makerere university kampala report

TRANSCRIPT

OFFICE OF THE AUDITOR GENERAL

THE REPUBLIC OF UGANDA

MAKERERE UNIVERSITY

REPORT AND OPINION OF THE AUDITOR GENERAL ON THE FINANCIAL

STATEMENTS OF MAKERERE UNIVERSITY FOR THE FINANCIAL YEAR ENDED

30TH JUNE, 2015

OFFICE OF THE AUDITOR GENERAL

UGANDA

ii

TABLE OF CONTENTS

LIST OF ACRONYMS ........................................................................................................... iii

DETAILED REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF

MAKERERE UNIVERSITY FOR THE YEAR ENDED 30TH JUNE, 2015 .......................................... 5

1.0 INTRODUCTION .......................................................................................................................... 5

2.0 BACKGROUND INFORMATION.................................................................................................. 5

3.0 FINANCING OF THE UNIVERSITY ............................................................................................ 6

4.0 OBJECTIVES OF THE UNIVERSITY .......................................................................................... 6

5.0 AUDIT OBJECTIVES .................................................................................................................... 6

6.0 AUDIT PROCEDURES PERFORMED .......................................................................................... 7

7.0 AUDIT FINDINGS ........................................................................................................................ 8

8.0 FINANCIAL STATEMENTS ........................................................................................21

iii

LIST OF ACRONYMS

ACRONYM MEANING

CAES College of Agricultural and Environmental Sciences

CEDAT College of Engineering, Design, Art and Technology

CEES College of Education and External Studies

CEMAS Centralised Education Management System

CHUSS College of Humanities and Social Sciences

COBAMS College of Business and Management Sciences

COCIS College of Computing and Information Sciences

CONAS College of Natural Sciences

DAP Deposit Administration Plan

GoU Government of Uganda

MUBS Makerere University Business School

NSSF National Social Security Fund

PDE Procurement and Disposal Entity

PDU Procurement and Disposal Unit

PPDA Public Procurement and Disposal of Public Assets

SIDA Swedish International Development Cooperation Agency

TAI Treasury Accounting Instruction

UGX Uganda Shillings

WIP Work in Progress

1

REPORT OF THE AUDITOR GENERAL

ON THE FINANCIAL STATEMENTS OF MAKERERE UNIVERSITY FOR THE YEAR

ENDED 30TH JUNE, 2015

THE RT. HON. SPEAKER OF PARLIAMENT

I have audited the accompanying financial statements of Makerere University for the year

ended 30th June, 2015. These financial statements comprise of the Statement of Financial

Position as at 30th June, 2015, Statement of Financial Performance, Statement of Changes in

Equity, Cash flow Statement, together with other accompanying statements, notes and

accounting policies.

Management Responsibility for the Financial Statements

Under Article 164 of the Constitution of the Republic of Uganda, 1995 (as amended) and

Section 45 of the Public Finance Management Act, 2015, the Accounting Officer is

accountable to Parliament for the funds and resources of the University. The Accounting

Officer is also responsible for the preparation of financial statements in accordance with the

requirements of the Public Finance Management Act 2015, and the Financial Management

Guidelines for Public Universities, 2009, and for such internal controls as management

determines are necessary to enable the preparation of financial statements that are free

from material misstatements, whether due to fraud or error.

Auditor’s Responsibility

My responsibility as required by Article 163 of the Constitution of the Republic of Uganda,

1995 (as amended) and Sections 13 and 19 of the National Audit Act, 2008 is to express an

opinion on the financial statements based on my audit. I conducted my audit in accordance

with the International Standards on Auditing. The standards require that I comply with

ethical requirements and plan and perform the audit to obtain reasonable assurance on

whether the financial statements are free from material misstatement.

An audit involves performing audit procedures to obtain audit evidence about the amounts

and disclosures in the financial statements as well as evidence supporting compliance with

relevant laws and regulations. The procedures selected depend on the Auditor’s judgment,

including the assessment of risks of material misstatement of the financial statements

2

whether due to fraud or error. In making those risk assessments, the Auditor considers

internal controls relevant to the entity’s preparation and fair presentation of financial

statements in order to design audit procedures that are appropriate in the circumstances,

but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal

controls. An audit also includes evaluating the appropriateness of accounting policies used

and the reasonableness of accounting estimates made by management, as well as

evaluating the overall presentation of the financial statements.

I believe that the audit evidence I have obtained is sufficient and appropriate to provide a

basis for my opinion.

Part “A” of my report sets out my opinion on the financial statements. Part “B” which forms

an integral part of this report presents in detail all the significant audit findings made during

the audit which have been brought to the attention of management and will form part of my

Annual Report to Parliament.

Opinion

In my opinion, the financial statements of the Makerere University for the year ended 30th

June 2015 are prepared, in all material respects, in accordance with Section 51 of the Public

Finance Management Act, 2015, and the Financial Management Guidelines for Public

Universities, 2009.

Emphasis of Matter

Without qualifying my opinion, I draw your attention to the following matters disclosed in

the financial statements;

Un-accounted for Funds

I noted that accountabilities totaling to UGX.511,171,395 of which UGX.219,399,310

were personal advances to staff which had remained outstanding for a period of

more than one year, and UGX.291,772,085 administrative advances remained

outstanding. The funds were advanced to staff to carry out various activities of the

University. In the absence of the relevant accountability documents, it was not

possible to confirm that the funds were used for the intended purposes.

3

Non-Disclosure of Donor Grants

During the year total donor grants reported amounted to UGX.10,983,905,581,

however, this only related to the SIDA – SAREC projects. All other none bilateral

donor grants/projects, such as; Africa Centre for Systematic Reviews & Knowledge

Translation, Post Abortion Care Study, among others were not disclosed. Without

proper disclosure of donor funding, I could neither ascertain how much the university

received from other donors nor confirm if those funds were used for the intended

purposes.

Management of Pension Liabilities

During the year, outstanding pension liabilities of the university had decreased from

UGX.30,406,365,541 to UGX.29,927,548,933 indicating a meager payment of

pension arrears of only UGX.478,816,608. This pension liability has been outstanding

for over 10 years.

Other Matters

In addition to the matters raised above, I consider it necessary to communicate the

following matters other than those presented or disclosed in the financial statements;

Transfers to Personal Bank Accounts

Contrary to the Treasury Accounting Instructions, it was noted that payments

totalling to UGX.776,009,229 were made by various colleges for supplies, and

meeting costs of different activities through staffs’ personal bank accounts. There

was no evidence to show that the staff were appointed as imprest holders, and no

reasons were given to justify the payments to the individuals’ bank accounts.

Leasing of University Land at Kololo

I noted that the University leased out land located on Plots 34 – 36a on Prince

Charles Drive, Kololo, to a private investor without the full knowledge of the Minister,

at a cost of UGX.1,500,000,000. The proceeds from the transactions were

transferred directly to the university expenditure account and expensed. I further

4

noted that this transaction was not disclosed and reported in the financial statements

under the memorandum statement of disposal of physical assets.

Staffing Gaps

A review of the staff structure of the university with emphasis on the academic and

administrative staff revealed that there were major staffing gaps between the

established positions compared to the currently filled positions. Out of 2,774

established academic positions, only 1,333 (48%) are filled, leaving a staffing gap of

1,441 positions (52%).

John F.S. Muwanga AUDITOR GENERAL

21St December, 2015

5

PART “B”

DETAILED REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS

OF MAKERERE UNIVERSITY FOR THE YEAR ENDED 30TH JUNE, 2015

This section outlines in detail the audit scope, audit findings, my recommendations and

management responses in respect thereof.

1.0 INTRODUCTION

Article 163 (3) of the Constitution of the Republic of Uganda, 1995 (as amended)

requires me to audit and report on the public accounts of Uganda and all public

offices including the courts, the central and local government administrations,

universities, and public institutions of a like nature and any public corporation or

other bodies or organizations established by an Act of Parliament. Accordingly, I

carried out the audit of the University to enable me report to Parliament.

2.0 BACKGROUND INFORMATION

Makerere University was established in 1922 as a Technical School. The School,

which was later renamed Uganda Technical College, opened its doors to 14 day -

students who began studying Carpentry, Building and Mechanics. The College soon

began offering various other courses in Medical Care, Agriculture, Veterinary

Sciences and Teacher Training. It expanded over the years to become a Center for

Higher Education in East Africa in 1935. In 1937, the College started developing into

an institution of Higher Education, offering Post-School Certificate Courses.

In 1949, it became a University College affiliated to the University College of London,

offering courses leading to the general degrees of its then mother institution. With

the establishment of the University of East Africa on 29th June, 1963, the special

relationship with the University of London came to a close and degrees of the

University of East Africa were instituted.

On 1stJuly, 1970, Makerere became an independent National University of the

Republic of Uganda, offering Undergraduate and Postgraduate Courses leading to its

own awards.

The University currently offers not only day, but also evening and external study

programmes to a student body of about 30,000 undergraduates and 3,000

postgraduates (both Ugandan and Foreign). It is also a very active centre for

research, and operates two (2) external campuses in Fortportal and Jinja since 2010.

6

The University has since July 2011 become a Collegiate University, consisting of nine

(9) Colleges and one (1) School, operating as semi-autonomous units of the

University.

3.0 FINANCING OF THE UNIVERSITY

The University was financed by grants from the Central Government

(UGX.89,180,150,472), and grants from Foreign Governments

(UGX.10,983,905,581), while UGX.92,305,331,082 was collected as Non-Tax

revenue, and UGX.6,832,584,000 as other revenues. This brings total revenue that

was available to the university to UGX.199,301,971,135 representing about 86.4% of

the budgeted amount of UGX.230,757,799,581, for the year under review.

4.0 OBJECTIVES OF THE UNIVERSITY

The University has the following objectives;

To improve organisational and operational efficiency;

To improve and develop human resources;

To create ability to mobilize and allocate resources better;

To improve the University’s capacity and quality in areas of teaching and

learning;

To enhance the University’s capacity to conduct high-quality and relevant

research;

To improve the capacity and quality as well as relevance of the University’s

Services, and;

To build new physical infrastructures to cater for more students and improve

the quality of education.

5.0 AUDIT OBJECTIVES

The audit was carried out in accordance with International Standards on Auditing

and accordingly included a review of the accounting records and agreed procedures

as was considered necessary. In conducting my reviews, special attention was paid

to establish;

a. Whether the financial statements have been prepared in accordance with

consistently applied accounting policies and fairly present the revenues and

expenditures for the period and of the financial position as at the end of the

period.

7

b. Whether all funds were utilized with due attention to economy and efficiency

and only for the purposes for which the funds were provided.

c. Whether goods and services financed have been procured in accordance with

the Government of Uganda Procurement regulations.

d. To evaluate and obtain a sufficient understanding of the internal control

structure of the University, assess control risk and identify reportable

conditions, including material internal control weaknesses.

e. Whether management was in compliance with the Government of Uganda

financial regulations.

f. Whether all necessary supporting documents, records and accounts have

been kept in respect of all activities, and are in agreement with the financial

statements presented.

6.0 AUDIT PROCEDURES PERFORMED

The following audit procedures were undertaken;

a. Revenue

Obtained schedules of all revenues collected and reconciled the amounts to the

cashbooks and bank statements.

b. Expenditure

The payment vouchers were examined for proper authorization, eligibility and

budgetary provision, accountability and support documentation.

c. Internal Control system

Reviewed the internal control system and its operations to establish whether sound

controls were applied throughout the period audited.

d. Procurement

Reviewed the procurement of goods and services by the University during the period

under review and reconciled with the approved procurement plan.

e. Fixed Asset Management

Reviewed the use and management of the University assets during the period under

audit

f. University’s Financial Statements

Examined on a test basis, evidence supporting the amounts and disclosures in the

financial statements; assessed the accounting principles used and significant

estimates made by management; as well as evaluating the overall financial

statement presentation.

8

7.0 AUDIT FINDINGS

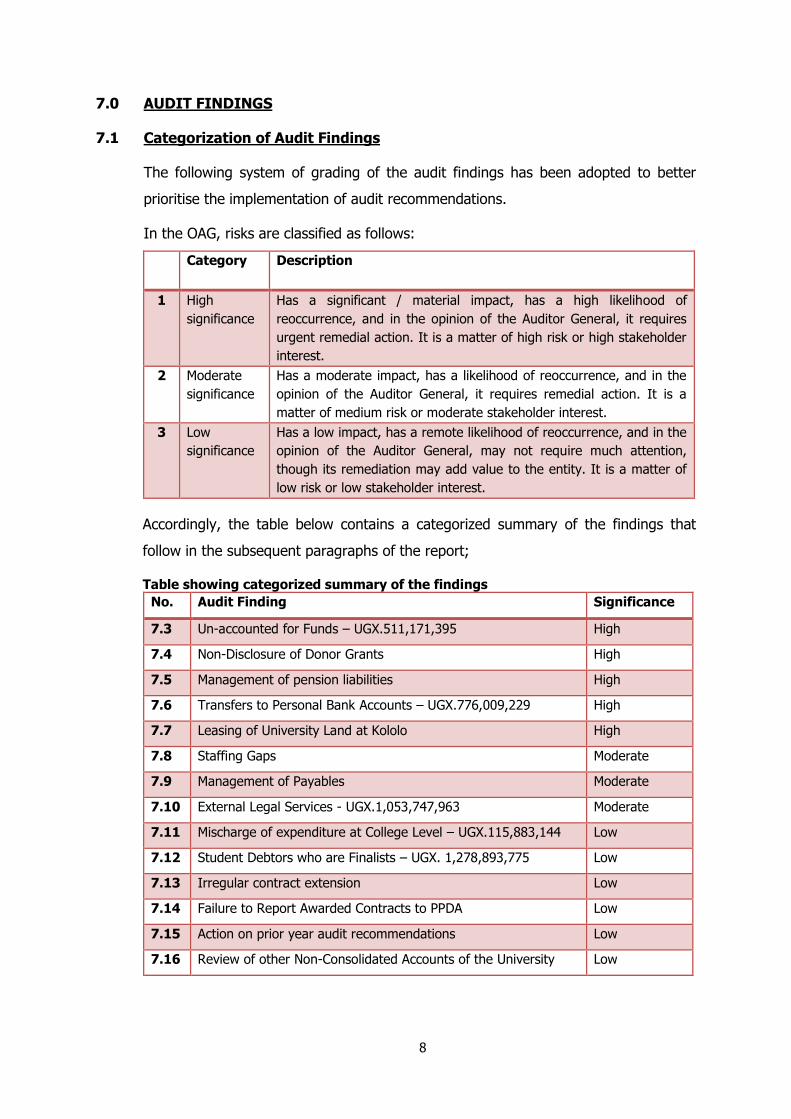

7.1 Categorization of Audit Findings

The following system of grading of the audit findings has been adopted to better

prioritise the implementation of audit recommendations.

In the OAG, risks are classified as follows:

N

o

Category Description

1 High

significance

Has a significant / material impact, has a high likelihood of

reoccurrence, and in the opinion of the Auditor General, it requires

urgent remedial action. It is a matter of high risk or high stakeholder

interest.

2 Moderate

significance

Has a moderate impact, has a likelihood of reoccurrence, and in the

opinion of the Auditor General, it requires remedial action. It is a

matter of medium risk or moderate stakeholder interest.

3 Low

significance

Has a low impact, has a remote likelihood of reoccurrence, and in the

opinion of the Auditor General, may not require much attention,

though its remediation may add value to the entity. It is a matter of

low risk or low stakeholder interest.

Accordingly, the table below contains a categorized summary of the findings that

follow in the subsequent paragraphs of the report;

Table showing categorized summary of the findings

No. Audit Finding Significance

7.3 Un-accounted for Funds – UGX.511,171,395 High

7.4 Non-Disclosure of Donor Grants High

7.5 Management of pension liabilities High

7.6 Transfers to Personal Bank Accounts – UGX.776,009,229 High

7.7 Leasing of University Land at Kololo High

7.8 Staffing Gaps Moderate

7.9 Management of Payables Moderate

7.10 External Legal Services - UGX.1,053,747,963 Moderate

7.11 Mischarge of expenditure at College Level – UGX.115,883,144 Low

7.12 Student Debtors who are Finalists – UGX. 1,278,893,775 Low

7.13 Irregular contract extension Low

7.14 Failure to Report Awarded Contracts to PPDA Low

7.15 Action on prior year audit recommendations Low

7.16 Review of other Non-Consolidated Accounts of the University Low

9

7.2 Un-accounted for Funds – UGX.511,171,395

Section 4.6.4 of the Makerere University Finance Procedures Manual, 2014 requires

that advances should be accounted for within 14 days following the completion of

the exercise, but in any case not later than 60 days. I however noted that

accountabilities totaling to UGX.511,171,395 of which UGX.219,399,310 were

personal advances to staff which had remained outstanding for a period of more

than one year, and UGX.291,772,085 as administrative advances remained

outstanding. The funds were advanced to staff to carry out various activities of the

University. In the absence of the relevant accountability documents, it was not

possible to confirm that the funds were used for the intended purposes.

In his response, the Accounting Officer promised to follow up on all outstanding

advances and where necessary, institute recovery measures, in case of total failure

to account by the responsible staff.

I advised the accounting Officer to strengthen controls over advances to staff and

ensure adherence with the University policy regarding accountability for funds.

7.3 Non-Disclosure of Donor Grants

During the year total donor grants reported amounted to UGX.10,983,905,581.

However, this only related to the SIDA – SAREC projects. All other none bilateral

donor grants/projects, such as; Africa Centre for Systematic Reviews & Knowledge

Translation, Post Abortion Care Study, among others were not disclosed. Without

proper disclosure of donor funding, I could neither ascertain how much the university

received from other donors nor confirm if those funds were used for the intended

purposes.

In their response, Management explained that the university only discloses grants

from bilateral sources. I advised the Accounting Officer to make a complete

disclosure of all donor funding received by the University, in line with the

requirements under Section 43(1) of the PFMA, 2015 that requires that all

expenditure to be incurred by Government on projects which are externally financed,

in a financial year have to be appropriated by Parliament.

7.4 Management of Pension Liabilities

During the year, outstanding pension liabilities of the university had decreased from

UGX.30,406,365,541 to UGX.29,927,548,933 indicating a meager payment of

10

pension arrears of only UGX.478,816,608. However, the pension liability has taken

long to be settled, yet it is amongst the reasons leading to staff strife at the

University. It was noted that this has been outstanding for over 10 years.

The Accounting officer in his response stated that, several appeals and requests

were made for these arrears to be settled by MOFPED. Besides, the University was

taken to the Industrial Court and there is high risk of interest and penalties being

charged if this obligation is not settled.

I advised the Accounting Officer to continue liaising with all the relevant stakeholders

to ensure that the obligation is settled without further delay with a view of saving the

government from unnecessary legal costs.

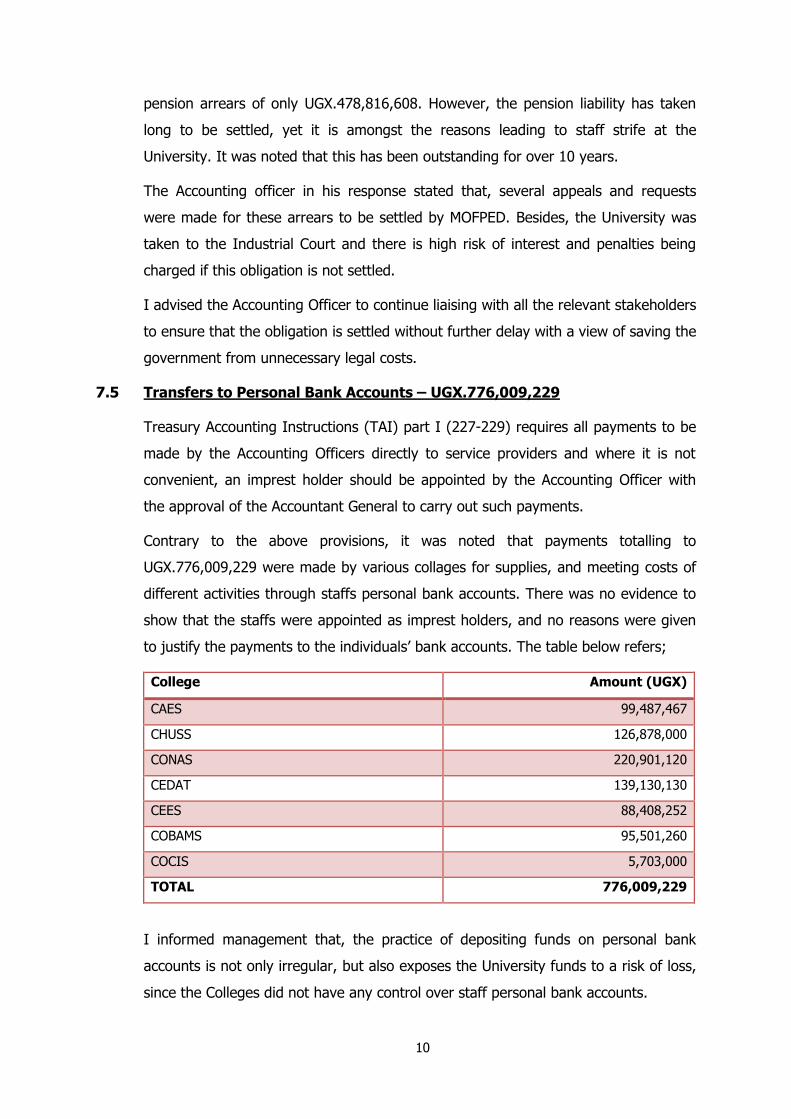

7.5 Transfers to Personal Bank Accounts – UGX.776,009,229

Treasury Accounting Instructions (TAI) part I (227-229) requires all payments to be

made by the Accounting Officers directly to service providers and where it is not

convenient, an imprest holder should be appointed by the Accounting Officer with

the approval of the Accountant General to carry out such payments.

Contrary to the above provisions, it was noted that payments totalling to

UGX.776,009,229 were made by various collages for supplies, and meeting costs of

different activities through staffs personal bank accounts. There was no evidence to

show that the staffs were appointed as imprest holders, and no reasons were given

to justify the payments to the individuals’ bank accounts. The table below refers;

College Amount (UGX)

CAES 99,487,467

CHUSS 126,878,000

CONAS 220,901,120

CEDAT 139,130,130

CEES 88,408,252

COBAMS 95,501,260

COCIS 5,703,000

TOTAL 776,009,229

I informed management that, the practice of depositing funds on personal bank

accounts is not only irregular, but also exposes the University funds to a risk of loss,

since the Colleges did not have any control over staff personal bank accounts.

11

The Accounting Officer in his response stated that these payments were for activities

which are field based. I advised management to desist from such practices and

adhere to the requirements under the Treasury Accounting Instructions.

7.6 Leasing of University Land at Kololo

According to Section 87(1c) of the PPDA, a procuring and disposing entity shall not

dispose of any strategic asset, without the prior approval of the Minister. Contrary to

this provision, it was established that the University leased out land located on Plots

34–36a on Prince Charles Drive, Kololo, to a private investor at a cost of

UGX.1,500,000,000 without the full knowledge of the Minister. It was noted that the

proceeds from the transaction were transferred directly to the university expenditure

account and expensed. I further noted that this transaction was not disclosed and

reported in the financial statements under the memorandum statement of disposal of

physical assets. In absence of proper disclosure and respective reporting of the

transaction, there is a risk that the proceeds from the transaction may not have been

put to proper use.

In response, the Accounting Officer stated that, the transaction was approved by the

University Council and that its respective proceeds were used to finance university

pressing needs. I advised the Accounting Officer to always adhere to the

requirements under the Law, while disposing any University asset. For completeness

and full disclosure, the disposal of such a strategic asset should in future be

disclosed and reported on accordingly.

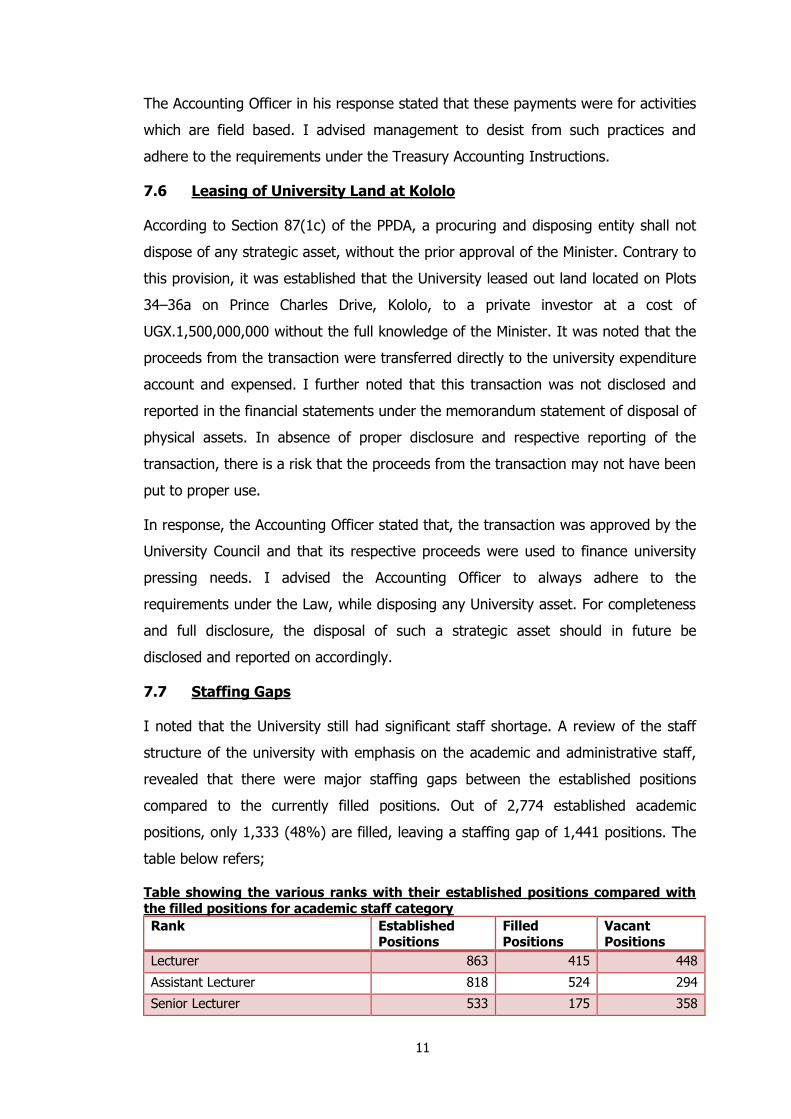

7.7 Staffing Gaps

I noted that the University still had significant staff shortage. A review of the staff

structure of the university with emphasis on the academic and administrative staff,

revealed that there were major staffing gaps between the established positions

compared to the currently filled positions. Out of 2,774 established academic

positions, only 1,333 (48%) are filled, leaving a staffing gap of 1,441 positions. The

table below refers;

Table showing the various ranks with their established positions compared with

the filled positions for academic staff category

Rank Established Positions

Filled Positions

Vacant Positions

Lecturer 863 415 448

Assistant Lecturer 818 524 294

Senior Lecturer 533 175 358

12

Rank Established

Positions

Filled

Positions

Vacant

Positions

Associate Professor 280 138 142

Professor 253 77 176

Research Fellow 16 3 13

Senior Research Fellow 4 1 3

Research Associate Professor 2 0 2

Research Professor 2 0 2

Dep. Illustrator (Asso. Prof) 1 0 1

Medical Illustrator (Prof) 1 0 1

Sen.Asst.Med. Illustrator(Sen. Lec) 1 0 1

Total 2,774 1,333 1,441

In addition, the university established 554 positions for administrative staff, but I

noted that only 168 (30%) are filled, leaving 383 positions vacant.

I informed management that lack of adequate staffing coupled with the demanding

workload on the existing staff may impact negatively on service delivery and

achievement of the university’s objectives. Worse still, segregation of duties may not

be adequately done as recommended.

I advised the Accounting Officer to liaise with the concerned stakeholders, to ensure

that the University’s staffing matters are addressed.

7.8 Management of Payables

At close of the financial year, the University maintained a payables balance of

UGX.21,776,933,009 despite a reduction from UGX.25,822,288,140 reported in the

previous financial year (2013/2014). These related to committed creditors and

deposits received. I informed management that Non – payment of debts could lead

to litigation for delayed payment which may also result into further liquidity

problems.

The Accounting Officer in his response stated that, the payables related to Staff

incentives brought about by industrial action by Academic staff to increase salaries.

Besides they also related to older periods as further as 2009. The University Council

had put in place a Council Committee to rationalize and review the sustainability of

the staff incentive.

I advised the Accounting officer to ensure clearance of obligations with the creditors

and also cease the practice of overcommitting government in line with the

requirements under the commitment control policy of government.

13

7.9 External Legal Services - UGX.1,053,747,963

During the year under review, audit noted that the university paid a total of

UGX.1,053,747,963 in fees and other payments to their external lawyers, for legal

services offered to the university. Audit noted the following;

There were cases in which payments, such as out of court settlements were

paid to the university lawyers and not to the recipients or their legal

representatives without any acknowledgment being sought. In addition, there

were no written instructions authorizing that the funds be paid to the

lawyers. I could not ascertain whether such funds were received by the

rightful recipients.

The university does not disclose any ongoing litigation as contingent liabilities

in the memorandum statements attached to the financial statements. This

despite the number of court cases the university is currently faced with.

Where the legal team has negotiated settlements on behalf of the university,

there is no evidence that the university management was invited to the

negotiations before they were approved and signed off or that they were

drafted and ratified by management. Instead, only court orders are filed.

There is a risk that out of court settlements are not conducted in a

transparent manner.

Whereas the university has an internal legal team, the university is still

spending a significant amount of funds as payment for external legal services.

There is a risk of wastage through payments for services that could have

been done in-house.

In his response, the Accounting officer explained that the University was improving

the capacity of the in-house legal services to be able to handle all legal services.

I advised the Accounting Officer;

To ensure that out of court settlements paid to the lawyers for onward

transmission to the beneficiaries are duly acknowledged by the beneficiaries.

To disclose in the financial statements all contingent liabilities from legal

cases involving the university.

To ensure that the University legal team is strengthened to enable it build

capacity in handling some of the legal cases. This will lead to cost savings to

the university.

14

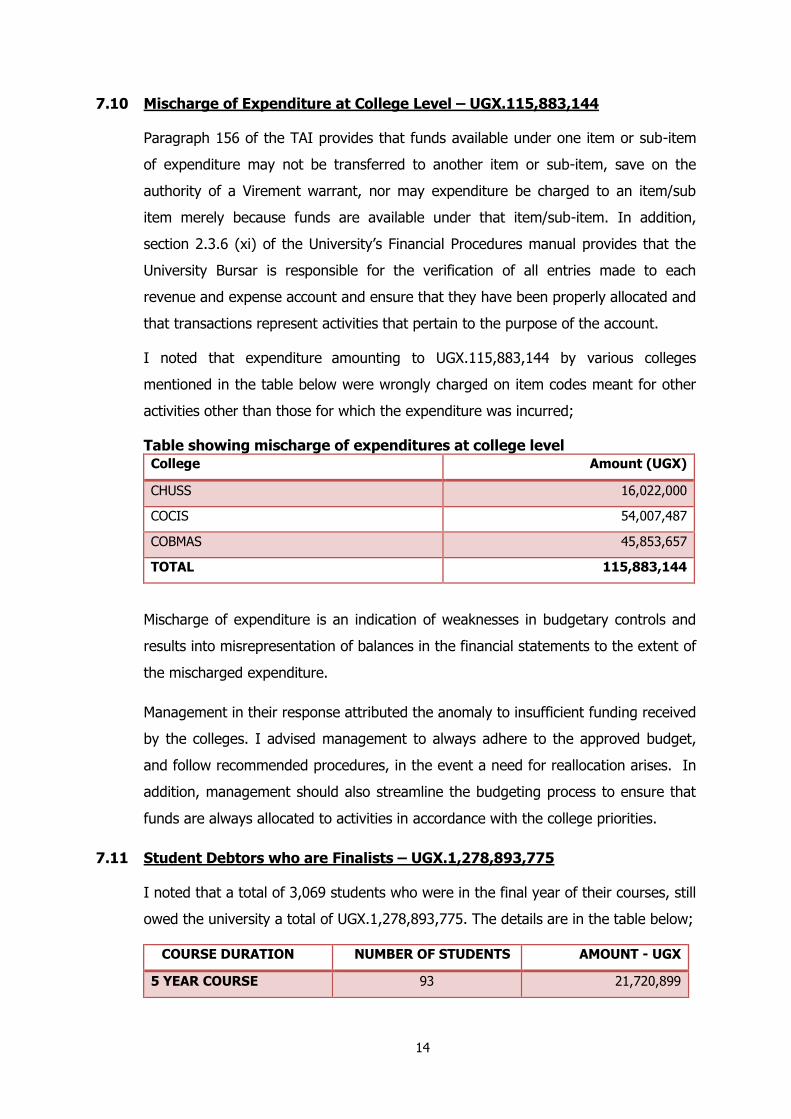

7.10 Mischarge of Expenditure at College Level – UGX.115,883,144

Paragraph 156 of the TAI provides that funds available under one item or sub-item

of expenditure may not be transferred to another item or sub-item, save on the

authority of a Virement warrant, nor may expenditure be charged to an item/sub

item merely because funds are available under that item/sub-item. In addition,

section 2.3.6 (xi) of the University’s Financial Procedures manual provides that the

University Bursar is responsible for the verification of all entries made to each

revenue and expense account and ensure that they have been properly allocated and

that transactions represent activities that pertain to the purpose of the account.

I noted that expenditure amounting to UGX.115,883,144 by various colleges

mentioned in the table below were wrongly charged on item codes meant for other

activities other than those for which the expenditure was incurred;

Table showing mischarge of expenditures at college level College Amount (UGX)

CHUSS 16,022,000

COCIS 54,007,487

COBMAS 45,853,657

TOTAL 115,883,144

Mischarge of expenditure is an indication of weaknesses in budgetary controls and

results into misrepresentation of balances in the financial statements to the extent of

the mischarged expenditure.

Management in their response attributed the anomaly to insufficient funding received

by the colleges. I advised management to always adhere to the approved budget,

and follow recommended procedures, in the event a need for reallocation arises. In

addition, management should also streamline the budgeting process to ensure that

funds are always allocated to activities in accordance with the college priorities.

7.11 Student Debtors who are Finalists – UGX.1,278,893,775

I noted that a total of 3,069 students who were in the final year of their courses, still

owed the university a total of UGX.1,278,893,775. The details are in the table below;

COURSE DURATION NUMBER OF STUDENTS AMOUNT - UGX

5 YEAR COURSE 93 21,720,899

15

4 YEAR COURSE 344 159,334,630

3 YEAR COURSE 2,375 765,395,921

2 YEAR COURSE 257 332,442,325

TOTAL 3,069 1,278,893,775

I informed management that there is a risk that the students may graduate without

the university recovering all the dues.

Management in their response indicated that these finalists with balances had been

submitted to the Academic Registrar to ensure recovery. I advised the Accounting

Officer to ensure the recovery of all dues before the students complete their final

exams.

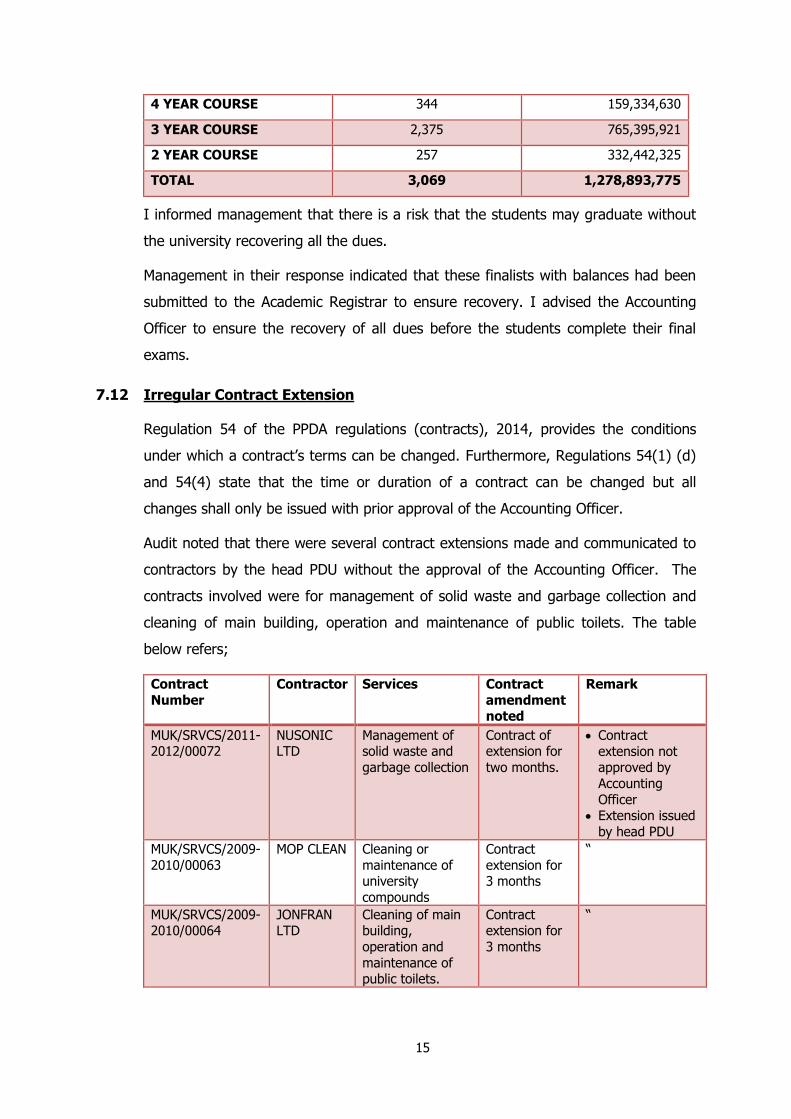

7.12 Irregular Contract Extension

Regulation 54 of the PPDA regulations (contracts), 2014, provides the conditions

under which a contract’s terms can be changed. Furthermore, Regulations 54(1) (d)

and 54(4) state that the time or duration of a contract can be changed but all

changes shall only be issued with prior approval of the Accounting Officer.

Audit noted that there were several contract extensions made and communicated to

contractors by the head PDU without the approval of the Accounting Officer. The

contracts involved were for management of solid waste and garbage collection and

cleaning of main building, operation and maintenance of public toilets. The table

below refers;

Contract

Number

Contractor Services Contract

amendment noted

Remark

MUK/SRVCS/2011-2012/00072

NUSONIC LTD

Management of solid waste and

garbage collection

Contract of extension for

two months.

Contract

extension not approved by

Accounting

Officer Extension issued

by head PDU

MUK/SRVCS/2009-

2010/00063

MOP CLEAN Cleaning or

maintenance of university

compounds

Contract

extension for 3 months

“

MUK/SRVCS/2009-2010/00064

JONFRAN LTD

Cleaning of main building,

operation and

maintenance of public toilets.

Contract extension for

3 months

“

16

In the absence of approval of contract extensions by the Accounting Officer, all such

extensions are irregular.

Management explained that prior to the Contracts Committee approval the

Accounting Officer endorsed the documents to confirm no objection to the contract

extension, and that after the Contracts Committee approval, the PDU Head, on

behalf of the Accounting Officer, communicated to the providers. However, no

evidence was availed to the effect.

I advised the accounting officer to observe strict adherence to the law regaring all

contract extensions.

7.13 Failure to Report Awarded Contracts to PPDA

In accordance with Regulation 20 (2) of the PPDA regulations (2014) and regulation

45(3), PDE’s are required to submit monthly reports by the 15th day of each month.

However, during the year, the University paid suppliers a total of UGX.1,574,033,758

as micro procurements below UGX.5 million, which were not reported to PPDA

regularly as required. I informed management that failure to submit monthly reports

is irregular.

The Accounting Officer in his response attributed the anomaly to staffing constraints

in the PDU due to staff resignations and retirement, and these had not been

replaced. I advised management to ensure that monthly reports on all procurement

activities are compiled and submitted as required by the law.

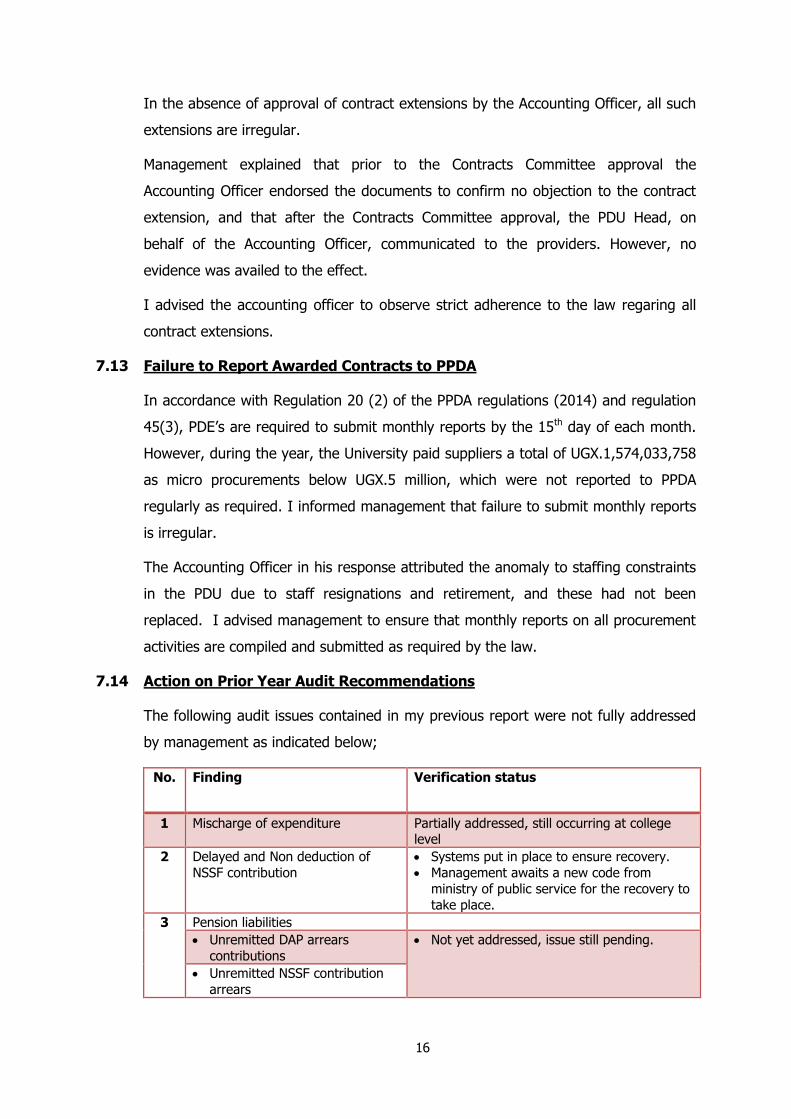

7.14 Action on Prior Year Audit Recommendations

The following audit issues contained in my previous report were not fully addressed

by management as indicated below;

No. Finding Verification status

1 Mischarge of expenditure Partially addressed, still occurring at college level

2 Delayed and Non deduction of

NSSF contribution

Systems put in place to ensure recovery.

Management awaits a new code from

ministry of public service for the recovery to

take place.

3 Pension liabilities

Unremitted DAP arrears

contributions

Not yet addressed, issue still pending.

Unremitted NSSF contribution

arrears

17

5 Accumulation of Payables Not yet addressed, still outstanding

6 Revenue shortfall

Not fully addressed

7 Management of receivables

Still outstanding, though fees collections are

ongoing.

8 Staffing Gaps Not yet addressed, restated to capture

managements response

9 Underutilisation of the integrated

tertiary system for revenue collection

A new system is being introduced by

MoFPED known as CEMAS

10 Land ownership Partially implemented

11 Lack of staff performance plans Not yet addressed

12

Failure by the system to generate reports

Addressed, a new system is being

introduced by MoFPED known as CEMAS

I have advised management to ensure that all recommendations are fully

implemented, so as to ensure enhanced accountability and better stewardship of the

resources allocated to the University.

7.15 Review of other Non-Consolidated Accounts of the University

A University operates a Guest House and a Printery, which are used to generate

internal revenue. However, a review of their operations revealed the following

anomalies;

7.15.1 University Guest House

a. Doubtful Revenue Reported

The total reported sales revenue in the Guest House’s statement of performance for

the year under review amounted to UGX.806,321,446. However a review of the

Guest House cashbook revealed that the total receipts in the year actually totaled to

UGX.1,101,545,665. This implies that the total sales revenue was understated by

UGX.295,224,219. By the time of writing this report, no response had been provided

by management.

I advised the Accounting Officer to ensure that the Guest House Manager accounts

for all the monies collected.

b. Failure to Bank Revenue Intact - UGX.446,860,974

The Head of Finance is responsible for ensuring that revenue collectors defined in

the University Regulations carry out their duties properly to ensure that all revenue

due to the University is properly collected in the approved manner and banked

intact.

18

In the period under review, an analysis of the cash book revealed that out of the

total collection by the Guest House amounting to UGX.806,321,446, a total of

UGX.446,860,974 was spent at source without first depositing the money in Guest

house main collection bank account (9030005965119) in Stanbic bank. Banking of

revenue intact, is a critical internal control procedure that ensures that all money

utilized by the guest house is duly approved and budgeted for.

The failure to bank revenue intact may have led to loss of revenue, and may also

hinder effective monitoring of expenditure and utilization of university revenue.

Management attributed the expenditure at source to Uganda Revenue Authority’s

issuance of an agency notice on the Guest house revenue collection bank account in

Stanbic bank because of un-cleared tax obligations.

I advised management to clear the URA tax obligations so that the agency notice is

lifted to enable effective revenue collection and monitoring.

7.15.2 University Printery (UP)

a. Non-disclosure of revenues – UGX.393,996,539

I noted that a sum of UGX.393,996,539 was paid to the University Printery collection

account by Makerere University for printing services. However, these funds were not

recorded in the cash book as receipts by the UP. Furthermore, the UP management

did not avail me with a copy of the bank statement to confirm whether these funds

were indeed received. Accordingly, these funds remained not accounted for by close

of audit. In addition, the total revenue reported by the Printery in its financial

statements was therefore understated.

Although the Printery Management explained that they did not receive the said

funds, this explanation could not be substantiated since no bank statement was

availed for review. I advised the Accounting Officer to follow up the matter with the

Manager and have the amounts fully acknowledged and accounted for.

b. Debtors/Receivables – UGX.845,634,281

The Printery debtors decreased by a paltry UGX.15,393,777 from UGX.845,634,281

in 2013/14 to UGX.830,240,504 in 2014/15, which is an indication of poor debt

recovery mechanisms, despite the fact that debtors constitute 30% of the total

assets of the Printery. The following additional observations were made;

19

Of the claimable debtors, a total of UGX.20,242,765 is Value Added Tax

(VAT) while Withholding Tax (WHT) is UGX.124,079,550. There are no

supporting documents in respect of these tax claims.

Of the total non-tax debt, UGX.545,843,725 or 82% is due from university

units or colleges.

There was no evidence to indicate that management was vigorously pursuing the

collection of the outstanding debtors/receivables. The failure on the part of

management to recover outstanding receivables may lead to accumulations beyond

recoverable levels which may necessitate writing off and this could result into

financial loss to the University Printery.

Management in their response indicated that debt recoveries from University Units

were ongoing with the help of university administration. I advised management to

ensure that proper debt recovery procedures are put in place so that all receivables

are collected within the allowable credit period.

c. Delays to Complete Jobs

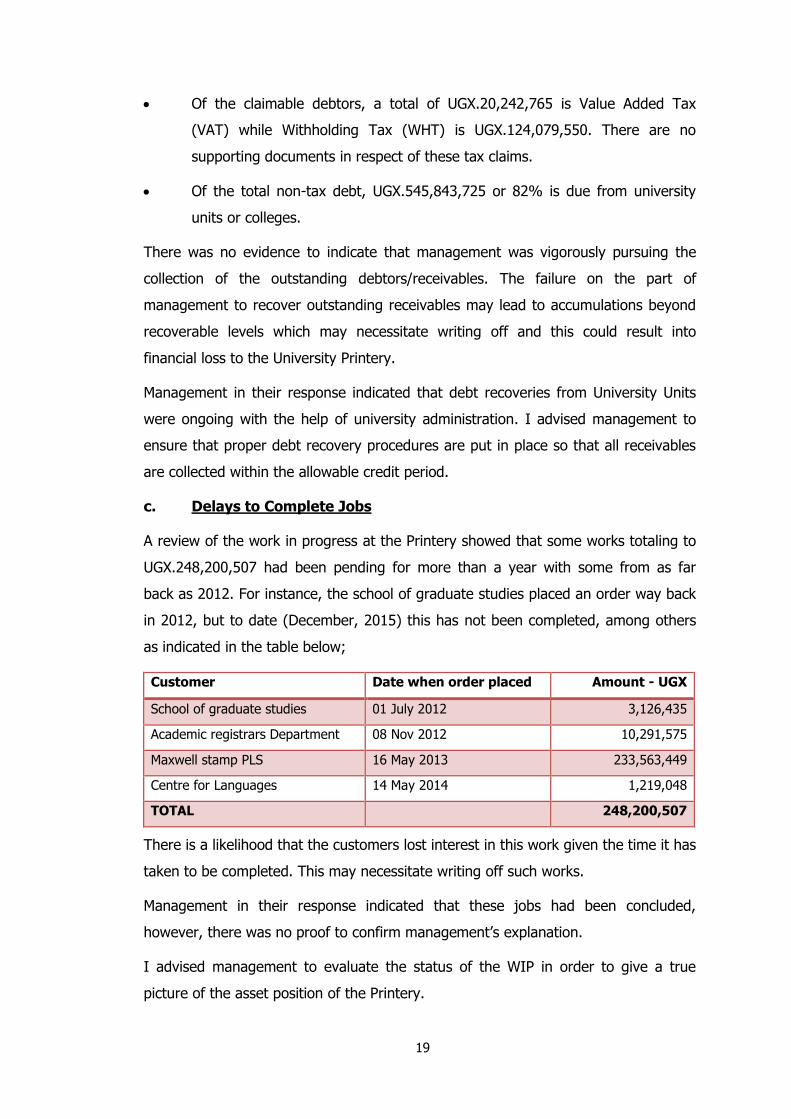

A review of the work in progress at the Printery showed that some works totaling to

UGX.248,200,507 had been pending for more than a year with some from as far

back as 2012. For instance, the school of graduate studies placed an order way back

in 2012, but to date (December, 2015) this has not been completed, among others

as indicated in the table below;

Customer Date when order placed Amount - UGX

School of graduate studies 01 July 2012 3,126,435

Academic registrars Department 08 Nov 2012 10,291,575

Maxwell stamp PLS 16 May 2013 233,563,449

Centre for Languages 14 May 2014 1,219,048

TOTAL 248,200,507

There is a likelihood that the customers lost interest in this work given the time it has

taken to be completed. This may necessitate writing off such works.

Management in their response indicated that these jobs had been concluded,

however, there was no proof to confirm management’s explanation.

I advised management to evaluate the status of the WIP in order to give a true

picture of the asset position of the Printery.

20

d. Profit appropriation

The management of the Printery did not have an approved formula of sharing profits

amongst the different stakeholders. Accordingly, I could not confirm whether the

30% share distributed to the University Council was in line with an approved

criterion.

Management explained that the profit sharing agreement was initially 10% and was

later increased to 30% by the Printery management. According to management, the

issue of profit sharing arises as a result of the constantly changing status of the

Printery. At the time of audit, it was a service center, which is not expected to share

profits. But when the status is later changed to that of a semi-autonomous business

unit, the Printery will formalize its profit sharing arrangements with the university.

I advised the Accounting Officer, to come up with a clear policy regarding sharing of

profits generated by the Printery, to eliminate the current ambiguity.

e. Redundant Machinery

A review of the financial statements show that the Printery has redundant machinery

with a netbook value of UGX.240,385,256 as reported in the financial statements for

2014/15. This machinery has remained redundant for more than two years.

Prolonged retention of idle assets can lead to the assets becoming obsolete. There is

also a risk of loss of assets through pilferage.

Although management explained that the disposal process had commenced, no proof

of this was availed for verification. I advised management to consider disposing all

idle assets to prevent further loss in value.

21

8.0 FINANCIAL STATEMENTS

APPENDIX 1

FINANCIAL STATEMENTS- CONSOLIDATED UNIVERSITY ACCOUNTS

22

APPENDIX 2

FINANCIAL STATEMENTS- NON CONSOLIDATED ACCOUNTS OF THE UNIVERSITY