man made fibers review - canaintex

TRANSCRIPT

Man Made Fibers Review

CANAINTEX Sept 2016

Alasdair Carmichael

Trusted commercial intelligencewww.woodmac.com

Trusted commercial intelligencewww.woodmac.com

2

Agenda

1. Introduction

2. The Fibers Big Picture

3. Polyester Continued Growth

4. Nylon, Spandex & Rayon Markets

5. Current China Developments

6. NAFTA Markets

7. Drivers of Price

Trusted commercial intelligencewww.woodmac.com

3

Product Coverage

Oil Refinery / Gas Field Petrochemical Complex Downstream Products

Fertilisers

Explosives

Resins

Plastics and Films

EOD’s/Detergents

Antifreeze

Polyester Fibers

Plastics

Acrylic Fibers

Plastic Coatings

Synth Rubbers

Tyres

Plastics & Foams

Nylons

Nylons, PC Resins

Plasticizers/Resins

Polyester Fibers &

Resins

Urethane Foams

Petroleum

Refining

Crude Oil

Reformate

Naptha

Gas Oil

Natural Gas

Processing

Natural Gas

Ethane

LPG

Methane

FeedstocksEnd Products

Intermediate

Petrochemicals

Basic

Petrochemicals

Gasoline

Kerosene Fuel OilDiesel

Jet

FuelLube

Oils

Asphalt

Reforming

Olefins

Plant

Aromatics

Separation

p-Xylene

Toluene

o-Xylene

Benzene

Crude C4s

Syngas

Ethylene

Propylene

g

Olefa

nt

Ar

Oma

tics

Processing Methanol

Ammonia

Urea

Polyethylenes

EDC/VCM/PVC

Ethylene

Oxide

Ethylene Glycol

Polypropylene

Acrylonitrile

Oxo-alcohols

Butadiene

Styrene

Cyclohexane

Cumene/Phenol/

Acetone

Phthalic Anhydride

DMT/PTA

TDI

Benzene / MDI

PCI Research Wood Mackenzie Future Research

3

Trusted commercial intelligencewww.woodmac.com

4

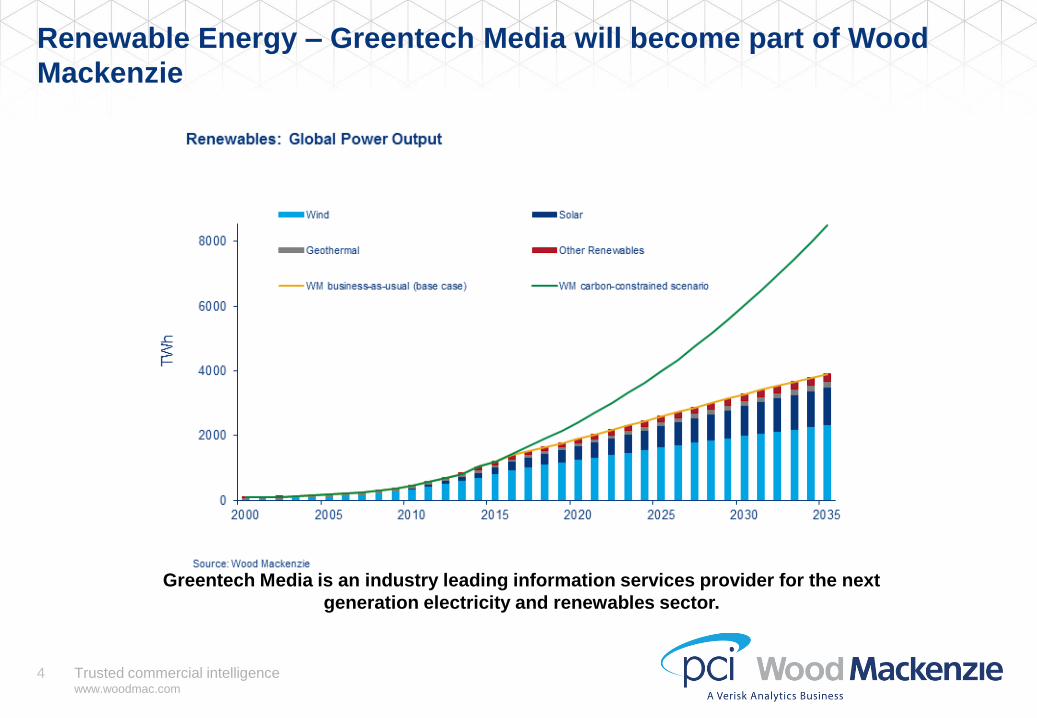

Renewable Energy – Greentech Media will become part of Wood

Mackenzie

Greentech Media is an industry leading information services provider for the next

generation electricity and renewables sector.

Trusted commercial intelligencewww.woodmac.com

5

Textile Mill Consumption (million tonnes)

0

20

40

60

80

100

120

19

91

19

94

19

97

20

00

20

03

20

06

20

09

20

12

20

15

20

18

20

21

20

24

20

27

20

30

Polypropylene

Cellulosics

Polyester

Nylon

Acrylic

Cotton

Wool

Trusted commercial intelligencewww.woodmac.com

6

Fibres in context 2015 (ktes)

1,705

3,532

4,098

5,325

24,055

48,030

Polyester

Cellulosics

Acrylic

Cotton

PP

Nylon

An Astronomers View

Trusted commercial intelligencewww.woodmac.com

7

Global Mill Consumption - 1980

Wool

Cotton 47%

Acrylic

Nylon

Polyester 17%

Cellulosics

Polypropylene

1980 = 30.3 million tons

Trusted commercial intelligencewww.woodmac.com

8

Global Mill Consumption - 2000

Wool

Cotton 38%

Acrylic

Nylon

Polyester 37%

Cellulosics

Polypropylene

2000 = 52.5 million tons

Trusted commercial intelligencewww.woodmac.com

9

Global Mill Consumption - 2015

Wool

Cotton 27%

Acrylic

Nylon

Polyester 55%

Cellulosics

Polypropylene

2015 = 87.8 million tons

Trusted commercial intelligencewww.woodmac.com

10

Global Mill Consumption - 2030

Wool

Cotton 24%

Acrylic

Nylon

Polyester 59%

Cellulosics

Polypropylene

2030 = 114.2 million tons

Trusted commercial intelligencewww.woodmac.com

11

All Fibers excluding Polyester grow 47% from 1991 – 2025 (million

tons)

0

20

40

60

80

100

120

Wool Cotton Acrylic Nylon Cellulosics Polyprop

Trusted commercial intelligencewww.woodmac.com

12

All Fibers including Polyester grow 173% from 1991 – 2025 (million

tons)

0

20

40

60

80

100

120

Wool Cotton Acrylic Nylon Cellulosics Polyprop Polyester

Trusted commercial intelligencewww.woodmac.com

13

China’s Dominance of Polyester Production (million tons)

-

10

20

30

40

50

60

70J,K,T

China

India

S.Asia

Turk/Afr/ME

Europe

Americas

China share of production: 1990 = 13%; 2000 = 26%; 2010 = 65%; 2015 = 69%

WTO

membership

Trusted commercial intelligencewww.woodmac.com

14

China’s Dominance of Polyester Production (million tons)

-

5

10

15

20

25

30

35

1990 1995 2000 2005 2010 2015

Rest China

Trusted commercial intelligencewww.woodmac.com

15

China Competitiveness (1)

• China starts with no basic advantage in oil prices, so why is polyester

(and other fibers) cheaper than in the West?

• Scale: Of the 12 largest polyester producers in the world 9 of them are

Chinese

0

500

1000

1500

2000

2500

3000

• Of the 3 non Chinese companies, 2 have operations in China

Polyester Plant

Capacities (000 tons)

Trusted commercial intelligencewww.woodmac.com

16

China Competitiveness (2)

• Polyester plants are highly integrated to raw materials.

• Plants financial structures are generally based on one profit center, not

multi centers.

• Plants have received significant state government benefits to provide

jobs. Land, loans, repayment terms, export subsidies.

• But can this last?

• 5 Year plan starting 2016 made it clear that Central government is

turning away from the policy of overbuild in established industries. It

takes time to work its way to the regional levels.

• Employment is not the driver that it was – demographics.

• Anti dumping and Countervailing duties are a greater factor in trade

Trusted commercial intelligencewww.woodmac.com

17

China Competitiveness (3)

• Banking Issues:

• Report from Bank for International Settlements (BIS) – Bankers Bank

• China facing full blown banking crisis, one of the measures BIS uses is

“credit to GDP gap” – a score of 10 signals a crisis “occurs in any of the

three years ahead”. In the Quarterly report BIS measures China current

score at 30.1

• Outstanding loans in China have reached $28 trillion – more than the

commercial banking systems of US & Japan combined. Corporate debt is

171% of GDP

• Peoples Daily states a very authoritative person warned that debt has

been “growing like a tree in the air” and called for an assault on “zombie

companies” saying that China cannot “continue to “force economic

growth by levering up” and the country must take its punishment.

Trusted commercial intelligencewww.woodmac.com

18

Polyester is Constantly Looking for Opportunities to Gain Share

All Fibers have to be aware of Polyester as it aims to take market

share – and it has been very successful at doing it!

Nylon developed in the late 1930s by DuPont. First commercial

Synthetic fiber – WW2, parachutes, ropes etc

Nylon applications in hosiery & intimate apparel: 1940s

Nylon into textured yarn – swimwear, and into Tirecord: 1950s

Nylon into carpets – 1960s

Nylon into Engineered Plastics 1970s

Nylon into Films 1980

Since then no new “segment” growth – applications like airbags, and

demographics etc have increased volume, but polyester has

effectively slowed growth by taking share of hosiery, intimate apparel,

tires, carpets, performance apparel, sports uniforms etc. from nylon.

Trusted commercial intelligencewww.woodmac.com

19

Demand for PA6+PA66 by Application

0

1000

2000

3000

4000

5000

6000

7000

8000

3819(84%)

1990 1995 20152005 20102000

4181(57%)

ktes/yr

+1.9%

3117(43%)

702(16%)

Non-Fibre Fibre

Trusted commercial intelligencewww.woodmac.com

20

Nylon Fiber Production 1990 – 2030 (000 tons)

-

500

1000

1500

2000

2500

3000

3500

4000

4500

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

Tex Fil Ind Fil Carpet Fil Staple

-

500

1000

1500

2000

2500

3000

3500

4000

4500

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

Tex Fil Ind Fil Carpet Fil Staple

Nylon 6

Fiber increases +71%

Nylon 66

Fiber decreases -8.5%

Trusted commercial intelligencewww.woodmac.com

21

Regional Spandex Capacities (000 tons)

0 100 200 300 400 500 600

NAM

SAM

EU + Turk

China

Korea

Taiwan

Japan

Rest Asia2015

2010

2000

0 20 40 60 80

NAM

SAM

EU + Turk

Korea

Taiwan

Japan

Rest Asia2015

2010

2000

Trusted commercial intelligencewww.woodmac.com

22

Global Spandex Consumption by End Use

Circular Knit28%

Warp Knit20%Hosiery

13%Woven

9%

Narrow8%

Seamless4%

Others18%

2015: 652,000 tons

Trusted commercial intelligencewww.woodmac.com

23

Rayon Staple Production (000 tonnes)

0

1000

2000

3000

4000

5000

6000

7000

JKT

China

India

South Asia

Turk/Afr/ME

Europe

Americas

Trusted commercial intelligencewww.woodmac.com

24

Viscose rayon staple output has grown rapidly

Even though viscose staple remains a small volume fibre.

Demand has grown strongly between 2000 and 2015:

» Rising incomes

» Demand for comfortable clothing

» Demand for nonwovens, including wipes

Fiber CAGR 2000-2015

Cotton 1.2%

Cellulosic Staple 7.0%

Cellulosic Filament -1.7%

Wool -1.8%

Acrylic Staple -2.9%

Nylon Staple -8.2%

Polyester Staple 4.4%

Polypropylene/other Staple -0.4%

Nylon Filament 0.8%

Polyester Filament 7.5%

Polypropylene/other Filament 1.9%

Total Fiber 3.6%

Trusted commercial intelligencewww.woodmac.com

25

Global Production of Viscose Staple Fiber (million tons)

0

1

2

3

4

5

N America S America W Europe E Europe Turkey

China India Asean Taiwan Japan

Trusted commercial intelligencewww.woodmac.com

26

Major Capacities of Viscose Staple Fiber (Rayon) 2016 (000 tons)

Lenzing & Birla account for 34% of global VSF capacity

The next 6 producers (all Chinese) share of global capacity is 41%

Global Capacity is 5.7 million tons and these 8 companies have 75% share

0

200

400

600

800

1,000

1,200

Trusted commercial intelligencewww.woodmac.com

27

Major Announced Expansions of VSF (Rayon) (000 tons)

0

200

400

600

800

1,000

1,200

1,400

1,600

Birla Lenzing Sateri Fulida

Planned NewCapacity

Lyocell Capacity

VSF Capacity

Trusted commercial intelligencewww.woodmac.com

28

China Market Developments

Hangzhou September 4 -5th 2016

Why is this relevant to a Synthetic Fibers paper?

Hangzhou is in Zhejiang province and is the center of a major industrial zone, with

Jiangsu Province and Shanghai as neighbors. It is the greatest concentration of the

polyester industry in the world. Also many of the downstream fiber and fabric producers

are in the area.

In order to make the G20 guests as welcome as possible the government “asked” most

industry to close for a period of at least 2 weeks to reduce pollution while the guests are

in town!

For 2 weeks container trucks and cargo delivery trucks in Hangzhou will be stopped

with a penalty od $14,000 and 15 days detention! – Serious stuff.

Trusted commercial intelligencewww.woodmac.com

29

China Market Developments

Hangzhou September 4 -5th 2016

We estimate the following Impact on Synthetic Fibers

PTA is the primary raw material for Polyester: 16 million tons closed

Polyester plants (fiber and plastics): 36 million tons closed

Many yarn spinners and fabric producers closed

All the textile printing, dyeing and finishing plants on the region will be closed

Plants expected to start to get back to production mid September, but probably end

Sept/early October before full production. Down time could be 1 month – or 3 million

tons of polyester – almost 4% of annual world production.

Trusted commercial intelligencewww.woodmac.com

30

NAFTA – Major Synthetic Fiber Capacities (000 tons)

0

200

400

600

800

1000

PTF PIF PCF P St NTF NIF NCF N St Acr

Mexico

USA

Canada

Trusted commercial intelligencewww.woodmac.com

31

NAFTA – Automotive Market, Light Vehicle Build (millions)

0

2

4

6

8

10

12

14

16

18

20

198

0

198

2

198

4

198

6

198

8

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

201

4

Trucks

Cars

Trusted commercial intelligencewww.woodmac.com

32

NAFTA – Automotive Market – Mexico Investments

New Automotive Plants in Mexico

Company Investment Date Announced Start Up # of Vehicles Location

Mazda $500m Jun-11 2014 140,000 Guanajuato

Honda $800m Aug-11 2014 200,000 Guanajuato

Nissan $2,000m Feb-12 2014 175,000 Aguascalientes

Nissan - Daimler $1,400m Jun-14 2017 300,000 Aguascalientes

Audi $1,300m May-13 2016 San Jose Chiapa

BMW $1,000m Jul-14 2019 150,000 San Luis Potosi

Kia $1,000m Aug-14 May-16 300,000 Monterrey

Toyota $1,000m May-15 2019 200,000 Guanajuato

Ford* $1,000m Jan-16 350,000 San Luis Potosi

Fiat Chrysler** Sep-16 Toluca

Major Expansions to Existing Automotive Plants in Mexico

GM (expansion) $3,600m Dec-14 2018 Various

VW $1,000m Mar-15 2017 125,000 Puebla

Ford* Feb-16 150,000 Cuautitlan

Trusted commercial intelligencewww.woodmac.com

33

NAFTA – Automotive Market – Synthetic Fibers Impact

Source: LMC Automotive

Recent Supply Chain Investments

• Goodyear investing $500m - Tires

• Michelin investing $500m - Tires

• Pirelli investing $200m – Tires

• Boxmark $100m – Seating

• Toray $100m – Airbags (10k tons of

N66)

Impact on Synthetic Fibers

• Estimated that an average new

vehicle uses:

• 15.4kgs of Polyester fiber

• 4.2kgs of Nylon

19 million vehicle build

• Polyester = 292,000 tons

• Nylon = 79,000 tons

Trusted commercial intelligencewww.woodmac.com

34

Oil Prices Monthly 1990 – Aug 2016, WTI $/barrel

0

20

40

60

80

100

120

140

160

1990 1995 2000 2005 2010 2015

26.66 yr

Average

$46.63

Sept 7th

Price

$46.27!

Trusted commercial intelligencewww.woodmac.com

35

Oil as a Driver of Polyester Fiber Prices, China Daily Spot Market

($/ton)

200

400

600

800

1000

1200

1400

Paraxylene

Oil

Sept 2014 Sept 2016

Trusted commercial intelligencewww.woodmac.com

36

Oil as a Driver of Polyester Fiber Prices, China Daily Spot Market –

indexed to Sept 2014

30

40

50

60

70

80

90

100

110

120

Oil

PX

PTA

MEG

Sept 2014 Sept 2016

Trusted commercial intelligencewww.woodmac.com

37

Nylon 6 & 66 cf Polyester Polymer Prices N. America ($/ton)

Nylon 6 prices fall as China builds too much fiber and raw materials capacity in 2015

-300

200

700

1200

1700

2200

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2010 2011 2012 2013 2014 2015 2016

6:66 delta(RHS) Nylon 66 Nylon 6 Polyester

Trusted commercial intelligencewww.woodmac.com

38

Cotton (Far East A index) vs Polyester Staple (Asia) c/kg

-100

0

100

200

300

400

500

198

9 Q

1

Q2

Q3

Q4

199

4 Q

1

Q2

Q3

Q4

199

9 Q

1

Q2

Q3

Q4

200

4 Q

1

Q2

Q3

Q4

200

9 Q

1

Q2

Q3

Q4

201

4 Q

1

Q2

delta Cotlook A* PES Staple Asia

Trusted commercial intelligencewww.woodmac.com

39

Cotton (A index) : Polyester Staple: Rayon (Asia) c/kg

50

70

90

110

130

150

170

190

210

230

2013 Jan 2014 Jan 2015 Jan 2016 Jan

Cotton A index PET St Asia Rayon

Trusted commercial intelligencewww.woodmac.com

40

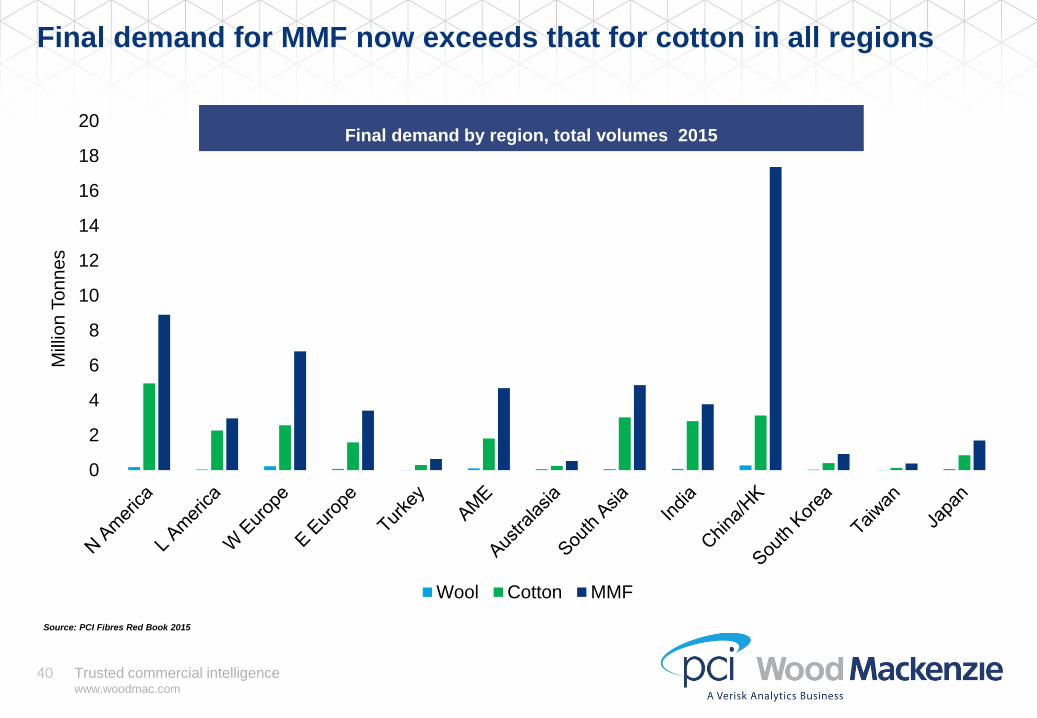

Final demand for MMF now exceeds that for cotton in all regions

Source: PCI Fibres Red Book 2015

0

2

4

6

8

10

12

14

16

18

20

Mill

ion

To

nn

es

Wool Cotton MMF

Final demand by region, total volumes 2015

Trusted commercial intelligencewww.woodmac.com

41

Thoughts

• Man Made Fiber growth continues with Polyester & Rayon leading.

• Global Business generally slow, but pricing is stable.

• Trade: Are we in a period of Free Trade or Greater Protectionism? TPP or

anti dumping??

• Will oil prices remain reasonably low? Our forecast is $XX/ barrel end of

2016.

• Overcapacity in Polyester and Nylon continues, large expansion in

Rayon.

• Do current Shipping Industry problems encourage local manufacture?

Muchas Gracias

Trusted commercial intelligencewww.woodmac.com

42

Disclaimer

This presentation has been prepared for Participants of the CANAINTEX Conference

on 23 – 24 September 2016 by Wood Mackenzie Limited. The presentation is intended

solely for the benefit of attendees and its contents and conclusions are confidential and

may not be disclosed to any other persons or companies without Wood Mackenzie’s

prior written permission.

The information upon which this presentation comes from our own experience,

knowledge and databases. The opinions expressed in this presentation are those of

Wood Mackenzie. They have been arrived at following careful consideration and

enquiry but we do not guarantee their fairness, completeness or accuracy. The

opinions, as of this date, are subject to change. We do not accept any liability for your

reliance upon them.

Strictly Private & Confidential

Europe +44 131 243 4400

Americas +1 713 470 1600

Asia Pacific +65 6518 0800

Email [email protected]

Website www.woodmac.com

Wood Mackenzie™, a Verisk Analytics business, is a trusted source of commercial intelligence for the world's

natural resources sector. We empower clients to make better strategic decisions, providing objective analysis

and advice on assets, companies and markets. For more information visit: www.woodmac.com

WOOD MACKENZIE is a trade mark of Wood Mackenzie Limited and is the subject of trade mark registrations and/or applications in

the European Community, the USA and other countries around the world.