maximizing efficiencies and process improvement in accounts payable scott shannon, senior vice...

TRANSCRIPT

Maximizing Efficiencies and Process Improvement in Accounts Payable

Scott Shannon, Senior Vice President

U.S. Bank – Global Treasury Management

Greg Hamilton, Vice President

J.P. Morgan – Public Sector Commercial Electronic Payments

2

Agenda■Landscape of Commercial Payments

■Why Checks remain popular for business

■Check Fraud

■ Why Single-Use Accounts

■ How Single-Use Accounts Work

■Organization and Supplier Benefits

■Distinctive Capabilities of Single-Use Accounts

■Support, Service and Supplier Enablement

3

Landscape of Commercial Payments

Source: Aberdeen Group, September 2009, Visa Middle Market Study 2007, RPMG 2007

Checks remain the principal form of payment. Small and medium-size transactions dominate payment activity.

Transactions by Payment Type

64% 76%

29% 13%

6%4%3% 6%

Checks

Card

ACH

Wire

Transactions Below $2,500

Transactions Between$2,500 - $10,000

76% of CFOs cite “lower invoice processing costs” as top AP goal

However, paper checks:

Can cost $1 to $5 per transaction

Offer little float, minimal controls, no visibility

Make fraud and misuse harder to detect

Do not earn rebates

4

Why do Checks Remain Popular for Business?

© 2010 PayStream Advisors, Inc. • www.paystreamadvisors.com

5

Why do Checks Remain Popular for Business?

Patty Murphy, the Tacoma Group

“Companies want to collect payments at the speed of light, but would prefer to disburse funds by Pony Express.”

6

Why do Checks Remain Popular for Business?

Transportation Invoice Processing and Payment – Benchmark Report 2010, American Shipper

“Payment is a group exercise …Group exercises require standards. This is clearly lacking in the transportation industry.”

7

Why do Checks Remain Popular for Business?

Transportation Invoice Processing and Payment – Benchmark Report 2010, American Shipper

“Many invoices are disputed … (and) end up in the hands of people making phone calls, sending e-mails, and eventually mailing checks. A cycle that started in an electronic environment has derailed into a manual exercise.”

8

Why do Checks Remain Popular for Business?

The state of B2B Payments, Mastercard Advisors, July 2008

“…change is not pursued because there is a fear of losing valuable eProcurement data, especially line item detail. These perceptions enable less efficient processes such as paper check payments to remain in place.”

9

Why do Checks Remain Popular for Business? Inertia (banks and customers) Data security standards Float Accounting software flexibility Existing lockbox infrastructure Fear factor Reconciliation processes built around pre-existing

payment methods Cultural and regional factors However…

10

Organizations with Attempted Payment FraudAll organizations

Percent of organizations subject to attempted payment fraud

Source: 2011 AFP Payments Fraud and Control Survey

From 2009 to 2010, 29% of organizations experienced

an increase in payment fraud

2004 2005 2006 2007 2008 2009

55%

68%72% 71% 71% 73%

2010

71%

11

Organizations with Attempted Payment FraudBy payment type

Source: 2011 AFP Payments Fraud and Control SurveySource: 2011 AFP Payments Fraud and Control Survey

0 20 40 60 80 100

Wire transfer

ACH credits

Corporate/commercialpurchasing cards

Consumercredit/debit cards

ACH dedits

Checks

2010

12

Why So Much Check Fraud? Low risk

FBI receives too many reports of criminal activity related to check fraud, kiting and counterfeit checks to follow-up on most cases.

Low barriers to entry Readily available scanners, printers and

software Relatively easy access to the banking system

Access to account information Online auctions, classified ads and dating

services Mail theft Phishing

13

Why So Much Check Fraud?

The nature of checks

Paper-based

Clearing process is slow

Government regulated

Card-based payments havesome advantages

Real time authorizations

More technology can be built into the card

Industry regulated

14

Who is liable for check fraud losses?

Customer Standard “Ordinary Care” for a business means

observance of reasonable commercial standards prevailing in the area of the business by similar businesses.

Exercise care in hiring and supervision. Examine bank statements within a

reasonable time to detect fraud. Evaluate and acquire appropriate fraud

prevention products. Notify the bank immediately when fraud

is suspected. Consult legal counsel.

Bank Standard “Ordinary Care” for a bank requires

following reasonable commercial standards observed by other banks in their region.

Exercise ordinary care to prevent losses from counterfeit and forged items.

Act in good faith in accordance with reasonable commercial standards of fair dealing.

Act in good faith, and follow procedures similar to those of comparable banks, they may not be found negligent for failure to detect fraud.

Uniform Commercial Code

15

What Banks are Doing To Combat Fraud Installing and improving systems to detect

fraudulent checks during high speed check processing:

Utilize sophisticated fraud detection software to identify potential fraudulent activity at the account level

Not a replacement/substitute for Positive Pay services

Offering a variety of fraud mitigating services tailored to the needs of business to meet their disbursement needs

Requiring customers to take action if fraud occurs Positive Pay, open a new account and

close the compromised account, indemnity agreement

16

What Municipalities Can Do

Establish tight controls over the storage and distribution of check stock; keep in locked quarters, seal empty boxes, maintain an inventory list and conduct audits

Keep mechanical signature plates in secure areas separate from check stock

Use consistent check stock throughout the account

17

What Municipalities Can Do

Use check stock that contains multiple security features It’s the best way to prevent Payee alterations, thwart

check fraud at retail store locations Criminals would rather attack an account that’s easy

to penetrate than one with a lot of roadblocks You can and should “advertise” your security features

right on your check, including the use of Positive Pay

18

What Municipalities Can Do

Bolster your internal controls : Ensure separation of duties - check

writers should not reconcile the accounts

Delegate separate individuals for invoicing and collecting and posting funds to Accounts Receivable

Establish and document policies for all accounting functions

Update and review procedures with your employees

Conduct periodic reviews of procedures

19

What Municipalities Can Do

Reconcile your accounts in a timely manner Notify the bank immediately if

fraud is suspected. A bank’s Terms and Conditions often give a specific time limit of 15 or 30 days

Use online information reporting prior to arrival of statement

Check background references whenhiring decisions are made

Use appropriate bank solutions Add Payee Verification to your

Positive Pay service Consider electronic alternatives…

20

Factors Driving Electronic Payment Processes

Source: Federal Reserve and NACHA research

Given the tangible benefits electronic payments deliver over paper-based checks, it is not surprising that adoption of electronic payments has significantly increased over the past five years, while check usage has declined.

Benefits

Cost reduction

Decreased paper consumption

Compression of procure-to-pay cycle

Ability to capture rebates and early payment discounts

Improved visibility

Reduction in fraud

21

Top Factors Driving Focus On Electronic Payments

Reduce Procure-to-Pay Transaction Costs

Maximize Rebates & Incentives

Improve Employee Convenience

Reduce Procure-to-Pay Cycle Time

Improve Employee Productivity

A majority of clients cite the move to electronic payments as an essential step in reducing procure-to-pay costs.

Source: PayStream Advisors, “Electronic Payments: Streamline P2P, Reduce Costs” Q2 2010

22

The Payables Continuum

23

What are Single-Use Accounts?An electronic, credit card-based payment solution, Single-Use Accounts act like checks but offer controls similar to ACH, as well as the following benefits:

Check-like controls with commercial card advantages

A unique, 16-digit virtual account number for each payment

Payment-specific authorization

Only active for a defined time period (e.g., 5 or 50 days)

Credit limit equals the exact payment amount – to the penny

Only authorized for specific merchant category codes

Reduced fraud and employee misuse

Automated matching of merchant transactions to G/L

Accepted by suppliers at POS

24

Why Single-Use Accounts?

Examples•Business Retail•Office Supplies

Examples•Lodging•MRO•Office Equipment•Professional Services

Single-Use Accounts are increasingly replacing checks because they can improve efficiencies, increase working capital and deliver rebate revenue.

Rebate earning solutions

Automation benefits

Check/Wire/ACH

Commercial Cards

Single Use Accounts

25

How Do Single-Use Accounts Work?

VISA OR MASTERCARD

YOUR ERP SYSTEM

SUPPLIER

5. Reconciliation, billing and payment

1. Payment file

2. Supplier notification

4. Transaction data

3. Supplier payment

Single-Use Accounts streamline payments, resulting in reduced costs and new revenue opportunities

26

Direct Integration Into Your AP Systems

Single-Use Accounts leverage existing business processes & systems

■Fully electronic so you can eliminate manual payment processing

■Seamlessly integrates with your existing AP or ERP systems (iDoc, PeopleSoft, XML, CSV and others)

■Follows existing business processes and rules so only approved invoices are paid

■Unlimited electronic remittance details via e-mail or portal

■Card data masking for secure e-mail transmission

■Automated supplier communications and reminders

■Batch file process is as simple as ACH

27

Benefits to the Organization and the Supplier

■ Greater control: ability to set credit limit and validity period, reduces the chance of fraud

■ Processing saves: automation replaces costly manual process

■ Improved reporting and reconciliation: spend data to support vendor negotiations; simpler/faster reconciliation

■ New revenue streams: increased rebates; extended float

■Faster payment: improves Days Sales Outstanding

■Unlimited Electronic remittance data via secure e-mail or portal

■Process Efficiency and Cost Savings: no check handling; no A/R collections

■Reduced risk of supplier/employee fraud

Organization Benefits Supplier Benefits

28

Distinctive Capabilities of Single-Use Accounts

Rebates

Check-Like Controls

Savings Through Automation

Supplier Services

29

Check-Like Controls

Single-Use Accounts offer the highest level of security

Granular authorization controls act like checks but work like cards

One-to-one relationship of account numbers to payments

The account credit limit equals the exact payment amount – to the penny

Each account is only active for a defined time period (i.e. 5 or 50 days)

The account only authorizes for specific merchant category codes

No cards are distributed to employees (AP controlled)

30

Savings Through Automation

Improve Supplier Payment Processing

■Suppliers get paid sooner, improving their days receivables outstanding (DRO)

■Provides suppliers with electronic remittance data

■Streamlines supplier process (no checks to handle/deposit)

■Reduces administrative costs: no check processing costs, courier fees and A/R collections

■Reduced risk of supplier/employee fraud

Automate Buyer Reconciliation

■Automatically matches each supplier transaction to purchase detail (e.g., order, invoice, receipt)

■Simple process to handle payment exceptions

■Regularly scheduled reconciliation file loads directly into your AP system

■Minimizes time spent on supplier reconciliation issues

■Virtually eliminates employee and merchant misuse

Reconciliation data ties directly to your AP system; suppliers get paid faster and reduce administrative costs

31

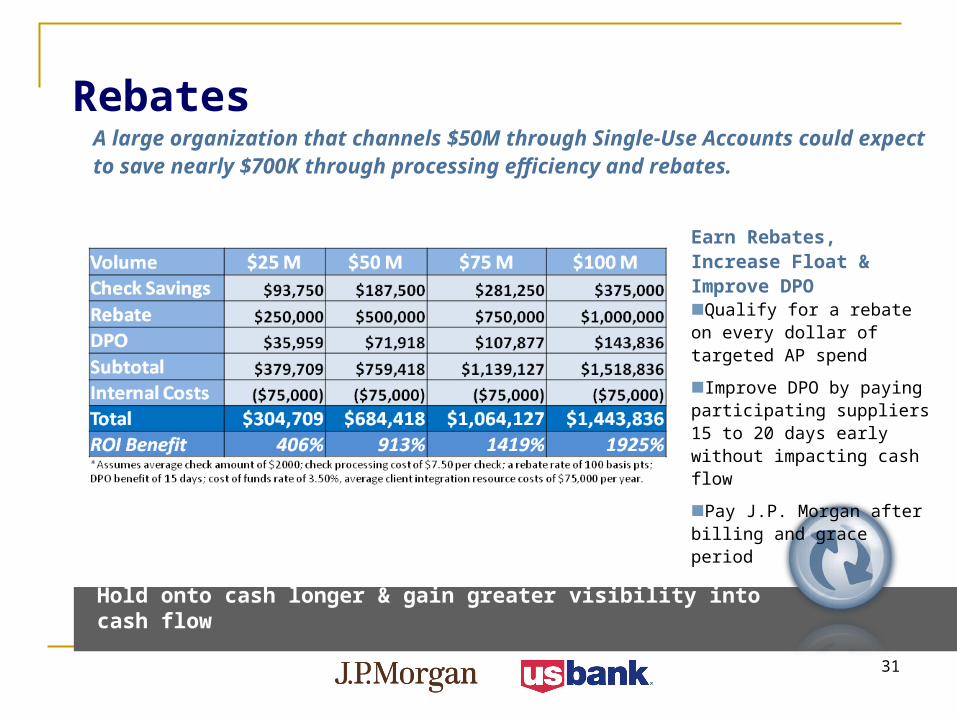

Hold onto cash longer & gain greater visibility into cash flow

RebatesA large organization that channels $50M through Single-Use Accounts could expect to save nearly $700K through processing efficiency and rebates.

Earn Rebates, Increase Float & Improve DPO■Qualify for a rebate on every dollar of targeted AP spend

■Improve DPO by paying participating suppliers 15 to 20 days early without impacting cash flow

■Pay J.P. Morgan after billing and grace period

32

Supplier Campaign Methodology

Supplier Services Program Manager•Recommend Best Practice Payment Policy•Supplier Analysis & Segmentation•Campaign Strategy•Develop Communications•Progress tracking•Customer Training

Client Campaign Lead•Implement Best Practice Payment Policy•Approve Campaign & Collateral•Coordinate Internal Comm. & Training•Coordinate Supplier Issues with Internal Stakeholders

Large/Strategic Suppliers (High $/Low #)

Relationship Manager

Small Suppliers (Low $/Large #)

Mail, Fax, E-Mail, Automated Calling

Midsize Suppliers

(Mid $/Mid #)

E-Mail, Fax, Mail, Calling

Non Accepting/ Fee Issue Suppliers

Merchant Services

33

Industry Practices

Best Practices: Your Role in Supplier Enablement Success

“ ”Single-Use Accounts scales to our business model, delivers real cost savings over checks and has helped us qualify for additional rebates.

Issuer Best PracticesProvide a dedicated Supplier Enrollment Project ManagerDevelop supplier segmentation and campaign recommendations Use all forms of supplier outreachProvide Relationship Managers for large suppliersLeverage Merchant Support for non-card-accepting suppliers

Client Best PracticesPromote card as a primary form of paymentPay participants more quicklyAllocate AP and Procurement resources

Ad

op

tio

n R

ate

34

Why Single-Use Accounts Make Sense

Offer all the benefits of normalCommercial Card Solutions

Combine flexibility of Commercial Card with the security of ACH

Deliver cost savings, control, revenue enhancement and process efficiencies

Supported by dedicated implementation team and ongoing customer service

Let us help you automate the rich “middle ground” of payments… and reap the benefits

35

How Single-Use Accounts Differ from Other Methods

FeatureSingle-Use Accounts

Checks ACH Payment Cards

Electronic payment process

Rebate potential

Improved DSO

Electronic remittance

Specified payment date range

Specified payment amount (e.g., to the penny)

Electronic reconciliation

Ability to stop payment

Ongoing per-payment fees

Single-Use Accounts combine the best of card, ACH, and check and is a powerful addition to your payables process to fill the gaps when other payments fall short

36

Implementing Single-Use Accounts

Review SolutionImplement(30-90 days*)

Service & Support

■Identify project resources

■Review Technical Requirements CSV-formatted Payment File

Master Vendor List

File Signed / Encrypted (PGP)

SFTP transport

■Conduct Technical Q & A

■Determine readiness

■Develop interface file(s) Payment Instruction File

Master Vendor List, Load via Import File or Manual Entry

■Integration & User Testing

■Launch Solution

■Ramp-to-Value

■Program Coordinator Team Day-to-day servicing and

maintenance

Program Administrator’s main point of contact

■Technical Support

* Implementation time may vary depending on customer readiness and ability to support system to system integration.

Dedicated implementation specialists guide and support the implementation process

37

Thank You!