lecture21 hyperinflations monetarypolicy - sscc - homenwilliam/econ702_files/lect21-17.pdf ·...

TRANSCRIPT

Lecture 21HyperinflationsMonetary Policy

Noah Williams

University of Wisconsin - Madison

Economics 312/702

Williams Economics 312/702

Monetary Policy

Conduct of monetary policy may have dramaticimplications for economic outcomes.Main example in US: The “Great Inflation” of the 1970s.Sustained double digit annual inflation rates, accompaniedby slow economic growth and recession.Problems on much larger scales internationally.Hyperinflations in Latin America in 1980s had annualinflation rates in hundreds to thousands of percents.Bolivia: 1281% (1984), 11,750% (1985), 276% (1986).Argentina and Brazil in hundreds of percents.Other hyperinflation examples: Hungary 1946, Zimbabwe2006-2009.

Williams Economics 312/702

Argentina: Inflation and Real Money

1970 1975 1980 1985 1990 1995 2000 2005−1

0

1

2Lo

g va

lue

of m

onth

ly g

ross

infla

tion

rate

1970 1975 1980 1985 1990 1995 2000 20054

5

6

7

Log

valu

e of

rea

l (ba

se−

mon

ey)

bala

nces

Inflation

Real balances

Williams Economics 312/702

Brazil: Inflation and Real Money

1980 1985 1990 1995 2000 2005−1

0

1Lo

g va

lue

of g

ross

infla

tion

rate

1980 1985 1990 1995 2000 20054

6

8

Log

valu

e of

rea

l (ba

se−

mon

ey)

bala

nces

Inflation

Real balances

Williams Economics 312/702

Highest Monthly Inflation Rates in History

Country Month Monthly rate Daily Doubling TimeHungary July 1946 4.19× 1016% 207% 15 hoursZimbabwe Nov. 2008 7.96× 1010% 98 % 24.7 hoursYugoslavia Jan. 1994 3.13× 108% 64.6% 1.4 daysGermany Oct. 1923 29,500 % 20.9% 3.7 daysGreece Oct. 1944 13,800% 17.9 % 4.3 daysChina May 1949 2,178 % 11 % 6.7 days

Williams Economics 312/702

German Hyperinflation

Williams Economics 312/702

Zimbabwe Hyperinflation

Williams Economics 312/702

Zimbabwe Hyperinflation

Most recent hyperinflation episode was Zimbabwe.Official inflation rates: 2001-2004: 120-500%. 2005:585.84%, 2006: 1,281.11% , 2007: 66,212.3% 2008:231,150,888.87%. Even higher during late 2008Problem began with land reforms (land confiscation),leading to collapse in output.In early 2006, government printed ZW$21 trillion to pay ofIMF loans. In May 2006, printed additional $60 trillion tofund police, military salaries. Value of currency began tocollapse.New currencies in 2006, 2007, 2008. Chop off zeros.From January to December 2008, the money supply growthrose from 81,143% to 658 billion percent.

Williams Economics 312/702

Zimbabwe CurrencyAugust 2006: New dollar = 1000 old dollarsNew ZW $1000 = $1.50 US

Williams Economics 312/702

Zimbabwe Currency

Jan 1. 2008: ZW$10 million = $1.66 US

Williams Economics 312/702

Zimbabwe Currency

Jul 1. 2008: ZW$100 billion = $0.13 US

Williams Economics 312/702

Zimbabwe Currency

Aug. 1, 2008: New currency ZW$10 billion = ZWR$1New ZWR $100 trillion = ZW$1014 = ZW$1027 pre-2006New ZWR $100 trillion = $300 US on 1/1/09, $30 US on 1/16Now selling on eBay as collector’s item.

Williams Economics 312/702

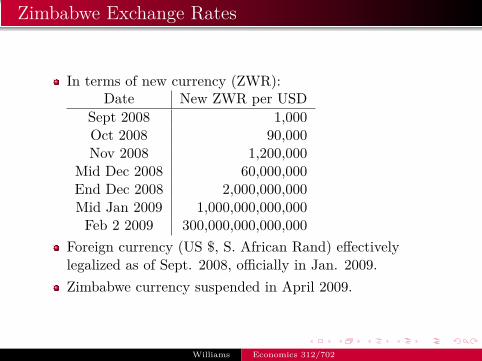

Zimbabwe Exchange Rates

In terms of new currency (ZWR):Date New ZWR per USD

Sept 2008 1,000Oct 2008 90,000Nov 2008 1,200,000

Mid Dec 2008 60,000,000End Dec 2008 2,000,000,000Mid Jan 2009 1,000,000,000,000Feb 2 2009 300,000,000,000,000

Foreign currency (US $, S. African Rand) effectivelylegalized as of Sept. 2008, officially in Jan. 2009.Zimbabwe currency suspended in April 2009.

Williams Economics 312/702

Zimbabwe Exchange Rates

In terms of original currency

Williams Economics 312/702

Inflation and Seignorage

Hyperinflations largely an issue of government finance.Seignorage: government revenue from creation of money.Consider money demand where inflation equal to expected,real interest rate and output constant:

MP = L(r + π, Y )

where π = M/M growth of money=inflation rate.Seignorage S given by real increase in money:

S = MP = MM

MP = πMP

Seignorage is the inflation tax: revenue = tax rate (π)times base M/P.

Williams Economics 312/702

Laffer Curve

Substituting back money demand:

S = πL(r + π, Y )

How does seignorage revenue depend on inflation rate?

Sπ = L(r + π, Y ) + πLR(r + π, Y )

L > 0 but LR < 0. For small π first term dominates, andSπ > 0. For large π, Sπ < 0. Hence get a Laffer curveCagan (1956) studied hyperinflations, used a particularfunctional form:

log MP = a − bR + logY

hence Sπ = (1− bπ) exp(−bπ). Maximal level S∗.

Williams Economics 312/702

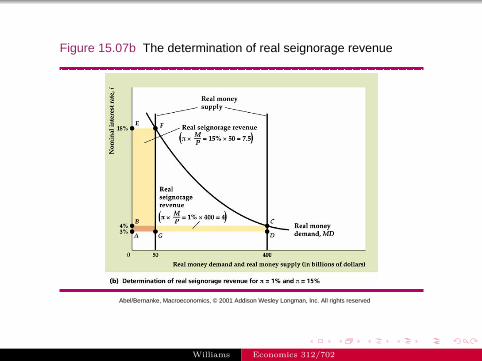

Abel/Bernanke, Macroeconomics, © 2001 Addison Wesley Longman, Inc. All rights reserved

Figure 15.07a The determination of real seignorage revenue

Williams Economics 312/702

Abel/Bernanke, Macroeconomics, © 2001 Addison Wesley Longman, Inc. All rights reserved

Figure 15.07b The determination of real seignorage revenue

Williams Economics 312/702

Abel/Bernanke, Macroeconomics, © 2001 Addison Wesley Longman, Inc. All rights reserved

Figure 15.08 The relation of real seignorage revenue to the rate of inflation

Williams Economics 312/702

Laffer CurveEven moderate seignorage needs can lead to high inflation.

0 100 200 300 400 500 600 700 800 900 10000

1

2

3

4

5

6

7

8

9

10Laffer Curve

Inflation Rate in Percent

Sei

gnor

age

Rev

enue

in P

erce

nt o

f GD

P

Williams Economics 312/702

Seignorage Revenue: Argentina

1970 1975 1980 1985 1990 1995 2000 2005−0.05

0

0.05

0.1

0.15

0.2

0.25

0.3Seigniorage: ratio of Diff money to nominal gdp

Williams Economics 312/702

Seignorage Revenue: Brazil

1975 1980 1985 1990 1995 2000 2005−0.01

0

0.01

0.02

0.03

0.04

0.05Seigniorage: ratio of Diff money to nominal gdp

Williams Economics 312/702

Seignorage and Hyperinflation

If seignorage revenue maximized at hundreds of percents(or lower), why have we seen even higher inflation rates?Cagan’s answer: gradual adjustment of expected inflationand money holdings. Assume r and Y are constant sodesired real money holdings are:

m = exp(a − b(r + π))Y = B exp(−bπ)

Suppose actual real money holdings m adjusts towarddesired:

mm = φ [log m(t)− logm(t)]

= β [logB − bπ(t)− logm(t)]

This is a partial adjustment model, perhaps due toadaptive expectations, where φ governs the speed ofadjustment

Williams Economics 312/702

Hyperinflations

No longer have inflation equal to expected inflation.

m = MP −

MP2 P = M

PMM − M

PPP

⇒ mm = M

M − π

S = MP = M

PMM = m M

M

So π = S/m − mm substitute in and solve:

mm = φ

[logB − b( S

m −mm )− logm(t)

]= φ

1− bφ

[logB − b S(t)

m(t) − logm(t)]

Williams Economics 312/702

Dynamics of Money and Inflation

The evolution of real money is:

mm = φ

1− bφ

[logB − b S(t)

m(t) − logm(t)]

As long as S < S∗ there are two steady states m:

mm = 0⇒ m = B exp(−b S

m ), π = Sm

If in a lower m steady state where S < S∗ but then a shockto money demand hits, will converge to the higher m steadystate. That is, the high m, low π steady state is stable.

Williams Economics 312/702

Dynamics of Hyperinflation

−5 −4.5 −4 −3.5 −3 −2.5 −2 −1.5 −1 −0.5 0−2.5

−2

−1.5

−1

−0.5

0

0.5

Log Real Money Holdings

Cha

nge

in L

og R

eal M

oney

Hol

ding

s

S=.08S=.12

Increasein required seignorage may lead to hyperinflation.

Williams Economics 312/702

Hyperinflation

Suppose economy initially in a steady state where requiredseignorage is less than S∗. But then required S increases tomore than S∗. If there were immediate adjustment, thisequilibrium would not be sustainable. But with partialadjustment, this implies ever accelerating inflation andmoney growth and declining real balances.In Germany after WWI, inflation reached 322% per month,but Cagan estimated the inflation rate that maximizesseignorage at only 20% per month.

Williams Economics 312/702

The Federal Reserve System

Monetary policy in US administered by the FederalReserve. Leadership of the Fed is provided by the Board ofGovernors in Washington, D.C.7 governors, appointed by the President, and have 14-yearterms. Chairman of the Board of Governors hasconsiderable power, and has a term of 4 years.Monetary policy decisions are made by the Federal OpenMarket Committee (FOMC): consists of the 7 governorsplus 5 presidents of the Federal Reserve Banks on arotating basis (with the New York president always on).FOMC meets eight times a year, may meet more.

Williams Economics 312/702

The Twelve Federal Reserve DistrictsAddresses andphone numbersBanksBranches

BostonNew YorkPhiladelphiaClevelandRichmondAtlantaChicagoSt. LouisMinneapolisKansas CityDallasSan FranciscoBoard

The Federal Reserve officially identifies Districts by number and Reserve Bank city.In the 12th District, the Seattle Branch serves Alaska, and the San Francisco Bank serves Hawaii. The System servescommonwealths and territories as follows: the New York Bank serves the Commonwealth of Puerto Rico and the U.S. VirginIslands; the San Francisco Bank serves American Samoa, Guam, and the Commonwealth of the Northern Mariana Islands. TheBoard of Governors revised the branch boundaries of the System in February 1996.

Home | About the FedAccessibility | Contact usLast update: December 13, 2005

FRB: Federal Reserve Districts and Banks http://www.federalreserve.gov/otherfrb.htm

1 of 1 4/21/2009 4:14 PM

Williams Economics 312/702

Fed Balance Sheet

Traditionally, largest asset was holdings of Treasurysecurities, also owns gold, makes loans to banks, and holdsother assets including foreign exchange and federal agencysecurities.Largest liability is currency outstanding. Another liabilityis deposits by banks.Fed makes profit on security portfolio, which it pays toTreasury. In 2015 transferred $97.7 billion to Treasury.In response to financial crisis and recession of 2007-present,balance sheet of Fed has expanded to include wide array ofassets, direct bank lending, and mortgage-backed securities.

Williams Economics 312/702

Williams Economics 312/702

Fed Policy Instrument

Main instrument of conventional policy is the FederalFunds rate. An extremely short-term interest rate: the rateon overnight loans from one bank to another.Uses as implicit means of changing money supply. Policycarried out via open market operations by trading desk atNew York Fed. Buy and sell government securities so thatmarket for overnight cash clears at the target rate.Again in response to recent crisis and recession, directlending and other purchases of assets have become animportant component of policy response. “Unconventional”monetary policy.

Williams Economics 312/702

Policy Interest Rates

-1

0

1

2

3

4

5

6

7

2000 2002 2004 2006 2008 2010 2012 2014 2016

research.stlouisfed.org

DiscountRate(DISCONTINUED)PrimaryCreditRateFederalFundsTargetRange-UpperLimitFederalFundsTargetRange-LowerLimitFederalFundsTargetRate(DISCONTINUED)

(Percent)

Williams Economics 312/702

Other Policy Instruments

Also can adjust reserve requirements, minimum fraction ofeach type of deposit that a bank must hold as reserves.Discount window lending: lending reserves to banks so theycan meet depositors’ demands or reserve requirements,interest rate on such called the discount rate, role of lenderof last resort.A discount loan increases the monetary base, increases indiscount rate discourage borrowing, reduce the monetarybase.In past, Fed discouraged banks from borrowing from thediscount window. Instead, banks borrow from each other inthe Federal funds market. Interest rate is the Fed fundsrate. In recent years has encouraged discount windowborrowing.

Williams Economics 312/702

1 Discount Window includes primary, secondary and seasonal credit programs.2 The PDCF, TSLF and AMLF will remain in operation through April 30, 2009 as announced on December 2, 2008.3 ECB and SNB created December 12, 2007; BOC, BOE, and BOJ created September 18, 2008; RBA, Sveriges Riksbank, DNB, and Norges Bank created September 24, 2008; Reserve Bank of New Zealand created October 28, 2008; Banco Central do Brazil, Banco de Mexico, Bank of Korea, and Monetary Authority of Singapore created October 29, 20084 TOP auctions are sales of options granting the right to enter into TSLF borrowing.5 The TALF is expected to go live around February 2009. The Federal Reserve reserves the right to review and make adjustments to these terms and conditions – including size of program, pricing, loan maturity, and asset and borrower eligibility requirements – consistent with the policy objectives of the TALF.

6 Through the CPFF the FRBNY provides financing to an SPV that purchases eligible three-month unsecured and asset-backed commercial paper from eligible issuers.7 Through the MMIFF the FRBNY will provide senior secured funding to a series of private sector SPVs to finance the purchase of certain money market instruments from eligible investors.8 Reverse repos are collateralized with U.S. Treasuries.9 PDCF and TSLF collateral expanded on September 14, 2008.10 Includes non-U.S. dollar denominated securities.11 Includes auto loans, student loans, credit card loans, or small business loans guaranteed by the U.S. SBA12 Open market operations are authorized for terms of up to 65 business days.

13 28-day and 84-day terms may vary slightly to account for maturity dates that fall on Bank holidays.14 Primary credit loans are generally overnight. Loans may be granted for term beyond a few weeks to small banks, subject to additional administration. 15 Maximum maturity of term increased from overnight to 30 days on August 17, 2007, and to 90 days on March 16, 2008.16 Foward selling TAF auctions announced on September 29, 2008 will be conducted in November with terms targeted to provide funding over year-end.17 Loans are targeted to span potentially stressed financing dates, such as quarter-ends.18 TOP auctions may be conducted on multiple dates for a single loan and may be conducted well in advance of a loan period. 19 Data only available on days when operations are conducted.20 Data published on Thursday, as of close of business on Wednesday.

Federal Reserve Bank of New YorkDecember 2008

Discount Window1

Securities Lending

Depository institutions

Primary credit-eligible depository institutions

Primary credit-eligible depository institutions Primary dealers Primary dealers

Forms of Federal Reserve Lending to Financial Institutions

Full range of Discount Window

collateral U.S. Treasuries

No (loans are bond-for-bond)

No (loans are bond-for-bond)Yes Yes Yes

Yes Yes No N/A No

All All

FRBNY FRBNY

As requested(standing facility)

Every other week,or as necessary16 Daily

Schedule 1: Every other week

Schedule 2: Weekly

Funds Funds Funds U.S. Treasuries U.S. Treasuries

Typically overnight, but up to

several weeks14

Up to 90 days15 28 days or 84 days13,16 Overnight 28 days13

All

Regular OMOs

Single-TrancheOMO Program

Who can participate? Primary dealers Primary dealers

What collateral can be pledged?

Is there a reserve impact?

U.S. Treasuries, agencies,

agency MBS, but typically agency MBS

Yes Yes

What is the term of loan?

Typically, term is overnight–14 days12

Is prepayment allowed if term is greater than

overnight?

No No

Which Reserve Banks conduct

operations?FRBNY FRBNY

How frequently is the program

accessed?

Typically once or more daily

Typically weekly

What are they borrowing? Funds

28 days13

(announced March 7, 2008)

Term DiscountWindow Program

(announcedAugust 17, 2007)

Term AuctionFacility

(announcedDecember 12, 2007)

Term SecuritiesLending Facility

(announcedMarch 11, 2008)2

(announced March 16, 2008)2

Primary dealers

Funds

Full range of tri-party repo

system collateral9,10

Yes

Overnight

N/A

FRBNY

Primary Dealer Credit Facility

Full range of Discount Window

collateral

Full range of Discount Window

collateral

Schedule 1: U.S. Treasuries, agencies, agency MBS

Schedule 2: Schedule 1 plus all

invesment grade debt securities9

Where are statistics reported

publicly?

H.4.1 - Factors Affecting Reserve

Balances20

Securities lending activity

TemporaryOMO activity19

Temporary OMO activity19

H.4.1 - Factors Affecting Reserve

Balances20

H.4.1 - Factors Affecting Reserve

Balances20

Term securities lending facility

activity19

Primary dealers

No (loans are bond-for-bond)

U.S. Treasuries

Schedule 2 TSLF collateral

Typically 2 weeks or less17

No

FRBNY

As necessary18

Term SecuritiesLending Facility

Options Program4

(announcedJuly 30, 2008)

Term securitieslending facilty

options programactivity19

(announcedSeptember 21, 2008)

U.S. and London broker-dealer subsidiaries of

Goldman Sachs, Morgan Stanley, Merrill Lynch

Funds

Full range of Discount Window

collateral and tri-party repo system collateral10

Yes

Overnight

N/A

FRBNY

H.4.1 - Factors Affecting Reserve

Balances20

Transitional Credit Extensions

As requested(standing facility)

As requested(standing facility)

As requested(standing facility)

Yes

Funds

First-tier ABCP

ABCP maturity date(270-day maximum)

No

FRB Boston

Despository institutions, bank holding companies,

U.S. branches and agencies of foreign banks

H.4.1 - Factors Affecting Reserve

Balances20

ABCP Money Market Fund

Liquidity Facility(announced

September 19, 2008)2

As requested(standing facility)

TAF Activity19

Funds

U.S. Treasuries, agencies,

agency MBS8

Eligible CP issuers6 Eligible Money Market

Mutual Funds7

FundsFunds and

subordinated note

Newly issued 3-month unsecured and asset-

backed CP from eligible U.S. issuers

U.S. dollar-denominated certificates of deposit, bank notes and commercial paper

issued by highly rated financial institutions

3 months N/A

N/A

FRBNY FRBNY

N/A

Yes Yes

U.S. Dollars

Central banks pledge foreign currency and lend against

eligible collateral in their jurisdiction

Yes

Overnight to 3 months

No

FRBNY

Typically on schedule with FRBNY TAF auctions or as requested

by central banks

Select central banks to lend on to banks in their jurisdiction3

Reciprocal Currency Arrangements

Commercial Paper Funding Facility

Money Market Investing Funding

Facility(announced

October 21, 2008)

As requested(standing facility)

As requested(standing facility)

H.4.1 - Factors Affecting Reserve

Balances20

H.4.1 - Factors Affecting Reserve

Balances20

H.4.1 - Factors Affecting Reserve

Balances20

(first announced December 12, 2007)3

(announced October 7, 2008)

All U.S. persons that own eligible collateral

Funds

Recently originated U.S. dollar-denominated

AAA ABS11

At least one year

Yes

FRBNY

Yes

Term Asset-Backed Securities Loan

Facility5

(announced November 25, 2008)

Monthly

TALF activity19

Williams Economics 312/702

Policy Decisions and Conduct

FOMC meets 8 times per year to set target rate.Directives from Congress to pursue price stability and fullemployment.Prior to meetings intensive staff briefings, laying out policyoptions, scenarios, and likely effects.For many years the Fed resisted committing to an explicitinflation target. Now explicitly 2%. Many other centralbanks around the world explicitly announce inflationtargets, target interest rate paths.

Williams Economics 312/702

Release Date: March 16, 2016

For release at 2:00 p.m. EDT

Information received since the Federal Open Market Committee met in January suggests thateconomic activity has been expanding at a moderate pace despite the global economic and financialdevelopments of recent months. Household spending has been increasing at a moderate rate, and thehousing sector has improved further; however, business fixed investment and net exports have beensoft. A range of recent indicators, including strong job gains, points to additional strengthening ofthe labor market. Inflation picked up in recent months; however, it continued to run below theCommittee's 2 percent longer-run objective, partly reflecting declines in energy prices and in pricesof non-energy imports. Market-based measures of inflation compensation remain low; survey-basedmeasures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment andprice stability. The Committee currently expects that, with gradual adjustments in the stance ofmonetary policy, economic activity will expand at a moderate pace and labor market indicators willcontinue to strengthen. However, global economic and financial developments continue to poserisks. Inflation is expected to remain low in the near term, in part because of earlier declines inenergy prices, but to rise to 2 percent over the medium term as the transitory effects of declines inenergy and import prices dissipate and the labor market strengthens further. The Committeecontinues to monitor inflation developments closely.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rateat 1/4 to 1/2 percent. The stance of monetary policy remains accommodative, thereby supportingfurther improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal fundsrate, the Committee will assess realized and expected economic conditions relative to its objectivesof maximum employment and 2 percent inflation. This assessment will take into account a widerange of information, including measures of labor market conditions, indicators of inflationpressures and inflation expectations, and readings on financial and international developments. Inlight of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actualand expected progress toward its inflation goal. The Committee expects that economic conditionswill evolve in a manner that will warrant only gradual increases in the federal funds rate; the federalfunds rate is likely to remain, for some time, below levels that are expected to prevail in the longerrun. However, the actual path of the federal funds rate will depend on the economic outlook asinformed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings

Printer Version - Board of Governors of the Federal Reserve System https://www.federalreserve.gov/newsevents/press/monetary/20160316a.htm

1 of 2 3/30/2016 2:58 PM

Williams Economics 312/702

Press Release

Release Date: December 16, 2008

For immediate release

The Federal Open Market Committee decided today to establish a target range for the federal fundsrate of 0 to 1/4 percent.

Since the Committee's last meeting, labor market conditions have deteriorated, and the available dataindicate that consumer spending, business investment, and industrial production have declined. Financial markets remain quite strained and credit conditions tight. Overall, the outlook foreconomic activity has weakened further.

Meanwhile, inflationary pressures have diminished appreciably. In light of the declines in the pricesof energy and other commodities and the weaker prospects for economic activity, the Committeeexpects inflation to moderate further in coming quarters.

The Federal Reserve will employ all available tools to promote the resumption of sustainableeconomic growth and to preserve price stability. In particular, the Committee anticipates that weakeconomic conditions are likely to warrant exceptionally low levels of the federal funds rate for sometime.

The focus of the Committee's policy going forward will be to support the functioning of financialmarkets and stimulate the economy through open market operations and other measures that sustainthe size of the Federal Reserve's balance sheet at a high level. As previously announced, over thenext few quarters the Federal Reserve will purchase large quantities of agency debt and mortgage-backed securities to provide support to the mortgage and housing markets, and it stands ready toexpand its purchases of agency debt and mortgage-backed securities as conditions warrant. TheCommittee is also evaluating the potential benefits of purchasing longer-term Treasury securities. Early next year, the Federal Reserve will also implement the Term Asset-Backed Securities LoanFacility to facilitate the extension of credit to households and small businesses. The Federal Reservewill continue to consider ways of using its balance sheet to further support credit markets andeconomic activity.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Christine M.Cumming; Elizabeth A. Duke; Richard W. Fisher; Donald L. Kohn; Randall S. Kroszner; SandraPianalto; Charles I. Plosser; Gary H. Stern; and Kevin M. Warsh.

In a related action, the Board of Governors unanimously approved a 75-basis-point decrease in thediscount rate to 1/2 percent. In taking this action, the Board approved the requests submitted by theBoards of Directors of the Federal Reserve Banks of New York, Cleveland, Richmond, Atlanta,Minneapolis, and San Francisco. The Board also established interest rates on required and excessreserve balances of 1/4 percent.

Printer Version - Board of Governors of the Federal Reserve System http://www.federalreserve.gov/newsevents/press/monetary/20081216b.htm

1 of 1 4/21/2009 4:36 PM

Williams Economics 312/702

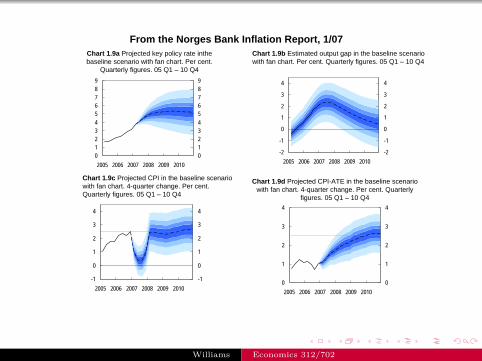

Chart 1.9a Projected key policy rate inthebaseline scenario with fan chart. Per cent.

Quarterly figures. 05 Q1 – 10 Q4

0123456789

2005 2006 2007 2008 2009 20100123456789

-2

-1

0

1

2

3

4

2005 2006 2007 2008 2009 2010-2

-1

0

1

2

3

4

-1

0

1

2

3

4

2005 2006 2007 2008 2009 2010-1

0

1

2

3

4

0

1

2

3

4

2005 2006 2007 2008 2009 20100

1

2

3

4

Chart 1.9b Estimated output gap in the baseline scenario with fan chart. Per cent. Quarterly figures. 05 Q1 – 10 Q4

Chart 1.9c Projected CPI in the baseline scenario with fan chart. 4-quarter change. Per cent. Quarterly figures. 05 Q1 – 10 Q4

Chart 1.9d Projected CPI-ATE in the baseline scenario with fan chart. 4-quarter change. Per cent. Quarterly

figures. 05 Q1 – 10 Q4

From the Norges Bank Inflation Report, 1/07

Williams Economics 312/702

Chart 3 Key policy rate in the baseline scenario in IR 3/06 with fan chart and key policy rate in

the baseline scenario in MPR 1/07 (red line). Per cent. Quarterly figures. 04 Q1 – 09 Q4

0123456789

2004 2005 2006 2007 2008 20090123456789

30% 50% 70% 90%

Source: Norges Bank

Chart 5 Key policy rate in the baseline scenario in IR 3/06 with fan chart and the isolated effect of stronger krone exchange rate (red line). Per cent. Quarterly figures. 04 Q1 – 09 Q4

0123456789

2004 2005 2006 2007 2008 20090123456789

Williams Economics 312/702