macroeconomicdeterminantsofstockmarket ...personal.lse.ac.uk/mele/files/macrovol_slides.pdf ·...

TRANSCRIPT

Macroeconomic Determinants of Stock Market

Volatility and Volatility Risk-Premia

Valentina Corradi

University of Warwick

Walter Distaso

Imperial College Business School

Antonio Mele

London School of Economics

February 2011

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Background

• Ample evidence that stock market volatility varies over time

Introduction 1

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Post WWII Stock market volatility

1960 1965 1970 1975 1980 1985 1990 1995 2000 20050

5

10

15

20

25

30

35stock market volatility, with NBER recessions & expansions

Rolling estimates of S&P return volatility. Annualized, percent. Avg: 14.18. Avg during

expansions: 13.50 (−4%). Avg during recessions: 17.39 (+23%)

Introduction 2

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

What we do in this paper

• Develop a no-arbitrage model in which stock market volatility is explicitlyrelated to a number of macroeconomic and unobservable factors

— Stock volatility is linked to these factors through no-arbitrage restrictions— Under fairly standard conditions on the dynamics of the factors and risk-aversion corrections, our model is solved in closed-form, and is amenable toempirical work

— We use the model to quantitatively assess how volatility and volatility-relatedrisk-premia change in response to business cycle conditions∗ We do not calibrate the model. We estimate it.

Introduction 3

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

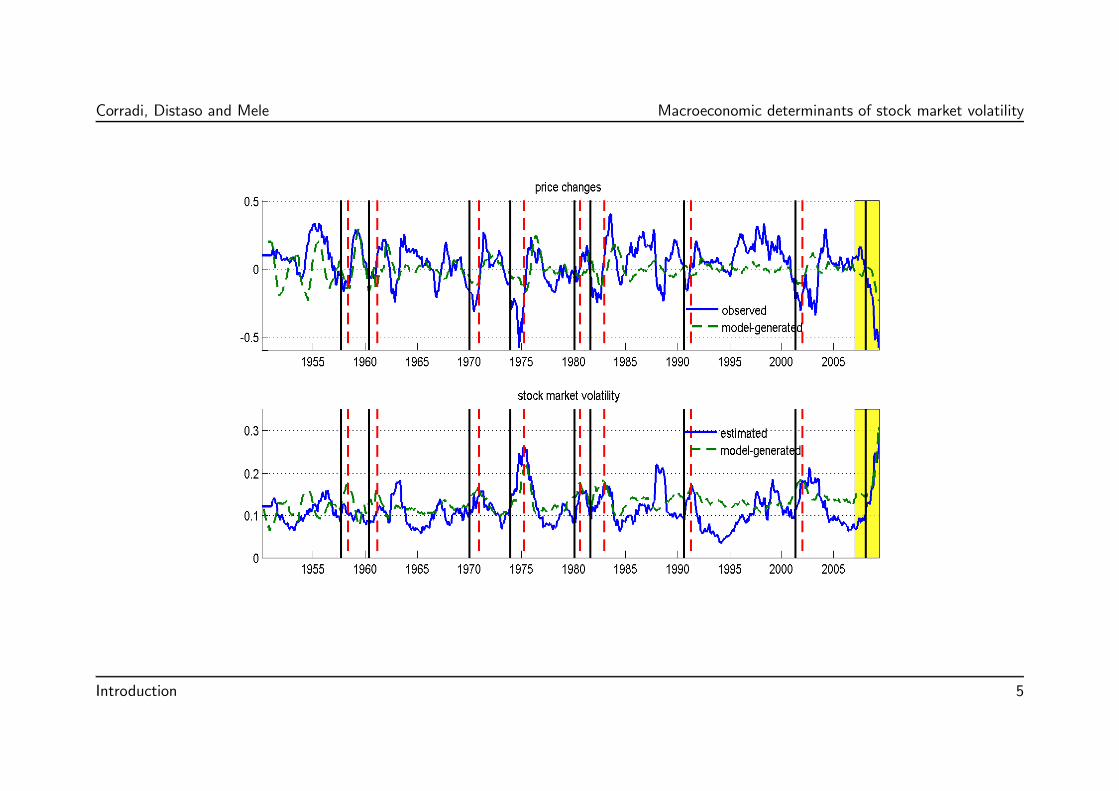

→ Model predictions

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 20050

0.05

0.1

0.15

0.2

0.25

stock market volatility

estimatedmodel−generated

Introduction 4

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Introduction 5

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Standard option pricing literature

• Empirical/statistical literature, from Mandelbrot & Fama (’60) to Engle (’80):time-varying volatility, ARCH models, stochastic volatility, Riskmetrics, etc.

• In the option pricing literature, many asset pricing models have taken on boardthis robust empirical feature

— Hull and White (1987), Heston (1993)–derivatives on stocks and currencies— (Fong and Vasicek (1991), Longstaff and Schwartz (1992)–derivatives oninterest rates)

• These models are used in everyday practice

• Theoretically though, these models inherit much the same “reduced-form”flavor as the statistical models for volatility that motivated them in the firstplace

Introduction 6

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Standard stochastic volatility models: return volatility is driven by latentfactor(s), partially correlated with asset returns.

• Leading example: Heston’s (1993) model,

dS (t)

S (t)= μdt+ σ (t) dW1 (t)

dσ2 (t) = κ(v − σ2 (t))dt+ σ (t)³ρdW1 (t) +

p1− ρ2dW2 (t)

´where S (t) is the stock price, σ (t) is the instantaneous standard deviation,W1 (t) and W2 (t) are two independent Brownian motions, μ, κ, v areconstants, and ρ is the instantaneous, constant, conditional correlation betweenasset returns and volatility.

Introduction 7

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Three key issues

(i) These latent factors do not bear a direct economic interpretation. Where doesthe volatility factor σ2 (t) come from?

(ii) Even more fundamentally, where does the stock price, S (t), come from?Shouldn’t the asset price and its volatility evolve endogenously, in equilibrium?

(iii) The model implies, by assumption, that volatility can not be forecast bymacroeconomic factors such as industrial production or inflation. But thiscircumstance is counterfactual.

Introduction 8

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Stock volatility and business cycle conditions

financial volatility and real economy

Real Industrial Production Rate (%)

Pred

icte

d vo

latil

ity (a

nnua

lized

, %)

-1.2 -0.6 0.0 0.6 1.2 1.8 2.4

4

8

12

16

20

24

28Predictive regression

Real Industrial Production Rate (%)

Pred

icte

d vo

latil

ity (a

nnua

lized

, %)

-1.2 -0.6 0.0 0.6 1.2 1.8 2.4

8

10

12

14

16

18

20

22

Introduction 9

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Volatility risk-premium

— Difference between future expected volatility under Q and P

Introduction 10

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

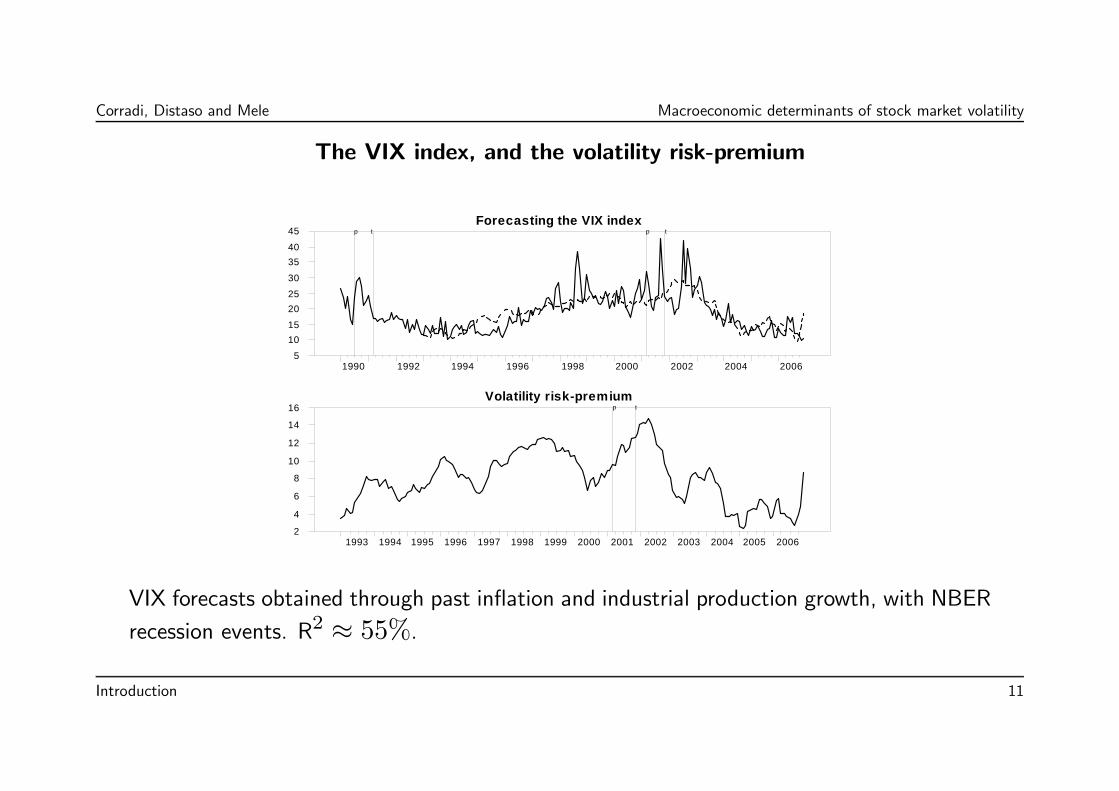

The VIX index, and the volatility risk-premium

Forecasting the VIX index

1990 1992 1994 1996 1998 2000 2002 2004 20065

1015

2025

30

3540

45 p t p t

Volatility risk-premium

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 20062

4

6

8

10

12

14

16 p t

VIX forecasts obtained through past inflation and industrial production growth, with NBER

recession events. R2 ≈ 55%.

Introduction 11

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Introduction 12

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

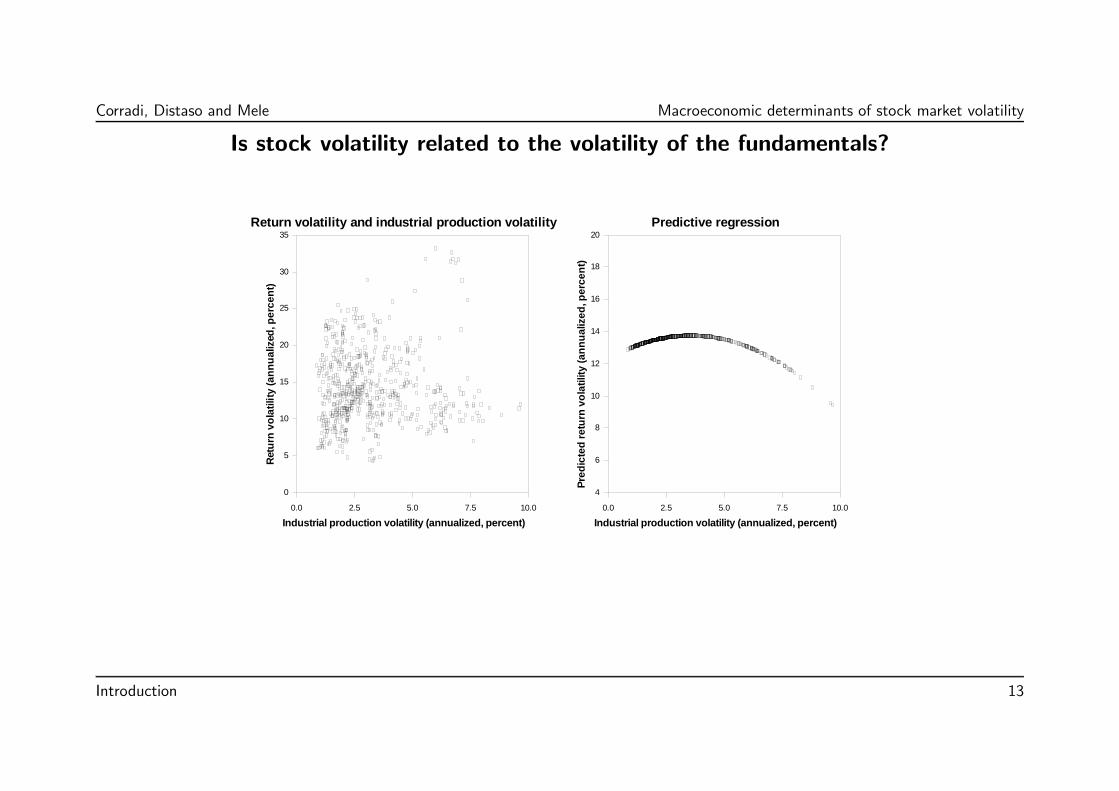

Is stock volatility related to the volatility of the fundamentals?

Return volatility and industrial production volatility

Industrial production volatility (annualized, percent)

Retu

rn v

olat

ility

(ann

ualiz

ed, p

erce

nt)

0.0 2.5 5.0 7.5 10.0

0

5

10

15

20

25

30

35Predictive regression

Industrial production volatility (annualized, percent)

Pred

icte

d re

turn

vol

atili

ty (a

nnua

lized

, per

cent

)

0.0 2.5 5.0 7.5 10.0

4

6

8

10

12

14

16

18

20

Introduction 13

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

To sum up: empirical facts and issues

• Stock market volatility is higher in bad times than in good times: It is relatedto the level of the fundamentals.

• Stock market volatility doesn’t seem to be related to the volatility of thefundamentals.

• Explaining these facts is challenging.

— As financial economists we know very well how to get started, when theobjective is to model risk-premia and/or relate these premia to the businesscycle.

— We feel more embarrassed, when it comes to explain stock market volatility.

Introduction 14

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Related literature

• Important predecessors to this paper: Bollerslev, Gibson and Zhou (2005),Bollerslev and Zhou (2005).

— Estimate the volatility risk premium, which they try to explain withmacreconomic variables

— Main difference: We determine, endogenously, return volatility, volatilityrisk premia, and their dependence on macroeconomic variables, through ano-arbitrage model

• In this paper, we do not develop a general equilibrium model.— Cross-equations restrictions arise through the weaker requirement of absenceof arbitrage opportunities

— Similar as the no-arbitrage VAR introduced by Piazzesi and her co-authorsin the yield curve literature

Introduction 15

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Outline

1/3 The model

2/3 Estimation strategy

3/3 Empirical analysis

Introduction 16

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

1/3 The model

1/3 The model 17

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Specify

— the dynamics of the macroeconomic and latent factors— asset payoff— risk premia

• “Essentially affine” model - explained below

— The resulting no-arbitrage price is an affine function of the factors

• We obtain a closed-form expression for

— Return volatility, a non-linear function of the factors

• We do not have a closed-form expression for the VIX index

— Approximate it through functional expansions

1/3 The model 18

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

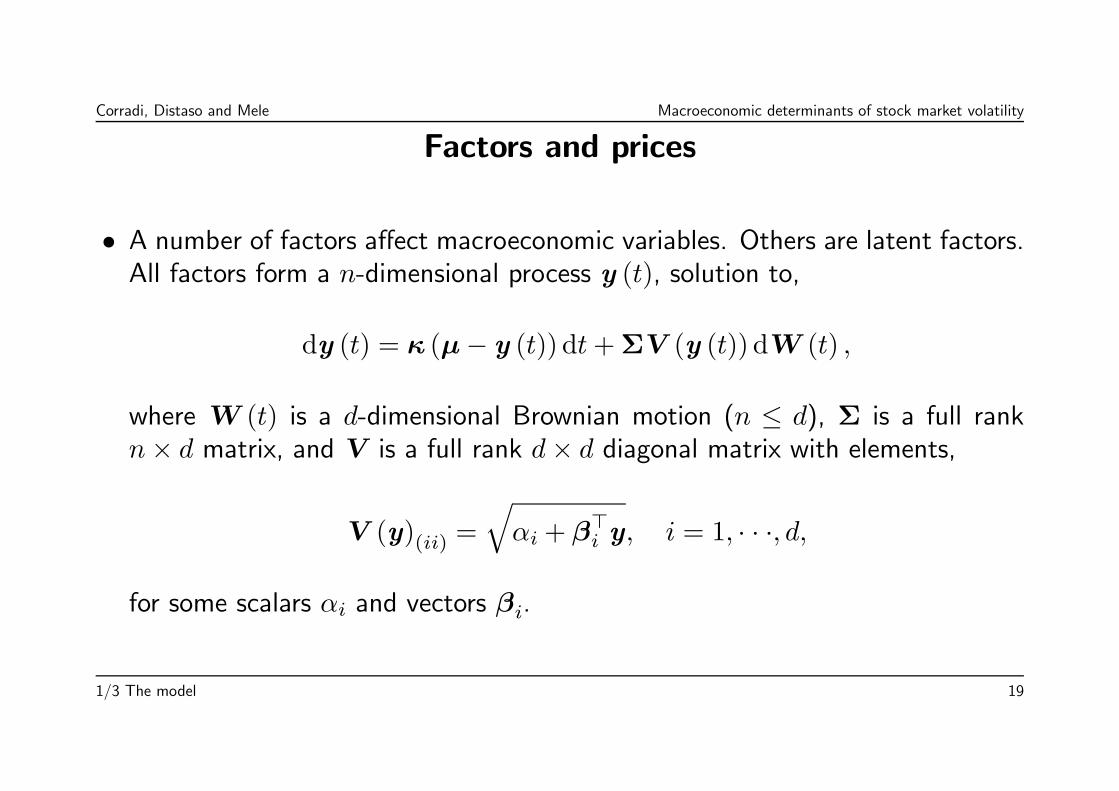

Factors and prices

• A number of factors affect macroeconomic variables. Others are latent factors.All factors form a n-dimensional process y (t), solution to,

dy (t) = κ (μ− y (t)) dt+ΣV (y (t)) dW (t) ,

where W (t) is a d-dimensional Brownian motion (n ≤ d), Σ is a full rankn× d matrix, and V is a full rank d× d diagonal matrix with elements,

V (y)(ii) =

qαi + β>i y, i = 1, · · ·, d,

for some scalars αi and vectors βi.

1/3 The model 19

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Factors

• We assume asset prices respond passively to movements in the factors affectingmacroeconomic conditions. For analytical convenience, we rule out feedbacksof asset prices to the real economy (e.g., the financial accelerator hypothesis(Bernanke, Gertler and Gilchrist, 1999))

• Formally, we assume that there exists a rational pricing function s (y (t)) suchthat the real stock price at time t, s (t) say, is s (t) ≡ s (y (t)).

— We do not study feedbacks such as s (y (t, s (·))) ≡ limn→∞ sn¡y¡t, sn−1

¢¢,

although we are currently considering such an extension - not trivial at all,in continuous time.

1/3 The model 20

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

No-arbitrage

• There is obviously no freedom in modeling risk-premia and stochastic volatilityseparately.

— Given a dividend process, volatility is uniquely determined, once we specifythe pricing kernel.

• Pricing kernel, ξ (t). We assume the short-term rate is constant, r, and therisk-premia, Λ, are functions of the state vector y:

dξ (t)

ξ (t)= −rdt−Λ (y (t)) · dW (t) .

1/3 The model 21

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

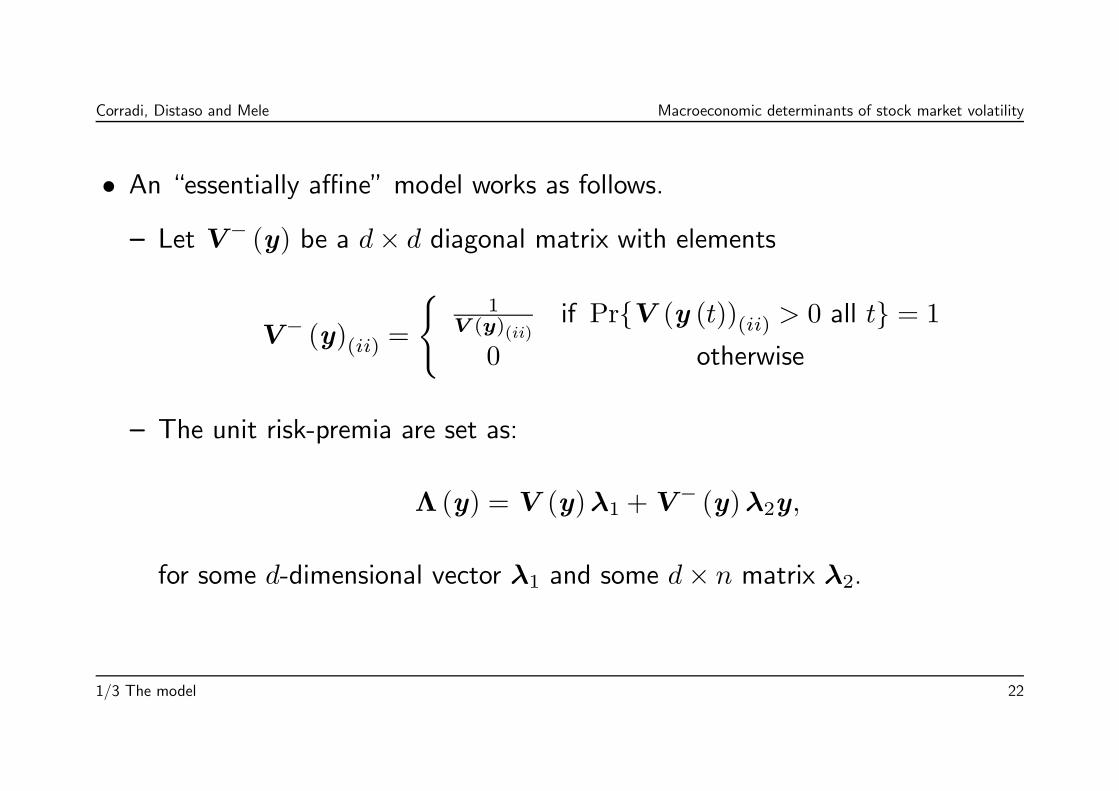

• An “essentially affine” model works as follows.

— Let V − (y) be a d× d diagonal matrix with elements

V − (y)(ii) =

(1

V (y)(ii)if Pr{V (y (t))(ii) > 0 all t} = 1

0 otherwise

— The unit risk-premia are set as:

Λ (y) = V (y)λ1 + V− (y)λ2y,

for some d-dimensional vector λ1 and some d× n matrix λ2.

1/3 The model 22

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Risk-premiaV (y) ·Λ (y) = V 2 (y)λ1 + λ2y

• If λ2 = 0d×n, the risk-premia Λ are driven by the state vector y only, throughthe volatility matrix V (y).

— While it is reasonable to assume that risk-premia are related to the volatilityof fundamentals, the previous specification of Λ is more general.

• Functional form for Λ: the same as that used by Duffee (2002) to modelthe yield curve. If the matrix, λ2 = 0d×n, then Λ collapses to the standard“completely affine” specification introduced by Duffie and Kan (1996).

1/3 The model 23

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Let (δ (y (t)))t≥0 be the instantaneous payoff to the asset. Assume,

δ (y) = δ0 + δ>y,

for some scalar δ0 and some vector δ.

• We have an easy proposition here.

1/3 The model 24

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Proposition. The rational price function s (y) is affine in the state vector y,viz

s (y) =δ0 + δ> (D + rIn×n)

−1c

r+ δ> (D + rIn×n)

−1y,

where

c = κμ−Σ¡α1λ1(1) · · · αdλ1(d)

¢>,

D = κ+Σh¡

λ1(1)β>1 · · · λ1(d)β

>d

¢>+ I−λ2

i,

I− is a d× d diagonal matrix with elements I−(ii) = 1 if Pr{V (y (t))(ii) > 0

all t} = 1 and 0 otherwise; and finally {λ1(j)}dj=1 are the components of λ1.

1/3 The model 25

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Implications

• So we have a no-arbitrage price. Stock market volatility can not be anythingwe want. In this model, it is:

σ (t) =

µ°°°δ> (D + rIn×n)−1ΣV (y (t))

°°°2¶12

δ0 + δ> (D + rIn×n)−1c

r+ δ> (D + rIn×n)

−1y (t)

• That is, volatility is restricted to change with the factors, y (t), as above.

— Stock price and volatility are endogeneous → Estimation issues.

1/3 The model 26

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

The model we estimateThree factors

• Two observable factors: industrial production and inflation. Let y1 (t) =CPI(t)

CPI(t−12) and y2 (t) =Ind.Prod(t)

Ind.Prod(t−12), with:

d

∙y1 (t)y2 (t)

¸=

∙κ1 κ1κ2 κ2

¸µ∙μ1μ2

¸−∙y1 (t)y2 (t)

¸¶dt

+

∙ pα1 + β1y1 (t) 0

0pα2 + β2y2 (t)

¸ ∙dW1 (t)dW2 (t)

¸where κ1 and κ2 are the speed of adjustment of inflation and industrialproduction growth towards their long-run means μ1 and μ2, and κ1 and κ2 arethe feedback parameters.

1/3 The model 27

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

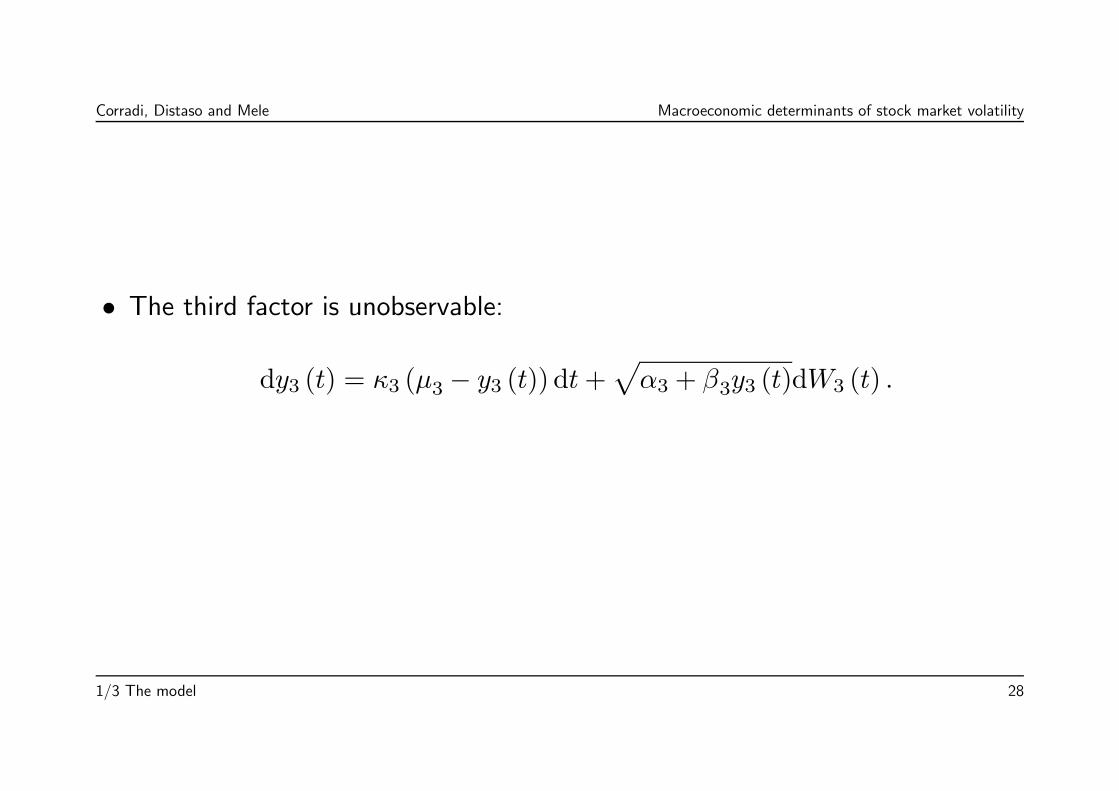

• The third factor is unobservable:

dy3 (t) = κ3 (μ3 − y3 (t)) dt+pα3 + β3y3 (t)dW3 (t) .

1/3 The model 28

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Under these conditions, the asset price is,

s (y) = s0 +3X

j=1

sjyj

s0 =1

r

⎡⎣δ0 + 3Xj=1

sj¡κjμj + κjμj − αjλ1(j)

¢⎤⎦sj =

δj¡r + κi + λ1(i)βi + λ2(i)

¢− δiκiQ2

h=1

¡r + κh + λ1(h)βh + λ2(h)

¢− κ1κ2

, for j, i ∈ {1, 2} and i 6= j

s3 =δ3

r + κ3 + λ1(3)β3 + λ2(3)

• Note, then, an important feature of the model. The parameters δi and λ(1)iand λ(2)i cannot be identified from the sole knowledge of asset price data andthe macroeconomic factors

1/3 The model 29

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

2/3 Estimation strategy

2/3 Estimation strategy 30

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

The identification problem

• Volatility does depend on macro-variables, but is endogenously determined.

— The usual approach to estimate stoch vol, doesn’t really work here.∗ Asset returns and volatility are both endogenous.· If I tilt the volatility dynamics, I am tilting the return dynamics as well,or vice-versa.

· We have to put all together to avoid endogeneity issues.— Need data on∗ macro∗ asset price∗ derivatives

2/3 Estimation strategy 31

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• We rely on a hybrid of Indirect Inference (Gourieroux, Monfort and Renault,1993) and Simulated Method of Moments (Duffie and Singleton, 1993)

— does not lead to asymptotic efficiency.

• Alternatively, we might have relied on efficient methods— Aıt-Sahalia (2008), closed-form approximations— Altissimo and Mele (2008), efficient simulated nonparametric estimator— Carrasco, Chernov, Florens and Ghysels (2007), simulated characteristicfunctions

— Fermanian and Salanie (2004), simulated nonparametric maximum likelihood— Gallant and Tauchen (1996), efficient method of moments

With these (efficient) approaches the issue of parameter estimation error(see below) becomes quite intricate, and beyond the scope of this paper.

2/3 Estimation strategy 32

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Three step procedure• First step: estimate φ|, the parameters under the physical probability for thetwo macroeconomics factors

— use data on inflation and industrial production, and match impulse-responsefunctions for these data

• Second step: estimate θ|, the parameters under the physical probability forthe stock price and the unobservable factor, for given λ|

— use data on S&P 500 only, and match impulse-response functions & momentsof ex-post returns and ex-post vol

• Third step: identify and estimate the risk-premium parameters, λ|

— use data on the VIX index, and match model-based and model-freeexpectation of volatility under Q

2/3 Estimation strategy 33

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

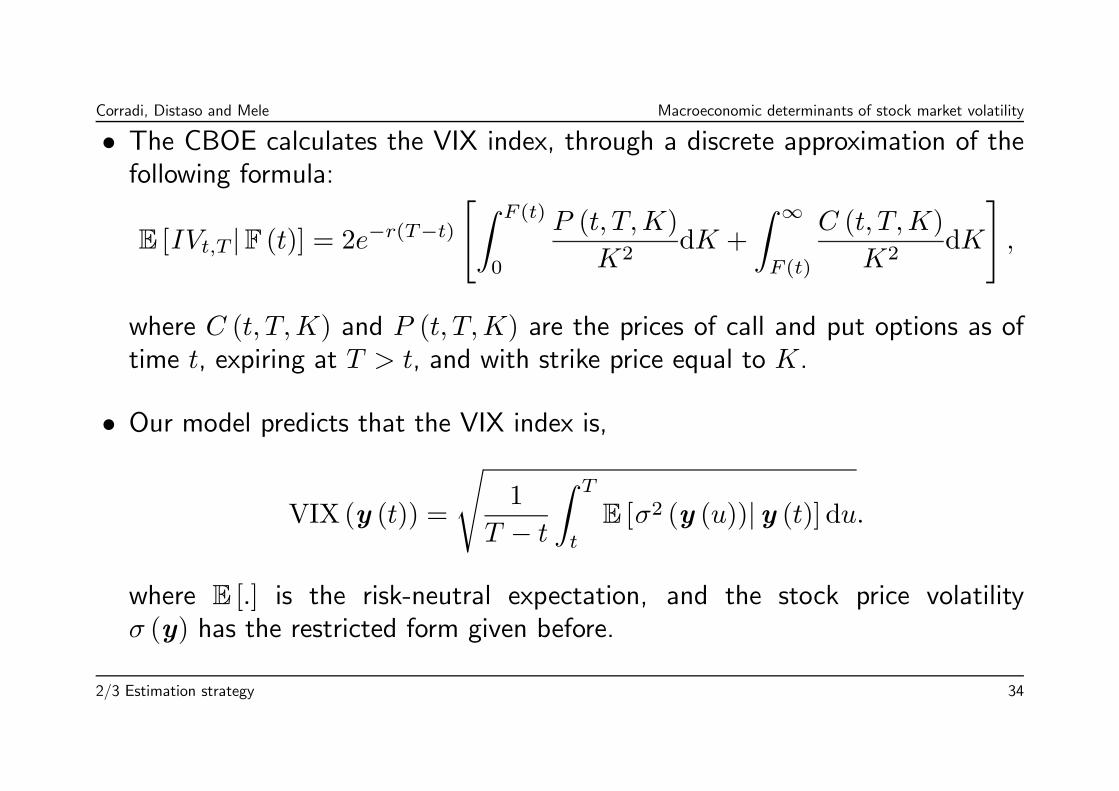

• The CBOE calculates the VIX index, through a discrete approximation of thefollowing formula:

E [IVt,T |F (t)] = 2e−r(T−t)"Z F (t)

0

P (t, T,K)

K2dK +

Z ∞F (t)

C (t, T,K)

K2dK

#,

where C (t, T,K) and P (t, T,K) are the prices of call and put options as oftime t, expiring at T > t, and with strike price equal to K.

• Our model predicts that the VIX index is,

VIX (y (t)) =

s1

T − t

Z T

t

E [σ2 (y (u))|y (t)] du.

where E [.] is the risk-neutral expectation, and the stock price volatilityσ (y) has the restricted form given before.

2/3 Estimation strategy 34

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Approximating the VIX index

• We know σ2 (y) in closed-form, not VIX (y).

— We use simulations

2/3 Estimation strategy 35

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

General ideas underlying Indirect Inference

),,( 1 Tyyy L=

);,( 1 θε ttt yfy −=

Model

Auxiliary parameter estimates )(~ θTb

ΩΘ∈

−∈ TTT bb )(~minargˆ θθθ

))(~,),(~()(~

1 θθθ Tyyy L=

Model-simulated data

Estimation of an auxiliary model on model-simulated data

Observed data

Auxiliary parameter estimates

Tb

Estimation of the

same auxiliary model on observed data

Indirect Inference Estimator

2/3 Estimation strategy 36

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

First step: Moment conditions for the macroeconomic factors

• Auxiliary models. Remember, φ| is the parameter vector for the processunderlying the macroeconomic factors.

• We estimate the following autoregressive models on both historical andsimulated data, for i = 1, 2,

yi,t = ϕi,0 +X

j∈{12,24}ϕi,1,jy1,t−j +

Xj∈{12,24}

ϕi,2,jy2,t−j + i,t, (1)

and

yhi,t (φ) = ϕi,0,h+X

j∈{12,24}ϕi,1,j,h·yh1,t−j (φ)+

Xj∈{12,24}

ϕi,2,j,h·yh2,t−j (φ)+ hi,t,

(2)where yh1,t (φ) is the h-th simulation of the t-th observation of the first factor,obtained using the deep parameter φ.

2/3 Estimation strategy 37

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

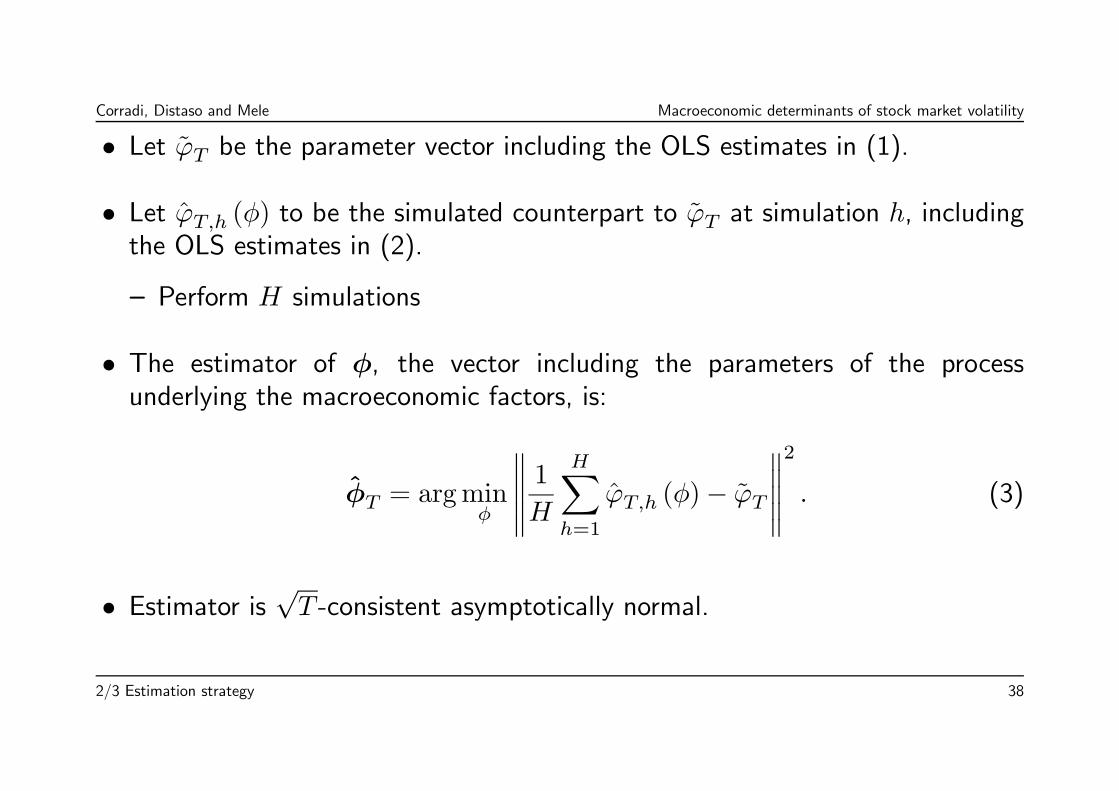

• Let ϕT be the parameter vector including the OLS estimates in (1).

• Let ϕT,h (φ) to be the simulated counterpart to ϕT at simulation h, includingthe OLS estimates in (2).

— Perform H simulations

• The estimator of φ, the vector including the parameters of the processunderlying the macroeconomic factors, is:

φT = argminφ

°°°°° 1HHXh=1

ϕT,h (φ)− ϕT

°°°°°2

. (3)

• Estimator is√T -consistent asymptotically normal.

2/3 Estimation strategy 38

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

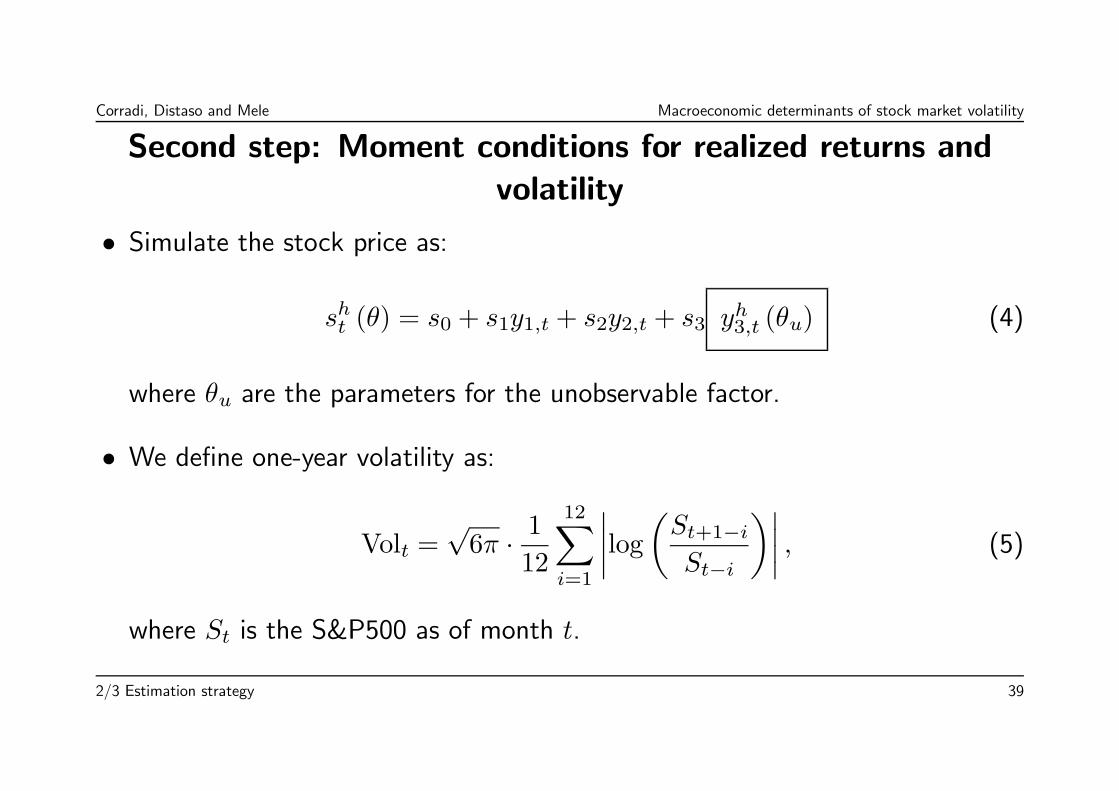

Second step: Moment conditions for realized returns andvolatility

• Simulate the stock price as:

sht (θ) = s0 + s1y1,t + s2y2,t + s3 yh3,t (θu) (4)

where θu are the parameters for the unobservable factor.

• We define one-year volatility as:

Volt =√6π · 1

12

12Xi=1

¯log

µSt+1−iSt−i

¶¯, (5)

where St is the S&P500 as of month t.

2/3 Estimation strategy 39

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Our estimator relies on the following two auxiliary models:

Rt = aR + bR1,12y1,t−12 + bR2,12y2,t−12 +Rt , (6)

where Rt = log (St/St−12), and

Volt = aV +X

i∈{6,12,18,24,36,48}φiVolt−i+ (7)

Xi∈{12,24,36,48}

bV1,iy1,t−i +X

i∈{12,24,36,48}bV2,iy2,t−i +

Vt .

2/3 Estimation strategy 40

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Let ϑT be the parameter vector containing the OLS estimates in (6) and (7).

• Let ϑT,h (θ) be the simulated counterpart to ϑT at simulation h.

• The estimator of θ, the vector including the parameters of the reduced-formparameters sj and the process of the unobservable factor, is:

θT = argminθ

°°°°° 1HHXh=1

ϑT,h (θ)− ϑT

°°°°°2

. (8)

• Estimator is√T -consistent asymptotically normal.

— Note, we achieve a gain in efficiency, as we are using sample data for y1,tand y2,t.

2/3 Estimation strategy 41

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

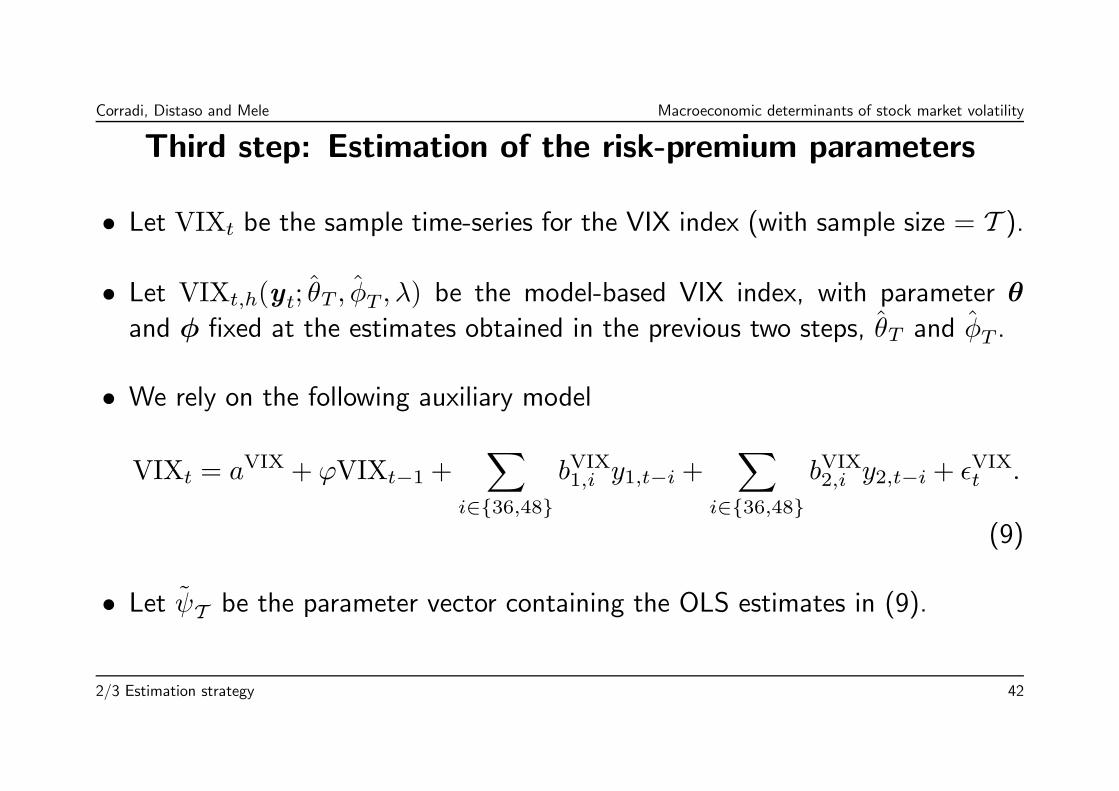

Third step: Estimation of the risk-premium parameters

• Let VIXt be the sample time-series for the VIX index (with sample size = T ).

• Let VIXt,h(yt; θT , φT , λ) be the model-based VIX index, with parameter θ

and φ fixed at the estimates obtained in the previous two steps, θT and φT .

• We rely on the following auxiliary model

VIXt = aVIX + ϕVIXt−1 +X

i∈{36,48}bVIX1,i y1,t−i +

Xi∈{36,48}

bVIX2,i y2,t−i +VIXt .

(9)

• Let ψT be the parameter vector containing the OLS estimates in (9).

2/3 Estimation strategy 42

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Let ψT ,h(θT , φT , λ) be the simulated counterpart to ψT , at simulation h.

— Obtained through simulations of the model-implied indexVIXt,h(yt; θT , φT , λ),with y1,t and y2,t fixed at their sample values.

The estimator of λ, the parameters underlying the risk-premium process, is:

λT = argminλ

°°°°° 1HHXh=1

ψT ,h(φT , θT , λ)− ψT

°°°°°2

. (10)

• Estimator is√T -consistent asymptotically normal.

— Again, we achieve an efficiency gain, as we are using sample data for y1,tand y2,t.

2/3 Estimation strategy 43

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Issues

• One, the new CBOE VIX index is available only since 1990, and so in the thirdstep, we use a sample of length T , with T < T . Asymptotics are a bit moreinvolved, but under regularity conditions, the estimator is still

√T -consistent

asymptotically normal.

• Two, parameter estimation error, as we simulate the VIX index withVIXt,h(yt; θT , φT , λ), where θT and φT are obtained in the previous steps.

— our std errors account for parameter estimation error

• In the previous 3-step procedure, we do not have closed-form expressions forthe variance-covariance matrix.

— Bootstrap the data, and show theoretically that the bootstrap work.— Simulations (the bootstrap) within simulations (indirect inference).

2/3 Estimation strategy 44

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

3/3 Empirical analysis

I: Stylized facts

II: Model’s predictions

3/3 Empirical analysis 45

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

3/3 Empirical analysis I:

Stylized facts

3/3 Empirical Analysis I: Stylized facts 46

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

First moments prediction

To save on notation, let us ignore feedback effects (y1 (t) ⊥ y2 (t)).

Our model, then, predicts that,⎡⎣ E (y1 (t)− y1 (t− 12)|F (t− 12))E (y2 (t)− y2 (t− 12)|F (t− 12))E (s (t)− s (t− 12)|F (t− 12))

⎤⎦=

⎡⎣¡1− e−12κ1

¢μ1¡

1− e−12κ2¢μ2P3

j=1 sj¡1− e−12κj

¢μj

⎤⎦−⎡⎣

¡1− e−12κ1

¢y1 (t− 12)¡

1− e−12κ2¢y2 (t− 12)P3

j=1 sj¡1− e−12κj

¢yj (t− 12)

⎤⎦ ,where sj are functions of the deep parameters of the model.

3/3 Empirical Analysis I: Stylized facts 47

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Return predictability and the business cycle

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000-60

-40

-20

0

20

40

60

S&P Returnst = 14.64(1.08)

− 9.09(1.22)

·Growtht−12 − 14.27(2.44)

·Inflt−12 +Residt

Standard errors in parenthesis / Centered R2 = 11%

These basic pieces of evidence are, of course, consistent with predictability

3/3 Empirical Analysis I: Stylized facts 48

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

What about *volatility* predictability?

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 20000

5

10

15

20

25

30

35

S&P return volatility

3/3 Empirical Analysis I: Stylized facts 49

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Forecasting stock market volatility with economic activity

Past Future

Const. 6.92 7.76 2.48 Const. 8.28

Growtht−12 — 0.29∗ 1.67 Growtht+12 0.21∗

Growtht−24 — 0.74 1.09 Growtht+24 1.62

Growtht−36 — 2.17 2.44 Growtht+36 −0.02∗Growtht−48 — 1.77 1.91 Growtht+48 0.12∗

Inflt−12 — 10.44 8.05 Inflt+12 3.55

Inflt−24 — −5.96 −5.49 Inflt+24 −0.81∗Inflt−36 — −1.42∗ −0.97 Inflt+36 −0.54∗Inflt−48 — 3.73 3.31 Inflt+48 4.33

Volt−12 0.43 — 0.37 R2 12.79

Volt−24 −0.17 — −0.09Volt−36 0.02∗ — 0.09

Volt−48 0.12 — 0.09

R2 16.38 26.01 34.52

3/3 Empirical Analysis I: Stylized facts 50

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

What about the VIX predictability?

Forecasting the VIX index with macroeconomic indicators

1990 1992 1994 1996 1998 2000 2002 2004 20065

10

15

20

25

30

35

40

45 p t p t

3/3 Empirical Analysis I: Stylized facts 51

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Forecasting the VIX index with economic activity

Past Future

Const. 2.60∗ 30.15 3.03∗ Const. 25.53

Growtht−1 — −5.12 0.51∗ Growtht+1 25.53

Growtht−12 — −3.69∗ −0.35∗ Growtht+12 −5.58Growtht−24 — 4.91 3.69 Growtht+24 −8.34Growtht−36 — 11.19 4.33 Growtht+36 −9.67Inflt−1 — −26.96 −9.14∗ Inflt+1 1.04∗

Inflt−12 — −22.62 −1.89∗ Inflt+12 −24.11Inflt−24 — −1.59∗ 5.85∗ Inflt+24 9.32∗

Inflt−36 — −6.02∗ −2.56∗ Inflt+36 20.71

VIXt−1 0.72 — 0.55 R2 55.04

VIXt−12 0.18 — 0.14∗

VIXt−24 −0.06∗ — −0.01∗VIXt−36 0.02∗ — 0.12∗

R2 66.87 54.12 71.03

3/3 Empirical Analysis I: Stylized facts 52

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Volatility risk-premia?

Volatility risk-premium

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 20060

5

10

15

20

25 p t

This is a very rough, preliminary estimate

3/3 Empirical Analysis I: Stylized facts 53

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Bottom line

Our model must be able to explain these stylized facts

We now turn to the performance of the model

3/3 Empirical Analysis I: Stylized facts 54

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

3/3 Empirical analysis II:

Model’s predictions

3/3 Empirical Analysis II: Model’s predictions 55

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Data

• Capital markets— S&P Compounded index (1950:01 - 2006:12)— VIX index.∗ Data for the VIX index are available daily, but only for the period followingJanuary 1990.∗ Information related to the CPI and the IP is made available to the marketbetween the 19th and the 23th of every month. Thus, to possibly avoidoverreaction to releases of information, we sample the S&P Compoundedindex and the VIX index every 25th of the month.

• Macroeconomic data— Gross inflation (1950:01 - 2006:12)— Gross industrial production growth (1950:01 - 2006:12)

3/3 Empirical Analysis II: Model’s predictions 56

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Inputs: the macroeconomic factors

3/3 Empirical Analysis II: Model’s predictions 57

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

First step: macroeconomic factors

Model:∙dy1 (t)dy2 (t)

¸=

∙κ1 κ1κ2 κ2

¸ ∙μ1 − y1 (t)μ2 − y2 (t)

¸dt+

∙ pα1 + β1y1 (t)dW1 (t)pα2 + β2y2 (t)dW2 (t)

¸

Estimate Std error

κ1 0.0331 3.4630·10−4μ1 1.0379 3.4855·10−3α1 2.2206·10−4 2.7607·10−6β1 −9.6197·10−7 1.0099·10−8κ2 0.5344 7.4482·10−3μ2 1.0415 4.9926·10−3α2 0.0540 3.5233·10−4β2 −0.0497 3.3939·10−4κ1 −0.2992 4.3054·10−3κ2 1.2878 1.8091·10−2

3/3 Empirical Analysis II: Model’s predictions 58

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

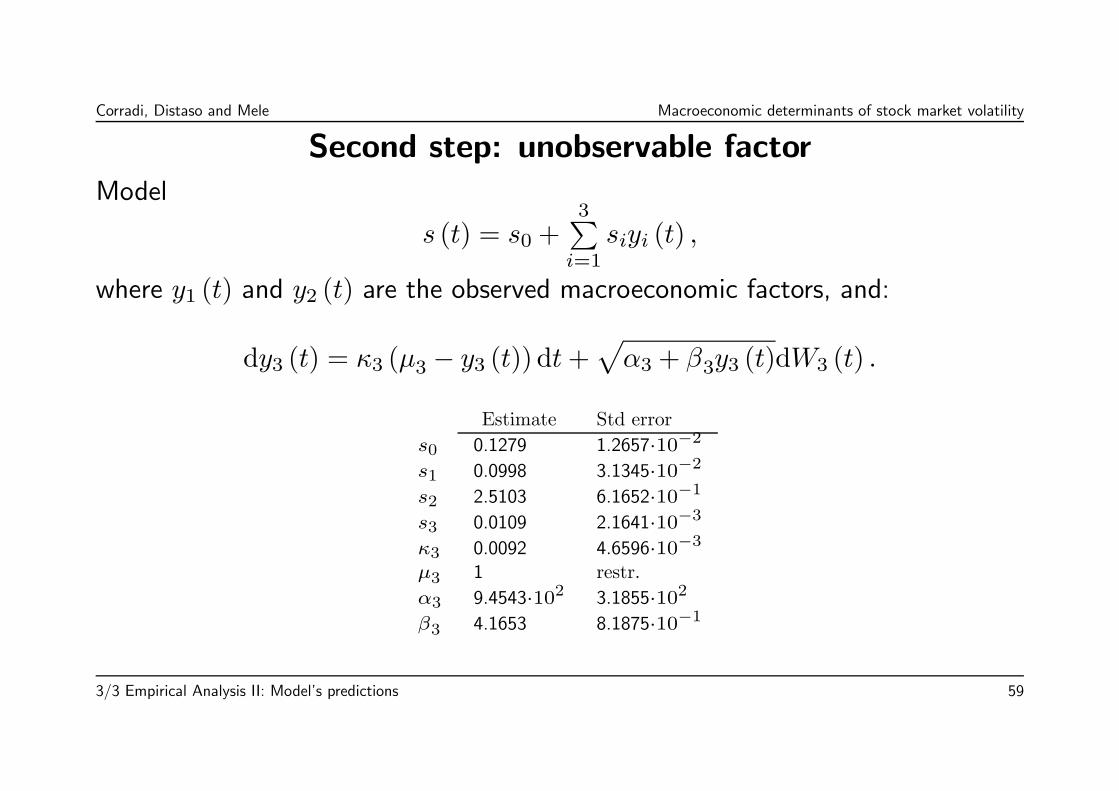

Second step: unobservable factor

Model

s (t) = s0 +3P

i=1siyi (t) ,

where y1 (t) and y2 (t) are the observed macroeconomic factors, and:

dy3 (t) = κ3 (μ3 − y3 (t)) dt+pα3 + β3y3 (t)dW3 (t) .

Estimate Std error

s0 0.1279 1.2657·10−2s1 0.0998 3.1345·10−2s2 2.5103 6.1652·10−1s3 0.0109 2.1641·10−3κ3 0.0092 4.6596·10−3μ3 1 restr.

α3 9.4543·102 3.1855·102β3 4.1653 8.1875·10−1

3/3 Empirical Analysis II: Model’s predictions 59

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

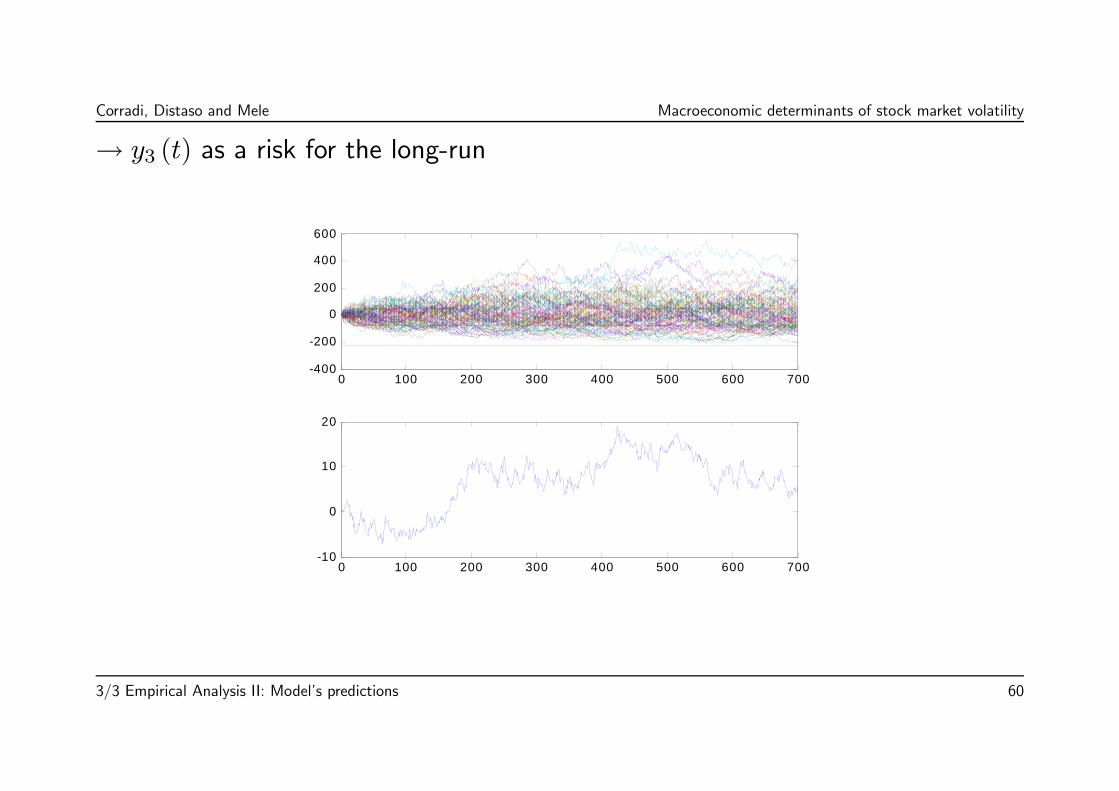

→ y3 (t) as a risk for the long-run

0 100 200 300 400 500 600 700-400

-200

0

200

400

600

0 100 200 300 400 500 600 700-10

0

10

20

3/3 Empirical Analysis II: Model’s predictions 60

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Third step: risk-premiaRisk-premia processes:

π1 (y1 (t)) = α1λ1(1) +¡β1λ1(1) + λ2(1)

¢y1 (t) (inflation)

π2 (y2 (t)) = α2λ1(2) +¡β2λ1(2) + λ2(2)

¢y2 (t) (industrial production)

π3 (y3 (t)) = α3λ1(3) +¡β3λ1(3) + λ2(3)

¢y3 (t) (unobservablef factor)

Estimate Std errorInflationλ1(1)λ2(1)

6.4605−0.1159

2.20120.0109

Ind. Prod.λ1(2)λ2(2)

53.68632.6201

6.46050.6845

Unobs.λ1(3)λ2(3)

2.20793.7559

0.94621.1159

3/3 Empirical Analysis II: Model’s predictions 61

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Predictions of the model

• We feed the model with macroeconomic data only (inflation and industrialproduction) and average over the unobserved factor through 1000 dynamicsimulations.

3/3 Empirical Analysis II: Model’s predictions 62

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Price changes predicted by the model

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005−0.4

−0.3

−0.2

−0.1

0

0.1

0.2

0.3

0.4

0.5price changes

3/3 Empirical Analysis II: Model’s predictions 63

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Price changes: Data vs model

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

−0.5

−0.4

−0.3

−0.2

−0.1

0

0.1

0.2

0.3

0.4

0.5price changes

observedmodel−generated (average)

3/3 Empirical Analysis II: Model’s predictions 64

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

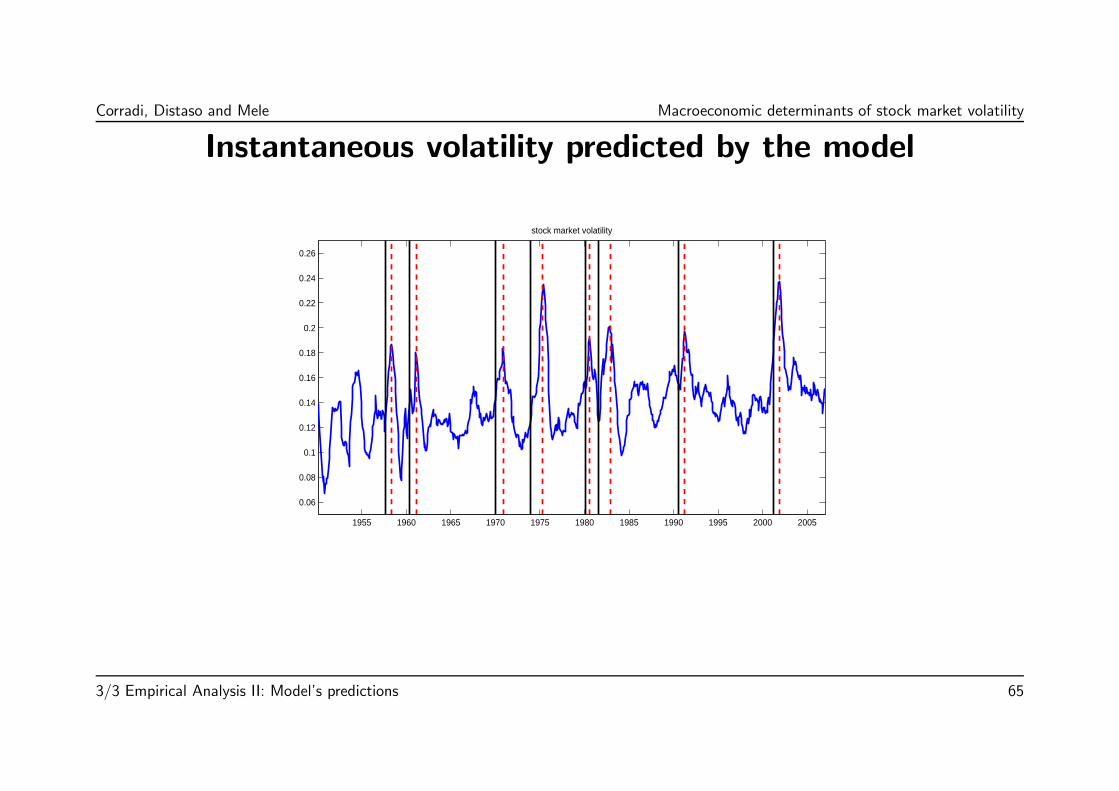

Instantaneous volatility predicted by the model

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0.22

0.24

0.26

stock market volatility

3/3 Empirical Analysis II: Model’s predictions 65

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Volatility: Data vs model

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 20050

0.05

0.1

0.15

0.2

0.25

stock market volatility

estimatedmodel−generated

3/3 Empirical Analysis II: Model’s predictions 66

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Big picture: Returns and volatility

3/3 Empirical Analysis II: Model’s predictions 67

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Decomposition

Percentage reductions in stock volatility and vol of vol

average std devwithout y1 ≈ 0 ≈ 0without y2 11% 78%without y3 69% −95%

• Shut down the gross inflation channel, y1.

— No sizeable effects → inflation seems to play a quite marginal role as adeterminant of stock market volatility, and its cyclical properties.

• Industrial production growth plays a quite important role.

3/3 Empirical Analysis II: Model’s predictions 68

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

— Fixing y2,t at its long run mean leads to about a 10% reduction in theaverage level of volatility

— The third unobservable factor is key in explaining the level of stock volatility∗ when y3,t is taken out of the picture, the average level of volatility dropsby nearly 70%.

— industrial production is needed to explain the cyclical swings of stockvolatility that we observe in the data.∗ When y2,t is frozen, the standard deviation of the model-implied stockvolatility drops dramatically to 78%.∗ When, instead, y3,t is frozen, we even observe an increase in the variabilityof stock volatility, of about 95%.

3/3 Empirical Analysis II: Model’s predictions 69

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Freezing the unobserved factor, y3

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 20050

0.05

0.1

stock market volatility

3/3 Empirical Analysis II: Model’s predictions 70

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Freezing the macroeconomic factors

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 20050

0.05

0.1

0.15

0.2

0.25

stock market volatility

estimatedmodel−generated

3/3 Empirical Analysis II: Model’s predictions 71

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

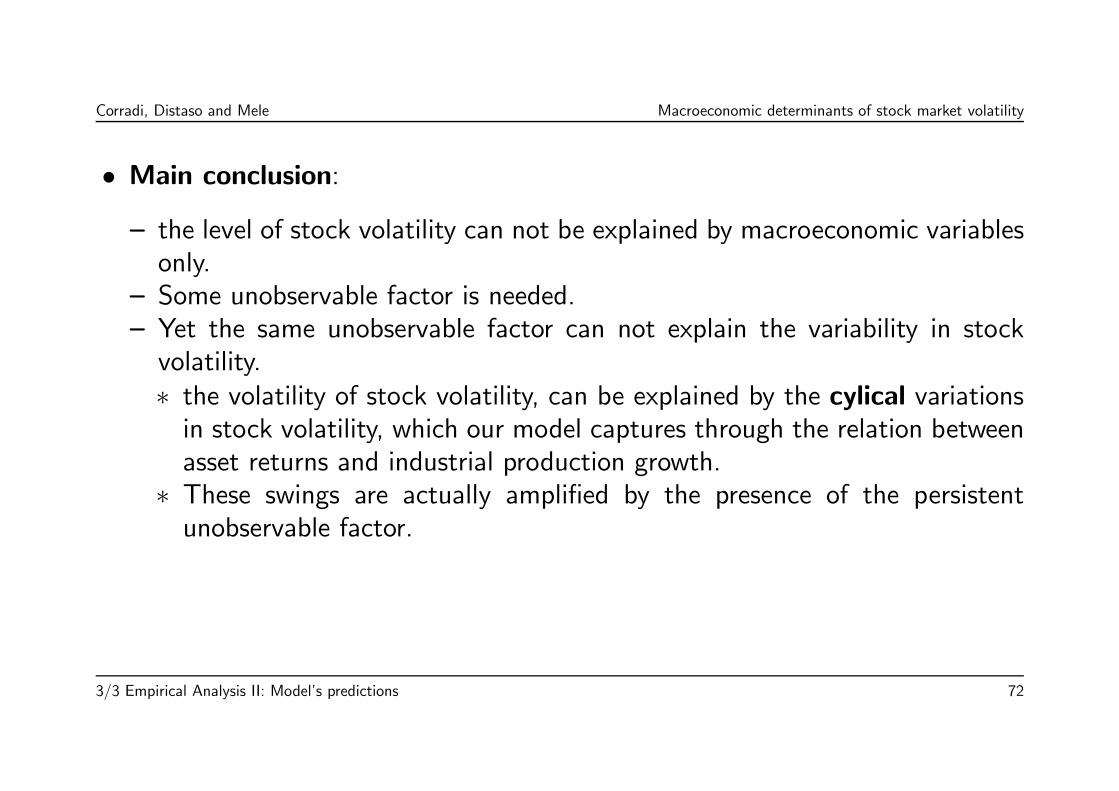

• Main conclusion:

— the level of stock volatility can not be explained by macroeconomic variablesonly.

— Some unobservable factor is needed.— Yet the same unobservable factor can not explain the variability in stockvolatility.∗ the volatility of stock volatility, can be explained by the cylical variationsin stock volatility, which our model captures through the relation betweenasset returns and industrial production growth.∗ These swings are actually amplified by the presence of the persistentunobservable factor.

3/3 Empirical Analysis II: Model’s predictions 72

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Next, the VIX index, and the volatility risk-premia

Remember,

• The VIX index predicted by the model is,r1

T − t

rE³R T

tσ2 (y (u)) du

¯y (t)

´,

where T − t = 12−1, E is the conditional expectation under the risk-neutralprobability, σ2 (y) is the instantaneous variance predicted by the model, andy is the vector of three factors: (i) inflation, (ii) industrial production growth,and (iii) one unobservable factor, obtained through 1000 dynamic simulations.

3/3 Empirical Analysis II: Model’s predictions 73

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

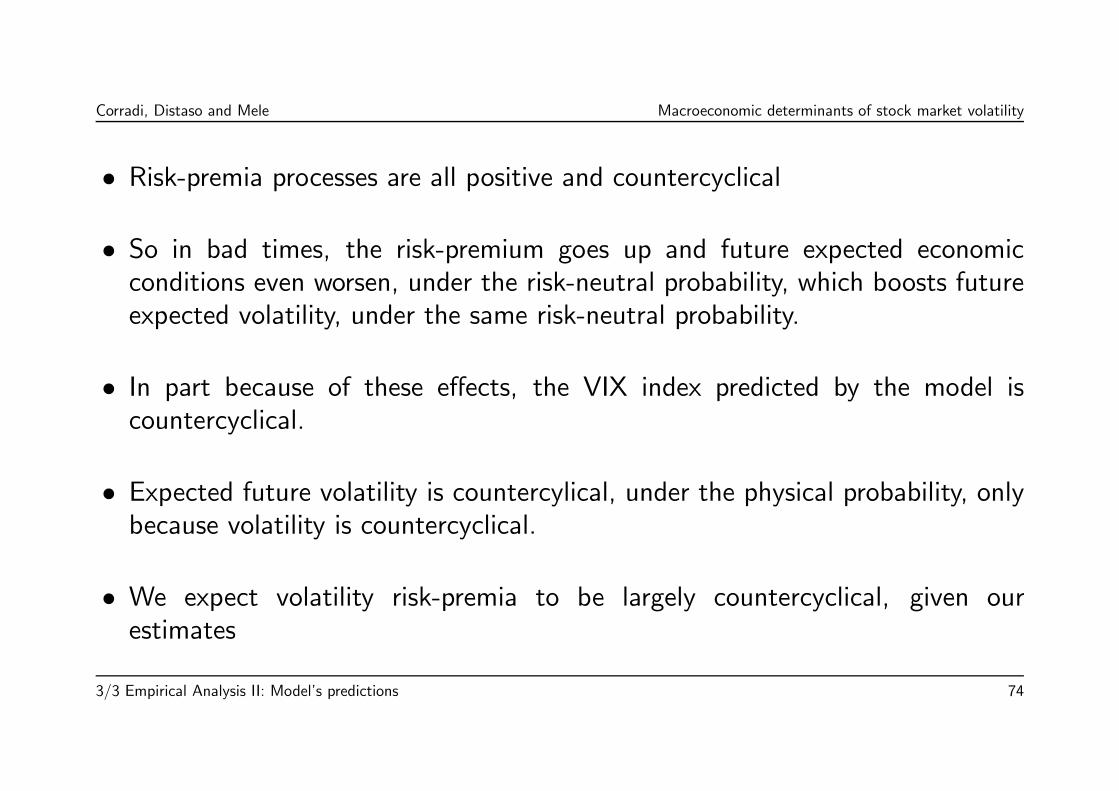

• Risk-premia processes are all positive and countercyclical

• So in bad times, the risk-premium goes up and future expected economicconditions even worsen, under the risk-neutral probability, which boosts futureexpected volatility, under the same risk-neutral probability.

• In part because of these effects, the VIX index predicted by the model iscountercyclical.

• Expected future volatility is countercylical, under the physical probability, onlybecause volatility is countercyclical.

• We expect volatility risk-premia to be largely countercyclical, given ourestimates

3/3 Empirical Analysis II: Model’s predictions 74

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• The volatility risk-premium predicted by the model is,

VRP(y (t)) ≡1

T − tE T

t σ2 (y (u)) du y (t) − ETt σ2 (y (u)) du y (t) ,

where E is the conditional expectation under the physical probability.

3/3 Empirical Analysis II: Model’s predictions 75

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Results

3/3 Empirical Analysis II: Model’s predictions 76

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

The Risk Neutral tilt:Reading business cycle expectations from the VIX index

0 0.2 0.4 0.6 0.8 10.99

1

1.01

1.02

1.03

1.04

1.05

1.06

1.07

1.08

1.09IP growth: time path under P (one month)

0 0.2 0.4 0.6 0.8 10.55

0.6

0.65

0.7

0.75

0.8

0.85

0.9

0.95

1

1.05IP growth: time path under Q (one month)

3/3 Empirical Analysis II: Model’s predictions 77

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

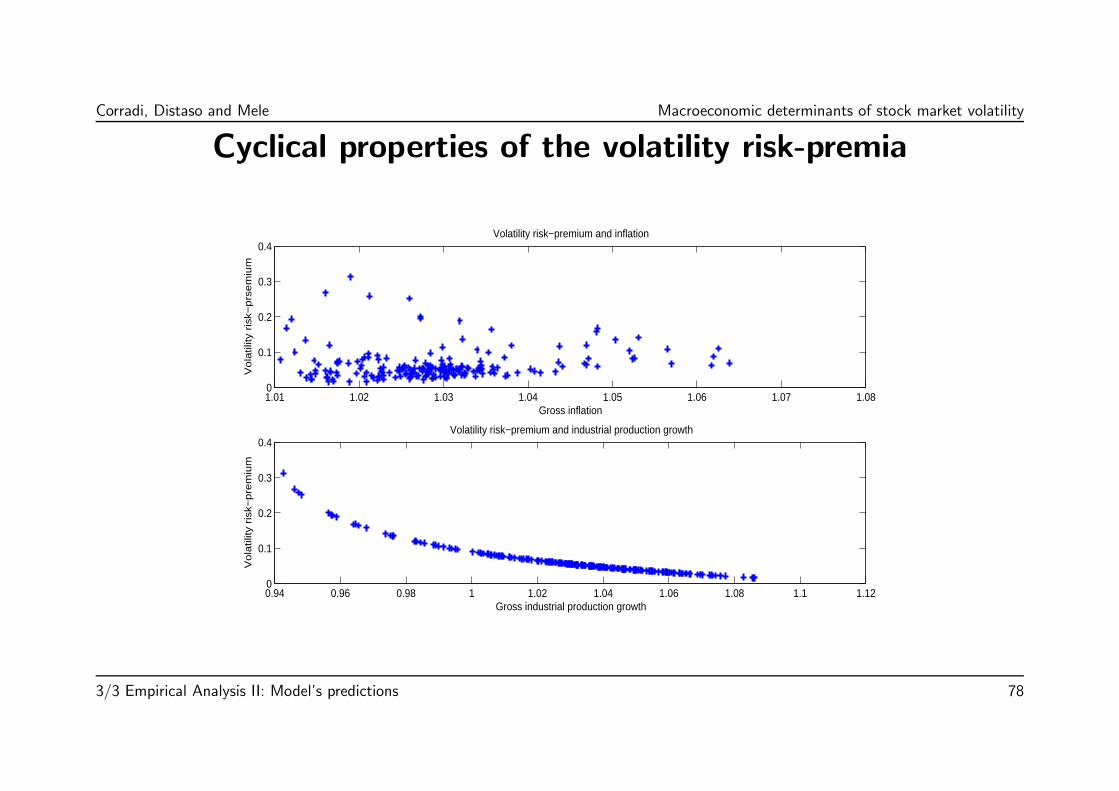

Cyclical properties of the volatility risk-premia

1.01 1.02 1.03 1.04 1.05 1.06 1.07 1.080

0.1

0.2

0.3

0.4Volatility risk−premium and inflation

Gross inflation

Vola

tility

ris

k−prs

em

ium

0.94 0.96 0.98 1 1.02 1.04 1.06 1.08 1.1 1.120

0.1

0.2

0.3

0.4Volatility risk−premium and industrial production growth

Gross industrial production growth

Vola

tility

ris

k−pre

miu

m

3/3 Empirical Analysis II: Model’s predictions 78

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

Conclusion

Conclusions 79

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Analyzes how stock market volatility and volatility risk-premia relate to thedevelopment of the business cycle.

— No-arbitrage: returns and volatility are endogeneous— Delicate identification issues

• Measurement methodology: Combined use of macroeconomic factors and risk-adjusted measures of stock price volatility — the VIX Index

• Statistical inference

Conclusions 80

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

• Main messages,

— The level of stock market volatility stems from some quite persistentunobservable factor.

— This unobservable factor, alone, can not explain the rich dynamics ofvolatility - only (and partially) its level.

— The business cycle is largely responsible for the random fluctuations of stockvolatility around its level

— Volatility risk-premia are countercyclical, certainly more so than stockvolatility alone.∗ Such a countercyclical behavior arises because the risk-compensation forthe fluctuation in the macroeconomic factors is large and countercyclical∗ These aspects might make the volatility premium anticipate thedevelopment of the business cycle in bad times.

Conclusions 81

Corradi, Distaso and Mele Macroeconomic determinants of stock market volatility

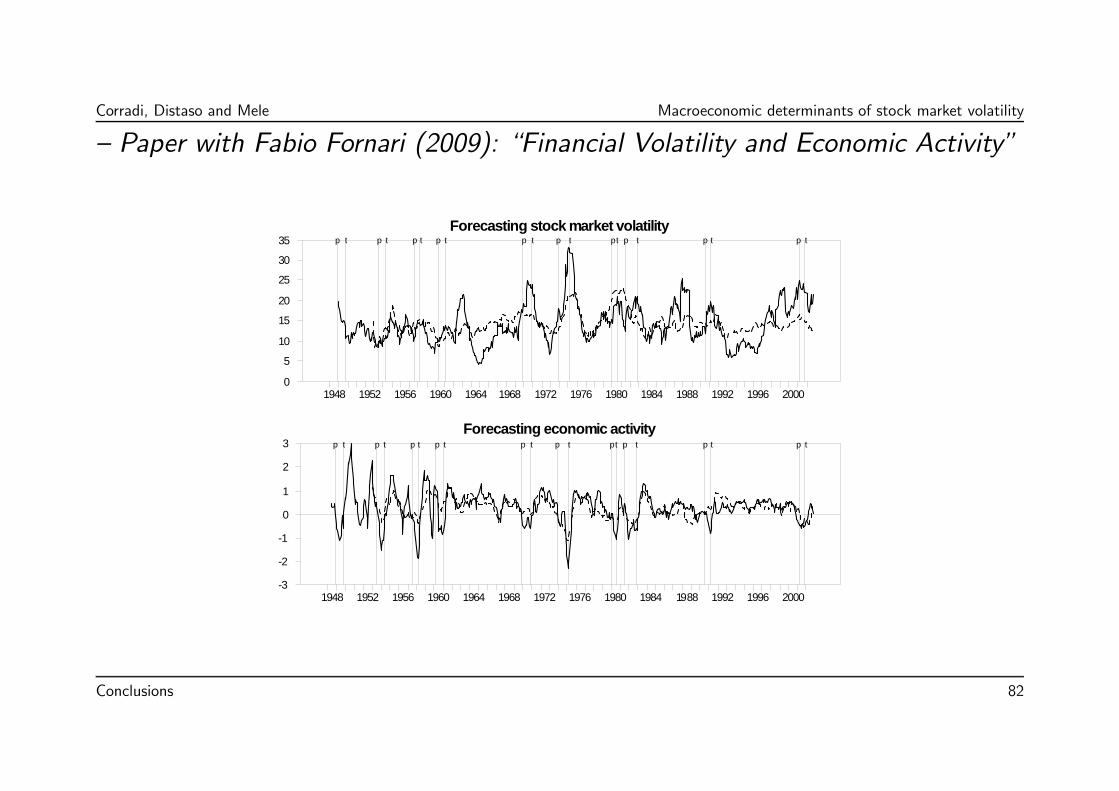

— Paper with Fabio Fornari (2009): “Financial Volatility and Economic Activity”

Forecasting stock market volatility

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 20000

5

10

15

20

25

30

35 p t p t p t p t p t p t pt p t p t p t

Forecasting economic activity

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000-3

-2

-1

0

1

2

3 p t p t p t p t p t p t pt p t p t p t

Conclusions 82