march 2016 ceri commodity report — crude oil · ceri commodity report -crude oil page 2 north...

TRANSCRIPT

Relevant • Independent • Objective

CERI Commodity Report – Crude Oil Editorial Committee: Paul Kralovic, Dinara Millington, Megan Murphy, Jon Rozhon, Allan Fogwill About CERI The Canadian Energy Research Institute is an independent, not-for-profit research establishment created through a partnership of industry, academia, and government in 1975. Our mission is to provide relevant, independent, objective economic research in energy and related environmental issues. For more information about CERI, please visit our website at www.ceri.ca or contact us at [email protected].

Figure 1: Tokyo Emissions Reductions: FY2010 to 2014

Source: Tokyo Metropolitan Government

Like any system, cap-and-trade is not without challenges. Chief among them is the setting of emissions targets. Set a target too stringent and it causes financial stress on the emitters and the economy; set a target too lax, and optimal reduction levels are not reached. This is what happened in Phase I of the European Union Emission Trading Scheme from 2005 to 2007. The caps were proposed by EU member states and approved by the European Commission. They were initially provided free to emitters and in “too generous an overall allocation... the oversupply drove the carbon price down to 0 in 2007”.3 In Australia, the cap-and-trade system has been highly politicized, with the system being changed according to the outcome of every national election since 2007.4 This highlights another challenge with cap and trade, the artificial nature of the market can be changed much more quickly than economic decision makers can react. There has been more success in New Zealand, which first legislated a trading scheme in 2008, though to make it palatable to all stakeholders, there presently exists no price signal and the system has been marginal at best in achieving emissions reductions over the years.5 Cap-and-trade systems in major emitting countries like China, Korea, and India are only now getting underway, so it is too early to judge these schemes.

Cap-and-Trade: Emissions Reductions Plan in Ontario Jon Rozhon Cap-and-Trade throughout the World A number of policy options exist for reducing greenhouse gases1 (GHGs) in any economy. There may be taxes applied to energy producers and consumers, energy efficiency measures can be legislated, and subsidies and financing may be made available for renewable energy alternatives to GHG-producing hydrocarbons. These policies and measures can be instituted across the economy in question – including the industrial, commercial, transportation, residential, agricultural, fossil fuel production and power sectors – and may all be targeted. Emissions cap and trade systems represent one way to reduce GHGs – a means that is usually directed at large industrial and power sector emitters. When cap-and-trade works well, it can be simple and effective in reaching GHG reduction goals: a government sets an emissions ceiling for a specific trading period, distributes allowances to large GHG emitters, and then those emitters trade or sell allowances to meet emissions obligations. Cap-and-trade, in theory, minimizes government interference and utilizes free market efficiencies. The invisible hand works to reduce carbon in the atmosphere at the lowest market price. One system that has appeared to work well is the one implemented by the Tokyo Metropolitan Government, which managed to reach a 25 percent emission reduction in FY 2014 after the 5th year of their cap-and-trade program.2 With a population in excess of 13 million people and a large, vibrant industrial base, Tokyo’s achievement in GHG emissions reduction is something for other cities and nations to note (see Figure 1).

March 2016

CERI Commodity Report — Crude Oil

CERI Commodity Report - Crude Oil

Page 2

North American Cap-and-Trade The United States has a long history of cap-and-trade programs of varying description to manage environmental externalities. Perhaps the most famous of these systems was the Acid Rain Program implemented in 1990 to reduce sulfur dioxide emissions – largely from the power sector. After 10 years, the US saw “an approximately 50 percent reduction from 1980 levels, when power-sector emissions were about 17.5 million tons”.6 This particular program was a textbook application of cap-and-trade principles: at the outset, the US federal government freely allocated allowances, and the power facility owners were permitted either to buy more allowances or reduce emissions. Their emissions reductions options were to install pollution controls, to change facility fuel mixes, or to scale back operations. When operators managed to reduce emissions below their allowance allocations, they could sell extra allowances or bank them. Incentives were therefore created to reduce emissions at the lowest cost.7 In the end, society met its SO2 emissions goals, electricity producers operated more cleanly, and the power system continued to supply ample energy to the nation. The Western Climate Initiative (WCI) is an ongoing emissions strategy, which began in 2007 as a US scheme but saw expansion into Canada (and at one point several Mexican states and a number of Canadian provinces that were “observers” to the initiative). The WCI was initially an agreement between the Governors of several western US states to consider various market-driven tools and government policies to deal with GHGs. However, today, the initiative is registered as a non-profit corporation and includes as participants only five jurisdictions: the US state of California, and the Canadian provinces of British Columbia, Quebec, Manitoba, and Ontario. Why the withdrawals? In the US, several governorships changed, with newly elected officials philosophically opposed to cap-and-trade as a way to address GHGs. Furthermore, when the recession hit North America in 2009, many of the states that rely on hydrocarbons as a pillar of their economies decided not to pass legislation “authorizing participation in WCI’s cap and trade…”8 Long-term climate change strategy took a backseat to short-term economic recovery for certain states and that remains the state of matters today. Ontario’s place in the WCI In the meantime, much has happened in Canada on the climate change front. Two of the remaining participants

in the WCI – Quebec and California – agreed in 2013 to link their emissions trading programs. During the Paris climate conference in 2015, Ontario, Quebec, and Manitoba signed a memorandum of understanding to harmonize their cap-and-trade programs under the WCI.9 Manitoba and Quebec each rely heavily on GHG-neutral hydro resources to power their economies. However, Ontario is not nearly as well endowed with hydropower as its eastern and western neighbours and therefore must rely on a more varied electricity energy mix that includes 28 percent natural gas (see Figure 2). Ontario is also home to Canada’s largest provincial economy, with a significant industrial sector. Figure 2: Ontario Electric Power Mix, April 2016

Source: IESO

Ontario has a long history of innovation in energy, being the only province that has developed a significant nuclear power industry – 20 total reactors. Ontario also made the decision to phase-out coal-powered generation, which it managed to complete in 2014. Over the past decade, the province has developed a renewable energy feed-in-tariff system, which permits both large and small renewable energy producers to feed their energy into the provincial grid and receive a subsidy. What does Ontario plan to achieve through cap-and-trade? The province provided details of its strategy through Bill 172, “Climate Change Mitigation and Low-carbon Economy Act, 2016”, which states two main goals: a) to reduce greenhouse gas in order to respond to climate change, to protect the environment and to assist

CERI Commodity Report - Crude Oil

Page 3

Ontarians to transition to a low-carbon economy; and b) to enable Ontario to collaborate and coordinate its actions with similar actions in other jurisdictions…”10 Everything will get started in 2017, with the intention of reducing greenhouse gases 37 percent below 1990 levels by 2030. Central to the plan is the sale of carbon allowances to industry that will garner in excess of $1.8 billion; the province intends to reinvest this revenue in programs aiming to improve the environment such as environmental research and development, public transportation, and renewable energy sources. The program emissions cap:

equates to the total number of carbon allowances that will be sold by the government, with one allowance being equal to one tonne of greenhouse gas emissions. Emitters are expected to purchase sufficient credits to cover their emissions in a given year … the plan allows for free credit allocation to competitively sensitive industries until the end of the first compliance review period in 2020.11

The province’s overall carbon strategy moves beyond the industry and power sectors to target homeowners and drivers, too, imposing a gasoline tax and natural gas home heating taxes. The challenges Ontario could face in implementing this carbon strategy through the WCI are similar to the ones noted above: much will depend on the province assigning the right number of carbon allowances – not too many and not to few. Management efficiency of the program will also be a significant factor in its success. It also depends on the political climate in Ontario; Canadian provinces are not immune to political debates over energy, as recent pipeline discussions have shown. As for the gasoline and home heating taxes, it could be that over the short term consumers may not notice the proposed 4.3 cents/litre gasoline tax and the approximately $5/month12 extra they will be paying to heat their homes; gasoline prices have plummeted since 2014 and natural gas has remained at a low price for over five years. However, there is a risk utilities and retailers could be required to purchase emissions units to account for their customers’ consumption, especially if the economy surges. They would inevitably attempt to pass these costs on to consumers, and that, coupled with the gasoline and natural gas taxes, could potentially cause a consumer backlash.

But the potential outcome is significant. A working carbon market including Canada’s largest province and America’s most populous state could possibly lower emissions at minimal cost to the economy, as opposed to simple taxation measures. Simple taxation could raise revenue but perhaps do little to lower emissions – emitters under a taxation scheme could pay their taxes and continue to emit as usual. This cap and trade market could make other jurisdictions take notice and possibly act, something that would support the objective of keeping global warming to below 2 degrees C, the defined goal of the 2015 Paris Climate Conference. Endnotes 1The major greenhouse gases are carbon dioxide; methane; nitrous oxide; ozone; CFC 12; HCFC-22; Sulfur Hexaflouride. 2Bureau of Environment, Tokyo Metropolitan Government. “Tokyo Cap and Trade: NEW The 5th Year Result of the Tokyo Cap-and-Trade Program.” https://www.kankyo.metro.tokyo.jp/en/climate/cap_and_trade.html Accessed April 5, 2016. 3Building a low-carbon economy – the UK’s contribution to tackling climate change. Committee on Climate Change. December 2008. Published by The Stationery Office. Copyright of the Crown. Page 149. https://www.theccc.org.uk/publication/building-a-low-carbon-economy-the-uks-contribution-to-tackling-climate-change-2/ Accessed April 5, 2016. 4ABC News. “Carbon tax: a timeline of its tortuous history in Australia”. July 16, 2014. http://www.abc.net.au/news/2014-07-10/carbon-tax-timeline/5569118 Accessed April 5, 2016. 5“New Zealand closes carbon trading loophole”. Reuters. May 16, 2014. http://www.reuters.com/article/new-zealand-carbon-idUSL3N0O20P820140516 Accessed April 5, 2016. 6Chan, Gabriel et al. The SO2 Allowance Trading System and the Clean Air Act Amendments of 1990: Reflections on Twenty Years of Policy Innovation. Harvard Kennedy School. January 2012. Page 4. www.hks.harvard.edu/m-rcbg/heep/papers/SO2-Brief_digital_final.pdf+&cd=7&hl=en&ct=clnk&gl=ca Accessed April 5, 2016. 7Chan et al. Page 5. 8Nesteroff, Mike. “The Western Climate Initiative is Dead, Long Live the WCI.” Sustainability & Climate Change Reporter. November 23, 2011. http://www.jdsupra.com/legalnews/the-western-climate-initiative-is-dead-50871/ Accessed April 5, 2016. 9Government of Ontario. “Ontario, Quebec and Manitoba Form a Dynamic Alliance to Fight Climate Change”. December 7, 2015. https://news.ontario.ca/opo/en/2015/12/ontario-quebec-and-manitoba-form-a-dynamic-alliance-to-fight-climate-change.html Accessed April 5, 2016. 10Murray, Hon. Glen R. Minister of the Environment and Climate Change. Bill 172. “Climate Change Mitigation and Low-carbon Economy Act, 2016.” Legislative Assembly of Ontario. http://www.ontla.on.ca/web/bills/bills_detail.do?locale=en&Intranet=&BillID=3740 Accessed April 6, 2016. 11Kroft, Jason and Luke Sinclair. “Ontario’s long awaited cap-and-trade plan.” Canadian Energy Law. February 26, 2016. http://www.canadianenergylaw.com/2016/02/articles/climate-change/ontarios-long-awaited-capandtrade-plan/?utm_source=Mondaq&utm_medium=syndication&utm_campaign=View-Original Accessed April 6, 2016. 12Kroft and Sinclair.

CERI Commodity Report - Crude Oil

Page 4

SOU

RC

E: E

IA.

SOU

RC

E: E

IA.

SOU

RC

E: N

RC

an, E

IA, B

ayte

x.

SOU

RC

E: E

IA, C

ERI.

-4-20246810

12

0

10

20

30

40

50

60

70 M

ar-

15

Ap

r-1

5M

ay

-15

Jun

-15

Jul-

15

Au

g-1

5Se

p-1

5O

ct-1

5N

ov-

15

De

c-1

5Ja

n-1

6Fe

b-1

6M

ar-

16

Ap

r-1

6

US$

/bb

l

Dif

fere

nti

al

WT

IB

ren

t

Sp

ot

Cru

de

Pri

ces

Sp

ot

Cru

de

Pri

ces

Sp

ot

Cru

de

Pri

ces

Sp

ot

Cru

de

Pri

ces

US

$/b

bl

WT

I -

Ed

mo

nto

n L

igh

tP

rice

Dif

fere

nti

als

WT

I -

Ed

mo

nto

n L

igh

tP

rice

Dif

fere

nti

als

WT

I -

Bre

nt

Pri

ce D

iffe

ren

tia

ls (U

S$

/bb

l)

Spot Price

sW

TI

Bre

nt

Cdn.L

ight*

H.H

ard

isty

Year-

to-D

ate

33.7

334.2

628.1

518.2

3

Quart

er-

to-D

ate

33.3

533.8

428.1

518.2

3

April 11, 2016

40.4

641.5

826.72

19.37

-200

20

40

60

80

10

0

12

0

14

0 Ma

r-1

0M

ar-

11

Ma

r-1

2M

ar-

13

Ma

r-1

4M

ar-

15

Ma

r-1

6

US

$/b

bl

Dif

fere

nti

al

WT

IE

dm

on

ton

Lig

ht

WT

I -

Ed

mo

nto

n L

igh

tP

rice

Dif

fere

nti

als

(US

$/b

bl)

20

25

30

35

40

45

50

12

34

US

$/b

bl

11

-Ja

n-1

61

2-F

eb

-16

12

-Ap

r-1

6

NN

YM

EX

WT

I C

rud

e F

orw

ard

Cu

rve

4

co

ntr

act

mo

nth

s

0

20

40

60

80

10

0

12

0 Ma

r-1

0M

ar-

11

Ma

r-1

2M

ar-

13

Ma

r-1

4M

ar-

15

Ma

r-1

6

US

$/b

bl

WT

IH

ard

isty

He

av

yW

CS

WW

TI

-H

ard

isty

He

av

yP

rice

Dif

fere

nti

als

WT

I -

Ca

na

dia

n H

ea

vy

Be

nch

ma

rks

(US

$/b

bl)

Relevant • Independent • Objective

Page 5

SOU

RC

E: E

IA, C

ERI.

SO

UR

CE:

NR

Can

.

SOU

RC

E: I

EA O

il M

arke

t R

epo

rt.

SOU

RC

E: E

IA W

eekl

y P

etro

leu

m S

tatu

s R

epo

rt.

0.5

0

0.7

5

1.0

0

1.2

5

1.5

0

1.7

5

2.0

0

2.2

5 Ma

r-1

5A

pr-

15

Ma

y-1

5Ju

n-1

5Ju

l-1

5A

ug-

15

Sep

-15

Oct

-15

No

v-1

5D

ec-

15

Jan

-16

Feb

-16

Ma

r-1

6A

pr-

16

US

$/g

al

RB

OB

Ga

soli

ne

He

ati

ng

Oil

NY

ME

X P

etr

ole

um

Pro

du

cts

NYM

EX P

rice

sUnle

aded G

aso

line

Heating O

il

Year-

to-D

ate

1.1

994

1.0

899

Quart

er-

to-D

ate

1.1

751

1.0

843

April 11, 2016

1.5

080

1.2

150

0.6

0

0.7

0

0.8

0

0.9

0

1.0

0

1.1

0

1.2

0

1.3

0

1.4

0

1.5

0 Ma

r-1

0M

ar-

11

Ma

r-1

2M

ar-

13

Ma

r-1

4M

ar-

15

Ma

r-1

6

CD

N/U

S$

CD

N/U

S$

Exc

ha

ng

e R

ate

49

.0%

49

.5%

50

.0%

50

.5%

51

.0%

51

.5%

52

.0%

52

.5%

0

10

20

30

40

50

60

70

80

90

10

0

11

0

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

MM

bp

d

To

tal

OE

CD

To

tal

No

n-O

EC

Dn

on

-OE

CD

De

ma

nd

sh

are

Oil

Dem

an

d in

Se

lec

ted

Co

un

trie

sG

lob

al

Oil

De

ma

nd

-20

%

0%

20

%

40

%

60

%

80

%

10

0%

To

tal

Ga

soli

ne

Jet

Fu

el

Dis

till

ate

Re

sid

ua

lP

rop

an

eO

the

r

%

UU

S P

rod

uct

s D

em

an

dM

arc

h 2

01

5 -

Ma

rch

20

16

Y-o

n-Y

ch

an

ge

CERI Commodity Report - Crude Oil

Page 6

SOU

RC

E: I

EA O

il M

arke

t R

epo

rt, C

ERI.

SO

UR

CE:

IEA

Oil

Mar

ket

Rep

ort

.

SOU

RC

E: I

EA O

il M

arke

t R

epo

rt.

SOU

RC

E: I

EA O

il M

arke

t R

epo

rt.

57

.0%

57

.5%

58

.0%

58

.5%

59

.0%

59

.5%

60

.0%

60

.5%

61

.0%

61

.5%

0

20

40

60

80

10

0

12

0

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

MM

bp

d

no

n-O

PE

C S

up

ply

OP

EC

Su

pp

lyn

on

-OP

EC

Sh

are

of

Glo

ba

l S

up

ply

SG

lob

al

Oil

Su

pp

ly

0

2,0

00

4,0

00

6,0

00

8,0

00

10

,00

0

12

,00

0

14

,00

0

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

Mb

pd

Ala

ska

Ca

lifo

rnia

Te

xa

sF

ed

era

l G

OM

Oth

er

Low

er

48

NG

LsO

the

r

US

Oil

Pro

du

ctio

nb

y r

eg

ion

0

50

0

1,0

00

1,5

00

2,0

00

2,5

00

3,0

00

3,5

00

4,0

00

4,5

00

5,0

00

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

Mb

pd

AB

L/M

/HA

B B

itu

me

nS

KO

the

rN

GLs

Sy

nth

eti

c

Ca

na

dia

n O

il P

rod

uct

ion

by

pro

du

ct

0

50

0

1,0

00

1,5

00

2,0

00

2,5

00

3,0

00

3,5

00

Fe

b-1

3F

eb

-14

Fe

b-1

5F

eb

-16

Mb

pd

OE

CD

No

rth

Am

eri

caO

EC

D E

uro

pe

OE

CD

Pa

cifi

c

OE

CD

Co

mm

erc

ial

Sto

cks

by

re

gio

n

Relevant • Independent • Objective

Page 7

SOU

RC

E: E

IA W

eekl

y P

etro

leu

m S

tatu

s R

epo

rt.

SOU

RC

E: I

EA O

il M

arke

t R

epo

rt.

-15

.0

-10

.0

-5.0

0.0

5.0

10

.0

15

.0

20

.0

Cru

de

Ga

soli

ne

Dis

till

ate

Pro

du

cts

To

tal

MM

b

US

Co

mm

erc

ial

Sto

cks

Feb

rua

ry 2

6 -

Ma

rch

25

, 20

16

M-o

n-M

Ch

an

ge

16

5

16

7.5

17

0

17

2.5

17

5

17

7.5

18

0

18

2.5

18

5

18

7.5

19

0

19

2.5

19

5

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

MM

b

Ca

na

dia

n S

tock

s o

n L

an

d

CERI Commodity Report - Crude Oil

Page 8

World Supply and Demand Balance (MMbpd)

OPEC Crude Oil Production (MMbpd)

WTI Price Projections ($US/barrel)

2013 2014 2015 2016 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

World Demand 91.9 92.9 94.7 95.9 91.9 92.1 93.3 94.1 93.6 94.1 95.6 95.5 94.8 95.2 96.6 96.8

OECD 46.0 45.7 46.2 46.1 45.8 44.8 45.9 46.4 46.4 45.3 46.6 46.3 46.1 45.5 46.6 46.3

non-OECD 45.9 47.1 48.5 49.7 46.1 47.3 47.4 47.7 47.1 48.8 49.0 49.2 48.7 49.7 50.1 50.4

World Supply 91.4 93.7 96.4 0.0 92.1 93.0 94.3 95.5 95.1 96.3 96.9 97.3 96.4 95.8 96.4 96.5

Non-OPEC 53.8 56.3 57.7 57.0 55.0 55.8 56.5 57.7 57.3 57.4 57.8 58.1 57.0 56.9 56.9 57.0

OPEC NGLs 6.3 6.5 6.7 6.9 6.4 6.4 6.6 6.6 6.6 6.7 6.7 6.8 6.8 6.8 6.9 6.9

OPEC Crude 27.4 27.7 28.1 28.2 30.7 30.8 31.2 31.2 31.2 32.2 32.4 32.4 32.6 32.1 32.6 32.6

Supply - Demand1 -0.6 0.8 1.7 -95.9 0.2 1.0 0.9 1.4 1.5 2.2 1.4 1.7 1.6 0.6 -0.2 -0.3

OECD

Stocks (MMbbls) 2566 2582 2652 2720 2712 2815 2905 2984 3015 3084 3112 3103

Days Cover 56 58 58 59 58 62 62 64 65 68 67 67

Sustainable

Capacity Jan-16 Feb-16 Mar-16 Jan-16 Feb-16 Mar-16

Saudi Arabia 12.26 10.21 10.22 10.16 2.05 2.04 2.10

Iran 3.60 3.00 3.22 3.30 0.60 0.38 0.30

UAE 2.93 2.93 2.78 2.73 0.00 0.15 0.20

Kuwait 2.83 2.83 2.83 2.83 0.00 0.00 0.00

Qatar 0.67 0.64 0.67 0.67 0.03 0.00 0.00

Angola 1.81 1.75 1.76 1.80 0.06 0.05 0.01

Nigeria 1.90 1.85 1.76 1.70 0.05 0.14 0.20

Libya 0.40 0.38 0.37 0.34 0.02 0.03 0.06

Algeria 1.12 1.10 1.10 1.11 0.02 0.02 0.01

Ecuador 0.55 0.53 0.55 0.54 0.02 0.00 0.01

Venezuela 2.46 2.35 2.37 2.35 0.11 0.09 0.11

Indonesia 0.72 0.70 0.71 0.72 0.02 0.01 0.00

Production Spare Capacity vs Production

2014 2015 2016 2017 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

High Price Case 39.88 45.10 37.40 39.60 40.70 41.80 44.00

Reference Case 93.28 48.71 36.25 41.00 48.49 57.85 46.47 42.03 34.00 36.00 37.00 38.00 40.00

Low Price Case 30.81 34.85 28.90 30.60 31.45 32.30 34.00

Relevant • Independent • Objective

Page 9

Data Appendix

CERI Commodity Report - Crude Oil

Page 10

A1: Historic Light Sweet Crude Futures Prices ($US per barrel)

A2: Historic Crude Product Futures Prices (¢US per gallon)

Notes (Tables A1 and A2): Prices are listed by contract month. Close: final contract close on the last day of trading. Last 3 Day Average Close: simple average con-

tract close on last three days of trading. Average When Near Month: simple average closing price on trading days when contract was near month. 12-Month Strip

Average: simple average of daily near 12-month contract closing prices in a given contract month. Spread: difference between one-month and two-month forward

prices in a given period. Source: New York Mercantile Exchange (NYMEX).

NYMEX Light Sweet Crude

Last 3 Day Avg. When 12-Month Spread

Close Average Near Mo. Strip Avg. (1-2 Mo.)

2013 96.82 97.37 97.01 97.45 -0.12

2014 96.53 96.37 96.73 87.56 0.54

2015 49.68 49.80 51.41 53.75 -0.78

1Q 2015 51.08 51.34 54.75 56.95 -0.47

2Q 2015 53.32 53.04 52.84 56.55 -1.51

3Q 2015 50.39 50.63 53.14 54.10 -0.42

4Q 2015 43.92 44.17 44.89 47.38 -0.70

1Q 2016 30.92 31.19 34.29 38.10 -1.44

Yr-on-Yr Chg. -39.5% -39.2% -37.4% -33.1%

Apr-15 45.72 44.78 47.98 52.78 -1.84

May-15 55.26 55.79 51.65 55.42 -1.57

Jun-15 58.98 58.56 58.89 61.46 -1.12

Jul-15 59.68 59.91 59.63 61.11 -0.41

Aug-15 50.36 50.47 54.66 53.70 -0.36

Sep-15 41.14 41.52 45.12 47.50 -0.49

Oct-15 45.83 45.73 44.47 46.73 -0.57

Nov-15 45.55 46.23 46.32 48.55 -0.51

Dec-15 40.39 40.56 43.88 46.86 -1.03

Jan-16 34.74 34.81 38.61 42.22 -1.39

Feb-16 26.55 28.14 33.74 36.96 -1.10

Mar-16 31.48 30.63 30.52 35.13 -1.83

Apr-16 41.45 40.27 36.44 40.15 -1.69

Yr-on-Yr Chg. -9.3% -10.1% -24.1% -23.9%

NYMEX Unleaded Gasoline NYMEX Heating Oil

Last 3 Day Avg. When 12-Month Spread Last 3 Day Avg. When 12-Month Spread

Close Average Near Mo. Strip Avg. (1-2 Mo.) Close Average Near Mo. Strip Avg. (1-2 Mo.)

2013 284.3 285.6 284.5 274.2 0.5 298.2 299.0 298.9 304.9 -0.5

2014 270.6 272.8 271.8 260.8 1.7 285.9 287.7 286.4 290.2 1.4

2015 168.8 166.0 166.4 157.8 0.5 174.8 171.9 173.2 179.6 0.5

1Q 2015 153.9 151.7 152.1 165.9 -9.1 194.4 189.3 188.0 186.9 5.3

2Q 2015 197.2 194.1 191.8 181.2 0.5 188.3 185.6 186.1 192.9 0.3

3Q 2015 185.7 180.9 186.1 156.3 8.6 171.5 167.9 170.0 179.2 -1.1

4Q 2015 138.4 137.2 135.5 127.8 1.9 145.0 144.9 148.7 159.5 -2.3

1Q 2016 114.0 112.5 111.5 125.9 -9.2 107.7 106.9 107.4 117.8 -2.0

Yr-on-Yr Chg. -25.9% -25.8% -26.7% -24.1% -44.6% -43.6% -42.9% -36.9%

Apr-15 178.0 179.3 182.6 172.6 0.3 171.8 172.6 178.2 183.2 1.8

May-15 205.0 202.3 189.9 180.4 0.1 197.6 194.7 184.0 191.9 -0.5

Jun-15 208.6 200.5 202.8 190.6 1.2 195.5 189.4 196.3 203.6 -0.4

Jul-15 209.0 205.6 206.9 180.1 3.7 188.7 186.2 188.9 197.6 -0.7

Aug-15 184.1 183.0 191.1 157.2 6.0 158.4 159.3 168.2 177.8 -1.3

Sep-15 164.0 154.0 160.4 131.6 16.3 167.4 158.2 152.8 162.1 -1.4

Oct-15 138.9 136.7 138.2 127.7 1.8 151.3 149.6 153.9 164.3 -2.1

Nov-15 140.5 136.8 134.9 128.3 1.8 149.9 148.6 149.9 161.4 -2.6

Dec-15 135.9 138.2 133.5 127.3 2.1 133.7 136.4 142.4 152.6 -2.3

Jan-16 126.7 125.8 125.4 137.4 -1.0 110.1 110.3 117.9 129.9 -3.1

Feb-16 110.3 107.6 109.4 123.6 -2.6 105.5 103.7 100.1 109.8 -1.7

Mar-16 105.0 104.1 99.5 116.7 -24.1 107.6 106.6 104.3 113.9 -1.3

Apr-16 143.6 145.3 139.9 137.4 -4.3 118.5 116.7 119.3 128.5 -1.2

Yr-on-Yr Chg. -19.3% -19.0% -23.4% -20.4% -31.0% -32.4% -33.0% -29.9%

Relevant • Independent • Objective

Page 11

A3: World Crude Oil Contract Prices (FOB, $US per barrel)

A4: North American Posted Crude Prices (FOB, $US per barrel)

Notes: 1. ANS is Delivered price on US West Coast. 2. Edmonton Light Sweet prices are discontinued as of May 1, 2014 and replaced by the Canadian Light Crude

blend which is traded daily on the Net Energy Index. 3. Hardisty Heavy. Posted prices are based on price at the end of each month. Sources: Oil & Gas Journal;

Natural Resources Canada.

Notes: 1. Urals is Delivered price at Mediterranean. Contract prices are based on prices at the end of each month. Source: OPEC Monthly Oil Market Report.

Saudi U.A.E. Oman U.K. Norway Russia Venez. Kuwait Ecuador Mexico Nigeria Indon.

Arab Lgt Dubai Oman Brent Ekofisk Urals1 T.J. Light Blend Oriente Isthmus Bonny Lgt Minas

2013 106.60 105.51 105.57 108.69 109.89 108.05 96.71 105.10 97.77 105.16 111.41 107.32

2014 97.07 96.61 96.94 99.00 99.78 98.01 86.87 95.21 87.25 93.58 100.77 98.63

2015 49.87 50.96 51.24 52.44 53.20 51.94 41.17 48.15 44.97 51.14 52.99 49.24

1Q 2015 50.15 52.03 52.77 53.97 54.96 53.30 44.05 48.36 45.02 49.87 54.57 52.13

2Q 2015 60.43 61.28 61.34 61.84 62.53 62.18 52.11 58.72 55.83 62.12 62.72 60.54

3Q 2015 49.01 49.80 49.92 50.29 50.93 49.75 37.94 47.70 42.85 49.96 50.62 45.46

4Q 2015 39.90 40.74 40.93 43.67 44.38 42.50 30.59 37.83 36.16 42.62 44.04 38.82

1Q 2016 29.95 30.47 31.50 33.91 34.41 32.30 22.67 27.89 26.73 31.39 33.72 31.64

Yr-on-Yr Chg. -40.3% -41.4% -40.3% -37.2% -37.4% -39.4% -48.5% -42.3% -40.6% -37.1% -38.2% -39.3%

Mar-15 52.20 54.66 55.12 55.93 57.18 55.07 45.79 50.52 45.79 51.41 56.75 54.11

Apr-15 57.73 58.55 58.66 59.50 60.51 59.70 49.49 55.96 52.73 59.10 60.65 58.55

May-15 62.62 63.54 63.60 64.32 64.86 64.33 55.09 60.92 58.04 63.78 65.31 62.98

Jun-15 60.94 61.76 61.77 61.69 62.21 62.52 51.74 59.29 56.71 63.48 62.19 60.09

Jul-15 54.95 56.15 56.23 56.54 57.02 55.84 44.43 53.85 47.78 55.62 56.77 51.86

Aug-15 46.52 47.87 47.87 46.72 47.53 46.22 35.26 45.28 39.75 46.56 47.07 42.46

Sep-15 45.56 45.38 45.65 47.61 48.24 47.19 34.13 43.96 41.03 47.71 48.01 42.05

Oct-15 45.37 45.84 46.07 48.56 49.23 47.49 35.48 43.61 39.91 46.90 49.16 42.13

Nov-15 40.64 41.79 42.10 44.30 45.10 43.05 31.87 38.39 36.40 43.29 44.81 40.79

Dec-15 33.70 34.59 34.61 38.16 38.80 36.97 24.42 31.49 32.18 37.68 38.16 33.53

Jan-16 26.35 26.81 27.48 30.75 31.45 29.15 20.80 23.92 24.03 30.03 30.40 30.80

Feb-16 28.77 29.44 30.37 32.46 32.86 30.87 21.38 26.77 24.70 28.68 32.24 29.49

Mar-16 34.74 35.15 36.66 38.51 38.91 36.87 25.83 32.99 31.45 35.45 38.53 34.62

Yr-on-Yr Chg. -33.4% -35.7% -33.5% -31.1% -32.0% -33.0% -43.6% -34.7% -31.3% -31.0% -32.1% -36.0%

United States Canada Light vs. Heavy

ANS1 Lost Hills Kern R. WTI WTS GCS

Okla.

Sw.

Kans.

Sw.

Mich.

So.

Wyo.

Sw.

CDN

Sweet2 HH3

2013 100.20 106.62 99.05 94.46 89.46 87.65 94.46 93.48 86.46 90.27 90.13 76.52

2014 94.79 94.13 87.39 88.44 83.44 82.19 88.44 85.77 80.44 83.52 82.59 73.85

2015 51.64 50.91 42.28 45.63 40.63 39.38 45.63 44.40 37.63 42.34 44.83 35.71

1Q 2015 60.55 52.27 41.63 46.33 41.33 40.08 46.33 44.42 38.33 42.56 43.14 35.08

2Q 2015 48.46 61.76 53.02 55.33 50.33 49.08 55.33 54.42 47.33 51.58 55.84 46.69

3Q 2015 57.69 47.85 40.37 42.58 37.58 36.33 42.58 41.50 34.58 39.26 41.85 33.90

4Q 2015 39.88 41.77 34.08 38.25 33.25 32.00 38.25 37.25 30.25 35.94 38.97 27.77

1Q 2016 34.14 33.54 27.08 31.67 26.67 25.42 31.67 30.75 23.67 30.20 28.28 18.11

Yr-on-Yr Chg. -43.6% -35.8% -34.9% -31.7% -35.5% -36.6% -31.7% -30.8% -38.3% -29.0% -34.4% -48.4%

Mar-15 42.65 54.47 42.95 48.00 43.00 41.75 48.00 44.25 40.00 44.18 44.58 37.01

Apr-15 46.82 61.44 51.15 53.75 48.75 47.50 53.75 52.75 45.75 49.90 50.79 40.34

May-15 46.61 62.72 54.05 56.25 51.25 50.00 56.25 55.25 48.25 52.47 57.96 47.93

Jun-15 51.94 61.13 53.85 56.00 51.00 49.75 56.00 55.25 48.00 52.38 58.78 51.79

Jul-15 57.76 49.87 41.75 43.50 38.50 37.25 43.50 42.50 35.50 39.87 46.29 44.14

Aug-15 57.55 47.72 40.65 42.00 37.00 35.75 42.00 40.75 34.00 37.97 36.85 25.94

Sep-15 57.76 45.95 38.70 42.25 37.25 36.00 42.25 41.25 34.25 39.95 42.49 31.85

Oct-15 41.44 47.09 38.85 43.00 38.00 36.75 43.00 42.00 35.00 40.84 43.88 31.40

Nov-15 40.48 42.46 33.85 38.25 33.25 32.00 38.25 37.25 30.25 35.96 39.83 28.25

Dec-15 37.72 35.76 29.55 33.50 28.50 27.25 33.50 32.50 25.50 31.01 33.41 23.80

Jan-16 37.72 31.62 24.85 30.00 25.00 23.75 30.00 29.00 22.00 27.87 30.49 13.73

Feb-16 41.77 31.78 25.15 29.25 24.25 23.00 29.25 28.25 21.25 27.03 27.94 22.19

Mar-16 22.94 37.21 31.25 35.75 30.75 29.50 35.75 35.00 27.75 35.71 26.19 18.50

Yr-on-Yr Chg. -46.2% -31.7% -27.2% -25.5% -28.5% -29.3% -25.5% -20.9% -30.6% -19.2% -41.2% -50.0%

CERI Commodity Report - Crude Oil

Page 12

A5: Crude Oil Quality Differentials (FOB, $US per barrel)

A6: Crude Oil Spot Prices and Differentials (FOB, $US per barrel)

Notes: 1. OPEC-Reference Basket is average price of seven crude streams: Algeria Saharan Blend, Dubai Fateh, Indonesia Minas, Mexico Isthmus, Nigeria Bonny

Light, Saudi Arabia Light and Venezuela Tia Juana Light. Source: OPEC Monthly Oil Market Report.

Notes: 1. Edmonton Light Sweet prices are discontinued as of May 1, 2014 and replaced by the Canadian Light Crude blend which is traded daily on the Net Energy Index. 2. Hardisty Heavy. Based on contract prices at the end of each month. Sources: OPEC Monthly Oil Market Report: Oil & Gas Journal; Natural Resources Canada.

Light vs. Heavy Sweet vs. Sour

Arab Lt Arab Hv Diff. Isthmus Maya Diff.

CDN

Sweet2 HH2 Diff. GCS WTS Diff.

2013 106.60 103.96 2.64 105.16 97.74 7.42 90.13 76.52 13.61 87.65 89.46 -1.81

2014 97.07 93.57 3.50 93.58 85.88 7.69 82.59 73.85 8.74 82.19 83.44 -1.25

2015 49.87 47.02 2.85 51.14 44.02 7.13 44.83 35.71 9.13 39.38 40.63 -1.25

1Q 2015 50.15 46.89 3.26 49.87 44.36 5.51 43.14 35.08 8.06 40.08 41.33 -1.25

2Q 2015 60.43 57.23 3.20 62.12 53.77 8.35 55.84 46.69 9.15 49.08 50.33 -1.25

3Q 2015 49.01 47.25 1.76 49.96 43.53 6.44 41.85 33.90 7.95 36.33 37.58 -1.25

4Q 2015 39.90 36.72 3.18 42.62 34.41 8.21 38.97 27.77 11.21 32.00 33.25 -1.25

1Q 2016 29.95 26.92 3.04 31.39 27.17 4.22 28.28 18.11 10.17 25.42 26.67 -1.25

Yr-on-Yr Chg. -40.3% -42.6% -37.1% -38.8% -34.4% -48.4% -36.6% -35.5%

Mar-15 52.20 49.34 2.86 51.41 45.67 5.74 44.58 37.01 7.58 41.75 43.00 -1.25

Apr-15 57.73 54.26 3.47 59.10 49.53 9.57 50.79 40.34 10.45 47.50 48.75 -1.25

May-15 62.62 59.42 3.20 63.78 55.16 8.62 57.96 47.93 10.03 50.00 51.25 -1.25

Jun-15 60.94 58.01 2.93 63.48 56.63 6.85 58.78 51.79 6.99 49.75 51.00 -1.25

Jul-15 54.95 53.55 1.40 55.62 50.53 5.09 46.29 44.14 2.15 37.25 38.50 -1.25

Aug-15 46.52 44.82 1.70 46.56 40.55 6.01 36.85 25.94 10.91 35.75 37.00 -1.25

Sep-15 45.56 43.37 2.19 47.71 39.50 8.21 42.49 31.85 10.64 36.00 37.25 -1.25

Oct-15 45.37 43.01 2.36 46.90 39.14 7.76 43.88 31.40 12.48 36.75 38.00 -1.25

Nov-15 40.64 37.00 3.64 43.29 35.36 7.93 39.83 28.25 11.58 32.00 33.25 -1.25

Dec-15 33.70 30.15 3.55 37.68 28.73 8.95 33.41 23.80 9.61 27.25 28.50 -1.25

Jan-16 26.35 22.50 3.85 30.03 24.47 5.56 30.49 13.73 16.76 23.75 25.00 -1.25

Feb-16 28.77 26.15 2.62 28.68 25.14 3.54 27.94 22.19 5.75 23.00 24.25 -1.25

Mar-16 34.74 32.10 2.64 35.45 31.89 3.56 26.19 18.50 7.69 29.50 30.75 -1.25

Yr-on-Yr Chg. -33.4% -34.9% -31.0% -30.2% -41.2% -50.0% -29.3% -28.5%

Spot Prices Differentials

WTI Brent Dubai Urals Basket1 WTI-Brent WTI-Dubai WTI-Urals WTI-Basket

2013 98.03 108.68 105.44 108.39 105.94 -11.87 -8.63 -11.58 -9.12

2014 93.28 98.94 96.52 97.97 96.19 -2.41 0.01 -1.44 0.34

2015 48.71 52.37 50.84 51.50 49.52 -2.69 -1.16 -1.82 0.16

1Q 2015 48.49 53.96 51.72 52.93 50.30 -2.88 -0.64 -1.85 0.78

2Q 2015 57.85 61.87 61.23 61.53 59.89 -8.55 -7.91 -8.21 -6.57

3Q 2015 46.47 50.44 50.01 49.75 48.16 -0.05 0.38 0.64 2.23

4Q 2015 42.03 43.71 40.71 42.30 39.72 0.21 3.21 1.62 4.20

1Q 2016 33.41 33.95 30.59 32.34 29.96 -3.03 0.33 -1.42 0.97

Yr-on-Yr Chg. -31.1% -37.1% -40.9% -38.9% -40.4%

Mar-15 47.79 56.05 54.53 54.82 52.46 -10.33 -8.81 -9.10 -6.74

Apr-15 54.46 59.79 58.37 59.44 57.30 -4.53 -3.11 -4.18 -2.04

May-15 59.27 64.35 63.58 63.67 62.16 -5.37 -4.60 -4.69 -3.18

Jun-15 59.80 61.63 61.84 61.57 60.21 -1.95 -2.16 -1.89 -0.53

Jul-15 50.90 56.48 56.20 55.87 54.19 -6.12 -5.84 -5.51 -3.83

Aug-15 42.86 46.60 47.64 45.76 45.46 -5.46 -6.50 -4.62 -4.32

Sep-15 45.45 47.61 45.45 46.98 44.83 -1.78 0.38 -1.15 1.00

Oct-15 46.20 48.51 45.92 47.31 45.02 -2.96 -0.37 -1.76 0.53

Nov-15 42.75 44.26 41.76 42.37 40.50 -3.87 -1.37 -1.98 -0.11

Dec-15 37.24 38.13 34.55 36.98 33.64 -3.39 0.19 -2.24 1.10

Jan-16 31.57 30.75 26.81 29.15 26.50 -4.20 -0.26 -2.60 0.05

Feb-16 30.38 32.46 29.33 30.87 28.72 -0.98 2.15 0.61 2.76

Mar-16 37.76 38.49 35.12 36.85 34.65 2.96 6.33 4.60 6.80

Yr-on-Yr Chg. -21.0% -31.3% -35.6% -32.8% -33.9%

Relevant • Independent • Objective

Page 13

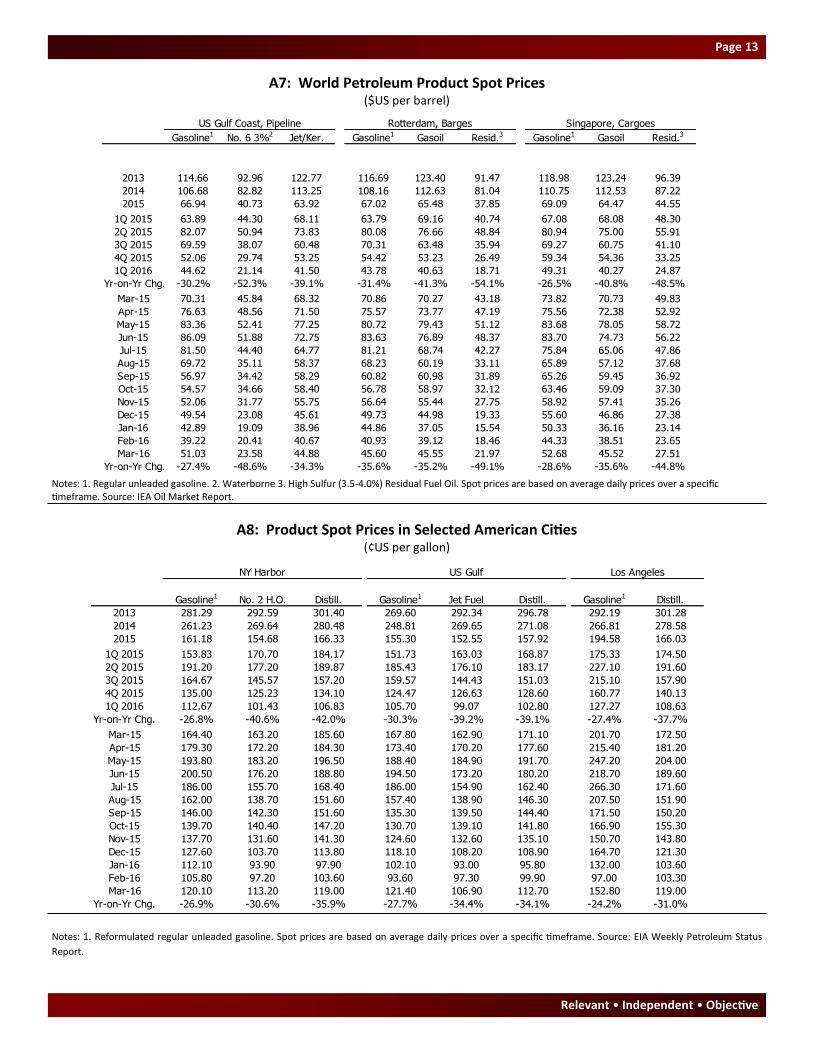

A7: World Petroleum Product Spot Prices ($US per barrel)

A8: Product Spot Prices in Selected American Cities (¢US per gallon)

Notes: 1. Reformulated regular unleaded gasoline. Spot prices are based on average daily prices over a specific timeframe. Source: EIA Weekly Petroleum Status

Report.

Notes: 1. Regular unleaded gasoline. 2. Waterborne 3. High Sulfur (3.5-4.0%) Residual Fuel Oil. Spot prices are based on average daily prices over a specific timeframe. Source: IEA Oil Market Report.

US Gulf Coast, Pipeline Rotterdam, Barges Singapore, Cargoes

Gasoline1 No. 6 3%2 Jet/Ker. Gasoline1 Gasoil Resid.3 Gasoline1 Gasoil Resid.3

2013 114.66 92.96 122.77 116.69 123.40 91.47 118.98 123.24 96.39

2014 106.68 82.82 113.25 108.16 112.63 81.04 110.75 112.53 87.22

2015 66.94 40.73 63.92 67.02 65.48 37.85 69.09 64.47 44.55

1Q 2015 63.89 44.30 68.11 63.79 69.16 40.74 67.08 68.08 48.30

2Q 2015 82.07 50.94 73.83 80.08 76.66 48.84 80.94 75.00 55.91

3Q 2015 69.59 38.07 60.48 70.31 63.48 35.94 69.27 60.75 41.10

4Q 2015 52.06 29.74 53.25 54.42 53.23 26.49 59.34 54.36 33.25

1Q 2016 44.62 21.14 41.50 43.78 40.63 18.71 49.31 40.27 24.87

Yr-on-Yr Chg. -30.2% -52.3% -39.1% -31.4% -41.3% -54.1% -26.5% -40.8% -48.5%

Mar-15 70.31 45.84 68.32 70.86 70.27 43.18 73.82 70.73 49.83

Apr-15 76.63 48.56 71.50 75.57 73.77 47.19 75.56 72.38 52.92

May-15 83.36 52.41 77.25 80.72 79.43 51.12 83.68 78.05 58.72

Jun-15 86.09 51.88 72.75 83.63 76.89 48.37 83.70 74.73 56.22

Jul-15 81.50 44.40 64.77 81.21 68.74 42.27 75.84 65.06 47.86

Aug-15 69.72 35.11 58.37 68.23 60.19 33.11 65.89 57.12 37.68

Sep-15 56.97 34.42 58.29 60.82 60.98 31.89 65.26 59.45 36.92

Oct-15 54.57 34.66 58.40 56.78 58.97 32.12 63.46 59.09 37.30

Nov-15 52.06 31.77 55.75 56.64 55.44 27.75 58.92 57.41 35.26

Dec-15 49.54 23.08 45.61 49.73 44.98 19.33 55.60 46.86 27.38

Jan-16 42.89 19.09 38.96 44.86 37.05 15.54 50.33 36.16 23.14

Feb-16 39.22 20.41 40.67 40.93 39.12 18.46 44.33 38.51 23.65

Mar-16 51.03 23.58 44.88 45.60 45.55 21.97 52.68 45.52 27.51

Yr-on-Yr Chg. -27.4% -48.6% -34.3% -35.6% -35.2% -49.1% -28.6% -35.6% -44.8%

NY Harbor US Gulf Los Angeles

Gasoline1 No. 2 H.O. Distill. Gasoline1 Jet Fuel Distill. Gasoline1 Distill.

2013 281.29 292.59 301.40 269.60 292.34 296.78 292.19 301.28

2014 261.23 269.64 280.48 248.81 269.65 271.08 266.81 278.58

2015 161.18 154.68 166.33 155.30 152.55 157.92 194.58 166.03

1Q 2015 153.83 170.70 184.17 151.73 163.03 168.87 175.33 174.50

2Q 2015 191.20 177.20 189.87 185.43 176.10 183.17 227.10 191.60

3Q 2015 164.67 145.57 157.20 159.57 144.43 151.03 215.10 157.90

4Q 2015 135.00 125.23 134.10 124.47 126.63 128.60 160.77 140.13

1Q 2016 112.67 101.43 106.83 105.70 99.07 102.80 127.27 108.63

Yr-on-Yr Chg. -26.8% -40.6% -42.0% -30.3% -39.2% -39.1% -27.4% -37.7%

Mar-15 164.40 163.20 185.60 167.80 162.90 171.10 201.70 172.50

Apr-15 179.30 172.20 184.30 173.40 170.20 177.60 215.40 181.20

May-15 193.80 183.20 196.50 188.40 184.90 191.70 247.20 204.00

Jun-15 200.50 176.20 188.80 194.50 173.20 180.20 218.70 189.60

Jul-15 186.00 155.70 168.40 186.00 154.90 162.40 266.30 171.60

Aug-15 162.00 138.70 151.60 157.40 138.90 146.30 207.50 151.90

Sep-15 146.00 142.30 151.60 135.30 139.50 144.40 171.50 150.20

Oct-15 139.70 140.40 147.20 130.70 139.10 141.80 166.90 155.30

Nov-15 137.70 131.60 141.30 124.60 132.60 135.10 150.70 143.80

Dec-15 127.60 103.70 113.80 118.10 108.20 108.90 164.70 121.30

Jan-16 112.10 93.90 97.90 102.10 93.00 95.80 132.00 103.60

Feb-16 105.80 97.20 103.60 93.60 97.30 99.90 97.00 103.30

Mar-16 120.10 113.20 119.00 121.40 106.90 112.70 152.80 119.00

Yr-on-Yr Chg. -26.9% -30.6% -35.9% -27.7% -34.4% -34.1% -24.2% -31.0%

CERI Commodity Report - Crude Oil

Page 14

B1: World Petroleum Supply and Demand Balance (million barrels per day)

Notes: 1. Totals for OECD and non-OECD supply include net refining gains; specific regions/groupings within each do not. 2. OPEC demand is an estimate based on

historical annual data. 3. Balance for World equals global stockbuilds (+) and stockdraws (-) for crude oil and petroleum products and miscellaneous gains and loss-

es. Regional surpluses (+) and deficits (-) are balanced through net-imports and stock changes in the short-term, and net-imports in the longer term. Supply includes

crude oil, condensates, NGLs, oil from non-conventional sources and processing gains. Demand is for petroleum products.

Source: IEA Oil Market Report.

OECD Non-OECD OPEC World

N. A. Europe Asia-Pac Total1 Asia Non-Asia FSU Total1 P. Gulf Non-Gulf Total2 Total3

Demand

2011 24.0 14.3 8.2 46.4 19.3 11.4 4.6 35.3 4.9 2.9 7.9 89.5

2012 23.6 13.8 8.5 45.9 19.9 12.0 4.6 36.5 5.1 3.0 8.2 90.7

2013 24.1 13.6 8.3 46.0 20.7 12.1 4.7 37.5 5.3 3.1 8.5 91.9

2014 24.1 13.5 8.1 45.7 21.2 12.1 4.9 38.2 5.5 3.2 8.9 92.9

2015 24.4 13.7 8.1 46.2 22.4 12.1 4.9 39.4 5.8 3.4 9.2 94.7

1Q 2014 23.9 13.0 8.9 45.8 21.0 11.6 4.6 37.2 5.5 3.2 8.9 91.9

2Q 2014 23.7 13.4 7.7 44.8 21.3 12.3 4.9 38.5 5.5 3.2 8.9 92.1

3Q 2014 24.4 13.9 7.7 45.9 20.8 12.6 5.1 38.5 5.5 3.2 8.9 93.3

4Q 2014 24.6 13.5 8.3 46.4 21.7 12.0 5.0 38.7 5.5 3.2 8.9 94.1

1Q 2015 24.2 13.4 8.7 46.4 22.0 11.3 4.6 37.9 5.8 3.4 9.2 93.6

2Q 2015 24.1 13.6 7.6 45.3 22.4 12.2 4.9 39.5 5.8 3.4 9.2 94.1

3Q 2015 24.7 14.1 7.8 46.6 22.3 12.5 5.0 39.8 5.8 3.4 9.2 95.6

4Q 2015 24.4 13.7 8.3 46.3 22.8 12.1 5.0 39.9 5.8 3.4 9.2 95.5

1Q 2016 24.1 13.5 8.6 46.1 22.9 11.4 4.8 39.1 6.0 3.5 9.6 94.8

Supply

2011 14.6 3.8 0.6 20.1 7.7 8.5 13.6 30.7 25.7 9.6 35.8 88.6

2012 15.8 3.5 0.6 21.0 6.9 8.0 13.8 29.6 26.2 10.6 37.6 90.9

2013 17.2 3.3 0.5 22.2 6.9 7.9 13.9 29.7 26.2 9.8 36.7 91.4

2014 19.1 3.3 0.5 24.1 6.8 8.1 13.9 29.8 26.8 9.0 37.5 93.7

2015 19.9 3.5 0.5 25.1 7.0 8.3 14.0 30.3 28.2 8.6 38.7 96.4

1Q 2014 18.3 3.5 0.5 23.5 6.8 8.0 13.9 29.7 26.7 9.0 36.3 92.1

2Q 2014 18.9 3.2 0.5 23.8 6.8 8.0 13.8 29.6 26.8 9.0 36.4 93.1

3Q 2014 19.3 3.1 0.5 24.1 6.8 8.2 13.8 29.8 26.9 9.3 37.0 94.2

4Q 2014 19.9 3.4 0.5 25.0 7.1 8.3 13.9 30.3 26.8 9.4 37.0 95.5

1Q 2015 20.0 3.4 0.4 25.0 7.1 8.3 14.0 30.4 27.3 8.8 36.9 95.1

2Q 2015 19.6 3.5 0.4 24.7 7.1 8.2 14.0 30.3 28.3 8.9 38.0 96.3

3Q 2015 20.1 3.4 0.5 25.1 7.0 8.1 13.9 30.0 28.7 8.6 39.1 97.0

4Q 2015 20.1 3.6 0.5 25.3 7.1 8.1 14.0 30.2 28.6 8.7 39.2 97.2

1Q 2016 19.7 3.5 0.5 24.9 6.9 7.9 14.2 30.1 28.9 8.5 39.4 96.4

Balance

2011 -9.4 -10.5 -7.6 -26.3 -11.6 -2.9 9.0 -4.6 20.8 6.7 28.0 -0.9

2012 -7.8 -10.3 -7.9 -24.9 -13.0 -4.0 9.2 -6.9 21.1 7.6 29.4 0.2

2013 -6.9 -10.3 -7.8 -23.8 -13.8 -4.2 9.2 -7.8 20.9 6.7 28.2 -0.5

2014 -5.0 -10.2 -7.6 -21.6 -14.4 -4.0 9.0 -8.4 21.2 5.7 28.6 0.8

2015 -4.5 -10.2 -7.6 -21.1 -15.4 -3.8 9.1 -9.1 22.4 5.3 29.5 1.7

1Q 2014 -5.6 -9.5 -8.4 -22.3 -14.2 -3.6 9.3 -7.5 21.2 5.8 27.4 0.2

2Q 2014 -4.8 -10.2 -7.2 -21.0 -14.5 -4.3 8.9 -8.9 21.3 5.7 27.6 1.0

3Q 2014 -5.1 -10.8 -7.2 -21.8 -14.0 -4.4 8.7 -8.7 21.3 6.1 28.1 0.9

4Q 2014 -4.7 -10.1 -7.8 -21.4 -14.6 -3.7 8.9 -8.4 21.3 6.1 28.1 1.4

1Q 2015 -4.2 -10.0 -8.3 -21.4 -14.9 -3.0 9.4 -7.5 21.5 5.4 27.7 1.5

2Q 2015 -4.5 -10.1 -7.2 -20.6 -15.3 -4.0 9.1 -9.1 22.5 5.5 28.8 2.2

3Q 2015 -4.6 -10.7 -7.3 -21.5 -15.3 -4.4 8.9 -9.8 22.9 5.2 29.9 1.4

4Q 2015 -4.3 -10.1 -7.8 -21.0 -15.7 -4.0 9.0 -9.7 22.9 5.3 29.9 1.7

1Q 2016 -4.4 -10.0 -8.1 -21.2 -16.0 -3.5 9.4 -9.0 22.9 5.0 29.7 1.6

Relevant • Independent • Objective

Page 15

B2: World Petroleum Production (million barrels per day)

B3: OECD Commercial Petroleum Stocks (million barrels)

Notes: 1. Production includes crude oil, condensates and NGLs. 2. Reserve-Production ratio is based on latest month production and British Petroleum reserve

estimates. Sources: IEA Oil Market Report and BP Statistical Review of World Energy.

Notes: 1. Product includes only finished petroleum products. 2. Total stocks include NGLs, refinery feedstocks, additives/oxygenates and other hydrocarbons. All

stocks are closing levels for respective reporting period. Source: IEA Oil Market Report.

OECD Non-OECD OPEC World

N. A. Europe Asia-Pac Total Asia Non-Asia FSU Total P. Gulf Non-Gulf Total Total1

2013 17.14 3.32 0.48 20.94 7.73 7.97 13.80 29.50 26.18 9.80 36.72 87.16

2014 19.08 3.32 0.51 22.91 6.88 8.16 13.87 28.90 26.77 8.96 37.48 89.29

2015 19.93 3.46 0.46 23.85 7.06 8.22 13.99 29.28 28.20 8.64 38.73 91.86

1Q 2015 19.88 3.41 0.43 23.72 7.90 8.39 14.05 30.33 27.26 8.81 36.94 90.99

2Q 2015 19.51 3.49 0.44 23.45 7.95 8.23 13.97 30.15 28.27 8.92 38.03 91.63

3Q 2015 20.05 3.35 0.50 23.91 7.01 8.21 13.92 29.15 28.66 8.63 39.13 92.19

4Q 2015 20.08 3.60 0.47 24.15 7.09 8.16 14.04 29.30 28.62 8.67 39.15 92.60

1Q 2016 19.73 3.54 0.46 23.73 6.94 8.00 14.18 29.13 28.94 8.50 39.35 92.21

Yr-on-Yr Chg. -0.8% 3.8% 7.0% 0.0% -12.2% -4.6% 0.9% -4.0% 6.2% -3.5% 6.5% 1.3%

Mar-15 20.11 3.48 0.37 23.96 8.01 8.41 14.06 30.48 27.82 8.89 37.55 91.99

Apr-15 20.12 3.54 0.45 24.12 7.98 8.22 14.01 30.22 28.09 9.10 37.96 92.30

May-15 19.54 3.53 0.39 23.46 7.89 8.23 14.01 30.13 28.22 8.98 38.00 91.59

Jun-15 19.58 3.45 0.49 23.52 8.03 8.22 13.97 30.21 28.66 8.80 38.35 92.08

Jul-15 20.01 3.44 0.49 23.94 7.90 8.16 13.93 30.00 28.67 8.81 38.36 92.30

Aug-15 20.03 3.36 0.51 23.91 7.94 8.21 13.88 30.03 28.60 8.80 38.17 92.11

Sep-15 19.65 3.31 0.48 23.44 7.95 8.17 13.92 30.04 28.66 8.84 38.37 91.85

Oct-15 19.93 3.53 0.46 23.93 7.05 8.16 13.94 29.15 28.46 8.76 39.09 92.17

Nov-15 20.06 3.60 0.49 24.15 7.18 8.15 14.07 29.40 28.71 8.70 39.23 92.78

Dec-15 20.01 3.65 0.47 24.13 7.09 8.33 14.08 29.48 28.69 8.62 39.15 92.76

Jan-16 19.83 3.55 0.44 23.83 6.96 8.00 14.19 29.15 29.02 8.59 39.47 92.45

Feb-16 19.80 3.49 0.46 23.75 6.95 7.99 14.19 29.13 28.92 8.53 39.33 92.21

Mar-16 19.58 3.57 0.46 23.61 6.92 8.01 14.16 29.10 28.90 8.41 39.24 91.95

Yr-on-Yr Chg. -2.6% 2.6% 24.3% -1.5% -13.6% -4.8% 0.7% -4.5% 3.9% -5.4% 4.5% 0.0%

R/P Ratio2 32.5 9.7 24.4 28.9 13.8 23.1 27.5 23.0 75.8 130.2 83.7 50.7

North America Europe Asia-Pacific OECD

Crude Product Total Crude Product Total Crude Product Total Crude Product1 Total2

2013 500 670 1,315 307 497 869 145 170 382 952 1,337 2,566

2014 553 727 1,443 311 505 880 157 169 389 1,020 1,401 2,712

2015 641 773 1,591 361 563 989 206 166 435 1,208 1,502 3,015

4Q 2014 553 727 1,443 311 505 880 157 169 389 1,020 1,401 2,712

1Q 2015 625 695 1,483 344 524 939 178 153 392 1,148 1,372 2,815

2Q 2015 626 735 1,537 344 523 939 201 165 430 1,171 1,423 2,906

3Q 2015 617 763 1,572 339 559 967 202 176 445 1,158 1,498 2,984

4Q 2015 641 773 1,591 361 563 989 206 166 435 1,208 1,502 3,015

Yr-on-Yr Chg. 16.0% 6.4% 10.2% 16.2% 11.5% 12.4% 31.3% -1.8% 11.8% 18.4% 7.2% 11.1%

Feb-15 601 693 1,454 322 526 914 173 158 392 1,096 1,377 2,761

Mar-15 625 695 1,483 344 524 939 178 153 392 1,148 1,372 2,815

Apr-15 638 704 1,512 350 520 939 171 158 391 1,158 1,382 2,842

May-15 629 725 1,528 344 532 947 198 168 430 1,171 1,425 2,905

Jun-15 626 735 1,537 344 523 939 201 165 430 1,171 1,423 2,906

Jul-15 617 738 1,542 339 526 933 205 170 439 1,161 1,434 2,914

Aug-15 614 759 1,564 343 553 964 205 178 449 1,162 1,490 2,976

Sep-15 617 763 1,572 339 559 967 202 176 445 1,158 1,498 2,984

Oct-15 642 745 1,576 347 556 972 205 169 439 1,194 1,469 2,987

Nov-15 647 762 1,593 346 570 982 191 170 428 1,184 1,503 3,003

Dec-15 641 773 1,591 361 563 989 206 166 435 1,208 1,502 3,015

Jan-16 661 780 1,614 358 588 1,014 192 167 425 1,210 1,534 3,053

Feb-16 675 769 1,620 357 591 1,018 198 163 423 1,230 1,523 3,060

Yr-on-Yr Chg. 12.4% 11.0% 11.4% 10.8% 12.4% 11.3% 14.4% 2.8% 8.0% 12.3% 10.6% 10.9%

CERI Commodity Report - Crude Oil

Page 16

B4: OPEC Crude Oil Production and Targets (million barrels per day)

Notes: 1. Does not include NGLs; OPEC production targets apply to crude oil only. 2. Iraq does not have an official OPEC target. 3. OPEC-10 production targets. 4. As

of latest month. Source: IEA Oil Market Report.

B5: OECD Refinery Activity Crude Input (MMbpd) - Utilization (percent) - Refining Margins ($US/barrel)

Notes: 1. Based on dated Brent being processed in average US Gulf cracking refinery. 2. Based on dated Brent in average Rotterdam cracking refinery. 3. Based on

spot Dubai in average Singapore hydroskimming refinery. Source: IEA Oil Market Report.

Non-Persian Gulf OPEC-11 OPEC-11

Arabia Iran UAE Kuwait Qatar Venez. Nigeria Libya Algeria Angola Ecuador Total1 Target Iraq2

2013 9.66 2.68 2.76 2.81 0.73 2.50 1.95 0.90 1.15 1.72 0.52 27.38 30.00 3.08

2014 9.72 2.81 2.76 2.80 0.71 2.46 1.90 0.46 1.12 1.66 0.55 27.65 30.00 3.33

2015 10.17 2.86 2.88 2.79 0.66 2.40 1.80 0.40 1.11 1.76 0.54 28.06 30.00 3.99

1Q 2015 9.87 2.82 2.84 2.80 0.67 2.39 1.81 0.37 1.11 1.77 0.55 26.99 30.00 3.50

2Q 2015 10.34 2.85 2.87 2.77 0.66 2.43 1.77 0.46 1.11 1.76 0.55 27.56 30.00 3.94

3Q 2015 10.29 2.87 2.92 2.78 0.64 2.40 1.80 0.38 1.12 1.77 0.53 28.19 30.00 4.25

4Q 2015 10.18 2.89 2.89 2.78 0.66 2.38 1.84 0.40 1.11 1.76 0.54 28.11 30.00 4.28

1Q 2016 10.21 3.17 2.81 2.83 0.66 2.36 1.77 0.36 1.10 1.77 0.54 28.30 30.00 4.28

Yr-on-Yr Chg. 3.4% 12.4% -1.1% 1.1% -1.5% -1.3% -2.2% -2.7% -0.9% 0.0% -1.8% 4.9% 22.3%

Mar-15 10.19 2.79 2.84 2.80 0.68 2.40 1.74 0.48 1.12 1.75 0.55 27.34 30.00 3.70

Apr-15 10.21 2.88 2.87 2.81 0.67 2.44 1.80 0.52 1.11 1.73 0.55 27.57 30.00 3.75

May-15 10.31 2.85 2.87 2.77 0.66 2.44 1.76 0.45 1.11 1.77 0.55 27.52 30.00 3.84

Jun-15 10.48 2.82 2.88 2.74 0.66 2.42 1.78 0.41 1.11 1.78 0.54 27.62 30.00 4.19

Jul-15 10.38 2.87 2.91 2.74 0.62 2.42 1.77 0.39 1.11 1.80 0.54 27.55 30.00 4.25

Aug-15 10.28 2.87 2.93 2.80 0.65 2.40 1.77 0.37 1.13 1.73 0.53 27.46 30.00 4.17

Sep-15 10.20 2.88 2.91 2.81 0.65 2.38 1.86 0.37 1.12 1.79 0.53 27.5 30.00 4.30

Oct-15 10.21 2.88 2.89 2.73 0.67 2.38 1.90 0.43 1.11 1.78 0.53 28.18 30.00 4.17

Nov-15 10.19 2.87 2.89 2.80 0.68 2.40 1.84 0.39 1.11 1.74 0.54 28.14 30.00 4.33

Dec-15 10.14 2.91 2.89 2.81 0.64 2.37 1.80 0.38 1.11 1.75 0.54 28.04 30.00 4.35

Jan-16 10.21 3.00 2.93 2.83 0.64 2.35 1.85 0.38 1.10 1.75 0.53 28.27 30.00 4.43

Feb-16 10.22 3.22 2.78 2.83 0.67 2.37 1.76 0.37 1.10 1.76 0.55 28.34 30.00 4.22

Mar-16 10.19 3.30 2.73 2.83 0.67 2.35 1.70 0.34 1.11 1.80 0.54 28.28 30.00 4.19

Yr-on-Yr Chg. 0.0% 18.3% -3.9% 1.1% -1.5% -2.1% -2.3% -29.2% -0.9% 2.9% -1.8% 3.4% 13.2%

Quotas3 8.05 3.34 2.22 2.22 0.73 1.99 1.67 1.47 1.20 1.52 0.43 30.00

Over/Under4 26.6% -1.2% 23.0% 27.5% -8.2% 18.1% 1.8% -76.9% -7.5% 18.4% 25.6% -5.7%

Persian Gulf

North America Europe Asia-Pacific OECD

Input Util. Margin1 Input Util. Margin2 Input Util. Margin3 Input Util.

2013 18.4 87.7 1.40 11.5 75.2 3.48 6.7 75.1 -1.63 36.6 81.0

2014 18.9 90.0 1.67 11.4 75.0 3.35 6.5 73.2 -1.98 36.8 81.6

2015 19.1 91.1 5.65 12.1 79.4 7.28 6.7 75.1 0.62 37.9 84.0

4Q 2014 18.9 90.0 -1.03 11.8 77.4 4.72 6.6 74.1 -0.1 37.3 82.6

1Q 2015 18.5 88.2 5.93 12.0 78.4 7.03 7.1 78.8 2.6 37.5 83.0

2Q 2015 19.4 92.3 5.89 11.8 77.4 8.10 6.4 71.8 0.5 37.6 83.2

3Q 2015 19.5 93.0 7.30 12.4 81.3 8.91 6.7 75.3 -1.1 38.6 85.5

4Q 2015 19.1 91.0 3.49 12.3 80.4 5.09 6.7 74.4 0.6 38.0 84.1

Yr-on-Yr Chg. 1.1% -438.1% 3.9% 7.8% 0.5% -605.9% 1.8%

Feb-15 18.4 87.7 8.01 12.2 79.9 6.60 7.2 80.0 2.6 37.7 83.6

Mar-15 18.6 88.7 6.98 11.8 77.5 8.75 6.9 76.8 2.5 37.3 82.6

Apr-15 19.1 91.1 4.55 11.8 77.6 7.71 6.7 75.2 0.5 37.7 83.4

May-15 19.3 92.2 5.58 11.9 78.0 7.40 6.4 71.0 0.7 37.6 83.2

Jun-15 19.6 93.7 7.53 11.7 76.5 9.18 6.2 69.2 0.2 37.5 83.0

Jul-15 19.8 94.2 9.75 12.3 80.8 9.53 6.8 75.4 -2.3 38.8 86.0

Aug-15 19.7 93.9 8.54 12.4 81.4 10.05 7.0 78.0 -1.4 39.1 86.5

Sep-15 19.0 90.7 3.60 12.5 81.7 7.15 6.5 72.4 0.2 38.0 84.1

Oct-15 18.2 86.9 4.12 12.4 81.0 4.24 6.4 71.1 -0.8 36.9 81.8

Nov-15 19.3 91.9 3.60 12.2 79.7 6.65 6.6 73.7 1.8 38.0 84.2

Dec-15 19.7 94.0 2.76 12.3 80.5 4.38 7.0 78.4 0.7 39.0 86.4

Jan-16 19.0 90.8 4.27 12.0 78.9 5.50 7.1 79.5 2.8 38.2 84.5

Feb-16 18.6 88.8 3.10 11.9 77.9 3.66 7.3 81.3 0.9 37.8 83.6

Yr-on-Yr Chg. 1.3% -61.3% -2.5% -45% 1.8% -63.8% 0.1%

Relevant • Independent • Objective

Page 17

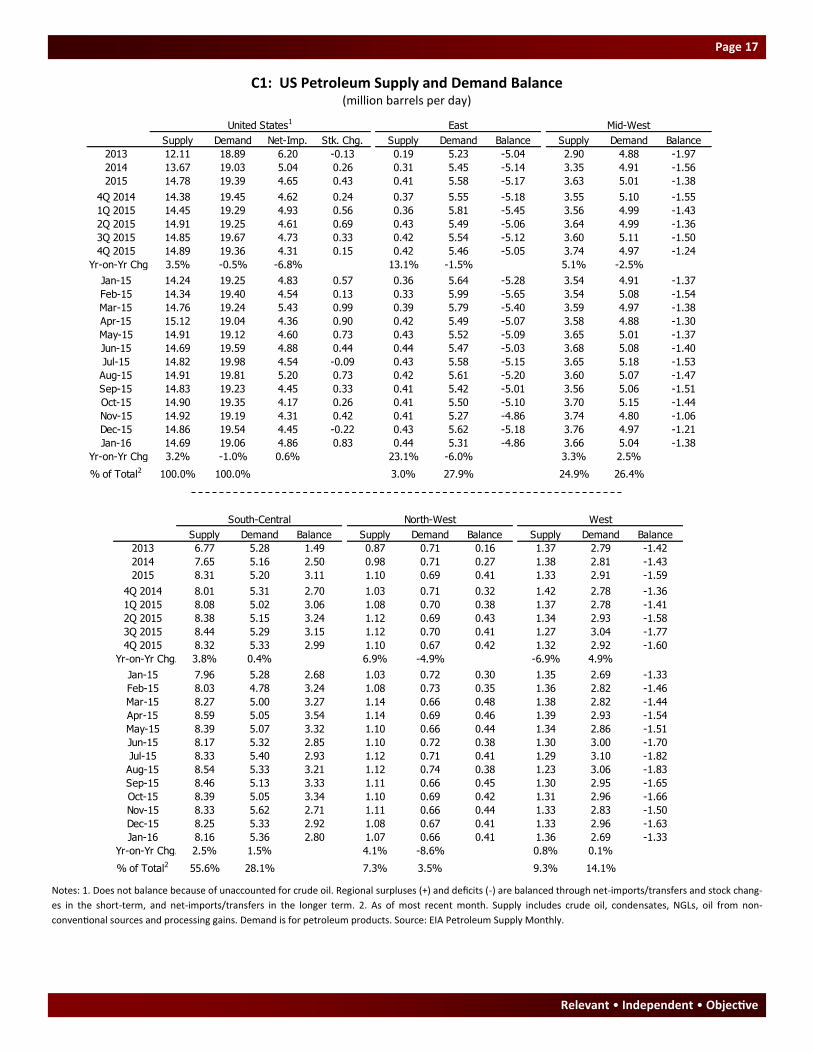

C1: US Petroleum Supply and Demand Balance (million barrels per day)

Notes: 1. Does not balance because of unaccounted for crude oil. Regional surpluses (+) and deficits (-) are balanced through net-imports/transfers and stock chang-

es in the short-term, and net-imports/transfers in the longer term. 2. As of most recent month. Supply includes crude oil, condensates, NGLs, oil from non-

conventional sources and processing gains. Demand is for petroleum products. Source: EIA Petroleum Supply Monthly.

United States1 East Mid-West

Supply Demand Net-Imp. Stk. Chg. Supply Demand Balance Supply Demand Balance

2013 12.11 18.89 6.20 -0.13 0.19 5.23 -5.04 2.90 4.88 -1.97

2014 13.67 19.03 5.04 0.26 0.31 5.45 -5.14 3.35 4.91 -1.56

2015 14.78 19.39 4.65 0.43 0.41 5.58 -5.17 3.63 5.01 -1.38

4Q 2014 14.38 19.45 4.62 0.24 0.37 5.55 -5.18 3.55 5.10 -1.55

1Q 2015 14.45 19.29 4.93 0.56 0.36 5.81 -5.45 3.56 4.99 -1.43

2Q 2015 14.91 19.25 4.61 0.69 0.43 5.49 -5.06 3.64 4.99 -1.36

3Q 2015 14.85 19.67 4.73 0.33 0.42 5.54 -5.12 3.60 5.11 -1.50

4Q 2015 14.89 19.36 4.31 0.15 0.42 5.46 -5.05 3.74 4.97 -1.24

Yr-on-Yr Chg. 3.5% -0.5% -6.8% 13.1% -1.5% 5.1% -2.5%

Jan-15 14.24 19.25 4.83 0.57 0.36 5.64 -5.28 3.54 4.91 -1.37

Feb-15 14.34 19.40 4.54 0.13 0.33 5.99 -5.65 3.54 5.08 -1.54

Mar-15 14.76 19.24 5.43 0.99 0.39 5.79 -5.40 3.59 4.97 -1.38

Apr-15 15.12 19.04 4.36 0.90 0.42 5.49 -5.07 3.58 4.88 -1.30

May-15 14.91 19.12 4.60 0.73 0.43 5.52 -5.09 3.65 5.01 -1.37

Jun-15 14.69 19.59 4.88 0.44 0.44 5.47 -5.03 3.68 5.08 -1.40

Jul-15 14.82 19.98 4.54 -0.09 0.43 5.58 -5.15 3.65 5.18 -1.53

Aug-15 14.91 19.81 5.20 0.73 0.42 5.61 -5.20 3.60 5.07 -1.47

Sep-15 14.83 19.23 4.45 0.33 0.41 5.42 -5.01 3.56 5.06 -1.51

Oct-15 14.90 19.35 4.17 0.26 0.41 5.50 -5.10 3.70 5.15 -1.44

Nov-15 14.92 19.19 4.31 0.42 0.41 5.27 -4.86 3.74 4.80 -1.06

Dec-15 14.86 19.54 4.45 -0.22 0.43 5.62 -5.18 3.76 4.97 -1.21

Jan-16 14.69 19.06 4.86 0.83 0.44 5.31 -4.86 3.66 5.04 -1.38

Yr-on-Yr Chg. 3.2% -1.0% 0.6% 23.1% -6.0% 3.3% 2.5%

% of Total2 100.0% 100.0% 3.0% 27.9% 24.9% 26.4%

South-Central North-West West Finished Petroleum Products

Supply Demand Balance Supply Demand Balance Supply Demand Balance

2013 6.77 5.28 1.49 0.87 0.71 0.16 1.37 2.79 -1.42

2014 7.65 5.16 2.50 0.98 0.71 0.27 1.38 2.81 -1.43

2015 8.31 5.20 3.11 1.10 0.69 0.41 1.33 2.91 -1.59

4Q 2014 8.01 5.31 2.70 1.03 0.71 0.32 1.42 2.78 -1.36

1Q 2015 8.08 5.02 3.06 1.08 0.70 0.38 1.37 2.78 -1.41

2Q 2015 8.38 5.15 3.24 1.12 0.69 0.43 1.34 2.93 -1.58

3Q 2015 8.44 5.29 3.15 1.12 0.70 0.41 1.27 3.04 -1.77

4Q 2015 8.32 5.33 2.99 1.10 0.67 0.42 1.32 2.92 -1.60

Yr-on-Yr Chg. 3.8% 0.4% 6.9% -4.9% -6.9% 4.9%

Jan-15 7.96 5.28 2.68 1.03 0.72 0.30 1.35 2.69 -1.33

Feb-15 8.03 4.78 3.24 1.08 0.73 0.35 1.36 2.82 -1.46

Mar-15 8.27 5.00 3.27 1.14 0.66 0.48 1.38 2.82 -1.44

Apr-15 8.59 5.05 3.54 1.14 0.69 0.46 1.39 2.93 -1.54

May-15 8.39 5.07 3.32 1.10 0.66 0.44 1.34 2.86 -1.51

Jun-15 8.17 5.32 2.85 1.10 0.72 0.38 1.30 3.00 -1.70

Jul-15 8.33 5.40 2.93 1.12 0.71 0.41 1.29 3.10 -1.82

Aug-15 8.54 5.33 3.21 1.12 0.74 0.38 1.23 3.06 -1.83

Sep-15 8.46 5.13 3.33 1.11 0.66 0.45 1.30 2.95 -1.65

Oct-15 8.39 5.05 3.34 1.10 0.69 0.42 1.31 2.96 -1.66

Nov-15 8.33 5.62 2.71 1.11 0.66 0.44 1.33 2.83 -1.50

Dec-15 8.25 5.33 2.92 1.08 0.67 0.41 1.33 2.96 -1.63

Jan-16 8.16 5.36 2.80 1.07 0.66 0.41 1.36 2.69 -1.33

Yr-on-Yr Chg. 2.5% 1.5% 4.1% -8.6% 0.8% 0.1%

% of Total2 55.6% 28.1% 7.3% 3.5% 9.3% 14.1%

CERI Commodity Report - Crude Oil

Page 18

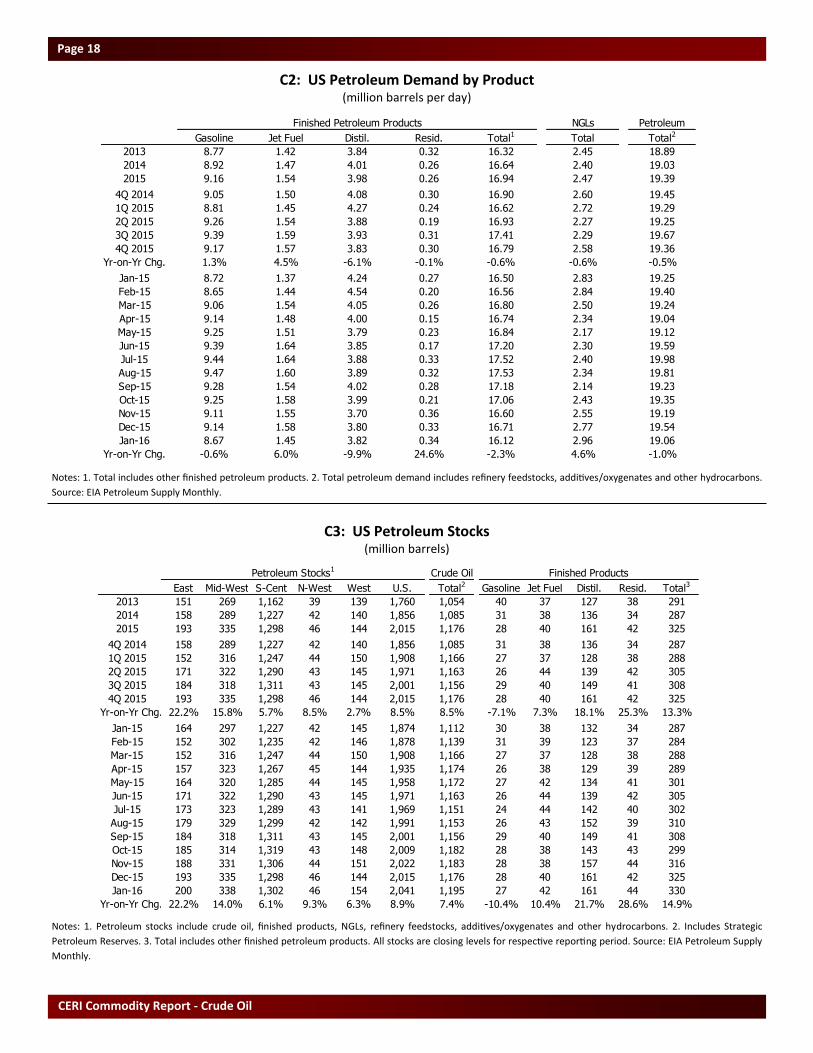

C2: US Petroleum Demand by Product (million barrels per day)

Notes: 1. Total includes other finished petroleum products. 2. Total petroleum demand includes refinery feedstocks, additives/oxygenates and other hydrocarbons.

Source: EIA Petroleum Supply Monthly.

C3: US Petroleum Stocks (million barrels)

Notes: 1. Petroleum stocks include crude oil, finished products, NGLs, refinery feedstocks, additives/oxygenates and other hydrocarbons. 2. Includes Strategic

Petroleum Reserves. 3. Total includes other finished petroleum products. All stocks are closing levels for respective reporting period. Source: EIA Petroleum Supply

Monthly.

Finished Petroleum Products NGLs Petroleum

Gasoline Jet Fuel Distil. Resid. Total1 Total Total2

2013 8.77 1.42 3.84 0.32 16.32 2.45 18.89

2014 8.92 1.47 4.01 0.26 16.64 2.40 19.03

2015 9.16 1.54 3.98 0.26 16.94 2.47 19.39

4Q 2014 9.05 1.50 4.08 0.30 16.90 2.60 19.45

1Q 2015 8.81 1.45 4.27 0.24 16.62 2.72 19.29

2Q 2015 9.26 1.54 3.88 0.19 16.93 2.27 19.25

3Q 2015 9.39 1.59 3.93 0.31 17.41 2.29 19.67

4Q 2015 9.17 1.57 3.83 0.30 16.79 2.58 19.36

Yr-on-Yr Chg. 1.3% 4.5% -6.1% -0.1% -0.6% -0.6% -0.5%

Jan-15 8.72 1.37 4.24 0.27 16.50 2.83 19.25

Feb-15 8.65 1.44 4.54 0.20 16.56 2.84 19.40

Mar-15 9.06 1.54 4.05 0.26 16.80 2.50 19.24

Apr-15 9.14 1.48 4.00 0.15 16.74 2.34 19.04

May-15 9.25 1.51 3.79 0.23 16.84 2.17 19.12

Jun-15 9.39 1.64 3.85 0.17 17.20 2.30 19.59

Jul-15 9.44 1.64 3.88 0.33 17.52 2.40 19.98

Aug-15 9.47 1.60 3.89 0.32 17.53 2.34 19.81

Sep-15 9.28 1.54 4.02 0.28 17.18 2.14 19.23

Oct-15 9.25 1.58 3.99 0.21 17.06 2.43 19.35

Nov-15 9.11 1.55 3.70 0.36 16.60 2.55 19.19

Dec-15 9.14 1.58 3.80 0.33 16.71 2.77 19.54

Jan-16 8.67 1.45 3.82 0.34 16.12 2.96 19.06

Yr-on-Yr Chg. -0.6% 6.0% -9.9% 24.6% -2.3% 4.6% -1.0%

Petroleum Stocks1 Crude Oil Finished Products

East Mid-West S-Cent N-West West U.S. Total2 Gasoline Jet Fuel Distil. Resid. Total3

2013 151 269 1,162 39 139 1,760 1,054 40 37 127 38 291

2014 158 289 1,227 42 140 1,856 1,085 31 38 136 34 287

2015 193 335 1,298 46 144 2,015 1,176 28 40 161 42 325

4Q 2014 158 289 1,227 42 140 1,856 1,085 31 38 136 34 287

1Q 2015 152 316 1,247 44 150 1,908 1,166 27 37 128 38 288

2Q 2015 171 322 1,290 43 145 1,971 1,163 26 44 139 42 305

3Q 2015 184 318 1,311 43 145 2,001 1,156 29 40 149 41 308

4Q 2015 193 335 1,298 46 144 2,015 1,176 28 40 161 42 325

Yr-on-Yr Chg. 22.2% 15.8% 5.7% 8.5% 2.7% 8.5% 8.5% -7.1% 7.3% 18.1% 25.3% 13.3%

Jan-15 164 297 1,227 42 145 1,874 1,112 30 38 132 34 287

Feb-15 152 302 1,235 42 146 1,878 1,139 31 39 123 37 284

Mar-15 152 316 1,247 44 150 1,908 1,166 27 37 128 38 288

Apr-15 157 323 1,267 45 144 1,935 1,174 26 38 129 39 289

May-15 164 320 1,285 44 145 1,958 1,172 27 42 134 41 301

Jun-15 171 322 1,290 43 145 1,971 1,163 26 44 139 42 305

Jul-15 173 323 1,289 43 141 1,969 1,151 24 44 142 40 302

Aug-15 179 329 1,299 42 142 1,991 1,153 26 43 152 39 310

Sep-15 184 318 1,311 43 145 2,001 1,156 29 40 149 41 308

Oct-15 185 314 1,319 43 148 2,009 1,182 28 38 143 43 299

Nov-15 188 331 1,306 44 151 2,022 1,183 28 38 157 44 316

Dec-15 193 335 1,298 46 144 2,015 1,176 28 40 161 42 325

Jan-16 200 338 1,302 46 154 2,041 1,195 27 42 161 44 330

Yr-on-Yr Chg. 22.2% 14.0% 6.1% 9.3% 6.3% 8.9% 7.4% -10.4% 10.4% 21.7% 28.6% 14.9%

Relevant • Independent • Objective

Page 19

C4: US Petroleum Net Imports by Source (million barrels per day)

Notes: 1. Total includes net-imports from Russia and Asia-Pacific region. 2. Total OPEC includes the other eight cartel members. 3. As of latest month. Source EIA

Petroleum Supply Monthly.

C5: US Regional Crude Oil Production (million barrels per day)

Notes: 1. California includes Federal Offshore crude oil production. 2. Gulf of Mexico includes Federal Offshore production adjacent to Texas and Louisiana. 3. Crude

oil Reserve-Production ratio as of latest production month. Crude oil production does not include NGLs. Source: EIA Petroleum Supply Monthly.

OPEC

Canada Mexico Lat. Am. Europe Africa M.E. Total1 Venez. S. Arabia Nigeria Total2 P. Gulf

2013 2.59 0.39 0.74 -0.08 0.37 1.99 6.20 0.71 1.32 0.24 3.47 1.99

2014 2.58 0.29 0.56 -0.12 0.17 1.85 5.04 0.71 1.16 0.04 2.98 1.86

2015 2.81 0.07 0.73 -0.18 0.17 1.49 4.65 0.75 1.05 0.06 2.65 1.50

4Q 2014 2.72 0.21 0.59 -0.07 0.15 1.41 4.62 0.64 0.88 0.03 2.50 1.41

1Q 2015 2.97 0.16 0.65 -0.12 0.13 1.39 4.93 0.68 0.93 0.04 2.49 1.40

2Q 2015 2.69 0.12 0.71 -0.14 0.15 1.61 4.61 0.74 1.16 0.02 2.67 1.61

3Q 2015 2.80 0.01 0.88 -0.15 0.22 1.32 4.73 0.79 1.01 0.08 2.58 1.33

4Q 2015 2.77 -0.01 0.70 -0.31 0.19 1.64 4.31 0.79 1.11 0.08 2.87 1.64

Yr-on-Yr Chg. 1.6% -105.1% 19.0% 322.1% 26.1% 16.2% -6.8% 23.2% 26.0% 203.7% 15.1% 16.4%

Jan-15 2.95 0.04 0.63 -0.12 0.12 1.32 4.83 0.60 0.82 0.04 2.36 1.33

Feb-15 2.93 0.09 0.51 -0.10 0.11 1.41 4.54 0.71 0.94 -0.01 2.55 1.42

Mar-15 3.03 0.34 0.82 -0.14 0.17 1.44 5.43 0.74 1.04 0.09 2.56 1.45

Apr-15 2.84 0.15 0.78 -0.36 0.14 1.52 4.36 0.80 1.20 0.03 2.63 1.53

May-15 2.51 0.03 0.71 0.05 0.19 1.71 4.60 0.77 1.21 0.05 2.82 1.72

Jun-15 2.73 0.20 0.63 -0.12 0.12 1.60 4.88 0.64 1.08 -0.01 2.55 1.60

Jul-15 2.53 -0.05 0.81 -0.10 0.24 1.45 4.54 0.70 1.17 0.11 2.63 1.46

Aug-15 2.98 0.09 1.03 -0.01 0.18 1.25 5.21 0.85 1.01 0.05 2.50 1.25

Sep-15 2.88 0.00 0.79 -0.34 0.25 1.28 4.45 0.81 0.86 0.08 2.61 1.28

Oct-15 2.43 0.03 0.67 -0.27 0.14 1.54 4.17 0.73 0.98 0.04 2.68 1.54

Nov-15 2.73 0.03 0.61 -0.33 0.20 1.65 4.31 0.77 1.23 0.08 2.91 1.65

Dec-15 3.14 -0.09 0.81 -0.32 0.22 1.72 4.45 0.86 1.12 0.13 3.02 1.73

Jan-16 3.19 -0.02 0.62 -0.17 0.23 1.51 4.86 0.65 1.05 0.12 2.82 1.51

Yr-on-Yr Chg. 8.1% -154.5% -0.8% 39.5% 94.1% 13.7% 0.7% 8.2% 28.9% 241.7% 19.7% 13.7%

% of Total3 65.7% -0.5% 12.8% -3.6% 4.7% 31.0% 100.0% 13.3% 21.7% 2.5% 58.1% 31.1%

Region of Origin

PAD District U.S. Major Producers

East Mid-West S-Cent N-West West Total Alaska Calif.1 Louis. Texas G. of Mex.2

2013 0.03 1.34 4.33 0.50 1.11 7.31 0.52 0.59 0.20 2.47 1.28

2014 0.04 1.62 5.00 0.58 1.11 8.35 0.50 0.60 0.19 3.04 1.35

2015 0.05 1.81 5.69 0.73 1.08 9.35 0.49 0.59 0.17 3.50 1.50

4Q 2014 0.04 1.77 5.32 0.63 1.08 8.85 0.47 0.61 0.19 3.26 1.43

1Q 2015 0.05 1.86 5.65 0.68 1.14 9.38 0.53 0.62 0.19 3.52 1.46

2Q 2015 0.05 1.77 5.65 0.73 1.09 9.28 0.49 0.59 0.17 3.54 1.43

3Q 2015 0.06 1.82 5.71 0.76 1.05 9.39 0.47 0.58 0.17 3.52 1.48

4Q 2015 0.05 1.78 5.75 0.75 1.02 9.35 0.46 0.56 0.17 3.41 1.65

Yr-on-Yr Chg. 6.7% 0.6% 8.1% 19.1% -5.8% 5.7% -2.9% -7.9% -8.9% 4.5% 15.4%

Jan-15 0.04 1.72 5.25 0.62 1.09 8.73 0.50 0.59 0.18 3.29 1.34

Feb-15 0.05 2.03 6.15 0.74 1.25 10.21 0.58 0.67 0.20 3.82 1.60

Mar-15 0.05 1.82 5.55 0.68 1.09 9.19 0.50 0.58 0.18 3.46 1.44

Apr-15 0.04 1.67 5.21 0.66 1.04 8.62 0.46 0.58 0.16 3.23 1.36

May-15 0.05 1.84 5.78 0.76 1.11 9.53 0.51 0.60 0.18 3.67 1.41

Jun-15 0.07 1.80 5.95 0.76 1.12 9.70 0.51 0.61 0.18 3.71 1.51

Jul-15 0.07 1.82 5.79 0.74 1.08 9.51 0.47 0.61 0.18 3.66 1.41

Aug-15 0.06 1.77 5.43 0.73 1.01 9.00 0.47 0.54 0.17 3.35 1.40

Sep-15 0.05 1.87 5.90 0.80 1.05 9.67 0.46 0.58 0.17 3.56 1.64

Oct-15 0.05 1.77 5.77 0.77 0.97 9.32 0.41 0.56 0.17 3.42 1.65

Nov-15 0.05 1.74 5.81 0.76 1.04 9.39 0.47 0.56 0.17 3.42 1.69

Dec-15 0.04 1.84 5.68 0.73 1.05 9.35 0.50 0.55 0.17 3.39 1.61

Jan-16 0.04 1.77 5.45 0.71 1.05 9.02 0.51 0.55 0.16 3.29 1.50

Yr-on-Yr Chg. 2.6% 2.4% 3.8% 13.7% -3.7% 3.3% 1.1% -7.7% -8.0% -0.1% 12.0%

R/P Ratio3 21.9 13.2 10.7 14.1 15.7 12.1 15.5 16.0 11.0 11.7 8.6

CERI Commodity Report - Crude Oil

Page 20

C6: US Refinery Activity Crude Input (MMbpd) - Utilization (percent)

Notes: 1) As of most recent month. Source: EIA Petroleum Supply Monthly.

C7: US Refinery Margins ($US per barrel)

Note: Based on specific crude being processed in average cracking refinery in a given area. As of February 2010, NY Harbor Arab Med. is now East Coast Composite.

Source: Oil and Gas Journal.

East Mid-West South-Central North-West West U.S.

Input Util. Input Util. Input Util. Input Util. Input Util. Input Util.

2013 1.10 85.1 3.42 90.7 8.22 90.4 0.58 92.7 2.56 84.8 15.88 89.2

2014 1.09 84.2 3.52 92.5 8.38 91.5 0.58 90.5 2.57 87.0 16.14 90.4

2015 1.15 90.7 3.59 93.1 8.70 93.4 0.60 93.2 2.58 88.2 16.61 92.3

4Q 2014 1.11 86.6 3.48 91.5 8.49 92.6 0.59 91.5 2.59 89.0 16.25 91.3

1Q 2015 1.14 90.9 3.60 93.8 8.54 93.2 0.60 92.6 2.63 91.5 16.51 92.9

2Q 2015 1.15 91.0 3.70 96.2 8.77 94.4 0.60 93.4 2.46 84.0 16.69 92.8

3Q 2015 1.15 90.4 3.65 94.6 8.77 93.5 0.61 94.2 2.67 91.0 16.85 93.2

4Q 2015 1.15 90.6 3.41 87.7 8.71 92.4 0.60 92.5 2.54 86.5 16.40 90.3

Yr-on-Yr Chg. 4.1% -2.1% 2.6% 1.7% -1.9% 0.9%

Jan-15 1.09 85.5 3.43 88.8 8.20 89.1 0.58 90.0 2.51 86.1 15.81 88.4

Feb-15 1.27 102.6 3.84 101.1 9.20 101.1 0.65 100.6 2.92 104.5 17.87 101.7

Mar-15 1.08 85.0 3.52 91.5 8.24 89.6 0.56 87.2 2.46 84.4 15.86 88.7

Apr-15 1.13 89.1 3.70 96.4 8.66 93.5 0.60 92.9 2.43 82.7 16.52 92.0

May-15 1.16 91.1 3.68 95.7 8.75 94.3 0.60 92.6 2.44 83.0 16.61 92.5

Jun-15 1.18 92.7 3.71 96.6 8.91 95.5 0.61 94.7 2.53 86.2 16.94 94.0

Jul-15 1.19 93.6 3.82 99.3 8.89 95.0 0.62 95.4 2.66 90.6 17.18 95.1

Aug-15 1.20 94.0 3.64 94.7 8.83 94.3 0.62 94.6 2.68 91.4 16.96 93.9

Sep-15 1.06 83.5 3.48 89.8 8.58 91.3 0.60 92.5 2.67 91.1 16.39 90.4

Oct-15 1.13 89.0 3.01 77.5 8.39 89.4 0.61 92.9 2.55 87.1 15.69 86.6

Nov-15 1.19 93.5 3.55 91.6 8.76 92.8 0.60 92.5 2.57 87.5 16.67 91.8

Dec-15 1.14 89.2 3.66 94.0 8.96 95.0 0.60 92.0 2.49 85.0 16.85 92.6

Jan-16 1.14 88.9 3.72 94.9 8.39 88.2 0.57 84.1 2.55 87.1 16.37 89.4

Yr-on-Yr Chg. 4.7% 8.6% 2.3% -1.5% 1.3% 3.5%

% of Total1 6.9% 22.7% 51.3% 3.5% 15.6% 100.0%

NY Harbor Chicago US Gulf Los Angeles

(East Coast Comp.) (WTI) (WTS) (ANS)

2013 9.20 21.63 12.83 10.25

2014 8.62 16.57 11.76 8.68

2015 12.86 18.05 12.96 19.50

1Q 2015 12.42 15.57 14.05 15.73

2Q 2015 17.81 18.79 15.02 21.83

3Q 2015 12.47 24.84 13.79 23.75

4Q 2015 8.74 12.99 8.98 16.67

1Q 2016 9.15 7.50 8.58 10.63

Yr-on-Yr Chg. -26.3% -51.9% -38.9% -32.4%

Mar-15 13.76 22.41 16.51 22.35

Apr-15 12.22 16.73 14.22 20.81

May-15 19.58 19.79 14.96 28.22

Jun-15 21.63 19.84 15.87 16.46

Jul-15 12.74 23.51 16.50 33.40

Aug-15 14.54 30.64 15.80 22.98

Sep-15 10.13 20.37 9.07 14.88

Oct-15 7.03 19.61 9.08 14.45

Nov-15 9.83 10.00 9.25 13.00

Dec-15 9.35 9.35 8.62 22.57

Jan-16 9.37 5.65 8.70 13.01

Feb-16 7.20 5.28 7.38 3.38

Mar-16 10.87 11.56 9.66 15.51

Yr-on-Yr Chg. -21.0% -48.4% -41.5% -30.6%

Relevant • Independent • Objective

Page 21

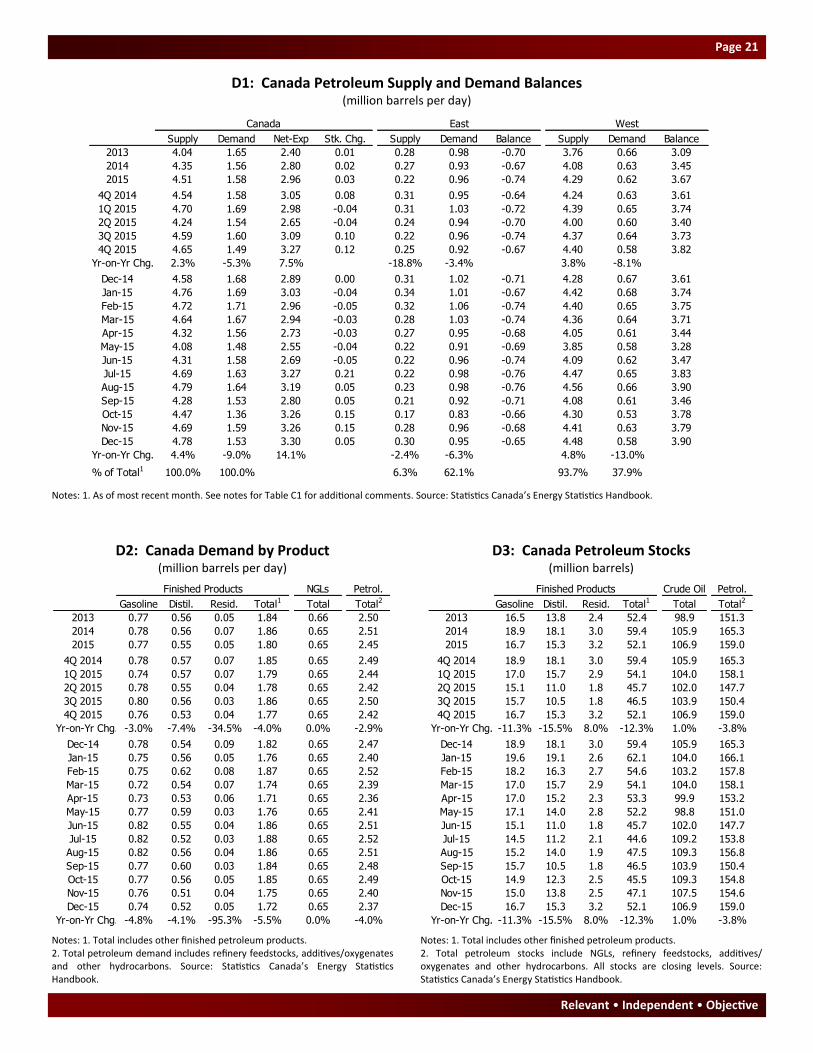

D1: Canada Petroleum Supply and Demand Balances (million barrels per day)

D2: Canada Demand by Product (million barrels per day)

Notes: 1. As of most recent month. See notes for Table C1 for additional comments. Source: Statistics Canada’s Energy Statistics Handbook.

D3: Canada Petroleum Stocks (million barrels)

Notes: 1. Total includes other finished petroleum products. 2. Total petroleum demand includes refinery feedstocks, additives/oxygenates and other hydrocarbons. Source: Statistics Canada’s Energy Statistics Handbook.

Notes: 1. Total includes other finished petroleum products. 2. Total petroleum stocks include NGLs, refinery feedstocks, additives/oxygenates and other hydrocarbons. All stocks are closing levels. Source: Statistics Canada’s Energy Statistics Handbook.

Canada East West

Supply Demand Net-Exp Stk. Chg. Supply Demand Balance Supply Demand Balance

2013 4.04 1.65 2.40 0.01 0.28 0.98 -0.70 3.76 0.66 3.09

2014 4.35 1.56 2.80 0.02 0.27 0.93 -0.67 4.08 0.63 3.45

2015 4.51 1.58 2.96 0.03 0.22 0.96 -0.74 4.29 0.62 3.67

4Q 2014 4.54 1.58 3.05 0.08 0.31 0.95 -0.64 4.24 0.63 3.61

1Q 2015 4.70 1.69 2.98 -0.04 0.31 1.03 -0.72 4.39 0.65 3.74

2Q 2015 4.24 1.54 2.65 -0.04 0.24 0.94 -0.70 4.00 0.60 3.40

3Q 2015 4.59 1.60 3.09 0.10 0.22 0.96 -0.74 4.37 0.64 3.73

4Q 2015 4.65 1.49 3.27 0.12 0.25 0.92 -0.67 4.40 0.58 3.82

Yr-on-Yr Chg. 2.3% -5.3% 7.5% -18.8% -3.4% 3.8% -8.1%

Dec-14 4.58 1.68 2.89 0.00 0.31 1.02 -0.71 4.28 0.67 3.61

Jan-15 4.76 1.69 3.03 -0.04 0.34 1.01 -0.67 4.42 0.68 3.74

Feb-15 4.72 1.71 2.96 -0.05 0.32 1.06 -0.74 4.40 0.65 3.75

Mar-15 4.64 1.67 2.94 -0.03 0.28 1.03 -0.74 4.36 0.64 3.71

Apr-15 4.32 1.56 2.73 -0.03 0.27 0.95 -0.68 4.05 0.61 3.44

May-15 4.08 1.48 2.55 -0.04 0.22 0.91 -0.69 3.85 0.58 3.28

Jun-15 4.31 1.58 2.69 -0.05 0.22 0.96 -0.74 4.09 0.62 3.47

Jul-15 4.69 1.63 3.27 0.21 0.22 0.98 -0.76 4.47 0.65 3.83

Aug-15 4.79 1.64 3.19 0.05 0.23 0.98 -0.76 4.56 0.66 3.90

Sep-15 4.28 1.53 2.80 0.05 0.21 0.92 -0.71 4.08 0.61 3.46

Oct-15 4.47 1.36 3.26 0.15 0.17 0.83 -0.66 4.30 0.53 3.78

Nov-15 4.69 1.59 3.26 0.15 0.28 0.96 -0.68 4.41 0.63 3.79

Dec-15 4.78 1.53 3.30 0.05 0.30 0.95 -0.65 4.48 0.58 3.90

Yr-on-Yr Chg. 4.4% -9.0% 14.1% -2.4% -6.3% 4.8% -13.0%

% of Total1 100.0% 100.0% 6.3% 62.1% 93.7% 37.9%

Finished Products NGLs Petrol.

Gasoline Distil. Resid. Total1 Total Total2

2013 0.77 0.56 0.05 1.84 0.66 2.50

2014 0.78 0.56 0.07 1.86 0.65 2.51

2015 0.77 0.55 0.05 1.80 0.65 2.45

4Q 2014 0.78 0.57 0.07 1.85 0.65 2.49

1Q 2015 0.74 0.57 0.07 1.79 0.65 2.44

2Q 2015 0.78 0.55 0.04 1.78 0.65 2.42

3Q 2015 0.80 0.56 0.03 1.86 0.65 2.50

4Q 2015 0.76 0.53 0.04 1.77 0.65 2.42

Yr-on-Yr Chg. -3.0% -7.4% -34.5% -4.0% 0.0% -2.9%

Dec-14 0.78 0.54 0.09 1.82 0.65 2.47

Jan-15 0.75 0.56 0.05 1.76 0.65 2.40

Feb-15 0.75 0.62 0.08 1.87 0.65 2.52

Mar-15 0.72 0.54 0.07 1.74 0.65 2.39

Apr-15 0.73 0.53 0.06 1.71 0.65 2.36

May-15 0.77 0.59 0.03 1.76 0.65 2.41

Jun-15 0.82 0.55 0.04 1.86 0.65 2.51

Jul-15 0.82 0.52 0.03 1.88 0.65 2.52

Aug-15 0.82 0.56 0.04 1.86 0.65 2.51

Sep-15 0.77 0.60 0.03 1.84 0.65 2.48

Oct-15 0.77 0.56 0.05 1.85 0.65 2.49

Nov-15 0.76 0.51 0.04 1.75 0.65 2.40

Dec-15 0.74 0.52 0.05 1.72 0.65 2.37

Yr-on-Yr Chg. -4.8% -4.1% -95.3% -5.5% 0.0% -4.0%

Finished Products Crude Oil Petrol.

Gasoline Distil. Resid. Total1 Total Total2

2013 16.5 13.8 2.4 52.4 98.9 151.3

2014 18.9 18.1 3.0 59.4 105.9 165.3

2015 16.7 15.3 3.2 52.1 106.9 159.0

4Q 2014 18.9 18.1 3.0 59.4 105.9 165.3

1Q 2015 17.0 15.7 2.9 54.1 104.0 158.1

2Q 2015 15.1 11.0 1.8 45.7 102.0 147.7

3Q 2015 15.7 10.5 1.8 46.5 103.9 150.4

4Q 2015 16.7 15.3 3.2 52.1 106.9 159.0

Yr-on-Yr Chg. -11.3% -15.5% 8.0% -12.3% 1.0% -3.8%

Dec-14 18.9 18.1 3.0 59.4 105.9 165.3

Jan-15 19.6 19.1 2.6 62.1 104.0 166.1

Feb-15 18.2 16.3 2.7 54.6 103.2 157.8

Mar-15 17.0 15.7 2.9 54.1 104.0 158.1

Apr-15 17.0 15.2 2.3 53.3 99.9 153.2

May-15 17.1 14.0 2.8 52.2 98.8 151.0

Jun-15 15.1 11.0 1.8 45.7 102.0 147.7

Jul-15 14.5 11.2 2.1 44.6 109.2 153.8

Aug-15 15.2 14.0 1.9 47.5 109.3 156.8

Sep-15 15.7 10.5 1.8 46.5 103.9 150.4

Oct-15 14.9 12.3 2.5 45.5 109.3 154.8

Nov-15 15.0 13.8 2.5 47.1 107.5 154.6

Dec-15 16.7 15.3 3.2 52.1 106.9 159.0

Yr-on-Yr Chg. -11.3% -15.5% 8.0% -12.3% 1.0% -3.8%

CERI Commodity Report - Crude Oil

Page 22

D4: Canada Crude Oil Production (million barrels per day)

Note: Total includes small amounts of production from Manitoba and Ontario. Source: Statistics Canada’s Energy Statistics Handbook.

D5: Canada Petroleum Imports by Source (thousand barrels per day)

Notes: 1. Includes all non-OPEC production. 2. Includes production by the other seven OPEC members. 3. As of most recent month. Sources: Statistics Canada’s

Energy Statistics Handbook.

Major Producers Canada Petroleum Type

Alta. Sask. B.C. N.W.T. Atlantic Total1 Light SCO Heavy Bitumen NGLs

2013 2.63 0.47 0.04 0.01 0.23 3.46 0.91 0.94 0.45 0.98 0.15

2014 2.91 0.51 0.05 0.01 0.22 3.76 0.94 0.95 0.46 1.21 0.22

2015 3.09 0.53 0.05 0.01 0.17 3.91 0.85 0.98 0.45 1.39 0.22

4Q 2014 3.04 0.53 0.05 0.01 0.22 3.90 0.95 1.00 0.46 1.28 0.27

1Q 2015 3.17 0.55 0.05 0.01 0.22 4.05 0.95 1.09 0.47 1.32 0.21

2Q 2015 2.81 0.51 0.05 0.01 0.15 3.61 0.83 0.81 0.45 1.28 0.21

3Q 2015 3.17 0.52 0.05 0.01 0.14 3.95 0.79 1.02 0.45 1.46 0.22

4Q 2015 3.19 0.52 0.06 0.01 0.17 4.00 0.82 0.98 0.44 1.51 0.25

Yr-on-Yr Chg. 5.2% -1.4% 5.0% 1.1% -22.2% 2.6% -13.4% -2.1% -4.2% 18.0% -7.8%

Dec-14 3.07 0.53 0.06 0.01 0.22 3.94 0.96 0.99 0.46 1.30 0.28

Jan-15 3.16 0.58 0.05 0.01 0.24 4.05 0.99 1.10 0.49 1.31 0.20

Feb-15 3.21 0.51 0.05 0.01 0.22 4.08 0.95 1.11 0.45 1.34 0.22

Mar-15 3.13 0.56 0.06 0.01 0.19 4.04 0.92 1.07 0.47 1.32 0.22

Apr-15 2.86 0.52 0.06 0.01 0.18 3.71 0.88 0.81 0.45 1.31 0.22

May-15 2.65 0.53 0.05 0.01 0.14 3.46 0.82 0.70 0.45 1.24 0.21

Jun-15 2.92 0.50 0.05 0.01 0.14 3.67 0.79 0.93 0.44 1.30 0.21

Jul-15 3.28 0.52 0.05 0.00 0.14 4.04 0.80 1.09 0.45 1.49 0.21

Aug-15 3.35 0.54 0.05 0.01 0.15 4.16 0.81 1.16 0.46 1.50 0.21

Sep-15 2.89 0.51 0.05 0.01 0.13 3.65 0.78 0.81 0.44 1.38 0.23

Oct-15 3.08 0.53 0.06 0.01 0.09 3.83 0.75 0.87 0.45 1.51 0.24

Nov-15 3.22 0.51 0.06 0.01 0.20 4.05 0.85 1.04 0.44 1.47 0.25

Dec-15 3.28 0.53 0.05 0.01 0.21 4.13 0.87 1.02 0.44 1.54 0.26

Yr-on-Yr Chg. 6.9% -1.6% -3.4% 4.7% -3.7% 4.7% -9.7% 2.5% -3.8% 18.2% -8.5%

Non-OPEC OPEC Imports

Mexico U.S. U.K. Norway Total1 Algeria Nigeria S. Arabia Venez. Total2 P. Gulf Total

2013 24 15 36 55 466 71 47 16 2 177 57 643

2014 17 164 3 12 453 38 27 0 1 90 23 543

2015 0 256 4 8 496 45 26 0 0 71 0 567

4Q 2014 21 118 2 19 451 43 21 0 0 64 0 515

1Q 2015 0 303 0 7 485 61 30 0 0 91 0 576

2Q 2015 0 344 15 11 592 12 21 0 0 33 0 625

3Q 2015 0 191 0 3 461 74 42 0 0 116 0 577