manager a company incorporated in malaysia under the companies act 1965 … · 2017-03-22 · a...

TRANSCRIPT

Date Of Constitution28 March 2017

ManagerPacific Mutual Fund Bhd (336059-U)a company incorporated in Malaysia under the Companies Act 1965

TrusteeCIMB Islamic Trustee Berhad (167913-M)

INVESTORS ARE ADVISED TO READ AND UNDERSTAND THE CONTENTS OF THE PROSPECTUS. IF IN DOUBT, PLEASE CONSULT A PROFESSIONAL ADVISER.

FOR INFORMATION CONCERNING CERTAIN RISK FACTORS, WHICH SHOULD BE CONSIDERED BY PROSPECTIVE INVESTORS, SEE ‘RISK FACTORS’ COMMENCING ON PAGE 11.

THIS PROSPECTUS IS DATED 28 MARCH 2017 AND EXPIRES ON 27 MARCH 2018.

www.pacificmutual.com.my 03-7725 9877

A member of the OCBC Group

i

MESSAGE FROM CEO Dear Investors,

We are pleased to present to you the Pacific Dynamic Global Islamic Fund (“the Fund”).

The Fund aims to provide capital growth and income in the medium to long term by investing in a global portfolio of Shariah-compliant equities, sukuk and Islamic money market instruments.

The Fund is suitable for investors who: • seek an actively managed Shariah-compliant portfolio; • seek access to global markets; • seek capital growth and income; and • have a medium to long-term investment horizon.

You should also consider the specific and principal risks affecting the Fund and other risk factors when investing in the Fund. For more details of these risks, please refer to page 7 and pages 11 to 13 of this prospectus.

There are fees and charges involved when investing in the Fund such as sales charge, management fee, trustee fee, switching fee, transfer fee and other expenses. Please refer to the ‘Key Information’ section on page 9 and ‘Fees, Charges And Expenses’ section on pages 24 and 25 for more information.

If you have any queries about the information in this prospectus or would like to know more about our Fund, please feel free to contact our client relations personnel at 03-7725 9877 or e-mail us at [email protected]. Alternatively, you may contact our branches or authorised distributors. Please refer to pages 58 and 59 for the full contact details.

Thank you.

Yours sincerely,

TEH CHI-CHEUN Executive Director, CEO and CIO

ii

RESPONSIBILITY STATEMENTS

This prospectus has been reviewed and approved by the Directors of Pacific Mutual Fund Bhd (“the Manager”) and they collectively and individually accept full responsibility for the accuracy of the information. Having made all reasonable enquiries, they confirm to the best of their knowledge and belief, that there are no false or misleading statements, or omission of other facts which would make any statement in the prospectus false or misleading.

STATEMENTS OF DISCLAIMER The Securities Commission Malaysia has authorised the Fund and a copy of this prospectus has been registered with the Securities Commission Malaysia.

The authorisation of the Fund, and registration of this prospectus, should not be taken to indicate that Securities Commission Malaysia recommends the said Fund or assumes responsibility for the correctness of any statement made, opinion expressed or report contained in this prospectus.

The Securities Commission Malaysia is not liable for any non-disclosure on the part of the Manager responsible for the said Fund and takes no responsibility for the contents in this prospectus. The Securities Commission Malaysia makes no representation on the accuracy or completeness of this prospectus, and expressly disclaims any liability whatsoever arising from, or in reliance upon, the whole or any part of its contents.

INVESTORS SHOULD RELY ON THEIR OWN EVALUATION TO ASSESS THE MERITS AND RISKS OF THE INVESTMENT. IF INVESTORS ARE UNABLE TO MAKE THEIR OWN EVALUATION, THEY ARE ADVISED TO CONSULT PROFESSIONAL ADVISERS.

No units will be issued or sold based on this prospectus later than one year after the date of this prospectus.

Investors should note that they may seek recourse under the Capital Markets And Services Act 2007 for breaches of securities laws and regulations including any statement in the prospectus that is false, misleading, or from which there is a material omission; or for any misleading or deceptive act in relation to the prospectus or the conduct of any other person in relation to the Fund.

While it is the duty of the Manager to ensure the Fund is being correctly valued or priced, the Manager cannot be held liable for any error in prices published in the newspapers and the websites of our distributor(s) for the Fund. Pursuant to the Guidelines on Unit Trust Funds issued by the Securities Commission Malaysia, where there is incorrect valuation or pricing of units, the Manager will take immediate remedial action to rectify the error, which extends to reimbursement of money by the Manager to the Fund and/or from the Fund to the unitholders or former unitholders. Rectification need not be extended to any reimbursement where it appears to the trustee that the incorrect pricing is of minimal significance.

While it is the duty of the Manager to ensure that all comments given to the media is accurate and true at the time the comments were given, misquotation may still occur either by the media or third parties, which are out of the Manager’s control. In such situations, the Manager and its employees hold no responsibility for any claims and liabilities due to the misquotations by the media and/or third parties, and are under no obligation to fulfil any expectation or demand in relation to the misquoted statements.

The distribution of this prospectus and offering, purchase, sale or transfer of units of the Fund in certain jurisdictions may be restricted by law. In these jurisdictions, other than Malaysia, the Manager has not applied to allow distribution of this prospectus or units of the Fund. Therefore, this prospectus does not constitute an offer or invitation to purchase units of the Fund in any jurisdiction in which such offer or invitation would be unlawful.

Investors should be aware that for investments of our Fund made via any of our IUTA, where applicable, any investment transactions are subject to the terms and conditions of the respective IUTA.

The Pacific Dynamic Global Islamic Fund has been certified as Shariah-compliant by the Shariah Adviser appointed for the said Fund.

The Shariah Adviser for Pacific Dynamic Global Islamic Fund confirms that the investment portfolio of this Fund comprise securities which have been classified as Shariah-compliant by the Shariah Advisory Council of the Securities Commission Malaysia (“SACSC”) and/or the Shariah Supervisory Board of Dow Jones Islamic Market Indices. For the securities which are not certified by the SACSC and/or the Shariah Supervisory Board of Dow Jones Islamic Market Indices, the status of the securities has been determined in accordance with the ruling issued by the Shariah Adviser.

iii

CONTENTS

Definitions ………………………………………………………………………………………. 1

Corporate Directory …………………………………………………………………………… 4

Key Information Of The Fund ………..…………………………………………….…….….. 6 • Key Information 6 • Standard Transaction Details Pertaining To Investing In The Pacific Dynamic Global Islamic Fund

Managed By Pacific Mutual 10

Risk Factors …………………………………………………………………………….………. 11 • General Risks 11 • Specific Risks 13

Understanding Of Shariah-Compliant Unit Trust Fund …………………….………....… 14 • Treatment For Disposal Of Shariah Non-Compliant Securities For The Fund 15 • Cleansing/Purification Process Of The Fund 15

More Information About The Pacific Dynamic Global Islamic Fund ………................. 17 • Investment Objective 17 • Potential Benefits 17 • Investment Policy And Strategy 17 • Permitted Investments 20 • Investment Restrictions And Limits 20 • Risk Management Strategies And Techniques 22 • Frequency Of Trading 23 • Bases Of Valuation Of Investments 23

Fees, Charges And Expenses ………………………………………………………….……. 24 • Sales Charge 24 • Redemption Charge 24 • Annual Management Fee 24 • Annual Trustee Fee 24 • Switching Fee 25 • Transfer Fee 25 • Expenses 25 • Rebates And Soft Commissions 25

Transaction Information ………………………………………………………………….…… 26 • Pricing Calculation 26 • Minimum Initial Investment 26 • Minimum Additional Investment 27 • Purchase 27 • Redemption 28 • Switching Facility 29 • Transfer 29 • Cooling-Off Period 29 • Distribution Policy And Reinvestment Policy 30 • Unclaimed Moneys 30 • Keeping Abreast Of Developments In The Fund 31 • Customer Service 31

iv

Salient Terms Of The Deed …………………………………………………………….…..… 32 • Your Rights As A Unitholder 32 • Your Liabilities As A Unitholder 32 • Your Limitations And Restrictions As A Unitholder 32 • Maximum Fees And Charges 32 • Permitted Expenses Payable Out Of A Fund’s Property 33 • Removal, Replacement And Retirement Of The Management Company 33 • Removal, Replacement And Retirement Of A Trustee 34 • Termination Of A Fund 34 • Meetings Of Unitholders 34

All About The Manager – Pacific Mutual Fund Bhd …………..………………………….. 35 • Our Shareholders 35 • Our Core Business 35 • Our Corporate Vision And Mission 35 • Our Investment Philosophy 35 • Our Roles And Responsibilities 35 • Our Financial Position 36 • Our People 36 • Material Litigation And Arbitration 43

Trustee Of The Fund, Its Duties And Responsibilities …………………………………... 44 • CIMB Islamic Trustee Berhad (167913-M) 44 • Delegation Of Share Custodial Functions 45 • Material Litigation And Arbitration 45 • The Trustee’s Responsibilities 45 • Trustee’s Statement Of Responsibility 45

Shariah Adviser ………………………………………………………………………………... 46 • More About BSSB 46 • Shariah Investment Guidelines Adopted by BSSB 47

Taxation Adviser's Letter ……………………………………………………………………. 50

Related Party Transactions / Conflict Of Interests …………………………………..…. 55 • CIMB Islamic Trustee Berhad’s Policy On Dealing With Conflict Of Interest Elements 55

Additional Information ………………………………………………………………….……. 56 • Policies And Procedures To Prevent Money Laundering Activities 56 • Prudential Control 56

Consents …………………………………………….………………………………………….. 56

Exemption Granted By The Securities Commission .………………………………...… 56

Documents Available For Inspection …………………………………………………...…. 56

Inspection Of The Register Of Unitholders …………………………………….……….... 57

Directors' Declaration…………………………………………………………………………. 57

List Of Pacific Mutual Fund Bhd Offices, Agency Offices And Institutional Unit Trust Advisers ………………………………………………………………………….…........ 58

1 Definitions

DEFINITIONS

The meaning of some terms in this prospectus is explained below:

Board of Directors / Independent Directors /

Directors

Directors of Pacific Mutual Fund Bhd

Bursa Malaysia The stock exchange managed or operated by Bursa Malaysia Securities Berhad. business day(s) A day on which the Bursa Malaysia is open for trading.

deed The deed and all supplemental deeds entered into between the Manager and the Trustee in relation to the Fund.

duration This is the tenure of a fixed income investment, taking into account any profit payments made during its tenure before maturity. A fixed income investment with no profit payments until maturity will have its duration the same as its tenure.

eligible market A market that is regulated by a regulatory authority, operates regularly, is open to the public and has adequate liquidity for the purposes of the Fund.

equity-related securities Shariah-compliant securities where the underlying asset is a Shariah-compliant equity security. The return on Shariah-compliant equity-related securities is dependent upon the performance of the underlying Shariah-compliant equities. For this Fund, the Shariah-compliant equity-related securities comprise only Shariah-compliant warrants and right issues that are issued in relation to Shariah-compliant equities in which the Fund has invested.

Fitch Fitch Ratings Fund Pacific Dynamic Global Islamic Fund

Funds For the purpose of this prospectus, unless the context otherwise requires, Funds mean all funds managed by the Manager.

Fund Category / Characteristic

Pacific Mutual categorises its Funds under the following characteristics: Fund Category Characteristic • Money Market • Islamic Money Market • Fixed Income • Sukuk

Conservative

• Balanced • Mixed Assets

Fairly Conservative

• Mixed Assets1 • Equity (Growth & Income)

Fairly Aggressive

• Equity (Growth) Aggressive 1 – Where the equity strategy is more aggressive e.g. emerging markets.

GST Tax levied on goods and services pursuant to the Goods and Services Tax Act 2014.

IOSCO International Organization of Securities Commissions

2 Definitions

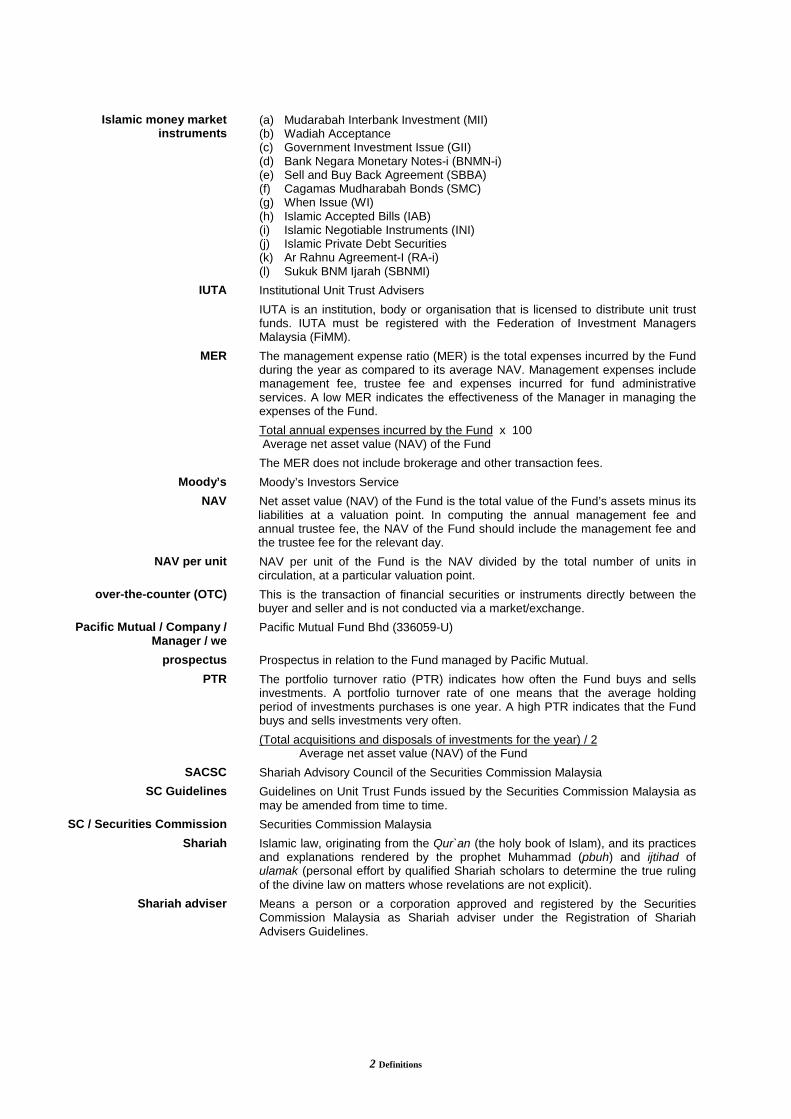

Islamic money market

instruments (a)

(b) (c) (d) (e) (f) (g) (h) (i) (j) (k) (l)

Mudarabah Interbank Investment (MII) Wadiah Acceptance Government Investment Issue (GII) Bank Negara Monetary Notes-i (BNMN-i) Sell and Buy Back Agreement (SBBA) Cagamas Mudharabah Bonds (SMC) When Issue (WI) Islamic Accepted Bills (IAB) Islamic Negotiable Instruments (INI) Islamic Private Debt Securities Ar Rahnu Agreement-I (RA-i) Sukuk BNM Ijarah (SBNMI)

IUTA Institutional Unit Trust Advisers IUTA is an institution, body or organisation that is licensed to distribute unit trust funds. IUTA must be registered with the Federation of Investment Managers Malaysia (FiMM).

MER The management expense ratio (MER) is the total expenses incurred by the Fund during the year as compared to its average NAV. Management expenses include management fee, trustee fee and expenses incurred for fund administrative services. A low MER indicates the effectiveness of the Manager in managing the expenses of the Fund. Total annual expenses incurred by the Fund x 100 Average net asset value (NAV) of the Fund The MER does not include brokerage and other transaction fees.

Moody’s Moody’s Investors Service NAV Net asset value (NAV) of the Fund is the total value of the Fund’s assets minus its

liabilities at a valuation point. In computing the annual management fee and annual trustee fee, the NAV of the Fund should include the management fee and the trustee fee for the relevant day.

NAV per unit NAV per unit of the Fund is the NAV divided by the total number of units in circulation, at a particular valuation point.

over-the-counter (OTC) This is the transaction of financial securities or instruments directly between the buyer and seller and is not conducted via a market/exchange.

Pacific Mutual / Company / Manager / we

Pacific Mutual Fund Bhd (336059-U)

prospectus Prospectus in relation to the Fund managed by Pacific Mutual. PTR The portfolio turnover ratio (PTR) indicates how often the Fund buys and sells

investments. A portfolio turnover rate of one means that the average holding period of investments purchases is one year. A high PTR indicates that the Fund buys and sells investments very often. (Total acquisitions and disposals of investments for the year) / 2 Average net asset value (NAV) of the Fund

SACSC Shariah Advisory Council of the Securities Commission Malaysia SC Guidelines Guidelines on Unit Trust Funds issued by the Securities Commission Malaysia as

may be amended from time to time. SC / Securities Commission Securities Commission Malaysia

Shariah Islamic law, originating from the Qur`an (the holy book of Islam), and its practices and explanations rendered by the prophet Muhammad (pbuh) and ijtihad of ulamak (personal effort by qualified Shariah scholars to determine the true ruling of the divine law on matters whose revelations are not explicit).

Shariah adviser Means a person or a corporation approved and registered by the Securities Commission Malaysia as Shariah adviser under the Registration of Shariah Advisers Guidelines.

3 Definitions

Shariah Adviser BIMB Securities Sdn Bhd (290163-X)

Shariah requirements Is a phrase or expression which generally means making sure that any human conduct must not involve any elements which are prohibited by the Shariah and that in performing that conduct all the essential elements that make up the conduct must be present and each essential element must meet all the necessary conditions required by the Shariah for that element.

short term / medium term / long term

Short term - below one year; medium term - one year to three years; long term - above three years.

sukuk Refers to certificates of equal value which evidence undivided ownership or investment in the assets using Shariah principles and concepts endorsed by the SACSC.

Trustee CIMB Islamic Trustee Berhad (167913-M)

unitholder The person for the time being who is registered pursuant to the deed as a holder of units, including a jointholder.

warrants Shariah-compliant warrants are financial instruments that give the buyer the right to purchase Shariah-compliant equity securities at a fixed price up to the expiry date of the Shariah-compliant warrants.

yield Yield is the return an investor will receive when holding a fixed income investment to maturity.

4 Corporate Directory

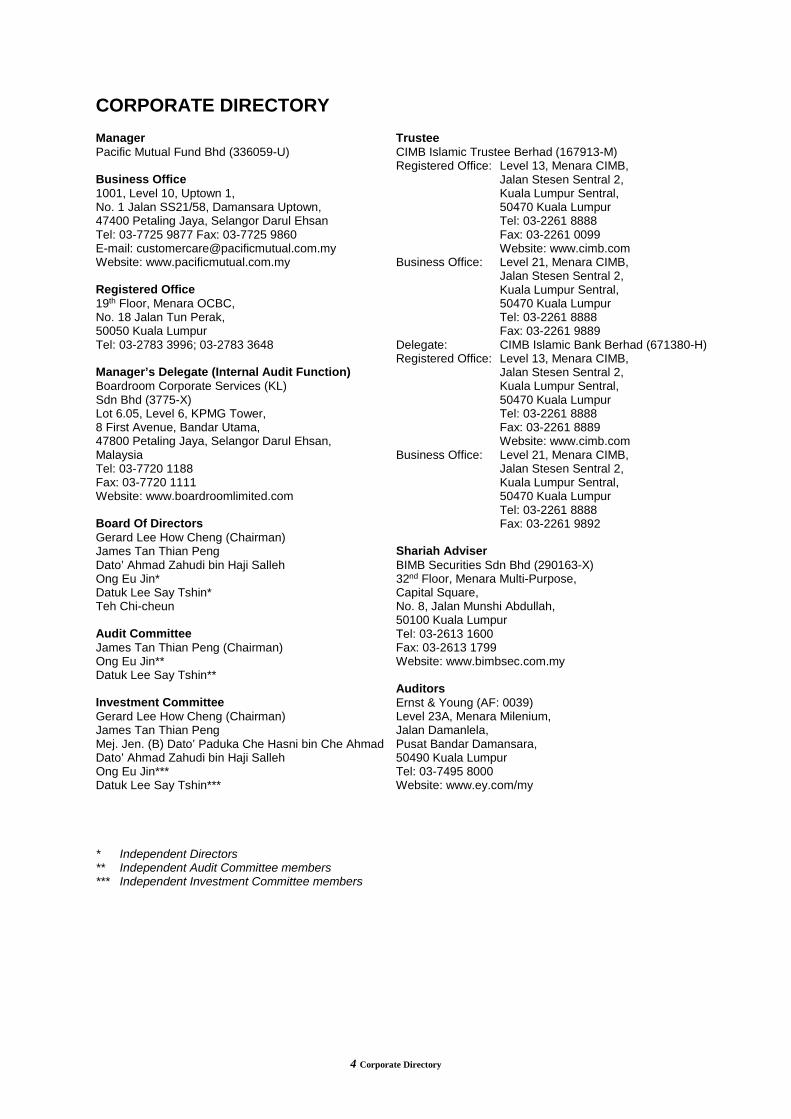

CORPORATE DIRECTORY

Manager Pacific Mutual Fund Bhd (336059-U) Business Office 1001, Level 10, Uptown 1, No. 1 Jalan SS21/58, Damansara Uptown, 47400 Petaling Jaya, Selangor Darul Ehsan Tel: 03-7725 9877 Fax: 03-7725 9860 E-mail: [email protected] Website: www.pacificmutual.com.my Registered Office 19th Floor, Menara OCBC, No. 18 Jalan Tun Perak, 50050 Kuala Lumpur Tel: 03-2783 3996; 03-2783 3648 Manager’s Delegate (Internal Audit Function) Boardroom Corporate Services (KL) Sdn Bhd (3775-X) Lot 6.05, Level 6, KPMG Tower, 8 First Avenue, Bandar Utama, 47800 Petaling Jaya, Selangor Darul Ehsan, Malaysia Tel: 03-7720 1188 Fax: 03-7720 1111 Website: www.boardroomlimited.com Board Of Directors Gerard Lee How Cheng (Chairman) James Tan Thian Peng Dato’ Ahmad Zahudi bin Haji Salleh Ong Eu Jin* Datuk Lee Say Tshin* Teh Chi-cheun Audit Committee James Tan Thian Peng (Chairman) Ong Eu Jin** Datuk Lee Say Tshin** Investment Committee Gerard Lee How Cheng (Chairman) James Tan Thian Peng Mej. Jen. (B) Dato’ Paduka Che Hasni bin Che Ahmad Dato’ Ahmad Zahudi bin Haji Salleh Ong Eu Jin*** Datuk Lee Say Tshin*** * Independent Directors ** Independent Audit Committee members *** Independent Investment Committee members

Trustee CIMB Islamic Trustee Berhad (167913-M) Registered Office: Level 13, Menara CIMB, Jalan Stesen Sentral 2, Kuala Lumpur Sentral, 50470 Kuala Lumpur Tel: 03-2261 8888 Fax: 03-2261 0099 Website: www.cimb.com Business Office: Level 21, Menara CIMB, Jalan Stesen Sentral 2, Kuala Lumpur Sentral, 50470 Kuala Lumpur Tel: 03-2261 8888 Fax: 03-2261 9889 Delegate: CIMB Islamic Bank Berhad (671380-H) Registered Office: Level 13, Menara CIMB, Jalan Stesen Sentral 2, Kuala Lumpur Sentral, 50470 Kuala Lumpur Tel: 03-2261 8888 Fax: 03-2261 8889 Website: www.cimb.com Business Office: Level 21, Menara CIMB, Jalan Stesen Sentral 2, Kuala Lumpur Sentral, 50470 Kuala Lumpur Tel: 03-2261 8888 Fax: 03-2261 9892 Shariah Adviser BIMB Securities Sdn Bhd (290163-X) 32nd Floor, Menara Multi-Purpose, Capital Square, No. 8, Jalan Munshi Abdullah, 50100 Kuala Lumpur Tel: 03-2613 1600 Fax: 03-2613 1799 Website: www.bimbsec.com.my Auditors Ernst & Young (AF: 0039) Level 23A, Menara Milenium, Jalan Damanlela, Pusat Bandar Damansara, 50490 Kuala Lumpur Tel: 03-7495 8000 Website: www.ey.com/my

5 Corporate Directory

Tax Advisers Ernst & Young Tax Consultants Sdn Bhd (179793-K) Level 23A, Menara Milenium, Jalan Damanlela, Pusat Bandar Damansara, 50490 Kuala Lumpur Tel: 03-7495 8000 Website: www.ey.com/my Company Secretaries Quah Boon Huat (MAICSA 7032217) Chong Yok Hua (MAICSA 0861045) 19th Floor, Menara OCBC, No. 18 Jalan Tun Perak, 50050 Kuala Lumpur Tel: 03-2783 3996; 03-2783 3648 Banker OCBC Bank (Malaysia) Berhad (295400-W) Menara OCBC, No. 18 Jalan Tun Perak, 50050 Kuala Lumpur Tel: 1300 88 5000 Solicitors For The Manager Soon Gan Dion & Partners Advocates and Solicitors 1st Floor, No. 73, Jalan SS 21/1A, Damansara Utama, 47400 Petaling Jaya, Selangor Federation Of Investment Managers Malaysia (FiMM) 19-06-1, 6th Floor, Wisma Tune, No. 19 Lorong Dungun, Damansara Heights, 50490 Kuala Lumpur Website: www.fimm.com.my

6 Key Information Of The Fund

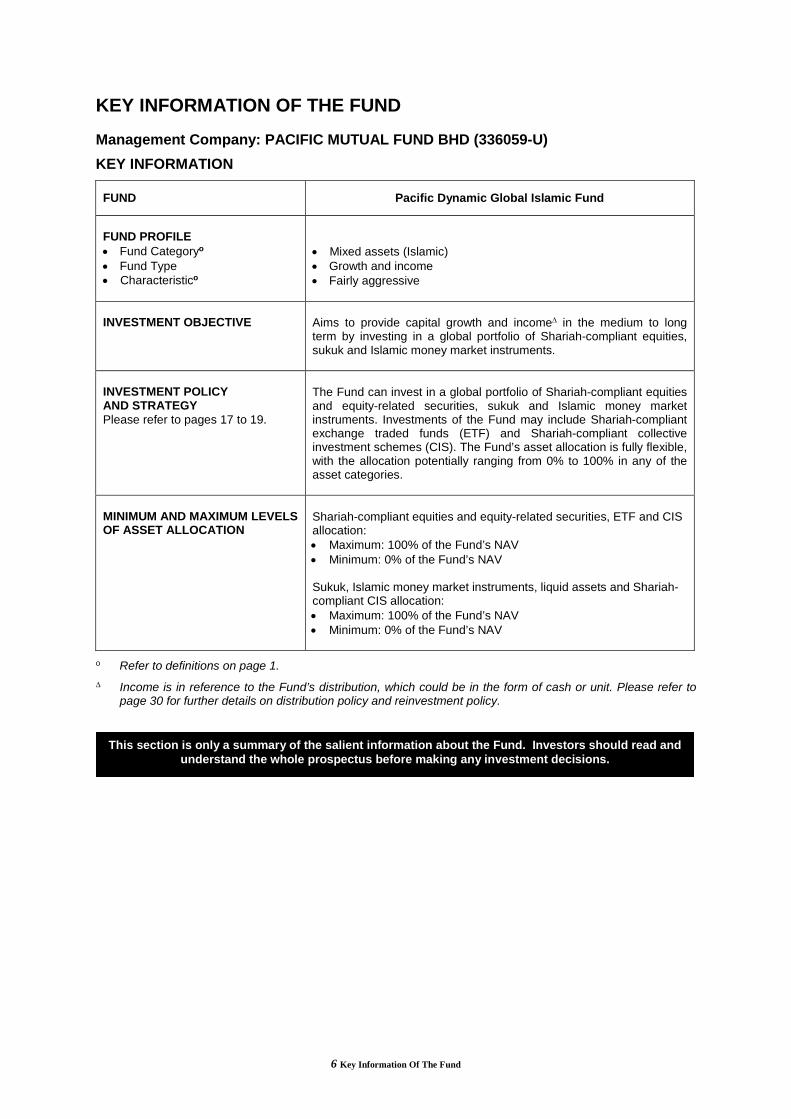

KEY INFORMATION OF THE FUND

Management Company: PACIFIC MUTUAL FUND BHD (336059-U)

KEY INFORMATION

FUND Pacific Dynamic Global Islamic Fund

FUND PROFILE • Fund Categoryo • Fund Type • Characteristico

• Mixed assets (Islamic) • Growth and income • Fairly aggressive

INVESTMENT OBJECTIVE

Aims to provide capital growth and income∆ in the medium to long term by investing in a global portfolio of Shariah-compliant equities, sukuk and Islamic money market instruments.

INVESTMENT POLICY AND STRATEGY Please refer to pages 17 to 19.

The Fund can invest in a global portfolio of Shariah-compliant equities and equity-related securities, sukuk and Islamic money market instruments. Investments of the Fund may include Shariah-compliant exchange traded funds (ETF) and Shariah-compliant collective investment schemes (CIS). The Fund’s asset allocation is fully flexible, with the allocation potentially ranging from 0% to 100% in any of the asset categories.

MINIMUM AND MAXIMUM LEVELS OF ASSET ALLOCATION

Shariah-compliant equities and equity-related securities, ETF and CIS allocation: • Maximum: 100% of the Fund’s NAV • Minimum: 0% of the Fund’s NAV Sukuk, Islamic money market instruments, liquid assets and Shariah-compliant CIS allocation: • Maximum: 100% of the Fund’s NAV • Minimum: 0% of the Fund’s NAV

o Refer to definitions on page 1. ∆ Income is in reference to the Fund’s distribution, which could be in the form of cash or unit. Please refer to

page 30 for further details on distribution policy and reinvestment policy.

This section is only a summary of the salient information about the Fund. Investors should read and understand the whole prospectus before making any investment decisions.

7 Key Information Of The Fund

FUND Pacific Dynamic Global Islamic Fund

PRINCIPAL RISKS Please refer to pages 11 to 13.

• Timing of asset allocation risk • Reclassification of Shariah status risk • Market risk • Country risk • Currency risk • Company specific risk • Warrants risk • Liquidity risk • Interest rate risk • Credit risk and default risk • ETF risk

INVESTOR PROFILE

Those seeking to invest in an actively managed Shariah-compliant portfolio; seeking access to global markets; seeking capital growth and income∆; and have a medium to long-term investment horizon.

DISTRIBUTION POLICY* Please refer to page 30.

Subject to the availability of income, distribution of income will be made once a year.

PERFORMANCE BENCHMARK

Composite Benchmark (50% in Dow Jones Islamic Market World Index [DJIM] and 50% in 3-Month Islamic Interbank Money Market [IIMM] Rate)

GENERAL INFORMATION Trustee

CIMB Islamic Trustee Berhad (167913-M)

Financial Year End

30 June

Initial Offer Period

28 March 2017 – 17 April 2017 (21 days)

Initial Offer Price

RM0.5000

∆ Income is in reference to the Fund’s distribution, which could be in the form of cash or unit. Please refer to

page 30 for further details on distribution policy and reinvestment policy.

* Income distributions are not guaranteed and may not be repeated. Distributions of income will only be made from realised gains or realised income obtained from the investments of the Fund.

8 Key Information Of The Fund

FUND Pacific Dynamic Global Islamic Fund

Switching Facility

To carry out a switching transaction, all you need to do is complete the transaction form or send a letter of request to our head office or any of our branches by 4.00 p.m. on any business day.

There are no restrictions on the number of switching transactions that you may carry out; however, all switching transactions are subject to the following conditions: • You may switch your investments into all other Funds managed by

the Manager except for wholesale Funds; • The Funds that you intend to switch into must have been in

existence for at least three months from the launch dates of those Funds;

• The minimum number of units to be switched is 1,000 units and the value of units switched must meet the minimum investment amount of the switch-in Funds, whichever is higher;

• The minimum number of units required to be held in the switch-out Fund is 500 units for a partial switch; and

• For the avoidance of doubt, if you have purchased units of the Fund through our IUTA, the switching transaction is subject to the terms and conditions of the IUTA.

Switching will be carried out at the respective prevailing NAV per unit of the Fund to be switched from and the Fund to be switched into on a business day, when we receive the switching request by 4.00 p.m. on any business day (subject to availability and terms of the Fund to be switched into). Please refer to page 29 for the terms and conditions of the switching facility for the Fund.

Transfer Facility Please refer to page 29.

Transfer facility is available for the Fund, free of charge.

MER**

Not available

PTR (times)**

Not available

** Refer to definitions on page 2.

9 Key Information Of The Fund

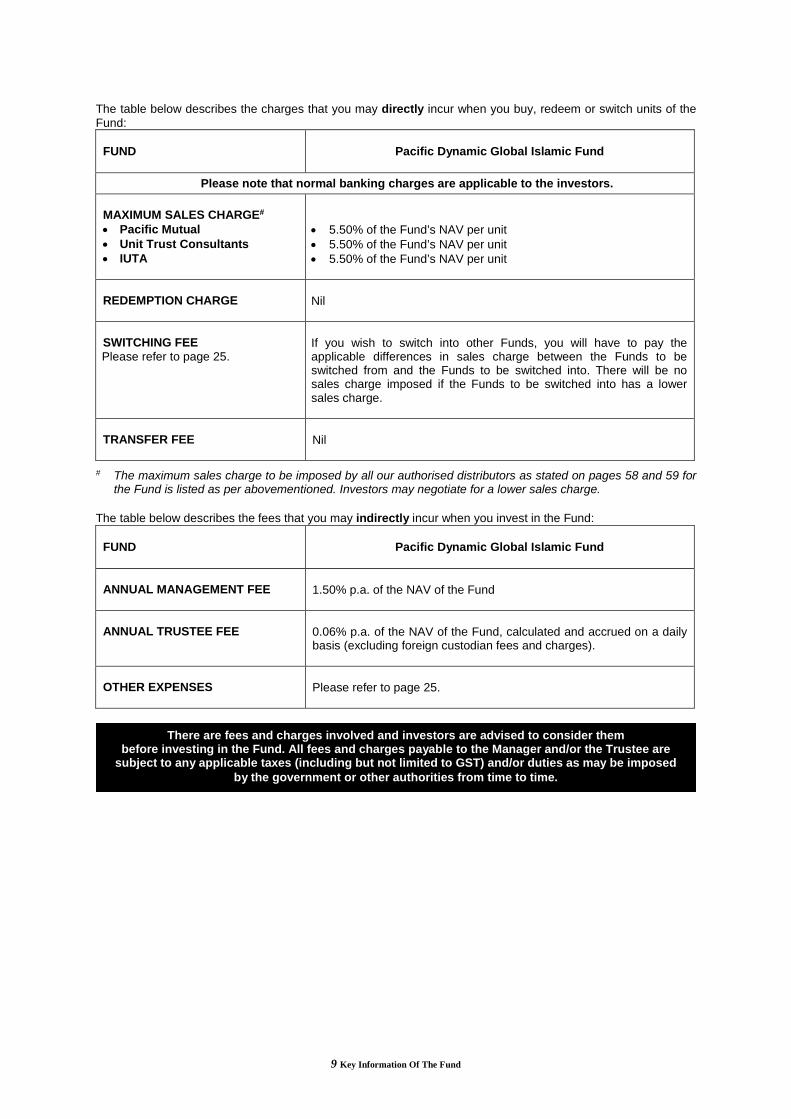

The table below describes the charges that you may directly incur when you buy, redeem or switch units of the Fund:

FUND Pacific Dynamic Global Islamic Fund

Please note that normal banking charges are applicable to the investors. MAXIMUM SALES CHARGE# • Pacific Mutual • Unit Trust Consultants • IUTA

• 5.50% of the Fund’s NAV per unit • 5.50% of the Fund’s NAV per unit • 5.50% of the Fund’s NAV per unit

REDEMPTION CHARGE

Nil

SWITCHING FEE Please refer to page 25.

If you wish to switch into other Funds, you will have to pay the applicable differences in sales charge between the Funds to be switched from and the Funds to be switched into. There will be no sales charge imposed if the Funds to be switched into has a lower sales charge.

TRANSFER FEE

Nil

# The maximum sales charge to be imposed by all our authorised distributors as stated on pages 58 and 59 for

the Fund is listed as per abovementioned. Investors may negotiate for a lower sales charge.

The table below describes the fees that you may indirectly incur when you invest in the Fund:

FUND Pacific Dynamic Global Islamic Fund

ANNUAL MANAGEMENT FEE

1.50% p.a. of the NAV of the Fund

ANNUAL TRUSTEE FEE

0.06% p.a. of the NAV of the Fund, calculated and accrued on a daily basis (excluding foreign custodian fees and charges).

OTHER EXPENSES

Please refer to page 25.

There are fees and charges involved and investors are advised to consider them before investing in the Fund. All fees and charges payable to the Manager and/or the Trustee are

subject to any applicable taxes (including but not limited to GST) and/or duties as may be imposed by the government or other authorities from time to time.

10 Key Information Of The Fund

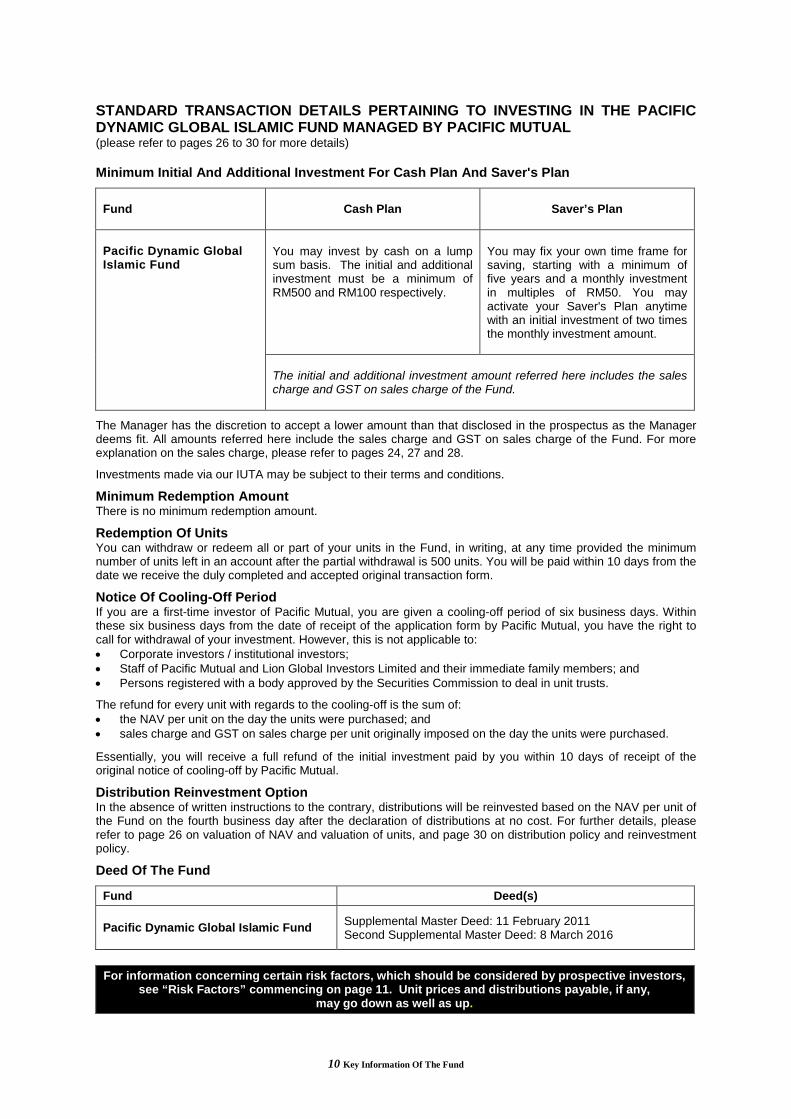

STANDARD TRANSACTION DETAILS PERTAINING TO INVESTING IN THE PACIFIC DYNAMIC GLOBAL ISLAMIC FUND MANAGED BY PACIFIC MUTUAL (please refer to pages 26 to 30 for more details)

Minimum Initial And Additional Investment For Cash Plan And Saver's Plan

Fund

Cash Plan Saver’s Plan

Pacific Dynamic Global Islamic Fund

You may invest by cash on a lump sum basis. The initial and additional investment must be a minimum of RM500 and RM100 respectively.

You may fix your own time frame for saving, starting with a minimum of five years and a monthly investment in multiples of RM50. You may activate your Saver's Plan anytime with an initial investment of two times the monthly investment amount.

The initial and additional investment amount referred here includes the sales charge and GST on sales charge of the Fund.

The Manager has the discretion to accept a lower amount than that disclosed in the prospectus as the Manager deems fit. All amounts referred here include the sales charge and GST on sales charge of the Fund. For more explanation on the sales charge, please refer to pages 24, 27 and 28.

Investments made via our IUTA may be subject to their terms and conditions.

Minimum Redemption Amount There is no minimum redemption amount.

Redemption Of Units You can withdraw or redeem all or part of your units in the Fund, in writing, at any time provided the minimum number of units left in an account after the partial withdrawal is 500 units. You will be paid within 10 days from the date we receive the duly completed and accepted original transaction form.

Notice Of Cooling-Off Period If you are a first-time investor of Pacific Mutual, you are given a cooling-off period of six business days. Within these six business days from the date of receipt of the application form by Pacific Mutual, you have the right to call for withdrawal of your investment. However, this is not applicable to: • Corporate investors / institutional investors; • Staff of Pacific Mutual and Lion Global Investors Limited and their immediate family members; and • Persons registered with a body approved by the Securities Commission to deal in unit trusts.

The refund for every unit with regards to the cooling-off is the sum of: • the NAV per unit on the day the units were purchased; and • sales charge and GST on sales charge per unit originally imposed on the day the units were purchased. Essentially, you will receive a full refund of the initial investment paid by you within 10 days of receipt of the original notice of cooling-off by Pacific Mutual.

Distribution Reinvestment Option In the absence of written instructions to the contrary, distributions will be reinvested based on the NAV per unit of the Fund on the fourth business day after the declaration of distributions at no cost. For further details, please refer to page 26 on valuation of NAV and valuation of units, and page 30 on distribution policy and reinvestment policy.

Deed Of The Fund

Fund Deed(s)

Pacific Dynamic Global Islamic Fund Supplemental Master Deed: 11 February 2011 Second Supplemental Master Deed: 8 March 2016

For information concerning certain risk factors, which should be considered by prospective investors, see “Risk Factors” commencing on page 11. Unit prices and distributions payable, if any,

may go down as well as up.

11 Risk Factors

RISK FACTORS

GENERAL RISKS The following are the general risks for the Fund:

• Company specific risk – This risk refers to the individual risk of the respective companies issuing securities. This risk could be a result of changes to the business performance of the company, consumer tastes and demand, lawsuits, competitive operating environment and management practices. Developments in a particular company which the Fund has invested in would result in fluctuations in the security price of that company and thus the value of the Fund's investments. This risk is mitigated by diversification in a portfolio comprised of securities of many companies.

In addition, this risk may occur when an investee company's business or fundamentals deteriorate or if there is a change in management policy resulting in a downward revision or even removal of the company's dividend policy. Such events may result in an overall decrease in dividend income received by the Fund and possible capital loss due to a drop in the security price of a company that cuts or omits its dividend payments. This risk may be mitigated by investing mainly in companies with a consistent historical record of paying dividends, strong cash flow, or operating in fairly stable industries.

• Country risk – Investments of the Fund in any countries may be affected by changes in the economic and political climate, restriction on currency repatriation or other developments in the law or regulations of the countries in which the Fund invests in. For example, the deteriorating economic condition of such countries may adversely affect the value of the investments undertaken by the Fund in those affected countries. This may cause the NAV or prices of the Fund to fall. This risk may be mitigated by conducting thorough research on the respective countries, their regulatory framework, economics, companies, politics and social conditions as well as minimising or omitting investments in countries that are economically or politically unstable or lack a regulatory financial framework and adequate investor protection legislation.

• Credit risk and default risk – Credit risk relates to the creditworthiness of the issuers of fixed income instruments and their expected ability to make timely payment of profits and/or principal. Any adverse situations faced by an issuer may impact the value as well as liquidity of fixed income instruments issued. In the case of fixed income instruments assigned a rating by a credit rating agency, this may lead to a lowering of the credit rating of the instrument. Default risk relates to the risk that an issuer of a fixed income instrument either defaults on payments or fails to make payments in a timely manner which will in turn adversely affect the value of the fixed income instrument and thus value of the Fund’s investment in such instruments. This risk is reduced by analysis of companies issuing such instruments, taking into account the credit rating (which must have a long-term rating of at least A2 by RAM Ratings or an equivalent rating) and diversification in a range of fixed income investments issued by different companies and Islamic licensed financial institutions.

• Currency risk – As the investments of the Fund are denominated in currencies other than Malaysian Ringgit (“Ringgit”), any fluctuations in the exchange rate between the Ringgit and the currencies in which the investments are denominated may have an impact on the value of these investments. If the currencies in which the investments are denominated depreciate against the Ringgit, this will have an adverse effect on the NAV of the Fund (on the reverse, if the foreign currencies appreciate against the Ringgit, the Fund’s NAV may increase). Any of such gains or losses arising from fluctuations in exchange rates may decrease or increase returns on investment in the Fund. This risk may be mitigated by reducing exposure to investments denominated in a currency that is expected to decline versus the Ringgit.

12 Risk Factors

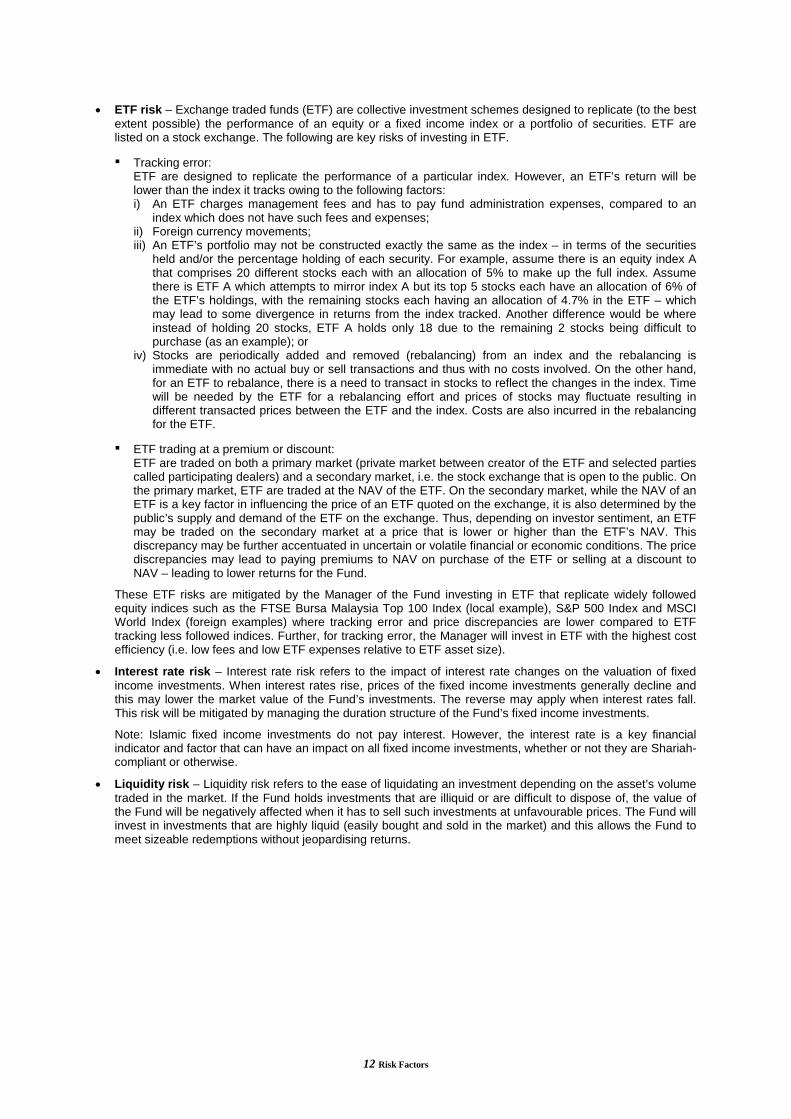

• ETF risk – Exchange traded funds (ETF) are collective investment schemes designed to replicate (to the best extent possible) the performance of an equity or a fixed income index or a portfolio of securities. ETF are listed on a stock exchange. The following are key risks of investing in ETF.

▪ Tracking error: ETF are designed to replicate the performance of a particular index. However, an ETF’s return will be lower than the index it tracks owing to the following factors: i) An ETF charges management fees and has to pay fund administration expenses, compared to an

index which does not have such fees and expenses; ii) Foreign currency movements; iii) An ETF’s portfolio may not be constructed exactly the same as the index – in terms of the securities

held and/or the percentage holding of each security. For example, assume there is an equity index A that comprises 20 different stocks each with an allocation of 5% to make up the full index. Assume there is ETF A which attempts to mirror index A but its top 5 stocks each have an allocation of 6% of the ETF’s holdings, with the remaining stocks each having an allocation of 4.7% in the ETF – which may lead to some divergence in returns from the index tracked. Another difference would be where instead of holding 20 stocks, ETF A holds only 18 due to the remaining 2 stocks being difficult to purchase (as an example); or

iv) Stocks are periodically added and removed (rebalancing) from an index and the rebalancing is immediate with no actual buy or sell transactions and thus with no costs involved. On the other hand, for an ETF to rebalance, there is a need to transact in stocks to reflect the changes in the index. Time will be needed by the ETF for a rebalancing effort and prices of stocks may fluctuate resulting in different transacted prices between the ETF and the index. Costs are also incurred in the rebalancing for the ETF.

▪ ETF trading at a premium or discount: ETF are traded on both a primary market (private market between creator of the ETF and selected parties called participating dealers) and a secondary market, i.e. the stock exchange that is open to the public. On the primary market, ETF are traded at the NAV of the ETF. On the secondary market, while the NAV of an ETF is a key factor in influencing the price of an ETF quoted on the exchange, it is also determined by the public’s supply and demand of the ETF on the exchange. Thus, depending on investor sentiment, an ETF may be traded on the secondary market at a price that is lower or higher than the ETF’s NAV. This discrepancy may be further accentuated in uncertain or volatile financial or economic conditions. The price discrepancies may lead to paying premiums to NAV on purchase of the ETF or selling at a discount to NAV – leading to lower returns for the Fund.

These ETF risks are mitigated by the Manager of the Fund investing in ETF that replicate widely followed equity indices such as the FTSE Bursa Malaysia Top 100 Index (local example), S&P 500 Index and MSCI World Index (foreign examples) where tracking error and price discrepancies are lower compared to ETF tracking less followed indices. Further, for tracking error, the Manager will invest in ETF with the highest cost efficiency (i.e. low fees and low ETF expenses relative to ETF asset size).

• Interest rate risk – Interest rate risk refers to the impact of interest rate changes on the valuation of fixed income investments. When interest rates rise, prices of the fixed income investments generally decline and this may lower the market value of the Fund’s investments. The reverse may apply when interest rates fall. This risk will be mitigated by managing the duration structure of the Fund’s fixed income investments.

Note: Islamic fixed income investments do not pay interest. However, the interest rate is a key financial indicator and factor that can have an impact on all fixed income investments, whether or not they are Shariah-compliant or otherwise.

• Liquidity risk – Liquidity risk refers to the ease of liquidating an investment depending on the asset’s volume traded in the market. If the Fund holds investments that are illiquid or are difficult to dispose of, the value of the Fund will be negatively affected when it has to sell such investments at unfavourable prices. The Fund will invest in investments that are highly liquid (easily bought and sold in the market) and this allows the Fund to meet sizeable redemptions without jeopardising returns.

13 Risk Factors

• Market risk – This risk refers to the possibility that an investment will lose value because of a general decline in financial markets cause by economic, political, social and/or other factors. This will result in a decline in the Fund’s NAV.

• Warrants risk – Warrants are financial instruments that give the buyer the right to purchase equity securities at a pre-determined price (“exercise price”) up to the expiry date of the warrants. The price movements of the equity security to which a warrant is linked affects the price of a warrant. Movements in price of an equity security will generally result in larger movements in the price of any warrants related to the equity – meaning that warrants are expected to have high price volatility relative to the equity security. This means that when the price of an equity security falls, warrants may underperform the equity security, i.e. the price of a warrant may fall more than the percentage fall in the price of the equity security to which it is related. On the reverse, a warrant may outperform the equity security to which it is related, i.e. the warrant price may rise by a percentage that is higher than the rise of the equity security.

Warrants have a limited life and will depreciate in value as they approach their expiry date. If at any time up to the expiry date of a warrant, the warrant’s exercise price is above the market price of the equity security, the warrant is “out of the money” and has little or no value. Warrants that are not exercised at maturity become worthless.

Holders of warrants are not entitled to any dividends that may be paid to investors in an equity security.

Warrants risk may be mitigated by conducting extensive fundamental analysis of the warrants’ equity securities in relation to the market price and exercise price of the warrants and to determine if they should continue to be held for the Fund.

SPECIFIC RISKS The Fund is subject to the following specific risks:

• Reclassification of Shariah status risk – This risk refers to the risk that the currently held Shariah-compliant investments in the Fund may be reclassified to be Shariah non-compliant. For Shariah-compliant securities, the reclassification may occur in the periodic review of the securities by the SACSC, the Shariah Adviser or the Shariah boards of the relevant Islamic indices. If this occurs, the Manager will take the necessary steps to dispose such investments. There may be opportunity loss to the Fund due to the Fund not being allowed to retain the excess capital gain derived from the disposal of the Shariah non-compliant investments. Please refer to pages 47 to 49 on the Fund’s Shariah methodology on the treatment of gains and losses as a result of the reclassification of Shariah non-compliant investments. This risk is mitigated by constantly monitoring the Shariah compliance status of the securities. Detailed fundamental analysis of business stability, financial position and debt ratio analysis of the issuers of the securities would also help to mitigate such risk. Business stability is assessed to ensure there are no frequent business acquisitions that may potentially lead to a security being Shariah non-compliant. Fundamental (balance sheet) analysis is undertaken to ensure that financial ratio benchmarks are not borderline and thus susceptible to being Shariah non-compliant with just small increases in debt levels (from conventional debt financing).

• Timing of asset allocation risk – This is the risk that given prevailing economic and financial market conditions, the Manager of the Fund makes inappropriate asset allocation decisions between the equity and fixed income asset categories, potentially resulting in lower returns to the Fund. To mitigate such risk, the Manager conducts detailed fundamental macro research and analysis on financial market trends and keeps regular updates on them. Factors such as economic and political conditions, interest rate environment, valuations of markets, liquidity and investor sentiment are taken into account before making asset allocation decisions or changes.

14 Understanding Of Shariah-Compliant Unit Trust Fund

UNDERSTANDING OF SHARIAH-COMPLIANT UNIT TRUST FUND

Similar to a conventional unit trust fund, a Shariah-compliant unit trust fund is a collective investment scheme, which pools money from investors with similar objectives in a special fund managed by professional fund managers. The pooled money will then be invested in a diversified portfolio of Shariah-compliant securities and other assets in accordance with the unit trust fund’s investment objective and as permitted under the SC Guidelines and regulations with the condition that all the investments must comply with Shariah requirements.

The main differences between a conventional unit trust fund and a Shariah-compliant unit trust fund exist in the following areas; objective of the fund, structure, investment strategy, operations and management, documentation, investment avenues and activities, and accounts and reporting.

The objective of a particular type of fund is normally to maximise returns that are usually composed of both capital and income growth. Achieving this objective will depend on, among others, the fund size, period of investment, investment strategy as well as the type of instruments that are invested in and the ability to manage risk. Accordingly, the objective of a particular Shariah-compliant unit trust fund is to achieve both capital and income growth within the scope of Shariah. Hence, the investment strategy will also need to be aligned with the objective of a Shariah-compliant unit trust fund.

As for the structure, a Shariah-compliant unit trust fund can be structured by applying various Shariah contracts such as Mudharabah, Wakalah Bil Istithmar, Wadiah and so on. In Malaysian context, the core contracts utilised in the process of structuring a Shariah-compliant unit trust fund are contracts of intermediation such as Wakalah or Mudharabah, which allow one party to act as an agent (manager) on behalf of a principal (capital owner) for an agreed fee or profit-sharing arrangement.

As for the operations and management of a Shariah-compliant unit trust fund, the manager ensures that the excess funds, such as liquid assets and cash, are invested/placed in Islamic money market instruments and as deposit with Islamic licensed financial institutions. All daily operations of a Shariah-compliant unit trust fund must comply with all the Shariah requirements of the Securities Commission and other relevant competent Shariah authorities. To ensure that the funds are managed and administered in accordance with Shariah requirements, unit trust management companies managing Shariah-compliant unit trust funds are required by the SC Guidelines to appoint a Shariah committee / Shariah adviser. The main function of the Shariah committee / Shariah adviser is to supervise and provide necessary advice to ensure that a Shariah-compliant unit trust fund offered to the public is managed and administered in accordance with Shariah requirements.

A Shariah-compliant unit trust fund’s trust deed and prospectus are drafted in accordance with Shariah requirements. Terminologies used in conventional trust deed and prospectus, which are not in compliance with the Shariah, such as interest-based instruments and interest income are avoided.

The investments of a Shariah-compliant unit trust fund include only instruments permitted by the Shariah such as Shariah-compliant equities and Shariah-compliant equity-related securities (such as Shariah-compliant warrants and options), sukuk, Islamic derivative products, Islamic structured products and Shariah-compliant deposit placements.

A Shariah-compliant unit trust fund is designed to provide investors with investment alternatives that comply with Shariah requirements. The investments exclude instruments deemed not permissible by the Shariah like all types of loan stocks, Shariah non-compliant securities, conventional interest paying bonds, interest bearing instruments and conventional futures and derivatives products.

15 Understanding Of Shariah-Compliant Unit Trust Fund

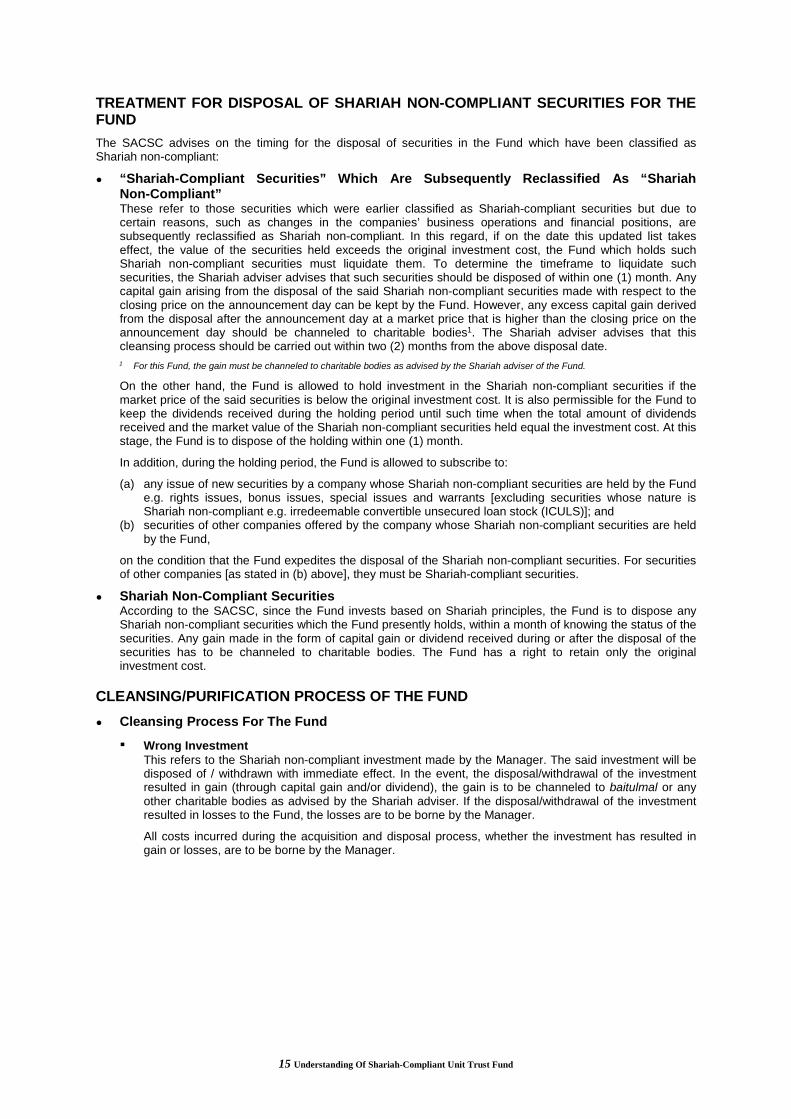

TREATMENT FOR DISPOSAL OF SHARIAH NON-COMPLIANT SECURITIES FOR THE FUND

The SACSC advises on the timing for the disposal of securities in the Fund which have been classified as Shariah non-compliant:

● “Shariah-Compliant Securities” Which Are Subsequently Reclassified As “Shariah Non-Compliant” These refer to those securities which were earlier classified as Shariah-compliant securities but due to certain reasons, such as changes in the companies’ business operations and financial positions, are subsequently reclassified as Shariah non-compliant. In this regard, if on the date this updated list takes effect, the value of the securities held exceeds the original investment cost, the Fund which holds such Shariah non-compliant securities must liquidate them. To determine the timeframe to liquidate such securities, the Shariah adviser advises that such securities should be disposed of within one (1) month. Any capital gain arising from the disposal of the said Shariah non-compliant securities made with respect to the closing price on the announcement day can be kept by the Fund. However, any excess capital gain derived from the disposal after the announcement day at a market price that is higher than the closing price on the announcement day should be channeled to charitable bodies1. The Shariah adviser advises that this cleansing process should be carried out within two (2) months from the above disposal date. 1 For this Fund, the gain must be channeled to charitable bodies as advised by the Shariah adviser of the Fund.

On the other hand, the Fund is allowed to hold investment in the Shariah non-compliant securities if the market price of the said securities is below the original investment cost. It is also permissible for the Fund to keep the dividends received during the holding period until such time when the total amount of dividends received and the market value of the Shariah non-compliant securities held equal the investment cost. At this stage, the Fund is to dispose of the holding within one (1) month.

In addition, during the holding period, the Fund is allowed to subscribe to:

(a) any issue of new securities by a company whose Shariah non-compliant securities are held by the Fund e.g. rights issues, bonus issues, special issues and warrants [excluding securities whose nature is Shariah non-compliant e.g. irredeemable convertible unsecured loan stock (ICULS)]; and

(b) securities of other companies offered by the company whose Shariah non-compliant securities are held by the Fund,

on the condition that the Fund expedites the disposal of the Shariah non-compliant securities. For securities of other companies [as stated in (b) above], they must be Shariah-compliant securities.

● Shariah Non-Compliant Securities According to the SACSC, since the Fund invests based on Shariah principles, the Fund is to dispose any Shariah non-compliant securities which the Fund presently holds, within a month of knowing the status of the securities. Any gain made in the form of capital gain or dividend received during or after the disposal of the securities has to be channeled to charitable bodies. The Fund has a right to retain only the original investment cost.

CLEANSING/PURIFICATION PROCESS OF THE FUND

● Cleansing Process For The Fund

▪ Wrong Investment This refers to the Shariah non-compliant investment made by the Manager. The said investment will be disposed of / withdrawn with immediate effect. In the event, the disposal/withdrawal of the investment resulted in gain (through capital gain and/or dividend), the gain is to be channeled to baitulmal or any other charitable bodies as advised by the Shariah adviser. If the disposal/withdrawal of the investment resulted in losses to the Fund, the losses are to be borne by the Manager.

All costs incurred during the acquisition and disposal process, whether the investment has resulted in gain or losses, are to be borne by the Manager.

16 Understanding Of Shariah-Compliant Unit Trust Fund

▪ Reclassification Of Shariah Status Of Investments For The Fund A security may be reclassified as Shariah non-compliant in the periodic review of the securities by the SACSC or any other relevant Islamic Shariah competent authorities such as the Dow Jones Islamic Index Shariah Supervisory Board. If the value of such Shariah non-compliant investment exceeds the original investment cost, such securities should be disposed as soon as practicable, which in any event such disposal should be done within one (1) month after the announcement day or receipt of such notice.

If the Shariah non-compliant investment is below the original investment cost, such securities is allowed to be kept until the total amount of dividends received and/or the market value/price equal the original investment costs. When the value of Shariah non-compliant investment equals the original investment cost, such securities should be disposed as soon as practicable, which in any event such disposal should be within one (1) month.

Any capital gains arising from the disposal of the Shariah non-compliant security made at the time of the announcement can be kept by the Fund. However, any excess capital gains derived from the disposal after the announcement day at a market price that is higher than the closing price on the announcement day is to be channelled to baitulmal or any charitable bodies within two (2) months from the disposal date as advised by the Shariah adviser.

● Purification Process For The Fund

▪ Zakat For The Shariah-Compliant Fund The Fund does not pay zakat on behalf of Muslim individuals and Islamic legal entities who are investors of the Fund. Thus, investors of the Fund are advised to pay zakat on their own.

For more information on the Shariah Investment Guidelines adopted by BIMB Securities Sdn Bhd (BSSB), kindly refer to pages 47 to 49.

17 More Information About The Pacific Dynamic Global Islamic Fund

MORE INFORMATION ABOUT THE PACIFIC DYNAMIC GLOBAL ISLAMIC FUND

INVESTMENT OBJECTIVE The Fund aims to provide capital growth and income∆ in the medium to long term by investing in a global portfolio of Shariah-compliant equities, sukuk and Islamic money market instruments.

Any material change to the Fund's investment objective would require unitholders' approval. ∆ Income is in reference to the Fund’s distribution, which could be in the form of cash or unit. Please refer to

page 30 for further details on distribution policy and reinvestment policy.

POTENTIAL BENEFITS By investing in this Fund, you will be able to reap the following benefits: • An actively managed Shariah-compliant portfolio; • Access to Shariah-compliant securities available in local and overseas markets; and • Potential for capital growth and income.

INVESTMENT POLICY AND STRATEGY In achieving the Fund’s investment objective, the Manager invests the Fund’s assets in the following investments that are available locally and overseas:

A. Equity asset class: • Shariah-compliant equities and equity-related securities. For this Fund, equity-related securities comprise

only warrants and rights that are issued in relation to equities in which the Fund has invested; • Shariah-compliant collective investment schemes (CIS) whose underlying investments are equities and

equity-related securities; • Shariah-compliant exchange traded funds (ETF) that track an equity index;

B. Fixed income asset class: • Sukuk and Islamic money market instruments; • Shariah-compliant CIS whose underlying investments are sukuk and/or Islamic money market

instruments; and • Islamic deposits.

Dynamic Asset Allocation Depending on expectations for economic and financial market conditions, there may be significant shifts into and out of asset categories via a dynamic asset allocation strategy and, active risk control measures for the Fund.

The dynamic asset allocation means there are no restrictions to the Fund’s percentage holdings in an asset category. The Fund may hold from 0% to 100% in Shariah-compliant equity asset class and 0% to 100% in Shariah-compliant fixed income asset class.

The dynamic asset allocation is to enable the Fund to: • Seek Shariah-compliant equity assets that generate capital and income returns during rising equity markets;

and • Mitigate risk by increasing allocation to Shariah-compliant fixed income assets which generate income and

offer capital safety˄ during declines in values of Shariah-compliant equity assets.

An internal allocation of cash and cash equivalent will be maintained to ensure that the Fund is able to meet redemption requests without jeopardising the Fund’s performance. ˄ Capital safety is in reference to fixed income assets that include Islamic deposits which do not fluctuate in

value and in short-term Islamic money market instruments. The Fund is not a capital guaranteed and capital protected fund.

18 More Information About The Pacific Dynamic Global Islamic Fund

• Investment Strategy For Equity Assets (Shariah-Compliant Equities, Equity-Related Securities, CIS And ETF) The Fund will invest in Shariah-compliant equities and ETF listed on the Malaysian stock exchange and in overseas stock exchanges. The Fund may also invest in Shariah-compliant CIS which meet the Fund’s objective.

The overseas stock exchanges in which the Fund may invest are in Australia, Belgium, Brazil, Canada, Chile, Denmark, France, Germany, Hong Kong S.A.R, Indonesia, Italy, Japan, Luxembourg, Netherlands, New Zealand, Norway, Philippines, Singapore, South Africa, South Korea, Spain, Sweden, Switzerland, Taiwan, Thailand, UK and US. The Fund may also invest in listed and unlisted securities of other foreign markets not listed above, where the regulatory authority is an ordinary or associate member of the IOSCO.

1. Investment process The Manager is guided by the following principles in managing this segment of the Fund: ▪ Extensive top-down analysis – local and global macroeconomic, social political issues and

sector/industry analysis is undertaken to determine their potential impact on equities. From these analyses, the broad equity allocation is determined followed by allocation to sectors.

▪ Extensive bottom-up analysis – to enable the Manager to identify individual investments suitable for inclusion in the Fund. Please refer to item 2 below (security selection) for the criteria used in this analysis.

▪ Valuations – analyse prices of investments to ensure the Fund does not overpay for what the investments are determined to be worth.

▪ Volatility (i.e. rate at which an equity security moves up or down) of returns.

2. Security selection From the large number of Shariah-compliant equities, ETF and CIS available locally and overseas, the Manager conducts detailed research and applies various filters to identify those investments that are suitable for inclusion as the Fund’s holdings. These filters are: ▪ Financial strength: Companies should produce cash flows that enable funding of their business

operations. Companies must also have strong balance sheets, i.e. hold cash reserves that exceed borrowings or are in a borrowing position where the borrowings can be serviced. This financial strength will enable the companies to withstand any business downturn.

▪ Sustainable competitive advantage: Factors such as having very experienced staff, access to natural resources, possessing strong brands or having patents – which enable a company to generate returns for the medium to long term.

▪ Management team that is experienced and of high calibre: Such a team would have a medium to long-term track record of growing a business and are expected to continue with the track record.

▪ Good corporate governance: Companies that have independent directors and protect the rights of minority shareholders (minority shareholders are those who do not have control of how a company is managed).

▪ For ETF, there is the consideration of how well an ETF’s performance mirror the index performance that it attempts to replicate. Fees charged by the ETF are also taken into consideration.

▪ For CIS, analysis is made of the performance track record of a CIS, the credentials of the manager of the CIS and its investment team and fees charged.

3. Portfolio construction The portfolio construction process involves combining the following: ▪ From the top-down and bottom-up analyses described above, the list of potential investments is

narrowed to one that fits the investment objective of the Fund. ▪ Analysis of valuations of investments is then applied to the list to further reduce it to a selection of

investments that will be included in the Fund. The valuation analysis includes financial tools such as price-to-earnings ratio*, price-to-book ratio**, historic and expected dividend payments to determine value.

* Price-to-earnings ratio: Ratio of the market price of an equity investment compared to its earnings. ** Price-to-book ratio: Ratio of the market price of an equity investment compared to its book value

(book value is the tangible assets of a company less all liabilities). Please also refer to the general risks commencing on page 11 and the section on the Fund’s permitted investments on page 20.

19 More Information About The Pacific Dynamic Global Islamic Fund

• Investment Strategy For Fixed Income Assets (Sukuk, Shariah-Compliant CIS, Islamic Money Market Instruments And Islamic Deposits) The Fund will invest in Malaysian Shariah-compliant fixed income investments that are available either by direct market purchases or indirectly via CIS. Any exposure to Shariah-compliant foreign fixed income investments will be made via Shariah-compliant CIS.

1. Investment process The Manager is guided by the following principles in managing this segment of the Fund: ▪ Extensive top-down analysis – Analysis is made of local and global macroeconomic conditions,

interest/profit rates expectations, currency and sector analysis to determine their impact on values of fixed income investments, in particular on sukuk. From these analyses, the Manager will set the allocation level of fixed income investments for the Fund, determine the duration and desired yield.

▪ Extensive bottom-up analysis – To enable the Manager to identify individual investments suitable for inclusion in the Fund. Please refer to item 2 below (security selection) for the criteria used in this analysis.

▪ Risk management by investing in a diverse portfolio of sukuk and Islamic money market instruments.

2. Security selection The Manager analyses the following factors to determine investment selection for the Fund: ▪ Credit quality: Indicates the capacity of a company issuing sukuk to meet repayment of the sukuk

and/or profits from the sukuk when they mature. Selection of sukuk focuses on business and financial risk at the issuer level. For inclusion in the Fund, a local sukuk issue must have at least a long-term rating of A2 by RAM Ratings or AID by MARC. The minimum short-term rating must be P2 by RAM Ratings or MARC-2ID by MARC. Any exposure to foreign sukuk will be via Shariah-compliant CIS – and the underlying investments of the CIS must be at least 80% invested in investment grade sukuk, i.e. rated as BBB and above by Standard & Poor’s or an equivalent rating by other international credit rating agencies (i.e. Fitch or Moody’s).

▪ Yield spread analysis: Yield spread is the difference in the rate of return between different sukuk usually of different credit quality. By tracking how particular patterns vary over time, the spread analysis provides an indication of the relative pricing of sukuk.

▪ Liquidity and marketability of sukuk: Liquidity and maturity profiling allows the Manager to determine the extent of liquidity risk and its commensurate returns. Liquidity risk is greater for thinly traded securities such as lower rated sukuk, sukuk that were part of a small issue or sukuk sold by an infrequent issuer.

▪ Analysis of sukuk issues: The analysis is to identify specific/unique risk with regards to the structure of sukuk by analysing sukuk agreements, terms and conditions of a sukuk issue and asset collateral (assets used in backing a sukuk issue).

3. Portfolio construction The portfolio construction process involves taking into account both the top-down and bottom-up analyses described above to construct a diversified portfolio focusing on credit quality, valuations and liquidity and marketability of the fixed income instruments.

Note: Interest rates are a general indicator that will have an impact on the management of a fund regardless of whether it is a Shariah-compliant fund or otherwise. It does not in any way suggest that this Fund will invest in conventional financial instruments. All the investments carried out for this Fund are in accordance with requirements of the Shariah.

Performance Benchmark The benchmark for the Fund is a composite of 50% in Dow Jones Islamic Market World Index (DJIM) and 50% in 3-Month Islamic Interbank Money Market (IIMM) Rate. The composite benchmark is reflective of the medium to long-term local and global asset (equity and fixed income) allocation of the Fund. The DJIM index is available from Bloomberg’s website, www.bloomberg.com. The IIMM rate is widely used by investment managers and publicly available from Bank Negara Malaysia’s website, iimm.bnm.gov.my. These data will also be published as a comparison against the Fund’s total return at least on a monthly basis in our publications and website, a year after the Fund’s inception. For the Fund’s composite benchmark data up to a year from the Fund’s inception, investors may request for data from the Manager.

The risk profile of the Fund is different from the risk profile of the benchmark.

20 More Information About The Pacific Dynamic Global Islamic Fund

PERMITTED INVESTMENTS Where permitted by the relevant authorities and consistent with the objective of the Fund, the Pacific Dynamic Global Islamic Fund is permitted to invest in the following permitted investments: • Foreign Shariah-compliant securities and Shariah-compliant equity-related securities (as approved by the

respective advisory council / Shariah adviser) traded in foreign markets under the rules of an eligible market and subject to the limit as may be permitted for investment by the relevant authorities from time to time;

• Shariah-compliant securities and Shariah-compliant equity-related securities listed on the Bursa Malaysia and any other market considered as an eligible market;

• Shariah-compliant securities issued by government and government-related agencies including Bank Negara Malaysia negotiable notes, government investment issues and any other government Islamic papers;

• Malaysian currency balances in hand, Malaysian currency placed with Islamic licensed financial institutions including Islamic negotiable instruments, Islamic accepted bills and placement of money at call with Islamic licensed financial institutions and any other Shariah-compliant instrument capable of being converted into cash within such time pursuant to the requirement under the relevant laws;

• Cagamas Islamic sukuk, unlisted sukuk that are either bank guaranteed or rated by RAM Holdings Berhad, Malaysian Rating Corporation Berhad or any other permitted rating agency;

• Units of other Shariah-compliant collective investment schemes that contribute to or meet the Fund’s objective; and

• Any other form of Shariah-compliant investments as may be agreed upon by the Manager and Trustee from time to time and permitted by the relevant authorities.

INVESTMENT RESTRICTIONS AND LIMITS The purchase of investments shall be subject to the following restrictions:

Spread Of Investments On Single Issuer • The value of the Fund's investments in the Shariah-compliant ordinary shares issued by any single issuer

must not exceed 10% of the Fund’s NAV or any other limit set by the Securities Commission; • The value of the Fund's investments in transferable Shariah-compliant securities and the Islamic money

market instruments issued by any single issuer must not exceed 15% of the Fund’s NAV or any other limit set by the Securities Commission; and

• The aggregate value of the Fund’s investments in transferable Shariah-compliant securities, Islamic money market instruments and Islamic deposits issued by or placed with (as the case may be) any single issuer / institution must not exceed 25% of the Fund’s NAV or any other limit set by the Securities Commission.

Exposure Limits The value of the Fund’s investments in unlisted Shariah-compliant securities must not exceed 10% of the Fund’s NAV or any other limit set by the Securities Commission. However, this exposure limit does not apply to “Shariah-compliant unlisted securities” that are: • Shariah-compliant equities not listed or quoted on a stock exchange but have been approved by the relevant

regulatory authority for such listing and quotation, and are offered directly to the Fund by the issuer; and • Sukuk traded on an organised OTC market.

Spread Of Investments On Groups Of Companies The value of the Fund's investments in transferable Shariah-compliant securities and the Islamic money market instruments issued by any group of companies must not exceed 20% of the Fund’s NAV or any other limit set by the Securities Commission.

21 More Information About The Pacific Dynamic Global Islamic Fund

Concentration Of Investments • The Fund's investments in transferable Shariah-compliant securities (other than sukuk) must not exceed 10%

of the Shariah-compliant security issued by any single issuer or any other limit set by the Securities Commission;

• The Fund’s investment in any class of sukuk of any single issuer must not exceed 20% of the sukuk issued by any single issuer or any other limit set by the Securities Commission; and

• The Fund’s investments in Islamic money market instruments must not exceed 10% of the instruments issued by any single issuer or any other limit set by the Securities Commission. This limitation will not apply to Islamic money market instruments that do not have a pre-determined issue size.

Shariah-Compliant Collective Investment Schemes • The Fund will only invest in other Shariah-compliant collective investment schemes in accordance with the

provisions and limits set by the Securities Commission; • The value of the Fund’s investments in units/shares of any Shariah-compliant collective investment schemes

must not exceed 20% of the Fund’s NAV or any other limit set by the Securities Commission; and • The Fund’s investments in Shariah-compliant collective investment schemes must not exceed 25% of the

units/shares in any one Shariah-compliant collective investment scheme or any other limit set by the Securities Commission.

Placement Of Islamic Deposits The value of the Fund’s placement in Islamic deposits with any single licensed financial institution must not exceed 20% of the Fund’s NAV or any other limit set by the Securities Commission.

The investment restrictions and limits must be complied with at all times based on the current value of the Fund's investments. However, the limits above may be breached by up to a maximum of 5% above the restrictions where the restriction is breached through a rise or fall of the NAV of the Fund (which could be due to fluctuations in value of the Fund’s investments, or from redemption of units or payments made out of the Fund). No additional investments may be made in the category of investment where the investment limit has been exceeded and the Manager will take all necessary steps and actions to rectify the breach within three months from the date of the breach. The limits and restrictions stated above do not apply to securities/instruments issued or guaranteed by the Malaysian government or Bank Negara Malaysia.

The Fund may source for Shariah-compliant financing from Islamic licensed financial institutions for the purpose of meeting redemption requests for units and lending of securities based on Islamic contract as permitted by the SC Guidelines or other relevant laws.

Note: Transferable Shariah-compliant securities refer to Shariah-compliant equities and equity-related securities, and sukuk.

22 More Information About The Pacific Dynamic Global Islamic Fund

RISK MANAGEMENT STRATEGIES AND TECHNIQUES Our risk management strategy is to conduct fundamental analysis of economic, financial and socio-political factors, both locally and globally, to ascertain the potential risk-reward of different asset classes. Individual stocks and fixed income investments are further screened by detailed analysis of each security and its underlying business and fundamentals. For this Fund, procedures will be made to ensure that all investments are fully in compliance with Shariah requirements.

The Fund’s portfolio risk is mitigated by diversifying across asset categories and industries/sectors. Percentage holdings in different asset categories are actively monitored and these percentages are raised or reduced from time to time depending on the risk-reward potential for each investment. This would include reallocation between asset classes to mitigate risk from expected declines in an asset class. Specific risk management strategies for the risks that the Fund is subject to can also be found on pages 11 to 13.

The Fund will be guided by the following general principles to control company specific risk*: • Ensure that the risk taken for any specific security is not too large1 and a reasonable spread of active risk2 is

maintained across different sectors. Investments which have low contributions3 to active risk will have larger position limits than investments which have high contributions4 to active risk. The limit per security will be within the limit set by the Investment Committee in compliance with the SC Guidelines; and

• Ensure that the risk associated with the overall position taken for the group of companies is not too large1 and within the limit set by the Securities Commission.

Notes: 1. Not too large: Each security is limited to a maximum of 10% of NAV. For investments in securities issued by a

group of companies, the limit is 20% of NAV. 2. Reasonable spread of active risk: The Manager employs active risk to outperform the Fund’s benchmark –

where active risk is the strategy to hold stocks in the Fund not in the same percentage as the benchmark’s (i.e. the equity component of the benchmark) holdings per stock. A reasonable spread, i.e. 20 to 30 securities, is an appropriate number to achieve the desired outperformance.

3. Low contributions: Securities whose prices fluctuate less than the relevant benchmark – i.e. lower risk, lower return potential.

4. High contributions: Securities whose prices fluctuate more than the relevant benchmark – i.e. higher risk, higher return potential.

In addition, the following investment procedures and internal controls are designed to control operational risk** for the Fund: • There is strict division of duties between securities trading, confirmation, settlement and valuation; • There are rules on trading and preventing employees to act on insider information. The Legal, Risk &

Compliance Department will monitor compliance and enforce disciplinary actions on any employee who has breached the code of conduct and compliance manual;

• There is daily computation of the Fund’s NAV and independent verification and reconciliation; • There are procedures for senior management, Trustee, Investment Committee and the Board of Directors to

be informed promptly, to investigate and to ensure timely and appropriate rectification of any deviation and non-compliance that may arise;

• There are limits to the placement maintained at Islamic licensed financial institutions to manage credit risk exposure;

• There are limits on shares traded with stock brokers to manage settlement risk exposure; and • There are limits and criteria set on credit rating of sukuk and Islamic money market instruments.

* Company specific risk refers to external risk associated with the listed company’s share price movements. ** Operational risk refers to the risk associated with inadequate systems and controls.

Specific Risk Management For Foreign Investments • Country and/or foreign securities risks and currency risk – Diversification of the foreign portion of the

portfolio in different countries/markets and currencies reduces potential losses to the Fund from a downtrend in any particular market or currency. Risk management is further enhanced through the implementation of monitoring processes to identify potential changes in valuation of investments due to changes in market, political and/or regulatory environment of the countries in which the Fund has invested in.

• Operational risk – Operational risk arising from international settlement and custody risks are managed through the appointment of an international global custodian.

23 More Information About The Pacific Dynamic Global Islamic Fund

FREQUENCY OF TRADING The Fund may engage in trading activities when opportunities arise. Opportunities would include but are not limited to arbitrage situations, discrepancies in valuation, expected liquidity surges and thematic plays. Where trading activities in the Fund results in an annualised portfolio turnover that exceeds 2.0 times at the end of every month, the Manager will be required to provide justification to the Fund’s Investment Committee.

BASES OF VALUATION OF INVESTMENTS Pursuant to the SC Guidelines, all assets of the Fund should be valued in a fair and accurate manner at all times. The Fund is generally valued in accordance with its respective asset classes: • Listed Shariah-compliant securities and equity-related securities will be valued based on the last done prices

as at the close of the business day of the respective stock exchanges on the same calendar day. Please refer to page 26 for details on the valuation of NAV. However, if a valuation based on the market price does not represent the fair value of Shariah-compliant securities or equity-related securities, or no market price is available due to situations beyond the Manager’s control or there is a suspension in the quotation of the Shariah-compliant securities for a period exceeding 14 days, or such other shorter period as agreed by the Trustee, then the Shariah-compliant securities shall be valued at fair value, as determined by the Manager, based on the methods approved by the Trustee after appropriate technical consultation;

• Unlisted sukuk will be valued on a daily basis based on fair value prices quoted by a bond pricing agency (BPA) registered with the Securities Commission. If the Manager is of the view that the price quoted by the BPA for a specific sukuk differs from the market price by more than 20 basis points, the Manager may use the market price provided that the Manager adheres to the requirements as stipulated in the SC Guidelines;

• In terms of a successful subscription to an Initial Public Offering (IPO), if any, the IPO securities will be valued at cost prior to their listing. These IPO securities will then be valued at their last done market price upon listing;