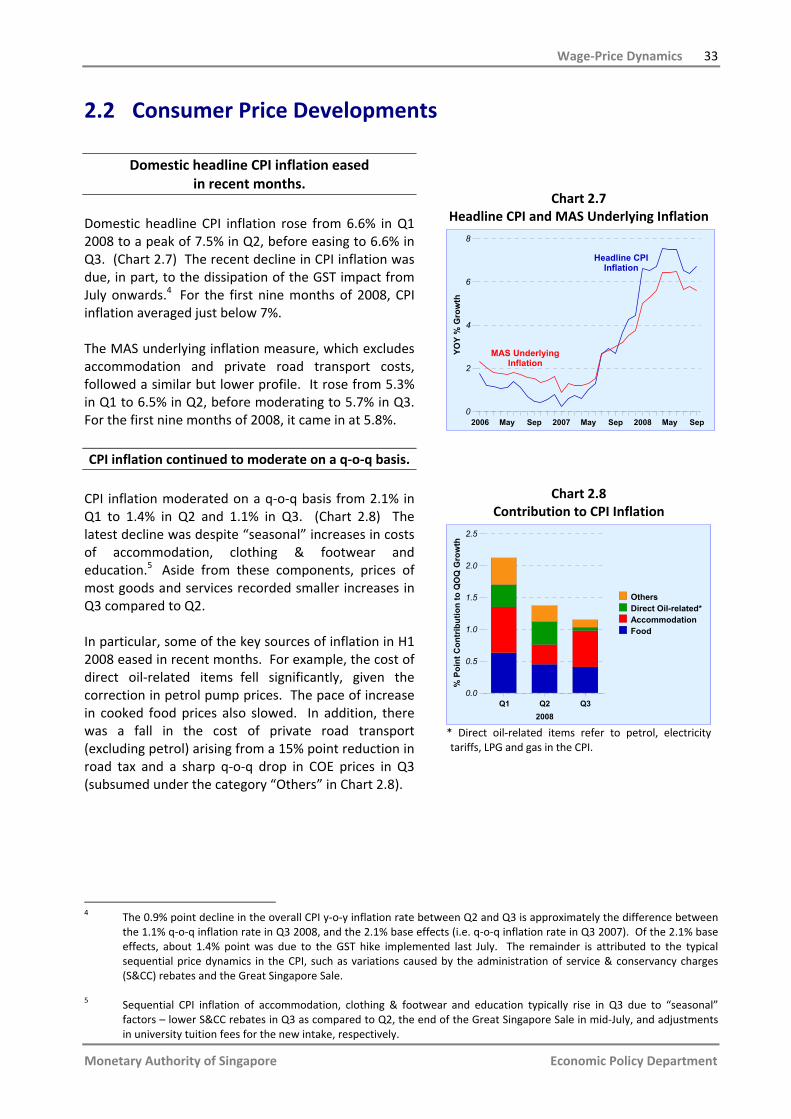

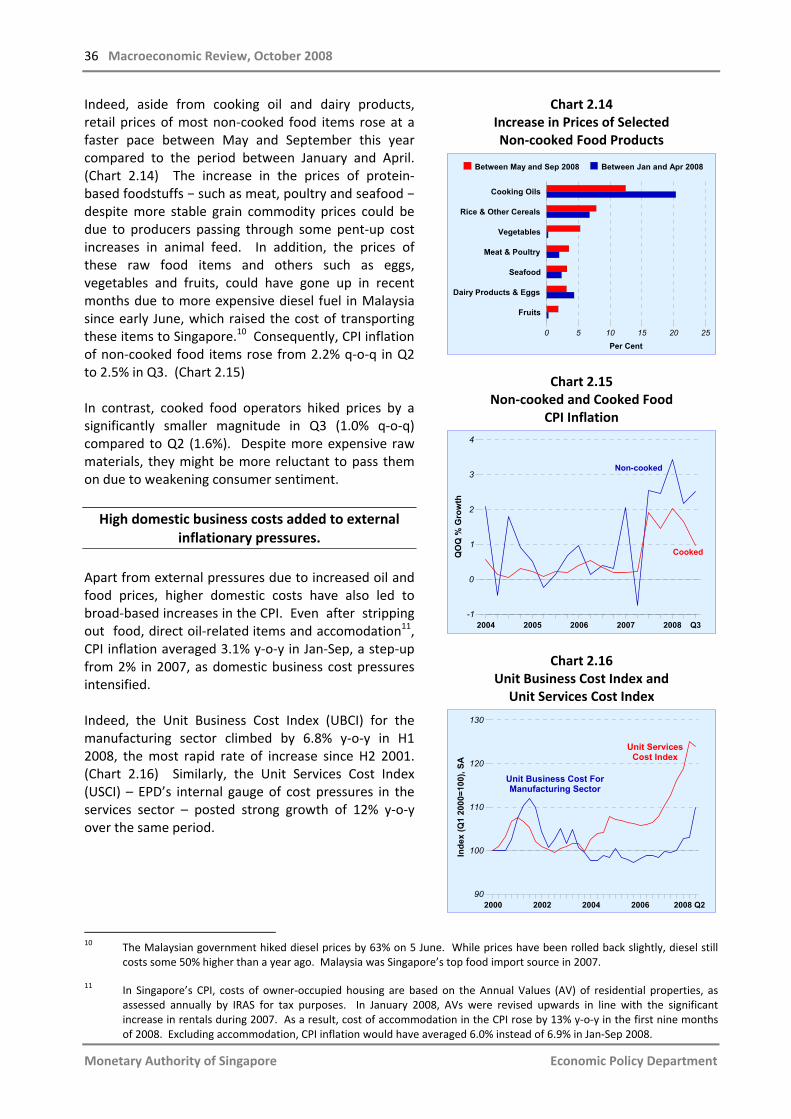

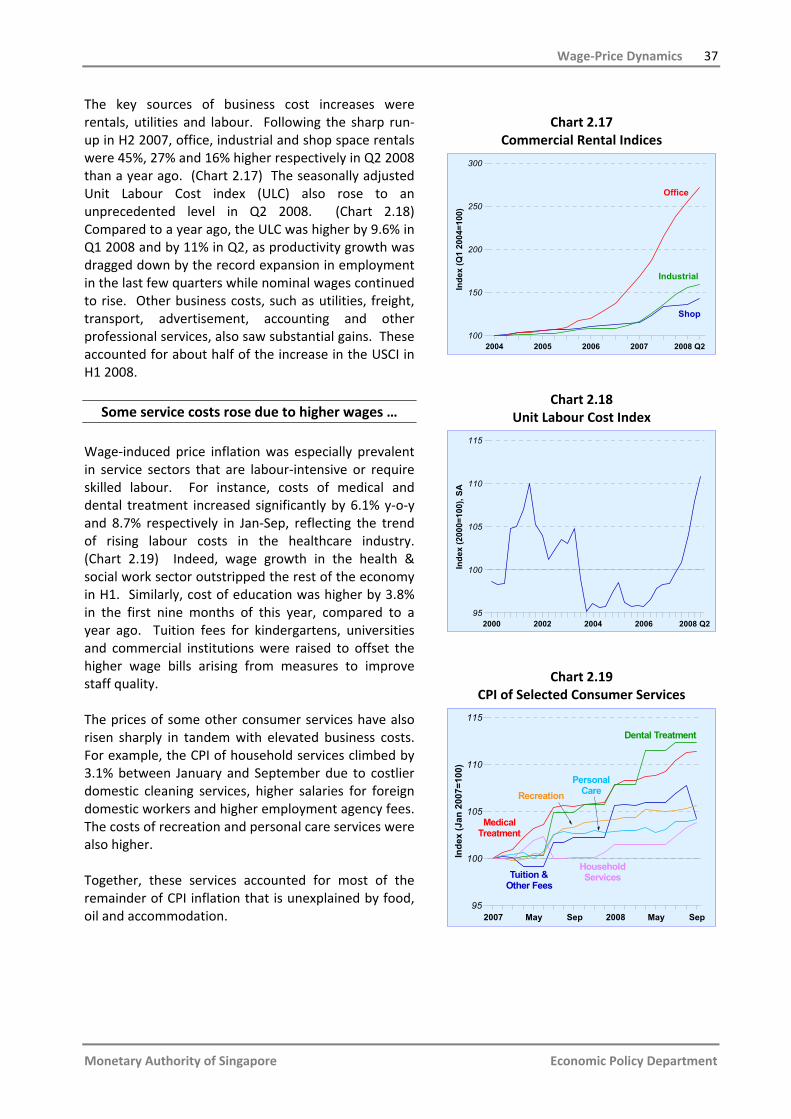

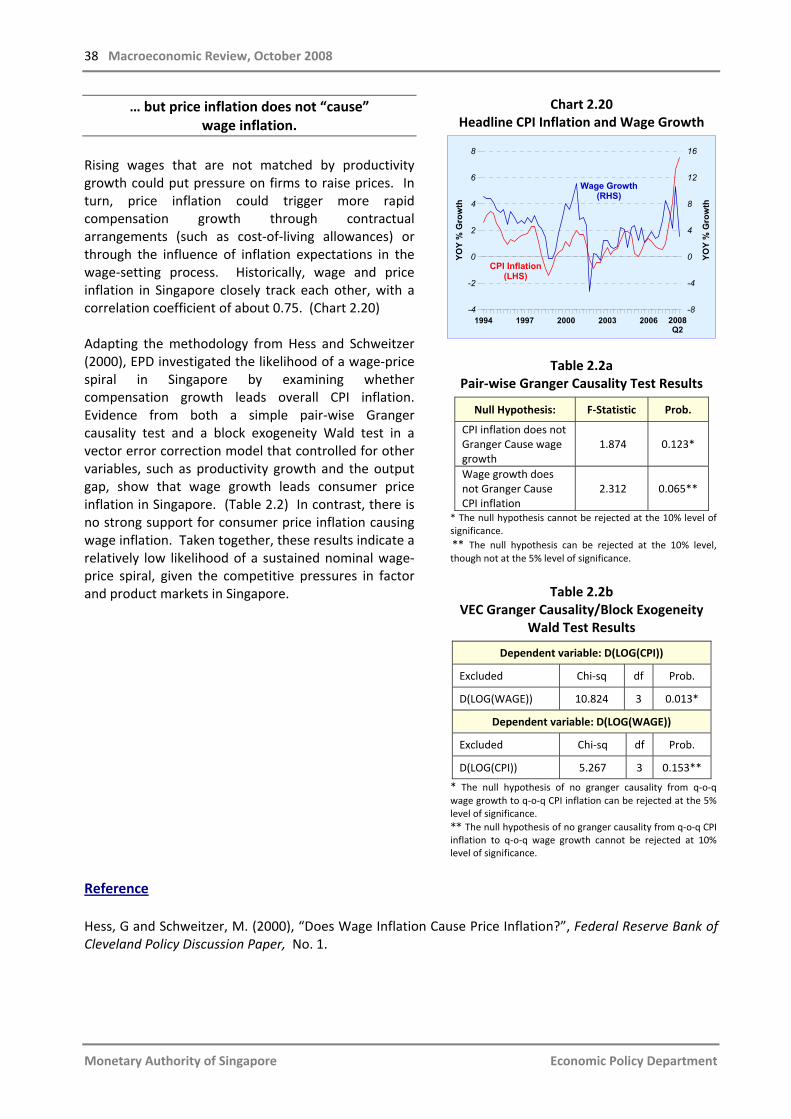

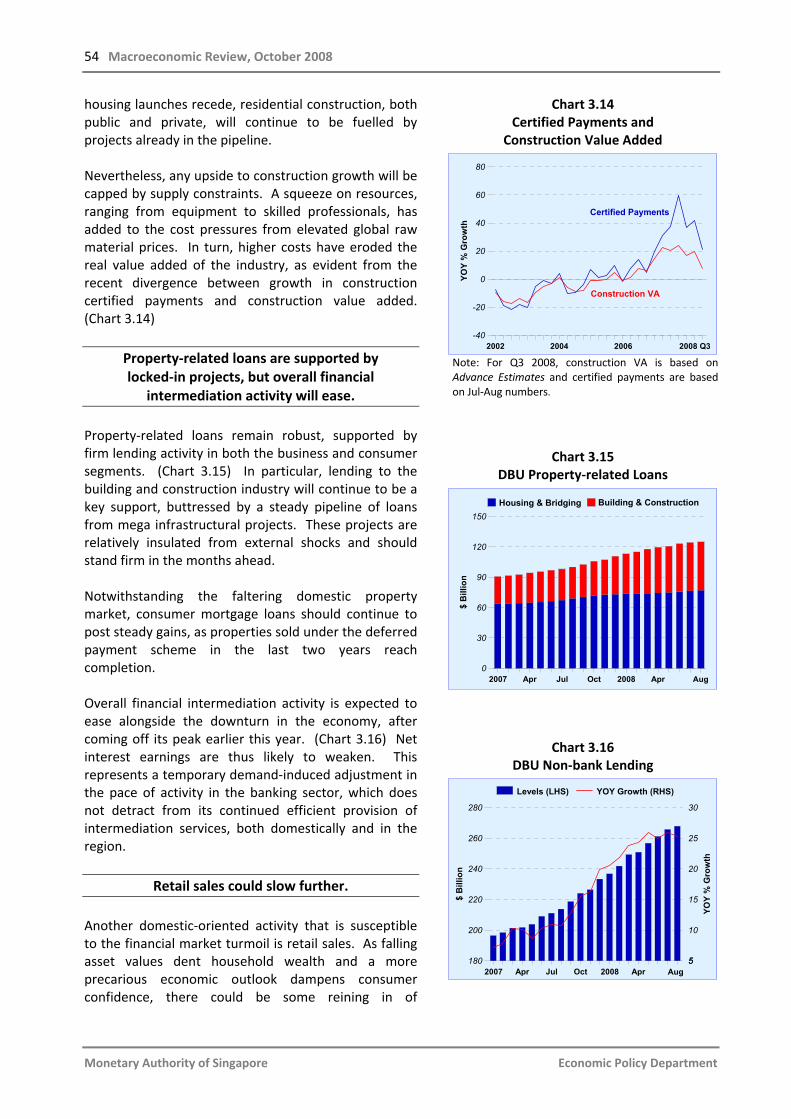

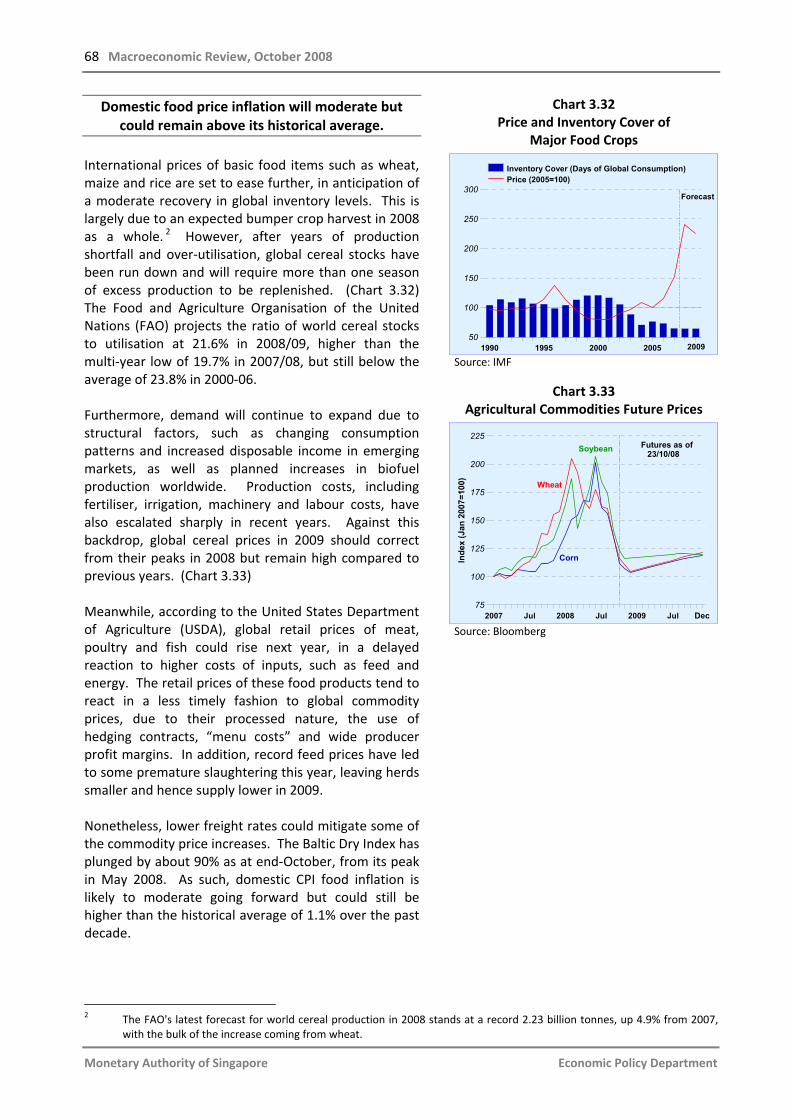

mas macroeconomic review

TRANSCRIPT

macroeconomic

economic policy departmentVolume VII, Issue 2

October 2008

MA

S Macroeconom

ic Review

Volum

e VII, Issue 1, A

pril 2008

Volume VII, Issue 2 October 2008

macro eco cover.indd 2 10/29/07 3:32:22 PM

Economic Policy Department Monetary Authority of Singapore

ISSN 0219-8908

Economic Policy Department Monetary Authority of Singapore

http://www.mas.gov.sg

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanised, photocopying, recording or otherwise, without the prior written permission of the copyright owner except in accordance with the provisions of the Copyright Act (Cap. 63). Application for the copyright owner's written permission to reproduce any part of this publication should be addressed to:

Economic Policy Department Monetary Authority of Singapore 10 Shenton Way MAS Building Singapore 079117

Printed by Chung Printing

macro eco cover.indd 3 10/29/07 3:32:22 PM

Published in October 2008

Monetary Authority of Singapore Economic Policy Department

Contents Preface i Highlights ii‐iii Monetary Policy Statement iv‐v 1 Macroeconomic Developments 1.1 External Developments 2

Box A: The Phillips Curve Revisited 5 1.2 Domestic Economy 10 1.3 Macroeconomic Policy 18

Box B: Review of MAS’ Money Market Operations in FY2007/08 25 2 Wage‐Price Dynamics 2.1 Labour Market Conditions 30 2.2 Consumer Price Developments 33

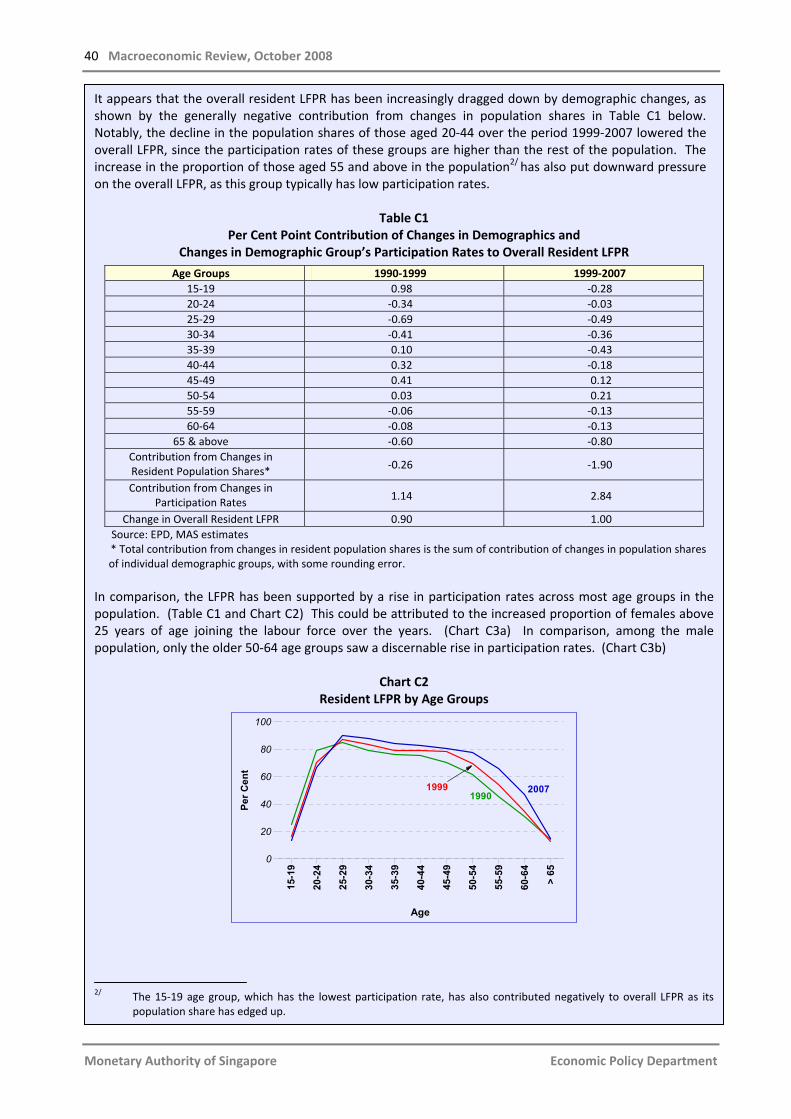

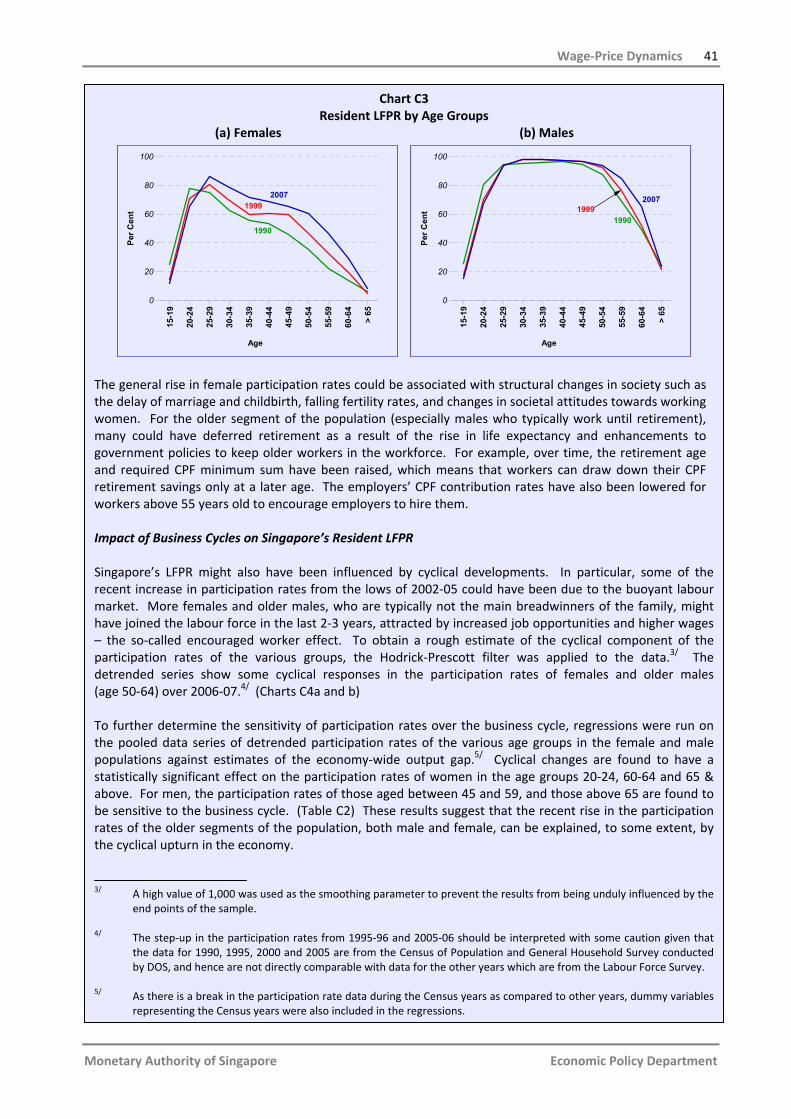

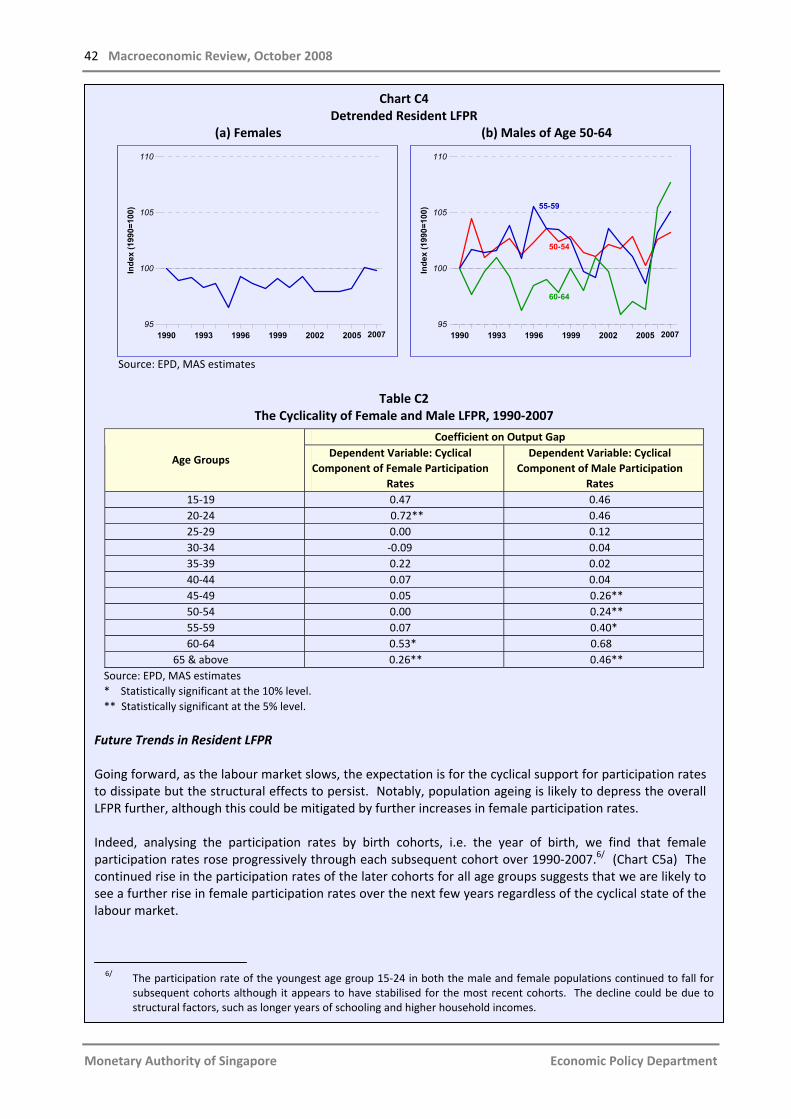

Box C: Recent Trends in Singapore’s Resident Labour Force 39 Participation Rate

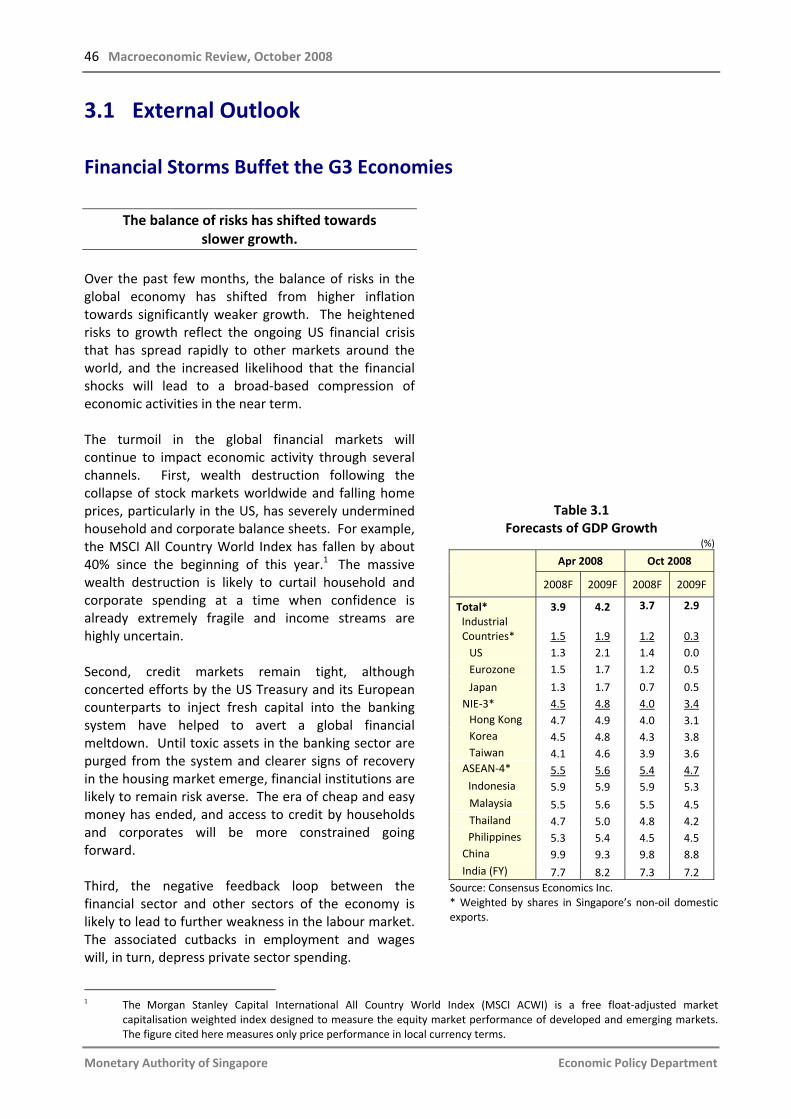

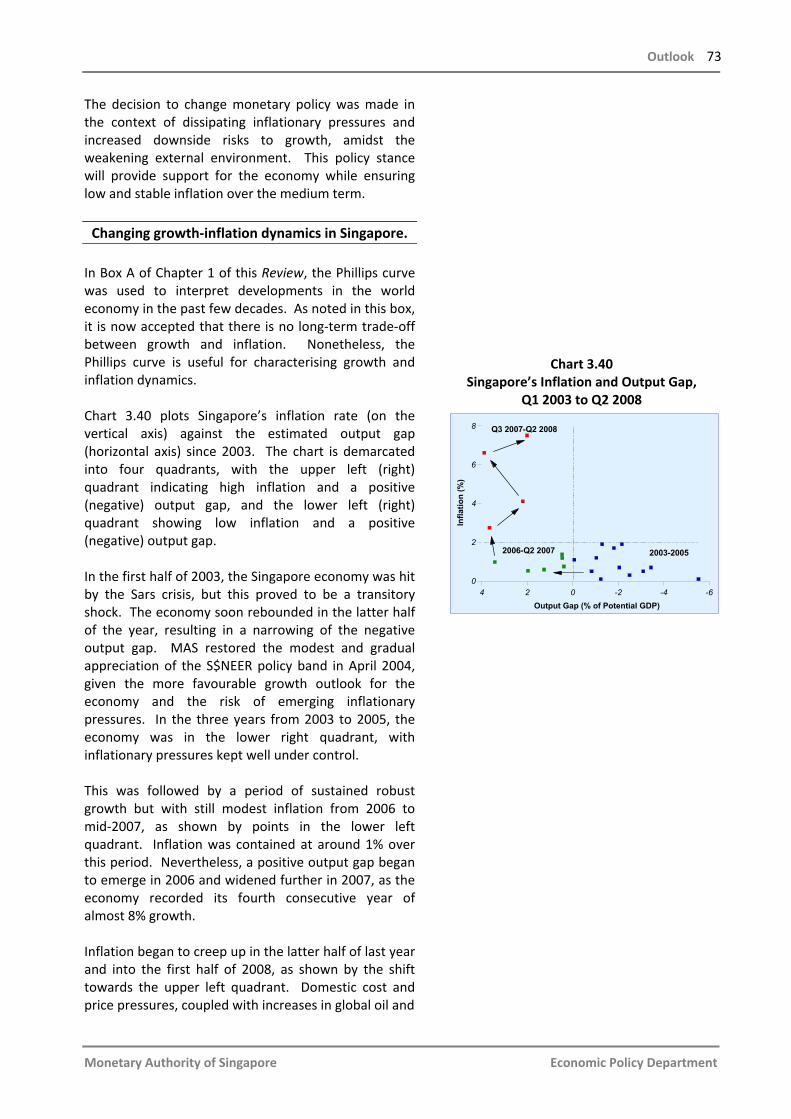

3 Outlook 3.1 External Outlook 46 3.2 Outlook for the Singapore Economy 50 Box D: Market Share Analysis of Regional Manufacturing Exports 60 3.3 Labour Market 65 3.4 Inflation 67 3.5 Monetary Policy 72 Special Features

Special Feature A: An Empirical Analysis of Exchange Rate Pass‐through 76 in Singapore

Special Feature B: Analysing Oil Price Shocks and their Impact on the 86 Singapore Economy Special Feature C: Economic Benefits from International Cooperation 92 on the Environment Statistical Appendix 94 List of Selected Publications 103

Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

LIST OF ABBREVIATIONS BCA Building & Construction Authority bpd barrels per day bps basis points COE Certificate of Entitlement CPF Central Provident Fund CPI consumer price index DLI Domestic Liquidity Indicator DOS Department of Statistics ECB European Central Bank EDB Economic Development Board EIA Energy Information Administration EPD Economic Policy Department FAO Food and Agriculture Organisation of the United Nations FI fiscal impulse FISIM financial intermediation services indirectly measured FX foreign exchange FY financial year HDB Housing Development Board IMF International Monetary Fund IPI Import Price Index IRAS Inland Revenue Authority of Singapore LFPR labour force participation rate LPG Liquid Petroleum Gas MMOs money market operations MMS Monetary Model of Singapore MOF Ministry of Finance m‐o‐m month‐on‐month MOM Ministry of Manpower MOT Ministry of Transport MPS Monetary Policy Statement MTI Ministry of Transport NEER nominal effective exchange rate NODX non‐oil domestic exports NORX non‐oil re‐exports NTUC National Trades Union Congress OECD Organisation of Economic Cooperation and Development OPEC Organisation of the Petroleum Exporting Countries PCE personal consumption expenditures q‐o‐q quarter‐on‐quarter REER real effective exchange rate SAAR seasonally adjusted annualised rate SGS Singapore Government Securities STB Singapore Tourism Board STI Straits Times Index UBCI Unit Business Cost Index ULC Unit Labour Cost USCI Unit Services Cost Index WTI West Texas Intermediate y‐o‐y year‐on‐year

Preface i

Monetary Authority of Singapore Economic Policy Department

Preface The Macroeconomic Review is published twice a year in conjunction with the release of the MAS Monetary Policy Statement. The Review documents the Economic Policy Department’s (EPD) analyses and assessment of macroeconomic developments in the Singapore economy, and shares with market participants, analysts and the wider public the basis for the policy decisions conveyed in the Monetary Policy Statement. It also features results from some of the in‐depth studies undertaken by the department on various economic issues facing Singapore. The Review was edited by Associate Professor Peter Wilson. We are grateful to Professor Sam Ouliaris for his assistance and guidance with the empirical analysis on the exchange rate pass‐through in Singapore and Professor Andrew Rose for his contribution of Special Feature C. The data used in the Review were drawn from the following government agencies: BCA, CPF Board, DOS, EDB, IE Singapore, LTA, MOF, MOM, MTI, STB and URA. The Review may be accessed in PDF format on the MAS website: http://www.mas.gov.sg/publications/macro_review/index.html. The Review may also be purchased at major bookstores, online (http://asp.marketasia.com.sg/Spore/sporeindex.asp), or on an annual subscription basis (details on the last page).

ii Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

Highlights The global financial crisis has entered uncharted waters. What was referred to, a little more than a year ago, as a US subprime mortgage problem has since evolved into worldwide financial turmoil, requiring urgent stabilisation measures by governments in both developed and developing countries. The financial turbulence has caused risk aversion on a wider scale and, subsequently, a sharp squeeze on liquidity and credit. This will have significant repercussions for other areas of economic activity. The full magnitude of the crisis is yet unknown and the efficacy of mitigating policy responses remains to be seen. However, the balance of risks has increasingly shifted away from earlier fears of rising inflationary pressures to concerns over significantly weaker economic growth. As a small and open economy with strong linkages with the global economy and international financial markets, Singapore will not be immune to this turbulence. Indeed, the economy has already weakened over the course of this year. GDP growth slowed from 7.7% last year to 4.6% in the first half of 2008 and is estimated to have slipped to ‐0.5% y‐o‐y in the third quarter. Moreover, growth is expected to remain below trend in 2009. Meanwhile, CPI inflation appears to have peaked in tandem with the cooling economy and the moderation in global commodity prices. A detailed review of recent developments in the external environment and the Singapore economy can be found in Chapters 1 and 2. In commemoration of the 50th anniversary of the seminal article by A. W. Phillips, who first documented the empirical relationship between wage inflation and the level of unemployment, Box A revisits the “Phillips Curve” relationship and considers the lessons that can be learnt from it since the 1970s. Previously in the Review, we had explored the concept of a weak synchronicity between the Asian and G3 economies. In Chapter 3, we reconsider this issue and suggest that Asia’s initial insulation arising from the weak synchronicity of its business cycle with developed countries might wane in the coming months. We also set out a framework that identifies the transmission channels through which global financial and economic shocks can affect domestic economic activity. This supplements our earlier analysis which categorised the prospects for different sectors of the economy according to their vulnerability to a slowdown in US demand. Some of these spillovers have already been felt while others will take time to filter through the system. We conclude this chapter with EPD’s outlook for the labour market and inflation, which envisages a moderation in employment growth and a decline in underlying inflation alongside the narrowing of the output gap. Looking beyond the immediate cyclical stresses confronting the economy, this Review discusses longer‐term structural challenges for Singapore. Box C examines trends in the resident labour force participation rate, and identifies female and older‐age cohorts as presenting opportunities to augment future labour force growth. Box D presents EPD’s findings on the changing export market shares of seven East Asian economies over the last five years, and highlights the continuous process of upgrading to higher value added exports that is evident among the advanced economies in Asia, including Singapore, thus ensuring their continuing relevance in global markets. We also include in this Review three Special features. Special Feature A is an econometric analysis of the effect of Singapore’s monetary policy on prices. In particular, it documents the magnitude of the exchange rate impact on consumer price changes across the business cycle, as well as the time lags for the transmission to be completed. This is especially pertinent today as the economy transits from a period of sustained above‐trend growth amidst rising external inflationary pressures to one characterised by weaker economic growth and a diminution of inflationary pressures. We find evidence of asymmetric effects in the pricing behaviour of wholesalers and retailers. For example, retailers appear to pass on a greater amount of an import cost increase to consumers during an economic upturn, compared to other periods.

Highlights iii

Monetary Authority of Singapore Economic Policy Department

Special Feature B examines in some detail the effect of oil price shocks on growth and inflation outcomes in Singapore, where a number of industries from transport‐hub services to rig‐building and petrochemicals are tied to oil prices. We also document the decline in industries’ dependence on oil since 2001 and highlight the importance of identifying the source and duration of an oil price shock in order to ascertain its impact on the economy. Finally, the current financial crisis has put the spotlight on the importance of global interdependence and the need for international co‐operation. This Review concludes with a Special Feature by Professor Andrew Rose of the University of California, Berkeley, on how international environmental agreements can be more forthcoming and how they can strengthen economic linkages between countries. The next issue of the Review will be released in April 2009.

Economic Policy Department Monetary Authority of Singapore

28 October 2008

iv Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

10 October 2008

Monetary Policy Statement

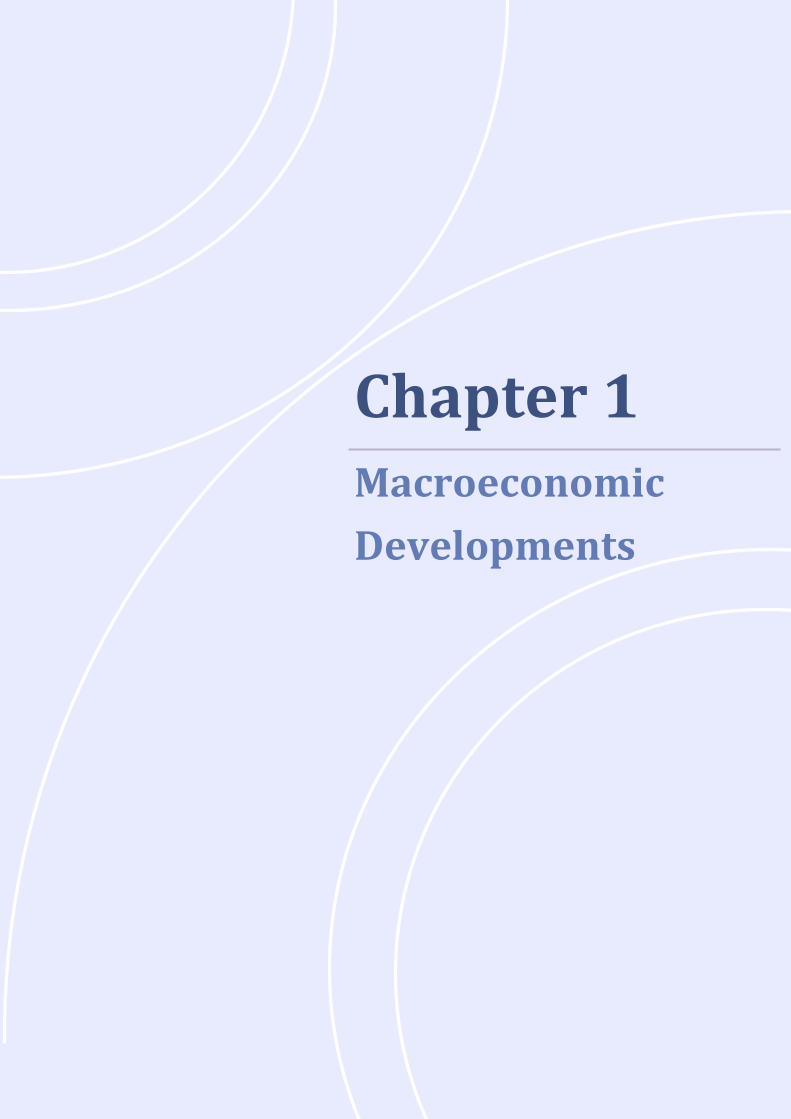

INTRODUCTION 1. MAS has maintained the policy of a modest and gradual appreciation of the Singapore dollar nominal effective exchange rate (S$NEER) policy band since April 2004. In October 2007, the policy was tightened through a slight increase in the slope of the band, following which the policy band was re‐centred at the then‐prevailing level of the S$NEER in April 2008. The policy stance has helped to mitigate inflationary pressures amidst sustained economic growth and rising global commodity prices.

Chart 1 S$ Nominal Effective Exchange Rate

Apr Jul Oct Jan Apr Jul Oct

96

98

100

102

104

106

Inde

x (5

Apr

200

7 =

100)

indicates release of Monetary Policy Statement

Appreciation

Depreciation

2007 2008

2. The S$NEER had fluctuated in the upper half of the policy band between April and July 2008, before easing since August against a broad‐based strengthening of the US$. (Chart 1) The pull‐back of the S$NEER also reflected heightened domestic growth concerns and a moderation of inflationary pressures. 3. Meanwhile, domestic interbank rates edged lower in tandem with the stronger S$ following the April monetary policy announcement. More recently, the strain in global money markets caused the domestic three‐month interbank rate to increase temporarily, but it has since eased to 1.88% at end‐September.

OUTLOOK FOR 2008 AND 2009 4. The Singapore economy has weakened over the course of 2008, alongside an escalation in the turmoil in financial markets and a more severe deceleration in global economic activity. The Advance Estimates released by the Ministry of Trade and Industry today show that Singapore’s GDP declined by

Monetary Policy Statement v

Monetary Authority of Singapore Economic Policy Department

6.3% on a quarter‐on‐quarter seasonally adjusted annualised basis in Q3 2008. On a year‐ago basis, activity also contracted mildly. The slowdown was generally broad based as external shocks were transmitted to the domestic economy via both the financial and trade channels. Nonetheless, certain industries, such as transport & storage, information & communications, and bank intermediation, continued to hold up, providing some support to GDP growth. 5. Looking ahead, the outlook for the global economy has deteriorated amidst heightened risk aversion and deleveraging in the financial sector. After a brief rebound in Q2 2008, economic conditions in the US have worsened as the effects of the fiscal stimulus package dissipated. The Japanese and Eurozone economies contracted in Q2 2008 and near‐term conditions remain difficult. Economies in Asia, including China and India, are also expected to slow. 6. These developments have presented new uncertainties for the Singapore economy. The risks to external demand conditions continue to be on the downside, and a more severe global downturn cannot be discounted. Slower growth in Asia will restrain activity in a range of services industries in Singapore such as transport‐hub and tourism. Against this less favourable environment, Singapore’s GDP growth forecast for 2008 has been revised from 4‐5% to around 3%. Economic growth will likely remain below its potential rate over the next few quarters. Prospects of a recovery in the latter half of 2009 will depend significantly on how conditions evolve in the G3 and regional economies. 7. CPI inflation has peaked, declining from 7.5% in Q2 2008 to 6.5% in July‐August on a year‐on‐year basis. In addition, it has fallen on a quarter‐on‐quarter basis, easing from 2.1% in Q1 to 1.4% in Q2 and 1.1% in July‐August. The sequential fall in CPI inflation reflects a moderation of both external and domestic price pressures. Externally, the recent sharp decline in commodity prices has helped to dampen global inflation. Domestically, the effects of past monetary policy tightening measures and the slowing economy have alleviated price pressures and eased resource constraints. Cost pressures have begun to recede, as evidenced by the recent fall in commercial rentals and more subdued wage increases. 8. CPI inflation is projected to come within the 6‐7% forecast range in 2008, while the MAS underlying inflation measure, which excludes accommodation and private road transport costs, is expected to be 5‐6%. Over the coming months and into early 2009, the headline inflation rate will continue to be impacted by the pass‐through of some earlier domestic cost increases. Nevertheless, CPI inflation is expected to trend down in 2009 as the global and domestic economies slow and for the year as a whole it is forecast to moderate to 2.5‐3.5%, with the MAS underlying inflation coming down to around 2%.

MONETARY POLICY 9. Against the backdrop of a weakening external economic environment and continuing stresses in global financial markets, the growth of the Singapore economy is expected to remain below potential in the period ahead. Concomitantly, external and domestic inflationary pressures are likely to ease. 10. MAS is therefore shifting its policy stance to a zero percent appreciation of the S$NEER policy band. This policy maintains the current level of the policy band, and there will be no re‐centring of the band or change to its width. MAS stands ready to intervene to dampen excessive volatility in the S$NEER should this become necessary. MAS will also continue to closely monitor developments in the external environment and their impact on the Singapore economy.

Chapter 1 Macroeconomic

Developments

2 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

1.1 External Developments Worsening Growth‐Inflation Dynamics The global economy faced challenging conditions

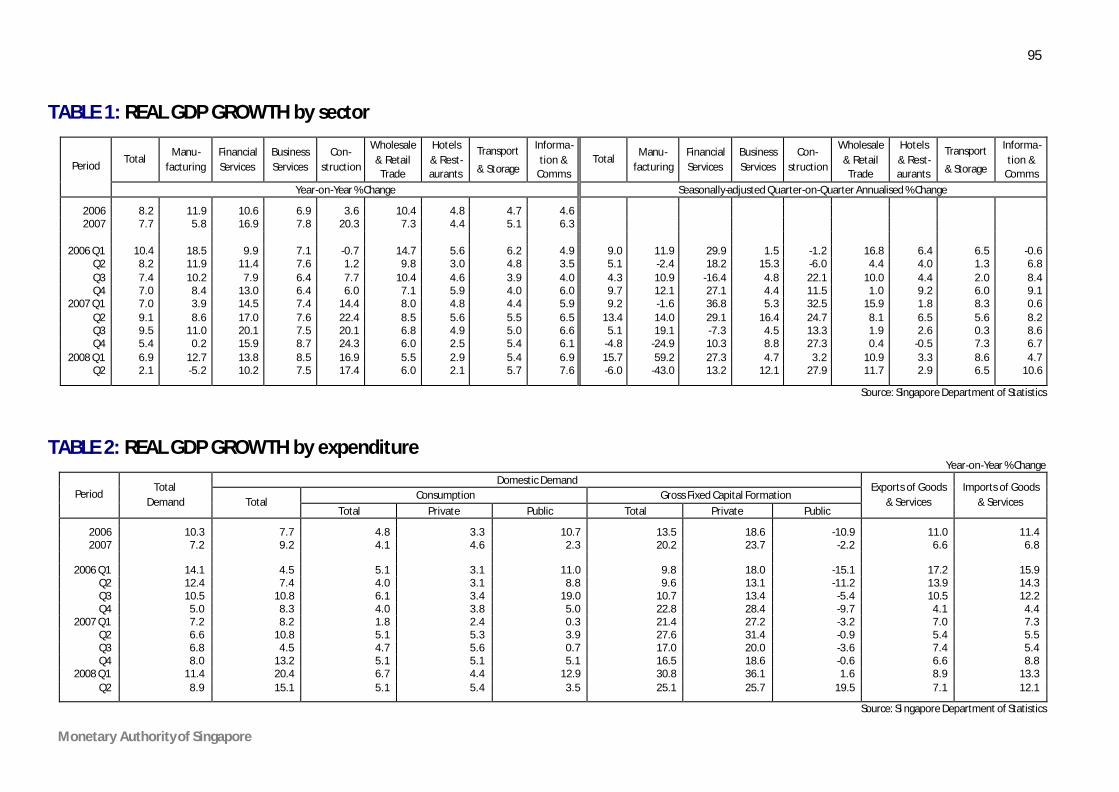

in H1 2008. The global economic environment proved challenging in the first half of 2008. The growth‐inflation mix in the G3 economies was particularly unfavourable, with growth turning down sharply and headline CPI inflation reaching multi‐year highs. (Charts 1.1 and 1.5) Box A on “The Phillips Curve Revisited” provides a historical perspective on the changing growth‐inflation dynamics that has confronted the global economy over the decades. In comparison, while headline CPI inflation in Asia ex‐Japan1 also surged, growth held up relatively well as domestic demand and exports to emerging markets helped to offset weaker demand from the G3 economies. Asia’s domestic demand was more robust, due in part to the healthier balance sheets of the banking, corporate and household sectors. These factors enabled Asia’s growth to become less synchronised with the business cycle in the G3 economies, at least in H1 this year. (Table 1.1)

Underlying US domestic demand was tepid in Q2 2008.

In the US, underlying domestic demand was tepid in Q2 2008, weighed down by the housing market correction, ongoing financial market turbulence and deteriorating labour market. Although growth picked up to 2.8% q‐o‐q SAAR in Q2 from 0.9% in Q1, this was primarily due to external demand and the one‐off government transfers to households. (Chart 1.2) Net exports contributed a significant 2.9% points to GDP growth, while fiscal disbursements to households boosted personal disposable income at an annualised rate of 17%, which temporarily lifted consumer spending. Even so, personal consumption growth only picked up slightly to 1.2% in Q2, compared with 0.9% in Q1 2008 and an average of 3.0% between Q1 2003 and Q4 2007.

Chart 1.1 G3 GDP Growth

2006 Q3 2007 Q3 2008 Q2-4

-2

0

2

4

6

QO

Q S

AA

R %

Gro

wth

Japan

USEurozone

G3*

Source: Datastream * Weighted by 2007 nominal GDP in US$, converted at the 2007 average exchange rate.

Table 1.1

GDP Growth y‐o‐y (%)

2008 2006 2007

Q1 Q2 Total* 5.0 5.0 5.0 4.2 Industrial Countries* 2.8 2.5 2.2 1.7 US 2.8 2.0 2.5 2.1 Eurozone 3.0 2.6 2.1 1.4 Japan 2.4 2.1 1.2 0.7

NIE‐3* 5.9 5.9 6.7 4.4 Hong Kong 7.0 6.4 7.3 4.2 Korea 5.1 5.0 5.8 4.8 Taiwan 4.9 5.7 6.3 4.3

ASEAN‐4* 5.5 6.1 6.5 6.0 Indonesia 5.5 6.3 6.3 6.4 Malaysia 5.8 6.3 7.1 6.3 Thailand 5.1 4.8 6.1 5.3 Philippines 5.4 7.2 4.7 4.6 China 11.6 11.9 10.6 10.1 India 9.8 9.3 8.8 7.9

Source: CEIC and Datastream * Weighted by shares in Singapore’s non‐oil domestic exports.

1 Asia ex‐Japan comprises ASEAN‐4 (Indonesia, Malaysia, the Philippines, Thailand), NIE‐3 (Hong Kong, South Korea,

Taiwan), China and India.

Macroeconomic Developments 3

Monetary Authority of Singapore Economic Policy Department

More recently, real consumer spending fell by an average of 2.9% m‐o‐m SAAR in July and August, as the effects of the tax rebates dissipated. Residential investment continued to decline at a double‐digit rate, as housing demand remained depressed.

Growth weakened sharply in the Eurozone and Japan …

In the Eurozone economies, growth momentum has decelerated significantly. Following a strong expansion of 2.7% q‐o‐q SAAR in Q1 2008, GDP growth in the Eurozone fell by 0.7% in Q2. This was the first contraction in nearly a decade, dragged down by slippage in Germany, France and Italy, the three largest economies in the Eurozone. The decline was across all the expenditure components of GDP except government consumption, as higher borrowing costs, rising inflation, housing market corrections and softening global demand dampened confidence and economic activity. The Japanese economy contracted by 3.0% q‐o‐q SAAR in Q2 2008, after two quarters of above 2% growth. In particular, private consumption fell at its sharpest rate in seven quarters, in tandem with the plunge in consumer confidence to its lowest point in 26 years. Corporate investment contracted at a more rapid pace in Q2 as firms continued to be constrained by falling profits and poor business sentiment. Exports, which supported growth throughout 2007 and Q1 2008, also registered their first decline in 13 quarters. … while Asia ex‐Japan remained relatively resilient. Asia ex‐Japan has been fairly resilient so far this year, with growth moderating only slightly from 7.4% y‐o‐y in Q1 2008 to 6.4% in Q2. The slowdown was more pronounced in the Northeast Asian economies of Hong Kong, Korea and Taiwan, where household and fixed investment spending growth slowed from 3.5% in Q1 to 1.0% in Q2 due to the global financial turmoil and surging inflation. (Chart 1.3) However, domestic demand growth in the resource‐rich Southeast Asian economies, especially Malaysia and Indonesia, held up well at 4.5% in Q2, reflecting the positive terms of trade shock from high commodity prices, such as for crude petroleum, palm oil and rice. (Chart 1.4) China also continued to power ahead, with growth reaching 10.4% in H1 2008, before moderating somewhat to 9.0% in Q3. The buoyant Chinese economy acted as a catalyst

Chart 1.2 Contribution to US GDP Growth

2006 Q3 2007 Q3 2008-4

0

4

8

GD

P Q

OQ

SA

AR

Gro

wth

% P

oint

Con

trib

utio

n to

-4

0

4

8

-4

QO

Q S

AA

R %

Gro

wth

Personal Consumption ExpendituresBusiness SpendingResidential Investments

Change in InventoriesNet ExportsGovernmentGDP (RHS)

Q2 Source: Bureau of Economic Analysis

Chart 1.3 Contribution to NIE‐3 GDP Growth

2006 Q3 2007 Q3 2008-2

0

2

4

6

8G

DP

YOY

Gro

wth

% P

oint

Con

trib

utio

n to

4.0

4.5

5.0

5.5

6.0

6.5

YOY

% G

row

th

OthersInvestment

Private Consumption

Govt Consumption

Net Exports

GDP Growth (RHS)

Q2

Source: CEIC

Chart 1.4 Contribution to ASEAN‐4 GDP Growth

2006 Q3 2007 Q3 2008-3

0

3

6

9

GD

P YO

Y G

row

th%

Poi

nt C

ontr

ibut

ion

to

5.2

5.6

6.0

6.4

6.8

YOY

% G

row

th

Q2

OthersInvestment

Private Consumption

Govt Consumption

Net Exports

GDP Growth (RHS)

Source: CEIC

4 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

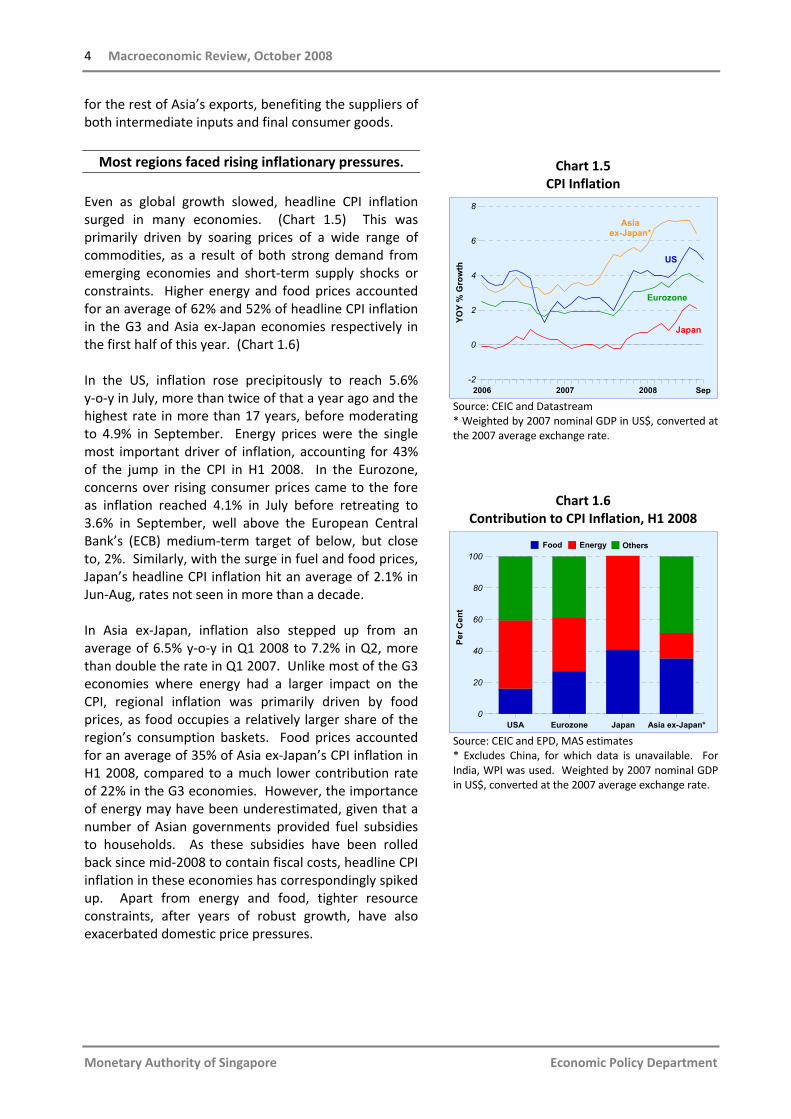

for the rest of Asia’s exports, benefiting the suppliers of both intermediate inputs and final consumer goods. Most regions faced rising inflationary pressures.

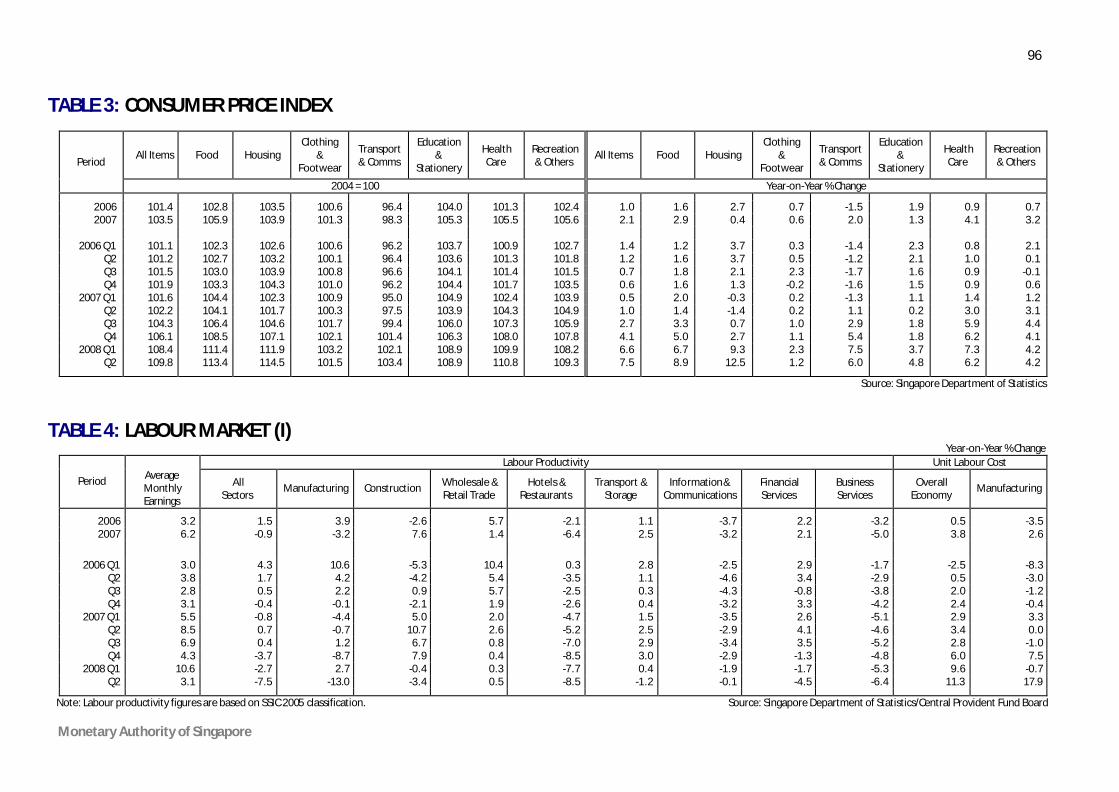

Even as global growth slowed, headline CPI inflation surged in many economies. (Chart 1.5) This was primarily driven by soaring prices of a wide range of commodities, as a result of both strong demand from emerging economies and short‐term supply shocks or constraints. Higher energy and food prices accounted for an average of 62% and 52% of headline CPI inflation in the G3 and Asia ex‐Japan economies respectively in the first half of this year. (Chart 1.6) In the US, inflation rose precipitously to reach 5.6% y‐o‐y in July, more than twice of that a year ago and the highest rate in more than 17 years, before moderating to 4.9% in September. Energy prices were the single most important driver of inflation, accounting for 43% of the jump in the CPI in H1 2008. In the Eurozone, concerns over rising consumer prices came to the fore as inflation reached 4.1% in July before retreating to 3.6% in September, well above the European Central Bank’s (ECB) medium‐term target of below, but close to, 2%. Similarly, with the surge in fuel and food prices, Japan’s headline CPI inflation hit an average of 2.1% in Jun‐Aug, rates not seen in more than a decade. In Asia ex‐Japan, inflation also stepped up from an average of 6.5% y‐o‐y in Q1 2008 to 7.2% in Q2, more than double the rate in Q1 2007. Unlike most of the G3 economies where energy had a larger impact on the CPI, regional inflation was primarily driven by food prices, as food occupies a relatively larger share of the region’s consumption baskets. Food prices accounted for an average of 35% of Asia ex‐Japan’s CPI inflation in H1 2008, compared to a much lower contribution rate of 22% in the G3 economies. However, the importance of energy may have been underestimated, given that a number of Asian governments provided fuel subsidies to households. As these subsidies have been rolled back since mid‐2008 to contain fiscal costs, headline CPI inflation in these economies has correspondingly spiked up. Apart from energy and food, tighter resource constraints, after years of robust growth, have also exacerbated domestic price pressures.

Chart 1.5 CPI Inflation

2006 2007 2008 Sep-2

0

2

4

6

8

YOY

% G

row

th

Japan

US

Eurozone

Asia ex-Japan*

Source: CEIC and Datastream * Weighted by 2007 nominal GDP in US$, converted at the 2007 average exchange rate.

Chart 1.6 Contribution to CPI Inflation, H1 2008

USA Eurozone Japan Asia ex-Japan*0

20

40

60

80

100

Per C

ent

OthersFood Energy

Source: CEIC and EPD, MAS estimates * Excludes China, for which data is unavailable. For India, WPI was used. Weighted by 2007 nominal GDP in US$, converted at the 2007 average exchange rate.

Macroeconomic Developments 5

Monetary Authority of Singapore Economic Policy Department

Box A The Phillips Curve Revisited

This year marks the 50th anniversary of the seminal article in Economica by the New Zealand‐born economist A. W. Phillips, who first documented the empirical relationship between the level of unemployment and the rate of change of money wage rates, or wage inflation. This box explores how the Phillips curve can be used to interpret economic developments over the decades since the 1970s. The Phillips curve in its original form showed an inverse relationship between the rate of unemployment and the rate of wage increases for the UK economy between 1861 and 1913. (Chart A1) It seemed to suggest that unemployment and inflation were linked in a systematic way that economists had not previously appreciated, and offered the tantalising possibility of a trade‐off over time between unemployment and price inflation, provided that productivity change was held constant and import price rises were not excessive. Years with low unemployment tended to have higher inflation, and years with high unemployment tended to have lower inflation.1/

Chart A1 The Phillips Curve for the UK, 1861‐1913

0 1 2 3 4 5

UK Unemployment Rate (%)

-3

0

3

6

9

12

UK

Wag

e In

flatio

n (%

)

Following Phillips’ 1958 paper, other economists such as Paul Samuelson and Robert Solow also found the same relationship for other countries, especially the US. They believed, incorrectly as it turned out, that there was a stable relationship between inflation and unemployment, such that the Phillips curve offered policymakers a “menu of choice” in terms of macroeconomic outcomes. By using monetary and fiscal policy to influence aggregate demand, policymakers could choose to move the economy to any point on the curve and read off the corresponding inflation and unemployment rates. For example, if the current rate of unemployment was deemed to be too high, policymakers could adopt expansionary fiscal and monetary policies to move to where the unemployment rate was lower but would be obliged to accept a higher rate of inflation as the trade‐off. The Great Inflation The misguided perception of a stable trade‐off between growth and inflation led many governments in the 1960s and 1970s to pursue overly expansionary monetary and fiscal policies to reduce unemployment, which resulted in persistently high inflation over that period. Sustained fiscal deficits also contributed to excessive aggregate demand pressures. Meltzer (2005) noted that “Neglecting or ignoring the effects of policy actions (i.e. fiscal deficits) on money growth or inflation was a major error in the 1960s and 1970s”. Policymakers at that time also thought that inflation could be reined in by wage‐price controls, under the

1/ Subsequent work on the Phillips curve replaced the unemployment rate with the output gap, but the inferences

remain the same.

6 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

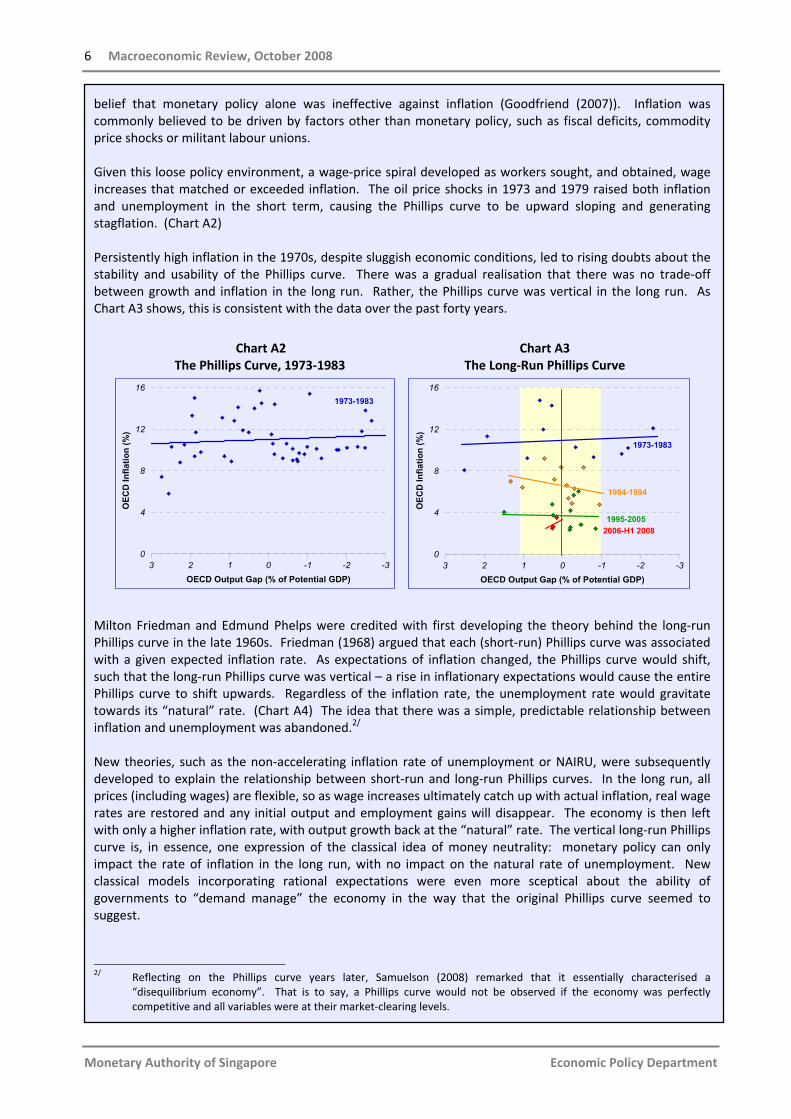

belief that monetary policy alone was ineffective against inflation (Goodfriend (2007)). Inflation was commonly believed to be driven by factors other than monetary policy, such as fiscal deficits, commodity price shocks or militant labour unions. Given this loose policy environment, a wage‐price spiral developed as workers sought, and obtained, wage increases that matched or exceeded inflation. The oil price shocks in 1973 and 1979 raised both inflation and unemployment in the short term, causing the Phillips curve to be upward sloping and generating stagflation. (Chart A2) Persistently high inflation in the 1970s, despite sluggish economic conditions, led to rising doubts about the stability and usability of the Phillips curve. There was a gradual realisation that there was no trade‐off between growth and inflation in the long run. Rather, the Phillips curve was vertical in the long run. As Chart A3 shows, this is consistent with the data over the past forty years.

Chart A2

The Phillips Curve, 1973‐1983 Chart A3

The Long‐Run Phillips Curve

-3-2-10123OECD Output Gap (% of Potential GDP)

0

4

8

12

16

OEC

D In

flatio

n (%

)

-3-2-10123OECD Output Gap (% of Potential GDP)

0

4

8

12

16

OEC

D In

flatio

n (%

)

1973-1983

1973-1983

2006-H1 20081995-2005

1984-1994

Milton Friedman and Edmund Phelps were credited with first developing the theory behind the long‐run Phillips curve in the late 1960s. Friedman (1968) argued that each (short‐run) Phillips curve was associated with a given expected inflation rate. As expectations of inflation changed, the Phillips curve would shift, such that the long‐run Phillips curve was vertical – a rise in inflationary expectations would cause the entire Phillips curve to shift upwards. Regardless of the inflation rate, the unemployment rate would gravitate towards its “natural” rate. (Chart A4) The idea that there was a simple, predictable relationship between inflation and unemployment was abandoned.2/

New theories, such as the non‐accelerating inflation rate of unemployment or NAIRU, were subsequently developed to explain the relationship between short‐run and long‐run Phillips curves. In the long run, all prices (including wages) are flexible, so as wage increases ultimately catch up with actual inflation, real wage rates are restored and any initial output and employment gains will disappear. The economy is then left with only a higher inflation rate, with output growth back at the “natural” rate. The vertical long‐run Phillips curve is, in essence, one expression of the classical idea of money neutrality: monetary policy can only impact the rate of inflation in the long run, with no impact on the natural rate of unemployment. New classical models incorporating rational expectations were even more sceptical about the ability of governments to “demand manage” the economy in the way that the original Phillips curve seemed to suggest.

2/ Reflecting on the Phillips curve years later, Samuelson (2008) remarked that it essentially characterised a

“disequilibrium economy”. That is to say, a Phillips curve would not be observed if the economy was perfectly competitive and all variables were at their market‐clearing levels.

Macroeconomic Developments 7

Monetary Authority of Singapore Economic Policy Department

Chart A4 The Stylised Long‐run Phillips Curve

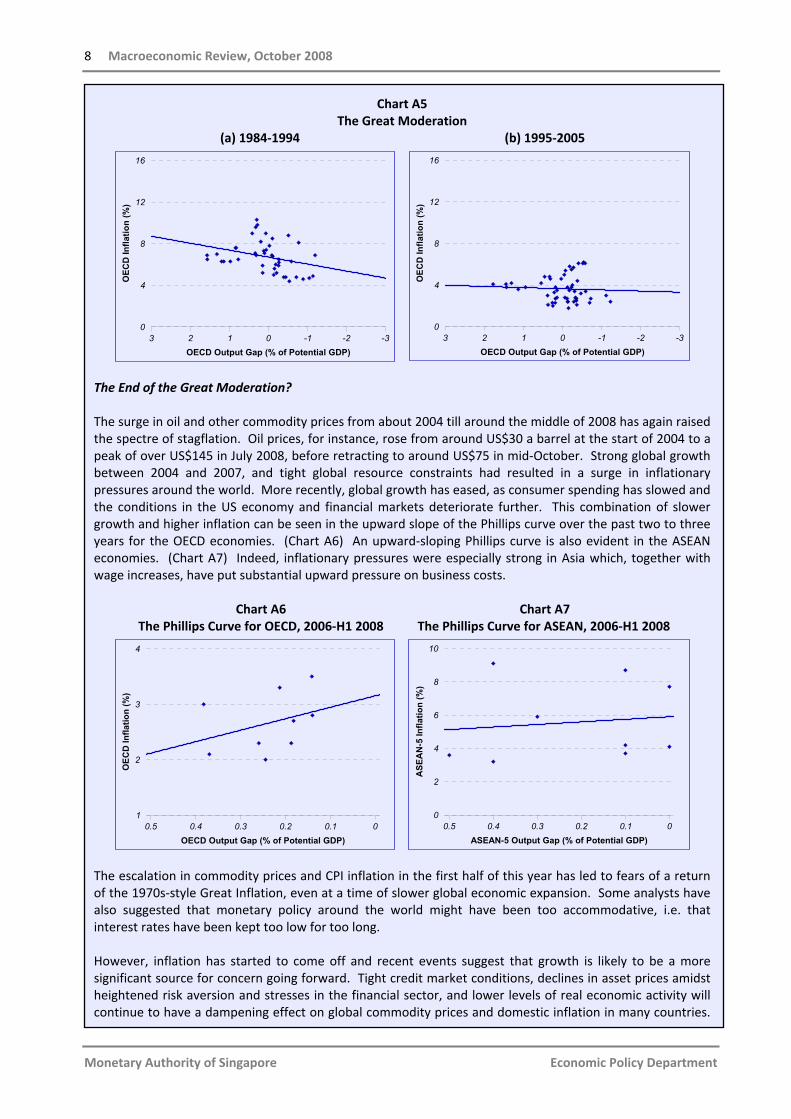

The Great Moderation Following the disappointment over the performance of the US economy in the 1970s (low growth and high inflation), then‐Fed Chairman Paul Volcker decided in October 1979 to impose very tight control over the money supply in an attempt to bring down inflation and inflationary expectations in the US. Volcker’s resolve – in the face of strong political pressure – was crucial in breaking the back of the high inflation psychology. The Fed funds rate rose to almost 20% in 1981 and the unemployment rate soared to 11% at the end of 1982. At the same time, many other OECD countries, such as the UK, also came round to the view that there was no long‐term trade‐off between growth and inflation and that tight monetary policy was necessary to reverse inflationary expectations. As inflation moderated, the Phillips curve edged down and became downward sloping again. The Great Moderation that followed was characterised by a substantial reduction in the variability of both output and inflation. Some studies have suggested that the variability of quarterly real GDP growth has declined by half since the mid‐1980s, while the variability of quarterly inflation has declined by about two‐thirds (see for example, Blanchard and Simon (2001)). Romer and Romer (2002) noted that aggregate demand policy during this period became “more temperate” and once again committed to low inflation. They contended that “the fundamental source of changes in policy has been changes in policymakers’ beliefs in how the economy functions”. Bernanke (2004) argued that “improved monetary policy has likely made an important contribution not only to the reduced volatility of inflation (which is not particularly controversial) but to the reduced volatility of output as well”. At the global level, other factors also contributed to the Great Moderation. Worldwide import tariff reductions and the emergence of China as a low‐cost “factory of the world” helped to keep goods prices down. At the same time, IT advances contributed to higher productivity growth, while the increased depth and sophistication of financial markets and more efficient inventory management techniques, made possible by advances in IT and communications technology, improved macroeconomic performance. The result was a period of sustained strong growth without escalating inflation, or what Bank of England Governor Mervyn King (2003) called a NICE – Non‐Inflationary Consistently Expansionary – period. Beginning in the mid‐1980s, the Great Moderation marked a golden age for the OECD in terms of sustained economic growth with low inflation. (Charts A5a and A5b) The power of the trade unions was weakened, commodity price inflation was subdued and inflationary expectations stabilised at lower levels. Globalisation in trade, investment and capital flows also proceeded at a rapid pace during this period. Samuelson (2008) noted that the US economy became “virtually a Say’s Law economy” in that a cowed US labour force – under threat from foreign lower‐wage, productive workers – had to accept jobs with lower real wages.

Long-run Phillips curve

InflationRate

UnemploymentRate

Natural rate ofunemployment

0

Lowinflation

Highinflation

8 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

Chart A5 The Great Moderation

(a) 1984‐1994 (b) 1995‐2005

-3-2-10123OECD Output Gap (% of Potential GDP)

0

4

8

12

16

OEC

D In

flatio

n (%

)

-3-2-10123OECD Output Gap (% of Potential GDP)

0

4

8

12

16

OEC

D In

flatio

n (%

)

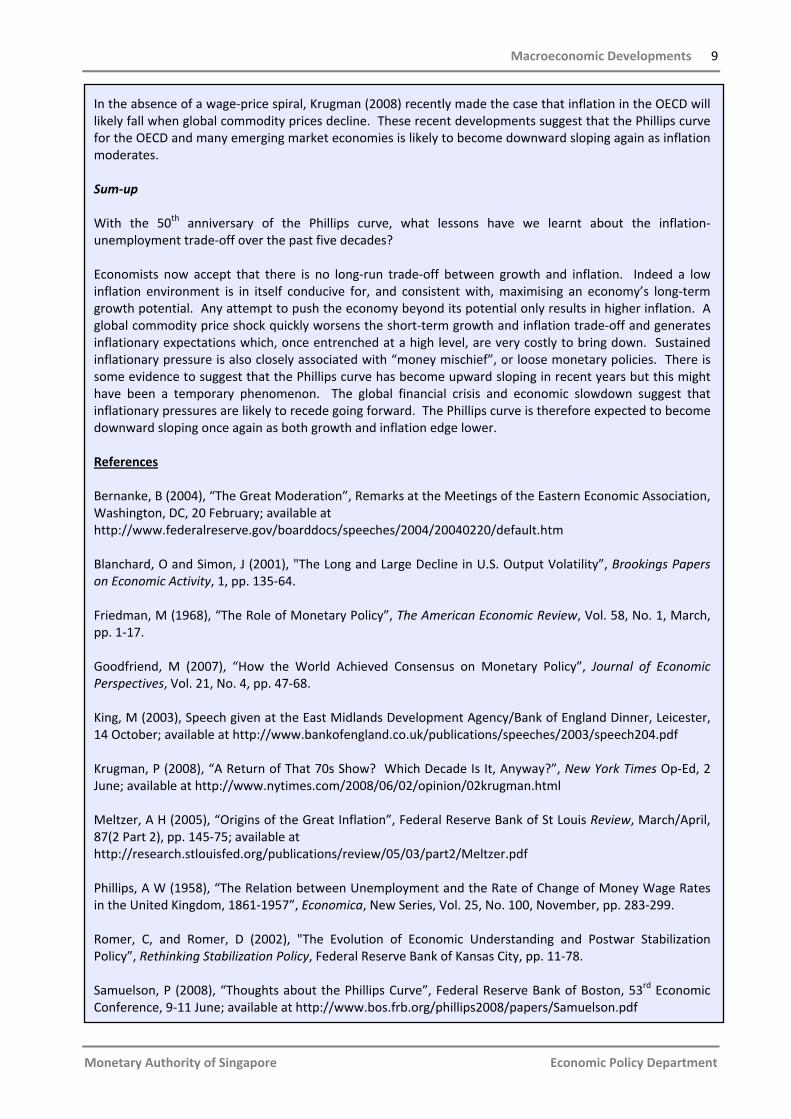

The End of the Great Moderation? The surge in oil and other commodity prices from about 2004 till around the middle of 2008 has again raised the spectre of stagflation. Oil prices, for instance, rose from around US$30 a barrel at the start of 2004 to a peak of over US$145 in July 2008, before retracting to around US$75 in mid‐October. Strong global growth between 2004 and 2007, and tight global resource constraints had resulted in a surge in inflationary pressures around the world. More recently, global growth has eased, as consumer spending has slowed and the conditions in the US economy and financial markets deteriorate further. This combination of slower growth and higher inflation can be seen in the upward slope of the Phillips curve over the past two to three years for the OECD economies. (Chart A6) An upward‐sloping Phillips curve is also evident in the ASEAN economies. (Chart A7) Indeed, inflationary pressures were especially strong in Asia which, together with wage increases, have put substantial upward pressure on business costs.

Chart A6 The Phillips Curve for OECD, 2006‐H1 2008

Chart A7 The Phillips Curve for ASEAN, 2006‐H1 2008

00.10.20.30.40.5OECD Output Gap (% of Potential GDP)

1

2

3

4

OEC

D In

flatio

n (%

)

00.10.20.30.40.5ASEAN-5 Output Gap (% of Potential GDP)

0

2

4

6

8

10

ASE

AN

-5 In

flatio

n (%

)

The escalation in commodity prices and CPI inflation in the first half of this year has led to fears of a return of the 1970s‐style Great Inflation, even at a time of slower global economic expansion. Some analysts have also suggested that monetary policy around the world might have been too accommodative, i.e. that interest rates have been kept too low for too long. However, inflation has started to come off and recent events suggest that growth is likely to be a more significant source for concern going forward. Tight credit market conditions, declines in asset prices amidst heightened risk aversion and stresses in the financial sector, and lower levels of real economic activity will continue to have a dampening effect on global commodity prices and domestic inflation in many countries.

Macroeconomic Developments 9

Monetary Authority of Singapore Economic Policy Department

In the absence of a wage‐price spiral, Krugman (2008) recently made the case that inflation in the OECD will likely fall when global commodity prices decline. These recent developments suggest that the Phillips curve for the OECD and many emerging market economies is likely to become downward sloping again as inflation moderates. Sum‐up With the 50th anniversary of the Phillips curve, what lessons have we learnt about the inflation‐unemployment trade‐off over the past five decades? Economists now accept that there is no long‐run trade‐off between growth and inflation. Indeed a low inflation environment is in itself conducive for, and consistent with, maximising an economy’s long‐term growth potential. Any attempt to push the economy beyond its potential only results in higher inflation. A global commodity price shock quickly worsens the short‐term growth and inflation trade‐off and generates inflationary expectations which, once entrenched at a high level, are very costly to bring down. Sustained inflationary pressure is also closely associated with “money mischief”, or loose monetary policies. There is some evidence to suggest that the Phillips curve has become upward sloping in recent years but this might have been a temporary phenomenon. The global financial crisis and economic slowdown suggest that inflationary pressures are likely to recede going forward. The Phillips curve is therefore expected to become downward sloping once again as both growth and inflation edge lower. References Bernanke, B (2004), “The Great Moderation”, Remarks at the Meetings of the Eastern Economic Association, Washington, DC, 20 February; available at http://www.federalreserve.gov/boarddocs/speeches/2004/20040220/default.htm Blanchard, O and Simon, J (2001), "The Long and Large Decline in U.S. Output Volatility”, Brookings Papers on Economic Activity, 1, pp. 135‐64. Friedman, M (1968), “The Role of Monetary Policy”, The American Economic Review, Vol. 58, No. 1, March, pp. 1‐17. Goodfriend, M (2007), “How the World Achieved Consensus on Monetary Policy”, Journal of Economic Perspectives, Vol. 21, No. 4, pp. 47‐68. King, M (2003), Speech given at the East Midlands Development Agency/Bank of England Dinner, Leicester, 14 October; available at http://www.bankofengland.co.uk/publications/speeches/2003/speech204.pdf Krugman, P (2008), “A Return of That 70s Show? Which Decade Is It, Anyway?”, New York Times Op‐Ed, 2 June; available at http://www.nytimes.com/2008/06/02/opinion/02krugman.html Meltzer, A H (2005), “Origins of the Great Inflation”, Federal Reserve Bank of St Louis Review, March/April, 87(2 Part 2), pp. 145‐75; available at http://research.stlouisfed.org/publications/review/05/03/part2/Meltzer.pdf Phillips, A W (1958), “The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861‐1957”, Economica, New Series, Vol. 25, No. 100, November, pp. 283‐299. Romer, C, and Romer, D (2002), "The Evolution of Economic Understanding and Postwar Stabilization Policy”, Rethinking Stabilization Policy, Federal Reserve Bank of Kansas City, pp. 11‐78. Samuelson, P (2008), “Thoughts about the Phillips Curve”, Federal Reserve Bank of Boston, 53rd Economic Conference, 9‐11 June; available at http://www.bos.frb.org/phillips2008/papers/Samuelson.pdf

10 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

1.2 Domestic Economy Cold Currents Hit the Economy

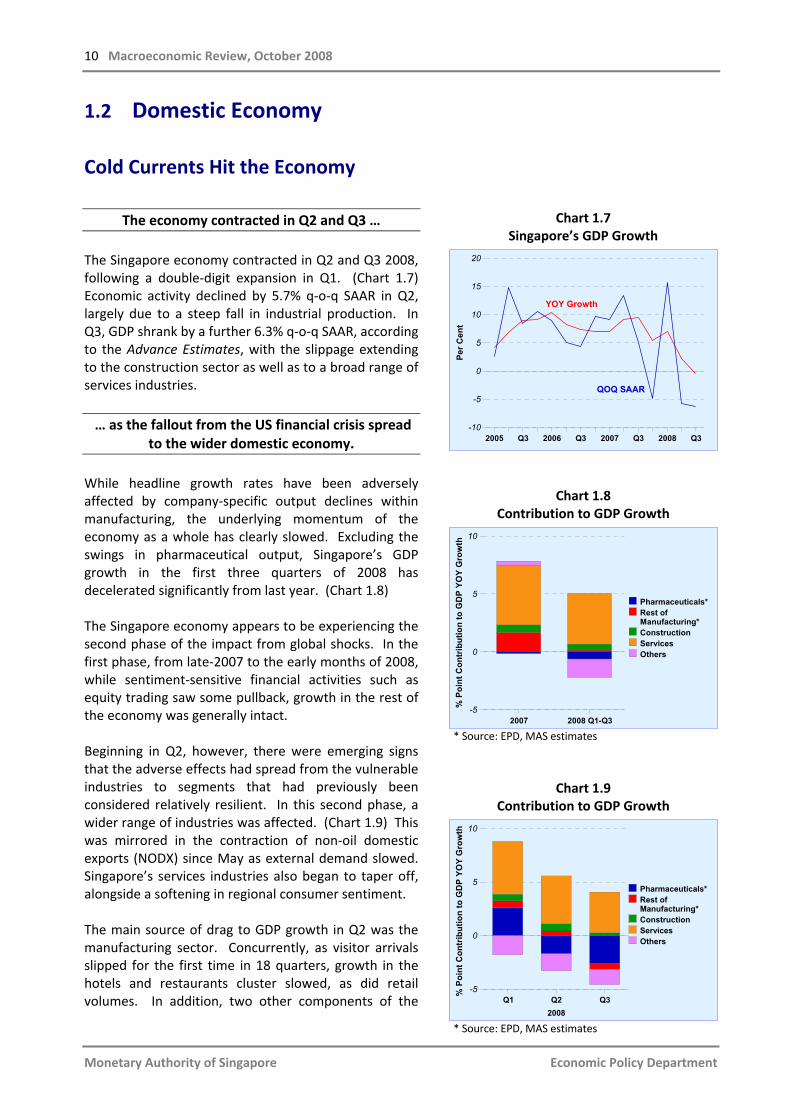

The economy contracted in Q2 and Q3 … The Singapore economy contracted in Q2 and Q3 2008, following a double‐digit expansion in Q1. (Chart 1.7) Economic activity declined by 5.7% q‐o‐q SAAR in Q2, largely due to a steep fall in industrial production. In Q3, GDP shrank by a further 6.3% q‐o‐q SAAR, according to the Advance Estimates, with the slippage extending to the construction sector as well as to a broad range of services industries. … as the fallout from the US financial crisis spread

to the wider domestic economy. While headline growth rates have been adversely affected by company‐specific output declines within manufacturing, the underlying momentum of the economy as a whole has clearly slowed. Excluding the swings in pharmaceutical output, Singapore’s GDP growth in the first three quarters of 2008 has decelerated significantly from last year. (Chart 1.8) The Singapore economy appears to be experiencing the second phase of the impact from global shocks. In the first phase, from late‐2007 to the early months of 2008, while sentiment‐sensitive financial activities such as equity trading saw some pullback, growth in the rest of the economy was generally intact. Beginning in Q2, however, there were emerging signs that the adverse effects had spread from the vulnerable industries to segments that had previously been considered relatively resilient. In this second phase, a wider range of industries was affected. (Chart 1.9) This was mirrored in the contraction of non‐oil domestic exports (NODX) since May as external demand slowed. Singapore’s services industries also began to taper off, alongside a softening in regional consumer sentiment. The main source of drag to GDP growth in Q2 was the manufacturing sector. Concurrently, as visitor arrivals slipped for the first time in 18 quarters, growth in the hotels and restaurants cluster slowed, as did retail volumes. In addition, two other components of the

Chart 1.7 Singapore’s GDP Growth

2005 Q3 2006 Q3 2007 Q3 2008 Q3-10

-5

0

5

10

15

20

Per C

ent

YOY Growth

QOQ SAAR

Chart 1.8 Contribution to GDP Growth

2007 2008 Q1-Q3-5

0

5

10

% P

oint

Con

trib

utio

n to

GD

P YO

Y G

row

th

Pharmaceuticals*Rest ofManufacturing*ConstructionServicesOthers

* Source: EPD, MAS estimates

Chart 1.9 Contribution to GDP Growth

Q1 Q2 Q32008

-5

0

5

10

% P

oint

Con

trib

utio

n to

GD

P YO

Y G

row

th

Pharmaceuticals*Rest ofManufacturing*ConstructionServicesOthers

* Source: EPD, MAS estimates

Macroeconomic Developments 11

Monetary Authority of Singapore Economic Policy Department

national accounts, namely taxes on products and financial intermediation services indirectly measured (FISIM) contributed negatively to overall growth. The financial services sector as a whole, however, exhibited unexpected resilience in Q2 in spite of poor sentiment in the financial markets. Manufacturing was weighed down by a range of

cyclical and industry‐specific factors … Manufacturing output contracted by 49% q‐o‐q SAAR in Q2, buffeted by company and industry‐specific factors, as well as cyclical pressures. The slump in manufacturing was attributed to sharp reversals in the biomedical and electronics clusters following strong expansions in Q1. (Chart 1.10) In particular, pharmaceutical production plunged by 92% q‐o‐q SAAR in Q2, due in part to a temporary switch in the product mix to lower value added active pharmaceutical ingredients (API). Other industry‐specific factors also contributed to the decline in pharmaceutical output. Specifically, plant capacity was utilised for the production of intermediate output, which is recorded as manufacturing output only when converted into the full API. Similarly, clinical and validation trials – for drugs planned for production in 2009 – took up capacity at plant facilities but did not contribute to manufacturing output. Competition from cheaper generic products, a phenomenon faced by the global drug industry, also took a bite out of pharmaceutical production in Q2. The manufacturing sector was further weakened by a contraction in electronics output, which fell by 25% in Q2. (Chart 1.11) This was caused by company‐specific factors in the infocomms & consumer electronics segment, namely the winding down of production at Motorola’s handset plant in Singapore. The closure of Motorola’s handset plant also adversely affected some of the domestic contract manufacturers in the PC peripherals segment. The semiconductor segment suffered its second consecutive quarter of decline, alongside a cyclical crunch in the global IT industry. As components of electronics end‐products, semiconductors tend to be the first to feel the squeeze from weak end demand. Moreover, the domestic semiconductor segment has

Chart 1.10 Contribution to Manufacturing

Output Growth

2008 Q1 2008 Q2-60

-30

0

30

60

90

Out

put Q

OQ

SA

AR

Gro

wth

% P

oint

Con

trib

utio

n to

Man

ufac

turin

g

TransportEngineeringChemicalsGeneralManufacturingIndustriesPrecisionEngineeringElectronicsBiomedical

Chart 1.11 Contribution to Electronics Output Growth

2008 Q1 2008 Q2-30

-20

-10

0

10

20

30

Out

put Q

OQ

SA

AR

Gro

wth

% P

oint

Con

trib

utio

n to

Ele

ctro

nics

SemiconductorsComputerPeripheralsData StorageInfocomms &ConsumerElectronicsOther Electronics

12 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

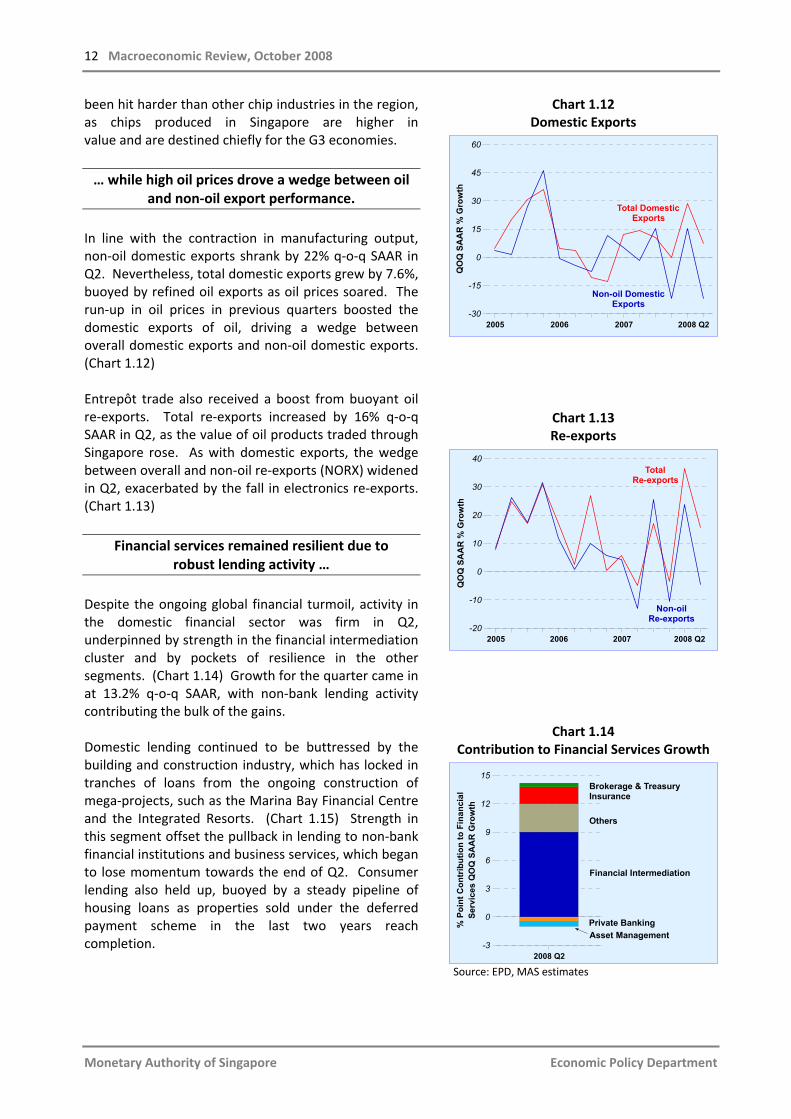

been hit harder than other chip industries in the region, as chips produced in Singapore are higher in value and are destined chiefly for the G3 economies. … while high oil prices drove a wedge between oil

and non‐oil export performance. In line with the contraction in manufacturing output, non‐oil domestic exports shrank by 22% q‐o‐q SAAR in Q2. Nevertheless, total domestic exports grew by 7.6%, buoyed by refined oil exports as oil prices soared. The run‐up in oil prices in previous quarters boosted the domestic exports of oil, driving a wedge between overall domestic exports and non‐oil domestic exports. (Chart 1.12) Entrepôt trade also received a boost from buoyant oil re‐exports. Total re‐exports increased by 16% q‐o‐q SAAR in Q2, as the value of oil products traded through Singapore rose. As with domestic exports, the wedge between overall and non‐oil re‐exports (NORX) widened in Q2, exacerbated by the fall in electronics re‐exports. (Chart 1.13)

Financial services remained resilient due to robust lending activity …

Despite the ongoing global financial turmoil, activity in the domestic financial sector was firm in Q2, underpinned by strength in the financial intermediation cluster and by pockets of resilience in the other segments. (Chart 1.14) Growth for the quarter came in at 13.2% q‐o‐q SAAR, with non‐bank lending activity contributing the bulk of the gains. Domestic lending continued to be buttressed by the building and construction industry, which has locked in tranches of loans from the ongoing construction of mega‐projects, such as the Marina Bay Financial Centre and the Integrated Resorts. (Chart 1.15) Strength in this segment offset the pullback in lending to non‐bank financial institutions and business services, which began to lose momentum towards the end of Q2. Consumer lending also held up, buoyed by a steady pipeline of housing loans as properties sold under the deferred payment scheme in the last two years reach completion.

Chart 1.12 Domestic Exports

2005 2006 2007 2008 Q2-30

-15

0

15

30

45

60

QO

Q S

AA

R %

Gro

wth

Total Domestic Exports

Non-oil Domestic Exports

Chart 1.13 Re‐exports

2005 2006 2007 2008 Q2-20

-10

0

10

20

30

40Q

OQ

SA

AR

% G

row

thTotal

Re-exports

Non-oil Re-exports

Chart 1.14 Contribution to Financial Services Growth

2008 Q2-3

0

3

6

9

12

15

Serv

ices

QO

Q S

AA

R G

row

th%

Poi

nt C

ontr

ibut

ion

to F

inan

cial Insurance

Financial Intermediation

Brokerage & Treasury

Asset ManagementPrivate Banking

Others

Source: EPD, MAS estimates

Macroeconomic Developments 13

Monetary Authority of Singapore Economic Policy Department

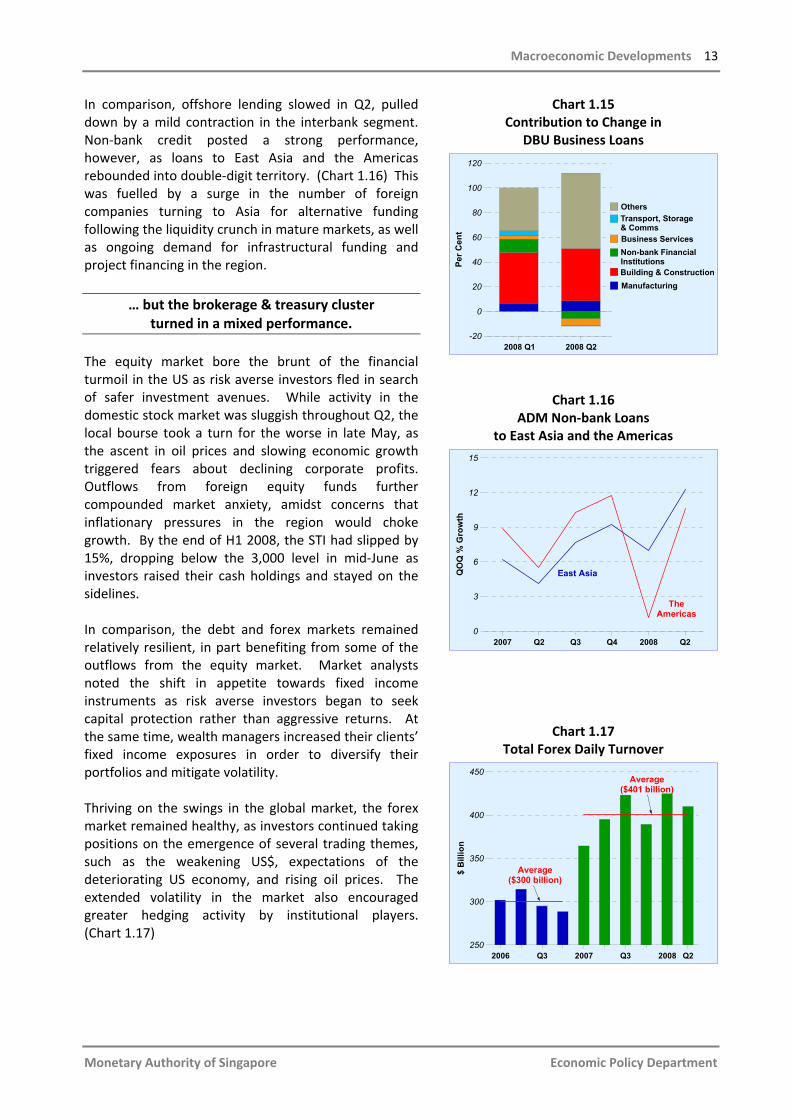

In comparison, offshore lending slowed in Q2, pulled down by a mild contraction in the interbank segment. Non‐bank credit posted a strong performance, however, as loans to East Asia and the Americas rebounded into double‐digit territory. (Chart 1.16) This was fuelled by a surge in the number of foreign companies turning to Asia for alternative funding following the liquidity crunch in mature markets, as well as ongoing demand for infrastructural funding and project financing in the region.

… but the brokerage & treasury cluster turned in a mixed performance.

The equity market bore the brunt of the financial turmoil in the US as risk averse investors fled in search of safer investment avenues. While activity in the domestic stock market was sluggish throughout Q2, the local bourse took a turn for the worse in late May, as the ascent in oil prices and slowing economic growth triggered fears about declining corporate profits. Outflows from foreign equity funds further compounded market anxiety, amidst concerns that inflationary pressures in the region would choke growth. By the end of H1 2008, the STI had slipped by 15%, dropping below the 3,000 level in mid‐June as investors raised their cash holdings and stayed on the sidelines. In comparison, the debt and forex markets remained relatively resilient, in part benefiting from some of the outflows from the equity market. Market analysts noted the shift in appetite towards fixed income instruments as risk averse investors began to seek capital protection rather than aggressive returns. At the same time, wealth managers increased their clients’ fixed income exposures in order to diversify their portfolios and mitigate volatility. Thriving on the swings in the global market, the forex market remained healthy, as investors continued taking positions on the emergence of several trading themes, such as the weakening US$, expectations of the deteriorating US economy, and rising oil prices. The extended volatility in the market also encouraged greater hedging activity by institutional players. (Chart 1.17)

Chart 1.15 Contribution to Change in

DBU Business Loans

2008 Q1 2008 Q2-20

0

20

40

60

80

100

120

Per C

ent

Transport, Storage& CommsBusiness ServicesNon-bank Financial Institutions

ManufacturingBuilding & Construction

Others

Chart 1.16 ADM Non‐bank Loans

to East Asia and the Americas

2007 Q2 Q3 Q4 2008 Q20

3

6

9

12

15Q

OQ

% G

row

th

The Americas

East Asia

Chart 1.17 Total Forex Daily Turnover

2006 Q3 2007 Q3 2008 Q2250

300

350

400

450

$ B

illio

n

Average($300 billion)

Average($401 billion)

14 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

Growth of services was subdued on softer regional demand.

Meanwhile, certain regional‐oriented industries softened towards the end of Q2 2008. Hospitality‐related sectors were hit as visitor arrivals declined by 0.7% y‐o‐y in Q2, the first quarterly fall since Q4 2003. (Chart 1.18) Against the backdrop of elevated room rates, average hotel occupancy dipped to a seasonally adjusted 84% in Q2, from 87% a year ago. In H1 2008, visitor arrivals totalled 5.1 million, prompting STB in August to flag the possibility that its target of 10.8 million visitor arrivals this year may not be met. The fall in visitor arrivals, coupled with greater caution in spending by residents, caused retail volumes (excluding motor vehicles) to contract sequentially in Q2 by 4.9% q‐o‐q SAAR. Keen demand for architectural and engineering services, due to the boom in construction activity in both the residential and commercial property segments, led to a 12.1% q‐o‐q SAAR increase in business services. Moreover, even as sales of private homes fell in Q2 alongside faltering market sentiment, real estate services held firm as commercial leasing activity remained brisk.

Taxes on products and FISIM also adversely impacted GDP growth.

Since the beginning of 2008, GDP growth has been weighed down by two components that are not directly captured in the value added of key sectors in the national accounts. (Chart 1.19) One component is taxes on products2, which comprises around 7% of GDP. These taxes include the goods and services tax (GST), stamp duty and excise duties. As the increase in taxes on products generally follows trend GDP growth, it seldom contracts, except in years where there are strong negative shocks. In H1 this year, however, taxes on products declined by a significant 13% y‐o‐y, following the fall in stamp duty from a record high in 2007 during the property market boom.

Chart 1.18

Visitor Arrivals and Hotel Room Rates

2006 Jul 2007 Jul 2008 Aug-10

0

10

20

30

40

50

YOY

% G

row

th

Visitor Arrivals*

Average Room Rate

* Data excludes Malaysian land arrivals.

Chart 1.19 Taxes on Products and FISIM

2007 Q2 Q3 Q4 2008 Q2-20

-10

0

10

20

YOY

% G

row

th

Taxes on Products FISIM*

* FISIM is a negative item in the national accounts.

2 See DOS Information Paper “Rebasing of the Singapore System of National Accounts to Reference Year 1995”, January

2003, for more details on taxes on products.

Macroeconomic Developments 15

Monetary Authority of Singapore Economic Policy Department

Besides taxes on products, another component which lowered overall GDP in H1 2008 was FISIM, which amounts to around 5% of GDP. This component is subtracted from overall GDP to account for the intermediate financial services consumed by other sectors. FISIM surged by 16% y‐o‐y in H1, dragging down headline GDP in the process. Together, these two components shaved 1.8% points off GDP growth in H1 this year.

The economy continued slipping in Q3 2008. In Q3 2008, the Singapore economy underwent further slippage, contracting by 6.3% q‐o‐q SAAR, according to the Advance Estimates. The economy thus appears to have entered a more advanced stage of weakness, with the deterioration of sectors reliant on regional demand adding to the strain from sentiment‐sensitive and G3‐oriented industries. Meanwhile, construction activity slowed to single‐digit y‐o‐y growth, as supply bottlenecks set in and high construction costs eroded gains in certified payments.

Manufacturing suffered a further drag from weak pharmaceuticals and infocomms output.

Manufacturing activity contracted by 11.5% y‐o‐y in Q3, according to the Advance Estimates. Pharmaceutical output weakness lingered as production was hit by routine maintenance and retooling shutdowns, as well as the spillover from industry‐specific pressures from the previous quarter. Electronics output also softened, following the phased relocation of Motorola’s handset production and the slowing global demand for IT.

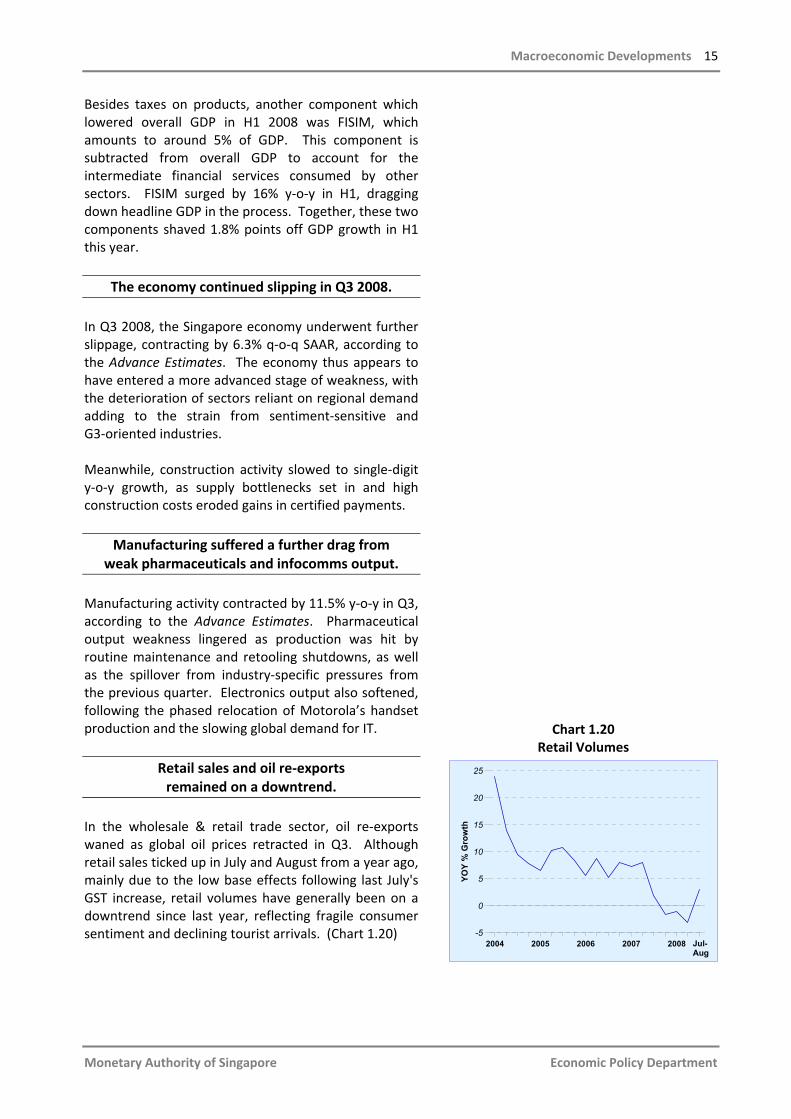

Retail sales and oil re‐exports remained on a downtrend.

In the wholesale & retail trade sector, oil re‐exports waned as global oil prices retracted in Q3. Although retail sales ticked up in July and August from a year ago, mainly due to the low base effects following last July's GST increase, retail volumes have generally been on a downtrend since last year, reflecting fragile consumer sentiment and declining tourist arrivals. (Chart 1.20)

Chart 1.20 Retail Volumes

2004 2005 2006 2007 2008-5

0

5

10

15

20

25

YOY

% G

row

th

Jul-Aug

16 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

Financial markets weakened further ... With global financial markets in upheaval, risk aversion remained high throughout Q3. Investor sentiment nose‐dived in mid‐September, as a fresh spate of market and credit‐related losses pushed global investment bank Lehman Brothers into bankruptcy and pressured Merrill Lynch, the world’s largest brokerage, into a takeover deal by Bank of America, while the remaining investment banks, Goldman Sachs and Morgan Stanley, relinquished their investment bank status to become bank holding companies. At the same time, the American International Group (AIG) faced severe liquidity pressures amidst a slew of downgrades, and was ultimately bailed out by the US Federal Reserve via an emergency loan, surrendering an 80% stake in the company. Weakness in the Eurozone and Japan also sent ripples throughout the region. In the domestic financial sector, sentiment‐sensitive industries such as the brokerage & treasury markets and fund management services deteriorated.

… causing the benchmark stock index to fall. Alongside similar losses in regional bourses, the Straits Times Index (STI) declined by 20% in Q3 after falling by 15% over the first half of the year. (Chart 1.21) As a result, the STI plummeted to 2,359 at end‐September, with the small‐cap and S‐share indices suffering drops of 51% and 69% respectively year‐to‐date. (Chart 1.22) Correspondingly, turnover volumes in the overall market plummeted to two‐year lows. The fund management industry was hit by declining asset values and lower discretionary funds under management as investors cut losses and increased their cash holdings. The Merrill Lynch Fund Manager Global Survey conducted in September suggests that risk appetite has fallen to a new low, with the majority of respondents overweighting bonds for the first time in the survey’s history. Emerging markets were rated underweight, reflecting net equity fund outflows from Asia in recent months. Notably, these responses were observed before the dramatic shifts in the US financial landscape in September, and sentiment is likely to have further weakened since then.

Chart 1.21 Stock Market Performance since

the Peak in 2007

Oct Jan Apr Jul Sep

10

20

30

40

50

60

70

80B

illio

n U

nits

2250

2500

2750

3000

3250

3500

3750

4000

Inde

x

Volume (LHS) STI (RHS)

2007 2008

Source: SGX

Chart 1.22 FTSE Small Cap and China Indices, Sep 2008

STI Small Cap Index China Index-80

-60

-40

-20

0

% G

row

th (Y

ear-

to-d

ate)

Source: SGX

Macroeconomic Developments 17

Monetary Authority of Singapore Economic Policy Department

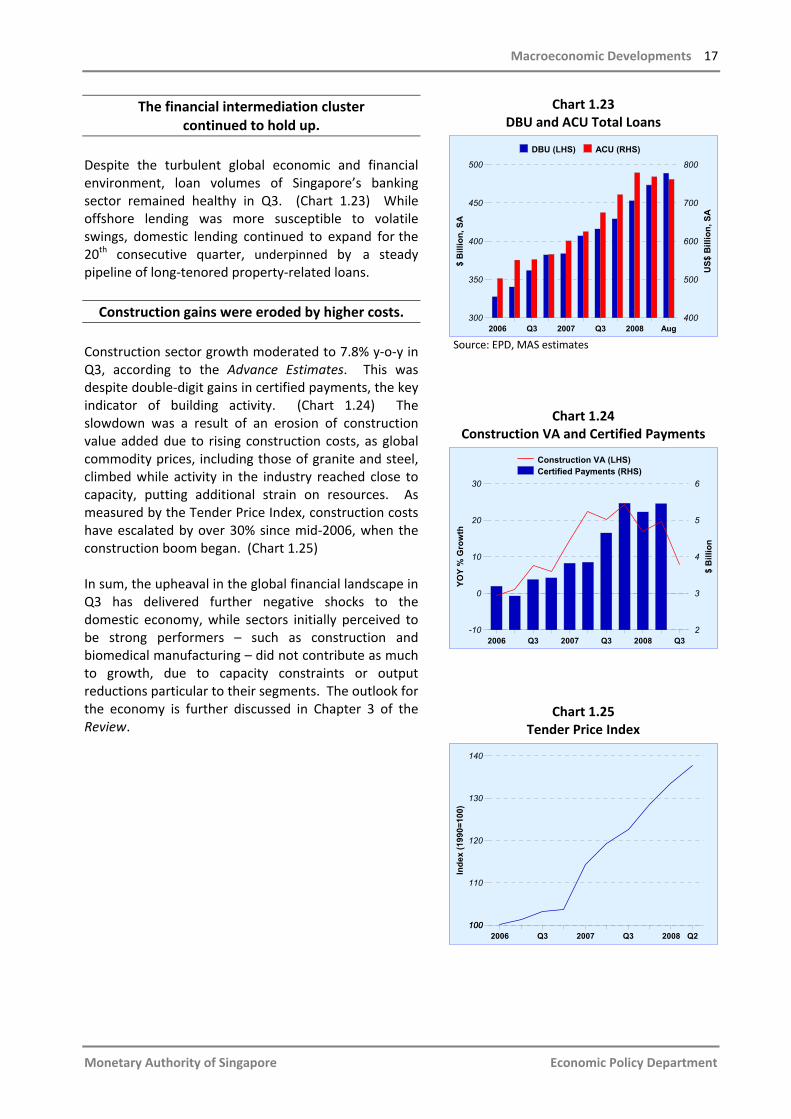

The financial intermediation cluster continued to hold up.

Despite the turbulent global economic and financial environment, loan volumes of Singapore’s banking sector remained healthy in Q3. (Chart 1.23) While offshore lending was more susceptible to volatile swings, domestic lending continued to expand for the 20th consecutive quarter, underpinned by a steady pipeline of long‐tenored property‐related loans. Construction gains were eroded by higher costs.

Construction sector growth moderated to 7.8% y‐o‐y in Q3, according to the Advance Estimates. This was despite double‐digit gains in certified payments, the key indicator of building activity. (Chart 1.24) The slowdown was a result of an erosion of construction value added due to rising construction costs, as global commodity prices, including those of granite and steel, climbed while activity in the industry reached close to capacity, putting additional strain on resources. As measured by the Tender Price Index, construction costs have escalated by over 30% since mid‐2006, when the construction boom began. (Chart 1.25) In sum, the upheaval in the global financial landscape in Q3 has delivered further negative shocks to the domestic economy, while sectors initially perceived to be strong performers – such as construction and biomedical manufacturing – did not contribute as much to growth, due to capacity constraints or output reductions particular to their segments. The outlook for the economy is further discussed in Chapter 3 of the Review.

Chart 1.23 DBU and ACU Total Loans

2006 Q3 2007 Q3 2008 Aug 300

350

400

450

500

$ B

illio

n, S

A

400

500

600

700

800

US$

Bill

ion,

SA

DBU (LHS) ACU (RHS)

Source: EPD, MAS estimates

Chart 1.24 Construction VA and Certified Payments

2006 Q3 2007 Q3 2008 Q3-10

0

10

20

30

YOY

% G

row

th

2

3

4

5

6

$ B

illio

n

Construction VA (LHS)Certified Payments (RHS)

Chart 1.25 Tender Price Index

2006 Q3 2007 Q3 2008 Q2100

110

120

130

140

100

Inde

x (1

990=

100)

18 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

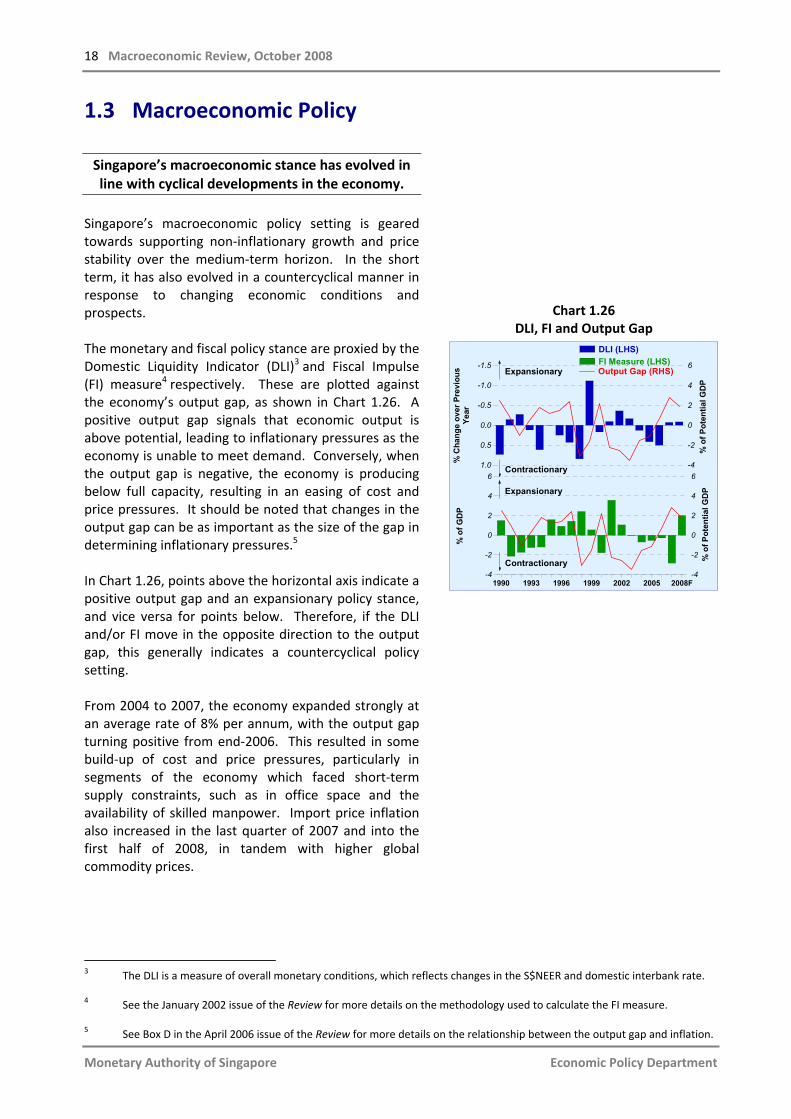

1.3 Macroeconomic Policy Singapore’s macroeconomic stance has evolved in line with cyclical developments in the economy.

Singapore’s macroeconomic policy setting is geared towards supporting non‐inflationary growth and price stability over the medium‐term horizon. In the short term, it has also evolved in a countercyclical manner in response to changing economic conditions and prospects. The monetary and fiscal policy stance are proxied by the Domestic Liquidity Indicator (DLI)3 and Fiscal Impulse (FI) measure4 respectively. These are plotted against the economy’s output gap, as shown in Chart 1.26. A positive output gap signals that economic output is above potential, leading to inflationary pressures as the economy is unable to meet demand. Conversely, when the output gap is negative, the economy is producing below full capacity, resulting in an easing of cost and price pressures. It should be noted that changes in the output gap can be as important as the size of the gap in determining inflationary pressures.5 In Chart 1.26, points above the horizontal axis indicate a positive output gap and an expansionary policy stance, and vice versa for points below. Therefore, if the DLI and/or FI move in the opposite direction to the output gap, this generally indicates a countercyclical policy setting. From 2004 to 2007, the economy expanded strongly at an average rate of 8% per annum, with the output gap turning positive from end‐2006. This resulted in some build‐up of cost and price pressures, particularly in segments of the economy which faced short‐term supply constraints, such as in office space and the availability of skilled manpower. Import price inflation also increased in the last quarter of 2007 and into the first half of 2008, in tandem with higher global commodity prices.

Chart 1.26 DLI, FI and Output Gap

1990 1993 1996 1999 2002 2005 2008F-4

-2

0

2

4

6

-4

-2

0

2

4

6

% o

f GD

P

Contractionary % o

f Pot

entia

l GD

P

-1.5

-1.0

-0.5

0.0

0.5

1.0 -4

-2

0

2

4

6

% C

hang

e ov

er P

revi

ous

Year

Expansionary

DLI (LHS)

Output Gap (RHS)FI Measure (LHS)

% o

f Pot

entia

l GD

P

Contractionary

Expansionary

3 The DLI is a measure of overall monetary conditions, which reflects changes in the S$NEER and domestic interbank rate. 4 See the January 2002 issue of the Review for more details on the methodology used to calculate the FI measure. 5 See Box D in the April 2006 issue of the Review for more details on the relationship between the output gap and inflation.

Macroeconomic Developments 19

Monetary Authority of Singapore Economic Policy Department

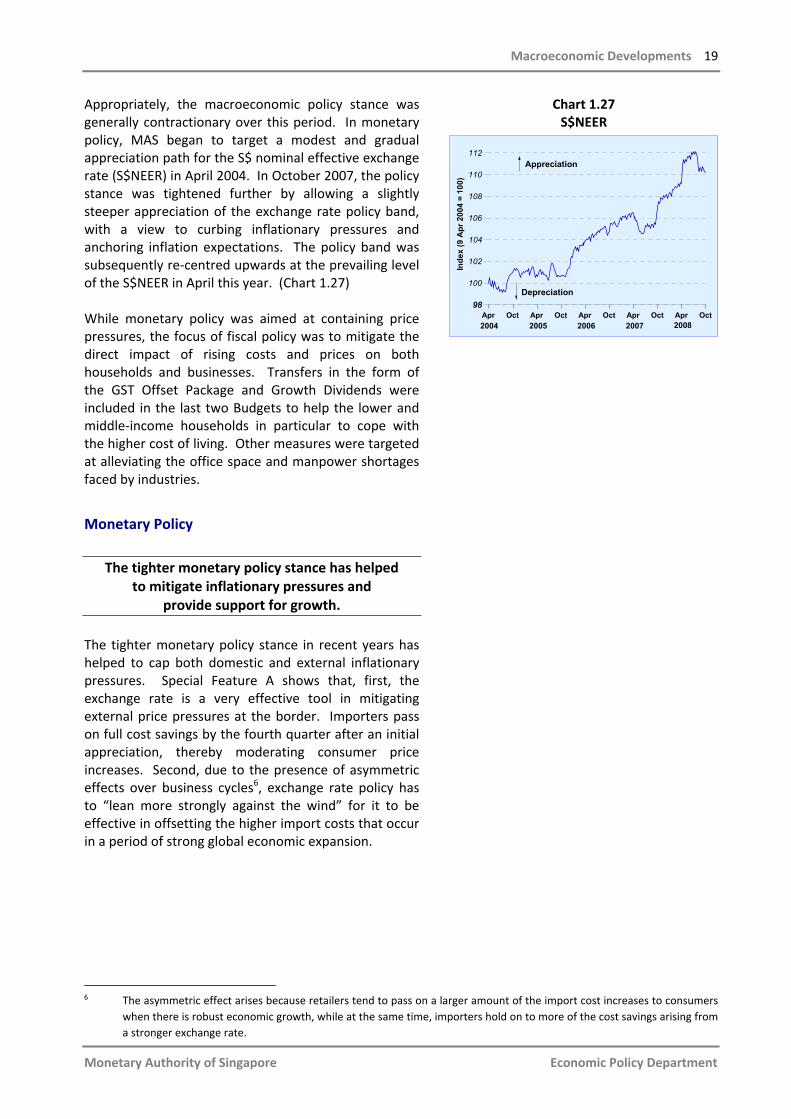

Appropriately, the macroeconomic policy stance was generally contractionary over this period. In monetary policy, MAS began to target a modest and gradual appreciation path for the S$ nominal effective exchange rate (S$NEER) in April 2004. In October 2007, the policy stance was tightened further by allowing a slightly steeper appreciation of the exchange rate policy band, with a view to curbing inflationary pressures and anchoring inflation expectations. The policy band was subsequently re‐centred upwards at the prevailing level of the S$NEER in April this year. (Chart 1.27) While monetary policy was aimed at containing price pressures, the focus of fiscal policy was to mitigate the direct impact of rising costs and prices on both households and businesses. Transfers in the form of the GST Offset Package and Growth Dividends were included in the last two Budgets to help the lower and middle‐income households in particular to cope with the higher cost of living. Other measures were targeted at alleviating the office space and manpower shortages faced by industries.

Monetary Policy

The tighter monetary policy stance has helped to mitigate inflationary pressures and

provide support for growth. The tighter monetary policy stance in recent years has helped to cap both domestic and external inflationary pressures. Special Feature A shows that, first, the exchange rate is a very effective tool in mitigating external price pressures at the border. Importers pass on full cost savings by the fourth quarter after an initial appreciation, thereby moderating consumer price increases. Second, due to the presence of asymmetric effects over business cycles6, exchange rate policy has to “lean more strongly against the wind” for it to be effective in offsetting the higher import costs that occur in a period of strong global economic expansion.

Chart 1.27 S$NEER

Apr Oct Apr Oct Apr Oct Apr Oct Apr Oct

98

100

102

104

106

108

110

112

98

Inde

x (9

Apr

200

4 =

100)

Appreciation

Depreciation

2004 200820072005 2006

6 The asymmetric effect arises because retailers tend to pass on a larger amount of the import cost increases to consumers

when there is robust economic growth, while at the same time, importers hold on to more of the cost savings arising from a stronger exchange rate.

20 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

In the absence of a S$NEER appreciation, cost and inflation pressures would have risen further.

Over a longer period, the tighter policy stance has also continued to foster medium‐term price stability as the basis for sustainable economic growth. Using the MAS macroeconometric model, a counterfactual simulation was conducted to assess the growth and inflation outcomes which would have occurred had MAS not allowed the S$NEER to appreciate between Q4 2005 and Q2 2008.7 The results show that GDP growth and CPI inflation in 2007 would have been higher at 8.9% and 3.8% respectively, compared to the 7.7% and 2.1% actually recorded. (Table 1.2) This would have aggravated the short‐term capacity constraints that the economy was already facing. The boost to GDP growth would be short‐lived as the underlying strong build‐up in cost pressures would cause growth to slow sharply to 3.3% by H1 2008, while pushing CPI inflation much higher to 10%. Growth and inflation outcomes would also have been much more volatile (as shown by the standard deviations in Table 1.2). Furthermore, higher inflation would have persisted into 2009, with GDP growth averaging some 1.7% points below the baseline. In the absence of MAS’ pre‐emptive monetary policy actions, the economy would have grown at a faster pace and stronger domestic price pressures would have resulted from the larger positive output gap. At the same time, the rise in global commodity prices would have led to higher import costs due to the loss of the filtering effect from a stronger exchange rate. In the event, the initiation of tighter monetary policy, particularly in the last two policy cycles, helped to bring down inflation. Without the tightening, domestic costs and inflationary pressures would have eventually impinged on growth. As such, there would still be appreciating pressures on the S$REER, arising from higher domestic cost inflation relative to Singapore’s major trading partners. Using the CPI as the price deflator, the S$REER is estimated to have risen by 1.9% q‐o‐q in Q2 2008. (Chart 1.28) On a monthly basis, it peaked in May 2008, before moderating as domestic CPI increased at a slower pace compared to our trading partners.

Table 1.2 Counterfactual Simulation Results Under

Alternative Monetary Policy Paths (%)

2007 H1 2008 Std Dev* Actual

GDP Growth

7.7 4.5 2.3

CPI Inflation

2.1 7.1 2.6

Counterfactual GDP Growth

8.9 3.3 3.4

CPI Inflation

3.8 10 3.7

* Over the period Q1 2006‐Q2 2008.

Chart 1.28 S$REER deflated by the CPI

1995 1997 1999 2001 2003 2005

80

85

90

95

100

105

110

115

80

Inde

x (J

an 1

995=

100)

REERCPI

NEER

2008

Relative CPI

Aug

7 The simulation effectively eliminated the 10% appreciation in the S$ trade‐weighted index that took place between Q4

2005 and mid‐2008.

Macroeconomic Developments 21

Monetary Authority of Singapore Economic Policy Department

Liquidity conditions remained tight despite some easing in recent months.

Overall liquidity conditions were tighter from April to July 2008, as shown by the positive DLI. (Chart 1.29) This was driven by the strengthening of the S$NEER. However, since August 2008, there has been some easing in liquidity conditions, with the DLI turning negative in line with the fall in the exchange rate. Nonetheless, there has been a trend tightening in liquidity conditions over the past year. (Chart 1.30) Overall domestic monetary conditions remain relatively tight, and still exert some degree of restraint on economic activity. In line with the slowdown in domestic economic activity, money demand growth has slowed. From a high of 24% y‐o‐y in Q2 2007, the growth of M2 moderated to 12% in Q1 2008 before easing further to 8.7% in August. This reflected, to some degree, the reduced demand for credit by the private sector. Loans to non‐bank customers (domestic credit to the private sector) rose by a monthly average of $3.1 billion in Jul‐Aug, compared with an increase of $4.1 billion in Q1 2008. While new loans, particularly to the property‐related sector (including housing loans), have continued to grow, the pace of increase has slowed considerably from the peak in Q4 last year. (Chart 1.31) Meanwhile, domestic interbank rates edged lower in tandem with the stronger S$ following the policy announcement in April 2008. The benchmark three‐month domestic interbank rate fell by 31 bps from 1.31% in end‐March to 1.0% in early August, the lowest level since September 2004. However, in the wake of the dislocation in global money markets and growing market expectations of a weaker S$, the benchmark rate rose to around 1.88% at end‐September. (Chart 1.32) MAS has temporarily kept a higher level of liquidity in the banking system through its money market operations (MMOs). Over the course of the year, MAS’ MMOs have ensured sufficient liquidity in the banking system to meet banks’ demand for reserve and settlement balances. The amount of liquidity in the banking system is estimated by taking into consideration the banking sector’s demand for funds and the net liquidity impact of autonomous money market factors. Box B at the end of the chapter provides a review of MAS’ MMOs in FY2007/08.

Chart 1.29

Domestic Liquidity Indicator

Apr Jul Oct Jan Apr Jul

-0.9

-0.6

-0.3

0.0

0.3

0.6

0.9

Cha

nge

from

Pre

viou

s Q

uart

er Tightening

Easing

Sep2007 2008

Exchange RateChanges

Interest RateChanges

DLI

Chart 1.30 Domestic Liquidity Indicator

Apr Jul Oct Jan Apr Jul

-2

-1

0

1

2

3C

umul

ativ

e C

hang

e

Tightening

Easing

Sep2007 2008

Chart 1.31 Domestic Credit to Private Sector

2007 Q2 Q3 Q4 2008 Q2 Q3*0

1

2

3

4

5

0

Ave

rage

Mon

thly

Cha

nge

($ B

illio

n)

Domestic Credit to Private Sector

Bank Loans to Property-related Sector

* Average of Jul‐Aug.

22 Macroeconomic Review, October 2008

Monetary Authority of Singapore Economic Policy Department

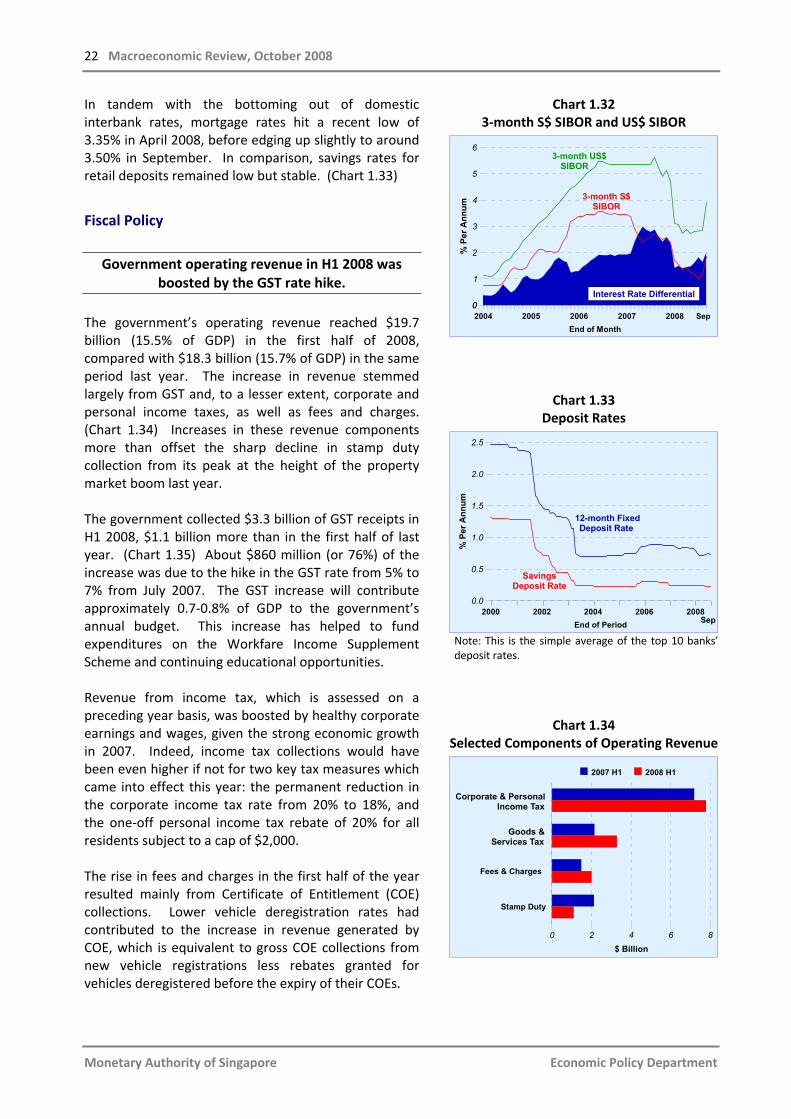

In tandem with the bottoming out of domestic interbank rates, mortgage rates hit a recent low of 3.35% in April 2008, before edging up slightly to around 3.50% in September. In comparison, savings rates for retail deposits remained low but stable. (Chart 1.33)

Fiscal Policy

Government operating revenue in H1 2008 was boosted by the GST rate hike.

The government’s operating revenue reached $19.7 billion (15.5% of GDP) in the first half of 2008, compared with $18.3 billion (15.7% of GDP) in the same period last year. The increase in revenue stemmed largely from GST and, to a lesser extent, corporate and personal income taxes, as well as fees and charges. (Chart 1.34) Increases in these revenue components more than offset the sharp decline in stamp duty collection from its peak at the height of the property market boom last year. The government collected $3.3 billion of GST receipts in H1 2008, $1.1 billion more than in the first half of last year. (Chart 1.35) About $860 million (or 76%) of the increase was due to the hike in the GST rate from 5% to 7% from July 2007. The GST increase will contribute approximately 0.7‐0.8% of GDP to the government’s annual budget. This increase has helped to fund expenditures on the Workfare Income Supplement Scheme and continuing educational opportunities. Revenue from income tax, which is assessed on a preceding year basis, was boosted by healthy corporate earnings and wages, given the strong economic growth in 2007. Indeed, income tax collections would have been even higher if not for two key tax measures which came into effect this year: the permanent reduction in the corporate income tax rate from 20% to 18%, and the one‐off personal income tax rebate of 20% for all residents subject to a cap of $2,000. The rise in fees and charges in the first half of the year resulted mainly from Certificate of Entitlement (COE) collections. Lower vehicle deregistration rates had contributed to the increase in revenue generated by COE, which is equivalent to gross COE collections from new vehicle registrations less rebates granted for vehicles deregistered before the expiry of their COEs.

Chart 1.32 3‐month S$ SIBOR and US$ SIBOR

2004 2005 2006 2007 2008End of Month

0

1

2

3

4

5

6

0

% P

er A

nnum

3-month US$ SIBOR

3-month S$ SIBOR

Interest Rate Differential

Sep

Chart 1.33 Deposit Rates

2000 2002 2004 2006 2008End of Period

0.0

0.5

1.0

1.5

2.0

2.5

% P

er A

nnum

Sep

12-month Fixed Deposit Rate

Savings Deposit Rate

Note: This is the simple average of the top 10 banks’ deposit rates.

Chart 1.34 Selected Components of Operating Revenue

Fees & Charges

Stamp Duty

0 2 4 6 8$ Billion

2007 H1 2008 H1

Corporate & PersonalIncome Tax

Goods &Services Tax

Macroeconomic Developments 23

Monetary Authority of Singapore Economic Policy Department

There were increases in both operating and development expenditure.