leveraging your broker/agent & insurance carrier to reduce insurance costs presented by mary kay...

TRANSCRIPT

Leveraging Your Broker/Agent & Insurance

Carrier to Reduce Insurance Costs

Presented byMary Kay Depperman, CSP

Objectives Answer Your Specific Questions Choosing an Insurance Broker/Agent Getting the Best from Insurance Carriers Components of a World Class Safety

Culture Benefits of being “Best in Class” WC 101-The Best Opportunity for Cost

Containment Through Timely Reporting and Alternative Duty Within 3 Days of Loss

Considerations When Choosing Insurance Broker Location-Local, National, International Experience in your Business Referrals Specialties-P & C, Surety, Benefits, Aviation,

International, Financial Services, Executive Protection

Program Choice-Risk vs. Guarantee Cost Loss Control Staff-OSHA to Best Practices Claims Advocates-Reserves to proper treatment Legal Staff-Contract Advice Input to your CFO or Risk Management

Working With Your Insurance Carrier

Be Prepared for the Loss Control Service Visit-Cattle call vs. Single Carrier

Claims Service Loss Control Services Use their On Line Services Communication Ask for Targeted Assistance for Both

Claims and Loss Control Have Plan to Reduce Losses

15 Specific Safety Practices For Best Safety

Culture1. Training-Safety meetings & 5 minute

Safety Talks2. Safety Rules and Enforcement3. Employee Safety Observations4. Injury and Incident Investigation5. Workplace Audits/Inspections to Identify &

Correct Unsafe Acts & Conditions6. Modified Duty and Return to Work

Program7. Continual Ergonomic Improvements8. Recognition & Communication

15 Specific Safety PracticesContinued

9. Wellness Program & Stretching Program10. Measuring and Benchmarking Safety

performance11. Hiring for Safety Attitude & Drug Testing12. Coaching and Motivating-Feedback13. Timeliness Response14. Management Lead Safety Organization15. Safety Department as a Resource

HighInsuranceCosts

ExcessiveFrequencySeverity

PoorEmployeeRelations

MuchLitigation

StatutoryIgnorance

Line/StaffConflict

BehaviorsEvidenceCommitteesQuick Fix

Quiet Transparent Integrated Equal

WORLD CLASS

SWAMP

Traditional

Progressive

Rate Your Organizations’ Safety Culture

Safety Without Any Management Process

Are you somewhere in between?

Be Honest!5%

21%

46%

28%

0%

Benefits of Best Safety Culture Achievement

Reduced Insurance Costs Healthy & Productive Employees Good Management & Employee

Relationship Higher Worker Morale Less Worries From OSHA Visits Higher Quality & Production

Leveraging To Reduce Costs Part 1

Choose a Good Insurance Broker/Agent

Work Toward Best Safety Culture Use Loss Control & Claims Consultants

Insurance Broker Insurance Carrier & On Line Services Outside Safety Consultants OSHA www.osha.gov College Interns

Leveraging To Reduce Costs

Part 2-WC 101 Know Your State’s Workers

Compensation Plan Report Claims Promptly to your

Insurance Carrier-Hours vs. Days Identify Alternative Job Duties in Advance Implement Alternative Duty within 3

Days of Injury Work with an Occupational Clinic that

Knows Your Operations Use Correct Job Classification Codes

Questions???

What is Workers Compensation?

No Fault Pays benefits for accidental injuries

and illnesses related to work Benefits include medical treatment,

rehabilitation and income replacement Income replacement is 2/3 of weekly

wage Three day waiting period

Cost Of WC Insurance

Premium is based on loss history Rate is customized to each

employer Experience modifier compares each

employer to their peers “Mod” calculated from a three year

rolling loss average

Three Year Rolling Average

2009 Mod = 2007, 2006, 2005 2010 Mod = 2008, 2007, 2006 2011 Mod = 2009, 2008, 2007 A good year stays with you for

three years and a bad year stays with you for three years.

Cost Of WC Insurance

Class 8810 Clerical = $0.28 Class 8742 Sales = $0.74 Class 3227 AL Ware Mfg. = $4.56 Class 4452 Plastic-Fab. Products =

$3.71 Class 7380 Drivers = $5.34 Class 9501 Painting = $4.58 Rates are per $100 of payroll

Cost of WC InsuranceHow Ex. Mod Affects Costs

Base Rate $4.56 Mod average 1.0 Final Rate $4.56

Base Rate $4.56 Mod Min 0.51 Final Rate $2.33

Base Rate $4.56 Mod Current 1.32 Final Rate $6.02

Base Rate $4.56 Mod Control 0.82 Final Rate $3.74

The Costs

RATE “ X” PAYROLL “X” MOD. = $100

TOTAL PREMIUM

RATE “ X” PAYROLL “X” MOD. = $100

TOTAL PREMIUM

Financial Impact

1

1.32

0.51

0.81

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Average Actual Lowest Controllable

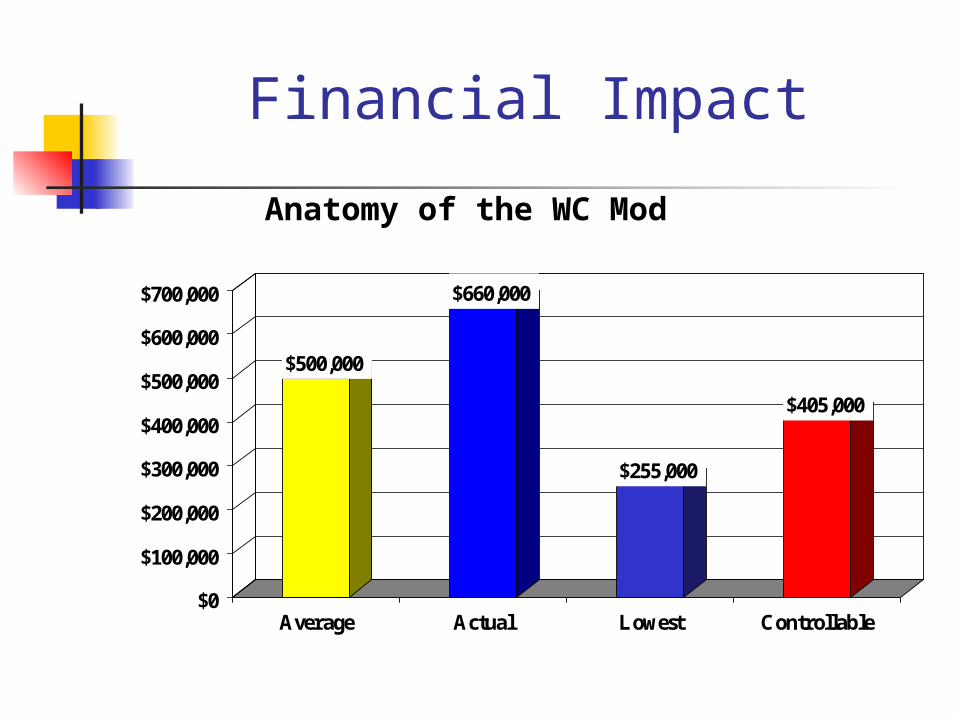

Anatomy of the WC Mod

Financial Impact

$500,000

$660,000

$255,000

$405,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

Average Actual Lowest Controllable

Anatomy of the WC Mod

Sales Required $405,000 of your premium is

under your control. At a 5% margin, additional sales

required = $8,100,000 How much additional product to

you have to produce and sell to generate the revenue to pay for premium above the minimum mod?

Hidden Cost of Accidents

Indirect Costs - time lost by others - hiring/training of replacement - lost efficiency - overtime premium - possible lost orders - tool/equipment damage - lost equipment utilization

Direct Costs

- medical

- insurance premium

- compensation payments

Prompt Reporting

Report within 24 hours Insurer will contact within 24 hrs.

EmployeeEmployerDoctor

Cost containment controls kick inMedical cost containmentReturn to work efforts

Accident Investigation

Express care to injured person Gather information Unsafe acts / Unsafe conditions Who, What, Why, When, Where,

How come Get to root cause(s) of loss

Medical Provider Form

Communicates with physician alternative work is available

Give contacts at Employer and Carrier

Asks physician to list any physical limitations

Sets tone for how claim will be handled

What is “Alternative Duty”?

Light duty work Rotated job duties Temporary in nature What jobs are available in your

operation?

What Changed July 1, 1998?

70% of the dollars paid by the WC carrier on medical only claims is not counted towards experience mod.

Med only means that no wage loss benefits are paid to employee

That means no wage loss more than three days or no wage loss of any kind 7 days after injury

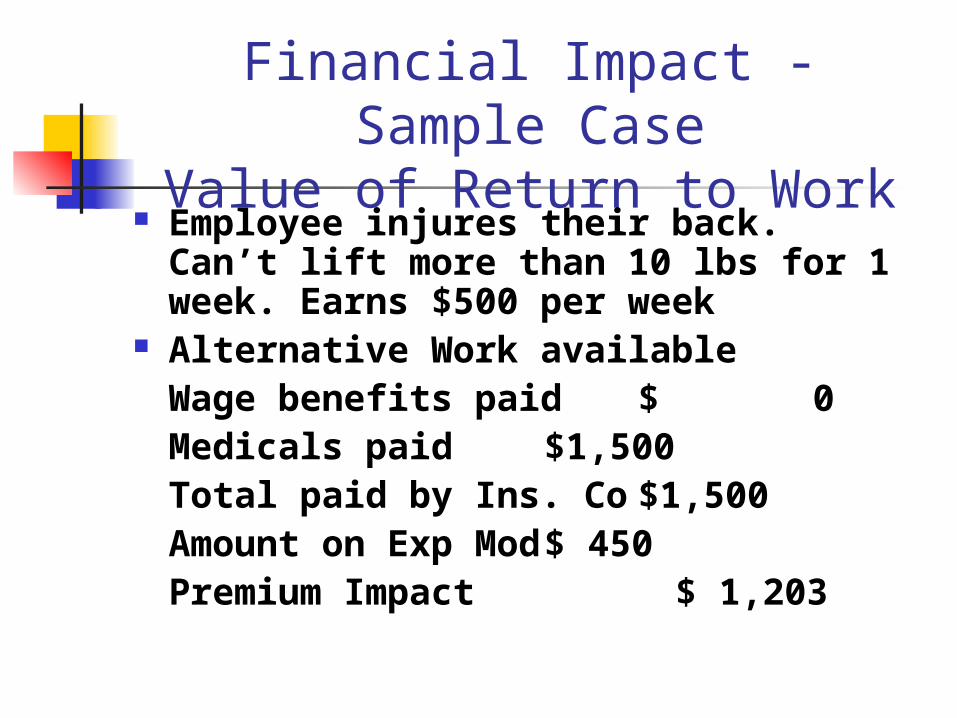

Financial Impact - Sample Case

Value of Return to Work Employee injures their back. Can’t lift

more than 10 lbs for 1 week. Earns $500 per week

Alternative Work availableWage benefits paid $ 0Medicals paid $1,500Total paid by Ins. Co $1,500Amount on Exp Mod $ 450Premium Impact $ 1,203

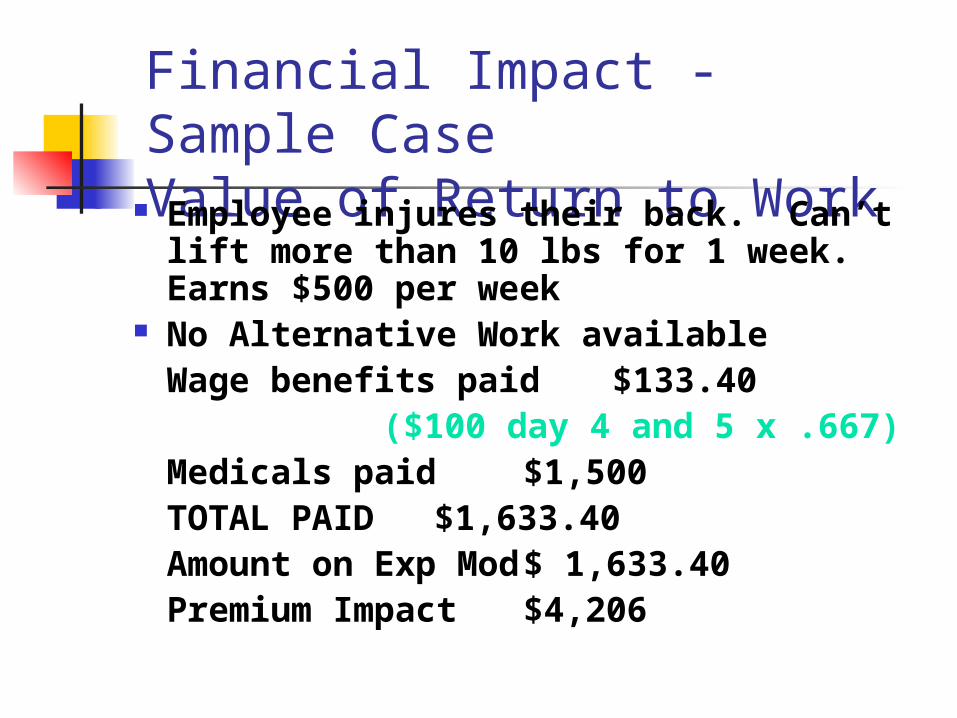

Financial Impact - Sample CaseValue of Return to Work Employee injures their back. Can’t lift more than 10 lbs for 1 week. Earns $500 per week

No Alternative Work availableWage benefits paid $133.40

($100 day 4 and 5 x .667)Medicals paid $1,500TOTAL PAID $1,633.40Amount on Exp Mod $

1,633.40Premium Impact $4,206

What does this mean? Lost time injuries

have more impact on mod.

Lost time injuries, as illustrated in the previous example, cost 3 to 4 times more in premium than medical only injuries.

Wrap up

Med only means “No Wage Loss”

Pay full wage during light duty work

Find alternative work Communicate - Be in control Reduce Insurance Costs