maximizing the hts opportunity: leveraging new satellite .../media/files/insights/apscc maximizing...

TRANSCRIPT

Attribution: Asia Pacific Satellite communications council (APSCC), APSCC 2013 Q3 newsletter, ISSN 1226-8844; URL: http://www.apscc.or.kr/upload/pdf/Q3%202013.pdf

Maximizing the HTS Opportunity: Leveraging New Satellite Architectures and Business Models to Grow Dave Bettinger, Chief Technology Officer and Senior Vice President of Engineering, iDirect

High Throughput Satellite (HTS) technology is a game-changing innovation from the space segment industry that, unlike any technology we’ve seen to date, will vault satellite communications into the mainstream. HTS can significant improve capacity economics. And this means greater opportunity for the satellite industry.

Along with opportunity, however, HTS brings new technical complexity. Most significantly, the industry must adapt to new satellite architectures. HTS satellites encompass a wide range of different bands, beam sizes and earth orbits – each with its distinct strengths and unique physics.

One example is Ka-band spot beams satellite. To gain throughput improvements, these spot beams continuously re-cycle frequency on the remote side, while connecting through a feeder link to a hub infrastructure. Other architectures have emerged that combine spot/wide beam Ku-band satellite and operate over MEO fleets.

New go-to-market business models

���HTS satellite architectures will impact the value chain – namely, who owns and manages infrastructure and who owns and manages customer relationships. That means diverse business models will emerge for bringing HTS capacity to market – from managed services developed by satellite operators and delivered through service providers to new levels of infrastructure sharing and collaboration. And these will co-exist with traditional business models. Success will require flexibility to adapt to any business model present or future.

There are four key models that are likely to define how HTS service is delivered in the marketplace.

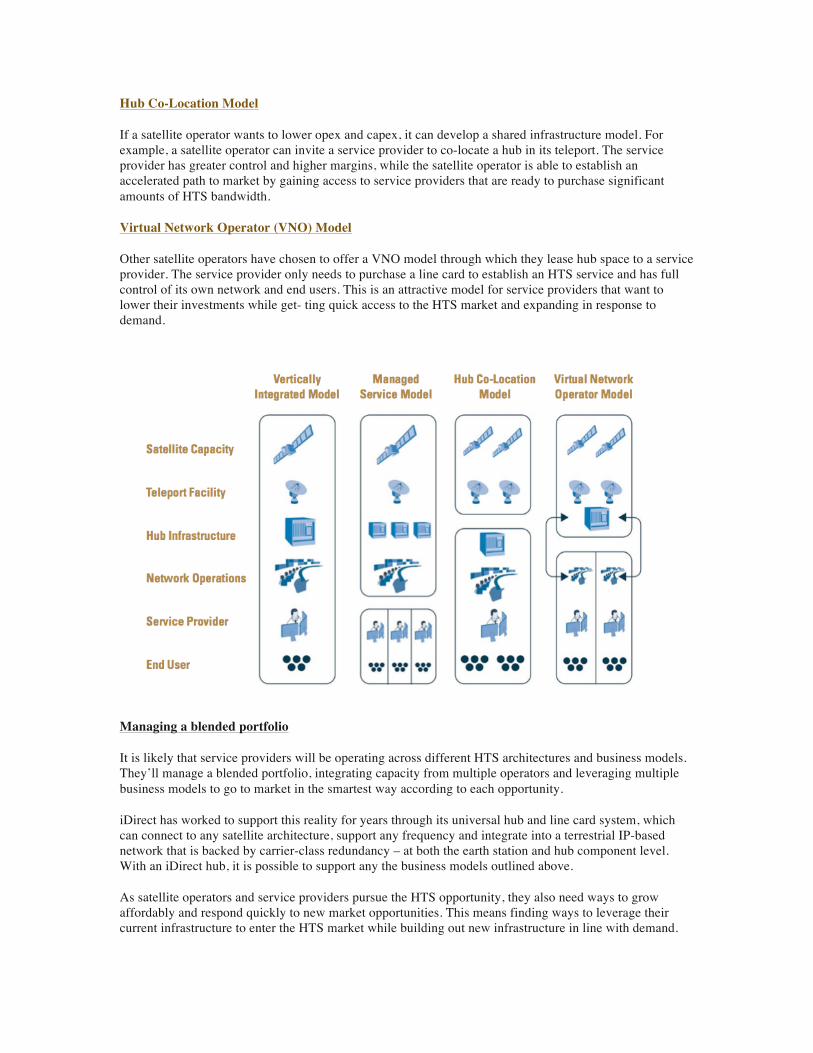

Vertically Integrated Model

The dominant way operators are delivering HTS capacity to the consumer market is through a vertically integrated service model.

In this model, a satellite operator owns and operates the entire value chain: the satellite, teleport, hub infrastructure, network operations, service provision and customer relationships. In the enterprise market, this model can make sense for highly targeted geographies or vertical industry offerings.

Managed Service Model

Another key HTS business model that has emerged is designed for a managed service. This is a spot-beam model where the ground segment infrastructure must be centrally located within the feeder link. The satellite operator owns and operates all infrastructure and network operations, relying on distributors to re-sell its service and manage customer relationships.

In this model, a satellite operator assumes responsibility for infrastructure and network management. Service providers have a narrower operations focus, but also a smaller capital outlay. And they gain speed to market – as they can immediately secure and market HTS capacity.

Hub Co-Location Model

If a satellite operator wants to lower opex and capex, it can develop a shared infrastructure model. For example, a satellite operator can invite a service provider to co-locate a hub in its teleport. The service provider has greater control and higher margins, while the satellite operator is able to establish an accelerated path to market by gaining access to service providers that are ready to purchase significant amounts of HTS bandwidth.

Virtual Network Operator (VNO) Model

Other satellite operators have chosen to offer a VNO model through which they lease hub space to a service provider. The service provider only needs to purchase a line card to establish an HTS service and has full control of its own network and end users. This is an attractive model for service providers that want to lower their investments while get- ting quick access to the HTS market and expanding in response to demand.

Managing a blended portfolio ���

It is likely that service providers will be operating across different HTS architectures and business models. They’ll manage a blended portfolio, integrating capacity from multiple operators and leveraging multiple business models to go to market in the smartest way according to each opportunity.

iDirect has worked to support this reality for years through its universal hub and line card system, which can connect to any satellite architecture, support any frequency and integrate into a terrestrial IP-based network that is backed by carrier-class redundancy – at both the earth station and hub component level. With an iDirect hub, it is possible to support any the business models outlined above.

As satellite operators and service providers pursue the HTS opportunity, they also need ways to grow affordably and respond quickly to new market opportunities. This means finding ways to leverage their current infrastructure to enter the HTS market while building out new infrastructure in line with demand.

Another key aspect of the iDirect hub is that it is a hub chassis designed to be populated with net- work line cards in a pay-as-you-grow manner. With iDirect’s hub and line card system, satellite opera- tors and service providers can leverage their existing infrastructure to launch and scale HTS networks.

To see how the iDirect platform can operate over diverse satellite architectures and support multiple business models, let’s examine what a typical growth plan might look like for a service provider expanding in the HTS era.

Imagine the service provider has a hub in Africa, and it’s supporting Ku- and C-band capacity. A new Ku-band high performance satellite becomes available, which uses a spot beam overlay to expand coverage. To tap into this capacity, the service provider can simply add new line cards – ones that have been engineered for high throughput bandwidth – to its existing hub infrastructure. It can then continue to add line cards and hubs as demand increases.

Imagine now that the service provider wants to add capacity in the Middle East through a Ka-band High Throughput Satellite. This satellite has a common feeder link that is only accessible from the satellite operator’s teleport. To launch a network, a service provider can co-locate a hub within a satellite operator’s teleport – and then add line cards to light up spot beams.

If the option exists, a service provider can distribute a managed service from a satellite operator – avoiding capital costs altogether, simplifying operations, and entering new markets faster. Another option is the VNO model, in which a service provider simple buys a line card and leases hub space from a satellite operator.

Other key considerations for HTS

���As satellite operators and service providers develop HTS expansion plans, it’s critical that they choose a universal IP hub that can support all frequencies and all satellite architectures, and their hub infra- structure can easily and affordably scale with demand. There are three other considerations that are worth mentioning here.

For satellite to become a more widely adopted technology, it must deliver carrier-class service reliability. This means higher levels of availability and bandwidth efficiency. It also means ensuring hub diversity to overcome rain fade and hub redundancy in the event of network failure.

Operators and service providers need to provide end users with easy to use and deploy terminals that are

targeted to their unique requirements and that are increasingly faster, more compact and afford- able.

Another key requirement for the HTS era is a single network management system (NMS) that makes large-scale deployments manageable. This includes tools that automate NOC operations, optimize network performance and provide extensive network monitoring and analysis. The NMS must be sync with billing and provisioning systems and extend core functionality and customized features to end users, who increasingly want to monitor and control key aspects of their networks.

A future of collaboration and innovation ���The next generation of satellite communications will introduce landmark changes that build on a decade of innovation and overcome longstanding cost and availability challenges that have limited market expansion. Satellite communications will become easier and more cost-effective to manage, positioning satellite as the logical answer to a much wider variety of users and applications, delivering the kind of constant connectivity that the world has been demanding for years.

To succeed in the future, satellite operators and service providers must choose the right mix of HTS business models and be able to integrate them with their existing non-HTS networks. They must become more market-driven to meet increasing end user demands. And they need an easy way to scale and manage their operations with greater flexibility in how they go to market to capture the most opportunity while minimizing risk and investment costs.

As demand for satellite communications accelerates in the HTS era, iDirect will continue to lead the way in developing high-performance, easy-to-use, and cost-effective ground infrastructure technology that pushes the entire satellite industry forward and achieves our vision of advancing a connected world.

Dave Bettinger is iDirect’s chief technology officer and senior vice president of engineering. Bettinger is responsible for the oversight of all technology decisions within iDirect and serves to drive strategic direction for product development, technology alliances, along with mergers and acquisitions. Bettinger currently services on the board of directors for the Global VSAT Forum and is an active member of the Telecommunications Industry Association, IEEE and IPv6 Forum. Bettinger is a graduate of Virginia Tech with a Masters of Science degree in Electrical Engineering and has been awarded six patents in the area of satellite communications.