lokesh final for spiral

TRANSCRIPT

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 1/112

A REPORT ON

SUMMER INTERNSHIP/ PROJECT WORK

For

__________ (J.M.Financial) __________

Submitted to

INDUKAKA IPCOWALA INSTITUTE OF MANAGEMENT(I2IM)

CHAROTAR UNIVERSITY OF SCIENCE AND TECHNOLOGY (CHARUSAT)

CHANGA

Prepared by

Lokesh Bhatiya

ID No.:09 mba 02

M.B.A. First Year

Under the Guidance of

Vaishali Shah

Jignesh Mochi

INDUKAKA IPCOWALA INSTITUTE OF MANAGEMENT(I2IM)

CHAROTAR UNIVERSITY OF SCIENCE AND TECHNOLOGY (CHARUSAT)

AT. & PO. CHANGA – 388 421 TA: PETLAD DIST. ANAND, GUJARAT

JULY 2010

DECLARATION

1

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 2/112

I, Lokesh Bhatiya, student of the two-year MBA programme at

Indukaka Ipcowala Institute of Management (I2IM) hereby declare

that the report on summer training and project work entitled “Risk

and Investment Behaviour of Investor ” is the result of my own work. I also

acknowledge the other works / publications cited in the report.

Place: Changa

Date: 31.07.2008

( )

(Lokesh Bhatiya)

2

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 3/112

Acknowledgement

As it is quite evident that any person before entering in the real world of

business he/she has to undergo training programme. Training holds very important

position in the overall position of education because one can feel the real place of the

real world of business through training.

I am thankful to Mr. Ghanshyam Vyas (Branch head JM Financial Pvt. Ltd.,

Baroda) for allowing us to undergo training.

I am also very thankful to Mr. Jignesh Mochi, Mr. Mulik for their guidance &

support during the summer training & summer project.

I also express my thanks to all the employees of the company for sharing their

valuable time to me from their tight schedule to give me valuable information.

I am very grateful to the G. Krishnamurthi (Principal) for allowing us to take

my training from such a reputed organisation. I am thankful to Mrs. Vaishali Shah for

helping me in every related aspect of training & project. I am very thankful to Mr.

Govind Dave for providing their valuable reference in arranging the summer training

in such a reputed organization.

SANNI M. PATEL

3

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 4/112

TABLE OF CONTENTS

4

Sr.No. Particular Page Number

PART 1 –ORGANISATIONAL PROFILE

1 Introduction 7

2 The company 9

a. • History 9

b. • Mission & Vision 12

c. •

Management structure14

d. • Products 18

3 Functional area 19

a. • Market & Marketing 19

b. • Production/Operation 22

c. • Human Resourses 24

4 Decision making 27

a. • Strategic decision area &Decision making process

27

b. • Tactical and Operationaldecision area & Decision making

process

28

c. • Formal & Informal power relations

29

5 Financial Analysis 30

a. • Profitability of the firm of last4 years

30

b. • Asset built up in the last 4years

33

c. • Key financial ratio &interpretation

36

d. • Financial health & future of the organization

37

6. My learning from the study of organization 38

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 5/112

5

PART 2-Project Study

7. Overview of the Project 75

8. Research Methodology 77

9. Data analysis, Finding & Interpretation 94

10 References

11. Appendices

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 6/112

EXECUTIVE SUMMARY OF ORGANIZATION PROFILE

The report contains the information about J.M. Financial and the core areas as

well as the services that it provides. It provides information about

Individual’s financial advisors

Equity brokerage group

Fixed deposits

It also contains different functional areas such as

Marketing management

Financial management

Human resources management

The report contain various tactical decisions, strategic, operational financials analysis

6

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 7/112

INTRODUTION

JM Financial group

JM Financial is an integrated financial services group offering wide range of

capital market service to its corporate and individual clients. The Group has business

interest in investment banking, institutional equity sale & broking, private &

corporate wealth management, research, equity broking, portfolio management, asset

management, commodity broking etc.

JM Financial service private limited

JM Financial service private limited is a private sector organization. TheRegister & Corporate office of this organization is in Mumbai and the branch office of

JM Financial is in 22 cities in India.JM Financial private limited (JM Financial

Services) is a full service wealth management and equity broking firm with a focus on

capital markets.

JM Financial services offers research-based instrument advisory and equity

trading services to high net worth individuals and corporate investors across wide

range of financial product.

Their domestic research capabilities, capital market expertise and an exclusive

level of personal attention enable them to design and execute customized investment

strategies for their clients.

• Private Wealth Group advising high net worth individuals

• Corporate wealth Group advising top approximately 500 Corporate

Treasuries

• Secondary Broking- Equity and derivatives

• Depository services

• Portfolio Management Service

• Distribution of

Mutual Funds – deft and equity

Equity IPO’s

Fixed income product

7

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 8/112

Real estate funds

Private equity

THE COMPANY

Evolution & History

JM Financial Limited was started in 1986 by JM Financial & Investment

Consultancy Services Private Limited (JM FICS) to engage in the business of stock

broking and securities.

JM Financial & JM FICS sponsored one of India’s first private sector mutualfund viz. JM mutual funds, JM financial mutual fund made a simultaneous launch of

three open ended funds in December, 1994. The trustee of this fund is JM Financial

Asset Management Pvt. Ltd.

JM Financial Group subsequently entered into in equity partnership with

Morgan Stanley in 1999. Morgan Staley is one of the world’s leading financial service

firms with approximately 45,000 employees in 390 offices across 23 countries

worldwide. Morgan Stanley has a presence is almost every financial market.

The partnership led to setting up of two joint venture companies, JM Morgan

Stanley Private Limited, with interest in the area of investment banking, retail

distribution, private wealth management and fixed income securities and JM Morgan

Stanley Securities Private Limited with operations in institutional equity sales and

trading. While JM Financial holds 51% of JM Morgan Stanley private limited with

49% being held by Morgan Stanley.

JM Morgan Stanley private limited operates in the area of retail distribution

and fixed income sales & trading through two wholly owned subsidiaries viz., JM

8

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 9/112

Morgan Stanley Financial Service Private Limited and JM Morgan Stanley Fixed

Income Securities Private Limited.

JM Financial Limited has approved the merger of JM Securities Private

Limited, a JM Financial group of company itself. This merger is subject to

satisfactory receipts of all statutory, regulatory, corporate and other approvals as may

be required, including but not limited to, approval of relevant high citst, Reserve Bank

of India, Stock Exchange, Securities Exchange Board of India, and share holders.

After the proposed merger JM Financial had expend its interest in equity

broking, investment banking, retail & fixed income broking, asset management,

commodities broking and equity financing business.

9

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 10/112

Awards

Year Name of Award Details

2009Finance Asia Country Awards for

AchievementBest Equity House, India

2009 Best Workplaces in India 2009Ranked among top 50 companies by Great

Places to Work Institute

2008 Best Workplaces in India 2008Ranked among top 50 companies by Great

Places to Work Institute

2008Outlook Money NDTV Profit

AwardsBest Merchant Banker - Runners Up

2007 Finance Asia Achievement Awards Best India Deal – for Vodafone’s $12 billion

acquisition of HTIL

2007 Finance Asia Achievement Awards Best Secondary Offering – for ICICI’s $4.6

billion simultaneous follow-on of ADRs and

domestic shares

2007 The Asset Triple A Regional Award Best Follow-on Offering - for ICICI’s $4.6

billion simultaneous follow-on of ADRs and

domestic shares

2007 ICRA Mutual Funds Awards Open Ended Sectoral–Healthcare-1 year

performance (till 31.12. 2006), Gold - JM

Healthcare Sector Fund

10

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 11/112

2006 CNBC TV18 – CRISIL Mutual Fund

Awards

EuroMoney Awards of Excellence

Floating Rate Plan - JM Floater Short Term

Plan

Best M&A House, India

2005 Finance Asia

Finance Asia

Best Follow-on Offering - ICICI Bank

USD1.75 billion concurrent ADR and

domestic share sale

Best India Deal - Reliance Industries USD4.8 billion restructuring

2004 Finance Asia

Asset Asian Awards

Asia Money

Asia Money

Asia Money

Best India Deal - USD 1.2 billion Tata

Consultancy Services IPO

Best Privatization - USD 2.4 billion ONGC

follow-on offering

Best Deal in India - OIL & Natural Gas

Corporation

Best Overall Strategy – Brokers

Best Overall Macroeconomics – Brokers

2002 CIRISL Best Fund Awards Best Performing Open-end Debt Scheme -JM Income Fund

2001 CIRISL Best Fund Awards Best Performing Open-end Debt Scheme -

JM Income Fund

Vision Statement

11

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 12/112

“To be the most trusted partner for every stakeholder in the financial world.”

Mission Statement

• Earning trust is a process (it can be gained and lost every day!)

• Sharing trust creates great teams

• Being trustworthy is the most efficient way of generating and retaining

long-term business

• Self–trust is the starting point of trusting others

JM believe:

• Earning trust is a process (it can be gained and lost every day!)• Sharing trust creates great teams (whether between employees or between

organisations)• Being trustworthy is the most efficient way of generating and retaining long-

term business• Self–trust is the starting point of trusting others

Believes

JM FINANCIAL have always sought to be a value-driven organization, where

its values direct its growth and success.

Integrity:

Integrity is fundamental to its business. JM FINANCIAL adhere to moral and

ethical principles in everything JM FINANCIAL do as professionals, colleagues and

corporate citizens. Its reputation based on its high standards of integrity is invaluable.

12

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 13/112

Teamwork:

JM FINANCIAL believe extensive teamwork is what makes it possible for us

to work together towards a common goal. JM FINANCIAL value and respect each

individual's commitment to group effort.

Client Focus:

JM FINANCIAL always put the interest of its clients before its own. JM

FINANCIAL understand its client needs, seek new opportunities for them, addressthem and deliver unique solutions as per their expectations. The success of its clients

is the biggest reward for us.

Innovation:

JM FINANCIAL understand its clients' needs and develop solutions for themost complex or the simplest, the biggest or the smallest financial transactions,

whether for individuals or institutions. Creativity and innovation are key factors to

everything JM FINANCIAL do. JM FINANCIAL encitsage new ideas which help us

address unique opportunities.

Implementation:

Its expertise, experience and its continuous focus on the quality of execution

ensures effective implementation of its strategies.

13

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 14/112

Performance:

JM FINANCIAL believe in development of its people and continuously hone

its skills, setting higher targets of performance for itsselves. JM FINANCIAL strive to

attract, develop and retain the best talent. JM FINANCIAL recognize and reward

talent based on merit.

Partnership:

Its relationships with all its stakeholders reflect its spirit of partnership.

Clients see us as trusted advisors, shareholders see us as partners and employees see

us as family. JM FINANCIAL respect, trust and support all its stakeholders.

Management Structure of J M Group

JM FINANCIAL is a private company and the offices are spread over thecountry. J M FINANCIAL has many branches in India. Its structure is discussed as

follow with the management hierarchy.

14

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 15/112

Management Structure of J M Group

15

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 16/112

Geographical Spread of JM Financial Services Pvt. Ltd.

16

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 17/112

Products

Primary Market:

IPO Offering - Debt and Equity Mutual Fund - Debt and Equity

Secondary Market:

Equity Advisory and Broking Fixed Income Advisory & Execution Future & Option Advisory & Broking

Buybacks Block Trade

Sales Services

Customized investment advisory and asset allocation of portfolio Portfolio Tracking for Mutual Funds Portfolio Tracking for Secondary Equity

17

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 18/112

FUNCTIONAL AREAS

Business segment of JM Financial service

Private wealth Group

Private Wealth Group (PWG) is a personalized investment advisory service

for high net worth individual with an investible surplus in excess of USD 1 mn.

(Rs 5 crore) with dedicated wealth managers for managing the client’s wealth.

PWG segment draws upon the full spectrum of firm resources & expertise in

capital markets for generating investment ideas and developing customizedinvestment solution for meeting their client’s financial goal.

Corporate wealth group

Corporate Wealth Group (CWG) at JM Financial provides research-based

investment advisory service to top 500 corporate treasuries for deployment of

surplus funds. A dedicated investment advisor supported by research and product

team is assigned to each corporate client.

Equity Brokerage Group

Equity Brokerage group (EBG) offers trading and research-based equity

advisory services to high net worth individuals, retail clients and corporates.

This group focuses on generating wealth for the client through stoke ideas and

trading strategies based on a combination of fundamental and research analysis.

Equity Brokerage Group distinguishes itself from others by focusing on

providing customized investment solutions and brokerage services to various

client segments.

18

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 19/112

Independent Financial Advisor Group

JM Financial service has developed one of the largest network of distribution

of financial product to retail investors through Independent Financial Advisors

(IFA).

JM Financial Group’s expertise in capital market and strong investment

banking franchise, helps them in launching public issues of companies with strong

fundamental and creditable promoter background for generating their clients.

Main Services

19

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 20/112

Target market

Target market of JM Financial is all those who wants to invest either in fixed

deposit or wands to invest in share market. JM financial also help the person who

wants to take expert advice. So the JM financial target market is as follow

• Broker

• Sub-broker

• Local agent

• Individual investor

• Senior citizen

• Conservative investor

• Aggressive investor

Market share of JMFS

Approximately JMFS captures 20% of total market share of overall broking

but the brighter part is that its market share is increasing year by year.

Competitors of JMFS

• Reliance Capital

• Kotak

• Karvy

• Shri Global traders

• Bajaj Holding

• Local broker

• VSE

20

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 21/112

Distribution channel

JMFS wants to reach deep in the market. It has very good link with sub

broker. So by sub broker chain company try to reach it`s target market.

Promotional measure

Company use all possible source of promotional measure to reach it’s target

market. The promotional measure includes

• Advertisement

• Sale promotion

• Publicity

• Development of franchise

• Development of sub broker

Measure of customer satisfaction taken by the company

• JMFS uses very simple technique to know customer satisfaction. Company

use

Feedback from filling

Direct contact with customer

Provide some addition service

Help in tax panning etc.

Try to advice the customer the satisfy customer financial need

Office timing

Monday to Friday 9.30 AM to 6.30 PM

Saturday 10.30 AM to 2.30

21

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 22/112

Attendance system

Attendance system in J M financial is very simple. All employees have to sign

in the register when they come & when they go out. In this way they record in time &

out time of any employ.

Critical working hour

Critical working hour in the organization is the trading time in the stock

market i.e. 9:55 AM to 3:30 PM.

Discipline

JM Financial is very particular about in & out time of employees. So all the

employees have to follow strict time schedule of the organization.

Human resource planning

Whenever there is requirement of manpower each & every branch send there

need to Head office. The branch also describes the job where the person is required.

The brief job description is also given by the branch office. Base on the

Requirement of the branch the head office takes the responsibility overall

human resource planning.

The HRP of the JM financial includes number of person require, type of

person required, number of person require in each & every branch, source of

recruitment whether it is eternal or external source & so on.

22

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 23/112

Process of HRP

Recruitment & Selection

After HRP recruitment and selection process starts. Head office provides

power to the branch head for recruitment & selection at junior level. Branch head

specify the requirement like skill, education, experience etc. After that though

interview recruitment & selection process done.

At senior management level recruitment & selection is Completed through

head office. JM Financial generally use advertisement etc. to generate the

application.After screening the application, some written test & interview is use for

final selection.

23

Each branch send their requirement to Head office

Head office collects the data of requirement of each

branchHead office check whether the person actually required

After that Head office do actual HRP for each branch

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 24/112

Level Source of recruitment Selection

method

Selection at

Junior management Level Internal source mainly

though reference

Interview Branch level

Senior management Level External source mainly

though advertisement

Interview Head office

level

Training & Development

Whenever a new employ is recruited training is provided to the new employ.

The number of days of training is depends on which types of work the person is going

to do. But it is on an average 15 days to 20 days training is provided to a new employ.

Promotion policy

Promotion is provided on JM Financial strictly on the merit based.

Performance appraisal plays the key role in the promotion. The employ who has

highly rated in his performance appraisal has better chance of getting promotion.

Transfer policy

Organization reserves the transfer whenever need arise. Organization can

transfer any employ at different branch in same city or different city.

24

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 25/112

Welfare facility of the organization

• Picnic once in a year

• Performance bonus

• Tea 3-4 times in a day

• Competition among employ child & some prize distribution

Budgetary control system

Budgetary system is control head office in Bombay. all the major decision

regarding the budget are taken at H.O , but execution is done at different branches .

Board meeting

The board meeting is held quarterly at head office. they make all the kind of

decisions including the regular work and also the researches they make .

Senior management decision

The senior management makes all the tactical decisions regarding all the

major investment in the different branches.

Operating decision

These decisions are made by the head of the branches the operating decisions

includes all the day to day working decisions

There is nice and smooth coordination among all the layers in the organizationthe work is allocated as per the qualification as well as the specialization.

Distribution Channel

JMFS wants to reach deep in the market. It has very good link with sub

broker. So by sub broker chain company try to reach it`s target market.

25

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 26/112

DECISION MAKING

Strategic Decision Area at JM Financial

JM Financial use a systematic method to identity strategic decision area. Thestrategic decision area is mainly concern with long term goals and objective of a firm.

External environment is a great impact on organizational strategic decision area.

The main strategic decisions areas in JM Financial are are:

Whether to open new branch or not

Where to open new branch

Where to close down the branch

Policy to deal with competition in long run

Decide the wage & salary structure to retain employ

Recruitment & selection decision

Overall firm plan to survival in the long run

Strategic Decision making process of firm

Key feature strategic decision making in JM Financial

Centralized decision making

Fully control by head office Mumbai

Key role top management

Decision for long run goal of a farm

Process of Strategic Decision making

1. Analysis of internal & external environment

2. Analysis of strength & weakness of firm

3. Find the list of need

4. Provide the priority of need

5. Make the final strategic decision

6. Get approval & implementation

26

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 27/112

Tactical & operational decisions in JM Financial

The main tactical & operational areas are

Day to day decision of firm

Decision to deal with short term competition

Decision of recruitment & selection at junior level

Key feature of operational decision at JM Financial

Centralized decision

Decision at head office Mumbai

Implemented by the branch head at respective branch

Process of operational & tactical decision

1. Branch head find the requirement of its own branch

2. It send its requirement at head office

3. It also send his idea view etc. what has to done to solve the problem

4. Branch head analysis all the requirement

5. Final decision taken by branch head

6. Implementation is done on respective branches

Formal power relation

JM Financial follow hierarchy for decision making. At branch level power is

in the hand of branch head. He is responsible for at branch activity. All other

employee at branch level has power to do their own work but branch head give final

approval.

27

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 28/112

But the strategic decision or operational decision all the power goes to top

management. Top management has a power to take long term and short term decision

of a firm. Branch manager has very little power in this regard.

Informal power relation

All though branch head has very little power in decision making but top

management always welcome his suggestion.

At branch level also branch head provide freedom to the employees for givingsuggestion in branch level decision making and suggestion play an important role in

decision making.

28

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 29/112

FINANCIAL ANALYSIS

JM Financial

Profit & Loss account ------------------- in Rs. Cr. -------------------

Mar '05 Mar '06 Mar '07 Mar '08 Mar '09

12 mths 12 mths 12 mths 12 mths 12 mths

Income

Sales Turnover 13.41 13.40 39.32 33.64 24.46

Excise Duty 0.00 0.00 0.00 0.00 0.00

Net Sales 13.41 13.40 39.32 33.64 24.46

Other Income -3.69 4.22 0.06 1,736.77 -1.74Stock Adjustments 0.00 0.00 0.00 0.00 0.00

Total Income 9.72 17.62 39.38 1,770.41 22.72

Expenditure

Raw Materials 0.00 0.00 0.00 0.00 0.00

Power & Fuel Cost 0.00 0.00 0.00 0.00 0.00

Employee Cost 0.00 0.15 1.29 3.68 4.44

Other Manufacturing

Expenses0.00 0.00 0.00 0.00 0.00

Selling and Admin Expenses 0.16 1.27 1.21 10.94 1.41Miscellaneous Expenses 0.08 0.45 1.13 3.83 3.41

Preoperative Exp Capitalised 0.00 0.00 0.00 0.00 0.00

Total Expenses 0.24 1.87 3.63 18.45 9.26

29

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 30/112

Mar '05 Mar '06 Mar '07 Mar '08 Mar '09

Particulars 12 mths 12 mths 12 mths 12 mths 12 mths

Operating Profit 13.17 11.53 35.69 15.19 15.20PBDIT 9.48 15.75 35.75 1,751.96 13.46

Interest 0.00 0.00 0.00 0.05 0.04

PBDT 9.48 15.75 35.75 1,751.91 13.42

Depreciation 0.02 0.02 0.03 0.10 0.27

Other Written Off 0.00 0.00 0.00 0.00 0.00

Profit Before Tax 9.46 15.73 35.72 1,751.81 13.15

Extra-ordinary items 0.00 -0.01 0.00 0.01 -0.02

PBT (Post Extra-ord Items) 9.46 15.72 35.72 1,751.82 13.13

Tax -0.01 0.45 0.42 391.63 5.17Reported Net Profit 9.48 15.27 35.31 1,360.16 7.97

Total Value Addition 0.24 1.87 3.62 18.46 9.26

Preference Dividend 0.00 0.00 0.00 0.00 0.00

Equity Dividend 2.83 7.50 15.00 75.00 15.00

Corporate Dividend Tax 0.40 1.05 2.55 12.75 0.05

Per share data (annualised)

Shares in issue (lakhs) 113.25 155.25 300.00 300.00 7,497.83

Earning Per Share (Rs) 8.37 9.83 11.77 453.39 0.11

Equity Dividend (%) 25.00 25.00 50.00 250.00 20.00

Book Value (Rs) 28.34 140.87 127.00 551.15 21.96

30

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 31/112

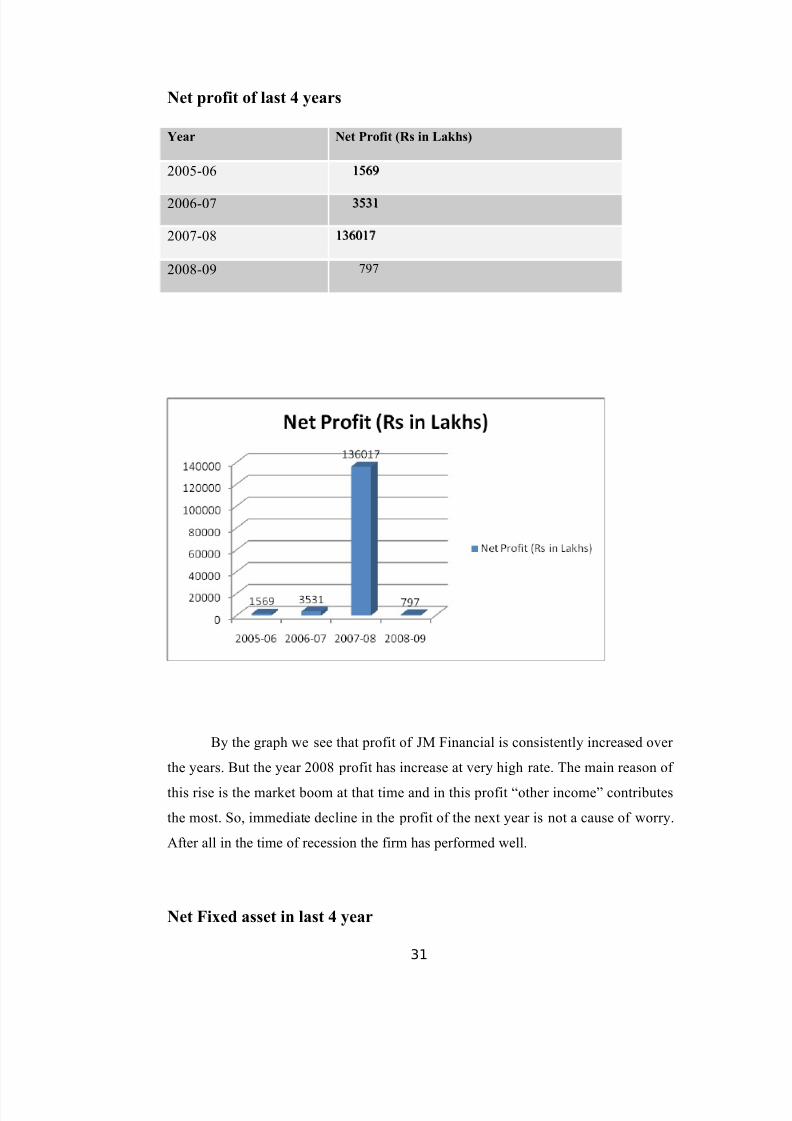

Net profit of last 4 years

Year Net Profit (Rs in Lakhs)

2005-06 15691569

2006-07 35313531

2007-08 136017136017

2008-09 797

By the graph we see that profit of JM Financial is consistently increased over

the years. But the year 2008 profit has increase at very high rate. The main reason of

this rise is the market boom at that time and in this profit “other income” contributes

the most. So, immediate decline in the profit of the next year is not a cause of worry.

After all in the time of recession the firm has performed well.

Net Fixed asset in last 4 year

31

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 32/112

JM Financial

Balance Sheet ------------------- in Rs. Cr. -------------------

Mar '05 Mar '06 Mar '07 Mar '08 Mar '09

12 mths 12 mths 12 mths 12 mths 12 mths

Sources Of Funds

Total Share Capital 11.29 15.50 29.98 29.98 74.97

Equity Share Capital 11.29 15.50 29.98 29.98 74.97

Share Application Money 0.00 12.37 0.00 0.00 0.00

Preference Share Capital 0.00 0.00 0.00 0.00 0.00

Reserves 20.81 203.19 351.02 1,623.46 1,571.40

Revaluation Reserves 0.00 0.00 0.00 0.00 0.00

Networth 32.10 231.06 381.00 1,653.44 1,646.37Secured Loans 0.00 0.00 0.00 0.00 0.00

Unsecured Loans 0.00 0.00 0.00 0.15 0.28

Total Debt 0.00 0.00 0.00 0.15 0.28

Total Liabilities 32.10 231.06 381.00 1,653.59 1,646.65

Mar '05 Mar '06 Mar '07 Mar '08 Mar '09

12 mths 12 mths 12 mths 12 mths 12 mths

Application Of Funds

Gross Block 1.09 1.09 1.18 1.90 2.34

Less: Accum. Depreciation 0.23 0.24 0.27 0.37 0.62

Net Block 0.86 0.85 0.91 1.53 1.72

Capital Work in Progress 0.00 0.00 0.00 0.04 0.00

Investments 31.13 148.16 350.65 1,521.43 1,524.08

Inventories 0.00 0.00 0.00 0.00 0.00

Sundry Debtors 0.00 0.00 0.00 0.00 0.00

Cash and Bank Balance 0.18 0.67 0.82 0.48 0.85

Total Current Assets 0.18 0.67 0.82 0.48 0.85

Loans and Advances 4.89 92.71 48.81 101.65 103.75

Fixed Deposits 0.00 0.00 0.00 238.65 150.68

Total CA, Loans &

Advances5.07 93.38 49.63 340.78 255.28

Deffered Credit 0.00 0.00 0.00 0.00 0.00

Current Liabilities 1.74 2.77 2.65 122.37 118.96

Provisions 3.23 8.55 17.55 87.81 15.46

Total CL & Provisions 4.97 11.32 20.20 210.18 134.42

32

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 33/112

Net Current Assets 0.10 82.06 29.43 130.60 120.86

Miscellaneous Expenses 0.00 0.00 0.00 0.00 0.00

Total Assets 32.09 231.07 380.99 1,653.60 1,646.66

Contingent Liabilities 3.59 3.59 3.58 3.80 4.27

Book Value (Rs) 28.34 140.87 127.00 551.15 21.96

Net Fixed asset in last 4 year

Year 2005-

06

2006-

07

2007-

08

2008-

09

Fixed Assets

(Rs in lakhs)

85.99 84.21 90.84 153.17

From the graph we see that JM Financial`s fixed asset has increased over the

years. By the end of 2008-09 the fixed asset of JM financial 172.67 lakhs which is

increased by 105.05% as compare to the year of 2005-06. So it shows that organization

is doing well and organization has enough funds to in invest in fixed assets.

33

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 34/112

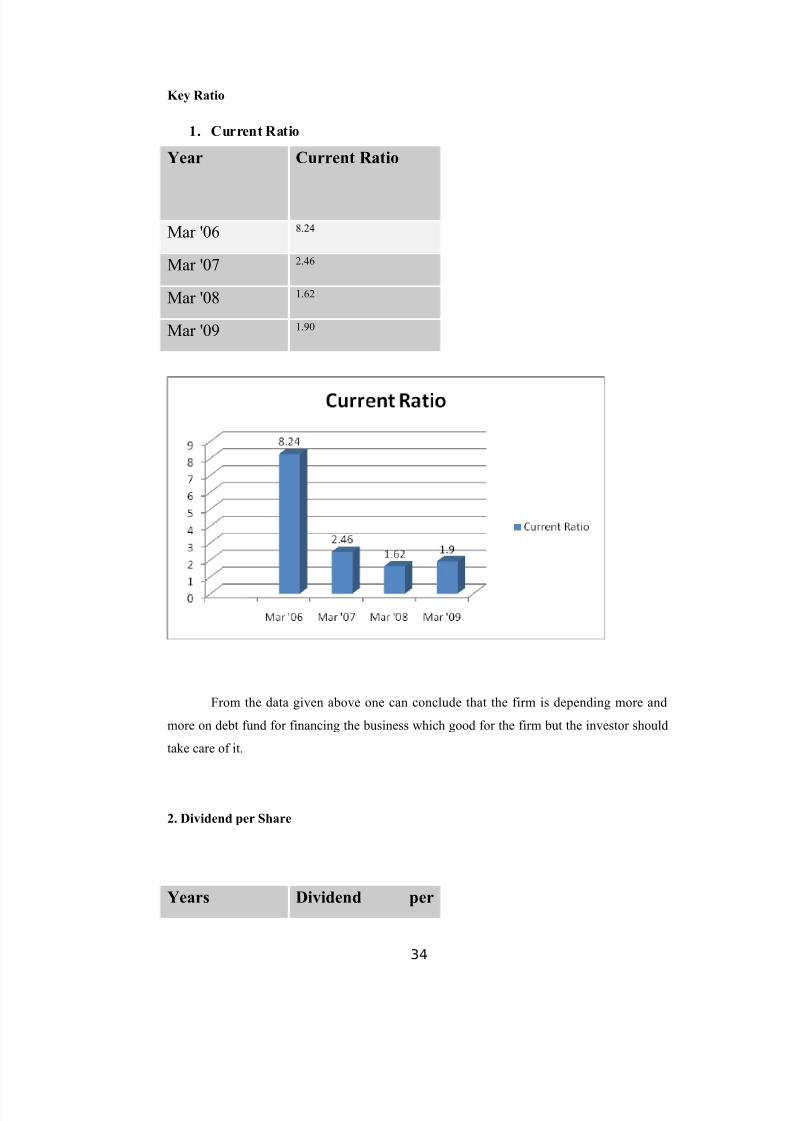

Key Ratio

1. Current Ratio

Year Current Ratio

Mar '06 8.24

Mar '07 2.46

Mar '08 1.62

Mar '09 1.90

From the data given above one can conclude that the firm is depending more and

more on debt fund for financing the business which good for the firm but the investor should

take care of it.

2. Dividend per Share

Years Dividend per

34

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 35/112

share

Mar '06 02.50

Mar '07 05.00

Mar '08 25.00

Mar '09 00.20

From the above graph we can one can say that dividend per share is increasing. From

the year 2006 to 2008 dividend per share has increased by 900%. But in 2009 it declined. The

reason is “Stock split “. The Share of JM has splited into 10 and now it of Rs.1 F.V. which

was previously of Rs 10 each.

3. Gross Profit Ratio

Year G.P. Ratio (in %)

March 2008 44.82

March 2009 61.04

35

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 36/112

The profit margin of the firm is considerably increased as compare to past year. The

profit margin has increased even after the year was of recession which is good sign factor.

Financial health of the organization

Financial health of the organization is very good the reasons are

The organization has performed well even in recession period.

The ratio of the organization is also very good

Organization has not any major loan liability it is also a good sign.

Organization EPS is also very good.

Future of the organization

JM Financial is growth oriented organization the future of JM Financial is looking

bright. It happen that JM Financial may not earn super normal profit like 2008 but in the long

run the future of the organization is very good.

36

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 37/112

MY LEANINGS FROM THE STUDY

The objective of the summer training at the M.B.A level is to develop the idea

about the industrial environment as well as business practices in order to develop the a

practical skills as a supplement to theoretical study of management in general . After

this training I realize how the real world works

Now I am in better position to understand the hierarchy how the different

department are loaded with responsibilities and accountability. How the top

management control the activities and the work of bottom level.

The study of organizational behaviour has help me to realize how an

individual’s behave in work stress what are relationship between the different

employees particularly at the operation level

The analysis and interpretation of cost has made me realize how important the

costing is for any organization weather production or a service particularly at the

J.M.F.S the cost cutting is high due to the recession.

In J.M. Finanacial, marketing is done through their strong contacts with their

clients and sub brokers whenever a new N.F.O or an I.P.O is comes they contact their

customers and inform them. The individual financial advisory groups stay in contacts

with customers and try build new through the existing ones.

Finance is the life blood of any organization here at the J.M.F.S I realize how

finance is related with all the other. The working pattern of J.M.F.S depends heavily

on the performance of the stock market this thing roves from the profit which J.M has

reached, when the stock market was 21000 mark in 2008

37

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 38/112

I also learned many new things as well from J.M such as how trading is done

how investors react in bull and bear period.I also got the idea about mutual fund &

How it works.

Mutual Fund Operation Flow Chart

Meaning

A Mutual Fund invests the pool of money collected from the investors in a

range of securities comprising equities, debt, money market instruments etc.

The main advantages of the mutual funds are

Capital appreciation

Dividend distribution

Diversified risk

Diversified porthfolio

We came to know various terms like of share market

Stock futures

Stoke option

Difference between share, mutual fund and fixed deposits

38

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 39/112

(A) MUTUAL FUND

1. INTRODUCTION:

A Mutual Fund is a trust that pools the savings of a number of investors who

share a common financial goal. The money thus collected is invested by the fund

manager in different types of securities depending upon the objective of the scheme.

These could range from shares to debentures to money market instruments. The

income earned through these investments and the capital appreciations realized by the

scheme are shared by its unit holders in proportion to the number of units owned by

them (pro rata). Thus a Mutual Fund is the most suitable investment for the common

man as it offers an opportunity to invest in a diversified, professionally managed

portfolio at a relatively low cost. Anybody with an inventible surplus of as little as a

few thousand rupees can invest in Mutual Funds. Each Mutual Fund scheme has a

defined investment objective and strategy.

A Mutual fund is

the ideal investment vehicle

for today’s complex and

modern financial scenario.

Markets for equity shares,

bonds and other fixed

income instruments, real estate, derivatives and other assets have become mature andinformation driven. Price changes in these assets are driven by global events

occurring in faraway places. A typical individual is unlikely to have the knowledge,

skills, inclination and time to keep track of events, understand their implications and

act speedily. A draft offer document is to be prepared at the time of launching the

fund. Typically, it pre specifies the investment objectives of the fund, the risk

associated, the costs involved in the process and the broad rules for entry into and exit

from the fund and other areas of operation. In India, as in most countries, these

sponsors need approval from a regulator, SEBI (Securities exchange Board of India)

39

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 40/112

in our case. SEBI looks at track records of the sponsor and its financial strength in

granting approval to the fund for commencing operations.

A sponsor then hires an asset management company to invest the funds

according to the investment objective. It also hires another entity to be the custodian

of the assets of the fund and perhaps a third one to handle registry work for the unit

holders (subscribers) of the fund. In the Indian context, the sponsors promote the

Asset Management Company also, in which it holds a majority stake. In many cases a

sponsor can hold a 100% stake in the Asset Management Company (AMC). E.g. Birla

Global Finance is the sponsor of the Birla Sun Life Asset Management Company

Ltd., which has floated different mutual funds schemes and also acts as an asset

manager for the funds collected under the schemes.

Characteristics:

• A mutual fund actually belongs to the investors who have pooled their funds.

• A mutual fund is managed by investment professionals and other service providers,

who earn a fee for their services, from the fund.

• The pool of funds is invested in a portfolio of marketable investments. The value of

the portfolio is updated every day.

• The investor’s share in the fund is denominated by ‘units’. The value of the units

changes with change in the portfolio’s value, every day. The value of one unit of

investment is called the Net Asset Value or NAV.

40

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 41/112

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 42/112

90), Bank of Baroda Mutual Fund (Oct 92). LIC established its mutual fund in June

1989 while GIC had set up its mutual fund in December 1990. At the end of 1993, the

mutual fund industry had assets under management of Rs.47,004 crores.

Third Phase – 1993-2003 (Entry of Private Sector Funds) With the entry of private

sector funds in 1993, a new era started in the Indian mutual fund industry, giving the

Indian investors a wider choice of fund families. Also, 1993 was the year in which the

first Mutual Fund Regulations came into being, under which all mutual funds, except

UTI were to be registered and governed. The erstwhile Kothari Pioneer (now merged

with Franklin Templeton) was the first private sector mutual fund registered in July

1993. The industry now functions under the SEBI (Mutual Fund) Regulations 1996.

The number of mutual fund houses went on increasing, with many foreign mutual

funds setting up funds in India and also the industry has witnessed several mergers

and acquisitions. As at the end of January 2003, there were 33 mutual funds with total

assets of Rs. 1,21,805 crores. The Unit Trust of India with Rs.44,541 crores of assets

under management was way ahead of other mutual funds.

Fourth Phase – since February 2003 In February 2003, following therepeal of the Unit Trust of India Act 1963 UTI was bifurcated into two separate

entities. One is the Specified Undertaking of the Unit Trust of India with assets under

management of Rs.29,835 crores as at the end of January 2003, representing broadly,

the assets of US 64 scheme, assured return and certain other schemes. It is registered

with SEBI and functions under the Mutual Fund Regulations. With the bifurcation of

the erstwhile UTI which had in March 2000 more than Rs.76,000 crores of assets

under management and with the setting up of a UTI Mutual Fund, conforming to the

SEBI Mutual Fund Regulations, and with recent mergers taking place among different

private sector funds, the mutual fund industry has entered its current phase of

consolidation and growth.

42

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 43/112

GROWTH IN ASSETS UNDER MANAGEMENT

Note: Erstwhile UTI was bifurcated into UTI Mutual Fund and the Specified

Undertaking of the Unit Trust of India effective from February 2003. The Assets

under management of the Specified Undertaking of the Unit Trust of India has

therefore been excluded from the total assets of the industry as a whole from February

2003 onwards.

43

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 44/112

3. MUTUAL FUND STRUCTURE:

The Structure Consists

The structure of mutual funds in India is governed by the SEBI Regulations,

1996. These regulations make it mandatory for mutual funds to have a 3-tier structure

of Sponsors-Trustee-AMC (Asset Management Company). The Trustees are

responsible to the investors in the mutual funds, and appoint the AMC for managing

the investment portfolio. The AMC is the business face of the mutual funds, as it

manages all the affairs of mutual funds. The mutual funds and AMC have to be

registered by the SEBI.

Sponsor

Sponsor is the person who acting alone or in combination with another body

corporate establishes a mutual fund. Sponsor must contribute at least 40% of the net

worth of the Investment Managed and meet the eligibility criteria prescribed under the

Securities and Exchange Board of India (Mutual Funds) Regulations, 1996.The

Sponsor is not responsible or liable for any loss or shortfall resulting from the

44

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 45/112

operation of the Schemes beyond the initial contribution made by it towards setting up

of the Mutual Fund

Trust

The Mutual Fund is constituted as a trust in accordance with the provisions of the

Indian Trusts Act, 1882 by the Sponsor. The trust deed is registered under the Indian

Registration Act, 1908.

Trustee

Trustee is usually a company (corporate body) or a Board of Trustees (body of

individuals). The main responsibility of the Trustee is to safeguard the interest of the

unit holders and inter-alia ensure that the AMC functions in the interest of investors

and in accordance with the Securities and Exchange Board of India (Mutual Funds)

Regulations, 1996, the provisions of the Trust Deed and the Offer Documents of the

respective Schemes. At least 2/3rd directors of the Trustee are independent directors

who are not associated with the Sponsor in any manner.

Asset Management Company (AMC)

The AMC is appointed by the Trustee as the Investment Manager of the

Mutual Fund. The AMC is required to be approved by the Securities and Exchange

Board of India (SEBI) to act as an asset management company of the Mutual Fund. At

least 50% of the directors of the AMC are independent directors who are not

associated with the Sponsor in any manner. The AMC must have a net worth of at

least 10 crores at all times.

Registrar and Transfer Agent

The AMC if so authorized by the Trust Deed appoints the Registrar and

Transfer Agent to the Mutual Fund. The Registrar processes the application form,

redemption requests and dispatches account statements to the unit holders.

Custodian

A custodian handles the investment back office of a mutual fund. Its responsibilities

include receipt and delivery of securities, collection of income, distribution of dividends, and segregation of assets between schemes.

45

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 46/112

4. MUTUAL FUND OPERATION:

HOW DOES A MUTUAL FUND WORK ?

Mutual Fund Operation Flow Chart

46

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 47/112

5. TYPES OF MUTUAL FUND:

47

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 48/112

A Mutual Fund may float several schemes, which may be classified on the

basis of its structure, its investment objectives and other objectives.

Type of Mutual Fund on the bases of constitution:

Open – Ended Schemes

As the name implies the size of the scheme (fund) is open – i.e. not specified

or pre-determined. Entry to the fund is always open, the investor who can subscribe at

anytime. Such fund stands ready to buy or sell its securities at anytime. The key

feature of Open-ended schemes is Liquidity. It implies that the capitalization of the

fund is constantly changing as investors sell or buy their shares. Further, the shares or

units are normally not traded on the stock exchange but are repurchased by the funds

at announced rates. Open-ended schemes have comparatively better liquidity despite

the fact that these are not listed. The reason is that investors can any time approach

mutual fund for sale of such units. No intermediaries are required. Moreover, the

realizable amount is certain since repurchase is at a price based on declared net asset

value (NAV). The portfolio mix of such schemes has to be investments, which are

actively traded in the market. Otherwise it will not be possible to calculate NAV. This

is the reason that generally open-ended schemes are equity based. In Open-ended

schemes, the option of dividend reinvestment is available.

Close-Ended Schemes

A Close – ended schemes have a definite period after which their shares/units

are redeemed. The scheme is open for subscription only during a specified period at

the time of launch of a scheme. Investors can invest in the scheme at the time of the

initial public issue and thereafter they can buy or sell the units of the scheme on the

stock exchanges where the units are listed. In order to provide an exit route to the

investors, some close-ended funds give an option of selling back the units to the

mutual fund through periodic repurchase at NAV related prices. In these types of

schemes, the size of the fund kept to be constant. SEBI regulations stipulate that at

least one of the two exit routes is provided to the investor i.e. either repurchase

facility or through listing on stock exchanges. These mutual funds schemes disclose NAV generally on weekly basis.

48

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 49/112

Interval schemes

Interval Schemes combine the features of both open-ended and close-ended

schemes. They are open for sale or redemption during pre-determined intervals at

NAV based prices.

Mutual Fund schemes by Investment Objectives:

EQUITY FUNDS

These funds invest a major part of their corpus in equities. The composition of the

fund may vary from scheme to scheme and the fund manager’s outlook on various

scrip’s. The Equity Funds are sub-classified depending upon their investment

objective, as follows:

1. Growth Fund:

Aim to provide capital appreciations over the medium to long term. These

schemes normally invest a majority of their funds in equities and are willing to bear

short term decline in value for possible future appreciation. These schemes are not for

investors seeking regular income or needing their money back in the short-term

2. Diversified Equity Fund:

Diversified equity funds are the most popular among investors. They invest in

many stocks across many sectors, and because they have the freedom to chop and

churn their portfolios as they like, diversified equity funds are a good proxy to the

stock market. If a general exposure to equities is what you want, they are a good

option. They can invest in all listed stocks, and even in unlisted stocks.

3. Equity – Linked Savings Schemes (ELSS):

Equity – linked savings schemes (ELSS) are diversified equity funds that

additionally offer income tax benefits to individuals. ELSS is one of the many section

49

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 50/112

80c instruments, along with the more popular debt options like the PPF, NSC and

infrastructure bonds. In this Section 80c grouping. ELSS is unique.

4. Index Fund:

An index fund is a diversified equity fund; with a difference- a fund manager has

absolutely no say in stock selection. At all times, the portfolio of an index fund

mirrors an index, both in its choice of stocks and their percentage holding. As of

March 2004, equity index funds tracked either the Sensex or the Nifty. So, an index

fund that mirrors the Sensex will invest only in the 30 Sensex stocks, which too in the

same proportion as their weight age in the index.

5. Sector Fund:

Sector funds invest in stocks from only one sector, or a handful of sectors. The

objective is to capitalize on the story in the sectors, and offer investors a window to

profit from such opportunities. It’s a very narrow focus, because of which sector

funds are considered the riskiest among all equity funds.

6. Mid – Cap Fund:

These are diversified funds that target companies on the fast – growth trajectory.

In the long run, share prices are driven by growth in a company’s turnover and profits.

Market players refer to them as ‘mid-sized companies’ and ‘mid-cap stocks’ with size

in this context being benchmarked to a company’s market value. So, while a typical

large cap stock would have a market capitalization of over Rs 1,000 crores, a mid-cap

stock would have a market value of Rs 250-2,000 crores.

50

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 51/112

DEBT FUNDS

These Funds invest a major portion of their corpus in debt papers. Government

authorities, private companies, banks and financial institutions are some of the major

issuers of debt papers. By investing in debt instruments, these funds ensure low risk

and provide stable income to the investors.

Debt funds are further classified as:

1. Gilt Funds:

Invest their corpus in securities issued by Government, popularly known as GOI

debt papers. These Funds carry zero Default risk but are associated with Interest Rate

risk. These schemes are safer as they invest in papers backed by Government.

2. Income Funds:

Income funds aim to maximize debt returns for the medium to longer term. Invest

a major portion into various debt instruments such as bonds, corporate debentures and

Government securities.

3. MIPs:

Invests around 80% of their total corpus in debt instruments while the rest of the

portion is invested in equities. It gets benefit of both equity and debt market. These

scheme ranks slightly high on the risk-return matrix when compared with other debt

schemes.

4. Short Term Plans (STPs):

Meant for investors with an investment horizon of 3-6 months. These funds

primarily invest in short term papers like Certificate of Deposits (CDs) and

Commercial Papers (CPs). Some portion of the corpus is also invested in corporate

debentures.

5. Liquid Funds:

Also known as Money Market Schemes, These funds are meant to provide easy

liquidity and preservation of capital. These schemes invest in short-term instruments

51

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 52/112

like Treasury Bills, inter-bank call money market etc. These funds are meant for

short-term cash management of corporate houses and are meant for an investment

horizon of 1day to 3 months. These schemes rank low on risk-return matrix and are

considered to be the safest amongst all categories of mutual funds.

6. Floating Rate Funds:

These income funds are more insulated from interest rate than their conventional

peers. In other words, interest rate changes, which cause the NAV of a conventional

debt fund to go up or down, have little, or no, impact on NAVs of floating rate funds.

BALANCED FUNDS

These funds, as the name suggests, are a mix of both equity and debt funds.

They invest in both equities and fixed income securities, which are in line with pre-

defined investment objective of the scheme. These schemes aim to provide investors

with the best of both the worlds. Equity part provides growth and the debt part

provides stability in returns.Each category of funds is backed by an investment

philosophy, which is pre-defined in the objectives of the fund. The investor can align

his own investment needs with the funds objective and invest accordingly.

HYBRID FUNDS

Growth and Income Fund:

Strike a balance capital appreciation and income for the investors. In these

funds portfolio is a mix between companies with good dividend paying record and

those with potential capital appreciation. These funds are less risky than growth funds

bit more than income funds.

52

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 53/112

6. COMPARISON OF MUTUAL FUND:

53

MutualFund

ObjectiveRisk

Investment

Portfolio

Who Should

Invest

Investment

Horizon

Equity

Funds

Long-term CapitalAppreciation

High Risk Stocks & SharesAggressive investors

Long term Inv.

3

years +

Balanced

Funds

Growth & Regular

Income

CapitalMarket Risk

and InterestRisk

Balanced ratio of equityand debt funds to ensure

higher returns at lower risk

Moderate &

Aggressive

2

years +

Index

Funds

To generate returnsthat arecommensurate withreturns of respectiveindices

NAV varieswith index

performance

Portfolio índices likeBSE, NIFTY etc

Aggressive investors.3

years +

Gilt Funds Security & IncomeInterest RateRisk

Government securitiesSalaried &conservative investors

12

months +

Bond

FundsRegular Income

Credit Risk &Interest RateRisk

Debentures,

Govt securities,Corporate Bonds

Salaried &conservative investors

12

months +

Money

Market

Liquidity +Moderate Income +Reservation of Capital

Negligible

Treasury Bills,Certificate of Deposits,Commercial Papers,Call Money

Park funds in currentA/cs or short-termBank Dep.

2 days

- 3 weeks

Short-termFunds

(Floating -

short-term)

Liquidity +Moderate Income

Little InterestRate

Call Money,CommPapers, TreasuryBills, CDs, Short-termGovt. securities.

Those with surplusshort-term funds

3 weeks -3 months

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 54/112

7. ADVANTAGES OF MUTUAL FUND:

Mutual Funds offer several benefits to an investor that are unmatched by the other

investment options. Last six years have been the most turbulent as well as exiting

ones for the industry. New players have come in, while others have decided to close

shop by either selling off or merging with others. Product innovation is now passé

with the game shifting to performance delivery in fund management as well as

service. Those directly associated with the fund management industry like

distributors, registrars and transfer agents, and even the regulators have become more

mature and responsible.

1. Affordability :

Small investors with low investment fund are unable to invest in high-grade or

blue chip stocks. An investor through Mutual Funds can be benefited from a portfolio

including of high priced stock.

2. Diversification :

Investor’s investment is spread across different securities (stocks, bonds, moneymarket, real estate, fixed deposits etc.) and different sectors (auto, textile, IT etc.).

54

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 55/112

This kind of a diversification add to the stability of returns, reduces the risk for

example during one period of time equities might underperform but bonds and money

market instruments might do well do well and may protect principal investment as

well as help to meet return objectives.

3. Variety :

Mutual funds offer a tremendous variety of schemes. This variety is beneficial in

two ways: first, it offers different types of schemes to investors

4. Professional Management:

Mutual Funds employ the services of experienced and skilled professionals and

dedicated investment research team. The whole team analyses the performance and

balance sheet of companies and selects them to achieve the objectives of the scheme.

5. Tax Benefits:

Depending on the scheme of mutual funds, tax shelter is also available. As per the

Union Budget-99, income earned through dividends from mutual funds is 100% tax

free. Under ELSS of open-ended equity-oriented funds an exemption is provided up

to Rs. 100,000/- under section 80C.

6. Regulation:

All Mutual Funds are registered with SEBI and they function within the

provisions of strict regulations designed to protect the interests of investors. The

operations of Mutual Funds are regularly monitored by SEBI.

55

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 56/112

8. DISADVANTAGES OF MUTUAL FUND:

The following are the disadvantages of investing through mutual fund:

• No control over cost:

Since investors do not directly monitor the fund’s operations, they cannot control the

costs effectively. Regulators therefore usually limit the expenses of mutual funds.

• No tailor-made portfolio:

Mutual fund portfolios are created and marketed by AMCs, into which investors

invest. They cannot made tailor made portfolio.

• Managing a portfolio of funds:

As the number of funds increase, in order to tailor a portfolio for himself, an investor

may be holding portfolio funds, with the costs of monitoring them and using hem,

being incurred by him.

• Delay in Redemption:

The redemption of the funds though has liquidity in 24-hours to 3 days takes formalapplication as well as needs time for redemption. This becomes cumbersome for the

investors.

• Non-availability of loans:

Mutual funds are not accepted as security against loan. The investor cannot deposit

the mutual funds against taking any kind of bank loans though they may be his assets.

56

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 57/112

9. RISK INVOLVED IN MUTUAL FUND:

THE RISK-RETURN TRADE-OFF

The most important relationship to understand is the risk-return trade-off.

Higher the risk greater the returns/loss and lower the risk lesser the returns/loss.

Hence it is up to you, the investor to decide how much risk you are willing to take. Inorder to do this you must first be aware of the different types of risks involved with

your investment decision.

MARKET RISK:

Sometimes prices and yields of all securities rise and fall. Broad outside

influences affecting the market in general lead to this. This is true, may it be big

corporations or smaller mid-sized companies. This is known as Market Risk. A

Systematic Investment Plan (“SIP”) that works on the concept of Rupee Cost

Averaging (“RCA”) might help mitigate this risk.

CREDIT RISK:

The debt servicing ability (may it be interest payments or repayment of

principal) of a company through its cash flows determines the Credit Risk faced by

you. This credit risk is measured by independent rating agencies like CRISIL who rate

companies and their paper

57

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 58/112

INFLATION RISK:

Things you hear people talk about: “Rs. 100 today is worth more than Rs. 100

tomorrow.” “Remember the time when a bus ride costed 50 paisa?”

“Mehangai Ka Jamana Hai.”

The root cause, Inflation. Inflation is the loss of purchasing power over time.

A lot of times people make conservative investment decisions to protect their capital

but end up with a sum of money that can buy less than what the principal could at the

time of the investment. This happens when inflation grows faster than the return on

your investment. A well-diversified portfolio with some investment in equities might

help mitigate this risk.

INTEREST RATE RISK:

In a free market economy interest rates are difficult if not impossible to

predict. Changes in interest rates affect the prices of bonds as well as equities. If

interest rates raise the prices of bonds fall and vice versa. Equity might be negatively

affected as well in a rising interest rate environment. A well-diversified portfolio

might help mitigate this risk.

POLITICAL/GOVERNMENT POLICY RISK:

Changes in government policy and political decision can change the

investment environment. They can create a favourable environment for investment or

vice versa. LIQUIDITY RISK:

Liquidity risk arises when it becomes difficult to sell the securities that one

has purchased. Liquidity Risk can be partly mitigated by diversification, staggering of

maturities as well as internal risk controls that lean towards purchase of liquid

securities.

58

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 59/112

10. NET ASSET VALUE:

Net Asset Value (NAV)

The net asset value of the fund is the cumulative market value of the assetsfund net of its liabilities. In other words, if the fund is dissolved or liquidated, by

selling off all the assets in the fund, this is the amount that the shareholders would

collectively own. This gives rise to the concept of net asset value per unit, which is

the value, represented by the ownership of one unit in the fund. It is calculated simply

by dividing the net asset value of the fund by the number of units. However, most

people refer loosely to the NAV per unit as NAV, ignoring the "per unit". We also

abide by the same convention.

Definition of NAV

Net Asset Value, or NAV, is the sum total of the market value of all the shares

held in the portfolio including cash, less the liabilities, divided by the total number of

units outstanding. Thus, NAV of a mutual fund unit is nothing but the 'book value.'

Calculation of NAV

The most important part of the calculation is the valuation of the assets owned

by the fund. Once it is calculated, the NAV is simply the net value of assets divided

by the number of units outstanding. The detailed methodology for the calculation of

the asset value is given below.

Asset value is equal to

Sum of market value of shares/debentures

+ Liquid assets/cash held, if any

+ Dividends/interest accrued Amount due on unpaid assets Expenses accrued but not

paid

59

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 60/112

NAV per unit = Other liabilities/ No. of units outstanding of the scheme

Details on the above items

For liquid shares/debentures, valuation is done on the basis of the last or closing

market price on the principal exchange where the security is traded.

For illiquid and unlisted and/or thinly traded shares/debentures, the value has to be

estimated. The value of fixed interest bearing securities moves in a direction opposite

to interest rate changes Valuation of debentures and bonds is a big problem since most

of them are unlisted and thinly traded. This gives considerable leeway to the AMCs

on valuation and some of the AMCs are believed to take advantage of this and adopt

flexible valuation policies depending on the situation.

Interest is payable on debentures/bonds on a periodic basis say every 6

months. But, with every passing day, interest is said to be accrued, at the daily interest

rate, which is calculated by dividing the periodic interest payment with the number of

days in each Period. Thus, accrued interest on a particular day is equal to the daily

interest rate multiplied by the number of days since the last interest payment date.

Usually, dividends are proposed at the time of the Annual General meetingand become due on the record date. There is a gap between the dates on which it

becomes due and the actual payment date. In the intermediate period, it is deemed to

be "accrued".

Expenses including management fees, custody charges etc. are calculated on a daily

basis.

NAV and its impact on the returns

We feel that a MF with lower NAV will give better returns. This again is due

to the wrong perception about NAV. An example will make it clear that returns are

independent of the NAV.

Say, you have Rs 10,000 to invest. You have two options, wherein the funds

are same as far as the portfolio is concerned. But say one Fund X has an NAV of Rs

10 and another Fund Y has NAV of Rs 50. You will get 1000 units of Fund X or 200

units of Fund Y.

60

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 61/112

After one year, both funds would have grown equally as their portfolio is

same, say by 25%. Then NAV after one year would be Rs 12.50 for Fund X and Rs

62.50 for Fund Y. The value of your investment would be 1000*12.50 = Rs 12,500

for Fund X and 200*62.5 = Rs 12,500 for Fund Y. Thus your returns would be same

irrespective of the NAV.

It is quality of fund, which would make a difference to your returns. In fact

for equity shares also broadly this logic would apply.

Misconception about NAV

This situation arises from the perception that a fund at Rs 10 is cheaper than

say Rs 15 or Rs 100. However, this perception is totally wrong and investors would

be much better off once they appreciate this fact.

Two funds with same portfolio are same, no matter what their NAV is. NAV

is immaterial. Why people carry this perception is because they assume that the NAV

of a MF is similar to the market price of an equity share. This, however, is not true.

61

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 62/112

11 . BASIC CONCEPTS OF LOADS:

1. Entry Load:

The load charged at the time of investment is known as entry load. It’s meant tocover the cost that the AMC spends in the process of acquiring subscriber’s

commission payable to brokers, advertisements, register expenses etc. The load is

recovered by way of charging a sale price higher than the prevailing NAV.

2. Exist Load:

Some AMC do not charge an entry load but they charged an exist load i.e., they

deduct a load before paying out the redemption proceeds. Psychologically, investors

are much more willing to pay exist loads as compared to entry loads.

3. Unit:

Units mean the investment of the unit holders in a scheme. Each unit represents one

undivided share in the assets of a scheme. The value of each unit changes, depending

on the performance of the fund.

62

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 63/112

12. FACTORS AFFECTING MUTUAL FUND:

1. Governmental Influences

Mutual fund business is a highly regulated business throughout the world as itseeks to ensure that quality and fairly priced schemes are available. Governmental

intervention thus in mutual fund market usually is most needed to ensure that insurers

are reliable. And in the developing countries the additional goal may be promotion of

domestic mutual fund industry and ensuring the national mutual fund industry

contributes to overall economic development. In a non technical sense mutual fund is

purchased in a good faith so the duty of government intervention in mutual fund

industry is to ensure that this principle of mutual fund is never defeated.

The ideology of government plays an important role in mutual fund industry also. For

example in the past during 1991, the P .V Narsimha Rao government strongly

believed in liberalization also liberalized the mutual fund sector which helped to allow

private players in the industry from 1993 and enhancing joint ventures with foreign

companies.

The present government with more focuses on foreign direct investments has declared

to favor the rise FDI in mutual fund to 49% which further enhances competition in the

industry.

2. Taxation Policy

Social equity being one of the motives behind tax collections, government gives

certain exemptions from such levying. One such exemption is deduction incurred by

taxpayers towards investment in mutual fund coverage. Similarly, capital invested in

infrastructure bonds etc is offered with certain concession under tax laws. The central

idea behind such exemptions is that the capitals so allocated by individuals reduce the

ultimate burden on the public infrastructure or helps in creating such infrastructural

facilities.

63

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 64/112

The income tax rules related to the mutual fund transactions can be classified

under:

A. Exemptions available to companies

• Expenses deductible from commission earned by distributor, banker, national

distributor.

• Tax concessions under risk management practices of an enterprise

• In growth option equity schemes there no long term capital gain by company.

• In dividend option equity schemes there no tax.

• Return received by charitable trust is total exempted from tax.

64

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 65/112

B. Tax rules governing investment by individuals

Deduction in respect of ELSS schemes (sec 80C): Investment in this fund

would enable you to avail the benefits under clause (xiii) of a section 80C of the

Income Tax Act investment made in the schemes up to 1 lakh by the eligible investor

for deduction under this section of the Act.

Since it will be an income deduction an investment of Rs 1 lakh in this fund

can save off Rs. 33600 from your tax payable liability (assuming you are in the

highest tax bracket).

Investor will receive tax free dividend in above case.

Investor will also receive tax free dividend by investing equity schemes in

dividend option Investors also receive tax free return by investing equity schemes in

growth option for long term capital gain.

Tax planning’s

An individual can think of health ELSS schemes purchase as a tool of tax planning exercise. For example people who are marginally affected by tax liability

can be as well purchase an ELSS fund get benefits of Rs. 33600 from tax. In this way

tax burden is become less by purchasing ELSS fund. Thus tax law offer benefit to

individuals/companies by way of exemptions/deductions of expenditure incurred

towards purchase of mutual fund various schemes coverage from total taxable

income.

3. Foreign Trade Regulations

With the vast potential for mutual fund in India due its large population in the country

many foreign companies are ready to enter into the Indian market. But companies can

be permitted in India through joint ventures with an Indian partner as well as come

separately and the foreign equity shall be restricted to only 25%. Another statement

also tells that Indian subsidiaries of foreign companies shall not be allowed to

participate in banking sector unless they entered in to joint ventures with the Indian

partners.

65

8/8/2019 Lokesh Final for Spiral

http://slidepdf.com/reader/full/lokesh-final-for-spiral 66/112

But at present the mutual fund regulator is in favor of hike in FDI cap from

25% to 49%, and is finalizing a report that will be submitted to the government for a

comprehensive legislation for the industry. The security exchange board of India and

association of mutual fund India have been advocating a hike in FDI limit for mutual

fund companies so that the foreign partners can infuse additional funds in these

companies to sustain their growth.

The government will need to amend the separate mutual fund Act for FDI capital as

well as domestic company as this is the statutory provision unlike sectors like civil

aviation and telecom, which have come through notification.

4. National Income

The relative importance of the mutual fund Market within a country will also

be dependent upon economic development. With greater rates of economic growth,

consumption of investment should increase as a result of increased income, and an

increased stock of assets requiring mutual fund. Furthermore, the development of

mutual fund is likely to facilitate greater economic growth, implying that economic

growth may be endogenous. Consistent with these arguments, studies find that the

level of financial development and economic development are positively related to thelevel of mutual fund across emerging markets.

5. Consumptions and Savings

The gross capital formation of any country is important for indication of its

growth in the future years. It is quite necessary to set up the rate of capital formation

so that a large stock of machines, tools and equipments are accumulated in a country.