market risk analysis prof ian giddy stern school of business new york university lib

Post on 22-Dec-2015

215 views

TRANSCRIPT

Market Risk Analysis

Prof Ian Giddy

Stern School of Business

New York University

LIB

Copyright ©1998 Ian H. Giddy Risk Analysis 5

Risk Management is a Process

Risk Management

DefineDefine MeasureMeasure ManageManage MonitorMonitor

Copyright ©1998 Ian H. Giddy Risk Analysis 6

Market Risk Measurement

VolumetricVolumetric Duration/ Duration/ PVof01PVof01

Option Option Sensitivity Sensitivity MeasuresMeasures

SimulationsSimulationsValueValue

atatRiskRisk

• Notional Amounts

• Linear risk measures

• Swap/ bond equivalents

• Non-linear risk measures

• Delta, gamma, vega, theta, rho

• No aggregation of risk measures across asset classes or instruments

• Limited market scenarios that could include market correlations

• Reprice portfolio• Parallel and non-

parallel curve shifts

• Aggregate portfolio risk per scenario

• Distribution of market moves and portfolio values

• Includes market correlations

• Reprice portfolio• Aggregate risk

measures within confidence interval

Where are we now? Where do we need to be?

Copyright ©1998 Ian H. Giddy Risk Analysis 7

An Overview of Corporate VAR

Mean

Estimates of Cash Flow Distribution

• Volatilities• Correlations

Base rates/ Currency market conditions

Historical rates/ Discrete scenarios

Model 1

Model 2

Model 3

Model 4

Interest Rates

Currencies

Equities

Commodities Impact on Earnings

Business 2

Business 1

Business 3

Transactional Database

Projected Revenues

Projected Operating Costs

PortfolioDatabase

Copyright ©1998 Ian H. Giddy Risk Analysis 8

Summary of “Value at Risk” Reporting

“At close of business each day tell me what the market risks are across all businesses and locations.”

Dennis Weatherstone, JP Morgan

Logical steps:Economic-value accounting (need market prices

or models)Volatilities and correlations of market pricesMeasurement of Risk ExposureManagement of riskMarket-price based performance measurement

Copyright ©1998 Ian H. Giddy Risk Analysis 9

Portfolio Diversification

DM position A$ position S$ position FIM position

Net effect?

Copyright ©1998 Ian H. Giddy Risk Analysis 10

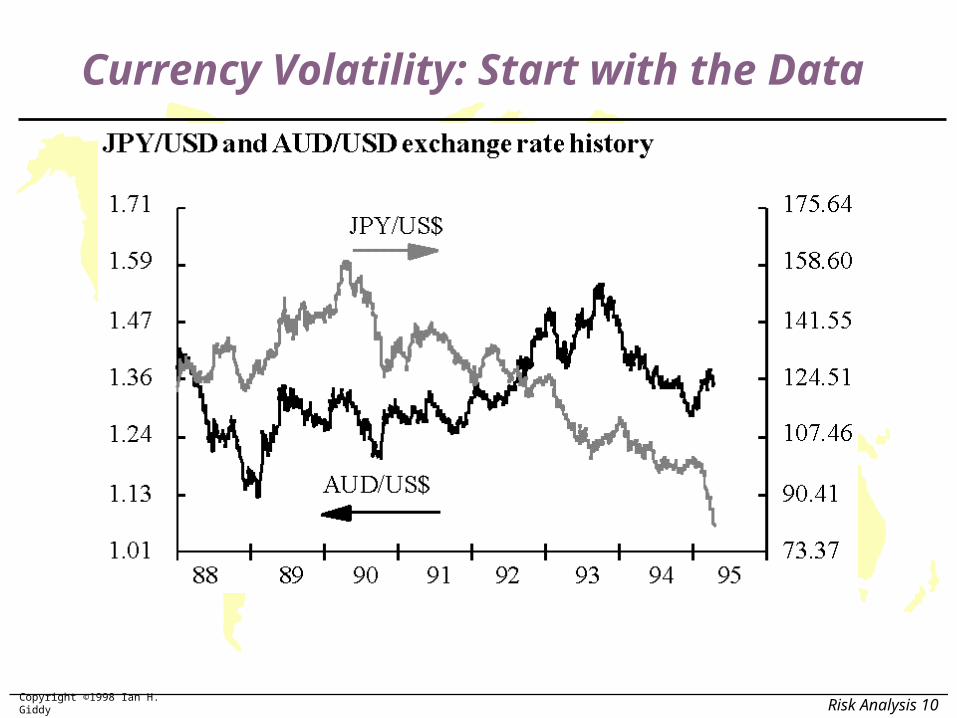

Currency Volatility: Start with the Data

Copyright ©1998 Ian H. Giddy Risk Analysis 11

Calculate Daily % Changes

%

S

S1

Copyright ©1998 Ian H. Giddy Risk Analysis 12

Predict Volatilities

RiskMetrics

(exponential smoothing)

BIS

(rolling historicals)

Copyright ©1998 Ian H. Giddy Risk Analysis 13

RiskMetrics Method Compared

RM

BIS

n

t t

t jj

n

21

21

2

2 2

1

1

0 94

1

( )

.

Copyright ©1998 Ian H. Giddy Risk Analysis 14

RiskMetrics Method Compared

Other methods include: Implied volatility from option prices Structured volatility models (ARCH, GARCH,

EGARCH) Stochastic volatility

The task of most models is to find

some historical pattern of volatility

and to use this to forecast volatility,

which seems to “cluster

Copyright ©1998 Ian H. Giddy Risk Analysis 15

Get Volatility and Correlation Estimates...eg from RiskMetrics

On the World Wide Web, RiskMetrics publications and data may be found at:

http://www.jpmorgan.com and http://www.riskmetrics.reuters.com

Copyright ©1998 Ian H. Giddy Risk Analysis 16

RiskMetrics Coverage

...plus about a dozen

commodities,term structure

of yields, more exotics...

each day, about 450

volatilities and 100,000

correlations.

Copyright ©1998 Ian H. Giddy Risk Analysis 17

Now More...(and Later, Customizable)

Copyright ©1998 Ian H. Giddy Risk Analysis 18

Estimated Volatilities

AUD

BEF

CAD

DKK

FFR

DEM

ITL

JPY

NLG

ESB

SEK

CHF

GBP

XEU

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5%

Standard Deviation

AUD

BEF

CAD

DKK

FFR

DEM

ITL

JPY

NLG

ESB

SEK

CHF

GBP

XEU

Cu

rren

cy

Currency Volatilities

Copyright ©1998 Ian H. Giddy Risk Analysis 19

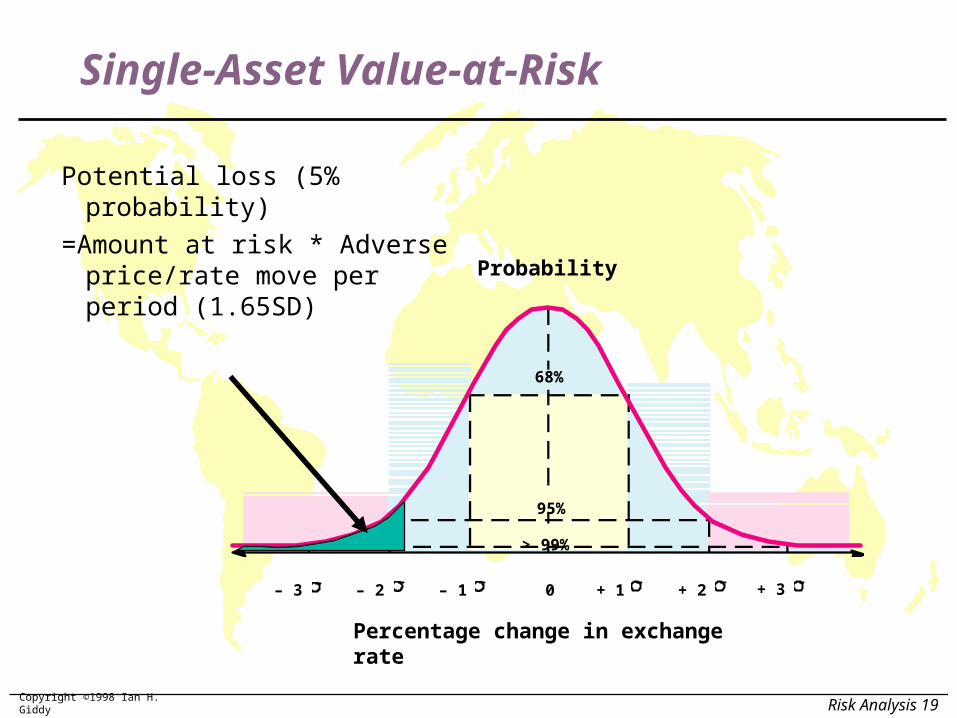

Single-Asset Value-at-Risk

Probability

Percentage change in exchange rate

68%

95%

> 99%

– 3 – 2 – 1 0 + 1 + 2 + 3

Potential loss (5% probability)

=Amount at risk * Adverse price/rate move per period (1.65SD)

Copyright ©1998 Ian H. Giddy Risk Analysis 20

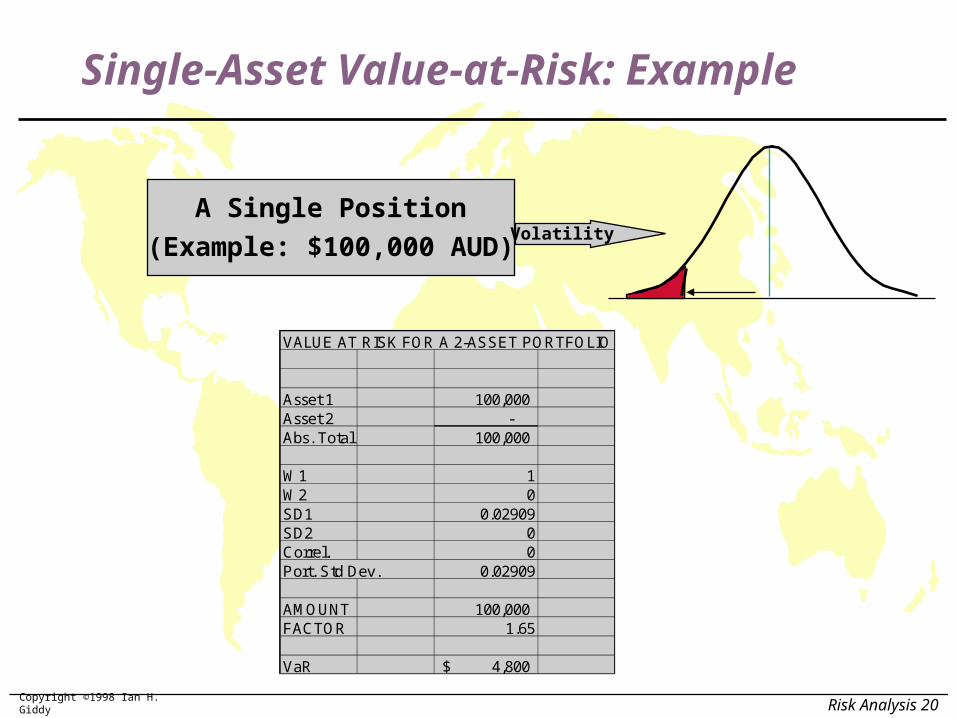

Single-Asset Value-at-Risk: Example

A Single Position

(Example: $100,000 AUD)Volatility

VALUE AT RISK FOR A 2-ASSET PORTFOLIO

Asset 1 100,000 Asset 2 - Abs. Total 100,000

W1 1W2 0SD1 0.02909SD2 0Correl. 0Port. Std Dev. 0.02909

AMOUNT 100,000 FACTOR 1.65

VaR 4,800$

Copyright ©1998 Ian H. Giddy Risk Analysis 21

Estimated Correlations

CAD AUD DEM JPY GBP ZAR

CAD

AUD

DEM

JPY

GBPZAR

-0.2

0

0.2

0.4

0.6

0.8

1

CO

RR

EL

AT

ION

Copyright ©1998 Ian H. Giddy Risk Analysis 22

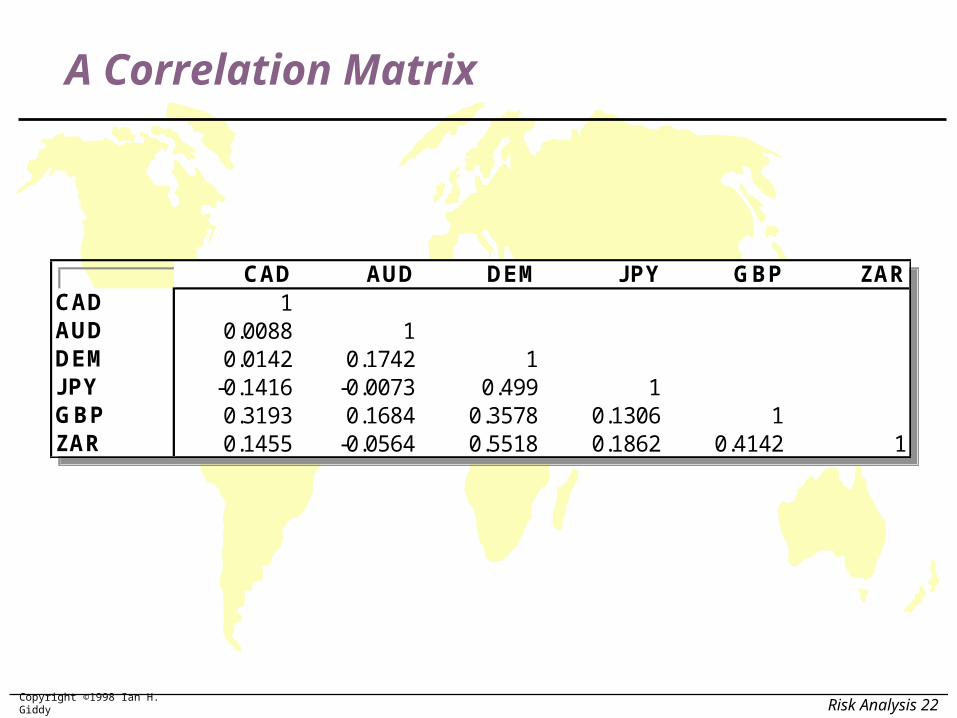

A Correlation Matrix

CAD AUD DEM JPY GBP ZARCAD 1AUD 0.0088 1DEM 0.0142 0.1742 1JPY -0.1416 -0.0073 0.499 1GBP 0.3193 0.1684 0.3578 0.1306 1ZAR 0.1455 -0.0564 0.5518 0.1862 0.4142 1

CAD AUD DEM JPY GBP ZARCAD 1AUD 0.0088 1DEM 0.0142 0.1742 1JPY -0.1416 -0.0073 0.499 1GBP 0.3193 0.1684 0.3578 0.1306 1ZAR 0.1455 -0.0564 0.5518 0.1862 0.4142 1

Copyright ©1998 Ian H. Giddy Risk Analysis 23

Measuring Portfolio Exposure: Two Assets

The variance of a 2-asset portfolio, :

where wA and wB are the weights of A and B in the portfolio.

To evaluate the gains and structure of a portfolio, we need a variance-covariance matrix:

$ AT RISK VOL. AUD BEF

AUD $50,000 2.909% 1

BEF $50,000 4.573% -0.273 1

P2

A2

A2

B2

B2

A B A B A B = w + w + 2 w w

Copyright ©1998 Ian H. Giddy Risk Analysis 24

Two-Asset Value-at-Risk: Example

Two Positions

(Example: $100,000 AUD & BEF)Volatility &

Correlation

VALUE AT RISK FOR A 2-ASSET PORTFOLIO

Asset 1 50,000 Asset 2 50,000 Abs. Total 100,000

W1 0.5W2 0.5SD1 0.02909SD2 0.04573Correl. -0.273Port. Std Dev. 0.02351

AMOUNT 100,000 FACTOR 1.65

VaR 3,879$

Copyright ©1998 Ian H. Giddy Risk Analysis 25

Return and Risk, Generalized

Portfolio return:

where wi are the weights of each asset in the portfolio. (Expected return is simply the weighted sum of the individual asset returns.)

Portfolio variance:

When i = j, the term wiwj becomes wi2

E(R ) = w E(R )pi=1

n

i i

P2

i=1

n

j=1

n

i j ij i j = w w

ij i j i 2

Copyright ©1998 Ian H. Giddy Risk Analysis 26

Portfolio Value at Risk

Mean

Value-at-RiskValue-at-Risk

+

=

EXPOSURES AND HEDGESCURRENCY Po s itio n Hedg e

1 CAD 460 -1382 AUD - 305 91.53 DEM 425 -127.54 JPY - 220 665 GBP 735 -220.56 ZAR 295 -88.5

EXPOSURES AND HEDGESCURRENCY Po s itio n Hedg e

1 CAD 460 -1382 AUD - 305 91.53 DEM 425 -127.54 JPY - 220 665 GBP 735 -220.56 ZAR 295 -88.5

Copyright ©1998 Ian H. Giddy Risk Analysis 27

A Management-Friendly Report

An example is FourFifteen™, named after J.P. Morgan's market risk report produced at 4:15 p.m. each day.

The "4:15 Report," a single sheet of paper, summarizes the Daily Earnings at Risk for J.P. Morgan worldwide.

Portfolio Risk Simulation USD Base. Vols. & correls. as of May 04, 1995.

AUD BEF CAD DKK FFR DEM ITL JPY NLG ESB SEK CHF GBP XEU USD Total

1 Mo 15 22 37

3 Mo -200 20 -30 160 - 50

6 Mo 25 -5 20

12 Mo -105 - 105

2 Yr 0

3 Yr 0

4 Yr 0

5 Yr 0

7 Yr 0

9 Yr 0

10 Yr 0

15 Yr 0

20 Yr 0

30 Yr 0

Equity 0

Implied - 196.1 59 22 -29 54 -145

Spot 23 23

Net - 196.1 82 22 -29 -122

Int. 502 262 5 139 400 740

Eq.

Fx 5,048 4265 1383 1820 8516

divers. -200 -347 -6 -83 -451

Net 5,350 4181 1383 1876 400 8805

R

ISK

($00

0)

RiskMetricsª

G

ov'

t B

on

ds

Zer

o C

ash

flo

w

FX

Copyright ©1998 Ian H. Giddy Risk Analysis 28

Exposure Report: Example

Portfo lio Ris k S imulationUSD Base. Vols. & correls . as of May 04, 1995.

AUD BEF CAD DKK FFR DEM ITL JPY NLG ESB SEK CHF GBP XEU USD Total

1 Mo 15 22 37

3 Mo -200 20 -30 160 - 50

6 Mo 25 -5 20

12 Mo -105 - 105

2 Yr 0

3 Yr 0

4 Yr 0

5 Yr 0

7 Yr 0

9 Yr 0

10 Yr 0

15 Yr 0

20 Yr 0

30 Yr 0

Equity 0

Implied - 196.1 59 22 -29 54 -145

Spot 23 23Net - 196.1 82 22 -29 -122

Int. 502 262 5 139 400 740

Eq.

Fx 5,048 4265 1383 1820 8516

divers . -200 -347 -6 -83 -451

Net 5,350 4181 1383 1876 400 8805

RIS

K ($

000)

RiskMetricsª

Gov

't B

onds

Zer

o C

ashf

low

FX

Copyright ©1998 Ian H. Giddy Risk Analysis 29

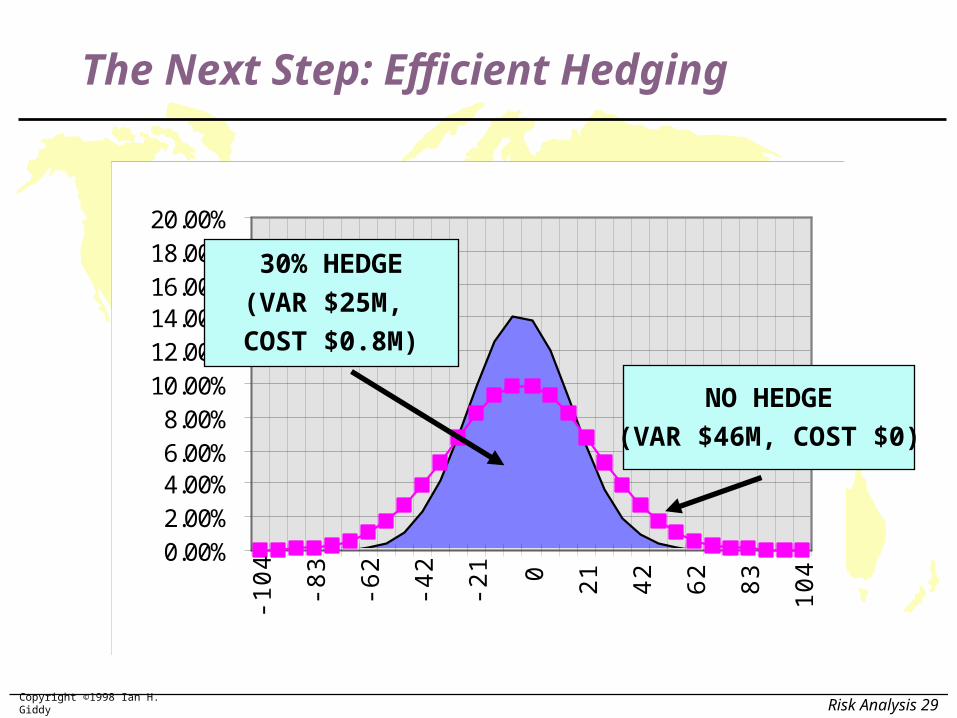

The Next Step: Efficient Hedging

0.00%2.00%4.00%6.00%8.00%

10.00%12.00%14.00%16.00%18.00%20.00%

-104 -83

-62

-42

-21 0 21 42 62 83 104

30% HEDGE

(VAR $25M,

COST $0.8M)

NO HEDGE

(VAR $46M, COST $0)

Copyright ©1998 Ian H. Giddy Risk Analysis 30

Efficient Hedging, Constrained

FX Hedging: Cost and Risk Computation (monthly data)EXPOSURES AND HEDGES POSITION RISKS CORRELATION MATRIXCURRENCY Pos ition Hedge WEIGHTCOST PREMIUM STD DEV VaR CAD AUD DEM JPY GBP ZAR

1 CAD 460 -138 0.01% 0.18% 0.99% 5.24 12 AUD - 305 91.5 0.00% 0.07% 2.52% 8.88 0.009 13 DEM 425 -127.5 0.01% 0.21% 2.84% 14 0.014 0.17 14 JPY - 220 66 -0.01% 0.43% 3.27% 8.32 -0.14 -0.01 0.499 15 GBP 735 -220.5 -0.01% -0.12% 2.56% 21.7 0.319 0.17 0.358 0.131 16 ZAR 295 -88.5 -0.02% -0.78% 1.21% 4.13 0.146 -0.06 0.552 0.186 0.414 1

TOTAL 2440 732 62.3Hedge% 30%Currency Portfo lio "return" -0.02% ($0.8) Portfo lio Std Deviation 0.61%

nhVAR (95%)= 25 46

HEDGE COST= ($0.8) $0

0.00%2.00%4.00%

6.00%8.00%

10.00%12.00%14.00%

16.00%18.00%20.00%

-104 -83

-62

-42

-21 0 21 42 62 83 104

NO HEDGE

Copyright ©1998 Ian H. Giddy Risk Analysis 31

Efficient Hedging, Constrained

FX Hedging: Cost and Risk Computation (monthly data)EXPOSURES AND HEDGES POSITION RISKS CORRELATION MATRIXCURRENCY Pos ition Hedge WEIGHTCOST PREMIUM STD DEV VaR CAD AUD DEM JPY GBP ZAR

1 CAD 460 -460 0.02% 0.18% 0.99% 0 12 AUD - 305 305 0.00% 0.07% 2.52% 0 0.009 13 DEM 425 -425 0.02% 0.21% 2.84% 0 0.014 0.17 14 JPY - 220 113.23 -0.01% 0.43% 3.27% 5.77 -0.14 -0.01 0.499 15 GBP 735 -735 -0.02% -0.12% 2.56% 0 0.319 0.17 0.358 0.131 16 ZAR 295 803.22 0.12% -0.78% 1.21% 22 0.146 -0.06 0.552 0.186 0.414 1

TOTAL 2440 2841.5 27.7Hedge% 75%Currency Portfo lio "return" 0.12% $6.4 Portfo lio Std Deviation 0.25%

nh optVAR (95%)= 10 46 10

HEDGE COST= $6.4 $0 $6.40

0.00%2.00%4.00%6.00%8.00%

10.00%12.00%14.00%16.00%18.00%20.00%

-104 -83

-62

-42

-21 0 21 42 62 83 104

NO HEDGE

Copyright ©1998 Ian H. Giddy Risk Analysis 32

FIRM'S INT'LBUSINESS

BOOKED &ANTICIPATED

TRANSACTIONS

REPORTINGSYSTEM

SCHEDULE OFFX FLOWS

PORTFOLIOANALYSIS OF

FX EXPOSURE

NETEXPOSURESIN FOREIGN

CURRENCIES

MEASUREMENTOF FX RISK BY

CURRENCY

RISKMANAGEMENT

DECISIONS

CORRELATIONDATA

VOLATILITYDATA

HEDGINGTRANSACTIONS

The VaR Management Cycle

This process can be undertaken on a monthly cycle basis, as the institution revises its estimates of future business and as new data on volatilities and correlations are acquired.

Copyright ©1998 Ian H. Giddy Risk Analysis 33

Value at Risk: Assessment

Value at Risk and RiskMetrics: A method for quantifying risk in dynamic,

uncertain environments Based on the observation that volatilities

and correlations are somewhat persistent The RiskMetrics estimates are in the

ballpark of other, more sophisticated, methods

Copyright ©1998 Ian H. Giddy Risk Analysis 34

Value at Risk: Assessment

Copyright ©1998 Ian H. Giddy Risk Analysis 35

Value at Risk: Assessment

Copyright ©1998 Ian H. Giddy Risk Analysis 36

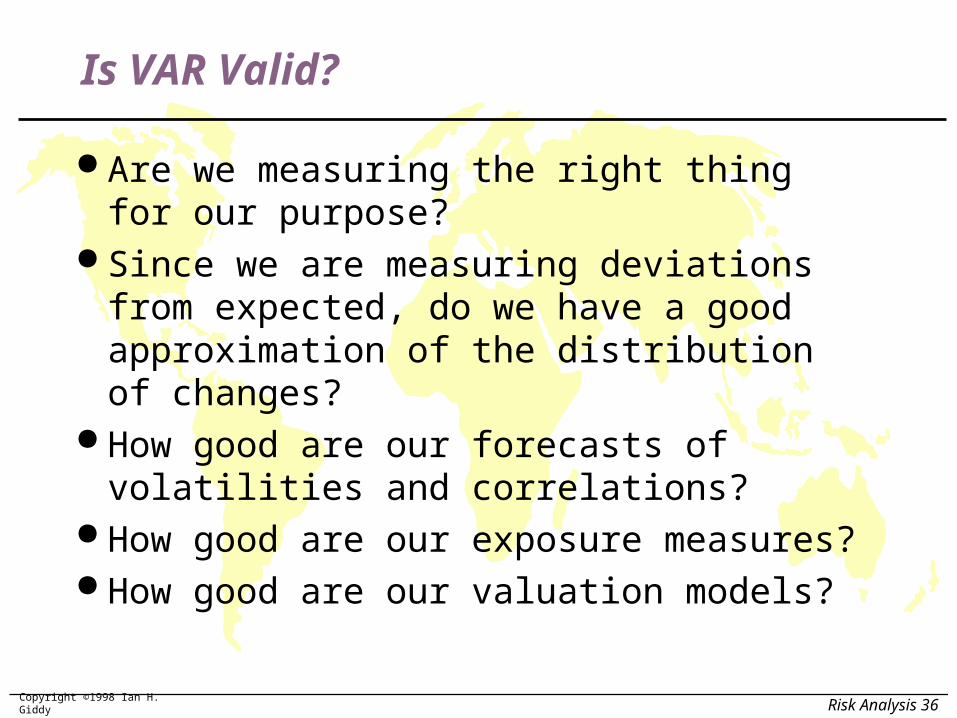

Is VAR Valid?

Are we measuring the right thing for our purpose?

Since we are measuring deviations from expected, do we have a good approximation of the distribution of changes?

How good are our forecasts of volatilities and correlations?

How good are our exposure measures? How good are our valuation models?

Copyright ©1998 Ian H. Giddy Risk Analysis 37

Alternatives

Worst-case analysis Scenario analysis Historical simulation Monte-Carlo simulation Sensitivity measures

Copyright ©1998 Ian H. Giddy Risk Analysis 38

Mean

What Happens in the Tails?

For credit and capital purposes, we want to know about the probability, size and impact of extreme events.

Worst-Case Analysis:How skewed?How many?How large?Probability of extreme events?

Copyright ©1998 Ian H. Giddy Risk Analysis 39

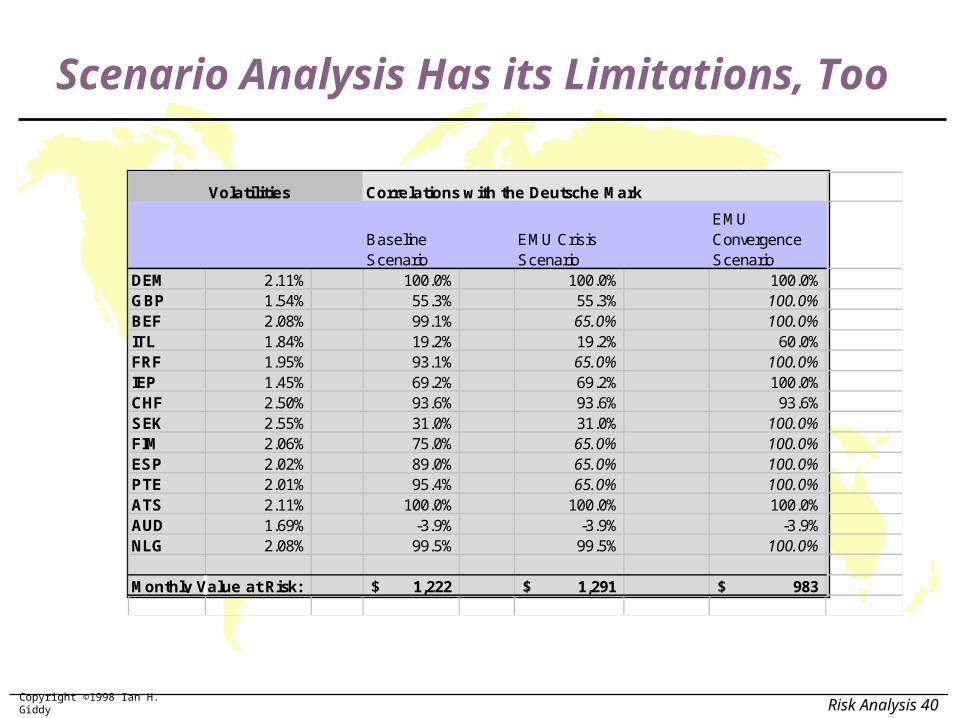

Baseline ScenarioThis scenario assumes that current predictions of volatilities and correlations are valid for Publicorp’sFX risk management horizon. As is shown in the table below, the monthly volatility -- defined asthe standard deviation of percentage changes in the dollar value of foreign currencies -- rangesfrom 1.69% for the Canadian dollar to 2.55%% for the Swedish Krona. The correlations betweenthe DM and the core European currencies are very high - for example, the French franc has a 98%correlation with the DM - while the other European currencies have a positive but lowercorrelation coefficient. In particular, the British pound’s correlation with the DM is 55%. Thetable shows that the Value-at-Risk (VaR) for Publicorp’s existing, unhedged positions is $1.222million.

EMS Crisis ScenarioUnder this scenario, we assume that the “inner core” European currencies, the mark, guilder andAustrian schilling, remain closely linked, but that the correlations between German mark and theBelgian franc, the French franc, Finnish markka, Spanish peseta and Portuguese escudo all fall to65%. The result of this is to increase the VaR to $1.291 million -- not a dramatic increase.

EMS Convergence ScenarioThe third scenario is one in which the correlations among all the major European Unioncurrencies rise to 100%. This could be regarded as the “single currency in Europe” scenario.Because of Publicorp’s offsetting long and short positions in these currencies, the result is a reductionin currency exposure: the monthly VaR drops to below $1 million.

EMU Scenario Analysis for Publicorp

Copyright ©1998 Ian H. Giddy Risk Analysis 40

Volatilities Correlations with the Deutsche Mark

Baseline Scenario

EMU Crisis Scenario

EMU Convergence Scenario

DEM 2.11% 100.0% 100.0% 100.0%GBP 1.54% 55.3% 55.3% 100.0%BEF 2.08% 99.1% 65.0% 100.0%ITL 1.84% 19.2% 19.2% 60.0%FRF 1.95% 93.1% 65.0% 100.0%IEP 1.45% 69.2% 69.2% 100.0%CHF 2.50% 93.6% 93.6% 93.6%SEK 2.55% 31.0% 31.0% 100.0%FIM 2.06% 75.0% 65.0% 100.0%ESP 2.02% 89.0% 65.0% 100.0%PTE 2.01% 95.4% 65.0% 100.0%ATS 2.11% 100.0% 100.0% 100.0%AUD 1.69% -3.9% -3.9% -3.9%NLG 2.08% 99.5% 99.5% 100.0%

Monthly Value at Risk: 1,222$ 1,291$ 983$

Scenario Analysis Has its Limitations, Too

Copyright ©1998 Ian H. Giddy Risk Analysis 41

The Alternative: Full-Valuation Methods

Prices, rates, and

estimated variances

and covariances

Monte Carlo

Simulation

Generate

Scenarios

Full

Valuation

Distribution of

Values

Distribution of

Values

Delta-Gamma

Valuation

Estimated value

changes

Estimated value

changes

MODELS

Copyright ©1998 Ian H. Giddy Risk Analysis 42

The Sharpe ratio.(actual return relative to actual risk)

The risk ratio.(actual return relative to prospective risk)

The efficiency ratio.(actual risk relative to prospective risk)

Use risk-return performance measures to evaluate individual trader performance.

Using a VaR Measure for Trading-Portfolio Performance Evaluation

Copyright ©1998 Ian H. Giddy Risk Analysis 46

Performance Evaluation: ExampleFARMCO: PERFORMANCE EVALUATIONOct. 1 1995

Predicted exposures Spot Forward

Expected Return Volatility Hedge

CAD -200758 1.3374 1.3405 1.0% 1.79 150000DEM 22365 1.4288 1.4165 2.5% 3.82 0JPY -15688 100.39 97.83 2.0% 3.71 10000Portfolio expected profit 1,180 Portfolio total VaR 9,337 Portfolio diversified VaR 5,210 Expected gain, relative to risk (VaR) 23%April 1 1996

Actual Exposures

Actual Spot

Actual Return

Actual Volatility Hedge

CAD -220400 1.3736 2.5% 2.1 150000DEM 24000 1.3901 1.9% 4.2 0JPY -11500 97.00 -0.8% 5.3 10000Portfolio actual profit 1,278 Portfolio total VaR 11,251 Portfolio diversified VaR 5,913 Actual gain, relative to actual risk (VaR) 22%

Adjusted gain, based on predicted exposures 788 Adjusted gain, relative to actual risk (VaR) 13.3%Adjusted gain, relative to ex-ante risk (VaR) 15.13%

Copyright ©1998 Ian H. Giddy Risk Analysis 47

Performance Measurement: Roadmap

FINANCIAL SIDE

OPERATIONAL SIDE

EXPOSURES Known Anticipated

Map exposures

Map risks

Manage risks

Measure performance Take actions to improve

performance

MARKET PRICES

MARKET VOL & CORR.

RISK MEASUREMENT VaR Worst-case scenario, etc.

RISK MANAGEMENT Hedging Investment or trading

PERFORMANCE MEASUREMENT Relative return Relative risk.

INCENTIVES ALLOCATION OF RESOURCES.

Copyright ©1998 Ian H. Giddy Risk Analysis 48

Performance evaluation: “the science of attribution”

Why did we make/lose money?The market; the FX manager; my

lousy instructions? How much should I tip this FX

manager? Would I use this method again? How good is my performance

measurement system?

Treasury Performance Measurement: Conclusion

Copyright ©1998 Ian H. Giddy Risk Analysis 49

Summary: Market Risk Management is a Process

Risk Management

DefineDefine MeasureMeasure ManageManage MonitorMonitor

Copyright ©1998 Ian H. Giddy Risk Analysis 55

Ian H. Giddy

Professor of Finance

Stern School of Business

New York University

44 West 4th Street, New York, NY 10012, USA

Tel 212-998-0332; Fax 212-995-4233

Email: [email protected]

World Wide Web: http://giddy.org