mamba minerals (asx:mab) potential large scale hematite

TRANSCRIPT

Mamba Minerals (ASX:MAB)

Potential large scale hematite iron ore

project in Canada’s Labrador Trough

Snelgrove Lake advantages

Location One of the world’s safest most politically stable regions for mining

Investment

High level of regional investment by Asian steel mills demonstrates

market interest

Infrastructure

Access to common user rail and port with available capacity reduces

capex

Power Low cost hydro electricity reduces opex

Resource

33km strike of Sokoman Formation represents a massive iron range

for a potentially large resource with 5-8km of hematite

Results Drilling results confirm significant width and depth of ore body

Product Low impurity product (Phosphorus, Aluminium) increases sales price

Potential Results to date suggest potential for a substantial hematite resource

and a large magnetite resource providing exploration upside

Progress

Airborne surveys, detailed ground gravity surveys and a targeted 8

hole 800m drilling program are complete

Location

Labrador Trough, Canada

One of the world’s safest

most politically stable

regions for mining

Excellent global trade

relationships, no

resource nationalism,

clear and sound policy

for mining

Canada is the 5th

largest iron ore exporter

in the world

Schefferville

Labrador City

Snelgrove

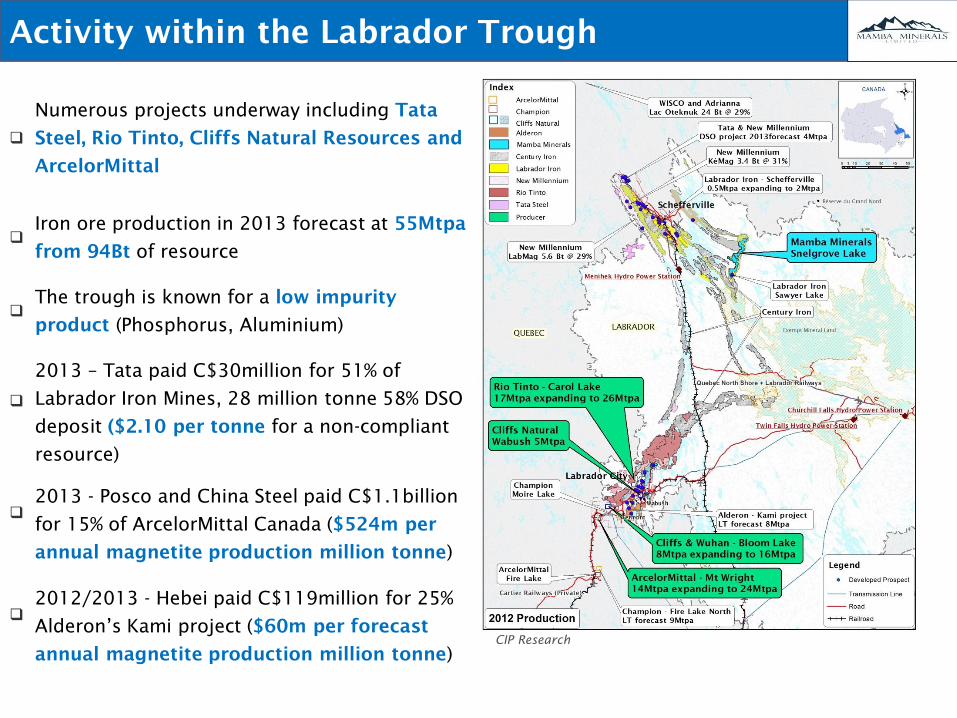

Activity within the Labrador Trough

Numerous projects underway including Tata

Steel, Rio Tinto, Cliffs Natural Resources and

ArcelorMittal

Iron ore production in 2013 forecast at 55Mtpa

from 94Bt of resource

The trough is known for a low impurity

product (Phosphorus, Aluminium)

2013 – Tata paid C$30million for 51% of

Labrador Iron Mines, 28 million tonne 58% DSO

deposit ($2.10 per tonne for a non-compliant

resource)

2013 - Posco and China Steel paid C$1.1billion

for 15% of ArcelorMittal Canada ($524m per

annual magnetite production million tonne)

2012/2013 - Hebei paid C$119million for 25%

Alderon’s Kami project ($60m per forecast

annual magnetite production million tonne)

CIP Research

Labrador Trough mix of hematite and magnetite

78% of the iron ore resources in the Labrador Trough are magnetite, 20% are a blend of

magnetite and Hematite with 2% being hematite only

Production By Company 2013

ArcelorMittal

Cliffs NaturalResources

IOC

Labradore IronMines

New Millenium

Company Deposit Type Forecast Production 2013 (Mtpa) ArcelorMittal / Posco and China Steel Magnetite/Hematite 18

Cliffs Natural Resources / Wuhan Magnetite/Hematite 15

IOC (RIO) Magnetite/Hematite 18

Labrador Iron Mines Hematite 2

New Millennium / Tata Hematite 2

Total 55

Production By Product 2013

Magnetite/Hematite

Hematite

CIP Research

By Resource

Magnetite

Magnetite/Hematite

Hematite

55km southeast of Schefferville and

200km north of Labrador City, towns

with significant mining services

available

50km east of the Menihek

Hydroelectric Plant which provides

low cost electricity at C$0.05/kwh

50km east of the common carrier

railway with available capacity,

connecting to the Port of Sept-Iles

600km to the Port of Sept-Iles, where

a C$220m 50Mtpa expansion is

underway to construct a multi-user

deep-water dock with two ship

loaders and two conveyor lines.

Infrastructure access for Snelgrove

Menihek Hydro Power Station

Schefferville

Railway to the Port

50Mtpa Port expansion

New port development

New state of the art multi-user berth

to provide 50Mtpa for an estimated

$220m to be completed March 2014

Funding from Canadian Government

25%, Port of Sept-Iles 25% and mining

companies 50%

Dredging completed

Ship-Loader contract awarded

Major civil / structural contract awarded

Mobilisation for pile driving completed

Construction on time and budget

Exploration

Huge iron formation with hematite targets

33km strike of Sokoman Formation represents a

massive iron range hosting hematite and

magnetite type ore deposits

Geological mapping, aeromagnetic and gravity

surveys and preliminary metallurgical testing

are complete

Potential for hematite direct-shipping ore

deposits similar to the Sawyer Lake deposit just

500m from the Snelgrove boundary (historic non-

compliant resource of 12Mt @ 62% Fe)

Ground gravity and magnetic data has been used

to identify target areas with 5-8km of hematite

outlined

Drill hole plan with target deposit types

Phase 1 drilling program complete:

8 holes, 4 targeting hematite in the

south and 4 targeting magnetite in

the northern section of the property

Drill hole MM-13-05 was the

hematite discovery hole in the CLC

deposit.

MM-13-06 & MM-13-08 better

defined the true width of the CLC

deposit now estimated to be 170m

MM-13-07 tested the Blaire deposit

MM-13-01 to MM-13-04 tested

magnetite targets in the north

Mamba discovers massive hematite project

Discovery drill hole (MM-13-05) targeting

hematite intersected 303m of massive

hematite and remained open in mineralisation

at 235m below surface

The second hole (MM-13-06) to test this

target had the azimuth reversed perpendicular

to mineralisation dip to better test the true

width

The second hole hit hematite after only 8m of

ground cover and has returned a 92m

intersection of mineralisation

The true width of the ore body is now

estimated to be 170m

Hematite target is ~5-8km long

CLC Deposit

Vertical cross section of CLC deposit drilling

Target for Summer program

Assay results on hematite discovery hole

First assays from the discovery hole (announced

May 3rd

) returned 101m averaging 52% Fe

hematite with high grade intervals of 63% and

65%

Assays confirm the deposit contains very low

aluminium (0.50% Al2O3) and low phosphorus

(0.053% P), providing the potential to attract a

premium price with the balance, after Fe, being

mostly silica

Silica content is expected to be economically

removed using a conventional mechanical

upgrading process of crushing, screening and

de-sanding, generating a target 62% Fe saleable

iron ore fines product (high level metallurgical

test work underway)

Length Grade Vertical depth

33m 52% 59m

9m 55% 92m

9m 54% 101m

9m 50% 122m

16m 52% 160m

7m 53% 181m

18m 52% 216m

Total 101m 52%

World class partners with Labrador Trough experience

Exploration manager Project originator and exploration advisor

King & Bay has managed the exploration programs

for a number of the Labrador trough explorers and

developers

Altius is a project generator and royalty business

with a focus on Canada and a history of success

Alderon Iron Ore – Kami project Alderon Iron Ore – Kami project

Cap-Ex Iron Ore – Various projects

Century’s Iron – Astray, Grenville, Menihek and

Schefferville projects

Ridgemont Iron Ore – Lac Virot Rio Tinto – Geotite Bay

Massive specular hematite-rich sample from Snelgrove

Exploration and test work program

Detailed ground gravity survey work underway on hematite

targets

Ground gravity will use 100m spacing to provide more accurate

targets for the drilling program

Metallurgical test work program analysing grindability and silica

removal underway

A targeted 8 hole 800m drilling program focused on high grade

hematite targets is now complete

Mamba Minerals (ASX:MAB) capital structure

Item Number

Shares on Issue 70,550,086

Options to Altius

(Exercisable at A$0.25, expiring 31/8/15)

17,000,000

Options on Issue to Hilton Nathanson

(Exercisable at A$0.50, expiring 15/12/15)

500,000

Performance Shares (based equally on 100m tonnes,

200m tonnes, 600m tonnes, 1 billion tonnes &

positive feasibility study).

32,000,000

Current Market Capitalisation (at A$0.50) – non diluted A$35 million

Major Shareholders:

GAB superfund

Pershing Nominees (Blackswan Equities ) Hilton Nathanson

Michael O’Keeffe

12.71%

6.99%

6.08%

5.85%

Mamba board

Michael O’Keeffe (Non-Executive Chairman) was on the Board of Riversdale Mining at the time of

its inception in 2004 and was appointed Chief Executive and Executive Chairman in 2006. He

held these positions at the time Rio Tinto completed its acquisition of Riversdale Mining for

approximately $4 billion in 2011. Prior to his involvement with Riversdale Mining, Mr O’Keeffe

was Managing Director of Glencore Australia. He is currently Chairman of Riversdale Resources,

an emerging coal development company in North America.

Mr Richard (Dick) Wright (Non-Executive Director) has held various executive and director level

roles for both private and publicly listed companies in Australia, Europe and the United States.

This includes being Project Director of Roy Hill at Hancock Prospecting, Managing Director of

Fluor Daniel and Executive Chairman of Adrail and Paladio Ltd. Mr Wright has significant

expertise in the development of strategy, implementation and delivery of multi-billion dollar

resource projects including iron ore processing.

Niall Lenahan (Non-Executive Director) has extensive experience in the mining industry across a

number of commodities, including gold, base metals, minerals sands and coal. He has served as

a CFO and Company Secretary of Riversdale Mining Ltd from 2006 -2011, including a period as

Finance Director.

Appendix

Fines product

High grade hematite ore is referred to as direct

shipping ore (DSO) because it is mined and processed

using a relatively simple crushing, screening and

de-sanding process

Can be blended with other products to ensure the

desired concentration of contaminant materials

The Pilbara fines to lump ratio is about 70:30

Rio Tinto's Yandicoogina mine produce more than 95

per cent fines

Fortescue metals group producers only fines

Australian Production Lump vs Fines

Rio Tinto, BHPB Lumps Rio Tinto, BHPB, FMG Fines

Pellets: 8 – 20mm Lump: 6.3 – 30mm Fines: 0 – 6.3mm

Concentrate: <0.15mm

Pellet Feed: <0.05mm

Seaborne trade of Iron Ore dominated by fines

Target for Summer program

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Millio

n w

et to

nn

es

Calendar Year

Global Seaborne Trade

Pellets

Concentrates

Fines

Lumps

Pilbara Seaborne Trade

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009 2010 2011 2012

Millio

n w

et to

nn

es

Calendar Year

Rio Tinto, BHPB Pellets

Rio Tinto, BHPB, FMG Fines

Rio Tinto, BHPB Lumps

CIP Research

Fines and lump prices relatively close

Target for Summer program

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US$/t @

6

2%

Fe

Australian Reference Fines

Australian Reference Lumps

Brazil – Vale BF Pellets

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

2004 2005 2006 2007 2008 2009 2010 2011 2012

$ premium for Australian Lump

US$

/t @

6

2%

Fe

CIP Research

Iron ore market share

Target for Summer program

Rio Tinto

BHP Billiton

FMG

Other Australia

Vale

Samarco CSN MMX

Anglo American Other Brazil Other South

America

India

Mauritania

South Africa

Other Africa

China (62.5% Fe equivalent)

C.I.S.

North America

Europe

Other

World Production 2012

Seaborne trade dominated by Big 3 with FMG closing

CIP Research

Vale

Rio Tinto BHP Billiton

Kumba

FMG

CSN

LKAB

SNIM

Indian Exporters

Others

Seaborne Exporters 2012

ASX is currently the best exchange for iron ore exploration companies

considering that:

Australia is the world’s largest iron ore exporter accounting for half of

global seaborne supply

There are 5 times as many “pure play” ASX-listed iron ore exploration stocks

than on the TSX with a combined market capitalisation 12 times the TSX(i)

EV/Resource average of A$0.89/t for iron ore exploration companies(ii)

even

though many projects are stranded without infrastructure

Better coverage of the companies due to the existence of well regarded

mining analysts

Monitored by global institutional and strategic mining investors

ASX: The Main Market for Global Iron Ore

Source: (i) Bloomberg 11 Sep 2013; (ii) Bloomberg 11 Sep 2013 and CIP research

Private and Confidential 24

“Pure Play” Iron Ore Exploration Companies

There are 5 times as many “pure play” ASX-listed iron ore exploration stocks than on the TSX

with a combined market capitalisation 12 times the TSX (excludes FMG, RIO and BHP) and 7

times the TSX in terms of EV/Resources multiples

Source: Bloomberg (10 Sep 2013)

Note: (i) Excludes ASX & TSX listed companies with market cap. less than $A10m or greater than $1b; (ii) Based on A$/C$ of 0.95

Private and Confidential 25

8.81

4.21

3.19

0.57 0.54 0.41 0.32 0.25 0.21 0.14 0.13 0.11 0.11 0.08 0.08 0.07 0.07 0.06 0.05 0.04 0.03 0.02 -

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

MGX BCI IFE AGO RHI WDR NFE SDL BCK AQA GWR CTM GRR FMS IXR JMS IRD HAR CFE GBG IOH EQX

(A$

/t)

ASX EV/Resource Multiples

ASX Average 0.89X

ASX Iron Ore Exploration Companies Valuation

Examination of iron ore exploration trading multiples on the ASX indicates comparable valuation

of 8.81x to 0.02x of JORC Resource multiples

Sources: Bloomberg (13 Sep 2013), Company filings

Notes: Excludes ASX iron ore exploration companies with market cap less than A$20 million

Private and Confidential 26

TSX Iron Ore Exploration Companies Valuation

Examination of iron ore exploration trading multiples in the TSX indicates 7 times lower

EV/Resource multiples when compared to those of ASX companies

Sources: Bloomberg (13 Sep 2013), Company filings

Notes: Excludes TSX iron ore exploration companies with market cap less than C$10million

A$/C$ = 0.95

0.72

0.10

0.01 0.00 0.00 0.00 - -

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

LIM ADV FEO CHM NML FER ADI

(A$

/t)

TSX EV/Resource Multiples

TSX Average 0.12X

ASX Average 0.89X

Private and Confidential 27

China still forecast for long term growth

Lower growth rates currently but still very significant in absolute volumes

Strong economy

Stimulus packages for US$157Billion in infrastructure projects

FMG

Global urban population and GDP growth

China steel production to grow to 1Bt

Close to Europe

94 Billion tonnes of resource

Labrador Trough companies and resources

Company Project Deposit Type

M+I+I

Resources (Mt) Fe Grade (%)

Resource

Ownership (Mt)

Attributable

Fe

Adriana / Wisco Lac Otelnuk Magnetite 23,740 29.7% 9,496 2,821

Alderon / Hebei Rose Central Magnetite 705 29.0% 529 153

North Rose Magnetite 836 30.2% 627 189

Mills Lake Magnetite 256 29.6% 192 57

ArcelorMittal / Posco &

China Steel Canada ex Baffin Magnetite/Hematite 7,893 29.8% 6,709 1,996

Cap-ex Ventures Block 103 Magnetite 7,200 29.2% 7,200 2,102

Century Iron Mines/

Wuhan Rainy Lake Magnetite 15,954 30.0% 9,572 2,872

Hayot Lake Magnetite 1,723 31.3% 579 181

Duncan Lake Magnetite 1,614 24.5% 484 121

Champion Iron Mines Fire Lake North Hematite 1,456 30.0% 1,456 437

Bellechase Magnetite/Hematite 215 29.0% 215 62

Harvey Tuttle Magnetite/Hematite 947 25.0% 717 179

Moire Lake Magnetite/Hematite 581 29.7% 581 173

Oil Can Magnetite/Hematite 1,896 29.7% 1,896 563

Attikamagen Magnetite 1,723 31.3% 758 237

Cliffs / Wuhan Bloom Lake Magnetite/Hematite 1,051 29.8% 366 110

Cliffs Wabush Hematite 69 37.5% 69 26

IOC / Rio Carol Lake Magnetite/Hematite 3,042 43.2% 1,786 772

Labradore Iron Mines Houston Project Hematite 26 57.2% 26 15

Redmond Hematite 3 56.3% 3 2

Knob Lake Hematite 6 56.7% 6 3

James Hematite 7 57.4% 7 4

Denault Hematite 7 54.8% 7 4

New Millenium / Tata DSO Project Hematite 95 59.1% 19 11

New Millenium KeMag Magnetite 3,463 31.3% 1,247 390

LabMag Magnetite 5,741 29.5% 2,067 609

Howell’s Magnetite 7,600

Iac Ritchie Magnetite 4,767 30.5% 4,767 1,454

Oceanic Iron Ore Hopes Advanc Magnetite/Hematite 1,610 32.2% 1,610 518

Total 94,226 CIP Research

CIP DISCLAIMER

Presentation of General Background

This document contains general background information about the activities of Mamba Minerals Limited (“Mamba” or “the

Company”) current as at the date of this presentation. It is information in a summary form only and does not contain all the

information necessary to fully evaluate any transaction or investment. It should be read in conjunction with Mamba’s other

periodic and continuous disclosure requirements to the ASX available at www.asx.com.au.

This presentation may include forward-looking statements. These forward-looking statements are based on management’s

expectations and beliefs concerning future events. Forward-looking statements are necessarily subject to risks, uncertainties and

other factors, many of which are outside the control of Mamba that could cause actual results to differ materially from such

statements. Mamba makes no undertaking to subsequently update or revise the forward-looking statements made in this release

to reflect events or circumstances after the date of this release.

Capital Investment Partners (CIP) believes to the best of its knowledge information and general advice contained in this

presentation is accurate as at the date of issue. To the fullest extent permitted by law, each of CIP and its directors, officers,

employees and advisers excludes and disclaims all liability for any direct or indirect expenses, losses, costs or damages

whatsoever arising in any way for any representation, act or omission, whether express or implied (including responsibility to any

person by reason of negligence). Except for any liability that cannot be excluded by law, CIP does not accept any responsibility in

relation to the Information or the general advice. This presentation has been prepared using publically available information and

we do not make any representation or warranty that it is accurate, complete or up to date. Opinions expressed are subject to

change without notice. CIP and its employees own shares and performance shares in MAB. Gavin Argyle is a significant

shareholder of MAB.

There are a number of risks, both specific to Mamba and of a general nature which may affect the future operating and financial

performance of Mamba and the value of an investment in Mamba including and not limited to economic conditions, stock market

fluctuations, iron ore demand and price movements, timing of access to infrastructure, timing of environmental approvals,

regulatory risks, operational risks, reliance on key personnel, reserve and resource estimations, native title and title risks, foreign

currency fluctuations, and mining development, construction and commissioning risk

Competent Persons Statement

The information in this report that relates to Exploration Results is based on information compiled by Mr Greg Burns and Mr Barry

Knight who are members of the Australian Institute of Mining and Metallurgy. Mr Burns is a director of the company and an

employee of CIP. Mr Burns and Mr Knight have sufficient experience which is relevant to the style of mineralisation and type of

deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004

Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Mr Burns and Mr

Knight consents to the inclusion in the report of the matters based on his information in the form and context in which it

appears.

CIP Contact Details

Capital Investment Partners

Canada

Suite 800

1199 West Hastings Street

Vancouver, British Columbia

V6E 3T5

T +1 604 687 2038

F +1 604 687 3141

Australia

Level 7, BGC Centre

28 The Esplanade

Perth, Western Australia

6000

T +61 8 9421 2111

F +61 8 9421 2100

Hong Kong

3812-13, 38/F Two IFC

8 Finance Street

Central,

Hong Kong

T +852 3978 2811

Mamba Minerals

www.mamba.com.au

Canada

Suite 800

1199 West Hastings Street

Vancouver, British Columbia

V6E 3T5

T +1 604 687 2038

F +1 604 687 3141

Australia

Level 7, BGC Centre

28 The Esplanade

Perth, Western Australia

6000

T +61 8 9421 2111

F +61 8 9421 2100

Australia

Level 1,

91 Evans Street

Rozelle, Melbourne, NSW

2039

T +61 8 9421 2111

F +61 8 9421 2100

Mamba Contact Details