manual on do

DESCRIPTION

loan makingTRANSCRIPT

MANUAL ON DOCUMENTATION

Indian Overseas BankCentral office

763 Anna Salai, Chennai – 600 002

R.V. SHASTRI Indian Overseas BankChairman & Managing Director Central Office

Chennai – 600 002

Date : 18.01.2000

FOREWORD

Lending is an important function of banking. Documentation is a vital

aspect governing the advances portfolio. Proper documentation is sine qua non

for effective recovery of the loans advanced and it needs to be ensured that

documentation is perfect. Understanding this need, the Bank is bringing out

this updated manual on Documentation. A thorough reading of this Manual and

frequent reference will enhance the quality of documentation, thus enabling

the Bank to have a set of enforceable documents on a continuous basis.

I appreciate the efforts put in by Shri. V. Sreenivasan, Faculty member,

Staff College, Chennai and Shri. K. Elangovan, former Deputy Chief Officer,

Legal Services Department, in bringing out this updated Manual. It is earnestly

hoped that branches would make effective use of this publication to ensure

documentation is perfect in all respects.

R.NATARAJAN Indian Overseas BankGeneral Manager Central Office

Chennai – 600 002

Date : 18.01.2000

PFEFACE

Manual on documentation was first brought out in the year 1983 and the

second edition in 1992. The banking scenario witnessed a sea of change during

the last decade; as a result, a number of new forms/documents were

introduced, besides amending many. In the process, a few documents became

redundant as well . Hence, this third edition which is in your hands.

2. In the previous editions, specimen of documents with distinctive

number alone were given. But in this edition, specimen documents even without

distinctive numbers have been incorporated. By this process, the present

edition is made comprehensive and complete in itself without the need for

cross- references to the previous editions.

3. Considerable efforts have gone into updating this manual. Branches

should make use of this manual to the fullest extent and ensure that proper

documents are taken for each advance. While getting documents executed,

Branches should be guided by Bank’s Book of instruction and other circulars

issued from time to time. Any suggestion regarding this publication is welcome

and may be addressed to Management Services Department, Central Office.

Contents

Page No.

Part I Introduction to Documentation 3-15

Part II Description of documents with distinctive numbers 19-20

Part III Types of advance and documents to be taken 23-31

Part IV General guidelines on each type of advance 35-61

Part V Specimen of formats:

Sec. (A) Documents with distinctive number 67-244

Sec. (B) Documents without distinctive numbers 247-395

Part VI Important circulars on documentation 399-460

PART –I

INTRODUCTION TO DOUCMENTATION

General

1. Documentation is an essential part of

Bank lending. It establishes a legal

relationship between the lending

banker and borrower as the terms

and conditions are reduced in

writing. Hence correct

documentation is essential to ensure

the safety of an advance. The

documents should be rightly

stamped, properly executed and

should effectively create the

necessary charge on the security.

The documents should mention the

correct name of the parties, contain

proper recitals, give a detailed

description of the security, if any,

to be charged, the consideration,

rate of interest, terms of payment

and other important conditions

agreed to. Any deviation from the

standard form should not be

permitted without obtaining the

requisite permission from the

Controlling Administrative Office.

The legal formalities as to

registration of charge with the

Registrar if Assurances and/or the

Registrar of Companies should be

compiled with, within time wherever

necessary. All sanction letters are to

be advised to borrowers in form

F568 in duplicate. One copy is to

be retained along with documents

after obtaining the signature of the

borrower as a token of acceptance

of terms and conditions.

2. Stamping

Section 17 of the Indian Stamp

Act, states that all documents

chargeable with duty and

executed by any person in India

shall be properly and duly

stamped before or at the time of

execution. An unstamped or

insufficiently stamped documents

will not be admitted in evidence

or form the basis of a suit.

Permission however can be

accorded in certain cases by the

court or an appropriate authority

to admit an unstamped or

insufficiently stamped document

in evidence, on payment of

certain penalties in addition to

the duty with which the

document is chargeable or in the

case of an Instrument

insufficiently stamped the amount

required to make up the

required stamp duty. It must

however, be remembered that

unstamped or insufficiently

stamped promissory note, or bill

of exchange is an invalid

document ab initio and cannot

be admitted in evidence even on

payment of duty and or any

penalty.

In some states like Punjab, an

unstamped or insufficiently

stamped acknowledgment will be

invalid and cannot be admitted in

evidence even on payment of

penalty. Similarly in the States of

Madhya Pradesh and Uttar

Pradesh, the defect in stamp

duty on a receipt cannot be cured

by paying penalty.

Stamps

3. Stamps are of different kinds:

Impressed Stamps (Stamp Paper)

a. Judicial Stamp Paper (Used

for filing suits in civil courts)

b. Non-Judicial Stamp Paper

(Used for all commercial

documents, such as

agreement, sale deed,

partition deed, gift deed,

Settlement deed, Power of

Attorney, Mortgage deed,

Lease deed etc).

c. Hundi Paper

Adhesive Stamps

a. Special adhesive stamp used in

the place of non-judicial stamp

paper

b. Revenue Stamp

c. Foreign Bill Stamp

d. Share Transfer Stamp

e. Insurance Stamp.

f. Notary Stamp

g. Consular Stamp

h. Brokers’ Note Stamp

i. Court Fee Label Stamp

4. Adhesive revenue stamps are affixed on

promissory notes, receipts and

acknowledgement of debts (Revival

letters. Balance confirmation letters).

Revenue stamps are cancelled by the

borrowers by singing across or otherwise.

The best way of canceling a revenue

stamp is by ensuring that the executant

signs over all the stamps, in such a

manner, that the signature extends even

beyond the stamps.

5.Special Adhesive Stamps, when affixed to

documents are cancelled by the treasury

by punching dates across them. Special

Adhesive Stamps are affixed on

Agreements. Bill of Lading, Insurance,

Bills of Exchange, Shares, etc.

Sometimes, the treasury impresses or

engrosses the stamp value on the

documents when Special Adhesive

Stamps are not available. If special

Adhesuve Stamps or impressed

/engrossed documents are not readily

available documents may be executed

on non-judicial stamp paper for the

requisite value of stamps. The stamp duty

must be in accordance with the provision

of the stamp law in force in the respective

states.

As per the Stamp rules, a document should

begin on non-judicial Stamp Paper and if it

is affixation of special adhesive stamp, the

Stamp should appear on the face of the

document. Therefore the non judicial

Stamp Paper should be made as the first

page and the beginning portion of the

standard format should be written or typed

on it and such portion of the standard format

should be struck of under authentication of

the executants signature. The non-judicial

Stamp Paper should form part of the

standard format and should be stapled or

stitched so that it appears as the first page

of the document. The executant should sign

each page of the document including the

non- judicial stamp paper.

Procedure to be followed only in places

where Branch Managers are empowered

to affix and cancel stamps:

6. In certain states, the Managers of the

nationalised banks have been declared

as “Proper Officers” for the purpose of

Rule 10 of the Stamp Act, 1889.

Accordingly they are empowered to affix

and impress special adhesive stamps.

The managers are required to obtain the

required numbers of special Adhesive

Stamps under various denomination by

remitting the value in cash in the Treasury.

The stamp for the required amount can be

affixed by the Branch Manager on the

documents as and when necessary. The

following procedure should be followed.

a. Required Special Adhesive Stamps

shall be affixed by the Branch Manager

on the printed forms in the space

provided for, if no space is provided, the

stamps may be affixed on the right side

top of the first page of the form.

b. Such Special Adhesive Stamps shall

be affixed on the printed forms as stated

above, before or at the time of

execution of the documents by the

borrower. Any stamps affixed after

execution of the documents will amount

to contravention of law.

c. Branch seal, should be put on the

Adhesive Stamps so as to cancel the

stamps. If more than one stamp is

affixed, each stamp should bear the

Bank seal.

d. Branch Manager should put his signature

across the stamp and put the date under

the signature. This must be done

immediately after affixing the stamp on

the form. On no account the date put by

the Manager should be later than the

date of execution of the document by the

borrower.

e. The stamp may be affixed and cancelled

with date by Branch Manager in

minimum required forms or as and when

the form is required to be used.

Branches should not affix the stamps on

the forms in bulk.

f. Branch Managers alone are empowered

to affix the stamps and put the seal on

them with their signature.

g. In all other places where the managers

are not empowered to cancel the

stamping it must be cancelled by an

authority so designated by the Act (viz.

a treasury). Refer para 5 above for

details.

Bill of exchange stamps

7. Usance Bills drawn and payable in India.

Usance Bills drawn in India and payable

outside India, and Usance Bills drawn

outside India and payable in India, are

liable for stamp duty. Usance Bills drawn

in India and payable in India or outside

should be drawn on hundi paper or

Special Adhesive Stamp should be used

and cancelled by Treasury before

execution. On usance Bills drawn outside

India and payable in India. Foreign Bill

Stamps’ are to be affixed before

negotiation or presentation.

Execution

8. All documents must be executed in the

presence of the Manager or Deputy

Manager or any official. The parties

should sign in full according to their

specimen signatures. If a document

consists of a number of pages, all of them

should be signed by the borrower. As far

as possible, there should be no correction

or over-writing or interlineations in the

document. Correction or over-writing or

interlineations, if any, must be

initialled/signed by the executants. All

blank spaces in the document should be

filled with the relevant particulars and

authenticated by the executants in

addition to signing at the end of each

page. The execution of documents and

disbursement of the advance should be

on the same date preferably. However

documents should not be dated later

than the date of advance.

Documents execution register

9. The date, names of executants, amount

/ limit of the advance and the nature of

documents executed should be clearly

entered in the register. The entries in the

register should be signed by the

Manager/Deputy Manager after verifying

that the executed documents are in order.

No entry need be made in the register in

regard to documents for advances against

fixed and other deposits, jewel loans,

personal and small loans and agricultural

advances

Documentation cum Due Date Register and

Diary for Renewal of documents are to be

maintained by the branches to ensure

timely renewal of documents. Refer GM’s

Circular No.21 of 1983 dated 3-12-83 given

in page No.401. Branches should preserve

the documents borrower wise and limit wise.

Loan documents relating to a particular limit,

say, CC Limit or Term Loan limit should be

kept under a docket giving the following

details on the docket sheet.

1. Name of the borrower

2. Nature of credit facility

3. Amount

4. Date of document.

5. Form number of

documents

6. Due date for taking

confirmation of balance/

revival letter.

7. Date of current sanction

letter.

Executants

10. All persons competent to

contract, can execute documents.

However a minor, lunatic or an

undischarged insolvent cannot execute

any document.

Execution of documents by illiterate

persons

11. a. In the case of illiterate

persons left hand thumb impression of

the borrowers should be obtained.

Thumb impression of a person once

affixed to a document cannot be

disputed as not belonging to him and

therefore, it can be treated as a

proper mode of execution of by

illiterate person. To vouch-sale about

the person affixing the thumb

impression, it can be certified as

belonging to a particular individual.

Such a certificate cannot be treated

as an attestation (witnessing) to the

contents of the documents. In such

cases a certificate has to be added as

under: “Contents of the above were

read over and explained to the

executant(s) in vernacular language

and he/she understood the same

before affixing his/her impression.”

Left Hand thumb impression of

Shri/Smt …………….. taken by

……………. (in whose presence the

left hand thumb impression was

taken). Before the certificate the

concerned officer should sign and

indicate his designation.

Execution of documents by blind

persons

11.b.1 Loans can be granted to blind

persons individually. In that case, the

loan document should be read over

and explained to the blind borrower

before he executes the same and a

letter to that effect may be taken

from a witness as per Annexure

11. Further the borrower may be

asked to open a SB Account. The

Loan amount may be released

through that account.

2. When the blind person desire sanction

of a loan jointly with another person whom

he considers reliable, the loan may be

granted to them jointly. In such an event

while obtaining the document the

contents of the document as well as

terms and conditions of the sanction

should be read and explained to the

borrower in the presence of a witness as

detailed above.

3. In case of advances made to a blind

person jointly with another person,

alternatively the other borrower may be

authorised by the blind person to execute

the loan documents, sign the revival

letter and / or confirmation of balance,

create mortgage, charge etc. by

executing a special power of attorney

(attested by notary public or First Class

Magistrate) and the loan documents

could be executed by the other borrower

agent. Before obtaining the document

from the agent the contents of the Power

of Attorney should be read over and

explained to the blind person in the

presence of a witness and only when he

confirms the execution of such a Power

of Attorney, the documents should be

obtained. The fact of such confirmation

should be recorded under the signature of

the witness as detailed above.

4. The witness may be another customer or

a person known to the bank but should not

be related to the blind person. Staff

members should not be a witness.

Attestation (Witnessing)

12. Some documents are required to

be compulsorily attested while

others are not. Mortgage deed,

Gift deed, Sale deed of

immovable property or Will

require to be attested atleast by

two witnesses. Other documents

should not be attested unless

provision has been made in the

document for such attestation.

Renewal

13. In India under the Limitation Act,

Demand Promissory Note cannot

be used upon after three years

from the date of their execution.

The documents have, therefore,

to be renewed before expiry of 3

years. Branch should, therefore

diarise for renewal of the

pronotes 9 months before they

become time barred.

Comprehensive

14. Comprehensive Renewal letter in F 301

(Revised) must be obtained from the

borrower within three years from the date

of execution of the loan documents or

within three years from the date of the last

revival letter. Revival letter (F.301) meant

for the borrowers should be obtained from

them for all types of borrowal accounts

after 27 months if the date of loan

documents/last Revival letter, but before

expiry of 3 years from the date of loan

documents/last revival letter. It can be

taken now for all borrowal accounts

(including borrowal accounts where DPN

is not taken) since has been revised to

revive loan agreement and DPN.

Comprehensive Revival letter (F.301B)

meant for guarantors should be obtained

from guarantors for all type of borrowal

accounts after 27 months of date of

guarantee document/last Revival Letter,

but before 3 years from such date. (Even

though Madras High Court had held that

borrower’s acknowledgement will not

extend the limitation as against the

guarantor, the Supreme Court had held

very clearly in Margaret Lalitha Samuel Vs

Indo Commercial Bank case that such

borrower acknowledgement shall extend

the limitation against the guarantor also)

Confirmation of balance should be

obtained each year from the borrowers for

all cash credit accounts and overdraft

except loan accounts and it should be

obtained each year from the guarantors

for all borrowal accounts.

Limitation for filing a suit against the

borrower and guarantor will get extended for

further period of three years by their

confirmation of balance, Revival Letter and

part payment under their signature.

Whenever revival letters are taken, details

should be entered in the Documents

Execution Register immediately below the

documents listed, taking care to mention the

name of executants and the date.

Special precautions

Advances to Limited Companies

15.1.The Branch Manager should verify the

Memorandum and Articles of

Association of the borrower company

to ensure that it authorises the

company (a) to engage itself in the

activities for which the loan/advances

is considered by the bank and (b) to

borrow money against the security of

its assets. The Articles of Association

should have a clause empowering the

Board of Directors of the borrower

company to borrow money by creating

mortgage/charges on the whole or part

of the undertaking. The Branch

Manager should ensure that the

provisions of Section 293 (i) (a) & (b)

of the Companies Act, 1956 are

compiled with, wherever necessary.

15.2 Section 293 (i) (a) & (b) of the Indian

Companies Act 1956 (Restrictions on

powers of Board) run as under:

1. The Board of Directors of a public

company or of a private company which

is a subsidiary of a public company shall

not except with the consent of such

public company or subsidiary general

meeting.

a. Sell, lease or otherwise dispose of the

whole, or substantially the whole, of the

undertaking of the company, or where

the company owns more than one

undertaking, of the whole, or

substantially the whole of any such

undertaking.

b. Borrow moneys after the commencement

of this Act, where the moneys to be

borrowed, together with the moneys

already borrowed by the Company

(apart from temporary loans obtained

from the Company’s bankers in the

ordinary course of business) will exceed

the aggregate the paid-up capital of the

Company and its free reserves, that is to

say reserves not set apart for any

specific purpose.

15.3 It is therefore necessary before

allowing advances (other than

Temporary loans obtained from the

Company’s Bankers i.e Loan repayable

on demand or within six months from the

date of the loan, such as short term cash

credit arrangements discounting of Bills

and other short term loans of seasonal

character) to (i) Public Limited

Companies or (ii) Private Limited

Companies which are subsidiaries of

Public Limited Company to verify that

the total borrowings of the Company do

not exceed the paid-up capital plus free

reserves, if the borrowing should exceed

these limits, a prior resolution

authorising such an excess has to be

passed in a General Body Meeting of the

Company Certified copies of such

resolutions must be obtained and kept

with the documents.

15.4 A certified copy of the resolution

passed at a meeting of the Board of

Directors of the Company aurthorising

the advance stating the terms and

conditions thereafter etc should be

obtained . The resolution should further

state the names of person or persons

who would execute the documents on

behalf of the company. In the case of a

mortgage, the resolution should also

state the name(s) of the person/persons

who are authorised to deposit the title

deeds on behalf of the Company. All

resolutions of the company should be

certified by the Chairman of the Meeting.

15.4.a. Documentation procedure when

Private Limited companies change

into Public Limited Companies.

As per the provision of Sec 43(A) of

Companies Act a private limited

company will become a public limited

company when the average annual turn

over exceed a certain limit prescribed by

Central government. A private limited

company shall become a public limited

company when it accept deposits after

an invitation is made by an

advertisement or renew deposits from

public.

When a private limited company changes

into a public limited company, its rights and

liabilities already undertaken to the bank are

not affected and therefore, it may not be

necessary to disturb the loan documents

already executed by the company. It may

not also be necessary to close and open the

account for the reason of conversion of

private limited company into a public limited

company. Branches should follow the under

noted procedure in this eventually.

1. Copy of the amended Certificate of

Incorporation issued by the Registrar

of Companies should be obtained

and kept on branch records.

2. Confirmation of Balance and Revival

letter should be obtained from the

public limited company indicating that

it is formerly known as private limited

company e.g:- for ABC Ltd (formerly

known as XYZ LTD)……..Authorised

Signatory

3. The change of the name is to be

noted in the ledger and accounts.

4. No correction is required in the loan

documents already executed by the

company. However, while taking

further documents in future, the

company should execute the

documents in their new name as a

public limited company. Refer

circular 7(e) 6/96-97 dt 30/10/96 for

the procedure to be adopted in case

of change in the name of the limited

company.

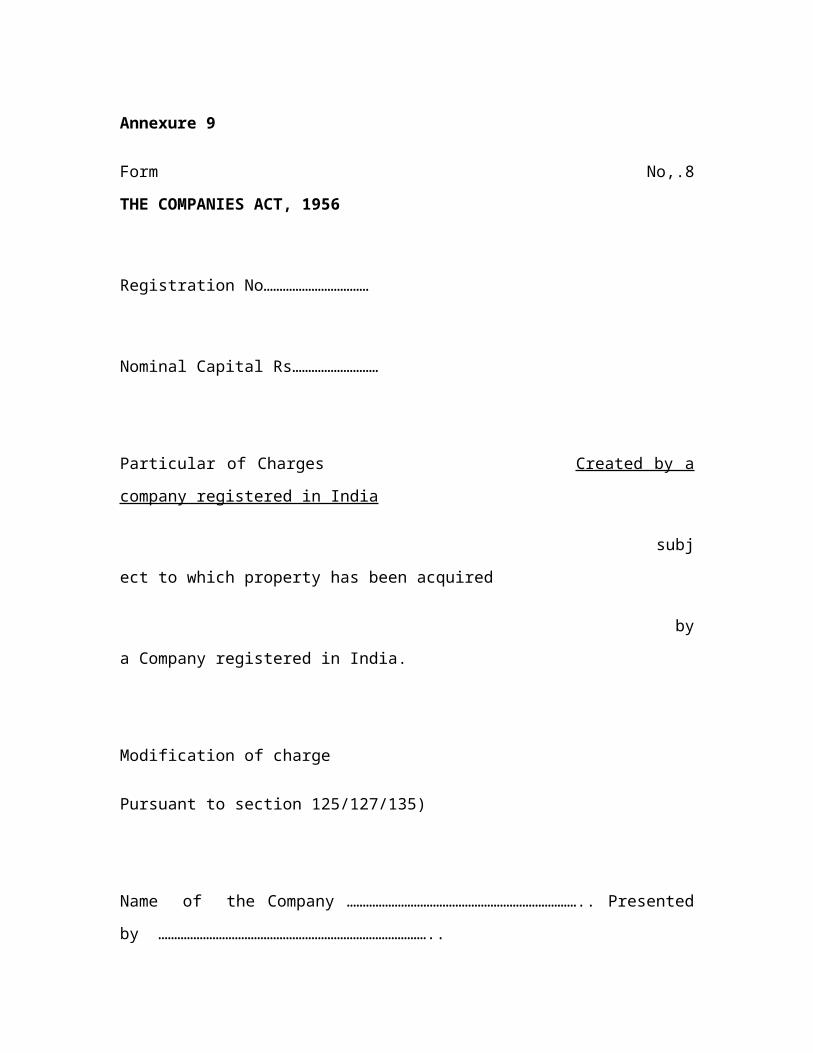

15.5 Registration of charges:

In the case of all companies

including Private Limited Companies,

certain charges on their assets have to be

compulsorily registered with the Registrar

of Joint Stock Companies under Section

125 of the Companies Act 1956.

The following charges require compulsory

registration:

a. a charge for the purpose of

securing any issue of debentures;

b. a charge on uncalled share

capital of the company;

c. a charge on any immovable

property, wherever situate or any

interest therein;

d. a charge on any book debts

of the company;

e. a charge, not being a pledge

on any movable property of the

company(i.e. hypothecation charge);

f. a floating charge on the

undertaking (or) any property of the

company including stock-in-trade ;

g. a charge on calls made but

not paid;

h. a charge on a ship or any

share in a ship;

i. a charge on goodwill, on a

patent or licence under a patent, on a

trade mark , or on a copyright or a

licence under a copyright.

15.6. It should be noted that the charge has

to be registered in Form 8 along with

Form 13 within 30 days of its creation

after verification of prior charge, if any,

by making a search in the books of the

Registrar of Companies(ROC).

Registrar may allow for registration

upto 30 days after expiry of 30 days, if

the delay is genuine. When the terms

and conditions or extent of operation of

any charge already registered are

modified, a modification of charge

should also be registered in Form 8

along with Form 13 under the

provisions of Section 135 of the

Companies Act within 30 days . An

increase in the rate of interest higher

that the rise in RBI rate, constitutes a

modification of charge and hence has

to be registered with the Registrar of

Companies . When the existing limit

of advance is enhanced or additional

facility is sanctioned to the company, it

is not necessary that the account

should be closed and new account

opened for the total limit on the basis

of fresh documents. It is sufficient to

take documents only for the enhanced

portion of the limits or the additional

facility and register such charge with

the Registrar of Companies within the

prescribed time of 30 days. A

declaration in the form of a negative

lien that the assets are free and

unencumbered and an undertaking

that the said assets shall not be sold,

mortgaged, pledged hypothecated or

in any way encumbered without

previous consent of the bank in

writing , should be obtained in Form

419 . This document does not require

filling of any charge with Registrar of

Companies as, such a document does

not create any charge on any property

of the company. For detailed

procedure of filling charge with ROC

refer circulars 7 (e) 3/95-96 dt

27.06.95 and 7 (e) 1/96-97 dt.

12.06.96.

15.7 Affixing of Company’s common Seal

necessary wherever it is stipulated

either in the Article of Association of

the Company or in the resolution

passed by the Board of Directors.

There are some advantages in proving

a document containing Common Seal.

Therefore in all loan documents such

as DPN, Hypothecation Agreement

and indemnities executed by the

Company, branches may insist for

Common Seal of the Company , which

should be affixed in the presence of

the Directors/Secretary authorised

under a Board resolution.

15.8 Before granting an advance any form

to a limited company , a search should

invariably be made in the Office of the

Registrar of Companies to ascertain if

any prior charge exists over the

security offered.

Advances to partnership Firm

16. Though a partner has implied power

to borrow or pledge the movable

property of the firm, the loan or

advances documents should be

signed by all the partners .If,

however , one or more partners are

specially authorised by the

partnership deed or by a letter is

signed by all the partners of the firm,

the documents may be signed by

such authorised partners . Execution

of the documents should be under

the firm’s rubber stamp . Format of

letter of authority is given in

Annexure.

Sec 49 of Indian Partnership Act reads

where there are joint debt due from the

firm and also separate debts due from

any partner, the property of the firm

shall be applied in the first instance in

payment , of the debts of the firm and

if there is any surplus, then the share

of each partner shall be applied in

payment of his separate debts or paid

to him. The separate property of any

partner shall be applied first in the

payment of his separate debts and the

surplus (if any) in the payment of the

debts of the firm.

In view of this provision , branches

should obtain the personal guarantee

of all the partners, for the debts of the

firm.

Sole proprietary concern

17. The proprietor of the concern

should sign the loan or advance

documents as proprietor by affixing

the rubber stamp of his concern.

Pegging of Deposits/Loan

18. Branches who have got credit

limits sanctioned , with the stipulation

that the investments by way of

deposits and loans by the

partners/directors should be pegged

during the currency of the advance,

should obtain letters from the

depositors undertaking not to withdraw

their deposits/loans during the

currency of the loan to the borrower,

such letter of pegging should be

obtained in Form F 418.

Title Deeds

19. a.The title deeds must be

deposited by the owner of the property

or his agent, specially authorised for

such purpose by a power of attorney ,

who must attend the office of the Bank

for the purpose. If there are more than

one owner , and all cannot attend , a

power of attorney in the name of one

of them must be executed by the

others, for depositing the title deeds.

Where the title deeds are in favour of

a partnership firm, and all the partners

of the firm cannot attend the bank’s

office , they must execute /authorise

by a power of attorney one or more of

them to attend and deposit the deeds

on their behalf. This power of attorney

must be notarially attested and be kept

along with title deeds. If the borrower

is a company, a resolution delegating

the powers to one of the Directors or

to one of their officers, to deposit the

title deeds must be passed by the

Board of Directors. The power of

attorney/certified copy of the resolution

should be kept along with the title

deeds. The execution of power of

attorney must be notarially attested.

Whenever a third party offers immovable

property as mortgage security, personal

guarantee should be obtained from such

third party. Otherwise it can be contended

that there was no consideration for the

mortgage.

The title deeds , should be originals, Copies

of title deeds should not be accepted without

prior reference to Central Office. The

narration in the specified form as given in

page No. of this manual (para 12

Chapter XG of Book of instructions) has to

be made in the Title Deeds Register by an

Officer of the Bank and witnessed by two

Officers. The borrower should not sign the

register and no acknowledgement of receipt

should be passed on to him by the Bank.

The borrower should however execute a

letter of confirmation of deposits of title

deeds in Form F379 preferably on the next

day of the deposit. For purpose of

extending the scope of security of equitable

mortgage (viz, mere deposit of title deeds or

deposit accompanied by Registered

Memorandum) the mortgagor should call at

the Branch. A supplementary narration

should be entered in the title deed register

as per narration given in page No. On

the next day, a confirmation letter in Form

No. 379A should be obtained from the

owners. The encumbrance Certificate for

the period during the date of earlier title

deed narration and the supplementary

narration should be obtained and kept on

record. If there is any intervening

encumbrance, the matter should be referred

to the sanctioning authority.

In the case of Limited Companies, the

supplemental narration should be obtained

as given in Page No. of this manual and the

confirmation letter signed by the authorised

signatory of the company on the next day as

detailed in Form No. 379A. It is necessary

to file modification of charge since the

supplemental narration is for the purpose of

extending the scope of security.

Revival of Mortgage

19b. Mortgage by deposit of title deeds of

registered mortgage is valid for a period

of 12 years from the date of mortgage.

To extend the mortgage beyond this

period any one of the following

procedure should be adopted.

i. Before the lapse of 12

years from the date of mortgage branch

should obtain balance and security

confirmation letter as per the format

given in Annexure2. The balance and

security confirmation letter should be

properly filled and signed by the

borrower/guarantor over Revenue

stamps as in the case of Revival letter.

ii. The branch can also

create a fresh equitable mortgage by

redeposit of title deed provided there is

NIL encumbrance during the indemnity

period. Care should be taken to obtain

nil encumbrance till date of redeposit of

title deeds.

iii. In case of Registered

Mortgages branch should not arrange for

redeposit title deeds. The period of

limitation can be extended by an

endorsement by the mortgagor on the

Registered Mortgage Deed as to the

repayment of principal and interest. The

endorsement should be made on any of

the reverse page of the Registered

Mortgage Deed and the endorsement

should be on the following lines; “I/We

hereby confirm and acknowledge my/our

indebtness in the outstanding sum of

Rs……………(Rupees

Only ) as on ……………………..and

further acknowledge that the debt is

secured by this Registered Mortgage

and that the Mortgage security is in full

force and effect.

Place:

Date

Signature of Mortgagor

Alternatively it will suffice if branches

takes security confirmation letter within

12 years from the date of the Registered

Mortgage Deed and follow the procedure

outlined in para 19.1 (i)

Guarantees

20.a. Joint Stock Company(Limited

Company)

Branches should examine the

Memorandum and Articles of Association of

the company to see if it has power to give a

guarantee or offer security. Whenever

branches have to examine this aspect of

power either. In the Memorandum and

Articles of Association or in the power of

Attorney , specific guidance will have to be

given that the authority to give a guarantee

or to create a mortgage ought to be clearly

spelt out and not to be interred from general

terms.

20.b. Partnership

As the giving of guarantee is

outside the normal business of a partnership

, it is always advisable to require all the

partners of the firm to join in signing a

guarantee given on its behalf, unless an

individual partner has express authority to

give a guarantee, binding the firm. It is

however preferable to obtain guarantees of

all the partners in their individual capacities.

Guarantees should be obtained in

all cases on Form 111 from the guarantor

either prior to or simultaneously with the

execution of loan documents by the

borrower. If it is a case of securing and

existing advance , the appropriate form of

guarantee is Form 111A .This may be noted

carefully as Form 111 is not a valid

document for guarantee relating to existing

debts.

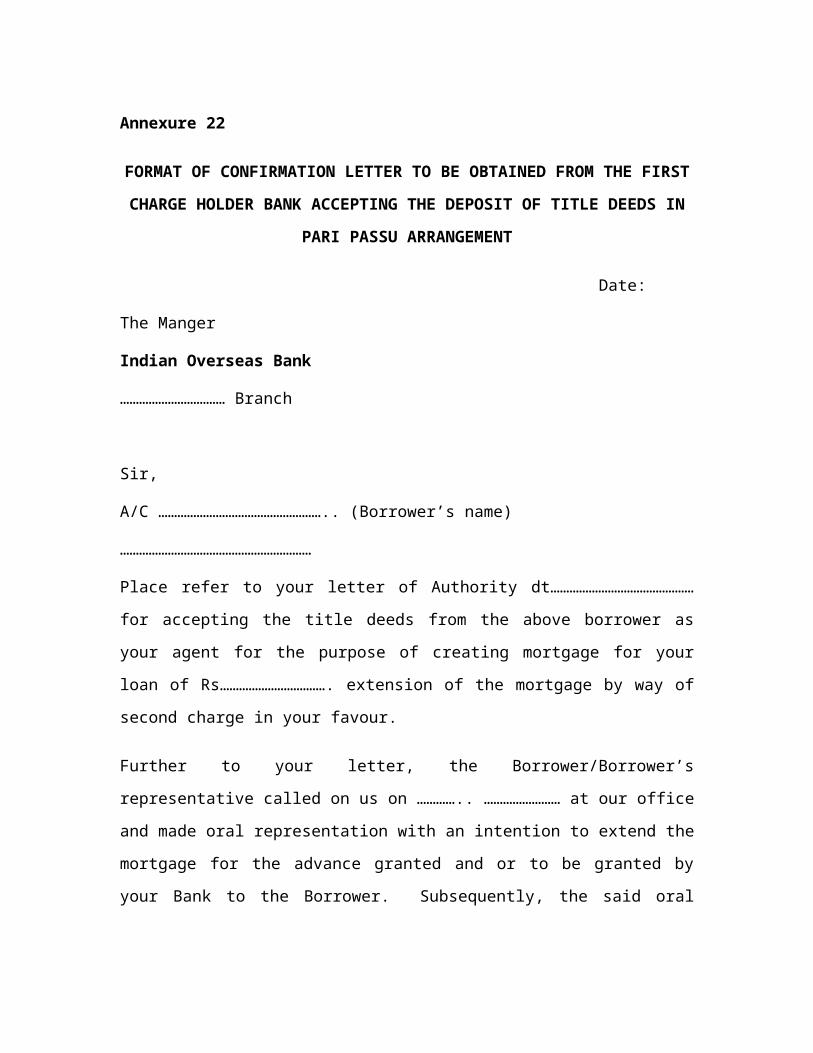

Consortium Advances

21. In consortium advances, two or more

financial institution join together in

meeting the financial requirements of a

borrower . They share the securities on

pari passu basis or in such manners as

per the terms of the agreement among

themselves.

Generally, the following procedure is

adopted before entering into pari passu

agreement.

1. When the working capital

facilities are granted against the security

of current assets , single window

concept is to be adopted . The following

documents are to be executed. Refer

Permanent Circular ADV.541/89 dated

23-6-89.

a. Board Resolution to be passed

by the Borrower Company.

b. Resolution to be passed by the

member banks for appointing the

First Lead Bank and Second

Lead Bank.

c. Resolution to be passed by the

Second Lead Bank.

d. Letter of authority to be given by

the member banks to the First

Lead Bank.

e. Letter of authority to be given by

the member banks to the Second

Lead Bank.

f. Working capital consortium

agreement between the borrower

and the Participating Banks- to

be signed by the Borrower , the

first Lead Bank for self and on

behalf of other banks.

g. Joint Deed of Hypothecation to

be executed by the Borrower

company in favour of the

Participating Banks - to be

signed by the borrower only.

h. Inter – see Agreement between

the participating Banks- to be

executed by the consortium

banks only.

i. Undertaking letter from the

Borrower company for creating

Second charge and on Fixed

Assets- to be obtained by the

First Lead Bank.

j. Revival Letter (RL) to be signed

by the Borrower Company- to be

obtained by the First Lead Bank.

2. 2. When term loans are granted against

the security of immovable property ,

the Lead Bank examines the title to

the property. The opinion on title

deeds obtained from the

advocates/solicitors is circulated

among the participants.

The participating Banks exchange

among themselves a letter ceding pari

passu charges expressing their willingness

to share the security equally without

claiming any priority. The format of the letter

will be ordinarily as follows , but it may be

varied according to circumstances.

“Dear Sirs,

Letter ceding pari passu charges

Financial assistance to

…………………………………………………

…………………..

We Indian Overseas Bank (IOB) hereby

agree and confirm that notwithstanding

anything to the contrary contained in or by

virtue of the mortgage and charge created/

to be created by …………………………….

(hereinafter called “the Borrower” ) in our

favour in respect of the Borrower’s

immovable and movable properties to

secure the term loan of Rs………………

with the interest and other monies payable

by the Borrower to us in respect thereof,

the mortgage and charge of IOB shall in

all respect rank pari passu with the

mortgages and charges created / to be

created by the Borrower in favour of

1……………………In respect of its term

loan of Rs………..

2…………….In respect of its term loan

of Rs……………..

(Name of the participating

Institutions with the detail of

their amount of loan)

together with interest thereon at the

respective rates, compound interest in case

of default , commitment charges ,

prepayment premia, costs,

charges ,expenses and their monies

payable by the Borrower to you under your

Heads of Agreement /loan agreement

sanction letters entered into by the Borrower

issued by you to the Borrower without any

preference or priority of one over the other

or others of them for all purposes and to all

intents.

We all authorise you to make a mention of

the pari passu charge in favour of ourselves

and/or your institutions on the assets of the

Borrower company in the form of particulars

of charge required to be filled by the

borrower with the Registrar of Companies

pursuant to the Companies Act, 1956 . We

hereby further agree to undertake and

confirm that we shall enter into a pari passu

agreement with you and the Borrower

defining the rights and obligations of the

parties Inter –se and also providing that the

securities created/to be created by the

Borrower under or by virtue of the aforesaid

mortgages and charges shall rank pari

passu in point of security and for the

purpose of realization without any

preference or priority of one over the other

or others for all purposes and to all intents

and including specific provisions regarding

insurance, custody of insurance policies ,

custody of title deeds, application and

realisation of sale proceeds etc. in such

form and in such manner as may be

mutually agreed upon.

We also request you to issue a

similar letter to us conceding pari passu

charge in our favour on the Borrower’s

assets in respect of our above term

loans if not already issued.

Yours faithfully,

…………………

A joint equitable mortgage is created in

favour of all the participating Institutions.

The lead bank accepts the title deeds

for itself and on behalf of other

participants as their agent.

In respect of the movable machineries,

each participating bank may either take

its own hypothecation deed or they may

take a joint deed of hypothecation as

agreed between them. Finally a pari

passu agreement is executed by all the

participants.

Before execution of the pari passu

agreement and other joint documents,

the lead bank or the Solicitors nominated

by the participants circulate the drafts

among the participants for the purpose

of getting their approval. The

suggestions made by the participating

institutions as may be agreed upon, will

be incorporated in the drafts.

If the borrower is a company, whenever

charge is created over its assets in

favour of the institutions either

individually or jointly, it should be

registered with the Registrar of

Companies. When there is any change

in the terms and conditions of the charge

due to subsequent execution of

documents, modification of charge is to

be filed.

Insurance

22. All securities such as stocks, buildings,

machineries, vehicles etc. charged to

the bank should be insured for the full

value in the joint names of the bank and

the borrower and the relative Insurance

policy(ies) should be held with the

security documents. Insurance should

cover risks of theft, damage due to fire

and riots. Cover for any special type of

risk depending on the location of

godown, nature of machinery or stocks

should be taken in consultation with

Central Office. In cases of insurance for

machineries, cover should be available

for erection, break down, etc. wherever

necessary.

In case of goods delivered under trust, a

suitable endorsement in the policy must

be obtained, as ordinary policies do not

cove goods held under trust. While

obtaining cover notes/policies it should

be ensured that proposal forms have

been filled in and filed by the borrower

with the Insurance Company.

Insurance may be waived in the following

cases.

Category Type of risk Type of assetsa. All category of Priority Sector advances Fire & Other risks Equipment and upto and inclusive of Rs.10,000 Current assets b. Advances to SSI Sector upto and inclusive of Rs.25,000 by way ofi. Composite loans to artisans village Fire -do-

and cottage industries.ii. All term loans Fire Equipmentiii. Working Capital where these are against non- hazardous goods/Current assets Fire Current assets

Where however, Insurance of vehicles of machinery or other equipment/assets is compulsory under the provisions of any law or where such a requirement is stipulated in the refinance scheme of any refinancing agency or as part of a Government sponsored programmes such as IRDP, Insurance should not be waived even if the relative credit facility does not exceed Rs.10,000 or Rs.25,000 as the case may be.

Obtention of Documents on behalf of

other branch

23. Branch which requests the other

branch to obtain documents, should fill

up the form in all respects and

forward the same to the branch, where

it has to be duly stamped and got

executed. At the executing branch,

party should call in person and

execute the documents in the

presence of the Manager. The

Manager should get himself satisfied

about the identity of the party.

Manager shall forward the documents

to the concerned branch under

registered post, with acknowledgement

due and in the covering letter should

state specifically that the named

executant had called on the branch in

person and executed the documents.

Mention should be made on the time

and date of execution also. The other

branch should keep this letter along

with the documents. If at the branch

where documents has to be enforced,

higher stamp duty is payable, the

deficient stamp will have to be paid.

In states where our Branch Managers

are authorised as ‘proper officers’ to

cancel special adhesive stamps, they

can affix the deficient stamp and

cancel with their full signature

mentioning the actual date of

cancellation. In other states, such

deficient stamp duty must be made

good by the Treasury

Officials/collector of stamps.

In case of Sub Limits

23.A it is the practice to allow certain

parties to enjoy sub limits at various

centres on the basis of proposals

submitted by one branch. In such

cases, the parent branch (proposals

submitting branch) should obtain

documents in the aggregate for the

entire limits, arrange for insurance,

creation and registration of charge

etc and confirm to the other branches

that they are holding valid documents

and insurance cover covering the

entire limits.

Transferring of Advance Account

from one branch to another

24. Advance accounts can be

transferred from one branch to

another at the written request of the

borrower and on obtaining permission

from Central Office/Regional Office.

While Regional Office can accord

permission for transferring an account

within the region, in cases where

limits have been sanctioned under the

discretion of the Regional Manager, a

report should be sent to Central

Office, detailing the reasons for such

transfer of an account. In case of

limits sanctioned by Central Office,

and where inter regional transfer is

involved, prior permission from

Central Office is necessary. It is also

necessary for the Regional

Office/Central Office to obtain the

concurrence of the transferee branch

for effecting transfer of a borrowal

account.

Branches should first obtain a letter,

requesting for transfer of the account,

duly countersigned by the guarantor,

as per specimen provided in

Annexure 3. On obtaining the

permission from Regional

Office/Central Office, Branch should

transfer the account, after debiting

interest upto the date of transfer.

Branch should note to forward the

following, along with the debit advice,

under registered post with

acknowledgement due. It is also

incumbent on the part of the transferor

branch to rectify all the rectifiable

mistakes pointed out by the

Inspectors/Auditors in the previous

inspection reports, before the account

is transferred.

1. Copy of permission

received from Regional Office/

Central Office for transferring the

account.

2. Copy of the letter of

request from the party duly

countersigned by the guarantor

as per Annexure 3.

3. Loan documents and

the insurance policies on the

assets charged to the Bank.

4. Latest copy of

sanction endorsement of limits

(copies of all sanction

endorsements)

5. F 209 upto the date

of transfer from the last

sanction.

6. Relevant extract of

the Inspection report on the

account and reply of the Branch.

7. A confidential note

prepared by the Manager of the

transferor branch giving a critical

comment on the conduct of the

account, the past experience

with the borrower and his

recommendations about the

party.

On receipt of the above, the

transferee branch should open the

account on the account on the basis

of the advice received from

transferor branch. While doing so,

branch should also ensure that

interest for the interegnum period is

calculated and debited (interegnum

period is the time lag between the date

of transfer from the transferor branch

and the date of debiting the account at

the transferee branch). Transferee

branch should obtain debit

confirmation letter from the borrower

and guarantor on the date of debit.

If the credit facilities are secured by a

mortgage, while transferring the

facilities, branches need not disturb

the title deeds lodged with the

transferor branch. However, branches

should seek instructions from Legal

Services Department whenever any

enhancement is made in the limits

already sanctioned prior to the transfer

of facilities, as a supplemental

narration has to be recorded.

In the case of limited companies,

while ensuring that all the above

formalities are complied with,

branches should note to obtain a

resolution passed by the directors, at

their meeting, for transferring the

account. A supplemental agreement

as per specimen provided in Annexure

9 & 10 should be filed along with form

8 and from 13 with the Registrar of

Companies, for modification of charge,

within 30 days from the date of

execution of supplemental agreement.

Branches should also note to obtain

necessary endorsement from the

Insurance Company in the Insurance

policies.

Branch should seek instructions from

Legal Services Department in respect

of documentation whenever accounts

are transferred inter-State.

Transfer of a borrowal account may

involve transfer of outstanding under

contingent liability also. In such cases,

transferor branch, may transfer the

outstandings, including the contingent

liabilities, but should handle

documents very expeditiously

whenever received under letter of

credit opened by the transferor

branch, as it is not possible to advise

the negotiating Bank/beneficiary of

the guarantee about the transfer of

account to another branch. On

receipt of bills, transferor branch

should examine the documents and

ensure that there is no discrepancy

and forward the documents

immediately to the transferee branch

under registered post with

acknowledgement due. In case of any

discrepancy the negotiating Bank

should be advised about the

discrepancy in the usual manner and

advising the Bank that the Branch is

holding the document at the

negotiating Bank’s risk and

responsibility. However, the

documents should be forwarded to the

transferee branch immediately.

Similarly, when a claim under a

guarantee issued by the transferor

branch is received, the transferor

branch should immediately forward the

letter to the transferee branch under a

copy to Regional Office and Central

Office. An acknowledgement should

be sent to the beneficiary of the

guarantee, wherein, inter alia, the

branch should state that the account

has been transferred to another

branch and the matter has been

referred to them and request the

beneficiary to contact the transferee

branch. In all these type of cases, it is

the duty of the Chief/Senior

Manager/Deputy Manager to ensure

prompt steps.

While taking over an account from

another bank

25. Branches can take over a borrowal

account from another bank on

obtaining permission from Central

Office. (in case of accounts where the

aggregate credit facilities exceed

Rs.50 lakhs from the Banking System

‘No Objection Letter’ from the other

Bank is necessary). Branches should

follow the following procedure while

taking over an account.

1. Obtain permission from Central

Office

2. Obtain a letter from the

transferor Bank listing out the

dues from the borrower

3. Obtain a letter of confirmation

from the borrower as to the

correctness of the outstanding.

4. Obtain documents as per this

Manual.

5. Obtain letter of authority

authorising payment to the

transferor bank.

6. Comply with the instructions

issued by Central

Office/Regional Office in

respect of advances from time

to time.

7. To the debit of the Loan/Cash

Credit account, prepare a

cheque on Reserve Bank of

India State Bank of India or

Bankers Cheque favouring the

Bank mentioning the name of

the borrower viz., ABC Bank

A/C: XYZ Ltd.,

8. Draft a covering letter, in which

clearly indicate as to the

appropriation of the amount as

per instructions of the borrower

and call for “No due Certificate”

and “No lien certificate” from

the transferor Bank.

9. Send the Bankers Cheque

/cheque along with the covering

letter through our bank

messenger only.

In case of limited companies , In

addition to the above, the following

formalities should be complied with

1. Conduct a search in the files

of the Registrar of Companies

and take out a list of subsisting

charges ; if any second charge

is in evidence , branch should

seek instructions from Legal

Services Department enclosing

a copy of list of charges priority

wise and copy of sanction from

Central Office to taking over of

the account.

2. Exchange the Bankers

Cheque/Cheque on Reserve

Bank of India /State Bank of

India for Form 17 (Satisfaction

of charge) No due Certificate

and No Lien Certificate.

3. File Form 17 (given by the

transferor Bank) and Form 8

and Form No:13 (creation of

charge in our favour with the

Register of Companies

Preferably on the same day).

Branches should not commit to the

Bank either in writing or orally as to the

other outstandings which have not

been covered under the arrangement.

Branches should not disburse the

money directly to the borrower for

remitting the same at the other bank

for adjusting the outstanding under any

circumstances . The Bankers cheque/

cheque favouring the transferor bank

should be sent only through our Bank’s

messenger. For other detailed

procedure on take over of borrowal

accounts from other banks, refer

permanent circular Adv.234/98 dated

28.4.98.

Regularisation of time–barred debt

For any reason, if a loan

account is time-barred for enforcing

personal remedy in the absence of any

revival letter or confirmation of

balance, or any letter of

acknowledgement or payment under

the borrower’s signature, the matter

should be immediately reported to

Regional Office and the concerned

advances Department at Central

Office. In consultation with Regional

Office/ concerned Advances

Department , remedial measures

should be taken to revive the time-

barred debt.

There are two ways to revive a

time-barred debt. viz.

a. New loan account

can be opened after taking fresh

loans /security /guarantee

documents for the present

outstanding together with upto date

interest along with a written request

to close the debit balance in the old

(time –barred) account out of the

new loan amount.

b. Without closing and

opening the account an express

promise agreement can be taken

from the borrower and fresh

guarantee F111A can be taken from

the guarantor.(If there is any

mortgage security , only this method

should be adopted instead of first

one).

Modification of charge

27. In para 15(6) above, it has been

laid down that when the existing limit

of advance is enhanced or additional

facility is sanctioned to the company,

to obtain documents for the

enhanced portion/additional facility

supplemental deeds are to be

obtained in any of the following three

cases and the deed in respect of

each case is prescribed hereunder.

(Refer permanent circular ADV

423/88 dated 31.5.88)

Enhanced limit with the same

security 110F

Enhanced limit with additional security

110G

Same limit with additional security

110H

Creation of Collateral Security

(Machineries & Current Assets)

General Hypothecation Agreement

28. Whenever a sanction endorsement

contain a stipulation that

machineries or current assets or

book debts should be held as

collateral security for other credit

limit(s) ,branches should obtain the

general Hypothecation Agreement

for collateral securities in

F.No.110E. This is to be obtained

in addition to the usual loan

documents take for the concerned

limits.

The General Hypothecation

Agreement (110E) must specify the

nature and amount of credit facilities

for which collateral security has been

stipulated and schedule column

should be filled in appropriately eg.

All present and future ------ of the

borrower at the factory premises or

elsewhere.

Branches should note that we can

secure only movable things in

hypothecation agreements.

Therefore, in the schedule column

either land or building should not be

mentioned as hypothecated security.

29. When limits are enhanced where

pronotes and connected documents

are taken afresh for the full limits the

old account should be closed by

transfer to a new account on the

basis of new documents. In the case

of cash credit or overdraft, the

borrower should be asked to issue a

cheque against the new account

equal to the outstandings in the

account inclusive of interest upto the

date of closure and the amount of

the cheque which must be endorsed

by the borrowers should be credited

to the old account. Both the debit to

the new account and the credit to the

old account should be treated as

cash transaction.

This procedure should be followed

in all cases where documents are taken not

withstanding the limit being the same,

reduced or enhanced. This however will

not be applicable in the case of LIMITED

COMPANIES when the existing limit of

advance is enhanced or additional facility

is sanctioned to a firm/company , it is not

necessary to obtain fresh documents for

the total limits and to close and open a new

account , to obviate disturbing the security

mortgaged. It is sufficient to take

documents only for the enhanced portion

of the limits or the additional facility.

Procedure to be followed by our bank

while ceding second charge on current

assets in favour of financial institutions.

30. Branches must obtain prior

approval of the competent authority

before ceding second charge on the

current assets of the company. Further

our ceding second charge on the

current asset should be on a reciprocal

basis. Hence branches should only

agree for ceding second charge on the

current assets provided Financial

Institutions cede in our favour second

charge on the fixed assets to secure

the working capital facilities extended

by us to the company. Further

branches are aware that by our bank

ceding second change on the current

assets in favour of the Financial

institution, we cast upon ourselves the

responsibility of safeguarding.

Financial Institutions interest also. Our

responsibility towards Financial

Institutions includes informing

Financial Institution, the fact that our

bank is contemplating action against

the borrower for realisation of our dues

and to pass on the surplus, if any, to

the Financial Institutions. Hence

branches should keep with the

documents, our letter ceding second

charge in favour of the Financial

Institution and also make note of the

same in “Document Execution

Register”. Similarly branch should

record the fact that Financial

Institution have ceded second charge

on the fixed assets in favour of the

bank. Draft of No-objection letter to be

given to the borrower in respect of

ceding second charge on current

assets is appended in Annexure 16.

Procedure for creation of second

charge on fixed assets in our

favour, where first charge has

already been created in favour of

other financial institutions.

31. As first step, a consent letter/no

objection letter from the first charge

holder either addressed to the

borrower or bank should be obtained

for extending second charge on fixed

assets for facilities granted by the

bank. Normally the first charge

holder will address the consent letter

to the borrower added with some

conditions. Thereafter,

hypothecation deed will have to be

obtained by bank creating second

charge on machinery. Then an

authorisation letter should be sent

by the Bank to the first charge holder

requesting them to act as agent for

the purpose of extending the

mortgage.

In order to extend the mortgage by

way of equitable mortgage, the

borrower should call at the office of

the first charge holder and authorise

them to continue to hold the title deeds

on behalf of the Bank also as

continuing collateral security for the

working capital facilities or any other

facilities granted/to be granted by the

Bank. Subsequently, the borrower

should confirm his representation by

writing a letter to the first charge

holder with a copy endorsed to the

Bank. Based on such representation

and the letter received from the

borrower, the first charge holder

should confirm in a letter addressed to

the Bank that the mortgage has been

extended in favour of the Bank.

When a borrower is a limited

company, Board resolution should be

passed authorising a Director to

extend the mortgage and execute

necessary documents as may be

required by the Bank for purpose of

creating a second charge on the fixed

assets.

The extended mortgage will cover the

fixed assets such as land, building,

fixtures, fittings, plant and machinery

(fixed) in order to have a second

charge on movable machinery, it may

be necessary to have hypothecation of

machinery, for the concerned limits as

stated above. When any of the

working capital limits such as cash

credit/packing credit is already

secured by stocks by a hypothecation

deed F.251B/F 110A a supplemental

hypothecation deed in F 110H should

be obtained for securing machinery. In

respect of other working capital

facilities for which there is no earlier

letter of Hypothecation, F110E should

be taken for the aggregate of such

limits mentioning therein the schedule

as:

“All present and future machinery of

the borrower including vehicles at the

factory premises or elsewhere.”

In respect of Limited Company

borrower, modification of charge

should be filed based on F110-H in

respect of limits for which charges

have been already filed on stocks. In

respect of other limits, fresh charges

should be filed based on F110E.

On extension of mortgage also these

charges may have to be modified.

In order to put notice of our Bank

holding the second charge on

machinery branch should arrange for

display of a hypothecation board with

the following wordings at the business

premises/ factory of borrower after

obtaining the consent of the first

charge holder.

The machinery in this premises are

hypothecated to:

1)………………………………Bank

……………….(Name of the first

chargeholder)

2.Indian Overseas Bank

Refer Annexure regarding format of

letters/undertaking to be executed.

32.Where lending rate is at par or

has gone below RBI lending rate:

Wherever advances are granted with

lending rates at par or below the RBI

lending rate, branches may henceforth

obtain DPN which does not contain

RBI interest clause.

Accountability

33. No advance should be released

without first obtaining proper

documents complete in all respects.

The second in command of the

branch (i.e) Assistant Manager

/Deputy Manager/Senior Deputy

Manager /Manager/Senior Manager,

as the case may be, should give a

certificate to the Branch Manager

before disbursement of advances that

all the relevant documents for

releasing the facility have been

obtained duly filled in and completed

and signed by the execucants in the

capacity intended. The format of the

certificate is given in Annexure 13.

This certificate should be obtained in

respect of each loan/advances.

Branch Chief Manager /Senior

Manager/Manager/Senior Deputy

Manager/Deputy Manager should not

disburse the loan/credit facility without

obtaining this certificate.

The branches manned by only one

officer (i.e) Manager, the Manager

should himself send the above

certificate to his Regional Manager as

per Annexure 14.

Death of Borrower

34. On receipt of the report that a

borrower is deceased, the branch

should take up the matter immediately

with the respective Regional Office

regarding documentation, Branch

should simultaneously obtain a letter

of undertaking as per Annexure 35

signed by all the legal heirs of the

deceased borrower.

PART-II

DESCRIPTION OF DOCUMENTS WITH

DISTINCTIVE NUMBERS

PART – III

TYPES OF ADVANCES AND DOCUMENTS TO BE TAKEN

Part IV

GENERAL GUIDELINES ON EACH TYPE ADVANCE

Advances against Government

Securities/Relief Bonds/

National Deposit Scheme

1. Ensure ownership of the borrower

or the guarantor, as the case may

be, of the security.

2. Owner should deliver the security to

the Bank, duly endorsed in favour

of the Bank

3. In case of advance against security

standing in the name of third party,

obtain letter from the owner

authorising the Bank to hold the

certificate as security for the

advance to the borrowers.

4. Obtain documents as per

instructions.

5. Forward the Government

Promissory Notes to Public Debit

office to ensure that endorsements

are in order and Government

Promissory Notes are genuine (If

there are a number of

endorsements, ask the party to

have in renewed before

endorsement to be Bank).

6. Enter all the particulars in the

Security Ledger and Loan Ledger.

7. Retain margin as per instructions.

8. On obtention of the Government

Promissory Notes from Public Debt

Office, release the loan amount.

9. In the case of National Deposit

Scheme, Bank should get the

deposit receipt discharged by the

depositor, without specifying any

date on the reverse of the receipt in

the column “Receipt of Discharge”

at the time of granting advance.

Advance against Indira Vikas Patra

1. Obtain documents and

application cum security deliver

letter as Annexure 15.

2. Repayment programme not to

exceed 36 months depending

upon the maturity pattern of

patra.

3. Margin at such stipulated rate of

paid up value of patra inclusive

of interest accrued for each

completed year from the date of

issue.

4. Indira vikas Patra are payable

only on the due date, and

premature closure is not

permitted. They are payable on

maturity to the holder and no

endorsement is required. No

lien can be registered, as the

patra are issued without

mentioning the name, Branch

should be very careful for the

sale custody of the patras

lodged to them as security.

Advance against National

Savings Certificate/ Kisan Vikas

Patra/10 year social security

certificate

1. Ensure ownership of borrower

or guarantor as the case may

be, of the security.

2. Retain stipulated margin on the

face value of certificate at the

time of granting advance.

3. Borrowers should not

discharge NSCs if they are

pledged as security. At the

time of enforcement of

certificates, they are to be

discharged by the bank, as

bank being the pledgee is

deemed to be the holder of

certificate as per rule No.16(i),

of National Savings Certificate

Rules, 1982 Refer Annexure

12.

4. When the loan is fully repaid

return the certificates to the

borrower along with the letter

addressed to Post Office

concerned informing that loans

have been paid and the

certificates may be transferred

into the name of pledgor.

Obtain acknowledgement in

F396.

5. For advance against Kisan

vikas Patra, documents as

applicable to advance against

NSC may be taken with

suitable modification.

6. For advance against 10 year

Social Security Certificate,

documents as applicable to

advance against NSC may be

taken with suitable

modification. Margin on the

invested value of certificate

and suitable repayment

programme not exceeding 36

months may be fixed

depending upon maturity of

certificates.

Margin and repayment as per

stipulation in the sanction or latest

guidelines, if any

Advances against Units of Unit

Trust of India

1. Obtain documents as

applicable to Govt. Securities.

2. Obtain relative Unit Certificates.

3. Obtain blank transfer deed

signed by the owner of the

Units.

4. Obtain letter of authority as per

Annexure 7.

5. Forward the letter of authority to

the office of the Trust.

Forwarding letter as per

Annexure 8.

6. Follow-up and obtain the

confirmation that the Unit Office

had made a note on its record

that the certificate is held in the

Bank as security and the grant

the advance.

Advance against Term Deposits

1. Obtain prescribed document

and got the deposit receipt duly

discharged by the depositor(s).

2. Enter particulars in the Loan

Ledger, particulars must contain

the details of security, its

distinctive number, date of

issuing of security its maturity

date and value etc.

3. Verify the signature of the party

with specimen on record.

4. Prepare the debit cash voucher

in case loan is disbursed as

cash or transfer debit voucher

and credit voucher crediting the

amount to the account as per

instructors of the borrower, in

writing.

5. Post the amount in the loan

ledger.

6. In case of loan against Term

Deposits (Fixed Deposit

/Recurring Deposit) record the

lien in the Term Deposit register

and Due date Register in the

case of fixed

Deposit/Reinvestment Deposits.

Also record on the face of the

receipt or RD pass books as the

case may be “UNDER LIEN TO

BANK’ in red ink.

7. In case of term deposits held at

a different branch, before

granting the loans forward the

deposit receipt duly discharged

under Regd. Post and ensure

(1) Verification of the discharge

of the FDR (2). Lien has been

marked in the books of Deposit

Receipt issuing branch.

8. Margin for advance against

deposit receipts should conform

to the directives on the subject

from the Reserve Bank of India.

Retaining a margin lower than

prescribed by the Reserve Bank

of India should be avoided.

9. In case where deposits stand

more than in one name and where

all the depositor are not able to

discharge the deposit receipt, the

depositors, who discharges the

receipt should be authorised by all

the other joint depositors to

discharge the receipt for the

purpose of availing of an advance

from the bank there against.

* F60 H is Loan Application-cum-letter

of Authority. If the borrowers(s) and

depositor(s) are different, the Loan

Application should be signed by the

borrower(s) and the Letter of Authority

should be signed by the depositor(s).

Advance against Shares and

Debentures

Ensure

1. Actively Quoted Shares and

debentures of limited liability

companies registered under

the Companies Act, declaring

dividend for the last 3 years.

2. Shares are fully paid for

3. Shares stand in the name of

the borrower as far as

possible.

4. Any alteration in the share

certificate bears attestation by

the company under its stamp.

5. Neither torn nor stamped with

any Bank stamp nor mutilated.

6. Shares not of a private limited

company.

Procedure

1. Obtain prescribed documents.

2. All shares under pledge to the

Bank are accompanied by Blank

Transfer Deeds in duplicate signed

by the shareholder duly witnessed

by other than husband or wife of

the shareholder. Witness is to be

easily traceable.

3. One set of transfer deed is to be

dated and other undated. In the