long-term and short-term prospects for feed...

TRANSCRIPT

Long-Term and Short-Term Prospects for Feed Costs

Presented to The Annual Pork Financial Management Conference

June 17, 2011

Bill Lapp, President Advanced Economic Solutions™

Corn Is King “When corn sneezes, the other food commodities catch a cold”

Corn67%Oats

0%

Wheat11%

Barley1%

Soybeans19%

Milo2%

Corn Represents 2/3rds ofAll Crops Produced in the US

(Basis 2009 production data)

May 2011 Advanced Economic Solutions 2

Importance of Outside Influences on Agriculture Prices

Corn & Other Ag

Commodities

Global

Economic

Growth

Value of US $

Think Globally, Act Locally

May 2011 Advanced Economic Solutions 3

The Value of the US Dollar Has Declined By 1/3rd Since 2002

May 2011 Advanced Economic Solutions 4

GDP Growth (Real Ave Annual %)

1990-99 2000-09 2010-11

World 2.9 3.5 4.7

China 9.3 9.6 10.0

Developing 3.3 6.0 6.8

US 3.1 1.8 2.9

Advanced 2.7 1.7 2.8

May 2011 Advanced Economic Solutions 5

China’s Growing Appetite For Food:

- To paraphrase Seinfeld,

“its real, and its spectacular….”

80

90

100

110

120

130

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Chinese Per Capita Meat Consumption (2000=100)

May 2011 Advanced Economic Solutions 6

Contributions to Global Demand Growth: 2000-10

CHINA

Wheat 0%

Rice 5%

Coarse Grains 17%

Soymeal 51%

Vegoil 28%

BIOFUELS

Ethanol (Corn) 46%

Biodiesel (Vegoil) 43%

May 2011 Advanced Economic Solutions 7

Growth in World Grain / Oilseed Demand 1990-2000 2000-10 Annual Yld

Growth Rate MM Acres (2011)

Annual Acreage “Gap”

- Rice 1.5% 1.1% 1.1% 395 0 MM

- Wheat 0.4% 1.1% 1.1% 555 0 MM

- Coarse Grains 0.8% 2.5% 2.1% 775 3 MM

- -- Eaten 0.7% 1.4%

- -- Burned 4.8% 23.1%

Oilseed Meal 4.2% 3.9% 1.1% 543 15 MM

- -- Soymeal 5.4% 4.2% 1.2% 260 8 MM

- Vegoil 4.8% 5.1%

- -- Eaten 4.5% 3.5%

- -- Burned 7.3% 13.5%

- Palm 8.4% 5.5%

May 2011 Advanced Economic Solutions 8

Where Will The Acres Come From?

May 2011 Advanced Economic Solutions 9

US, 28.9 , 27%

Non-US, 80.0 , 73%

1970-80 Acreage Expansion: 109 mm acres (8%)

US, 10.5 , 19%

Non-US, 44.3 , 81%

2000-2010 Acreage Expansion: 54 mm acres (4%)

What To Expect in the Coming Years…

• Strong global food growth, led by China – Growth rates that will generally exceed gains in yields

– But the influence of ethanol leveling off

• High prices to encourage more acres planted – Mostly outside the US

• Generally low stock levels – Implying more volatility, weather-related price spikes

• US fiscal policy that drives a weaker US $ – Weak dollar EQUALS Higher commodity prices

May 2011 Advanced Economic Solutions 10

Volatility Is Here…. (even if you choose to ignore it)

May 2011 Advanced Economic Solutions 11

The New Plateau….

May 2011 Advanced Economic Solutions 12

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.0018

66

1876

1886

1896

1906

1916

1926

1936

1946

1956

1966

1976

1986

1996

2006

AVERAGE U.S. CORN PRICES: (1866-2010)

End Stocks – Price Scatter Diagrams • This was a useful tool for predicting prices, but has become

less meaningful in past 4 years

• All have shifted upward and to the right since 2006/07

June 2011 Advanced Economic Solutions 13

2007

20062008

2009

2010

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Co

rn F

utu

res

Pri

ce

Corn Stocks as % of Usage

Annual Corn Prices vs. Ending Corn Stocks-Use Ratio

Outlook for Feed Costs

• The overall situation for grains has become “tighter” since mid-2010, and will remain tight through most of 2011 and into 2012

– Prices will remain generally strong, and volatility will remain high

– Changes in supply/demand will dramatically impact prices

• Ending stocks – Corn: 10/11F 620 mm (4.6% of usage) ---- 11/12F 631 mm (4.7% of usage) ---- critically tight

– Soybeans: 10/11F 176 mm (5.3% of usage) ---- 11/12F 200 (6.0% of usage) ---- extremely tight

• Key unknowns during the next six months – Production, based on changes in planted area & yields

– Ethanol demand & policy

– Chinese corn/sb imports

• External factors will remain important drivers of prices in the coming year

– This includes the value of the US dollar and Chinese monetary policy

June 2011 Advanced Economic Solutions 14

US Corn Supply/Demand

June 2011 Advanced Economic Solutions 15

- Stocks at the end of the 10/11 crop year are forecast to decline to a bare

minimum 4.6%, tightest since mid-90s

- Even with an increase to 91.7mm acres, stocks at the end of 11/12 are

projected to build only modestly

2007/08 2008/09 2009/10F 2010/11F 2011/12FProj Proj Proj

Planted Acres 93.5 86.0 86.4 88.2 91.7

Harv. Acres 86.5 78.6 79.5 81.4 84.3

Yield (bu./acre) 150.7 153.9 164.7 152.8 160.0

Production 13038 12092 13092 12447 13495

Carryin 1614 1614 1673 1708 620

Total Supply 14362 13730 14773 14170 14128

Fuel 3027 3708 4560 5015 5083

Total FSI (incl Fuel) 4442 5025 5938 6390 6408

Feed & Resid 5859 5187 5142 5340 5239

Exports 2438 1845 1985 1820 1850

TOTAL USE 12738 12057 13065 13550 13497

Ending Stocks 1624 1673 1708 620 631

% of Use 12.7% 13.9% 13.1% 4.6% 4.7%

US Corn Supply/Demand

(Million Acres/Bushels)

June 2011 Advanced Economic Solutions 16

Lowest Stocks-Use Ratio On Record

– for both this year and next year!

5.0%

10.0%

14.9%

19.2%18.1%

19.5%

16.3%

11.5%

9.4%

18.5%17.6%

11.6%12.7%

13.9%13.1%

4.6% 4.7%

0%

5%

10%

15%

20%

25%9

5

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

U.S. Corn Stocks-Use Ratio (10/11 & 11/12 Forecast)

June 2011 Advanced Economic Solutions 17

- Current Expected: 13.47 B (91.5 planted & 160 BPA) – would imply December corn

futures trading near $6.00-6.50 this fall

- Low Side Estimate: 12.89 B (91.0 planted & 154 BPA) – would imply need for

rationing and December corn trading over $9 later this year

- High Side Estimate: 13.96 B (92.5 planted & 164 BPA) – would imply adequate

supplies & some stock building, lead December corn toward $5.50

- Corn acreage was pegged at 92.2 mm in 2011 by USDA - But a better estimate may be 91.7 mm

Mayl 2011 Advanced Economic Solutions 18

93.5 92.2

70

75

80

85

90

958

9/9

0

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

Millio

n A

cre

s

US Corn Acreage (2011-13 Forecast)

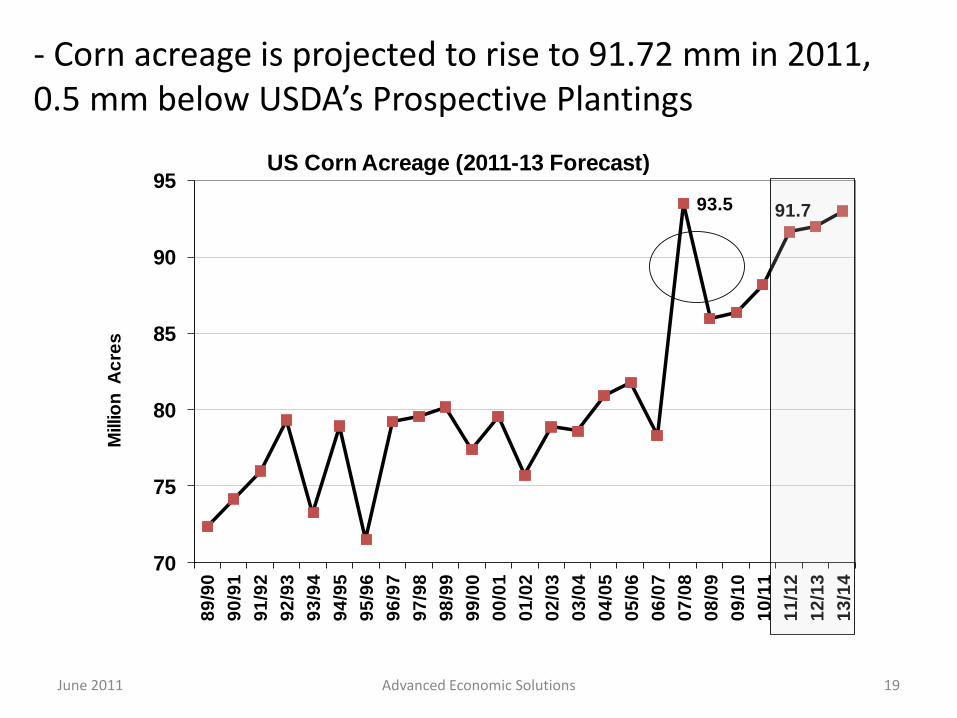

- Corn acreage is projected to rise to 91.72 mm in 2011, 0.5 mm below USDA’s Prospective Plantings

June 2011 Advanced Economic Solutions 19

93.5 91.7

70

75

80

85

90

95

89

/90

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

Millio

n A

cre

s

US Corn Acreage (2011-13 Forecast)

- CORN Yields: 2010 US corn yields were forecast at 165.0 BPA in August, but finished 7% lower at 152.8 BPA - 2011 yields are projected at 160.0 – actual trend depends upon what years are included in the analysis

Mayl 2011 Advanced Economic Solutions 20

80

90

100

110

120

130

140

150

160

1707

7

79

81

83

85

87

89

91

93

95

97

99

01

03

05

07

09

11

bp

aUS Corn Yields

2011 Projected at 160.0

2011 TREND YIELD OPTIONS:

1977-10 157.8

1982-10 159.6

1987-10 161.8

1992-10 161.5

1997-10 162.0

- 2010/11 corn demand base forecast to reach 13.55 B (+4%) - Growth in demand continues to be led by ethanol - Feed/residual revised up to 5.34 B (+3%) after release of 3/1 stks

June 2011 Advanced Economic Solutions 21

5564 5795 6158 5995 5545 58595187 5142 5340

15871900

1918 21332125

2438

1845 1985 1820

1345 1369

1383 1415 1420

1415

1317 1378 1375

996

11681324 1604 2120

3027

37084560

5015

0

2000

4000

6000

8000

10000

12000

14000

02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11

MM

Bu

she

ls

Annual Corn Usage (10/11F)

Ethanol

Food Use

Exports

Feed Use

June 2011 Advanced Economic Solutions 22

50155234

-

1,000

2,000

3,000

4,000

5,000

6,00002 03 04 05 0

6

07

08 09 10 11 12 13

U.S. Corn Used For Ethanol

Ethanol Grind Has risen sharply, but growth will slow going forward

June 2011 Advanced Economic Solutions 23

200

250

300

350

400

450

S O N D J F M A M J J A

MM

Bu

she

ls U

sed

(1 Bushel of Corn Produces Approximately 2.70 Gallons of Ethanol)

Sept-Aug Monthly Ethanol Production - Corn Usage (MM Bus)

07/08

08/09

09/10

10/11

10/11F

Source: Dept of Energy

Where Would The Price of Corn Be without Ethanol?

June 2011 Advanced Economic Solutions 24

1.602.002.402.803.203.604.004.404.805.205.606.006.40

89

/90

91

/92

93

/94

95

/96

97

/98

99

/00

01

/02

03

/04

05

/06

07

/08

09

/10

11

/12

AverageFarm Price

ModelW/OutEthanol

(Adopted from a model developed by Drs. Steve Meyer & Thomas Elam)

June 2011 Advanced Economic Solutions 25

05/06 06/07 07/08 08/09 09/10 10/11 11/12

(Sept-Aug, MM Bus) Proj Proj

Acres Planted (mil.) 72.0 75.5 64.7 75.7 77.5 77.4 76.6

Acres Hvstd. (mil.) 71.3 74.6 64.1 74.7 76.4 76.6 75.6

Yield (bu./acre) 43.0 42.9 41.7 39.7 44.0 43.5 44.0

Production 3063 3197 2677 2967 3359 3329 3327

Carryin 256 449 574 205 138 151 176

Imports 3 10 10 10 10 11 12

TOTAL SUPPLY 3322 3656 3261 3182 3507 3491 3515

Crush 1739 1806 1800 1662 1752 1642 1665

Exports 945 1108 1159 1279 1501 1545 1550

Seed/Stock Adj 189 169 98 103 103 128 100

TOTAL USE 2873 3082 3056 3044 3356 3315 3315

Ending Stocks 449 574 205 138 151 176 200

% of Use 15.6% 18.6% 6.7% 4.5% 4.5% 5.3% 6.0%

US Soybean Supply/Demand

(Million Acres/Bushels)

June 2011 Advanced Economic Solutions 26

24

26

28

30

32

34

36

38

40

42

44

467

6/7

7

78

/79

80/

81

82/

83

84/

85

86/

87

88/

89

90/

91

92

/93

94

/95

96

/97

98

/99

00

/01

02

/03

04

/05

06

/07

08

/09

10

/11

Bu

she

ls P

er

Acr

e

U.S. Soybean Yields

In spite of record crops, soybean stocks remain extremely tight through end of 11/12

June 2011 Advanced Economic Solutions 27

7.1%6.4%

4.5%

8.6%

15.6%

18.6%

6.7%

4.5% 4.5%5.3%

6.0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

01/0

2

02/0

3

03/0

4

04

/05

05

/06

06

/07

07/0

8

08/0

9

09/1

0

10/1

1

11/1

2

SOYBEAN ENDING STOCKS-USE RATIO(10/11 & 11/12 Forecast)

S American Soybean Crops Continue To Be Revised Up

June 2011 Advanced Economic Solutions 28

43.5 52.5 51.0 53.0 57.0 59.0 61.0 57.8

73.0 72.5

30.0

35.5 33.0 39.0

40.5 48.8 46.2

32.0

49.5 53.0

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11

Brazil and Argentina Soybean Production (10/11F)

Argentina

Brazil

China Imports Have Risen Dramatically - Account for 44 mm Acres of Demand -

June 2011 Advanced Economic Solutions 29

16.9

25.828.3 28.7

37.841.1

50.354.5

58.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11

Chinese Soybean Imports (10/11 & 11/12 Forecast)

Food Inflation is accelerating - Dealing with a $40 B cost bubble….

May 2011 30 Advanced Economic Solutions

Forecast: CPI-Food up 4-6% by December 2011

Long-Term and Short-Term Prospects for Feed Costs

Presented to The Annual Pork Financial Management Conference

June 17, 2011

Bill Lapp, President Advanced Economic Solutions™