march 12, 2019 an ideal blend - icici direct

TRANSCRIPT

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Init

iatin

g C

overage

March 12, 2019

CMP: | 440 Target: | 500 ( 14%) Target Period: 12 months

M&M Financial Services ( MAHFIN)

BUY

Rural dominance & normal monsoons – An ideal blend

Mahindra and Mahindra Financial Services (MMFS) is a subsidiary of

Mahindra & Mahindra group, one of the largest business conglomerates in

the country. MMFS is predominantly into rural, semi urban vehicle financing

with advances at ~| 58,240 crore as on December 31, 2018 and wide

customer base of 5.3 million. It is headed by Ramesh Iyer (MD, Vice

Chairman), who has decades of experience in Indian financial sector. MMFS

operates 1313 branches in 27 states servicing ~5.3 million customers.

Strong business momentum led by rural cash flow, high NIM

For MMFS, AUM has grown at 23% CAGR with volatile spells in FY09-18.

AUM grew at 32% CAGR in 09-14, slowed down in FY15-17 to 10% and then

revived to 16% in FY16-18 to | 55,100 crore. We expect AUM to grow at

20% CAGR in FY19-21E to | 94,996 crore. Robust infrastructure spends and

recent farmer friendly schemes are expected to support rural cash flows.

Current NIM at ~8% is expected to remain stable over the next two years as

it has already moderated from highs of 9.2% in the past.

Operating leverage to kick in; productivity to improve ahead

As loan book growth picks up, we expect MMFS to benefit from expenses

incurred on employee and branch expansion. Opex/AUM ratio is seen

moderating by ~10 bps to 2.9% in FY21E. Likewise, CI ratio is expected to

reduce from 39.7% in FY18 to 36.5% in FY21E.

RoA improvement led by steady asset quality, productivity

Post impact of bad monsoon, RoA revived from 1% in FY17 to 1.9% in FY18

and further to 2.3% in 9MFY19. Likewise, RoE improved from 6.4% in FY17

to 11.3% in FY18, on the back of strong NII growth at 16% YoY and reduction

in CI ratio from ~42% to ~39% in FY18. With steady credit cost and stable

yields, we expect RoA to improve further to 2.4% in FY21E.

Buoyancy in rural India to benefit; valuation to sustain, BUY

Buoyancy in rural India and MMFS’ focus on rural financing are expected to

support valuations. MMFS has ingredients to sustainably command

premium valuation - 1) rural reach providing huge opportunity with pricing

power, 2) robust AUM growth (AUM, earnings CAGR of 20%, 25%,

respectively, in FY18-21E), 3) higher rural income led by farm loan waivers

and cash flow receipt during election, 4) strong management and 5)

adequate risk management with limited losses. We value core auto business

at 2.6x FY21E ABV (1.8x FY21E BV) and add | 50 as value for subsidiaries

like housing that is picking up pace. Assuming 20% holding company

discount in lieu of subsidiaries, we initiate coverage with BUY

recommendation and a target price of | 500 per share.

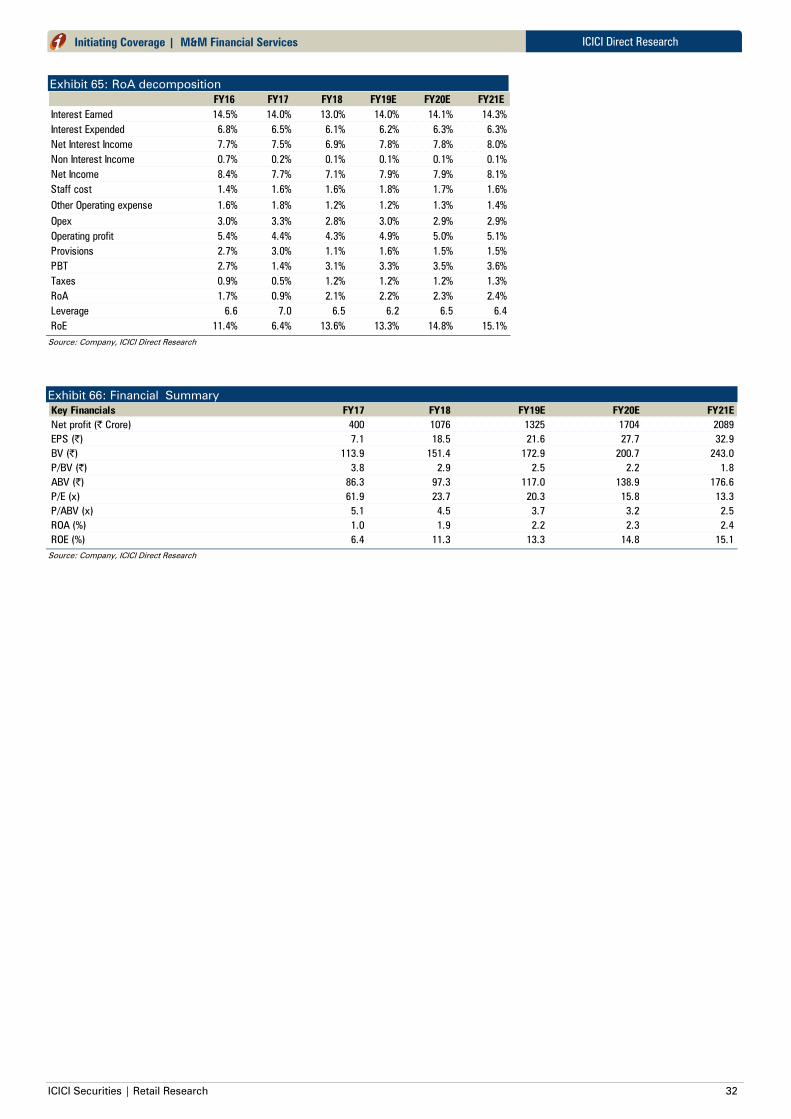

Key Financial Summary

Key Financials FY17 FY18 FY19E FY20E FY21E

Net profit (| Crore) 400 1076 1325 1704 2089

EPS (|) 7.1 18.5 21.6 27.7 32.9

BV (|) 113.9 151.4 172.9 200.7 243.0

P/BV (|) 3.8 2.8 2.5 2.1 1.8

ABV (|) 86.3 97.3 117.0 138.9 176.6

P/E (x) 60.7 23.2 19.9 15.5 13.1

P/ABV (x) 5.0 4.4 3.7 3.1 2.4

ROA (%) 1.0 1.9 2.2 2.3 2.4

ROE (%) 6.4 11.3 13.3 14.8 15.1

Source: ICICI Direct Research, Company

Stock data & valuation summary

Amount

Market Capitalisation | 27000 crore

Net worth | 10306 crore

52 week H/L 537 / 351

Equity Capital | 123 crore

Face Value | 2

DII Holding (%) 12.98

FII Holding (%) 27.14

Key Highlights

MMFS, being rural auto financier,

poised to benefit from underlying

buoyancy in rural India

Adequate capital – no near term

dilution

Experienced management and strong

parentage to support valuation

Price performance

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0

100

200

300

400

500

600

Mar-

19

Sep-

18

Apr-

18

Nov-

17

May-

17

Dec-

16

Jul-

16

MMFS (R.H.S) Nifty (L.H.S)

Source: BSE

Research Analyst

Kajal Gandhi

Vishal Narnolia

Harsh Shah

ICICI Securities | Retail Research 2

ICICI Direct Research

Initiating Coverage | M&M Financial Services

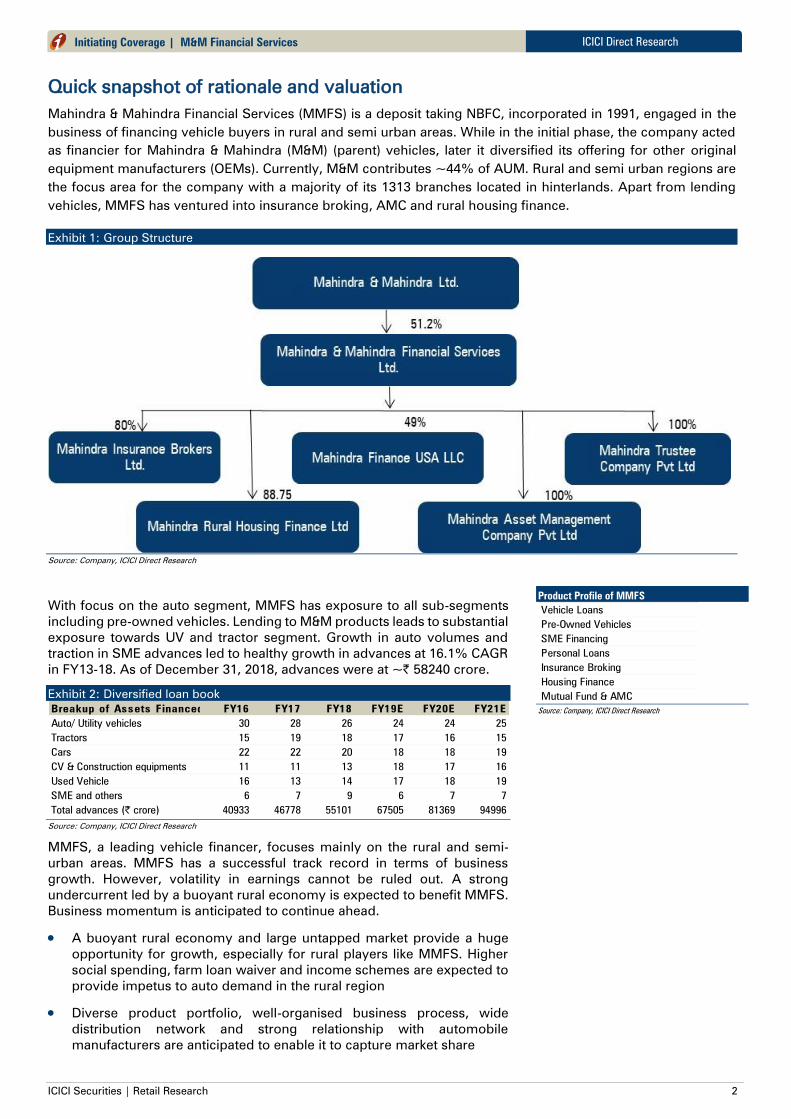

Quick snapshot of rationale and valuation

Mahindra & Mahindra Financial Services (MMFS) is a deposit taking NBFC, incorporated in 1991, engaged in the

business of financing vehicle buyers in rural and semi urban areas. While in the initial phase, the company acted

as financier for Mahindra & Mahindra (M&M) (parent) vehicles, later it diversified its offering for other original

equipment manufacturers (OEMs). Currently, M&M contributes ~44% of AUM. Rural and semi urban regions are

the focus area for the company with a majority of its 1313 branches located in hinterlands. Apart from lending

vehicles, MMFS has ventured into insurance broking, AMC and rural housing finance.

Exhibit 1: Group Structure

Source: Company, ICICI Direct Research

With focus on the auto segment, MMFS has exposure to all sub-segments

including pre-owned vehicles. Lending to M&M products leads to substantial

exposure towards UV and tractor segment. Growth in auto volumes and

traction in SME advances led to healthy growth in advances at 16.1% CAGR

in FY13-18. As of December 31, 2018, advances were at ~| 58240 crore.

Exhibit 2: Diversified loan book

Breakup of Assets Financed (%)FY16 FY17 FY18 FY19E FY20E FY21E

Auto/ Utility vehicles 30 28 26 24 24 25

Tractors 15 19 18 17 16 15

Cars 22 22 20 18 18 19

CV & Construction equipments 11 11 13 18 17 16

Used Vehicle 16 13 14 17 18 19

SME and others 6 7 9 6 7 7

Total advances (| crore) 40933 46778 55101 67505 81369 94996

Source: Company, ICICI Direct Research

MMFS, a leading vehicle financer, focuses mainly on the rural and semi-

urban areas. MMFS has a successful track record in terms of business

growth. However, volatility in earnings cannot be ruled out. A strong

undercurrent led by a buoyant rural economy is expected to benefit MMFS.

Business momentum is anticipated to continue ahead.

A buoyant rural economy and large untapped market provide a huge

opportunity for growth, especially for rural players like MMFS. Higher

social spending, farm loan waiver and income schemes are expected to

provide impetus to auto demand in the rural region

Diverse product portfolio, well-organised business process, wide

distribution network and strong relationship with automobile

manufacturers are anticipated to enable it to capture market share

Product Profile of MMFS

Vehicle Loans

Pre-Owned Vehicles

SME Financing

Personal Loans

Insurance Broking

Housing Finance

Mutual Fund & AMC

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 3

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Margins are expected to jump in FY19E. Healthy balance of credit and

borrowing mix is expected to keep margins steady ahead

Ind-As, reflecting real stress, led to a decline in NPA. An improvement

in asset quality is anticipated to continue ahead

Healthy credit growth and robust operational performance are expected

to improve RoA by ~20-30 bps in FY19-21E

We expect NII to grow at 25.7% CAGR in FY18-21E to | 7020 crore while

PAT is expected to grow at a CAGR of 24.7% over the same period to | 2087

crore. Margins are expected to be in the region of ~8% by FY21E.

Considering slow auto sales by OEMs and a tight liquidity environment, we

expect strong players like MMFS to capture market share and thereby

continue to grow AUM. The positive ALM position indicates that MMFS is

relatively immune to liquidity shocks positive ALM in shorter tenure buckets)

though a rise in CoF is expected to keep margins steady. Capital adequacy

remains strong at 19.4%. We factor in capital raising in FY21E to fund

balance sheet growth.

Exhibit 3: AUM growth at ~20% in FY19-21E

34,13336,878

40,933

46,778

55,101

67,505

81,369

94,996

8.0

11.0

14.3

17.8

22.5

20.5

16.7

0

5

10

15

20

25

0

15,000

30,000

45,000

60,000

75,000

90,000

105,000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)(| crore)

Gross AUM AUM growth (%)

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 4

ICICI Direct Research

Initiating Coverage | M&M Financial Services

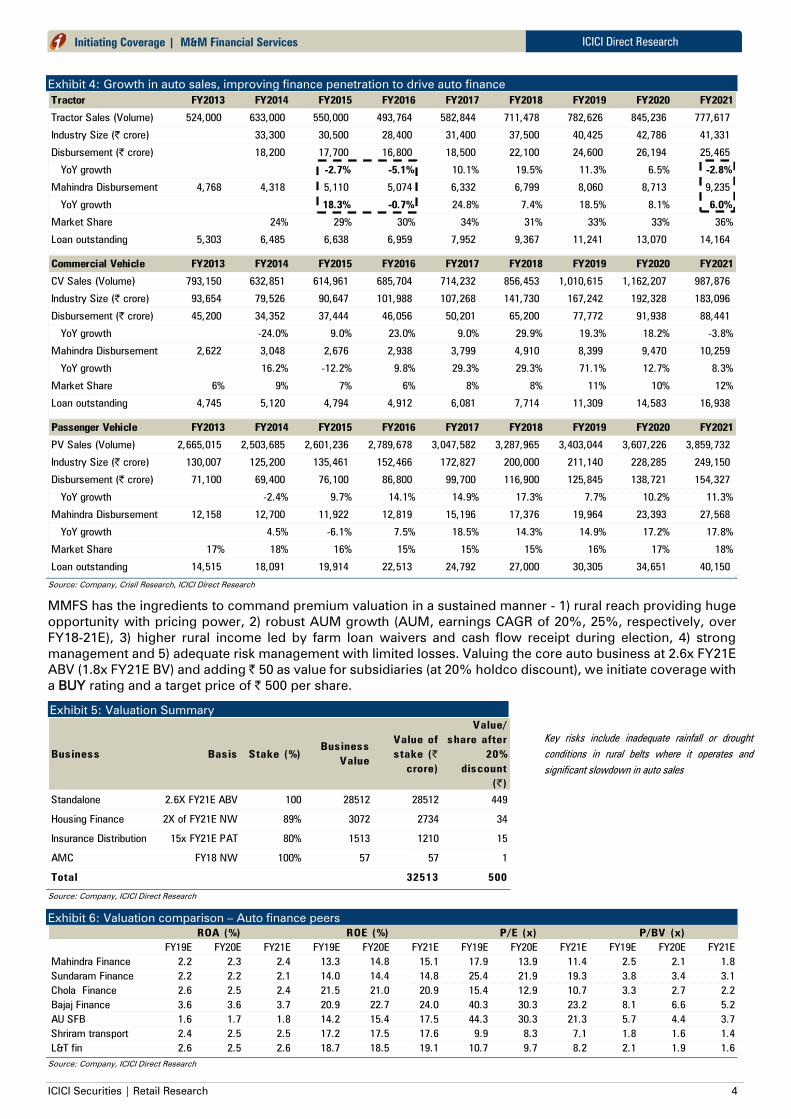

Exhibit 4: Growth in auto sales, improving finance penetration to drive auto finance

Tractor FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020 FY2021

Tractor Sales (Volume) 524,000 633,000 550,000 493,764 582,844 711,478 782,626 845,236 777,617

Industry Size (| crore) 33,300 30,500 28,400 31,400 37,500 40,425 42,786 41,331

Disbursement (| crore) 18,200 17,700 16,800 18,500 22,100 24,600 26,194 25,465

YoY growth -2.7% -5.1% 10.1% 19.5% 11.3% 6.5% -2.8%

Mahindra Disbursement 4,768 4,318 5,110 5,074 6,332 6,799 8,060 8,713 9,235

YoY growth 18.3% -0.7% 24.8% 7.4% 18.5% 8.1% 6.0%

Market Share 24% 29% 30% 34% 31% 33% 33% 36%

Loan outstanding 5,303 6,485 6,638 6,959 7,952 9,367 11,241 13,070 14,164

Commercial Vehicle FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020 FY2021

CV Sales (Volume) 793,150 632,851 614,961 685,704 714,232 856,453 1,010,615 1,162,207 987,876

Industry Size (| crore) 93,654 79,526 90,647 101,988 107,268 141,730 167,242 192,328 183,096

Disbursement (| crore) 45,200 34,352 37,444 46,056 50,201 65,200 77,772 91,938 88,441

YoY growth -24.0% 9.0% 23.0% 9.0% 29.9% 19.3% 18.2% -3.8%

Mahindra Disbursement 2,622 3,048 2,676 2,938 3,799 4,910 8,399 9,470 10,259

YoY growth 16.2% -12.2% 9.8% 29.3% 29.3% 71.1% 12.7% 8.3%

Market Share 6% 9% 7% 6% 8% 8% 11% 10% 12%

Loan outstanding 4,745 5,120 4,794 4,912 6,081 7,714 11,309 14,583 16,938

Passenger Vehicle FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020 FY2021

PV Sales (Volume) 2,665,015 2,503,685 2,601,236 2,789,678 3,047,582 3,287,965 3,403,044 3,607,226 3,859,732

Industry Size (| crore) 130,007 125,200 135,461 152,466 172,827 200,000 211,140 228,285 249,150

Disbursement (| crore) 71,100 69,400 76,100 86,800 99,700 116,900 125,845 138,721 154,327

YoY growth -2.4% 9.7% 14.1% 14.9% 17.3% 7.7% 10.2% 11.3%

Mahindra Disbursement 12,158 12,700 11,922 12,819 15,196 17,376 19,964 23,393 27,568

YoY growth 4.5% -6.1% 7.5% 18.5% 14.3% 14.9% 17.2% 17.8%

Market Share 17% 18% 16% 15% 15% 15% 16% 17% 18%

Loan outstanding 14,515 18,091 19,914 22,513 24,792 27,000 30,305 34,651 40,150

Source: Company, Crisil Research, ICICI Direct Research

MMFS has the ingredients to command premium valuation in a sustained manner - 1) rural reach providing huge

opportunity with pricing power, 2) robust AUM growth (AUM, earnings CAGR of 20%, 25%, respectively, over

FY18-21E), 3) higher rural income led by farm loan waivers and cash flow receipt during election, 4) strong

management and 5) adequate risk management with limited losses. Valuing the core auto business at 2.6x FY21E

ABV (1.8x FY21E BV) and adding | 50 as value for subsidiaries (at 20% holdco discount), we initiate coverage with

a BUY rating and a target price of | 500 per share.

Exhibit 5: Valuation Summary

Business Basis Stake (%)

Business

Value

Value of

stake (|

crore)

Value/

share after

20%

discount

(|)

Standalone 2.6X FY21E ABV 100 28512 28512 449

Housing Finance 2X of FY21E NW 89% 3072 2734 34

Insurance Distribution 15x FY21E PAT 80% 1513 1210 15

AMC FY18 NW 100% 57 57 1

Total 32513 500

Source: Company, ICICI Direct Research

Exhibit 6: Valuation comparison – Auto finance peers

ROA (%) ROE (%) P/E (x) P/BV (x)

FY19E FY20E FY21E FY19E FY20E FY21E FY19E FY20E FY21E FY19E FY20E FY21E

Mahindra Finance 2.2 2.3 2.4 13.3 14.8 15.1 17.9 13.9 11.4 2.5 2.1 1.8

Sundaram Finance 2.2 2.2 2.1 14.0 14.4 14.8 25.4 21.9 19.3 3.8 3.4 3.1

Chola Finance 2.6 2.5 2.4 21.5 21.0 20.9 15.4 12.9 10.7 3.3 2.7 2.2

Bajaj Finance 3.6 3.6 3.7 20.9 22.7 24.0 40.3 30.3 23.2 8.1 6.6 5.2

AU SFB 1.6 1.7 1.8 14.2 15.4 17.5 44.3 30.3 21.3 5.7 4.4 3.7

Shriram transport 2.4 2.5 2.5 17.2 17.5 17.6 9.9 8.3 7.1 1.8 1.6 1.4

L&T fin 2.6 2.5 2.6 18.7 18.5 19.1 10.7 9.7 8.2 2.1 1.9 1.6

Source: Company, ICICI Direct Research

Key risks include inadequate rainfall or drought

conditions in rural belts where it operates and

significant slowdown in auto sales

ICICI Securities | Retail Research 5

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Company Background

Mahindra & Mahindra Financial Services (MMFS) is a deposit taking NBFC, incorporated in 1991, engaged in the

business of financing vehicle buyers in rural and semi urban areas. While in the initial phase, the company acted

as financier for M&M (parent) vehicles, later it diversified its offering for other original equipment manufacturers

(OEMs). Currently, M&M contributes ~44% of AUM. Rural and semi urban regions are the focus areas of the

company with a majority of its 1313 branches located in hinterlands. Apart from lending vehicles, MMFS has

ventured into insurance broking, AMC and rural housing finance.

Exhibit 7: Group structure

Source: Company, ICICI Direct Research

MMFS started business as Maxi Motors Financial Services Ltd in 1991. Later,

in 1992, the name of the entity was changed to Mahindra & Mahindra

Financial Services Ltd. In the initial phase, the company began financing

M&M utility vehicles. However, later in 2002, MMFS ventured into non M&M

vehicles in rural and semi urban areas. Further, commercial vehicle and

construction equipment finance were added in its product boutique. In 2011,

MMFS entered into a JV with Rabobank subsidiary for tractor financing in

USA. Small and medium enterprises (SME) financing as a product was

added to the portfolio in FY14. With emphasis on and better understanding

of rural regions and with the objective of diversification in product mix,

MMFS started its home finance business with a new subsidiary – Mahindra

Rural Housing Finance Ltd.

As of December 31, 2018, advances were at ~| 58240 crore. Product

offerings include vehicle financing for auto and utility vehicles, tractors, cars,

commercial vehicles, three wheelers, and construction equipment. Apart

from new vehicles, pre-owned vehicle financed across products including

cars, multi-utility vehicles, tractors, and commercial vehicles. MMFS is

engaged in providing housing finance for new houses, renovation and

improvements. SME financing services includes lending to auto dealers and

suppliers in the supply chain of parent (M&M) primarily for equipment

finance and working capital finance.

Shareholding Pattern (Q3FY19)

Shareholders Holding (%)

Promoters 51.19

Institutional investors 40.11

Others 8.7

Source: BSE

Top Shareholders

Top shareholders Holding (%)

Mahindra Group 51.2

Blackrock Global Funds 1.5

Blackrock Global Funds 1.5

SBI AMC 2.9

UTI AMC 2.4

HDFC Standard Life Ins 2.3

Kotak Mahindra AMC 1.3

Axis AMC 1.1[

Source: BSE

ICICI Securities | Retail Research 6

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Exhibit 8: Product Profile

Vehicle Loans Auto and utility vehicles, tractors, cars, commercial vehicles and construction equipment

Pre-Owned Vehicles Pre-owned cars, multi-utility vehicles, tractors and commercial vehicles

SME Financing Project finance, equipment finance and working capital finance

Personal Loans Personal loans typically for weddings, children‟s education, medical treatment and working capital

Insurance Broking Insurance solutions to rural customers - retail and corporations through subsidiary MIBL

Housing Finance Loans for buying, renovating, extending and improving homes in rural and semi-urban India through subsidiary MRHFL

Mutual Fund & AMC Asset management company/investment manager - Mahindra Mutual Fund

Source: Company, ICICI Direct Research

Exhibit 9: Diversified Loan Book

Breakup of Assets Financed (%)FY16 FY17 FY18 FY19E FY20E FY21E

Auto/ Utility vehicles 30 28 26 24 24 25

Tractors 15 19 18 17 16 15

Cars 22 22 20 18 18 19

CV & Construction equipments 11 11 13 18 17 16

Used Vehicle 16 13 14 17 18 19

SME and others 6 7 9 6 7 7

Source: Company, ICICI Direct Research

Advances growth remained healthy at 16.1% CAGR in FY13-18 to ~| 51000

crore. Growth in auto volumes and traction in SME advances contribute to

advancement of book. On the earnings front, the company reported healthy

growth at 19.3% CAGR in FY10-15. However, two consecutive years of poor

monsoons adversely affected the repayment capacity of borrowers, thereby

impacting asset quality and profitability. Subsequently, RoA witnessed a dip

from ~2.7% in FY15 to ~1% in FY18. This has revived post FY18 with a

revival in monsoons, leading to a reversal in profitability and return ratios.

PAT was at | 1076 crore in FY18 while RoA inched up to 1.9%.

Exhibit 10: Financial Metrics

| crore FY16 FY17 FY18 FY19E FY20E FY21E

AUM 40933 46778 55101 67505 81369 94996

GNPA (%) 8.0 9.0 8.5 7.8 7.1 6.7

RoA (%) 1.9 1.0 1.9 2.1 2.2 2.3

RoE (%) 11.4 6.4 11.3 13.6 13.3 14.8

Cost to Income (%) 36.1 42.9 38.6 39.6 38.0 37.0

Source: Company, ICICI Direct Research

Subsidiaries

Mahindra Insurance Brokers Ltd

MMFS offers insurance broking through its subsidiary - Mahindra Insurance

Brokers (MIBL). Started in 2004 as a wholly-owned subsidiary, currently

MMFS holds ~80% stake in the company. This company is engaged in

insurance broking for both life and non-life products, especially targeting

rural customers. Currently, it has 1063 employees covering ~ 2 lakh villages.

It has served ~1 crore insurance cases for both life and non-life insurance.

In 9MFY19, MIBL’s profits grew ~46% YoY to | 44.8 crore.

Mahindra Rural Housing Finance Ltd

MMFS undertakes rural housing finance business through its subsidiary -

Mahindra Rural Housing Finance (MRHFL). Currently, MMFS holds ~88.75%

stake in the venture, with the balance held by NHB and MRHFL Employee

Welfare Trust. Incorporated in 2008, MRHFL addresses rising demand for

home finance in rural areas thereby filling the void in organised housing

finance in rural region. Majority of loans disbursed are to customers in

villages with an average annual household income of ~| 1.5-1.9 lakh. As of

December 31, 2018, MRHFL has an outstanding loan book of | 7301 crore

with PAT reported at | 168.5 crore for 9MFY19.

Geographical diversification

% loans FY17 FY18 9MFY19

North 27 27 28

South 21 20 20

East 21 23 25

West 21 21 18

Central 10 9 9

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 7

ICICI Direct Research

Initiating Coverage | M&M Financial Services

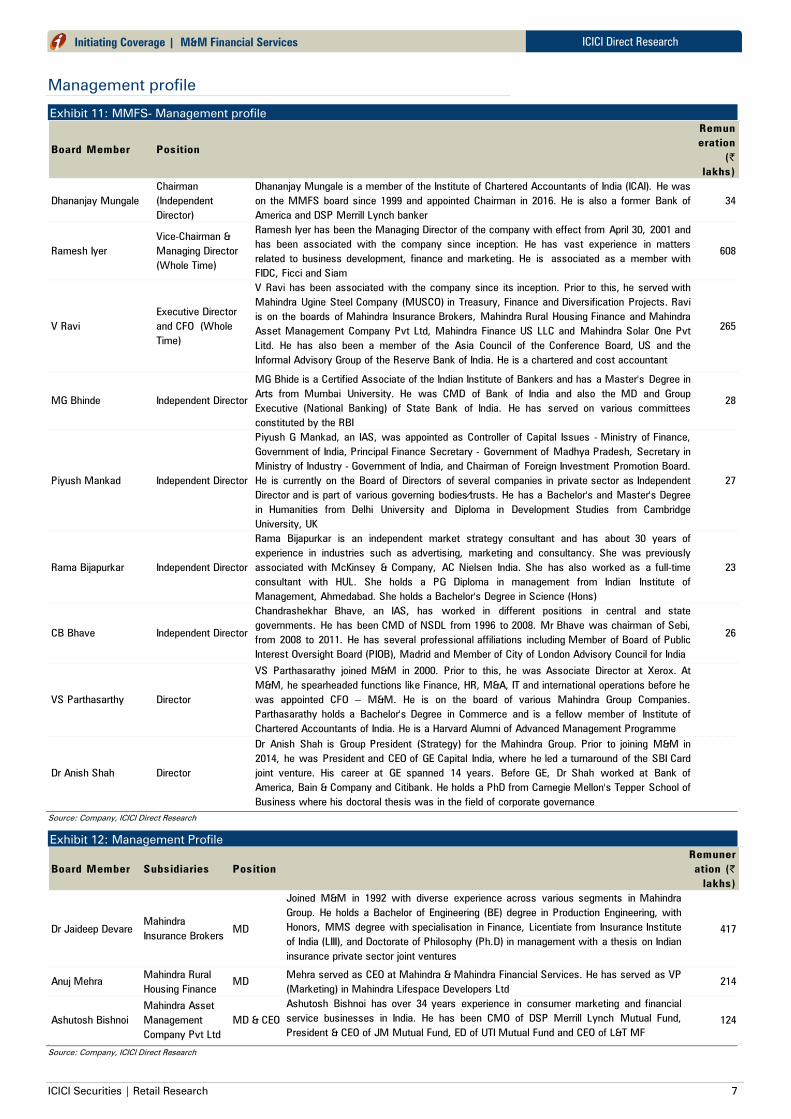

Management profile

Exhibit 11: MMFS- Management profile

Board Member Position

Remun

eration

(|

lakhs)

Dhananjay Mungale

Chairman

(Independent

Director)

Dhananjay Mungale is a member of the Institute of Chartered Accountants of India (ICAI). He was

on the MMFS board since 1999 and appointed Chairman in 2016. He is also a former Bank of

America and DSP Merrill Lynch banker

34

Ramesh Iyer

Vice-Chairman &

Managing Director

(Whole Time)

Ramesh Iyer has been the Managing Director of the company with effect from April 30, 2001 and

has been associated with the company since inception. He has vast experience in matters

related to business development, finance and marketing. He is associated as a member with

FIDC, Ficci and Siam

608

V Ravi

Executive Director

and CFO (Whole

Time)

V Ravi has been associated with the company since its inception. Prior to this, he served with

Mahindra Ugine Steel Company (MUSCO) in Treasury, Finance and Diversification Projects. Ravi

is on the boards of Mahindra Insurance Brokers, Mahindra Rural Housing Finance and Mahindra

Asset Management Company Pvt Ltd, Mahindra Finance US LLC and Mahindra Solar One Pvt

Litd. He has also been a member of the Asia Council of the Conference Board, US and the

Informal Advisory Group of the Reserve Bank of India. He is a chartered and cost accountant

265

MG Bhinde Independent Director

MG Bhide is a Certified Associate of the Indian Institute of Bankers and has a Master's Degree in

Arts from Mumbai University. He was CMD of Bank of India and also the MD and Group

Executive (National Banking) of State Bank of India. He has served on various committees

constituted by the RBI

28

Piyush Mankad Independent Director

Piyush G Mankad, an IAS, was appointed as Controller of Capital Issues - Ministry of Finance,

Government of India, Principal Finance Secretary - Government of Madhya Pradesh, Secretary in

Ministry of Industry - Government of India, and Chairman of Foreign Investment Promotion Board.

He is currently on the Board of Directors of several companies in private sector as Independent

Director and is part of various governing bodies⁄trusts. He has a Bachelor's and Master's Degree

in Humanities from Delhi University and Diploma in Development Studies from Cambridge

University, UK

27

Rama Bijapurkar Independent Director

Rama Bijapurkar is an independent market strategy consultant and has about 30 years of

experience in industries such as advertising, marketing and consultancy. She was previously

associated with McKinsey & Company, AC Nielsen India. She has also worked as a full-time

consultant with HUL. She holds a PG Diploma in management from Indian Institute of

Management, Ahmedabad. She holds a Bachelor's Degree in Science (Hons)

23

CB Bhave Independent Director

Chandrashekhar Bhave, an IAS, has worked in different positions in central and state

governments. He has been CMD of NSDL from 1996 to 2008. Mr Bhave was chairman of Sebi,

from 2008 to 2011. He has several professional affiliations including Member of Board of Public

Interest Oversight Board (PIOB), Madrid and Member of City of London Advisory Council for India

26

VS Parthasarthy Director

VS Parthasarathy joined M&M in 2000. Prior to this, he was Associate Director at Xerox. At

M&M, he spearheaded functions like Finance, HR, M&A, IT and international operations before he

was appointed CFO – M&M. He is on the board of various Mahindra Group Companies.

Parthasarathy holds a Bachelor's Degree in Commerce and is a fellow member of Institute of

Chartered Accountants of India. He is a Harvard Alumni of Advanced Management Programme

Dr Anish Shah Director

Dr Anish Shah is Group President (Strategy) for the Mahindra Group. Prior to joining M&M in

2014, he was President and CEO of GE Capital India, where he led a turnaround of the SBI Card

joint venture. His career at GE spanned 14 years. Before GE, Dr Shah worked at Bank of

America, Bain & Company and Citibank. He holds a PhD from Carnegie Mellon's Tepper School of

Business where his doctoral thesis was in the field of corporate governance

Source: Company, ICICI Direct Research

Exhibit 12: Management Profile

Board Member Subsidiaries Position

Remuner

ation (|

lakhs)

Dr Jaideep Devare

Mahindra

Insurance BrokersMD

Joined M&M in 1992 with diverse experience across various segments in Mahindra

Group. He holds a Bachelor of Engineering (BE) degree in Production Engineering, with

Honors, MMS degree with specialisation in Finance, Licentiate from Insurance Institute

of India (LIII), and Doctorate of Philosophy (Ph.D) in management with a thesis on Indian

insurance private sector joint ventures

417

Anuj MehraMahindra Rural

Housing Finance

MDMehra served as CEO at Mahindra & Mahindra Financial Services. He has served as VP

(Marketing) in Mahindra Lifespace Developers Ltd

214

Ashutosh Bishnoi

Mahindra Asset

Management

Company Pvt Ltd

MD & CEO

Ashutosh Bishnoi has over 34 years experience in consumer marketing and financial

service businesses in India. He has been CMO of DSP Merrill Lynch Mutual Fund,

President & CEO of JM Mutual Fund, ED of UTI Mutual Fund and CEO of L&T MF

124

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 8

ICICI Direct Research

Initiating Coverage | M&M Financial Services

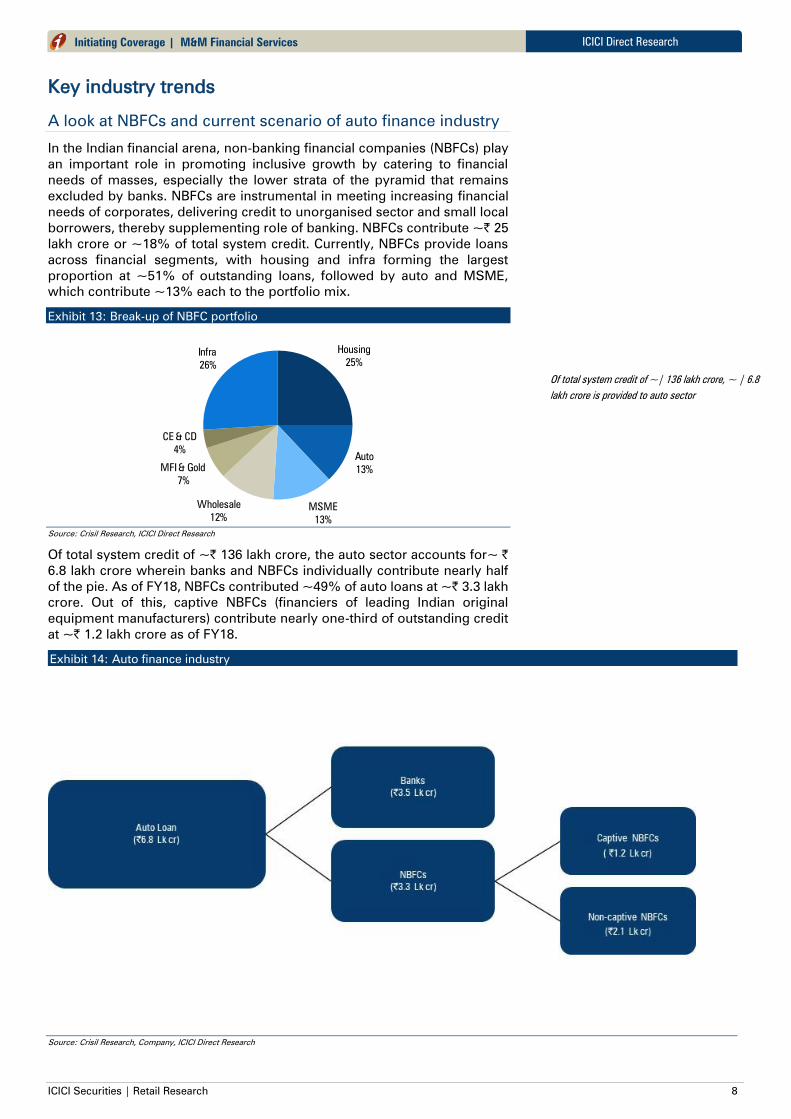

Key industry trends

A look at NBFCs and current scenario of auto finance industry

In the Indian financial arena, non-banking financial companies (NBFCs) play

an important role in promoting inclusive growth by catering to financial

needs of masses, especially the lower strata of the pyramid that remains

excluded by banks. NBFCs are instrumental in meeting increasing financial

needs of corporates, delivering credit to unorganised sector and small local

borrowers, thereby supplementing role of banking. NBFCs contribute ~| 25

lakh crore or ~18% of total system credit. Currently, NBFCs provide loans

across financial segments, with housing and infra forming the largest

proportion at ~51% of outstanding loans, followed by auto and MSME,

which contribute ~13% each to the portfolio mix.

Exhibit 13: Break-up of NBFC portfolio

Housing

25%

Auto

13%

MSME

13%

Wholesale

12%

MFI & Gold

7%

CE & CD

4%

Infra

26%

Source: Crisil Research, ICICI Direct Research

Of total system credit of ~| 136 lakh crore, the auto sector accounts for~ |

6.8 lakh crore wherein banks and NBFCs individually contribute nearly half

of the pie. As of FY18, NBFCs contributed ~49% of auto loans at ~| 3.3 lakh

crore. Out of this, captive NBFCs (financiers of leading Indian original

equipment manufacturers) contribute nearly one-third of outstanding credit

at ~| 1.2 lakh crore as of FY18.

Exhibit 14: Auto finance industry

Source: Crisil Research, Company, ICICI Direct Research

Of total system credit of ~| 136 lakh crore, ~ | 6.8

lakh crore is provided to auto sector

ICICI Securities | Retail Research 9

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Among banks, HDFC Bank has the highest market share at ~11.3% of total

auto loans. Other banks with substantial market share are SBI (9.8%),

IndusInd Bank (5.4%) and Axis Bank (4.6%). Among NBFCs, Shriram

Transport Finance (STFC) has the highest auto loan portfolio forming

~13.4% market share, followed by MMFS (6.6%), Chola (4.6%) and

Sundaram Finance (3.4%).

Exhibit 15: Prominent players in auto finance

SBI, 9.8%

HDFC Bank, 11.3%

IndusInd Bank, 5.4%

Axis Bank, 4.6%

Other

banks,

13.1%

Mahindra Finance,

6.6%

Shriram Transport

Finance, 13.4%

Cholamandalam

Finance, 4.6%

Sundaram Finance

Ltd, 3.4%

Others,

14.0%

Source: Company, Crisil Research,, ICICI Direct Research

A look at the auto loan portfolio of NBFCs highlights that while non-bank

financiers are present in all segments, used vehicles (CV, PV) contribute

nearly a third of their loan portfolio. A relatively extensive presence in rural

areas, ability to evaluate borrower’s income (self-employed borrowers) and

valuation of used vehicle have enabled NBFCs to garner majority market

share. Apart from used assets, CV and PV form ~20% and ~25%,

respectively, of the outstanding portfolio.

Exhibit 16: Break-up of auto loan of NBFC

CV

20%

PV

25%

2 & 3 W

2%

Tractors

7%

Used Vehicle

36%

Others

10%

Source: Company, Crisil Research, ICICI Direct Research

Trends in auto financing industry

The Indian auto finance industry witnessed healthy growth at 13.5% CAGR

in FY13-18, led by traction in auto volumes as well as a gradual improvement

in financial penetration. In terms of auto volumes, various segments,

including tractors and CV, contributed to the growth trajectory in a different

scenario. For example, growth in tractor volumes remained robust in FY14,

post which poor monsoons had a substantial impact on the momentum in

FY15-16. Traction in CV (M&HCV) remained strong in FY15-16 but lost steam

in FY17. A gradual improvement in finance penetration and loan to value

(LTV) is seen leading to higher disbursement from ~51% in FY13 to ~54%

in FY18. This is expected to continue ahead contributing to growth in the

auto finance industry.

ICICI Securities | Retail Research 10

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Exhibit 17: Growth in auto loans in last five years

3.6 3.64.1

4.7

5.6

6.8

7.9

9.3

0%

5%

10%

15%

20%

0

2

4

6

8

10

FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

(| crore)

Total auto loans YoY growth (RHS)

Demonetisatio

Bad

Monsoon

(FY15-16)

GST(July,2017)Change in NPA

recognition norms

for NBFC

(April,2018)

Source: Crisil Research, ICICI Direct Research

Exhibit 18: Gradual pick-up in finance penetration in auto segment

52.0%

51.2% 51.1%

52.9%

54.1%53.8%

54.5%

55.4%

56.6%

48%

50%

52%

54%

56%

58%

0

100000

200000

300000

400000

500000

FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020 FY2021

(| crore)

New sales value Disbursement Penetration

Source: Crisil Research, ICICI Direct Research

While the auto finance industry witnessed AUM growth at 13.5% CAGR in

FY13-18, NBFCs grew at a faster pace of 14.5% CAGR during the same

period. Understanding of customer profile, product customisation to suit

customer needs, expertise in asset valuation (especially in used assets)

along with faster turnaround time have enabled NBFCs to grow their loan

book. This has led to an increase in market share of NBFCs from 47% in FY13

to ~50% in FY17. However, in FY18, banks with increased focus towards

retail loans witnessed an increase in market share by ~100 bps to 51%.

Exhibit 19: NBFCs contribute ~49% of auto finance in FY18

53% 54% 52% 53% 50% 51%

47% 46% 48% 47% 50% 49%

0%

20%

40%

60%

80%

100%

FY13 FY14 FY15 FY16 FY17 FY18

Bank NBFC

Source: Company, Crisil Research, ICICI Direct Research

Banks and NBFCs form two major financiers in the formal auto finance

industry. A peculiar feature to be noted is that each participant has its

focused sub-segment in terms of geography, customer and products. While

ICICI Securities | Retail Research 11

ICICI Direct Research

Initiating Coverage | M&M Financial Services

banks concentrate on urban business, NBFCs have garnered dominant

market share in rural areas because of their reach in remote regions. While

banks have a higher market share in the new vehicle segment, NBFCs cater

to the used vehicle segment.

Exhibit 20: Banks lead pie in PV;NBFC dominates in used vehicle business

55%

75%

50% 50%

22% 25%

45%

25%

50% 50%

78% 75%

0%

20%

40%

60%

80%

100%

CV PV Others Tractors Used Vehicle 2/3 W

Bank NBFC

Source: Crisil Research, ICICI Direct Research

NBFC market continues to remain buoyant

The auto finance industry is expected to grow at 17% CAGR in FY19-20E to

~| 9.3 lakh crore (Crisil Research). Among financiers, growth of banks is

expected to be higher at 17-19%, led by higher focus on retail segment and

growth in new vehicle (PV and MHCV) while NBFCs will continue to

dominate in the used vehicle and low ticket (two and three wheeler)

segment. Therefore, the market share of banks in auto finance is expected

to increase ~100 bps to ~52% in FY20E.

Exhibit 21: NBFC market share in auto finance to remain buoyant

53% 54% 52% 53% 50% 51% 51% 52%

47% 46% 48% 47% 50% 49% 49% 48%

0%

5%

10%

15%

20%

0%

25%

50%

75%

100%

FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Banks NBFC YoY growth (RHS)

Source: Crisil Research, ICICI Direct Research

Captive financier gaining market share; trend to continue ahead

Auto finance NBFCs are broadly divided into two sub-segments – captive

and non-captive financiers. Captive financier are the ones formed by original

equipment manufacturers (OEM) and are generally engaged in providing

finance assistance for purchase of the parent’s vehicles. Non-captive

financiers, on the other hand, have a product portfolio spanning across

manufacturers. In FY13-18, there was steady growth in the loan book of

captive financers, which led to an increase in their market share from 15.5%

in FY13 to 18% in FY18.

ICICI Securities | Retail Research 12

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Exhibit 22: Captive financer to grow faster at 19.7%CAGR in FY19-20E

0.71.2

1.7

1.4

2.1

2.8

0

1

2

3

4

5

FY15 FY18 FY20E

(| lakh crore)

Captive Non-captive

Source: Crisil Research, ICICI Direct Research

The main advantage for captive financiers is access to a large dealer network

of OEMs where significant proportion of auto loans originate. In addition,

captive financiers also provide loans to channel partners. This trend is

expected to continue ahead in FY19-20E, with captive NBFCs seen growing

at a relatively faster pace of 19.7% CAGR. MMFS, being a captive financier,

is set to benefit from this prevailing trend in the auto finance segment.

Buoyant rural economy & under-penetration to drive industry

The state of the rural economy and pace of infrastructure activity are primary

factors, which define growth as well as asset quality for rural financiers. Farm

output and realisation are two important aspects, which drive the health of

small borrowers. In FY09-13, healthy output and better realisation led to

higher growth for rural financiers while lower farm production and a muted

rise in MSP in FY13-16 impacted the rural economy and thereby asset quality

and earnings of rural lenders.

Apart from agriculture, pace of construction activity is another important

driver of financial health of rural economy. With signs of a pick-up in

construction activity, expect rural economy to tread recovery path ahead.

Higher social spending to support rural economy

Rural spending is an integral part of the Indian growth story. To boost rural

income, production and consumption, the government has been

undertaking various measures. It has been increasing allocation in existing

rural based schemes and initiating new schemes. The outlay towards rural

upliftment in the last three years has been growing at 14.3% CAGR.

Schemes like Mahatma Gandhi National Rural Employment Guarantee

Scheme (MNREGA), National Rural Livelihood Mission and Pradhan Mantri

Awas Yojana-Grameen has seen consistent growth. Increase in cash inflow,

led by the government’s support, is seen strengthening the rural economy.

This, in turn, should drive growth in consumption.

Exhibit 23: Allocation to MGNREGA witnessed jump from FY17 onwards

0%

5%

10%

15%

20%

25%

30%

0

100

200

300

400

500

600

700

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E

Amount (| bn) Growth (%)

Source: Ministry of rural development,, ICICI Direct Research

Cement Demand showing sign of recovery

-4%

0%

4%

8%

12%

16%

0

100000

200000

300000

FY08 FY11 FY14 FY17

Amount (in tonnes) Growth (%)

Source: EAindustry.nic.in, ICICI Direct Research

ICICI Securities | Retail Research 13

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Farm loan waiver to support tractor sales

Farm loan waivers are the flavour of the season. States have unveiled loan

waivers of ~| 2,29,100 crore since 2014. Further, possibility of loan waivers

cannot be ruled out going into general elections in 2019. Post farm loan

waiver, an uptick in tractor sales is witnessed with a lag. In 2014, 2017 &

2018, an uptick of 20.8%, 18% & 22.1%, respectively, was witnessed in

tractor volume post announcement of loan waivers. With | 102100 crore of

farm loan waiver announced in the current fiscal, tractor sales are seen

remaining healthy, thereby providing impetus to tractor finance.

The government recently announced an income support scheme for small

farmers wherein farmer are eligible for basic income of | 6000 per annum.

Along with this, various state governments have announced different

versions of basic income schemes for small and marginal farmers.

Implementation of such schemes will remain positive for demand for two

wheelers, brightening the outlook for auto finance.

Exhibit 24: Farm loan waiver and tractor volumes in India

States (| in crore) Year Cost of Loan Waiver Tractor Sales Growth (%)

Andhra Pradesh 2014 24,000

Telangana 2014 17,000

Tamil Nadu 2016 6,000

Uttar Pradesh 2017 36,000

Maharashtra 2017 34,000

Punjab 2017 10,000

Karnataka 2018 34,000

Rajasthan 2018 8,000

Madhya Pradesh 2018 36,000

Rajasthan 2018 18,000

Chhattisgarh 2018 6,100

18.0

22.1

20.8

Source: RBI, government estimates, ICICI Direct Research

Used CV market – potential to witness pick up ahead

The used vehicle segment witnessed moderation led by slower new vehicle

sale in previous years. Unutilised capacity and slowdown in infra activities

led to an extension in the replacement cycle for fleet operators, adversely

impacting volumes in the used market. In addition, financiers remained

cautious while lending to small fleet operators and first-time buyers with a

weaker credit profile, which acted as a deterrent for growth in the used

segment. Given healthy capacity addition in new CV in FY16-18 and lag in

replacement, pre-owned vehicle segment is expected to witness increased

traction from FY21E onwards. However, in FY18-20E, growth in used CV

space is seen remaining moderate.

Pent up demand in CV space led by migration to BS-VI norms

The government has fast-tracked the migration of newer vehicles to the BS-

VI regime by April 2020, four years earlier than the prior scheduled time,

thus leapfrogging entire BS-V emission norms. This will lead to pre-buying

of commercial vehicle in 2019, leading to surge in sale of new CV in FY20E.

Improvement in finance penetration & LTV to support growth

The Indian auto finance market has been growing at a healthy pace of 13.5%

CAGR in FY13-18. Currently, auto finance penetration & loan to value (LTV)

at 74% & 72% respectively are at par with developed countries. Finance

penetration for PV & utility vehicle is at 77%, 73%, respectively, while CV is

higher at ~95%. Going ahead, sharing of borrower’s information with credit

bureaus is seen aiding financiers to access borrowers credit profile, thereby

providing scope for an increase in LTV. Penetration in the commercial

vehicle is expected to remain steady while PV & utility vehicles are projected

to reach 79% & 77%, respectively, by FY22, fuelled by growth beyond Tier

Finance penetration & LTV across vehicle

segment

Finance

penetration

(%)

LTV (%)

PV 77 75-80

Utility Vehicle 73 75-80

New MHCVs >97 80-85

New LCVs >97 75-80

Tractors 90 76

Used PV 15 75

Source: Company, Crisil Research, ICICI Direct Research

ICICI Securities | Retail Research 14

ICICI Direct Research

Initiating Coverage | M&M Financial Services

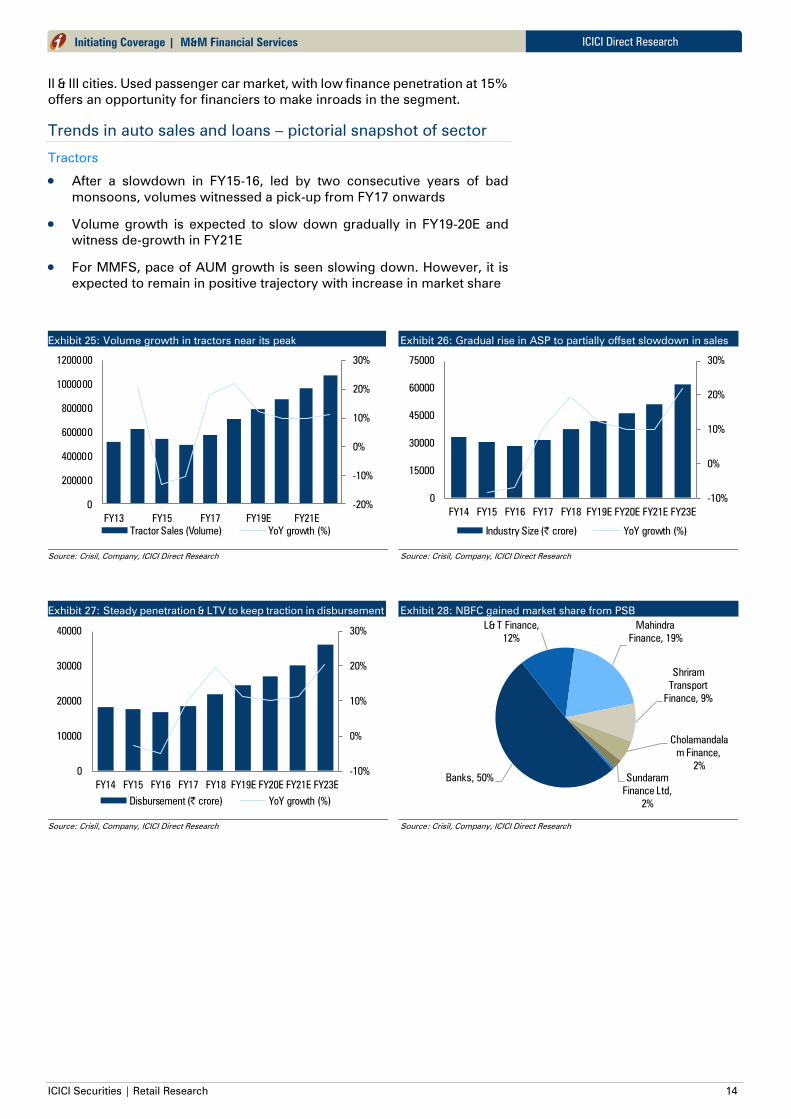

II & III cities. Used passenger car market, with low finance penetration at 15%

offers an opportunity for financiers to make inroads in the segment.

Trends in auto sales and loans – pictorial snapshot of sector

Tractors

After a slowdown in FY15-16, led by two consecutive years of bad

monsoons, volumes witnessed a pick-up from FY17 onwards

Volume growth is expected to slow down gradually in FY19-20E and

witness de-growth in FY21E

For MMFS, pace of AUM growth is seen slowing down. However, it is

expected to remain in positive trajectory with increase in market share

Exhibit 25: Volume growth in tractors near its peak

-20%

-10%

0%

10%

20%

30%

0

200000

400000

600000

800000

1000000

1200000

FY13 FY15 FY17 FY19E FY21E

Tractor Sales (Volume) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 26: Gradual rise in ASP to partially offset slowdown in sales

-10%

0%

10%

20%

30%

0

15000

30000

45000

60000

75000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E FY23E

Industry Size (| crore) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 27: Steady penetration & LTV to keep traction in disbursement

-10%

0%

10%

20%

30%

0

10000

20000

30000

40000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E FY23E

Disbursement (| crore) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 28: NBFC gained market share from PSB

Banks, 50%

L& T Finance,

12%

Mahindra

Finance, 19%

Shriram

Transport

Finance, 9%

Cholamandala

m Finance,

2%

Sundaram

Finance Ltd,

2%

Source: Crisil, Company, ICICI Direct Research

ICICI Securities | Retail Research 15

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Commercial vehicles

Volume trajectory in CV has remain volatile in the past, with healthy

growth seen in FY18 and FY19E

Axle load norms are expected to partly offset volume growth in initial

months of CY19. Implementation of BS-VI is expected to lead to pent up

demand in FY20E. In FY21E, volumes may see a dip; ASP may move up

Pent up demand in FY20E may lead to volume growth in industry as well

as MMFS. In FY21E, CV volume may dip. MMFS is expected to witness

slower growth in AUM led by increase in market share

Exhibit 29: Improving rural economy & higher infra outlay to boost CV

-30%

-20%

-10%

0%

10%

20%

30%

0

300000

600000

900000

1200000

1500000

FY13 FY15 FY17 FY19E FY21E

CV Sales (Volume) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 30: Pent up demand in FY20E led by migration to BSVI norms

-20%

-10%

0%

10%

20%

30%

40%

0

50000

100000

150000

200000

250000

FY13 FY14 FY15 FY16 FY17 FY18 FY19EFY20EFY21E

Industry Size (| crore) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 31: Steady penetration & LTV to keep traction in disbursement

-40%

-20%

0%

20%

40%

0

25000

50000

75000

100000

125000

FY13 FY15 FY17 FY19E FY21E

Disbursement (| crore) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 32: Prominent player in CV finance

HDFC Bank,

16.4%

IndusInd

Bank, 15.7%Kotak

Mahindra

Bank, 10.7%

Other banks,

12.3%

Mahindra

Finance, 7.9%

Magma

Fincorp , 2.6%

Cholamandala

m Finance,

16.1%

Sundaram

Finance Ltd,

9.1%

AU Small

Finance Bank

, 1.6%

Equitas

Holdings ,

1.6%

India Infoline

Holdings Ltd,

2.8%

Manappuram

Finance, 0.4%

Source: Crisil, Company, ICICI Direct Research

ICICI Securities | Retail Research 16

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Passenger vehicles

Steady volume growth is seen in FY16-18, which is expected to continue

ahead

Incremental volume growth & gradual increase in ASP (led by higher

traction in UV volume) is expected to keep sales traction broadly steady

MMFS is seen grabbing finance market share by ~100 bps, thereby

witnessing steady growth in AUM

Exhibit 33: Lower PV penetration bodes well for volume growth

-10%

0%

10%

20%

0

1500000

3000000

4500000

FY13 FY14 FY15 FY16 FY17 FY18 FY19EFY20EFY21E

PV Sales (Volume) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 34: Tilt towards UV to boost industry growth

-5%

0%

5%

10%

15%

20%

0

100000

200000

300000

400000

FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Industry Size (| crore) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 35: Volume & improved finance availability to boost growth

-10%

0%

10%

20%

30%

40%

50%

60%

0

50000

100000

150000

200000

250000

300000

FY13 FY15 FY17 FY19E FY21E

Disbursement (| crore) YoY growth (%)

Source: Crisil, Company, ICICI Direct Research

Exhibit 36: Banks dominate new PV finance market

HDFC Bank,

23.8%

IndusInd

Bank, 2.6%

Other banks,

48.6%

Mahindra

Finance, 7.8%Magma

Fincorp , 1.1%

Shriram

Transport

Finance,

6.9%

Cholamandala

m Finance,

1.6%Sundaram

Finance Ltd,

2.3%

Shriram City

Union Finance

, 1.1%

AU Small

Finance Bank

, 1.3%

Source: Crisil, Company, ICICI Direct Research

ICICI Securities | Retail Research 17

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Investment Rationale

MMFS, a leading vehicle financer, focuses mainly on the rural and semi-urban areas. MMFS has a successful track

record in terms of business growth. However, volatility in earnings cannot be ruled out. A strong undercurrent

led by buoyant rural economy is expected to benefit MMFS. Business momentum may continue ahead.

Diverse product portfolio, well-organised business process, wide

distribution network and strong relationship with automobile

manufacturers are expected to enable it to capture market share

Margins may jump in FY19E. Healthy balance of credit and borrowing

mix are expected to keep margins steady ahead

Ind-As, reflecting real stress, led to a decline in NPA. Improvement in

asset quality is expected to continue ahead

Healthy credit growth and robust operational performance may improve

RoA by ~20-30 bps in FY19-21E

Rural, semi-urban vehicle finance – Huge untapped market

India, predominantly a rural economy, continues to remain plagued by huge

proportion of population being under banked or un-banked. Availability of

auto finance remains weak, along with uneven disparity when seen in terms

of geographic presence. In terms of vehicle sales, major OEMs like Maruti

Suzuki, two-wheeler maker Hero Motor and tractor maker M&M generate

~35-50% of their sales from rural areas. However, penetration of auto

financier remains higher in top cities owing to easy credit availability and

better customer appraisal. Higher quantum of cash sales and weak credit

profile of the customers, on the other hand, keeps rural areas on a weak

footing in terms of credit outlay. Based on Crisil Research, financial

penetration (PV & UV) in top 20 cities is ~80% while other cities have

penetration ratio lower at ~65% with rural penetration even lower.

A buoyant rural economy and large untapped market provides huge

opportunity for growth. Apart from growth in auto sales, rise in financial

penetration is another important factor to drive growth of the auto finance

industry. Expansion beyond cities in rural areas is seen increasing

penetration of financiers while availability of customer credit profile is

expected to improve loan to value (LTV). MMFS, with a significant presence

in semi-urban and rural areas stands to benefit from untapped automobile

demand and low penetration of finance in rural areas.

Key strengths to act as pillar supporting growth

India is a country, which is not only large in terms of geography but also in

terms of culture, attitude and natural conditions. Such huge diversity acts as

a major challenge in doing business. MMFS, with extensive penetration

across semi-urban and rural India has gained exceptional knowledge of local

characteristics of these diversified markets. A diverse product portfolio, well-

organised business process, wide distribution network and strong

relationship with automobile manufacturers are key strengths of MMFS.

Wide reach in rural area

MMFS has a strong network of ~1313 branches with more than ~18733

employees on the ground. Customer facing staff, including field officers, are

localites. Therefore, they are well aware of local conditions and customers.

This network and local understanding of customers provides it a handsome

advantage for growth in rural regions.

ICICI Securities | Retail Research 18

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Product portfolio to suit rural customers

With over two decades of lending expertise in rural & semi-urban markets,

the company has developed an understanding of the demands of

customers. Therefore, it is able to customise products to suite customer

needs, which acts as a key strength. In addition, such knowledge is also

instrumental in keeping a lid on asset quality in the long run.

Large dealer network of parent

A wide branch network and strong relationship with dealers aid business

growth. The large dealer network of the parent provides additional thrust to

growth. Currently, MMFS has access to more than 1000 dealers of the

parent, from where a loan originates, providing direct access to customers

and, thereby, business growth.

Lower intensity of competition

MMFS competes primarily with moneylenders along with smaller NBFCs.

High interest rates charged by these competitors makes MMFS a preferred

choice among rural customers. A strong brand name leads to trust and

simplified processes along with fast paperwork, providing an advantage

over competition.

Buoyant rural economy to drive credit growth

India has made significant progress in automotive growth so far, driven by

urban consumers. However, the government’s vision for economic growth

and development across all strata of the country is expected to pave the way

for rural India to complement growth in auto volumes ahead. Low tractor

density compared to global peers, two consecutive years of normal

monsoon, better crop production, government spending and increasing use

of tractors in non-agricultural sectors may drive tractor volumes ahead. The

government focuses on increasing infra spending and approval to large

projects - ‘Bharatmala’ (worth | 7 lakh crore to build ~83,000 km of roads by

2022) to lead to traction in commercial vehicle demand. Tipper sales are

expected to get a boost with an improvement in mining/construction

activity. As per Crisil, the CV market is expected to grow at 5-7% CAGR in

FY19-23. Rising disposable income and a shift towards UV over passenger

car is seen leading to growth in the PV segment.

MMFS has, over time, transformed from a single product financing single

vendor company to financier present across auto segments catering to

various manufacturers. AUM growth has remained healthy at 22.7% CAGR

in FY11-18, with phase of slower growth seen in FY15-16, led by bad

monsoon. A shift is also witnessed in asset mix with growth tilting towards

pre-owned vehicles and SME segment. In FY11, new vehicle finance (PV,

UV, tractors) formed ~85% of AUM, which has now reduced to 66% in FY18.

Exhibit 37: MMFS AUM mix (FY14-21E)

29 31 31 30 27 25 23 23

19 18 17 1717

17 16 15

24 23 24 2322

2019 19

15 13 12 1314

17 18 18

9 10 10 98 9 10 10

4 5 6 8 12 13 14 15

0

20

40

60

80

100

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)

SME and others Pre-owned vehicles

Commercial vehicles and Construction equipments Cars and Non M&M UVs, Tractors & SCVs

Tractors (M&M) Auto/ Utility vehicles (M&M)

Source: ICICI Direct Research, Company

ICICI Securities | Retail Research 19

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Penetration in newer geographies and a gradual improvement in

productivity of existing branches is seen driving AUM growth ahead.

However, volatility in auto volumes and increasing competition from banks

may limit overall traction. We expect overall AUM to grow at 19.9% CAGR

in FY19-21E to | 94996 crore.

Among product classes, growth in cars/UVs (contribute ~49% of advances),

in last three years, has remained slower at ~11% CAGR on the back of single

digit growth in volume. Competitive pressure in PV segment and slower sale

of M&M in UV may keep incremental traction lower at ~14% CAGR in FY19-

21E. Tractor (17% of AUM) and CV (14% of AUM) constituted high growth

segment in FY16-9MFY19. Positive growth in last three years and high base

are seen impacting volume growth in tractors in FY21E. Hence, MMFS is

expected to witness a slowdown. However, traction is expected to remain

positive with gain in market share. For CVs, tapering off of low base and

recent increase in axle load is seen impacting volumes. However,

anticipated pent up demand in H2FY20E (led by BS VI) is seen offsetting the

pressure. Post FY20E, volumes are seen dipping with ASPs increasing,

leading to muted sales. A gradual increase in market share is expected to

keep traction in disbursement but velocity is seen declining. We expect

~30% CAGR in FY19-21E in AUM of CV. Pre-owned vehicles (~8% of AUM)

and SME (~12% of AUM) are expected to witness highest momentum and

drive loan growth. The proportion of these segments is seen increasing from

~20% in FY18 to ~25% in FY21E.

Exhibit 38: Robust growth in disbursements

25,400 24,331 26,706

31,659

37,773

47,320

55,337

63,537

-4.2

9.8

18.5 19.3

25.3

16.9

14.8

-10

0

10

20

30

0

15,000

30,000

45,000

60,000

75,000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)| crore

Disbursements Growth (%)

Source: Company, ICICI Direct Research

Exhibit 39: AUM growth at ~20% in FY19-21E

34,13336,878

40,933

46,778

55,101

67,505

81,369

94,996

8.0

11.0

14.3

17.8

22.5

20.5

16.7

0

5

10

15

20

25

0

15,000

30,000

45,000

60,000

75,000

90,000

105,000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)(| crore)

Gross AUM AUM growth (%)

Source: Company, ICICI Direct Research

Post two years of muted growth in FY15-16, led by deficient monsoon, a

continuous pick-up has been witnessed in the last three fiscals. Combined

with this, an increase in MSP is adding to the growth potential of auto sales.

MMFS, with a substantial presence in rural areas, benefited from a revival in

rural sentiment. Subsequently, AUM growth began inching northwards with

18% YoY growth in FY18 to touch | 55101 crore. A wider reach in untapped

Tractor Volume growth (%)

FY16 FY17 FY18

FY19-

FY22E

CAGR

Tractor -10 18 22 7-9

Source: Company presentation, Crisil, ICICI Direct Research

Loan-to-value expected to increase to ~77% for cars

and ~76% for UVs in FY22 from76% and 73%

respectively

By FY22, penetration levels are projected to increase

to 79% for cars and 77% for UVs from 77% and 73%

respectively

ICICI Securities | Retail Research 20

ICICI Direct Research

Initiating Coverage | M&M Financial Services

rural and semi-urban areas, strong positioning and increasing penetration

are expected to provide advantage to MMFS and drive credit growth ahead.

We expect AUM to grow at 19.9% CAGR in FY19-21E to | 94996 crore.

Exhibit 40: Growth in auto sales and improving finance penetration to drive auto finance

Tractor FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020 FY2021

Tractor Sales (Volume) 524,000 633,000 550,000 493,764 582,844 711,478 782,626 845,236 777,617

Industry Size (| crore) - 33,300 30,500 28,400 31,400 37,500 40,425 42,786 41,331

Disbursement (| crore) - 18,200 17,700 16,800 18,500 22,100 24,600 26,194 25,465

Mahindra Disbursement 4,768 4,318 5,110 5,074 6,332 6,799 8,060 8,713 9,235

Market Share 24% 29% 30% 34% 31% 33% 33% 36%

Loan outstanding 5,303 6,485 6,638 6,959 7,952 9,367 11,241 13,070 14,164

Commercial Vehicle FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020 FY2021

CV Sales (Volume) 793,150 632,851 614,961 685,704 714,232 856,453 1,010,615 1,162,207 987,876

Industry Size (| crore) 93,654 79,526 90,647 101,988 107,268 141,730 167,242 192,328 183,096

Disbursement (| crore) 45,200 34,352 37,444 46,056 50,201 65,200 77,772 91,938 88,441

Mahindra Disbursement 2,622 3,048 2,676 2,938 3,799 4,910 8,399 9,470 10,259

Market Share 6% 9% 7% 6% 8% 8% 11% 10% 12%

Loan outstanding 4,745 5,120 4,794 4,912 6,081 7,714 11,309 14,583 16,938

Passenger Vehicle FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020 FY2021

PV Sales (Volume) 2,665,015 2,503,685 2,601,236 2,789,678 3,047,582 3,287,965 3,403,044 3,607,226 3,859,732

Industry Size (| crore) 130,007 125,200 135,461 152,466 172,827 200,000 211,140 228,285 249,150

Disbursement (| crore) 71,100 69,400 76,100 86,800 99,700 116,900 125,845 138,721 154,327

Mahindra Disbursement 12,158 12,700 11,922 12,819 15,196 17,376 19,964 23,393 27,568

Market Share 17% 18% 16% 15% 15% 15% 16% 17% 18%

Loan outstanding 14,515 18,091 19,914 22,513 24,792 27,000 30,305 34,651 40,150

Source: Company, Crisil Research, ICICI Direct Research

Strong parentage and positive ALM to benefit in liquidity crises

The recent liquidity crises emphasised the importance of better-rated

lenders with strong parentage and positive ALM mismatch. MMFS is a well-

rated NBFC - Crisil rates its long-term debt instruments as AA+. This enables

MMFS to raise funds at competitive rates.

On the borrowing mix, the proportion of banks has been on a decline from

45.9% in FY12 to 39% in FY18 while proportion of mutual funds and

insurance companies has increased from 29.2% to 43.8% during the same

period. However, post the liquidity crunch seen in recent months, the

proportion of mutual funds declined to ~22% in 9MFY19 compared to

~28.1% in FY18. However, it still continues to remain a significant source of

borrowing. In addition, contribution of banks has witnessed an increase from

39% in FY18 to ~41% in 9MFY19, indicating confidence of lenders. To tide

over the liquidity crises, MMFS has raised ~ | 1000 crore from parent (M&M)

highlighting the advantage of a strong parentage. Given strong

fundamentals, favourable ALM and healthy rating, we expect MMFS to be

able to garner incremental borrowing at competitive rate, thereby enabling

it to maintain its margins and providing advantage to gain market share.

ICICI Securities | Retail Research 21

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Exhibit 41: Borrowing mix

58.6%48.3%

42.0% 46.1%39.0% 42.3% 41.5%

7.9%

14.4%18.9%

21.2%28.1% 22.7% 21.7%

10.0% 14.3% 18.0% 7.8%15.8%

14.2% 14.6%

9.8% 6.3% 4.6% 12.1%

9.3% 12.4% 11.9%

13.7% 16.8% 16.5% 12.8%7.8% 8.4% 10.4%

0%

20%

40%

60%

80%

100%

FY14 FY15 FY16 FY17 FY18 H1 FY19 9MFY19

Banks Mutual Fund Insurance Co. & Institutions Banks for Assignment Others

Source: Company, ICICI Direct Research

One of the problems faced by NBFCs is large proportion of ALM mismatch

led by short-term borrowings funding long-term loans. This nature of

business creates a vacuum in the borrowing mix that makes it vulnerable in

times of liquidity crunch. MMFS, on the other hand, remained largely

unaffected owing to nearly one-third of asset and liabilities getting repriced

every year. ALM, on a cumulative basis, remains positive (that is more

advances will mature compared to borrowings) in all the buckets from one

month to five years (refer Exhibit below).

Exhibit 42: ALM remains positive across various buckets (9MFY19)

35693131

1936

4495

5794

7793

9742

0

2500

5000

7500

10000

Upto 1 month Upto 2

months

Upto 3

months

Upto 6

months

Upto 1 year Upto 3 years Upto 5 years

Cumulative Mismatch - Positive (| crore)

Source: Company, ICICI Direct Research

Up-tick in margins in FY19E; to remain steady ahead

MMFS commands strong pricing power owing to widespread access to rural

areas across India. In most areas of operation, least/negligible competition

exists due to absence of other financial institutions, with moneylenders as

the only option available to borrowers. This enables it to pass on any

increase in cost thereby maintaining healthy margins.

For MMFS, asset quality has played an important role in movement of

margins. After remaining at ~18% in FY10-14, yields fell ~300 bps to ~15%

in FY17 led by increase in NPA due to bad monsoon. Similarly, margins, at

~10% earlier, declined to ~8.4% in FY17 and 7.6% in FY18.

Exhibit 43: Loan book increasing towards CV and Tractors

Breakup of Assets Financed (%)FY16 FY17 FY18 FY19E FY20E FY21E

Auto/ Utility vehicles 30 28 26 24 24 25

Tractors 15 19 18 17 16 15

Cars 22 22 20 18 18 19

CV & Construction equipments 11 11 13 18 17 16

Used Vehicle 16 13 14 17 18 19

SME and others 6 7 9 6 7 7

Source: Company, ICICI Direct Research

Higher NIMs compared to peers

7.6

6.3

7.8

4.3

0.0

2.0

4.0

6.0

8.0

MMFS CFC STFC SFC

NIM on AUM (%)

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 22

ICICI Direct Research

Initiating Coverage | M&M Financial Services

In FY19E, yields and, thereby, margins are anticipated to witness a surge

owing to 1) improvement in NPA and subsequent interest reversal, 2) focus

on high yield products - tractor and used vehicle, and 3) recent hike in

lending rates. MMFS has not recognised income on Stage 3 assets.

Therefore, reduction in Stage 3 assets is expected to boost interest

recognition and, thereby, margins in FY19E. Calculated NIM is seen jumping

~100 bps to 8.7% in FY19E.

Focus on product mix and customer engagement are expected to keep

yields broadly stable ahead. Liquidity crunch and liabilities slated for

repricing at higher rates are expected to keep cost of funds higher ahead.

Ind-As allows recognition of income on net NPAs. Hence, effect of asset

quality on margins may fizzle out from FY20E onwards. Hence, margins are

expected to remain steady in FY20E. Improving productivity and anticipated

capital raising may lead to ~10 bps increase in margins to ~8.6% in FY21E.

Exhibit 44: NIM to surge in FY19E; to remain broadly steady thereafter….

9.2

8.47.6

8.78.5 8.6

16.2

15.5

14.2

15.1 15.3 15.4

9.59.1

8.48.6 8.7 8.7

6

9

12

15

18

FY16 FY17 FY18 FY19E FY20E FY21E

Net Interest Margins Yield on Gross AUM Cost of borrowing

(%)

Source: Company, ICICI Direct Research

Business expansion drives cost; operating leverage to kick in

For MMFS, one of the major components of opex is employee expense, as

the business needs investment in human resource to touch base with

customers (field staff). Over the years, MMFS has been increasing branches

and employee strength adding to opex. However, in the last five years,

opex/AUM has been in a tight range of 2.8-3.2%. As of 9MFY19, opex/AUM

was at ~3%.

Going ahead, we expect the branch count to increase to 1584 in FY21E from

1284 in FY18. Likewise, employee strength is set to increase from ~18733

in FY18 to ~22176, keeping employee per branch on a blended basis

broadly steady at ~14 in FY21E.

Employee productivity, measured in terms of contracts per employee, has

been on a gradual increase since FY10, except FY15-16, wherein contracts

per employee declined led by two consecutive years of bad monsoon. With

consecutive years of normal monsoon and positive vehicle sales, employee

productivity is seen increasing with contract per employee touching ~40 in

FY21E. In addition, increase in disbursement per contract is expected to

improve productivity.

Employee expense rose at faster pace in Q3FY19, led

by 1) higher employee addition at ~881 in Q3FY19

and 2) one-off incentive to employees as the

company completed 25 years of operations

Higher operational cost compared to peers

3.3

3.0

1.8

2.1

0.0

1.0

2.0

3.0

4.0

MMFS CFC STFC SFC

Op.costs/avg AUM (%)

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 23

ICICI Direct Research

Initiating Coverage | M&M Financial Services

Exhibit 45: Opex/advances

3.11

2.89

3.05

3.28

2.91 2.90 2.90 2.90

2.6

2.8

3.0

3.2

3.4

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

%

Source: Company, ICICI Direct Research

Though, investment in business expansion in recent quarters has kept

opex/AUM on the higher side, the ratio is seen subsiding as operating

leverage kicks in. Therefore, opex is seen growing at 22.2% CAGR in FY19-

21E to | 2598 crore. Also, opex to AUM is seen declining at ~2.9% in FY20-

21E, after inching up at ~3% in FY19E.

Exhibit 46: Number of employees

16,459

17,43317,85617,659

18,35018,48618,733

20,760

21,518

22,176

12000

15000

18000

21000

24000

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19EFY20EFY21E

In N

o's

Source: Company, ICICI Direct Research

Exhibit 47: Rise in contract per employee to aid productivity

28.3

30.6 31.5

29.2 28.5

30.1

33.4

35.6

37.9

39.9

20

25

30

35

40

45

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19EFY20EFY21E

(In Nos)

Source: Company, ICICI Direct Research

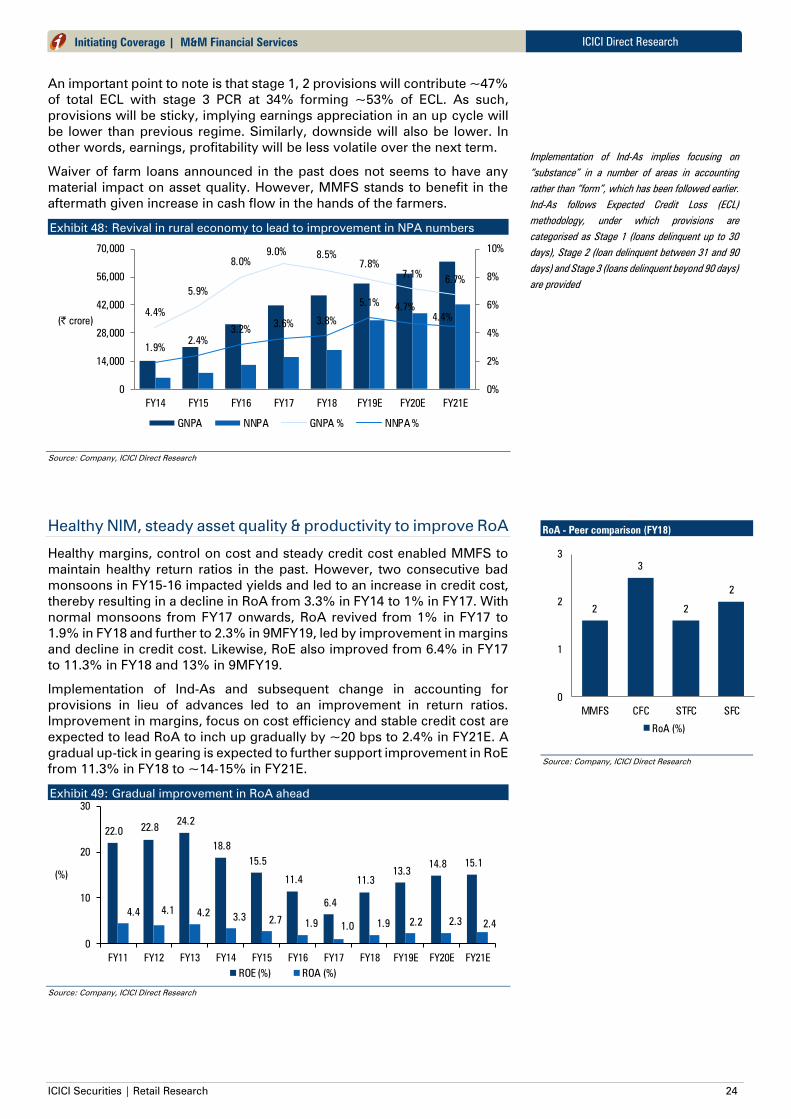

Headline NPA to improve; credit cost to remain at current level

For MMFS, headline NPA numbers have remained volatile over the years.

GNPA was at 3% in FY13, surging to 9% in FY18, led by two consecutive

bad monsoons and implementation of NPA recognition norms (180 days to

90 days). With a pick-up in rural economy, asset quality witnessed an

improvement, which is seen continuing ahead with GNPA at ~6.7% in

FY21E. We expect ~64% PCR on an overall basis, 4.4% NNPA for FY21E.

Though GNPA has remained high owing to volatile cash flows of the

borrower and dependence on agriculture, as per the management actual

loss ratio remains lower. Customers postpone payment but eventually pay

leading to loss given default (LGD) remaining low.

Implementation of Ind-As is seen bringing back rationality on NPA

recognition (as Stage III) and interest income write-backs. The expected loss

methodology also incorporates loss on interest income. As such interest

reversals are not required under Ind-As. This will lower volatility in earnings.

Implementation of Expected Credit Loss (ECL) methodology under Ind-As is

seen keeping overall provision levels higher compared to the earlier regime.

The reason for higher credit cost is attributable to increase in provision on

standard advances classified under stage 1 and 2 category. Provision in lieu

of advances classified as Stage 3 will be relatively lower as LGD and

probability of default are considered.

Gross NPA as percentage of loans

8.5

2.9

9.2

1.3

0

2

4

6

8

10

MMFS CFC STFC SFC

GNPL (% of loans)

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 24

ICICI Direct Research

Initiating Coverage | M&M Financial Services

An important point to note is that stage 1, 2 provisions will contribute ~47%

of total ECL with stage 3 PCR at 34% forming ~53% of ECL. As such,

provisions will be sticky, implying earnings appreciation in an up cycle will

be lower than previous regime. Similarly, downside will also be lower. In

other words, earnings, profitability will be less volatile over the next term.

Waiver of farm loans announced in the past does not seems to have any

material impact on asset quality. However, MMFS stands to benefit in the

aftermath given increase in cash flow in the hands of the farmers.

Exhibit 48: Revival in rural economy to lead to improvement in NPA numbers

4.4%

5.9%

8.0%

9.0%8.5%

7.8%

7.1%6.7%

1.9%2.4%

3.2%3.6% 3.8%

5.1%4.7%

4.4%

0%

2%

4%

6%

8%

10%

0

14,000

28,000

42,000

56,000

70,000

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

GNPA NNPA GNPA % NNPA %

(| crore)

Source: Company, ICICI Direct Research

Healthy NIM, steady asset quality & productivity to improve RoA

Healthy margins, control on cost and steady credit cost enabled MMFS to

maintain healthy return ratios in the past. However, two consecutive bad

monsoons in FY15-16 impacted yields and led to an increase in credit cost,

thereby resulting in a decline in RoA from 3.3% in FY14 to 1% in FY17. With

normal monsoons from FY17 onwards, RoA revived from 1% in FY17 to

1.9% in FY18 and further to 2.3% in 9MFY19, led by improvement in margins

and decline in credit cost. Likewise, RoE also improved from 6.4% in FY17

to 11.3% in FY18 and 13% in 9MFY19.

Implementation of Ind-As and subsequent change in accounting for

provisions in lieu of advances led to an improvement in return ratios.

Improvement in margins, focus on cost efficiency and stable credit cost are

expected to lead RoA to inch up gradually by ~20 bps to 2.4% in FY21E. A

gradual up-tick in gearing is expected to further support improvement in RoE

from 11.3% in FY18 to ~14-15% in FY21E.

Exhibit 49: Gradual improvement in RoA ahead

22.0 22.8

24.2

18.8

15.5

11.4

6.4

11.3

13.3 14.8 15.1

4.4 4.1 4.2 3.3

2.7 1.9 1.0 1.9 2.2 2.3 2.4

0

10

20

30

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

(%)

ROE (%) ROA (%)

Source: Company, ICICI Direct Research

Implementation of Ind-As implies focusing on

“substance” in a number of areas in accounting

rather than “form”, which has been followed earlier.

Ind-As follows Expected Credit Loss (ECL)

methodology, under which provisions are

categorised as Stage 1 (loans delinquent up to 30

days), Stage 2 (loan delinquent between 31 and 90

days) and Stage 3 (loans delinquent beyond 90 days)

are provided

RoA - Peer comparison (FY18)

2

3

2

2

0

1

2

3

MMFS CFC STFC SFC

RoA (%)

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 25

ICICI Direct Research

Initiating Coverage | M&M Financial Services

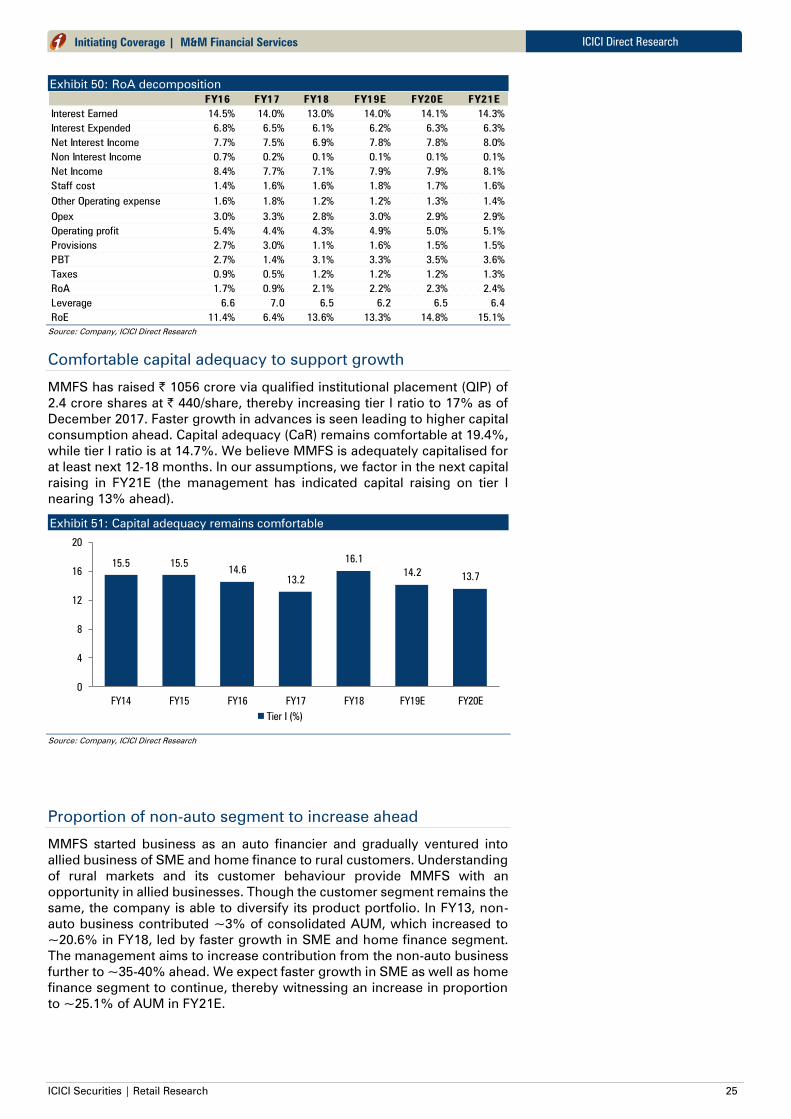

Exhibit 50: RoA decomposition

FY16 FY17 FY18 FY19E FY20E FY21E

Interest Earned 14.5% 14.0% 13.0% 14.0% 14.1% 14.3%

Interest Expended 6.8% 6.5% 6.1% 6.2% 6.3% 6.3%

Net Interest Income 7.7% 7.5% 6.9% 7.8% 7.8% 8.0%

Non Interest Income 0.7% 0.2% 0.1% 0.1% 0.1% 0.1%

Net Income 8.4% 7.7% 7.1% 7.9% 7.9% 8.1%

Staff cost 1.4% 1.6% 1.6% 1.8% 1.7% 1.6%

Other Operating expense 1.6% 1.8% 1.2% 1.2% 1.3% 1.4%

Opex 3.0% 3.3% 2.8% 3.0% 2.9% 2.9%

Operating profit 5.4% 4.4% 4.3% 4.9% 5.0% 5.1%

Provisions 2.7% 3.0% 1.1% 1.6% 1.5% 1.5%

PBT 2.7% 1.4% 3.1% 3.3% 3.5% 3.6%

Taxes 0.9% 0.5% 1.2% 1.2% 1.2% 1.3%

RoA 1.7% 0.9% 2.1% 2.2% 2.3% 2.4%

Leverage 6.6 7.0 6.5 6.2 6.5 6.4

RoE 11.4% 6.4% 13.6% 13.3% 14.8% 15.1%

Source: Company, ICICI Direct Research

Comfortable capital adequacy to support growth

MMFS has raised | 1056 crore via qualified institutional placement (QIP) of

2.4 crore shares at | 440/share, thereby increasing tier I ratio to 17% as of

December 2017. Faster growth in advances is seen leading to higher capital

consumption ahead. Capital adequacy (CaR) remains comfortable at 19.4%,

while tier I ratio is at 14.7%. We believe MMFS is adequately capitalised for

at least next 12-18 months. In our assumptions, we factor in the next capital

raising in FY21E (the management has indicated capital raising on tier I

nearing 13% ahead).

Exhibit 51: Capital adequacy remains comfortable

15.5 15.514.6

13.2

16.1

14.213.7

0

4

8

12

16

20

FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Tier I (%)

Source: Company, ICICI Direct Research

Proportion of non-auto segment to increase ahead

MMFS started business as an auto financier and gradually ventured into

allied business of SME and home finance to rural customers. Understanding

of rural markets and its customer behaviour provide MMFS with an

opportunity in allied businesses. Though the customer segment remains the

same, the company is able to diversify its product portfolio. In FY13, non-

auto business contributed ~3% of consolidated AUM, which increased to

~20.6% in FY18, led by faster growth in SME and home finance segment.

The management aims to increase contribution from the non-auto business

further to ~35-40% ahead. We expect faster growth in SME as well as home