math104– chapter 8 math of finance 8.1: introduction percents – write 30% as a decimal – what...

TRANSCRIPT

MATH104– Chapter 8Math of Finance8.1: Introduction

• Percents– Write 30% as a decimal– What is the definition of percent

Percents, decimals, fractionsPercent Decimal Fraction7%

3.5%

2 ¼ %

3/5

.8

½ %

2

Applications• For a $60,000 house, find a 20% down payment

----------------------• On a $40,000 salary, calculate a 8% raise

• Calculate your final pay after the 8% raise

Salary…

• If you received a 2% salary increase, and now make $32,640, what was your previous salary?

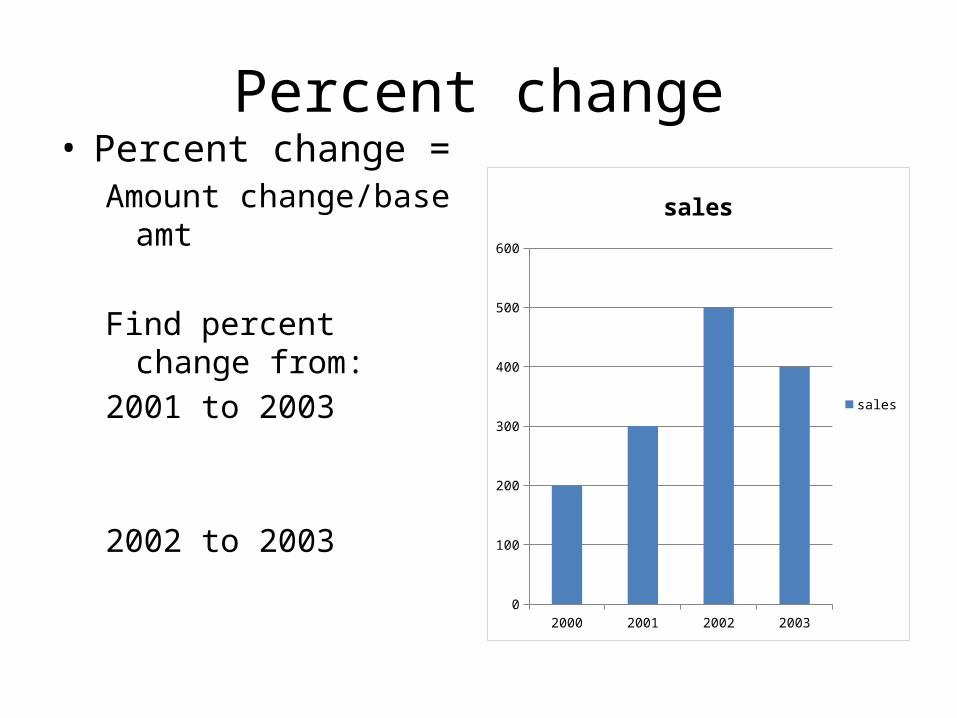

Percent change• Percent change =

Amount change/base amt

Find percent change from:2001 to 2003

2002 to 2003

2000 2001 2002 20030

100

200

300

400

500

600

sales

sales

Stock ex

If the stock market went down 50% today, what percent increase would you need tomorrow to return to the previous level?

• Percent change from Jan 1 to Jan 2

• From Jan 2 to Jan 3 1-Jan 2-Jan 3-Jan

0

2000

4000

6000

8000

10000

12000

14000

Dow Jones

Sales Tax

• On a $8000 car, calculate a 6% sales tax.

• What is the total paid?

FICA tax• Calculate FICA (Social Security and Medicare)

on a $140,000 income if you:– Are not self employed– you pay 7.65% FICA on the first $102,000 – And you pay 1.45% on the income exceeding

$102,000

Federal Income Tax– pg. 447

1. AGI=Gross income – Adjustments= 2. Taxable income = AGI – (Exempt + Deduct)=

3. Tax computation (see table on p. 448)

Income tax= tax computation – tax credit

Do p. 447Marital status ____Number of kids ____Gross income ____Adjustments

Deductions

Tax credit ____

1. AGI=Gross income – Adjustments=

2. Taxable income = AGI – (Ex +Ded)=

3. Tax computation (see table on p. 448)

Income tax= tax computation – tax credit

Fed Tax Ex

Marital status ____Number of kids ____Gross income ____Adjustments

Deductions

Tax credit ____

1. AGI=Gross income – Adjustments=

2. Taxable income = AGI – (Ex +Ded)=

3. Tax computation (see table on p. 448)

Income tax= tax computation – tax credit

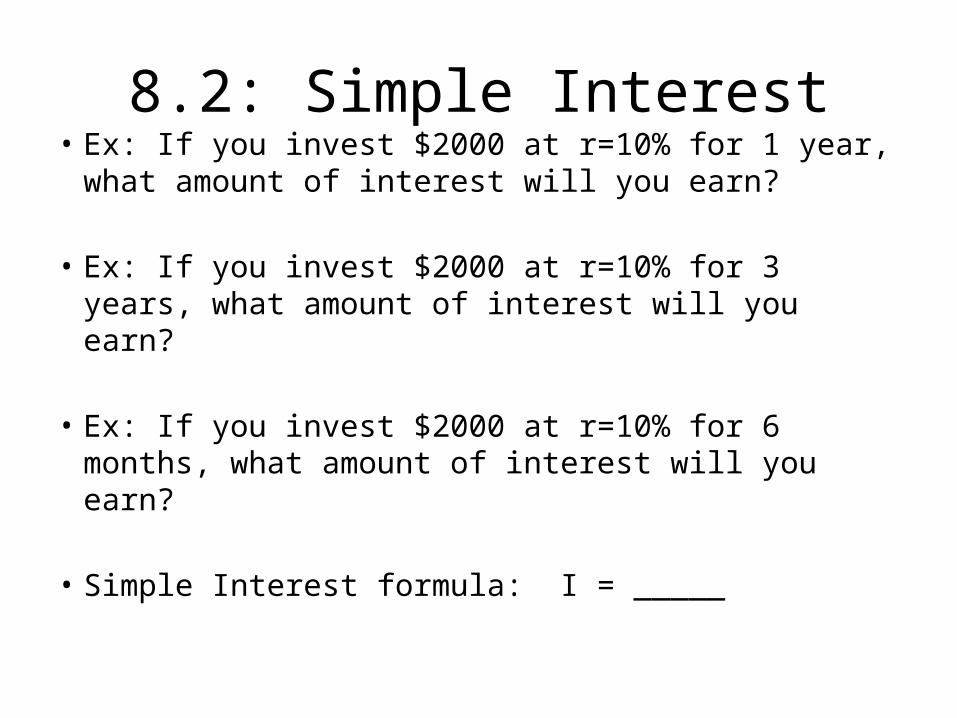

8.2: Simple Interest• Ex: If you invest $2000 at r=10% for 1 year, what

amount of interest will you earn?

• Ex: If you invest $2000 at r=10% for 3 years, what amount of interest will you earn?

• Ex: If you invest $2000 at r=10% for 6 months, what amount of interest will you earn?

• Simple Interest formula: I = _____

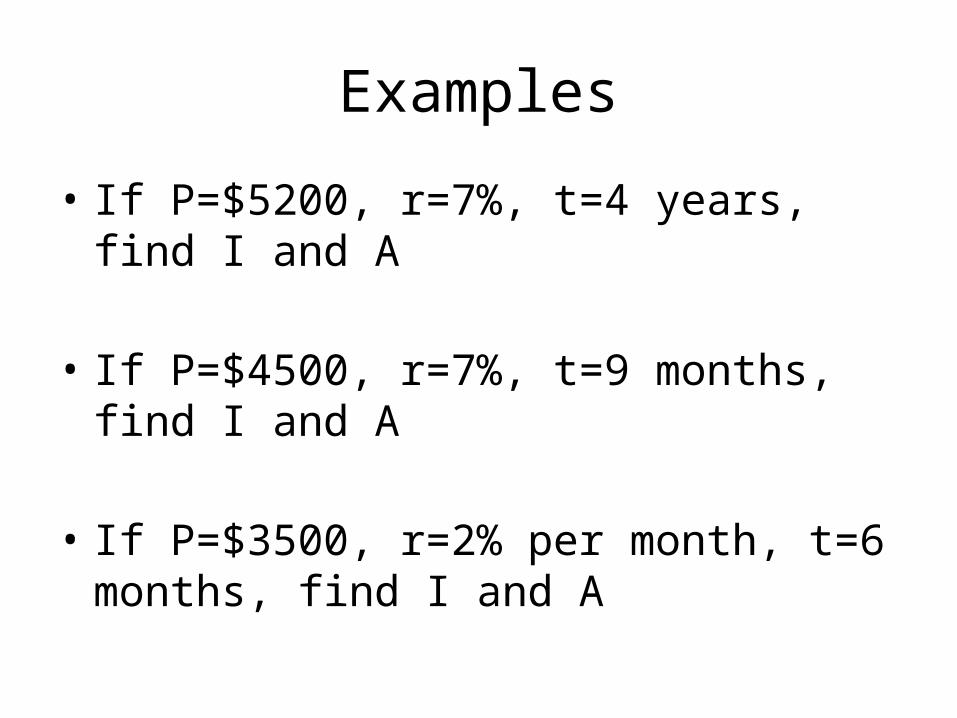

Examples

• If P=$5200, r=7%, t=4 years, find I and A

• If P=$4500, r=7%, t=9 months, find I and A

• If P=$3500, r=2% per month, t=6 months, find I and A

Example

• If P=$2300, r=2 ¼ %, t=10 years, find I and A

Solve for another variable

• If simple interest is calculated to be I=$400, where r = 8%, and t = 2 years, find P

Solve for Principal

• Since I=Prt and A=P+I, then• A=P+Prt=P(1+rt)• If you borrow money at r=7% for 3 years and

you pay back $6050, how much money did you borrow?

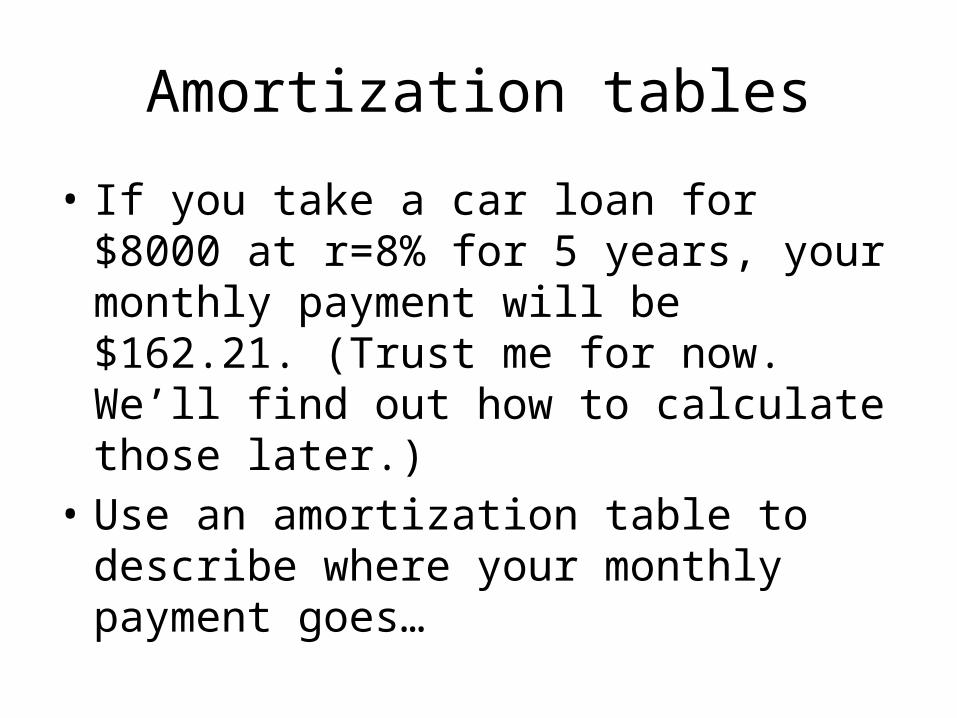

Amortization tables

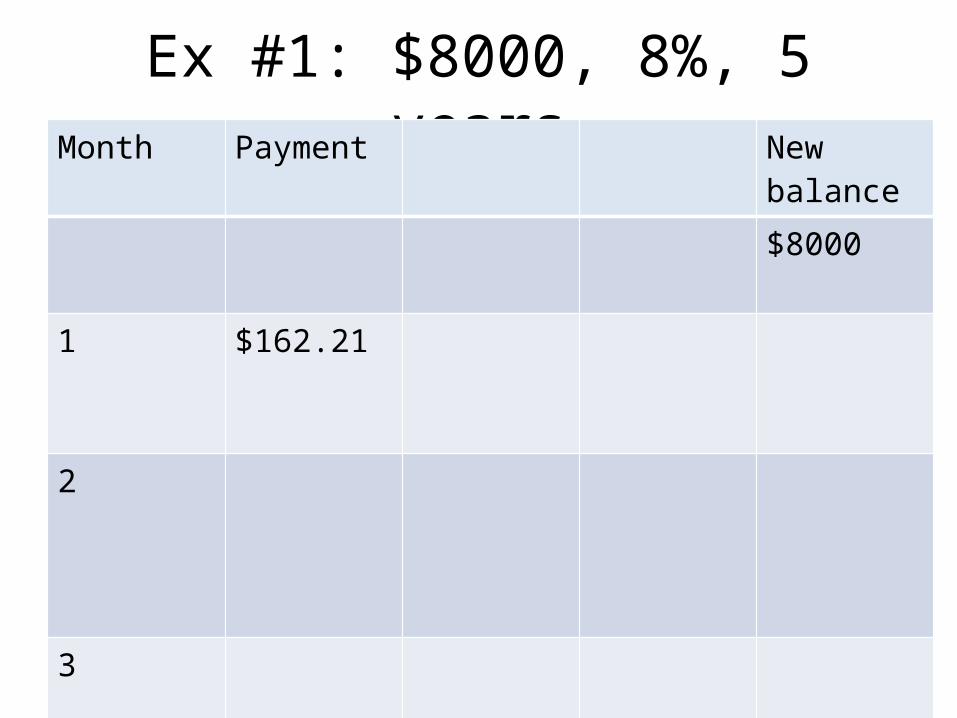

• If you take a car loan for $8000 at r=8% for 5 years, your monthly payment will be $162.21. (Trust me for now. We’ll find out how to calculate those later.)

• Use an amortization table to describe where your monthly payment goes…

Ex #1: $8000, 8%, 5 yearsMonth Payment New

balance

$8000

1 $162.21

2

3

Ex #2: $8000, 5%, 3 years: Month Payment New

balance

$8000

1 $239.77

2

8.3: Compound Interest

• Definition—• Example: Consider borrowing $1000 at r=5%,

compounded annually.• How much will you have at the end of each

year…

Compound- example P=$1000, r=5%, compounded annually

Year Starting balance Amount at year’s end

1 1000 A=P+I=1000+(1000*.05)

2

3

Compound- example P=$1000, r=5%, compounded annuallyYear Starting balance Amount at year’s end

1 1000 A=P+I=1000+(1000*.05) = 1000 + 50 = $1050=1000 ( 1 + .05) = $1050

2 1050

A= 1050 + (1050*.05)=1050(1+.05)= $1102.50=1000(1+0.05)(1+0.05)= 1000(1+.05) 2 = $1102.50

3 1120.50 A= 1102.50 + (1102.50 * .05)= $1157.63=1102.50 (1+.05)=1050(1+.05) (1+.05)=1000(1+.05)(1+.05)(1+.05)= 1000(1+.05) 3 = $1157.63

$1000 Compounded quarterly, at 8%Quarter Start.balance Amount at quarter’s end

1 1000 A=P+I =1000 + (1000*.08 *1/4)=1000+(1000* .08/4)=1000 (1 + .08/4) = 1020

2 1020 A= 1020 + (1020*.08*1/4) = 1020 (1+.08/4)=1000 (1+.08/4)(1+.08/4)=1000 (1 +.08/4) 2 = 1040.40

3 1040.40 A=1040.40 + (1040.4*.08*1/4)=1040.4 (1+.08/4)=1000 (1+.08/4) 3 = 1061.21

4 1061.21 A=1061.21 + (1061.21*.08*1/4)=1061.21 (1+.08/4)=1000 (1+.08/4) 4 = 1082.43

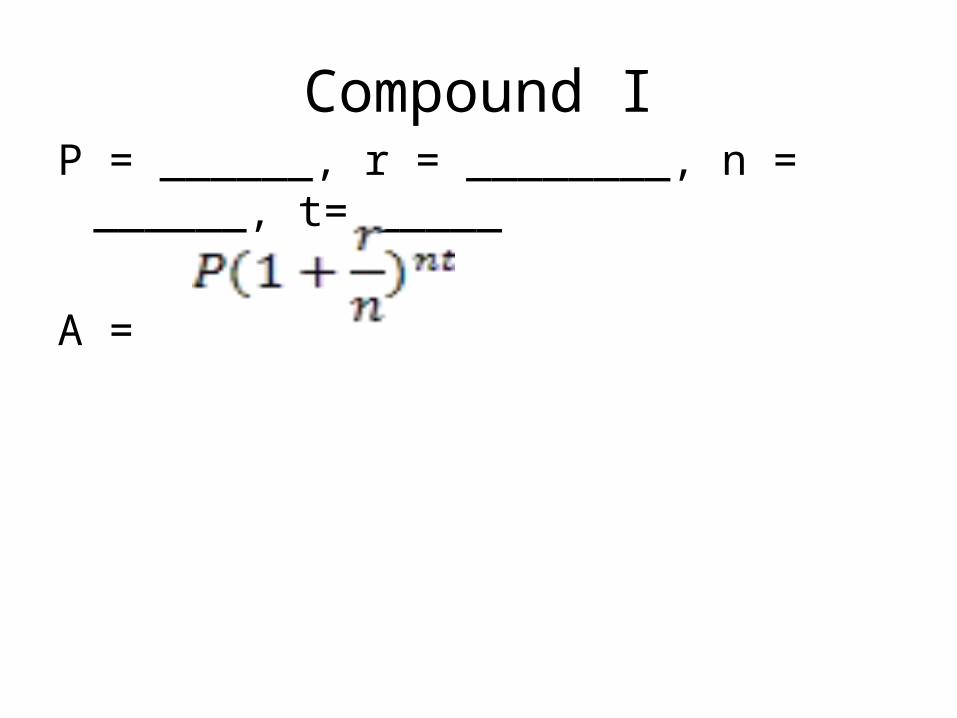

Compound interestP = ______, r = ________, n = ______, t= _____A =

Compound IP = ______, r = ________, n = ______, t= _____

A =

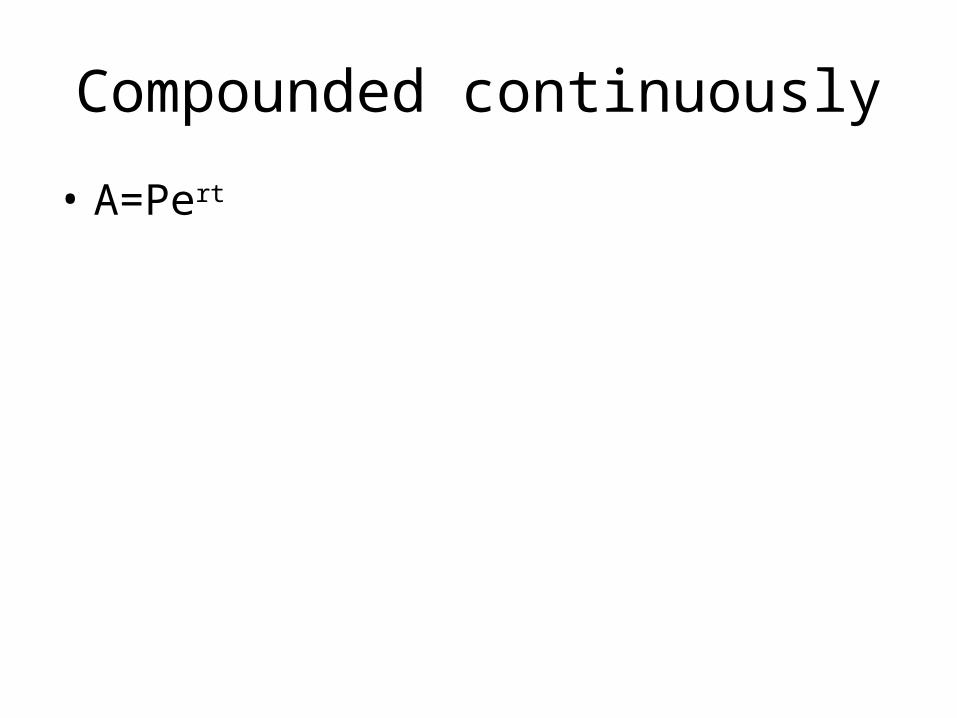

Compounded continuously

• A=Pert

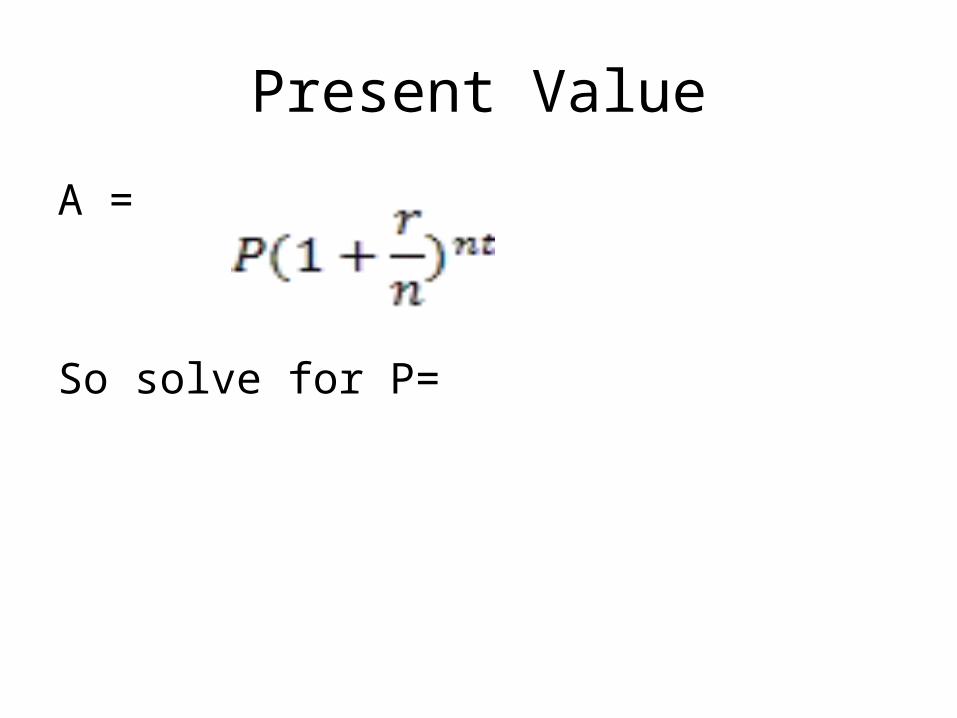

Present Value

A =

So solve for P=

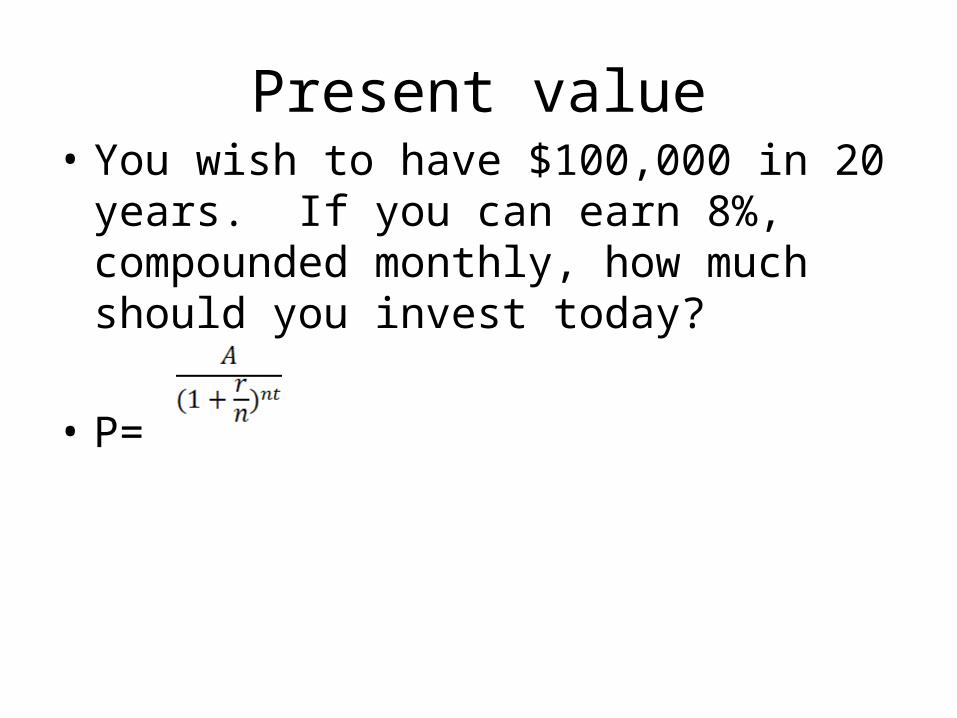

Present value• You wish to have $100,000 in 20 years. If you

can earn 8%, compounded monthly, how much should you invest today?

• P=

Effective yield

• Use A =

8.4: Intro to Annuities

If you invest $100 at the end of every year, at r=5%, you’ll have:

End of 1st year: 100End of 2nd year: 100 + (1.05)*100 End of 3rd year: End of 4th year:

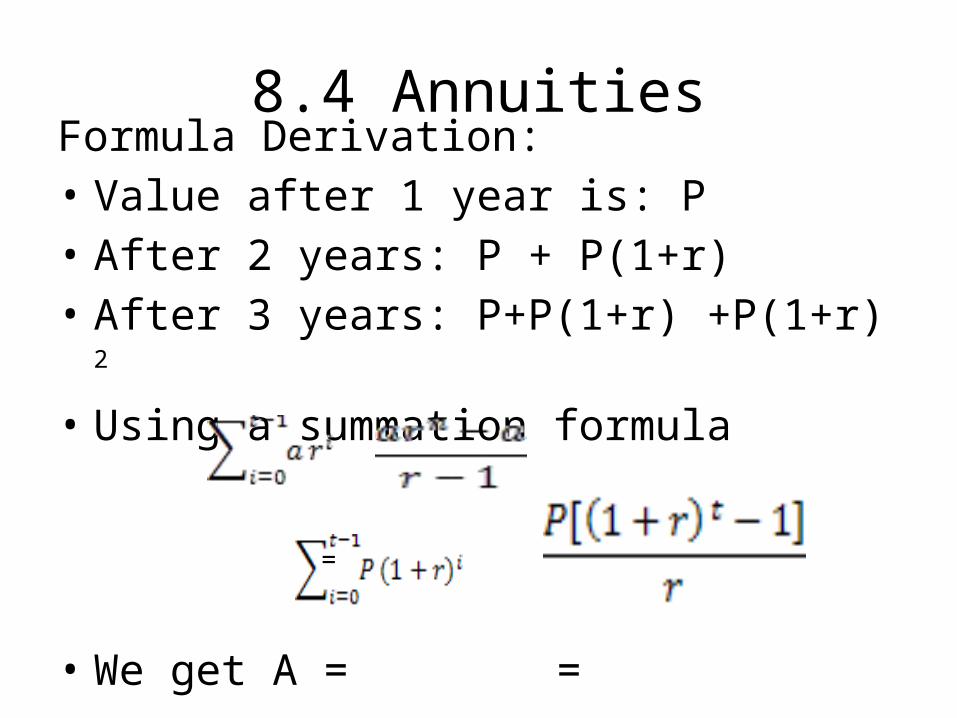

8.4 AnnuitiesFormula Derivation:• Value after 1 year is: P• After 2 years: P + P(1+r)• After 3 years: P+P(1+r) +P(1+r) 2

• Using a summation formula

=

• We get A = =

Annuity compounded once a year

• A =

Ex # 1: Annuity, compounded quarterly

We plan to deposit _____ each quarter for ___ years, at a rate of ___, compounded quarterly.

Find the total amount, A, in the account at the end.• P = ___ , r = ___ , n =____ , t = ____

• A =

Ex #2: Annuity compounded monthlyWe plan to deposit _____ each _____ for ___ years, at a rate of ___,

compounded monthly.Find the total amount, A, in the account at the end.P = ___ , r = ___ , n =____ , t = ____

A =

Calculate the interest• In the previous example, A= ___________ and P = __________

Find the amount you invested to contribute to the final amount

Find the amount of interest that contributed to the total

Ex #3: Annuity compoundedWe plan to deposit ___ each _____ for ___ years, at a rate of

___, compounded _______. Find the total amount, A, in the account at the end.

P = ___ , r = ___ , n =____ , t = ____

A =

• Also, find amount invested

• Find interest earned

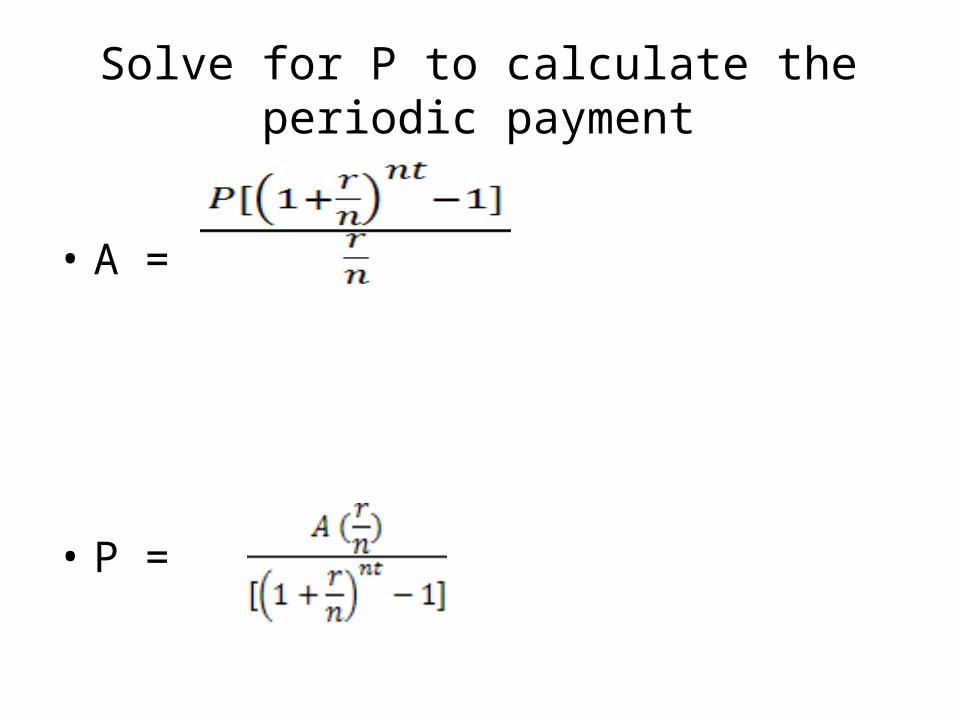

Solve for P to calculate the periodic payment

• A =

• P =

Ex #1: Find P, the periodic paymentWe plan to have __________in ___ years. If we can earn a rate of ___,

compounded _______, how much should we invest each ____. (In other words, find the periodic payment P).

A = ___ , r = ___ , n =____ , t = ____

• P =

• Also, find amount invested

• Find interest earned

Ex #2: Find P, the periodic paymentWe plan to have __________in ___ years. If we can earn a rate of

___, compounded _______, how much should we invest each ____. (Find periodic payment P).

A = ___ , r = ___ , n =____ , t = ____

• P =

• Also, find amount invested

• Find interest earned

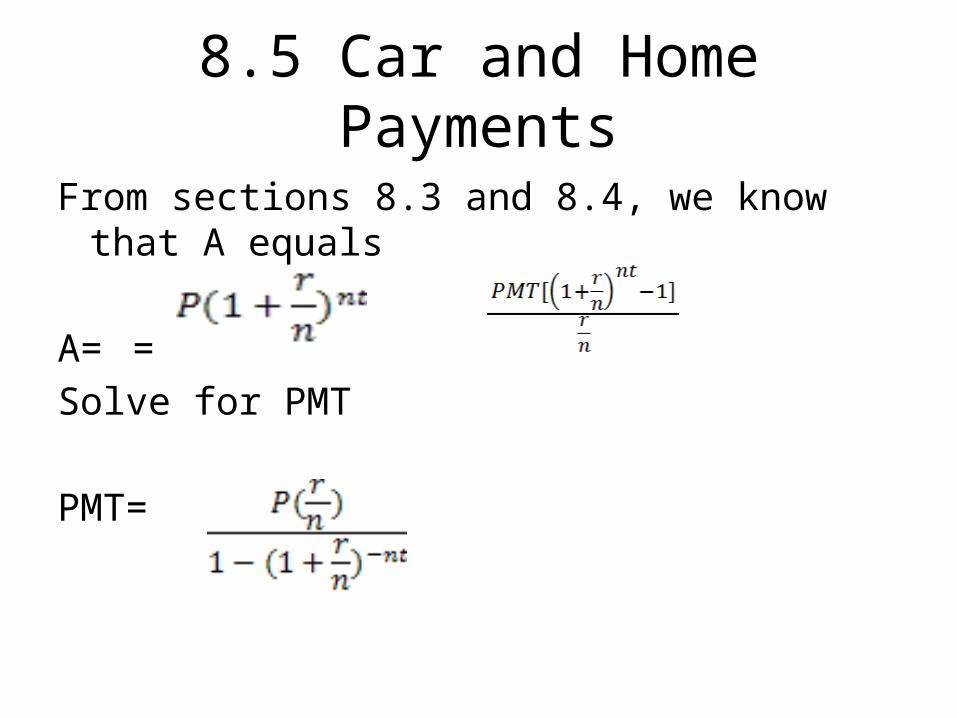

8.5 Car and Home Payments

From sections 8.3 and 8.4, we know that A equals

A= =

Solve for PMT

PMT=

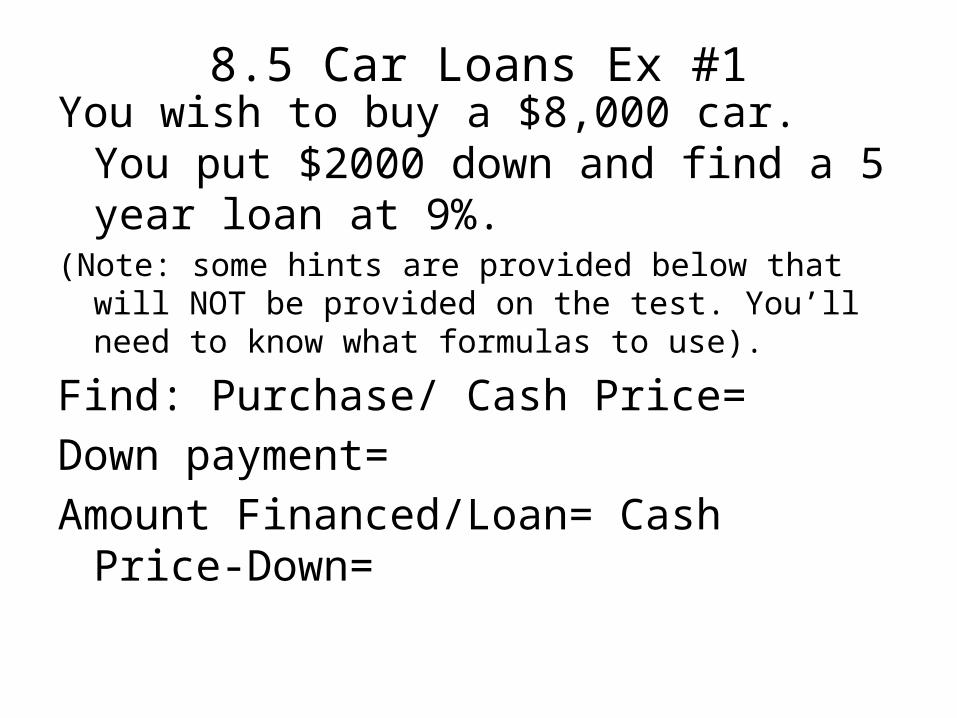

8.5 Car Loans Ex #1You wish to buy a $8,000 car. You put $2000

down and find a 5 year loan at 9%. (Note: some hints are provided below that will NOT be provided

on the test. You’ll need to know what formulas to use).

Find: Purchase/ Cash Price=Down payment=Amount Financed/Loan= Cash Price-Down=

… Car Ex #1: $8,000 car. $2000 down, 5 yrs at 9%.

Monthly payment = PMT = =

Total installment price/ total price paid= (monthly amount*no. months)+down=

Total interest paid/ finance charge= total installment price – cash price=

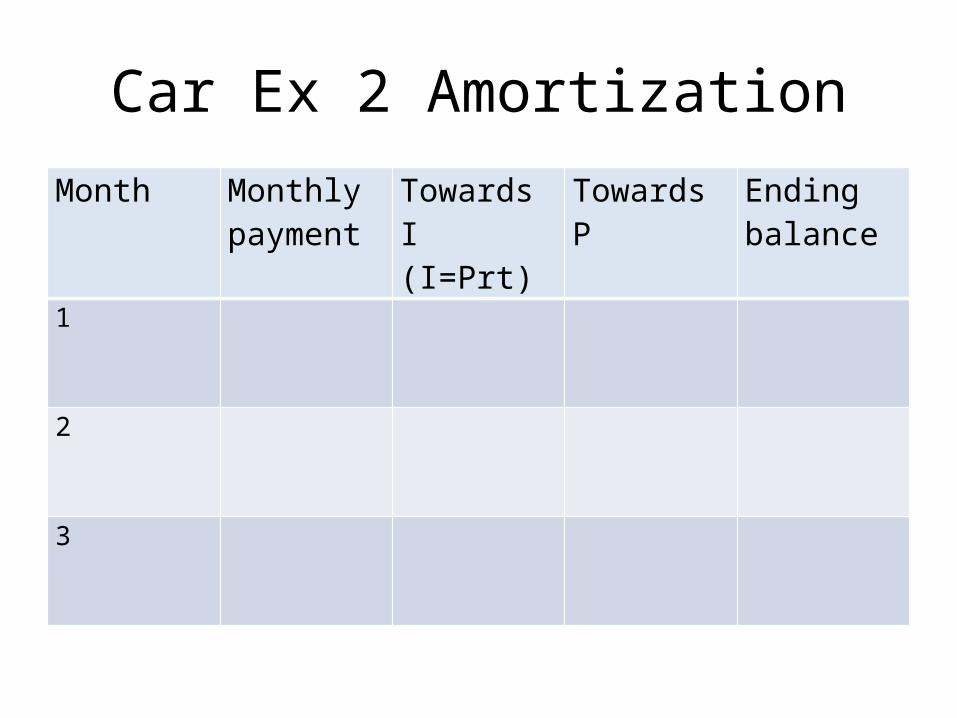

Car Ex 1– Amortization Month Monthly

paymentTowards I (I=Prt)

Towards P Ending balance

1

2

3

Car Ex #2You wish to buy a $10,000 car. You put $3000 down

and find a __ year loan at __%.

Down payment=Amt Financed/Loan= Cash Price - Down=Monthly payment PMT = = ...

…Car Ex 2

Total installment price/ total price paid= (monthly amount*no. months)+down=

Total interest paid/ finance charge= total installment price – cash price=

Car Ex 2 AmortizationMonth Monthly

paymentTowards I (I=Prt)

Towards P Ending balance

1

2

3

8.5 Home MortgagesYou wish to buy a $110,000 house with 20%

down. Loan: 8.5% for 30 years, with 3 points.Insurance: $50/ mn; property taxes: $150/mnDown payment=Amount Financed/Loan= Cash Price-Down*Points (paid at closing)= percentage of loan= ..

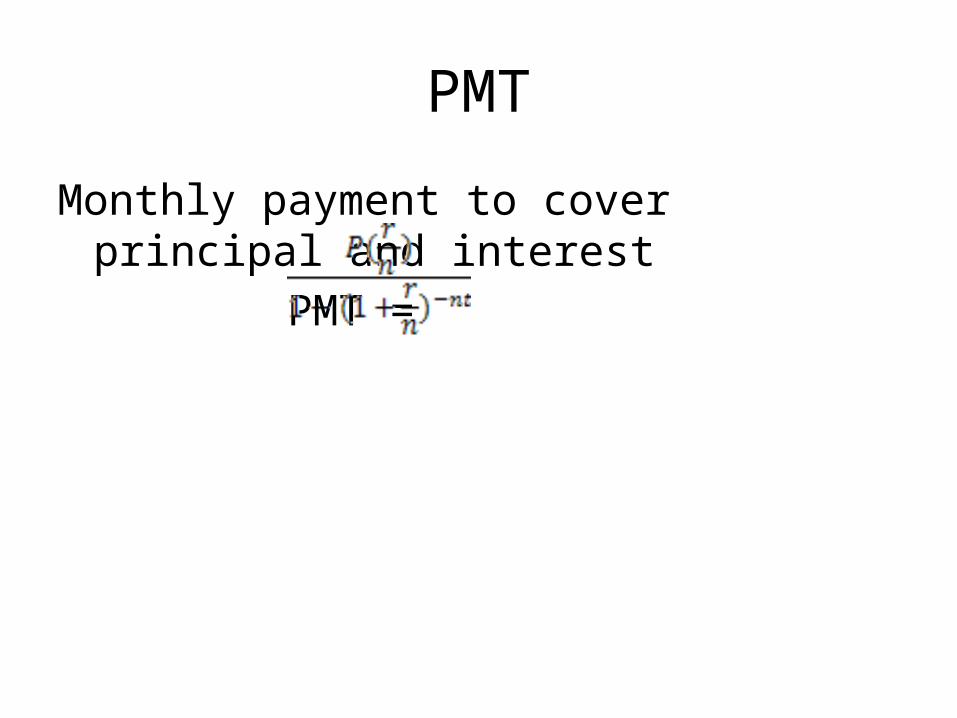

PMT

Monthly payment to cover principal and interest PMT =

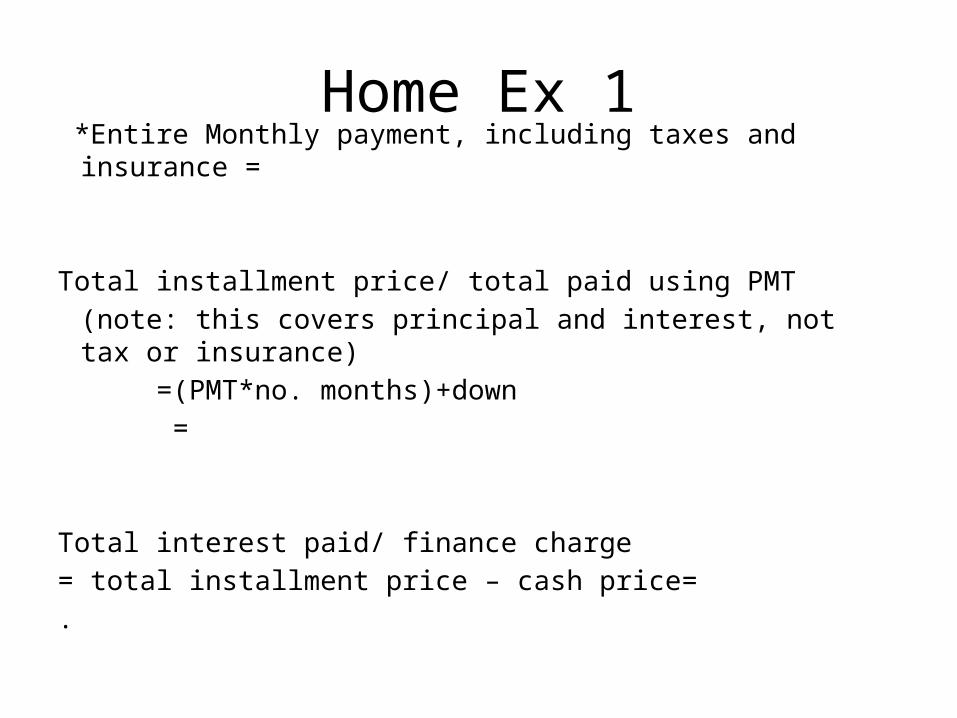

Home Ex 1 *Entire Monthly payment, including taxes and insurance =

Total installment price/ total paid using PMT(note: this covers principal and interest, not tax or insurance)

=(PMT*no. months)+down = Total interest paid/ finance charge= total installment price – cash price=.

Home Ex 1 AmortizationMonth Monthly

paymentTowards I (I=Prt)

Towards P Ending balance

1

2

Saving money on a home What are some ways to save money on the final total

amount paid?______________ _________ ___________ _______________ _____________ Give an example of two specific changes you would

make to save money on this home_______________ _______________.Next, we’ll redo the above problem...

Redo Home Ex 1Redo above example: Purchase Price stays the sameDown payment=Amt Financed/Loan= Cash Price-Down =*Points (paid at closing)= percentage of loan= Monthly paymt= PMT = =

*Entire Monthly payment, including taxes and insurance =

Home Ex 1--revisedTotal installment price/ total paid using PMT

(note: principal and interest, not tax or insurance) =(PMT*no. months)+down = Total interest paid/ finance charge= total installment price – cash price=

Month Monthly payment

Towards I (I=Prt)

Towards P Ending balance

1

Home Ex #2

You wish to buy a $150,000 house with 20% down. Loan: 5 ¼ % for 20 years, with 2 points.

Insurance: $60/ mn; property taxes: $170/mnDown payment=Amount Financed/Loan= Cash Price-Down*Points (paid at closing)= percentage of loan= Monthly payment to cover principal and interest PMT = .

Home Ex 2

*Entire Monthly payment, including taxes and insurance =

Total installment price/ total paid using PMT(note: this covers principal and interest, not tax or insurance)

=(PMT*no. months)+down = Total interest paid/ finance charge = total installment price – cash price=

Home Ex 2 AmortizationMonth Monthly

paymentTowards I (I=Prt)

Towards P Ending balance

1

Home Ex #3You wish to buy a $________ house with __%

down. Loan: ___% for __ years, with __ points.Insurance: $__/ mn; property taxes: $__/mnDown payment=Amount Financed/Loan= Cash Price-Down*Points (paid at closing)= percentage of loan= Monthly payment to cover principal and interest PMT =

Home Ex 3

*Entire Monthly payment, including taxes and insurance =

Total installment price/ total paid using PMT(note: this covers principal and interest, not tax or insurance)

=(PMT*no. months)+down =

Total interest paid/ finance charge = total installment price – cash price=

Home Ex 3 AmortizationMonth Monthly

paymentTowards I (I=Prt)

Towards P Ending balance

1

Credit Card Amortization problem• Consider a $10,000 debt, paid back over 20 years at R=21%. • Calculate monthly payment: PMT=

• Calculate first month interest and principal payments: I=

Month Monthly payment Towards I (I=Prt)

Towards P Ending balance

1 $177.76