manufacturing priority agenda

DESCRIPTION

Securing Industry in Kenya for Shared ProsperityTRANSCRIPT

5talkline 62

Imagine Impulse Line and Capillary-FreeMultivariable Level MeasurementEliminate mechanical issues with Endress+Hauser’s new Electronic Diff erential Pressure Systems

Electronic Diff erential Pressure for Level MeasurementDeltabar FMD72

ReliableSafeCost Eff ective

Manufacturing Priority Agenda

SECURING INDUSTRY IN KENYA FOR SHARED PROSPERITY

i

Table of ContentsForeword ................................................................................................................. ii

Abbreviations ............................................................................................................

MPA 2015: SECURING INDUSTRY IN KENYA FOR SHARED PROSPERITY .....................iii

Introduction .............................................................................................................iv

DEFINING THE BENEFITS OF THE KENYAN MANUFACTURING SECTOR ...................... v

Contribution to Kenyan GDP .................................................................................................................................................vi

Contribution to job creation ....................................................................................................................................................vi

Value addition by the manufacturing sector ........................................................................................................... vii

Contribution to public finance ............................................................................................................................................. vii

Consumer benefits of manufacturing ........................................................................................................................... vii

International trade and foreign exchange earnings .......................................................................................... vii

Investment ..........................................................................................................................................................................................viii

PILLAR ONE: Securing investment ............................................................................. 1

PILLAR TWO: Securing markets

– by leveraging on the ‘Buy Kenya, Build Kenya’ initiative and export competiveness .... 5

PILLAR THREE: Securing Infrastructure .....................................................................11

PILLAR FOUR: Securing Constitutional Gains .............................................................15

PILLAR FIVE: Securing Justice for the Economy .......................................................... 17

PILLAR SIX: Securing Security ..................................................................................19

PILLAR SEVEN: Securing the Future of Industry .........................................................21

Spotlight on agro-processing as a driver for industrial growth ..................................... 25

Conclusion .............................................................................................................. 32

References .............................................................................................................. 32

ii

Abbreviations

ACA Anti Counterfeit Authority

ADR Alternative Dispute Resolution

AGOA African Growth and Opportunity Act

AU African Union

CET CommonExternalTariff

CFTA Continental Free Trade Area Agreement

COMESA Common Market for Eastern and Southern Africa

CRA Commission for Revenue Allocation

DRC Democratic Republic of Congo

EAC East Africa Community

EAC HQ East Africa Community Headquarters

EACMA East Africa Community Management Act

EPZ Export Promotion Zones

ES Entreprise Survey

EU European Union

FDI Financial Direct Investment

FTA Free Trade Area Agreement

GDP Gross Domestic Product

GMO GeneticallyModifiedFoods

HCDA Horticultural Crops Development Authority

IBEC Intergovernmental Budget and Economic Council

ICT Information and Communication Technology

IDF Import Declaration Fee

KAM Kenya Association of Manufacturers

KARI Kenya Agricultural Research Institute

KCB Kenya Copyright Board

KEBS Kenya Bureau of Standards

KEMRI Kenya Medical Research Institute

iii

KEPHIS Kenya Plant Health Inspectorate Service

KIP Kenya Industrial Property Institute

KNBS Kenya National Bureau of Statistics

KWS Kenya Wildlife Service

KRA Kenya Revenue Authority

Ksh Kenya Shilling

LAPPSET Lamu Port and South Sudan Ethiopia Transport

MSMEs Micro, Small and Medium Enterprise

MW Megawatts

NACOSTI National Commission for Science, Technology and Innovation

NEMA National Enviroment Management Authority

NLC National Land Commission

NSSF National Social Security Fund

R&D Research and Development

SADC Southern African Development Community

SCT Single Customs Territory

SEZ Special Economic Zones

SME Small Medium sized Entreprises

STI Science, Technology and Innovation

TFDA Tanzania Foods and Drugs Authority

UAE United Arab Emirates

UK United Kingdom

US United States

USD United States Dollars

VAT Value Added Tax

WDI World Bank Indicators

WEF World Economic Forum

WRMA Water Resource Management Authority

iv

Foreword

Established in 1959, Kenya Association of Manufacturers (KAM) is the largest manufacturing association in Kenya, representing small and large manufacturers in every industrial sector. KAM is the consistent voice of the sector and the leading advocate for a policy agenda that helps manufacturers compete both within Kenya, regional and globally and create jobs.

We partner with Government to address a wide range of policy and administrative issues that affectthecostofdoingbusinessinKenya.Ateveryturn,weworkonbehalfofmanufacturersin Kenya to advance policies that help them do what they do best: create economic strength and jobs.

Every year, KAM prepares the Manufacturing Priority Agenda – a concise guide presentation on the most burdensome challenges facing industry in Kenya and which should receive the highest attention in our engagement with the Government and related public authorities throughout the year. The agenda is developed from engagements with our members and observations of emerging public policy as well as other regulations and review of the business environment.

Different issues affecting trade and the business environment take on different hues,sometimes gaining importance or sometimes retreating in the background in the light of more pertinentissuesorastheyareresolvedbyGovernment.Thiscallsforadifferentagendaeveryyear given the changing economic environment and considerations on the competitiveness of Kenya.

In 2015, we have organized the Agenda under the broad theme of ‘SECURING INDUSTRY FOR SHARED PROSPERITY’. This is informed by our deep conviction that manufacturing is critical to the transformation of Kenya and creation of new jobs in addition to assisting the Government deliver on its promise to the Kenyan people.

We have further collated the agenda into seven themes These seven pillars, if strengthened will lead to a more competitive environment for the whole industrial sector resulting in economic gains for the whole country.

Your (manufacturing) sector is a central pillar of our economy,…… without you, this country cannot achieve the goals of Vision 2030…..

Our economy needs a large number of new non-agricultural jobs to diversify, to cut poverty sharply, and to employ our young people. Without a strong manufacturingsector,ourchancesoffindingmanymore non-agricultural jobs are low.

H.E President Uhuru Kenyatta, CGH, President and Commander in Chief of the Defence Forces of the Republic of Kenya - 9th December, 2014

v

Top on our agenda this year is the need to secure investments and to secure new markets while strengthening the old ones. Without vibrant markets for our exports, we cannot grow thesectorsignificantly.Exportswillenablethecountrytoeffectivelydealwiththefiscalandmonetary challenges by reducing the current reliance on domestic consumption as a major economic driver. The ‘Buy Kenya, Build Kenya initiative’ if well implemented, will in turn help ussecurethedomesticmarketasafirststepandcriticalstep.

Our concerns about Infrastructure relate to the need to get our goods to the markets and in good time. Energy and Transportareimportantinfrastructural issuesthataffectthedayto day running of amanufacturing firmand Infrastructure that supports development andindustrialization is needed. Transport in particular impacts on cost of goods and services and ongoing government projects in this area are laudable and need to be seen to completion.

The other four pillars include securing constitutiongainsbyovercomingproblemsaffectingbusinesses due the implementation of 2010 Constitution which if unchecked have potential to be disruptive to business, We also need to secure justice for the economy awakening the judiciary to the commercial implications of their rulings while maintaining their impartiality. Attending to security threatswhichhavearippleeffectthroughouttheeconomyandthreateninvestments and also securing the future of industry by supporting sectors which will catalyse industrial growth. At the end, we discuss at length the agro processing industry which is a key promoter of industrialisation in agricultural based economies.

KAMoffers thisAGENDAas a contribution to shapingGovernmentpolicy in 2015 towardsrealization of the Vision of an industrialized middle income country and the promotion of shared prosperity in Kenya.

Pradeep Paunrana Chairman, Kenya Association of Manufacturers

vi

Manufacturing Priority Agenda: Securing Industry in Kenya for Shared Prosperity

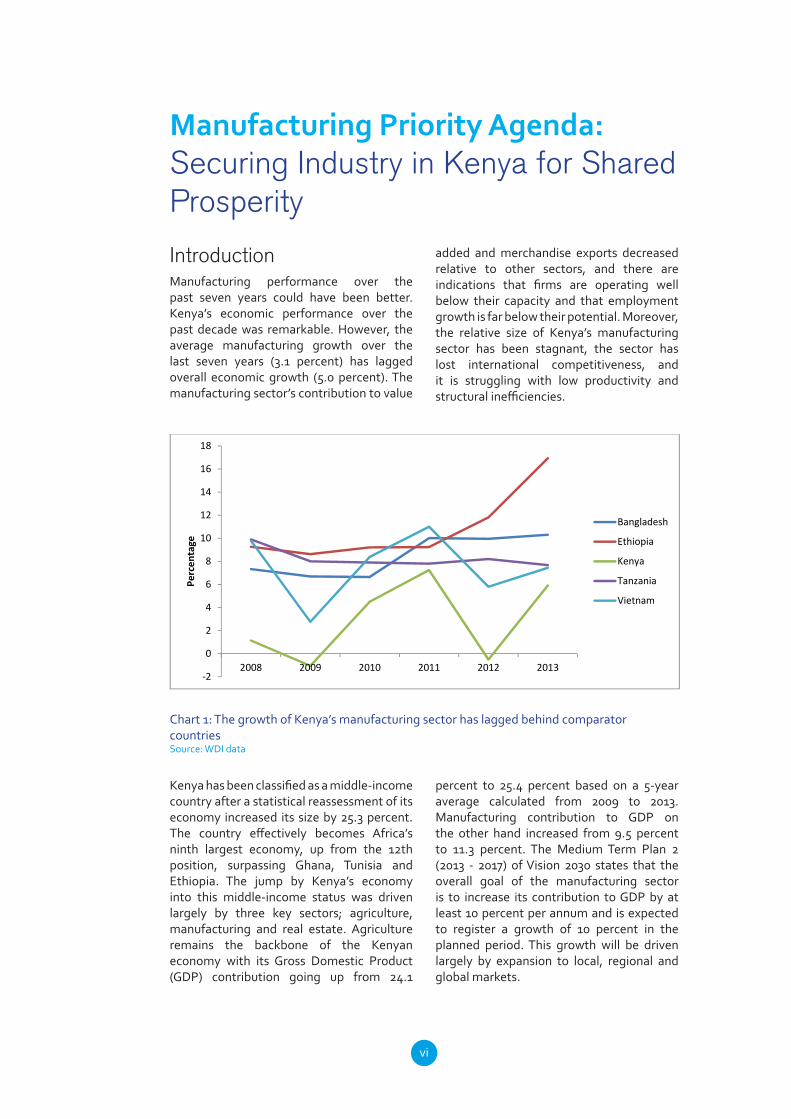

Introduction Manufacturing performance over the past seven years could have been better. Kenya’s economic performance over the past decade was remarkable. However, the average manufacturing growth over the last seven years (3.1 percent) has lagged overall economic growth (5.0 percent). The manufacturing sector’s contribution to value

added and merchandise exports decreased relative to other sectors, and there are indications that firms are operating wellbelow their capacity and that employment growth is far below their potential. Moreover, the relative size of Kenya’s manufacturing sector has been stagnant, the sector has lost international competitiveness, and it is struggling with low productivity and structuralinefficiencies.

-2

0

2

4

6

8

10

12

14

16

18

2008 2009 2010 2011 2012 2013

Percen

tage

Bangladesh

Ethiopia

Kenya

Tanzania

Vietnam

Chart 1: The growth of Kenya’s manufacturing sector has lagged behind comparator countries Source: WDI data

Kenyahasbeenclassifiedasamiddle-incomecountry after a statistical reassessment of its economy increased its size by 25.3 percent. The country effectively becomes Africa’s ninth largest economy, up from the 12th position, surpassing Ghana, Tunisia and Ethiopia. The jump by Kenya’s economy into this middle-income status was driven largely by three key sectors; agriculture, manufacturing and real estate. Agriculture remains the backbone of the Kenyan economy with its Gross Domestic Product (GDP) contribution going up from 24.1

percent to 25.4 percent based on a 5-year average calculated from 2009 to 2013. Manufacturing contribution to GDP on the other hand increased from 9.5 percent to 11.3 percent. The Medium Term Plan 2 (2013 - 2017) of Vision 2030 states that the overall goal of the manufacturing sector is to increase its contribution to GDP by at least 10 percent per annum and is expected to register a growth of 10 percent in the planned period. This growth will be driven largely by expansion to local, regional and global markets.

vii

Manufacturing has the potential to play a particularly important role in putting Kenya on a sustainable growth path, through; its direct contribution to creating quality employment, strong linkages with other parts of the economy, ability to raise capital accumulation, smooth volatility in the economy, and facilitate global integration and knowledge spillovers which are critical to the process of structural transformation. Kenyan industrialists need to have in place policies that make the east African country a better place to invest, a better place to innovate and a better place from which to export.

Total food products32%

Beverages and tobacco products

8%Chemicals and

chemical products6%

Printing and reproduction of recorded media

5%

Rubber and plastic products

5%

Fabricated metal except machinery

and equipment4%

Other non-metallic mineral

products4%

Coke and refined petroleum products

4%

Basic metals4%

Paper and paper

products3%

Micro and small enterprises**

9%

Other manufacturing***

16%

Share of total manufacturing in 2013

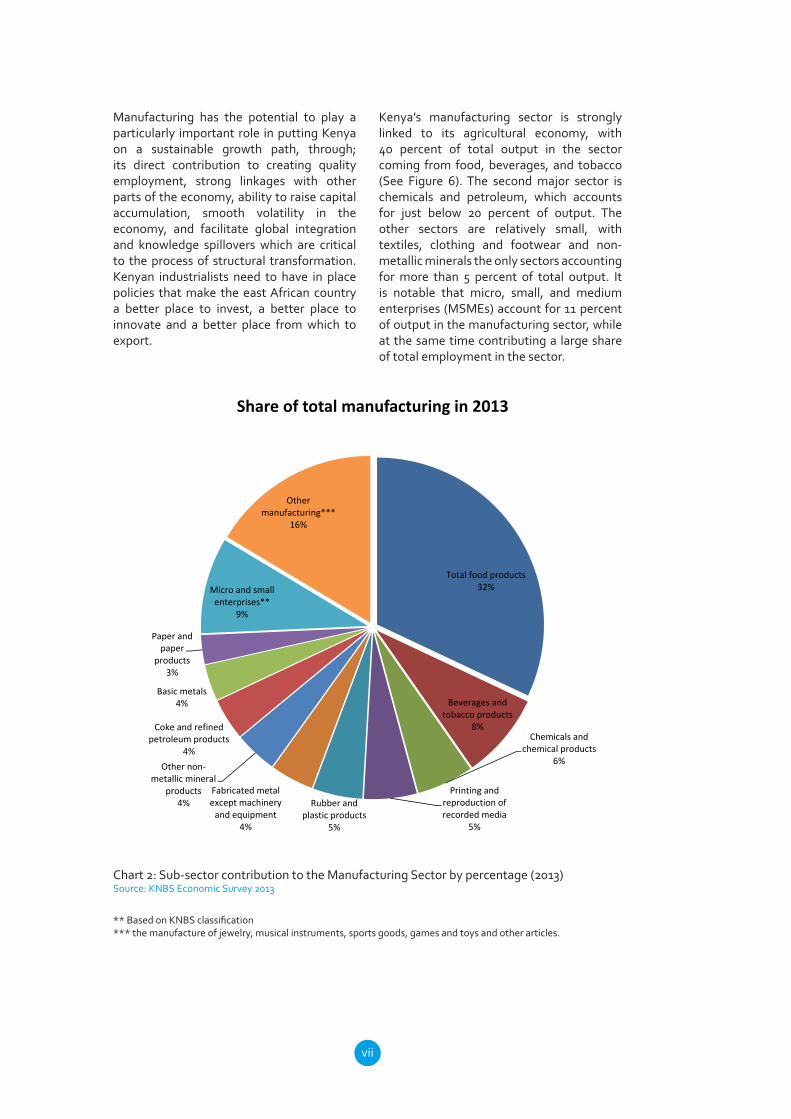

Kenya’s manufacturing sector is strongly linked to its agricultural economy, with 40 percent of total output in the sector coming from food, beverages, and tobacco (See Figure 6). The second major sector is chemicals and petroleum, which accounts for just below 20 percent of output. The other sectors are relatively small, with textiles, clothing and footwear and non-metallic minerals the only sectors accounting for more than 5 percent of total output. It is notable that micro, small, and medium enterprises (MSMEs) account for 11 percent of output in the manufacturing sector, while at the same time contributing a large share of total employment in the sector.

Chart 2: Sub-sector contribution to the Manufacturing Sector by percentage (2013) Source: KNBS Economic Survey 2013

**BasedonKNBSclassification*** the manufacture of jewelry, musical instruments, sports goods, games and toys and other articles.

viii

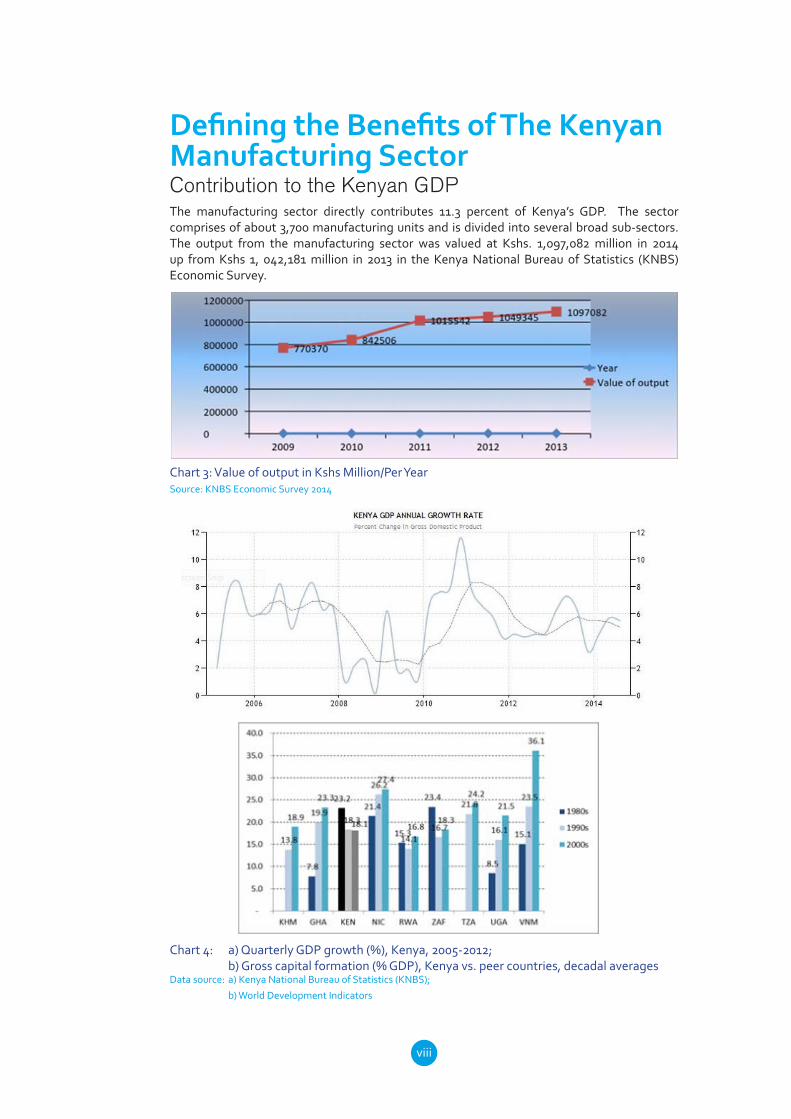

Chart 3: Value of output in Kshs Million/Per Year Source: KNBS Economic Survey 2014

Chart 4: a) Quarterly GDP growth (%), Kenya, 2005-2012; b) Gross capital formation (% GDP), Kenya vs. peer countries, decadal averages Data source: a) Kenya National Bureau of Statistics (KNBS);

b) World Development Indicators

Defining the Benefits of The Kenyan Manufacturing SectorContribution to the Kenyan GDP The manufacturing sector directly contributes 11.3 percent of Kenya’s GDP. The sector comprises of about 3,700 manufacturing units and is divided into several broad sub-sectors. The output from the manufacturing sector was valued at Kshs. 1,097,082 million in 2014 up from Kshs 1, 042,181 million in 2013 in the Kenya National Bureau of Statistics (KNBS) Economic Survey.

ix

Contribution to job creationThe Manufacturing sector employed over 280,300 people directly in 2013 up from 271,000 people in 2012. The informal sector contributes a further employment of 1.6 million people.

Chart 5: Employee Compensation in Ksh Million/ Per Year Source: KNBS Economic Survey 2014

Value Addition by the manufacturing sectorThesectorofferssignificantmultipliereffectsthrougheconomywidelinkages.Forexample,more than 25 percent of output in Kenya’s transport sector is used as an input to other domestic sectors,includingmanufacturing.Manufacturingfirms,especiallythoseintheagroprocessingsector, source critical inputs from the agricultural economy.

Chart 6: Manufacturing value added in Ksh Million/ Per Year Source: KNBS Economic Survey 2014

x

Chart 7: Value of Total Exports and Imports to African Countries

Contribution to Public FinanceGiventhefiguresaboveitisclearthatthemanufacturingsectoralsomakesahugecontributionto the tax revenue in terms of income tax receipts from employees, social security contributions andcorporationtaxleviedonprofits.

In 2012, Kenya collected Kshs. 93.3 billion in excise taxes, up from Kshs. 69.9 billion in 2009. It is estimated that additional government revenue will be raised from the manufacturing sector’s supply chain and through taxation of the activities supported by the spending of employees working in the manufacturing sector and its supply chain.

Consumer Benefits of ManufacturingThe manufacturing sector produces a variety of goods. This is of great benefit to localconsumerssincethegoodsareofhighquality,affordableandeasilyavailable.Buyinglocallymade products is a source of great pride to Kenyans since it eases reliance on imported goods. Imported goods are not always up to standard and can sometimes be counterfeited.

International Trade and Foreign Exchange earningsAbout two thirds (or 66 percent) of goods/commodities produced by the manufacturing sector in Kenya are consumed locally while the remaining third are exported. Overall, exports in 2012 increased by 12.2 percent to reach US$ 9.4 billion (23.2 percent of GDP), up from US$ 8.4 billion (24.9 percent of GDP), in nominal USD terms. The African market is the largest destination of Kenya’s exports taking up 48 percent while 26 percent of our goods go to the East African Community. The European Union is Kenya’s second main trading partner and accounts for 24 percent of Kenyan exports, of which 7.8 percent go to the UK1.

InvestmentThe Kenyan manufacturing sector has attracted both local and international investors through Foreign Direct Investment (FDI) and joint ventures. The manufacturing sector, particularly within global production networks, provides domestic firms andworkerswith exposure toforeign technology and knowledge. This may come through foreign direct investment in the sector, through the import of capital equipment embodying foreign knowledge, exporting to internationalbuyers,orcompetingwithforeignfirmsinregionalandglobalmarkets.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

South Africa

Rwanda Egypt Tanzania Uganda Burundi Other

Exports

Imports

1 Manufacturing Survey 2012. A survey of the Manufacturing Sector in Kenya (2012). Nairobi: Kenya Association of Manufacturers.

1

The manufacturing sector grew by 4.8 percent in 2013 compared to 3.2 percent in 2012 as given in the country’s rebased statistics released last year. This was against an expected growth of 10 percent per annum targeted in Vision 2030. Manufacturers rely on a stable, balanced and common-sense regulatory environment to create jobs and fuel economic growth. However, the burden of unnecessarily costly and duplicative rules weighs heavily on ability for the sector to grow and create jobs. To secure investment in the manufacturing sector, there is need for Government to guarantee investors a stable policy environment and provide an investment climate that facilitates the growth of industry.

Recommendations Policy stability for investment: The

regulatory environment should be stable to support long term investment and should be enforceable. Implementation or enforcement of regulations should be similar across the board without fear or favour. The implementers should be knowledgeable of the business environment and realities and have the ability to enforce the law and introduction of any new regulations should be done in consultation with industry. Legislations should also be fair and give a win-win outcome for all stakeholders because policy stability within the region is critical for all businesses.

PILLAR 1: SECURING INVESTMENT

2

1. The Government should commit to having policies in place for a given time period, forexamplefiveyears,toenable long term planning and investment by industry.

2. All laws should be supported by government policy. In many cases, County governments draft laws without policy guidance.

3. There should be a review of lawsandpoliciesaffectingbusinesstoreflectthecurrentbusiness environment and needs such as the Contract Law, VAT Act, Income Tax, Public Procurement and Disposal Act, Companies Act, Land Laws and Labour Laws.

4. Taxation that promotes industrialisation: Taxation structures nationally and regionally should support manufacturing by local industries. We currently have a structure that supports imports and not local manufacturing where finishedproductsandrawmaterials attract the same VAT rates. The taxation policy should ensure that where finishedproductsareexempt,input towards manufacturing a similar product locally should be exempt or zero rated to make locally manufactured products competitive.

i. Value Added Tax

a. The VAT Act 2013 to be reviewed to resolve any anomalies that would make imports cheaper than locally manufactured products where there is local capacity to manufacture.

• Identify key industries which manufacture products wherethefinishedproductisVATexemptandtherawmaterials for manufacture of the same product are vatable (16%).

• Gazette the same for the purposes of administration and audit of the scheme.

b. VAT refund backlog is cleared and a queuing system is developed with timelines for accruing refunds.

ii. Elimination of Import Declaration Fee for Industrial Goods

Eliminate IDF on industrial raw materials, plants machinery & equipment to make Kenya more competitive and thus a preferred investment destination. Currently, Kenya charges Import Declaration Fee (IDF) of 2.25 percent while Tanzania charges 1.2 percent and Uganda 0.8 percent, respectively.

iii. Tax Procedures & Excise Tax Law

The conclusion and implementation of the Tax Procedures and Excise Duty Bill 2014 should be expedited. The Bill is anticipated to simplify the process of tax assessment and payment. Currently Kenya has 41 business taxes enforced under 16 different taxregimes. This makes Kenya a high tax yield country with tax revenue to GDP ratio of 1:5.

iv. Income tax

The review of the Income Tax Bill should be expedited.

v. Facilitative Revenue Authority

Kenya Revenue Authority (KRA) is responsible for maintaining the trade eco-system by facilitating trade without compromising any of its fundamental roles of collecting, controlling and managing of taxes. KRA being the key custodian of tax policy implementation should be facilitative to business and conclusively address all the challenges currently being faced by business to reduce cargo turnaround time due to delays at the port.

• Streamline the function of trade and industry within the Government: Government structures should support industrialisation and trade by centralising industry issues under one Ministry as far as is possible in order to facilitate the industrial sector.

Quick WIN

Quick WIN

3

1. The Government should create a One Stop Shop as a clearing house for issuesaffectingindustryunderoneMinistry.

2. AllissuesaffectingindustryshouldbecoordinatedbythesameMinistry.

3. ThecreationoftheOfficeoftheRegistrarofIndustriestocollateinformation and data about industry and its subsectors would contribute tomoreefficiencyinindustrialresearchandsupportfact-baseddecisionmaking nation wide.

• Streamline Regulatory Institutions to avoid duplication of roles: Regulations and regulatory frameworks are important to address or prevent three market failure problems: natural monopolies, inadequate consumer information, protection of the common good and considerations of equity and protecting the poor. Although effectiveregulation is important for proper functioning of businesses especially where there are many enterprises of small or medium sizes, regulations can also become burdensome and hinder enterprise growth. Regulations becomeburdensomewhen theyare;many,difficult toadministerandcomply with and when similar regulations are administered by more than one agency.

• In addition to many regulatory agencies, there is a duplication of roles and mandates of the implementing institutions. This leads to numerous visits to industrial firms by public officials from these institutions anddiscouragesfirmsfromcomplyingwiththesame,providinganavenuefor extortion and bribes by public officials. Manufacturing firms inKenya, like in many developing countries, are required to obtain licenses and pay various fees in addition to meeting other business regulatory requirements. While the need for regulations is appreciated, the nature and the manner that these regulations are administered may lead to onerous regulatory regimes which could in turn discourage investors due to the increase in the cost of doing business. Regulators should facilitate business and reduce overlaps in regulations that are in some cases a hindrance to doing business. To maintain the manufacturing momentum and encourage hiring, the Kenyan Government needs policies more attuned to the realities of global competition. Our regulatory system produces unnecessarily costly rules, duplicate mandates, and impediments to innovation and barriers to our international competitiveness. If we are to succeed in creating a more competitive economy, we must reform our regulatory system so that manufacturers can innovate and make better products instead of spending hours and resources complying with manifold inefficient and burdensomeregulations. Manufacturers are committed to adopting international best practice and regulatory reforms that protect the environment and ensure public health and safety, while also promoting economic growth and job creation. The time has come for members of both parties to work together to reform our regulatory system.

Quick WIN

4

Corruption: Corruption and bad management practices eat into the nation’s wealth, channeling money away from public projects and the people most dependent on Government support. Countless studies have shown that corruption can interrupt investment, restrict trade, reduce economic growth and distort the facts and figuresassociated with Government spending. Corruption also harms the chances of success for small and micro enterprises and it has been demonstrated that around the world, small businesses pay more than twice as much of their earnings as larger companies, limiting their ability to grow and create jobs.2 The elimination of opportunities for corruption by reforming institutions to minimize discretion is crucial and appropriate checks and balances are needed. Secondly, the government needs to be able to detect corruption when it occurs and this requires strong auditing mechanisms. The new Constitution strengthens checks and balances as well as the independence of oversight agencies, so it will help in this area as well. Thirdly, government needs to punish corrupt individuals to the full extent of the law.

2 Corruption Watch, http://www.corruptionwatch.org.za/content/about-us-0 retrieved on 23 January 23, 2015

Quick WIN

Quick WIN

1. The recommendations of the Presidential Parastatal Reform taskforce report should be implemented and the overlapping regulatory roles be streamlined.

2. The streamlining of overlapping regulatory roles of devolved functions between County and National Government should be expedited.

3. There is a need to address overlapping regulatory roles including:• Appraising the approval process for

importation of industrial inputs such as refined sugar, spare parts, Foodhandler certificates regulated byKEMRI and the County Governments..

•FoodhandlercertificatesregulatedbyKEMRI and the County Governments.

• Standards on water and sanitation regulated by NEMA, KEBS and WARMA.

• Regulation of disposable medical - Pharmacy and Poisons Board, Nursing Council of Kenya and KEBS.

• Regulation of GMO issues by the - National Bio-Safety Authority, the Ministry of Agriculture and KEPHIS.

• The health requirement in the textile and apparel sector is not necessary as it can be adequately covered under NEMA Environmental Audit.

• The conservancy fee charged by some County Governments for the wood and furniture sector should be waived because the Kenya Wildlife Service (KWS) imposes similar charges.

• The waste transport license, disposal license, incinerator and waste quality affluentdischargeareallregulatedbyboth County Government and NEMA. This results in double taxation.

1. Thereshouldbezerotolerance,stiffpenalties for corruption cases and leadership by example.

2. All processes should be automated

3. More consumer awareness should be created.

5

PILLAR 2: SECURING MARKETS The BUY KENYA, BUILD KENYA Initiative and EXPORT COMPETITIVENESS

Markets are central in the development of the manufacturing sector. In order to grow the sector, for the increased purchase of locally manufactured products by the Kenyan Government, private sector and citizens cannot be overlooked. In encouraging imports we are actually creating jobs in foreign countries and draining our foreign revenues. ‘A Buy Kenya; Build Kenya’ philosophy needs to be inculcated in the minds of all Kenyan citizens.

In Kenya, exports would enable the country to effectively deal with the fiscal andmonetary challenges as it reduces the current reliance on domestic consumption as a major economic driver. Kenya maintains an open trade policy and is export oriented. This must be safeguarded and further enhanced. The government should actively pursue initiatives to grow and diversify Kenyan exports.

RecommendationsPublic Procurement -Affirmativeaction inpublicprocurementfor local industrialproductsby government agencies and the public support for Kenyan products is needed. The Public Procurement framework should boost industrial growth in line with Vision 2030 by giving primary preference and reservations to what is procured. Secondary preference and reservations should go to the contractor hence boosting locally produced goods and services in the spirit of ‘Buy Kenya Build Kenya’ policy.

6

Quick WIN

Local Content: Trillions of dollars of goods and services will be procured over the next ten years in prospecting for oil, gas and mineral resources around the globe. Billions of Kenya shillings will also be spent on large infrastructure projects by Government. Over the same period, more money will be spent on goods and services procured by public and privatecompaniesandofficialdevelopmentagencies to construct water, power, buildings and transportation infrastructure and to purchase associated manufactured equipment and components. It is critical that asignificantproportionofthis expenditurebenefit local labourandproducers inKenyaand utilize local content.

1. Thereisneedforfinalisationofthe policy and the enactment of legislation on local content that promotes utilisation of locally produced goods and services by private companies contracted by Government for mining exploration and huge infrastructural projects.

2. A local content Committee should be established to monitor compliance on local content.

3. The monitoring of local content compliance for ongoing projects like Standard Gauge Railway for the 40% by value material content should be implemented.

The Fight against Illicit trade, fakes and substandard goods: From the 2013 enterprise survey conducted by the World Bank, one out of four private sector firmsin Kenya considers informal competition as the biggest obstacle. The improvement ofafirms’experience indealingwithcrimeandfinancial services is consistentwith thechangeofafirms’perceptionofthebusinessenvironment. The percentage of firmschoosingaccesstofinanceandcrimeasthemost important obstacle for their day-to-day operations declined significantly from 2007to 2013. The same holds for tax rates and transportation related obstacles. Currently, the practice of competitors in the informal sector is most often chosen as the top obstacle. About 24 percent of firms chosethisobstacle in2013,afigurethat isalmosttwice as high as in 2007.

Quick WIN

1. The Public Procurement Act should be reviewed to ensure that the law isclearonthedefinitionofa‘localmanufacturer’ vis a vis a ’locally registered company’ and this review should be implementable to promote preference for local products.

2. A monitoring mechanism needs to be put in place to track compliance in preference for local products in public procurement by Government.

3. An annual Kenya’s Manufacturing Expo should be organised in partnership with Government Procurement Entities to source for locally manufactured goods under the “Buy Kenya Build Kenya Initiative”.

7

Quick WIN

The east African region losses between US$500 and US$ 600 million per year on trade in counterfeit goods. In 2012, KAM carried out an inaugural study on the impact of the counterfeit menace and established that KenyanManufacturers(firms)werelosing40percent of their market share to counterfeit products in the market. The Confederation of Tanzania Industries estimated a loss of 15 percent to 25 percent in revenue per annum. The value of illicit trade and primarily the sale of counterfeit goods, is estimated at US$ 650 billion worldwide.

Review of Anti-Counterfeit Act and AgencyA review of the Anti- Counterfeit Act 2008 to create a more responsive Agency with adequate resources and mandate is required.

Review of the ACA and overhaul to make it an effective agency for inter- agencycollaborationandintroducestiffermonetarypenalties, deportation of aliens, and forfeiture of assets is urgent. We recommend that as ACA merges with KCB and KIPI due diligence must be done to raid the entity of the unqualified and non-performingelements if the fight against counterfeitgoods has to have any meaningful impact. In addition the following should also be done;

Implementation of Enforcement Manual Against Illicit Trade Improve inter-agency collaboration through the implementation of the ‘Enforcement Manual to combat Illicit Trade’. The Anti-counterfeit Act, 2008 invokes appointment of inspectors across a number of agencies for the purposes of combating the menace from various fronts. This is yet to be implemented.

Consumer AwarenessThe Government should create consumer awareness on counterfeit goods in partnership with manufacturers. Consumer awareness, as one way of combating

counterfeiting, is a core mandate of the Anti-Counterfeit Agency as stipulated by the Anti-Counterfeit Act, 2008. The Agency must be held accountable for delivering on its mandate.

Use of ICT to curb illicit trade Capitalize on the use of ICT and develop applications for law enforcement officersand consumers to assist in detection of Best practice in the use of ICT in the fightagainst counterfeits in developed and many industrializing countries includes; use of Holograms, markers and tracking devices and efficient relay of information. Kenya(manufacturing industry and ACA) cannot affordtoloseoutonthisfront.

1. A review of the Anti- Counterfeit Act 2008tointroducestiffermonetarypenalties, longer jail terms, deportation of illegal immigrants, and forfeiture of assets is urgent.

2. The Implementation of the ‘Enforcement Manual to combat Illicit Trade’ which was published last year would improve inter-agency collaboration and ensure Judiciary determines cases brought before them expeditiously.

3. The Government in partnership with manufacturers needs to create consumer awareness on counterfeit goods and capitalise on the use of ICT for consumers to assist in detection of counterfeit goods in the market.

8

Quick WIN

Access to the EAC MarketImplementation of the EAC Single Customs Territory and Common Market

Figures from the 2014 Economic survey indicate that Kenya’s exports to the East African Community have reduced by a staggering 7.4 percent from about Kshs. 134 billion in 2012 to Ksh 124 billion in 2013. Kenya’s exports to Tanzania reduced from Ksh 46 billion to 40 billion in 2013 while exports to Uganda reduced from Ksh 67 billion to Ksh 65 billion and to Rwanda from Ksh 16 billion to Ksh 13 billion. On the other hand, our Partners’ states are quickly improving their industries and local supply. These can be attributed to trade policies that are supportive to industrialization, an area that adversely affects manufacturing.These policies allow for zero tariffs on rawmaterial for manufacturing over and above the provisions of EAC Customs Management Act (EACMA). Non-tariff barriers; such aslack of recognition of the EAC rules of origin certified by the Kenya Revenue Authority,restrictive trade requirements by regulatory bodies like the Tanzania Foods and Drugs Authority (TFDA), numerous levies and charges including discriminatory excise duties and red tape at border points.

Promoting export competitiveness: Misinterpretation of article 25 of EAC protocol, which states: ‘The treatment provided for under article 25 is being applied to a company rather than to the goods which then subjects goods manufactured using duty paid raw materials to attract 25% import duty rather than zero duty’ has been problematic for manufacturers. This means that for goods manufactured from raw materials, duty paid on these goods shall not attract Common External Tariff (CET)rate but rather the preferential tariff ratesbased on rules of origin. The EAC should work at enhancing the capacity to manage the scenario described above but not floutthe protocol in the name of a lack of capacity to reconcile records and thereby imposing duty on Kenyan manufactured goods. A uniform application of the law, for EAC goods enjoying export promotion incentives and sold within the EAC market and for those outside the EAC market, is necessary in order to have a level playing field for allmanufacturing industries in the region.

1. The Amendment of Part F of the Customs Union Protocol on Export Promotion Schemes to provide for manufacturing for Local Market and for Export should be done. Kenya needs to fast track the gazettement and implementation of the revised EAC Rules of Origin adopted by the Council of Ministers in November 2014.

Quick WIN

1. Kenya should spearhead the streamlining of export procedures within the EAC to ensure that there ismutualrecognitionofcertificatesand documentation within EAC.

2. The establishment of a regular monitoring, evaluation and review mechanism by Kenya to ensure that the Single Customs Territory and EAC Common Market is working for Kenyan industry should be expedited.

The country should also champion the establishment of the EAC Regional Printers located at the EAC headquarters to expedite the publication of regional laws and regulations.

9

Quick WIN

Review of CET in EAC to promote manufacturing: The current Common External Tariff (CET) in the EAC needs tobe reviewed. Currently, there are more exceptions to the rules with numerous stays of application sought by EAC Partner States. OneofthebenefitsenvisagedintheCustomsUnion is increased intra-regional trade through the elimination of tariff barriers.However, this has not been fully realised. Various anomalies exist in the current EAC CET that should be addressed holistically once and for all. They occur in the form of import duty rates that may not conform to the three band structure of raw materials, intermediate products and finishedproducts. Items included in the sensitive list also account for distortions in the CET and need to be reviewed. KAM has in the past tackled these anomalies through the annual budget process which has led to the review of various CET rates for short term periods (for example, one year) and others for the long term (as is the case for paper sector). In other instances, items set aside as sensitive attract higher duty rates than provided for in the current three band structure of the EAC CET. These challenges have led to the high cost of manufacturing for these products whoseinputsaresubjecttohightariffsandahigher cost of essential consumer goods and dependency on imports, which are cheaper than other similar goods.

1. Kenya should promote the implementation of the EAC CET that encourages the development of the industrial sectors’ value chains and tariffdifferentialsforexample,juiceconcentrates and paper.

2. For a 2015 CET Review, Kenya has to identify and correct any anomalies existing in the EAC CET. KAM will work with the Government to identify and provide such anomalies.

A gradual consolidation of the items in the sensitive list into the three band tariffstructure to avoid member states coming up with their own individual sensitive lists is necessary. This will create a level playing fieldforallmanufacturersintheregion.

Access to other MarketsExpansion of markets: The expansion of the external market through the conclusion of regional, bilateral and other trade agreements and special arrangements that will deliver such markets. These include; the Tripartite Free Trade Area Agreement, the AU Continental Free Trade Area Agreement (CFTA), Implementation of Economic Partnership Agreements between EU and EAC, implementation of the Special Status Agreement between Kenya and Ethiopia, and the conclusion of Bilateral Preferential Trade Agreements between Kenya and othercountries.Thereisalsoneedtofinaliseon double taxation agreements with key economic partners. Small and medium-sized businesses often lack the know-how and capacity to meet the requirements of formal trading across borders. Even mid-sized companiesoftenfindaccess to informationand financial resources difficult, which arenecessary to adjust to the price, quality, and safety standards in new markets. Measures need to be put in place to assist with access to information and support transparent procedures of formalization, such as licenses and standards.

10

Quick WIN

1. The conclusion of a business friendly Tripartite (COMESA, EAC, and SADC) Free Trade Area should be fast tracked.

2. Export expansion grants and the Export Development Fund need to be established tofinanceexportpromotionandrelatedactivities.

3. Support for entrepreneurs to enter new markets through various support such assectorspecificmarketsurveysandinformation,incubationprograms,cheapfinancingofservicingexportsordersandproductdevelopmentandimprovingcompetitivenessatthefirmlevelwouldpromoteentrepreneurshipinthecountry.

4. The implementation of the Special Status Agreement between Kenya and Ethiopia and the Bilateral Agreement between Kenya and Nigeria has been lagging and it needs to be fast tracked.

5. Kenya supports the AU initiated Continental Free Trade Area negotiations.

6. The conclusion of Trade Agreements with additional markets in Africa and the Gulf States such as the DRC, Congo Brazzaville, UAE and Ghana among others.

11

PILLAR 3: SECURING INFRASTRUCTURE

Due to the key role that the provision of energy plays, the cost of the products from a manufacturing process are related to the cost of energy, other factors such as efficiency of production, cost of labor andraw materials notwithstanding. The higher the cost of energy, the higher the price of the products. The cost per unit of electricity in Kenya is high and volatile depending on the amount of thermal energy in the system which is susceptible to changes in international oil prices. In 2013, industry witnessed an increase in prices which will subsequently rise by up to 25 percent by the endof the tariff reviewperiod inJuly2015.The current cost and quality of electricity is discouraging new investments and constraining the expansion of industries. This isworsenedby frequentpowerfluctuations

and unscheduled interruptions and is a cause of lost time and equipment damage due to poor power quality. Forward planning which is crucial in an industrial firm is virtuallyunattainable in conditions of unpredictable power supply.

We acknowledge that a lot has been done by the current government to increase energy supply and stabilize it. Still, the country is not yet energy secure and capacity expansion has not kept up with demand. In Kenya, over 60 percent of energy generated into the national grid is used in manufacturing enterprises. Kenya needs to generate up to 41,300 MW of energy by 2030 and we need to look at all new sources. Added to the challenge of inadequate supply is the quality issue. Industrial investors experience losses

12

Contribution to Kenyan GDPContribution to Job CreationValue addition by the Manufacturing Sector

SECURING INDUSTRY IN KENYA FOR SHARED PROSPERITY

PILLAR ONESecuring Investment

• Policy stability for investment

• Taxation that promotes industrialisation

• Streamlining the function of trade and industry within the Government

• Streamlining Regulatory Institutions to avoid the duplication of roles

• Fighting Corruption

PILLAR TWOSecuring Markets – by

buoying the ‘Buy Kenya, Build Kenya’ Policy and Export Competiveness

Expanding the local market•Public procurement and

local content policies that support local manufacturing

• fightingagainstillicit trade, fakes and substandard goods

Expanding the EAC Market • Implementation of the

EAC Single Customs Territory and Common Market

• Promoting export competitiveness

• Review of CET in EAC to promote manufacturing

Expanding external markets

PILLAR THREESecuring Infrastructure

• Energy

• Water

• Transport and Infrastructure

• Land for Investment

PILLAR FOURSecuring

Constitutional Gains

• Elimination of Double Taxation

• Facilitiation of inter county trade through harmonised country revenue laws

Focus on agro processing as a dey driver for industrial growth

13

SECURING INDUSTRY IN KENYA FOR SHARED PROSPERITY

PILLAR FOURSecuring

Constitutional Gains

• Elimination of Double Taxation

• Facilitiation of inter county trade through harmonised country revenue laws

PILLAR FIVESecuring Justice for the Economy

• A judicial system awake to commercial realities.

• Faster resolution of commercial disputes

PILLAR SIXSecuring Security

• Curbing rampant insecurity and the creation of safer communities

• Crime prevention

• Restoration of Investor confidence

• Cheaper security costs

PILLAR SEVENSecuring the

Future of Industry

• Support for Small and Medium Enterprises (SMEs)

• Renewed strategy in the establishment of Special Economic Zones (SEZs), Export Processing Zones (EPZs) and Industrial Parks.

• Education and training

• Promotion of Innovation

Focus on agro processing as a dey driver for industrial growth

International Trade and Foreign exchange earningsConsumer benefits of ManufacturingContribution to Public FinanceInvestment

14

duetopowersupplyqualityfluctuationsandinterruptions and the majority have been forced to invest in generators which are costlytoobtainandoperate.Industrialfirmsestimate that power interruptions cost them about 7 percent of sales annually.

Transport is a factor that impacts on cost of goods and services. Kenya uses fivedominant modes of transport, that is, road, rail, water, air and pipeline. Road transport is by far the largest mode of transport with a share of over 70 percent of the transport sectoroutput.Airtransportisalsosignificantwith a share of 18 percent, while water and pipeline account for 4 percent and 2 percent respectively. The share of rail transport in total transport output is insignificant. TheGovernment is currently constructing the Standard Gauge Railway which will improve efficiency and hopefully reduce the cost oftransport by rail.

The port of Mombasa on the Kenyan coast plays a strategic role in trade facilitation both for Kenya and the neighbouring countries, three of which are landlocked. Manufacturers’ in particular face numerous challengeswithinefficientportperformanceand hold the view that Mombasa port performance, transit costs and procedures lie at the heart of the logistics supply chain. The launch of the Lamu Port and South Sudan Ethiopia Transport Corridor project (LAPSSET) in March 2012 is welcome due to its great potential to further link Kenya up with the region bolster trade. The plan must receive the requisite investment to achieve this.

RecommendationsEnergy: Globally, one in five people lackaccess to electricity. Providing electricity access to these 1.3 billion people is paramount to reducing poverty, driving economic development and improving social equality. A comparison of the electricity costs between Kenya and key competitor countries like China, India and South Africa, shows that Kenya is quite un-competitive on cost and the quality of power.

The government should continue with plans to increase energy security through investment in least cost segment such as geothermal, renewable energy alternatives and other least cost energy sectors. The country should enhance exploitation of geothermal, solar, wind and biomass resources to supply at least 5,200 MW for domestic and institutional energy requirements by 2030. The Government has committed to deliver 5,000 MW by 2016 and there is need to deliver this promise while industry adjusts to the increased capacity and expands operations.

Water: Recently, the World Economic Forum (WEF) listed water scarcity as one of the three global systemic risks of the highest concern and assessment based on a broad global survey on risk perception among representatives from business, academia, civil society, governments and international organizations. Freshwater scarcity manifests itself in the form of declining groundwater tables, reduced river flows, shrinking lakesand heavily polluted waters bodies, but also in the increasing costs of supply and treatment, intermittent supplies and conflicts over

Quick WIN

1. An increase in public investment in electricity generation and the expedition of investment in transmission and distribution can ensure utilization of capacity.

2. Government should also encourage greater private sector investments in geothermal, renewable energy alternatives and other least cost energy sectors.

3. The establishment of clear rules for private generators’ “open access” to the transmission network should be set down in the energy policy.

15

water. Water shortage and pollution also poseaphysical risktocompanies,affectingoperations and supply chains. Energy generation for example requires water in large volumes. This is clear for hydropower, where water fuels energy generation. Beyond hydropower, large amounts of water are required for cooling thermal power plants, which generate 75 percent of global electricity supply. We need energy for pumping, storing, transporting and treating water; we need water for producing almost all kinds of energy. An increase or decrease in onewillimmediatelyaffecttheother.

As a water scarce country, the water supply is inadequate for industry and the standards and capacity of the water supply pipes are questionable due to the frequent bursts experienced in various locations. Climate change and a growing population are two indicators that Kenya and the whole African Content can no longer rely solely on traditional sources of water. Finding alternative water sources must be the priority for government.

Waste water management: The current supply from Nairobi City and satellite towns is at the moment 580,000 m3/day against a demand of 750,000 m3 /day. Demand on the other hand is estimated to reach 860,000 m3 /day by 2017 and 1.2M m3 /dayby2035.Given thesefigures, largeandsustained investments in expanding water supply are required. Even if 20 percent of supply of water ends up as waste water, the potential volume of wastewater may rise from 116,000 m3 /day to 172,000 m3 /day by 2017 and to 600,000 m3/day by 2035 – which is equivalent to today’s supply. Kenya needs a very pragmatic policy and regulations to encourage the use of wastewater.

Current sanitation situation: According to a desk study carried out by the Water and Sanitation Program, it is estimated that poor sanitation costs the country Ksh 27 billion shillings (US$324 million)3 annually. The newly adopted Kenyan Constitution has

spelled out sanitation as a human right and there is need to urgently address sanitation challenges in Industrial Area and other parts of the country.

1. The amendment of the Water Bill to streamline management of water by reducing the multiple water regulatory bodies.

2. The state or county water recycling strategy and policy must be part of development planning.

3. The establishment of elaborate effluentwatertreatmentplantsandtheir proper operation as provided for in Water Policy.

4. There is need to expand waste water and sewer infrastructure especially in Industrial Area as the sewer system is inadequate to manage the current population and industries.

5. The Government needs to provide incentives to Industries that treat andre-usetheireffluentwaste.KAM can facilitate the process by providing Government with namesoffirmsthatundertakesuchtreatment of waste water.

Transport infrastructure: We acknowledge that there is significant effort towardsthe improvement of infrastructure which includes the development of the Standard Gauge Railway, the Mombasa port expansion with 20 Berths coming on board soon, the expansion of airports and construction of roads. Kenya needs to continually improve port infrastructure, customs processes and the capacity to track and trace freight goods. This will improve efficiency ofport or airport supply chains reduce costs

3 Up-scaling Basic Sanitation for the Urban Poor in Kenya http://www.afriwater.org/sanitation/186-up-scaling-basic-sanitation-for-the-urban-poor-in-kenya retrieved on 23 January 2015

Quick WIN

16

and save time for improved efficiency oftrade for manufactures. By developing road, rail, air and maritime transport infrastructure, as well as the energy supply and telecommunications systems, service flows to manufacturing will also improve.The collection of revenue for improvement of infrastructure should be ring fenced to ensurethatitdeliversthedesiredbenefits.

so from the respective Cabinet Secretary or the County Executive Committee Member and to ensure that the land owner is fully compensated for such an acquisition. This power should be exercised in instances where the Government’s focus is to increase local industries for the growth of the country’s economy. The same idea should also be used in all the counties such that specific areasin the counties are set aside as land for the establishment of industries. For towns with industrial areas, such areas should be strictly used for industrial purposes and more land sourced for industrial expansion.

Currently the major way to access to industrial land is purchase of agricultural land and conversion through the ‘change of user’ process. Expecting industrialists to get land through the market makes it very expensive andaffectsplansforde-concentrationfromthe main industrial towns of Nairobi.

According to Article 65 of the Constitution of Kenya, 2010, a non-citizen or a company not fully owned by Kenyans cannot hold title to land for any tenure exceeding 99 years. Article 65 (3) of the constitution further provides that, a company or a body corporate shall be regarded as a citizen only if the same is wholly owned by one or more citizens. It is not enough that the body corporate is partially owned by a Kenyan, it must be wholly owned by a citizen. Clear regulations for the operationalisation of Article 65 are needed to ensure that investors have certainty when investing in the Country.

Land for investment: Access to land remains one of the gravest hindrances to new investment in industry and it is critical for counties and national government to build land banks for industrial investment. The country should use compulsory acquisition and zoning to build land banks. The new Land Act No. 6 of 2012 in Part VIII bestows on the National Land Commission (NLC) power to compulsorily acquire land when necessary upon receipt of a request to do

Quick WIN

1. The Implementation of the Port Charter.

2. The commencement of the free port project at Mombasa Port.

2. The delivery of the Standard Gauge Railway in time with the involvement of the local sector for transfer of knowledge.

3. The commencement of the construction of an airport in Nakuru or Naivasha with well-constructed cold storage facilities for perishables to ease the burden of transportation of fragile products to export markets and concurrently promote tourism.

4. Theclearclassificationofroadsandthe authorities/bodies responsible for each road.

5. The prioritisation of road maintenance especially those with a high economic potential such as feeder roads to Agricultural productive and industrial areas. Quick

WIN1. The enactment of Regulations for

operationalisation of Article 65 of the Constitution to provide investor confidence

2. Governments at national and county level need to set aside and build land banks for industrial investors in key towns.

17

PILLAR 4: SECURING CONSTITUTIONAL GAINS

The Constitution of Kenya 2010 introduced the devolved system of Government. While devolution was meant to improve service delivery in the country, it has also brought about a number of challenges for Kenyan manufacturers because of the introduction of regulations unfavourable to businesses by county governments. Manufacturers are now confronted by double taxation where members pay similar charges and levies in more than one county, which is tantamount to a trade barrier or hindrance. As the main consumers of public sector services, the manufacturing sector is also very keen on good service delivery but only if county governments are more attentive to this key sector. The devolved government will also give powers of self-governance to the people and thus enhance participation of the local communities in making decisions on issues thataffectsthem.

The Government is mandated to secure gains to business under the Constitution of Kenya 2010. Businesses are the main actors in mobilizing and distributing wealth and

resources in a county. Article 209 (5) of the Constitution is very clear on this point;

“Taxation and other revenue raising powers of a county shall not be exercised in a way that prejudices national economic policies, economic activities across county boundaries or national mobility of goods, services, capital or labor.”

The promulgation of the New Constitution in August 2010 provides a strong legal foundation for the enhancement of participatory governance through devolved structures at county level.

The Fourth schedule of the Constitution gives counties the power to ensure and coordinate the participation of communities and locations in governance at the local level and in assisting communities and locations to develop their administrative capacities for the effective exercise of the functions,powers and participation in the governance at the local level.

18

RecommendationsFor devolution to work for business, facilitation of inter-county trade through inter-county consultations for harmonized County Revenue Laws for the smooth flowof goods and services within the Country is required. The Capacity Building of County Governments is also important to ensure compliance with the Constitution and other Devolution legislations. Centralized Revenue Administration for coordinated andimprovedcollectionefficiencyofcountyrevenues is necessary.

Enactment of County Revenue Laws There is need to enact all the relevant County Revenue Legislations in all the Counties. These include The Revenue Administration Law, Trade License Law, Rating Laws, Finance Laws and Public Participation Laws. KAM has worked with CRA to develop County Revenue Legislations for the County Governments which are Constitutional, which can improve revenue administration and maximize revenue collection and attract investment into the Counties. County Governments should also be assisted to develop tariffs and pricing policy for theprovision of public services as per Section 120 of the County Government Act.

National Framework for Constitutional and Harmonized Fees and ChargesThe development and institutionalization of a National framework on County Taxation and Business Licensing as an overarching guide for development of Revenue laws in the Counties. Article 209 (5). There is urgent need to invoke the provisions of the constitution on taxation and licensing to protect investments and encourage new ones to be established and to thrive anywhere in the country. Towards this end, appropriate legislation should be put in place to guide county governments of taxation and business licensing.

National Public Participation Policy and Law Enactment of a National Policy and Law on Public Participation for guidance to the National and County Government on the parameters that meet the constitutional threshold. There is need to put in place legislation to guide national and county governments on public involvement (particularly when coming up with policy or legislation of any form), as provided for in the constitution.

County Industrialization Policies and Audit of county performance on business facilitationA national industrialization Conference for the Council of Governors is proposed during which the Industrialization Agenda will be shared between the National and County Governments. We propose an annual audit and scorecard of County performance on business facilitation.

Quick WIN1. The development and

institutionalization of a National framework on County Taxation and Business Licensing as an overarching guide for development of Revenue laws in the Counties.

2. The enactment of a National Policy and Law on Public Participation to provide guidance to the National and County Government on the parameters of public participation that meet the constitutional threshold.

3. The development and enactment of the County Government Printers Bill inordertoimproveefficiencyandavailability of information from the Counties.

19

PILLAR 5: SECURING JUSTICE FOR THE ECONOMY

While it is true that judges need to be protected from outside influences whichcould bias their decision, even unbiased decisions must accurately interpret the law. Inaccurate or well-meaning decisions which fail to appreciate commercial realities and implicationswilldecreaseconfidence inthelegal system and increase uncertainty in economic activity. Also, accuracy alone is insufficient for a high quality court system.Disputes need resolution and decisions rendered in a timely manner so as to provide investors with the security and certainty necessary to promote investment. Thus, the judicial system must not only be impartial, it mustbeaccurateandefficientaswell.

The businesses in a jurisdiction should not lose confidence in a court system thatabandons a perceived forum for the rational andefficientresolutionofbusinessdisputesby seasoned and knowledgeable jurists. They has a fundamental role to play in dispensing justice and balancing the interests of various stakeholders in commercial disputes. In this regard, the courts can subtly achieve a paradigm shift in the handling of business disputes by using their powers to interpret and apply the law and to make rules.

20

RecommendationsThe judiciary should facilitate the resolution of business or commercial disputes in a quick, efficient and effective manner to ensurethat judiciaries in effect become a catalystfor economic growth. The courts have to be innovative and adopt best practices to fulfilltheirobjectiveandroleincontributingto investor confidence, promoting soundbusiness practices and the resultant economic growth.

Quick WIN

1. The establishment of the Business Court Users Committees for a focused discussion on the challengesaffectingthebusinesscommunity

2. The establishment of Alternative Dispute Resolution (ADR) mechanisms in partnership with business for speedy resolution of disputes.

3. Strengthening of the Intergovernmental Budget and Economic Council (IBEC) through legislation so that it is able to deal moreeffectivelywithcross-countrytrade matters and issues.

21

PILLAR 6: SECURING SECURITY

According to the World Bank Enterprise Survey (ES) 2013, losses due to crime have declined since 2007 but security expenses have become more burdensome. The usage and cost of security services in Kenya have both increased between 2007 and 2013. More firmspayforsecurityandtheyalsopaymore:2% of total annual sales in 2007 vs. 4% in 2013. Security expenses are higher in Kenya than in other countries at the same income level and in all countries with ES data. More firmsinKenyapayforsecurityservicesthaneverywhereelse(82%offirmscomparedtoan average of 60% for low income countries). On the other hand, losses due to theft and vandalism as a percentage of total annual sales have declined and are currently at par with other low income countries.

Crime prevention can reduce the long term costs associated with the criminal justice system and the costs of crime, both economic and social, can achieve a significant returnon investment in terms of savings in justice, welfare, health care, and the protection of social and human capital. A safe and secure society is an important foundation for the delivery of other key services. Community safety and security is a prerequisite for sound economic growth through continuing business investment as well as community well-being and cohesion. International experience has shown that effective crimeprevention can both maintain and reinforce the social cohesion of communities and assist them to act collectively to improve their quality of life.

22

Rampant insecurity is detrimental to the economic growth and shudders economic opportunities for the people. Rampant insecurity affects investors’ confidenceand increases the cost of doing business as companies increase spending on security. Until rampant insecurity is arrested, Kenyan economy will suffer and economicopportunities for our people of Kenya will nosedive.

Recommendations There is need for the reorganization of the security apparatus in Kenya to restore investor confidence and end insecurity.A collaborative approach by all players in security is required as insecurity and crime cannot be tackled in isolation. The enhancement of security surveillance will lead to proactive crime prevention. An integrated approach to security that involves collaboration with business community will also go a long way in improving security

Quick WIN

2. The explicit coordination of National Security Agencies.

3. The implementation of community policing at urban and semi urban areas.

4. Use of modern technology to address critical security issues.

5. Promote structured PPPs in security management.

23

PILLAR 7: SECURING THE FUTURE OF INDUSTRY

The importance of the manufacturing sector in development has been globally acknowledged. In Kenya, the realization of the country’s long-term development policy framework, Kenya Vision 2030, whose goal is for the country to become a newlyindustrialisedeconomy,identifiesthemanufacturing sector as a key driver in the attainment of this goal. The sector is seen as an important pillar in the achievement of Kenya’s development. Indeed, it contributes significantly to wage employment as wellas to Kenya’s merchandise exports and accounts for a significant proportion of

informal employment within the small and medium-sized enterprise (SME) sector. The long term vision of the sector presented in industrial policy (Republic of Kenya, 2012) is to enable Kenya become a regional leader in industrial growth and development contributing to more than 15 percent of the annual national GDP.

There is need to secure the future of industry in order to achieve the desired growth in the sector by resolving key challenges that could lead to the rapid and sustainable growth of the sector.

24

Recommendationsa. Support for SMEsThe SME sector is the largest provider of employment in most countries, especially of new jobs, SMEs are a major source of technological innovation and new products. SMEs are the engine of growth. SMEs are essential for a competitive and efficientmarket. SMEs with high turnover and adaptability play a major role in removing regional and sector imbalances in the economy. Easy entry and exit of SMEs make economies more flexible and morecompetitive. A large number of SMEs creates competitive market pressure. SMEs also play an essential role as subcontractors in the downsizing, privatization and restructuring of large companies. SMEs are important for poverty reduction. SMEs tend to employ poor and low-income workers. SMEs are sometimes the only source of employment in poor regions and rural areas. Self-employment is the only source of income for many poor and SMEs play a particularly important role in developing countries where poverty is most severe. The establishment of a Small Business Administration under the Officeof thePresident toprovidefinancingand incentives for SMEs and monitor the implementation of the policies and legislations to promote SMEs will go a long way towards achievement of this goal.

b. Enactment of Prompt Payment legislation

There is need to enact legislation for prompt payment of businesses for goods and services supplied by SMEs. This legislation will provide interest penalties for late payments in order to cushion SMEs from late payments. Prompt payment is critical to the performance and operations of any business and more so that the small and medium sized enterprises (SMEs).

c. Preference and Reservation for SMEs

Promotion of SMEs through preference and reservation in public procurement.

d. Incubation centers for SMEsEstablishment of incubation centers for SMEs.

e. Training for SMEs which includes short practical courses such as4;

•Cash-flow Management, How to bidand Prepare tender documents, Export Preparation).

• Marketing and Exporting.

• Export Development Corporation (EDC) to inform of new markets & regulatory issues of imports and New Exporters’ Programme).

• Intellectual Property Management Training for SMEs.

• Corporate Governance for SMEs.

4 The Role of Government in Supporting Entrepreneurship & SME Development. (2011) Mohammed Bin Rashid Establishment For SME Development. DUBAI SME 2011

Quick WIN1. AffordablefinancingforSMEsector.

2. Promotion of SMEs through preference and reservation in public procurement.

3. Establishment of incubation centres for SMEs.

f. Renewed strategy in the establishment of Special Economic Zones (SEZ), Export Processing Zones (EPZ) and Industrial Parks.

25

Quick WIN

1. Enact an SEZ Bill that provides incentives for industries inside and outside zones to encourage domestic production and necessary backward and forward linkages and does not leadtoconflictingincentivesforplayers in and out of the zones.

2. Creation of Industrial Parks with supportive infrastructure.

3. Heavy investment in high technology value added products in designated EPZ areas.

4. Each County to establish an Industrial Park.

g. Education and training Kenya has a lot to learn in stepping up measures to harness technology, innovation, productivity and promoting linkages between industry and universities, polytechnic institutes and other training institutions. Improvement of policy on Research and Development (R&D), innovation, and technology utilization. The government must commit itself to delivering quality higher education that meets the requirements for industry and the growing economy by reviewing curricula to be demand driven, better adapted to latest industrial technology. National polytechnics and other technical training institutes need to have their infrastructure upgraded in order to meet the needs of industry. There is need to transform theoretical knowhow to practical usage.

Sufficient resources must be allocated toscience and engineering. Tax incentives to industry for investment in research and development to promote increased private-sector R&D through increased government spending on Research and Development in Industry through a R&D fund. Utilization of large infrastructural projects like Standard Gauge Railway and LAPPSET for transfer of skills and knowledge to Kenyans for future maintenance of the infrastructure and to open up opportunities to develop the same in other African countries.

Quick WIN

1. Review of Curriculum: Commence review of Educational curriculum to cure the mismatch between the graduants industry requirements. Review of the education curricula to respond to the changing needs of industry

2. Commence review of the National Educational curriculum to cure the mismatch between the grandaunts and the industry requirements.

h. Promote innovation In order to boost productivity, there is need for broad-based innovation and investment in knowledge capital. Innovation is the engine of the ‘creative destruction’ process that spurs economic dynamism and transformation and is at the centre of the development process. The Science, Technology and Innovation Act of 2013 is an attempt to improve on the STI institutional framework, in a bid to complement the policy goals of Vision 2030. The Act creates the Kenya Innovation Agency that is the implementation arm for the country’s STI agenda and policy, proposed by National Commission for Science, Technology and Innovation NACOSTI and funded by the Research Fund. It will institutionalize linkages between universities, research institutions, the private sector, the Government, and other actors. It will lead the creation of science and innovation parks, institutes or schools, or designate existing institutions as centres of excellence in priority sectors.

i. Review of CurriculumCommence review of the National Educational Curriculum to cure the mismatch between the granduates and the industry requirements. Review of the education curricula to respond to the changing needs of industry.

The international experience suggests that gradual partial subsidies to high quality projects are more effective than indirect

26

support by tax exemptions. Supporting these high quality projects, in conjunction with firmsanduniversityprojects(seebelow)canhave a positive impact on the amount and quality of R&D. Support firm cooperationand private sector-university linkages by providing subsidies to high quality innovation projects that involve several firms and/orfirmsandacademicinstitutions.

Quick WIN1. Finalize and implement the projected

institutional framework in the Science, Technology and Innovation Act of 2013.

2. Improvedfinancingandincentivestostimulate Research and Development (R&D).

3. Establishment of research centres that will develop new and innovative ways of manufacturing.

4. Establish centers of excellence to promote innovation and showcase the new techniques and technologies.

27

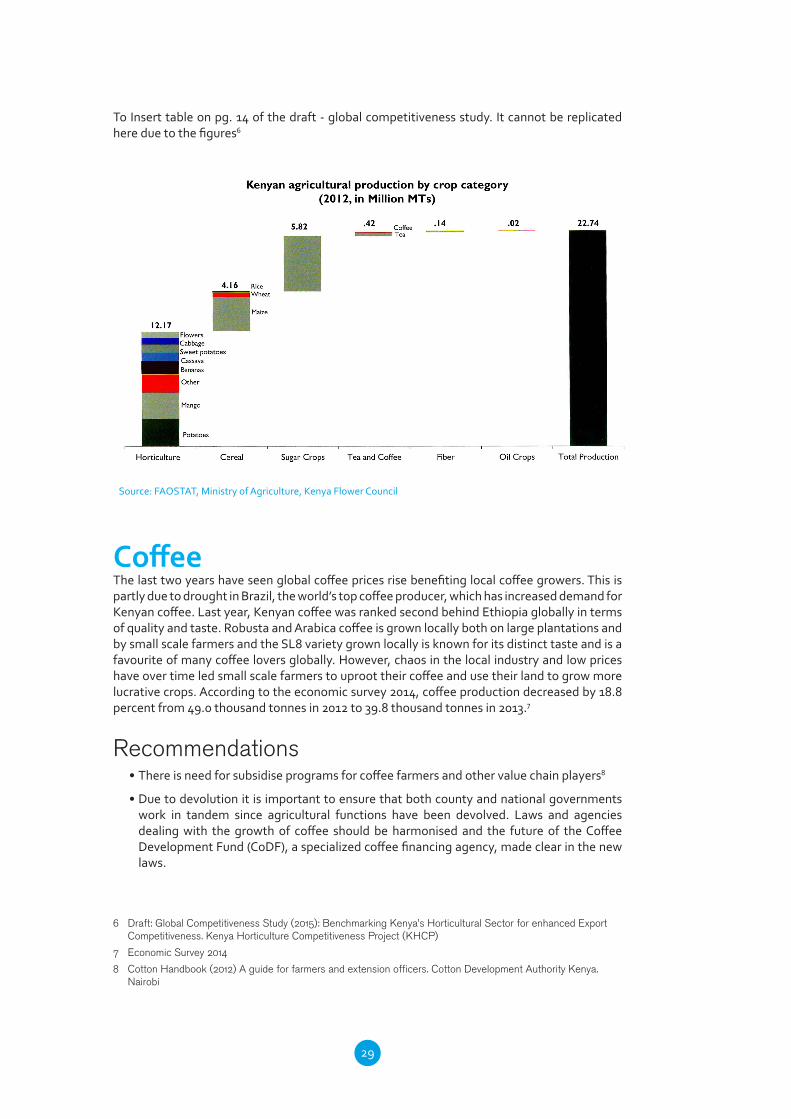

SPOTLIGHT ON AGROPROCESSING AS A DRIVER FOR INDUSTRIAL GROWTHAgriculture in KenyaThis year, our agenda will also focus on Agro-processing since agriculture is Kenya’s economic mainstay though often threatened by erratic weather patterns due to sole reliance on rainfall water. The major crops grown in the country include horticultural produce, cereals such as wheatandbarleyandcashcropssuchastea,coffee,tobacco,sugarcane,sisalandpyrethrum.Less than 8 percent of the land in Kenya is used for Agriculture and only about 20 percent of the land is suitable for farming. About half of all crops grown in the country are grown through subsistence farming which requires fertilisers to enrich the soil for the production of crops. Most of the fertilizer used is imported.

The agriculture sector contributes about 25.3 percent to the GDP, and is the source of about 75 percent of industrial raw materials and 60 percent of export earnings. The sector accounts for 65 percent of Kenya’s total exports, 18 percent and 60 percent of the formal and total employment respectively.

While most of the crops are grown for foreign markets, it is also important to consider regional demand. More than two-thirds of global manufacturing activity takes place in industries that tend to locate close to demand.5 Proximity to demand is an important factor as it reduces logistics and transport costs and also increases access to raw materials and suppliers. Still, thesectorhassufferedseveralchallengeswhichhaveseenthecontributionofkeycropslikecotton, sugar-cane, pyrethrum, sisal among others decline.

Source: Economic Survey

5 McKinsey, http://www.mckinsey.com/ retrieved on 23 January 2015

28

Value Addition in the Agricultural sectorEven though Kenya is a horticultural giant in the region, secondary and tertiary value addition still has a long way to go since cottage industries need to be transformed into proper industries. Value-added agriculture generates several billion dollars in economic impact. There is need to look at the agro-processing sector in Kenya and establish a Working Committee on therecoveryofthesector.Agroprocessingoffersimmenselinkagestoothermanufacturingsectors and emerging trends already point to the successful development of countries such as China due to the development of their agro processing sectors.

Kenya’s status as an agro-based economy points to agriculture as the lynchpin to industrialization given the close proximity to raw materials, suppliers and regional demand. Manufacturing involves upstream operations which are those close to the source and involves the conversion of raw materials into intermediary products while downstream activities involvetheconversionofintermediaryproductsintofinishedgoods.NocompanyinKenyaasyet has an extensive regional presence whose value chain sources inputs or feeds them into all threeEastAfricanCountries.Traditionalexportscontinue todominate thefieldand feweffortshavebeenmadetoexpandtonewproducts.Theautomationofagro-processescouldhelp us leap into secondary and tertiary value addition and turn cottage industries into fully fledgedmanufacturingfirms.Agroprocessingvaluechainsareimportantforthecreationofemployment and earning of foreign exchange.