macro 3q themes - docs.hedgeye.com

TRANSCRIPT

MACRO 3Q THEMES 11 JULY 2012

DISCLAIMER • Hedgeye Risk Management is not a broker dealer and does not make investment

recommendations. This presentation does not constitute an offer to sell, or a solicitation of an offer to buy any security.

• This research is presented without regard to individual investment preferences or risk parameters; it is general information and does not constitute specific investment advice.

• This presentation is based on information from sources believed to be reliable. Hedgeye Risk Management is not responsible for errors, inaccuracies or omissions of information.

• For more information, including Terms of Use of our information, please go to www.hedgeye.com

© 2012 Hedgeye Risk Management LLC All rights reserved.

2

2Q 2012 Themes Recap

• LAST WAR; FED FIGHTING: We take a historical look at U.S. Federal Reserve policy to contextualize the impact of Ben Bernanke's Policy to Inflate, Extend & Pretend rock-bottom interest rates, and Burn the Buck on the broader economy and financial markets from Main Street to Wall Street.

• BERNANKE’S BUBBLES: A highlight of the top ten leverage price bubble charts perpetuated and encouraged by The Bernank's policy stance.

• ASYMMETRIC RISKS: In a macro environment of slow global growth and historically low interest rates we present asymmetric risks to capitalize on over the intermediate term. Low equity market volatility is but one signal of what's ahead for investors.

3

“UNDER CAPITALISM, MAN EXPLOITS MAN. UNDER COMMUNISM IT’S JUST THE OPPOSITE.”

-JOHN KENNETH GALBRAITH

4

GROWTH SLOWING’S SLOPE

3Q 2012

GROWTH SLOWING’S SLOPE

5

Consensus Growth Estimates Are Still Too High

6

Other Than Japan, Global Growth’s Slope Is Going The Wrong Way

7

The Domestic Job Market Is Hampering Growth (And Equities) In The U.S.

8

Is This Q3 of 2008? The Treasury Yield Spread (10s To 2s) Says Yes!

9

Long-Term, The Question Remains – Will The Yield Spread Mean Revert To Zero?

10

The Doctor Agrees – Why Not Copper $1.50 - $2.00/lb?

11

And Gentleman Who Prefer Bonds Are Getting Paid By #GrowthSlowing

12

Why Not $60 Oil? Brent Remains In A Bearish Formation

13

$60 Oil Would Be Great For The 71% = Huge Consumption Growth Tailwind

14

But, In The Short Run, We Are Not All Dead Yet

15

All The While, Gold Is On Life Support – Is The Fed Out of Bullets?

16

THE CLIFF

3Q 2012 THE CLIFF

17

The 112th Congress Created A Spending Cliff in 2013 . . .

• On August 2, 2011, the United States public debt was projected to meet its statutory limit

• The advent of the Tea Party led to a showdown over what had been formerly a routine course of action in increasing the debt ceiling

• Ultimately, a compromise was reached via the Budget Control Act of 2011: If Congress failed to act and produce a deficit reduction bill of at least $1.2

trillion in cuts, then Congress could grant a $1.2 trillion increase in the debt ceiling, but this would trigger “sequestration”

Across the board cuts of $1.2 trillion split between security and non-security from 2013 to 2021

18

…Which Coincides With A Series Of Tax Increases

• Lower tax rates afforded by the 2010 extension of the “Bush Tax Cuts” expire on DEC 31, 2012;

• Provisions of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010, which expired on DEC 31, 2011 will be felt by consumers in 2013 as they file their 2012 tax returns;

• The Middle Class Tax Relief and Job Creation Act of 2012 Expires on DEC 31, 2012; • Various other tax relief measures, including the partial expensing of investment property,

expire on DEC 31, 2012; and • Provisions for Obamacare that increase tax rates on earnings and investment income for high

income taxpayers begin in JAN 2013.

“Education is when you read the fine print. Experience is what you get if you don’t.” -Pete Seeger

Key planned tax increases include:

19

Averting The Cliff Is Unlikely

20

And Betting On A Tea Party Compromise In 2012 Ahead Of The Cliff Is Even More Unlikely

21

Consensus Expectations Are Not Pricing In The Cliff

1. CONSENSUS: Bloomberg consensus GDP growth estimates for 2013 are +2.4%

2. REALITY: The CBO has incorporated all spending cuts and revenue increases and has an estimate of +0.5% GDP growth for 2013

3. PROBABILITY: THE CLIFF COULD REASONABLY EQUATE TO A 2% - 3% DRAG ON GROWTH IN 2013

22

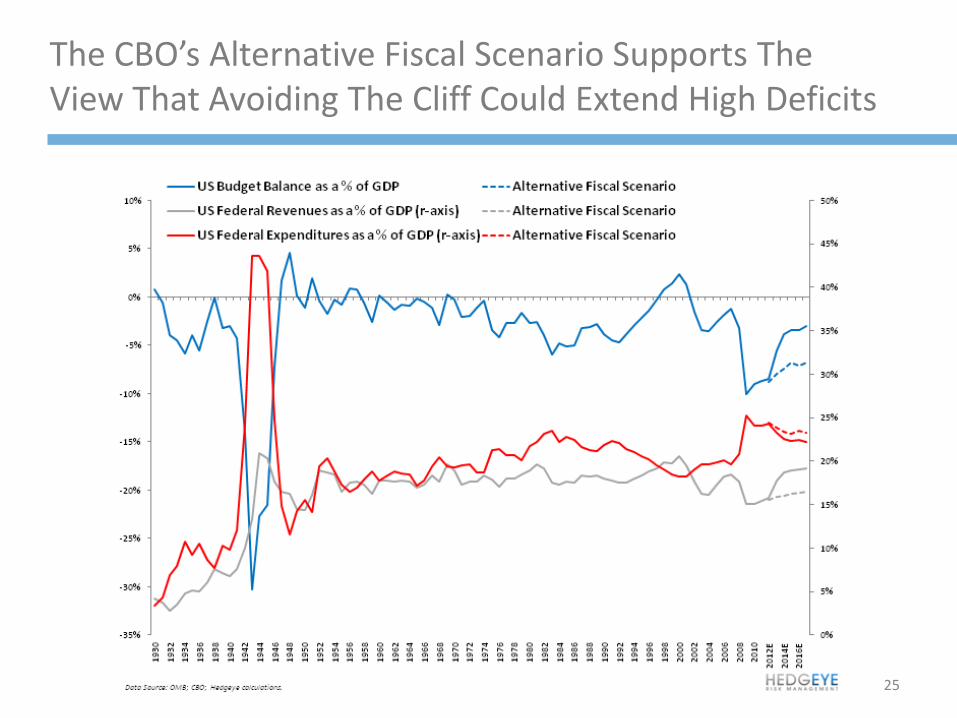

If Policymakers Do Manage To Avert The Fiscal Cliff, Federal Debts And Deficits Will Continue To Grow Unabated…

23

…Especially With Federal Expenditures Set To Remain Elevated Over The Long Term

24

The CBO’s Alternative Fiscal Scenario Supports The View That Avoiding The Cliff Could Extend High Deficits

25

As a Result, U.S. Debt Growth Will Increase If The Fiscal Cliff Is Resolved Poorly

26

And Just In Time For The Cliff… Another Debt Ceiling Showdown!

27

Based On Our Growth Assumptions, Both Cliff And Debt Ceiling Debates Could Occur Simultaneously

28

So In The Last Six Months Of A Presidential Election Year, Congress Has To…

1. Try to avert a meaningful cut in federal spending (or absorb the pain)

2. Agree on avoiding massive looming tax increases

3. Negotiate another debt ceiling compromise

29

“DEMOCRACY’S THE WORST FORM OF

GOVERNMENT EXCEPT FOR ALL THE OTHERS.” -WINSTON CHURCHILL

30

OBAMA VS ROMNEY

3Q 2012

OBAMA VS ROMNEY

31

From Now Until November, Obama Versus Romney Will Be A Critical Macro Factor

The race is within the margin of error on national poll aggregates.

32

Obama Has An Advantage In The Electoral College

Date Source: Real Clear Politics

33

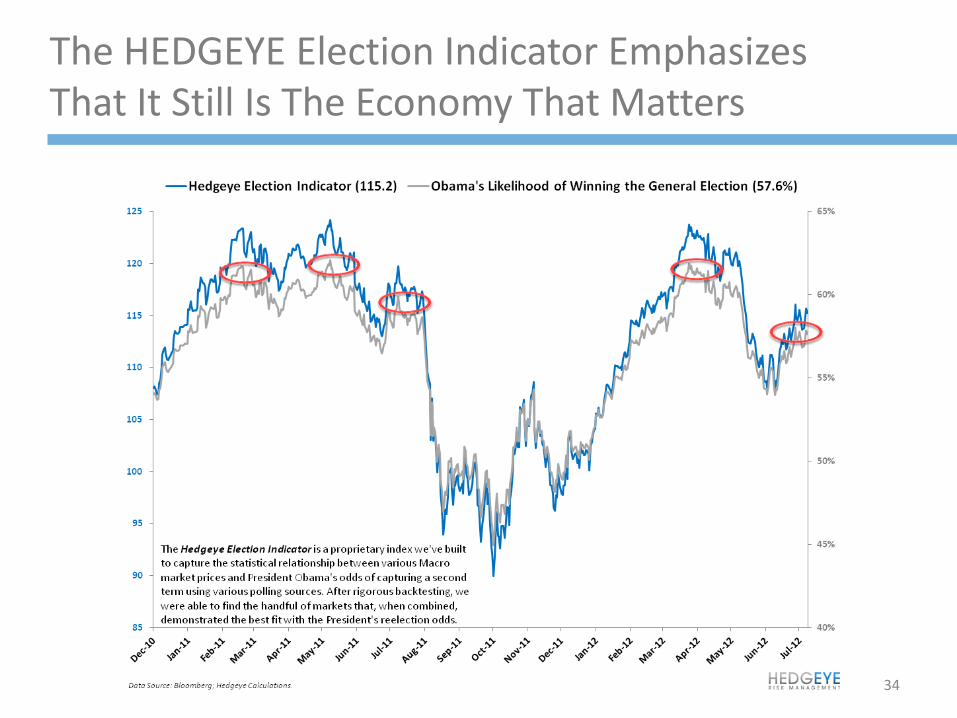

The HEDGEYE Election Indicator Emphasizes That It Still Is The Economy That Matters

34

Almost As Important As The Presidency Is Control Of Congress

• Currently based on the Real Clear Politics poll aggregate, the Democrats have a narrow +1.3 advantage in the generic congressional vote That said, Republicans have led in the last 3 major polls

• According to InTrade, the Republicans are at a 53.4% probability of controlling the Senate

• In terms of the House of Representatives, the Republicans are just over 80%

• But, with Congressional approval at ~18%, nothing is certain in terms of re-election / incumbency

35

Remember Reagan: Under Romney Presidency, Regime Change At The Fed Could Be Dramatic

“I’d be looking for somebody new. I think Ben Bernanke has overinflated the amount of currency that he’s created. QE 2 did not work, it did not get Americans back to work, it did not get the economy going again … We’re growing now at one to one-and-a-half percent.”

Republican Nominee Mitt Romney, September 6th, 2011

36

Obama Has Been More Tight Lipped On His Intentions Relating To Bernanke

• Bernanke was originally a Bush appointee in February 2006 to a 14-year term and a 4-year term as Chairman

• President Obama re-appointed Bernanke to a 4-year term in 2009

• In 2010, Bernanke was approved by the Senate by a margin of 70 – 30, the narrowest margin ever for the Governor of the Fed

• From a political perspective, separating himself from Bernanke may be a prudent move for Obama, though it could prove difficult

37

Consumers Feel Like It’s the 1970s – Fear Mongering Doesn’t Work

38

Got #GrowthSlowing? ISM Does = Lowest Since 2009

39

Got Central Planning? Small Business Confidence Gets It – That’s A Cliff Too

40

In Terms Of Economic Policy, President Obama Has Made A Proactive Strike

• In a ceremony at the White House on July 9, 2012, President Obama proposed extending the Bush tax cuts, but only for those making less than $250,000

• According to President Obama:

"I'm not proposing anything radical here. I just believe that anybody making over $250,000 a year should go back to the income tax rates we were paying under Bill Clinton.“

"The money we're spending on these tax cuts for the wealthy is a major driver of our deficit," Obama said, adding that they are also the "least likely to promote growth.

• This policy, while political in nature, is consistent with recent polls from both the National Journal and Bloomberg that indicated 2/3rds of those polled approved of extending the tax cuts for those that make under $250,000

41

But The Differences Between The Candidates Remain Meaningful

Obama Romney

Author of Obamacare Would repeal Obamacare

Repeal Bush tax cuts for households making over $250K

Make Bush cuts permanent

Lower corporate taxes manufacturing industries

Lower corporate taxes to 25% across the board

Favor increased stimulus spending to grow economy

Focus on increased deregulation

Cut some spending and increase taxes on the wealthy to narrow deficit

Cut non-discretionary security spending by 5%

42

Romney Will Make Sure That Obama Is Dancing With The Bear Through November

43

The Election Will Have A Direct Impact On The U.S. Dollar

1. Obama Presidency, Republican Senate and Republican House -> Dollar bullish?

2. Obama Presidency, Democratic Senate, Republican House –> Dollar bearish?

3. Romney Presidency, Democratic Senate, Republican House -> Dollar bullish?

4. Romney Presidency, Republican Senate, Republican House -> Dollar bullish?

44

As In The U.S., Politics Will Be In The Focus Across Europe Throughout The Summer

45

As The “Haves” Continue To Borrow From The “Have Nots”

46

Declining Confidence Broadly In Europe Will Increase The Political Discord

47

Meanwhile, The Solutions From The Eurocrats Continue To Have Predictable Outcomes

Data Source: Greenlight Capital 48

Current HEDGEYE Macro Positions

LONG -> Utilities via XLU SHORT -> Industrials via XLI -> Energy via XLE -> Gold via NG (Nova Gold)

49

THIS PRESENTATION WAS PREPARED BY: KEITH MCCULLOUGH, DARYL JONES, MATT HEDRICK AND DARIUS DALE.

FOR MORE INFORMATION AND A COMPLETE LISTING OF RESEARCH PLEASE VISIT: WWW.HEDGEYE.COM

OR EMAIL: [email protected]

3Q 2012

OBAMA VS ROMNEY

50

Macro 3Q Themes Presentation

Initial Publication: July 11th 2012