managing longevity risk presenter(s): jennifer haid · page 5 institutional approaches to managing...

TRANSCRIPT

Longevity Seminar

Sponsored by

Managing Longevity Risk

Presenter(s):

Jennifer Haid

Management of longevity risk

Jennifer Haid

24 February 2015

Page 2

Agenda

The Who? What? Where? Why? And How? of longevity risk

management:

► Part 1: The institutional market

► Part 2: The retail market

Presentation title1 January 2014

Page 3

The institutional market

1 January 2014 Presentation title

Page 4

NL

UK

Longevity’s global footprint

CAN

Growth market: Indexed benefits; mark-to-

market accounting and good saturation of

DB plans.

A limited number of transactions have

been executed; however, the first buy-in

transaction closed in 2013; and the first

longevity swap was executed in 2013

covering $150 million of liabilities.

Estimated size of CND DB market is $1.4

trillion USD (approx 45% private). 1

Existing market: significant deal flow of

buy-in, buy-out and longevity transactions.

Total value of private sector DB liability in

excess of 2.3 trillion USD (approx 90%

private) 1; current appetite from UK insurers

is only 10 billion GBP per annum.

US market highlights Canadian market highlights

► A prolonged low interest rate environment and a decade of poor

asset returns have lead to significant unfunded liabilities

► Plan sponsors are educated and know the issues; but do not

have the resources to sell off the risks

► Many US plan sponsors are considering implementing asset

focused solutions like LDI; a smaller subset are showing

increased interest in discussing risk transfer strategies.

► New accounting regime is in place effective Jan 1, 2013

► Update tables and mortality improvement scales have been

released that can be customized to the underlying population (i.e.,

by income band)

► Larger corporate plans and holders of closed DA blocks are

quantifying the true life expectancy of their participants and

evaluating risk mitigation techniques

USA

Growth market: Corporate sponsors are

developing de-risking strategies to manage

the financial and longevity risks associated

with DB plans.

Buy-in transaction executed in 2011; Buy-

out transactions continue to be executed:

there is sizeable deal flow at the mid-

market level and in the jumbo market.

Estimated size of US DB market is 7.9

trillion USD (approx 70% private). 1

Potential growth market: top 4 Dutch

pension funds showed significant

increases in liabilities following recent

improvements in life expectancy.

The Dutch market is the second largest in

the EU: Estimated size of DB market is

$1.3 trillion USD (approx 70% private). 1

Whilst a number of transactions have been

completed, the market still developing.

1 Source: Towers Watson, “Global Pensions Asset Study 2014”, January 2014

Page 5

Institutional approaches to managing the risk

Plan sponsor

Pension fund Insurer

Plan participants

Description

Str

uctu

re

Buy-out

Company and trustees transfer all risk to

a third-party insurer

Individual annuities are purchased for

members of the pension plans

Insurer is responsible for plan

administration

A group annuity to be held by the Pension

Trust as a plan investment is purchased

Plan sponsor may require collateral

against insurer default

Plan sponsor is responsible for plan

administration

Buy-in

Plan sponsor

Pension fund Insurer

Plan participants

May be implemented as part of a broader

LDI strategy

Actual longevity experience is swapped

for the counterparty’s expectations of

future longevity experience

Longevity insurance

Plan sponsor

Pension fundProvider / counter

party

Plan participants

Ris

k r

eta

ined b

y

corp

ora

te

None. Policyholder behavior risk (withdrawal,

early retirement, etc.)

Operational risk (plan administration)

Regulatory risk (financial reporting,

PBGC, etc.)

Fiduciary obligation

Interest rate and inflation risk

Market and credit risk

Policyholder behavior risk (withdrawal,

early retirement, etc.)

Operational risk (plan administration)

Regulatory risk (financial reporting,

PBGC, etc.)

Fiduciary obligation

Ris

k a

ssum

ed b

y

carr

ier

Interest rate / inflation risk

Market and credit risk

Policyholder behavior risk (withdrawal,

early retirement, etc.)

Operational risk (plan administration)

Regulatory risk (financial reporting,

PBGC, etc.)

Longevity risk

Interest rate / inflation risk

Market and credit risk

Longevity risk

Longevity risk

Page 6

Risk transfer in action

► Corporate sponsors in the US market are looking for innovative solutions to manage the risk in their plans and the market is developing quickly

► The table below highlights recent notable transactions in the US market.► The total annual volume for the US market of the regular ‘flow’ market (defined as transactions

under $1 billion) is estimated at $3-$5 billion in 2014.

Provider Description Pension liability

settled

Date

Motorola Annuity purchase, lump sums $3.1 billion 2014

Bristol-Myers Squibb Annuity purchase $1.4 billion 2014

GM Annuity purchase, lump sums $26 billion 2012

Verizon Annuity purchase $7.5 billion 2012

Hickory Springs Protected buy-in $75 million 2011

Total transactions USD $38.1 billion

In the past five years, corporate plan sponsors have upgraded their self assessment of their

awareness and effective management of the financial risks associated with their DB plans; however, longevity risk remains poorly understood.

Page 7

Evolution of solution development in the US and Canada

► There has been increased focus by UK plan sponsors on de-risking their plans This has led to more plans targeting buy-in and buy-out transactions as a long term strategy.

► The market has evolved from simple buy-out and buy-in arrangements to include “do-it-yourself” buy-ins and collateralized buy-ins

► The graphic below summarizes the most recent innovations in product design.

► Corporate sponsors are looking for innovative solutions to manage the risk in their plans and the market is developing quickly

► For Canadian companies, longevity risk has become a risk to be monitored

► In the US, individual lump-sum ‘buy-outs’ are gaining traction; Motorola, Ford, GM and Verizon have included lump sums as part of their de-risking strategies

► In the past five years, plan sponsors have upgraded their self assessment of their awareness and effective management of the financial risks associated with their DB plans; however, longevity risk remains a challenge. Large plan sponsors are engaging industry experts to help quantify the risk

► In both markets, buy-out and buy-in transactions have been executed within the past few years and deal flow is growing.

United States and CanadaUnited Kingdom

*Ernst & Young, “Insurance solutions for pension schemes, Insurance Provider Survey”, July 2014.

Page 8

The retail market

1 January 2014 Presentation title

Page 9

► Four out of ten newly retired couples will outlive their financial assets if

they attempt to maintain their pre-retirement standard of living (9 out of

10 for those without DB income)

► Americans like these must plan to reduce their standard of living by an

average of 20% to minimize their likelihood of outliving their financial

assets (40% for those without DB income)

► Seven out of ten middle market households approaching retirement will outlive their financial assets if they attempt to maintain their pre-retirement standard of living (nearly 10 out of 10 for those without DB income)

► Americans like these must plan to reduce their standard of living by an average of 30% to minimize their likelihood of outliving their financial assets (50% for those without DB income)

The middle American retirement problem

Source: Americans for Secure Retirement and Ernst & Young as of February 2009

Page 10

Products to address the middle American retirement problem

► A starting allocation of insurance, investment, and annuity products that satisfy the desired outcomes of the individual

► Investment Products► Mutual funds

► Dividend solutions

► Bond and CD ladders

► Market-linked securities

► Separately managed accounts

► Income protection► Investment-linked or synthetics

► Annuities and variations

► Insurance products► Life insurance

► Long term care insurance

Investments

InsuranceIncome

Advice

Page 11

Sample case study

Susan Smith

► Demographics

► Current age: 65

► Retirement age: 65 (this year)

► Gender: female

► Marital status: single

► Net worth: $1 million

► Sources of guaranteed income

► Social Security: $26,000

► Pension: none

► Goals

► Income: maximize spending in retirement

with a high likelihood of not exhausting her

assets

► Bequest: none

Page 12

Sample case study (cont.)

Approach

► Simulation type: Monte Carlo

► Variable mortality

► Variable health care events

► Stochastic economic scenarios

► Interest rates

► Inflation

► Asset returns

► Asset volatility

Metrics

► Consumption = after-tax real income

► Real annual dollars Susan can consume while

succeeding in 90% of the tested scenarios

► Coverage ratio = severity of a shortfall

► Median percentage of Susan’s consumption target

which is covered by guaranteed income sources in

failed scenarios

On

On

On

Variable

Variable

Variable

Variable

Product Allocation

Equity 60%

Bond 40%

SPIA 0%

DIA 0%

VA with GLWB 0%

FIA with GLWB 0%

Benchmark portfolio

Measure Value

Success Rate 90%

Consumption $44,800

Coverage ratio 46%

Outcome

Source: EY Retirement Analytics™

Page 13

Sample case studyConsidering only mutual funds

Source: EY desk research, EY Retirement Analytics™

Page 14

Sample case studyConsidering mutual funds and annuities with GLWB riders

Source: EY desk research, EY Retirement Analytics™

Page 15

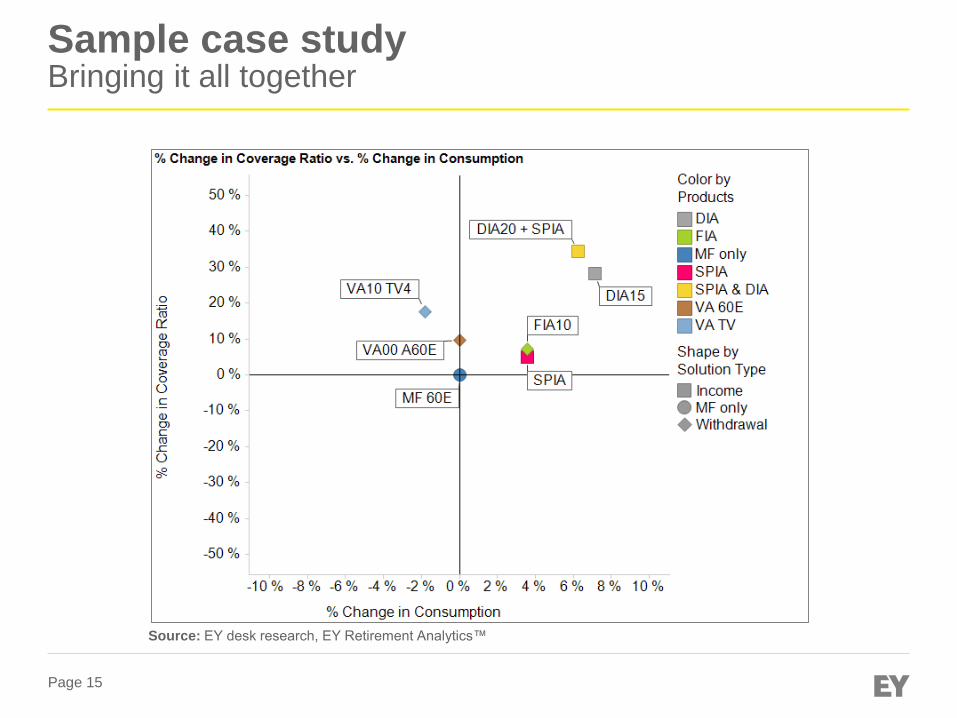

Sample case studyBringing it all together

Source: EY desk research, EY Retirement Analytics™

Page 16

Customer valueDo annuity products add value?

► The unique risks in retirement require different products/solutions/strategies

► Product allocation can incorporate investment, annuity and insurance solutions – and

evaluation through an outcome based framework allows for a direct comparison

40%

60%

Initial asset allocation

Bonds

Equity

12.5%

30.0%

45%

12.5%

Final asset allocation

SPIA

Bonds

Equity

DIA20

Demographics Single female, age 65

Portfolio value $1,000,000

Investment risk tolerance Moderate

After-tax, real income $44,800

Coverage ratio 46%

Income objective Maximize

Bequest objective None

Retirement risk tolerance Conservative

After-tax, real income $47,600

Coverage ratio 62%

Transactions

Life insurance None

Long term care None

For customers with income goals, portfolios that include annuity products can increase

consumption and provide downside protection in the event of failure.

Page 17

Key takeaways

► There is no silver bullet, but the US market continues to

evolve

► The understanding of longevity by the individuals and

institutions in the US market is the catalyst for effective

longevity management

Presentation title1 January 2014

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction

and advisory services. The insights and quality

services we deliver help build trust and confidence

in the capital markets and in economies the world

over. We develop outstanding leaders who team to

deliver on our promises to all of our stakeholders. In

so doing, we play a critical role in building a better

working world for our people, for our clients and for

our communities.

EY refers to the global organization, and may refer

to one or more, of the member firms of Ernst &

Young Global Limited, each of which is a separate

legal entity. Ernst & Young Global Limited, a UK

company limited by guarantee, does not provide

services to clients. For more information about our

organization, please visit ey.com.

© 2015 Ernst & Young LLP

All Rights Reserved.

ey.com