managing your company by the numbers presented by judith miller, j. miller & company 1 sponsored...

TRANSCRIPT

MANAGING YOUR COMPANY BY THE NUMBERS

Presented by Judith Miller, J. Miller & Company

1

Sponsored by:

I - INTRODUCTIONS

My goals: To define, simplify and track the numbers essential to

the operation of a successful construction company I hope that you will be able to:

To identify major components of success at each stage and for every function;

To determine which measurements of success are appropriate for your company;

To understand how to develop the processes for obtaining reliable and timely measurements;

To balance simplicity with completeness in your measurements.

2

FIRST, SOME GUIDELINES

We’re going to look only at what is vitally important to the discussion; we won’t become mired in minutia;

We’ll work from the point of view that simple is better – “KISS” in action;

We’ll use the 80/20 rule to separate the vital from the “noise.”

3

UNIQUE QUALITIES - Construction companies share some unique

qualities: Each project is unique; A project works against schedules & budgets to

produce specific results; A construction team cuts across many organizational

& functional lines involving every department in the company;

Projects come in various shapes, sizes & complexities.

4

SOME DEFINITIONS:

WHAT IS A SYSTEM? A system is a series of

instructions which, when followed by employees suitable for the job, produce the same desired result every time

The “desired result” for good financial management consists of accurate and timely reports, both company and job

The appropriate level of reporting detail depends on the company’s stage of growth

DEFINITIONS, AGAIN WHAT IS MANAGEMENT?

To manage: to control the course of affairs by actions (1609)*

Manager: one skilled at handling the affairs of a business (1705)*

“If you hire, fire or spend money in your job, your job is one of management.” (1)

“Accounting and other related financial control disciplines are the most neglected control functions in contracting firms. The result … is a wide variety of operational problems.”

* Oxford English Dictionary

WHY NUMBERS MATTER ? The Best case: used before the fact

to predict and plan and thereby control;

The Worst case: never done, the company runs from crisis to crisis;

Better than nothing: done after the fact as historical analysis thus providing some benchmarks against which to relate the future.

“Every time a number is calculated and understood, thinking takes place. Thinking leads to action.” (101 Business Ratios)

7

NUMBERS DRIVE RESULTS - Owner & managers’ job is to

understand how to use the financial/job cost information to better manage the business

We need not only the information from the financial and job cost reports themselves, but also information correlated across multiple reports at one time.

From this information we establish goals, put into place strategies and tactics to meet those goals and then measure our progress toward them.

8

RATIOS, BENCHMARKS & TRENDS -

Ratios compare one number to another: Typically expressed as a percentage (such as gross and net profit); Sometimes expressed as a single number (such as AR turnover). They allow us to discuss complex financial terms in simple

language. When we say our slippage is 25%, we know we’re completing our jobs 25%

less efficiently that we bid them – that is we’re over budget. Solve this problem to increase our gross profit dollars and therefore, given

good overhead control, our bottom line.

Combine with another ratio to form an index For example - the success equation

Customer satisfaction + net profit: by itself, net profit does not predict future success. A flash-in-the-pan start-up company can produce high net profits, only to fail the next year. Happy customers, on the other hand, drive repeat business.

Combine these two metrics to form the Customer Satisfaction Net Profit Index — CSNPI or “Snippy.”

9

BUILD YOUR OWN “SNIPPY”- Set a net profit goal (something between 5% and 12%

is right for most construction companies). Use your past history as a guide, but set a goal one or two percentage points higher than previously attained.

Measure customer satisfaction. This requires writing a simple customer-satisfaction survey that scores answers on a 1-to-5 scale. A good target score is 4.

Add the two together. If net profit for the first half of 2011 averaged 6%. Set a new net profit goal of 7.5%. Add that to the Customer Satisfaction target of 4, and the Snippy benchmark for the second half of 2012 is 11.5 (7.5 + 4).” [From the Benchmark Column in Remodeling Magazine, September 2005

10

OTHER CRITICAL RATIOS/INDEXES Slippage – measures the inefficiency (or increased efficiency) of

production Bid gross profit – produced gross profit / bid gross profit 38% - 34.3% / 38% = 9.7% ( NOT 3.7%, a huge difference)

Labor burden – measuring the total costs to the company of maintaining employees provides a good measure of the company’s ability to develop a strong culture where all employees Total labor costs (per hour or annualized) – gross wages / gross

wages $39 - $20 / $20 = 95%

Owner pay - correlating total costs for owner compensation to total volume provides a good reflection of not only owner success but allows the owner to compare his/her earnings to others. Total owner pay / total volume $100,000 / $1,000,000 = 10%

11

CRITICAL RATIOS/INDEXES - 2 Back log - this ratio relates the total amount of

work to be produced to the annual volume budget projection and reflects how quickly the company might run out of work. $ in backlog / annual budget volume x 12 months $450,000 / $1,500,000 x 12 = 3.6 months

Current ratio - this ratio tells you whether or not you have enough working capital in current assets (those to be converted into cash within the next rolling 12 months) to cover your current liabilities (those to be paid within the same period). Current assets / current liabilities $250,000 / $125,000 = 2

12

CRITICAL RATIOS/INDEXES - 3 Debt to equity - Debt to equity – tells

you who really owns the business, creditors (total liabilities) or you as owner (equity). Total liabilities / Total Equity $350,000 / $350,000 = 1 to 1

Return on equity – this number tells you how much money your current investment in the company is generating. Net Income / Total Equity $150,000 / $350,000 = 42.8%

13

CRITICAL RATIOS/INDEXES - 4 AR/AP turnover net – as companies grow, they lose

focus on the time in which outstanding client invoices are paid, thus reducing the effective cash flow. This measurement tells you whether or not you’re borrowing to pay current liabilities or you’re receiving your accounts receivable collections rapidly enough to pay. AR / annualized volume x 260 – AP / annualized COGS x 260 $250,000 / $4,000,000 x 260 = 16.25 average days to collect your

receivable invoices $125,000 / $2,400,000 x 260 = 13.5 average days to pay COGS

payable invoices 16.25 – 13.5 = 2.75 days borrowing to fund our AP

14

BENCHMARKS - A benchmark provides a goal against which

we measure our performance. Standard benchmarks should be defined by

each company for the ratios critical to your performance above.

One of the most important benchmarks for any owner should be focused on meeting the owner’s retirement goals It is impossible to predict how much any

one individual needs for retirement, however if you’ve not established a benchmark for yours, in both lump sum and as an annual contribution, do so today – use the tools on the web, consult with a financial advisor or read up on the subject in your local library: whatever you do, DO IT NOW!

15

BENCHMARKS FOR YOU - Other benchmarks relate to departmental

efficiencies. Below are some of the most important. Marketing - % of annual volume spent on

marketing for companies > $3,000,000 = 4-5%: roofers might be significantly higher

Sales – visits to sales 70% Production – slippage < 2% Finance – net profit between 7 and 10% Owner – hours worked per week < 50 Customer satisfaction – 4 on a scale of 5

16

TRENDLINES - A benchmark is line in the sand against which

we measure ourselves. But comparing actual performance with a benchmark is a static measurement. Unless we've reached the goal, we have no idea whether we're moving closer to it or further away.

To find where we’re headed, we need trend analysis. A trend line is dynamic; it indicates which direction we have been moving and predicts which direction we will move in the future.

Use a rolling 12 month average to indicate trends, not just positions on the graph.

Source: “CEO Tools” by Kraig Kramers17

II - THE HEART OF THE MATTER At each stage of company

development, different metrics illustrate company progress

The goal should be reliable, consistent, timely and vital numbers appropriate to each stage

No more than 7 indicators should be tracked per function or department

Work towards the development of a company dashboard – the earlier you start to develop a dashboard the more useful it becomes

18

MEASUREMENT BY FUNCTION -

Regardless of the stage of growth and regardless of the product sold, each company must control 5 primary functions: Leadership & ownership Marketing, sales & estimating Production Finance & administration Resource development

19

LEADERSHIP & OWNERSHIP In many remodeling companies,

the owner also provides leadership; they are, however, distinctly different: Ownership provides vision,

strategy and direction Leadership turns that vision,

strategy and direction into measurable actions

As companies move through stages 1 through 5, ownership and leadership functions become more complex & diverge

20

MARKETING, SALES & ESTIMATING -

Marketing, sales & estimating are all part of the primary business function of bringing appropriate work to the company and selling it to the client’s budget Marketing: develops the company

image in the eyes of the community Sales: turns potential contracts into

actual Estimating: quantifies expectations

derived from the sales process

21

BASIC #s - M/S/E -

MARKETING & SALES:

Leads/visits/sales % Most profitable job type Average job size Close ratio % $ per lead

22

PRODUCTION - Production makes reality of the sales

concept: Primary goal: to finish the project safely

On time On budget As specified

Primary components: Construction execution plan Field schedules – time plan Construction budget - money plans Resources plan – people, materials & money

Primary method: plan, organize & control

23

BASIC #s – Production

Average labor burden % Slippage in % Bid gross profit % # FTE (full time equivalents) Productivity / FTE Company current capacity Customer satisfaction

24

FINANCE & ADMINISTRATION - Finance & administration

measure and assist all other components of company processing Determine and compile

measurement standards Evaluate and develop

process and procedure standards

Monitor and control departmental communications

25

BASIC #s - Finance

Break-even $ Working capital $ Produced GPM % Net profit % AR/AP turnover

26

RESOURCES - Resources -projects and

protects the company’s ability to produce to the promised level of quality Resource development

determines how best to apply company resources, including cash, equipment, employees and subs

Resource development controls career paths, job descriptions & evaluations and employee motivation

27

BASIC #s - Resources

# employee reviews scheduled/held # W-9s missing when preparing

1099s Insurance costs as % of annual

volume # employees participating in 401(k),

HSA, etc. Workers’ comp mod rate

28

MEASUREMENT BY STAGE - 1 Owner does it all and

manages finances simply: Looks at the past – only at tax

time Cash based income statement Overhead mixed with COGS Sole proprietor business type Uses mark-up to calculate bid

price NEEDS to understand job

costs and to learn basic bookkeeping principles

#s AT STAGE 1

Marketing: customer satisfaction Sales: most and least profitable job

types Estimating: # hours per contract $ Finance: start up equity & net

profit Resource development: # hours

worked Ownership: personal annual

budget

MEASUREMENT BY STAGE - 2 Owner begins to delegate and

develops greater need for financial management: Moves to computer-based registers Separates overhead and COGS Changes in company structure require

better financial organization: Hiring employees Purchase of tools and vehicles

NEEDS to understand overhead and to learn to read monthly profit/loss

#s AT STAGE 2

Sales: visit to sale ratio; average job size

Production: bid & produced gpm Finance: overhead % and $; annual

profit plan Resource development: employee

productivity Ownership: retirement funding needs

MEASUREMENT BY STAGE - 3

Owner delegates everything EXCEPT sales: Considers incorporation Moves into out-of-home office space Quantity and complexity of information increases Employees become important part of company

structure – require accurate costing information to assist estimating

Job costing becomes imperative NEEDS to understand the Balance Sheet and to

learn ratio analysis

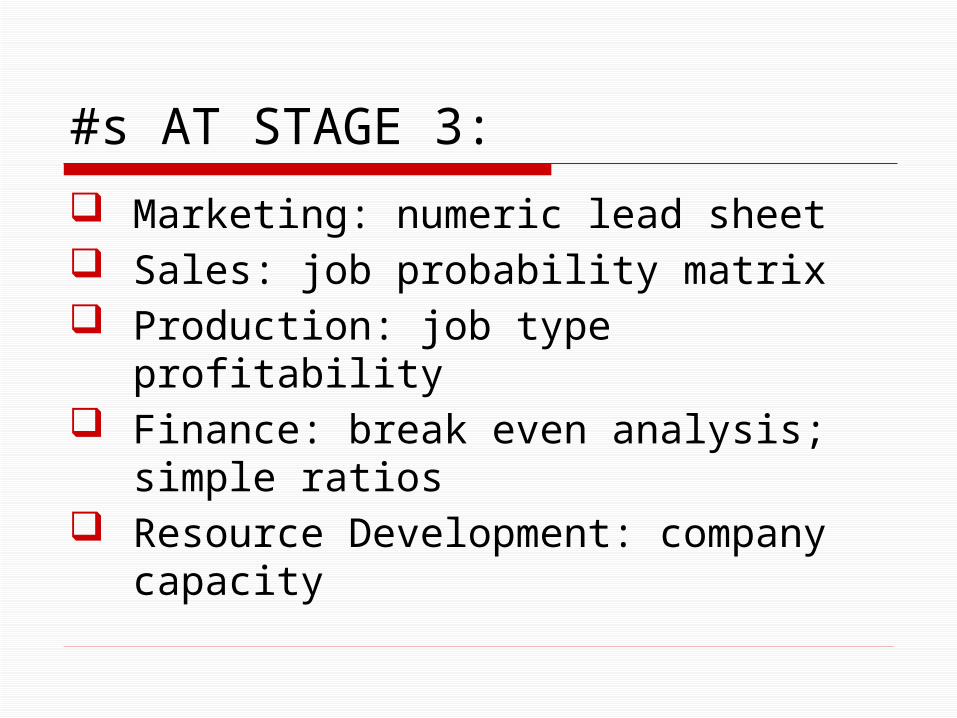

#s AT STAGE 3:

Marketing: numeric lead sheet Sales: job probability matrix Production: job type profitability Finance: break even analysis; simple

ratios Resource Development: company

capacity

MEASUREMENT BY STAGE - 4

Owner delegates everything Financial management is

now dispersed among company departments

Simple, accurate and timely benchmarks used by the owner, prepared by others

Planning becomes more important

NEEDS to understand trend analysis and cash flow projections

#s AT STAGE 4:

Marketing: cost per lead; cost per sale Sales: sales person productivity Estimating: unit and assembly costing Production: partial incentive based

compensation Finance: ROE; cash flow projections Resource development: training budget Ownership: board of directors

MEASUREMENT BY STAGE - 5

Owner positions company to operate without him/her

Effects of previous financial management decisions are now apparent: Does the company have value

independent from the owner? How is that value measured? Can it be reproduced? At what cost?

#s AT STAGE 5:

Marketing & sales: predictable lead sources

Production: slippage <2% both for job as a whole as well as by line item

Finance: 3 year budgets for P&L, balance sheet and cash flow

Resource development: employee productivity increases

Ownership: exit strategy goals

WHY BUILD A DASHBOARD -

A dashboard looks at company performance from a macro view

A dashboard turns data into information

Information can be more easily understood by more people

Graphic information tells a story The more complex the

organization the more useful a dashboard.

39

40

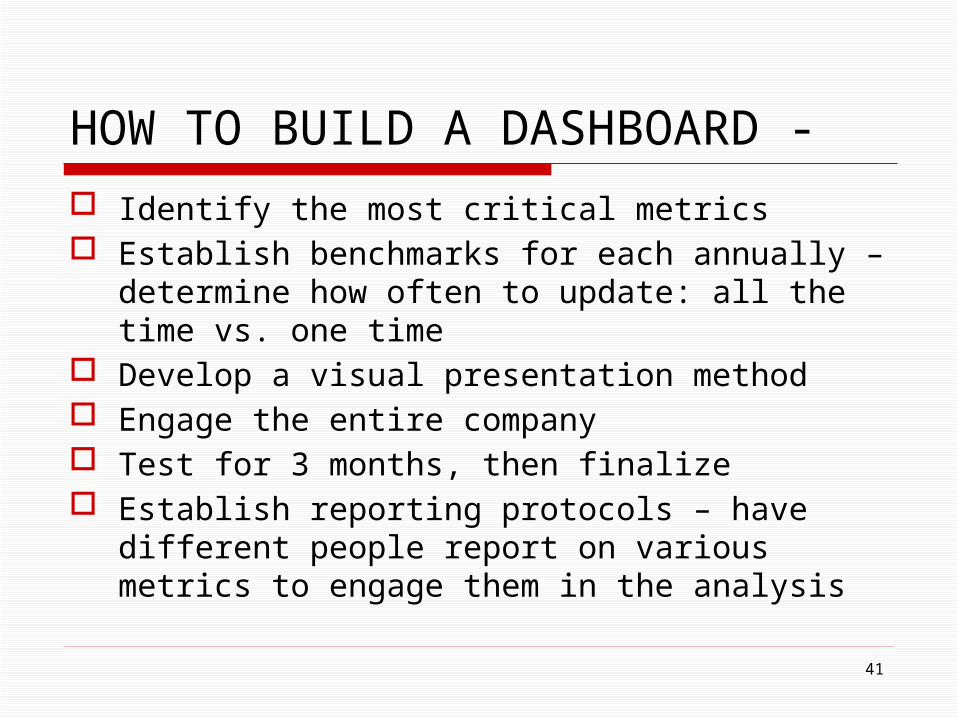

HOW TO BUILD A DASHBOARD -

Identify the most critical metrics Establish benchmarks for each annually –

determine how often to update: all the time vs. one time

Develop a visual presentation method Engage the entire company Test for 3 months, then finalize Establish reporting protocols – have different

people report on various metrics to engage them in the analysis

41

42

WHAT’S THE POINT ? Running a business consists of:

Selling a product Producing it Managing the organization

Running by the numbers in every department at every stage is critical to the success of any company

If this type of management is not your interest, sub it out as you do board up!

43

QUESTIONS & ANSWERS -

Thank you for your attention! Thank you to Business

Mentors for inviting me to speak with you today.

Contact me at: jfmiller@remodelservices.

com www.remodelservices.com

44