levy of service tax levy of service tax pradeep. k mittal member central council of the institute of...

TRANSCRIPT

LEVY OF SERVICE TAXLEVY OF SERVICE TAX

Pradeep. K MittalPradeep. K MittalMember Central Council of Member Central Council of The Institute of Company The Institute of Company

Secretaries of India, New DelhiSecretaries of India, New Delhi AdvocateAdvocate

Delhi High CourtDelhi High Court

CommercialCommercial or Industrial or Industrial Construction ServiceConstruction Service

According to Section 65 of Finance Act,1994, the terms According to Section 65 of Finance Act,1994, the terms “Commercial or Industrial Construction service”Means- “Commercial or Industrial Construction service”Means-

a)a) Construction of a new building or a civil Construction of a new building or a civil structure or a part thereof ; or structure or a part thereof ; or

b)b) Construction of pipeline or conduit ; orConstruction of pipeline or conduit ; or

c)c) Completion and finishing services such as Completion and finishing services such as glazing, plastering, painting, floor and wall tiling, glazing, plastering, painting, floor and wall tiling, wall covering and wall papering,wood and metal wall covering and wall papering,wood and metal joinery and carpentry, fencing and railing, joinery and carpentry, fencing and railing, construction of swimming pools, acoustic construction of swimming pools, acoustic applications or fittings and other similar services, in applications or fittings and other similar services, in relation to building or civil structure; orrelation to building or civil structure; or

d)d) repair, alteration, renovation or restoration of, repair, alteration, renovation or restoration of, or similar services in relation to, building or civil or similar services in relation to, building or civil structure, pipeline or conduit,structure, pipeline or conduit,

Which is (a) used, or to be used, primarily for ; or (b) occupied, or to be occupied, primarily with ;or (c) engaged ,or to be engaged, primarily in, commerce or industry, or work intended for commerce or industry, but does not include such service provided in respect of roads, airports, railways, transport terminals, bridges tunnels and dams.

SCOPE OF TAXABLE SCOPE OF TAXABLE SERVICESERVICE

The construction services provided by a Developer or Builder or Contractor to any person in relation to new construction,repairs,alteration or restoration of buildings, civil structures or parts thereof which are used,occupied or engaged for purpose of commerce and industry is subject to payment of Service Tax.

However, self construction, no Service Tax.However, self construction, no Service Tax.========================================================================================

a) Residential Buildings, offices of a) Residential Buildings, offices of government,and all other non commercial government,and all other non commercial buildings buildings and structures. and structures.

b) Constructions of Roads, Airports, Railways, b) Constructions of Roads, Airports, Railways, transport terminals, bridges, tunnel and dams transport terminals, bridges, tunnel and dams are excluded from this category of service are excluded from this category of service

c) Construction of Houses, Schools, temples, c) Construction of Houses, Schools, temples, Government building for non-commercial Government building for non-commercial

purposes etc. would not be covered under this purposes etc. would not be covered under this category of service. category of service.

EXCLUSIONS:EXCLUSIONS:

Further, if the building is both for residential Further, if the building is both for residential and and commercial purposes, service tax is payable commercial purposes, service tax is payable in case in case such immoveable property is treated as such immoveable property is treated as commercial commercial property by the local/Municipal property by the local/Municipal authority.authority.

(CBEC Circular 17.9.2004 & FAQ JUNE,06)(CBEC Circular 17.9.2004 & FAQ JUNE,06)

======================================

In order to construct, erect and develop any Building, Factory, Malls, Office Complex, Flatted Factories and other immoveable properties meant to be let out for commercial purposes, the developer, builder or contractor has to purchase cement, steel, construction materials, electrical equipments, generators, electrical, fittings, sanitary pipes and fittings, sliding windows,doors,glasses,tiling, paints,grills etc.

Besides the above, the developer/contractor also avail the services of various professionals like Architects,Chartered Engineers, RCC consultants, security services, Consulting Engineer, Interior designer etc.

The Contractor would be raising a consolidated bill The Contractor would be raising a consolidated bill or running account bills from time to time for such or running account bills from time to time for such construction services. The gross amount charged by construction services. The gross amount charged by any person providing the taxable service in relation any person providing the taxable service in relation to commercial or industrial building is the taxable to commercial or industrial building is the taxable value.value.

When the consideration is partly in money and When the consideration is partly in money and partly in terms of supply of cement, steel or other partly in terms of supply of cement, steel or other materials, the gross value shall be total of such materials, the gross value shall be total of such monetary consideration and money equivalent of the monetary consideration and money equivalent of the other non monetary consideration. It is quite likely other non monetary consideration. It is quite likely that non-monetary consideration could not be that non-monetary consideration could not be ascertained, gross amount charged by the same ascertained, gross amount charged by the same service provider for providing similar services shall service provider for providing similar services shall be taxable value.be taxable value.

The Notification No.15/2004 dated 10.09.2004 (now substituted by Notification No.1/2006 dt.1.3.2006) says that taxable service provided by a commercial concern to any person in relation to construction service is exempt from service tax leviable under Section 66 of the Finance act,1994 as is in excess of Service Tax Calculated on a value which is equivalent to 33% of the gross amount charged.

Further the Notification says that abatement to the extent of 67% of the gross value of the taxable services would be allowed provided the gross amount charged is inclusive of the value of the goods and materials supplied or provided or used for this service and the service provider does not avail the benefit under CENVAT credit scheme or the benefit of Notification No.12/2003 –ST dated 20.06.2003.

SERVICE TAX PAID ON VARIOUS SERVICES SERVICE TAX PAID ON VARIOUS SERVICES AVAILED FOR PROVIDING CONSTRUCTION AVAILED FOR PROVIDING CONSTRUCTION SERVICESERVICE

In order to construct, erect and develop any Building, factory, Godown, Flats, Malls, Office Complex, Flatted Factories and other immoveable properties meant to be let out for commercial purpose, the developer /contractor has to purchase cement, steel, construction materials, electrical equipments, generators, electrical fittings, sanitary pipes and fittings, sliding windows, doors, glases, tiling, paints, grills etc.

Besides the above, the developer/contractor also Besides the above, the developer/contractor also avail the services of various professionals like avail the services of various professionals like Architects, Chartered Engineers, RCC consultants, Architects, Chartered Engineers, RCC consultants, security Services, Consulting Engineer, Interior security Services, Consulting Engineer, Interior designer, Electrical Engineer, AC Engineer etc.designer, Electrical Engineer, AC Engineer etc.

The Question that arises for consideration is as to The Question that arises for consideration is as to whether the assessee will the entitled to avail the Cenvat whether the assessee will the entitled to avail the Cenvat Credit of the excise duty paid on purchase of Credit of the excise duty paid on purchase of construction material i.e. cement, steel, electrical construction material i.e. cement, steel, electrical equipments, generators, sanitary pipe fittings, sliding equipments, generators, sanitary pipe fittings, sliding windows, glasses, tiling, paints, grills etc. and service windows, glasses, tiling, paints, grills etc. and service tax paid to various professionals like architects, RCC tax paid to various professionals like architects, RCC consultants, security services, consulting engineer, consultants, security services, consulting engineer, interior designer etc.interior designer etc.

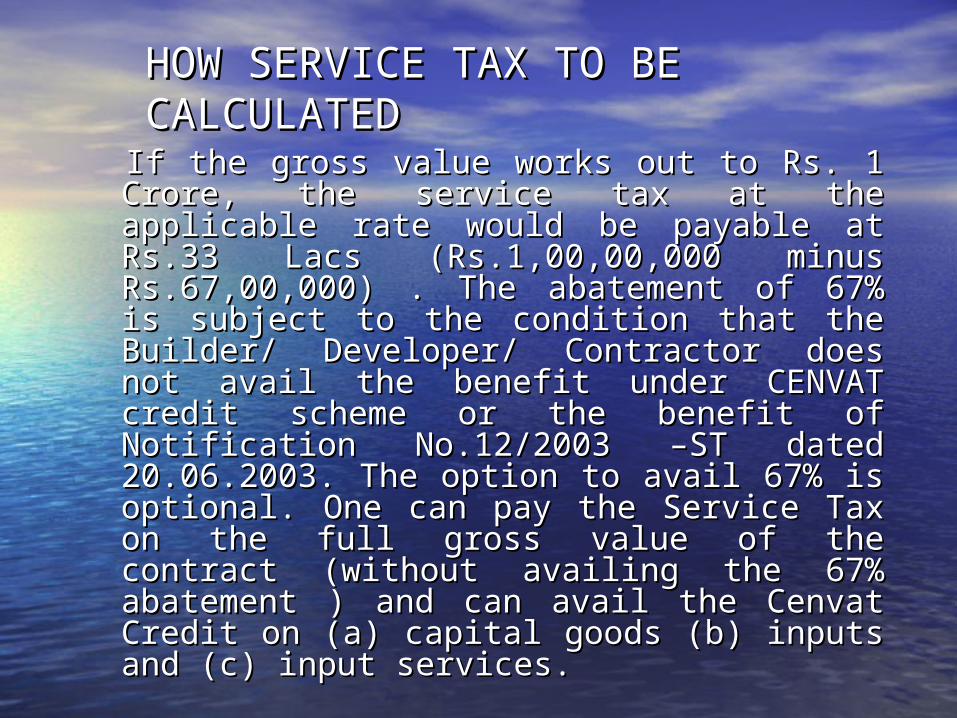

HOW SERVICE TAX TO BE HOW SERVICE TAX TO BE CALCULATEDCALCULATED

IIf the gross value works out to Rs. 1 Crore, the f the gross value works out to Rs. 1 Crore, the service tax at the applicable rate would be payable service tax at the applicable rate would be payable at Rs.33 Lacs (Rs.1,00,00,000 minus at Rs.33 Lacs (Rs.1,00,00,000 minus Rs.67,00,000) . The abatement of 67% is subject Rs.67,00,000) . The abatement of 67% is subject to the condition that the Builder/ Developer/ to the condition that the Builder/ Developer/ Contractor does not avail the benefit under Contractor does not avail the benefit under CENVAT credit scheme or the benefit of CENVAT credit scheme or the benefit of Notification No.12/2003 –ST dated 20.06.2003. Notification No.12/2003 –ST dated 20.06.2003. The option to avail 67% is optional. One can pay The option to avail 67% is optional. One can pay the Service Tax on the full gross value of the the Service Tax on the full gross value of the contract (without availing the 67% abatement ) contract (without availing the 67% abatement ) and can avail the Cenvat Credit on (a) capital and can avail the Cenvat Credit on (a) capital goods (b) inputs and (c) input services.goods (b) inputs and (c) input services.

InputInput

"Input" means- "Input" means-

(i) all goods, except light diesel oil, high speed (i) all goods, except light diesel oil, high speed diesel oil and motor spirit, commonly known diesel oil and motor spirit, commonly known as petrol, used in or in relation to the as petrol, used in or in relation to the manufacture of final products whether directly manufacture of final products whether directly or indirectly and whether contained in the final or indirectly and whether contained in the final product or not and includes lubricating oils, product or not and includes lubricating oils, greases, cutting oils, coolants, accessories of greases, cutting oils, coolants, accessories of the final products cleared along with the final the final products cleared along with the final product, goods used as paint, or as packing product, goods used as paint, or as packing material, or as fuel, or for generation of material, or as fuel, or for generation of electricity or steam used in or in relation to electricity or steam used in or in relation to manufacture of final products or for any other manufacture of final products or for any other purpose, within the factory of production; purpose, within the factory of production;

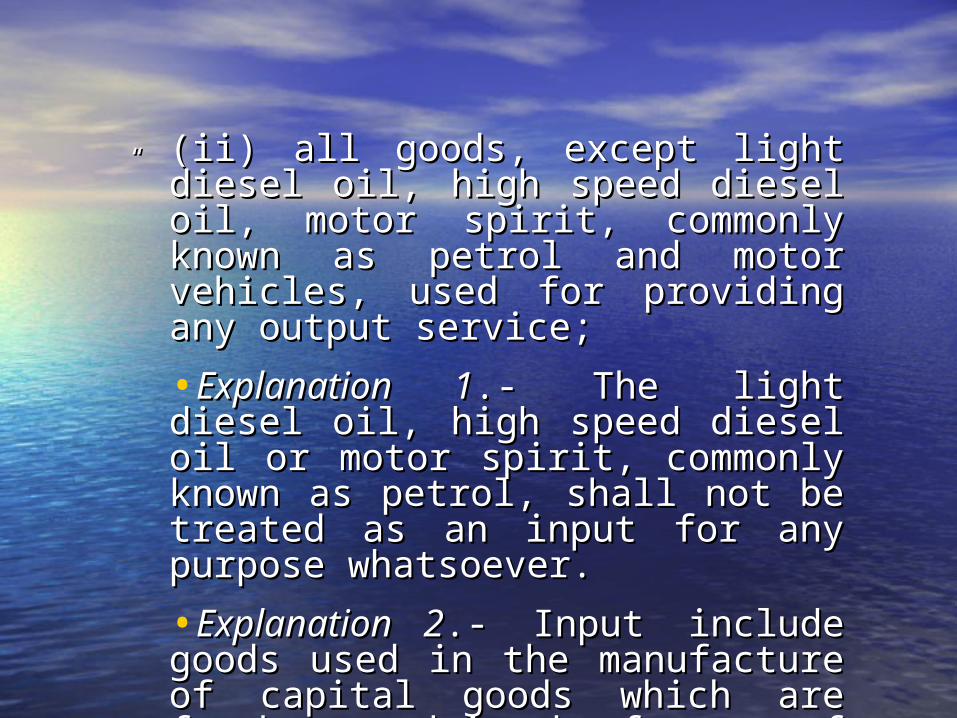

“ “ (ii) all goods, except light diesel oil, high (ii) all goods, except light diesel oil, high speed diesel oil, motor spirit, commonly speed diesel oil, motor spirit, commonly known as petrol and motor vehicles, used for known as petrol and motor vehicles, used for providing any output service; providing any output service;

•Explanation 1Explanation 1.- The light diesel oil, high .- The light diesel oil, high speed diesel oil or motor spirit, commonly speed diesel oil or motor spirit, commonly known as petrol, shall not be treated as an known as petrol, shall not be treated as an input for any purpose whatsoever.input for any purpose whatsoever.

•Explanation 2Explanation 2.- Input include goods used in .- Input include goods used in the manufacture of capital goods which are the manufacture of capital goods which are further used in the factory of the further used in the factory of the manufacturer;manufacturer;

Input serviceInput service "Input service" means any service,-"Input service" means any service,-(i) used by a provider of taxable service for providing an (i) used by a provider of taxable service for providing an output service; oroutput service; or(ii) used by the manufacturer, whether directly or (ii) used by the manufacturer, whether directly or indirectly, in or in relation to the manufacture of final indirectly, in or in relation to the manufacture of final products and clearance of final products from the place of products and clearance of final products from the place of removal, and includes services used in relation to setting removal, and includes services used in relation to setting up, modernization, renovation or repairs of a factory, up, modernization, renovation or repairs of a factory, premises of provider of output service or an office relating premises of provider of output service or an office relating to such factory or premises, advertisement or sales to such factory or premises, advertisement or sales promotion, market research, storage upto the place of promotion, market research, storage upto the place of removal, procurement of inputs, activities relating to removal, procurement of inputs, activities relating to business, such asbusiness, such as

accounting, auditing, financing, recruitment and accounting, auditing, financing, recruitment and quality control, coaching and training, computer quality control, coaching and training, computer networking, credit rating, share registry, and networking, credit rating, share registry, and security, inward transportation of inputs or security, inward transportation of inputs or capital goods and outward transportation upto capital goods and outward transportation upto the place of removalthe place of removal

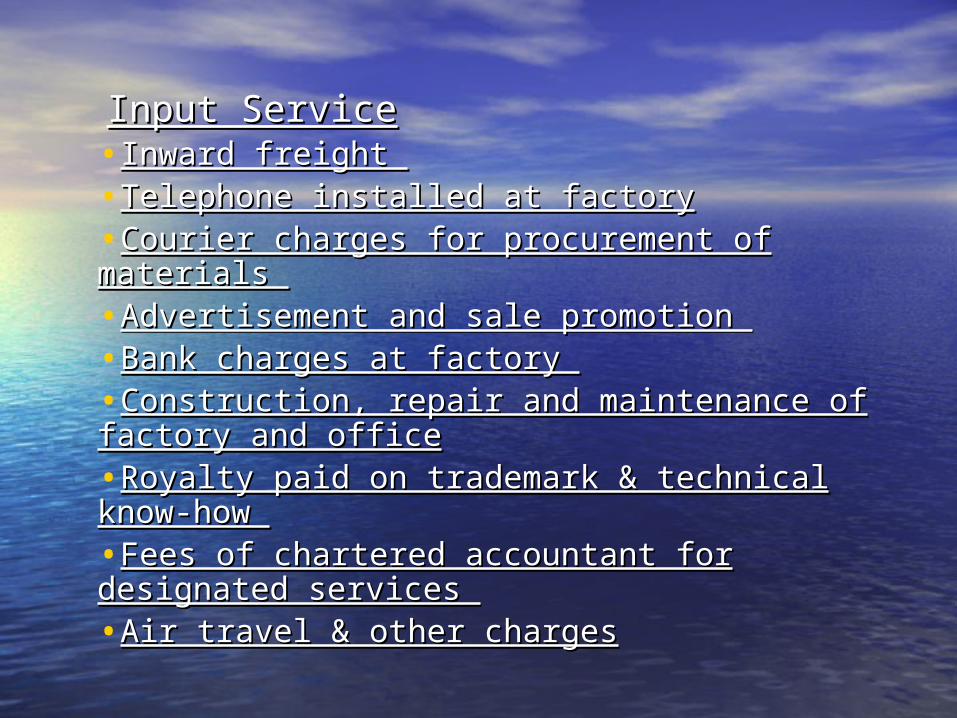

Input ServiceInput Service•Inward freight Inward freight •Telephone installed at factoryTelephone installed at factory•Courier charges for procurement of materials Courier charges for procurement of materials •Advertisement and sale promotion Advertisement and sale promotion •Bank charges at factory Bank charges at factory •Construction, repair and maintenance of Construction, repair and maintenance of factory and officefactory and office•Royalty paid on trademark & technical know-Royalty paid on trademark & technical know-how how •Fees of chartered accountant for designated Fees of chartered accountant for designated services services •Air travel & other chargesAir travel & other charges

LEVY OF SERVICE TAX ON RENTING LEVY OF SERVICE TAX ON RENTING OF IMMOVABLE PROPERTYOF IMMOVABLE PROPERTY

The person who has given the premises on lease or on some other arrangement) under this category of service would also be entitled to the benefit of Cenvat credit in respect of the inputs, capital goods and input services, in terms of the provisions of Cenvat Credit Rules,2004.

Though, the scope of availing such Cenvat credit on inputs and capital goods is very much limited, there is enormous scope for availing Cenvat Credit on various input services, such a commercial/industrial construction services, insurance services, repairs and maintenance services, architects services, interior decoration services, etc

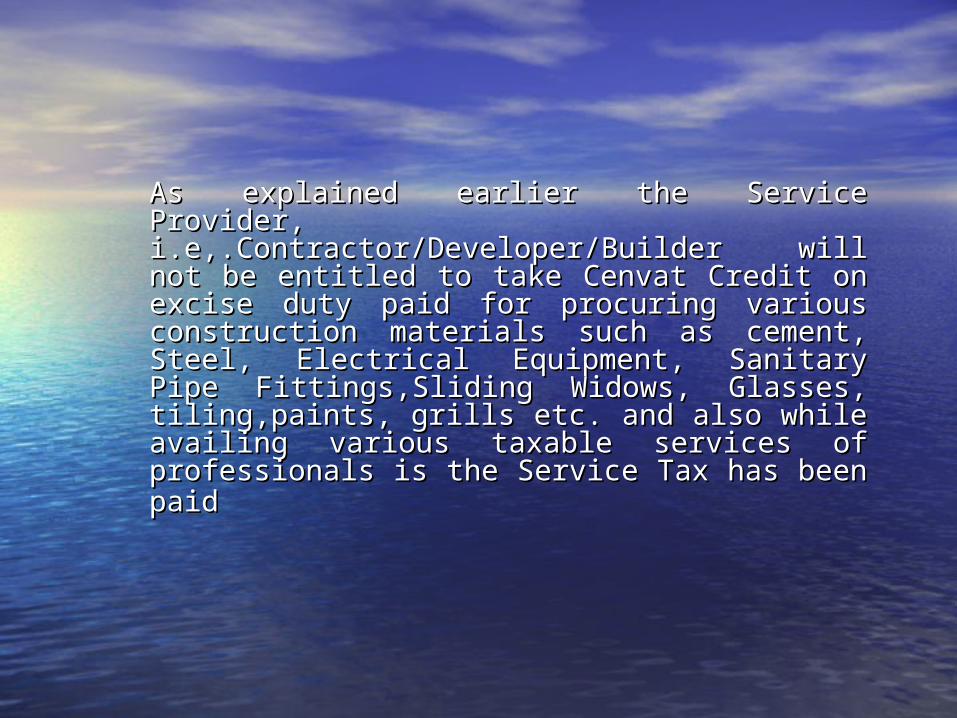

As explained earlier the Service Provider, As explained earlier the Service Provider, i.e,.Contractor/Developer/Builder will not be i.e,.Contractor/Developer/Builder will not be entitled to take Cenvat Credit on excise duty entitled to take Cenvat Credit on excise duty paid for procuring various construction paid for procuring various construction materials such as cement, Steel, Electrical materials such as cement, Steel, Electrical Equipment, Sanitary Pipe Fittings,Sliding Equipment, Sanitary Pipe Fittings,Sliding Widows, Glasses, tiling,paints, grills etc. and Widows, Glasses, tiling,paints, grills etc. and also while availing various taxable services of also while availing various taxable services of professionals is the Service Tax has been paidprofessionals is the Service Tax has been paid

either (i) after availing benefit of abatement of either (i) after availing benefit of abatement of 67% of gross value or on composition 67% of gross value or on composition scheme,i.e 2% (now after budget 4% ) since scheme,i.e 2% (now after budget 4% ) since the basic condition is that no Cenvat Credit is the basic condition is that no Cenvat Credit is permissible. However, the Principal would be permissible. However, the Principal would be well within its right to take the Cenvat Credit well within its right to take the Cenvat Credit in respect of the service tax charged by the in respect of the service tax charged by the Service provider in his running account bills Service provider in his running account bills raised from time to time.raised from time to time.

However, the Department has now issued a Circular However, the Department has now issued a Circular No.98/1/2008-ST.dated 4.1.2008(2008) S.T.R. C43 . No.98/1/2008-ST.dated 4.1.2008(2008) S.T.R. C43 . The levy of Service tax on various construction related The levy of Service tax on various construction related services (commercial/ industrial construction service, services (commercial/ industrial construction service, residential construction service,etc) is always beset with residential construction service,etc) is always beset with lot of practical complications, due to the unique nature lot of practical complications, due to the unique nature of this industry and the nuances of this new levy, of this industry and the nuances of this new levy, compounded by half baked instructions issued by the compounded by half baked instructions issued by the CBEC, in the guise of “clarifying “. The recent attempt CBEC, in the guise of “clarifying “. The recent attempt of the CBEC to “clarify” would beat all its siblings, in of the CBEC to “clarify” would beat all its siblings, in terms of its utter disregard to the legal provisions and terms of its utter disregard to the legal provisions and portrayal of lack of even elementary knowledge of the portrayal of lack of even elementary knowledge of the subject.subject.

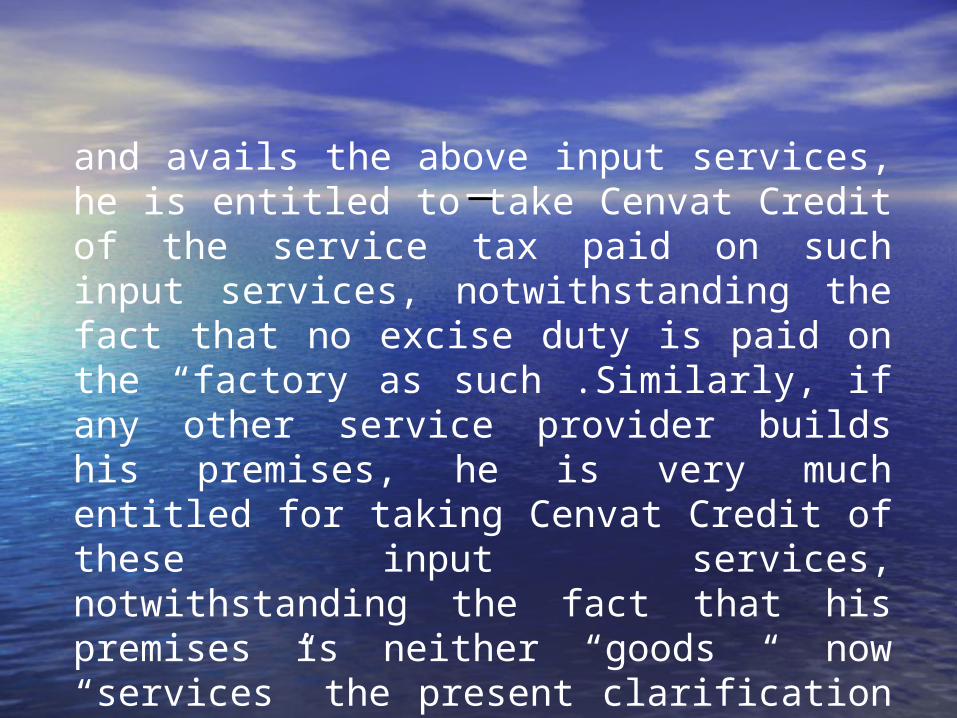

The clarification appears to be in blatant violation of the statutory provisions. The definition of the terms” input service” as per Rule 2(1) of the CCR,2004 refers to “ service used in relation to setting up, modernization, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises”In other words , if a manufacturer builds a factory (which is nothing but an immovable property),

and avails the above input services, he is entitled to take Cenvat Credit of the service tax paid on such input services, notwithstanding the fact that no excise duty is paid on the “factory as such .Similarly, if any other service provider builds his premises, he is very much entitled for taking Cenvat Credit of these input services, notwithstanding the fact that his premises is neither “goods “ now “services” the present clarification has been drafted, in total disregard to the above statutory provision.

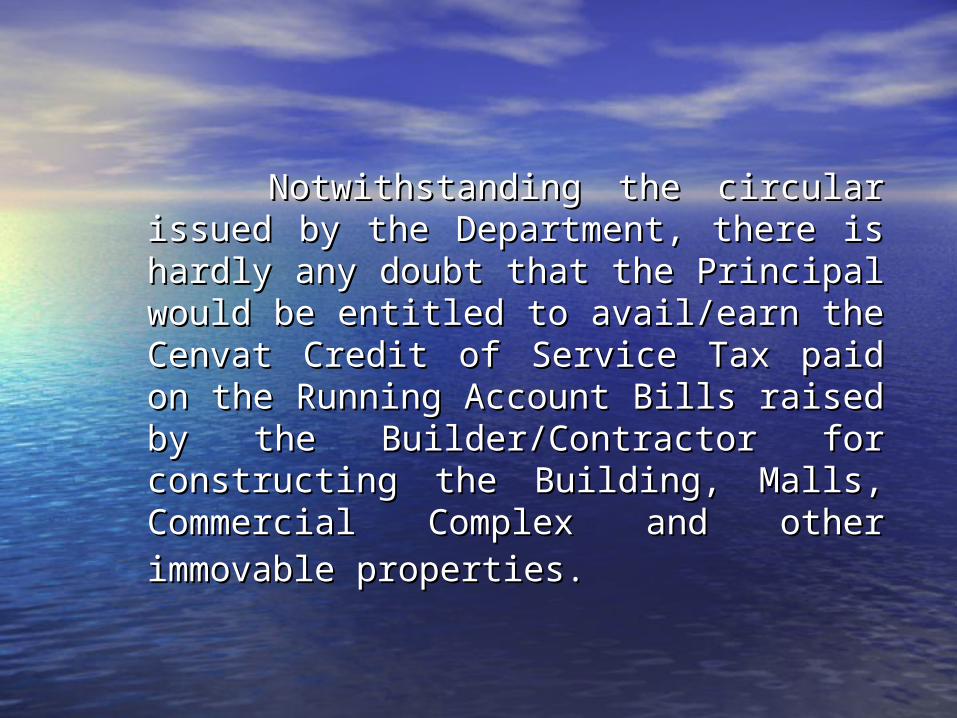

Notwithstanding the circular issued by the Notwithstanding the circular issued by the

Department, there is hardly any doubt that the Department, there is hardly any doubt that the Principal would be entitled to avail/earn the Principal would be entitled to avail/earn the Cenvat Credit of Service Tax paid on the Cenvat Credit of Service Tax paid on the Running Account Bills raised by the Running Account Bills raised by the Builder/Contractor for constructing the Building, Builder/Contractor for constructing the Building, Malls, Commercial Complex and other Malls, Commercial Complex and other

immovable properties.immovable properties.

The Service tax so paid by the Principal on the The Service tax so paid by the Principal on the aforesaid Running Account bills can be utilized aforesaid Running Account bills can be utilized for payment of Service Tax on taxable service of for payment of Service Tax on taxable service of Renting of Immovable Property,i.e, Malls, Renting of Immovable Property,i.e, Malls, shopping Complex, office Complex, commercial shopping Complex, office Complex, commercial Complex and other immoveable property put to Complex and other immoveable property put to commercial use.commercial use.

Scope of Commercial or Industrial Scope of Commercial or Industrial Construction ServiceConstruction Service

Post construction completion and finishing Post construction completion and finishing services such as glazing, plastering, painting , services such as glazing, plastering, painting , floor and wall tiling ,wall covering and wall floor and wall tiling ,wall covering and wall papering, wood and metal joinery and carpentry, papering, wood and metal joinery and carpentry, especially if undertaken as an isolated or stand especially if undertaken as an isolated or stand alone contract, are also specifically included. alone contract, are also specifically included. Thus post construction completion and finishing Thus post construction completion and finishing services are specifically included in the services are specifically included in the definition of commercial or industrial definition of commercial or industrial construction services.construction services.

It the contract for construction of commercial It the contract for construction of commercial complex is a single contract and the complex is a single contract and the construction of road is not recognized as a construction of road is not recognized as a separate activity as per the contract, then the separate activity as per the contract, then the service tax would be leviable on the gross service tax would be leviable on the gross amount charged for construction including the amount charged for construction including the value of construction of roads.value of construction of roads.

THANK YOUTHANK YOU