march 2017 owners ready for the rising tide of 1,000m², a deadweight of approximately 5,000t and an...

TRANSCRIPT

MARCH 2017

OWNERS READY FOR THE RISING TIDE

CONTENTS

Production and Administration: Seabrokers Ltd, AberdeenFor your free copy ofSeabreeze, email:[email protected]

The Seabreeze Monthly Market Report is distributed worldwide through our offices in Aberdeen, Stavanger and Rio de Janeiro.

© Seabrokers Group 2017

ABOUT SEABROKERS GROUPThe Seabrokers Group was established in 1982. We provide a unique and varied range of services to clients. The Seabrokers Group has an experienced workforce within Shipbroking, Real Estate, Facilities Management, Construction, Cranes & Transportation, Sea Surveillance and Safe Lifting Operations. Our head office is located in Stavanger, but we also have offices in Aberdeen, Bergen and Rio de Janeiro.

The Seabrokers Group is different – and we are proud of this fact. Our information, experience and knowledge provide us with the ability to perform in our diverse business areas.

Seabrokers Chartering AS and Seabrokers Ltd are certified by DNV GL in line with Management System Standard ISO 9001:2008.

OUR OFFICES:STAVANGER BERGEN SKIENABERDEEN RIO DE JANEIRO

www.seabrokers-group.com

3 OSV MARKET ROUND-UP

6 OSV AVAILABILITY, RATES & UTILISATION - NORTH SEA

7 MONTHLY OSV SPOT RATES - NORTH SEA

8 FEATURE VESSEL

9 OSV NEWBUILDINGS, CONVERSIONS, SALE & PURCHASE

11 SUBSEA

14 RENEWABLES

15 RIGS

16 CONUNDRUM CORNER & DUTY PHONES

SHIPBROKING

SECURALIFT

SEA SURVEILLANCE

REAL ESTATE

FOUNDATIONS

CRANES & TRANSPORTATIONYACHTING

FACILITY MANAGEMENT

SEABREEZE 3

OSV MARKET ROUND-UPAHTS OWNERS ENJOY RISING RATES North Sea AHTS owners have endured tough times during the market downturn, but that has all changed in recent weeks with a prolonged period of tightness on the spot market allowing some owners to pick up lucrative fixtures with rates of GBP 50,000-70,000 (NOK 535,000-750,000). This is a huge jump from the GBP 10,000-15,000 (NOK 105,000-160,000) rates that were prevalent in late 2016 and the early stages of this year. So what has happened for market dynamics to change so significantly?

Firstly, this has only happened because so many vessels are laid up. The market remains oversupplied, however owners’ attempts to bring the supply-demand balance more in their favour has helped improve their trading conditions. But there has been a considerable increase in rig move activity, with several rigs being reactivated for spring/summer drilling campaigns. With such a reduction on the supply side for the anchor handling market, it sometimes takes just two or three rig moves in quick succession to tighten availability significantly. With the rising rates comes the temptation to reactivate laid-up tonnage; however, if more than a few owners do this, then there will be abundant supply again. The reactivation decision remains a tough one for owners to make.

UK AWARDS 25 FRONTIER LICENCESThe UK’s Oil and Gas Authority has offered for award 25 new licences from its 29th Licensing Round. This was the first round in two decades to focus solely on frontier, under-explored areas of the Rockall Basin, Mid-North Sea High, and part of the East Shetland Platform.

The 25 new frontier licences cover a total of 111 blocks or part blocks, with operatorships awarded to 17 companies: Alpha Petroleum, Ardent Oil, Azinor Catalyst, BP, Centrica, Chrysaor, Decipher Energy, Draupner Energy, ExxonMobil, Nautical Petroleum, North Sea Natural Resources, Shell, Simwell Resources, Statoil, TAQA, The Steam Oil Production Company

and Zennor Petroleum.

Two of the areas which were the focus of this round (the Rockall Basin and Mid-North Sea High) were the subject of a 2015 seismic acquisition programme which was funded by the UK Government.

In contrast, the forthcoming 30th Licensing Round will focus on mature areas of the UK Continental Shelf. This is expect-ed to be the most significant UK offshore round in recent decades, with an extensive number of prospects and undeveloped discoveries on offer. The 30th Round is scheduled to be launched during the latter half of the second quarter of 2017.

BILLION BARREL POTENTIAL AT UK DISCOVERYFollowing the successful closure of the 29th Licensing Round, there was more good news for the UK offshore sector, with Hurricane Energy reporting continued success from its exploration campaign west of the Shetland Islands.

Hurricane has just concluded its drilling programme with semisubmersible rig Transocean Spitsbergen, with a successful discovery made at its Halifax exploration well. Significantly, Hurricane’s initial analysis suggests that Halifax is actually connected to its earlier Lancaster

discovery. If this is confirmed to be accurate, Hurricane expects that the Greater Lancaster area will be “the largest undeveloped discovery on the UK Continental Shelf” with speculation that a single large hydrocarbon accu-mulation could contain as much as one billion barrels of oil.

The Greater Lancaster Area is located around 60 miles west of Shetland, some 100 miles north of mainland Scotland. Water depths are in the region of 150m (492ft). Hurricane is currently targeting first production for mid-2019.

4 SEABREEZE

OSV MARKET ROUND-UP

Simon Møkster Shipping has received term contracts from Repsol Sinopec Resources UK Ltd for three of its PSVs.

Incumbent PSV Brage Supplier has had her contract extended for at least four more months, keeping her busy until at least

August 2017. Meanwhile, Repsol Sinopec is adding two more Møkster PSVs to its UK fleet. The Brage Trader (pictured) and Stril Odin have been chartered for one-well firm (estimated at 90 days) to support the Stena Spey while she is drilling at the Shaw field in the Central North Sea.

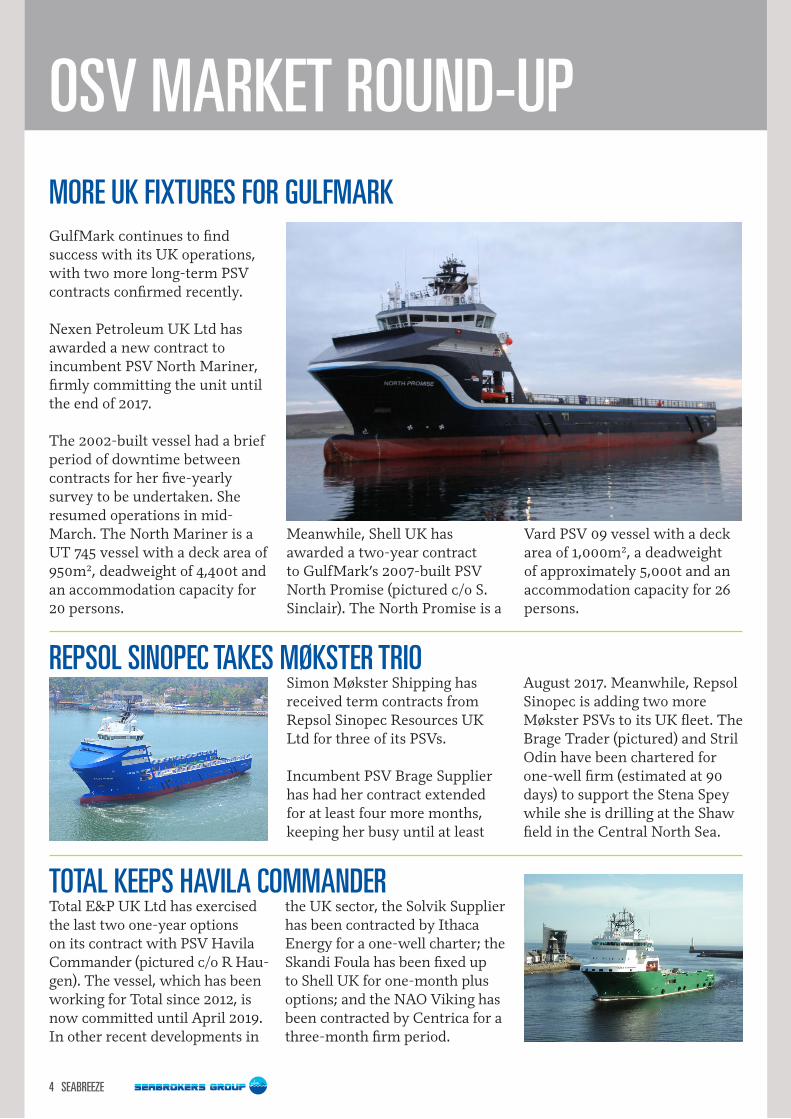

GulfMark continues to find success with its UK operations, with two more long-term PSV contracts confirmed recently.

Nexen Petroleum UK Ltd has awarded a new contract to incumbent PSV North Mariner, firmly committing the unit until the end of 2017.

The 2002-built vessel had a brief period of downtime between contracts for her five-yearly survey to be undertaken. She resumed operations in mid-March. The North Mariner is a UT 745 vessel with a deck area of 950m², deadweight of 4,400t and an accommodation capacity for 20 persons.

Meanwhile, Shell UK has awarded a two-year contract to GulfMark’s 2007-built PSV North Promise (pictured c/o S. Sinclair). The North Promise is a

Vard PSV 09 vessel with a deck area of 1,000m², a deadweight of approximately 5,000t and an accommodation capacity for 26 persons.

REPSOL SINOPEC TAKES MØKSTER TRIO

MORE UK FIXTURES FOR GULFMARK

Total E&P UK Ltd has exercised the last two one-year options on its contract with PSV Havila Commander (pictured c/o R Hau-gen). The vessel, which has been working for Total since 2012, is now committed until April 2019. In other recent developments in

the UK sector, the Solvik Supplier has been contracted by Ithaca Energy for a one-well charter; the Skandi Foula has been fixed up to Shell UK for one-month plus options; and the NAO Viking has been contracted by Centrica for a three-month firm period.

TOTAL KEEPS HAVILA COMMANDER

SEABREEZE 5

OSV MARKET ROUND-UP

DeepGreen Resources is to partner with Maersk Supply Service on a project to recover polymetallic nodules from the Clarion Clipperton Zone of the Pacific Ocean. The NORI D Project is to be conducted in cooperation with the Republic of Nauru, with Maersk committing

one anchor handler and one subsea support vessel for five marine campaigns between 2017 and 2019. The anchor handler will support environmental studies of the seabed, while the subsea vessel will utilise its deck capacity and crane capabilities for testing the nodule harvester

prototype. Maersk’s contribution of USD 25 million will convert to common shares in DeepGreen Resources.

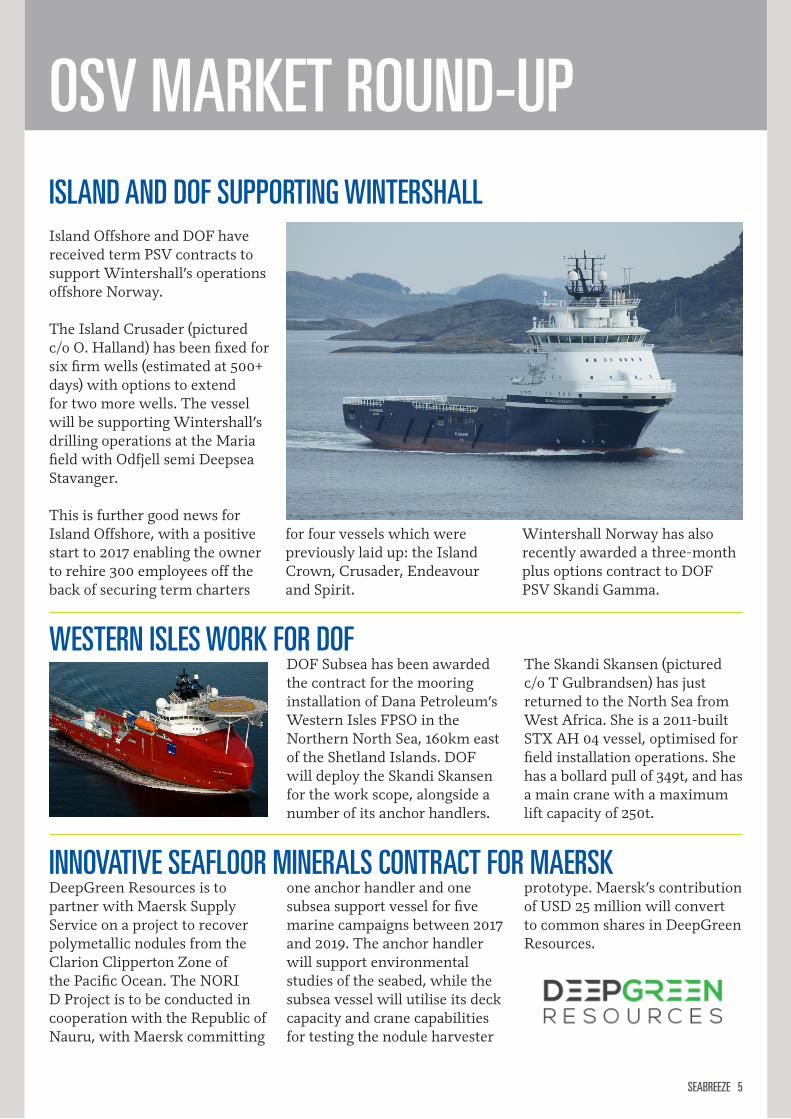

DOF Subsea has been awarded the contract for the mooring installation of Dana Petroleum’s Western Isles FPSO in the Northern North Sea, 160km east of the Shetland Islands. DOF will deploy the Skandi Skansen for the work scope, alongside a number of its anchor handlers.

The Skandi Skansen (pictured c/o T Gulbrandsen) has just returned to the North Sea from West Africa. She is a 2011-built STX AH 04 vessel, optimised for field installation operations. She has a bollard pull of 349t, and has a main crane with a maximum lift capacity of 250t.

Island Offshore and DOF have received term PSV contracts to support Wintershall’s operations offshore Norway.

The Island Crusader (pictured c/o O. Halland) has been fixed for six firm wells (estimated at 500+ days) with options to extend for two more wells. The vessel will be supporting Wintershall’s drilling operations at the Maria field with Odfjell semi Deepsea Stavanger.

This is further good news for Island Offshore, with a positive start to 2017 enabling the owner to rehire 300 employees off the back of securing term charters

for four vessels which were previously laid up: the Island Crown, Crusader, Endeavour and Spirit.

Wintershall Norway has also recently awarded a three-month plus options contract to DOF PSV Skandi Gamma.

WESTERN ISLES WORK FOR DOF

INNOVATIVE SEAFLOOR MINERALS CONTRACT FOR MAERSK

ISLAND AND DOF SUPPORTING WINTERSHALL

6 SEABREEZE

OSV RATES & UTILISATION

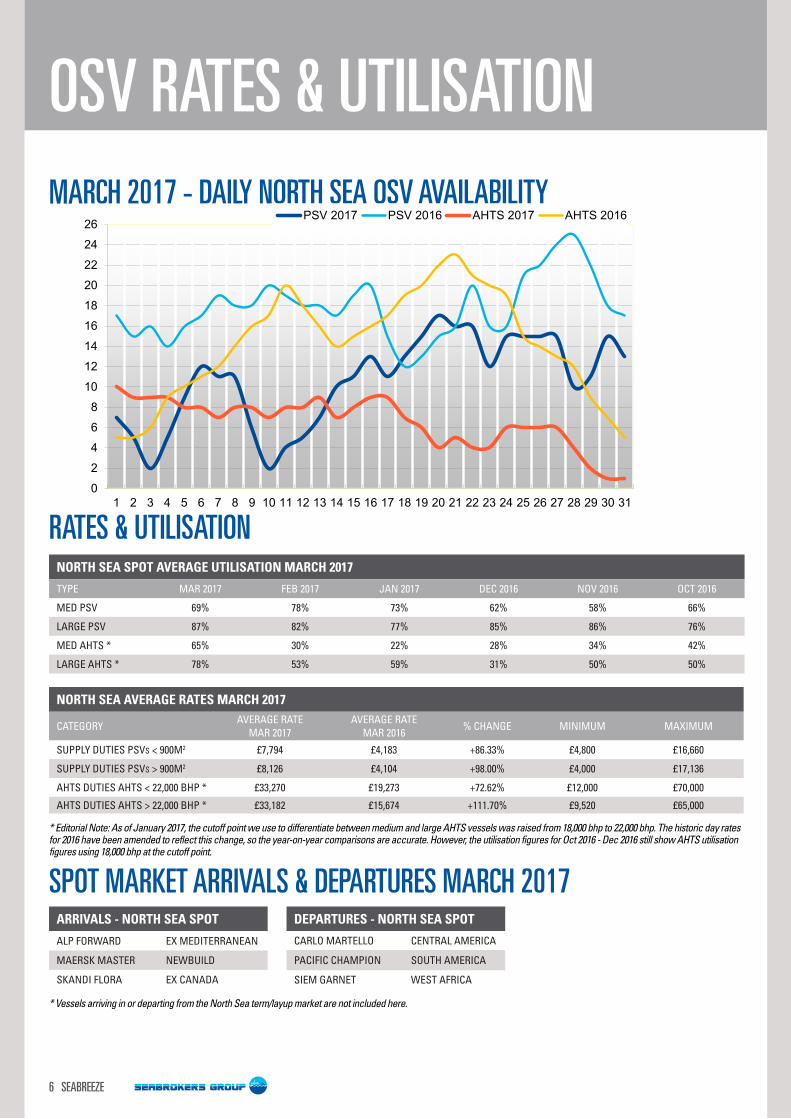

NORTH SEA SPOT AVERAGE UTILISATION MARCH 2017

TYPE MAR 2017 FEB 2017 JAN 2017 DEC 2016 NOV 2016 OCT 2016

MED PSV 69% 78% 73% 62% 58% 66%

LARGE PSV 87% 82% 77% 85% 86% 76%

MED AHTS * 65% 30% 22% 28% 34% 42%

LARGE AHTS * 78% 53% 59% 31% 50% 50%

MARCH 2017 - DAILY NORTH SEA OSV AVAILABILITY

NORTH SEA AVERAGE RATES MARCH 2017

CATEGORYAVERAGE RATE

MAR 2017AVERAGE RATE

MAR 2016% CHANGE MINIMUM MAXIMUM

SUPPLY DUTIES PSVS < 900M2 £7,794 £4,183 +86.33% £4,800 £16,660

SUPPLY DUTIES PSVS > 900M2 £8,126 £4,104 +98.00% £4,000 £17,136

AHTS DUTIES AHTS < 22,000 BHP * £33,270 £19,273 +72.62% £12,000 £70,000

AHTS DUTIES AHTS > 22,000 BHP * £33,182 £15,674 +111.70% £9,520 £65,000

RATES & UTILISATION

DEPARTURES - NORTH SEA SPOT

CARLO MARTELLO CENTRAL AMERICA

PACIFIC CHAMPION SOUTH AMERICA

SIEM GARNET WEST AFRICA

SPOT MARKET ARRIVALS & DEPARTURES MARCH 2017

* Vessels arriving in or departing from the North Sea term/layup market are not included here.

ARRIVALS - NORTH SEA SPOT

ALP FORWARD EX MEDITERRANEAN

MAERSK MASTER NEWBUILD

SKANDI FLORA EX CANADA

* Editorial Note: As of January 2017, the cutoff point we use to differentiate between medium and large AHTS vessels was raised from 18,000 bhp to 22,000 bhp. The historic day rates for 2016 have been amended to reflect this change, so the year-on-year comparisons are accurate. However, the utilisation figures for Oct 2016 - Dec 2016 still show AHTS utilisation figures using 18,000 bhp at the cutoff point.

02468

101214161820222426

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31

PSV 2017 PSV 2016 AHTS 2017 AHTS 2016

SEABREEZE 7

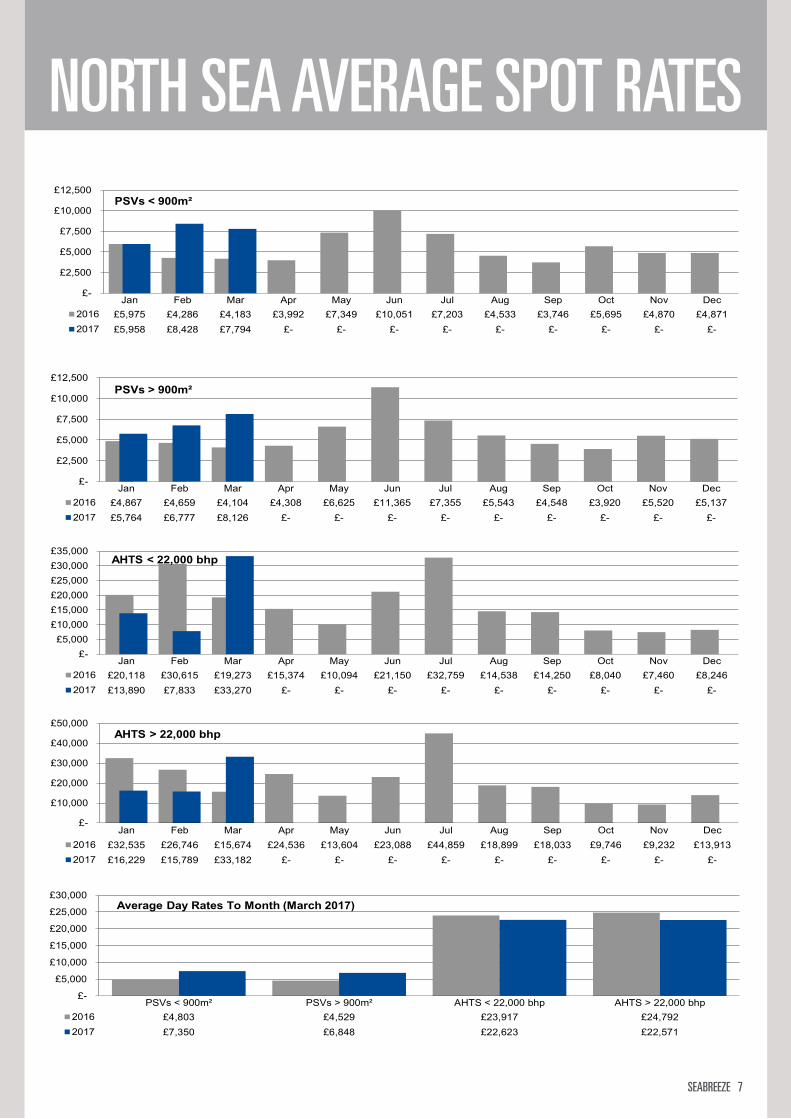

NORTH SEA AVERAGE SPOT RATES

£-

£10,000

£20,000

£30,000

£40,000

£50,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £32,535 £26,746 £15,674 £24,536 £13,604 £23,088 £44,859 £18,899 £18,033 £9,746 £9,232 £13,9132017 £16,229 £15,789 £33,182 £- £- £- £- £- £- £- £- £-

Rig Moves

£-

£10,000

£20,000

£30,000

£40,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £20,118 £30,615 £19,273 £15,374 £10,094 £21,150 £32,759 £14,538 £14,250 £8,040 £7,460 £8,2462017 £13,890 £7,833 £33,270 £- £- £- £- £- £- £- £- £-

PSVs > 900M2

£-

£5,000

£10,000

£15,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £4,867 £4,659 £4,104 £4,308 £6,625 £11,365 £7,355 £5,543 £4,548 £3,920 £5,520 £5,1372017 £5,764 £6,777 £8,126 £- £- £- £- £- £- £- £- £-

PSVs < 900M2

£-

£10,000

£20,000

£30,000

£40,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £5,975 £4,286 £4,183 £3,992 £7,349 £10,051 £7,203 £4,533 £3,746 £5,695 £4,870 £4,8712017 £5,958 £8,428 £7,794 £- £- £- £- £- £- £- £- £-

All Cargo Runs

£-

£5,000

£10,000

£15,000

£20,000

£25,000

PSVs < 900m² PSVs > 900m² AHTS < 22,000 bhp AHTS > 22,000 bhp2016 £5,998 £5,397 £19,734 £22,6882017 £- £- £- £-

Average Day Rates To Month (June 2013)

£-

£10,000

£20,000

£30,000

£40,000

£50,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £32,535 £26,746 £15,674 £24,536 £13,604 £23,088 £44,859 £18,899 £18,033 £9,746 £9,232 £13,9132017 £16,229 £15,789 £33,182 £- £- £- £- £- £- £- £- £-

Rig Moves

£-

£10,000

£20,000

£30,000

£40,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £20,118 £30,615 £19,273 £15,374 £10,094 £21,150 £32,759 £14,538 £14,250 £8,040 £7,460 £8,2462017 £13,890 £7,833 £33,270 £- £- £- £- £- £- £- £- £-

PSVs > 900M²

£-

£5,000

£10,000

£15,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £4,867 £4,659 £4,104 £4,308 £6,625 £11,365 £7,355 £5,543 £4,548 £3,920 £5,520 £5,1372017 £5,764 £6,777 £8,126 £- £- £- £- £- £- £- £- £-

PSVs < 900M²

£-

£10,000

£20,000

£30,000

£40,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £5,975 £4,286 £4,183 £3,992 £7,349 £10,051 £7,203 £4,533 £3,746 £5,695 £4,870 £4,8712017 £5,958 £8,428 £7,794 £- £- £- £- £- £- £- £- £-

All Cargo Runs

£-

£5,000

£10,000

£15,000

£20,000

£25,000

PSVs < 900m² PSVs > 900m² AHTS < 22,000 bhp AHTS > 22,000 bhp2016 £5,998 £5,397 £19,734 £22,6882017 £- £- £- £-

Average Day Rates To Month (June 2013)

£-

£10,000

£20,000

£30,000

£40,000

£50,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £32,535 £26,746 £15,674 £24,536 £13,604 £23,088 £44,859 £18,899 £18,033 £9,746 £9,232 £13,9132017 £16,229 £15,789 £33,182 £- £- £- £- £- £- £- £- £-

Rig Moves

£-

£10,000

£20,000

£30,000

£40,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £20,118 £30,615 £19,273 £15,374 £10,094 £21,150 £32,759 £14,538 £14,250 £8,040 £7,460 £8,2462017 £13,890 £7,833 £33,270 £- £- £- £- £- £- £- £- £-

PSVs > 900M2

£-

£5,000

£10,000

£15,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £4,867 £4,659 £4,104 £4,308 £6,625 £11,365 £7,355 £5,543 £4,548 £3,920 £5,520 £5,1372017 £5,764 £6,777 £8,126 £- £- £- £- £- £- £- £- £-

PSVs < 900M2

£-

£10,000

£20,000

£30,000

£40,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £5,975 £4,286 £4,183 £3,992 £7,349 £10,051 £7,203 £4,533 £3,746 £5,695 £4,870 £4,8712017 £5,958 £8,428 £7,794 £- £- £- £- £- £- £- £- £-

All Cargo Runs

£-

£5,000

£10,000

£15,000

£20,000

£25,000

PSVs < 900m² PSVs > 900m² AHTS < 22,000 bhp AHTS > 22,000 bhp2016 £5,998 £5,397 £19,734 £22,6882017 £- £- £- £-

Average Day Rates To Month (June 2013)

£-

£10,000

£20,000

£30,000

£40,000

£50,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £32,535 £26,746 £15,674 £24,536 £13,604 £23,088 £44,859 £18,899 £18,033 £9,746 £9,232 £13,9132017 £16,229 £15,789 £33,182 £- £- £- £- £- £- £- £- £-

AHTS > 22,000 bhp

£- £5,000

£10,000 £15,000 £20,000 £25,000 £30,000 £35,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £20,118 £30,615 £19,273 £15,374 £10,094 £21,150 £32,759 £14,538 £14,250 £8,040 £7,460 £8,2462017 £13,890 £7,833 £33,270 £- £- £- £- £- £- £- £- £-

AHTS < 22,000 bhp

£-

£2,500

£5,000

£7,500

£10,000

£12,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £4,867 £4,659 £4,104 £4,308 £6,625 £11,365 £7,355 £5,543 £4,548 £3,920 £5,520 £5,1372017 £5,764 £6,777 £8,126 £- £- £- £- £- £- £- £- £-

PSVs > 900m²

£-

£2,500

£5,000

£7,500

£10,000

£12,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2016 £5,975 £4,286 £4,183 £3,992 £7,349 £10,051 £7,203 £4,533 £3,746 £5,695 £4,870 £4,8712017 £5,958 £8,428 £7,794 £- £- £- £- £- £- £- £- £-

PSVs < 900m²

£-

£5,000

£10,000

£15,000

£20,000

£25,000

£30,000

PSVs < 900m² PSVs > 900m² AHTS < 22,000 bhp AHTS > 22,000 bhp2016 £4,803 £4,529 £23,917 £24,7922017 £7,350 £6,848 £22,623 £22,571

Average Day Rates To Month (March 2017)

8 SEABREEZE

FEATURE VESSEL

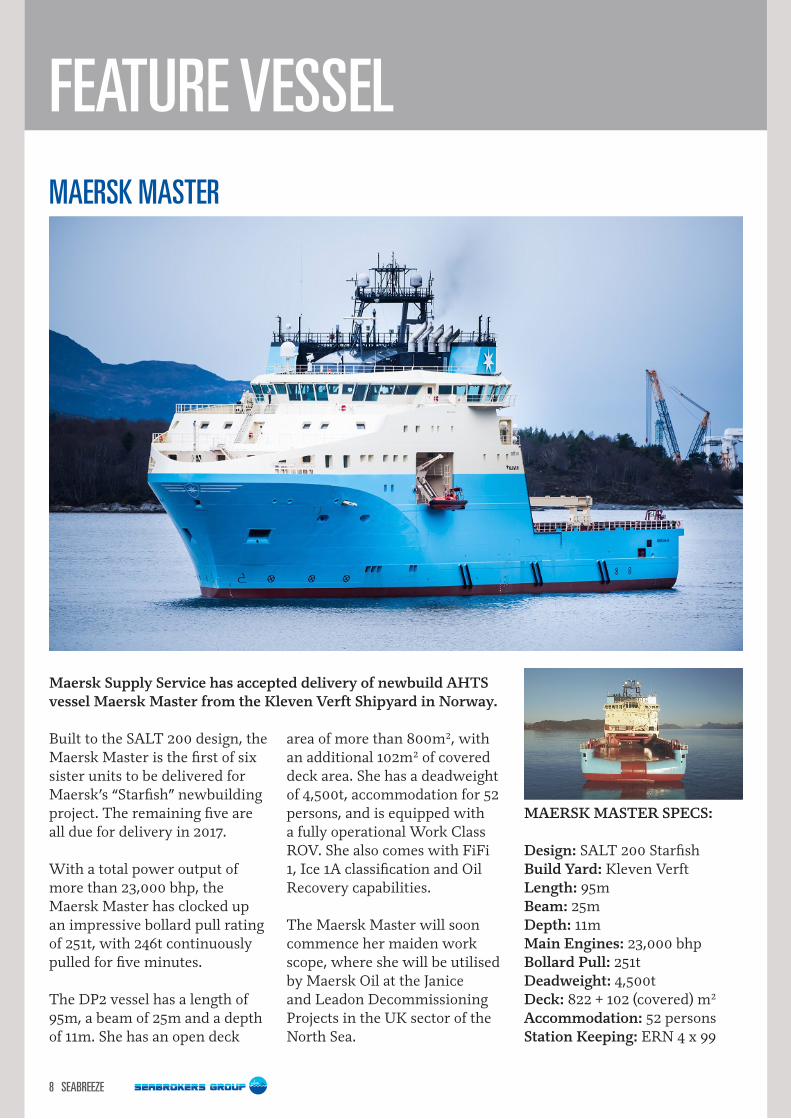

Maersk Supply Service has accepted delivery of newbuild AHTS vessel Maersk Master from the Kleven Verft Shipyard in Norway.

MAERSK MASTER SPECS:

Design: SALT 200 StarfishBuild Yard: Kleven VerftLength: 95mBeam: 25mDepth: 11mMain Engines: 23,000 bhpBollard Pull: 251tDeadweight: 4,500tDeck: 822 + 102 (covered) m²Accommodation: 52 personsStation Keeping: ERN 4 x 99

MAERSK MASTER

Built to the SALT 200 design, the Maersk Master is the first of six sister units to be delivered for Maersk’s “Starfish” newbuilding project. The remaining five are all due for delivery in 2017.

With a total power output of more than 23,000 bhp, the Maersk Master has clocked up an impressive bollard pull rating of 251t, with 246t continuously pulled for five minutes.

The DP2 vessel has a length of 95m, a beam of 25m and a depth of 11m. She has an open deck

area of more than 800m², with an additional 102m² of covered deck area. She has a deadweight of 4,500t, accommodation for 52 persons, and is equipped with a fully operational Work Class ROV. She also comes with FiFi 1, Ice 1A classification and Oil Recovery capabilities.

The Maersk Master will soon commence her maiden work scope, where she will be utilised by Maersk Oil at the Janice and Leadon Decommissioning Projects in the UK sector of the North Sea.

SEABREEZE 9

OSV NEWBUILDINGS, S&P

Standard Drilling has entered into new agreements to buy nearly 3.5 million more shares in New World Supply Ltd (NWS), increasing its equity stake by 10.6%. Added to the 15.6% share from its initial purchase, Standard Drilling now holds 26.2% of the company. NWS owns six Damen

PSV 3300 vessels: the World Diamond, Emerald, Opal, Pearl, Peridot (pictured c/o D Dodds) and Sapphire. The 2013-built vessels are all currently in layup. They were purchased en-bloc by NWS from World Wide Supply for a total consideration of USD 27.5 million in January 2017.

Newbuild PSV Bravante II has been delivered to the Bravante Group by Estaleiro São Miguel in São Gonçalo, Brazil.The Bravante II was ordered during Petrobras’ Prorefam Fleet Renewal Process, and has been chartered to Petrobras for an

eight-year contract. The vessel was built to Rolls Royce’s UT 755 SE design, which meets the specifications for Petrobras’ PSV 4500 requirements. She has an approximate length of 88m, moulded breadth of 19m and a deck area of around 855m².

An unnamed Norwegian compa-ny has entered into an agreement with Farstad to acquire AHTS vessel Far Shogun (pictured c/o G. Vinnes). In relation to this, DOF will enter into an agreement with the new owners for the manage-ment and operation of the vessel, which will be renamed Skandi

Bergen. DOF has a further option to purchase the vessel at a price corresponding to the outstanding debt, or 50-60% of historical build costs. Delivery of the Far Shogun to her new owners will take place in June or July 2017. The 2010-built UT 731 CD vessel is currently working in Australia.

STANDARD DRILLING INCREASES PSV INVESTMENT

FAR SHOGUN JOINING DOF FLEET

All four of Atlantic Towing’s newbuild Damen PSV 5000 vessels are now in Canada. The Atlantic Griffon, Atlantic Heron, Atlantic Shrike (pictured c/o E. Moakler) and Paul A. Sacuta were built by Damen Shipyards Galaţti in Romania with oufitting work taking place at Irving Shipbuilding in Canada. The vessels were built

to Damen’s PSV 5000 design, but the Paul A. Sacuta has been outfitted with a 100-ton crane and equipped for IMR activities. The vessels will be utilised by Atlantic Towing to fulfil its 10-year offshore support contract with ExxonMobil Canada Properties and Hibernia Management and Development Company Ltd.

ATLANTIC TOWING NEWBUILDS IN CANADA

BRAVANTE II DELIVERED IN BRAZIL

10 SEABREEZE

OSV NEWBUILDINGS, S&P

ETP Engenharia in Brazil has delivered the final six Fast Supply Vessels of a 12-unit series to Baru Offshore, a subsidiary of Inter-tug. All of the vessels have been contracted by Petrobras, and were built to an Incat Crowther design in line with Petrobras’ UT4000 FSV specifications. The

last six vessels in the series have been named Baru Serrana, Sinu, Sirius, Taurus, Tesoro and Vega. They have capacity to carry 42,000 litres of ship’s fuel, 90,000 litres of cargo fuel, 10,000 litres of ship’s water, and 88,000 litres of fresh water. They have a cargo deck area of 225m².

FINAL SIX FAST SUPPLY VESSELS DELIVERED TO BARU

BIGROLL WELCOMES FINAL MC NEWBUILD

PGS has completed its newbuild programme with the delivery of its fourth and final Ramform Titan-class seismic acquisition vessel. A naming ceremony was held for the Ramform Hyperion on March 22nd at the Mitsubishi Heavy Industries Shipbuilding Co. yard in Nagasaki, Japan. This follows the earlier deliveries

of the Ramform Titan in 2013, Ramform Atlas in 2014, and Ramform Tethys in 2016. With a 70m broad stern, these vessels can tow more streamers (24) than any other vessel, and they can also tow extremely wide streamer spreads, allowing for the most efficient coverage of a large exploration area.

RAMFORM HYPERION DELIVERED IN JAPAN

RECENT DELIVERIES OF NEWBUILD OSVSNAME TYPE/DESIGN OWNER/ MANAGER COMMITMENT

ATLANTIC GRIFFON DAMEN PSV 5000 ATLANTIC TOWING CANADA

ATLANTIC HERON DAMEN PSV 5000 ATLANTIC TOWING CANADA

ATLANTIC SHRIKE DAMEN PSV 5000 ATLANTIC TOWING CANADA

BRAVANTE II ROLLS ROYCE UT 775 SE PSV BRAVANTE GROUP SOUTH AMERICA

MAERSK MASTER SALT 200 AHTS MAERSK SUPPLY SERVICE NORTH SEA

PAUL A. SACUTA DAMEN PSV 5000 IMR ATLANTIC TOWING CANADA

BigRoll Shipping has accepted delivery of Module Carrier vessel BigRoll Beaufort, the fourth and final newbuild in its MC Class series. This follows the earlier deliveries of BigRoll Barentsz, BigRoll Bering and BigRoll Baffin. The DP2 vessels have a length of 173m, a breadth of

42m and a deadweight of around 20,000mt. They have been specifically designed to deliver modules and equipment for large scale projects, and with Finnish Swedish 1A Ice Class they are highly suited for operations in remote areas including the Arctic.

SEABREEZE 11

SUBSEA

One of the major takeaway points from IHS Markit’s CERAWeek in March was that exploration is not dead and that now is the time to invest. With the industry underin-vesting since the collapse of oil prices in mid-2014, and with a strong focus on cost reduction throughout the industry, now is the time when oil companies are in the best position to reap some rewards for the hardship they have been enduring.The industry is not going to right

itself quickly and IHS Markit has only forecast a modest growth in global exploration spending through to 2020. However, the strong focus on cost savings, reduced spending and lowering breakeven points, has allowed some companies to cut spending in 2017 but actually increase the number of wells they will drill this year.Total has reduced its exploration budget by 40% compared to 2014 highs, allowing them to plan to drill 27 wells in 2017 with

a budget of USD 1.25 billion, compared to spending USD 1.4 billion on drilling 19 wells in 2016.With new cost recalibrations in the industry, it has created new opportunities for exploration. This sentiment has been ex-pressed by various oil companies over the past few weeks.IHS Markit has stated that the next five-to-six years could be one of the best times for explora-tion in the last 15 years.

FAR SUPERIOR DELIVERED

SUBSEA MARKET ROUND-UP

Farstad Shipping has taken delivery of the IRM support vessel Far Superior (pictured

c/o O. Halland) in Kristiansand, Norway. The Vard 3 17-designed vessel has now commenced a five-year firm charter, with up to five years of options, with TechnipFMC.Under the terms of the deal, TechnipFMC has the right to utilise the vessel up to 320 days per year. The DP2 newbuild has a length

of 98m, and she is equipped with a 150t AHC offshore crane, two Oceaneering work-class ROVs and accommodation for 85 persons. The Far Superior was delivered from VARD’s shipyard in Vung Tau, Vietnam on 16 January before mobilising to Norway for final delivery to Farstad.

SHELL APPROVES FID ON KAIKIASShell Offshore and MOEX North America have taken the final investment decision (FID) to execute phase one of the Kaikias deep water project in the US Gulf of Mexico.This will be the the first project the oil and gas company has approved in 18 months, and this has been made possible by reducing the costs by around 50% through a simplified design and learning from prior lessons.

The project will be tied back to the nearby Shell-operated Ursa production hub and will be developed in two phases, with the first phase due to start production in 2019. Shell has announced that phase one will generate profit even with oil prices lower than USD 40 a barrel. The development of the first phase includes three wells, which are designed to produce up to 40,000 barrels of

oil equivalent per day (boe/d) at peak rates.Shell is the operator of the field with 80% interest, while MOEX holds the remaning 20% interest.

12 SEABREEZE

SUBSEA

Ultra Deep Solutions has con-firmed that the multipurpose diving support and construction vessel Lichtenstein is close to delivery at the Merchants Indus-try Holdings yard in China. They have advised that the MT6024-designed newbuild is expected to depart the yard by early April and mobilise to Asia to commence a long-term charter of five years.

The DP2 Lichtenstein has a length of 121 metres, and she is equipped with an 18-man twin bell saturation diving system for operations down to a water depth of 300 metres. She has a 140-tonne crane and accommo-dation for 130 persons. The vessel will also feature two 150 HP work-class ROVs and will have two self-powered hyperbaric lifeboats.

LICHTENSTEIN NEARING COMPLETION

Subsea 7 has completed its acquisition of Seaway Heavy Lifting. Subsea 7 already held a 50% stake in the company but purchased the remaining 50% share from K&S Baltic Offshore Limited on March 10, 2017 for USD 279 million. An additional consideration of up to USD 40 million will be paid in 2021 on the condition that certain perfor-mance targets are met.

The wholly-owned purchase increases Subsea 7’s partici-pation in Renewables, Heavy Lifting and Decommissioning services. Seaway Heavy Lifting will fall within a new business unit called Renewables and Heavy Lifting.The acquisition has added both the 1985-built Stanislav Yudin and the 2011-built Oleg Strash-nov derrick vessels, which are

equipped with a 2,500t revolving crane and a 5,000t revolving crane respectively, to Subsea 7’s fleet.

SUBSEA 7 COMPLETES ACQUISITION OF SEAWAY

STATOIL TO INVEST BILLIONS OFFSHORE NORWAYStatoil has submitted field development plans to Norwegian authorities for two fields in the Norwegian Sea, which will see an investment of NOK 19.8 billion. The capital expenditure of the revised plan for development and operation of the fields will be NOK 15.7 billion for the Njord field and NOK 4.1 billion on the Bauge field. Under the plan both the Njord A platform and the Njord Bravo floating storage and offloading vessel will be upgrad-ed, in addition to building a new

subsea facilities, drilling new wells and performing extensive marine operations.When the original plan was submitted, Statoil had expected the Njord development to be shut down in 2013, however due to new technology, project improvements and close coop-eration with partners and the supply industry, Statoil now sees opportunities to create consider-able value for another 20 years.The company stated that further development of the Njord area,

includes the upgrading of the Njord installations and develop-ment of the Bauge field. The Bauge development will be the first use of the Cap-X tech-nology, which is a next-genera-tion subsea production system and will cost less to produce and install. The Bauge field devel-opment concept includes one subsea template, two oil produc-ers and one water injector.Both projects will come on stream at the end of 2020.

SEABREEZE 13

SUBSEA

DOF has awarded Westcon Yards Floro a contract for the reconstruction of IMR vessel Skandi Darwin (ex-Olympic Commander). LOS Shipping bought the MT 6015-designed vessel in February and thereafter, DOF signed a management and operation agreement with the new owner. The interior works that Westcon

Yards will carrying out include building an ROV hangar module with foundations for an ROV launch and recovery system, the installation of new offshore cranes, new life boats and other upgrades. The conversion is due to be completed around mid-June. DOF plans to engage the Skandi Darwin on an IMR contract for

Shell on their Prelude FLNG project offshore Australia.

An undisclosed oil and gas E&P company, understood to be Rep-sol Oil & Gas, has awarded Alam Maritim Resources an IMR contract valued at around RM 99

million (USD 22.4 million).The contract has a duration of two years with options to extend by a further year.

ALAM MARITIM SECURES IMR CONTRACT

WESTCON TO RECONSTRUCT SKANDI DARWIN

Global Marine Systems has pur-chased the subsea construction,

installation and trenching vessel Maersk Recorder from Maersk Supply Service, and renamed her CS Recorder. Global Marine Systems plans to utilise the 2000-built vessel for telecoms installation projects globally. The CS Recorder will be equipped with a plough system and an ROV in preparation to

undertake the full range of tele-coms cable installation projects. The 106m-long vessel replaces the Cable Innovator following its reassignment in the fourth quarter of 2016 to become a dedicated maintenance vessel for the North America Maintenance Zone submarine cable contract, which is firm until 2024.

GC Rieber Shipping has entered into a four-month time charter agreement for the SX 121-de-signed pipelay vessel Polar Onyx.The charter has recently com-menced and will see the vessel continue to operate off West Africa. Market sources suggest that the 130-metre long vessel, which is

equipped with a 250-tonne crane and accommodation for 130 persons, is operating on Tullow Oil’s Jubilee Turret Remediation project. There are in excess of two month options available that could extend the charter period. The 2014-built vessel is also equipped with a 275-tonne

Huismann Vertical Lay System and is SPS-2008 classed.

POLAR ONYX SECURES FOUR-MONTH CHARTER

GLOBAL MARINE ADDS VESSEL TO ITS FLEET

14 SEABREEZE

RENEWABLES

Spliethoff has ordered six mul-tipurpose vessels (MPVs) at the Zhejiang Ouhua Shipbuilding yard in China. The newbuilds,

to be targeted at the offshore wind market, will have a length of 165 meters, a deadweight of around 18,000 tonnes and will be equipped with a heavy lift crane. The new R-class vessels will be designed in accordance with the Polar Code and are therefore highly suitable to trade in remote areas such as the

Arctic. The first in the series will be named Raamgracht and she is scheduled for delivery in January 2019, followed by the remaining five vessels at regular intervals of two months. The remaining five vessels will be named Realengracht, Reguliersgracht, Rijpgracht, Ringgracht and Rozengracht.

SPLIETHOFF ORDERS SIX MPVS

UK RENEWABLES ACTIVITY RAMPING UP

The UK Government is set to open the second Contracts for

Difference (CfD) Allocation Round on April 3, when it will make a total of GBP 290 million available for renewable energy projects, including offshore wind. Developers can submit their applications by April 21 and the round will close on September 11, 2017. The CfD round is

for projects planned to be commissioned in 2021/2022 and 2022/2023. Strike price of GBP 105/MWh is targeted for offshore wind projects to be delivered in 2021/22, and for those to start generating energy in 2022/23, the strike price is GBP 100/MWh.

POLAR QUEEN COMMENCES SENVION CHARTERIn early March, GC Rieber Shipping’s construction support vessel Polar Queen commenced her seven-month charter with Senvion GmbH. The ST-254L-CD-designed Polar Queen is supporting turbine commissioning at the

332MW Nordsee One wind farm in the German North Sea. A motion-compensated Uptime gangway has been installed for the transfer of personnel and cargo. The contract can be extended by a further three months.

A2SEA CLOSE TO BEING SOLDBerlingske Business has reported that Danish offshore installations specialist A2Sea is close to being sold.Dong Energy and Siemens Wind Power have been looking to offload the joint venture since last summer and bids have been

submitted for their perusal. It has been reported that Euro-pean owners DEME, Fred Olsen, MPI Offshore and Vroon are pos-sible buyers, as well as China’s ZMPC with figures thought to be in the region of USD 200 million to USD 250 million.

A2Sea’s vessels can no longer transport Siemens’ largest offshore wind turbines.

SEABREEZE 15

RIGS

Borr Drilling Ltd has entered into a Letter of Intent to acquire Transocean’s entire jackup fleet for an approximate price of USD 1.35 billion. This would entail the purchase of 15 jackups, of which 10 are in service and

five are under construction at Keppel FELS in Singapore. Borr Drilling’s current fleet consists of two jackups: the 2013-built Borr Drilling Ran and Borr Drilling Frigg, which were recently acquired from Hercules Offshore.

OIL PRICE VS RIG UTILISATION

RIG UTILISATION AND DAY RATESUTILISATION

MAR2017

MAR 2016

MAR 2015

MAR 2014

MAR 2013

NORTHWEST EUROPE 53.0% 69.2% 92.2% 98.9% 97.8%

SOUTH AMERICA 76.3% 82.3% 93.5% 96.4% 97.8%

US GULF 31.7% 38.8% 54.4% 70.5% 71.0%

RECENT DAY RATE BENCHMARKS LOW (USD) HIGH (USD)

UK HARSH HIGH SPEC JACKUPS 75,000 100,000

NORWAY HARSH HIGH-SPEC JACKUPS 143,000 143,000

UK HARSH STANDARD SEMISUBS 100,000 115,000

NORWAY HARSH HIGH-SPEC SEMISUBS 170,000 175,000

GLOBAL ULTRA-DEEPWATER SEMISUBS 127,500 222,295

GLOBAL ULTRA-DEEPWATER DRILLSHIPS 155,000 225,000

INACTIVE RIGS NORTHWEST EUROPE

NAME TYPE STATUSBIDEFORD DOLPHIN SS WARM STACK

BORGLAND DOLPHIN SS WARM STACK

BORGSTEN DOLPHIN TR COLD STACK

BORR DRILLING RAN JU COLD STACK

BREDFORD DOLPHIN SS COLD STACK

BYFORD DOLPHIN SS WARM STACK

COSLINNOVATOR SS WARM STACK

COSLPIONEER SS COLD STACK

DEEPSEA METRO II DS COLD STACK

ENERGY ENDEAVOUR JU COLD STACK

ENERGY ENHANCER JU COLD STACK

ENSCO 70 JU COLD STACK

ENSCO 102 JU WARM STACK

ENSCO 120 JU WARM STACK

GSF GALAXY II JU COLD STACK

GSF GALAXY III JU COLD STACK

GSF MONARCH JU COLD STACK

GSP SATURN JU COLD STACK

MAERSK GIANT JU WARM STACK

MAERSK INSPIRER JU WARM STACK

MAERSK REACHER JU WARM STACK

MAERSK RESOLUTE JU WARM STACK

MAERSK RESOLVE JU WARM STACK

OCEAN GUARDIAN SS WARM STACK

OCEAN NOMAD SS COLD STACK

OCEAN PRINCESS SS COLD STACK

OCEAN VANGUARD SS COLD STACK

PARAGON C461 JU WARM STACK

PARAGON C462 JU WARM STACK

PARAGON C463 JU WARM STACK

PARAGON C20051 JU WARM STACK

PARAGON C20052 JU WARM STACK

PARAGON HZ1 JU WARM STACK

PARAGON MSS1 SS WARM STACK

POLAR PIONEER SS COLD STACK

ROWAN GORILLA VI JU WARM STACK

ROWAN NORWAY JU WARM STACK

ROWAN STAVANGER JU WARM STACK

SEDCO 711 SS COLD STACK

SEDCO 712 SS HOT STACK

SEDCO 714 SS COLD STACK

SERTAO DS COLD STACK

SONGA DEE SS COLD STACK

SONGA DELTA SS COLD STACK

SONGA TRYM SS COLD STACK

STENA DON SS WARM STACK

SWIFT 10 JU WARM STACK

TRANSOCEAN BARENTS SS WARM STACK

TRANSOCEAN PROSPECT SS COLD STACK

TRANSOCEAN SEARCHER SS COLD STACK

WEST ALPHA SS COLD STACK

WEST EPSILON JU COLD STACK

WEST HERCULES SS COLD STACK

WEST NAVIGATOR DS COLD STACK

WEST VENTURE SS COLD STACK

WILHUNTER SS COLD STACK

BORR DRILLING TO BUY TRANSOCEAN JACKUPS

WEST MIRA BOUGHT BY SEATANKERSSeadrill has reached a settlement agreement with Hyundai Samho Heavy Industries in South Korea for newbuild semisubmersible rig West Mira. Seadrill is to receive a cash settlement of USD 170 mil-lion in full settlement of the rig

dispute. As part of the agreement, asset holding company Seatankers (a related party) has purchased the West Mira from the yard. Seadrill will perform commercial and technical management, and has a right of first refusal to buy the rig.

Source: IHS-Petrodata

$39.07

$42.25

$47.13 $48.48$45.07 $46.14 $46.19

$49.73

$46.44

$54.07 $54.89 $55.49$52.53

69.2% 68.2% 68.0% 66.3% 64.6%60.5%

57.4% 57.7%55.0%

51.6% 52.3% 53.3% 53.0%

82.3%78.6% 77.1%

75.1% 74.3% 74.8%77.6% 78.4% 76.8% 76.0% 74.4% 75.6% 76.3%

38.8% 39.5% 37.8% 36.8% 36.0% 35.4% 35.1% 35.2% 35.1% 33.5% 32.8% 33.4% 31.7%

$25

$30

$35

$40

$45

$50

$55

$60

30%

40%

50%

60%

70%

80%

90%

100%

Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16 Nov 16 Dec 16 Jan 17 Feb 17 Mar 17Average Brent Crude US$ / Bbl Northwest Europe Rig UtilisationSouth America Rig Utilisation US Gulf Rig Utilisation

HEADING Quiatis imaximilitem num enis porum ne dolles qui rerum id min corepta dolo quo conet il id quisto que voluptatus eatis re ventur? Hilibust quis as mincias peribustis qui dolorit officatus aut preiumquas qui iuscimu sapelest, esto odio. Itatecum cus acerum ipidunture corporpores et int faccum remperi onsequi

16 SEABREEZE

NEW CHARTERS FOR ODFJELLOdfjell Drilling has been awarded three new fixtures recently, one for its sixth generation semi Deepsea Stavanger, and two short-term charters for its third generation semi Deepsea Bergen.

Odfjell has signed a Letter of Award with an unnamed “oil major” for a one-well contract with the Deepsea Stavanger offshore South Africa. The rig is just returning to work for a six-well contract with Wintershall offshore Norway, having been idle since mid-2016. The Wintershall campaign is expected to keep her occupied until the fourth quarter of 2018, with the South Africa charter to follow thereafter. The one-well contract will have an estimated drilling duration of around 60-80 days, and has a total value of up to USD 55 million, including mobilisation and demobilisation.

Odfjell has also received two Letters of Intent from undisclosed parties for separate one-well plus options charters for Deepsea Bergen in Norway. The campaigns are scheduled for the fourth quar-ter of 2017 and first quarter of 2018, with an esti-mated duration of 140 days for the two firm wells combined. The rig is currently fixed to Statoil until July 2017, with a one-well contract with Faroe Petroleum to follow before these new charters.

CONUNDRUM CORNERThe answer to last month’s teaser :- This word I know? Six letters it contains. Take away the last... and only twelve remains. What is the word?

The correct answer was :- Dozens

This month, our poser is as follows:

Many have heard me, but no one has seen me, and I will only speak when spoken to. What am I?

Answers back to [email protected].

THE SEABREEZE ARCHIVEFor the current or archive copies of Seabreeze go to: http://www.seabrokers.co.uk/ - see under Shipbroking / Market Reports. If you wish to Subscribe or Unsubscribe please contact: [email protected]

CONUNDRUM CORNER, DUTY PHONES

SEABROKERS GROUP CONTACTSSEABROKERS HEAD OFFICEForusbeen 78 - 4033 Stavanger - Norway Tel: (+47) 51 80 00 00 Internet: www.seabrokers-group.com SEABROKERS CHARTERING AS - STAVANGERDuty Telephone ++47 51 815400 (24 Hrs) E-mail [email protected]

SEABROKERS LTD - ABERDEENDuty Telephone ++44 1224 747744 (24 Hrs) Duty Mobile ++44 7802 304129E-Mail [email protected]

SEABROKERS BRAZIL LTDA - RIO DE JANEIRO Duty Telephone ++55 21 3505 4200 (24 Hrs) E-mail [email protected] SECURALIFT AS - STAVANGERTelephone ++47 51 800000 E-mail [email protected]

SEA SURVEILLANCE AS - BERGEN Telephone ++47 55 136500E-mail [email protected]

SEABROKERS EIENDOM AS - STAVANGER Telephone ++47 51 800000 E-mail [email protected] SEABROKERS SERVICES AS - STAVANGER Telephone ++47 51 800000E-mail [email protected]

SEABROKERS FUNDAMENTERING AS - STAVANGERTelephone ++47 51 800000 E-mail [email protected]

SEABROKERS KRAN & TRANSPORT AS - STAVANGER Telephone ++47 51 800000E-mail [email protected]