living legacy ® iii introducing s henandoah l ife i nsurance c ompany presentation form #5409a –...

TRANSCRIPT

LIVING LEGACY®III

Introducing

SHENANDOAH LIFEINSURANCE COMPANY

Presentation Form #5409A – 3/07

Universal Life Insurance Policy Form L-1038-10/06

Single Premium Immediate Annuity (SPIA) A-3009-2/99

TheAnnuityAnnuity

Alternative

Living Legacy® III

Financial Realities Eventually, everyone with money

will have two choices...

Spend itor

pass it on to their loved ones.

Living Legacy® III

Financial Goals

The availability of funds for emergencies

Maximizing our estate

Minimizing taxes

Plus...

Until then we must be concerned about:

The safety of our money

Living Legacy® III

Peace of Mind

We all want safety for our money and accessibility during a time of need.

We all want to reduce federal income taxes for ourselves and our loved ones.

We all want to be prepared, financially,if we become permanently confined to a qualified nursing facility or become terminally ill.

Living Legacy® III

Peace of Mind

We all want our heirs to receive our estate...

without Uncle Sam being on our list of beneficiaries.

Living Legacy® III

Solving Tomorrow’s Solving Tomorrow’s Concerns…Concerns… Today.Today.

Living Legacy® III

How It Works:

Your existing non-qualified annuity money or qualified money* can be transferred to Shenandoah Life’s “10-Year Temporary Life Single Premium Immediate Annuity” via a 1035 exchange or qualified rollover/transfer.

You, as the policyowner, assign the annuity payouts to Shenandoah Life to be used to pay the premium on a Universal Life policy.

Living Legacy® III

* Funds from Roth IRA & SIMPLE IRA not accepted.

How It Works:

Shenandoah Life issues a Universal Life policy and the Immediate Annuity is irrevocably assigned to pay the life premiums for the next ten (10) years or until the annuitant’s death, whichever is sooner.

The taxable gain on the annuity disbursement is spread over the 10-year payout period, and you, the annuitant, receive a 1099 each year for 10 years.

Living Legacy® III

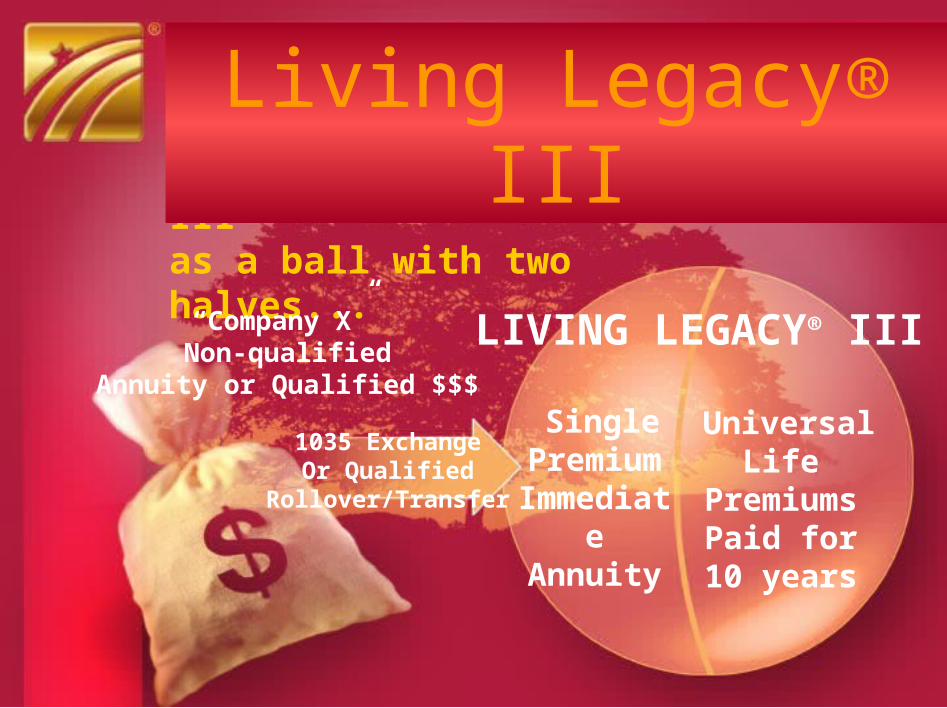

Think of LIVING LEGACY® III as a ball with two halves...

“Company X” Non-qualified

Annuity or Qualified $$$

1035 ExchangeOr Qualified

Rollover/Transfer

LIVING LEGACY® III

SinglePremium

ImmediateAnnuity

Universal LifePremiums

Paid for10 years

Living Legacy® III

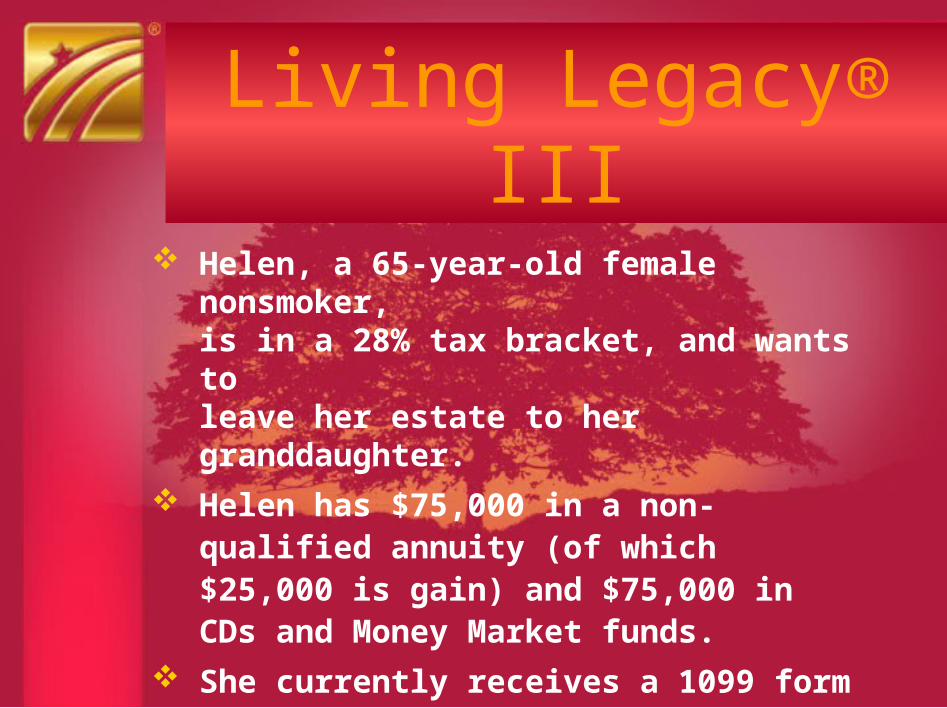

Helen, a 65-year-old female nonsmoker, is in a 28% tax bracket, and wants to leave her estate to her granddaughter.

Helen has $75,000 in a non-qualified annuity (of which $25,000 is gain) and $75,000 in CDs and Money Market funds.

She currently receives a 1099 form each year indicating taxable income on her CDs and Money Market Funds only.

Example:Living Legacy® III

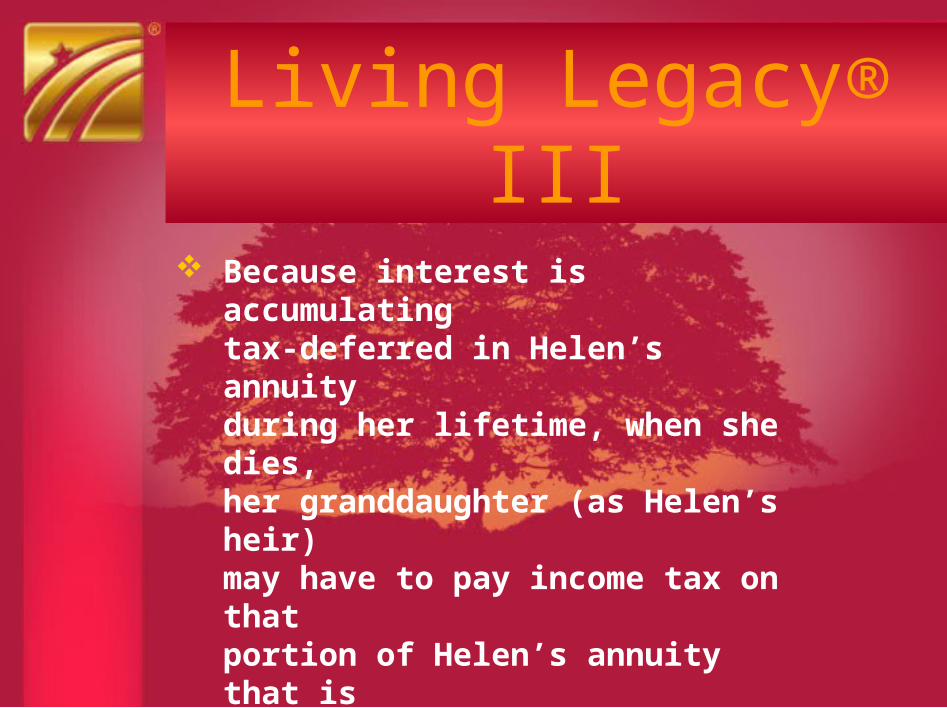

Because interest is accumulating tax-deferred in Helen’s annuity during her lifetime, when she dies, her granddaughter (as Helen’s heir) may have to pay income tax on that portion of Helen’s annuity that is considered gain ($25,000), depending on the payout option selected. This may cause Helen’s granddaughter to be in a higher tax bracket.

Example(continued)

Living Legacy® III

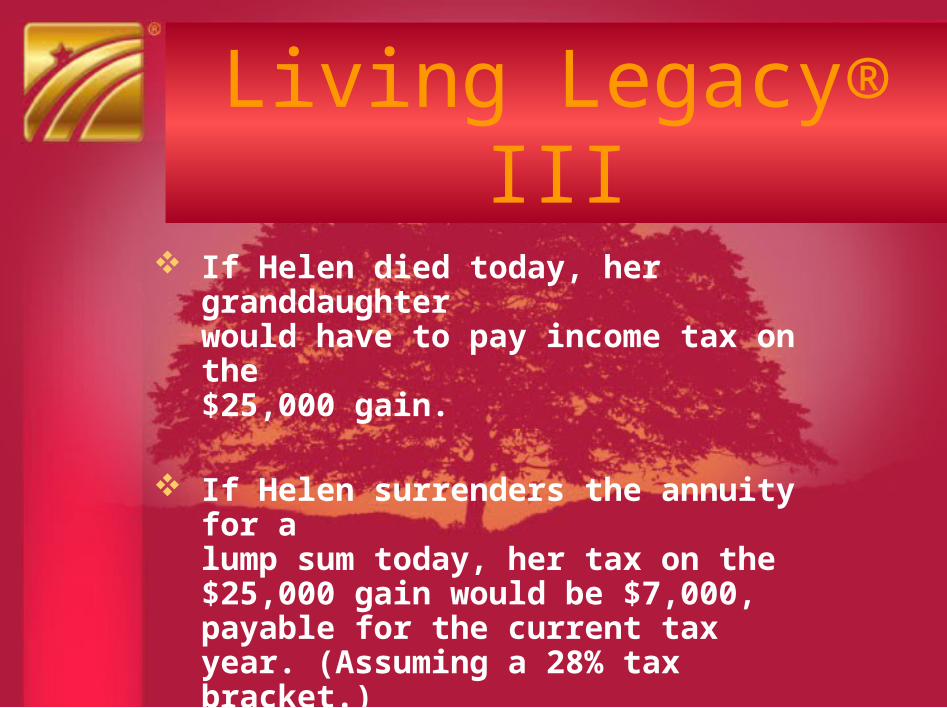

If Helen died today, her granddaughter would have to pay income tax on the $25,000 gain.

If Helen surrenders the annuity for a lump sum today, her tax on the $25,000 gain would be $7,000, payable for the current tax year. (Assuming a 28% tax bracket.)

Example(continued)

Living Legacy® III

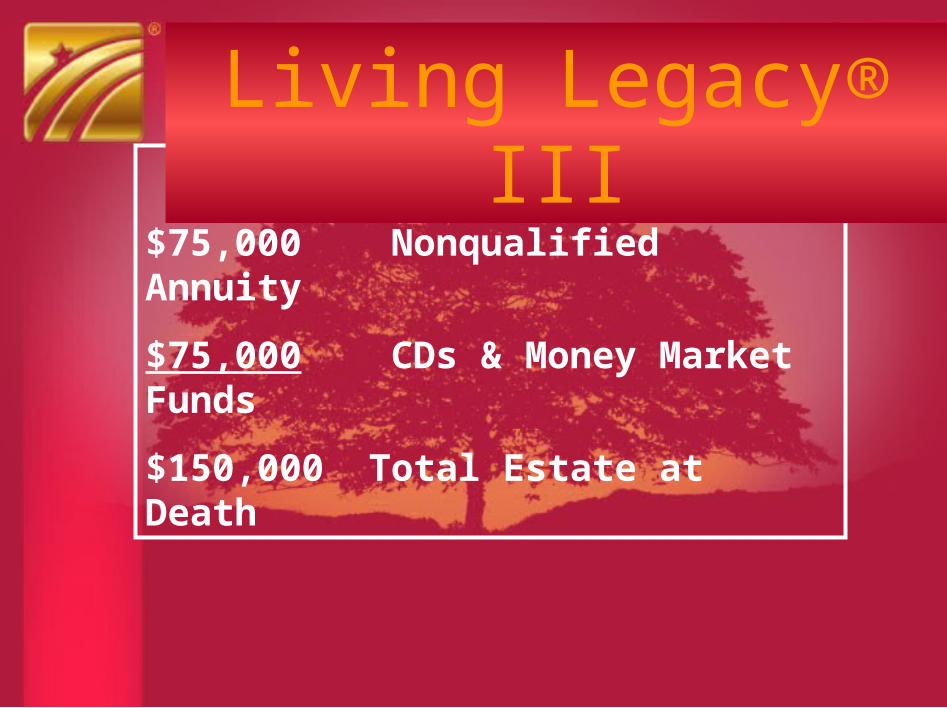

Helen’s Current Portfolio

$75,000 Nonqualified Annuity

$75,000 CDs & Money Market Funds

$150,000 Total Estate at Death

Example(continued)

Living Legacy® III

Helen met with an insurance agent representing Shenandoah Life and completed a worksheet to

determine if Living Legacy® III

is right for her, and to choose which funds she wanted to reallocate to Living Legacy® III.

Example(continued)

Living Legacy® III

Helen decided to transfer the $75,000 in annuity money to Living Legacy® III, with her granddaughter listed as the named beneficiary of the UL policy, and to keep the CDs and Money Market Funds available for other possible uses during her retirement.

Example(continued)

Living Legacy® III

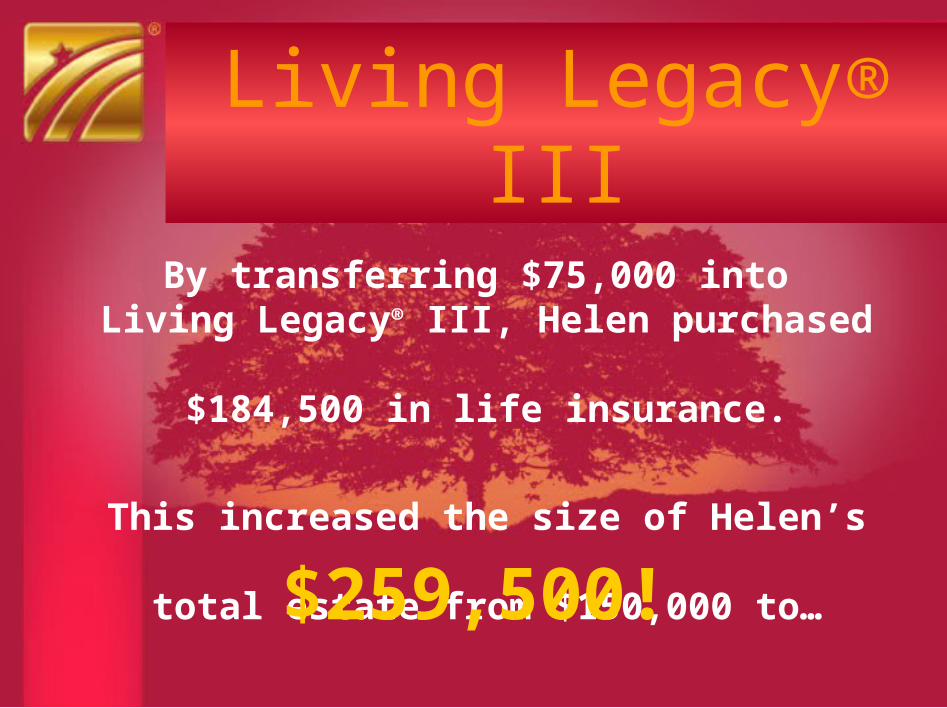

By transferring $75,000 into Living Legacy® III, Helen purchased

$184,500 in life insurance.

This increased the size of Helen’s total estate from $150,000 to…

Example(continued)

$259,500!

Living Legacy® III

Helen’s estate before purchasing a Living Legacy® III policy:

$75,000 annuity

$75,000 CD and money market funds

$150,000 estate at death

Helen’s estate after purchasing Living Legacy® III:

$184,500 Living Legacy® III life insurance coveragepurchased with $75,000 annuity

$75,000 CD and money market funds

$259,000 total estate at death!

Living Legacy® III

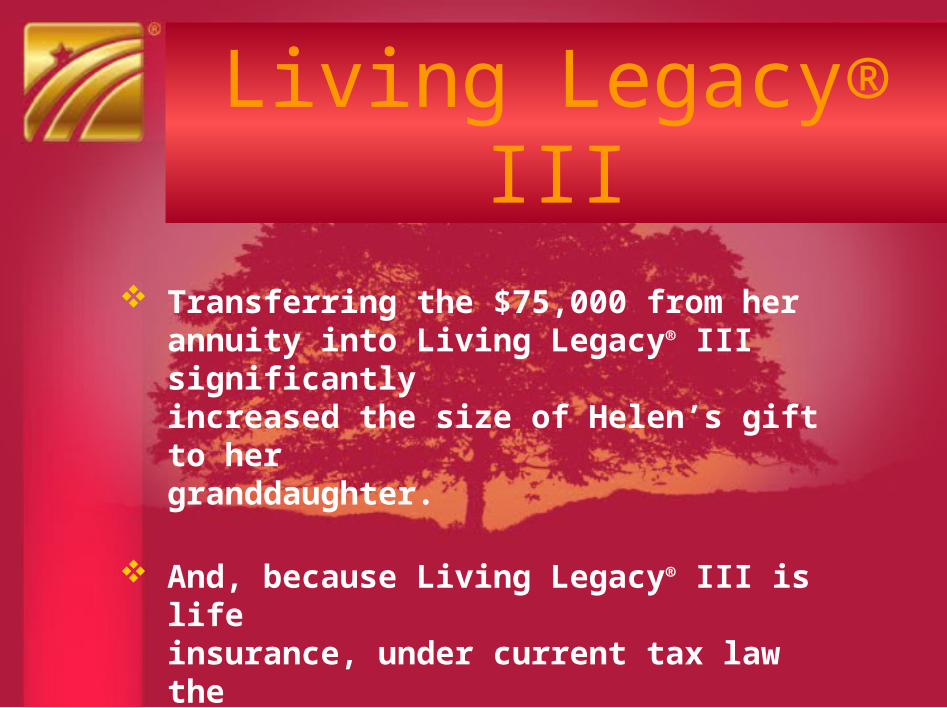

Transferring the $75,000 from her annuity into Living Legacy® III significantly increased the size of Helen’s gift to her granddaughter.

And, because Living Legacy® III is life insurance, under current tax law the benefit will pass to her granddaughter income tax free.

Example(continued)

Living Legacy® III

Over the next 10 years, Helen will receive a1099 annual reporting form, while the money

from the SPIA in Living Legacy® III pays into

the Universal Life insurance policy.

Instead of paying $7,000 in tax on the gain in the annuity at once, as she would if she cashed in the annuity, Helen will only be required to report as income a portion of the gain each year for the first 10 years.

Example(continued)

Living Legacy® III

After 10 years, the annuity terminates and there is no additional gain to report on this transaction. Should Helen die prior to the end of the 10 years at any time following issue of the Living Legacy® III policy, her named beneficiary (her granddaughter) would receive the larger, income tax-free life insurance benefit of $184,500* rather than the smaller taxable annuity benefit.

*Assumes non-guaranteed elements will continue unchanged for all years shown. Actual results may be more or less favorable. Benefits are subject to terms and conditions of the policy and vary by age and health status.

Example(continued)

Living Legacy® III

What’s more: The insurance proceeds pass outside

probate to Helen’s granddaughter as her designated beneficiary.

And her granddaughter will receive the insurance proceeds without having to pay income taxes on the money.

The information provided is not intended as legal or tax advice. If legal advice or other expert assistance is required, the services of a competent professional should be sought. The information provided is intended to be accurate based on Shenandoah Life’s understanding and interpretation of current tax laws, which are subject to change.

Living Legacy® III

Additional Features

GUARANTEED DEATH BENEFITGUARANTEED DEATH BENEFIT!*!*

The life insurance policy has a The life insurance policy has a guaranteed death benefitguaranteed death benefit

Option to Purchase a Deferred Annuity Option to Purchase a Deferred Annuity

if Life Policy Cannot Be Issuedif Life Policy Cannot Be Issued

*Initial death benefit is guaranteed for the life of the contract provided no loans or withdrawals have been taken, there are no changes in face amount and provided the policy has not been reinstated. Death benefit paid in the event of suicide, during the first two policy years (one year in CO), may be limited to premiums paid, less any withdrawals or outstanding policy loan balance.

Living Legacy® III

Accelerated Benefit Accelerated Benefit RiderRider

With

Nursing Home Provision

Additional FeatureLiving Legacy® III

* State variations apply to policies and the Accelerated Benefit Rider. Rider Form R-2021-2/99 Rev. 1/01, and R-2020-9/98 TX Rev. 1/01. State suffixes to form numbers may be applicable where there are state-specific versions of the form.

Accelerated Benefit RiderWith Nursing Home Provision

Benefit Triggers* In the event insured is diagnosed as

terminally ill (life expectancy of 24 months or less) or

If insured enters a qualified institution with the expectation that such confinement shall be permanent or

If the insured has been continuously confined to a qualified institution for at least 6 months (this condition not approved in all states)

Living Legacy® III

*Not approved in all states. State variations apply.

Company will pay lump sum or, upon request, equal monthly installments for a fixed period

Accelerated Death Benefit will be the maximum approved by state, not to exceed the lesser of 80% (75% in Illinois) of the face amount of the policy or $250,000.

Accelerated Benefit RiderWith Nursing Home Provision

This presentation is not complete without your full review of the Summary and Disclosure statement for the ABR, which provides full explanation of all conditions, limitations, fees, possible tax consequences, and state-specific regulations. Proceeds payable under this rider may be taxable. Consult with a professional tax advisor prior to requesting such benefits.

Living Legacy® III

Benefits of Living Legacy® IIIare subject to terms and conditions of the policy and vary by age and health status.

Living Legacy® III

Visit us at www.shenlife.com

SM

Living Legacy® III

TheAnnuityAnnuity

Alternative

Living Legacy® III