managing competition v2-3 - eth z · managing competition ... wb world bank ... intermediate...

TRANSCRIPT

EssayonDevelopmentPolicy

Managingcompetition

HowwillcontractfarmingandzoningofTanzania’scottongrowingareaaffectsectorperformance?

DerekGeorge

NadelMASCycle2010‐2012

March2012

ii

AbbreviationsAr/Br GradesforcottonqualityinTanzania:Arstandsfor“whiteclean”,

Brfor“dullstained”CDTF* CottonDevelopmentTrustFundECGA EasternCottonGrowingAreaFBG FarmerBusinessGroupFOT FreightonTruck(tradingexpression)GoT GovernmentofTanzaniaMOFA MinistryofAgricultureNGO Non‐GovernmentalOrganizationRLDC* RuralLivelihoodDevelopmentCompanySSA Sub‐SaharanAfricaTACOGA* TanzaniaCottonGrowersAssociationTCA* TanzaniaCottonAssociationTCB* TanzaniaCottonBoardTCMB TanzaniaCottonMarketingBoard(predecessorofTCB)TGT* TanzaniaGatsbyTrust ToT TrainingofTrainersWB WorldBankWCGA WesternCottonGrowingArea*DescriptionavailableinANNEX1:CottonStakeholders

iii

CottoninTanzania:FactSheet1Cotton is one of Tanzania’s main export commodities and contributes directly or

indirectly to the livelihoods of about 40% of its population. As a cash crop, cotton

representsamajorsourceofincomeandemployment,offeringeconomicopportunities

to between 350’000 and 500,000 smallholder farmers cultivating the crop on plots

rangingfrom1to10acres.Totalannualproductionvariesgreatly(between100’000to

more than 350’000 tons in good years), depending onweather conditions and highly

volatile world market prices. Once ginned, about 70 to 80% of the lint is exported,

mainly to Asia, while oil and cake is sold on largely informal domestic markets. The

remaining lint is used by the domestic spinning and textile industry. For a list of the

stakeholders in the Tanzanian cotton industry, see ANNEX1: Cotton Stakeholders.

Cotton cultivation is generally done manually under rain‐fed conditions and with

minimal use of inputs, such as fertilizers and chemicals. Cotton is handpicked, which

generallyentitlesapremiuminworldmarkets.Therearetwocottongrowingzonesin

Tanzania: thewesterncottongrowingzone (WCGA)of Shinyanga,Mwanza,Tabora,

Mara, Singida, Kagera and Kigoma

regions, accounting for 97‐99% of

production;and theeasterncotton

growingzone(ECGA)ofMorogoro,

Coast,Tanga,Iringa,Kilimanjaroand

Arusha regions producing the

remaining 1‐3%. Shinyanga and

Mwanza are the two largest cotton

growing regions. Planting begins in

Decemberfortheunimodalareasof

thewesternpartofthecountry,with

harvesting in late June and

marketingbeginninginAugust.

Planting begins between February

andMarchintheeasternportionofthecountry,withharvestinginearlyAugusttolate

October.

1ITCandTCB(2011:2‐5).

Source:TCB2012

iv

TableofContents

1Introduction.................................................................................................................... 1

2InputCreditandQuality:theChallengeofProvidingPublicGoodsinaCompetitive

Setting ............................................................................................................................... 4

2.1ABriefHistoryofSectorLiberalization .............................................................................................................4

2.2NegativeConsequencesonProductivityandQuality ..................................................................................5

3.ContractFarmingasPossibleSolution............................................................................ 6

4.NewRegulatoryFrameworkandCurrentStateofPlay ................................................... 7

5CategorizationandLessons ........................................................................................... 10

6Conclusion .................................................................................................................... 14

ANNEX1:CottonStakeholders......................................................................................... 15

ANNEX2:CompositionofKeyIndicatorsofSectorPerformance ...................................... 19

Bibliography .................................................................................................................... 20

1

1IntroductionUnlikethoseofotherAfricancountries,Tanzania’scottonsectorhasbeencharacterized

by a high degree of openness and competition ever since complete liberalization in

1994.Ahighnumberoflicensedcottonseedbuyers(currently35),thetopfiveofwhich

accountforonlyabout40percentofseedcottonpurchases(andthesetopfivetypically

changefromyeartoyear)2hasensuredthatproducersgetahighshareofworldmarket

prices (62%of the FOT lint price on averagebetween1990 and2005).However, the

sector has performed poorly onmaintaining quality control or assisting producers to

accessqualityinputsandextensionservices,aspresentedinmoredetailbelow.

In “Organization and Performance of Cotton Sectors in Africa”, a comprehensive

comparativestudyonbehalfoftheWorldBank,Tschirley,Poulton,Labasteetal.(2009)

have developed a conceptual framework based on the idea that “economic systems

benefitfrombothcompetitionandcoordination,butthatintherealworldofimperfect

markets andweak states there is likely to be a trade‐off between them”3. Along that

competition‐cooperationaxis, theyelaborateatypologyofcottonsectors inSSAbased

on the structure of the market for the purchase of seed cotton and the regulatory

framework inwhich farmersand firmsoperate.Theydistinguishnationalmonopolies,

localmonopolies,concentratedsystemsandcompetitivesystems,aswellashybridsof

the above. Inmonopolistic systems, cotton ginning companieshave an exclusive right

andimplicitobligationtobuyallcottonseedofferedbyfarmerseitheroverthewhole

territoryofthecountry(nationalmonopoly)oroveradelimitedgeographicalarea(local

monopoly).Theyfeature,ingeneral,asingle‐channelmarketingsystemforbothinputs

andoutputs. Concentrated and competitive systemsdiffer in that the former typically

hasalownumberofdominantbuyers,whereasinthelatteralargenumberofsmaller

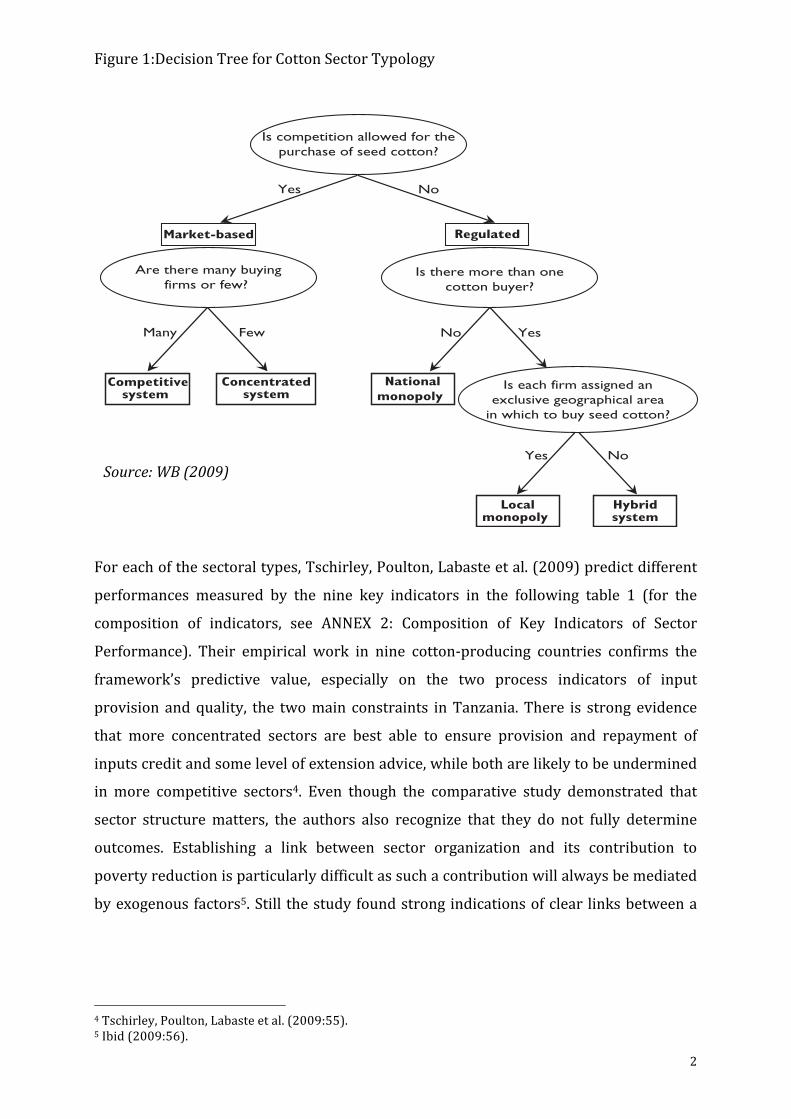

buyerscompetewitheachother.Thetypologyisillustratedinthedecisiontreebelow.

2Tschirley,Poulton,Labasteetal.(2009:47).3ibid(2009:XXVI).

2

Figure1:DecisionTreeforCottonSectorTypology

Foreachofthesectoraltypes,Tschirley,Poulton,Labasteetal.(2009)predictdifferent

performances measured by the nine key indicators in the following table 1 (for the

composition of indicators, see ANNEX 2: Composition of Key Indicators of Sector

Performance). Their empirical work in nine cotton‐producing countries confirms the

framework’s predictive value, especially on the two process indicators of input

provision andquality, the twomain constraints inTanzania.There is strong evidence

that more concentrated sectors are best able to ensure provision and repayment of

inputscreditandsomelevelofextensionadvice,whilebotharelikelytobeundermined

in more competitive sectors4. Even though the comparative study demonstrated that

sector structurematters, the authors also recognize that they do not fully determine

outcomes. Establishing a link between sector organization and its contribution to

povertyreductionisparticularlydifficultassuchacontributionwillalwaysbemediated

byexogenousfactors5.Still thestudyfoundstrongindicationsofclear linksbetweena

4Tschirley,Poulton,Labasteetal.(2009:55).5Ibid(2009:56).

!

46 POULTON AND TSCHIRLEY

Figure 4.1 Decision Tree for Cotton Sector Typology

Is competition allowed for thepurchase of seed cotton?

Yes No

Market-based Regulated

Are there many buyingfirms or few?

Is there more than onecotton buyer?

Many Few Yes No

Competitivesystem

Concentratedsystem

Nationalmonopoly

Localmonopoly

Hybridsystem

No Yes

Is each firm assigned anexclusive geographical area

in which to buy seed cotton?

Source: Authors.

For market-based systems, two further distinctions can be made: those with“many” buyers of seed cotton (competitive systems) and those with “few” suchbuyers (concentrated systems). Necessarily subjective, this distinction is never-theless meaningful when one compares a country such as Tanzania (more than30 buyers) with Zambia before 2006 (one dominant buyer, one large competi-tor, and two or three other very small buyers).

COMPETITION AND COORDINATION

Poulton et al. (2004: 521) defined coordination as “effort or measures designedto make players within a market system act in a common or complementaryway or towards a common goal.” They noted that the pursuit of effective coor-dination “may . . . require effort or measures designed to prevent players frompursuing contrary paths or goals.” In the neoclassical ideal of perfect competi-tion, the only coordination required is vertical coordination between players atdifferent levels of the system, and this coordination is fully achieved through

Source:WB(2009)

3

healthycottonsector,asmeasuredbythechosenindicators,andtheimpactofthesector

onpovertywithinagivencountry6.

Table1:ExpectedPerformanceacrossKeyIndicators

Source:WB(2009)In this framework, Tanzania embodies the “ideal” competitive sector: out of the nine

countriescomparedintheWBstudy,itistheonlyonetofullybelongtothatcategory.

However,twoyearsafterthepublicationofthestudyandwithhelpfromdevelopment

partners,Tanzaniahasembarkedonanambitiouspathtocomprehensivereformofits

cottonsectorinanattempttoaddresstheproductivityandqualityproblemsthathave

longpreventedittofullyexploitthesector’spotential.

Informedby thatconceptual framework, thisessaywillattempt tocategorize thenew

sector organization that will emerge from ongoing reforms within the typology

developedbyTschirley et al (2009).What typeof cotton sectorwill emerge from the

reform?WherewillthenewregulatoryframeworkplaceTanzania’scottonsectoronthe

competition‐cooperation axis? What are the prospects of resolving the quality and

productivity problems without compromising the gains liberalization achieved on

6Idem.

!

58 POULTON AND TSCHIRLEY

Table 4.3 Expected Performance along Key Indicators

Nationalmonopoly andlocal monopoly Concentrated Competitive

Process indicatorsQuality and

marketingMedium High Low

Pricing Low if left to companies alone

Low High

Input provision High Medium LowExtension High Medium LowResearch High Medium Low

Valorization of by-products

No clear prediction

Intermediate outcome indicators

Yield High High LowCompany cost

EfficiencyLow Medium High

Final outcome indicatorsFarmer welfare No clear predictionOverall

competitivenessNo clear prediction

Macro Impact No clear prediction

Source: Authors.

more difficult for companies to monitor than is input delivery. Third, even forcompanies committed to increasing farm-level productivity, the return toextension is likely to take longer to appear and to be more difficult to identifythan the return to input delivery. For all these reasons, commitment to exten-sion is likely to be harder to maintain than commitment to input delivery;especially where systems come under stress (for example, because of increasedcompetition in concentrated systems), extension effort may be sacrificed fornarrower loan monitoring and recovery.

As we close this chapter, it is important to note that the type and quality ofsector regulation will have a strong effect on performance for all indicators. Thejob of regulation may be thought of as seeking correction in areas where anunregulated sector is likely to perform poorly, while preserving that sector’sstrengths. The corollary is that the predictions in table 4.3 may be most accuratein situations where regulation is weak, which it typically is in Africa. However,as has already been described (chapter 3), there are ongoing efforts to buildmore effective regulatory regimes for the cotton sector in several of the study’sfocus countries.

4

pricingandefficiency?Theanswerstothesequestionswillguideanattempttoidentify

the implications of and apply pertinent lessons from theWB case study to the local

circumstancesinTanzaniatoinformthefurtherprocess.

Tothatend,thefirstsectionofthisessaywillbrieflyoutlinethedetrimentaleffectsof

theopeningof theseedcottonmarketto freecompetition.Chapter3willdescribethe

emergence of the consensus to address them through the introduction of contract

farming.Chapter4willoutlinetheboldnewrulesandcollaborativearrangementsthat

arebeingimplementedinthewholecountrypresently.Chapter5willcriticallydiscuss

thelikelyoutcomesofthereformalongsomeofthekeyindicatorsintable1andidentify

keylessonsfromTschirley’etal(2009)pertinenttotheTanzanianexperience.

2InputCreditandQuality:theChallengeofProvidingPublicGoodsinaCompetitiveSetting

2.1ABriefHistoryofSectorLiberalizationPriorto1994, formostofthepost‐independenceperiod, thesectorwasdominatedby

regional cooperative unions and primary societies that held a monopoly on cotton

production and ginning. Primary societies stored and sold cotton to the cooperative

unionsforafixedgovernment‐setprice,andtheunionsinturnginnedthecottonfora

fixed margin7. Export was still the responsibility of the government through the

Tanzania Cotton Marketing Board (TCMB). Together with the cooperative unions it

handled all marketing services for the industry, including the provision of seeds and

otherinputs.Bytheearlynineties,manycooperativeunionswerebesetbyproblemsof

corruption and financial mismanagement8. Most had accumulated huge debts, were

making losses andmanaged to surviveonly throughgovernment subsidiesanddonor

support9.Thisprompted theGoT to formally abolish themonopolyheldby theTCMB

and unions to allow free competition in cottonmarketing and ginning. Price controls

werereplacedbyindicativefloorfarm‐gatepricesannouncedatthestartoftheharvest

season. In a context of booming world market prices for cotton, enthusiastic private

operators rapidly captured significant market shares and gradually crowded out

cooperatives(onlyafewremain). Farmerswerepaidmorepromptlyupondeliveryof

their produce (cooperatives’ delayed payments and inflation had sometimes strongly

7Baffes(2002:2).8PoultonandMaro(2009:4).9Baffes(2002:3).

5

dentedfarmers’earnings)andreceivedasignificantlyhighershareofexportpricesthan

theydidpriortoliberalization10.Asaresult,cottonproductionrosesharplyin1995and

199611.

2.2NegativeConsequencesonProductivityandQualityHowever,asworldmarketpricesdeclinedandtheexchangerateappreciatedinthelate

nineties,themoreproblematicconsequencesofliberalizationbegantomakethemselves

felt and total production decreased strongly. As extensively discussed by Poulton &

Maro (2009) andBaffes (2002), the collapse of the cooperative‐led input distribution

scheme pushed up prices for chemical pesticides and seeds. Asmost farmers did not

haveaccess to credit to finance thepurchaseof inputsatmarketprices,useof inputs

declinedsharply,resultinginloweryields.Thecollapseoftheinputdistributionscheme

was most dramatic for insecticides, as the heavy competition for cotton made input

creditrecoveryrisky12.Evenseeddistribution facedmajorproblems,as investment in

oilmillsincreasedprocessingcapacityinthemainproductionzoneby50%,andmany

ginneriesdecidedtosellmoreseedtothemills13.Therelativelyeasyentryforprivate

actors favored the emergence of small‐scale traders not interested in providing input

credit. Many of the new private ginning companies purchased cotton on an irregular

basis, leaving their ginneries unutilized for a year or two either because they were

unable to secure working capital, or because prices were deemed too high to make

processing cotton worthwhile14. These companies had little incentive to invest in

downwardactivities.

QualityofTanzaniancottonalsosufferedfromliberalization.Besidesthelowerrateof

pesticideuse,competitionamongginnersalsoledtotheabandonmentofarrangements

for thegeographical separationofdifferent cottonvarieties suited todifferentnatural

environments,whichaffectedthegeneticpurityofseeds15.Despiteunder‐utilizationof

their ginneries, in the years immediately following liberalization cooperative unions

wereoftenunwillingtolettheirnewprivatecompetitorsrenttheirginneriestoprocess

theircottononacontractbasis.Thisencouragedtheexpansionofginningcapacity,as

10Ibid(2002:4).11PoultonandMaro(2009:1).12Tschirley,Poulton,Boughton(2006:15).13Idem.14PoultonandMaro(2009:13).15Baffes(2002:6).

6

thenewentrantsoftenhadtobuildtheirownginneries.Asaresult,buyershavetended

tobelessqualitysensitive,asthebenefitsofbetterutilizationoftheirginningcapacity

often outweighs the cost of accepting lower quality cotton. The practice of grading

cotton according to quality (Ar and Br) has largely disappeared, and handpicked

Tanzanian cotton that used to fetch a quality‐premium on world markets now faces

penaltiesforitsreputationofpoorquality.Cheatingonweightsandscalesduringcotton

purchase by middlemen has also encouraged deliberate contamination of cotton by

farmers who seek to artificially increase the weight of their product to offset their

losses16.

Finally,theindicativefloorpricesannouncedbythemainregulatorTCBatthestartof

every buying season still causes much disruption in marketing of cotton, as growers

mistake them for the fixed uniform government set prices of the pre‐reform era. At

times of soaring world market prices, and especially in regions where competition

among buyers is high, the actual price paid to farmers usually rises to significantly

higherlevelsthantheusuallyconservativeTCBindicativepriceastheseasonadvances.

There, farmerswhosoldearly tend to feel cheated.On thecontrary, in regionswhere

competition is restrained by remoteness and poor infrastructure, buyers enjoying

virtualmonopoliespurchasecottonfortheTCBfloorpriceeventhoughinneighbouring

regionsthecurrentmarketpriceisdoublethatamount,causingmuchdiscontentamong

farmers,whomayeventuallyabandoncottoncultivationcompletely.Conversely,when

worldmarketprices fall significantly in the courseof thebuying season,marketing is

alsodisrupted,asfarmersareveryreluctanttosellatapricebelowtheTCBindicative

price.

3.ContractFarmingasPossibleSolutionEventhoughratherinconsequentialschemeswereputinplacein2001toimproveinput

supply (CDTFandpassbookschemeseeANNEX1:CottonStakeholders), at theeveof

the regulatory reforms in 2011, Tanzanian yields and quality remained among the

lowest in SSA. Persistent ginner underinvestment in productionwas compounded by

underinvestment by growers themselves, either for lack of access to finance and

preferenceforlow‐inputextensiveproductionasamitigationstrategyagainstpriceand

weatherrisk.

16Cuvelier,Rüegg,Sigalla(2011:18).

7

Facedwith the challengeof deliveringpublic goods such as seasonal input credit and

extensionservicesinacompetitivemarketwithincompletepropertyrights,manyother

cotton‐producing countries in SSA chose to reverse the course of liberalization and

reinstate national or local monopolies. In Tanzania the political commitment to

liberalization remained strong. Stakeholders were looking for ways to preserve the

achievements of liberalizationwhilemanaging the adverse effects of competition to a

certaindegree.

ContractfarmingwasbynomeansanovelideawhenRLDC,aSwissNGOfirstpromoted

itinwesternTanzaniain2006/7.Itsprojectsthatincentivizedfiveginningcompaniesto

mobilize farmer groups for contract farming and providing them with a range of

services such as inputs, implements, extension and storage facilities on credit basis

demonstrated that contract farming could be an effectivemeans of tackling themain

bottlenecksofthesector.

In2008/9,theTanzaniaGatsbyTrust,asubsidiaryoftheGatsbyCharitableFoundation,

launched a similar pilot project in Mara region, and rapidly scaled up the project to

includeBariadidistrictofShinyangaregion(Bariadiproducesabout70%ofTanzania’s

cotton). By 2010/11, TGT had linked over 38’000 farmers to seven major ginning

companies.Even thoughon sucha scale credit repayment rates (for seeds,pesticides,

spraypumpsandcashloans)weremodest(58%overall),inputuseandaverageyields

rosesignificantly(to411kg/acrefromabaselineof310kg/acre)17,convincingtheTCB

toscaleupcontractfarmingnationwide.

4.NewRegulatoryFrameworkandCurrentStateofPlayIn January2011, theTCBannounced that starting2012, itwouldnot issue licenses to

cotton buyers who have not entered into contract farming arrangements with their

suppliers,i.e.providedaminimumamountofseeds,pesticidesandprivateextensionon

a loan basis to a minimum number of producers. The production contract templates

promotedbyTCBdonotincludepredefinedprices;theyonlycommitproducerstosell

their entire harvest to the contracting company within a certain timeframe at the

prevailingTCBindicativefloorprice(nobodywouldbewillingtosetapriceattimeof

17Anderson,Ian;TGT,pers.comm.,23.02.2012.

8

planting).Inordertobartradersandmiddlemenfromtheindustry,theTCBruledthat

onlyownersofginneries(endbuyers)wouldbeeligibleforlicensing18.

As contractual counterpart for the ginners and backbone of the new system, cotton

growersacrossthecountrywerecalledupontoorganizeintoFarmerBusinessGroups

(FBG).With TGT funding and using a ToT approach, task forces comprising of hired

professional trainers and district authorities were formed in 25 cotton producing

districtstosensitizefarmers,registernewlyformedgroupsandbuildtheircapacityon

agriculturalbusinessmanagementandagronomicpractices.Thefieldworkwascarried

out by 500 Ward Extension Officers (WAEO, public extension officers) under close

supervision from TGT hired trainers19. 9’829 FBGs had been formed as of November

2011,eachcomprisingofbetween50and70cottongrowers20.Thevisionwastomake

thegroupscreditworthyandcommerciallyviableagribusinessentities,withleadership

empoweredtomakemarketing,investmentandproduction‐relateddecisionsonbehalf

of their respective membership21. Under the new system, FBGs would negotiate

contractswithandcollect,bulk,storeandtransportthecottontothebuyers,andreduce

transactioncostsofservicedeliverytothefarmers.

In order to avoid the problem of side selling and credit default that had ridden past

experimentsincontractfarming,theTCBoptedforaparticulartypeofzoningsystemin

implementing its new policy. The approach consisted of dividing up all of the cotton

growingareainthecountryinto12clearlydelimitedzones(Table2)ineachofwhich

onlyalimitednumberofbuyerswillbelicensedtoenterintoproductioncontractsand

purchasecotton.Movementofseedcottonacrosszonesisprohibited.Ginnerswillhave

tocompeteforcontractsintheirallocatedzoneonthebasisofinputsandservicesthey

areabletoprovide.

In a second step, after a thorough audit of their books and equipment, ginners were

invitedtoexpresstheirinterestforoperationinamaximumoffivezones.Inanintense

negotiation process with ginners, for every zone TCB/TGT defined minimum

requirementsforlicensing,bothintermsofFBG’stosignupandinputcredittocommit

(channeledthroughtheCDTF).Ginnersacceptingtheresultingzonalrequirementswere

provisionallyawardedwiththerighttovieforcontractswithFBGsinthatzone.18TCB(2011).19Wise,Hillary;TNS,pers.comm.,02.05.2011.20TGTpresentation,Mwanza,03.11.2011.Manyofthegroupsformedonthemistakenexpectationofgettingfreehandoutshowever,sosomeoftheFBGssubsequentlydissolvedandre‐formedintofewer,more“serious”groupswishingtoengageinandrespectproductioncontracts.21TCB(2011).

9

Table 2 shows the number of groups ginners were able to sign up per zone, as of

February1st,2012.Notalloftheginnersmanagedtoqualifyintheirallocatedzones(red

backgroundmeansbelowminimum).Failingfulfillmentoftheminimumrequirements,

ginnerswill losetheright topurchasecotton in thatzone.Groupsthatsignedupwith

ginnersthatturnouttobeunqualifiedwillbereallocatedtootherginnersinthesame

zonewhofulfilltherequirements.

Table2:CurrentNumberofFBGscontractedperGinnerperZone

Source:TGT(2012)Asshown in the table, the totalnumberofFBGsundercontractamounted to3,686 in

earlyFebruary.AccordingtothelatestdatafromTGT,thenumberhasrisento4700as

the “signing season” ends and pesticides are being distributed to farmers under

10

contract22.Undernewrules,independentgrowersnotundercontractwillstillbeableto

market their cotton as usual (market transactionwith ginners), although they should

only be able to sell to ginners licensed in their zone. All information about FBG

membership,productioncontractssigned,extendedinputcreditaswellasseedcotton

purchasesandloansatisfactionisenteredintoadatabasedubbedPambaNettohelpall

stakeholderskeeptrackofmutualcommitmentsandeasetheenforcementofrulesand

monitoring.PambaNet canalsobeused to send textmessages toFBG leaders’mobile

phonesinordertokeepgrowersinformedonprices23amongotherthings.

Thelogicunderpinningthenewregulatoryframeworkisstraightforward.Asistypically

the case in environments characterized by strong competition and weak horizontal

coordinationamongfirms,goodsthatgeneratepositiveexternalitieslikeinvestmentin

inputcredit,extensionandqualitycontrolsystemsareunderprovided.Contractfarming

privatizesthebenefitsofsuchinvestments.Theformalizationofmutualcommitmentsin

writtencontractsrecordedinacentraldatabasetogetherwiththezoningarrangement

makes opportunistic behavior by both buyers and producers much more difficult.

Zoningismeanttostrikeabalancebetweenthetwoextremesofexcessivecompetition

underwhichcottonbuyersandprocessorswouldbereluctanttoinvestbecauseofthe

risk of side‐selling and credit default on the one hand, and a monopoly that would

severelypenalizefarmersbykeepingpriceslowontheother.

5CategorizationandLessonsInordertorelatetheinsightsoftheWBcomparativestudytothecurrentdevelopments

inthecottonsector,itmustbeattemptedtocategorizethetypeofmarketstructurethat

is likely to emerge from such a regulatory framework. The current arrangement does

notmatchanyofthestylizedsectoraltypesdescribedbytheWBstudyperfectly,itcan

only be described as “hybrid”. It exhibits features of all of the sectoral types:

concentrated,localmonopolyandcompetitive.

Clearly, the new regulatory frameworkwill bring about an evolution towards amore

concentratedsystem,as someof thesmaller less financially soundginnerswillnotbe

able to comply with the new investment requirements. As table 2 indicates, some

22Anderson,Ian;TGT,pers.comm.,23.02.2012.23Mtunga,Marco;TCB,pers.comm.,03.05.2012.

11

ginnershavenotqualifiedinanyofthezones.Eventhoughtheyareintheoryeligibleto

reapplyforalicensethefollowingyear,thesefirmsarelikelytobeunableorunwilling

tocontinueoperatingunderthenewcircumstances. Ahigherdegreeofconcentration

will replace competition among buyers on the market (based on price) with a

competitionfor themarket(contractswithproducers,basedontheservicesofferedto

the groups). From their country‐comparison, Tschirley, Poulton, Labaste et al. (2009)

concludethat“Concentratedsectorshaveperformedwellonabroadrangeofindicators.

They have scored highly on quality and service delivery (input and extension).24“

However, thissector typehasadisappointing trackrecordoncottonpricing. It isalso

inherentlyunstable.Experience inZimbabweandZambiahas shown that theentryof

new investors with no capacity or background in promoting input use can quickly

undermine productivity and quality25. Evidence even suggests that in a concentrated

setting, the entry of new investors can rapidlyunwindprogress on yields andquality

beforeithasanypositiveeffectonpricespaidtofarmers.Therefore,theWBconcludes

that in concentrated systems regulators must provide an environment in which a

small(er) number of buyers can coordinate input credit provision and quality

enhancement, while ensuring that farmers receive remunerative prices.26 In the

Tanzanian context, thismeans thekey challengewill be tomaintain the current strict

licensing rules (not lower the requirements on input credit andminimumnumber of

FBGsundercontract),whilestillretainingsomecontestabilitytoincentivizeincumbent

licensed ginners in a zone to continue paying attractive prices. Contestability is

particularly hard to achieve as specific assets of the incumbents resulting from past

activity have the dimension of sunk costs for potential rivalswho intend to enter the

market.27Newinvestorsshouldbeselectedcarefullyaccordingtotheircommitmentto

invest long‐term in productivity and quality. The WB observes that in concentrated

sectors company cost‐efficiency is usually lower than under competitive systems. In

Tanzaniahowevercost‐efficiencyshouldnotdeclinetoomuchasmanyofthefirmsthat

will leave the industry are among the least efficient and are riddled with debt. No

exceptions should be made for smaller firms if they do not meet the requirements.

Indeed, one of the key findings of theWB study is that “such firmsmust bemade to

24Tschirley,Poulton,Labasteetal.(2009:164).25Ibid(2009:81).26Idem.27Araujo‐Bonjean,Combes,Plane(2003:15).

12

adhere to strict codesof conduct if theirpresencewithin a sector is todomoregood

thanharm”28.

The degree of concentration induced by the reforms varies greatly geographically, as

table2illustrates.Asinsomezonesasingleginnerwillenjoyadefactomonopoly,these

regionsbestmatch the “localmonopoly” category.How important thatelementof the

hybridsystemwillbecomedependsonhowmanyginnerswillemergefromthereform

processaftersomeyears.Inthelocalmonopolyregions,accordingtothestudyfindings,

improvements in inputcredit, extensionandqualityshouldbemorepronounced than

elsewhere, and repayment rates higher. So should the negative effects on pricing and

companycostefficiency.ExperienceswithlocalmonopoliesinMozambiqueshowthatin

practice performance on input credit, extension and quality varies greatly across

concessions29.Thesameconsiderationsas for theconcentratedsystemapply:when it

becomesapparentthataparticularginnerwillbetheonlyonetosecureabuyinglicense

in a given zone, the company’s culture and track record should receive extra

consideration. Transparent rules for license allocation, performance evaluation and

reallocationareparamount.Thethreatofentryofnewcompaniesmaynotbeenoughto

avoid a strong decline in producer prices however. According to the WB, “more

formalizedapproachestopricesettingmaybeneededtoensureremunerativepricesto

farmers”30.

Finally,thehybridsystemthatisbeingputinplacewillretainacompetitiveelementat

leastforatransitionalperiod.Untilallproducersadoptcontractfarming,therewillstill

besomescopeforcompetitionbetweenginnersinagivenzonefortheseedcottonfrom

uncontractedproducers.Whilethismightcontributetokeepingproducer‐priceshigh,it

willinevitablycreateamarketinwhichbrokersandcompanybuyingagentswilltryto

exploitarbitragepossibilities.Theexistenceofsuchamarketincreasestheriskofside‐

sellingbycontractedproducers,andcouldunderminequalityimprovements.

Which one of the stylized sector types the Tanzanian cotton sector will come to

resemble most will be conditioned by many factors, including the evolution of the

minimum input packages andminimum FBG quotas, the number of ginners able and

willing to invest under these rules, and the rate of contract farming adoption among

28Idem.29Tschirley,Poulton,Labasteetal.(2009:161).30Ibid(2009:80).

13

cottongrowers.Butthecurrentstateofplaysuggeststhatdirectprice‐competitionfor

seed cotton will decline strongly: according to TGT, the 4700 FBGs that will be

contracted by ginners represent about 80% of committed cotton growers in the

country31. Table 2 leaves no doubt that in most regions the zonal requirements will

lowerthenumberofactivebuyers.Thus,atleastforthetimebeing,thesectorisclearly

movingtowardsagreaterdegreeofconcentrationand,insomemoreperipheralregions

wherecottonproductionislowerandoperatingandtransportcostshigherforginners,

(contestable) localmonopolies.The insightsof theWBcomparativestudysuggestthat

such a transformation is prone to improve productivity and quality. However, the

danger is that theperformanceonproducerpricesandcompanycostefficiencymight

decline. Maintaining cost efficiency can be achieved through the annual competitive

retendering of buying rights and setting of high indicative prices. The risk of lower

prices is somewhat mitigated in Tanzania by ginners’ need to increase capacity

utilizationandtheirknowledgethatfarmersmoveinandoutofcottonproductionbased

largelyonprices32.Butisthecurrentpricingmodelstilladequate?

TheannouncementbytheTCBofapan‐territorialindicativepricehasregularlycaused

disruptions in marketing because of intra‐seasonal fluctuations (over the course of

harvest)ofworldmarketpricesforlint,anddifferentcostconditionsforginnersacross

thecottongrowingarea.Stakeholdersarenowworkingonanewmodelinwhichpan‐

territorialindicativepriceswouldbereadjustedonaweeklybasis.Giventheprevalence

of contract farming without predetermined prices, such a model might still cause

marketingdisruptionsbecauseofdisagreementbetweenfarmersandginnersontiming

of sales. A possible solution to this predicament could be a “ristourne” model: the

announcementofaguaranteedminimumpricetoproducersatthestartoftheseason,

witha top‐up later ifworldprices remainedat the initial levelor increased.33 Ideally,

such a pricing model should allow for differentiated prices across zones to reflect

differentcostconditions.

StrengtheningthefledglingCottonGrowersAssociation(TACOGA)wouldmakeitmuch

easier to implement such a model. If TACOGA was able to bargain with ginners for

remunerative prices on the basis of solid knowledge of world prices, realized export

prices,qualitypremiumsobtained,andcoststructurebornebyginnersitwouldgreatly

31Anderson,Ian;TGT,pers.comm.,15.03.2012.32Baffes(2002:4).33Badiane,Ghura,Goreuxetal.(2002:20).

14

increase acceptabilityof fluctuatingprices among farmers34.A functional andefficient

organizationabletobothfacilitatecommunicationandlearningamongstproducersand

speak on their behalf to buyers and regulators would greatly enrich the stakeholder

dialogueandhelpmakecontractfarmingasuccess.Suchanorganizationisparticularly

important if themovetowardsaconcentratedormonopolisticsectorstructureproves

sustainable. But the WB concludes from the study findings that enabling farmer

organizations to play a more effective role in sector governance offers significant

advantagesirrespectiveofsectortype.35RLDChasundertakenthetaskofreformingand

strengtheningTACOGA,butitislikelytobealong‐termproject.

6ConclusionInanswer to the introductoryquestions, it canbeassertedwithsomeconfidence that

Tanzania’scottonsector looksset tobecomemoreconcentratedandoffermorescope

for horizontal collaboration between buyers on public goods provision. The approach

chosenbyTCBwiththeadviceandsupportfromitspartnerTGTintegratesthelessons

learnt fromreformexperience inother sub‐Saharan countries and is in linewithbest

practices recommendedby recent research findingson sectororganization suggesting

that “hybrid approaches within competitive sectors need to avoid protecting ginners

entirely from competitive pressure from within the country.“36 It appears suited to

tackle the challenge of preserving achievements from liberalization on pricing and

efficiencywhileimprovingthequalityandproductivityissues.

Thecomingmarketingseasonwillputthenewregulationstoacritical firsttest.Short

term success of the new regulatory framework will depend on the ability of ginning

firms to recoup their investment in input credit and extension as well as convincing

cottongrowersofthebenefitsofcontractfarming.Inthelongrun,theabilityofthemain

regulator TCB to continuously enforce the rules (without outside support) will be

decisive.Evidence fromUganda’s experiencewith adifferent zoning scheme indicates

thatitisdifficultforregulatorstoresistpoliticalpressurefromsmallerginnerstolower

the requirements for buying licenses37. Strengthening sector governance and

accountability of the regulator towards all stakeholders, including farmers will

ultimatelybethegreatestchallengeforsustainabilityofthenewhybridsectormodel.34Tschirley,Poulton,Labasteetal.(2009:166).35Ibid(2009:173).36Ibid(2009:179).37Baffes(2009:6).

15

ANNEX1:CottonStakeholdersTanzaniaCottonBoard(TCB)

A statutory body that promotes growth of production / processing / marketing of

Tanzaniacotton,theroleoftheTCBistoputinplacealegalandregulatoryframework

toimproveanddevelopthecottonindustry.

TheCotton IndustryActof2001gave thenewlycreatedTanzaniaCottonBoard(TCB,

successor of TCMB) sweeping new powers as only regulator of the industry. Among

other things, the TCB is responsible for licensing buyers of seed cotton, exporters of

cottonlintandginoperators;formulatingregulationsforcottoncultivation,marketing,

processing,importation,exportationandstorageofcottonseed/lint,establishingquality

standardsof cottonseed/lintaswell asdetermining thequantityof cottonseed tobe

kept by ginners for planting the following season.Wholly funded by the government

since2006,thenewbodyisledbyaBoardofDirectorscomprisingofrepresentativesof

parliament,MOFA,buyersandfarmers(usuallyanMPfromacottongrowingregion).

http://www.cotton.or.tz/index.php

CottonDevelopmentTrustFund(CDTF)andPassbookScheme

The Cotton Development Trust Fund [CDTF] is an independent Tanzanian institution

which brings together stakeholders of the cotton industry. It is a service delivery

institution of the Tanzanian cotton industry andwas established in 2006 to take the

placeofitsforerunner,theCottonDevelopmentFund[CDF].

CDF was established in mid‐1999 by the Tanzania Cotton Board [TCB] to involve

stakeholdersininitiativestorestoreorderintheindustryfollowingemergenceofahost

ofproblemswhichwerecausedbythe1990sliberalizationofagriculturalmarketsand

governmentwithdrawalfromdirectinvolvementinproductionandtrading.

Major functionsof theFundare to oversee cottondevelopment, inparticular through

facilitationof the importationandefficientdistributionof inputs. Initially fundedbya

3% levy on cotton exports, it finances the purchase of seeds and pesticides to be

distributedtoregisteredproducersatbelow‐marketprices,withthefundmakingupthe

difference. A forced saving mechanism, the fund involved no subsidy, and is

administeredbytheTCB.Since2006,thetrustfundcollectsvariablecontributionsfrom

ginners(commensuratetotheamountofcottonpurchased,butchangingeveryyear)to

collectivelyimportchemicalinsecticides(bytender)anddistributethemtobuyerstobe

16

soldon to farmers. Linked to that fund, apassbook schemewasput inplace to assist

producers accessing pesticides. At the buying post, the quantity of cotton sold is

recorded in a passbook owned by registered cotton producers. At the start of the

followingseason,theproducersareentitledtoclaimpesticidesuptothevaluerecorded

in their passbooks38. Even though itmay have contributed to the bumper harvests of

2004/5, the system has been riddled with problems and has made a very limited

contributiontotheintensificationofcottonproduction.39

http://www.cotton.or.tz/index.php/tcb/cdtf/the_cotton_development_trust_fund_cdtf/

RuralLivelihoodDevelopmentCompany(RLDC)

The Rural Livelihood Development Programme (RLDP) is an initiative of the

GovernmentofSwitzerlandandsupportedthroughtheSwissAgency forDevelopment

and Cooperation (SDC). The main concern of RLDP is the high rural poverty in the

Central Corridor of Tanzania which is manifested by very low incomes and frequent

food shortages including lack of reliable/sustainable markets and employment. The

programme aims at making market systems work better for the welfare of rural

producersapplyingthe‘makingmarketsforthepoor’approach(M4P).Theprogramme

iscurrentlyaddressingmarketconstraintsinsixsub‐sectors,namelyCotton;Sunflower;

Dairy;Rice;PoultryandRuralradio.

RLDP is jointly managed by two Swiss International NGOs, Helvetas Swiss

Intercooperation (HSI) and Swisscontact (SC). It is implemented through the Rural

Livelihood Development Company (RLDC), a non‐profit organization that has been

establishedin2005.

RLDChasmadeseveralinterventionsinthecottonsector,includingenhancingorganic

cotton farming, supporting trainingandmanagementcapacitiesofproducergroupsas

well as mobilizing and educating farmers on latest cottonmarket information. Other

activities include improving farmer extension services through increasedoutreachvia

business partners. Also, RLDC is supporting training in advanced agronomic practices

throughfarmerfieldschools(FFS),organizingexchangevisitsandprovidingagricultural

inputservices.Anotherfieldof interventionisthestrengtheningofmarketsystemsby

facilitatingconstructionofcollectioncentersandinvestmentinginneriesandoilmills.

38Poulton,p.3139OrganizationandPerformance,p.77

17

RLDCalsocloselycollaborateswithpublicstakeholdersforpurposesofnetworkingand

uses their support to improve the sector’s business environment. These include the

TanzaniaCottonBoard(TCB),thatputsinplacealegalandregulatoryframeworkofthe

cotton sector and functions as the register for authorized seed buyers aswell as the

TanzaniaGatsbyTrust.

http://www.rldc.co.tz/

TanzaniaCottonAssociation(TCA)

The association comprises of and represents all companies holding licenses as cotton

buyersandginners.ItisthelobbyofthePrivateSectorinthecottonindustry.

TheAssociationhasclosetiestotheCottonBoardandisregularlyconsulted. It isalso

representedduringtheannualfloor‐pricesettingmeeting.

TanzaniaCottonGrowersAssociation(TACOGA)

The Tanzanian Cotton Growers’ Association (TACOGA) was registered by personal

initiativeofanex‐cooperativeemployeeinOctober2002,butfundingtocreateastrong,

grassrootsorganizationhasbeenlacking.TCBhasprovidedsomefinancialassistanceto

enable foundermembers of the organization tomeet and thebenefits ofmembership

are being promoted by “lead” farmerswho havewon awards in annual competitions

organizedbyTCB.Currently,TACOGAisfundedexclusivelybytheCottonDevelopment

Fund(CDF)thatwasestablishedin1997andisfundedthroughalevyonallseedcotton

purchasedinthecountry.

AstheapexorganizationofTanzaniancottonproducers,TACOGAholdstwoseatsinthe

CottonDevelopmentFund(CDF),andis invitedtothestakeholdermeetingsorganized

by TCB on a regular basis. In particular, TACOGA representatives are invited to

commonly negotiate the floor price for seed cotton that is defined every year at the

beginning of the buying season in a price‐settingmeeting involving the TCB, the TCA

(apexorganizationofthecottonbuyers),andgovernmentrepresentatives.

The organization has a membership base of about 30’000 members. Every cotton

growerinthecountrycanjoinuponpaymentofaone‐offadmissionfeeof2000TSH.The

boardofTACOGA iscomposedof12memberselectedbydistrict representatives.The

last electionswere held inMarch 2011,when about three quarters of the incumbent

boardmemberswerereplaced.

18

TanzaniaGatsbyTrust(TGT)

TanzaniaGatsbyTrust(TGT)isregisteredasacharitableTrustinTanzaniasince1992

under the Trustees’ Incorporation Ordinance, Cap 375 for poverty alleviation by

enabling hundreds of Small and Medium sized Enterprises (SMEs) to carry out

productiveandprofitableenterprises.Its“CottonandTextileDevelopmentProgramme”

was initiated from discussions between Lord David Sainsbury; the Settler of the UK

GatsbyCharitableFoundation(GCF)andTanzaniangovernmentofficials.Itcomprisesof

thefollowingelements:

1. CottonSubsectorStudywithafocusonthelong‐termpotentialforamajorincrease

intheoutputofTanzania’scottonandtextilesectorwithaviewtomaximizingits

potentialcontributiontothegenerationofincreasedGDP,exports,farmerincomes

andmanufacturingemployment.

2. A development strategy for Cotton and Textile programme with ambitious but

achievableobjectives:

a. Increaseofcottonproductionfrom700,000balesto1,500,000balesperannum.

b. Raiseyieldsfrom750kg/hato1500kg/haby2010and2,500kg/haby2015.

c. Increase the proportion of lint consumed in the domestic textile industry from

30%to90%by2015.

3. Conservation Agriculture (CA) to Cotton growing aims at increasing the

productivity/yield at the farm level based on well‐developed crop management

practices for both cotton and food production. CA is a unique agriculture practice

thatinvolvessimultaneouslysustaineduseoffourprinciplesthatare;

o Minimumsoildisturbance(ideallynoTillingandDirectseeding)

o Permanentsoilcover(ideally100%+usingcropresidualsand/orGreenmanure

covercrops)

o Multi‐cropping(idealcroprotation)

o Theintegrationofcropandlivestockproduction

4. Strategy for Textile that envisages increasing the value addition of the domestic

consumption of cotton lint. This requires subsequent increase of both local and

foreigndirectinvestment.Thepotentialismainlyoncontinuedproducts(e.g.towels,

bed sheets) andproductionofAfricanbaseddesign themes for theexportmarket.

Forthistobeachievedthereisaneedtosupportthedevelopmentofskillsthatwill

19

beable tosupport theseproductionsstagesof textileengineeringanddesign from

theuniversitytovocationalcollegelevel.

The rolling out of contract farming countrywide, including mobilization of cotton

growersintoFarmerBusinessGroups(FBG)ispartofTGT’sCDTFprogramthatisbeing

implementedjointlywiththeTCB.

http://www.gatsby.or.tz/;http://www.gatsby.org.uk/

ANNEX2:CompositionofKeyIndicatorsofSectorPerformance

Source:WB(2009)

!

A TYPOLOGY OF AFRICAN COTTON SECTORS 57

Table 4.2 Key Indicators of Cotton Sector Performance

Type of indicator Measurement

Process indicatorsQuality and marketing Estimated average realized premium over

the Cotlook A Index on world markets (US$/lb lint)

Pricing Mean percentage of FOT price paid to farmers

Input provision Percentage of cotton farmers receiving input credit

Adequacy and quality of input credit package, if provided

Repayment rateExtension Percentage of companies providing

assistanceQualitative assessment

Valorization of by-products Price of cotton seeds

Research Number of varieties released and taken up in past 10 years

Intermediate outcome indicatorsYield Kg of seed cotton produced per hectare

Company cost efficiency Adjusted farm gate price to FOT cost (US$/kg lint)

Final outcome indicatorsFarmer welfare Returns per day of family labor (US$/day)

Number of farm households participating in sector

Number

Overall competitiveness Ratio of total FOT cost to total FOT value

Macro impact Total value added per capita (including value of seed sales)

Net budgetary contribution per capita (taxes paid minus transfers received)

Source: Authors.Note: FOT = free on truck (i.e. ex-ginnery).

“free ride” on many of the fixed costs (such as travel cost and time) associatedwith input delivery. Yet delivery of input and extension advice are not likely tobe perfect complements. Within any sector type, this arrangement suggeststhat performance on extension is likely to be weaker, or more fragile in theface of stress, than is performance on input credit—for three reasons. First,delivering anything other than the most basic extension advice directly linkedto input use requires a higher level of training of field agents than does deliv-ery of input. Second, extension delivery—and especially its effectiveness—is

20

BibliographyAraujo‐Bonjean,Catherine;Combes,Jean‐LouisandPlane,Patrick(2003).Preserving

VerticalCoordinationintheWestAfricanCottonSector.CERDIUniversitéd’Auvergne,

EtudesetDocumentsE2003.03.Availableat:

http://publi.cerdi.org/ed/2003/2003.03.pdf

Badiane,Ousmane;Ghura, Dhaneshwar;Goreux,LouisandMasson,Paul(2002),Cotton

SectorStrategiesinWestandCentralAfrica.World Bank, Policy Research Working

Paper 2867. Available at: http://www-

wds.worldbank.org/external/default/WDSContentServer/IW3P/IB/2002/10/12/000094946

_02080604014034/additional/118518322_20041117182540.pdf

Baffes,John(2002).Tanzania’sCottonSector:ConstraintsandChallengesinaGlobal

Environment.WorldBank,AfricaRegionWorkingPaperSeriesNo.42.Availableat:

http://www.worldbank.org/afr/wps/wp42.pdf

Baffes,John(2009).TheCottonSectorofUganda.WorldBank,AfricaRegionWorking

PaperSeriesNo.123.Availableat:

http://www.worldbank.org/afr/wps/WPS_123_Uganda_Cotton_Case_Study.pdf

Cuvelier,Alain;Rüegg,MajaandSigalla,Ajuaye(2011).EnablingGrowthandRaising

ProducerIncomesintheCottonSubsector:LessonsandExperiencefromtheCentral

CorridorofTanzania.RuralLivelihoodDevelopmentCompany.Availableat:

http://www.rldc.co.tz/docs/capexcotton.pdf

ITCandTCB(2011).CottonFromTanzania.Availableat:

http://www.cotton.or.tz/images/uploads/cotton_tanzania_brochure_10_aug_2011.p

df

Poulton,ColinandMaro,Wilbald(2009).TheCottonSectorofTanzania.WorldBank,

Africa Region Working Paper Series No. 127. Available at:

http://www.worldbank.org/afr/wps/WPS127_Tanzania_Cotton_Case_Study.pdf

21

TCB(2011).Cottonindustrytoadoptcontractfarmingsystem.TCBpressrelease,

10.01.2011.Availableat:

http://www.cotton.or.tz/index.php/news_events/more/cotton_industry_to_adopt_c

ontract_farming_system

Tschirley,David;Poulton,ColinandBoughton,Duncan(2006).TheManyPathofCotton

SectorReforminEasternandSouthernAfrica:LessonsfromaDecadeofExperience.

FoodSecurityInternationalDevelopmentWorkingPapers54565,MichiganState

University.Availableat:http://ideas.repec.org/p/ags/midiwp/54565.html

Tschirley,David;Poulton,ColinandLabaste,Patrick(eds.)(2009).Organizationand

performanceofcottonsectorsinAfrica:learningfromreformexperience.Washington,

DC:TheWorldBank.