lending policy 2015

TRANSCRIPT

1

Karnataka State Financial Corporation

LENDING POLICY 2015

2

Ref No KSFC/HO/RMD/CMD/C-4889/2014-15 Dated : 29-01-2015

CIRCULAR No: 991

Sub: Lending Policy 2015

A Note on Lending Policy 2015 was placed before the Board inits meeting held on 8th January 2015. I am happy to inform that theBoard has apporved the Lending Policy 2015. While approving the lendingpolicy, the Board also took note of the changes recommended for theexisting lending policy. The Board observed that the covention centreactivity and the industrial estate and Software Technology Parks, whichwere hither to classified under CRE sector, may be classified underservices & other sector as provided in the RBI guidelines. This lendingpolicy will come into effect immediately. This lending policy will be invogue till new lending policy is introduced.

The lending policy 2015 as approved by the Board is enclosed tothis Circular. Any points of doubts on these guidelines shall be referred toExecutive Director-I, Head Office for clarification.

(Vanditha Sharma)Chairperson & Managing Director

To :All the Branch ManagersDGM’s of Super ‘A’ Grade BO’sAll Principal Officers / Section Heads in HOAll General Managers

Executive DirectorsLibrary

3

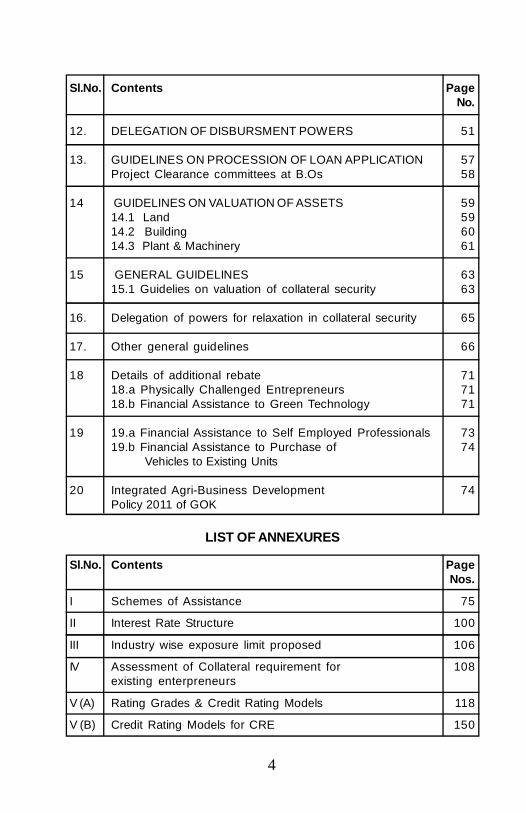

Sl.No. Contents PageNos.

1 PREAMBLE 51. Objectives of Lending policy 8

2 ELIGIBLE ACTIVITIES FOR FINANCIAL ASSISTANCE 92.1 As listed out in the SFCs Act 102.2 Activities permitted by SIDBI 11

3 DIFFERENT SCHEMES OPERATED IN THECORPORATION 11

4 POLICY ON LINES OF ACTIVITY 124.1 Thrust Sector 144.2 Normal Sector 194.3 Restricted Sector 354.4 Prohibited Sector 39

5 MSMEs DEFINITION 40

6 POLICY ON EXPOSURE LIMITS 41a. Policy on minimum loan size 41b. Policy on upper limit on the loan amount 41 & limit of accommodationc. Group-wise exposure 42

7 POLICY ON SECTOR WISE EXPOSURE 42

8 POLICY ON REPAYMENT PERIOD 43

9 GUIDELINES ON PROMOTERS EQUITY 45AND PROFITABILITY9.1 Debt Equity ratio (DER) 459.2 Debt Service Coverage Ratio (DSCR) 459.3 Maximum Assistance 459.4 Promoter’s contribution 469.5 Interest rate structure 46

10 POLICY ON FORECLOSURES / PRE-PAYMENTS 4610.1 Policy on Time Standard in Processing 47 of Loan Applicatins

11 DELEGATION OF LOAN SANCTIONING POWERS 47

4

Sl.No. Contents PageNo.

12. DELEGATION OF DISBURSMENT POWERS 51

13. GUIDELINES ON PROCESSION OF LOAN APPLICATION 57Project Clearance committees at B.Os 58

14 GUIDELINES ON VALUATION OF ASSETS 5914.1 Land 5914.2 Building 6014.3 Plant & Machinery 61

15 GENERAL GUIDELINES 6315.1 Guidelies on valuation of collateral security 63

16. Delegation of powers for relaxation in collateral security 65

17. Other general guidelines 66

18 Details of additional rebate 7118.a Physically Challenged Entrepreneurs 7118.b Financial Assistance to Green Technology 71

19 19.a Financial Assistance to Self Employed Professionals 7319.b Financial Assistance to Purchase of 74 Vehicles to Existing Units

20 Integrated Agri-Business Development 74Policy 2011 of GOK

Sl.No. Contents PageNos.

I Schemes of Assistance 75

II Interest Rate Structure 100

III Industry wise exposure limit proposed 106

IV Assessment of Collateral requirement for 108existing enterpreneurs

V (A) Rating Grades & Credit Rating Models 118

V (B) Credit Rating Models for CRE 150

LIST OF ANNEXURES

5

Lending policy 2015

PREAMBLE:

The fast changing economic scenario calls for a vibrant lendingpolicy to respond to the needs of MSMEs and service sector inthe State. Besides, the lending institutions have to evaluate therisk perceptions periodically in the wake of the changes and designthe lending norms judiciously to maintain quality loan portfolio.

Recognizing this need, the Karnataka State Financial Corporationhas been formulating a comprehensive lending policy documentsince 2001-02 and revising the same periodically. This policydocument helps credit dispensing functions to create healthy loanportfolio. The Lending Policy document provides preciseguidelines to the pertinent areas of project guidance, acceptance,appraisals, credit rating and loan sanctioning.

The overall growth of GDP for 2013-14 is placed at 4.9 percentas compared 4.5 percent for 2012-13.The agriculture, industryand service sectors have registered growth rates of 4.6 percent,0.7 percent and 6.9 percent respectively. The Indian Industryended the fiscal year 2013-14 on a negative note. Index ofIndustrial Production (IIP), the official measure of Industrial activityin India, registered a growth of (-) 0.1percent vis-à-vis 1.1 percentduring 2012-13. Manufacturing sector registering a 0.9 percentfall in its output during 2013-14 ended at (-) 0.2 percent growth.The mining sector had growth of (-) 1.9 percent as compared to(-) 2.2 percent during previous year. This was because of 1.6percent fall in output of crude oil. Natural gas production too fellby 9.3 percent. The only main sub-segment of the industry thatreported a growth during 2013-14 is electricity at 6 percent. Thegrowth was driven by 12.4 percent growth in nuclear powergeneration followed by thermal power generation and hydro powergeneration by 5.2 percent and 4.5 percent, respectively.

The Service Sector grew at 6.9 percent during 2013-14 comparedto seven percent during the previous year. However, the real estate

6

and business services, financing and insurance growth was 11.2percent compared to previous year’s 10.9 percent.

Vision 2020 for Karnataka seeks to propel a holistic growth bypromoting equitable development of sectors and districts byproviding employment to all sections of people and regions of theState. Development of industrial sector is of vital importance toensure the overall growth of the economy.

Karnataka has been spearheading the growth of Indian Industry,particularly in terms of high-technology industries in the areas ofelectrical and electronics, information and communicationtechnology, biotechnology and more recently nano technology.

The Karnataka’s Gross State Domestic Product (GSDP) reachedRs.3,11,628 crore in 2013-14 (at constant price 2004-05) fromRs.3,03,444 crore in 2012-13.

Despite the drought conditions in the State, the GSDP growthrate of agriculture and allied activities was registered at 3.6%during 2013-14 as against the negative growth of 4.9% in 2012-13. The Industry sector grew at 1.2% during 2013-14 which islower than growth rate of 4.4.% recorded during the previous year.The service sector growth at 7.2% during 2013-14 is lower thanthe growth rate of 8.4% during the previous year.

Total value of exports of Karnataka during 2013-14 wasRs.2,90,418 crore whereas all India export is Rs. 20,70,108 crore.The share of Karnataka’s export in all India export is 14.03%whereas share of software exports is 40%.

MSMEs form an important and growing segment of Karnataka’sindustrial sector. During 2013-14, 25,966 units with a proposedinvestment of Rs.2,850.56 crores and employment potential of1,67,347 persons have been registered .

During the year, the State Level Single Window ClearanceCommittee approved 209 projects with a proposed investment

7

of Rs 3,548.21 crores having employment potential to 43,759persons. Projects with an investment of Rs.50 crores and aboveare cleared by the State High Level Clearance Committee(SHLCC). The number of projects cleared by SHLCC during 2013-14 is 46 with a proposed investment of Rs.38,653.38 crore andcreating employment to 1,27,692 persons.

Karnataka is the first State in the country to launch State TextilePolicy. The “Nuthana Javali Neeethi –2013-18” is implementedafter the completion of Suvarna Vastra Neethi – 2008-13. Thenew policy is proposed to attract investments in textile sector tothe tune of Rs.10,000 crore and provide employment to five lakhpersons.

Department of Horticulture had formulated a new scheme forrejuvenation and strengthening of hi-tech floriculture in 2013-14with subsidy for replanting of old plants(variety) with new varietiesgrown in green house, subsidy for replacement of polythene sheetof green house and subsidy for electricity used for cold storage ofhi-tech floriculture.

The Government of Karnataka has accorded administrativeapproval for establishing Rice Technology Park with the State-of-the-Art Technology for processing, grading, packaging, branding,marketing and export of rice in Karatagi of Gangavathi Taluk ofKoppal District.

The new policies released by Government of Karnataka likeKarnataka i4 Policy: IT, ITES, Innovation, Incentives Policy isenvisaged to reposition Bangalore and Karnataka as the preferredGlobal Investment Destination for IT/ITES/BPO Sectors.Bangalore is today the second largest IT cluster on the planetwith about 9 lakh direct and about 27 lakh indirect employmentsecond only to the Silicon valley.

The State Textile Policy is proposed to attract investments in Textilesector to the tune of Rs.10,000 crore and provide employment tofive lakhs persons.

8

The Aerospace Policy 2012-2022, highlights the potential ofKarnataka to emerge as an Aerospace Hub for Asia in the next 5years and as one of the top global Aerospace and MRODestinations by 2022.The Aerospace Policy has a mission toattract investments of Rs.60,000 crores over next 10 years,providing additional employment to one lakh (direct & Indirect)persons. One of the strategies of the policy is to assist indeveloping MSME and large scale industries equally in AerospaceSector. Policy also proposes to establish “Aerospace parks” atpotential locations like Mysore, Hubli, Mangalore and Belgaum.These parks will have a comprehensive infrastructure facilitywhich enables the units to operate on “Plug and Play” concept.

The New Industrial Policy 2014-19, New Tourism Policy 2014-19, Solar Policy 2014-2021 are set to boost the industrial vigor inthe State.

Karnataka has robust and vibrant environment for establishmentof new industries and for expansion/ modernization / diversificationof existing units in manufacturing sector, service sector and agri-based sectors. Karnataka State Financial Corporation is invitingthe entrepreneurs to utilize the facilities available in the State byavailing financial assistance from KSFC at the competitive interestrate in a customer friendly environment.

The Lending Policy 2015 attempts to throw light on various areasof operation of KSFC, eligible activities, different schemes,delegation powers for loan sanction and disbursement, interestrate and rebates thereon and other general guidelines.

1. Objectives of the Lending Policy 2015:

The broad objectives of the lending policy of theCorporation are outlined hereunder.

a. To establish a comprehensive credit strategy to fulfil thecorporate mandate as per the SFC Act, 1951, amended from time

9

to time, and undertake all such activities directly or indirectly, thatare beneficial to the MSME Sector.

b. To ensure efficient delivery of credit with focus on asset growthand quality coupled with growth in income.

c. To encourage various functionaries to innovate and evolvecompetitive products based on market requirements.

d. To provide indicative guidelines to various policy & functionallevel officers of the Corporation for measures to be taken forimproving the credit delivery and customers satisfaction.

e. To encourage expansion and diversification of credit portfolio,especially through coverage of thrust areas / industries / sectors/ newer areas of business, loan syndication etc. and profitabledeployment of the Corporation’s funds.

f. To strengthen the risk management systems and ensure closemonitoring of the credit portfolio so as to prevent fresh slippagesinto NPAs.

g. To explore new channels of credit delivery for the benefit ofMSMEs.

2. ELIGIBLE ACTIVITIES FOR FINANCIAL ASSISTANCE:

The SFCs Act prescribes broadly the types of activities,which are eligible for financial assistance from the Corporation.The Act also provides for SIDBI to include newer areas of activitiesfor financial assistance from time to time. This apart, theCorporation has also evolved its own schemes under broadguidelines of SFCs Act depending upon market potential. Theactivities which are eligible for financial assistance from theCorporation are grouped into following two broad categories:

(a) Activities as listed out in the SFCs Act;(b) Activities specifically permitted by SIDBI;

10

2.1. As listed out in the SFCs Act:-The State Financial Corporation’s (Amendment) Act, 2000,

provides the list of activities which can be covered under the listof industrial concern engaged or to be engaged in :

(i) Manufacture, preservation or processing of goods;(ii) Mining or development of mines;(iii) Hotel industry;(iv) Transport of passengers or goods by road or by water

or by air (or by rope way or by lift);(v) Generation or distribution of electricity or any other form

of power;(vi) Maintenance, repair, testing or servicing of machinery of

any description or vehicles or vessels or motorboats or trailers or tractors;

(vii) Assembling, repairing or packing any article with the aidof machinery or Power:

(viii) Setting up or development of an industrial area orindustrial estate;

(ix) Fishing or providing shore facilities for fishing ormaintenance thereof:

(x) Providing weigh bridge facilities;(xi) Providing engineering, technical, financial management,

marketing of Other services or facilities for industry;(xii) Providing medical, health or other allied services;(xiii) Providing software or hardware services relating to

information technology, telecommunications orelectronics including satellite linkage and audio orvisual cable communication;

(xiv) Setting up or development of tourism related facilitiesincluding amusement parks, convention centres,restaurants, travel and transport (including those atairports), tourist service agencies and guidance andcounselling services to the tourists;

(xv) Construction;(xvi) Development, construction and maintenance of roads;(xvii) Providing commercial complex facilities and community

centres including conference halls;

11

(xviii) Floriculture;(xix) Tissue culture, fish culture, poultry farming, breeding and

hatcheries;(xx) Service industry, such as altering, ornamenting,

polishing, finishing, oiling, washing, cleaning orotherwise treating or adapting any article orsubstance with a view to its use, sale transport, deliveryor disposal;

(xxi) Research and development of any concept technology,design, process or product whether in relation to anyof the matter aforesaid, including any a c t i v i t i e sapproved by the Small Industries Bank; or

(xxii) Such other activity as may be approved by the SIDBI;

2.2 Activities permitted by SIDBI:i) Construction / buying of ready-built showrooms and sales

out-lets (only fixed assets are eligible for financing, itemskept for sale are not eligible for financing);

ii) Construction / buying of ready-built area for establishingdepartmental stores and shopping malls (only fixed assetsare eligible for financing, items kept for sale are not eligiblefor financing);

iii) Setting up of Medical Stores (only fixed assets are eligiblefor financing, items kept for sale are not eligible forfinancing);

iv) Setting up of vocational training centres for impartingtechnical knowledge to entrepreneurs for setting up andrunning units efficiently and to produce quality goods;

v) Setting up entertainment industry including production offilms.

vi) Such other activity as may be approved by the SIDBI.

3. DIFFERENT SCHEMES OPERATED IN THECORPORATION:

Based on the activities permitted under the SFCs Act theCorporation has formulated various schemes for extending

12

financial assistance.

1. Acquisition of private vehicles;2. Corporate loans;3. Construction activity.4. Acquisition of Existing Assets/ Enterprises.5. Privileged Entrepreneurs Scheme.

6. Assistance to Professional Educational Institutions forInfrastructure shall be covered under the constructionactivity scheme

7. Interest subsidy scheme of Government of Karnataka forSC/ST entrepreneurs.

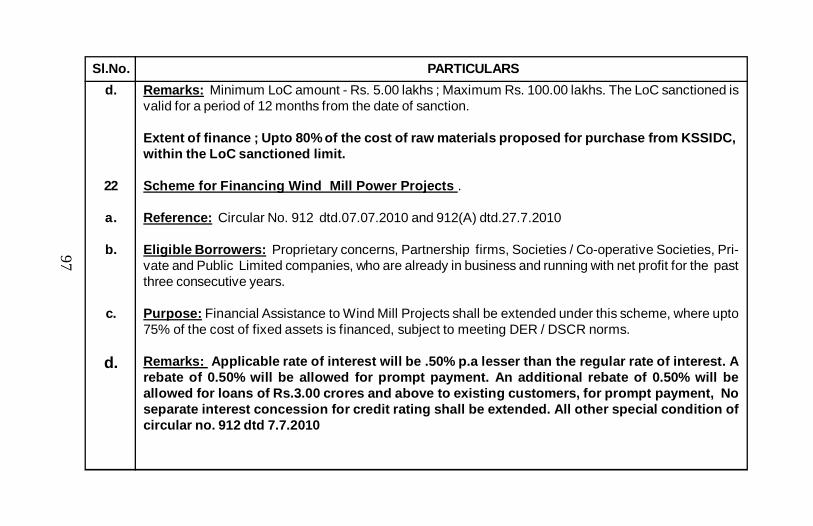

8. Scheme for Micro Finance activity.9. Line of Credit (LoC) for Raw-material Purchase by

MSMEs from KSSIDC.10. Scheme for financing wind mill power projects.11. Soft Seed Capital Assistance of Govt. Of Karnataka for

SC/ST entrepreneurs.12. Restructured TUF scheme of Govt. Of India13. CLCSS Scheme of Govt. Of India

Brief particulars of various schemes is given at Annexure-I. For more details / procedure in each scheme, correspondingcirculars may be referred.

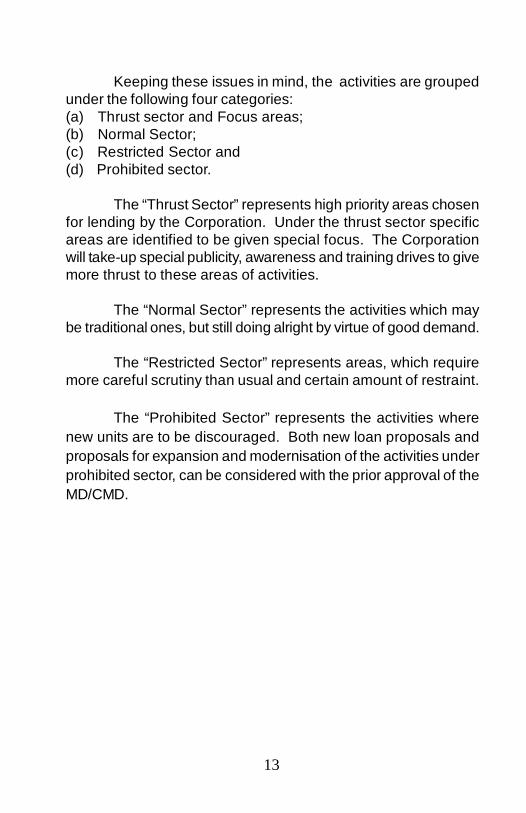

4. POLICY ON LINES OF ACTIVITY:It is a known fact that saturation, obsolescence, un-viability,

economy of scales, geographical factors, environmental issues,infrastructure, global economy/markets etc., do have a bearingon lines of industrial / business activity to be encouraged forfinancing. Some of these parameters keep changing from timeto time depending upon the external environment and environmentwithin the industry. It is therefore essential to make a periodicalreview of the performance of these activities in order to determinethe policy on supporting any activity in a particular period of timeand at a particular geographical location.

13

Keeping these issues in mind, the activities are groupedunder the following four categories:(a) Thrust sector and Focus areas;(b) Normal Sector;(c) Restricted Sector and(d) Prohibited sector.

The “Thrust Sector” represents high priority areas chosenfor lending by the Corporation. Under the thrust sector specificareas are identified to be given special focus. The Corporationwill take-up special publicity, awareness and training drives to givemore thrust to these areas of activities.

The “Normal Sector” represents the activities which maybe traditional ones, but still doing alright by virtue of good demand.

The “Restricted Sector” represents areas, which requiremore careful scrutiny than usual and certain amount of restraint.

The “Prohibited Sector” represents the activities wherenew units are to be discouraged. Both new loan proposals andproposals for expansion and modernisation of the activities underprohibited sector, can be considered with the prior approval of theMD/CMD.

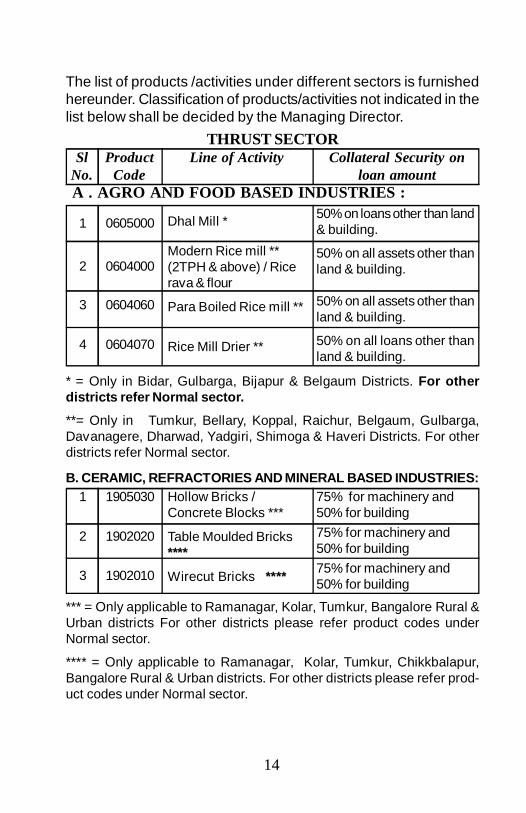

14

THRUST SECTORSl

No.Product

CodeLine of Activity Collateral Security on

loan amountA . AGRO AND FOOD BASED INDUSTRIES :

1

2

3

4

0605000

0604000

0604060

0604070

Dhal Mill *

Modern Rice mill **(2TPH & above) / Ricerava & flour

Para Boiled Rice mill **

Rice Mill Drier **

50% on loans other than land& building.

50% on all assets other thanland & building.

50% on all assets other thanland & building.

50% on all loans other thanland & building.

The list of products /activities under different sectors is furnishedhereunder. Classification of products/activities not indicated in thelist below shall be decided by the Managing Director.

B. CERAMIC, REFRACTORIES AND MINERAL BASED INDUSTRIES:1

2

3

1905030

1902020

1902010

Hollow Bricks /Concrete Blocks ***

Table Moulded Bricks****

Wirecut Bricks ****

75% for machinery and50% for building75% for machinery and50% for building75% for machinery and50% for building

*** = Only applicable to Ramanagar, Kolar, Tumkur, Bangalore Rural &Urban districts For other districts please refer product codes underNormal sector.

**** = Only applicable to Ramanagar, Kolar, Tumkur, Chikkbalapur,Bangalore Rural & Urban districts. For other districts please refer prod-uct codes under Normal sector.

* = Only in Bidar, Gulbarga, Bijapur & Belgaum Districts. For otherdistricts refer Normal sector.

**= Only in Tumkur, Bellary, Koppal, Raichur, Belgaum, Gulbarga,Davanagere, Dharwad, Yadgiri, Shimoga & Haveri Districts. For otherdistricts refer Normal sector.

15

E. DRUGS AND PHARMACEUTICALS :1 1713010 Pharmaceutical formula-

tion of Allopathic Drugs75% on all assets otherthan land & building.

F. ELECTRICAL AND ELECTRONICS INDUSTRIES :1

2

3

4

5

6

7

8

9

3402230

3500000

3402000

3402180

3402190

3402240

2301211

2504000

2504010

AutomotiveElectronics

DG set / MobileGenerator

ElectronicComponents

Electronic MeasuringInstruments

Electronic WeighingSystem

Manufacturing of ElectroMedical Equipment

Mfg. of UPS

Non conventionalenergy – Windmill

Non conventionalenergy – Bio Waste

100% on all assets otherthan land & building.

30% for units & 100% formobile generator.

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building.

30% on all assets other thanland & building.

50% on all assets other thanland & building

50% on all assets other thanland & building.

50% on all assets other thanland & building.

75% on all assets otherthan land & building.

100% in the form of fixedassets

C. CHEMICAL AND ALLIED INDUSTRIES :1

2

1702000

1703000

Fertilizer Granulation /Mixing

Paints, varnishes,lacquers

100% on all assets otherthan land & building.

50% on all assets otherthan land and building

D. CONSTRUCTION ACTIVITY :1

2

2811000

2812000

Godown / warehouse –other than agri basedproducts

Infrastructure Projects

16

F. ELECTRICAL AND ELECTRONICS INDUSTRIES :10

11

12

2504020

3402550

2302000

Non conventionalenergy – Solar

PCBAssembly

Power generation plant-Hydel

50% on all assets other thanland & building.

100% on all loans other thanland & building

50% on all assets other thanland & building

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

G. ENGINEERING, MECHANICAL AND ALLIED PRODUCTS1

2

3

4

5

6

7

8

9

10

2219000

2406000

2406020

3603022

2203220

2107020

2203000

2105000

2406190

2203170

Aerospace RelatedActivity

Automobile Ancillaryunits

Authorised Automobileservicing and calibration/ wheel balancing

Other automobileservicing and calibration/ wheel balancing

CAD/CAM/R & DFacility centers

CNC Centers

Diamond and Carbidetipped tools and dies

Machine Tools

Metal Fasteners – nails,nut, bolts etc.

Mfg. of AutomobileComponents

Precision MachineComponents

50% on all assets otherthan land & building

30% on all assets otherthan land & building

30% on all assets otherthan land & building

50% on all assets otherthan land & building

100% on intangible assetsand 50% on equipment /machinery.

30% on all assets otherthan land & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

30% on all assets otherthan land & building

17

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

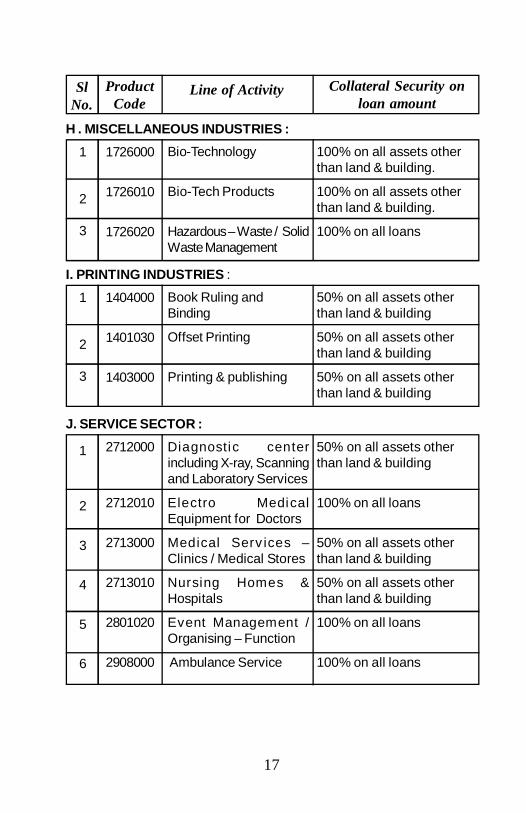

H . MISCELLANEOUS INDUSTRIES :1

2

3

1726000

1726010

1726020

Bio-Technology

Bio-Tech Products

Hazardous – Waste / SolidWaste Management

100% on all assets otherthan land & building.

100% on all assets otherthan land & building.

100% on all loans

I. PRINTING INDUSTRIES :

1

2

3

1404000

1401030

1403000

Book Ruling andBinding

Offset Printing

Printing & publishing

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

J. SERVICE SECTOR :

1

2

3

4

5

6

2712000

2712010

2713000

2713010

2801020

2908000

Diagnostic centerincluding X-ray, Scanningand Laboratory Services

Electro MedicalEquipment for Doctors

Medical Serv ices –Clinics / Medical Stores

Nursing Homes &Hospitals

Event Management /Organising – Function

Ambulance Service

50% on all assets otherthan land & building

100% on all loans

50% on all assets otherthan land & building

50% on all assets otherthan land & building

100% on all loans

100% on all loans

18

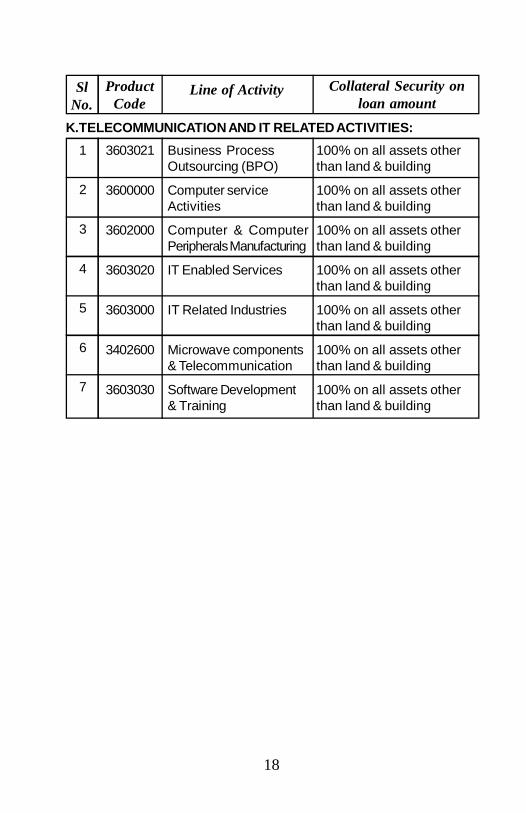

K.TELECOMMUNICATION AND IT RELATED ACTIVITIES:1

2

3

4

5

6

7

3603021

3600000

3602000

3603020

3603000

3402600

3603030

Business ProcessOutsourcing (BPO)

Computer serviceActivities

Computer & ComputerPeripherals Manufacturing

IT Enabled Services

IT Related Industries

Microwave components& Telecommunication

Software Development& Training

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

19

4.2 NORMAL SECTORA . AGRO AND FOOD BASED INDUSTRIES :

1

2

3

4

5

6

0617000

0608000

608010

0610020

0613120

0613120

Animal and PoultryFeeds

Bakery products

Biscuit / Confectionery – Tieup with Reputed Brand

Brown Sugar (Jaggerypowder)

Coffee Curing *

Coffee Roasting &Grinding

100% on all assets otherthan land & building.

100% for the loan allocatedfor interiors and partitionsand 50% for otherequipment.

100% on all assets otherthan land & building.

100% on all assets otherthan land & building

100% on all loans otherthan land & building

100% on all loans otherthan land & building

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

7

8

9

10

11

12

13

14

612020

0613150

0614050

0605000

0605020

0704000

0612010

0613200

Cold Storage

Decortication ofTamarind seeds

Desiccated CoconutPowder

Dhal Mill

Fried Grams

Fruit Juices

Ice plant

Masala Powder

100% on all assets otherthan land & building.

50% on all loans otherthan land & building

100% on all assets otherthan land & building

100% on all loans otherthan land & building.

100% on all assets otherthan land & building.

100% on assets otherthan land & building

100% on assets otherthan land & building

50% on all assets otherthan land and building

20

21

22

23

24

25

26

0604080

0613160

0614030

0604060

0622000

620000

Paddy Harvester

Papads & Pickles

Pepper & Other Spices

Para Boiled Rice mill **

Plates and OtherProducts from ArecanutLeaves –Subject toensuring proper markettie-up.

Poultry Farm *** -[agreement with reputedcompanies like Godrej,Suguna, CP etc.]

100% on all loans

50% on all assets otherthan land and building

100% on all loans otherthan land & building

75% on all assets otherthan land & building.

50% on all assets otherthan land & building

150% on all loan amount

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

15

16

17

18

19

20

0613000

0609000

0703010

0604000

0616000

0610000

Meat, Fish and theirproducts

Milk Dairy & dairyproducts PRocessing

Mineral Water

Modern Rice mill ** (2TPH& above) / Rice rava & flour

Mushroom

New Sugar Mil l(Composite with Ethanolproduction & Co-generation power )

100% on all loans otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

75% on all assets otherthan land & building.

100% on all loans otherthan land & building

100% on all loans otherthan land & building

21

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

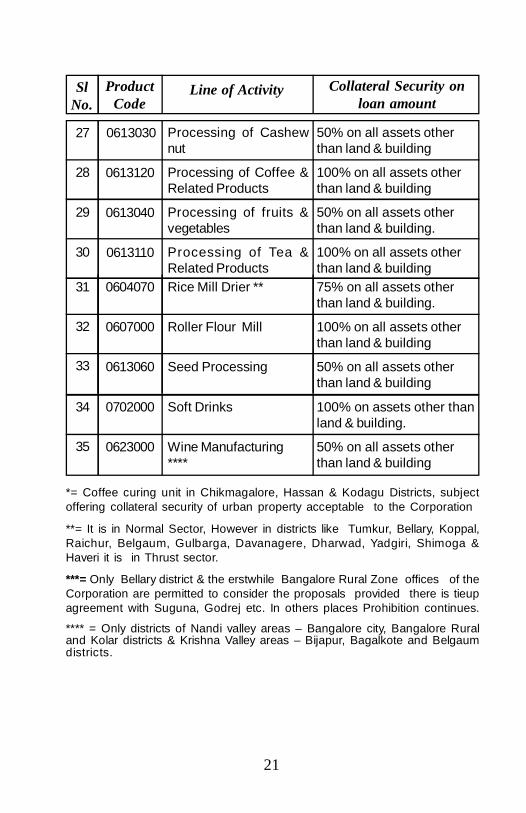

31

32

33

0604070

0607000

0613060

Rice Mill Drier **

Roller Flour Mill

Seed Processing

75% on all assets otherthan land & building.

100% on all assets otherthan land & building

50% on all assets otherthan land & building

27

28

29

30

0613030

0613120

0613040

0613110

Processing of Cashewnut

Processing of Coffee &Related Products

Processing of fruits &vegetables

Processing of Tea &Related Products

50% on all assets otherthan land & building

100% on all assets otherthan land & building

50% on all assets otherthan land & building.

100% on all assets otherthan land & building

34

35

0702000

0623000

Soft Drinks

Wine Manufacturing****

100% on assets other thanland & building.

50% on all assets otherthan land & building

*= Coffee curing unit in Chikmagalore, Hassan & Kodagu Districts, subjectoffering collateral security of urban property acceptable to the Corporation

**= It is in Normal Sector, However in districts like Tumkur, Bellary, Koppal,Raichur, Belgaum, Gulbarga, Davanagere, Dharwad, Yadgiri, Shimoga &Haveri it is in Thrust sector.

***= Only Bellary district & the erstwhile Bangalore Rural Zone offices of theCorporation are permitted to consider the proposals provided there is tieupagreement with Suguna, Godrej etc. In others places Prohibition continues.

**** = Only districts of Nandi valley areas – Bangalore city, Bangalore Ruraland Kolar districts & Krishna Valley areas – Bijapur, Bagalkote and Belgaumdistricts.

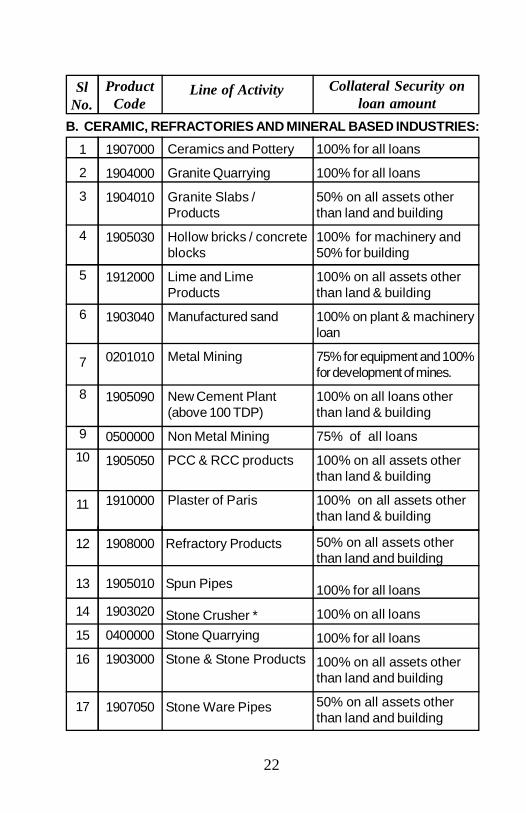

22

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

B. CERAMIC, REFRACTORIES AND MINERAL BASED INDUSTRIES:1

2

3

4

5

6

7

8

9

10

11

1907000

1904000

1904010

1905030

1912000

1903040

0201010

1905090

0500000

1905050

1910000

Ceramics and Pottery

Granite Quarrying

Granite Slabs /Products

Hollow bricks / concreteblocks

Lime and LimeProducts

Manufactured sand

Metal Mining

New Cement Plant(above 100 TDP)

Non Metal Mining

PCC & RCC products

Plaster of Paris

100% for all loans

100% for all loans

50% on all assets otherthan land and building

100% for machinery and50% for building

100% on all assets otherthan land & building

100% on plant & machineryloan

75% for equipment and 100%for development of mines.

100% on all loans otherthan land & building

75% of all loans

100% on all assets otherthan land & building

100% on all assets otherthan land & building

12

13

14

15

16

17

1908000

1905010

1903020

0400000

1903000

1907050

50% on all assets otherthan land and building

100% for all loans

100% on all loans

100% for all loans

100% on all assets otherthan land and building

50% on all assets otherthan land and building

Refractory Products

Spun Pipes

Stone Crusher *Stone Quarrying

Stone & Stone Products

Stone Ware Pipes

23

*= Units coming up in safe zone area only are to be financed.

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

18

19

20

1902020

1902010

1901000

Table Moulded Bricks

Wirecut Bricks

Vitrified tiles / ClayTiles / Mosaic Tiles

100% for machinery and50% for building

100% for machinery and50% for building

100% on all assets otherthan land and building

1

2

3

4

5

1707020

1720000

1906050

1704000

1722000

Agarabathi Chemicals

Analysis of Chemicals

Consumer GlassProducts

Dyes and Dyestuffs

Electroplating

50% on all assets otherthan land and building

100% on all assets otherthan land and building

50% on all assets otherthan land and building

100% on all assets otherthan land and building

100% on all assets otherthan land and building

C. CHEMICAL AND ALLIED INDUSTRIES :

6

7

8

9

10

11

1713025

1707040

0610040

1710000

1711000

1906020

Enzymes & Vitamins

Essential and AromaticOil

Ethanol

Industrial Alcohol &Alcoholic products

Industrial Gases

Industrial GlassProducts

75% on all assets otherthan land and building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land and building

100% on all assets otherthan land and building

50% on all assets otherthan land and building

24

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

12

13

14

15

16

1714000

1707000

0300000

1705000

1705020

Lubricant Oil & grease

Perfumery & Cosmetics

Petroleum Products /Industrial Solvents

Tamarind – IndustrialStarch

Starch -Maize

50% on assets other thanland & building.

50% on all assets otherthan land and building

75% on all assets otherthan land & building

100% on all assets otherthan land & building

50% on assets other thanland & building.

D: CONSTRUCTION ACTIVITY:1 2802000 Commercial Complexes

/ Office complexes /Shop-ping complexes / Readybuilt office space

100% for loan allocated forinteriors and partitions and50% for plant &machinery.An exclusive col-lateral security of not lessthan 25% of the loan amountin respect of CRE projectscoming up on JDA basisshall be taken. However,where the freehold rights ofthe entire land (including thelandlord’s share) is mort-gaged to the Corporation, ex-clusive collateral security to-wards building loan need notbe insisted

2

3

4

2208050

3200000

2807000

Earth moving equipment

Industrial Complexes /Estates

Professional EducationalInstitutions Infrastructure

100% of all loan.

75% for loans allocatedfor assets other than land& building.

100% on all assets otherthan land & building

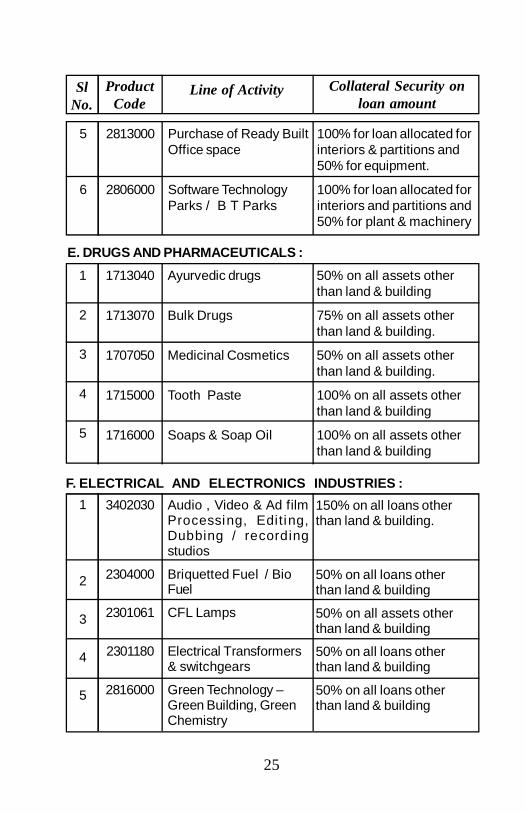

25

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

5

6

2813000

2806000

Purchase of Ready BuiltOffice space

Software TechnologyParks / B T Parks

100% for loan allocated forinteriors & partitions and50% for equipment.

100% for loan allocated forinteriors and partitions and50% for plant & machinery

1

2

3

4

5

1713040

1713070

1707050

1715000

1716000

Ayurvedic drugs

Bulk Drugs

Medicinal Cosmetics

Tooth Paste

Soaps & Soap Oil

50% on all assets otherthan land & building

75% on all assets otherthan land & building.

50% on all assets otherthan land & building.

100% on all assets otherthan land & building

100% on all assets otherthan land & building

E. DRUGS AND PHARMACEUTICALS :

1

2

3

4

5

3402030

2304000

2301061

2301180

2816000

Audio , Video & Ad filmProcessing, Editing,Dubbing / recordingstudios

Briquetted Fuel / BioFuel

CFL Lamps

Electrical Transformers& switchgears

Green Technology –Green Building, GreenChemistry

F. ELECTRICAL AND ELECTRONICS INDUSTRIES :150% on all loans otherthan land & building.

50% on all loans otherthan land & building

50% on all assets otherthan land & building

50% on all loans otherthan land & building

50% on all loans otherthan land & building

26

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

6

7

8

9

10

11

12

13

1304080

2218000

2600000

2602000

2303100

2303110

2303120

2301210

Insulating Materials(used in electricaltransformers and aspacking material ofautomobiles and graniteslabs)

Measuring Instruments

Motion Picture / TVSerial Production

Photo Printing / ColourProcessing Lab

Solar Cookers

Solar Heaters

Solar Lamps / Lights

Storage Battery

F. ELECTRICAL AND ELECTRONICS INDUSTRIES :50% on all loans otherthan land & building

100% on all assets otherthan land & building

200% on all loan

75% on all assets otherthan land & building.

50% on all assets otherthan land and building

50% on all assets otherthan land and building

50% on all assets otherthan land and building

100% on all loans otherthan land & building

1

2

3

4

5

1203000

2406030

2003000

2011000

2004030

Aluminum Furniture andFixtures

Automobile Spares

Bar, Wire and Tube Drawing/ Barbed wire fencing

Deep Drawing (Pressedcomponents)

Die Castings

100% on all assets otherthan land & building

30% on all assets otherthan land & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

30% on all assets otherthan land & building

G. ENGINEERING, MACHANICAL AND ALLIED PRODUCTS

27

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

6

7

8

9

10

11

12

13

14

15

2301030

2301250

2104000

2218010

2406080

2714010

2107000

2008000

2007000

2107051

Electrical Consumergoods

Electrical Furnaces

Galvanising

Gauges and Valves

Gears

General EngineeringWork Shop

Hand tools & otherforged tools

Heat Treatment

Heavy StructuralFabrication

Industrial Abrasives

50% on all assets otherthan land & building

50% on all assets otherthan land & building

100% on all assets otherthan land & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on assets other thanland & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

50% on all assets otherthan land & building

G. ENGINEERING, MACHANICAL AND ALLIED PRODUCTS

16

17

18

19

20

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

2107070

2110000

2704000

2107080

2301240

Industrial Chains

Industrial MetalComponents

Jewelry Manufacturing

Locks, Hinges &Latches

Machinery Mfrg. –Medical equipment

28

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

21

22

23

24

25

26

27

28

29

30

50% on all assets otherthan land & building

30% on all assets otherthan land & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

75% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

2407000

2200000

2004000

2005000

2009000

2108000

2709000

2001000

1206000

2107030

Manufacture ofAutomobiles

Manufacture of MachineTools

Metal Castings

Metal Forging

Metal Powder Coating

Metal Ware &Utensils – Aluminum,Copper, Brass & Silver

Metallic Arts & CraftsManufaturing

Mini Steel Plant

Modular Furniture /Interiors

Other Metal Products

31

32

33

34

35

2707000

2108050

2301310

2002000

2101000

Pen and StationeryArticles

PP Caps

Repairs and ServicingElectrical Items

Re-Rolling Mills

Sheet Metal Product(Fabrication)

100% on assets other thanland & building.

50% on assets other thanland & building.

50% on all assets otherthan land & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

29

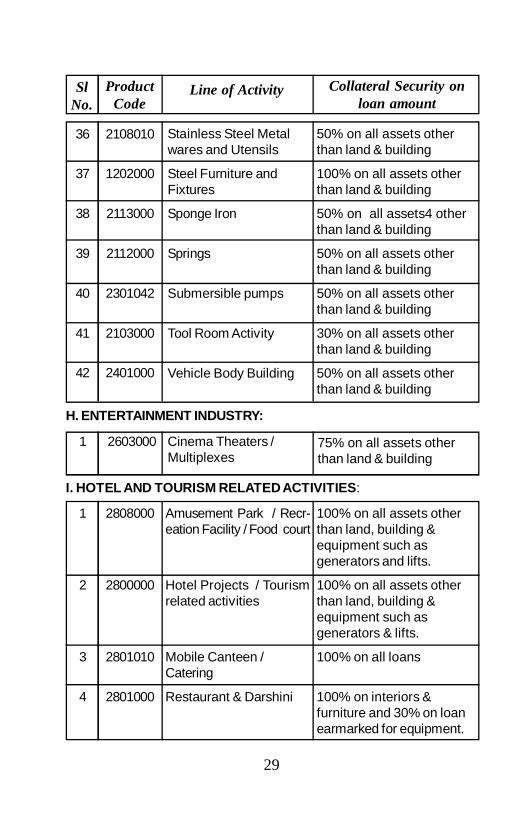

36

37

38

39

40

41

42

2108010

1202000

2113000

2112000

2301042

2103000

2401000

Stainless Steel Metalwares and Utensils

Steel Furniture andFixtures

Sponge Iron

Springs

Submersible pumps

Tool Room Activity

Vehicle Body Building

50% on all assets otherthan land & building

100% on all assets otherthan land & building

50% on all assets4 otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

30% on all assets otherthan land & building

50% on all assets otherthan land & building

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

H. ENTERTAINMENT INDUSTRY:

1 2603000 Cinema Theaters /Multiplexes

75% on all assets otherthan land & building

1

2

3

4

2808000

2800000

2801010

2801000

Amusement Park / Recr-eation Facility / Food court

Hotel Projects / Tourismrelated activities

Mobile Canteen /Catering

Restaurant & Darshini

I. HOTEL AND TOURISM RELATED ACTIVITIES:

100% on all assets otherthan land, building &equipment such asgenerators and lifts.

100% on all assets otherthan land, building &equipment such asgenerators & lifts.

100% on all loans

100% on interiors &furniture and 30% on loanearmarked for equipment.

30

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

5

6

7

2804000

2808000

2810000

Resorts

Ropeway Facilities

Travel & transport /Tourist Service Agencies

I. HOTEL AND TOURISM RELATED ACTIVITIES:100% on all assets other thanland, building & equipmentsuch as generators & lifts.

100% on all assets otherthan land & building

100% on all loans

1

2

3

4

1002010

0901010

0901020

0901030

ComputerisedEmbroidery

Cotton - Ginning

Cotton - Pressing(bailing)

Cotton – Spinning

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

J . JUTE, TEXTILE & WOOL INDUSTRIES

5

6

7

8

9

10

Cotton ThreadProcessing

Cotton Weaving –Powerloom

Ready Made Garments – aminimum of 50 machines

Ready Made Garments forothers–less than 50 machines

Silk and Art SilkWeaving – Handloom

Silk and Art SilkWeaving – Powerloom

Silk Twisting &Reeling

0901043

0901042

1002000

0902031

0902032

0902010

50% on all assets otherthan land & building

75% on all assets otherthan land & building

50% for all loans otherthan land & building.

100% for all loans otherthan land & building.

50% on assets other thanland & building

75% on all assets otherthan land & building

50% on all assets otherthan land & building.

31

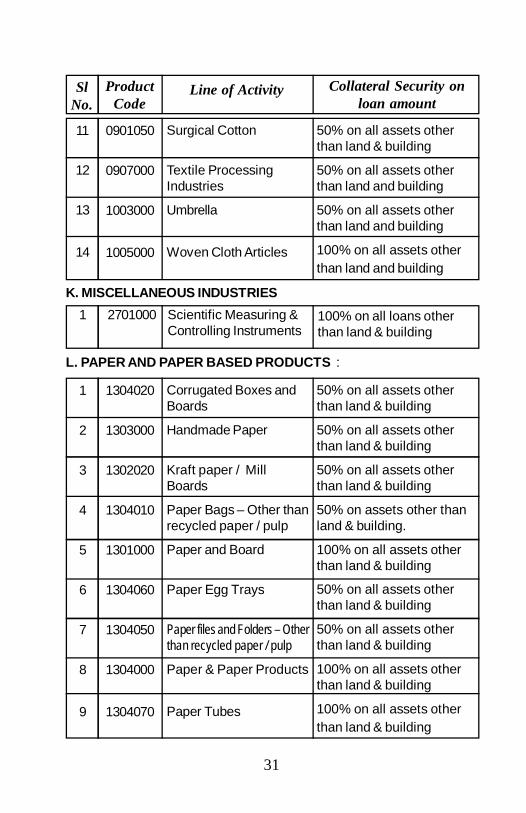

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

11

12

13

14

Surgical Cotton

Textile ProcessingIndustries

Umbrella

Woven Cloth Articles

0901050

0907000

1003000

1005000

50% on all assets otherthan land & building

50% on all assets otherthan land and building

50% on all assets otherthan land and building

100% on all assets otherthan land and building

K. MISCELLANEOUS INDUSTRIES1 2701000 Scientific Measuring &

Controlling Instruments100% on all loans otherthan land & building

1

2

3

4

5

6

7

8

9

Corrugated Boxes andBoards

Handmade Paper

Kraft paper / MillBoards

Paper Bags – Other thanrecycled paper / pulp

Paper and Board

Paper Egg Trays

Paper files and Folders – Otherthan recycled paper / pulp

Paper & Paper Products

Paper Tubes

1304020

1303000

1302020

1304010

1301000

1304060

1304050

1304000

1304070

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on assets other thanland & building.

100% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

L. PAPER AND PAPER BASED PRODUCTS :

32

6

7

8

Plastic Packing Materials[ Exceeding 40 microns]

Plastic Pipes, Conduits

Plastic Woven Sacks

3710040

3710010

3710041

50% on assets other thanland & building.

50% on all assets otherthan land and building

75% on all assets otherthan land and building

1

2

3

4

Computer Stationery

Digital & Flexo Printing

Printing Graphics

Xerox, Photo Copying /STD

1301090

1401080

1401050

1405000

100% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on all assets otherthan land & building

100% on all assets otherthan land & building

N. PRINTING INDUSTRY :

O. RESIDENTIAL ACTIVITY:

1 2805000 Residential Apartments/ Group housing*

Land will be taken as additional secu-rity. An exclusive collateral security ofnot less than of 25% of the loan amountin respect of CRE projects coming upon JDA basis shall be taken. However,

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

1

2

3

4

5

Fibre Glass Products

Plastic ConsumerGoods

Plastic Films

Plastic Industrial Goods

Plastic Monofilaments

3710070

3710060

3710020

3710050

3710030

100% on all assets otherthan land & building

50% on all assets otherthan land and building

50% on assets other thanland & building.

50% on all assets otherthan land & building.

50% on assets other thanland & building.

M. PLASTIC INDUSTRIES :

33

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

1

2

3

4

5

6

7

Consumer RubberProducts

Industrial RubberProducts / IncludingRubber

Industrial – V Belts andFan Belts

Mixing of Rubber

Rubber Hoses & Pipesetc.

Rubber Foot Wear

Rubberised Coir andFoam Rubber

1607000

1608000

1605000

1611000

1608050

1606000

1609000

50% on machinery excludingthe loan amount earmarkedtowards land & building.

50% on machinery excludingthe loan amount earmarkedtowards land & building.

50% on all assets otherthan land & building

50% on assets other thanland & building.

50% on assets other thanland & building

50% on all assets otherthan land & building

50% on machinery excludingthe loan amount earmarkedtowards land & building.

P. RUBBER AND RUBBER PRODUCTS

2 2809000 Residential LayoutDevelopment

here the freehold rights of the entireland (including the landlord’s share) ismortgaged to the Corporation,exclusive collateral security towardsbuilding loan need not be insisted

100% on the loan amount

* All CRE Proposals shall be accepted with the prior approval from the Managing Director/CMD.In respect of other activities specified in the construction such as Infrastructure projects, forma-tion of residential layouts etc., the sanctioning authority continues to be the MD/CMD.

8

9

10

Tread Rubber

Tyres and Tubes

Tyre Retreading

1603000

1601000

1604000

50% on assets other thanland & building

50% on assets other thanland & building.

50% on assets other thanland & building.

34

R. TELECOMMUNICATIONS & IT RELATED ACTIVITIES:1 3603010 Internet Service Provider 125% on all assets other

than land and building

S. TRANSPORT VEHICLES1

2

3

4

5

6

7

8

2901000

2902000

2903000

2904000

2902000

2909000

2909000

2691000

Buses

Cars,Vans and Tractors*

Goods Carrier (Trucks )

LMVs

Public Carrier

Vehicles to ExistingUnits / Promoters

Vehicles to SelfEmployed Professionals

Helicopter Services

100% on all assets

100% on all assets

100% on all assets

100% on all assets

100% on all assets

30% on all assets

30% on all assets

100% on all loans* Maximum limit for sanction of loan for private vehicles can be Rs.15.00 lakhs.

T. WOOD AND WOOD BASED PRODUCTS :1

2

3

1304030

1104000

1103000

Card Board Boxes

Plywood

Veneers for Plywood

50% on all assets otherthan land & building

50% on all assets otherthan land & building

50% on assets other thanland & building.

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

Q. SERVICE SECTION:1

2

3300000

2713040

Consulting Service

Gym/Health Club

100% on all assets otherthan land & building

100% on loans other thanland & building

35

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

1

2

3

4

5

6

7

8

9

10

11

Arecanut & ScentedSupari

Floriculture

Green House

Oil Mill [Expellers]

Poha and Cheera Mill

Pulverizing of Grains

Refined Edible Oil

Refined Non Edible Oil

Solvent extraction –Edible Grade

Solvent extraction –Non Edible Grade

Sugar Mills (CompositeMills)

0613100

621010

0621000

0602000

0604040

2711000

0601010

0601060

1706000

1706060

0610000

100% on all assets otherthan land & building

100% on assets other thanland & building.

100% on all loans

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on all assets otherthan land & building

100% on assets other thanland & building.

100% on assets otherthan land & building

100% on assets otherthan land & building

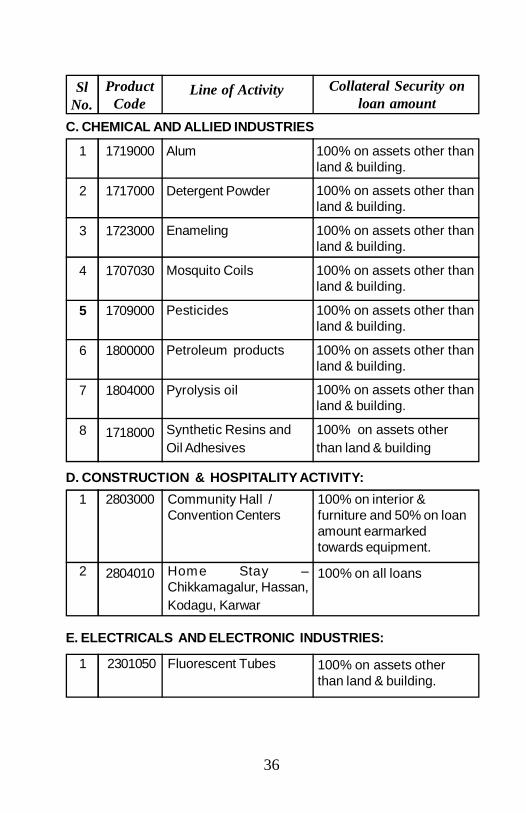

A . AGRO AND FOOD BASED INDUSTRIES :4.3 RESTRICTED SECTOR

B. CERAMIC, REFRACTORIES AND MINERAL BASED INDUSTRIES1

2

3

1905060

1909000

1913000

AC Pipes, Sheets andFittings

Quartz PowderCrucibles

Silica Products

100% on all assets otherthan land & building

100% on assets otherthan land & building.

100% on assets otherthan land & building

36

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

1

2

3

4

5

6

7

8

1719000

1717000

1723000

1707030

1709000

1800000

1804000

1718000

100% on assets other thanland & building.

100% on assets other thanland & building.

100% on assets other thanland & building.

100% on assets other thanland & building.

100% on assets other thanland & building.

100% on assets other thanland & building.

100% on assets other thanland & building.

100% on assets otherthan land & building

C. CHEMICAL AND ALLIED INDUSTRIES

Alum

Detergent Powder

Enameling

Mosquito Coils

Pesticides

Petroleum products

Pyrolysis oil

Synthetic Resins andOil Adhesives

D. CONSTRUCTION & HOSPITALITY ACTIVITY:1

2

2803000

2804010

Community Hall /Convention Centers

Home Stay –Chikkamagalur, Hassan,Kodagu, Karwar

100% on interior &furniture and 50% on loanamount earmarkedtowards equipment.

100% on all loans

E. ELECTRICALS AND ELECTRONIC INDUSTRIES:

1 2301050 Fluorescent Tubes 100% on assets otherthan land & building.

37

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

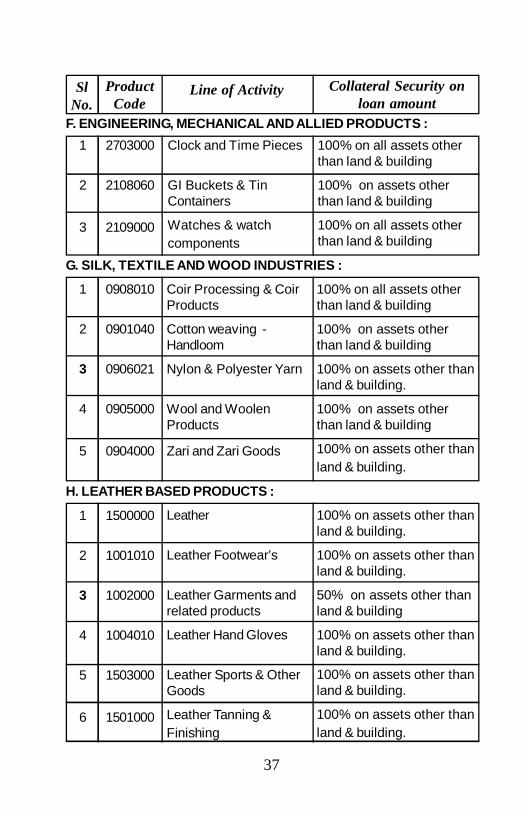

F. ENGINEERING, MECHANICAL AND ALLIED PRODUCTS :1

2

3

2703000

2108060

2109000

Clock and Time Pieces

GI Buckets & TinContainers

Watches & watchcomponents

100% on all assets otherthan land & building

100% on assets otherthan land & building

100% on all assets otherthan land & building

1

2

3

4

5

Coir Processing & CoirProducts

Cotton weaving -Handloom

Nylon & Polyester Yarn

Wool and WoolenProducts

Zari and Zari Goods

0908010

0901040

0906021

0905000

0904000

100% on all assets otherthan land & building

100% on assets otherthan land & building

100% on assets other thanland & building.

100% on assets otherthan land & building

100% on assets other thanland & building.

G. SILK, TEXTILE AND WOOD INDUSTRIES :

1

2

3

4

5

6

Leather

Leather Footwear’s

Leather Garments andrelated products

Leather Hand Gloves

Leather Sports & OtherGoods

Leather Tanning &Finishing

1500000

1001010

1002000

1004010

1503000

1501000

100% on assets other thanland & building.

100% on assets other thanland & building.

50% on assets other thanland & building

100% on assets other thanland & building.

100% on assets other thanland & building.

100% on assets other thanland & building.

H. LEATHER BASED PRODUCTS :

38

SlNo.

ProductCode

Line of Activity Collateral Security onloan amount

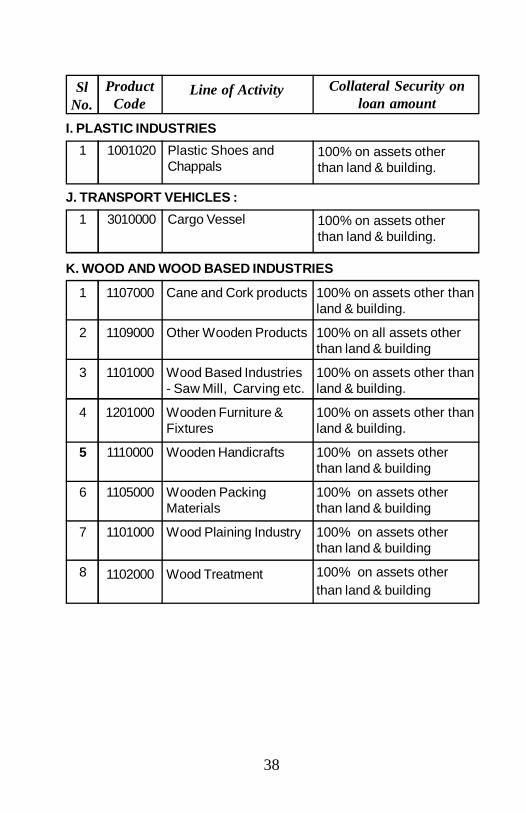

I. PLASTIC INDUSTRIES1 1001020 Plastic Shoes and

Chappals100% on assets otherthan land & building.

J. TRANSPORT VEHICLES :1 3010000 Cargo Vessel 100% on assets other

than land & building.

1

2

3

4

5

6

7

8

1107000

1109000

1101000

1201000

1110000

1105000

1101000

1102000

100% on assets other thanland & building.

100% on all assets otherthan land & building

100% on assets other thanland & building.

100% on assets other thanland & building.

100% on assets otherthan land & building

100% on assets otherthan land & building

100% on assets otherthan land & building

100% on assets otherthan land & building

K. WOOD AND WOOD BASED INDUSTRIES

Cane and Cork products

Other Wooden Products

Wood Based Industries- Saw Mill, Carving etc.

Wooden Furniture &Fixtures

Wooden Handicrafts

Wooden PackingMaterials

Wood Plaining Industry

Wood Treatment

39

SlNo.

ProductCode

Line of Activity

4.4 PROHIBITED SECTOR

1245678910

170201006131500610020060403006150000620000061200008000000603000

Bone & Fish MealDecortication of other seedsKandasari SugarMini Rice MillMalt ExtractionPoultry FarmSaltTobacco Processing and its ProductsVanaspathi

A . AGRO AND FOOD BASED INDUSTRIES :

1234567

1704020171203007010000703000171202017080001903040

Acid, Base and NaptholsAcid - SlurryAlcoholic BeveragesCarbonated water (Aerated water )Nitro Glycerin Based Industrial ExplosiveSafety Matches and Fire WorksSoap Stone polishing

B. CHEMICAL AND ALLIED INDUSTRIES :

1 2301210 GLS LampsC. ELECTRICAL AND ELECTRONICS INDUSTRIES :

1 2805010 Service ApartmentsD. HOTEL AND TOURISM RELATED ACTIVITIES :

12

09060103710043

Cellulosic & Synthetic FibreJute Bags

E. JUTE AND TEXTILE INDUSTRIES :

12

38010011905090

Borewell RigsMini Cement Plant

F. MISCELLANEOUS INDUSTRIES :

1 2906000 Auto rickshawsG. TRANSPORT VEHICLES :

40

5. MSMEs Definition to be followed:

Definitions of Micro, Small & Medium Enterprises

In accordance with the provisions of Micro, Small & Medium EnterprisesDevelopment (MSMED) Act, 2006, the Micro, Small and MediumEnterprises (MSME) are classified into two Classes:

5.1. Manufacturing Enterprises: The enterprises engaged in themanufacture or production of goods pertaining to any industryspecified in the first schedule to the Industries (Development andRegulation) Act, 1951. The Manufacturing Enterprises are defined interms of investment in Plant & Machinery.

a Micro enterprises where investment in plant andmachinery does not exceedRs.25.00 lakhs.

b Small enterprises where the investment in plant andmachinery is more than Rs.25.00lakhs but not exceeding Rs.5.00 crores.

c Medium enterprises Where the investment in plant andmachinery is more than Rs.5.00 croresbut does not exceed Rs.10.00 crores.

5.2 Service Enterprises: The enterprises engaged in providing orrendering of services are defined in terms of investment in equipment.

a Micro enterprises engaged in providing services where theInvestment in equipment is not morethan Rs.10.00 lakhs.

b Small enterprises engaged in providing services where theInvestment in equipment is more thanRs.10.00 lakhs but does not exceedRs.2.00 crores.

c Medium enterprises Engaged in providing services where theinvestment in equipment is more thanRs.2.00 crores but does not exceedRs.5.00 crores.

41

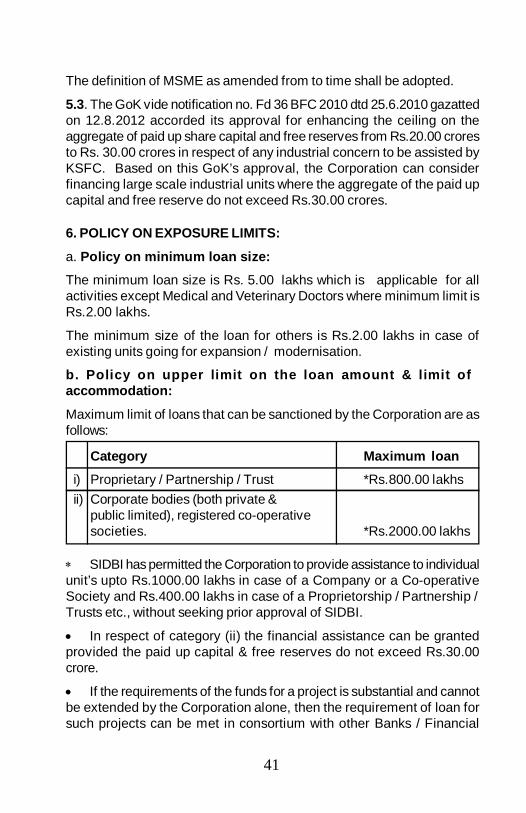

The definition of MSME as amended from to time shall be adopted.

5.3. The GoK vide notification no. Fd 36 BFC 2010 dtd 25.6.2010 gazattedon 12.8.2012 accorded its approval for enhancing the ceiling on theaggregate of paid up share capital and free reserves from Rs.20.00 croresto Rs. 30.00 crores in respect of any industrial concern to be assisted byKSFC. Based on this GoK’s approval, the Corporation can considerfinancing large scale industrial units where the aggregate of the paid upcapital and free reserve do not exceed Rs.30.00 crores.

6. POLICY ON EXPOSURE LIMITS:

a. Policy on minimum loan size:

The minimum loan size is Rs. 5.00 lakhs which is applicable for allactivities except Medical and Veterinary Doctors where minimum limit isRs.2.00 lakhs.

The minimum size of the loan for others is Rs.2.00 lakhs in case ofexisting units going for expansion / modernisation.

b. Policy on upper limit on the loan amount & limit ofaccommodation:

Maximum limit of loans that can be sanctioned by the Corporation are asfollows:

Category Maximum loan

i) Proprietary / Partnership / Trust *Rs.800.00 lakhsii) Corporate bodies (both private &

public limited), registered co-operativesocieties. *Rs.2000.00 lakhs

SIDBI has permitted the Corporation to provide assistance to individualunit’s upto Rs.1000.00 lakhs in case of a Company or a Co-operativeSociety and Rs.400.00 lakhs in case of a Proprietorship / Partnership /Trusts etc., without seeking prior approval of SIDBI.

In respect of category (ii) the financial assistance can be grantedprovided the paid up capital & free reserves do not exceed Rs.30.00crore.

If the requirements of the funds for a project is substantial and cannotbe extended by the Corporation alone, then the requirement of loan forsuch projects can be met in consortium with other Banks / Financial

42

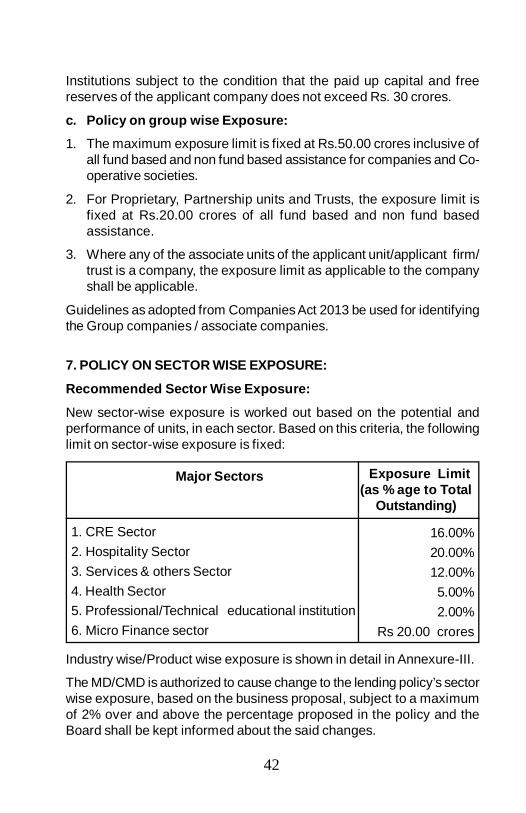

Institutions subject to the condition that the paid up capital and freereserves of the applicant company does not exceed Rs. 30 crores.

c. Policy on group wise Exposure:

1. The maximum exposure limit is fixed at Rs.50.00 crores inclusive ofall fund based and non fund based assistance for companies and Co-operative societies.

2. For Proprietary, Partnership units and Trusts, the exposure limit isfixed at Rs.20.00 crores of all fund based and non fund basedassistance.

3. Where any of the associate units of the applicant unit/applicant firm/trust is a company, the exposure limit as applicable to the companyshall be applicable.

Guidelines as adopted from Companies Act 2013 be used for identifyingthe Group companies / associate companies.

7. POLICY ON SECTOR WISE EXPOSURE:

Recommended Sector Wise Exposure:

New sector-wise exposure is worked out based on the potential andperformance of units, in each sector. Based on this criteria, the followinglimit on sector-wise exposure is fixed:

Major Sectors

1. CRE Sector2. Hospitality Sector3. Services & others Sector4. Health Sector5. Professional/Technical educational institution6. Micro Finance sector

Exposure Limit(as % age to Total

Outstanding)

16.00%20.00%12.00%5.00%2.00%

Rs 20.00 crores

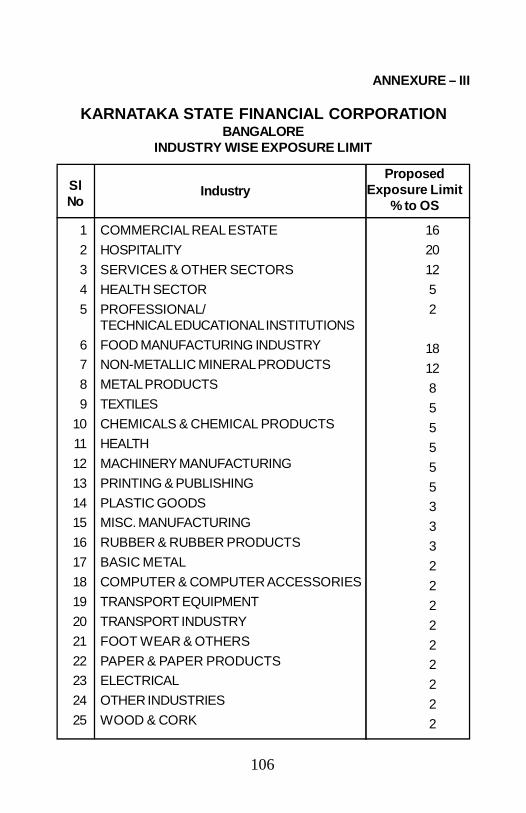

Industry wise/Product wise exposure is shown in detail in Annexure-III.

The MD/CMD is authorized to cause change to the lending policy’s sectorwise exposure, based on the business proposal, subject to a maximumof 2% over and above the percentage proposed in the policy and theBoard shall be kept informed about the said changes.

43

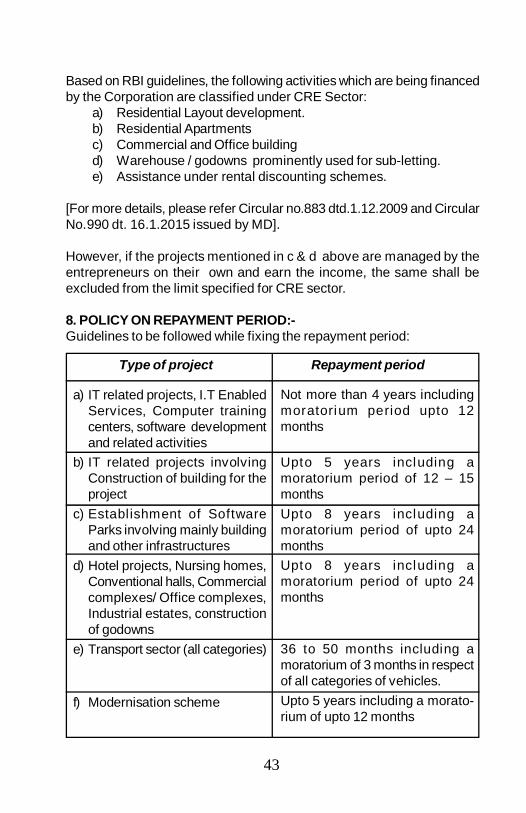

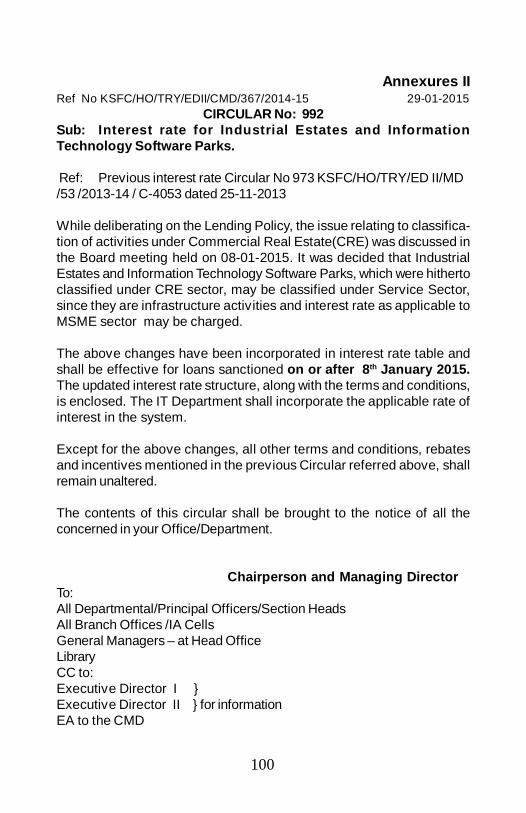

Based on RBI guidelines, the following activities which are being financedby the Corporation are classified under CRE Sector:

a) Residential Layout development.b) Residential Apartmentsc) Commercial and Office buildingd) Warehouse / godowns prominently used for sub-letting.e) Assistance under rental discounting schemes.

[For more details, please refer Circular no.883 dtd.1.12.2009 and CircularNo.990 dt. 16.1.2015 issued by MD].

However, if the projects mentioned in c & d above are managed by theentrepreneurs on their own and earn the income, the same shall beexcluded from the limit specified for CRE sector.

8. POLICY ON REPAYMENT PERIOD:-Guidelines to be followed while fixing the repayment period:

Type of project Repayment period

a) IT related projects, I.T EnabledServices, Computer trainingcenters, software developmentand related activities

b) IT related projects involvingConstruction of building for theproject

c) Establishment of SoftwareParks involving mainly buildingand other infrastructures

d) Hotel projects, Nursing homes,Conventional halls, Commercialcomplexes/ Office complexes,Industrial estates, constructionof godowns

e) Transport sector (all categories)

f) Modernisation scheme

Not more than 4 years includingmoratorium period upto 12months

Upto 5 years including amoratorium period of 12 – 15monthsUpto 8 years including amoratorium period of upto 24monthsUpto 8 years including amoratorium period of upto 24months

36 to 50 months including amoratorium of 3 months in respectof all categories of vehicles.Upto 5 years including a morato-rium of upto 12 months

44

g) Rehabilitation Scheme:

(i) Period of relief(ii) Repayment of total liability(iii) Overall repayment periodfrom the date of firstdisbursement

h) Corporate Loan Scheme

i)Privileged Entrepreneurs Scheme

j) Construction activity / Propertydevelopment (Build & Sell):-construction of Group Housing,commercial complexes,software technology parks, BTparks.

SSI UNITS MSI UNITS

Upto 5 years Upto 7 years7 to 10 years 7 to 10 yearsUpto 20 years Upto 20 years

Not exceeding 24 monthsexcluding a maximum moratoriumperiod of 6 months

Upto 24 months including a maxi-mum moratorium period upto 6months.

k) Corporate loan for ConstructionActivity :- Infrastructure projectwith road, flyover, bridges..

l) (a) Cinema Theaters /Multiplexes(b) Feature films, TV serials,software for visual mediapublicity

m) All other schemes

Upto 3 years including amoratorium of 6 to 18 months,depending upon the progress inproject implementation period

Up to 3 years including amoratorium of 6 to 18 monthsdepending upon the progress inproject implementation period.Upto 5 years including amoratorium of 24 months.Single repayment in the13th monthor before the release of the featurefilm, TV serials, software for visualmedia publicity whichever is earlier.

Upto 6 years including a morato-rium period varying between 6 to 9months in the case of only machin-ery / equipment and 6 to 18 monthsin case of involvement of buildingconstruction for the project.

While the above gives a broad guideline for fixing the repayments, longerrepayment / moratorium could be given based on the location of the unit, typeof industry, profitability, security available etc., provided there are strongreasons supporting such fixation. Such recommendations should be madevery judiciously.

45

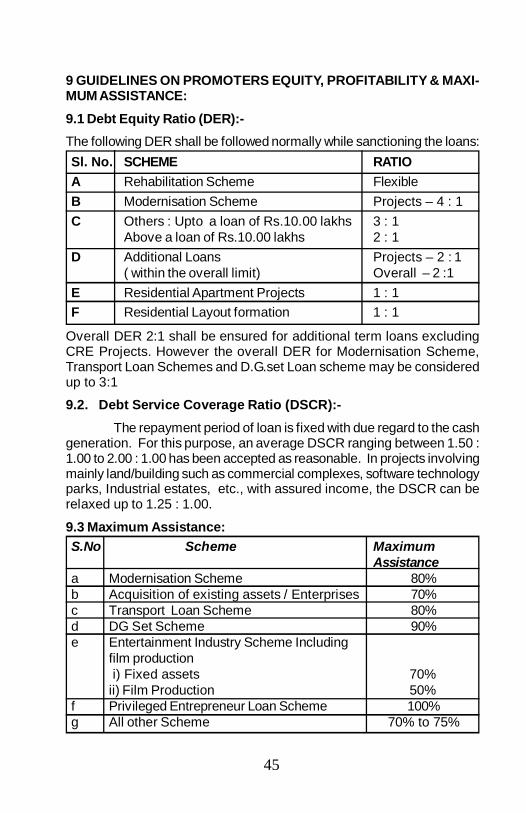

9 GUIDELINES ON PROMOTERS EQUITY, PROFITABILITY & MAXI-MUM ASSISTANCE:9.1 Debt Equity Ratio (DER):-The following DER shall be followed normally while sanctioning the loans:Sl. No. SCHEME RATIOA Rehabilitation Scheme FlexibleB Modernisation Scheme Projects – 4 : 1C Others : Upto a loan of Rs.10.00 lakhs 3 : 1

Above a loan of Rs.10.00 lakhs 2 : 1D Additional Loans Projects – 2 : 1

( within the overall limit) Overall – 2 :1E Residential Apartment Projects 1 : 1F Residential Layout formation 1 : 1

Overall DER 2:1 shall be ensured for additional term loans excludingCRE Projects. However the overall DER for Modernisation Scheme,Transport Loan Schemes and D.G.set Loan scheme may be consideredup to 3:1

9.2. Debt Service Coverage Ratio (DSCR):-The repayment period of loan is fixed with due regard to the cash

generation. For this purpose, an average DSCR ranging between 1.50 :1.00 to 2.00 : 1.00 has been accepted as reasonable. In projects involvingmainly land/building such as commercial complexes, software technologyparks, Industrial estates, etc., with assured income, the DSCR can berelaxed up to 1.25 : 1.00.

9.3 Maximum Assistance:S.No Scheme Maximum

Assistancea Modernisation Scheme 80%b Acquisition of existing assets / Enterprises 70%c Transport Loan Scheme 80%d DG Set Scheme 90%e Entertainment Industry Scheme Including

film production i) Fixed assets 70%ii) Film Production 50%

f Privileged Entrepreneur Loan Scheme 100%g All other Scheme 70% to 75%

46

9.4 Promoter’s contribution:-

The following norm may be followed while sanctioning the loan:

Particulars Minimum percentage on project cost

a) All district / regions 22.5%

b) Rehabilitation scheme Flexible

c) DG Set loan 10%

9.5 INTEREST RATE STRUCTURE:

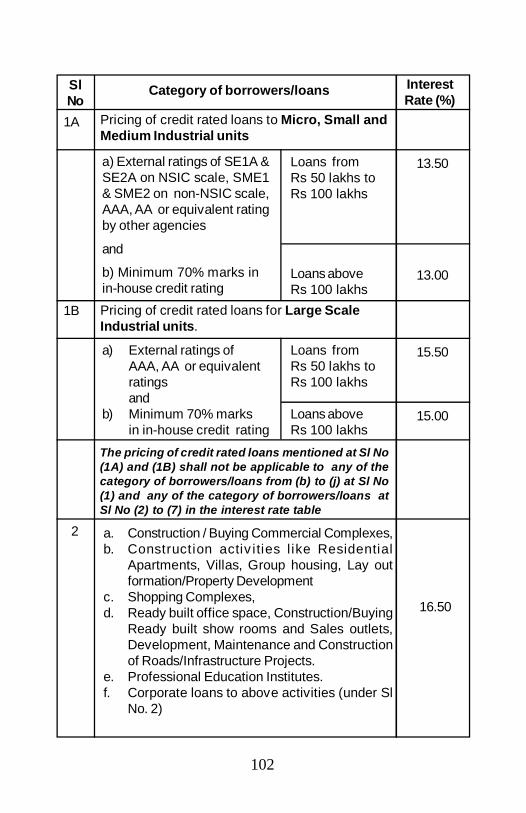

The present interest rate structure applicable for different categories isgiven at Annexure-II. This is subject to revision from time to time asapproved by the Board.

10. POLICY ON FORECLOSURES / PRE-PAYMENTS:-

Prepayment / foreclosure premium will be charged as follows:

1. In respect of pre-payment of loan instalments upto 02 quarters or06 months in a financial year- no pre-payment penalty shall becharged;

2. In respect of foreclosure of loan accounts where remaininginstalments is more than 2 quarters or six months but less thanone year – foreclosure premium at 1.5% shall be charged on theentire outstanding loan balance as on the date of foreclosure;

3. In respect of loan accounts where remaining instalments is morethan one year – foreclosure premium at 2% shall be charged onthe entire outstanding loan balance as on the date of foreclosure;

Note: In respect of loan accounts where remaining instalments is lessthan 6 months, no foreclosure premium shall be charged. However, thisexemption as well as exemption available as per sub-para 1 above willnot be applicable in respect of foreclosure of cases mentioned at sub-para 2 & 3 above;

However, the policy of foreclosure / pre-payment of the accounts in re-spect of the following category of account without collecting the foreclo-sure / pre-payment premium will continue.

47

(a) Closure of accounts on OTS.

(b) NPAs under SWS / SRTO loans and Composite loans.

(c) Doubtful accounts.

(d) Prepayment / fore-closure by sale of secured / personal propertiesincluding cases of commercial complexes / residential apartmentwhere pre-payment is out of saleproceeds of the premises financed.

(e) NPAs in respect of loans sanctioned up to Rs.2.00 lakhs.

(f) Privileged Entrepreneur loan and corporate loan.

(g) Prepayment/foreclosure on account of repayments received throughadjustment of subsidies such as investment subsidy, CLCSS,MOFPI,NHB,interest subsidies etc.

Concerned Branch Manager can approve the pre-closure / fore closuressubject to collection of premium as mentioned above.

10.1 POLICY ON TIME STANDARD IN PROCESSING OF LOANAPPLICATION:

The appraisal section shall finalise the credit appraisal within 10 days inrespect of cases where the project cost is below Rs.100.00 lakhs andwithin 20 days in respect of cases where the project cost is aboveRs.100.00 lakhs and submit the loan memorandum for sanction to theappropriate sanctioning authority through proper channel.

The appropriate loan sanctioning authority should decide on the loanmemorandum within three days in respect of cases where the projectcost is upto Rs.100.00 lakhs and within seven days in respect of caseswhere the project cost is above Rs.100.00 lakhs. However, the abovetime limit in respect of cases placed before the Board and EC shall besubject to relaxation based on the date of meeting of Board / EC.

11.A. DELEGATION OF LOAN SANCTIONING POWERS (GENERAL):

[Delegation of loan sanction and disbursement powers as per circularno. 950 dtd 31.3.2012 issued by Managing Director is incorporated].

48

Corporate LoanRs.10.00 lakhswithin overall limit ofRs.50.00 lakhsRs.10.00 lakhswithin overall limit ofRs.75.00 lakhsRs.25.00 lakhswithin overall limit ofRs.100.00 lakhsRs.50.00 lakhswithin overall limit ofRs.150.00 lakhsRs.100.00 lakhswithin overall limit ofRs.300.00 lakhsRs.250.00 lakhswithin overall limit ofRs.500.00 lakhsRs.500.00 lakhswithin overall limit ofRs.1000.00 lakhsRs.500.00 lakhswithin overall limit ofRs.2000.00 lakhs

Additional LoanWithin overall limit ofRs.50.00 lakhs

Within overall limit ofRs.75.00 lakhs

Within overall limit ofRs.100.00 lakhs

Within overall limit ofRs.150.00 lakhs

Within overall limit ofRs.300.00 lakhs

Within overall limit ofRs.500.00 lakhs

Within overall limit ofRs.1000.00 lakhs

Above Rs.1000.00lakhs

New LoanRs.50.00lakhs

Rs.75.00lakhs

Rs.100.00lakhs

Rs.150.00lakhs

Rs.300.00lakhs

Rs.500.00lakhs

Rs.1000.00lakhs

AboveRs.1000.00lakhs

Sanctioning Authority

BMs of ‘B’ GradeBranch Offices

AGMs of ‘A’ GradeBranch Offices

DGMs of Super ‘A’Grade BranchOfficesGeneral Managers

Executive Directors

Managing Director

ExecutiveCommittee

Board

Sl. No1

2

3

4

5

6

7

8

Sanctioning powers (Maximum Amount)

B. DELEGATION OF LOAN SANCTIONING POWERS FOR EXISTINGGOOD CUSTOMERS:Sl. Sanctioning Authority Sanctioning powers (Maximum Amount)

Corporate Loan Privileged Entrepreneur Loan1 BMs of ‘B’ Grade

Branch Offices Rs.10.00 lakhs Rs.10.00 lakhs2 AGMs of ‘A’ Grade

Branch Offices Rs.20.00 lakhs Rs.20.00 lakhs3 DGMs of Super ‘A’

Grade Branch Offices Rs.35.00 lakhs Rs.35.00 lakhs4 General Managers Rs.50.00 lakhs Rs.50.00 lakhs5 Executive Directors Rs.100.00 lakhs Rs.100.00 lakhs6 Managing Director Rs.250.00 lakhs Rs200.00 lakhs7 Executive Committee Rs.500.00 lakhs —

49

Note:

Eligibility Criteria of Existing Good Customers:

1. The units should have availed loan of Rs10 lakhs or more fromKSFC in the past and should have a good track record for at least3 years.

2. The account should have been in standard category during the last3 years.

3. In respect of rescheduled cases and cases covered under DRS-RSR, the account should be regular and in standard category forthe previous 3 years.

4. The unit should be working on profitable lines i.e., the units shouldhave earned net profits at least during the last 3 years as evidencedby the audited financial statements.

5. Where the loan accounts are closed more than 3 years back, theproposals should be treated as a proposal from a new customer.

In respect of these categories of borrowers, the respective sanc-tioning authority can sanction corporate / PE loan as detailed abovewithout linking to the overall limit of term loans and WCTL. How-ever, if the project for which latest loan sanctioned is under imple-mentation, the sanctioning of corporate / PE loan in such casesshall fall within the delegated powers of the earlier loan sanctioningauthority. Further, the corporate loan and PE loans shall not ex-ceed 150% of the aggregate loan amount disbursed of live accountsand of the term loan accounts closed in the last 3 years (excludingthe proposed loan).

50

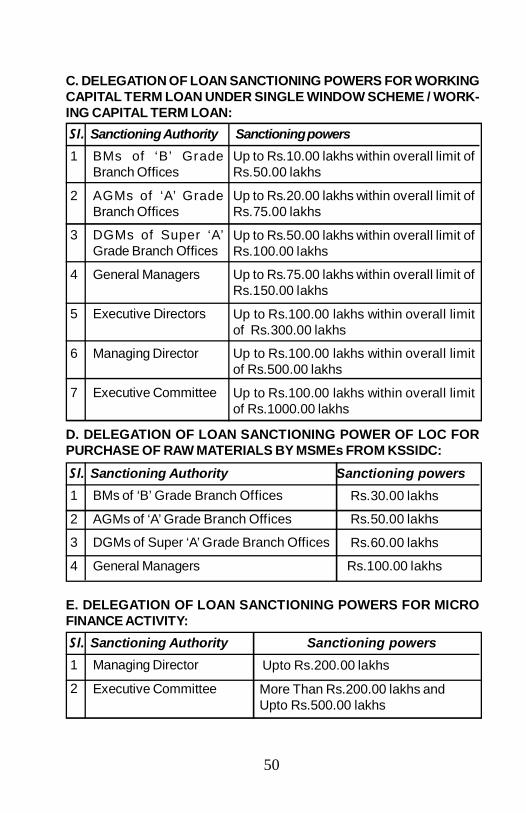

C. DELEGATION OF LOAN SANCTIONING POWERS FOR WORKINGCAPITAL TERM LOAN UNDER SINGLE WINDOW SCHEME / WORK-ING CAPITAL TERM LOAN:Sl. Sanctioning Authority Sanctioning powers1

2

3

4

5

6

7

BMs of ‘B’ GradeBranch Offices

AGMs of ‘A’ GradeBranch Offices

DGMs of Super ‘A’Grade Branch Offices

General Managers

Executive Directors

Managing Director

Executive Committee

Up to Rs.10.00 lakhs within overall limit ofRs.50.00 lakhs

Up to Rs.20.00 lakhs within overall limit ofRs.75.00 lakhs

Up to Rs.50.00 lakhs within overall limit ofRs.100.00 lakhs

Up to Rs.75.00 lakhs within overall limit ofRs.150.00 lakhs

Up to Rs.100.00 lakhs within overall limitof Rs.300.00 lakhs

Up to Rs.100.00 lakhs within overall limitof Rs.500.00 lakhs

Up to Rs.100.00 lakhs within overall limitof Rs.1000.00 lakhs

D. DELEGATION OF LOAN SANCTIONING POWER OF LOC FORPURCHASE OF RAW MATERIALS BY MSMEs FROM KSSIDC:Sl. Sanctioning Authority Sanctioning powers1

2

3

4

BMs of ‘B’ Grade Branch Offices

AGMs of ‘A’ Grade Branch Offices

DGMs of Super ‘A’ Grade Branch Offices

General Managers

Rs.30.00 lakhs

Rs.50.00 lakhs

Rs.60.00 lakhs

Rs.100.00 lakhs

E. DELEGATION OF LOAN SANCTIONING POWERS FOR MICROFINANCE ACTIVITY:Sl. Sanctioning Authority Sanctioning powers1

2

Managing Director

Executive Committee

Upto Rs.200.00 lakhs

More Than Rs.200.00 lakhs andUpto Rs.500.00 lakhs

51

All proposals under the Micro finance activity scheme which meets theeligibility criteria, shall be processed after obtaining “in principle clearance”from the Managing Director/CMD. The Corporate limit on micro financingexposure is fixed at Rs.20 crores. The exposure of the Corporation toa micro finance institution shall not exceed 15% of its (MFI) totaldebts.

Note: The sanctioning powers indicated at Table B & D are exclusivepowers and loans can be sanctioned in addition to overall limits indicatedat Table-A. However, the additional and corporate loans in Table-A andworking capital loan indicated at Table-C should be within the overallmaximum limit indicated for the respective sanctioning authorities in Table-A.

12. DELEGATION OF DISBURSEMENT POWERS:

12.1 LOAN DISBURSEMENT:

a. Branch Managers:

The Branch Managers are empowered to disburse loans in respect ofsanctions done by various authorities up to Rs.5.00 crore at a time afterensuring the compliance of terms and conditions of loan sanction.However, the BMs are empowered to relax minor conditions like nonreceipt of copy of IT returns, renewed license, WC arrangements andappointment of skilled persons. This does not apply to conditionsspecifically laid down by higher / sanctioning authorities.

Further, all these conditions shall be complied before release of last 35%of the term loan amount. Further, the Branch Managers are authorizedto release the moneys directly to KIADB for purchase of KIADB land bythe promoters assisted by KSFC after obtaining interim documents of allthe promoters / PG holders, loan agreement and undertaking letter etc.However, the BM shall ensure that the guidelines issued vide circularno.919 dated 17.09.2010 is complied with.

b. General Managers: