management accounting fundamentals - cga-education.org · part 1 – flexible budgets (topic 8.1)...

TRANSCRIPT

Management AccountingFundamentals

Module 8Flexible budgets and

decentralizationLectures and handouts by:Shirley Mauger, HB Comm, CGA

2

Module 8 - Table of Contents

8.1 Flexible budgets8.2 Variable overhead variances8.3 Overhead rates and standard costing8.4 Fixed overhead budget and volume variances8.5 Computer illustration 8-1: Fixed costs in a flexible

budget8.6 Full income statement variance analysis8.7 Decentralization in organizations8.8 Segment reporting8.9 Revenue variance and marketing expense analysis8.10 Rate of return and residual incomeReview question: Variance analysis, working backwards

from dataReview question: Segmented statementsReview question: Segmented statements, ROI and residual

incomeReview question: Multiple choice

1

2

N/A

3

456

78

9

Part Content

3

Part 1

Flexible budgetsVariable overhead

variances

Topics 8.1-8.2

MA1 – MODULE 8

Part 1 – Flexible budgets (Topic 8.1)Prepare a flexible budget, and explain the advantages of theflexible budget approach over the static budget approach. (Level 1)

4

Static budget

• Designed for only one level of activity

• If activity is lower than budget, variable cost varianceswill usually be favorable

• When analyzing variances, volume and spendingvariances are combined so cannot be controlled.

• Does not indicate whether output was producedefficiently

Part 1 – Flexible budgets (Topic 8.1)Prepare a flexible budget, and explain the advantages of theflexible budget approach over the static budget approach. (Level 1)

5

Flexible budget

• Designed to cover a range of activity

• Can be used to develop budgeted costs atany point within the relevant range

• Usually compares actual and budgetedresults at the same level of activity

• Identifies the ability to control costs, andefficiency.

Part 1 – Flexible budgets (Topic 8.1)

6

What is the static-budget operating income?

Parker Co. manufactures and sells desks.Budgeted variable costs per desk are:

Direct materials cost $ 130Direct manufacturing labour 52Variable overhead 48Total variable costs/unit $ 230

•Budgeted selling price is $300 per desk•Fixed overhead costs are expected to be $52,500•The static budget for the year 2008 is based on selling1,500 desks

Stop the audio, turn to page 1 of handout 1.(ma1_mod8_handout1.pdf)

Part 1 – Flexible budgets (Topic 8.1)

7

1. What is the static-budget operating income?

Parker Co.

Unit costs StaticBudget

Activity level 1,500Sales: $ 300 $ 450,000Variablecosts 230 (345,000)Fixedoverhead 52,500 (52,500)Income fromoperations $ 52,500

Part 1 – Flexible budgets (Topic 8.1)

8

Actual costs incurred….

Parker Co.

Actual StaticBudget

Activity level 1,300 1,500Sales: $300 $410,000 $450,000Variablecosts $230 (330,000) (345,000)Fixedoverhead (61,500) (52,500)Income fromoperations $ 18,500 $52,500

Part 1 – Flexible budgets (Topic 8.1)

9

Budget variances….

Parker Co.

Actual Variance StaticBudget

Activity level 1,300 200 1,500Sales: $300 $410,000 $40,000U $450,000Variablecosts $230 (330,000) 15,000F (345,000)Fixedoverhead (61,500) 9,000U (52,500)Income fromoperations $ 18,500 $ 34,000U $52,500

Part 1 – Flexible budgets (Topic 8.1)

10

Budget variances….

Parker Co.

Actual Variance StaticBudget

Activity level 1,300 200 1,500Sales: $300 $410,000 $40,000U $450,000Variablecosts $230 (330,000) 15,000F (345,000)Fixedoverhead (61,500) 9,000U (52,500)Income fromoperations $ 18,500 $ 34,000U $52,500

Is this reallyfavorable?

Part 1 – Flexible budgets (Topic 8.1)

11

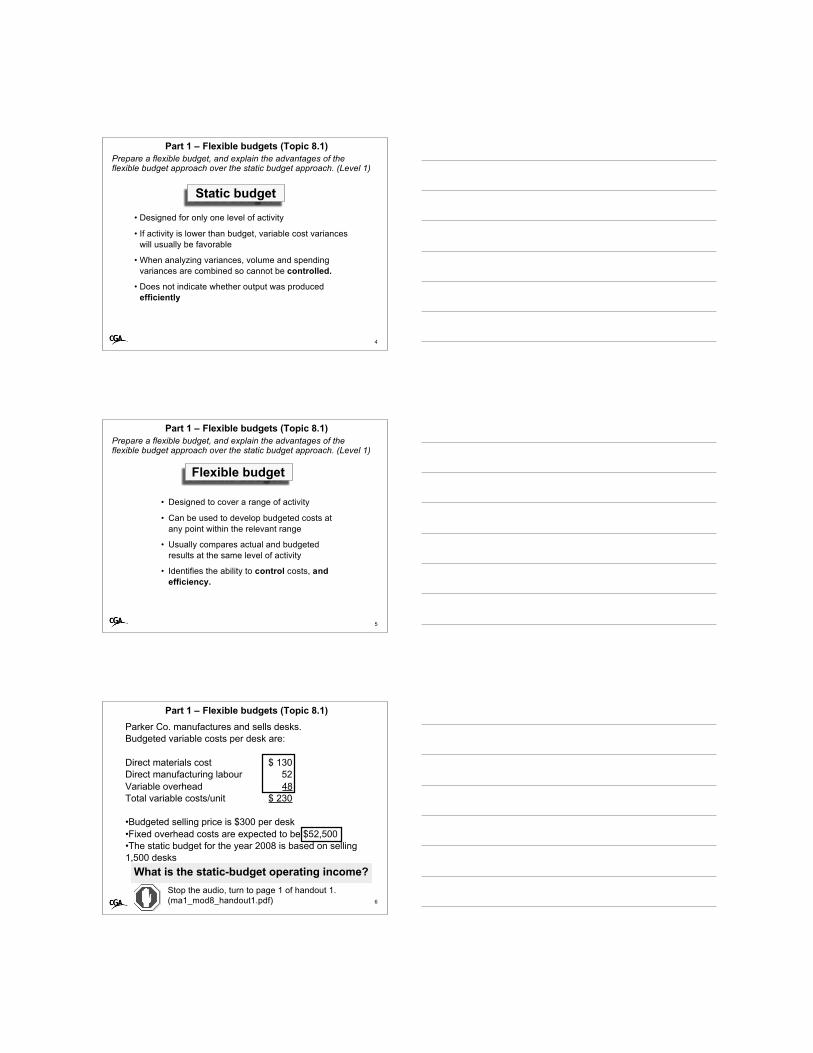

2. Prepare a flexible budget at the actuallevel of operations.

Parker Co.

Actual FlexibleBudget

StaticBudget

Activity level 1,300 1,300 1,500Sales: $300 $410,000 $450,000Variablecosts $230 (330,000) (345,000)Fixedoverhead (61,500) (52,500)Income fromoperations $ 18,500 $52,500

Part 1 – Flexible budgets (Topic 8.1)

12

2. Prepare a flexible budget at the actuallevel of operations.

Parker Co.

Actual FlexibleBudget

StaticBudget

Activity level 1,300 1,300 1,500Sales: $300 $410,000 $390,000 $450,000Variablecosts $230 (330,000) (345,000)Fixedoverhead (61,500) (52,500)Income fromoperations $ 18,500 $52,500

$300 per unitx 1,300 units

Part 1 – Flexible budgets (Topic 8.1)

13

2. Prepare a flexible budget at the actuallevel of operations.

Parker Co.

Actual FlexibleBudget

StaticBudget

Activity level 1,300 1,300 1,500Sales: $300 $410,000 $390,000 $450,000Variablecosts $230 (330,000) (299,000) (345,000)Fixedoverhead (61,500) (52,500)Income fromoperations $ 18,500 $52,500

$230 per unitx 1,300 units

Part 1 – Flexible budgets (Topic 8.1)

14

2. Prepare a flexible budget at the actuallevel of operations.

Parker Co.

Actual FlexibleBudget

StaticBudget

Activity level 1,300 1,300 1,500Sales: $300 $410,000 $390,000 $450,000Variablecosts $230 (330,000) (299,000) (345,000)Fixedoverhead (61,500) (52,500) (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

Fixed costsremain the same

Part 1 – Flexible budgets (Topic 8.1)

15

The flexible budget variance is also calledbudget variance.

Parker Co.

Actual Flexiblebudget

variance

FlexibleBudget

Salesvolume

variance

StaticBudget

Activity level 1,300 0 1,300 200U 1,500Sales: $300 $410,000 $20,000 F $390,000 $450,000Variablecosts $230 (330,000) 31,000 U (299,000) (345,000)Fixedoverhead (61,500) 9,000 U (52,500) 0 (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

Part 1 – Flexible budgets (Topic 8.1)

16

A sales volume variance identifies the variancesresulting from changes in activity levels.

Parker Co.

Actual Flexiblebudget

variance

FlexibleBudget

Salesvolume

variance

StaticBudget

Activity level 1,300 0 1,300 200U 1,500Sales: $300 $410,000 $20,000 F $390,000 $ 60,000 U $450,000Variablecosts $230 (330,000) 31,000 U (299,000) 46,000 F (345,000)Fixedoverhead (61,500) 9,000 U (52,500) 0 (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

Part 1 – Flexible budgets (Topic 8.1)

17

A sales volume variance identifies the variancesresulting from changes in activity levels.

Parker Co.

Actual Flexiblebudget

variance

FlexibleBudget

Salesvolume

variance

StaticBudget

Activity level 1,300 0 1,300 200U 1,500Sales: $300 $410,000 $20,000 F $390,000 $ 60,000 U $450,000Variablecosts $230 (330,000) 31,000 U (299,000) 46,000 F (345,000)Fixedoverhead (61,500) 9,000 U (52,500) 0 (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

Fixed OH nevershows a sales

volume variance

Part 1 – Flexible budgets (Topic 8.1)

18

A closer look at overhead…

Parker Co.

Actual Flexiblebudget

variance

FlexibleBudget

Salesvolume

variance

StaticBudget

Activity level 1,300 0 1,300 200U 1,500Sales: $300 $410,000 $20,000 F $390,000 $ 60,000 U $450,000Variablecosts $230 (330,000) 31,000 U (299,000) 46,000 F (345,000)Fixedoverhead (61,500) 9,000 U (52,500) 0 (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

Part 1 – Flexible budgets (Topic 8.1)

19

STANDARD COST CARD – 1 DESK

Direct materials: $126Direct labour (5 hours at $12/hour 60Variable overhead (5 DLH at $8.80/hour) 44*Fixed overhead (5 DLH at $7.00/hour) 35Total standard costs per desk: $265

(*Based on a denominator level of activity of 1,500 desks)

Part 1 – Flexible budgets (Topic 8.1)

20

Parker Co.

Actual Flexiblebudget

variance

FlexibleBudget

Salesvolume

variance

StaticBudget

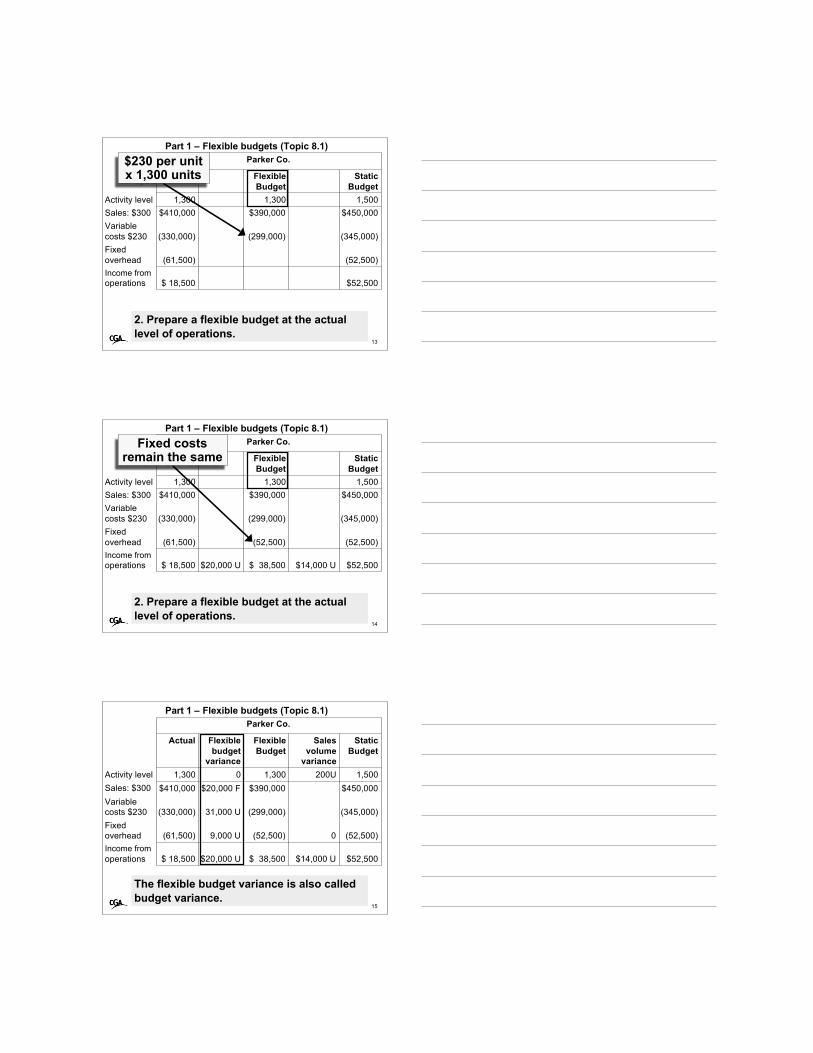

Activity level 1,300 0 1,300 200U 1,500Sales: $300 $410,000 $20,000 F $390,000 $ 60,000 U $450,000Direct mat. (180,000) (189,000)Direct labour (87,800) (90,000)Variable OH (62,200) (66,000)Fixed OH (61,500) 9,000 U (52,500) 0 (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

DM: 1,500 x $126DL: 1,500 x $ 60VOH: 1,500 x $ 44

Part 1 – Flexible budgets (Topic 8.1)

21

Parker Co.

Actual Flexiblebudget

variance

FlexibleBudget

Salesvolume

variance

StaticBudget

Activity level 1,300 0 1,300 200U 1,500Sales: $300 $410,000 $20,000 F $390,000 $ 60,000 U $450,000Direct mat. (180,000) (163,800) (189,000)Direct labour (87,800) (78,000) (90,000)Variable OH (62,200) (57,200) (66,000)Fixed OH (61,500) 9,000 U (52,500) 0 (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

DM: 1,300 x $126DL: 1,300 x $ 60VOH: 1,300 x $ 44

Part 1 – Flexible budgets (Topic 8.1)

22

Parker Co.

Actual Flexiblebudget

variance

FlexibleBudget

Salesvolume

variance

StaticBudget

Activity level 1,300 0 1,300 200U 1,500Sales: $300 $410,000 $20,000 F $390,000 $ 60,000 U $450,000Direct mat. (180,000) 16,200 U (163,800) 25,200 F (189,000)Direct labour (87,800) 9,800 U (78,000) 12,000F (90,000)Variable OH (62,200) 5,000 U (57,200) 8,800F (66,000)Fixed OH (61,500) 9,000 U (52,500) 0 (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

What drives variable overhead costs?

Part 1 – Flexible budgets (Topic 8.1)

23

An activity base for variable overhead:

• Should be a causal relationship• Should not be expressed in a currency• Should be simple and easy to understand

Part 1 – Flexible budgets (Topic 8.1)

24

Parker Co.

Actual Flexiblebudget

variance

FlexibleBudget

Salesvolume

variance

StaticBudget

Activity level 1,300 0 1,300 200U 1,500Sales: $300 $410,000 $20,000 F $390,000 $ 60,000 U $450,000Direct mat. (180,000) 16,200 U (163,800) 25,200 F (189,000)Direct labour (87,800) 9,800 U (78,000) 12,000F (90,000)Variable OH (62,200) 5,000 U (57,200) 8,800F (66,000)Fixed OH (61,500) 9,000 U (52,500) 0 (52,500)Income fromoperations $ 18,500 $20,000 U $ 38,500 $14,000 U $52,500

Explain the $5,000variance

3. Calculate the variable overhead spending andefficiency variances.

Efficiency variance:(2) – (3)

Spending variance:(1) – (2)

25

Variable overhead variances(1)

AQ x AR$62,200(given)

(3)SQ x SR

Total variance (1)-(3)

(2)AQ x SR

Part 1 – Variable overhead variances (Topic 8.2)Prepare a variable overhead performance report using theflexible budget to show only a spending variance and to showboth spending and efficiency variances. (Level 1)

Efficiency variance:(2) – (3)

Spending variance:(1) – (2)

26

Variable overhead variances(1)

AQ x AR$62,200(given)

(3)SQ x SR

5 hours x 1,500desks x $8.80 =

$57,200

Total variance $62,200 - $57,200=$5,000 U

(2)AQ x SR

Part 1 – Variable overhead variances (Topic 8.2)

Efficiency variance:(2) – (3)

Spending variance:$62,200-68,640 =

$6,440 F

27

Variable overhead variances(1)

AQ x AR$62,200(given)

(3)SQ x SR

5 hours x 1,500desks x $8.80 =

$57,200

Total variance $62,200 - $57,200=$5,000 U

(2)AQ x SR

6 hours x 1,300desks x $8.80 =

$68,640

Part 1 – Variable overhead variances (Topic 8.2)

Efficiency variance:$68,640-57,200 =

$11,440 U

Spending variance:$62,200-68,640 =

$6,440 F

28

Variable overhead variances(1)

AQ x AR$62,200(given)

(3)SQ x SR

5 hours x 1,500desks x $8.80 =

$57,200

Total variance $62,200 - $57,200=$5,000 U

(2)AQ x SR

6 hours x 1,300desks x $8.80 =

$68,640

Part 1 – Variable overhead variances (Topic 8.2)

29

What is the significance of the:Spending variance?•If based on actual hours worked it indicates how muchshould have been spent on variable overhead.

Efficiency variance?•If based on actual hours worked it indicates how manymore resources were used as a result of inefficient use ofthe activity base. (DLH in this case)

(AQxAR)-(AQ-SR)$62,200 – (6500 hours x $8.80)

$62,200-68,640 = $6,440 F

(AQxSR)-(SQ-SR) (6500 hours x $8.80)-(7,500 hours x $8.80)

$68,640-57,200 = 11,440 U

Part 1 – Variable overhead variances (Topic 8.2)

30

Part 2Overhead rates and standard

costingFixed overhead budget and

volume variancesFull income statement variance

analysis

Topics 8.3-8.6

MA1 – MODULE 8

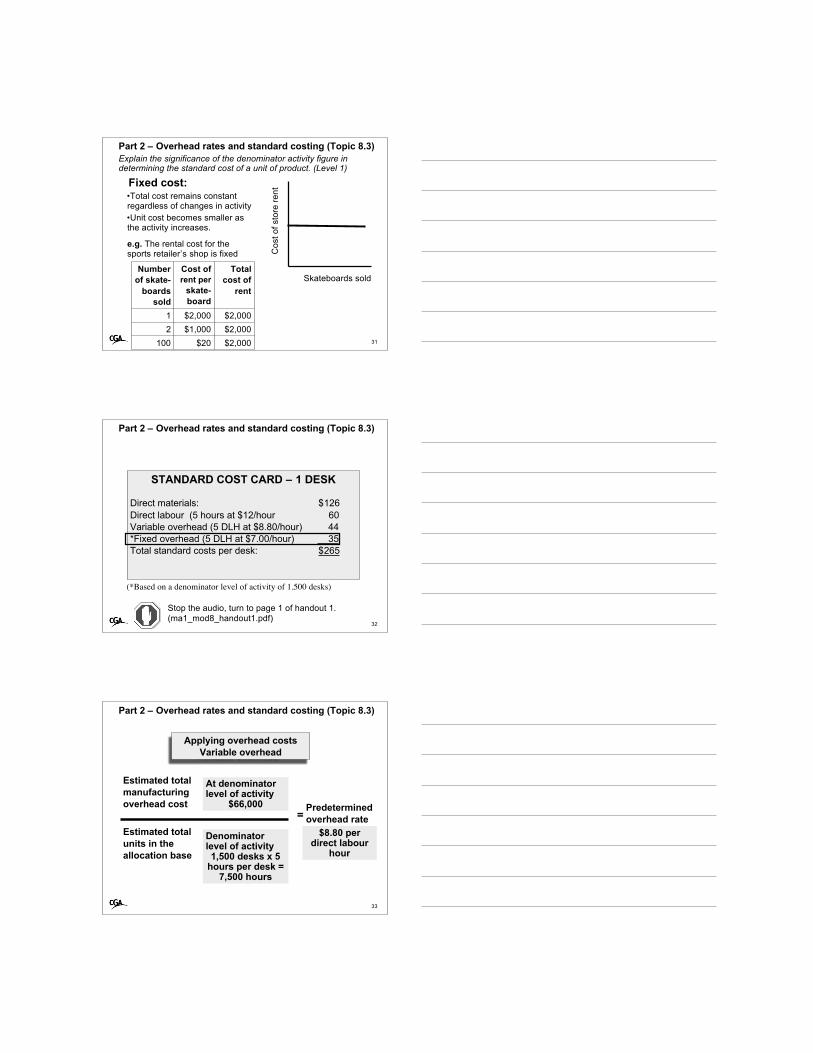

Part 2 – Overhead rates and standard costing (Topic 8.3)Explain the significance of the denominator activity figure indetermining the standard cost of a unit of product. (Level 1)

31

Fixed cost:•Total cost remains constantregardless of changes in activity•Unit cost becomes smaller asthe activity increases.

e.g. The rental cost for thesports retailer’s shop is fixed

Skateboards soldC

ost o

f sto

re re

ntNumber

of skate-boards

sold

Cost ofrent per

skate-board

Totalcost of

rent

1 $2,000 $2,0002 $1,000 $2,000

100 $20 $2,000

32

STANDARD COST CARD – 1 DESK

Direct materials: $126Direct labour (5 hours at $12/hour 60Variable overhead (5 DLH at $8.80/hour) 44*Fixed overhead (5 DLH at $7.00/hour) 35Total standard costs per desk: $265

(*Based on a denominator level of activity of 1,500 desks)

Part 2 – Overhead rates and standard costing (Topic 8.3)

Stop the audio, turn to page 1 of handout 1.(ma1_mod8_handout1.pdf)

Part 2 – Overhead rates and standard costing (Topic 8.3)

33

Predeterminedoverhead rate

Applying overhead costsVariable overhead

=

Estimated totalmanufacturingoverhead cost

Estimated totalunits in theallocation base

At denominatorlevel of activity

$66,000

Denominatorlevel of activity1,500 desks x 5

hours per desk =7,500 hours

$8.80 perdirect labour

hour

Part 2 – Overhead rates and standard costing (Topic 8.3)

34

Predeterminedoverhead rate

Applying overhead costsFixed overhead

=

Estimated totalmanufacturingoverhead cost

Estimated totalunits in theallocation base

At denominatorlevel of activity

$52,500

Denominatorlevel of activity1,500 desks x 5

hours per desk =7,500 hours

$7.00 perdirect labour

hour

Part 2 – Overhead rates and standard costing (Topic 8.3)

35

Applying overhead costs ina standard costing system

Fixed overhead

Manufacturing overhead

Actualcosts

incurred

Overheadapplied

Manufacturing overhead

$61,500 1,300 desks at$7 per DLH x 5hours =$45,500$16,000underapplied

Volume variance:(2)-(3)

Budget variance:(1)-(2)

36

Fixed overhead variances(1)

Actual cost$61,500

(3)AU x SQ x SR

Total variance (1)-(3)

(2)BU x SQ x SR

Budgeted units= Denominatorlevel of activity

Part 2 – Fixed overhead budget and volume variances(Topic 8.4)

Compute and properly interpret the fixed overhead budget andvolume variances. (Level 1)

Volume variance:(2)-(3)

Budget variance:(1)-(2)

37

Fixed overhead variances(1)

Actual cost$61,500

(3)AU x SQ x SR

1,300 desks x 5hours x $7=

$45,500

Total variance $61,500 - $45,500 = $16,000 U

(2)BU x SQ x SR

Budgeted units= Denominatorlevel of activity

Part 2 – Fixed overhead budget and volume variances(Topic 8.4)

Volume variance:(2)-(3)

Budget variance:(1)-(2)

38

Fixed overhead variances(1)

Actual cost$61,500

(3)AU x SQ x SR

1,300 desks x 5hours x $7=

$45,500

Total variance $61,500 - $45,500 = $16,000 U

(2)BU x SQ x SR

1,500 desks x 5hours x $7=

$52,500

Part 2 – Fixed overhead budget and volume variances(Topic 8.4)

Volume variance:(2)-(3)

Budget variance:$61,500 - $52,500 =

$9,000 U

39

Fixed overhead variances(1)

Actual cost$61,500

(3)AU x SQ x SR

1,300 desks x 5hours x $7=

$45,500

Total variance $61,500 - $45,500 = $16,000 U

(2)BU x SQ x SR

1,500 desks x 5hours x $7=

$52,500

Part 2 – Fixed overhead budget and volume variances(Topic 8.4)

More was spentthan planned

Volume variance:$52,500 - $45,500 =

$7,000 U

Budget variance:$61,500 - $52,500 =

$9,000 U

40

Fixed overhead variances(1)

Actual cost$61,500

(3)AU x SQ x SR

1,300 desks x 5hours x $7=

$45,500

Total variance $61,500 - $45,500 = $16,000 U

(2)BU x SQ x SR

1,500 desks x 5hours x $7=

$52,500

Part 2 – Fixed overhead budget and volume variances(Topic 8.4)

200 less units wereproduced and sold

Part 2 – Full income statement variance analysis (Topic 8.6)Prepare an income statement incorporating variance analysis.(Level 2)

41

Direct Materials

Direct Labour

Variable Manufacturing OH

Fixed Manufacturing OH

Variable Selling and Admin Exp.

Fixed Selling and Admin Exp.

VariableCosting

AbsorptionCosting

ProductCosts

PeriodCosts

ProductCosts

PeriodCosts

© McGraw-Hill Ryerson Limited., 2004

Product and period costs

Part 2 – Full income statement variance analysis (Topic 8.6)

42

Direct Mat.

Direct Labour

VMOH

FMOH

Variable S&A

Fixed S&A

AbsorptionCosting

ProductCosts

PeriodCosts

© McGraw-Hill Ryerson Limited., 2004

Product and period costs

Write off allvariances to cost

of goods sold

No variances.Report as period

costs

43

Income statement format – Absorption costing

Part 2 – Full income statement variance analysis (Topic 8.6)

Sales $xxxCost of goods sold (standard costs) $xxx

Writeoff variancesDirect materials price and quantity xxxDirect labour rate and efficiency xxxVariable overhead spending and efficiency xxxFixed overhead spending and volume xxx

Adjusted cost of goods sold xxxGross profit xxxVariable selling and administration xxxFixed selling and administration xxx

Net income $xxx

Part 2 – Full income statement variance analysis (Topic 8.6)

44

VariableCosting

ProductCosts

PeriodCosts

© McGraw-Hill Ryerson Limited., 2004

Product and period costs

Direct Mat.

Direct Labour

VMOH

FMOH

Variable S&A

Fixed S&A

Write off allvariances to cost

of goods sold

No variances.Report as period

costs

45

Income statement format – Variable costing

Part 2 – Full income statement variance analysis (Topic 8.6)

Sales $xxxCost of goods sold (standard costs) $xxx

Writeoff variancesDirect materials price and quantity xxxDirect labour rate and efficiency xxxVariable overhead spending and efficiency xxx

Adjusted cost of goods sold xxxVariable selling and administration xxx xxx

Contribution margin xxxFixed manufacturing overhead xxxFixed selling and administration xxx

Net income $xxx

46

Part 3

Decentralization inorganizations

Segment reporting

Topics 8.7-8.8

MA1 – MODULE 8

Part 3 – Decentralization in organizations (Topic 8.7)Differentiate between cost centres, profit centres, andinvestment centres, and explain how performance is measuredin each. (Level 2)

47

Board of directors

CEO

Westerndivision

Easterndivision

Director ofhumanresources

Consumerproducts

Industrialproducts

Consumerproducts

Industrialproducts

DecentralizationDecision making isspread throughoutthe organization

48

Segment

‘Any part or activity of an organizationabout which the manager seeks cost,revenue or profit data.’

Chapter 12, p.547

Part 3 – Decentralization in organizations (Topic 8.7)

49

Responsibilityaccounting

• Gives managers greater control over theirsegments

• Keeps decisions in the hands of people whosee and understand the problems

• Serves as a motivating tool

• Enhances employee development

• Promotes job satisfaction

• Provides a basis for evaluation

Part 3 – Decentralization in organizations (Topic 8.7)

Part 3 – Decentralization in organizations (Topic 8.7)

50

Performance is measuredbased on control over:

Investmentcentre

Costcentre

Profitcentre

Costs RevenuesInvest-ments

Part 3 – Decentralization in organizations (Topic 8.7)

51

Board of directors

CEO

Westerndivision

Easterndivision

Director ofhumanresources

Consumerproducts

Industrialproducts

Consumerproducts

Industrialproducts

Responsibility centres

Costcentre

Profit centres

Investmentcentre

Part 3 – Segment reporting (Topic 8.8)Prepare a segmented income statement using the contributionformat, and explain the difference between traceable fixed costsand common fixed costs. (Level 1)

52

Segment reporting

• Provides more information on profitability thancompany wide reports

• Can highlight problems and opportunities withinan organization

• Reduces the effects of cross subsidization• Costs not traced directly to the segment• Costs allocated using an inappropriate base

Part 3 – Segment reporting (Topic 8.8)

53

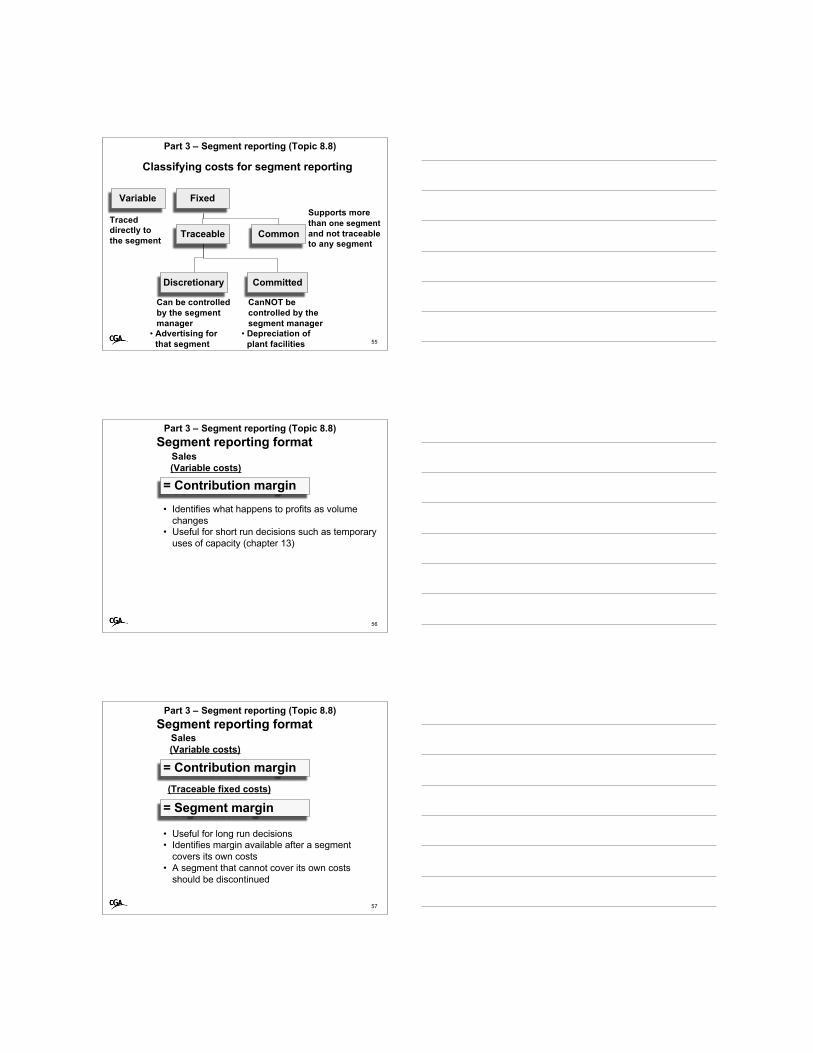

Classifying costs for segment reporting

Traceddirectly tothe segment

Variable Fixed

Variable costof goods sold

Stop the audio, turn to page 4 of handout 1.(ma1_mod8_handout1.pdf)

Part 3 – Segment reporting (Topic 8.8)

54

Classifying costs for segment reporting

Traceddirectly tothe segment

Variable Fixed

Traceable Common

Supports morethan one segmentand not traceableto any segment

• Salary of the CEO• Shared

equipment costs

Directly supportsthe segment. Canbecome commonas segments arefurther divided.• Salary of the

segment manager.

Part 3 – Segment reporting (Topic 8.8)

55

Classifying costs for segment reporting

Traceddirectly tothe segment

Variable Fixed

Common

Supports morethan one segmentand not traceableto any segment

Can be controlledby the segmentmanager

CanNOT becontrolled by thesegment manager

• Advertising forthat segment

• Depreciation ofplant facilities

Traceable

Discretionary Committed

Part 3 – Segment reporting (Topic 8.8)

56

• Identifies what happens to profits as volumechanges

• Useful for short run decisions such as temporaryuses of capacity (chapter 13)

= Contribution margin

Sales(Variable costs)

Segment reporting format

Part 3 – Segment reporting (Topic 8.8)

57

• Useful for long run decisions• Identifies margin available after a segment

covers its own costs• A segment that cannot cover its own costs

should be discontinued

= Contribution margin

Sales(Variable costs)

(Traceable fixed costs)

= Segment margin

Segment reporting format

Part 3 – Segment reporting (Topic 8.8)

58

= Contribution margin

Sales(Variable costs)

(Traceable fixed costs)

= Segment margin

• Corporate wide income

Segment reporting format

= Net income(Common costs)

Part 3 – Segment reporting (Topic 8.8)

59

Restructuring a segmented income statement

Stop the audio, and turn to problem12-16, page 592-593 and page 5 ofhandout 1.

Part 3 – Segment reporting (Topic 8.8)

60

Restructuring a segmented income statementS. Europe Mid.Europe N.Europe

Sales € 300,000 €800,000 €700,000Territorial expenses

Cost of goods sold 93,000 240,000 315,000Salaries 54,000 56,000 112,000Insurance 9,000 16,000 14,000Advertising 105,000 240,000 245,000Depreciation 21,000 32,000 28,000Shipping 15,000 32,000 42,000

Total territorial expenses 297,000 616,000 756,000Income/loss before corp.exp. 3,000 184,000 (56,000)Corporate expenses

Advertising (general) 15,000 40,000 35,000General administrative 20,000 20,000 20,000

Total corporate expenses 35,000 60,000 55,000Net operating income(loss) €(32,000) €124,000 €(111,000)

VariableCosts

problem 12-16, page 592-593

Part 3 – Segment reporting (Topic 8.8)

61

Restructuring a segmented income statementS. Europe Mid.Europe N.Europe

Sales € 300,000 €800,000 €700,000Territorial expenses

Cost of goods sold 93,000 240,000 315,000Salaries 54,000 56,000 112,000Insurance 9,000 16,000 14,000Advertising 105,000 240,000 245,000Depreciation 21,000 32,000 28,000Shipping 15,000 32,000 42,000

Total territorial expenses 297,000 616,000 756,000Income/loss before corp.exp. 3,000 184,000 (56,000)Corporate expenses

Advertising (general) 15,000 40,000 35,000General administrative 20,000 20,000 20,000

Total corporate expenses 35,000 60,000 55,000Net operating income(loss) €(32,000) €124,000 €(111,000)

Traceablefixed costs

problem 12-16, page 592-593

Part 3 – Segment reporting (Topic 8.8)

62

Restructuring a segmented income statementS. Europe Mid.Europe N.Europe

Sales € 300,000 €800,000 €700,000Territorial expenses

Cost of goods sold 93,000 240,000 315,000Salaries 54,000 56,000 112,000Insurance 9,000 16,000 14,000Advertising 105,000 240,000 245,000Depreciation 21,000 32,000 28,000Shipping 15,000 32,000 42,000

Total territorial expenses 297,000 616,000 756,000Income/loss before corp.exp. 3,000 184,000 (56,000)Corporate expenses

Advertising (general) 15,000 40,000 35,000General administrative 20,000 20,000 20,000

Total corporate expenses 35,000 60,000 55,000Net operating income(loss) €(32,000) €124,000 €(111,000)

Commonfixed costs

problem 12-16, page 592-593

Part 3 – Segment reporting (Topic 8.8)

63

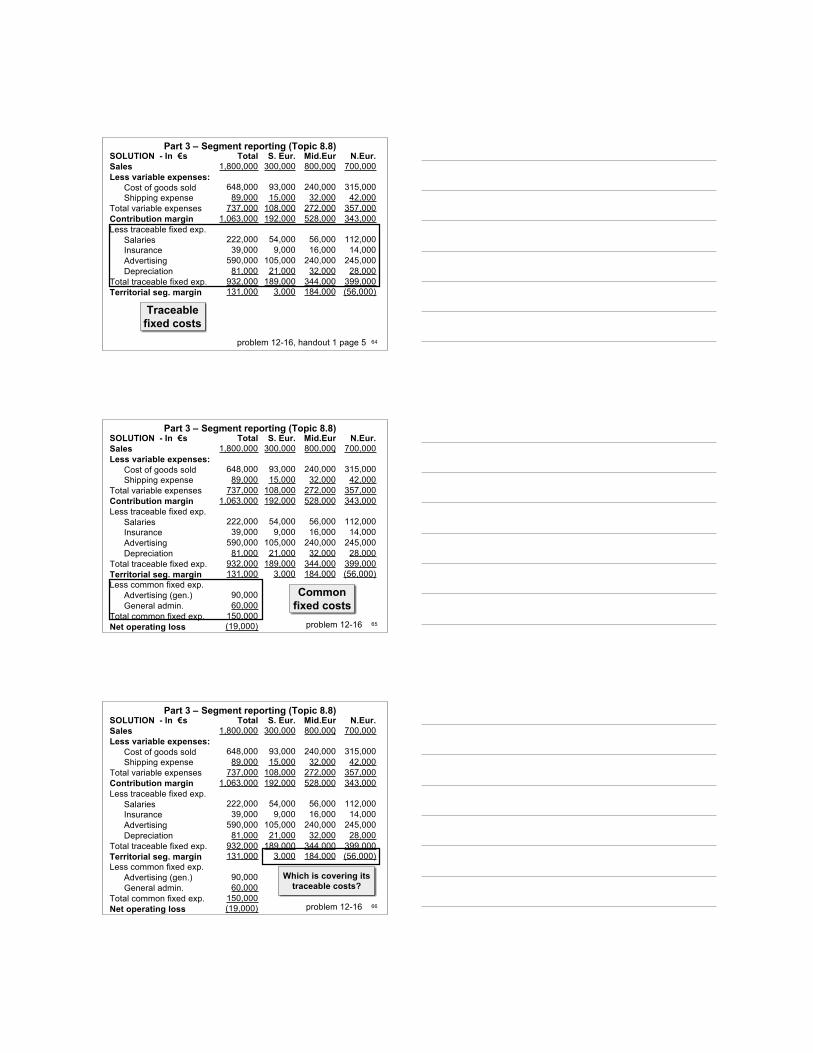

SOLUTION - In €s Total S. Eur. Mid.Eur.

N.Eur.Sales 1,800,000 300,000 800,000 700,000Less variable expenses:

Cost of goods sold 648,000 93,000 240,000 315,000Shipping expense 89,000 15,000 32,000 42,000

Total variable expenses 737,000 108,000 272,000 357,000Contribution margin 1,063,000 192,000 528,000 343,000

VariableCosts

problem 12-16, handout 1 page 5

Part 3 – Segment reporting (Topic 8.8)

64

SOLUTION - In €s Total S. Eur. Mid.Eur.

N.Eur.Sales 1,800,000 300,000 800,000 700,000Less variable expenses:

Cost of goods sold 648,000 93,000 240,000 315,000Shipping expense 89,000 15,000 32,000 42,000

Total variable expenses 737,000 108,000 272,000 357,000Contribution margin 1,063,000 192,000 528,000 343,000Less traceable fixed exp.

Salaries 222,000 54,000 56,000 112,000Insurance 39,000 9,000 16,000 14,000Advertising 590,000 105,000 240,000 245,000Depreciation 81,000 21,000 32,000 28,000

Total traceable fixed exp. 932,000 189,000 344,000 399,000Territorial seg. margin 131,000 3,000 184,000 (56,000)

Traceablefixed costs

problem 12-16, handout 1 page 5

Part 3 – Segment reporting (Topic 8.8)

65

SOLUTION - In €s Total S. Eur. Mid.Eur.

N.Eur.Sales 1,800,000 300,000 800,000 700,000Less variable expenses:

Cost of goods sold 648,000 93,000 240,000 315,000Shipping expense 89,000 15,000 32,000 42,000

Total variable expenses 737,000 108,000 272,000 357,000Contribution margin 1,063,000 192,000 528,000 343,000Less traceable fixed exp.

Salaries 222,000 54,000 56,000 112,000Insurance 39,000 9,000 16,000 14,000Advertising 590,000 105,000 240,000 245,000Depreciation 81,000 21,000 32,000 28,000

Total traceable fixed exp. 932,000 189,000 344,000 399,000Territorial seg. margin 131,000 3,000 184,000 (56,000)Less common fixed exp.

Advertising (gen.) 90,000General admin. 60,000

Total common fixed exp. 150,000Net operating loss (19,000)

Commonfixed costs

problem 12-16

Part 3 – Segment reporting (Topic 8.8)

66

SOLUTION - In €s Total S. Eur. Mid.Eur.

N.Eur.Sales 1,800,000 300,000 800,000 700,000Less variable expenses:

Cost of goods sold 648,000 93,000 240,000 315,000Shipping expense 89,000 15,000 32,000 42,000

Total variable expenses 737,000 108,000 272,000 357,000Contribution margin 1,063,000 192,000 528,000 343,000Less traceable fixed exp.

Salaries 222,000 54,000 56,000 112,000Insurance 39,000 9,000 16,000 14,000Advertising 590,000 105,000 240,000 245,000Depreciation 81,000 21,000 32,000 28,000

Total traceable fixed exp. 932,000 189,000 344,000 399,000Territorial seg. margin 131,000 3,000 184,000 (56,000)Less common fixed exp.

Advertising (gen.) 90,000General admin. 60,000

Total common fixed exp. 150,000Net operating loss (19,000)

Which is covering itstraceable costs?

problem 12-16

Part 3 – Segment reporting (Topic 8.8)

67

SOLUTION - In €s Total S. Eur. Mid.Eur. N.Eur.Sales 1,800,000 300,000 800,000 700,000Less variable expenses:

Cost of goods sold 648,000 93,000 240,000 315,000Shipping expense 89,000 15,000 32,000 42,000

Total variable expenses 737,000 108,000 272,000 357,000Contribution margin 1,063,000 192,000 528,000 343,000Less traceable fixed exp.

Salaries 222,000 54,000 56,000 112,000Insurance 39,000 9,000 16,000 14,000Advertising 590,000 105,000 240,000 245,000Depreciation 81,000 21,000 32,000 28,000

Total traceable fixed exp. 932,000 189,000 344,000 399,000Territorial seg. margin 131,000 3,000 184,000 (56,000)Less common fixed exp.

Advertising (gen.) 90,000General admin. 60,000

Total common fixed exp. 150,000Net operating loss (19,000) problem 12-16

S. Europe sales are lowerthan mid. Europe, however,

salaries are comparable

Part 3 – Segment reporting (Topic 8.8)

68

SOLUTION - In €s Total S. Eur. Mid.Eur.

N.Eur.Sales 1,800,000 300,000 800,000 700,000Less variable expenses:

Cost of goods sold 648,000 93,000 240,000 315,000Shipping expense 89,000 15,000 32,000 42,000

Total variable expenses 737,000 108,000 272,000 357,000Contribution margin 1,063,000 192,000 528,000 343,000Less traceable fixed exp.

Salaries 222,000 54,000 56,000 112,000Insurance 39,000 9,000 16,000 14,000Advertising 590,000 105,000 240,000 245,000Depreciation 81,000 21,000 32,000 28,000

Total traceable fixed exp. 932,000 189,000 344,000 399,000Territorial seg. margin 131,000 3,000 184,000 (56,000)Less common fixed exp.

Advertising (gen.) 90,000General admin. 60,000

Total common fixed exp. 150,000Net operating loss (19,000) problem 12-16

S. Europe spends less onadvertising than mid. Europe.Is this a reason for low sales?

Part 3 – Segment reporting (Topic 8.8)

69

SOLUTION - In €s Total S. Eur. Mid.Eur.

N.Eur.Sales 1,800,000 300,000 800,000 700,000Less variable expenses:

Cost of goods sold 648,000 93,000 240,000 315,000Shipping expense 89,000 15,000 32,000 42,000

Total variable expenses 737,000 108,000 272,000 357,000Contribution margin 1,063,000 192,000 528,000 343,000Less traceable fixed exp.

Salaries 222,000 54,000 56,000 112,000Insurance 39,000 9,000 16,000 14,000Advertising 590,000 105,000 240,000 245,000Depreciation 81,000 21,000 32,000 28,000

Total traceable fixed exp. 932,000 189,000 344,000 399,000Territorial seg. margin 131,000 3,000 184,000 (56,000)Less common fixed exp.

Advertising (gen.) 90,000General admin. 60,000

Total common fixed exp. 150,000Net operating loss (19,000) problem 12-16

N. Europe spends twiceas much on sales

salaries as Mid. Europe

Part 3 – Segment reporting (Topic 8.8)

70

SOLUTION - In €s Total S. Eur. Mid.Eur. N.Eur.Sales 100 100 100 100Less variable expenses:

Cost of goods sold 36 31 30 45Shipping expense 5 5 4 6

Total variable expenses 41 36 34 51Contribution margin 59 64 66 49Less traceable fixed exp.

Salaries 12 18 7 16Insurance 2 3 2 2Advertising 33 35 30 35Depreciation 5 7 4 4

Total traceable fixed exp. 52 63 43 57Territorial seg. margin 7 1 23 (8)Less common fixed exp.

Advertising (gen.) 5General admin. 3

Total common fixed exp. 8Net operating loss (1)

N. Europe’scontribution

margin is lowerproblem 12-16

Part 3 – Segment reporting (Topic 8.8)

71

SOLUTION - In €s Total S. Eur. Mid.Eur.

N.Eur.Sales 100 100 100 100Less variable expenses:

Cost of goods sold 36 31 30 45Shipping expense 5 5 4 6

Total variable expenses 41 36 34 51Contribution margin 59 64 66 49Less traceable fixed exp.

Salaries 12 18 7 16Insurance 2 3 2 2Advertising 33 35 30 35Depreciation 5 7 4 4

Total traceable fixed exp. 52 63 43 57Territorial seg. margin 7 1 23 (8)Less common fixed exp.

Advertising (gen.) 5General admin. 3

Total common fixed exp. 8Net operating loss (1)

N. Europe is notcovering its

traceable costs

problem 12-16

72

Part 4

Revenue variance andmarket expense

analysis

Topic 8.9

MA1 – MODULE 8

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

Analyze variances from revenue targets. (Level 1)

73

Static-budgetvariances

Flexible-budgetvariance

Sales-volumevariance

Pricevariance

Efficiency variance

MixVariance

YieldVariance

Stop the audio, and turnto handout 1, pages 6-9

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

Analyze variances from revenue targets. (Level 1)

74

Sales MixVariance

Sales QuantityVariance

Market sharevariance

Market sizevariance

Static-budgetvariances

Flexible-budgetvariance

Sales-volumevariance

Pricevariance

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

75

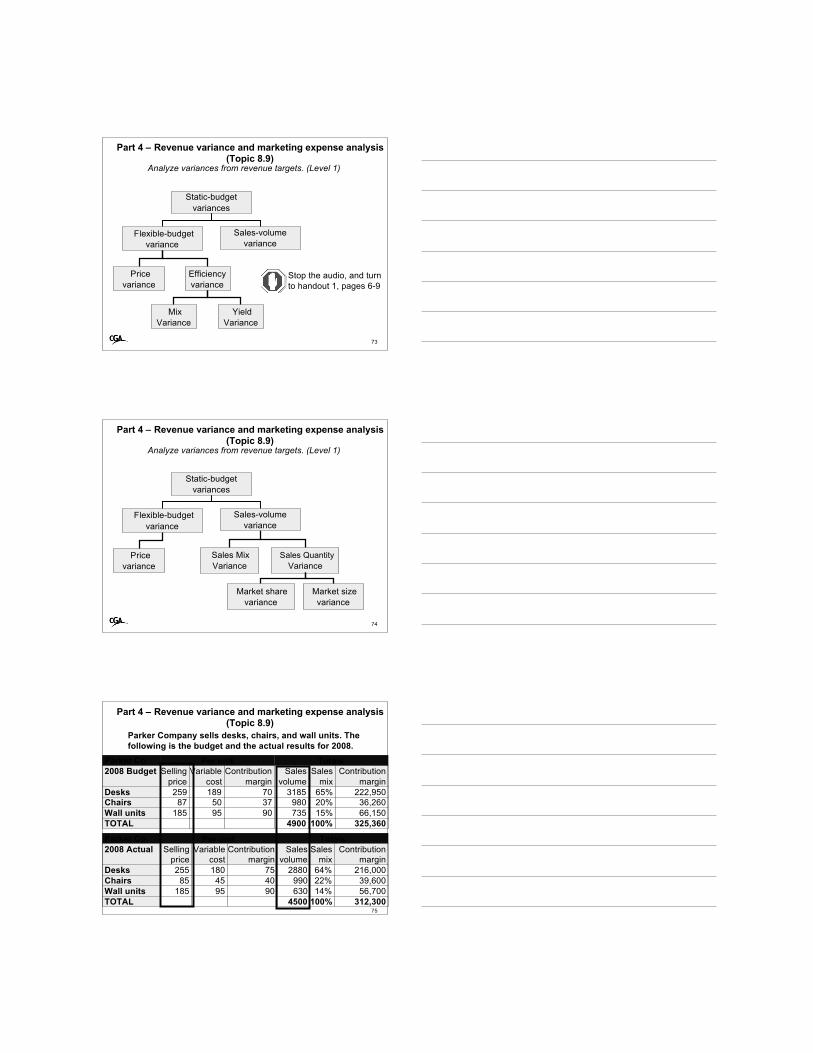

Parker Co. Per unit Totals2008 Budget Selling

priceVariable

costContribution

marginSales

volumeSales

mixContribution

marginDesks 259 189 70 3185 65% 222,950Chairs 87 50 37 980 20% 36,260Wall units 185 95 90 735 15% 66,150TOTAL 4900 100% 325,360

Parker Co. Per unit Totals2008 Actual Selling

priceVariable

costContribution

marginSales

volumeSales

mixContribution

marginDesks 255 180 75 2880 64% 216,000Chairs 85 45 40 990 22% 39,600Wall units 185 95 90 630 14% 56,700TOTAL 4500 100% 312,300

Parker Company sells desks, chairs, and wall units. Thefollowing is the budget and the actual results for 2008.

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

76

Sales MixVariance

Sales QuantityVariance

Market sharevariance

Market sizevariance

Static-budgetvariances

Flexible-budgetvariance

Sales-volumevariance

Pricevariance

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

77

Parker Co. - Static BudgetActual

ResultsStatic

BudgetStatic Budget

VarianceDesks 734,400 824,915 90,515 UChairs 84,150 85,260 1,110 UWall units 116,550 135,975 19,425 UTOTAL 935,100 1,046,150 111,050 U

How much of the variance is due to the factthat they sold less and how much of it is dueto the fact that the selling price has changed?

1. Prepare the static budget

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

78

2. Prepare the flexible budget

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

79

Parker Co.Flexible and Sales volume variances

ActualResults

FlexibleBudget/Price

Variance

FlexibleBudget

SalesVolume

Variance

StaticBudget

Desks 734,400 745,920 824,915Chairs 84,150 86,130 85,260Wall units 116,550 116,550 135,975TOTAL 935,100 948,600 1,046,150

Bud.sell.price Act.unitsDesks $259 x 2880 = $745,920Chairs $87 x 990 = $86,130Wall units $185 x 630 = $116,550

2. Prepare the flexible budget

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

80

Parker Co.Flexible and Sales volume variances

ActualResults

FlexibleBudget/Price

Variance

FlexibleBudget

SalesVolume

Variance

StaticBudget

Desks 734,400 11,520U 745,920 78,995U 824,915Chairs 84,150 1,980U 86,130 870 F 85,260Wall units 116,550 0 116,550 19,425 U 135,975TOTAL 935,100 13,500 U 948,600 97,550 U 1,046,150

Sales price variance

2. Prepare the flexible budget

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

81

How much of this variance is due to a change in the salesmix of the three products and how much of it is due to anoverall change in the number of units sold?This next analysis will be based on contribution margin

Parker Co.Flexible and Sales volume variances

ActualResults

FlexibleBudget/Price

Variance

FlexibleBudget

SalesVolume

Variance

StaticBudget

Desks 734,400 11,520U 745,920 78,995U 824,915Chairs 84,150 1,980U 86,130 870 F 85,260Wall units 116,550 0 116,550 19,425 U 135,975TOTAL 935,100 13,500 U 948,600 97,550 U 1,046,150

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

82

Sales MixVariance

Sales QuantityVariance

Market sharevariance

Market sizevariance

Static-budgetvariances

Flexible-budgetvariance

Sales-volumevariance

Pricevariance

3. Prepare the sales mix and sales quantity variances

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

83

Based on contribution margin:Act.sls. CM

Desks: 2880 x $70 = $201,600Chairs: 990 x $37 = $36,630Wall units: 630 x $90 = $56,700TOTAL $294,930

Parker Co.Flexible and Sales volume variances

ActualResults

FlexibleBudget/Price

Variance

FlexibleBudget

SalesVolume

Variance

StaticBudget

Desks 734,400 11,520U 745,920 78,995U 824,915Chairs 84,150 1,980U 86,130 870 F 85,260Wall units 116,550 0 116,550 19,425 U 135,975TOTAL 935,100 13,500 U 948,600 97,550 U 1,046,150

$325,360

3. Prepare the sales mix and sales quantity variances

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

84

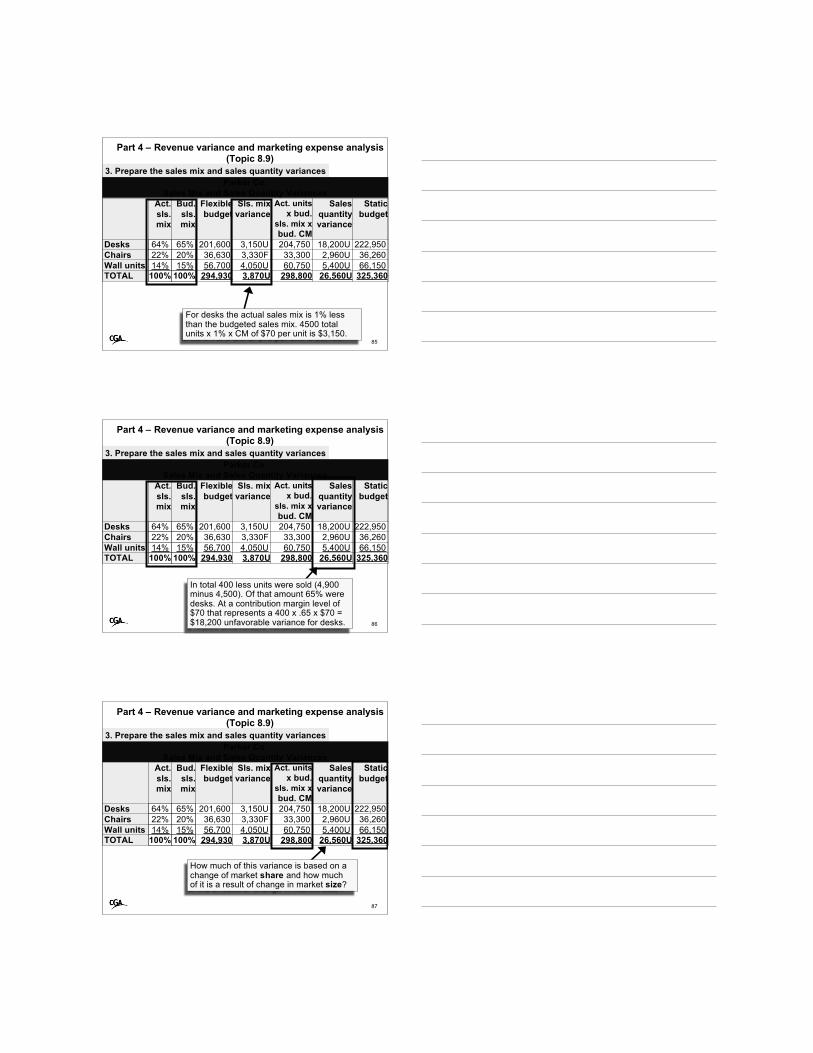

Desks: 4500 x 65% x $70= $204,750Chairs 4500 x 20% x $37 = $33,300Wall units 4500 x 15% x $90 = $60,750

Parker Co.Sales Mix and Sales Quantity Variances

Bud.sls.mix

Flexiblebudget

Sls. mixvariance

Act. unitsx bud.

sls. mix xbud. CM

Salesquantityvariance

Staticbudget

Desks 65% 201,600 204,750 222,950Chairs 20% 36,630 33,300 36,260Wall units 15% 56,700 60,750 66,150TOTAL 100% 294,930 298,800 325,360

3. Prepare the sales mix and sales quantity variances

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

85

For desks the actual sales mix is 1% lessthan the budgeted sales mix. 4500 totalunits x 1% x CM of $70 per unit is $3,150.

Parker Co.Sales Mix and Sales Quantity Variances

Act.sls.mix

Bud.sls.mix

Flexiblebudget

Sls. mixvariance

Act. unitsx bud.

sls. mix xbud. CM

Salesquantityvariance

Staticbudget

Desks 64% 65% 201,600 3,150U 204,750 18,200U 222,950Chairs 22% 20% 36,630 3,330F 33,300 2,960U 36,260Wall units 14% 15% 56,700 4,050U 60,750 5,400U 66,150TOTAL 100% 100% 294,930 3,870U 298,800 26,560U 325,360

3. Prepare the sales mix and sales quantity variances

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

86

In total 400 less units were sold (4,900minus 4,500). Of that amount 65% weredesks. At a contribution margin level of$70 that represents a 400 x .65 x $70 =$18,200 unfavorable variance for desks.

Parker Co.Sales Mix and Sales Quantity Variances

Act.sls.mix

Bud.sls.mix

Flexiblebudget

Sls. mixvariance

Act. unitsx bud.

sls. mix xbud. CM

Salesquantityvariance

Staticbudget

Desks 64% 65% 201,600 3,150U 204,750 18,200U 222,950Chairs 22% 20% 36,630 3,330F 33,300 2,960U 36,260Wall units 14% 15% 56,700 4,050U 60,750 5,400U 66,150TOTAL 100% 100% 294,930 3,870U 298,800 26,560U 325,360

3. Prepare the sales mix and sales quantity variances

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

87

How much of this variance is based on achange of market share and how muchof it is a result of change in market size?

Parker Co.Sales Mix and Sales Quantity Variances

Act.sls.mix

Bud.sls.mix

Flexiblebudget

Sls. mixvariance

Act. unitsx bud.

sls. mix xbud. CM

Salesquantityvariance

Staticbudget

Desks 64% 65% 201,600 3,150U 204,750 18,200U 222,950Chairs 22% 20% 36,630 3,330F 33,300 2,960U 36,260Wall units 14% 15% 56,700 4,050U 60,750 5,400U 66,150TOTAL 100% 100% 294,930 3,870U 298,800 26,560U 325,360

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

88

Sales MixVariance

Sales QuantityVariance

Market sharevariance

Market sizevariance

Static-budgetvariances

Flexible-budgetvariance

Sales-volumevariance

Pricevariance

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

89

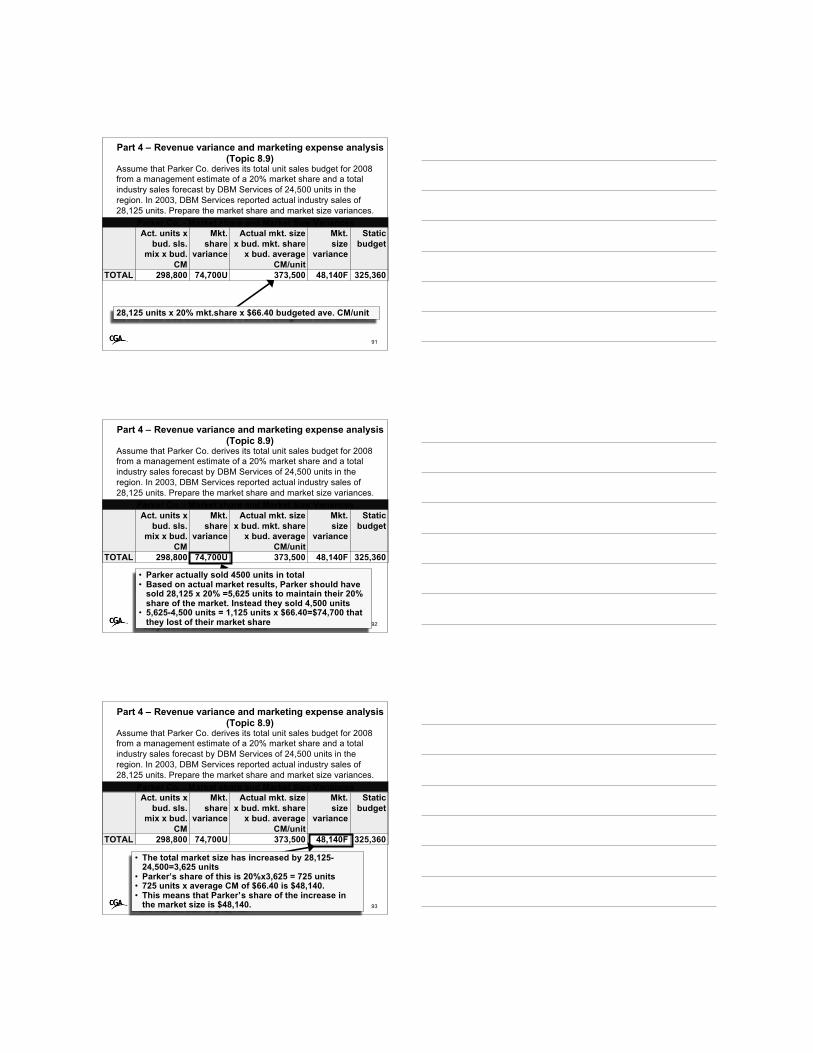

Assume that Parker Co. derives its total unit sales budget for 2008from a management estimate of a 20% market share and a totalindustry sales forecast by DBM Services of 24,500 units in theregion. In 2003, DBM Services reported actual industry sales of28,125 units. Prepare the market share and market size variances.

Parker Co. - Market share and Market Size VariancesAct. units x

bud. sls.mix x bud.

CM

Mkt.share

variance

Actual mkt. sizex bud. mkt. share

x bud. averageCM/unit

Mkt.size

variance

Staticbudget

TOTAL 298,800 325,360

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

90

Budgeted average CM:Desks: $70x3185units=$222,950Chairs: $37x980 units=$ 36,260Wall units: $90x735 units=$ 66,150 TOTAL $325,360/4900 units=$66.40

Assume that Parker Co. derives its total unit sales budget for 2008from a management estimate of a 20% market share and a totalindustry sales forecast by DBM Services of 24,500 units in theregion. In 2003, DBM Services reported actual industry sales of28,125 units. Prepare the market share and market size variances.

Parker Co. - Market share and Market Size VariancesAct. units x

bud. sls.mix x bud.

CM

Mkt.share

variance

Actual mkt. sizex bud. mkt. share

x bud. averageCM/unit

Mkt.size

variance

Staticbudget

TOTAL 298,800 74,700U 373,500 48,140F 325,360

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

91

28,125 units x 20% mkt.share x $66.40 budgeted ave. CM/unit

Assume that Parker Co. derives its total unit sales budget for 2008from a management estimate of a 20% market share and a totalindustry sales forecast by DBM Services of 24,500 units in theregion. In 2003, DBM Services reported actual industry sales of28,125 units. Prepare the market share and market size variances.

Parker Co. - Market share and Market Size VariancesAct. units x

bud. sls.mix x bud.

CM

Mkt.share

variance

Actual mkt. sizex bud. mkt. share

x bud. averageCM/unit

Mkt.size

variance

Staticbudget

TOTAL 298,800 74,700U 373,500 48,140F 325,360

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

92

Assume that Parker Co. derives its total unit sales budget for 2008from a management estimate of a 20% market share and a totalindustry sales forecast by DBM Services of 24,500 units in theregion. In 2003, DBM Services reported actual industry sales of28,125 units. Prepare the market share and market size variances.

Parker Co. - Market share and Market Size VariancesAct. units x

bud. sls.mix x bud.

CM

Mkt.share

variance

Actual mkt. sizex bud. mkt. share

x bud. averageCM/unit

Mkt.size

variance

Staticbudget

TOTAL 298,800 74,700U 373,500 48,140F 325,360

• Parker actually sold 4500 units in total• Based on actual market results, Parker should have

sold 28,125 x 20% =5,625 units to maintain their 20%share of the market. Instead they sold 4,500 units

• 5,625-4,500 units = 1,125 units x $66.40=$74,700 thatthey lost of their market share

Part 4 – Revenue variance and marketing expense analysis(Topic 8.9)

93

Assume that Parker Co. derives its total unit sales budget for 2008from a management estimate of a 20% market share and a totalindustry sales forecast by DBM Services of 24,500 units in theregion. In 2003, DBM Services reported actual industry sales of28,125 units. Prepare the market share and market size variances.

Parker Co. - Market share and Market Size VariancesAct. units x

bud. sls.mix x bud.

CM

Mkt.share

variance

Actual mkt. sizex bud. mkt. share

x bud. averageCM/unit

Mkt.size

variance

Staticbudget

TOTAL 298,800 74,700U 373,500 48,140F 325,360

• The total market size has increased by 28,125-24,500=3,625 units

• Parker’s share of this is 20%x3,625 = 725 units• 725 units x average CM of $66.40 is $48,140.• This means that Parker’s share of the increase in

the market size is $48,140.

94

Part 5

Rate of return andresidual income

Topic 8.10

MA1 – MODULE 8

Part 5 – Rate of return and residual income (Topic 8.10)Compute and interpret the return on investment and residualincome and list the strengths and weaknesses of each method.(Level 1)

95

Return oninvestment

(ROI)

Measuring performance ofinvestment centres

Net operating income Sales Sales Average operating

assets

x

MarginManagement’s abilityto control expenses inrelation to sales

TurnoverAmount of salesgenerated by theinvestment in assets

Part 5 – Rate of return and residual income (Topic 8.10)Compute and interpret the return on investment and residualincome and list the strengths and weaknesses of each method.(Level 1)

96

Return oninvestment

(ROI)

Measuring performance ofinvestment centres

• Percentages are easy to understand andcompare with other divisions/companies

• Forces control of investments in assets and costs• Includes major ingredients of profitability

Advantages

Disadvantages• May encourage short run increases in ROI or

changes that are inconsistent with strategies• A manager may not be able to control

committed costs• Ignores product quality• May reject profitable investment opportunities to

maximize ROI

Part 5 – Rate of return and residual income (Topic 8.10)Compute and interpret the return on investment and residualincome and list the strengths and weaknesses of each method.(Level 1)

97

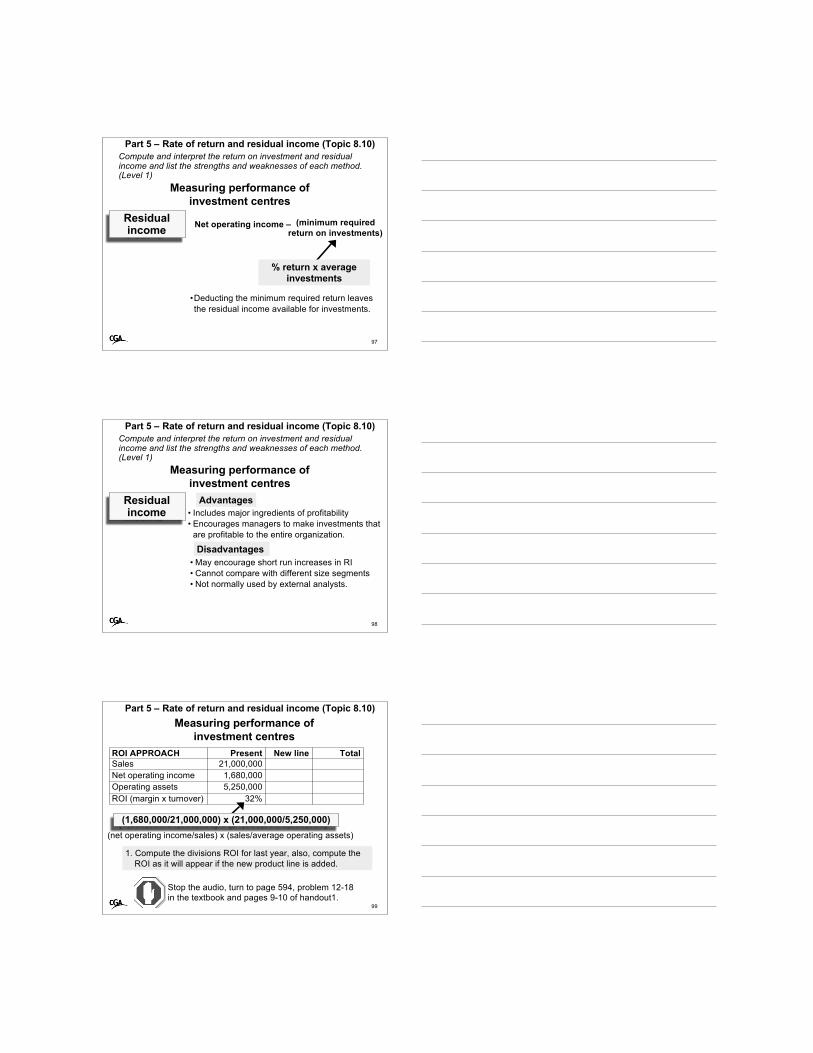

Residualincome

Measuring performance ofinvestment centres

Net operating income – (minimum requiredreturn on investments)

% return x averageinvestments

•Deducting the minimum required return leavesthe residual income available for investments.

Part 5 – Rate of return and residual income (Topic 8.10)Compute and interpret the return on investment and residualincome and list the strengths and weaknesses of each method.(Level 1)

98

Measuring performance ofinvestment centres

• Includes major ingredients of profitability• Encourages managers to make investments that

are profitable to the entire organization.

Advantages

Disadvantages• May encourage short run increases in RI• Cannot compare with different size segments• Not normally used by external analysts.

Residualincome

ROI APPROACH Present New line TotalSales 21,000,000Net operating income 1,680,000Operating assets 5,250,000ROI (margin x turnover) 32%

Part 5 – Rate of return and residual income (Topic 8.10)

99

Measuring performance ofinvestment centres

Stop the audio, turn to page 594, problem 12-18in the textbook and pages 9-10 of handout1.

(1,680,000/21,000,000) x (21,000,000/5,250,000)(net operating income/sales) x (sales/average operating assets)

1. Compute the divisions ROI for last year, also, compute theROI as it will appear if the new product line is added.

ROI APPROACH Present New line TotalSales 21,000,000 9,000,000Net operating income 1,680,000 630,000*Operating assets 5,250,000 3,000,000ROI (margin x turnover) 32% 21%

Part 5 – Rate of return and residual income (Topic 8.10)

100

Measuring performance ofinvestment centres

(630,000/9,000,000) x (9,000,000/3,000,000)

*(9,000,000-(65% of 9,000,000)-2,520,000)

Problem 12-18, page 594

1. Compute the divisions ROI for last year, also, compute theROI as it will appear if the new product line is added.

(net operating income/sales) x (sales/average operating assets)

ROI APPROACH Present New line TotalSales 21,000,000 9,000,000 30,000,000Net operating income 1,680,000 630,000 2,310,000Operating assets 5,250,000 3,000,000 8,250,000ROI (margin x turnover) 32% 21% 28%

Part 5 – Rate of return and residual income (Topic 8.10)

101

Measuring performance ofinvestment centres

(2,310,000/30,000,000) x (30,000,000/8,250,000)

Problem 12-18, page 594

(net operating income/sales) x (sales/average operating assets)

1. Compute the divisions ROI for last year, also, compute theROI as it will appear if the new product line is added.

Part 5 – Rate of return and residual income (Topic 8.10)

102

Measuring performance ofinvestment centres

2. Fred has no incentive to accept theinvestment if it will reduce his ROI from32% to 28%.

3. Yet it will increase the company’s overallROI of 18%

ROI APPROACH Present New line TotalSales 21,000,000 9,000,000 30,000,000Net operating income 1,680,000 630,000 2,310,000Operating assets 5,250,000 3,000,000 8,250,000ROI (margin x turnover) 32% 21% 28%

Problem 12-18, page 594

Part 5 – Rate of return and residual income (Topic 8.10)

103

Measuring performance ofinvestment centres

RESIDUAL INCOME APPROACH Present New line TotalNet operating income $1,680,000Minimum net operating income 787,500Residual income $ 892,500

Problem 12-18, page 594

Operating assets x minimum rate of return(5,250,000 x 15%)

4. a. Compute the East Division’s residual income for lastyear, also compute the residual income as it will appear ifthe new product line is added

Part 5 – Rate of return and residual income (Topic 8.10)

104

Measuring performance ofinvestment centres

RESIDUAL INCOME APPROACH Present New line TotalNet operating income $1,680,000 $ 630,000Minimum net operating income 787,500 450,000Residual income $ 892,500 $ 180,000

Problem 12-18, page 594

Operating assets x minimum rate of return(3,000,000 x 15%)

4. a. Compute the East Division’s residual income for lastyear, also compute the residual income as it will appear ifthe new product line is added

Part 5 – Rate of return and residual income (Topic 8.10)

105

Measuring performance ofinvestment centres

RESIDUAL INCOME APPROACH Present New line TotalNet operating income $1,680,000 $ 630,000 $2,310,000Minimum net operating income 787,500 450,000 1,237,500Residual income $ 892,500 $ 180,000 $1,072,500

Problem 12-18, page 594

Operating assets x minimum rate of return(8,250,000 x 15%)

4. a. Compute the East Division’s residual income for lastyear, also compute the residual income as it will appear ifthe new product line is added

Part 5 – Rate of return and residual income (Topic 8.10)

106

Measuring performance ofinvestment centres

RESIDUAL INCOME APPROACH Present New line TotalNet operating income $1,680,000 $ 630,000 $2,310,000Minimum net operating income 787,500 450,000 1,237,500Residual income $ 892,500 $ 180,000 $1,072,500

Problem 12-18, page 594

4.b. Using this approach, Fred is inclined to acceptthe project because it will increase the EastDivision’s residual income.

107

Part 6

Review question:Variance analysis – workingbackward from variance data

(download the additional questions handout: ma1_mod8_handout1.pdf)

MA1 – MODULE 8

108

Case 11-27 pages 538-539Handout page 11

1. How many units were produced last period?2. How many metres of direct materials were

purchased and used?3. What was the actual cost per metre of material?4. How many actual direct labour hours were worked?

Part 6 – Review question: Variance analysis – workingbackward from variance data

Stop the audio, read and attempt thequestion in the textbook then come back tolisten to the solution.

109

Case 11-27 pages 538-539Handout page 11

5. What was the actual rate per direct labour hour?6. How much actual variable manufacturing overhead

cost was incurred?7. What is the total fixed manufacturing overhead

cost in the flexible budget?8. What were the denominator hours for last period?

Part 6 – Review question: Variance analysis – workingbackward from variance data

110

Part 7

Review question:Segmented statements;

Product-line analysis

(download the additional questions handout: ma1_mod8_handout1.pdf)

MA1 – MODULE 8

111

Case 12-31 pages 604-605Handout pages 12 and 13

1. Prepare a new income statement segmented byproduct lines

2. Do you agree with Aiken’s decision to cut backproduction of line A?

3. What points would you make for or againstelimination of line C?

Part 7 – Review question: Segmented statements

Stop the audio, read and attempt thequestion in the textbook then come back tolisten to the solution.

112

Case 12-31 pages 604-605Handout pages 12 and 13

4. a. Prepare a segmented income statement showingline C segmented by markets

b. What points revealed by this statement wouldyou want to bring to the attention of management?

Part 7 – Review question: Segmented statements

113

Part 8

Review question:Segmented statement analysis:

ROI and residual income

(download the additional questions handout: ma1_mod8_handout1.pdf)

MA1 – MODULE 8

114

Question 1 March, 1992 examHandout pages 14 thru 15

Q1 By employing as many different measures as youcan, demonstrate which of Divisions A, B, or C hasperformed the best in 1991

Interpret the results

Part 8 – Review question: Segmented statement analysis:ROI and residual income

Stop the audio, read and attempt thequestion in the handout then come back tolisten to the solution.

115

Question 1 March, 1992 examHandout pages 14 thru 15

Q1 By employing as many different measures as youcan, demonstrate which of Divisions A, B, or C hasperformed the best in 1991

Interpret the results

Part 8 – Review question: Segmented statement analysis:ROI and residual income

116

Question 1 March, 1992 examHandout pages 14 thru 15

Q1 By employing as many different measures as youcan, demonstrate which of Divisions A, B, or C hasperformed the best in 1991

Interpret the results

Part 8 – Review question: Segmented statement analysis:ROI and residual income

117

Part 9

Review questions:Multiple Choice Questions

(download the additional questions handout: ma1_mod8_handout1.pdf)

MA1 – MODULE 8

118

Multiple choice questionsHandout pages 16 thru 19Now working on page 16

Q1 Which variances does DEF Manufacturing have?

Q2 What does this mean for the standard direct labourhours allowed for April’s output?

Q3 What was the amount of overhead cost applied towork in process for May?

Part 9 – Review questions: Multiple choice

Stop the audio, read and attempt thequestion in the handout then come back tolisten to the solution.

119

Multiple choice questionsHandout pages 16 thru 19Now working on page 17

Q4 a. What was the variable overhead efficiencyvariance?b. What was the fixed overhead production volumevariance?

Q5 What would be the total flexible budget if total linesprinted increased to 2,600,000?

Part 9 – Review questions: Multiple choice

120

Multiple choice questionsHandout pages 16 thru 19Now working on page 18

Q6 What is the flexible budget for 40,000 and 20,000units, respectively?

Q7 How does the application of JIT principles improvereturn on investment?

Q8 What is the amount of invested capital?Q9 What was Rai’s invested capital in 2002?

Part 9 – Review questions: Multiple choice

121

Multiple choice questionsHandout pages 16 thru 19Now working on page 19

Q10a. Which single note to the financial results would bemost appropriate in a report to management?

b. Which of the following would be the mostappropriate conclusion in the report to management?

Part 9 – Review questions: Multiple choice