leijonhufvud on new keynesian economics and the economics

TRANSCRIPT

Hans-Michael Trautwein1

Leijonhufvud on New Keynesian Economics

and the Economics of Keynes

1 Introduction

In a famously unpublished paper on The Uses of the Past, which Axel Leijonhufvud presented

at the ESHET 2006 conference in Porto and on other occasions, he has compared the evolution

of economic thinking to the growth of a decision tree (Leijonhufvud 2006). The basic

understanding is that currently predominant theories have developed out of earlier decisions

about modelling standards that, at the time of their making, appeared plausible and feasible

for reducing complexity. However, those modelling conventions may create blind spots that

critically limit their scope. In his semi-centennial classic On Keynesian Economics and the

Economics of Keynes (1968) and in many of his later writings, Leijonhufvud has amply

demonstrated that it is possible to detect the blind spots by looking at research questions in

theories that branched off at lower forks of the Econ tree. Moreover, climbing out on those

older branches by way of analytical reconstruction or other methods may lead to new ideas.

The theme that Leijonhufvud has extracted from the Economics of Keynes and other writers

in the inter-war period is the incompleteness of information in large, complex economic

systems that may lead to failures in the intertemporal coordination of activities. Fifty years

ago, Leijonhufvud attacked post-war Keynesian Economics (the old Neoclassical Synthesis)

for its adherence to a frictions view that reduces macroeconomic pathologies to deviations

from optimal general equilibrium, which are caused by nominal rigidities and other spanners

in the works of the price mechanism. With the rise of New Keynesian Economics as an integral

part of the New Neoclassical Synthesis, based on dynamic stochastic general equilibrium

(DSGE) modelling, Leijonhufvud has pointed out time and again, that standard

macroeconomics may have made much technical progress since the 1960s, but is still stuck in

the frictions view. Referring to the global financial crisis of recent vintage, he considers DSGE

modelling conventions to be fundamentally obstructive to analysing core problems of

1 FK II-VWL, Carl von Ossietzky Universität Oldenburg, 26111 Oldenburg, Germany;

[email protected]. Draft prepared for the 22nd ESHET conference at the Universidad Complutense de Madrid, 7-9 June 2018.

2

macroeconomic coordination and instability. However, some New Keynesians – and even the

occasional Post Keynesian – claim that they have now found ways to deal with those problems

within their DSGE frameworks.

The aim of this paper is to describe continuity and change in Leijonhufvud’s critique of Old

and New Keynesians, and to assess some contrary claims of progress made in the DSGE world.

Section 2 summarizes Leijonhufvud’s reinterpretation of Keynes in critique of (Old) Keynesian

Economics. Section 3 provides an account of his criticism of New Keynesian Economics which,

in comparison with his systematic assessments of older Keynesianism, he has made in more

scattered remarks; here these will be directly related to the representative DSGE model of pre-

crisis New Keynesianism. Section 4 describes some recent attempts to deal with macro-

economic instability within DSGE frameworks. Section 5 takes stock of the progress made or

forgone in the light of Leijonhufvud’s interpretation of Keynes. For the sake of simplicity, his

first name Axel (a trademark of its own among the literati) will serve as substitute for his

complicated surname (old Swedish spelling for Lionhead) throughout the text of the following

sections, while Leijonhufvud will mostly be encaged in parentheses for referencing.

2 Keynes and the Keynesians: Axel’s suggested interpretation

Leijonhufvud’s 1968 treatise On Keynesian Economics and the Economics of Keynes was based on

the dissertation that had earned him a doctoral degree at Northwestern University the year

before.2 His original intention for that project had been the construction of a debt deflation

theory that would explain the difference between ordinary recessions and great depressions

(Leijonhufvud 1998: 174, Snowdon 2004: 123). The 1960s were the time, when it was commonly

claimed that ‘we are all Keynesians now’, on the belief that Keynesian economics had managed

to eliminate the threat of economic depression once and for all. Yet, Axel found it unacceptable

that standard Keynesian economics was lacking a convincing framework for analysing the

emergence and dynamics of grave system failures such as the Great Depression. Learning that

Irving Fisher had already developed a debt-deflation theory in a (then half-forgotten)

contribution to the first volume of Econometrica (Fisher 1933), he gave up on the original

intention. Yet, still wondering why debt deflation could not be accommodated in standard

macroeconomics, he took his time for a close reading of John Maynard Keynes’s Treatise on

Money (1930) and General Theory of Employment, Interest and Money (1936). This resulted in an

accumulation of notes and unfinished manuscripts that would not make a coherent PhD thesis

2 This section is based on Trautwein (2018) and Axel’s interviews with Snowdon (2004) and Jayadev and Mason (2015) for biographical information.

3

before time was up for Axel’s acting assistant professorship at the UCLA (University of

California, Los Angeles). To avoid going home to Sweden without a PhD degree, Axel

reorganized his writings into an admissible thesis, in a way that is certainly not taught as

standard fare in PhD courses: As he would jokingly put it ex post, he made the footnotes of his

unfinished manuscripts into text and the text into footnotes.

The more general theory

The result was an interpretation of Keynes that differed substantially from the conventional

understanding. This had already become apparent in a preview article, published in the

American Economic Review under the title ‘Keynes and the Keynesians: A Suggested

Interpretation’ (Leijonhufvud 1967). The title echoed John Hicks’s famous 1937 essay on ‘Mr

Keynes and the “Classics”; A Suggested Interpretation’, the birthplace of IS-LM analysis.

Axel’s interpretation was diametrically opposed to Hicks’s downgrading of Keynes’s General

Theory to a special case, characterized as ‘Economics of Depression’ (Hicks 1937: 155).

‘To be a Keynesian, one need only realize the difficulties of finding the market-

clearing vector [of prices]... The only thing which Keynes “removed” from the

foundations of classical theory was the deus ex machina – the auctioneer which is

assumed to furnish, without charge, all the information needed to obtain the

perfect coordination of the activities of all traders in the present and through the

future. Which, then, is the more “general theory” and which the “special case”?

Must one not grant Keynes his claim to having tackled the more general problem?’

(Leijonhufvud 1967: 404, 410 – italics in the original)

The positive answer to the last question became the leitmotif of the dissertation, which earned

Axel international recognition and, as collateral benefit, tenure at the UCLA. The removal of

the Walrasian auctioneer assumption was a key point, since his critique of Keynesian

economics centred on the latter’s implicit use of neo-Walrasian logic.3

By the mid-1960s, macroeconomists had come to regard the IS/LM model in the tradition of

Hicks (1937) and Hansen (1949: ch. 5) as a framework that accommodated both Walrasian

general equilibrium and Keynesian underemployment. It represented the workhorse model of

3 Later on, Axel (Leijonhufvud 1998: 177) admitted that ‘ “getting rid of the auctioneer” was… a big part of [his] own ‘struggle to escape’ from the neo-Walrasians,’ while ‘it cannot have been a problem that Keynes had with his own classical mentor, Marshall.’ In the corresponding footnote, he explained: ‘I’m afraid that I may be the one responsible for this “anthropomorphication” of Walras’s hypothetical market process. In my 1967 article, “Keynes and the Keynesians”, I wanted to dramatize the contention that (modern) general equilibrium theory was cheating on the obligation to explain how the information required for the orderly coordination of activities was generated and communicated. Clerk Maxwell’s famous thought-experiment in physics carne to mind and I introduced Walras’s auctioneer as my counterpart to Maxwell’s demon.’ (1998: 186 fn. 12)

4

the Neoclassical Synthesis. Although the Walrasian auctioneer was not explicitly invoked in

standard IS/LM analysis, general equilibrium defined the benchmark position, in which all

intertemporal plans for consumption and production are fully coordinated. Keynes’s general

theory of unemployment was confined to three special cases: liquidity traps, investment traps,

and nominal wage rigidities. The first two looked indeed like belonging within the special

category of depression economics, in which inscrutable market psychology did the trick. After

Modigliani (1944), more general explanations of Keynesian underemployment had therefore

been reduced to nominal wage rigidities, to frictions in the price mechanism.

For Axel, the trouble with the rigidities approach of the Neoclassical Synthesis is its tacit

assumption of system stability. Absent such impediments, the price mechanism would

automatically return the economy to full employment with perfect coordination of all plans,

‘as if’ the Walrasian auctioneer or some other contrivance of costless recontracting had

matched them before any sales and purchases would take place.

As indicated by the above quotation from 1967, Leijonhufvud (1968) argued that much of the

innovative content of Keynes’s General Theory (1936) lay in eschewing any such heroic

assumptions and to emphasize the incompleteness of information and resulting failures in the

intertemporal coordination of activities in large, complex economic systems. In a range of

variations, he made this the principal theme of his own work for the decades to come – note

the titles of his later collections of essays: Information and Coordination (1981a) and

Macroeconomic Instability and Coordination (2000a).

‘Will the market system “automatically” coordinate economic activities? Always?

Never? Sometimes very well, but sometimes pretty badly? If the latter, under what

conditions, and with what institutional structures, will it do well or do badly? I

regard these questions as the central and basic ones in macroeconomics.’

(2000b: 45)

Spanning half a century, the continuity in Axel’s work on these big questions is remarkable.

Younger economists might habitually attribute this to cognitive inflexibility on his part, but –

as will be argued further below – the blame ought rather to be put on stagnation in the

evolution of macroeconomics.

The stickiness of wages and prices: a nonproblem

Even so, there is some change in Axel’s accentuation of the ‘Economics of Keynes’ that will be

of interest for his critique of the New Keynesians. In 1968, he believed that Keynes’s essential

contribution to macroeconomics could be characterized simply by turning the basic market

mechanism in the doctrines of Keynes’s teacher Marshall upside down:

5

‘In the Keynesian macrosystem the Marshallian ranking of price- and quantity-

adjustment speeds is reversed: In the shortest period flow quantities are freely

variable, but one or more prices are given, and the admissible range of variation

for the rest of the prices is thereby limited. The “revolutionary” element in the

General Theory can perhaps not be stated in simpler terms.’

(Leijonhufvud 1968: 52)

Referring to John Hicks’s concept of ‘false trading’ (1939: 128-29) and Bob Clower’s dual-

decision hypothesis (1965: 287-90), Axel emphasized that effective demand is co-determined

by the income effects ‘caused by the transactions which do not take place because of false prices’

(Leijonhufvud 1968: 55 – italics in the original). The transactions forgone tighten budget

constraints, leading to cutbacks in effective demand which generate feedback loops that

produce unemployment rather than preventing it, as the classical price mechanism would do.

Before long, however, Axel began to regret his emphasis on Keynes’s reversal of the

Marshallian ordering of adjustment speeds, because it had become a reference for Barro and

Grossman (1971) and others in their quest for a Neo-Keynesian Synthesis (Leijonhufvud 1998:

178, Backhouse and Boianovsky 2013: 60, 72). Their models of rationing equilibria in different

market constellations were based on the assumption of fixed prices, hence taking the rigidities

approach of the Neoclassical Synthesis to the extreme. Axel went in the opposite direction:

Referring to chapter 19 in Keynes’s General Theory, he argued that price flexibility might lead to

greater unemployment (rationing of labour supply), when interest rates fail in coordinating

intertemporal plans for consumption and production. The flexibility (volatility) of asset prices

in financial markets poses a threat to macroeconomic stability, while conventional rigidities of

wages and prices help to prevent aggregate demand and output from spiralling downwards.

In other words, financial markets clear even when interest rates diverge from their values

consistent with general equilibrium; price and wage responses to such interest-rate deviations

tend to push goods and labour markets out of equilibrium. In certain market constellations

price flexibility (in the generic sense) causes or exacerbates rationing rather than being its cure.

Axel described this as ‘the radical discovery of Keynes’ (Leijonhufvud 1998: 178):

‘[A]n excess supply in one market does not necessarily have a counterpart in an

excess demand elsewhere. Hence, the contractionary impulse in one part of the

system need not be offset by an expansionary stimulus elsewhere.’

Corridors and connections

In two companion pieces written in the 1970s, Axel elaborated on this key point of that special

Neo-Keynesian Synthesis, proposed by ‘the group known euphoniously as the

Leijonhufvudians’, which is ‘all chief and no injuns’ (Leijonhufvud 1981b: 195). The first piece

6

is on Effective Demand Failures (1973), the second on The Wicksell Connection: Variations on a

Theme (1981b). The first paper is well known for the concept of ‘Corridor Stability’, a key

element of the Leijonhufvudian Synthesis. The concept is based on Adam Smith’s and

Friedrich Hayek’s classical characterizations of the typical market economy as a complex

dynamical system with a large number of independently planning agents who coordinate their

plans in a variety of distinctive activities while having only dispersed local knowledge of the

markets. Axel set the focus on the limits of the system’s self-regulatory capacities, hence also

on the limits of the stabilizing properties of price flexibility:

‘The system is likely to behave differently for large than for moderate

displacements from the ‘full coordination’ time-path. Within some range from the

path (referred to as ‘the corridor’ for brevity), the system’s homeostatic

mechanisms work well, and deviation-counteracting tendencies increase in

strength. Outside that range, these tendencies become weaker as the system

becomes increasingly subject to ‘effective demand failures’... Inside the corridor,

multiplier-repercussions are weak and dominated by neoclassical market

adjustments; outside the corridor, they should be strong enough for effects of

shocks to the prevailing state to be endogenously amplified.’ (1973: 32-33)

In the early 1970s, when macroeconomics was divided in the camps of old-style Keynesians

and Monetarists, Axel used the corridor metaphor to suggest that the seemingly incompatible

perspectives of neoclassical optimism and Keynesian pessimism can be reconciled. The

boundaries of the corridor represented the borderline between the domains of ‘monetarist’

and ‘fiscalist’ policies, i.e. between rule-based stabilization of the price level (and ‘hands off

otherwise’) inside the corridor, and active demand management outside of it.

Four decades later, when the world economy had been hit by a global financial crisis, while

macroeconomics had converged on a New Neoclassical Synthesis with New Keynesian

flavour, Axel had shifted the emphasis from his quest for a synthesis to confrontational

reflections on the ‘economics of the crisis and the crisis of economics’ (Leijonhufvud 2014).

Critical developments in the real world prompted him to expand the corridor concept to a

broader range and deeper reaches of macroeconomic instabilities, such as stagflation, high

inflation, financial crises, and mismanaged transitions from central planning to market

economies (Leijonhufvud 2000a, Trautwein 2018). Critical choices of modelling strategies in

the academic world, more specifically in the ruling paradigms of macroeconomics, have

brought him to expose their fundamental inability to address the coordination problems

underlying these instabilities.

7

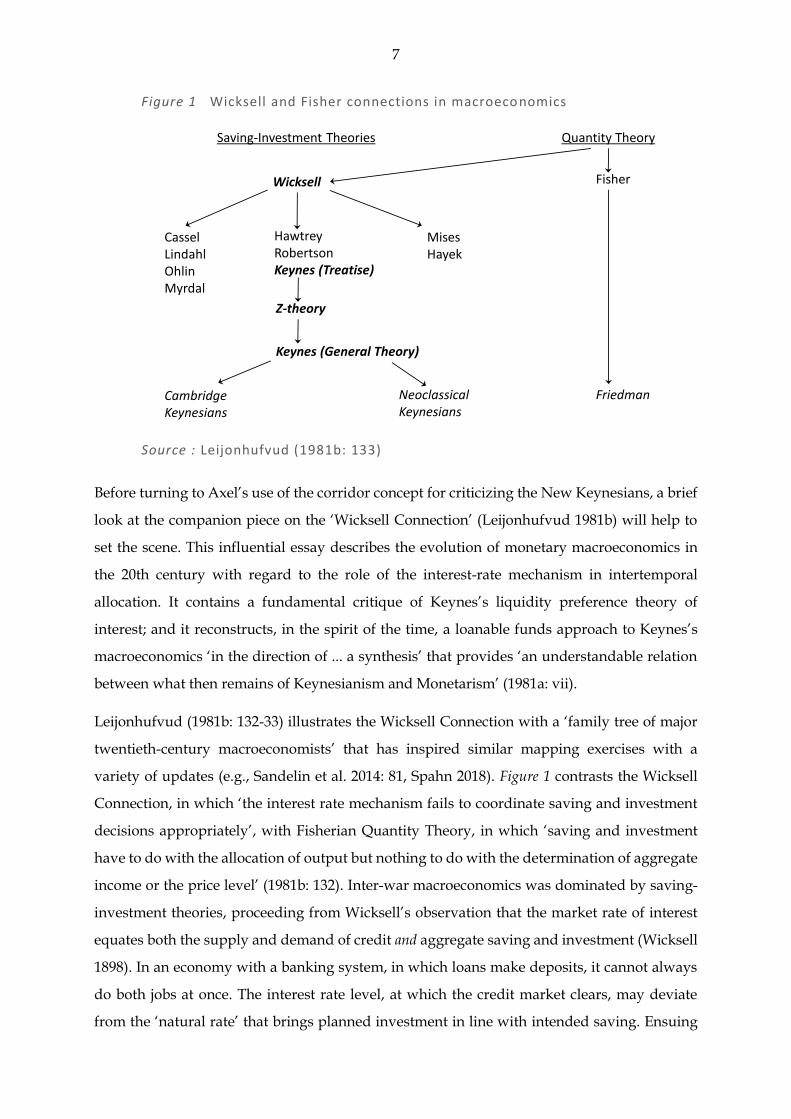

Figure 1 Wicksell and Fisher connections in macroeconomics

Source : Leijonhufvud (1981b: 133)

Before turning to Axel’s use of the corridor concept for criticizing the New Keynesians, a brief

look at the companion piece on the ‘Wicksell Connection’ (Leijonhufvud 1981b) will help to

set the scene. This influential essay describes the evolution of monetary macroeconomics in

the 20th century with regard to the role of the interest-rate mechanism in intertemporal

allocation. It contains a fundamental critique of Keynes’s liquidity preference theory of

interest; and it reconstructs, in the spirit of the time, a loanable funds approach to Keynes’s

macroeconomics ‘in the direction of ... a synthesis’ that provides ‘an understandable relation

between what then remains of Keynesianism and Monetarism’ (1981a: vii).

Leijonhufvud (1981b: 132-33) illustrates the Wicksell Connection with a ‘family tree of major

twentieth-century macroeconomists’ that has inspired similar mapping exercises with a

variety of updates (e.g., Sandelin et al. 2014: 81, Spahn 2018). Figure 1 contrasts the Wicksell

Connection, in which ‘the interest rate mechanism fails to coordinate saving and investment

decisions appropriately’, with Fisherian Quantity Theory, in which ‘saving and investment

have to do with the allocation of output but nothing to do with the determination of aggregate

income or the price level’ (1981b: 132). Inter-war macroeconomics was dominated by saving-

investment theories, proceeding from Wicksell’s observation that the market rate of interest

equates both the supply and demand of credit and aggregate saving and investment (Wicksell

1898). In an economy with a banking system, in which loans make deposits, it cannot always

do both jobs at once. The interest rate level, at which the credit market clears, may deviate

from the ‘natural rate’ that brings planned investment in line with intended saving. Ensuing

Saving-Investment Theories Quantity Theory

Wicksell Fisher

CasselLindahlOhlin Myrdal

HawtreyRobertsonKeynes (Treatise)

MisesHayek

Z-theory

Keynes (General Theory)

Cambridge Keynesians

NeoclassicalKeynesians

Friedman

8

saving-investment imbalances tend to create macroeconomic instability. Wicksell set the focus

on cumulative processes of inflation, whereas his followers in Stockholm, Cambridge and

Vienna developed a large variety of theories of cumulative changes in the levels and structures

of prices, production and income.

Axel pointed out that the Keynes of the Treatise (1930) belongs to this Wicksell Connection,

setting the focus on deflation, though not on quantity adjustments, while the Keynes of the

General Theory (1936) let deflationary pressure result in a (potentially persistent) contraction of

output and employment. However, as Axel critically remarked about this turn:

‘Keynes so obfuscated the interest rate mechanism that the later Keynesian

literature almost entirely lost track of Wicksell’s theme. The basic idea remains

central in the General Theory. (Its middle name was “Interest”, after all.) In

Keynes’s last variation, however, the theme comes in a guise that has proven the

almost perfect disguise. The failure to recognize its presence and role has proved

productive of much later misunderstanding and confusion.’

(Leijonhufvud 1981b: 134)

Already when working on his dissertation (1968: 28 and passim), Axel had noted that much of

the confusion had originated from Keynes’s insistence on aggregate saving being a ‘mere

residual’ (Keynes 1936: 64) of aggregate income adjustment to investment, irrespective of the

level of interest rates. The ‘almost perfect disguise’ of Wicksell’s theme is Keynes’s liquidity

preference theory of interest. Axel denounced it as a bootstrap theory: ‘theoretically unsound,

empirically false, and practically dangerous’ (Leijonhufvud 1981b: 171, 195). In its place, he

reconstructed a ‘Z-Theory’: an interpolation between the Treatise and the General Theory that

retains a key role for the interest-rate mechanism. It is another core element in the

Leijonhufvudian version of a Neo-Keynesian Synthesis, which differs substantially from both

Keynesian Economics and the GT-Economics of Keynes:

‘My views on the interest mechanism consist of a basic D. H. Robertson Loanable

Funds theory, complicated, when needed, by Keynesian bear/bull speculation (as

in the Treatise) and/or Fisherian inflation rate speculation.’ (1981b: 195)

Since capital goods are heterogeneous and entrepreneurs hold subjective expectations of

future demand, the ‘natural rate of interest’ will not be known to industrial and financial

investors ex ante (1981b: 197). Axel’s combination of Robertson, Keynes & Fisher gives ample

space to the ‘dark forces of time and ignorance’ to produce inconsistent beliefs about future

prospects. It provides a framework for analysing saving-investment imbalances that lead to

self-amplifying deviations from general equilibrium.

9

3 Axel in DSGE wonderland

Axel’s Z-Theory was not the only attempt to create a Neo-Keynesian alternative to the

Neoclassical Synthesis. As mentioned above with reference to Barro and Grossman (1971),

there were other approaches to restoring the message of Keynes’s General Theory that full

employment equilibrium is, at best, a special case. Yet the lines of thinking were so different

that it seems more appropriate to speak of Neo-Keynesian Syntheses, i.e. in plural. While

Clower and Leijonhufvud set the focus on disequilibrium states that result from coordination

failures of the price mechanism, Barro and Grossman – as well as Jean-Pascal Benassy, Jacques

Drèze, Edmond Malinvaud and other (predominantly European) economists – turned to ‘non-

Walrasian equilibrium modelling’ under the assumption of fixed prices (cf. De Vroey 2016: ch.

7). They were thus taking the rigidity approach of the Neoclassical Synthesis to the extreme.

New Keynesian Economics I and II

A similar divergence of approaches can be observed in the development of New Keynesian

Economics that came in two stages. At stage I, the term refers to ‘a somewhat loose cluster of

models’ (Leijonhufvud 2009: 750) which formed essentially in the 1980s and early 1990s, in

opposition to the New Classical paradigm that had evolved from Robert Lucas’s monetary

theory of the business cycle (MBC) and the Real Business Cycle (RBC) approach of Finn

Kydland and Edward Prescott. While the New Classicals insisted on what they considered as

standard Walrasian microfoundations, the New Keynesians made use of more modern

microeconomics for rigorous modelling of involuntary unemployment and other Keynesian

themes. Greenwald and Stiglitz (1987: 121-23) postulated that a general theory must account

for fluctuations and the persistence of unemployment, make use of careful distinctions

between saving and investment, and show that disturbances in demand underlie the cyclical

behaviour of macroeconomic aggregates. They claimed that this could be achieved by models

based of imperfect information (incomplete and/or asymmetric), containing such ingredients

as efficiency wages, capital market imperfections, credit rationing and a revised view of

monetary policy as an institutional arrangement to stabilize credit, not just the price level. The

stage I manifesto of Greenwald and Stiglitz was based on an outlook on the economics of

Keynes that had much in common with Axel’s approach. Yet, their agenda was soon relegated

to the periphery of New Keynesian Economics, mark I. The reference collection of Mankiw

and Romer (1991) neatly divided New Keynesian Economics in two different lines, with a first

volume on ‘Imperfect Competition and Sticky Prices’ and a second on ‘Coordination Failures

and Real Rigidities’. As the blurb reads:

10

‘Volume 1 focuses on how friction in price setting at the microeconomic level leads

to nominal rigidity at the macroeconomic level, and on the macroeconomic

consequences of imperfect competition, including aggregate demand externalities

and multipliers. Volume 2 addresses recent research on non-Walrasian features of

the labor, credit, and goods markets.’

The description of volume 2 looks like a rather vacuous reference to an assortment of partial

analyses, and it was the literature of volume 1 that set the stage for New Keynesian Economics,

mark II. The frictions line gradually converged with New Classical RBC theory. Ever since the

surveys of Goodfriend and King (1997) and Clarida, Galí and Gertler (1999) were published,

it has become customary to use the label ‘New Keynesian Economics’ (NKE) interchangeably

with ‘New Neoclassical Synthesis’ (NNS).

Axel has criticized the frictions line of NKE all along their way, although his focus in the 1980s

and 1990s was mostly on Lucasian New Classical Economics and Real Business Cycle theory,

the then reigning paradigms. While his comments on Keynesian economics in the old

Neoclassical Synthesis are easily accessible in systematic and comprehensive assessments, his

criticism of NKE is more dispersed in scattered remarks and short sections of pieces written

with other purposes (such as commenting on the state of the economy after the global financial

crisis, reviewing particular publications or outlining the evolution of macroeconomics in

longer perspective). Moreover, they contain only few specific references to the literature.4 In

order to map out Axel’s views on NKE and to assess the claims to progress made in the DSGE

world after the global financial crisis, it is therefore useful to identify and outline a New

Keynesian reference model to which Axel’s criticism can be systematically applied.

The New Keynesian reference model

Figure 2 presents an update on Leijonhufvud’s map of Wicksell and Fisher connections (Figure

1). It shows that the NKE-NNS consensus view even has an explicit Wicksell connection, as it

ends up with Michael Woodford’s canonical book on Interest and Prices (2003). Apart from

recycling the title of Knut Wicksell’s pathbreaking Geldzins und Güterpreise (Interest and Prices,

1898), Woodford has made explicit use of the Wicksellian concepts of a natural rate of interest,

a cashless economy and a feedback-rule for monetary policy that moves interest rates in

reaction to changes in the price level. Hence, he describes his version of NKE-NNS theory as

‘neo-Wicksellian framework’ (Woodford 2003: 49). It has been argued that Woodford’s

approach is fundamentally different from, if not incompatible with, Wicksell’s and Keynes’s

4 An exception is his comment on the New Keynesian model of unemployment presented by Galí, Smets and Wouters (2012) in Leijonhufvud (2011a and 2014: 769-72).

11

Figure 2 Wicksell and Fisher connections, update

Adapted from Sandelin, Trautwein and Wundrak (2014: 81)

concerns with investment-saving imbalances and concomitant macroeconomic instabilities

(Boianovsky and Trautwein 2006, Tamborini et al. 2014). It is, at any rate, perched on a branch

of the econ-theorizing decision tree quite distant from the offshoot represented by Axel’s Z-

theory. For this reason, and because Woodford’s (2003) framework has set a standard for

current DSGE modelling and claims to being an all-encompassing synthesis of 20th century

macroeconomics (Woodford 2009), it may serve as frame of reference for the following

summary of Axel’s critical comments on New Keynesian DSGE.5

5 Passing references to Woodford are made in Leijonhufvud (2007: 3 and 2009: 750).

12

The core model in Woodford (2003: 243-47) is a system of three equations that determine the

dynamics of output, inflation and the key interest rate.

The first equation is superficially similar to the IS equation of the old Neoclassical Synthesis,

but claimed to rest on rigorous microeconomic foundations. It is obtained by deriving the first

order condition for intertemporally optimal consumption and leisure of the representative

household. The IS relation describes a negative relation between output and interest rate

variables in terms of gaps, i.e. the gap between the actual rate of output and the ‘natural rate’

is set in relation with the gap between the ‘natural rate of interest’ and the actual rate which

might deviate from the former because of technology and policy shocks. The ‘natural rate of

output’ is taken from RBC theory, representing ‘a virtual equilibrium for the economy at each

point in time… that one would have if prices and wages were not in fact sticky’ (Woodford

2003: 9 – italics in the original). The natural rate of interest is ‘just the real rate of interest

required to keep aggregate demand equal at all times to the natural rate of output’ (2003: 248).

Assuming that the representative household holds (Muth-)rational expectations, the gap

between actual and potential output – and implicitly, by Okun’s law, also the rate of

unemployment – is thus determined by the expected values for future output and inflation (in

the calculation of the real interest rate), by contemporaneous shocks to the real rate of interest

and by shifts of the nominal rate of interest, the policy variable in the system.

The second equation is an aggregate supply function (AS) in terms of a New Keynesian

Phillips curve: Current inflation corresponds to the rationally expected future inflation plus

the current output gap, modified by a rigidity parameter. The firms act in monopolistic

competition and set their prices in a staggered fashion, conveniently modelled as the result of

a Calvo lottery. A significant fraction of the profit-maximizing firms will react to interest-rate

shocks by varying their output rather than prices. Price stickiness increases with the degree

of strategic complementarity between the price-setting of the suppliers of different goods. The

output effects of shocks can thus become large and persistent.

The third equation is a Taylor rule for monetary policy (MP). The central bank reacts to output

gaps and to deviations of current inflation from the inflation target by varying the nominal

rate of interest, its control instrument, in the same direction, yet possibly with different

intensity. The Taylor rule, which resembles a dynamic and expanded version of Wicksell’s

rule, closes the model by permitting the simultaneous determination of the nominal interest

rate, the inflation rate and the output gap. It leads to the policy conclusion that targeting zero

maximizes social welfare, since price level stability disarms the critical friction. It prevents

nominal rigidities in the firms’ price setting from taking effect. Woodford (2003: 238) argues

13

that ‘[i]n this way it is established that a nonmonetarist analysis of the effects of monetary

policy does not involve any theoretical inconsistency of departure from neoclassical

orthodoxy.’

Classicals and Moderns

Before turning to Axel’s critique of DSGE-based New Keynesianism, it is worthwhile to take a

look at another dual taxonomy of the evolution of economics, introduced in Mr Keynes and the

Moderns (Leijonhufvud 1998), at about the time when the New Neoclassical Synthesis was

emerging. Here, Axel contrasts the ‘British Classical School’ (naming Marx as a first example)

with ‘the Moderns’, characterizing Keynes as ‘the last of the great classical theorists’ and his

General Theory ‘properly understood [,] as a generalization of classical theory’ (1998: 170).

Considering that the Wicksell|Fisher Connections in the taxonomy of Figure 1 follow a vertical

timeline, the dividing line between the Classicals and the Moderns runs horizontally between

Keynes and those who came after him. Thus, the New Classical Economics of Figure 2 belong

to the Moderns in Axel’s taxonomy, but he concedes that many macroeconomists of the pre-

Lucasian did or do not unambiguously belong to the camp of the Moderns.6 The essential

differences between the two ‘traditions’ are captured by his table in Figure 3:

Figure 3 The two traditions

Source: Leijonhufvud (1998: 171)

6 Axel also argues in Leijonhufvud (1998) and elsewhere that the distinction between Classicals and Moderns overlaps with differences between Marshallian and Walrasian traditions in neoclassical economics. See De Vroey (2016: ch. 19) for some further discussion of the ‘Marshall-Walras Divide’.

14

The Classicals sought to uncover the laws of motion of the economy, in which the agents follow

specified aims, but do not necessarily succeed in achieving them. The behaviour of the agents

is described as adaptive, i.e. they learn in trial-and-error processes, conditioned by institutions

that ‘shape the fitness landscape in which agents move and they will not do equally well

independent of the rules that govern their interactions’ (1998: 170). Time matters, both in the

understanding of adaptive behaviour as a process in which the sequencing of decisions is

important, and in the understanding of the evolution of the institutions that condition the

agents’ behaviour.

The Moderns, by contrast, focus on ‘the logical principles of efficient allocation’ in which

behaviour is ‘optimizing ex ante’ (1998: 170). Since agents in the private sector, at least, form

rational expectations, they have all relevant information for maximizing utility or profit,

including the objective probability. The only information that would alter their behaviour is

the realization of shocks, which by definition could not be reliably predicted. In the perspective

of the Moderns, the existence of institutions requires extra justification, since they are not

considered as integral parts of market mechanisms. Many Moderns have a tendency to deny

that (some, not necessarily all) political institutions exist because they basically provide

solutions to coordination problems in markets and other arenas. Instead they see them as

potential troublemakers that create frictions in the price mechanism and distortions of

incentives for private-sector agents.

The last aspect, which has been discussed in greater depth in Axel’s paper on The Long Swings

of Economic Understanding (Leijonhufvud 2004a), refers primarily to the New Classical side of

the new synthesis. The New Keynesian message of Woodford’s DSGE model can be

interpreted in a more ‘Classical’ fashion by Axel’s standards: The main task of central banking

is described as ‘management of expectations’, in order to counteract ‘inefficiency in the real

allocation of resources’ which may result from a ‘general tendency of prices to move in the

same direction’ inherent in the market system (Woodford 2003: 15, 5). Yet, since New

Keynesian Economics has followed an intertemporal-optimization-cum-frictions approach,

the juxtaposition of Classicals and Moderns in Figure 3 helps nevertheless to prepare the

ground for Axel’s more specific criticism levelled at the New Keynesians.

The trouble with DSGE

Discussing ‘the state of macrotheory’ shortly after the outbreak of the global financial crisis,

Axel notes that the New Neoclassical Synthesis ‘has brought us back full circle to [the] notion

of the economy as a stable equilibrium system with frictions’ (Leijonhufvud 2011b: 2).

15

‘The Old Neoclassical Synthesis, which reduced Keynesian theory to a general

equilibrium model with ‘rigid’ wages, was an intellectual fraud the widespread

acceptance of which inhibited research on systemic instabilities for decades.

Insofar as the New Synthesis represents a return to this way of thinking about

macroproblems it risks the same verdict.’ (2009: 750)

Axel is certainly willing to concede that macroeconomics has made technical progress since

the times of the old Neoclassical Synthesis (see, e.g., 1998: 181-82, 2011a: 1, 2011b: 2, 8). Yet, as

he is reported to have quipped (here in Roger Farmer’s paraphrase): Living near Hollywood

has made him realize ‘that the developments in modern macro-economics are much like those

in the movies – modern plots are sadly lacking but the special effects are truly spectacular’

(Farmer 2008: xii). It should be noted, though, that there is crucial difference between

Hollywood and modern macro: The film industry tends to conceal the tricks that produce the

special effects, whereas macroeconomists are proud of making them explicit as ‘rigorous

microtheoretical foundations’. It is to several of those tricks that Axel reacts negatively.

The IS relation is the prime target of Axel’s attacks, because it describes the intertemporal

coordination of economic activity as the successful outcome of the optimizing choice of a

representative household that holds rational expectations. This makes it impossible to analyse

the coordination problems that cause financial crises, mass unemployment and other

explananda of macroeconomic theory (Colander et al. 2008: 236, Leijonhufvud 2014: 770-72).

Savings-investment imbalances cannot be addressed in this framework.

‘DSGE models are… peculiarly prone to fallacies of composition, most particularly

so, of course, in their representative agent versions. The models are blind to the

consequences of too many people trying to do the same thing at the same time.

The representative lemming is not an intertemporal optimising creature.’

(2009: 753)

Even if some heterogeneity is introduced to allow, for instance, for critical intermediation of

credit through a banking sector (as will be discussed in the following section), the route to

analysing macroeconomic instabilities remains blocked by further special requirements that

the dynamic-stochastic-general-equilibrium character of the DSGE technology imposes on the

private-sector agents in the model.

Already in his distinction between the Classicals and the Moderns, Axel had pointed out the

high demands on cognitive competence for intertemporal optimization:

‘The logic of optimizing choice is essentially timeless. It does, however, require all

the utility-relevant consequences of alternative decisions to be taken into account.

16

When the step from an atemporal to a temporal context is taken, this comes to

mean all possible alternative futures for all time.’ (1998: 182)

More specifically, under the rational expectations assumption, New Keynesian Economics

treats ‘the evolution of an economy as if it were a fully determined (albeit stochastic) process

accurately foreseen by all inhabitants’ (2014:773).

‘[T]he future actually realised is always a random draw from the universally

believed and true Gaussian distribution of possible futures. This assumption

makes the economy a closed system. Agents are supposed to possess

(probabilistic) knowledge of an objective reality – a reality that they have been able

to learn. The Gaussian lottery might produce a gain or a loss. But the quality of the

individual investor’s information about the state of the market and his ability to

draw the proper inferences from it have no bearing on the outcome of the lottery’

(2011b: 3)

Yet, even the assumption of rational expectations is not sufficient to make intertemporal

optimization fully consistent. A standard requirement of DSGE models (as any intertemporal

Walrasian models) is that budget constraints are binding all the time over an infinite time

horizon. For satisfying the requirement of optimality, moreover, the transversality condition

must hold: No capital is left over at the end (whatever that means in infinity).

‘[T]rusting in the transversality condition is surely nothing but pure and utter

superstition. This figment of economic imagination simply has no counterpart in

the world of experience. Every bubble that ever burst is proof of this fact. It should

be removed from our models. From the standpoint of the DSGE tradition, the

consequences would of course be drastic. If you remove the capstone from a

Roman arch, everything crumbles. Remove the transversality condition from

DSGE models and everything unravels. Without it, there is nothing to guarantee

that individual intertemporal plans are consistent with one another. The system

lacking an empirical counterpart to the mathematical economist’s transversality

condition is likely to experience periodic credit crises. Such crises reveal

widespread, interlocking violations of intertemporal budget constraints.’

(2014: 772)

In the New Keynesian twist of DSGE modelling intertemporal optimization does not,

however, directly coincide with the social optimum in terms of potential output. The IS

relation sets the focus on ‘intertemporally optimal’ gaps between actual and potential output.

The latter is defined as the monopolistic competition flex-price analogy of the Ramsey-Prescott

optimal growth path of RBC theory. Output gaps are derived from frictions in the price

mechanism that are introduced with the rigidity parameter in the AS relation, also known as

New Keynesian Phillips curve. Axel is hardly more enthusiastic about that concept than he

17

was about the use of the Phillips curve in the context of the old Neoclassical Synthesis. In the

1960s, when wage and price inflation began to occur and wage-rigidity based IS-LM analysis

could not handle it, the Phillips curve was simply pasted on ad hoc. It became ‘the Achilles heel

of the IS-LM brand of Keynesian economics’ (2011b: 1) because it allowed Milton Friedman

(1968) to restate the Quantity Theory of Money in differences and to introduce the concept of

a natural rate of unemployment. This in turn paved the way for New Classical

Macroeconomics and its concept of continuous intertemporal equilibrium (2009: 749).

Axel’s objections to the frictions-approach in the New Keynesian Phillips curve are twofold.

In regard to theoretical substance, it suffers from a lack of macrofoundations:

‘Economists talk freely about “inflexible” or “rigid” prices all the time, despite the

fact that we do not have a shred of theory that could provide criteria for judging

whether a particular price is more or less flexible than appropriate to the proper

functioning of the larger system.’ (2009: 750)

In regard to empirical relevance, Axel doubts that ‘a little stickiness’ of the kind introduced by

the Calvo lottery device plus some strategic complementarity, ‘could account for the

behaviour of real rates and the real distortions in all the years since the recovery from the

dotcom crash’ (2009: 749 n. 2).

’[A] single “rigidity” does not take us very far in making the models “fit” the data.

So we now have large-scale DSGE models with more than a dozen “frictions” and

“market imperfections” with more to be added, you can be sure, when the models

do not fit outside the original sample.’ (2014: 761-62)

With such ad-hocery, the links to the ‘rigorously microfounded’ core model of the NNS are

certainly loosened beyond what used to be permitted by the modelling conventions in the

Moderns tradition.

When it comes to monetary policy in terms of the Taylor-rule reaction function of the central

bank (MP), Axel has many things to say, whereof only two will be mentioned here. The first is

that the real rate of interest, on which the IS and MP equations in the representative model

interact, is a constructed variable without correspondence to reality:

’What does exist is the money rate of interest from which one may construct a

distribution of perceived “real” interest rates given some distribution over agents

of inflation expectations. Intertemporal non-monetary general equilibrium (or

finance) models deal in variables that have no real world counterparts.’ (2009: 749)

Woodford’s cashless DSGE economy is such a model, and it evades the issue by assuming

identical inflation expectations across the economy. Since it excludes heterogeneity among the

18

households, distributional neutrality of inflation targeting is automatically ensured. Axel

points out that this will no longer apply in situations ‘when monetary policy comes to involve

choices of inflating or deflating, of favouring debtors or creditors, of selectively bailing out

some and not others, of guaranteeing some private sector liabilities and not others, of allowing

or preventing banks to collude’ (2009: 748-749).

This is, of course, a comment on the situation in 2008/09 when the global financial crisis made

the distributive consequences of monetary policy, conventional or unconventional, evident.

Some years before the outbreak of the crisis Axel had already suspected that ‘modern

macroeconomics leaves too little room for the extremes of instability’ (2004: 821). The pre-crisis

consensus view of NKE-NNS did in no way permit to describe the core of the crisis as what

Axel (along with many others) perceives it to be: a balance sheet recession in the banking sector

that followed from excessive leverage, maturity mismatch and increased interconnectivity. In

order to make room for it in his own framework, Axel has refined his original corridor concept

(Leijonhufvud 2011b: 6-7, 2014: 766-68). He now identifies three zones or regions of the state-

space representation of the private sector in the economy:

Region 1: Self-stabilization of the market system inside the corridor; the price mechanisms

work to the extent that ‘negative feedback controls dominate in all markets and “stabilisation

policies” in the conventional sense are not useful’ (2011b: 6).

Region 2: Destabilization outside the corridor, but the deviation-amplifying mechanism of

(positive) feedbacks is bounded in ‘business cycles’ such that conventional macroeconomic

policies can ensure market liquidity and stabilize aggregate demand.

Region 3: Destabilization with unbounded interaction of positive feedback loops, ‘dangerous

instabilities, such as default avalanches… [t]he worst outcome in this region of dangerous

instability’ being ‘the “black hole” of a Fisherian debt-deflation catastrophe’ (2014: 767); such

situations require strong, fast and unconventional measures for stabilization of the economy,

but Axel warns that not all kinds of unconventional policies will get it right (2009: 753, 2014:

772).

DSGE modelling of the New Keynesian kind can, at the most, deal with certain cases in Region

2. Even if more recent versions can accommodate multiple equilibria, some of which are

unstable, it is not equipped to deal with instabilities type Region 3. In thinking about this, the

refinement of the corridor concept is not the only piece of theory in which Axel finds himself

returning to his earlier work. The financial crisis has also urged him to think about wider

consequences of the admission of false trading, the pinpoint on which his original

19

reinterpretation of Keynes had started turning. False trading makes budget constraints diverge

from their hypothetical path in continuous general equilibrium; or, to put it in an Edgeworth-

Bowley box:

‘The disequilibrium trade shifts the initial endowment. In a financial crisis, this

problem becomes infinitely worse. Not only do defaults shift the endowments

about, but they keep changing the dimensions of the box. Furthermore, a great

many agents will suffer Knightian uncertainty about what their endowments may

be and what they may end up being. The probability that the system would settle

in any one of its multiple initial equilibria is basically zero.’ (2014: 771)

This leads Axel to the conclusion that DSGE modelling has shown itself ‘an intellectually

bankrupt enterprise’ (2008: 6), ‘hopelessly inadequate for dealing with financial crises and

their aftermaths.’

‘Certainly, the claims that these models have “sound microtheoretical

foundations” and are “particularly suitable for forecasting and policy analysis” are

without merit. It is particularly unfortunate at this time that so many central banks

have sunk so much intellectual capital in the DSGE enterprise.’ (2011a: 6)

4 What progress on coordination failures in the DSGE world?

Axel was by no means alone to criticize the New Neoclassical Synthesis after the outbreak of

the financial crisis. With the strong and widely acclaimed indictments of bankruptcy and

squandering of intellectual capital, DSGE macroeconomics ought to be a dead horse by now.

But not so: DSGE is considered to be the workhorse technology even ten years after.

[from here on just preliminary notes; manuscript to be completed before the conference]

• DSGE-based literature proliferating in many directions and at high levels of

complexity & technical sophistication – including:

o investment and capital accumulation

o unemployment

o financial intermediaries and banking crises

o transnational propagation of asymmetric market developments

o endogenous business cycles (Post Keynesian DSGE!)

• introduction of heterogeneity and a wider array of shocks and frictions,

based on new models for standard reference, such as Smets & Wouters (2007)

20

• DSGE models not merely standard in academic literature, but continues also

to be used by central banks, IMF, EU Commission, OECD etc. as „core policy

[evaluation] tool“ (Lindé, Smets & Wouters 2016) – in the following with a

focus on financial frictions

agent heterogeneity required

introduction of financial markets and intermediaries (generally: banks)

requires partial abandoning of representative agent framework:

borrowers and lenders to be distinguished by rates of time preference, risk

preferences etc.

progressive extensions

1) Cúrdia & Woodford (2008) …

households: two types with different impatience to consume

= savers/borrowers financial intermediation by banks time-varying

spread between deposit and lending rates of interest = wedge w r t policy rate

= additional friction, nested in standard DSGENKE 2003

2) Boissay, Collard & Smets (2014); Christiano, Motto & Rostagno (2014) …

households are lenders, firms borrowers, banks financial intermediaries

external finance premium, w r t balance sheet & leverage of borrower

= wedge w r t policy rate; partly additional friction, partly specific extension

3) Brzoza-Brzezina, Kolasa & Makarski (2013) …

households with different rates of time preference: savers/borrowers

financial intermediation by banks collateral constraint, quantitative

friction restricting output, acting on balance sheets and leverage of both

borrowers and banks

4) Gertler & Kiyotaki (2010); Goodhart, Kashyap, Tsomoco & Vardiakis (2012)…

like 2) with external finance premium, but now affecting balance sheet &

leverage of both borrowers and (merely intermediating) banks

financial accelerator working as wedge w r t policy rate

5) Jakab & Kumhof (2015) …

like 4), but now with banks that finance loans by money creation

large jumps in lending & monetary aggregates, procyclical bank leverage,

with deleveraging and credit rationing in downturns

21

Banking crises

1) Angeloni & Faia (2013) …

representative household (with transversality constraint!), representative

bank, producing firms (with NK-PC); productivity and monetary shocks

increase bank leverage & risk, cause occasional bank runs and restrictions of

output

2) Boissay, Collard & Smets (2014) …

“textbook DSGE model that features a non-trivial banking sector“

heterogeneous banks interbank market, beset with problems of asymmetric

information and moral hazard credit booms followed by financial

recessions, more severe & persistent than other recessions (competitive firms:

no NK-PC)

Policy coordination

1) Angeloni & Faia (2013); Lindé, Smets & Wouters (2016) …

using DSGE models to discuss global financial crisis as failure in coordination

of monetary policy and macroprudential financial regulation

2) Googling ‚Coordination in DSGE‘ gives only papers on coordination of policies,

mainly monetary policy with financial regulation or fiscal policy

Post-Keynesian (!) DSGE alias Endogenous Business Cycles (Roger E.A. Farmer 2014,

2017)

1) replacing infinitely lived representative household with overlapping

generations no completeness of markets, since most of the traders did not

live when they were opened basic friction: grim reaper

2) OLG model introduces uncertainty about behaviour of future generations:

animal spirits become fundamental in the system, on which to form rational

expectations multiple equilibria sunspot model of endogenous BC

3) labour market modelled with Keynesian search theory: beliefs about future

value of stock market (animal spirits) determine AS and AD

restriction of job matching between unemployment and vacancies

22

5 Taking stock

Has New Keynesian Economics managed to overcome Axel’s objections? If so, to which

extent?

First impression

Yes!

• Impressive progress in describing coordination by financial intermediation

(including money creation) and coordination failures, at least in dealing with

banks and financial crises

• … and thereby introducing heterogeneity that seems to allow for I-S

imbalances

• … but: bewildering complexity! Apparent trade-offs between rigour, realism

and communicative plausibility

Strategies for progressing from DSGENKE 2003

• Repairs – may save the logic, but do not always lead to more convincing

characterizations (e.g., consumer credit in Cúrdia & Woodford 2008)

• Adding frictions – to frictions (as in Smets & Wouters 2007) may improve

the empirical fit, but is rarely more than theoretical ad-hocery

• Extension-building – by single focus on specific friction, may be more rigorous,

but tends to take the G out of DSGE, requiring a lot of ceteris paribus

• All-embracing language – (as in Farmer‘s Post Keynesian DSGE) tends to make

key concepts of macroeconomic theorizing rather vacuous

Optimistic critique and skeptical question

• Blanchard (2008, 2018): Current DSGE models seriously flawed by unappealing

assumptions, dubious methods of estimation, unconvincing normative

implications, bad communication devices… but all of it improvable

• Small final question: how can banking crises leave ‚rationally expected‘

intertemporal budget constraints of households unaffected? Transversality

condition explicitly stated in Angeloni & Faia (2013), probably ‘deeply

embedded‘ (implicit) in other models… what if not? When will we hear the

23

capstone falling and the arch crumbling?

[to be completed before the conference]

References

Backhouse, Roger and Mauro Boianovsky (2014), Transforming Modern Macroeconomics:

Exploring Disequilibrium Microfoundations, 1956–2003. Cambridge: Cambridge University

Press.

Barro, Robert and Herschel Grossman (1971), A general disequilibrium model of income and

employment, American Economic Review 61(1): 82-93.

Boianovsky, Mauro and Hans-Michael Trautwein (2006), Wicksell after Woodford, Journal of

the History of Economic Thought 28 (2): 171-185.

Clarida, Richard, Jordi Galí and Mark Gertler (1999), The Science of Monetary Policy: A New

Keynesian Perspective, Journal of Economic Literature 37 (4), 1661-1707.

Clower, Robert (1965), The Keynesian Counter-Revolution: A Theoretical Appraisal, in The

Theory of Interest Rates, ed. by Hahn, Frank and Frank P.R. Brechling, 103-125.

Colander, David, Peter Howitt, Alan Kirman, Axel Leijonhufvud and Perry Mehrling (2008),

Beyond DSGE Models: Towards an Empirically Based Macroeconomics, American Economic

Review 98(2): 236-240.

De Vroey, Michel (2016), A History of Macroeconomics from Keynes to Lucas and Beyond.

Cambridge: Cambridge University Press.

Farmer, Roger E.A. (ed., 2008), Macroeconomics in the Small and the Large. Essays on

Microfoundations, Macroeconomic Applications and History in Honor of Axel Leijonhufvud,

Cheltenham: Edward Elgar.

Farmer, Roger E.A. (2017), Post Keynesian Dynamic Stochastic General Equilibrium Theory,

European Journal of Economics and Economic Policies: Intervention 14: 2, 173–185.

Fisher, Irving (1933), The debt-deflation theory of the Great Depression, Econometrica 1 (4),

337–357.

Friedman, Milton (1968), The Role of Monetary Policy, American Economic Review 58 (1): 1-17.

Galí, Jordi, Frank Smets and Raf Wouters (2012), Unemployment in an Estimated New

Keynesian Model, NBER Macroeconomics Annual 26 (1): 329-360.

Goodfriend, Marvin and Robert King (1997), The New Neoclassical Synthesis and the Role of

Monetary Policy, NBER Macroeconomics Annual 1997 12, 231-296.

Greenwald, Bruce and Joseph Stiglitz (1987), Keynesian, New Classical and New Keynesian

Economics. Oxford Economic Papers 39 (1), 119–133.

Hansen, Alvin (1949), Monetary Theory and Fiscal Policy, New York: McGraw Hill.

Hicks, John R. (1937), Mr Keynes and the “Classics”; A Suggested Interpretation, Econometrica

5 (2), 147-159.

24

Hicks, John R. (1939), Value and Capital, Oxford: Clarendon Press.

Jayadev, Arjun and Josh Mason (2015), [Transcript of] Interview with Axel Leijonhufvud, URL:

https://www.ineteconomics.org/uploads/transcripts/Transcript-Leijonhufvud-Inter-

view.pdf

Keynes, John Maynard (1930), A Treatise on Money (2 vols.), London: Macmillan.

Keynes, John Maynard (1936), The General Theory of Employment, Interest and Money. London:

Macmillan.

Leijonhufvud, Axel (1967), Keynes and the Keynesians: A Suggested Interpretation, American

Economic Review 57 (2), 401-10.

Leijonhufvud, Axel (1968), On Keynesian Economics and the Economics of Keynes. A Study in

Monetary Theory, New York: Oxford University Press.

Leijonhufvud, Axel (1973), Effective Demand Failures, Swedish Journal of Economics 75 (1), 27-

48.

Leijonhufvud, Axel (1981a), Information and Coordination. Essays in Macroeconomic Theory, New

York: Oxford University Press.

Leijonhufvud, Axel (1981b), The Wicksell Connection: Variations on a Theme, in Leijonhufvud

(1981a), 131-202.

Leijonhufvud, Axel (1998), Mr Keynes and the Moderns, European Journal of the History of

Economic Thought 5(1): 169-88.

Leijonhufvud, Axel (2000a), Macroeconomic Instability and Coordination. Selected Essays of Axel

Leijonhufvud, Cheltenham: Edward Elgar.

Leijonhufvud, Axel (2000b), Keynesian Economics: past confusions, future prospects, in

Leijonhufvud (2000a), 33-51.

Leijonhufvud, Axel (2004a), The long swings of economic understanding, in Kumaraswamy

Velupillai (ed.), Macroeconomic Theory and Economic Policy: Essays in Honour of Jean-Paul

Fitoussi, London: Routledge, 115-127.

Leijonhufvud, Axel (2004b), Celebrating Ned, Journal of Economic Literature 42 (3): 811-821.

Leijonhufvud, Axel (2006), The Uses of the Past (Invited Lecture at the annual conference of the

European Society for the History of Economic Thought – ESHET, Porto), URL:

https://core.ac.uk/download/pdf/11829511.pdf

Leijonhufvud, Axel (2007), Monetary and Financial Stability, CEPR Policy Insight no. 14

(October 2007), London: Centre for Economic Policy Research.

Leijonhufvud, Axel (2008), Keynes and the Crisis, CEPR Policy Insight no. 23 (May 2008),

London: Centre for Economic Policy Research.

Leijonhufvud, Axel (2009), Out of the corridor: Keynes and the crisis, Cambridge Journal of

Economics 33 (4), 741-757.

Leijonhufvud, Axel (2011a), Axel in Wonderland: DSGE, URL: www-ceel.economia.unitn.it/

staff/leijonhufvud/files/dsge.pdf.

Leijonhufvud, Axel (2011b), The Nature of an Economy, CEPR Policy Insight no. 53 (February

2011), London: Centre for Economic Policy Research.

25

Leijonhufvud, Axel (2014), Economics of the crisis and the crisis of economics, European Journal

of the History of Economic Thought 21 (5), 760-774.

Mankiw, Gregory and David Romer (1991), New Keynesian Economics, vol. 1: Imperfect

Competition and Sticky Prices, vol. 2: Coordination Failures and Real Rigidities. Cambridge, MA:

MIT Press.

Modigliani, Franco (1944), Liquidity Preference and the Theory of Interest and Money,

Econometrica 12 (1): 45-88.

Sandelin, Bo, Hans-Michael Trautwein and Richard Wundrak (2014), A Short History of

Economic Thought (3rd ed.), London: Routledge.

Snowdon, Brian (2004), Outside the Mainstream: An Interview with Axel Leijonhufvud’.

Macroeconomic Dynamics 8 (1), 117-145.

Spahn, Heinz Peter (2018), [Entry on] New Keynesian Economics, forthcoming in: The Elgar

Companion to John Maynard Keynes, ed. by Dimand, Robert and Harald Hagemann,

Cheltenham: Edward Elgar, 2018.

Tamborini, Roberto, Hans-Michael Trautwein and Ronny Mazzocchi (2014), Wicksell, Keynes,

and the New Neoclassical Synthesis: What Can We Learn for Monetary Policy?, Economic

Notes 43 (2): 79-114.

Trautwein, Hans-Michael (2018), [Entry on] Axel Leijonhufvud, forthcoming in: The Elgar

Companion to John Maynard Keynes, ed. by Dimand, Robert and Harald Hagemann,

Cheltenham: Edward Elgar, 2018.

Wicksell, Knut (1898), Geldzins und Güterpreise. Eine Studie über die den Tauschwert des Geldes

bestimmenden Ursachen, Jena: Gustav Fischer; tr. 1936: Interest and Prices. A Study of the Causes

Regulating the Value of Money, London: Macmillan.

Woodford, Michael (2003), Interest and Prices. Foundations of a Theory of Monetary Policy.

Princeton: Princeton University Press.