market pulp outlook - pwc west fraser hinton canada -120 nbsk q4 2006 tembec smooth rock fallscanada...

TRANSCRIPT

HAWKINS WRIGHT

Market pulp outlook PwC 24th Annual Global Forest & Paper Industry Conference Vancouver, May 2011

HAWKINS WRIGHT

Macro-economic factors have been most influential in past 2 cycles…

0

50

100

150

200

250

'80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10

Index 2005=100

Pulp prices versus other commodities

The Economist Industrial Commodity (US$) Price Index

NBSK Market Pulp Price

Source: The Economist, Hawkins Wright

HAWKINS WRIGHT

Prices trending down in most major currencies since July 2010

50

60

70

80

90

100

110

120

130

140

150

160

170

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Index Jan 2006 = 100

Euro zone (€)

US $

Canada (C$)

Brazil (real)

China (yuan)

April 2011

Note: NBSK (PIX) prices converted into other currencies and expressed as an index. The exception is Brazil which is a conversion of the BEKP (PIX) price. Data: FOEX (PIXprices) and OANDA.com (exchange rates).

Pulp prices (PIX) in US dollars and other currencies

HAWKINS WRIGHT

Prices have increased despite apparent over-capacity…

75%

80%

85%

90%

95%

100%

105%

0

200

400

600

800

1000

1200

Shipmenttocapacityratio

AverageNBSKprice,US$/t

AverageNBSKprice Shipment‐ capacityratio

HAWKINS WRIGHT

…because capacity has been under-utilised

2,750

3,000

3,250

3,500

3,750

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11

(000s t)

World-20 BCP production and shipments, 3 month moving average

3 month average BCP production

3 month average BCP shipments

Source: PPPC, Hawkins Wright

Market related

Chilean earthquake

Extended maintenance

?

HAWKINS WRIGHT

Pulp mill closures since 2005…

Year Company Mill CountryImpact on mkt pulp Grade

Date of closure

2010 Sappi Usutu Swaziland -190 UKP Q1 20102009 M-Real Alizay France -70 BHKP Q2 2009

Botnia Kaskinen Finland -210 Birch Q1 2009CMPC Laja Chile -110 BSKP Q1 2009Rottneros Miranda Spain -150 BEKP Q1 2009Marathon Pulp Marathon Canada -200 NBSK Q1 2009Boise Inc. St. Helens USA -85 NBSK Q1 2009

2008 Evergreen Pulp Samoa USA -200 NBSK/UKP Q4 2008International Paper Bastrop USA -100 SBSK/fluff Q4 2008Continental Management Baikal Russia -200 NBSK/UKP Q4 2008Smurfit Pontiac Canada -200 NBHK Q4 2008UPM-Kymmene Tervasaari² Finland -210 NBSK Q4 2008Stora Enso Norrsundet Sweden -300 NBSK Q4 2008Catalyst Paper Elk Falls Canada -190 NBSK Q4 2008Kertas Nusantara Mangkajang Indonesia -150 BHKP Q3-2008Stora Enso Kemijärvi Finland -120 NBSK Q2 2008Rottneros Utansjö Sweden -180 BCTMP Q2 2008

2006 West Fraser Hinton Canada -120 NBSK Q4 2006Tembec Smooth Rock FallsCanada -200 NBSK Q3 2006Cascades Fjordcell Canada -15 NBSK Q3 2006Weyerhaeuser Cosmopolis USA -140 Specialty 2H 2006Fraser Papers Berlin USA -135 NMHW Q2 2006Bowater Thunder Bay Canada -210 NBSK/NBHK Q2 2006Korsnas Gavle Sweden -70 NBSK Q2 2006Weyerhaeuser Prince Albert Canada -130 NBSK Q2 2006Western FP Squamish Canada -275 NBSK Q1 2006

2005 Domtar Quevillon Canada -195 NBSK Q4 2005Neenah Paper Terrace Bay Canada -125 NMHW Q2 2005Rottneros Utansjo Sweden -70 BSP Q1 2005

TOTAL 2005-2010 -4,550

• Theescala*oninpulppricesfrom2006‐08wasduetorisingcosts…

• ….4.6milliontonnesofcapacityclosedpermanently

HAWKINS WRIGHT

In spite of closures, net capacity continued to grow…

Since 2007: Mucuri, Fray Bentos, Tres Lagoas, Rizhao, plus brownfield expansions in Iberia, Indonesia, and elsewhere

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Annual change in capacity (thousand tonnes)

Total capacity (thousand tonnes)

Annual change in BCP capacity

BSKP

BHKP

FORECAST

HAWKINS WRIGHT

Re-starting capacity Pulp supply is very price elastic….

Company Mill Country Capacity Grade Date of restart

Kertas Nusantara E.Kalimantan Indonesia +250 BHKP Q2-2011Arauco Arauco Chile +500 BSKP Q1-2011APRIL Kerinci iii Indonesia +600 BHKP Q4-2010Buchanan Terrace Bay Canada +350 BSKP Q4-2010Paper Excellence (APP) Mackenzie Canada +230 BSKP Q3-2010Baikalsky Lake Baikal Russia +100 UKP/DP Q3-2010Fortress Papers Thurso Canada +250 BHKP Q2-2010Catalyst Crofton (II) Canada +90 BSKP Q2-2010Stora Enso Sunila Finland +320 BSKP Q1-2010Tembec Chetwynd Canada +220 BCTMP Q1-2010Svilocell Svishtov Bulgaria +150 BHKP Q4-2009Stora Enso Enocell Finland +650 BSKP/BHKP Q4-2009Catalyst Paper Crofton (I) Canada +210 BSKP Q4-2009Nanaimo Forest Products Harmac Canada +110 BSKP Q3-2009

Total +4,030

HAWKINS WRIGHT

- 1,000 2,000 3,000 4,000 5,000 6,000

AracruzWeyerhaeuser

AraucoSodra

APRILTembec

International PaperStora Enso

Canfor*Koch Celulose

Ilim PulpWest Fraser**

Mercer InternationalBowater

Metsa BotniaENCECMPC

CenibraVotorantim

Parson & Whittemore

Capacity '000 t/y

BSKP

BHKP

UKP

Mech

2005

- 1,000 2,000 3,000 4,000 5,000 6,000

FibriaAPRIL

AraucoAPP

Georgia PacificCMPCSodra

Stora EnsoWeyerhaeuser

SuzanoBotnia/M-real

UPM-KymmeneDomtar

IlimMercer

IPENCE

West FraserCanfor Corporation

Cenibra

Capacity '000 t/y

BSKP

BHKP

UKP

BCTMP

2011

HAWKINS WRIGHT

Brazil and Uruguay BEKP, 2013-2015

Fibria (Três Lagoas )

• EldoradoCeluloseePapel:TrêsLagoas,1.5milliont/y,Q42012

• Suzano:Maranhão,+1.3‐1.5milliont/y,Q22013

• MontesDelPlata:1.3milliont/y,Q22013

• CMPC:Guaiba,+1.3‐1.5milliont/y,2014/15

• Suzano:Piauí,+1.3‐1.5milliont/y,2014/15

• Fibria:TrêsLagoasII,VeracelII• Klabin(Paraná)• Cenibra

Eldorado Celulose e Papel (Três Lagoas )

Suzano (Maranhão)

Suzano (Piauí)

CMPC (Guaiba)

Montes del Plata (Colonia)

HAWKINS WRIGHT

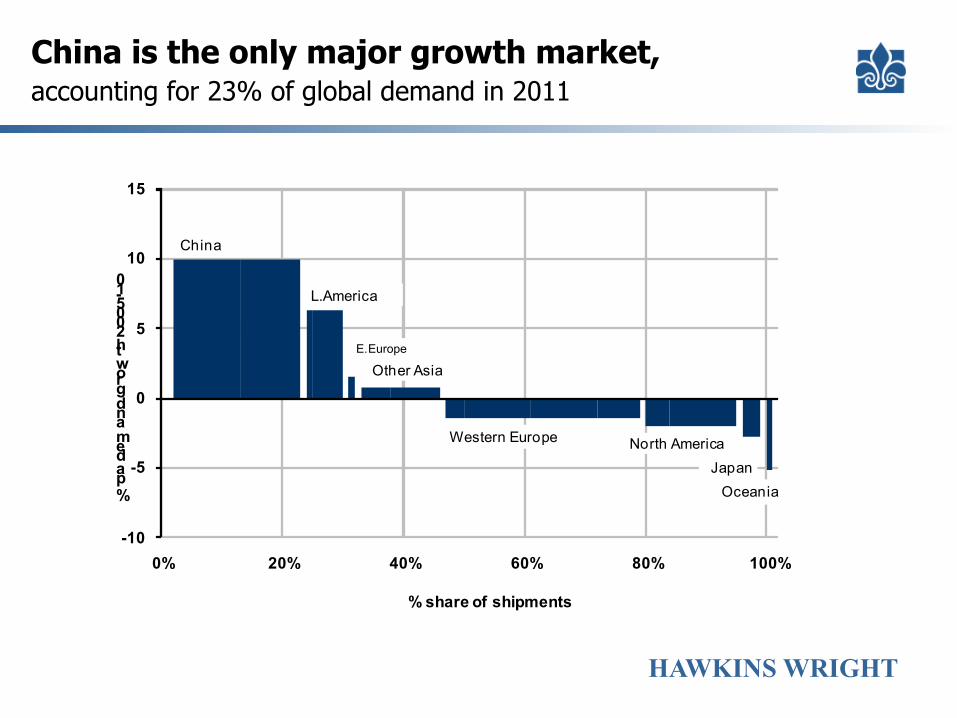

China is the only major growth market, accounting for 23% of global demand in 2011

-10

-5

0

5

10

15

0% 20% 40% 60% 80% 100%

% pa demand growth 2005-10

% share of shipments

China

L.America

E.Europe

Western Europe

JapanNorth America

Other Asia

Oceania

HAWKINS WRIGHT

Bleached pulp demand: China, Asia, & rest of world

‐

5

10

15

20

25

30

35

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011(f)

Milliontonnes

China

Restofworld

OtherAsia(ex‐Japan)

HAWKINS WRIGHT

Chinese pulp imports

0

1

2

3

4

5

6

7

8

9

10

11

12

13

1995 1997 1999 2001 2003 2005 2007 2009

milliontonnes

BCTMP

BHKP

BSKP

-

200

400

600

800

1,000

1,200

1,400

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

thousand tonnes

March 2011

HAWKINS WRIGHT

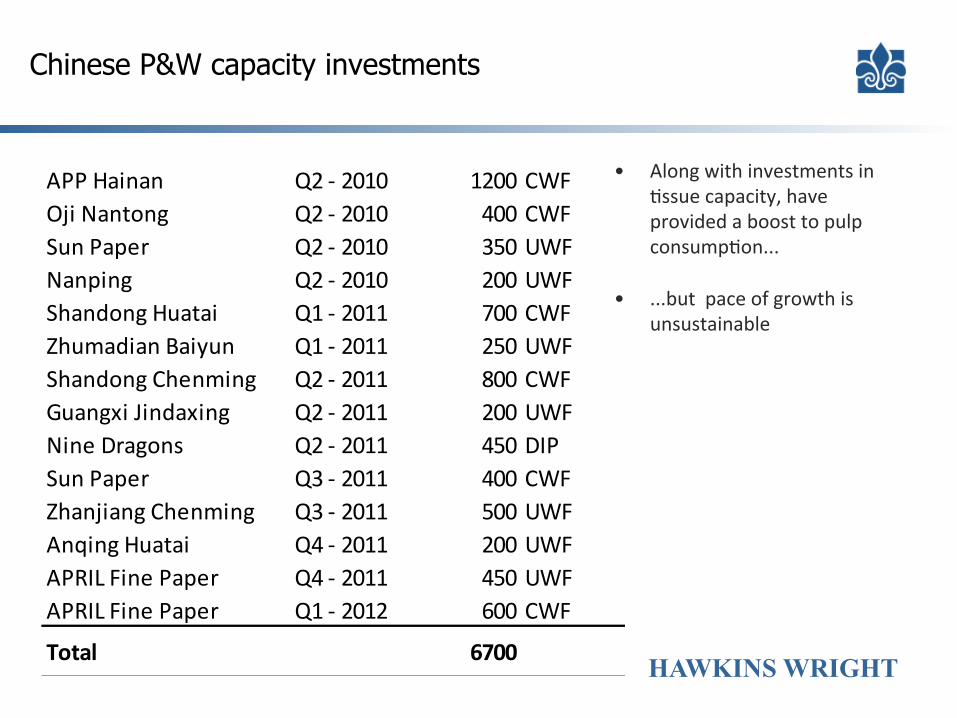

Chinese P&W capacity investments

APPHainan Q2‐2010 1200 CWFOjiNantong Q2‐2010 400 CWFSunPaper Q2‐2010 350 UWFNanping Q2‐2010 200 UWFShandongHuatai Q1‐2011 700 CWFZhumadianBaiyun Q1‐2011 250 UWFShandongChenming Q2‐2011 800 CWFGuangxiJindaxing Q2‐2011 200 UWFNineDragons Q2‐2011 450 DIPSunPaper Q3‐2011 400 CWFZhanjiangChenming Q3‐2011 500 UWFAnqingHuatai Q4‐2011 200 UWFAPRILFinePaper Q4‐2011 450 UWFAPRILFinePaper Q1‐2012 600 CWF

Total 6700

• Alongwithinvestmentsin*ssuecapacity,haveprovidedaboosttopulpconsump*on...

• ...butpaceofgrowthisunsustainable

HAWKINS WRIGHT

China growth

• DriversofChinesepaperproduc*onandimportedfibredemandinclude…> Chinesepaperdemand> Exportsectordemand> ExportsofP&B> Displacementofoldcapacity> Levelofdomes*cpulpproduc*on(dissolvingpulpconversions?)

HAWKINS WRIGHT

Summary

• Pulpwillremainstronglycorrelatedtocommoditycycles

• Costsremainthekeylongtermdriver

• Supply‐sideremainsveryfragmented,andiscon*nuallyundergoingstructuralchange

• IncreasinginfluenceofChina

• Vola*lityisheretostay

HAWKINS WRIGHT

www.hawkinswright.com

• Market intelligence > Pulpwatch

− Published 12 times a year covering developments in international pulp and paper markets > Multiclients

− Outlook for market pulp demand, supply and prices − Defining the China market

> Consulting − Feasibility studies/due diligence/ price forecasting