mas notice 645 total debt servicing ratio & mas notice...

TRANSCRIPT

MAS Notice 645 Total Debt Servicing Ratio & MAS Notice 632 Residential Property Loan With effect from 29 June 2013, Saturday (Condensed presentation deck for external parties)

1

Highlights of new measures effective 29 June 2013

2

1. Consider monthly repayments of new loan and all other debts.

2. Applies to property loans for Singapore & overseas residential/non-

residential properties, to individuals or entities set up solely to purchase

property;

3. Total debt servicing ratio (TDSR) is capped at 60%.

4. Calculate new loan repayments using min 3.5% for residential property

loans;

5. All borrowers to be mortgagors (OTP on or after 29 Jun 13);

6. Guarantors to be co-borrowers;

7. For joint borrowings, the income-weighted average age of borrowers to

be used;

8. Haircut of at least 30% on variable income & rental; and

9. Haircut on the value of financial assets if used in calculating income.

Applications of MAS Notice 645 & MAS Notice 632

3

Notice 632 Residential Property Loan

Notice 645 Total Debt Servicing Ratio

• Properties in Singapore & overseas

• Residential, commercial, industrial

(including land, construction loan)

• Individuals & entities set up specifically

to purchase properties

• Singapore residential properties

• Individuals and entities purchasing

properties.

TDSR for loan eligibility LTV, tenor, income-weighted average age,

borrower to be mortgagor

Ap

plica

tio

n

Exclu

sio

n • Bridging Loan up to 6 months

• Credit facility secured by pool of

collateral including property where the

market value of the subject property is <

50% of the pool of collateral

• Credit facility granted by a bank to a

Property Developer to purchase

residential property for development.

60%

Instalment

(Single)

Existing

Instalment

(Joint)

Credit Card (unsecured

revolving)

Secured

Revolving

Guarantor HDB or

EC fr Dev

Instalment

on subject

loan

3.5% for HL

Existing:

Statement

Apportion to

income

contribution

for existing

joint debts

(evidence of

joint’s income)

Min

Payment in

latest stmt

or interest on

full limit

Outstanding

in latest stmt

or interest on

full credit limit

20% of

credit

facilities

(including

corporate)

Excluded MI of existing

property if buying HDB/EC

from developer

• 1st resi pty to be sold

• No o/s facility on any pty except

HL on 1st pty to be sold

• No other pty singly or jointly

Total Debt Servicing Ratio for PHL & HDB

70% average

last 12 months

exc. employer

CPF; OR

70% NOA

divided by 12

100% Fixed +

70% Variable

OR

100% NOA

divided by 12

70% if borrower

is the landlord.

Submit stamped

tenancy agreement

with min 6 months

% deduction on

value divide 48

% Deduction Pledge ≥ 4yr

for subject loan

Unpledged /

Pledge < 4 yr

SGD Deposit 0% 70%

Non Pty Asset 30% 70%

Fixed Variable Fixed +

Variable Rental Assets

(unpledged)

100% monthly

income

exclude

employer CPF

≤

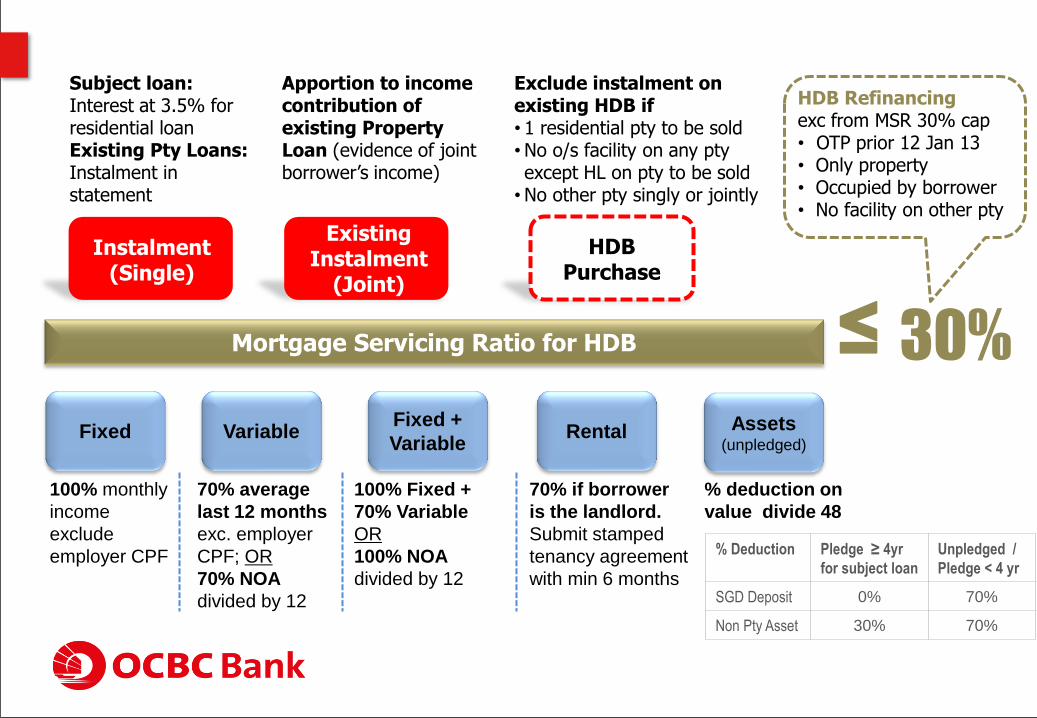

HDB Refinancing exc from MSR 30% cap • OTP prior 12 Jan 13 • Only property • Occupied by borrower • No facility on other pty

30%

HDB Purchase

Exclude instalment on existing HDB if • 1 residential pty to be sold • No o/s facility on any pty except HL on pty to be sold

• No other pty singly or jointly

Mortgage Servicing Ratio for HDB

Instalment (Single)

Existing Instalment

(Joint)

≤

Apportion to income contribution of existing Property Loan (evidence of joint borrower’s income)

Subject loan: Interest at 3.5% for residential loan Existing Pty Loans: Instalment in statement

70% average

last 12 months

exc. employer

CPF; OR

70% NOA

divided by 12

100% Fixed +

70% Variable

OR

100% NOA

divided by 12

70% if borrower

is the landlord.

Submit stamped

tenancy agreement

with min 6 months

% deduction on

value divide 48

% Deduction Pledge ≥ 4yr

for subject loan

Unpledged /

Pledge < 4 yr

SGD Deposit 0% 70%

Non Pty Asset 30% 70%

Fixed Variable Fixed +

Variable Rental Assets

(unpledged)

100% monthly

income

exclude

employer CPF

Applications of MAS Notice 645 & MAS Notice 632

6

Notice 632 Residential Property Loan

Notice 645 Total Debt Servicing Ratio

• Properties in Singapore & overseas • Residential, commercial, industrial

(including land, construction loan) • Individuals & entities set up specifically

to purchase properties

• Singapore residential properties • Individuals and entities purchasing

properties.

TDSR for loan eligibility LTV, tenor, income-weighted average age, borrower to be mortgagor

Ap

pli

ca

tio

n

Ex

clu

sio

n • Bridging Loan up to 6 months

• Credit facility secured by pool of collateral including property where the market value of the subject property is < 50% of the pool of collateral

• Credit facility granted by a bank to a Property Developer to purchase residential property for development.

Income weighted average age (IWAA) is computed for joint

borrowings in order to determine tenure (guided by MAS 632)

7

Income of Younger Borrower >

Income of Older Borrower

Income of Younger Borrower <

Income of Older Borrower

Outcome IWAA is lower

Loan tenure is longer

IWAA is higher

Loan tenure is shorter

Income-

Weighted

Average Age

(IWAA)

A age 30 earns $7,000 pm

B age 50 earns $3,000 pm

IWAA = (30 x $7K) + (50 x $3K)

$7K + $3K

= 36 years

A age 30 earns $3,000 pm

B age 50 earns $7,000 pm

IWAA = (30 x $3K) + (50 x $7K)

$3K + $7K

= 44 years

Loan Tenure

Please refer to MAS

632 LTV chart

(next slide)

Max Tenure = 35 yrs (60% LTV) Max age of 75 years less IWAA, capped

at 35 years. As 75 – 36 = 39 is higher

than cap, max is 35 years

Tenure for 80% LTV = 29 yrs Tenure ≤ 30 years & < age 65 on

maturity, i.e. tenure is 65 - 36 = 29 years

Max Tenure = 31 Years (60% LTV) Max age of 75 years less IWAA, capped

at 35 years. As 75 – 44 = 31 is lower than

cap, max is 31 years

Tenure for 80% LTV = 21 years Tenure ≤ 30 years & < age 65 on

maturity, i.e. tenure is 65 - 44 = 21 years

≤ 65

yrs

> 65

yrs

Up to

30 Yrs

31 to

35 Yrs

Note: LTV for corporate entities is 20%

80% 60%

Loan

Tenure

Sum of Tenure

& Age of

Borrower (at application)

Loan-

To-Value

No of Home

Loans including

this application

5% 10% Cash

Down

Payment

1st

Home Loan

60%

10%

≤ 65

yrs

> 65

yrs

Up to

30 Yrs

31 to

35 Yrs

50% 30%

25% 25%

2nd

Home Loan

30%

25%

≤ 65

yrs

> 65

yrs

Up to

30 Yrs

31 to

35 Yrs

40% 20%

25% 25%

3rd & sub.

Home Loan

20%

25%

8

No change to LTV rules under MAS 632 for Singapore Properties for

New Purchase w.e.f. 12 Jan 13 (OTP/S&P Date)

Every $100K loan or $125K house price requires $750 monthly

income (max 80% LTV for 30 years tenure)

9

House Price Loan Amount Monthly Income

$ 125,000 $ 100,000 $ 750

$ 750,000 $ 600,000 $ 4,500

$ 1,000,000 $ 800,000 $ 6,000

$ 1,250,000 $ 1,000,000 $ 7,500

$ 1,500,000 $ 1,200,000 $ 9,000

Every

$100K loan

+$750 income

10

$1000 debt requires additional $1,670 monthly income to

support the commitment. Every $100K deposits will reduce

monthly income required by $625.

House Price Loan Amount

Monthly

Income

(30 Yrs)

Monthly

Income with

$1000 Debt

Monthly Income

with $1K Debt +

$100K Deposits*

$125,000 $100,000 $750 $2,420 $1,795

$750,000 $600,000 $4,500 $6,160 $5,535

$1,000,000 $800,000 $6,000 $7,660 $7,035

$1,250,000 $1,000,000 $7,500 $9,160 $8,535

$1,500,000 $1,200,000 $9,000 $10,650 $10,025

* Deposits placed with a Singapore Bank and must show evidence of funds prior to the first loan drawdown

(latest bank statement prior to solicitor’s advice to drawdown)

11

Before After

Household Income (S$) 10,000 10,000

Max monthly repayment with 60% TDSR 6,000 6,000

1st Property Buyer, Max LTV 80%

Interest rate 2.80% 3.50%

Tenure (years) 30 30

Max loan amount on $6K monthly repayment 1,460,225 1,336,165

Max 1st property value 1,825,285 1,670,210 (-8%)

Illustration No 1: For a first time private property buyer with

average household income of $10K and no debts, the buyer can

afford property priced 8% lower than before the TDSR rules.

Illustration No 2: For a 2nd time property buyer with an existing

home loan, the max property price he can afford is 8% less than

prior to the new rules

12

Before After

Household Income (S$) 10,000 10,000

Max monthly repayment with 60% TDSR 6,000 6,000

Existing Home Loan

Loan Amount 800,000 800,000

Interest Rate 1.30% 1.30%

Tenure (years) 30 30

Monthly Repayment 2,685 2,685

2nd Property Buyer, Max LTV 50%

Interest rate 2.80% 3.50%

Tenure (years) 30 30

Max loan amount with existing HL $800K HL 806,816 738,270

Max 2nd property value 1,613,631 1,476,539 (-8%)

13

Disclaimer

The information provided herein is intended for general information and discussion purposes only. It does not

take into account the specific investment objectives, financial situation or particular needs of any particular

person.

Without prejudice to the generality of the foregoing, please seek advice from an independent financial and legal

adviser regarding the information provided herein taking into account your specific objectives, financial situation

or particular needs before you make a commitment to purchase any property and/or borrow from any entity or

institution to finance the purchase of the property. This does not constitute an offer or solicitation to provide loan

or financing to any particular person or to enter into a transaction.

No representation or warranty whatsoever (including without limitation any representation or warranty as to

accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without

limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should

not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct

any inaccuracy that may become apparent at a later time. All information presented is subject to change without

notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or

indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward looking statement regarding future

events or future performance of countries, assets or markets. Actual events or results may differ materially. Past

performance figures are not necessarily indicative of future or likely performance. Any reference to any specific

entity, authority, area, figures, property or asset class in whatever way is used for illustrative purposes only and

does not constitute a recommendation on the same.

This presentation and its contents are considered proprietary information and may not be reproduced or

disseminated in whole or in part without OCBC Bank’s written consent.