liquidity rules now the binding constraint for large banks rules... · liquidity rules now the...

TRANSCRIPT

July 6, 2016

Liquidity Rules Now the Binding Constraint for Large Banks

Challenges for Large Banks Create Opportunities for Regional and Community Banks

Thomas W. Killian, Principal

(212) 466-7709

On June 23rd all 33 U.S. bank holding companies with $50 billion or more in assets passed the quantitative

component of the Federal Reserve Board’s 2016 Comprehensive Capital and Analysis Review (CCAR)

severely adverse case stress test with more than sufficient capital above required minimum levels. 1 On June

29th, 31 of these banks also passed the qualitative component of the CCAR stress test. 2 For these large

banks attention has now shifted to liquidity as the binding constraint in planning.

The liquidity requirements for large banks are being finalized with comments due on August 5 th for the Net

Stable Funding Ratio (NSFR).3 Once the NSFR is completed, large U.S. bank holding companies with $50

billion or more in assets will have four overlapping and interrelated liquidity requirements consisting of the:

Liquidity Coverage Ratio

Net Stable Funding Ratio

Method 2 GSIB Capital Buffer

Comprehensive Liquidity Assessment and Review

With the NSFR as the final piece of the liquidity requirement puzzle soon falling into place, bank

management teams and Boards of Directors, along with bank equity and debt investors are now taking a

fresh look at the challenges for these large banks and specifically for the eight global systemically

important banks (GSIBs)4 and the opportunities for regional and community banks not subject to these

1 Dodd-Frank Act Stress Test 2016: Supervisory Stress Test Methodology and Results. Board of Governors of the Federal Reserve System. June2016. Page 13.2

Comprehensive Capital Analysis and Review 2016: Assessment Framework and Results, Board of Governors of the Federal Reserve System.June 2016. Page 14. (Please see Appendix A for more details on the results of the CCAR stress tests.).3 Notice of Proposed Rulemaking. Net Stable Funding Ratio: Liquidity Risk Measurement Standards and Disclosure Requirements. Office of theComptroller of the Currency (OCC), Department of the Treasury, Board of Governors of the Federal Reserve System, and the Federal DepositInsurance Corporation. Page 13.4

Current GSIBs include Bank of America Corporation, The Bank of New York Mellon Corporation, Citigroup Inc., The Goldman Sachs Group, Inc.,JP Morgan Chase & Co., Morgan Stanley, State Street Corporation and Wells Fargo & Company.

2

liquidity requirements.5 This note will provide an overview of each of these liquidity requirements, outline

the applicability of each based primarily on asset size, and discuss the interplay and overlap between the

rules and the timeline for full implementation. In conclusion, we will provide recommendations of funding,

investment and lending opportunities for regional and community banks with less than $50 billion in assets

that may be attractive given the liquidity constraints faced by large banks.

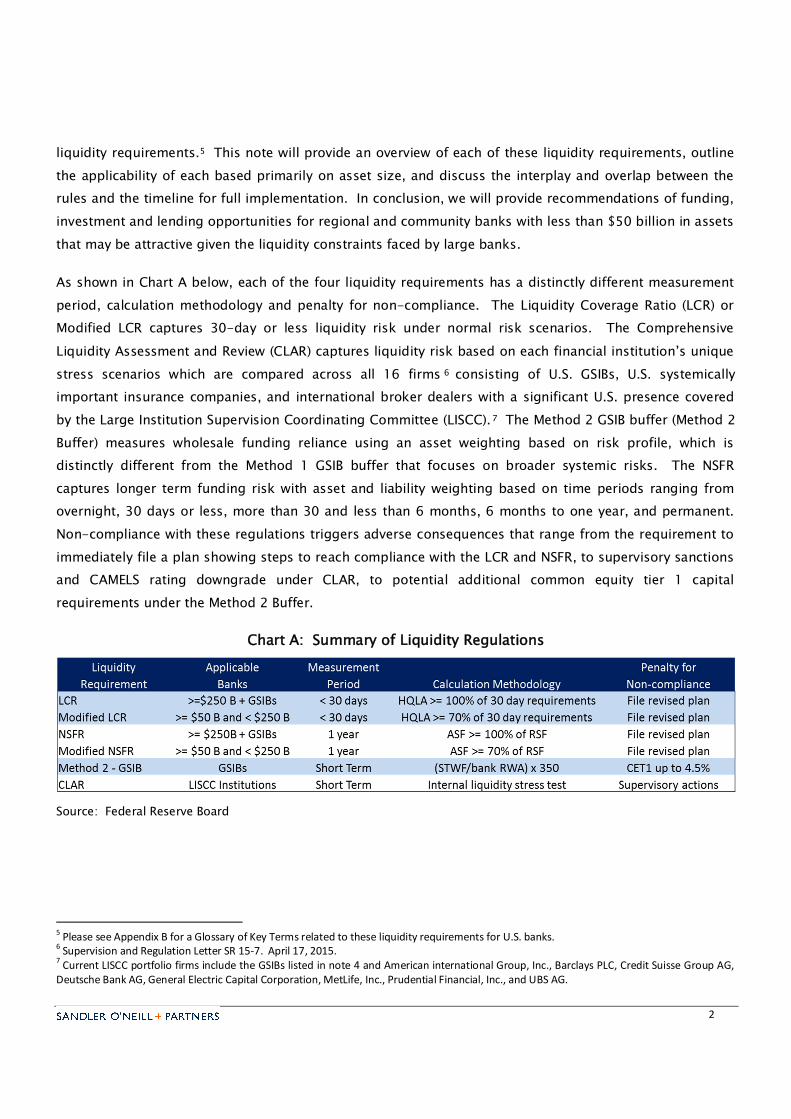

As shown in Chart A below, each of the four liquidity requirements has a distinctly different measurement

period, calculation methodology and penalty for non-compliance. The Liquidity Coverage Ratio (LCR) or

Modified LCR captures 30-day or less liquidity risk under normal risk scenarios. The Comprehensive

Liquidity Assessment and Review (CLAR) captures liquidity risk based on each financial institution’s unique

stress scenarios which are compared across all 16 firms 6 consisting of U.S. GSIBs, U.S. systemically

important insurance companies, and international broker dealers with a significant U.S. presence covered

by the Large Institution Supervision Coordinating Committee (LISCC).7 The Method 2 GSIB buffer (Method 2

Buffer) measures wholesale funding reliance using an asset weighting based on risk profile, which is

distinctly different from the Method 1 GSIB buffer that focuses on broader systemic risks. The NSFR

captures longer term funding risk with asset and liability weighting based on time periods ranging from

overnight, 30 days or less, more than 30 and less than 6 months, 6 months to one year, and permanent.

Non-compliance with these regulations triggers adverse consequences that range from the requirement to

immediately file a plan showing steps to reach compliance with the LCR and NSFR, to supervisory sanctions

and CAMELS rating downgrade under CLAR, to potential additional common equity tier 1 capital

requirements under the Method 2 Buffer.

Chart A: Summary of Liquidity Regulations

Source: Federal Reserve Board

5 Please see Appendix B for a Glossary of Key Terms related to these liquidity requirements for U.S. banks.6 Supervision and Regulation Letter SR 15-7. April 17, 2015.7

Current LISCC portfolio firms include the GSIBs listed in note 4 and American international Group, Inc., Barclays PLC, Credit Suisse Group AG,Deutsche Bank AG, General Electric Capital Corporation, MetLife, Inc., Prudential Financial, Inc., and UBS AG.

3

Compliance with these liquidity requirements has historically been considered less burdensome than the

Basel III capital requirements. This changed when the Fed implemented the requirement to classify

commercial deposits as either operating or non-operating under the Method 2 Buffer calculation

announced in July 2015. Operating deposits8 require quantitative documentation of their use to support

transaction activity and are assumed to be very stable with little need for liquidity coverage. All other cash

deposits are classified as non-operating deposits that are assumed to be highly unstable and must be

covered by high quality liquid assets (HQLA)9 which generally have a lower yield. As a result, the return on

investment for deploying non-operating deposits is much lower than the return potential for operating

deposits which do not require coverage by HQLA and can be invested in much higher yielding investments

and loans. JP Morgan served notice of the importance of this change in liquidity measurement with their

more than $200 billion reduction in non-operating deposits at year-end 2015. Overall, in 2015, the U.S

GSIBs were estimated to have proactively pushed nearly $400 billion in non-operating deposits off their

balance sheets.

Liquidity management is now viewed as a bigger challenge to their business than Basel III capital rules,

according to large bank CEOs participating in the Board’s February meeting of the Federal Advisory Council.

“Liquidity rules require banks to put a high amount of liquidity aside for commercial deposits and will raise

the cost of credit on a systemic basis, impeding long-term economic growth. By devaluing the deposits

that commercial customers provide, more deposits are being pushed off bank balance sheets into off-

balance-sheet funds.” 10 Large, commercially-oriented institutions with a lower percentage of retail

deposits than competitors will be most impacted. This could create a significant market opportunity for

regional and community banks (not subject to these liquidity requirements) to offer expansive depository

services to commercial accounts that will be looking for new banking relationships.

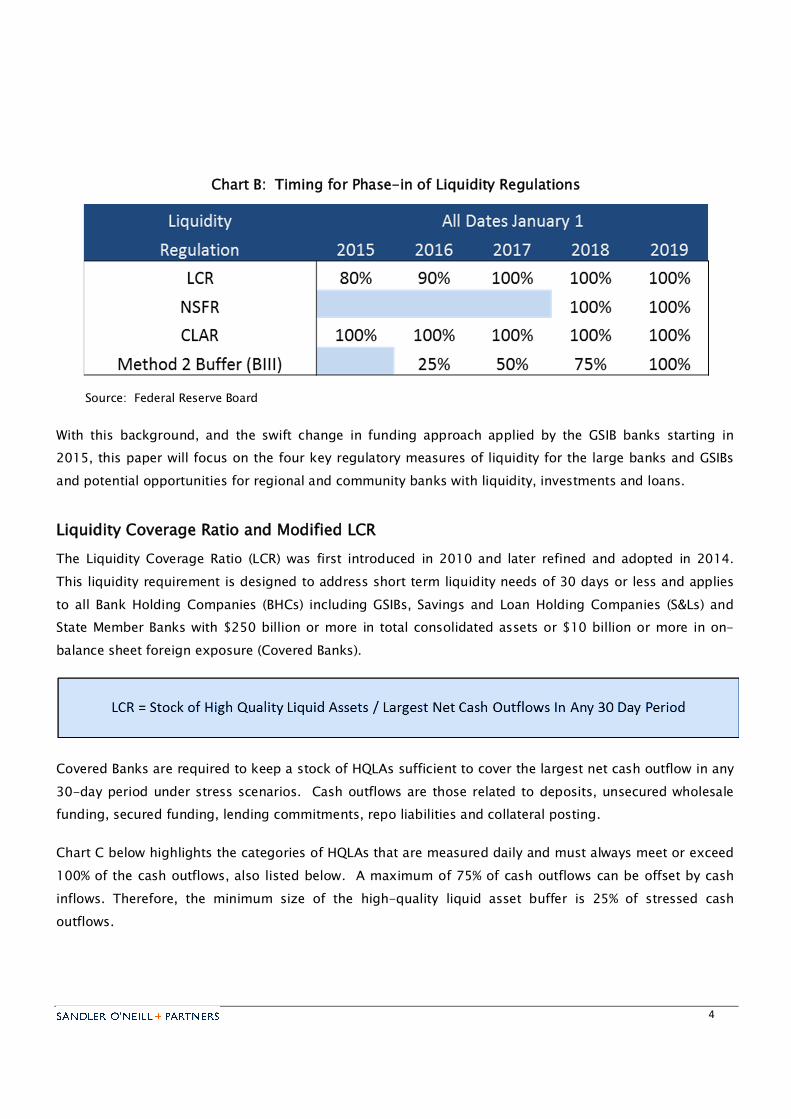

The timing for the effectiveness of liquidity regulation is coming quickly with full phase-in of the LCR

effective January 1, 2017. The CLAR is already in place and being implemented on a confidential basis with

the 16 LISCC supervised institutions. As highlighted below in Chart B, the NSFR is expected to become

effective in 2018 while the Method 2 Buffer phases-in to be fully effective in 2019.

8Operating deposits include deposits from bank clients with a substantive dependency on the bank where deposits are required for certain

activities (i.e. clearing, custody or cash management activities). Non-operating deposits are all other unsecured wholesale deposits, bothinsured and uninsured. (See Appendix C for more details on the requirements for operating deposits.)9 Guidance and Templates Regarding Liquidity Coverage Ratio Disclosure Standards. http://www.sama.gov.sa/en-US/Laws/Documents/Section%20B/4.%20BCBS%20Document%20regarding%20Liquidity%20Coverage%20Ratio%20Disclosure%20Standards.pdf10

Record of Meeting. Federal Advisory Council and Board of Governors. Wednesday, February 3, 2016. Page. 12.

4

Chart B: Timing for Phase-in of Liquidity Regulations

Source: Federal Reserve Board

With this background, and the swift change in funding approach applied by the GSIB banks starting in

2015, this paper will focus on the four key regulatory measures of liquidity for the large banks and GSIBs

and potential opportunities for regional and community banks with liquidity, investments and loans.

Liquidity Coverage Ratio and Modified LCR

The Liquidity Coverage Ratio (LCR) was first introduced in 2010 and later refined and adopted in 2014.

This liquidity requirement is designed to address short term liquidity needs of 30 days or less and applies

to all Bank Holding Companies (BHCs) including GSIBs, Savings and Loan Holding Companies (S&Ls) and

State Member Banks with $250 billion or more in total consolidated assets or $10 billion or more in on-

balance sheet foreign exposure (Covered Banks).

Covered Banks are required to keep a stock of HQLAs sufficient to cover the largest net cash outflow in any

30-day period under stress scenarios. Cash outflows are those related to deposits, unsecured wholesale

funding, secured funding, lending commitments, repo liabilities and collateral posting.

Chart C below highlights the categories of HQLAs that are measured daily and must always meet or exceed

100% of the cash outflows, also listed below. A maximum of 75% of cash outflows can be offset by cash

inflows. Therefore, the minimum size of the high-quality liquid asset buffer is 25% of stressed cash

outflows.

5

Chart C: Liquidity Coverage Ratio (LCR)

Source: Federal Reserve Board

In meeting the LCR, at least 60% of the HQLAs maintained by Covered Banks must be Level 1 assets with a

maximum of 40% Level 2 assets permitted as described below in Chart D:

Chart D: Components of HQLA

Source: Federal Reserve Board

6

After industry pressure, the regulators recently agreed to permit investment grade rated general obligation

bonds issued by Public Sector Entities (PSEs) to be included in Level 2B assets but limited the amount to 5%

of total HQLA and with any single issuer limited to 2 times average daily trading volume.

As shown below in Chart E, aside from cash and U.S. Treasury securities, GNMA securities are the most

attractive to meet the HQLA requirements with 0% haircut to fair value and 100% inclusion in HQLA. FNMA

and FHLMC securities each have a 15% haircut with a maximum of 40% inclusion in HQLA. Investment

grade corporate debt and general obligation muni debt have a 50% haircut of fair value with 15% and 5%

inclusion in HQLA. Non-agency RMBS and non-investment grade municipal bonds are excluded from

HQLA.

Chart E: HQLA Haircuts and Inclusion Percentages

Source: Federal Reserve Board

BHCs and S&Ls with $50 billion or more in total consolidated assets but less than $250 billon are subject to

a modified version of the LCR (Modified LCR). These banks are required to keep a stock of HQLA that is

sufficient to cover 70% of the largest net cash outflow in any 30-day stress period.

Banks with total assets of less than $50 billion are not subject to the LCR or Modified LCR and have

substantial flexibility to meet the Dodd-Frank Act (DFA) liquidity requirements without haircuts on fair

value or limits for inclusion in liquidity.

7

Net Stable Funding Ratio and Modified NSFR

With a focus on a one-year timeframe, the NSFR is being designed to complement the short-term 30-day

focus of the LCR. The NSFR was first introduced in 2010, revised in 2014, and is now being finalized with

the request for comments due on August 5, , 2016. The NSFR is expected to become effective on January 1,

2018. As of December 31, 2015, the regulatory agencies estimate that the NSFR would apply to 15 bank

holding companies with $250 billion or more in assets and a modified version of the NSFR (Modified NSFR)

would apply to the 20 bank holding companies with $50 billion or more in total consolidated assets but

less than $250 billion. The agencies estimate that these 35 institutions would need to raise approximately

$39 billion in Available Stable Funding (ASF).11

As currently proposed, the NSFR requires Covered Banks to maintain an amount of ASF consisting of

capital, deposits, wholesale funding and other liabilities and including net payables on derivatives to more

than offset the required stable funding needs of the institution over a period of one year. BHCs subject to

the Modified NSFR must keep ASF to meet 70% of RSF.

The current proposal mandates that ASF is calculated by first determining the carrying value or book value

of the Covered Bank’s capital and liabilities. This value is then multiplied by a factor that weighs the

likelihood of the source of funds being available based on BIS and U.S. regulatory guidelines. The ASF

amount is the sum of the weighted amounts. Chart F below summarizes the key sources of AFS and the

weighting factors assigned to each. Note that non-operational deposits, highlighted in red, provide NO AFS

support thus reinforcing the difficulty with Covered Banks continuing to provide this deposit service.

Chart F: Sources of Available Stable Funding and Weighting Factors

Source: Federal Reserve Board and the Basel Committee on Banking Supervision

11 Notice of Proposed Rulemaking. Net Stable Funding Ratio: Liquidity Risk Measurement Standards and Disclosure Requirements. May 3,2016. Office of the Comptroller of the Currency, Department of the Treasury, Board of Governors of the Federal Reserve System, and FederalDeposit Insurance Corporation. Page 145.

8

The required stable funding (RSF) amount is calculated by first identifying the carrying value or book value

of the Covered Bank’s assets and off-balance-sheet liabilities. These values are then multiplied by a factor

that weighs the likelihood of the use of funds being needed based on BIS and U.S. regulatory guidelines.

The RSF amount is the sum of the weighted amounts. Chart G below summarizes the key uses of RSF and

the weighting factors assigned to each.

Chart G: Uses of Required Stable Funding and Weighting Factors

Source: Federal Reserve Board and the Basel Committee on Banking Supervision

Note that the RSF relies on the definitions of Level 1, Level 2A and Level 2B assets from the LCR. There is

also a significant distinction in the RSF calculation required for different types of lending. Low risk-

weighted loans to retail customers and small and medium-sized enterprises with a remaining maturity of

one year or less require a 50% RSF factor. Residential mortgages and other unencumbered performing

loans with a remaining maturity of one year or more require a 65% RSF factor. All other assets, including

loans to financial institutions, encumbered assets and project finance loans with a maturity greater than

one year require a RSF factor of 100%. Similarly, off-balance sheet committed and non-cancellable lines of

credit have 100% RSF and require sufficient ASF to cover the potential draw down under the commitment.

9

BHCs subject to the NSFR and the Modified NSFR may have an incentive to reduce long-term lending for

loans with risk weightings greater than 35% and a RSF factor of 85% or more. As a result, the NSFR rules

may create long-term lending opportunities for regional and community banks that are not subject to the

NSFR or Modified NSFR.

Method 2 Buffer

In 2010, the BIS introduced an additional common equity tier 1 (CET1) capital cushion ranging from 1.0% to

2.5% for BHCs greater than $250 billion in assets that have been identified as GSIBs by the Financial

Stability Board (FSB). The exact cushion is set by the FSB based on the GSIB’s ratings across five categories

of risk, all equally weighted at 20%. These categories are size, interconnectedness, substitutability,

complexity, and cross-jurisdictional activity. The top 75 global institutions are selected as GSIBs annually

using the Method 1 weighting shown below in Chart H. While this methodology is used to select the GSIBs

and apply a CET1 buffer from 1.0% to 2.5%, the U.S. regulatory agencies did not feel that this Method 1

buffer provided sufficient protection against reliance on wholesale funding and illiquidity of investments.

To address this concern, in 2015 the U.S. regulatory agencies introduced the Method 2 Buffer with a capital

cushion ranging from 1.0% to 4.5% that (i) replaced the category of substitutability with reliance on short-

term wholesale funding (STWF), (ii) reduced the weighting for size and cross-jurisdictional activity, and (iii)

dramatically increased the weighting for STWF and investment in Level 3 assets along with trading and

available for sale securities.

Chart H: Method 1 vs. Method 2 Categories and Weightings

Source: Federal Reserve Board and Basel Committee on Banking Supervision

10

The Method 2 Buffer heavily penalizes reliance on STWF, which is calculated as weighted average short-

term wholesale funding / risk weighted assets x 350. With these changes in calculation methodology the

typical basis point range of GSIB scores increased from 130 to 729 under Method 1 to 130 to 929 under

Method 2.

The July 2015 calculation of the Method 1 and Method 2 Buffer amounts shown below in Chart I illustrate

the significant penalty that JPM, C, GS, MS and BAC would be required to pay for their higher reliance on

wholesale funding and investment in illiquid securities. JPM’s 4.50% Method 2 surcharge represented 200

basis points of additional CET1 it would be forced to add over the Method 1 surcharge amount, a

substantial penalty relative to peers. By year-end 2015, JPM had reduced their Method 2 buffer from 4.5%

to 3.5% by reducing non-operating deposits by more than $200 billion, decreasing Level 3 assets, and

reducing OTC derivatives.12

Chart I: Method 1 vs Method 2 GSIB Buffer Amounts as of July 2015

Source: Federal Reserve Board

Clearly, the weightings assigned to STWF, Level 3 assets and trading and available for sale securities in the

Method 2 calculation provide a strong capital incentive for the GSIBs to avoid reliance on wholesale funding

and non-operating deposits and investing in less liquid assets. As illustrated below in Chart J, the

weighting factors for unsecured wholesale funding range from 25% to 100% for remaining maturities of less

than 30 days to up to 365 days. These weightings significantly gross up the STWF score with the results

discussed above.

12JP Morgan Chase & Co. Q4 2015 Earnings Presentation, page 4.

11

Chart J: Weighting Methodology for Short Term Wholesale Funding

Source: Federal Reserve Board

Comprehensive Liquidity Analysis and Review

In 2012, the Federal Reserve Board created the CLAR program to conduct an annual review of the liquidity

practice for each of the firms covered by the Large Institution Supervision Coordinating Committee (LISCC).

The CLAR is a company-prepared liquidity stress test that uses a number of liquidity indicators, such as

funding concentrations, to measure liquidity vulnerabilities beyond those captured by the LCR with the

measurements captured over multiple time horizons. Regulators also review the stress tests that each firm

uses to make its funding decisions and determine liquidity needs. The CLAR does not include a specific

quantitative post-stress test minimum. But LISCC firms must meet the LCR requirements that have a

forward looking stress testing component. Weakness in liquidity positions by LISCC banks are addressed

through supervision direction, ratings downgrades or enforcement actions.13 The CLAR results are not

released to the public but provide the Board with a perspective on the liquidity vulnerabilities and funding

concentrations in the system as a whole. As such, it is difficult to determine whether the CLAR program

represents a more binding constraint on liquidity management at the large banks than the LCR, NSFR, or

Method 2 Buffer. But the CLAR is clearly a tool that the Board is using annually to confidentially assess

funding risk among the systemically important banks and other financial institutions in the U.S.

13Governor Daniel K. Tarullo. Board of Governors of the Federal Reserve System. Speech at the Clearing House 2014 Annual Conference.

November 20, 2014.

Components of STWF RM <30 days RM 31 to 90 RM 91 to 180 RM 181 to 365

o Secured funding by Level 1 Assets 25.00% 10.00% 0.00% 0.00%

o Secured funding by Level 2A Assets

o Unsecured wholesale funding non FE

o Brokered Deposits and brokered sweep 50.00% 25.00% 10.00% 0.00%

o Covered asset exchanges of Level 1 asset

for level 2A liquid asset

o Short positions w/ Level 1 or 2A borrowed

security

o Funding transaction secured by Level 2B

liquid assets 75.00% 50.00% 25.00% 10.00%

o Covered asset exchanges and short

positions other than as described above

o Unsecured wholesale funding - FE 100.00% 75.00% 50.00% 25.00%

o Any other component of STWF

12

Opportunities for Regional and Community Banks

Regional and community banks with less than $50 billion in assets are not subject to the LCR, NSFR, CLAR

or the Method 2 Buffer governing liquidity14. This provides the broad majority of regional and community

banks with significant flexibility to tailor their deposit and loan products to meet their local market

requirements and client needs as larger competitors are focused on optimizing for LCR, NSFR or Method 2

Buffer treatment. Similarly, investment portfolio decisions can be made with a focus on the risk and return

profile of the securities rather than an emphasis on the HQLA treatment for the securities and compliance

with the LCR and NSFR requirements.

With that background, we think there are at least five broad types of opportunities that may be attractive to

regional and community banks:

Non-operating deposits: The LCR, NSFR, Method 2 Buffer, and CLAR all penalize non-operating

deposits with very high assumed run-off rates which have to be covered with HQLA. Pursuant to the

definition of operational deposits15, a bank must prove that a depository account is an operating

account. If the account does not meet 1 of the 7 qualifications, it will be assumed to be a non-

operating account.16 This creates a market opportunity for regional and community banks who are

not required to comply with the LCR, NSFR, Method 2 Buffer or the CLAR liquidity requirements to

pursue offering deposits accounts that do not meet the definition of “operating” to commercial

customers.

Selected Level 2A and Level 2B investments: Level 2A and Level 2B assets face substantial haircuts

and limitations towards inclusion in HQLA. Covered Banks and others subject to the LCR, NSFR,

Method 2 Buffer and CLAR are forced to optimize their investment portfolios based on maximizing

their value towards HQLA rather than the overall performance characteristics of the securities. For

example, as highlighted below in Chart K, the average composition of the HQLA portfolio for GSIB

banks in the Basel Committee on Banking Supervision’s Monitoring Report as of March 2016 was

substantially over-weighted towards Level 1 assets with very limited inclusion of Level 2A or 2B

assets. The GSIB banks maintained excess Level 1 assets at 88.50% of HQLA while only required to

hold 60%. This means that roughly 28.5% of the Level 1 assets could theoretically be reallocated to

higher yielding Level 2A or 2B assets. Conversely, the GSIB banks could have maintained 25% Level

2A and 15% Level 2B but only maintained 9.50% and 1.90%, respectively.17 In this way, the GSIB

banks were not optimizing their investment portfolios of HQLA but prioritizing compliance with the

LCR requirements with substantial cushion.

14 Excluding banks with $10 billion or more in foreign assets.15 Section 329.4 (b) of the FDIC Law, Regulations and Related Acts.16

Please see Appendix C for a complete listing of the qualifications to be considered an operating account.17

Basel Committee on Banking Supervision. Basel III Monitoring Report. March 2016. Page 26. http://www.bis.org/bcbs/publ/d354.pdf

13

Chart K: Weighting Methodology for Short Term Wholesale Funding

Source: Basel Committee on Banking Supervision, Federal Reserve Board

The GSIBs have substantial capacity to optimize their investment portfolios and still remain within

the HQLA limitations. One could reasonably expect to see the GSIBs reallocate HQLA from Level 1

to Level 2A and 2B assets over the next year or two as they become more comfortable with the LCR

calculations. Conversely, regional and community banks face no such restrictions to comply with

the LCR and NSFR requirements and can focus on finding value within the Level 2A and 2B

categories, particularly if there continues to be an absence of demand on the part of the GSIBs.

Level 3 Investments: Both the Method 1 Buffer and the Method 2 Buffer significantly penalize

investments in FASB Level 3 assets. Level 3 assets are by definition less liquid than Level 1 or Level

2 assets but may have attractive risk/return characteristics appropriate for regional and community

banks to consider. Within limits established in the regional and community bank’s investment

policy, additional investment in Level 3 assets can provide attractive risk/reward without concern

about the negative impact on the GSIB buffer calculation. However, such investments may be more

appropriately classified as held-to-maturity investments rather than available-for-sale investments

given the lack of demonstrated liquidity.

Committed Lines of Credit: Non-cancellable, committed lines of credit and liquidity facilities are

assumed to be 100% drawn in the LCR and NSFR stress scenarios and require a 100% liquidity

allocation under the LCR and NSFR. As such, the GSIB and large banks will reprice these

commitments to reflect that liquidity requirement. For regional and community banks not subject

to the LCR or NSFR, this may provide a new business opportunity where they can price the credit

exposure based on the actual risk of usage rather than the stress scenario’s modeled risk.

14

High Risk Weighted Term Loans: High risk weighted multi-year loans require 100% funding under

the LCR and NSFR. GSIB and Advanced Approaches banks subject to the LCR and NSFR will be

expected to keep 100% coverage of these loans in HQLA or ASF. This may force the larger banks to

reprice such loans or require that they can be sold rather than retained on balance sheet.

Community and regional banks may use this as an advantage in pursuing corporate term loans

particularly from corporations and commercial accounts with non-operating deposits that the larger

banks no longer wish to maintain.

SUMMARY

With the requirements for the NSFR to be finalized after receipt of comments in August 2016, the

framework for liquidity management will soon be complete with four interrelated and overlapping

measures: the LCR, NSFR, Method 2 Buffer, and the CLAR. These requirements are most directly relevant

to banking organizations with $50 billion or more in assets and have implications for the attractiveness and

pricing for operating and non-operating deposits, investments, loans and committed lines of credit.

Several of the GSIB banks have already served notice that the rules will have a significant impact on their

lines of business -- significantly reducing non-operating deposits in 2015 in response to the liquidity

penalty and additional capital buffer associated with non-operating deposits.

Prudent regional and community bank management teams and Boards of Directors can take advantage of

these dislocations from the implementation of the LCR, NSFR, Method 2 Buffer and CLAR and position their

banks with products and services that their clients need and the large banks can no longer cost effectively

provide.

15

Thomas W. Killian is a Principal of Sandler O’Neill + Partners, L.P. His 38-year career in commercial and investment

banking includes seven years of commercial banking experience with NationsBank, structuring and arranging leveraged

finance transactions; two years with Salomon Brothers, transacting capital markets and advisory assignments for a

variety of major corporations; five years with J.P. Morgan, managing financial advisory and capital raising activities for

banks and thrifts in the Western region of the United States; and 24 years with Sandler O’Neill, advising banks, thrifts,

and insurance companies on a variety of capital markets, strategic advisory and M&A assignments.

At Sandler O’Neill, Mr. Killian has managed the successful execution of 13 M&A transactions representing over $2.4

billion in deal value and $8.5 billion of capital raising transactions. Most recently, he advised the FDIC on the successful

least cost resolution of Doral Bank using a multiple acquirer strategy. He has co-managed the Sandler O’Neill team

responsible for successfully completing 17 pooled trust preferred transactions that raised over $7 billion for

approximately 650 financial institutions. Included in Mr. Killian's capital raising transactions are eight recapitalization

and restructuring transactions that involved complex capital structures designed to preserve tax benefits for the

issuing institutions. He functions as a primary resource in structuring and implementing complex capital markets

transactions for financial institutions and has written extensively on the impact of Basel III rules and the Dodd-Frank

requirements on capital structure and strategic planning for U.S. banks.

Mr. Killian holds a Bachelor of Science from the University of North Carolina at Chapel Hill, where he was a John Motley

Morehead Merit Scholar, and a Masters in Business Administration from Northwestern University's J.L. Kellogg Graduate

School of Management. He has represented Sandler O’Neill in conferences with the Federal Financial Institutions

Examination Council, the Federal Reserve, the Federal Deposit Insurance Corporation, and SNL Financial to discuss

capital structure, Dodd-Frank and Basel III related issues. His articles have appeared in Bank Accounting & Finance, U.S.

Banker and Modern Bankers, a publication of the Peoples Bank of China.

Mr. Killian is also a founding board member of Students Bridging the Information Gap, a 501(c)(3) charity that provides

computers, books and other support to African schools and orphanages.

16

Appendix – A

Summary of Federal Reserve Actions on 2016 CCAR Capital Plans

On June 23rd, all 33 of the bank holding companies subject to the 2016 CCAR capital planning exercise

passed the quantitative requirement of the CCAR severely adverse case stress test with capital levels in

excess of minimum requirements. On June 29th, the Federal Reserve Board announced the results of the

qualitative requirements with 30 passed with no objection, one was passed with a conditional non-

objection and two were declined.

There are 8 U.S.-based GSIBs designated with ”*” in the chart below. Of the 16 LISCC institutions, 10 were

subject to the CCAR test as noted by the LISCC designation. The other six LISCC institutions were U.S-

based insurance companies or foreign broker dealers with substantial U.S. operations.

Ally Financial Inc * LISCC Morgan Stanley LISCC Deutsche Bank Trust Corporation

American Express Company Santander Holdings

BancWest Corporation

* LISCC Bank of America Corporation

* LISCC The Bank of New York Mellon Corporation

BB&T Corporation

BBVA Compass Bancshares, Inc.

BMO Financial Corp.

Capital One Financial Corporation

* LISCC Citigroup Inc.

Citizens Financial Group, Inc.

Comerica Incorporated

Discover Financial Services

Fifth Third Bancorp

* LISCC The Goldman Sachs Group, Inc.

HSBC North America Holdings Inc.

Huntington Bancshares Incorporated

* LISCC JPMorgan Chase & Co

KeyCorp

M&T Bank Corporation

MUFG Americas Holdings Corporation

* LISCC Northern Trust Corporation

The PNC Financial Services Group, Inc.

Regions Financial Corporation

* LISCC State Street Corporation

SunTrust Banks, Inc.

TD Group US Holdings LLC

U.S. Bancorp

* LISCC Wells Fargo & Co

Zions Bancorporation

* designates one of eight U.S. based Global Systemically Important Banks (GSIB)

LISCC designates one of sixteen Large Institution Supervision Coordinating Committee and includes American International Group, Inc.,

Barclays, PLC, Credit Suisse Group AG, General Electric Capital Corporation , MetLife, Inc., Prudential Financial, Inc., UBS AG

Conditional

Non-objection (1) Objection (2)No Objection (30)

17

Appendix – B

Liquidity Requirements - Selected Glossary of Key Terms (1)

Advanced Approaches Banks - large, internationally active banking organizations with at least $250 billion in total consolidated

assets or at least $10 billion in total on-balance sheet foreign exposure--and includes the depository institution subsidiaries of

those firms.

Available Stable Funding (ASF) - Capital, deposits, wholesale funding and other liabilities, and equity including net payables on

derivatives. Calculated by multiplying the book value or carrying value of the capital and liabilities by the factor that weighs the

probability of the funds being available based on BIS and U.S regulatory guidelines.

CET1 - Common equity tier 1 capital as defined in the Basel III final capital rules.

CLAR – Comprehensive Liquidity Assessment and Review is a confidential, company-prepared liquidity stress test applicable to

the unique funding needs of each of 8 U.S. GSIBs, U.S. systemically important insurance companies and international broker

dealers that have a substantive U.S. presence and are subject to supervision by the LISCC.

Covered Banks - also referred to as Advanced Approaches banks.

GSIB – Global Systemically Important Bank as determined by the Financial Stability Board and updated yearly.

HQLA: High Quality Liquid Assets consisting of at least 60% Level 1 assets and 40% Level 2 assets.

Large Institution Supervision Coordinating Committee (LISCC) – Committee responsible for supervising the regulation of 8 U.S.

GSIBs, U.S. systemically important insurance companies and international broker dealers that have a substantive U.S. presence.

Level 1 High Quality Liquid Assets – Consists of cash and marketable securities, central bank reserves and 0% risk weighted

sovereign debt. HQLA required to comprise at least 60% Level 1 assets with 0% haircut from fair value.

Level 2A High Quality Liquid Assets – Consists of central bank and GSE assets qualifying for 20% risk weighting including FNMA

and FHLMC securities and qualifying covered bonds rated AA- or better. Total Level 2 assets capped at 40% of HQLA with 15%

haircut to fair value.

Level 2B High Quality Liquid Assets – Consists of qualifying investment grade corporate bonds and liquid GO muni bonds along

with major index common stocks. Total Level 2B assets capped at 15% of HQLA with haircuts of 50% to fair value for qualifying

corporate bonds and common stocks, and 5% of HQLA for investment grade liquid GO muni bonds.

Liquidity Coverage Ratio (LCR) – Applies to banks with $250 billion or more in total assets. Requires these banks to maintain

sufficient High Quality Liquid Assets (HQLA) to cover the peak cash outflow in any 30-day period. These banks are required to

have at least 60% Level 1 assets and are limited to no more than 40% of all Level 2 assets consisting of Level 2A and Level 2B

assets with a further limit of 15% on Level 2B assets

Method 1 Buffer – Under the Basel III framework, GSIBs are subject to an additional CET1 surcharge based on an indicator

approach to determining risk that consists of 5 categories including: size, interconnectedness, substitutability, complexity, and

cross jurisdictional activity. The amount of buffer using this methodology generally ranges from 1.0% to 2.5%. The Method 1

framework is used annually by the Financial Stability Board (FSB) for determining the top 75 international banks that will be

regulated as GSIBs.

18

Method 2 Buffer – The Board has established an alternative GSIB buffer, Method 2 Buffer, that replaces the substitutability

factor from Method 1 with a measure to capture reliance on short term wholesale funding (STWF), reduces the weighting for size

and cross jurisdictional activity and dramatically increases the weighting for STWF and investment in Level 3 assets along with

trading and AFS securities. The Method 2 buffer generally results in higher surcharge level for U.S. GSIBs due to the use of STWF

by these banks. The amount of the buffer generally ranges from 1.0% to 4.5%.

Modified Liquidity Coverage Ratio (Modified LCR) – Applies to banks with $50 billion or more in total assets but less than $250

billion in assets. Calculated the same way as the LCR except that these banks are only required to maintain HQLA to meet 70% of

the largest next cash outflow in any 30-day period.

Modified Net Stable Funding Ratio (Modified NSFR) – Applies to banks with $50 billion or more in total assets but less than $250

billion in total assets. Requires these banks to maintain sufficient ASF sufficient to meet at least 70% of RSF.

Net Stable Funding Ratio (NSFR) – Applies to banks with $250 billion or more in total assets. Requires these banks to maintain

sufficient ASF sufficient to more than offset RSF.

Non-operating Deposits: – All other deposits without quantitative documentation to support transaction activity.

NPR – NSFR Notice of Proposed Rule-making with comments due by August 5, 2016.

Operating Deposits: – Deposits that meet Section 329.4 (b) requirements to be considered operational deposits to support

transaction activity. Please see Appendix B for more details.

Required Stable Funding (RSF) – Investments, loans and other assets that require funding. Relies on the LCR definition of Level

1, Level 2A, and Level 2B investments. Calculated by multiplying the book value or carrying value of the assets by factors that

weigh the probability of the funds being needed based on BIS and U.S regulatory guidelines.

RWA – Risk weighted assets which comprise the denominator in the risk weighted assets ratio applicable to GSIB BHCs.

STWF – Short Term Wholesale Funding component of the Method 2 GSIB buffer. Calculated as weighted average short term

wholesale funding / risk weighted assets x 350. Weighting methodology divided into 4 timeframes and 4 types of funding with

varying run-off rate assumptions for each.

(1) This is intended to provide a brief summary of the key terms mentioned in this liquidity note. For more details on these key terms please

refer to the relevant Notice of Proposed Rulemaking or Federal Register for the LCR, NSFR, CLAR and the Method 2 GSIB Buffer.

19

Appendix – C

Section 329.4 (b) Operational Deposit

In order to recognize a deposit as an operational deposit as defined in Section 329.3:

(1) The related operational services must be performed pursuant to a legally binding written agreement, and:

i. The termination of the agreement must be subject to a minimum of 30 calendar days notice period; or

ii. As a result of termination of the agreement or transfer of services to a third-party provider, the customer providing the

deposit would incur significant contractual termination costs or switching costs;

(2) The deposit must be held in an account designated as an operational account;

(3) The customer must hold the deposit at the FDIC-supervised institution for the primary purpose of obtaining the operational

services provided by the FDIC-supervised institution;

(4) The deposit account must not be designed to create an economic incentive for the customer to maintain excess funds

therein through increased revenue, reduction in fees or other offered economic incentives.

(5) The FDIC supervised institution must demonstrate that the deposit it empirically linked to the operational services and that it

has a methodology that takes into account the volatility of the average balance for identifying any excess amount, which

must be excluded from the operational deposit amount;

(6) The deposit must not be provided in connection with the FDIC-supervised institution’s provision of prime brokerage services,

which, for the purposes of this part are a package of services offered by the FDIC-supervised institution whereby the FDIC-

supervised institution, among other services, executes, clears, settles, and finances transactions entered into by the

customer or a third-party entity on behalf of the customer (such as executing brokers), and where the FDIC-supervised

institution has a right to use or rehypothecate assets provided by the customer, including in connection with the extension

of margin and other similar financing of the customer, subject to applicable law and includes operational services provided

to a non-regulated fund; and

(7) The deposits must not be for arrangements in which the FDIC-supervised institution (as correspondent) holds deposits

owned by another depository institution bank (as respondent) and the respondent temporarily places excess funds in an

overnight deposit with the FDIC-supervised institution.

Source: FDIC Law, Regulations, Related Acts – Rules and Regulations.

20

General Information and Disclaimers

This report has been prepared and issued by Sandler O’Neill + Partners, L.P., a registered broker-dealer

and a member of the Financial Industry Regulatory Authority, Inc. The information contained in this report

(except information regarding Sandler O’Neill and its affiliates) was obtained from various sources that we

believe to be reliable, but we do not guarantee its accuracy or completeness. Additional information is

available upon request. The information and opinions contained in this report speak only as of the date of

this report and are subject to change without notice. Contact information for Sandler O’Neill and the

author of this report is available at www.sandleroneill.com.

This report has been prepared and circulated for general information only and presents the author’s views

of general market and economic conditions and specific industries and/or sectors. This report is not

intended to and does not provide a recommendation with respect to any security. This report does not take

into account the financial position or particular needs or investment objectives of any individual or

entity. The investment strategies, if any, discussed in this report may not be suitable for all

investors. Investors must make their own determinations of the appropriateness of an investment strategy

and an investment in any particular securities based upon the legal, tax and accounting considerations

applicable to such investors and their own investment objective. Investors are cautioned that statements

regarding future prospects may not be realized and that past performance is not necessarily indicative of

future performance.

This report does not constitute an offer, or a solicitation of an offer, to buy or sell any securities or other

financial instruments, including any securities mentioned in this report. Nothing in this report constitutes

or should be construed to be accounting, tax, investment or legal advice.

Neither this report, nor any portion thereof, may be reproduced or redistributed by any person for any

purpose without the written consent of Sandler O’Neill.

© 2016 Sandler O'Neill + Partners, L.P. All rights reserved.