life underwriter training council course underwriter training council course disability income lutc...

TRANSCRIPT

LIFE UNDERWRITER

TRAINING COUNCIL

COURSE

DISABILITY INCOME

LUTC 211

WORKBOOK

THE LIFE UNDERWRITER

TRAINING COUNCIL

Established 1947 by American Life Convention

Life Insurance Agency Management Association (now LIMRA)

Life Insurance Association of America

The National Association of Life Underwriters

FORTY-SECOND EDITION

© THE LIFE UNDERWRITER TRAINING COUNCIL • 1998

7625 WISCONSIN AVE., BETHESDA, MD 20814-3560

All Rights Reserved.

WO

RK

BO

OK

Workbook W-3

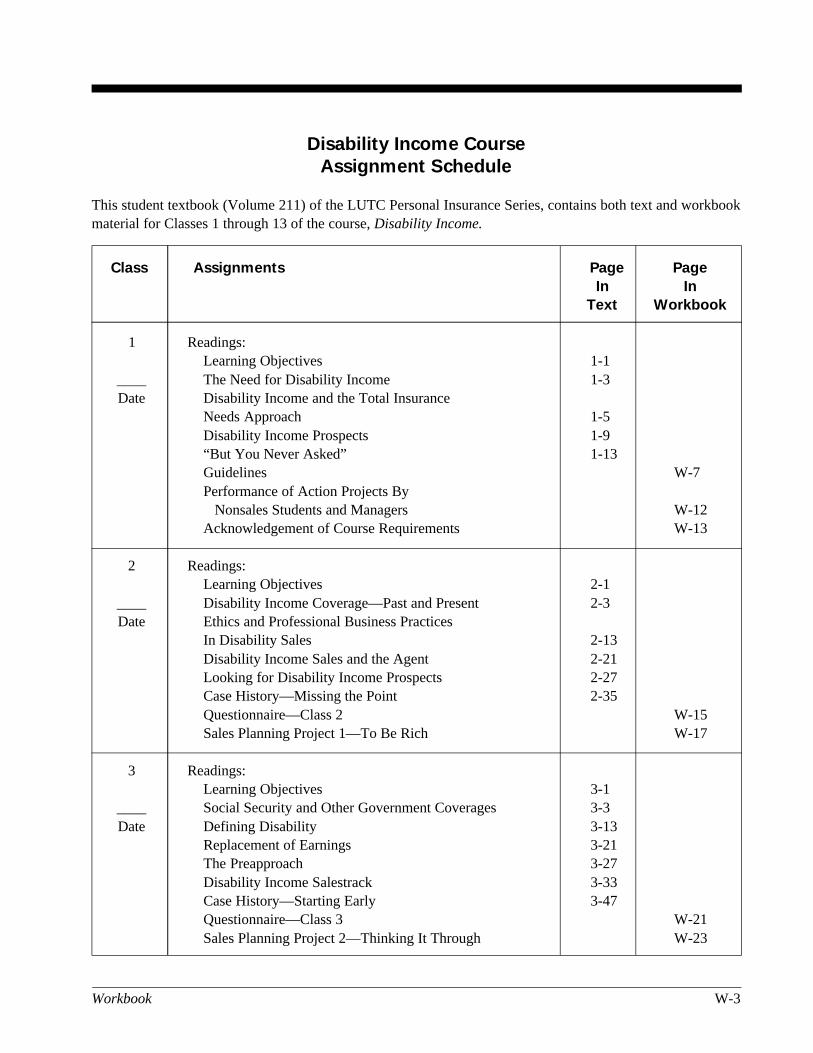

Disability Income Course

Assignment Schedule

This student textbook (Volume 211) of the LUTC Personal Insurance Series, contains both text and workbookmaterial for Classes 1 through 13 of the course, Disability Income.

Class Assignments Page Page

In In

Text Workbook

1 Readings:Learning Objectives 1-1

____ The Need for Disability Income 1-3Date Disability Income and the Total Insurance

Needs Approach 1-5Disability Income Prospects 1-9“But You Never Asked” 1-13Guidelines W-7Performance of Action Projects By Nonsales Students and Managers W-12Acknowledgement of Course Requirements W-13

2 Readings:Learning Objectives 2-1

____ Disability Income Coverage—Past and Present 2-3Date Ethics and Professional Business Practices

In Disability Sales 2-13Disability Income Sales and the Agent 2-21Looking for Disability Income Prospects 2-27Case History—Missing the Point 2-35Questionnaire—Class 2 W-15Sales Planning Project 1—To Be Rich W-17

3 Readings:Learning Objectives 3-1

____ Social Security and Other Government Coverages 3-3Date Defining Disability 3-13

Replacement of Earnings 3-21The Preapproach 3-27Disability Income Salestrack 3-33Case History—Starting Early 3-47Questionnaire—Class 3 W-21Sales Planning Project 2—Thinking It Through W-23

W-4 Disability Income

Class Assignments Page Page

In In

Text Workbook

4 Readings:Learning Objectives 4-1

____ How Much Coverage Is Available? 4-3Date Analyzing Needs 4-7

How to Approach the Prospect UsingDisability Income Coverage 4-15The Art of Fact Finding 4-21Case History—Asking the Right Questions 4-31Questionnaire—Class 4 W-25Action Project 1—Are You Covered? W-27

5 Readings:Learning Objectives 5-1

____ When Coverage Begins and Ends 5-3Date Policy Definitions 5-9

What Is Not Covered? 5-15Other Policy Provisions 5-19Tax Implications of Personal Disability Income Insurance 5-27Disability Income and Other Sales 5-29Case History—Average Doesn’t Even Come Close 5-35Questionnaire—Class 5 W-31Sales Planning Project 3—Analyzing Coverage W-33

6 Readings:Learning Objectives 6-1

____ When Is Coverage Renewable? 6-3Date Disability Income Availability 6-7

Additional Policy Benefits and Riders 6-13Modifying Coverage 6-21Avoiding Overinsurance 6-27Case History—In It Together 6-31The Hobart Case 6-35Questionnaire—Class 6 W-37Action Project 2—Is It Enough? W-39

Workbook W-5

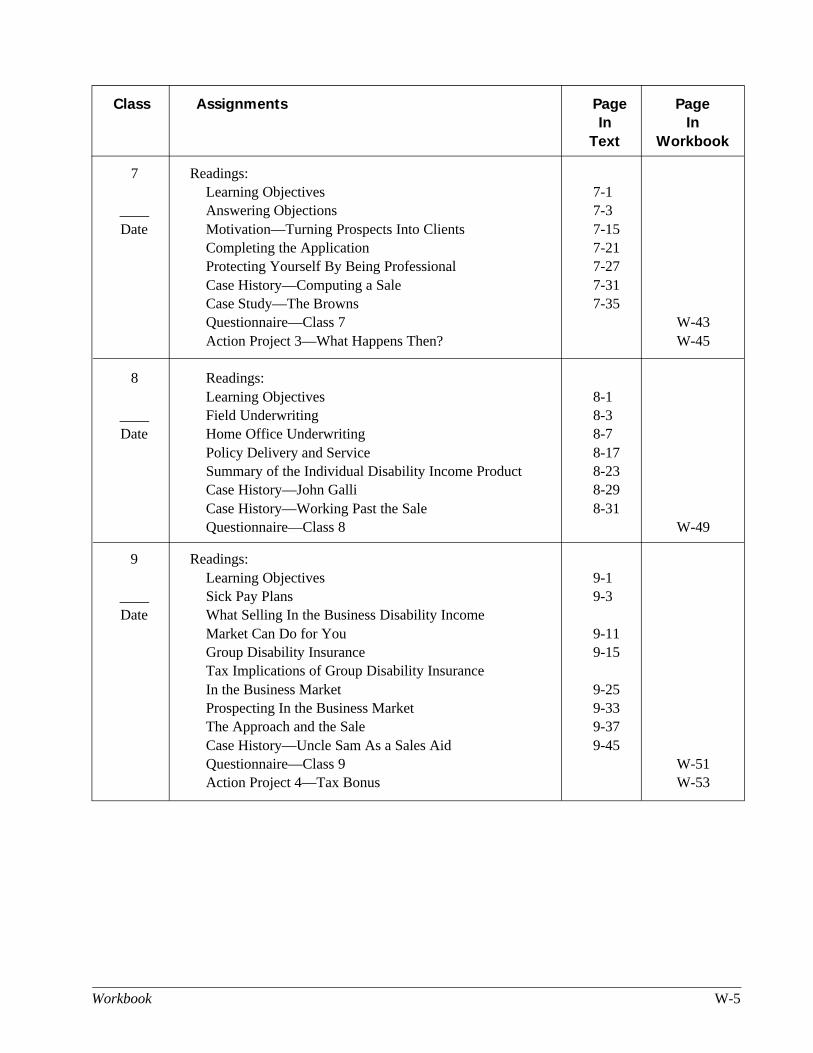

Class Assignments Page Page

In In

Text Workbook

7 Readings:Learning Objectives 7-1

____ Answering Objections 7-3Date Motivation—Turning Prospects Into Clients 7-15

Completing the Application 7-21Protecting Yourself By Being Professional 7-27Case History—Computing a Sale 7-31Case Study—The Browns 7-35Questionnaire—Class 7 W-43Action Project 3—What Happens Then? W-45

8 Readings:Learning Objectives 8-1

____ Field Underwriting 8-3Date Home Office Underwriting 8-7

Policy Delivery and Service 8-17Summary of the Individual Disability Income Product 8-23Case History—John Galli 8-29Case History—Working Past the Sale 8-31Questionnaire—Class 8 W-49

9 Readings:Learning Objectives 9-1

____ Sick Pay Plans 9-3Date What Selling In the Business Disability Income

Market Can Do for You 9-11Group Disability Insurance 9-15Tax Implications of Group Disability InsuranceIn the Business Market 9-25Prospecting In the Business Market 9-33The Approach and the Sale 9-37Case History—Uncle Sam As a Sales Aid 9-45Questionnaire—Class 9 W-51Action Project 4—Tax Bonus W-53

W-6 Disability Income

Class Assignments Page Page

In In

Text Workbook

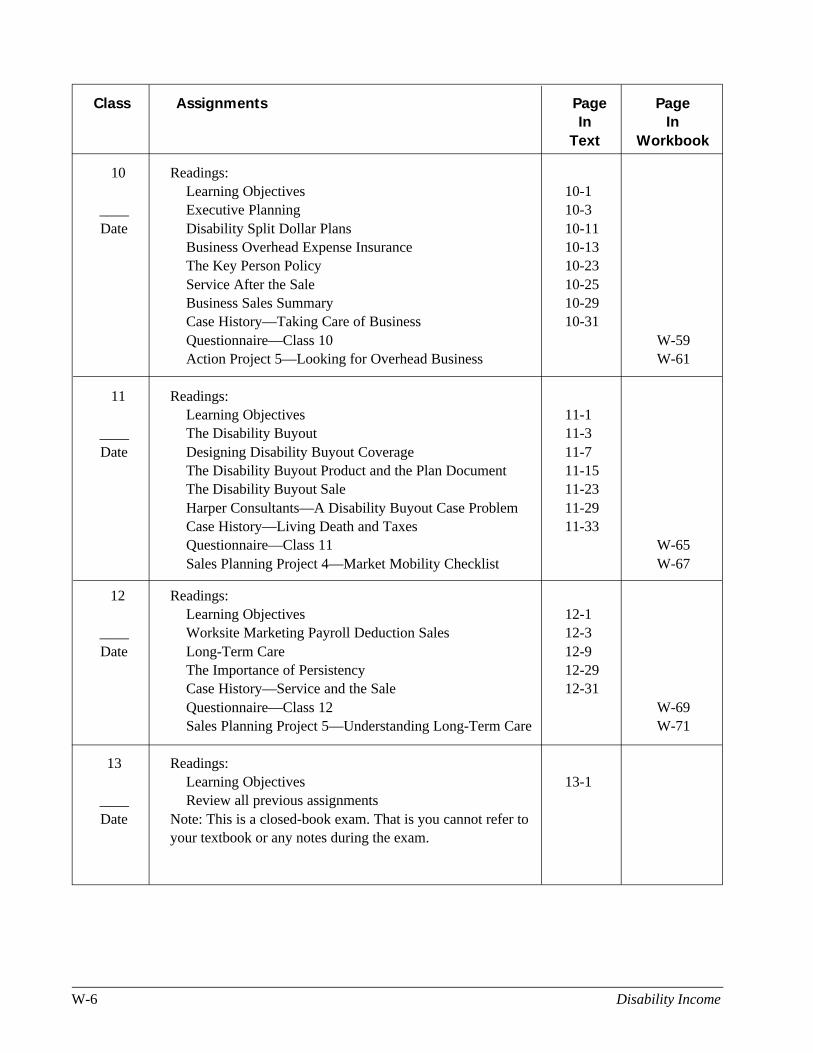

10 Readings:Learning Objectives 10-1

____ Executive Planning 10-3Date Disability Split Dollar Plans 10-11

Business Overhead Expense Insurance 10-13The Key Person Policy 10-23Service After the Sale 10-25Business Sales Summary 10-29Case History—Taking Care of Business 10-31Questionnaire—Class 10 W-59Action Project 5—Looking for Overhead Business W-61

11 Readings:Learning Objectives 11-1

____ The Disability Buyout 11-3Date Designing Disability Buyout Coverage 11-7

The Disability Buyout Product and the Plan Document 11-15The Disability Buyout Sale 11-23Harper Consultants—A Disability Buyout Case Problem 11-29Case History—Living Death and Taxes 11-33Questionnaire—Class 11 W-65Sales Planning Project 4—Market Mobility Checklist W-67

12 Readings:Learning Objectives 12-1

____ Worksite Marketing Payroll Deduction Sales 12-3Date Long-Term Care 12-9

The Importance of Persistency 12-29Case History—Service and the Sale 12-31Questionnaire—Class 12 W-69Sales Planning Project 5—Understanding Long-Term Care W-71

13 Readings:Learning Objectives 13-1

____ Review all previous assignmentsDate Note: This is a closed-book exam. That is you cannot refer to

your textbook or any notes during the exam.

Workbook W-7

GuidelinesLUTC is practical, on-the-job, sales training. As such, it requires that the stu-dent “get into the act” and participate fully.

The workbook is intended to help you actively participate. In it are theschedule for the course, text assignments, questionnaires, sales planning projectsand action projects. Supplementary material may be included for use as yourmoderator directs.

What you derive from LUTC depends on you. If you take full responsibilityfor accomplishing all the objectives along the way and if you make a persistenteffort to participate in the class sessions, you will improve your knowledge andskill. For some life underwriters, this experience has been the beginning ofhighly successful careers. What it is for you is your choice.

AssignmentsActive class participation will be encouraged by your moderator at every ses-sion. To augment this discussion, you will be given outside assignments toinsure that you will be ready to apply the principles you are studying. Thetimetable for these assignments can be found in the assignment schedule in thefront of this workbook section.

Assignment Schedule

The assignment schedule lays out the entire course’s work. By following it, youcan readily determine the material that will be covered in every class, and thework that is expected of you.

The dates of each session will be announced by your moderator. Insert thesedates in the spaces provided on the schedule.

Before Class—Assignments must be completed before the class meets. Be-fore attending each session you are expected to complete specific work.

• Read and study the pages of text assigned.Complete the written questionnaire. These questionnaires are found inthis workbook.

• Complete the sales planning project assigned.• Complete work on the action project and review it with your agency

head or sales supervisor prior to turning it in to the moderator.• Complete all other assignments indicated in the text or by your

moderator.

W-8 Disability Income

In Class—When you attend the class session, you are expected to beprepared.

Turn in assignments at the beginning of class. All assignments are sched-uled well in advance to allow sufficient time for accomplishment of objectives.Your moderator has been directed to penalize late papers by 50 percent. If morethan a week late, papers receive a zero. Participate in class discussions based onthe assigned text material, questionnaires, projects, and your experience in sell-ing insurance.

Texts

The purpose of LUTC is to develop sales skill and professionalism. Improvedability requires knowledge as well as practice. The text materials are designedto provide the knowledge that must form the foundation for better performance.Reading and studying the texts places all students at the same minimum level ofunderstanding with basic concepts and knowledge.

The texts are the product of efforts by many individuals—agents, fieldmanagers, trainers, home office specialists, company officers, authorities in theindustry, as well as members of the Content and Techniques Committees. Thesecommittees are comprised of a balance of field and home office specialists whoannually advise and assist the LUTC staff in its research and editing of the textmaterials. Finally, it should be noted that many suggestions ultimately incorpo-rated into the programs originally came from students themselves.

The written questionnaire for each class is based on the assigned text read-ing. It is intended as a means of highlighting some of the more important areasof the study material and as a test of your grasp of the material before youattempt to use it where it counts—in front of a prospect.

Some of the text material will be new to you; some of it will be a refresherof knowledge learned in the past. In either case, you will find it valuable andnecessary as preparation for the class discussions and the examination. Thebenefits you gain will be in direct proportion to the effort you expend. Everystudent will be expected to spend no less time in preparation for class discus-sion than the time allowed for discussions—two and one-half hours. To do lesswould be to deprive yourself of a unique opportunity to learn more aboutselling. It would also deprive your fellow students of the very important advan-tage of learning from you.

Cases

The LUTC program presents two types of case material for your study. Youmay consider both case histories and case studies.

Case History—The purpose of a case history is to stimulate thinking aboutsales ideas and activities. Each case is the story of an actual sales situation. Theapproach used by the agent may or may not be good in your estimation. Thekey point is to determine what you can learn from the example. How wouldyou handle a similar situation? Does the case suggest methods in the saleprocess that you want to adopt or avoid?

Workbook W-9

Incidentally, many case histories are submitted by LUTC students. If youhave a case that you feel might serve a good purpose in future editions of thetext, advise your moderator. He or she will help you prepare a description of thecase and submit it to LUTC headquarters for review.

Case Study—A case study provides you with an opportunity to activelyparticipate and practice some of the skills you are discussing and learning. Youwill be given a specific set of facts and circumstances about a sales situation.Then it will be your assignment to consider the situation and come up withspecific recommendations as well as provide and support your rationale forarriving at the conclusions.

The benefit of this activity is the sharing of the conclusions of many stu-dents. It is interesting and helpful to learn several different approaches to thesame set of facts.

Examinations

A final examination is included in all courses. You must pass the final examina-tion in order to pass the course. Passing is 70 percent. All fifty exam questionsare in the multiple-choice format.

Sales Planning Projects

Each sales planning project relates to the work of a life underwriter when notactually selling. The projects are arranged to give you a comprehensive andintegrated picture of various aspects of your sales methods, to highlight areas inwhich you may need strengthening, to increase your efficiency in prospecting,interview planning, and service.

It has been said that there is no such thing as a “born salesperson.” Somemay doubt the validity of this observation in its full meaning, but few woulddeny that the majority of top agents are successful because of their training—thehabits they acquired in learning their profession. Selling is not a mysteriouspower to hypnotize people. It is a scientific process that includes all the orga-nized forces of logic and emotion that a sales professional can develop. Everystep of a sale must be carefully planned and every phase of an agent’s total salesactivities must also be carefully planned.

Your presence in this LUTC class testifies to your recognition of these basicprinciples. A person does not become a life underwriter simply by signing acontract with an insurance company any more than a person could become aprofessional athlete simply by signing a contract. It takes organized efforts toreach the heights. No phase of selling can be neglected if the agent wants tobecome a true leader. This means careful, methodical learning of the skillsrequired, including prospecting, keeping records, analyzing success and failure,adapting the company’s products to the customer’s situation, needs, and wants.Note that these are, for the most part, demands made of the sales representativebefore and after facing a prospect. They are requirements in addition to actualselling. These are the things that must be done efficiently and habitually to achievesuccess. The sales planning projects are designed to emphasize this point.

Forms are provided for your use in developing each project. You will be

W-10 Disability Income

allowed one week or more to carry out each assignment. You are expected totake this opportunity to derive maximum benefit from the projects. Work on aproject should begin the day it is assigned. If the beginning is postponed untilthe last possible moment, you will find that you have missed the real purposeand have lost the real benefit.

Any one of the sales planning projects could generate the extra spark thathelps you increase your production substantially.

Action Projects

Knowledge misdirected is a waste of intelligence; skill unpracticed is a waste oftalent. No part of an LUTC course is more important than an action project.Action projects require you to take your newly sharpened skill to the marketplace for immediate use. You will find that each action project is a practical andprofitable means of immediately applying the ideas you gained today. And youwill find that immediate use of your new skill in front of a prospect will makethat skill yours for the rest of your career.

The action projects are a series of field-tested “sales missions” which aresimple in design, yet developed around ideas, markets, or approaches whichmight otherwise be neglected. They will readily fit into any agent’s normaloperations. Special preparation is not necessary. No extra research or study isinvolved. Nor are these assignments intended to replace any of your regularwork habits. On the contrary, an action project’s greatest value will be realizedonly if you treat it as an additional effort in your week’s regular activities.

Sales are almost inevitable, but they are not required for completion of theaction project. Only action is required. In every action project there will be aspecific brief assignment that calls for a personal contract with a number ofprospects for a definite purpose. The purpose will be clearly defined. An ap-proach will be suggested.

As you prepare for each project consider any appropriate sales materialavailable from your company or agency. Consult with your manager or supervi-sor to obtain guidance for completing the projects.

The action projects are the real test of the value of this course. Approachedwith the proper attitude they will be profitable for you.

Cooperation

Your moderator is an outstanding individual nominated by the life underwritersassociation and appointed by LUTC headquarters. He or she is not a teacher byprofession, but a full-time career representative in sales or management. Yourmoderator shares with you the demands of self-discipline and constant pressureof time. Consequently, the moderator cannot afford the luxury of catering toanyone who is negligent about the rules of LUTC or the class with respect tocompleting work on time, maintaining reasonable order, and respecting the rightsof others. The moderator needs and deserves the full cooperation of every student.If at times this means that one or two individuals must sacrifice their personal

Workbook W-11

preferences for the good of the group, they should be prepared to do so. The loss oftheir preferences will mean nothing a few months from now. The resultant benefitto all members of the group can be significant for years into the future.

Conclusion

Training experts generally agree that an effective system of training must in-clude adequate coverage of the material to be learned, immediate application,recognition of results, and repetition. On the first three points, the format of thecourse you are about to begin has qualified for many years. Principles andtechniques are an essential part of every class session; application is direct andimmediate; results are clearly perceived in daily field work, in the question-naires, and examinations, and in the weekly discussions.

The fourth point, repetition, is far more extensive in its reach. Each prin-ciple or technique must be put into practice often enough and for a long enoughperiod to make it a habitual part of your regular sales activities. This aspect ofthe training program is the exclusive responsibility of only one person—you.

To the degree that you try to use all you have learned, the benefits of LUTCwill be yours for the rest of your life.

Passing Requirements

Attendance—Your participation in the classroom discussion is crucial to the effectiveness of theLUTC program. Therefore, your attendance is also vital. To successfully complete the course, you mustattend at least 9 of the 12 regular classes. For 8 week courses, you must attend at least 6 of the 8 regularclasses. It means no more than 3 absences for thirteen week courses and no more than 2 absences for 8week courses. Lateness of more than 20 minutes is half an absence. So is early leaving. Missing more than40 minutes is a full absence. If you end the year with 31¦2 absences, you have exceeded the allowable limit of3. If you are in an 8-week course and end the year with 21¦2 absences, you have exceeded the allowable limitof 2.

Moderator’s Grade—Your moderator will record your grades for written questionnaires, projects,and participation in class sessions. These grades will be combined to obtain the average grade for allclassroom related work, the Moderator’s Grade.

Examination Grade—There will be a 50-question final examination at the end of the course. Thequestions will be multiple choice. A grade of 70 percent or higher is necessary to pass the exam.

Term Grade—The average of the Moderator’s Grade and the final examination score must be no lessthan 70 percent to obtain credit. This average is called the Term Grade.

Three Requirements—In summary, to qualify for successful completion of the course, you mustmeet each of the following three requirements:

1. Meet the attendance requirement for your course.2. Score 70 percent or more on the final examination, and3. Receive a Term Grade of at least 70 percent.

W-12 Disability Income

Performance of Action Projects

by Nonsales Students & Managers

All students are expected to do the Action Projects in the Disability Income Course. This applies tostudents who are nonproducers and to those in management. It includes, for example, students such asoffice secretaries, home office executives, state insurance commissioners, finance officer on a militarybase, and others who may not be licensed to sell life insurance.

If you cannot do the projects yourself, as they are shown, you are expected to handle the projectsin one of the following ways. (They are listed in order of LUTC’s preference.)

1. Select a local Disability Income Course student with your company, in your community, towork with in doing this project. Base your reports on this joint work.

2. If there is no local LUTC student from your company to work with, do joint work with oneof your company’s agents who is not in LUTC. This could be a former LUTC student, orsomeone without any LUTC experience.

3. If you are in management, and if it is not possible to work with an agent/student, assign theprojects to one or more of the agents under your supervision, and report these results.

4. If you have no agents to work with, and no agents under your supervision, arrange tointerview one or more agents each week, and use the interview as the basis of the projectreport. That is, on the project reporting form, relate what the agent did, and details of whattranspired.

5. If the four preceding options are unworkable for you, it is up to you to suggest alternatesolutions that you and your moderator agree on. For example, you may develop a presenta-tion to write out or give orally to the LUTC class when an Action Project is due. This may beon a specialty topic of yours. Or, another example, you may research a particular insurancetopic, or sales topic, and write it out, giving photocopies to all class members. Topics caninclude, for example, state laws, statistical information about insurance, actuarial studies,articles in insurance magazines, self-improvement topics, relationship insights, even a ques-tion about something that came up in calss and needs reserach for a clearer understanding.

Keep in mind, these five alternatives are special options for isolated instances. Almost everystudent in a LUTC class is licensed to sell insurance and is expected to complete the Action Projectsas assigned for a passing grade. That is, you are expected to do the prospecting activity and make thefollow-up approaches yourself.

If you need to do the projects in one of the ways shown above, discuss it in advance with yourmoderator. That is, let your moderator know about your situation. Talk over the alternatives with himor her. Get agreement on how to proceed. To safeguard yourself, put your agreement in writing,include both of your signatures and file.

Workbook W-13

Note to LUTC Students

Please read this page carefully, sign at the bottom, and return the bottom portion to your moderatorsafter having your supervisor sign the other side. Occasionally there are misunderstandings concerningthe requirements for successful completion of the course. The purpose of this memorandum is to insurethat the basic requirements of LUTC and the ground rules laid down by the moderator are clearlyunderstood. Failure to sign this form does not relieve you from these provisions.

Acknowlegement of Course Requirements

—To be signed by student—

It is my understanding, from the explanation received in the first class session and outlined in the Guidelinessection of the workbook, that successful completion of this LUTC course requires 80% attendance, a passingexamination score (70%), and an overall average (term grade) of 70% on all work for the year. Specifically, Iunderstand that:

1. Credit for the course will not be given to any student who fails to attend at least ten (10) classsessions, including the final exam. The maximum number of absences is three (3). Missing more than20 minutes of class is a half-absence. Missing more than 40 minutes of class is a full absence. It doesnot matter whether absences are due to illness, injury, business appointments, company or agencymeetings, vacations or conflicts in personal schedules. No attendance credit is given for attendance atan exam review session. I further understand that neither the LUTC chair or moderators has authorityto excuse absences, since the requirement applies impartially to all LUTC students.

2. Grades are assigned during the course by the moderator. Grades for participation in class discussions(and preparation for them), and scores made on Action Projects, Sales Planning Projects and Ques-tionnaires are averaged. That number is then averaged with the final examination to arrive at the TermGrade.

3. Written assignments are due at the beginning of the session in which they are due. Late papers areautomatically reduced by 50% up to one week late and to zero after that.

4. To receive credit for the course, I must sit for and receive a passing grade on a final examinationacceptable to LUTC. The nationally scheduled exam date cannot be changed. LUTC reserves theright to set aside the final examination of any class and require another examination.

5. Course results will be amiled out within four weeks after the final exam date, assuming all courserequirements have been met, including payment of tuition. These reports will indicate a “passing” or“not passing” status only. No numerical grade is assigned.

Return the bottom portion of this form to the moderator after your agency supervisor has signed the reverse side.

I have read the course requirements and understand them.

I further understand that recruiting or attempted recruiting of personnel of another company is not permitted inthe LUTC program or in connection therewith.

Finally, I understand that any student whose behavior adversely affects reasonable order and harmony in theLUTC class is subject to disenrollment without tuition refund, and may be barred from future participation inLUTC Courses.

From: _________________________________________ _________________________________________Print your name Date Student’s Signature

Workbook W-15

Name_______________________________________________ Date ______________________________

Questionnaire—Class 2

(Due Class 2)

(10 points each.)

1. Disability income insurance:

(1) was developed before the development of life insurance.(2) was developed before the development of property and casualty insurance.(3) was developed after both life and property and casualty insurance.(4) first appeared during the Great Depression.

2. The definition of “disability”:

(1) is standard in all products.(2) can differ greatly.(3) changes according to each disability.(4) is changed every three years by a Disability Board of Examiners.

3. Disability income coverage and medical coverage:

(1) are often both needed in times of illness or injury.(2) should never be sold to the same person since duplication of benefits would occur.(3) are different names for the same coverage.(4) both provide income replacement if the insured is ill or injured.

4. Which of the following statements is correct regarding guaranteed renewable policies?

(1) The premium cannot be changed.(2) Premiums may be changed unilaterally on an individual contract.(3) Coverage is guaranteed as long as premiums are paid.(4) Coverage is guaranteed renewable as long as the insured meets the employment and income criteria.

5. Disability income coverage:

(1) is an excellent “wrap-up” presentation in a total-needs approach.(2) can be closely related to the need for life insurance.(3) can be closely related to the need for property and casualty insurance.(4) all of the above.

W-16 Disability Income

6. In providing disability income coverage, an agent should:

(1) offer it only to professional people.(2) offer it only to prospects who are healthy.(3) offer it to all prospects who have a need for it.(4) offer it only to life clients, since they are the only people likely to have a need for it.

7. Which market would probably need disability income insurance?

(1) single wage earners.(2) single heads of households.(3) dual income households.(4) all of the above.

8. Licenses to sell disability income insurance are issued by:

(1) Department of Health and Welfare.(2) National Association of Securities Dealers.(3) State governments.(4) National Health Insurance Association (NHIA).

9. An agent’s legal and ethical responsibility is to:

(1) get the coverage needed issued for his or her client.(2) help the prospect present medical information in the most favorable light.(3) draw out as much detail as possible and present it fully.(4) keep information received from a prospect in confidence from the home office.

10. The voluntary organization of insurance companies created to promote ethical business practices is the:

(1) NAIC.(2) IMSA.(3) LUTC.(4) NALU.

Workbook W-17

Sales Planning Project 1

To Be Rich

Assigned Class 1—Due Class 2

This project requires you to prepare a disability income sales approach for presentation in class. You may usethe one suggested here, one provided by your company, or one you develop yourself. Beginning with Class 2,and during the remaining sessions, be prepared to present your sales approach in class exactly as you wouldto a prospect. It should take no longer than ten minutes to present.

An effective sales presentation contains a series of good sales ideas that lead the prospect to a positivedecision. When you tell the same sales story again and again, day after day, it becomes a part of you and anatural route to follow—to success.

Are You Rich?

“(Prospect), would you say you are rich? Except for rich people, most of us have a financialpicture that looks like this:

(At this point draw two horizontal lines—not too far apart. Label the top line “income”and the lower line “expenses.” See reverse side for illustration.)

“Most of us manage to keep a little of what we earn after expenses are paid. The differencebetween income and expenses—savings—may not be much. But as long as the income line isabove the expense line, we’ll be all right. Do we agree so far?

“Now, suppose something comes along to twist the directions of these lines. The ‘something’that will surely do it is disability. Then the income line heads south and the expense line goesup, like this:

(Draw income line down toward bottom of page, expense line up.)

“Savings are eaten up in a hurry—not just by medical bills, although they usually exceed anyinsurance coverage you have, but by ‘routine’ living costs. The difference between income andexpenses now is not savings, but DEBT.

“What do you do? There is a limit to what people will lend someone totally disabled and out ofwork. Relatives and friends would help, but they have their own problems—and wouldn’t theyrightfully expect you to use up your own resources before they begin contributing theirs?

“You could possibly sell your car or even your home, but I’m sure you wouldn’t want that—and there is a better way to solve the problem.

“In a manner of speaking, the better way is to be rich enough—not rich in the usual sense, butin the sense of having an extra source of money that can be called on when earnings stop...asource of money to take care of the disability problem.

“Let me show you how easily it can be arranged...”

Note: Please see Caution on page ii.

tt

INC

OM

E

DIS

AB

ILIT

Y

EX

PE

NS

ES

D E B T

t

t

t

OR

INC

OM

E

INS

UR

AN

CE

t

S A V I N G S

Workbook W-19

Name_______________________________________________ Date ______________________________

Sales Planning Project 1

To Be Rich

Assigned Class 1—Due Class 2

CERTIFICATION STATEMENT

I have prepared a disability income sales approach for presentation in class. When called on in class

by the moderator, I will do the best I can in demonstrating my proficiency.

SIGNED _______________________________________________ (Student)

Workbook W-21

1. The Social Security definition of disability is:

(1) modified in each individual case.(2) currently interpreted very liberally.(3) quite strict, so benefits are difficult to get.(4) fairly liberal, so many people will receive benefits.

2. Workers’ compensation benefits:

(1) vary widely by state.(2) cover all disabilities.(3) cover work-related accidents only.(4) are available only in a few states.

3. The definition of disability is:

(1) very subjective.(2) the same in every policy.(3) relatively unimportant in determining coverage in case of a claim.(4) usually determined by the courts after disability occurs.

4. A residual disability benefit:

(1) pays for presumptive disability.(2) encourages the insured to return to work.(3) forces the insured to remain at home until fully recovered.(4) is payable only for a limited time.

5. Under the residual benefit provision, benefits are:

(1) based on 50% of the insured’s base earnings.(2) proportional and based on a percentage of lost income.(3) unavailable if the insured is working part-time.(4) payable for the 30-day period after the insured’s return to work.

6. For what length of time are benefits payable under a presumptive disability clause?

(1) for the length of the benefit period in the basic policy(2) only if the insured is under a doctor’s care(3) until the insured returns to work in any occupation(4) until the insured returns to work in his or her regular occupation

Name_______________________________________________ Date ______________________________

Questionnaire—Class 3

(Due Class 3)

(10 points each.)

W-22 Disability Income

7. Using savings to replace income lost from disability:

(1) makes most expenses during disability tax deductible.(2) can make it difficult to meet other financial goals.(3) is the best solution for a period of disability under a year.(4) is the only option for self-employed people.

8. The amount of Social Security disability benefits an eligible individual will receive is:

(1) based on his or her Primary Insurance Amount (PIA).(2) 50% of his or her AIME.(3) based on the maximum limit of $61,200.(4) 75% of his or her gross income.

9. To qualify for Social Security disability benefits, a person must:

(1) be over age 65.(2) complete the 12-month waiting period.(3) be fully insured under Social Security.(4) have 15 consecutive years of covered work experience.

10. The Social Security offset provision that pays the difference between the insured amount and the amountreceived from Social Security benefits is known as the:

(1) all or nothing provision.(2) all, part or nothing provision.(3) direct offset provision.(4) income loss provision.

Workbook W-23

Name_______________________________________________ Date ______________________________

Sales Planning Project 2

Thinking It Through

Assigned Class 2—Due Class 3

Disability income coverage is one of the products you can offer your prospects and clients. However, you mayhave concentrated on life insurance, with disability income insurance taking a secondary role or no role at all.

This project focuses attention on your attitude, knowledge, and sales efforts in the area of disability incomecoverage. It will help you define your thoughts about disability income insurance, identify the activity you’vehad in selling the product, and formulate plans for future activity in the disability income area.

In completing the following questions, be totally honest with yourself. There are no “right” or “wrong”answers. This exercise is not planned to justify your outlook but to examine it. Consider each point carefully,and respond honestly. A serious effort to analyze your own sales record, attitude, and plans at this point willhelp you make the most of participation in this course.

1. (a) List the products you can offer your clients and prospects. (Consider life, health, disability income,property and casualty, etc.)

(b) Which product is your “lead line” and why?

2. (a) How many years and months have you been licensed to sell health insurance products?

(b) What kind of health insurance do you sell the most, and why?

W-24 Disability Income

3. Using a recent month as a basis (choose an example that seems typical to you), to what percentage ofprospects did you offer disability income coverage?

(a) by itself?

(b) as part of another sales presentation?

4. (a) Some of the people you talked with about other products were probably disability income prospects,too. Did you approach them about disability income coverage? If so, what were the results?

(b) If you did not approach these prospects, why not?

5. What production goals have you set for life insurance this year? What goal have you set for disabilityincome coverage?

6. What commission rate do you receive for a term life insurance policy? What for whole life? What foruniversal life? What rate do you receive for disability income protection?