m&a in 2015: successor liability under the fcpa · m&a in 2015: successor liability under...

TRANSCRIPT

M&A in 2015: Successor Liability Under the FCPA Norton Rose Fulbright US LLP Thursday, February 26, 2015

Speaker Marsha Z. Gerber Partner Norton Rose Fulbright US LLP Marsha Gerber is a partner in the Houston office with more than 25 years of work experience. She regularly leads anti-corruption and international trade controls due diligence initiatives for multi-national clients considering international acquisitions, joint ventures, and third party relationships and counsels boards of directors and audit committees of the board on related governance matters. Marsha also regularly represent clients faced with responding to government investigations and enforcement actions, including those of the Department of Justice, the Securities and Exchange Commission, the Office of Foreign Asset Control and Congress and interfaces with corporate boards in those representations.

Marsha also regularly develops and implements corporate compliance programs to help clients meet the US Sentencing Guidelines protocol, SOX requirements, and other relevant guidelines; develops and presents anti-corruption and trade controls training to employees of clients involved in international business operations, and counsels corporate executives and boards of directors regarding compliance obligations. She has years of experience working with the Foreign Corrupt Practices Act (FCPA) and other statutes and regulations affecting international commerce and corporate governance obligations. She also counsels clients in establishing effective records management protocols.

Other areas of practice during Marsha's career have included eCommerce/systems design matters, counseling on employment issues and handling employment disputes, banking (domestic and international), patent and trademark infringement, medical practice issues and disputes and construction industry matters.

As a trained mediator and arbitrator, Marsha is a member of both the panel of arbitrators of the American Arbitration Association and the panel of arbitrators of the International Centre for Dispute Resolution. She has served as an arbitrator for complex commercial, complex securities, employment and health care matters.

2

Speaker Cristina K. Lunders Sr. Associate Norton Rose Fulbright US LLP Cristina Lunders joined Norton Rose Fulbright's Houston office in 2006 and has significant experience in assisting clients with diverse regulatory needs, including investigations, compliance, and due diligence.

Cristina has worked with both public and private clients in governmental and internal investigations (including Foreign Corrupt Practices Act ("FCPA"), financial fraud, and employee misconduct investigations). Her investigations and litigation matters have often involved managing large document collections, reviews, and analyses, interviewing of key personnel and presenting findings to internal and governmental bodies.

In the compliance area, Cristina has drafted and implemented new and updated policies and procedures, provided relevant training to boards and other employees, and conducted risk assessments and audits. Her transactional due diligence work has involved a variety of clients and situations including M&A transactions, agents and joint venture partners.

For 20 months from 2010 through 2012, Cristina was seconded to the world's largest natural resources company and gained valuable insight from the client's perspective. She is aware of and fully understands the challenges that affect in-house compliance groups. During her secondment, Cristina led internal investigations, performed due diligence, conducted anti-corruption risk assessments and drafted and implemented anti-corruption policies and procedures. She also trained thousands of employees worldwide on international anti-corruption laws.

3

Speaker Paul Edward Sumilas Sr. Associate Norton Rose Fulbright US LLP Paul Sumilas joined the Washington D.C. office in 2011. As a senior associate, Paul focuses his practice on white collar criminal defense for both corporations and individuals, with an emphasis on the Foreign Corrupt Practices Act, insider trading, public corruption and federal election law.

Paul has extensive experience advising clients in relation to the FCPA and general anti-corruption compliance, including conducting internal investigations, designing and implementing compliance programs, conducting training for employees and third parties, and managing risk assessments. He has worked for multinational clients across a variety of industries (oil and energy, aerospace, telecommunications, financial services, retail, maritime) and around the world, including leading investigations and reviews in Latin America, Europe, and Asia. Paul's experience includes drafting and revising anti-corruption manuals, policies, and procedures; drafting and implementing investigation plans; interviewing witnesses; managing and assisting reviews of books and records; managing document collections, reviews, and productions; and preparing investigation reports and presentations for clients and government agencies.

Previously, Paul practiced law in the Washington D.C. office of an international law firm.

4

Continuing education information • We have applied for one hour of California, Texas, Virginia

CLE and New York non-transitional CLE credit. Newly admitted New York attorneys may not receive non-transitional CLE credit. For attendees outside of these states, we will supply a certificate of attendance which may be used to apply for CLE credit in the applicable bar or other accrediting agencies.

• Norton Rose Fulbright will supply a certificate of attendance to all participants who: 1. Participate in the web seminar by phone and via the web

2. Complete our online evaluation that we will send to you by email within a day after the event has taken place

5

Administrative information • Today’s program will be conducted in a listen-only mode. To

ask an online question at any time throughout the program, click on the question mark icon located on the toolbar in the bottom right side of your screen. Time permitting, we will answer your question during the session.

• Everything we say today is opinion. We are not dispensing legal advice, and listening does not establish an attorney-client relationship. This discussion is off the record. You may not quote the speakers without our express written permission. If the press is listening, you may contact us, and we may be able to speak on the record.

6

Introduction M&A activities can present anti-corruption risk to companies • Successor liability • Collateral consequences for pre-acquisition activity • Post-acquisition activities • Risk can be mitigated through appropriate due diligence, and

appropriate integration into an effective compliance program

7

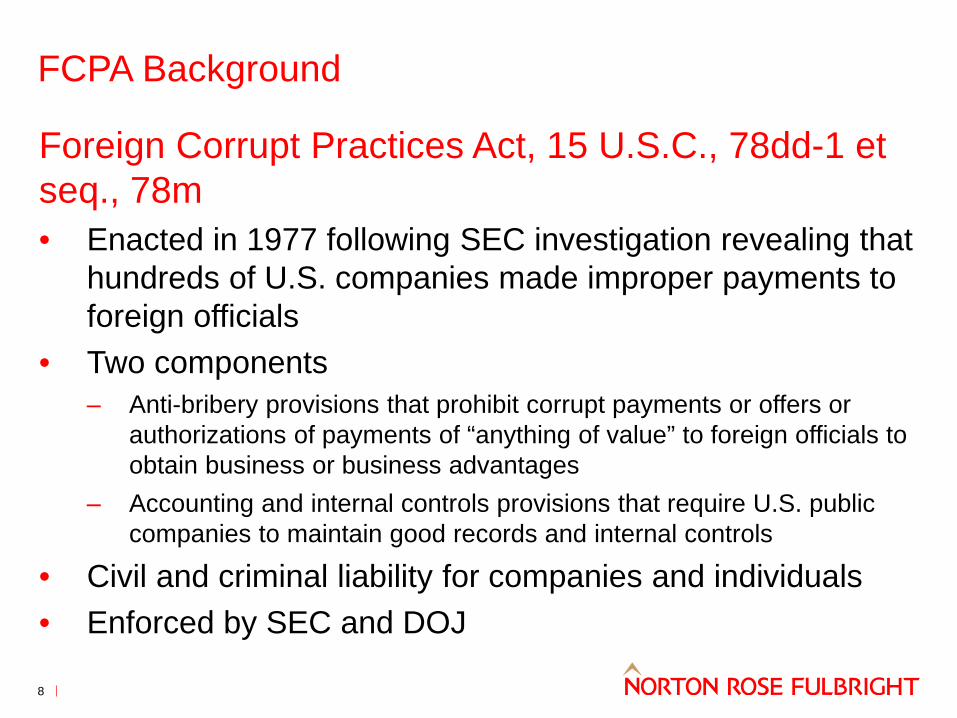

FCPA Background

Foreign Corrupt Practices Act, 15 U.S.C., 78dd-1 et seq., 78m • Enacted in 1977 following SEC investigation revealing that

hundreds of U.S. companies made improper payments to foreign officials

• Two components ‒ Anti-bribery provisions that prohibit corrupt payments or offers or

authorizations of payments of “anything of value” to foreign officials to obtain business or business advantages

‒ Accounting and internal controls provisions that require U.S. public companies to maintain good records and internal controls

• Civil and criminal liability for companies and individuals • Enforced by SEC and DOJ

8

FCPA Successor Liability

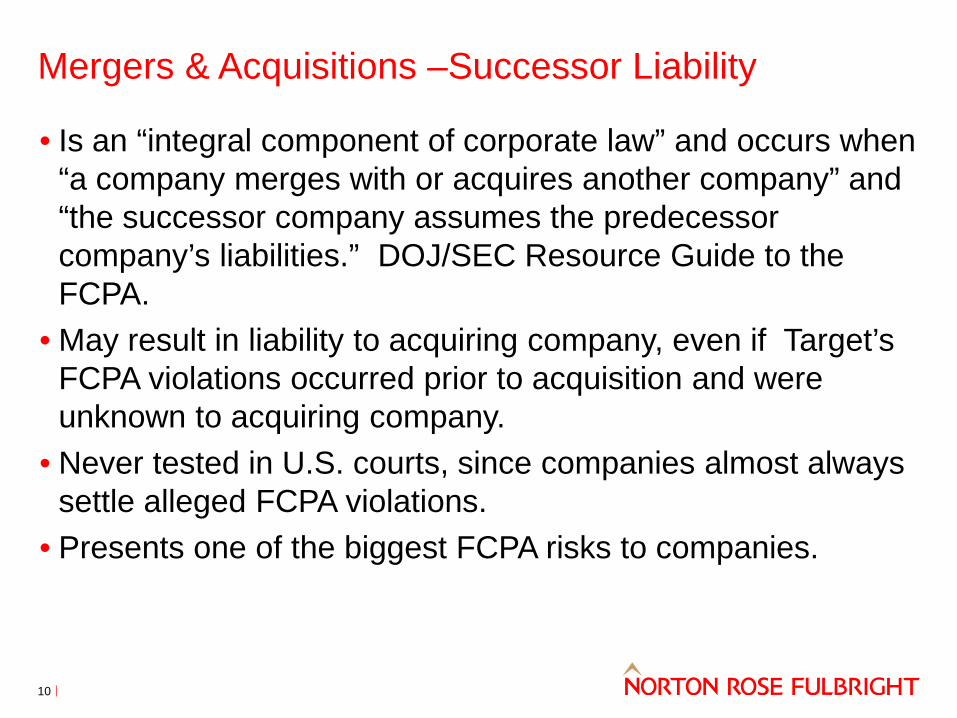

Mergers & Acquisitions –Successor Liability • Is an “integral component of corporate law” and occurs when

“a company merges with or acquires another company” and “the successor company assumes the predecessor company’s liabilities.” DOJ/SEC Resource Guide to the FCPA.

• May result in liability to acquiring company, even if Target’s FCPA violations occurred prior to acquisition and were unknown to acquiring company.

• Never tested in U.S. courts, since companies almost always settle alleged FCPA violations.

• Presents one of the biggest FCPA risks to companies.

10

Opinion Procedure Release 2014-02 • Requestor to acquire 100 percent of the shares of a non-US consumer products

company and its wholly-owned subsidiary from another non-US company, all of which operated outside of the United States, were not issuers of securities in the United States, and had “negligible” business contacts in the United States.

• During pre-acquisition due diligence, the requestor discovered potential improper payments by the target and “substantial” weaknesses in the target's accounting and recordkeeping. – Target had not implemented a code of conduct or compliance policies and procedures,

and employees did not demonstrate an adequate awareness of anti-bribery laws.

• DOJ declined to take any enforcement action with respect to any pre-acquisition bribery committed by the target. – Although “a company assumes certain liabilities when merging with or acquiring another

company . . . [s]uccessor liability does not, however, create liability where none existed before.”

– Requestor took measures to identify and address these bribery and recordkeeping problems and provided DOJ with integration plan.

11

Recent SEC/DOJ Guidance

Recent Guidance Comprehensive FCPA guide published by DOJ and SEC on November 14, 2012 • Devotes six pages to successor liability • Emphasizes importance of pre-acquisition due diligence and post-acquisition improvement of compliance programs and internal controls to: –Help acquirer accurately value Target –Reduce risk of future bribes –Allow potential violations to be handled via negotiation of

costs and responsibilities for investigation/remediation.

13

Recent Guidance Clarifies government’s decision-making process: • Has declined to take action against acquiring company when

it disclosed conduct, remediated, and cooperated. • Has taken action against successor company only in limited

circumstances, generally involving egregious or sustained violations or where successor participated in or failed to stop conduct after acquisition.

• More often pursues action only against predecessor company, especially when acquiring company uncovered and timely remedied the violation.

• Practical Advice: –Seek an OPR –Conduct risk-based due diligence and disclosure

14

Due Diligence Work Plan

DOJ and SEC Expectations • FCPA Due Diligence and Disclosure:

– Conduct thorough risk-based FCPA and anti-corruption due diligence on potential new business acquisitions;

– Ensure that the acquiring company’s code of conduct and compliance policies and procedures regarding the FCPA and other anti-corruption laws apply as quickly as is practicable to newly-acquired businesses or merged entities;

– Train the directors, officers, and employees of newly-acquired businesses or merged entities, and when appropriate, train agents and business partners, on the FCPA and other relevant anti-corruption laws and the company’s code of conduct and compliance policies and procedures;

– Conduct an FCPA-specific audit of all newly-acquired or merged businesses as quickly as practicable; and

– Disclose any corrupt payments discovered as part of the due diligence of newly-acquired businesses or merged entities.

16

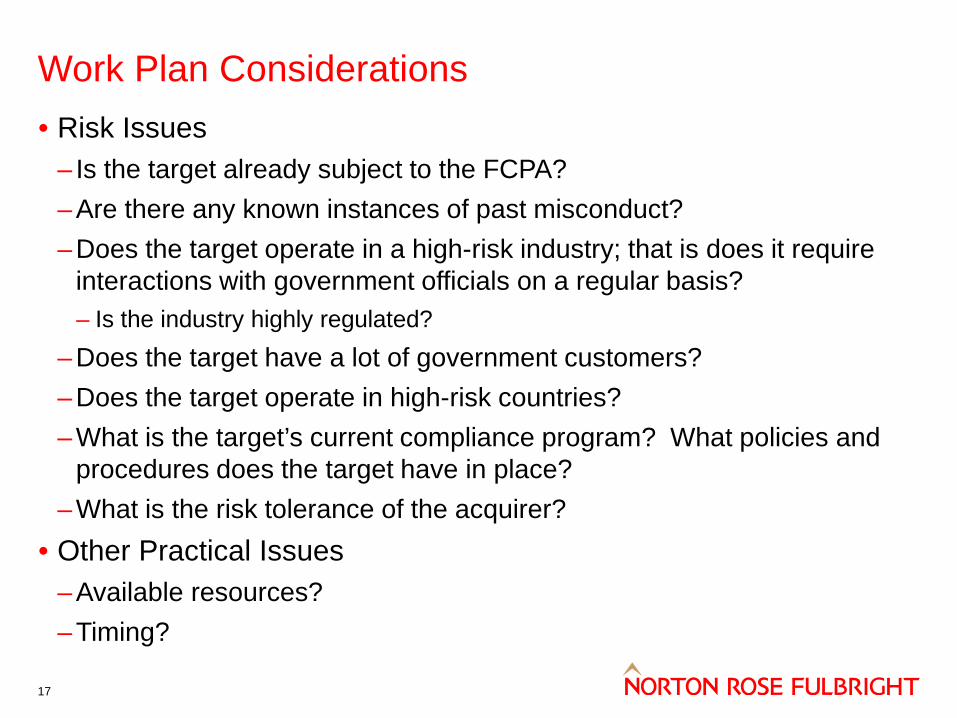

Work Plan Considerations • Risk Issues

– Is the target already subject to the FCPA? –Are there any known instances of past misconduct? –Does the target operate in a high-risk industry; that is does it require

interactions with government officials on a regular basis? – Is the industry highly regulated?

–Does the target have a lot of government customers? –Does the target operate in high-risk countries? –What is the target’s current compliance program? What policies and

procedures does the target have in place? –What is the risk tolerance of the acquirer?

• Other Practical Issues –Available resources? –Timing?

17

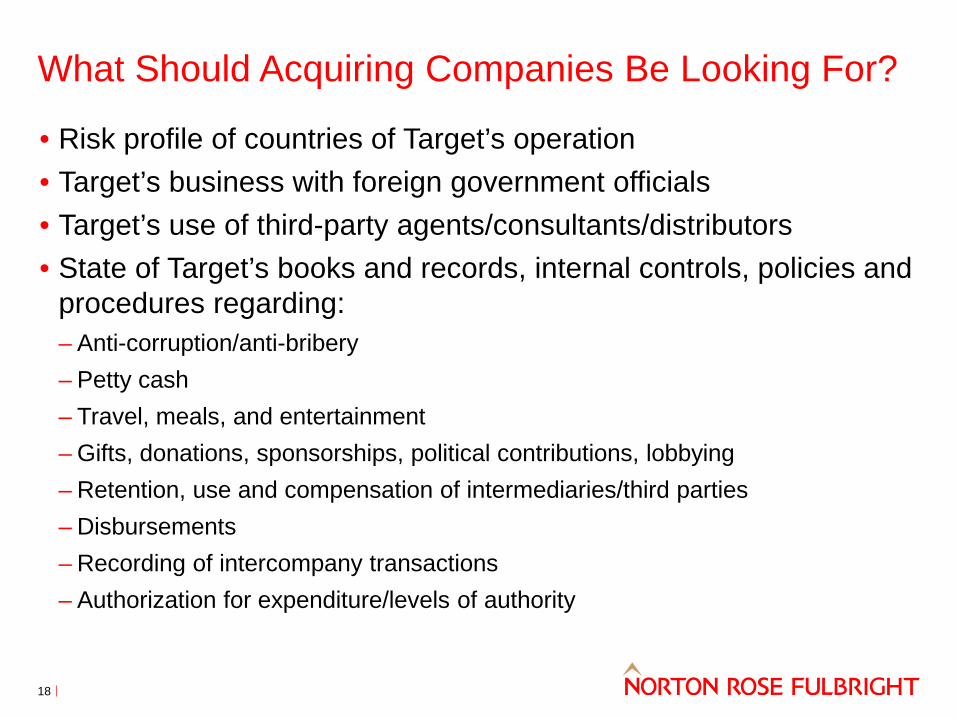

What Should Acquiring Companies Be Looking For? • Risk profile of countries of Target’s operation • Target’s business with foreign government officials • Target’s use of third-party agents/consultants/distributors • State of Target’s books and records, internal controls, policies and

procedures regarding: – Anti-corruption/anti-bribery – Petty cash – Travel, meals, and entertainment – Gifts, donations, sponsorships, political contributions, lobbying – Retention, use and compensation of intermediaries/third parties – Disbursements – Recording of intercompany transactions – Authorization for expenditure/levels of authority

18

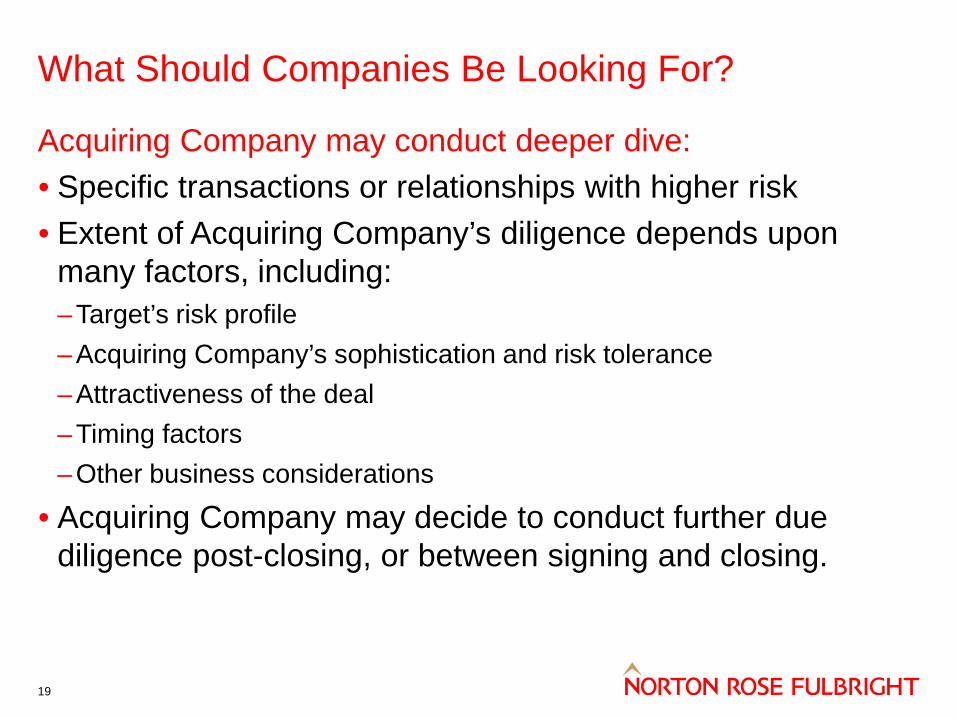

What Should Companies Be Looking For?

Acquiring Company may conduct deeper dive: • Specific transactions or relationships with higher risk • Extent of Acquiring Company’s diligence depends upon

many factors, including: –Target’s risk profile –Acquiring Company’s sophistication and risk tolerance –Attractiveness of the deal –Timing factors –Other business considerations

• Acquiring Company may decide to conduct further due diligence post-closing, or between signing and closing.

19

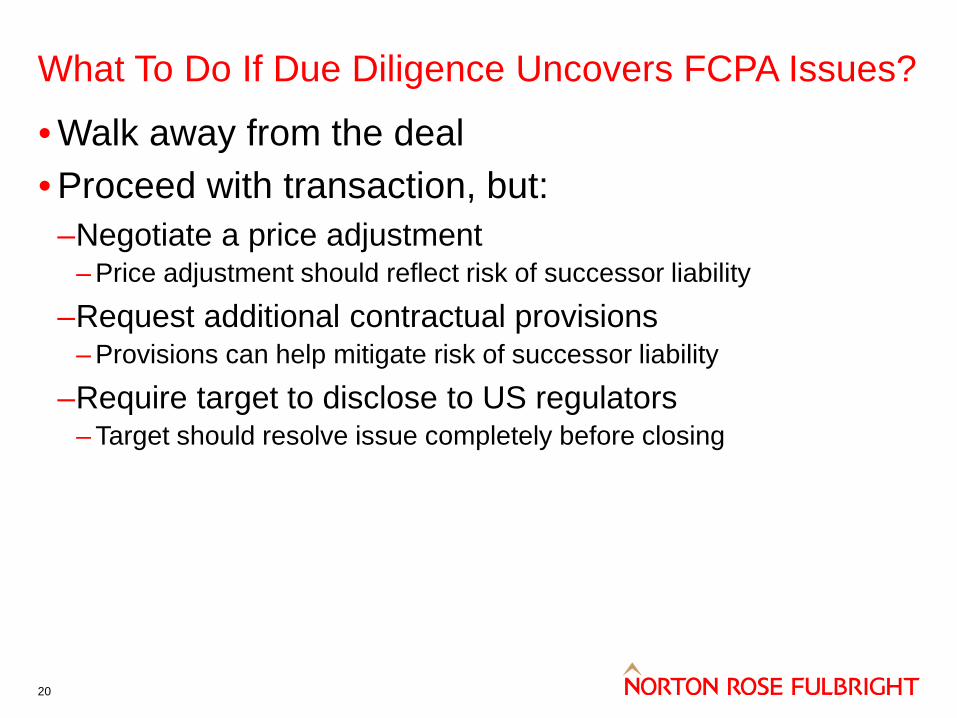

What To Do If Due Diligence Uncovers FCPA Issues?

• Walk away from the deal • Proceed with transaction, but:

–Negotiate a price adjustment – Price adjustment should reflect risk of successor liability

–Request additional contractual provisions – Provisions can help mitigate risk of successor liability

–Require target to disclose to US regulators – Target should resolve issue completely before closing

20

Structure of the Transaction/Contractual Provisions • Structure

–Nature of the acquisition (stock purchase versus asset purchase)

–Carve-outs • Contractual provisions

–Escrow provisions –Representations and warranties from knowledgeable

parties – Anti-Bribery – Books and Records – State of Internal Controls

–Termination of specific risk

21

Integration and Implementation

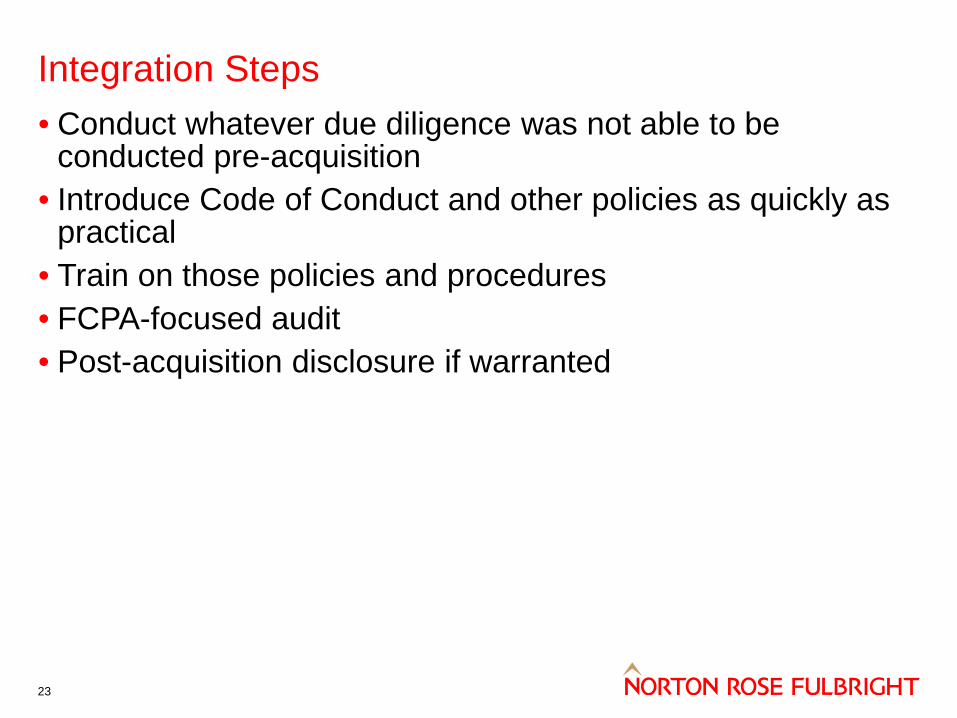

Integration Steps • Conduct whatever due diligence was not able to be

conducted pre-acquisition • Introduce Code of Conduct and other policies as quickly as

practical • Train on those policies and procedures • FCPA-focused audit • Post-acquisition disclosure if warranted

23

Post-Acquisition Integration

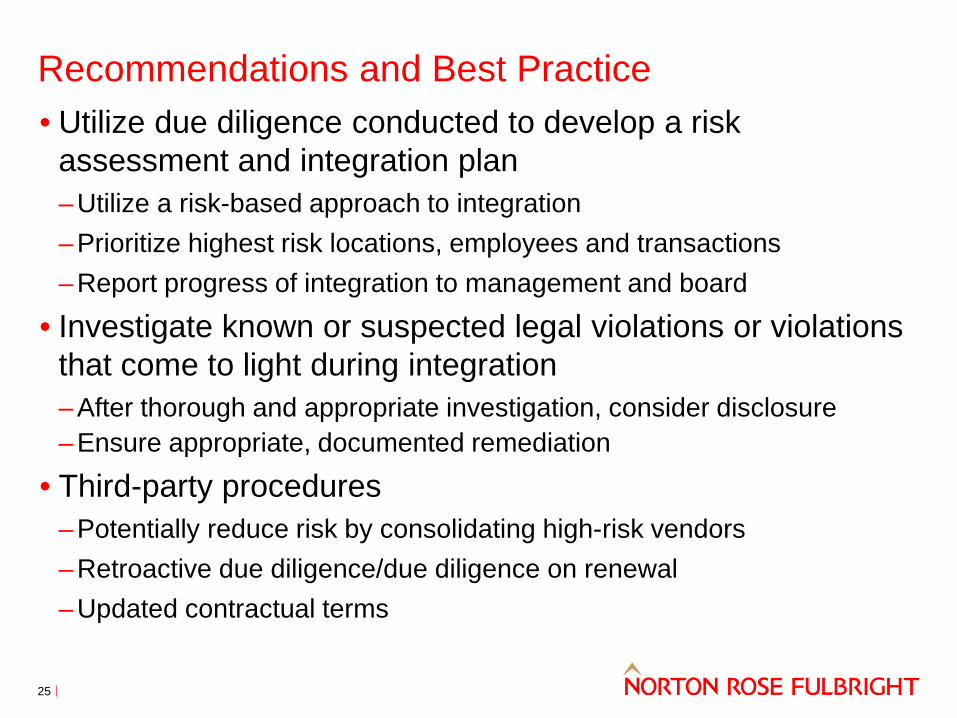

Recommendations and Best Practice • Utilize due diligence conducted to develop a risk

assessment and integration plan –Utilize a risk-based approach to integration –Prioritize highest risk locations, employees and transactions –Report progress of integration to management and board

• Investigate known or suspected legal violations or violations that come to light during integration –After thorough and appropriate investigation, consider disclosure –Ensure appropriate, documented remediation

• Third-party procedures –Potentially reduce risk by consolidating high-risk vendors –Retroactive due diligence/due diligence on renewal –Updated contractual terms

25

Recommendations and Best Practice • Consider accounting procedures and internal controls

– To what extent was the target subject to the same standards as the acquirer? – Books and records and internal controls requirements of the FCPA

– Appropriate record-keeping on highest risk payments (facilitating payments; expense reimbursements, especially gifts, meals, travel, and entertainment for government officials; payments through agents; political and charitable contributions)

– Petty cash – Vendor onboarding and maintenance

• Consider changes to target’s risk profile and compliance program – New anti-corruption regimes, high-risk geographic locations, or government

interactions – May warrant reevaluation of current compliance policies and resources – Update audit plan

26

Continuing education information

• If you are requesting CLE credit for this presentation, please complete the evaluation that you will receive from Norton Rose Fulbright.

• If you are listening to a recording of this web seminar, most state bar organizations will only allow you to claim self-study CLE. Please refer to your state’s CLE rules. If you have any questions regarding CLE approval of this course, please contact your bar administrator.

• Please direct any questions regarding the administration of this presentation to Terra Worshek at [email protected].

27

Disclaimer Norton Rose Fulbright US LLP, Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP and Norton Rose Fulbright South Africa Inc are separate legal entities and all of them are members of Norton Rose Fulbright Verein, a Swiss verein. Norton Rose Fulbright Verein helps coordinate the activities of the members but does not itself provide legal services to clients. References to ‘Norton Rose Fulbright’, ‘the law firm’ and ‘legal practice’ are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together ‘Norton Rose Fulbright entity/entities’). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a ‘partner’) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity. The purpose of this communication is to provide general information of a legal nature. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright.

29