lecture note-taking guide - oru accounting · lecture note-taking guide oral roberts university...

TRANSCRIPT

Lecture Note-Taking Guide

Oral Roberts UniversitySchool of BusinessTulsa, Oklahoma

Name _________________________

Lecture Note-Taking Guide

Oral Roberts UniversitySchool of BusinessTulsa, Oklahoma

© Copyright 2002, 2005 by M. Ray Gregg. All rights reserved.

Many educators agree “lecture” is the least effective way to convey information to students. Yet the “lecture” class is one of many important components in the Principles of Accounting

classes at Oral Roberts University. The lecture class provides students opportunities to combine seeing, hearing, and writing in order to introduce the lessons presented in each chapter. The purpose of this note-taking guide is to allow students to write less while listening, seeing, and leaving the room with more. Hopefully, the guide will allow students to think more in class and, therefore, better understand the concepts and principles being presented. Students should consider these suggestions intended to help them maximize their learning opportunities with the use of this note-taking guide:

1. Read and experience the first few pages of the textbook and information on the CD to determine your individual learning style. Follow the authors’ suggestions of ways in which you could approach the course materials considering your learning style.

2. Glance through the chapter (and perhaps the first homework assignment) BEFORE

attending lecture on Monday. Come to class prepared.

3. Attend class. Be on time.

4. Be attentive. Stay alert. Don’t distract your neighbors or yourself by talking or listening to those around you. Stay focused on the lesson being presented in class.

5. Take the note-taking guide to each lecture session. Write in the blanks as the

information becomes apparent in class. Listen to other explanations. Write other important information in the margins. Have questions? Write them in the margins as well; ask the questions in lecture, discussion, or lab as you desire. The objective of the note-taking guide is NOT to just fill in all the blanks, but to master the overall lesson. Attempt to learn in class.

6. Use the note-taking guide during the week as you solve

homework assignments. Review the information in the guide before the discussion groups to anticipate some of the information which may be covered there. Use the guide to review for quizzes and exams as well.

7. Seek help when you do not understand a concept. Other students who are enrolled

in the course or who have completed the course, lab assistants, and your professors are eager to help you master the material. Ask!

Hopefully, you find this note-taking guide to be a useful tool, and you will have a successful experience in accounting this semester!

Partnerships page 1 of 3

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Partnerships

Overview (major topics today and this week):

1. Characteristics

2.

3. Division of Income and Loss

4.

5. Withdrawal

6.

Characteristics

1. responsible for acts of other partners

2.

3. agreement is a contract

4.

5. capital and drawing accounts

6.

7. reward is share of profits — not an employee

Investments

1.

2.

Partnerships page 2 of 3

Division of Income and Loss

1. when there is no

2. agreement sometimes provides for:

original (ratio or “interest”)

time (“salary”)

Admitting a New Partner

1. when transaction is outside the partnership, the partnership accounts areNOT affected

2. capital account could be equal to amount invested, there could be a “_____________” to the OLD partners, or there could be a “_____________” to the new partner

Withdrawal of a Partner

1. when the partner takes ____________ than the capital account balance

2. when the partner takes ____________ than the capital account balance

Liquidation

1. a. Convert non-cash assets .

b. Distribute any to partners according to

their .

2. .

3. Distribute to partners according to

their (evidenced by their balances) .

Partnerships page 3 of 3

Exercise -- Division of Income

Chip and Dale have capital balances of $60,000 and $40,000, respectively. Thepartnership income sharing agreement provides for (1) interest at 10% on their capitalbalances, (2) salaries of $15,000 and $20,000, (3) and the remainder divided in a 2:1ratio.

(a) Prepare a schedule showing the division of net income, assuming net income is$60,000.

“Interest”

“Salary”

Totals $60,000

Based on this information the closing entry would be:

(b) Prepare a schedule showing the division of net income, assuming net income is$18,000.

Chip Dale Total

“Interest” $10,000

“Salary” 15,000 20,000

Remainder

Total $ 3,000 $15,000 $18,000

Corporations — Paid In page 1 of 4

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Corporations(paid in)

Overview

1. differences

2.

3. rights of preferred stock

4.

5. accounting for

Comparing Capital Section of Proprietorship, Partnership, Corporation

New name for capital = ___________________________________________

Two major sections of Stockholders’ Equity for corporation:

1. __________________________________________________________

2. __________________________________________________________

Principal Basic Rights of Stock

1.

2.

3. (maintain fractional share of ownership)

4.

Corporations — Paid In page 2 of 4

Characteristics of Preferred Stock

1.

Co A(non)

Co B(part)

2.

Co A(non)

Co B(cumulative)

3. preference to assets at

4.

5. may not have the right to

Issuing Stock at Par

*

*could also be “Common Stock” or “Preferred Stock”

Issuing Stock at More Than Par (premium)

Cash total

Preferred Stock

Paid-in Capital excess

Corporations — Paid In page 3 of 4

Issuing Stock at Less than Par (discount)

Cash total

par

Common Stock

Issuing No Par Stock

Cash total

total

Issuing No Par Stock With Stated Value

Cash total

Common Stock

Paid-in Capital in Excess of excess

Treasury Stock

What it is.

1. Stock of ,

2. that has been as fully paid ,

3. which is subsequently , and

4. not or .

What is isn’t.

1.

2.

Corporations — Paid In page 4 of 4

What is REALLY is.

1. return of to from whom

the Treasury Stock was

2.

Account for Treasury Stock at _____________________________________.

Purchase of Treasury Stock

Cash

Sale of Treasury Stock for More Than Cost

Cash received

Paid-in Capital from difference

Corporations — Retained Earnings page 1 of 6

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Corporations(retained)

Overview

1. What is (are) Retained Earnings?

2. How is it changed?

3.

4.

5.

Review from Last Week

Two major sections of Stockholders’ Equity for corporation:

1. __________________________________________________________

2. __________________________________________________________

What is Retained Earnings?

Synonyms:

Retained = ____________________________

Earnings = ____________________________

How is Retained Earnings Changed?

Retained Earnings *******

Corporations — Retained Earnings page 2 of 6

Components of Net Income

1.

2. _____________________________________

Requirements for Cash Dividends

1.

2.

3.

Misconceptions About Retained Earnings

Net Income Ö

Retained Earnings Ö

Ö

Important Dates for Cash Dividends

1.

2.

3.

Recording Cash Dividends(real life)

Date of Declaration

Date of Record

Corporations — Retained Earnings page 3 of 6

Date of Payment

Step 4 of Closing Entries

Recording Cash Dividends(per textbook)

1. Cash Dividends xx

Dividends Payable xx

2.

3. Dividends Payable xx

Cash xx

Stock Dividends

With CASH dividends stockholders receive __________________________.

With STOCK dividends stockholders receive _________________________.

Characteristics

1. __________________________________________________________

2. __________________________________________________________

3. shareholder must keep to

maintain proportionate share of

Dates for STOCK Dividends

1. Declaration2. Record3. ________________________________________________

Corporations — Retained Earnings page 4 of 6

Recording Stock Dividends(real life)

Date of Declaration

Date of Record

Date of Distribution

Step 4 of Closing Entries

Recording Stock Dividends(per textbook)

1. Stock Dividends mkt val

Stock Dividends Distributable par or sv

PIC in Excess of Par or SV — CS excess

2.

3. Stock Dividends Distributable par

Common Stock par

Corporations — Retained Earnings page 5 of 6

Comparing Cash and Stock Dividends

Consider this illustration of two identical corporations: same total assets, same liabilities,etc.

The first corporation (on the left) declares and pays a cash dividend while the second (onthe right) declares and distributes a stock dividend. Consider the position of theindividual stockholder in each situation. Reconsider later in the week after you haveworked homework and exercises in class.

Before the Dividends

After the Dividends

Corporations — Retained Earnings page 6 of 6

Stock Splits

Characteristics of Stock Splits

1. reduction in

2. entry required (memo only)

3. no change in paid-in, retained, or totalstockholders’ equity

Long-Term Liabilities page 1 of 6

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Long-Term Liabilities

Objectives:

1. Determine and record the selling price of bonds payable. 2. Determine and record amortization of premium and discount on bonds payable

using the straight-line method and the interest method.

Bonds Payable

Obligations incurred when issuing bonds:

I. “I promise I will pay you ___________________________________ at maturity.”

II. “I promise that, between now and then, I will pay you periodic _______________ at the ____________________ rate on the _____________________ amount.”

These two obligations can be envisioned on “time lines” as follows: The rate is sometimes called: _________________________________________ (specified) _________________________________________ (reflected in sales price of the bond) When ____________________ is GREATER than _________________ , the bonds are unattractive and will sell at a ___________________________________ . When ____________________ is LESS than _________________ , the bonds are attractive and will sell at a ________________________________________ .

Long-Term Liabilities page 2 of 6

Issuing Bonds at Face

The journal entry necessary to record the sale of the bonds at face would be:

face

face

Issuing Bonds at More Than Face

The journal entry necessary to record the sale of the bonds for more than face would be:

Cash received

difference

Bonds Payable

face

Long-Term Liabilities page 3 of 6

Issuing Bonds at Less Than Face

The journal entry necessary to record the sale of the bonds for less than face would be:

Cash received

difference

Bonds Payable

face

Referring to the advertisement from The Wall Street Journal, at 10 3/8% interest, the bonds must have been _________________ because the 99.82% advertised price meant the bonds were selling at a _______________. The market rate of interest must have been ___________________ than 10 3/8%.

Determining the Selling Price of Bonds

The selling price of the bonds is the sum of the “present values” of the two future “promises” made at the time the bonds are sold (refer to page 1): I. Present Value of Face (using factor from table) II. + Present Value of Interest Payments (using factor from annuity table) = Proceeds from Sale of Bonds

Long-Term Liabilities page 4 of 6

Exercise Bound Corporation issued $260,000, 9%, 10-year bonds on January 1, 2002, for $243,799. This price resulted in an effective interest rate of 10% on the bonds. Interest is payable semiannually on July 1 and January 1. Bound uses the effective-interest method to amortize bond premium or discount. Interest is not accrued on June 30. Instructions: Prepare the journal entries to record (to the nearest dollar) the following: a) the issuance of the bonds, b) the payment of interest and the discount amortization on July 1, 2002, and c) the accrual of interest and the discount amortization on December 31, 2002. (The amount of one interest payment is determined used the traditional “interest” formula, P x R x T: $260,000 x _________________ x 6/12 is ____________________ .) The following present value tables are useful in the calculations: Table C-1 is on page C3, and Table C-2 is on page C5 in the Appendix C at the back of the textbook. Present Value of $260,000 @ 10% semiannually is 260,000 x _______________ = ________________ + Present Value of Interest (one interest pmt x factor) is ________________ x ______________________ = ________________ = Proceeds from the Sale of Bonds

(Compare this result to the amount given in the exercise above.) (Note: For Problem16- 6A, present calculations (similar to those demonstrated here) to support determination of the selling price of the bonds. Allow the amount given in the textbook to serve as a “check figure.” Use lined notebook paper or pages from an unassigned problem in the Working Papers.) a) The journal entry to record the sale (issuance) of the bonds would be:

This exercise will be completed later. If not in lecture, please take this handout to your first discussion group this week.

Amortization of PREMIUM or DISCOUNT on Bonds

Objectives:

1. to match the correct expense with the correct year (income statement benefit)

2. to (gradually, systematically) eliminate the related Premium or Discount account OR

to change (raise or lower) the BCA to face by the time the bond matures (two ways to state the same balance sheet benefit)

Long-Term Liabilities page 5 of 6

Related Definition: Review: New: Equipment Bonds Payable - Accumulated Depreciation + (unamortized) Premium ______________________ - (unamortized) Discount = Book Value = Bond Carrying Amount

Journal Entries to Record Amortization Amortization of Premium

amount

amount

Amortization of Discount

amount

amount

Determining Amount of Amortization

Straight-Line Method (presented in chapter) Premium or Discount periods (Effective) Interest Method (presented in Appendix at end of chapter)

= same amount each period

Long-Term Liabilities page 6 of 6

Exercise

(continued from page 4)

(b) (1) Record the journal entry for the payment of the first semiannual interest on July 1 (amortization is to be recorded in a separate entry).

(b) (2) Record the journal entry for the amortization of the discount (using the effective

interest method) at the time of the first semiannual interest payment on July 1.

*

*

(c) (1) Record the journal entry for the accrual of interest at December 31.

(c) (2) Record the journal entry for the amortization of the discount (using the effective

interest method) at the time of the accrual of interest on December 31.

*

*

* Determine the amount of amortization (effective interest method) following the textbook examples on pages 653 and 654 and the chart below:

A B C D E

Interest Interest Discount Unamort. B.C.A.

Paid Expense Amort. Discount (face - D)

Pmt (face x contract) (E x mkt) (B - A) (D - C) (E + C)

16,201 243,799

1 490

2

3 11,700 12,240 540 14,656 245,344

4 11,700 12,267 567 14,089 245,911

5 11,700 12,296 596 13,494 246,506

Statement of Cash Flows page 1 of 7

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Statement of Cash Flows

I. History of Statement of Cash Flows

A. Prior to 1971

studied "funds flow" and "cash flow" but not required to be reported

B. 1971 through July 8, 1988

Statement of Changes in Financial Position required for all published financialstatements

1. working capital concept (most popular)2. cash concept

C. July 31, 1988 to present Statement of Cash Flows

1. considered a principal financial statement2. to be included whenever Balance Sheet and Income Statement information is

presented

II. Questions the financial statements attempt to answer (according to ALEX #1 illustration ofHoratio Algie's Tree Trimming Service in first semester)

A. Balance Sheet

Where does my business stand today?

B. Income Statement

How well did my business do this month (this year, etc.)?

C. Statement of Cash Flows

From where did cash come, and where did it go? (also mentioned in Chapter 1, pp. 5, 21, 22, 24)

Statement of Cash Flows page 2 of 7

III. Categories of sources ("inflows") and applications/uses ("outflows") of cash

Cash

Sources ("inflows"): Applications/Uses ("outflows"):

1. 1.

2. 2.

3. 3.

4. 4.

IV. Grouping sources/applications for Statement presentation

I.

II.

III.

V. Operating Activities

A. Preparer assumed to understand these underlying concepts:

1. Balance Sheet/income Statement interrelateda. Chapter 1, Exercise E1-6, we found net income from balance sheet data

b. Chapters 3, 4, 5, and others every AJE effected the BS and the IS

2. Net Income Ö Casha. Chapter 15, appropriations of retained earnings

Ö Cash

Ö Cash

= Cash

b. Income Statement prepared under accrual basisc. Results of operations reported on the income statement may result

in many balance sheet changes -- not limited to changes in cash.

Statement of Cash Flows page 3 of 7

INCOME STATEMENT

Sales xxxxxxxxxx

Cost of Goods Sold xx

Gross Profit xxxxxxxx

Expenses:Advertising xDepreciation xSalaries xRent xInsurance xInterest xUtilities x

Total Expenses xxxxxxx

NET INCOME x

BALANCE SHEET

Current AssetsCash xReceivables xInventory xPrePd Exp x xxxx

LT AssetsPP&E xxxAcc Depr x xx

TOTAL ASSETS xxxxxx

Current LiabilitiesAccts Pay xSal Pay x xx

LT LiabilitiesBonds Payable xx

Capital Stock xRetained Earnings x xxTOTAL LIAB & SE xxxxxx

d. If these positions are true for one current asset and one current liability, wecan assume they would be the same for all current assets and all currentliabilities, and, therefore, summarize as follows:

Statement of Cash Flows page 4 of 7

B. "Cash Provided by Operations" can be determined in three phases by changing NetIncome as follows:

1. add and deduct

(best example: )

2. add and deduct

(exceptions: dividends payable, marketable securities)

3. to avoid duplication, negate effect of loss (add) or gain (deduct) from sale of LTinvesting and financing activities (already in NI).

VI. Investing Activities

A. Determine in/outflows (referring to list of 4 sources/uses) by examining "non-current"accounts.

B. Current and "noncurrent" accounts1. Current "Non-Current"

Current Assets Long-Term AssetsCurrent Liabilities Long-Term Liabilities

Capital StockRetained EarningsRevenueExpenses

2. since significant cash transactions have one current and one "non-current" effect,easier to find them by examining “non-current” accounts

VII. Financing Activities

As for investing activities, determine in/outflows (referring to list of 4 sources/uses) byexamining "noncurrent" accounts.

VIII. Summary

A. "Tools" needed1. Comparative Balance Sheet (provided in textbook)2. Four categories of sources and uses of cash3. Cash Provided By Operations (CPBO) "Window"4. Data from "non-current" accounts (provided)5. "Pattern" to follow (textbook or other example)

B. "Know-How" needed (steps in preparing statement)1. from comparative balance sheet, prepare an "increase/decrease" column (this

becomes a "check-list" for making sure all changes were considered)

2. using "4 sources/4 uses" list, consider items of in/outflowa. convert NI to CPBO (three phases)b. use information from "noncurrent" accounts to find investing and financing

in/outflows.

Statement of Cash Flows page 5 of 7

IX. Sample Problem

The comparative balance sheet for Resurrection Company at April 30 of the current andpreceding year is presented at the top of the next page. Selected "non-current" accounts areprovided for additional information.

Prepare a statement of cash flows.

Statement of Cash Flows page 6 of 7

RESURRECTION COMPANYCOMPARATIVE BALANCE SHEET

IncreaseASSETS 4/30/x2 4/30/x1 (Decrease) U Cash $ 30,000 $ 4,000 $ 26,000 ____Accounts Receivable 21,000 10,000 11,000 ____Merchandise Inventory 30,000 36,000 (6,000) ____Equipment 180,000 150,000 30,000 ____Accumulated Depreciation (36,000) (30,000) (6,000) ____Land -0- 30,000 (30,000) ____ Total Assets $225,000 $200,000 $ 25,000

LIABILITIES AND STOCKHOLDERS’ EQUITYAccounts Payable $ 33,000 $ 40,000 $ (7,000) ____Salaries Payable 3,000 2,000 1,000 ____Dividends Payable 3,000 3,000 -0- ____Bonds Payable 20,000 60,000 (40,000) ____Common Stock 80,000 50,000 30,000 ____Paid in Cap. in Excess of Par--C. S. 39,000 15,000 24,000 ____Retained Earnings 47,000 30,000 17,000 ____ Total Liab. and Stockholders' Equity $225,000 $200,000 $ 25,000

Equipment5/1/x1 Balance 150,000 |Purchased for cash 30,000 |

|

Accumulated Depreciation| 5/1/x1 Balance 30,000| 4/30/x2 Depreciation Expense 6,000|

Land5/1/x1 Balance 30,000 | Sold for $28,000 30,000

|

Bonds Payableretired at maturity 40,000 | 5/1/x1 Balance 60,000

|

Common Stock| 5/1/x1 Balance 50,000| Issued for cash 30,000|

Paid in Capital in Excess of Par — Common Stock| 5/1/x1 Balance 150,000| Issued for cash 24,000|

Retained EarningsDividends declared 5,000 | 5/1/x1 Balance 30,000

| Net Income per I. Stmt. 22,000|

Statement of Cash Flows page 7 of 7

RESURRECTION COMPANYStatement of Cash Flows

For the Year Ended April 30, xxxx

Cash flows from operating activities:

Net income, per income statement $_________Add: _________________________ $_________

_________________________ _________

_________________________ _________

_________________________ _________ _________

$_________Deduct: _________________________ $_________

_________________________ _________ _________

Net cash flow ________________ _________ operating activities $_________

Cash flows from investing activities:

_________________________________ $_________

Less: ___________________________ _________

Net cash flow ________________ __________ investing activities _________

Cash flows from financing activities:

__________________________________ $_________

Less: ___________________________ $_________

___________________________ _________ _________

Net cash flow ________________ __________ financing activities _________

_______________ in cash $_________

Cash at the beginning of the year _________

Cash at the end of the year $

Introduction to Manufacturing page 1 of 2

Principles of Financial and Managerial Accounting II

Introduction to Manufacturing

The next lecture introduces accounting students to a topic that will be covered for the remainder of the semester. The lecture assumes students have had certain common experiences. In order to prepare for the upcoming material, before Monday’s lecture, students are urged to accomplish the activities described below. I. Please note in the syllabus that there is homework assigned for Monday. The

problem is from Chapter 20 and also serves as an introduction to the material that will be covered for the remainder of the semester.

II. Assuming it is true that “a picture is worth a thousand words,” students are

urged to complete a “virtual field trip” of an introduction to manufacturing operations available on the class web site at the following address:

http://oruaccounting.com Monday’s lecture assumes students have experienced the “virtual field trip” on the Internet. The note-taking guide on the next page should assist in recognizing some of the major lessons from the presentation. The object of the lesson is not to fill in every blank on the note-taking guide, but rather to see and learn from the presentation.

Please make an effort to be prepared for the presentation during next Monday’s lecture by investing some time in preparation before class.

http://oruaccounting.com

Introduction to Manufacturing page 2 of 2

Principles of Financial and Managerial Accounting II

Introduction to Manufacturing

List the three stages of production: 1. the purchase and storage of _______________________________ 2. ______________________________________________________ 3. storing and caring for the __________________________________ Name the three inventory accounts which parallel the three stages of production: 1. ______________________________ 2. ______________________________ 3. ______________________________ Name the three “elements of cost”: 1. Direct _________________________ 2. Direct _________________________ 3. ______________________________ Name the three sub-parts of manufacturing (factory) overhead: 1. Indirect ________________________ 2. Indirect ________________________ 3. Other

Job Order and Manufacturing Overhead page 1 of 5

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Manufacturing: Job Order, Flow of Costs Entries, Manufacturing Overhead

Major change from first semester and previous topics:

Service( Merchandise

(________________________ Another major change as we enter this topic:

Financial Accounting ________________________

Recommendations for self-study:

Chapter 20# great introduction# many new terms (vocabulary)# study Chapter 20 with any of next three chapters# good Questions recommended in syllabus# good exercises recommended in syllabus

Chapters 21 and 22# assume perpetual inventory# Job Order:_____________________________________________________________________

_____________________________________________________________________

Examples:_____________________________________________________________

# Process:_____________________________________________________________________

_____________________________________________________________________

Examples:_____________________________________________________________ From “Virtual Field Trip” . . . Stages of Production:

1. ________________________________________________________________

2. ________________________________________________________________

3. ________________________________________________________________

Job Order and Manufacturing Overhead page 2 of 5

Inventory Accounts (parallel to "stages of production"):

1. ________________________________________________________________

2. ________________________________________________________________

3. ________________________________________________________________

FLOW OF COSTS THROUGH MANUFACTURING T-ACCOUNTS

In the space below, complete the diagram of T-accounts and other information depictingthe FLOW OF COSTS through manufacturing accounts. Take care to draw it EXACTLYas it is illustrated on the screen. Use the diagram to assist in solving homeworkproblems and in understanding the flow of costs through the accounts.

Job Order and Manufacturing Overhead page 3 of 5

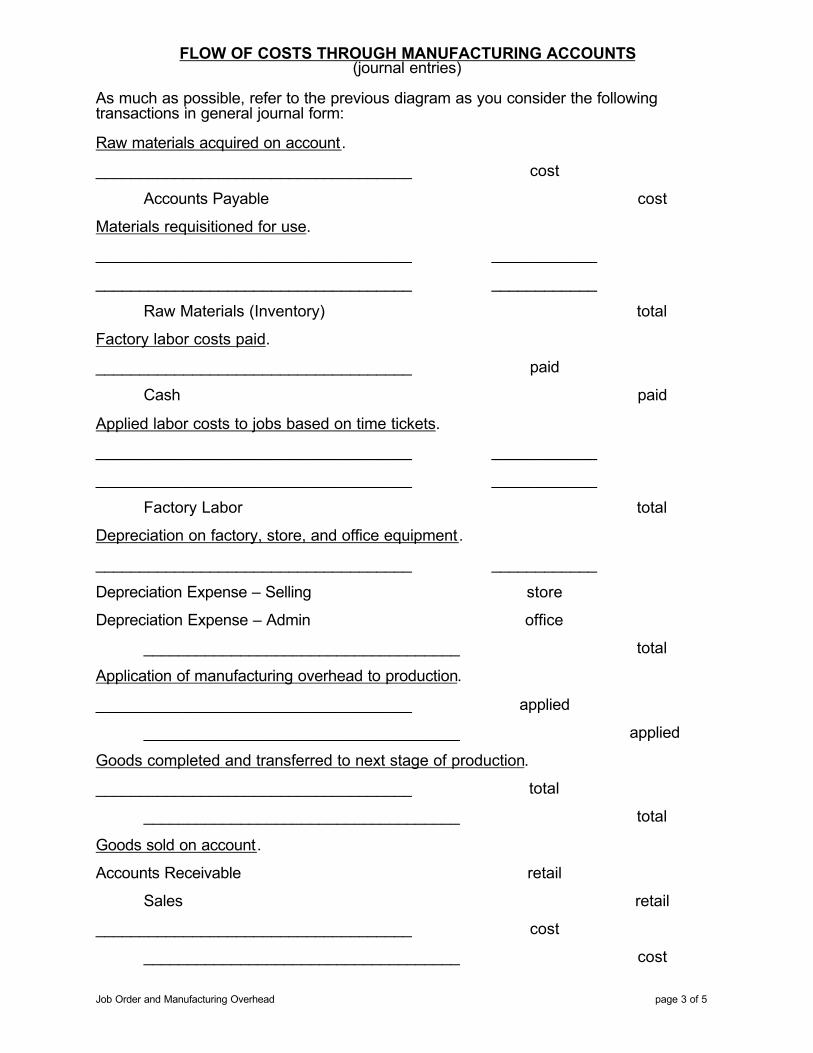

FLOW OF COSTS THROUGH MANUFACTURING ACCOUNTS(journal entries)

As much as possible, refer to the previous diagram as you consider the followingtransactions in general journal form:

Raw materials acquired on account.

____________________________________ cost

Accounts Payable cost

Materials requisitioned for use.

____________________________________ ____________

____________________________________ ____________

Raw Materials (Inventory) total

Factory labor costs paid.

____________________________________ paid

Cash paid

Applied labor costs to jobs based on time tickets.

____________________________________ ____________

____________________________________ ____________

Factory Labor total

Depreciation on factory, store, and office equipment.

____________________________________ ____________

Depreciation Expense – Selling store

Depreciation Expense – Admin office

____________________________________ total

Application of manufacturing overhead to production.

____________________________________ applied

____________________________________ applied

Goods completed and transferred to next stage of production.

____________________________________ total

____________________________________ total

Goods sold on account.

Accounts Receivable retail

Sales retail

____________________________________ cost

____________________________________ cost

Job Order and Manufacturing Overhead page 4 of 5

Control Accounts Subsidary Ledgers

________________________ ________________________

________________________ ________________________

________________________ ________________________

MANUFACTURING OVERHEAD (a.k.a. Factory Overhead)

Easier to associate _____________________ and ___________________with the

finished product than to associate ______________________ with the finished product.

Most Reliable Method:

Allocate total costs to units produced at year end when all ACTUAL costs are known.

Weakness: _____________________________________________________________

Alternative Method:

Allocate ACTUAL costs incurred on a month-to-monthbasis.

Consider examples of manufacturing plants in Bismarkand Brownsville.

Weakness: differences in costs incurred (some

seasonal) would _____________________________

_______________________ of the product produced.

Job Order and Manufacturing Overhead page 5 of 5

Best Alternative:

Use of predetermined ________________________________________________________

Not precise -- but reliable . . .

Manufacturing (Factory) Overhead Rate

estimated estimated *

*Common activity bases/drivers:

1. direct labor costs (dollars)

2. ________________________________________

3. machine hours

Application of Manufacturing (Factory) Overhead

actual activity for monthx ________________________________________= estimate (applied amount)

The journal entry necessary to assign (apply) overhead would be:

____________________________________ applied

____________________________________ applied

Manufacturing – Process Costing (Weighted-Average Method) page 1 of 4

Name ______________________________________

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II Manufacturing – Process Costing

Overview 1. Contrasting Job Order and Process methods

a. Which method for which industry? b. Similarities and differences

2. Allocation of Process Costs a. Equivalent Units of Production b. FIFO vs. Weighted Average c. Steps in cost allocation

3. Cost of Goods a. Finished b. Not Finished

Job Order vs. Process

Manufacturing – Process Costing (Weighted-Average Method) page 2 of 4

Conversion Costs _________________________ plus _____________________________ are “conversion costs.” All costs entering production other than direct materials are considered conversion costs. Equivalent Units of Production

- a measure of productive effort measured in ______________________________

- Becomes the basis for allocation of costs

Illustration X Company has several processing departments. Costs charged to Department 1 for February totaled $258,600 as follows: Work in Process, 2/1 Materials $12,000 Conversion Costs 9,000 $21,000 Materials added 72,000 Labor 103,500 Overhead 62,100 Records indicate that 3,000 units were in beginning Work in Process 30% complete as to conversion costs, 18,000 units were started into production, and 4,000 units were in ending work in process 60% complete as to conversion costs. Materials are entered at the beginning of each process. Instructions: (a) Determine the equivalent units of production and the unit costs for Department 1. (b) Determine the assignment of costs to goods transferred out and in process.

Manufacturing – Process Costing (Weighted-Average Method) page 3 of 4

Step 1 – Determine “physical flow” in units

Step 2 – Determine EUP for Materials and for Conversion Costs

Step 3 – Determine unit costs for materials, conversion costs, and total

Manufacturing – Process Costing (Weighted-Average Method) page 4 of 4

Step 4 – Allocate costs incurred to 1) goods finished (and journalize and post) and 2) not finished

General Journal

Step 4 – part 2)

Standard Costs page 1 of 4

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Standard Costs

Overview

1. Importance of standards2. Variances from standards3. Standards in the accounts4. Variances on the financial statements

Advantages of Standard Costs (from textbook page 1050)

1. Helps ____________________________ plan

2. _______________________ become more “cost conscious”

3. Helps set selling prices

4. Management more able to control __________________

5. Management deals with ___________________________

6. Simplify ____________________ costing and reduce clericalcosts

Variances from Standards

Standard Costs page 2 of 4

Example of Standard Cost Variances

Standard costs and actual costs for direct materials, direct labor, and manufacturingoverhead incurred for Titan Company in the manufacture of 5,000 units of product duringFebruary were as follows:

Standard Costs Actual Costs Direct Materials 7,000 pounds at $12 7,200 pounds at $11.50Direct Labor 2,000 hours at $15 1,850 hours at $15.50Mfg Overhead Rates per direct labor,

based on 100% of capacity of 2,500 labor hours: Variable costs, $13.20 $28,000 variable cost Fixed cost, $8.00 $20,000 fixed costs

Instructions: Determine (a) the total direct materials cost variance, the price variance,and the quantity variance; (b) the total direct labor cost variance, the price (rate)variance, and the quantity (time) variance; and (c) the total manufacturing overhead costvariance, the controllable variance, and the volume variance.

DIRECT MATERIALS COST VARIANCE

Total Materials Variance

Materials Price Variance

Materials Quantity Variance

Standard Costs page 3 of 4

DIRECT LABOR COST VARIANCE

Total Labor Variance

Labor Price (Rate) Variance

Labor Quantity (Time) Variance

MANUFACTURING OVERHEAD COST VARIANCE

Total Overhead Variance

(How Costs Behave)

In Total Per Unit

Variable Costs __________ __________

Fixed Costs __________ __________

Standard Costs page 4 of 4

W I P

FG

COGS

MO

FL

Overhead Controllable Variance

Overhead Volume Variance

Standard Costs in the Accounts

You are strongly urged to learn more about

recording standard costs in the accounts by

completing the lesson available on the class

web page (http://oruaccounting.com). It is a

continuation of the exercise above. The next

sheet in the Note-Taking Guide should assist

you in following along. It would be best to

complete it before you do your homework

assignment on this topic.

Standard Costs: Recording Variances in the Accounts page 1 of 3

Principles of Financial and Managerial Accounting II

Standard Costs Recording Variances in the Accounts

Introduction The lecture presentation explained the importance of using standard costs in manufacturing operations. The calculation of variances from standards and reporting these variances to management provides useful information for decision making purposes. Journal entries are needed to accumulate and report actual and standard costs in the accounting system. The presentation available on the class web site (http://oruaccounting.com) tells “the rest of the story” by illustrating the necessary entries. Things You Will Need

• Since this presentation is a continuation of the exercise used in lecture, you will need the data from the exercise from the note taking guide.

• Having the notes you took in lecture of the calculations of the variances would also be helpful and necessary.

• This handout should help you take notes as you read through the information presented. However, remember the main objective is not to fill in all the blanks, but rather to understand the material being presented.

When you see the calculator in the presentation, be sure to take the time to refer to the calculations you made previously and mentally “connect” them to the entries being made.

1

Copyright © 2002 by M. Ray Gregg. All rights reserved. 8

Materials Price VarianceRM

WIP

FG

COGS

A x S

FL

MOStandard costs are introduced into the accounting system when goods are acquired. The actual quantity acquired is recorded at the standard price.

MPV

u f

The difference between the price paid and the price that should have been paid is the Materials Price Variance.

Copyright © 2002 by M. Ray Gregg. All rights reserved. 11

Materials Quantity VarianceRM

WIP

FG

COGS

A x S

FL

MOActual direct materials used are credited to RM while WIP is debited with the standard amount which should have been used.

The difference between the standard quantity that should have been used and the actual quantity used is the Materials Quantity Variance.

MPV

A x S

S x S

MQV

u f

u f

Copyright © 2002 by M. Ray Gregg. All rights reserved. 14

Labor Price VarianceRM

WIP

FG

COGS

A x S

FL

MO

MPV

A x S

S x S

MQV

u f

u f

Factory Labor is debited for the actual hours worked at the standard price established. Wages Payable is credited with actual hours worked at the actual rate of pay.

LPV

u f

A x S

The difference between the actual price paid and the standard rate which should have been paid is the Labor Price Variance.

Copyright © 2002 by M. Ray Gregg. All rights reserved. 17

Labor Quantity VarianceRM

WIP

FG

COGS

A x S

FL

MO

MPV

A x S

S x S

MQV

u f

u f

Standard hours are used to assign Factory Labor costs to production yet Factory Labor is credited for actual hours employees worked.

LPV

u f

A x S

S x S

A x SLQV

The Labor Quantity Variance is the difference between the actual hours worked and the standard hours which should have been worked.

u f

Copyright © 2002 by M. Ray Gregg. All rights reserved. 23

Overhead VariancesRM

WIP

FG

COGS

A x S

FL

MO

MPV

A x S

S x S

MQV

u f

u f

Once calculated, the overhead controllable and volume variances are reflected in the accounts.

LPV

u f

A x S

S x S

A x SLQV

u f

actual

S x S

std

O C V

O V V

u f

u f

f u

Copyright © 2002 by M. Ray Gregg. All rights reserved. 28

Standards in the AccountsRM

WIP

FG

COGS

A x S

FL

MO

MPV

A x S

S x S

MQV

u f

u f

Standard amounts continue to be used to record the flow of costs through the remaining accounts.

LPV

u f

A x S

S x S

A x SLQV

u f

actual

S x S

std

O C V

O V V

u f

u f

std

std std

std

f u

Standard Costs: Recording Variances in the Accounts page 3 of 3

Journal

Date Account P.R. Debit Credit

1 Raw Materials

2

3 Accounts Payable

4

5 Work in Process

6

7 Raw Materials

8

9 Factory Labor

10

11 Wages Payable

12

13 Work in Process

14

15 Factory Labor

16

17 Manufacturing Overhead

18 Accounts Payable (etc.)

19

20 Work in Process

21 Manufacturing Overhead

22

23

24

25 Manufacturing Overhead

26

27 Finished Goods

28 Work in Process

29

30 Accounts Receivable retail

31 Sales retail

32

33 Cost of Goods Sold

34 Finished Goods

Variable and Absorption Costing page 1 of 3

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Cost and Revenue Relationships for Management

I. Absorption Costing and Variable CostingA. Chapter 23, pp. 954 - 957B. New format for ___________________ ________________C. Excellent decision tool

II. Differential AnalysisA. Chapter 27, pp. 1085-1090, 1093-1094B. No preferred formatC. Emphasizes making __________________ decision for _______________

reasons

Comparison of Costing Methods

Absorption Variable

1. ALL costs “ ” by the product: DM, DL, and MO become part of finished good.

1. DM, DL, and V MO become part of the cost of the finished good.

2. ______________ and variable manufacturing costs are included in COGS:

S - COGS = GP

2. Only _________________________ manufacturing costs are included in COGS:

S - __________ = MM - VE =

3. F MO is a _________________ cost. 3. F MO is a _________________ cost.

4. By placing F MO in product, some __________________ are taken to next period in __________________.

4. F MO is __________________ with time period and never taken to next period in __________________.

5. When inventory __________________ net income is ____________________.

5. When inventory __________________ net income is ____________________.

6. For ____________________ purposes.

Only acceptable method for financial reporting or tax purposes.

6. For __________ _________ purposes.

Not acceptable for financial reporting or tax purposes.

7. Better for _____________ decisions (need to cover __________ costs in long-run).

7. Better for _____________ decision making (concerned with covering __________ costs).

Variable and Absorption Costing page 2 of 3

Comparison of Absorption Costing and Variable Costing

The Rainey Company began operations in January of the current year. During the first year of operations the company manufactured 50,000 units, of which 44,000were sold at $40 per unit. Variable manufacturing costs were $12 per unit, and fixed manufacturing overhead was $260,000. Variable selling and administrativeexpenses were $4.50 per unit sold, and fixed selling and administrative expenses were $150,000. Instructions: (1) Prepare an absorption costing income statement,and (2) prepare a variable costing income statement in good form. (3) Calculate and explain the difference, if any, in the two net income amounts.

RAINEY COMPANYIncome Statement -- ABSORPTION Costing

For the Year Ended December 31, xxxx

SALES (__________ units x $_____) $

Cost of Goods Sold:

Variable Cost of Goods Manufactured (_______ x $______) $

Fixed Manufacturing Overhead 260,000

Cost of Goods Manufactured $ Less: Ending Inventory( _______ units x $________)

COST OF GOODS SOLD

GROSS PROFIT $

Selling and Administrative Expenses:Variable ($______ x ______ units) $ Fixed 150,000

INCOME FROM OPERATIONS $

RAINEY COMPANYIncome Statement -- VARIABLE Costing

For the Year Ended December 31, xxxx

SALES (________ units x $______) $

Variable Cost of Goods Sold:

Variable Cost of Goods Manufactured (_________ x $______) $

Less: Ending Inventory(__________ units x $______)

VARIABLE COST OF GOODS SOLD

_______________________ ______________ $

Variable Selling and Administrative Expenses

_______________________ ______________ $

Fixed Costs and Expenses:Manufacturing Overhead $ 260,000Selling and Administrative 150,000 410,000

INCOME FROM OPERATIONS $

Note: This example is for instructional purposes only; for homework follow the examples in the textbook.

Variable and Absorption Costing page 3 of 3

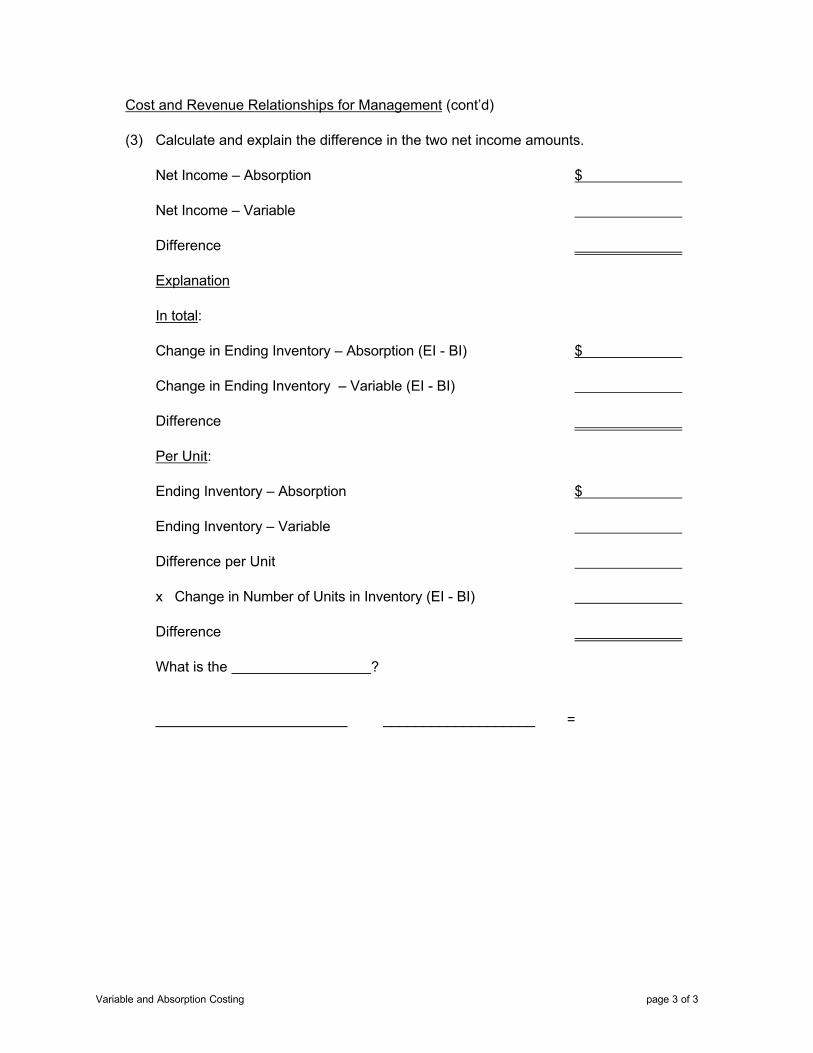

Cost and Revenue Relationships for Management (cont’d)

(3) Calculate and explain the difference in the two net income amounts.

Net Income – Absorption $

Net Income – Variable

Difference

Explanation

In total:

Change in Ending Inventory – Absorption (EI - BI) $

Change in Ending Inventory – Variable (EI - BI)

Difference

Per Unit:

Ending Inventory – Absorption $

Ending Inventory – Variable

Difference per Unit

x Change in Number of Units in Inventory (EI - BI)

Difference

What is the ?

________________________ ___________________ =

Break-Even Analysis page 1 of 4

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Break-Even Analysis

Objectives

1. determine the point in dollars and in units

2. determine net income

3. prepare a chart

4. determine the margin of safety in dollars and as a ratio (percentage)

5. determine the margin ratio

The Break-Even Point

You paid $5,000 for a car, drove it 6 months and sold it to a friend for $5,000.

How did you do? You gained how much? ___________________________________

Definition: the level of sales at which total is (exactly)

equal to total

Formula: _________________________________________________________

where Sales is _____________________________________

Fixed Costs are _______________________________

and Variable Costs are a ________________________

This formula might be remembered as being like the _________________________ on

our aunt’s or ___________________________ coffee table.

Break-Even Analysis page 2 of 4

Mathematical steps:1. ________________

2. ________________

3. ________________

Example to Illustrate the Break-Even Formula (also used throughout the class period)

Actual sales for Company A are $200,000 ($100 each), fixed costs (and expenses) are$60,000 and variable costs (and expenses) are 60% of sales. Compute the break-evenpoint in dollars.

Proof:Income Statement

Sales (at break-even) $ 150,000Less: Variable Costs (60%) 90,000________________________________ Less: Fixed Costs Net Income

Break-Even in UNITS:

Do you want to break even?

Target Net Income -- What must sales be to increase net income by $20,000?

Present net income:

Sales $200,000VC (60%) $120,000FC __________ 180,000Net Income

Break-Even Analysis page 3 of 4

Target Net Income

Break-Even Chart

Margin of Safety

W, K, & K: “…is the difference between actual … salesand sales at the break-even point.” p. 946

How “safe” are you?

RG & CW: “Margin of Safety” is the ____________________ actual sales over sales atthe break-even point.

Break-Even Analysis page 4 of 4

Income StatementSales $xx,xxxxLess: Cost of Goods Sold xxxxGross Profit $xx,0000

GP = GP percentage S

used to estimate goods destroyed in fire inExercise E6-15, page 262.

Income Statement -- Variable CostingSales $xx,xxxxLess: Variable Costs and Expenses xxxxContribution Margin $xx,0000

Continuing Previous Example

Actual sales for Company A are $200,000 ($100 each), fixed costs (and expenses) are$60,000 and variable costs (and expenses) are 60% of sales. Current net income is_____________________ and sales at the break-even point are _________________. Compute the margin of safety in dollars and as a ratio.

Remember?

Contribution Margin Ratio

Actual sales for Company A are $200,000 ($100 each), fixed costs (and expenses) are$60,000 and variable costs (and expenses) are 60% of sales. What is the contributionmargin ratio?

Capital Budgeting page 1 of 4

Date Account Title Ref Debit Credit

Asset? or Expense? 6,9006,900 Cash

14

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II

Capital Budgetingevaluating proposed capital expenditures

What is a capital expenditure?

From Chapter 10, page 412:

“Additions and improvements are costs incurred to increase the operating efficiency, productive capacity, orexpected useful life of the plant asset. These expenditures are usually material in amount and occur infrequently. Expenditures for additions and improvements increase the company’s investment in productive facilitiesand are generally debited to the plant asset affected. They are often referred to as___________________________________________.”

“So you bought a new ___________________________.”

debiting an ___________________ is a capital expenditure

Annual Rate of Return

measure of anticipated ______________________ of an investment alternative

Three ways to determine “average cost”:

1. Sum book value each year and divide bynumber of years.

2.

3.

Capital Budgeting page 2 of 4

Cash coming in (revenue) ! Cash going out (expense) =

Revenue ! Expense =

Even ”Streams” Uneven “Streams”

Limitations of Annual Rate of Return:

1. timing of ___________________________________________

2. timing of ___________________________________________

Cash Payback Period

time required to ______________________________________________

Capital Budgeting page 3 of 4

NCF x PV factor = PV of NCF – PV of expenditure acceptable + or 0 not acceptable —

Limitations of Cash Payback:

ignores overall _____________________ , cash flow _________________________ ,and cash flow beyond the payback period.

Discounted Cash Flow: Net Present Value Method

compares present value of ______________________________ with proposed outlay(already in today’s dollars)

_____________________ is built into the computation.

When there is an _______________ of future NCF over the ____________________, it

IS an _______________________ alternative.

(A demonstration exercise is on the next page.)

Capital Budgeting page 4 of 4

Capital Investment Analysis

Victory Company is considering the acquisition of machinery at a cost of $750,000. Themachinery has an estimated life of 5 years and no residual value. It is expected to provide yearlyincome of $37,500 and yearly net cash flows of $187,500. The company's minimum desired rateof return for discounted cash flow analysis is 6%. Compute the following:

(a) The annual rate of return.

= $ = _______%$

(b) The cash payback period.

= $ = _______ years$

(c) The excess (deficiency) of present value over the amount to be invested using the netpresent value method. Use the table of "Present Value of 1" in the appendix (and use the"memory" on your calculator).

Year Net Cash Flow Factor PV of NCF

1 $ $

2

3

4

5

Total $

Proposed expenditure

Excess $ 4444444444444