martin luffy [email protected] “ the digital journey ” 4 september 2014 insert picture

TRANSCRIPT

IBP Background and History

August 2014

1. The Business2.Technology Path3.Pitfalls and Obstacles Along the Way4.Role of the Senior Management Team

Background Information

• Specialty sub-contracting sector of the highly cyclical construction industry

• Mainly installing insulation products and installation for new housing

• Low-skilled work – commodity products• Started in 1995 with 1 location • Growth thru acquisition• Many small jobs – average ~ $2,000/job• Completed IPO in 1Q 2014 3

The second largest1 new residential insulation installer in the US with over 100 locations serving 47 states

Evolution into an Industry Leader

4

Service area covers more than 55% of total permits issued vs. 24% in 2005 with a #1 or #2 position in greater than half of the markets served2

Note: Shaded states are where we have a physical presence. Some dots represent multiple locations1 Based on internal estimates2 Based on permits issued in those markets

Investor Presentation - August 2014

Products & End Markets

Garage Doors Rain Gutters Closets & Shelving Shower Doors & MirrorsInsulation

Focused insulation installation offering, coupled with complementary products for end markets having significant cyclical upside

Net Revenue by End Market – LTM 6/14Net Revenue by End Market – LTM 6/14

5Investor Presentation - August 2014

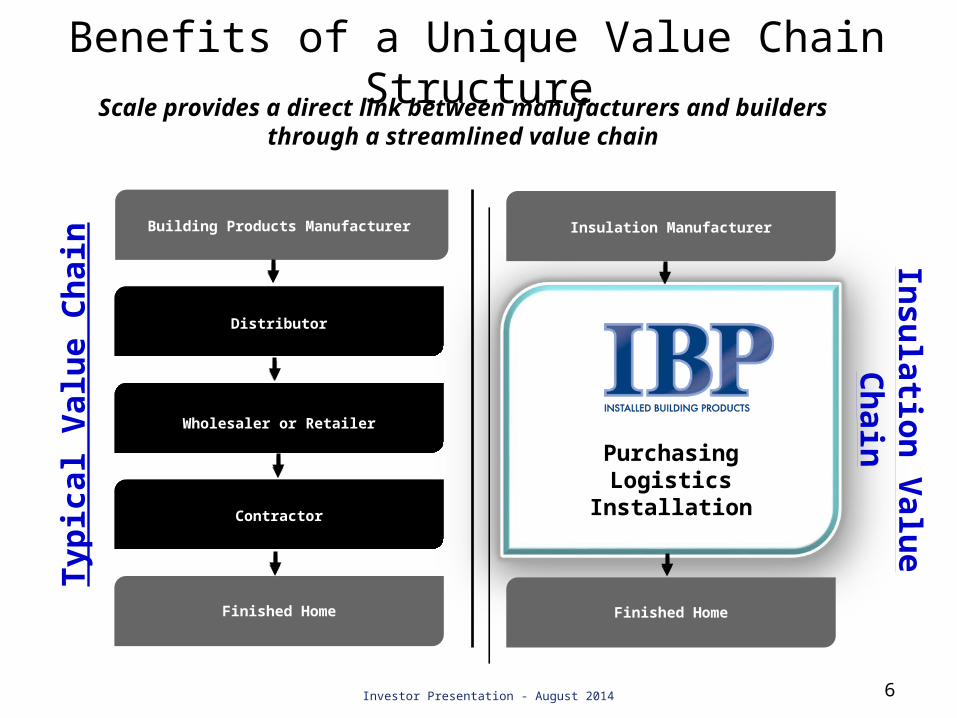

Benefits of a Unique Value Chain Structure

6

Scale provides a direct link between manufacturers and builders through a streamlined value chain

Building Products Manufacturer

Distributor

Wholesaler or Retailer

Contractor

Finished Home

Typ

ical

Val

ue

Ch

ain

Insulation Manufacturer

PurchasingLogistics

Installation

Finished Home

Insu

lation

Valu

e Ch

ain

Investor Presentation - August 2014

Strengths of Our Business

7

Local market leadership with national scaleLocal market leadership with national scale

Proven ability to gain market share Proven ability to gain market share

Multiple Ways to Drive Growth and ProfitabilityMultiple Ways to Drive Growth and Profitability

Proven acquisition track recordProven acquisition track record

Highly experienced and incentivized management teamHighly experienced and incentivized management team

Investor Presentation - August 2014

Clear Strategy for Value Enhancing AcquisitionsClear Strategy for Value Enhancing Acquisitions

• Maintains local trade names and existing management, strengthening the relationship between the Company and its customers

• Business is primarily won or lost at the local level

1. Local Market Leadership with National Scale

8

is served by 11 different IBP branches across 15 markets

Leading market positions serviced through local trade names

Investor Presentation - August 2014

Lo

cal I

BP

tra

de

nam

es

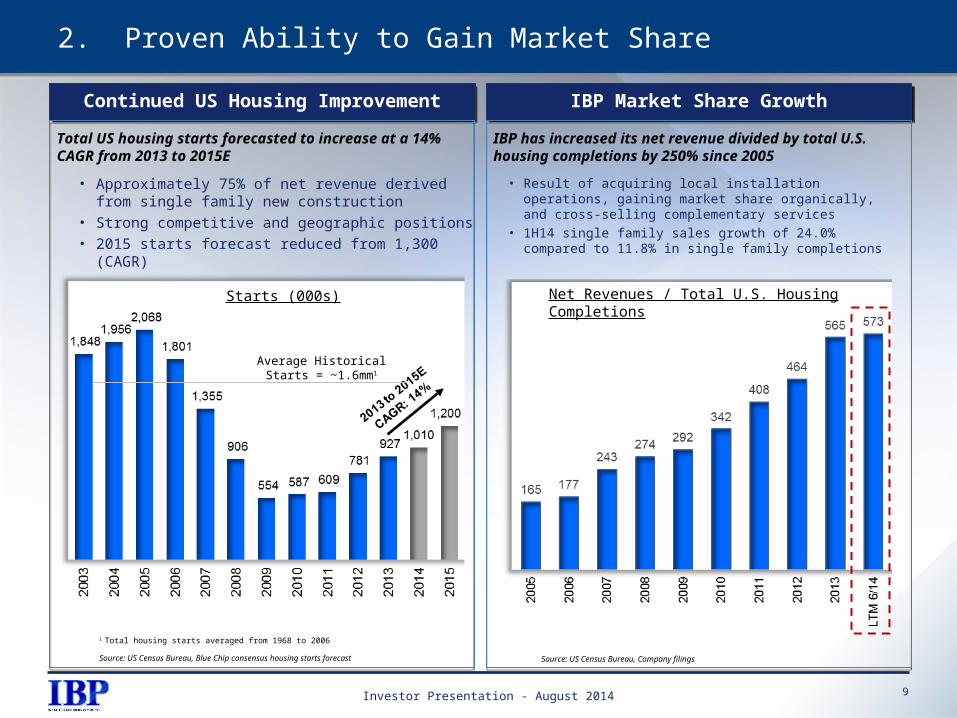

2. Proven Ability to Gain Market Share

9

Continued US Housing ImprovementContinued US Housing Improvement IBP Market Share GrowthIBP Market Share Growth

• Approximately 75% of net revenue derived from single family new construction

• Strong competitive and geographic positions• 2015 starts forecast reduced from 1,300 (CAGR)

Total US housing starts forecasted to increase at a 14% CAGR from 2013 to 2015E

Average Historical Starts = ~1.6mm1

1 Total housing starts averaged from 1968 to 2006

Source: US Census Bureau, Blue Chip consensus housing starts forecast Source: US Census Bureau, Company filings

IBP has increased its net revenue divided by total U.S. housing completions by 250% since 2005

• Result of acquiring local installation operations, gaining market share organically, and cross-selling complementary services

• 1H14 single family sales growth of 24.0% compared to 11.8% in single family completions

Investor Presentation - August 2014

Starts (000s) Net Revenues / Total U.S. Housing Completions

3. Multiple Ways to Drive Growth and Profitability

10

1 Per Blue Chip consensus housing starts forecast

Investor Presentation - August 2014

Asset lite model can accommodate growth without material capital needs

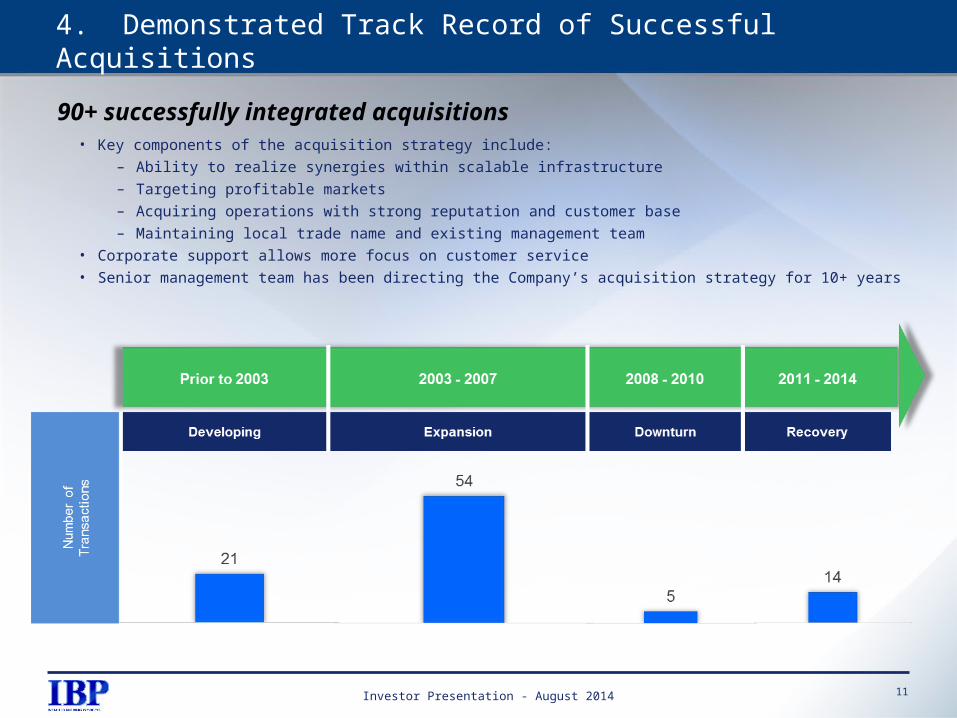

4. Demonstrated Track Record of Successful Acquisitions

90+ successfully integrated acquisitions

11

• Key components of the acquisition strategy include:

– Ability to realize synergies within scalable infrastructure

– Targeting profitable markets

– Acquiring operations with strong reputation and customer base

– Maintaining local trade name and existing management team

• Corporate support allows more focus on customer service

• Senior management team has been directing the Company’s acquisition strategy for 10+ years

Investor Presentation - August 2014

5. Highly Experienced and Incentivized Management Team

12

Strong operational focus and proven understanding of the industry

• Field management structure is comprised of deeply experienced managers at all levels

• Team has effectively managed through several housing cycles, established a proven acquisition strategy, and gained market share

• Senior management aligned with investors due to meaningful equity ownership in IBP

Investor Presentation - August 2014

6. Clear Strategy for Value Enhancing Acquisitions

Fragmented industry allows for geographic expansion through sizable acquisitions and strengthening of existing branches via smaller tuck-ins

13

Key Areas of Opportunity

• Extensive pool of potential acquisition targets with 1,000+ independent insulation contractors across the US

• Additional large-market entry opportunities (IBP currently covers 35 of the top 50 MSA’s1)

• Significant acquisition potential in attractive secondary markets

• Extensive pool of potential acquisition targets with 1,000+ independent insulation contractors across the US

• Additional large-market entry opportunities (IBP currently covers 35 of the top 50 MSA’s1)

• Significant acquisition potential in attractive secondary markets

Proven Model for Acquisitions

IBP branches

1 MSA, or Metropolitan Statistical Area, is an area that generally consists of at least one urbanized area of 50,000 or more inhabitants, plus adjacent territory that has a high degree of social and economic integration with the core area as measured by commuting ties

Investor Presentation - August 2014

TECHNOLOGY

14Investor Presentation - August 2014

What started as a environment where each branch had their own system quickly turned into

chaos at month-end close.

Opportunity #1 - Eliminating the long-term ramifications of allowing our acquired locations to operate on separate technology platforms while providing them with the operational flexibility to continue to run their business based on local market conditions.

TECHNOLOGY

15Investor Presentation - August 2014

Requiring data to support the enterprise and the 100+ locations

Opportunity 2: Building a coalition of sponsors/decision makers to agree on the definitions, timing and amount of data

16

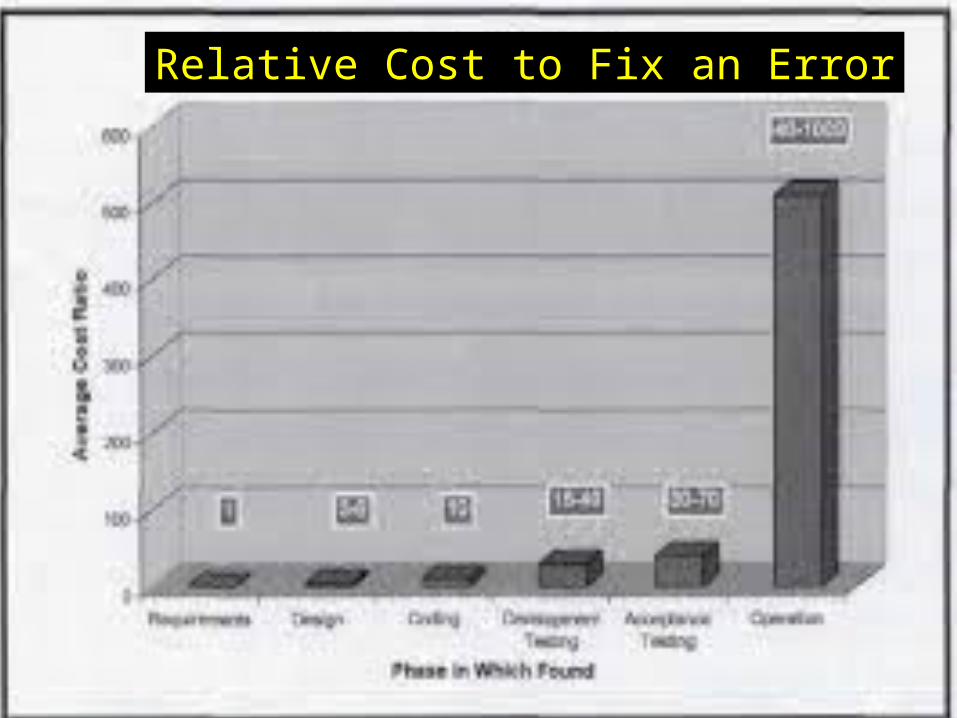

Relative Cost to Fix an Error

TECHNOLOGY

17Investor Presentation - August 2014

We ended up building an industry specific web-based system for our core branch operations and decided to utilize packaged software for other administrative functions such as Payroll, e-mail, HR and finance.

TECHNOLOGY

18Investor Presentation - August 2014

We called the system “jobCORE” – In addition to supporting our branches operationally, it provides a fully integrated reporting and dashboard environment for key business metrics

Opportunity #3 – Defining key metrics and timing of updates for the dashboard

TECHNOLOGY

19Investor Presentation - August 2014

Opportunity #4: Managing the change and not disrupting on-going operations while moving the branches to the new system

And we proceeded to implement jobCORE in our 100+ locations

TECHNOLOGY

20Investor Presentation - August 2014

By aggressively addressing the

TECHNOLOGY

21Investor Presentation - August 2014

We built a small team of professionals who travel to the branches to support the implementations and data conversions

22

TECHNOLOGY

23Investor Presentation - August 2014

What started as a few servers housed in a closet over 10 years ago has evolved into a large enterprise scale operation for our centrally

managed IT environment.

Opportunity #5 – Balancing the correct level of investment in people, process and technology to support the business without breaking the bank

TECHNOLOGY – Where are We Going?

24Investor Presentation - August 2014

1. Upgrading our technology to provide a reliable and scalable platform for the business as it grows

2. Supporting the overall general controls environment and SOX compliance disaster recovery, user access controls, segregation of duties across the business)

3. Maintaining a balanced investment approach that will be sustainable in the next downturn

TECHNOLOGY – Where are We Going?

25Investor Presentation - August 2014

Enterprise Data Warehouse

Providing a broader group of business users with better data access and appropriate reporting tools

ad-hoc reporting

TECHNOLOGY – Where are We Going?

26

Other technologies in pilot or expected to be utilized in the coming years:1.Mongo DB for mail archival – what is the need?2.Mobile applications – requirements and usage?3.GPS for vehicles – is there a real payoff?4.Tablets – mixed reviews from the business5.BYOD – is it secure?6.Systems support for SOX processes – required?

27

A. Technology “WILL” change, always B. Modern technology today will become

“Classical” tomorrowC. MODERN CIO’s will be able to identify the

technologies that will be EFFECTIVE for “THEIR ORGANIZATION” and will push for change in the status quo to EFFICIENTLY implement them into the daily routine of the “BUSINESS”

ABC’s for the “Modern” CIO

28

CIO’s job is to Drive . . . 1. Take could do’s and determine the should do’s2. Say no, manage the shoot, ready, aim approach3. Make every $ of spending count4. Tell the truth – Cost, budgets, etc. and here is what

we are not doing5. Do what you say you will do – Keep your promises6. Emerge as a leader to the enterprise.7. Fail to plan and you are planning to fail8. Build relationships with everyone in the business9. Force interaction with the C-suite, find reasons to talk

to them that are of interest to them10. Do not blindly follow the fad’s

Some parting thoughts . . .

29

We all have or will have career/transformational moments.

We need to make them, sometime by saying no to building stuff without support

from a sponsor and a defined and measured business objective.

Bottom line. . .

30

And if all else fails . . .