:

Please fill in the values above to have them entered in your report

52.3%

60.7%

66.3%71.6%

80.9%

100.0%

0%

20%

40%

60%

80%

100%

120%

2014 2015 2016 2017 2018 2019F

Title:

Source:

Please fill in the values above to have them entered in your report

Rp23,000

Rp240,000

Rp120,000

Rp320,000

Rp160,000

Rp160,000

Rp80,000

Rp80,000

Rp40,000

Rp80,000

Rp40,000

Rp80,000

Rp51,000Rp25,500

Rp80,000

Rp51,000Rp25,500

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Cla

ss I

Cla

ss II

Cla

ss I

Cla

ss II

Cla

ss I

Cla

ss II

Cla

ss I

Cla

ss II

Cla

ss III

Cla

ss I

Cla

ss II

Cla

ss III

PBI Paid workers (PPU)in gov institutions

Paid workers (PPU)in BUMN, BUMD

and private sector

PPU additional fammembers (from 4th

child)

Non-paid workers Non working group

Paid by Government Paid by Company Paid by Individual

Rp

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

10

Fragmented market

Indonesia’s healthcare industry is highly fragmented, with HEAL’s private

hospitals only representing 2.2% of the country’s private hospitals. Its

operational beds form a mere 0.8% of the country’s total beds in 2017 – despite

being the second-largest private hospital group in Indonesia. Mitra Keluarga’s

and Siloam Hospitals’ operational beds accounted for 0.7% and 1.0%,

respectively, of the country’s total beds in 2017. Given the small bed capacity of

individual hospitals and Indonesia’s growing population that continually pushes

for higher bed capacity, we expect both public and private hospital groups to

compete aggressively for a share of the expanding market.

Figure 12: Market share of private hospital groups in Indonesia (2017)

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS, MINISTRY OF HEALTH

Figure 13: Number of national beds and % share for listed hospitals

SOURCES: CGS-CIMB RESEARCH, MINISTRY OF HEALTH, COMPANY REPORTS

Figure 14: Breakdown of hospitals in Indonesia by type - hospitals in Indonesia are

still dominated by private healthcare providers as at 2017

Note: *Government General Hospitals (GH)

SOURCES: SOURCES: CGS-CIMB RESEARCH, MINISTRY OF HEALTH

Hospital GroupMarket share (% of total

national hospitals)

Market share (% of total

national beds)

Medikaloka Hermina 1.0% 0.8%

Siloam Hospitals 1.1% 1.0%

RS Mitra Keluarga 0.7% 0.7%

RS Awal Bros 0.4% 0.6%

Mayapada Hospital 0.1% 0.1%

RS Pondok Indah 0.1% 0.1%

Title:

Source:

Please fill in the values above to have them entered in your report

0.6%0.7% 0.8%, HEAL

1.0%, SILO

0.7%, MIKA

0%

1%

290,000

295,000

300,000

305,000

310,000

315,000

320,000

325,000

330,000

335,000

340,000

345,000

2015 2016 2017

National # of operational bed (LHS) (HEAL) % of national operational bed

(SILO) % of national operational bed (MIKA) % of national operational bed

Number of beds

Title:

Source:

Please fill in the values above to have them entered in your report

Government GH, 7%

Provincial government GH,

24%

Private GH, 48%

Special hospital, 21%

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

11

Doctor and bed scarcity

Indonesia has a shortage of doctors in the healthcare industry. Doctors per

1,000 capita was recorded at 0.5 in 2016, the lowest compared to neighbouring

Asian countries, i.e. Vietnam, Thailand, Malaysia, and India which were at 0.7,

0.6, 1.3, and 0.7, respectively. The Ministry of Health targets to improve the ratio

to 0.6 by 2021F (7% CAGR over FY18-21F), in part due to the government’s

2019F UHC programme. The UHC system is predicted by healthcare industry

players to increase the demand for doctors, along with an increase in number of

patients across Indonesia, as a greater part of the population utilises healthcare

services under the system.

Coupled with its relatively low doctor per capita ratio, Indonesia also has the

second-lowest ratio for hospital beds per 1,000 capita (source: CIA, Central

Intelligence Agency). In 2015, Indonesia maintained hospital beds per 1,000

capita at 1.2, about half compared to that of Singapore. We expect this to

improve by 2019F, boosted by UHC expenditure which should provide access to

health insurance for the greater public and increase the need for additional bed

capacity.

Figure 15: Doctors per 1,000 capita in

various countries (2016)

Figure 16: Hospital beds per 1,000 capita

in various countries (2015)

Figure 17: Indonesia's healthcare

expenditure as a % of GDP

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS SOURCES: CGS-CIMB RESEARCH, CIA LIBRARY SOURCES: CGS-CIMB RESEARCH, MINISTRY OF HEALTH,

FROST & SULLIVAN ESTIMATES

Growth driven by changing demographics and improving purchasing power

The expected increase in the demand for healthcare services is the main driver

for Indonesia’s continual expansion of hospital capacity. We believe the

assumption by healthcare industry players is that additional supply can be

absorbed completely by demand, given Indonesia’s relatively low percentage of

healthcare expenditure to GDP (3.6% in 2015). Global average healthcare

expenditure as a percentage of GDP is 9.9% as at 2015 according to the World

Healthcare Organization (WHO) Global Health Expenditure Database. According

to Frost & Sullivan, Indonesia’s healthcare expenditure as a percentage of GDP

is expected to rise to 4.3% (US$50.8bn) by 2020F.

Title:

Source:

Please fill in the values above to have them entered in your report

0.5

0.6

0.7 0.7

1.3

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Indonesia Thailand Vietnam India Malaysia

Title:

Source:

Please fill in the values above to have them entered in your report

0.81.2 1.3

1.92.4 2.5 2.7

3.43.8

5.8

11.5

0

2

4

6

8

10

12

14 Title:

Source:

Please fill in the values above to have them entered in your report

3.3%

3.6%

4.3%

0%

1%

2%

3%

4%

5%

2010 2015 2020F

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

12

Figure 18: Comparison of healthcare expenditure per capita in different countries

(2014)

SOURCES: CGS-CIMB RESEARCH, FROST & SULLIVAN

The middle class in Indonesia represents 67% of the country’s population as at

2018 (source: Statistics Indonesia, Badan Pusat Statistik, BPS) vs. 56% in 2010,

largely due to a shift towards urbanisation. While urbanisation is highly

correlated (source: WHO) with more people moving up from the lower-income to

the middle-income class, it also translates to a rising demand for healthcare

services due to an increase in lifestyle-related diseases, such as cardiovascular

disease, cancer and diabetes, to name a few. This inevitable byproduct of

urbanisation gives rise to the need for more sophisticated medical tools for

diagnostic and treatment purposes. In turn, this creates opportunity for players in

the healthcare industry in terms of new patients and volumes.

Since the implementation of the UHC in 2014, payment methods have changed,

with the out-of-pocket proportion of national healthcare expenditure decreasing

to c.48% in 2015 (vs. 57% in 2010). Over the same period, government

spending increased from 28% to 36%. The absolute value of out-of-pocket

expense, however, has increased. This indicates a better national healthcare

insurance system, in our view, and higher demand for healthcare services due to

an overall improvement in economic growth. Moving forward, we believe the

positive outlook on the country’s economic growth, coupled with 2019F UHC

coverage, could further boost the performance of the healthcare industry.

Figure 19: Indonesia's income level distribution

Note: *Population in 2010 amounted to 234.1m individuals and **population in 2018 amounted to 266.9m individuals

SOURCES: CGS-CIMB RESEARCH, INDONESIAN BANK RESTRUCTURING AGENCY (BANK PERBANKAN NASIONAL, BPPN), BPS

Title:

Source:

Please fill in the values above to have them entered in your report

99 135 142360 420 456

2,752

3,935

9,403

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Indonesia Philippines Vietnam Thailand China Malaysia Singapore UnitedKingdom

UnitedStates

US$

Title:

Source:

Please fill in the values above to have them entered in your report

0.5

42.14

90.1

68.6

32.8

0.8

58.7

120.1

61.5

25.8

0 20 40 60 80 100 120 140

Affluent

Middle Class

Aspiring Middle Class

Poor

Below Poverty Line

>7300

1460 -

7300

730 -

1460

278-7

30

<278

No. of individuals (m)

Per

ca

pit

a E

xpen

dit

ure

/ ye

ar

(US$

)

2018 2010

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

13

Figure 20: Shift in healthcare payment schemes (pre- and post-UHC in 2010-2015)

SOURCES: CGS-CIMB RESEARCH, MINISTRY OF HEALTH

A MORE STABLE MODEL

Pursuing growth at different paces

While MIKA has expanded at a cautious pace (six new hospitals in 2015-18),

SILO is more aggressive, with the opening of 15 new hospitals over 2015-18.

HEAL’s expansion strategy is more moderate than SILO’s, opening a total of

twelve new hospitals during the same period. We believe this strategy strikes the

right balance between development and growth while also supporting stable

margins. HEAL’s gross profit/EBITDA grew at a CAGR of 22%/20% over 2015-

18, much higher than peers, MIKA and SILO, at 10%/12% and 18%/9% over the

same period – mostly due to the balance between expansion and the proportion

of mature hospitals in the group’s portfolio. HEAL’s revenue growth was also at

a faster CAGR of 21.4% in 2015-18 (vs. MIKA’s and SILO’s CAGR at 8.2% and

12.9%, respectively, in the same period).

Figure 21: Comparison of HEAL, MIKA & SILO expansion plans,

based on respective companies’ guidance

Figure 22: HEAL's mature hospitals as a % of total hospitals vs.

expansion

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

0

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014 2015

Spending by Government (LHS) Spending from Out of pocket (LHS)

Spending by Private companies/ insurance (LHS) % Contribution from Government

% Contribution from Out of pocket expense % Contribution from Private/ insurance companies

Rptr

Title:

Source:

Please fill in the values above to have them entered in your report

22

24 28

32

36

40

20

23

31

35

40 42

12 12 12

21

27

33

0

5

10

15

20

25

30

35

40

45

2015 2016 2017 2018 2019F 2020F

SILO MIKA HEAL

No. of hospitals

Title:

Source:

Please fill in the values above to have them entered in your report54.5%

58.3%

57.1%

50.0% 50.0%

52.5%

44%

46%

48%

50%

52%

54%

56%

58%

60%

0

5

10

15

20

25

30

35

40

45

2015 2016 2017 2018 2019F 2020F

Total no of hospitals No. of new hospitals % of mature hospitals (RHS)

No. of hospitals

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

14

Greenfield expansion/hospital acquisition tends to lead to margin contraction, in

our view. The opening of new hospitals causes G&A expense (fixed costs) to

spike while revenue lags as patient traffic tends to be slower initially for new

hospitals. The opening of many new hospitals can have an adverse impact on

profitability. This was seen in SILO’s aggressive expansion in 2017 when it

opened eight new hospitals, which caused operating expense to rise to 36.7%

(vs. 2016’s 33.1%) while revenue grew by only 3% yoy. This is compared to

HEAL’s operating expense at 29.5% of revenue and 20% revenue growth for the

same period.

In HEAL’s case, its well-paced expansion has allowed for solid earnings growth.

This allows it to maintain a better proportion of mature hospitals in its portfolio. In

2015-18, HEAL’s mature hospitals formed 50-58% of its portfolio (Figure 23),

compared to SILO’s 30%. Mature hospitals, unlike new ones, contribute the

majority of revenue and are important, especially during the expansion period

when most new hospitals contribute losses.

To further illustrate, in 2015, six out of a total of 22 hospitals of HEAL’s oldest

hospitals that had operating for more than 10 years contributed to 52% of total

revenue. While we expect the proportion of HEAL’s mature hospitals to decline

to c.50% of total hospitals in 2019F due to the opening of four new hospitals in

both years (FY18-19F), we do not expect much erosion on profitability due to its

strategy of focusing on volumes instead of profit.

Figure 23: HEAL’s revenue contribution from mature hospitals

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Consistency and predictability

HEAL uses a simple and standardised design for its hospital buildings, which

allows it to benefit from cost efficiencies. In FY17, while its competitors MIKA

and SILO spent Rp300bn capex to build a new hospital, HEAL spent Rp150bn

for each new hospital (average cost per bed for HEAL is Rp0.91bn, vs. Rp1.5bn

for SILO and MIKA over a 5-year expansion period). We note that average cost

per bed is higher in the first phase of hospital operations due to land acquisition.

The impact of lower capex per new hospital is a shorter payback period, given

similar profitability profile (based on patient volume and cost of treatment) as its

competitors, in this case SILO. In 2019F, we expect HEAL’s ROE/ROIC to be

more attractive at 6%/11% compared to SILO’s 1.2%/1.9%, based on our

estimates.

Title:

Source:

Please fill in the values above to have them entered in your report52.0% 51.1%

48.4%

54.5%

58.3% 57.1%

0%

10%

20%

30%

40%

50%

60%

70%

2015 2016 2017

Revenue contribution from (Top 6) oldest hospitals Mature hospitals as a % of total hospitals

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

15

Figure 24: Comparison of hospitals' profitability matrix

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

Although MIKA’s historical performance suggests higher profitability in terms of

both ROIC and ROE, its future profitability may not be replicable, in our view, as

the company just started accepting more UHC patients through Kasih Group

(acquired in 4Q17) which we believe may hurt margins.

Focused market segment

HEAL has generally always been persistent in targeting the middle class, and

focusing more on patient volumes than margins, in our view. In 2018, MIKA and

SILO’s blended proportion of UHC patients amounted to around 21% and 28%,

respectively. In the same period, HEAL maintained a 50% blended UHC

proportion (65% of total inpatient admissions and 49% of outpatient visits), which

we attribute to being an early adopter of the programme.

Its proportion of UHC patients has risen to 50% as at 2018 and we believe it is

unlikely to increase further. UHC patients tend to mean slower per patient

revenue growth, thus a saturated proportion of UHC patient revenue is positive,

in our view. A recovery in private sector patients could also provide upside risk

for the company.

HEAL’s approach to market positioning is different from MIKA and SILO, which

have continual fluctuations in their allocated portion of UHC patients. SILO

started allocating 10% of total patient volume to UHC patients in 2015, while

MIKA extended its services for UHC patients in 4Q17.

Figure 25: Higher UHC contribution tends to lower revenue per

patient…

Figure 26: … which results in modest revenue growth from

pricing because as the number of patients from BPJS increases,

revenue per patient grows at a slower pace.

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

ROE 2015 2016 2017 2018 2019F 2020F

HEAL N/A 5.6% 8.8% 7.5% 6.3% 8.3%

MIKA 22.5% 20.1% 17.7% 14.5% 15.7% 17.7%

SILO 4.1% 3.5% 2.0% 0.3% 1.2% 1.2%

ROIC 2015 2016 2017 2018 2019F 2020F

HEAL N/A 15.8% 16.4% 13.2% 11.4% 14.0%

MIKA 61.7% 40.4% 23.2% 18.5% 21.3% 25.3%

SILO 6.5% 7.6% 3.9% 0.8% 1.9% 2.7%

Title:

Source:

Please fill in the values above to have them entered in your report

7.47.5

7.37.1 7.1

0.25 0.230.20 0.16 0.15

29%

45%50% 50% 50%

0%

10%

20%

30%

40%

50%

60%

0

1

2

3

4

5

6

7

8

2016 2017 2018 2019F 2020F

Avg revenue per inpatient Avg revenue per outpatient

BPJS contribution (RHS)

Rp m

Title:

Source:

Please fill in the values above to have them entered in your report

2.5%

-2.6%

-2.8%

0.0%

2.0%

-9.3%

-12.7%

-20.9%

-5.0%

0.0%

0%

10%

20%

30%

40%

50%

60%

-25%

-20%

-15%

-10%

-5%

0%

5%

2016 2017 2018 2019F 2020F

per Inpatient revenue growth (%) per Outpatient revenue growth (%)

BPJS contribution (%)

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

16

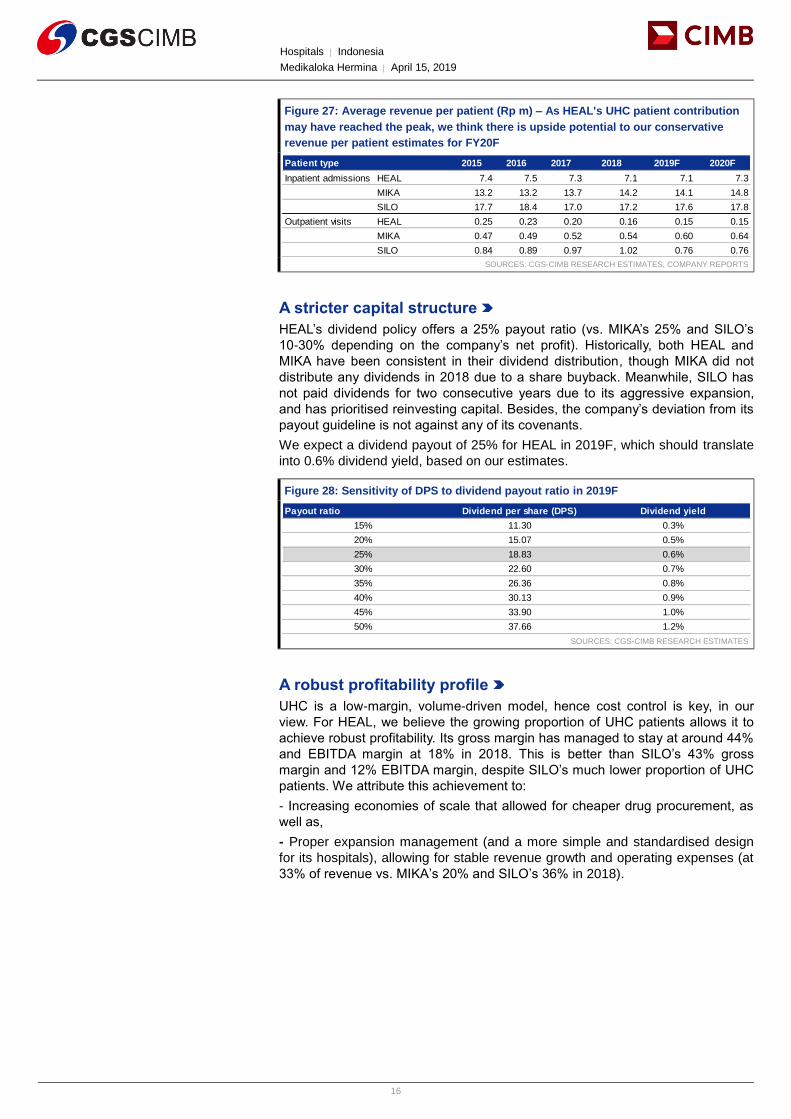

Figure 27: Average revenue per patient (Rp m) – As HEAL's UHC patient contribution

may have reached the peak, we think there is upside potential to our conservative

revenue per patient estimates for FY20F

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

A stricter capital structure

HEAL’s dividend policy offers a 25% payout ratio (vs. MIKA’s 25% and SILO’s

10-30% depending on the company’s net profit). Historically, both HEAL and

MIKA have been consistent in their dividend distribution, though MIKA did not

distribute any dividends in 2018 due to a share buyback. Meanwhile, SILO has

not paid dividends for two consecutive years due to its aggressive expansion,

and has prioritised reinvesting capital. Besides, the company’s deviation from its

payout guideline is not against any of its covenants.

We expect a dividend payout of 25% for HEAL in 2019F, which should translate

into 0.6% dividend yield, based on our estimates.

Figure 28: Sensitivity of DPS to dividend payout ratio in 2019F

SOURCES: CGS-CIMB RESEARCH ESTIMATES

A robust profitability profile

UHC is a low-margin, volume-driven model, hence cost control is key, in our

view. For HEAL, we believe the growing proportion of UHC patients allows it to

achieve robust profitability. Its gross margin has managed to stay at around 44%

and EBITDA margin at 18% in 2018. This is better than SILO’s 43% gross

margin and 12% EBITDA margin, despite SILO’s much lower proportion of UHC

patients. We attribute this achievement to:

- Increasing economies of scale that allowed for cheaper drug procurement, as

well as,

- Proper expansion management (and a more simple and standardised design

for its hospitals), allowing for stable revenue growth and operating expenses (at

33% of revenue vs. MIKA’s 20% and SILO’s 36% in 2018).

Patient type 2015 2016 2017 2018 2019F 2020F

Inpatient admissions HEAL 7.4 7.5 7.3 7.1 7.1 7.3

MIKA 13.2 13.2 13.7 14.2 14.1 14.8

SILO 17.7 18.4 17.0 17.2 17.6 17.8

Outpatient visits HEAL 0.25 0.23 0.20 0.16 0.15 0.15

MIKA 0.47 0.49 0.52 0.54 0.60 0.64

SILO 0.84 0.89 0.97 1.02 0.76 0.76

Payout ratio Dividend per share (DPS) Dividend yield

15% 11.30 0.3%

20% 15.07 0.5%

25% 18.83 0.6%

30% 22.60 0.7%

35% 26.36 0.8%

40% 30.13 0.9%

45% 33.90 1.0%

50% 37.66 1.2%

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

17

Figure 29: HEAL’s EBITDA margin is

stable despite growing UHC contribution

Figure 30: HEAL's economies of scale

allows its avg. cost per patient (for drugs)

to decline

Figure 31: Rise in operating expenses is

aligned with growing revenue

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY

REPORTS SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY

REPORTS SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY

REPORTS

MIKA’s EBITDA margin was the highest among the three at 36% in 2018.

However, moving forward, we have increasing concerns that this could decline

due to the company’s attempts to diversify its patient portfolio and extend

services to reach more UHC patients.

More able to ride UHC growth

2019 is the final year of the implementation of the government’s UHC initiative.

However, as UHC has been running at a deficit since its commencement in

2014, the government has been introducing a number of follow-up ministerial

decrees in order to suppress its ballooning deficit. As a hospital with high

exposure to UHC patients, HEAL is more vulnerable towards changes in

healthcare regulations, in our view. Yet, we see HEAL weathering the regulatory

changes. Patient volume managed to increase at a CAGR of 24% over FY15-18,

resulting in overall revenue CAGR of 21% in the same period (vs. MIKA’s 8%

and SILO’s 13%).

The steady growth, in our view, is mostly due to the referral system and disease

curtailment (listed above) under UHC. We believe HEAL’s hospital profile, which

is highly concentrated in type C hospitals (the first referral for general hospitals

under UHC) (81.3%, or 26 out of 32 hospitals in 2018), provides upside to its

patient base and profitability mix. A less complicated case mix results in higher

margins under the Indonesia Case Base Group (INA-CBG, which defines the

standard tariff under the UHC system) reimbursement scheme. On the other

hand, the effect on disease curtailment could lead to an improvement in the

hospital’s trade receivables from 25.4% of revenue in 2018 to 23% of revenue in

2019F, based on our estimates. This is based on the expectation that hospitals

will receive more upfront payments from patients (both out-of-pocket and

through insurance companies). We also expect better cashflow management by

BPJS Health to lead to stable receivable days at 84 in 2019F.

With 85% UHC coverage now, we are seeing extremely high waiting times,

especially when patients are seeking treatment for non-catastrophic diseases.

We expect to see a gradual increase in private healthcare services given the

separate queues for UHC and private patients, as seen over the past four

quarters, according to HEAL. Thus, we expect HEAL to maintain its strong

reputation and patient base, and streamline its efforts to focus on retention

instead of patient acquisition.

Title:

Source:

Please fill in the values above to have them entered in your report

19.7% 20.2%18.1% 18.4%

20.4%

29%

45%

50% 50% 50%

0%

10%

20%

30%

40%

50%

60%

2016 2017 2018 2019F 2020F

BPJS contribution (%) EBITDA margin (%)

Title:

Source:

Please fill in the values above to have them entered in your report

160.0

153.9

147.0

143.3

146.2

130

135

140

145

150

155

160

165

2016 2017 2018 2019F 2020F

Avg cost per patient

Rp m

Title:

Source:

Please fill in the values above to have them entered in your report31%

20%

14%

18%

17%

33%

16%

27%

18%

16%

0%

5%

10%

15%

20%

25%

30%

35%

2016 2017 2018 2019F 2020F

Revenue growth Operating expenses growth

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

18

Fewer benefits from industry consolidation

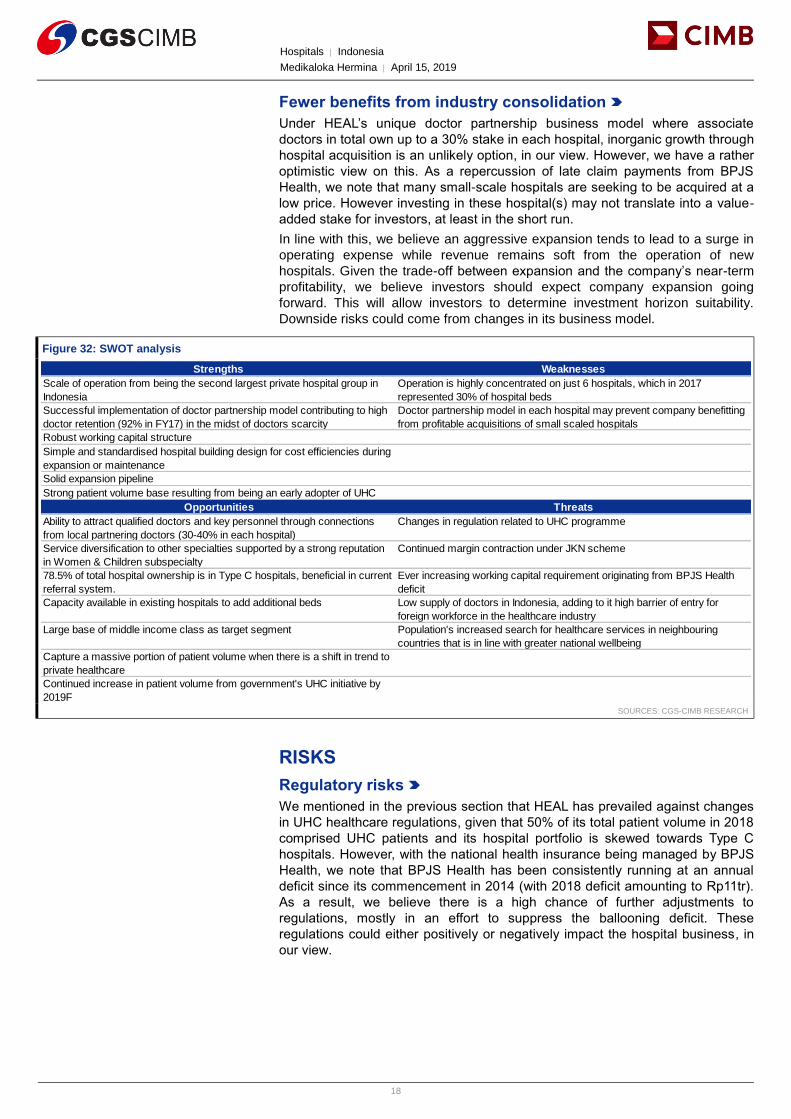

Under HEAL’s unique doctor partnership business model where associate

doctors in total own up to a 30% stake in each hospital, inorganic growth through

hospital acquisition is an unlikely option, in our view. However, we have a rather

optimistic view on this. As a repercussion of late claim payments from BPJS

Health, we note that many small-scale hospitals are seeking to be acquired at a

low price. However investing in these hospital(s) may not translate into a value-

added stake for investors, at least in the short run.

In line with this, we believe an aggressive expansion tends to lead to a surge in

operating expense while revenue remains soft from the operation of new

hospitals. Given the trade-off between expansion and the company’s near-term

profitability, we believe investors should expect company expansion going

forward. This will allow investors to determine investment horizon suitability.

Downside risks could come from changes in its business model.

Figure 32: SWOT analysis

SOURCES: CGS-CIMB RESEARCH

RISKS

Regulatory risks

We mentioned in the previous section that HEAL has prevailed against changes

in UHC healthcare regulations, given that 50% of its total patient volume in 2018

comprised UHC patients and its hospital portfolio is skewed towards Type C

hospitals. However, with the national health insurance being managed by BPJS

Health, we note that BPJS Health has been consistently running at an annual

deficit since its commencement in 2014 (with 2018 deficit amounting to Rp11tr).

As a result, we believe there is a high chance of further adjustments to

regulations, mostly in an effort to suppress the ballooning deficit. These

regulations could either positively or negatively impact the hospital business, in

our view.

Strengths Weaknesses

Scale of operation from being the second largest private hospital group in

Indonesia

Operation is highly concentrated on just 6 hospitals, which in 2017

represented 30% of hospital beds

Successful implementation of doctor partnership model contributing to high

doctor retention (92% in FY17) in the midst of doctors scarcity

Doctor partnership model in each hospital may prevent company benefitting

from profitable acquisitions of small scaled hospitals

Robust working capital structure

Simple and standardised hospital building design for cost efficiencies during

expansion or maintenance

Solid expansion pipeline

Strong patient volume base resulting from being an early adopter of UHC

Opportunities Threats

Ability to attract qualified doctors and key personnel through connections

from local partnering doctors (30-40% in each hospital)

Changes in regulation related to UHC programme

Service diversification to other specialties supported by a strong reputation

in Women & Children subspecialty

Continued margin contraction under JKN scheme

78.5% of total hospital ownership is in Type C hospitals, beneficial in current

referral system.

Ever increasing working capital requirement originating from BPJS Health

deficit

Capacity available in existing hospitals to add additional beds Low supply of doctors in Indonesia, adding to it high barrier of entry for

foreign workforce in the healthcare industry

Large base of middle income class as target segment Population's increased search for healthcare services in neighbouring

countries that is in line with greater national wellbeing

Capture a massive portion of patient volume when there is a shift in trend to

private healthcare

Continued increase in patient volume from government's UHC initiative by

2019F

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

19

Demographics and globalisation

Globalisation could lead to a pick-up in medical tourism to neighbouring

countries (i.e. Singapore, Malaysia, or Thailand) which are perceived to offer

superior quality, in our view, but with premium pricing – a downside to local

hospital patient volumes. So far, we have not seen nor do we expect this trend to

materialise, at least not in the next 12 months, as the affluent population still

represents a minuscule 0.3% of the total population (as at 2018).

Development risks

Risks embedded in the development of each greenfield hospital are timing and

licensing. Our channel checks suggest that construction of one hospital in

Indonesia takes around 12-18 months. If a company faces a delay in

construction or fixed costs, including the initial hiring of employees, this could

significantly raise operating expense – with no income support, in our view. We

believe this execution risk could have a significant impact, given the company’s

expansion guidelines (four new hospitals each year) until 2020F. The company

has stated that land acquisition has been secured for all of its expansion sites.

FORECASTS AND FINANCIALS

Net profit CAGR of 35% in FY18-21F

We project HEAL’s revenue to grow at a CAGR of 16% in 2018-21F – with

2019F revenue up by 18% yoy (vs. 2018’s 14% yoy). The company targets to

open four new hospitals this year, which we think could bring 2019F operational

beds to c.3,800. As we expect the 2019F occupancy rate to improve to 68% (vs.

66% in 2018), patient volume could grow by 15% yoy (vs. 2018’s 18%), based

on our estimates.

We forecast average per patient revenue growth at 0%/-5% for

inpatient/outpatient in 2019F (vs. 2018’s -3%/-21%). The improvement in per

patient revenue is due to the stabilising UHC proportion at 65%/49% for

inpatient/outpatient, as well as some tax adjustments that are no longer

expected in 2019F, according to management. We note that HEAL faced a deep

correction in outpatient revenue in 4Q18. Its outpatient revenue declined by 33%

yoy as the company incurred some tax adjustments in the quarter. Excluding this

adjustment, outpatient revenue declined by 9% yoy (vs. 9M18’s 1%).

HEAL’s economies of scale should bring its cost of revenue down, at a projected

0.5% pt yoy rate in 2019F, resulting in a GPM improvement to 44.8% (+0.2% pt

yoy). 2019F opex as a percentage of revenue may rise by 0.2% pt yoy due to

the opening of new hospitals, but 2019F EBIT margin should remain stable at

11.7% (vs. 2018’s 11.4%), based on our estimates.

Our 2019F net profit forecast is 18% below the Bloomberg consensus estimates,

mostly due to our recognising 70% of attributable net profit to the parent list co.

Other major differences relative to consensus forecasts, are our expectations of

higher cost savings as a result of economies of scale leading to a 44.8% 2019F

GPM (vs. consensus’ 42.9%), and a 2019F tax rate of around 31%, similar to

2018’s (vs. consensus which appears to be projecting a tax rate of 51%, in our

view).

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

20

Figure 33: Our forecast assumptions

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

FY18 net profit exceeded consensus

HEAL’s 2018 net profit reached Rp124bn, up 28% yoy. The results were above

Bloomberg consensus estimates by 117%. Meanwhile, revenue of Rp3.1tr

(+14% yoy) was in line with consensus forecasts.

Total patient volume grew by 18% yoy in 2018, with inpatient at +28% yoy and

outpatient at +18%, yoy. Its revenue per patient still declined, however- inpatient

by -3% yoy and outpatient by -21% yoy. The deep decline in outpatient revenue

was a result of the tax adjustment for pharmaceutical sales, as mentioned

above.

In terms of profitability, 2018 GPM rose 0.7% pt yoy. However, operating

expenditure as a percentage of revenue, spiked by 3.3% pts yoy (due to the

opening of four new hospitals), resulting in 2018 EBIT margin dropping by 2.7%

pts yoy to 11.4%. All in, 2018 net margin still improved as the company’s tax rate

fell from 38% in 2017 to 31%.

Figure 34: HEAL's FY18 results

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

2019F 2020F 2021F

No. of new hospitals 4 4 -

Total no. of hospitals 36 40 40

Total operational bed 3,778 4,178 4,378

Occupany rate 68% 72% 76%

Avg length of inpatient stay (ALoS) 2.5 2.5 2.5

Patient volume

Inpatient admissions 375 439 486

Outpatient visits 6,095 6,705 7,375

Avg. revenue per patient (Rpm)

Inpatient 7.14 7.28 7.43

Outpatient 0.15 0.15 0.15

FYE Dec (Rp bn) 4Q18 4Q17 yoy % 3Q18 qoq % 4QFY18 4QFY17 yoy %

chg chg Cum Cum chg

Revenue 770 714 7.7% 770.91 -0.1% 3,058 2,678 14.2%

COGS (409) (393) (441.49) (1,704) (1,509)

Gross profit 361 321 12.3% 329 9.6% 1,354 1,169 15.8%

Gross margin (%) 46.9% 45.0% 42.7% 44.3% 43.6%

Operating expenses (300) (222) (232.37) (1,004) (791)

EBITDA 122 150 -18.5% 147 -16.5% 553 542 2.1%

EBITDA margin (%) 15.9% 21.0% 19.0% 18.1% 20.2%

Depr & amort. 61 51 49.45 203 164

EBIT 61 99 -38.0% 97 -36.7% 350 378 -7.3%

EBIT margin (%) 8.0% 13.9% 12.6% 11.4% 14.1%

Interest expense (23) (40) (19.82) (131) (115)

Interest income 4 1 6.14 20 9

Others 20 (3) (1.87) 36 8

Pretax profit 62 57 9.8% 81.52 -23.5% 276 279 -1.2%

Tax (33) (31) (17.91) (85) (105)

Tax rate (%) -53.4% -54.3% -22.0% (0) (0)

Minority interests 15 39 22.47 67 101

Net profit 14 12 18.7% 41 -65.6% 124 98 27.5%

Core net profit 14 12 18.7% 41 -65.6% 124 98 27.5%

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

21

Impact of BPJS deficit

Under UHC, potential patients utilising the facility are either charged a small

amount (new regulations in 2019F) or are free of charge. The remaining cost of

services incurred by patients is regarded by the hospital as trade receivables

from BPJS Health. Hence, the BPJS deficit – and consequently, late payments –

has almost an immediate impact on the hospital’s working capital. This is a

common issue among healthcare industry players, which has led to a rise in the

acquisition of small-scale hospitals by major players.

We expect HEAL’s receivable days to improve from 2019F, on the back of

changes in BPJS Health regulations, as well as expectations of a recovery in

private healthcare services, translating to an increase in contribution from out-of-

pocket expenses and private insurance companies (with a stricter payment

scheme). We expect its receivables to stay at 84 days in 2019F from an

increasing trend of 43/60/84 days in 2016/17/18.

Figure 35: HEAL's payables, receivables, and inventory days

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

Efficiency drive

Historically, trade payable days (Figure 35) have shown a prolonged time for the

company to pay off its liabilities from an average of 115 days to 144 days in

2016-17. BPJS Health’s deficit has also contributed to a historical increase in

trade payable days, with hospitals often being forced to delay payments to

pharmaceutical companies due to the late payments received from BPJS Health.

However, we expect HEAL’s payable days to decrease in 2019F as

pharmaceutical companies are drawing attention to the necessity for the

government to control reimbursements to pharma and avoid cashflow problems

for pharmaceutical companies, especially taking into account payment

extensions from pharma suppliers overseas whereby Indonesia just represents a

mere 1% of their distribution.

Funding risk

Management guides for an optimal level of net debt-to-EBITDA ratio of 1-1.3x in

FY19F, taking into account the required funding for its expansion. In 2017, the

ratio exceeded its optimal level at 2x, but 2018 was back to 0.9x. We expect its

net debt-to-EBITDA to reach 0.9x in 2019F and 1x in 2020F – within its optimal

level.

Title:

Source:

Please fill in the values above to have them entered in your report

0

20

40

60

80

100

120

140

160

2016 2017 2018 2019F 2020F

Inventory days Receivable days Payables days

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

22

Figure 36: HEAL’s net debt-to-EBITDA ratio

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

Free cash flow to turn positive by 2019F

HEAL’s free cash flow (FCF) has historically been negative; it reached -Rp654bn

in 2018 and -Rp212bn in 2017. However, we expect FCF to turn positive in

2019F at Rp9bn.

Its 2020F FCF may return to negative territory, but should recover in 2021F as

we expect to see lower capex (the company guides for brownfield expansion

starting in 2021F).

Figure 37: HEAL's FCF vs. capex % to revenue

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

VALUATION AND RECOMMENDATION

Sector has de-rated by 44% since UHC implementation

Despite contributing to society’s welfare (improving national health status), the

introduction of the UHC programme has deteriorated the healthcare industry’s

valuation, in our view. The sector traded at 22x forward EV/EBITDA in Jan 2014

but now trades at 12.3x forward EV/EBITDA (at -2 s.d. below its historical 5-year

mean of 26x). We believe the de-rating was mainly driven by investor’s concerns

over the impact of the BPJS deficit on working capital insufficiency (liquidity) and

lower profitability resulting from changes in the patient mix.

Title:

Source:

Please fill in the values above to have them entered in your report

0.9x

1.8x

1.0x 1.0x 1.0x

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2016 2017 2018 2019F 2020F

Title:

Source:

Please fill in the values above to have them entered in your report

(74)

(212)

(654)

9

(41)21%

26%

23%19%

17%

0%

5%

10%

15%

20%

25%

30%

(700)

(600)

(500)

(400)

(300)

(200)

(100)

-

100

2016 2017 2018 2019F 2020F

FCFF (Rp bn) Capex % to revenue (RHS)

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

23

Figure 38: Healthcare sector forward EV/EBITDA de-rated as

BPJS Health deficit ballooned

Figure 39: …as did the sector’s forward P/E valuation

SOURCES: CGS-CIMB RESEARCH, BLOOMBERG SOURCES: CGS-CIMB RESEARCH, BLOOMBERG

Figure 40: MIKA’s forward EV/EBITDA Figure 41: MIKA’s forward P/E

SOURCES: CGS-CIMB RESEARCH, BLOOMBERG SOURCES: CGS-CIMB RESEARCH, BLOOMBERG

Figure 42: SILO’s forward EV/EBITDA Figure 43: SILO's forward P/E

SOURCES: CGS-CIMB RESEARCH, BLOOMBERG SOURCES: CGS-CIMB RESEARCH, BLOOMBERG

Title:

Source:

Please fill in the values above to have them entered in your report

-

5

10

15

20

25

30

35

40

45

Healthcare - rolling fwd EV/EBITDA 5-year mean

+1 s.d. +2 s.d.

-1 s.d. -2 s.d.

x

15x

12x

19x

26x

34x

41x

22x

Title:

Source:

Please fill in the values above to have them entered in your report

(100)

(50)

-

50

100

150

200

250

300

Healthcare - rolling fwd P/E 5-year mean

+1 s.d. +2 s.d.

-1 s.d. -2 s.d.

x

51x

-40x

26x

156x

221x

173x

Title:

Source:

Please fill in the values above to have them entered in your report

10

15

20

25

30

35

40

45

50

55

Mar-

15

May-

15

Jul-15

Sep-1

5

Nov-

15

Jan-1

6

Mar-

16

May-

16

Jul-16

Sep-1

6

Nov-

16

Jan-1

7

Mar-

17

May-

17

Jul-17

Sep-1

7

Nov-

17

Jan-1

8

Mar-

18

May-

18

Jul-18

Sep-1

8

Nov-

18

Jan-1

9

Mar-

19

Rolling EV/EBITDA 5-year mean +1 s.d.

+2 s.d. -1 s.d. -2 s.d.

x

25x

17x

25x

34x

42x

51x

40x

Title:

Source:

Please fill in the values above to have them entered in your report

-

10

20

30

40

50

60

70

Mar-

15

May-

15

Jul-15

Sep-1

5

Nov-

15

Jan-1

6

Mar-

16

May-

16

Jul-16

Sep-1

6

Nov-

16

Jan-1

7

Mar-

17

May-

17

Jul-17

Sep-1

7

Nov-

17

Jan-1

8

Mar-

18

May-

18

Jul-18

Sep-1

8

Nov-

18

Jan-1

9

Mar-

19

Rolling P/E 5-year mean +1 s.d.

+2 s.d. -1 s.d. -2 s.d.

x

41x

33x

41x

57x

65x

49x

Title:

Source:

Please fill in the values above to have them entered in your report

-

5

10

15

20

25

30

35

40

Rolling EV/EBITDA 5-year mean +1 s.d.

+2 s.d. -1 s.d. -2 s.d.

x

5x

2x

10x

19x

27x

36x

24x

Title:

Source:

Please fill in the values above to have them entered in your report

(100)

-

100

200

300

400

500

600

700

800

Rolling P/E 5-year mean +1 s.d.

+2 s.d. -1 s.d. -2 s.d.

x

76x

-24x

90x

204x

318x

432x

168x

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

24

After the general elections in Apr 2019, if the incumbent wins, we believe the

healthcare sector could gain some traction given that Mr. Jokowi is likely to

focus on the industry, in our view. This could lead to an increase in premium

membership fees and fee adjustments to INA-CBG reimbursement program,

which may help to improve hospital profitability. The new regulations on cost

sharing should help to improve hospital receivables as well – though the impact

could be minimal, in our view. As a result, we expect the sector to re-rate by

2019F.

Initiate coverage with an Add rating

We initiate coverage on HEAL with an Add rating and target price of Rp4,000

based on DCF valuation (WACC 10%, LTG 6%), implying 19x FY19F

EV/EBITDA (given 70% ownership) or 27x FY19F EV/EBITDA given 100%

ownership). The stock currently trades at 23x FY19F EV/EBITDA (assuming

70% ownership) or 16x FY19 EV/EBITDA (based on consolidated 100%

ownership), at a 23% discount to MIKA’s 30x FY19F EV/EBITDA but at a 188%

premium over SILO’s 8x FY19F EV/EBITDA. Nevertheless, HEAL offers a net

profit CAGR of 35% in 2018-21F (vs. MIKA’s 13%) – much more attractive

compared to peers.

We view HEAL as a good proxy for Indonesia’s healthcare industry as it is the

second-largest hospital group in terms of number of hospitals and operational

beds. It is also a good proxy for the UHC programme. As a first-mover, we

believe its revenue per patient has limited downside risk, unlike peers whose

revenue per patient may still decline, underpinned by rising contribution from

UHC patients. Its four new hospitals p.a. should support earnings growth without

much erosion on overall profitability, in our view.

Figure 44: Our DCF assumptions

SOURCES: CGS-CIMB RESEARCH ESTIMATES, COMPANY REPORTS

Risk free rate 8%

Market risk premium 7%

Equity beta 0.32

Cost of equity 10%

Cost of debt 13%

Cost of debt (1-T) 9%

Target debt 33%

Target equity 67%

Tax rate 31%

WACC 10%

LTG 6.0%

Assumptions

Hospitals │ Indonesia

Medikaloka Hermina │ April 15, 2019

25

Figure 45: DCF-based target price

SOURCES: CGS-CIMB RESEARCH ESTIMATES

DCF sensitivity to long-term growth rate (LTG)

We assume a 6% LTG, which we believe is reasonably conservative compared

to Indonesia’s nominal GDP growth of c.9.5% in FY18E and Bloomberg

consensus estimates of Indonesia’s GDP growth in FY20-21F of 8-9% (real

growth of 5-5.5% and inflation at 3-3.5%). Given the country’s relatively low

healthcare expenditure to GDP at c.3.4% in 2015 (vs. world average of 9.9%,

according to WHO), the 10 years’ FY10-20F projected CAGR is at 5.4%. The

challenge in Indonesia is hospital and doctor scarcity. While the higher tendency

to use generic drugs may have resulted in a relatively lower growth in

pharmaceutical spending (use of cheaper generic versions vs. patented drugs),

the last 5 years has nevertheless seen tremendous growth in pharmaceutical

spending.

Figure 46: Target price sensitivity to LTG

SOURCES: CGS-CIMB RESEARCH

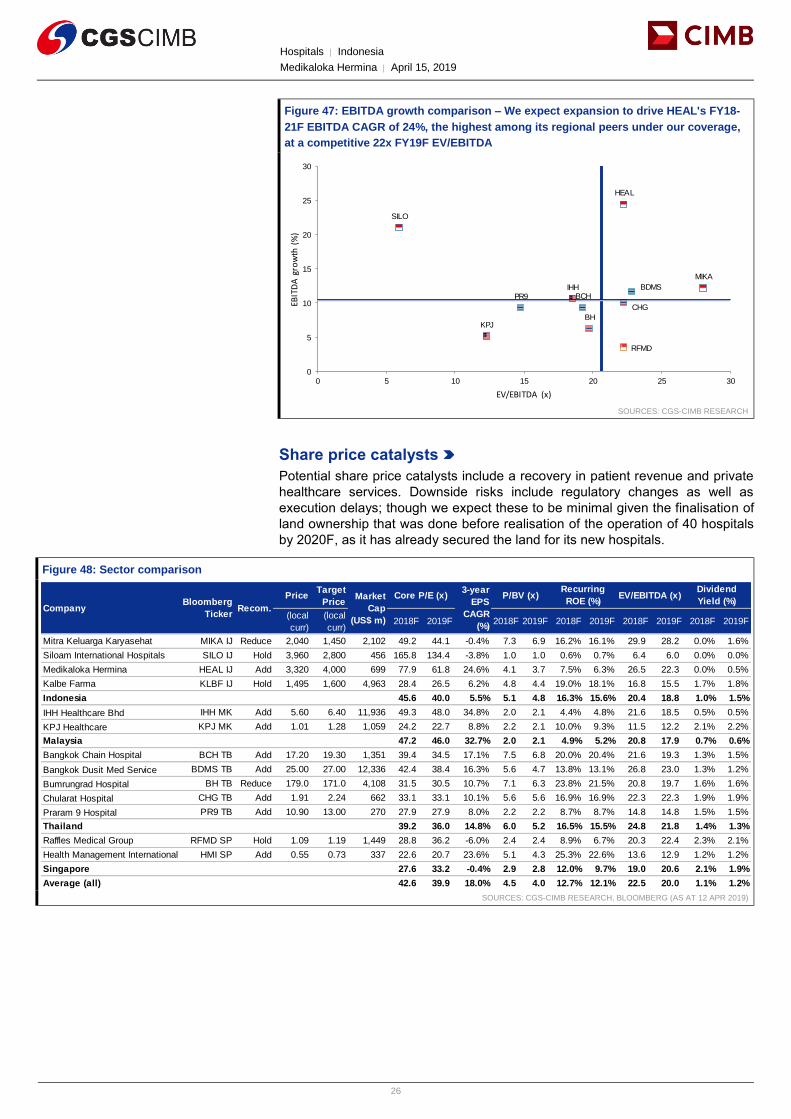

EV/EBITDA comparison with regional peers

In general, Indonesian hospitals’ EBITDA CAGRs in FY15-18 are higher than

those of their regional peers. The UHC factor aside, we believe the improvement

in purchasing factor is also a driver. We expect HEAL’s EBITDA to grow at 24%

CAGR in FY18-21F, backed by stable hospital expansion until 2020F (our

forecast period). The other growth driver is the addition of more operational

beds. In comparison, the simple average of peers’ EBITDA growth is at a CAGR