market trends - animpanimp.it/animp_/images/pdf_archivio/montefiore.pdf · (comperj, rnest) and...

TRANSCRIPT

Mauro Montefiore Chief Business Officer Technip Region B

24/10/2013 Le strategie di mercato per la filiera dell’impiantistica italiana 1

MARKET TRENDS

Market Trends

2

1. North America

2. Latin America

3. Russia, CIS and Southern

Eastern Europe (SEE)

4. North Africa – Egypt & Libya

North America

• US Market

• Overview

• By sector

• Canada Market

• Overview

• By sector

3

US Market

Unconventional Oil & Gas - shale Gas revolution:

Shale gas production today : 30% of total U.S. gas supply

Potentially more than $20b/year of investment in gas monetization

projects

Gas export opportunities

Inexpensive feedstock for petrochemical and fertilizer projects

Gas processing, ethylene, petrochem, fertilizers and LNG export :

31 high potential projects ($110b) out of 77 announced ($227b)

17 projects ($37b) already awarded

14 high potential projects ($73b) to be awarded - $38b by 2015

Overview

First wave award between 2012 and 2015 ($75b)

Second wave award between 2016 and 2020 (after impact of first wave)

Most probably a last group of projects (around 50%) will never be built

4

US Market

By sector

Capex for announced projects

5.000

15.000

25.000

35.000

45.000

55.000

2013-2014 2015-2016

M U

S $

UPSTREAM MARKET TREND North America - US

-

10.000

20.000

30.000

40.000

50.000

2013-2014 2015-2016

M U

S $

DOWNSTREAM MARKET TREND North America - US

5.000

15.000

25.000

35.000

45.000

55.000

2013-2014 2015-2016

M U

S $

MIDSTREAM MARKET TREND North America - US

Source: TPIT Internal Research

5

US Market

Gas processing and derivatives

Ethylene cracker

Global GDP growth: increasing demand for ethylene derivatives

Reduced ethane cost: ethylene cracking margins more attractive

ethylene cracker projects – 7 “high potential”

LNG/GTL

Shale gas developments : natural gas cost spread between US - Asia

LNG export facilities: 8 “high potential” LNG projects (roughly $70b)

Go-forward LNG prospects “large but uncertain” (potential for 1-2

projects/year)

Crude oil to natural gas price ratio: well above the minimum making GTL

projects viable – 2 “high potential”GTL projects

Fertilizer, PDH and Downstream Market Potential

Increased pricing and reduced natural gas costs: margins for ammonia

fertilizer production in NA dramaticallly increased

More than 20 Fertilizer ($22b) projects announced in North America – only few

serious initiatives – real potential: no more than one or two projects per year

Several major methanol projects emerging

Ethylene projects driving downstream derivative projects : several polymer

opportunities emerging

BG / Trunkline Lake Charles

Cheniere Corpus Christi

Cheniere Creole Trail

Cheniere Sabine Pass

Freeport

Sempra Lake Charles

Sasol GTL

Shell GTL

US Gulf Coast

North

America Asia Europe

$14-16/mmBTU $8 - 9/mmBTU $3-5/mmBTU

Jordan Cove

US West Coast

Dominion Cove Point

US East Coast

By sector

6

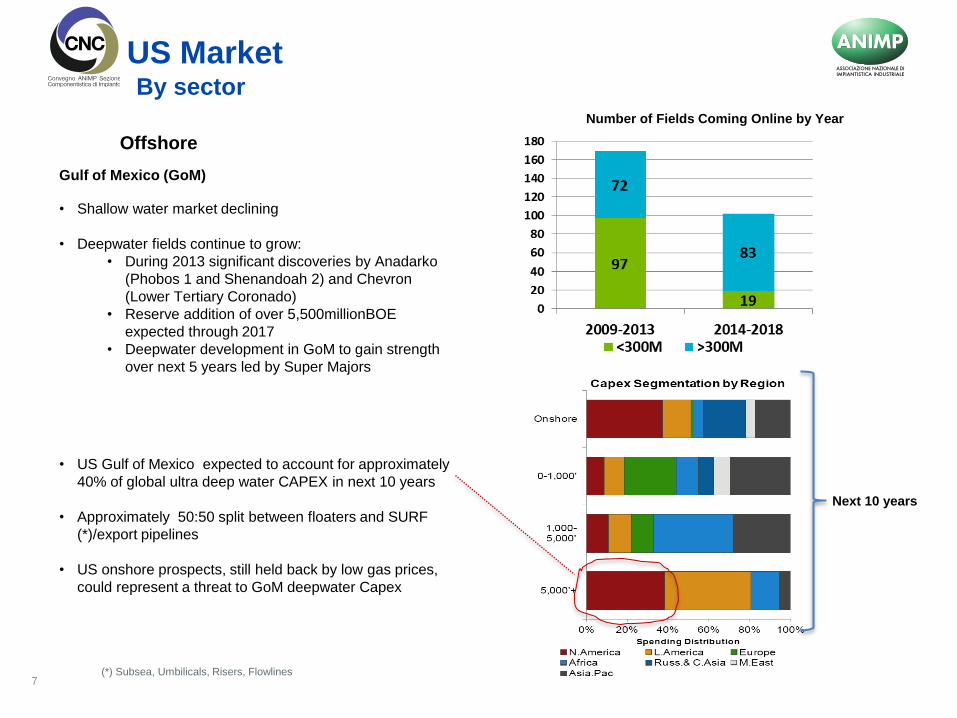

Offshore

Gulf of Mexico (GoM)

• Shallow water market declining

• Deepwater fields continue to grow:

• During 2013 significant discoveries by Anadarko

(Phobos 1 and Shenandoah 2) and Chevron

(Lower Tertiary Coronado)

• Reserve addition of over 5,500millionBOE

expected through 2017

• Deepwater development in GoM to gain strength

over next 5 years led by Super Majors

• US Gulf of Mexico expected to account for approximately

40% of global ultra deep water CAPEX in next 10 years

• Approximately 50:50 split between floaters and SURF

(*)/export pipelines

• US onshore prospects, still held back by low gas prices,

could represent a threat to GoM deepwater Capex

Next 10 years

US Market By sector

Number of Fields Coming Online by Year

(*) Subsea, Umbilicals, Risers, Flowlines 7

• Oil reserves :the 3rd largest oil reserves of the world, in excess of 173 billion bpd

• Oil production : up to 6.2 million bpd in 2030 (mainly unconventional reserves in Alberta)

• Oil sands production:

• from 1.6 million b/d in 2011 to 3.2 in 2020 and to 5.0 in 2030

• capital investment in Alberta oil sands: expected to exceed 180 B$ in the next decade

• Natural Gas: the 3rd largest natural gas producer in the world

• abundance of shale gas: developments in mega LNG projects (Pacific coast), GTL, gas processing and downstream

• Last 5 years: Chinese, Korean and Japanese investors acquired multi billion CAD stakes in oil sands and LNG

projects

• Today investors cautious - upstream developments to maintain the present pace (15-20 billion $/y) provided no significant

decrease in USA demand occur and limitation in export pipelines is overcome

• High workload and aging workforce causes shortage of resources in engineering, fabrication and erection

• The energy market : a cycle of expansion extending beyond the next decade.

Canada Market

Overview

8

Canada Market By sector

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

2013-2014 2015-2016

M U

S $

UPSTREAM MARKET TREND North America - Canada

Capex for announced projects

-

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

2013-2014 2015-2016

M U

S $

MIDSTREAM MARKET TREND North America - Canada

Source: TPIT Internal Research

9

Gas processing and derivatives

• Shale gas in North America affecting gas price (below 2$ per million

BTU) and threatening in medium terms export to USA

• Access to new markets – new LNG export facilities – LNG to Asia

• GTL conversion (Alberta)

• Gas monetization: petrochemical and fertilizer production

Oil production and refining

• Most of crude exported to USA; export pipeline capacity added

• Change in the future – export to Asia expected to grow

• Last 30 years: number of refineries from 44 to 18

• Most of upgrader projects cancelled due to: • narrow price differential,

• excess of refining capacity in USA,

• cost/schedule uncertainty

• Large number of SAGD (*) Projects (*) Steam Assisted Gravity Drainage

Different LNG projects may merge, only one

or two likely to be built by 2020

GTL Sasol Pre FEED 2015 2019

Canada Market By sector

10

Latin America

11

• Latin America Market

• Overview by country

• By sector

General

• Political uncertainty & debt of some Alba countries: delay on projects

Venezuela (PDVSA)

• 297 billion barrels oil proven resources; from 2,8mbpd up to 6mbpd in 2020

• $230b investments up to 2018 ($70b in downstream), out of which:

• $60b by JV partners: CNPC, Sinopec, Petrovietnam, Rosneft, Lukoil,

Gazpom, Chevron, Petrobras, Repsol, ENI etc.

• $35b Credit line from China

• Chinese and Russian investors more and more present

• Focus on production increase: 6 Heavy Oil Upgraders - Orinoco Basin

• Some JV partners holding / postponing commitment

Ecuador

• US$ 20bn up to 2018

• IOCs (Petrobras, Repsol, ENI, ENAP) reduced their local investments

• CNPC main investor in Pacific Refinery ($10b)

• Other projects not progressing for lack of financing

Bolivia

• US$ 10bn up to 2018 (mainly YPBF; limited contribution of foreign

investors like Petrobras; probably Braskem in the future);

• YPBF full control of the field of hydrocarbons; target to increase refining

capability from 45kbpd to 125kbpd by 2018

• Significant gas resources (even if not certified)

Cuba

• Potential projects in cooperation with PDVSA financed

from China (Cienfuegos and Matanzas refineries)

Venezuela & ALBA Countries

General

• Stability climate and investors trust;

• Investments: refineries modernization (new diesel / gasoline specs -

Mexico, Peru, Colombia) and gas production/distribution/monetization

• Impact of shale gas revolution to be evaluated

Mexico - PEMEX

• Investments: ~$20b per year up to 2018, 20% in downstream

• Focus in Tula Refinery, Reconfiguration of Salamanca Refinery and

Diesel Desulphurization Units (new specifications)

• Moving toward more flexible contracting system

Colombia

• ECOPETROL: $83b through 2020, inc. $12b in downstream

• Modernization of Cartagena & Barranca refineries: significant delays

• Long term potential in heavy crude upgrading and offshore

Peru

• Estimated country’s gas reserves 50 trillion cuft -more than 70% to be

confirmed/certified – future investments in fertilizers, petrochemicals and

LNG/GTL

• Petroperu / Repsol: investment in refining to meet new diesel and

gasoline specifications in 2016 (Talara, La Pampilla etc.)

• $30b investment in Oil & Gas up to 2018 - foreign investors (Petrobras,

Repsol, Ecopetrol, Pacific Rubiales and Braskem)

Chile

• Limited future investment to improve capacity and final products quality of the two existing refinery (Bio Bio and Acongaua)

• Investment mainly in mining and infrastructures

Pacific Alliance (Mexico, Colombia, Peru and Chile)

Latina America Market Overview by country

12

• Braskem: planning to invest in Brazil and abroad (both in

Latin America, i.e. Peru, Venezuela and in US);

• Chinese NOC (CNPC in Venezuela / Ecuador / Central

America, Sinopec and CNOOC in Brazil / Argentina /

Bolivia)

• Russian NOC (Rosneft & Lukoil in Venezuela, Gazprom in

Venezuela/Bolivia/Argentina)

• South America NOCs (Petrobras, PDVSA & Ecopetrol)

active in neighbouring countries

International Players in several

Latin America countries

• Issues in existing projects and debt of Petrobras:

investments potential slowdown

• Petrobras investments: $75b downstream - $147b upstream up to

2017

• Target: production increase from 2,1mbpd up to over 5mbpd in

2020

• Smaller investments in the field of ethanol, biodiesel and mining

• More than 95% of investments inside the Country

• Investment slowing down due to issues in existing projects

(Comperj, RNEST) and debt of Petrobras

• Looking for financing (almost 10MUS$ per year) through

recapitalization plan and several bilateral financing and

partnership deals

• Key projects:

• Several FPSO linked to pre-salt projects

• Petrobras Premium Refineries I & II – Chinese, Korean

and other international investors involved

• Petrobras Comperj Refinery 2nd Train, UFN4 and UFN5

Complex under evaluation

• Braskem Comperj Petrochemical Complex; negotiations

with Petrobras on gas supply conditions

• Opportunities in Biofuels – 2nd Generation Ethanol (BP

and Total)

Brazil

Latina America Market Overview by country

• Limited investment expected in the next years;

• Potential shale gas and shale oil resources under assesment • Among the planned projects:

• Baia Balanca Refinery (FEED underway) • Campana Refinery (FEED pre-qualification launched) • HDS new units in some of the existing refineries • Several Regassification Plant

• chances to be implemented low due to the economical situation of the country

Argentina

13

Latina America Market Overview by sector

Capex for announced projects

Source: TPIT Internal Research

14

Onshore accessible Market (m€); >50%GO

0

1000

2000

3000

4000

5000

6000

7000

2011A 2012A 2013F 2014 2015 2016

Other LAM

Pacific Alliance

(*)

Brazil

Venezuela &

ALBA

(*) Colombia, Mexico , Peru, Chile

Onshore by Product Line

Latina America Market Overview by sector

0

1000

2000

3000

4000

5000

6000

7000

2011 2012 2013 2014 2015 2016

Other

Fertilizers

Petrochemicals

Refining

Oil production and refining

Heavy Oil Upgraders in Venezuela (potential in other countries)

Shale Oil: Argentina (27Bbl), Venezuela(13Bbl), Colombia (7Bbl), Brazil

(5Bbl)

Oil products: internal demand increase; new refineries or modernization (Brazil, Ecuador, Venezuela, Perù, Colombia, Mexico etc.)

USA no longer a captive market for LAM crudes – LAM looking to Far East

Excess US Refining Capacity challenging economics of Refinery Upgrading

Gas processing and derivatives

Shale Gas: Argentina (800tcf),Brazil (245tcf),Venezuela (170tcf),Colombia

(55 tcf)

Gas production increase in several countries (in particualr Peru, Bolivia)

Petrochemical and fertilizers: internal demand increase; investment

decisions affected by shale gas revolution in USA

Gas Monetization projects in South America: competition against US

LNG : terminals (Colombia, Uruguay, Caribbean and Central American

Countries) and small-size LNG liquefaction plants for local use (Bolivia,

Peru)

Petrochemicals: new Petrochemical complexes in Mexico and potentially in

Brazil, Peru and Bolivia – Braskem as a key player

Fertilizers: significant investments in Brazil - other potential initiatives in

Peru

Investments: low Average GO factor and long decision process

Limited financial resources – e.g. debt situation of some NOCs

Cost / schedule overruns on projects draining NOCs’ resources/confidence

15 Source: TPIT Internal Research

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2013 2014 2015 2016

NorthAmerica

Middle East& CaspianSeaLatinAmerica

Europe

Asia &Pacific

Africa

+44%

Subsea CAPEX: Latin America the largest contributor

$U

SB

$0

$1

$2

$3

$4

$5

$6

$7

2013 2014 2015 2016

Africa Asia & Pacific

Europe Latin America

Middle East & Caspian Sea North America

$US 20 bn $US 23 bn

$US13B $US16B

Floating Platform CAPEX: Latin America the 2° contributor

In Brazil:

Many opportunities with Pre-Salt developments offshore Brazil (High-Pressure

High-Temperature Fields) - water depths from Deep to Ultra-Deep

Petrobras to invest $147B in E&P up to 2017

3 Cessão Onerosa (Transfer of Rights) FPSOs to be awarded in 4Q 2013 and 3 in

2014

Auction for Libra Field (up to 42 billion BOE) will require at least 17 FPU

Petrobras announced need of 100 FPSO in the decades of 2020-2030

New Build:

59%

Converted:

41%

Latina America Market Overview by sector

Offshore

2013-2016: CAPEX breakdown by regions

16

17

Russia - CIS - SEE

• Russia - CIS - SEE

• Overview by country

• By sector

Russia - CA - SEE Market Overview by country

• No substantial pace change in 2013 - limited investments

• With the exception of Kazakhstan and Azerbaijan, foreign financing key

factor to select contractors (Korean in Uzbekistan, Japanese, Korean and

Chinese in Turkmenistan), unless specific technological content applies

• Local content in some countries a differentiator

• Azerbaijan

High potential market - Western-type contracting approach.

Funds not an issue

Koreans entering into the market

SOCAR main investor- domestic/abroad investments (Turkey, Georgia, Kyrgistan)

Uzbekistan

Significant gas resources - subject to foreigners partners interest (Kogas, Indorama, Sasol, Lukoil, etc.) – market controlled by Koreans

Kazakhstan

Development of existing Oil/Gas fields (Kashagan, Karachganak, etc);

Modernization of refineries (Shymkent and Pavlodar)

Turkmenistan

• Gas resources and dominant presence of Koreans, Chinese and Japanese.

• Japanese contractors favoured by recent governmental agreements

CIS

• Market: significant increase expected

• Oil & Gas sector reorganization (led by Rosneft)

• Refining: substantial investments in modernization (Rosneft,

Gazpromneft, Bashneft) to comply with more stringent requirement

(Euro V 2015 specifications) - 124 future units in existing refineries by

2020. Major Projects Capex 34B€ up to 2020; 1 - 2 new Refineries to

be launched on 2016

• Gas processing: first NG world producer (20% worldwide production);

Gazprom (70% production) monopolistic approach limits investments;

however two non-Gazprom major LNG EPC projects (Yamal and

Sakhalin) under way – opening of gas processing market in the future;

• Petrochemicals: focus on ethylene, PE, PP (Sibur, UPC, Lukoil and

Rosneft) - 6 petrochemical clusters to be developed: West-Siberian,

Volga River, Caspian, East-Siberian, North-Western and Far-Eastern.

• Market drivers: Surplus of petrochemical feedstock, low size of

existing petrochemical facilities (avg 300 kT/year) compared to

worldwide economical scale (1 MT/year), technological obsolescence

• Relevance of local content

• Russian Majors investing also abroad (Rosneft, Lukoil, etc.)

• Growing investment cooperation between Russia and China

• Rosneft to export to China 365mln tons of crude oil over next 25 years;

Russia is China’s biggest energy supplier.

RUSSIA

• Still recession

• Refining: improve profitability and compliance to Euro V

• Polyolefins/derivatives: opportunity of domestic market growth

• Potential investments in gas, re-gasification and export facilities pending

developments in shale gas and offshore fields in East Mediterranean Sea

SEE

18

Russia - CA - SEE Market Overview by sector

Capex for announced projects

Source: TPIT Internal Research 19

20

Russia - CA - SEE Market Overview by sector

Onshore accessible Market (m€); >50%GO

Onshore by Product Line

0

1000

2000

3000

4000

5000

6000

7000

2011A 2012A 2013 2014 2015 2016

GasProc

Petrochemicals & Fertilizers

Refining

0

1000

2000

3000

4000

5000

6000

7000

2011A 2012A 2013 2014 2015 2016

SEE

Central Asia

Russia

20

A developing market expected to stabilize growth pace in the medium term - driven by Russia

Oil production and Refining

• Investments for deep conversion to increase the profitability of

large size refineries

• Refineries mondernization to increase energy efficiency and to

comply with EURO V specifications and 1-2 new Refineries to

be launched in 2016

Gas processing and derivatives

LNG/GTL

• Mega LNG projects in Russia (Yamal, Sakhalin,Vladivostok)

• LNG export facilities linked to the development of offshore field in the East Mediterranean basin

• In Central Asia future investments aimed at shipping the extracted gas to China which is financing and building pipelines.

• New GTL in Uzbekistan

Petrochemicals

Integration of Refining and Petrochemicals Plants for

profitability increase (SOCAR future complex)

Several prospects for Ethylene plants and Petrochemicals

derivates (Sibur, Rosbeft, UPC, Lukoil in Russia)

Fertilizers

Fertilizers initiatives depending on Gas price evolution

Source: TPIT Internal Research

Offshore

Russia - CA - SEE Market Overview by sector

Caspian see: among the first three contributors to the Fixed

Platform CAPEX

Northern Caspian Sea: a shallow water area (between 5 and 10

meters of water depth on average) - Artificial Islands (Kalamkas)

and Fixed Platforms Clusters the preferred Field Development

solutions

Kazakhstan: two large projects in the future (Kalamkas, Pearls)

Russia: Kuvikina Field Development

Caspian Sea

$US 15 bn $US 15 bn

• Cyprus offshore gas reserves: Government awarded licenses for six

blocks to Noble, JV Eni-KOGAS and Total - up to 40 tcf

corresponding to approx. €4B/year in Government revenue

• Total estimated natural gas reserves for Cyprus:in the range of 60tcf.

• The East Mediterranean basin: up to 100 tcf of gas resources

becoming one of the main producers in the region

Mediterranean Sea

$U

SB

CAPEX for Fixed Platforms by Regions

The Arctic under appraisal - may hold up to 13% of the

global oil reserves, 30% of the gas reserves with 80% of

these reserves located Offshore

Arctic Sea

• Potential key offshore projects in Black Sea states : Neptun Deep,

Khan Asparuh and Skifska blocks

• Rosneft and ExxonMobil could revitalize Tuapse Trough project

(11,500 square kilometers - 1,000 to 2,000 meters water depth) in

the Russia Continental Shelf of the Black Sea

• Discovered in 2003 and with 3D seismic survey completed in 2010,

the Tuapse Trough project is very similar to Gulf of Mexico

deepwater project.

Black Sea

21

22

North Africa – Egypt and Libya

• Egypt and Libya Market

• Overview by country

• By sector

Egypt and Libya Market Overview by country

Investment restarted

Army supporting Country stabilization road map, aiming

at GDP growth

Country targets: double gas production and “zero”

balance of trade in petroleum products

Foreign investors renewed interest for the Country:

BP report a new important gas discovery

BG, Shell, ENI are planning to increase

production from the existing gas fields

On September 2013 GCC countries announced

that will lead the investments in Petrochemicals

and Refinery (30b$)

On September 2013 Sinopec bought 33% of

Apache Egypt (3,1b$) to pursue new Western

Desert oil discoveries

On September 2013 Total has acquired a large

portion of the fuel stations

EGYPT

Still a “stand by” period

Control of Libyan territory is the key issue to stabilize

the Country for steady operations and new projects

Potential developments:

ENI target to increase production from fields

connected to Mellitah complex

NOC aiming at 2mb/d of oil, 0,8mb/d of new

refinery capacity (LERCO, Zwara, Tobruk), 1

mt/y of LNG (new train in Brega) and a new JV

for Polyethylene in RASCO.

Repsol-OMV, ENI, Conoco Philips, Total will be

the pioneers of the new Oil Exploration &

Production

LYBIA

23

Egypt and Libya Market

Overview by sector

-

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2013-2014 2015-2016

M U

S $

DOWNSTREAM MARKET TREND AFRICA - Egypt and Libya

Libya

Egypt

Capex for announced projects

24 Source: TPIT Internal Research

Egypt and Libya Market Overview by sector

Investments Key contributor to the stabilization of the

countries economy

Egypt

Investments driven by the need to fill the gap between internal demand and potential refining capabilities

Libya

Recovery of the production level before arab spring

Oil production and Refining

• Egypt: refining plan (new refinery and revamping of existing) to reduce negative balance of trade: a new Refinery (SRPC Soukhna Refinery) and upgrading of the existing ones (Midor)

• Libya: existing refineries looking at foreign investments for upgrading (LERCO: Ras Lanuf Revamping)

Gas processing and derivatives

Egypt: large proven gas reserves; foreign investments needed to fully re-start:

• In E&P (currently slow by only few IOC’s mainly in off-

shore)

• In Petrochemical (also aimed to promote plastics

clusters) – new potential Petrochemical Complex

(Tahrir) -

• In Fertilizer complex to boost agriculture

Libya: new E&P potential investments (ENI, BP, Repsol, Conoco & Total) – potential future projects in LNG and Ethylene

-

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

2011A 2012A 2013F 2014 2015 2016

Libya Petrochemical

Libya Refinery

Libya LNG

Libya upstream

Egypt Petrochemical

Egypt Refinery

Egypt LNG

Egypt upstream

Onshore accessible Market (m€); >50%GO

25 Source: TPIT Internal Research

Mauro Montefiore Chief Business Officer Technip Region B

24/10/2013 Le strategie di mercato per la filiera dell’impiantistica italiana 26

MARKET TRENDS

THANK YOU !