lawyers professional liability (lpl) cfpb coverage...

TRANSCRIPT

Lawyers Professional Liability (LPL) Title Agent Errors & Omissions (E&O) CFPB Coverage Cyber Liability Escrow Security Bond/Computer Crime Fraudulent Wire Coverage

Broad Professional Services Defined as:◦ Services performed or advice given by the Insured in the Insured’s practice as a lawyer, arbitrator, mediator, or Title

Agent.◦ Services as a notary public.◦ Services as a trustee, administrator, conservator, executor, guardian, receiver or in a similar fiduciary capacity except

when any insured is a beneficiary or distribute of any trust or estate serviced and the fee accruing from such work inures to the benefit of any Insured.

Broad “Insured” Definition: includes “Predecessor in Business” and “Successor in Business” with 30 day notice period; includes independent contractors for “Professional Services” performed on the Insured’s behalf and within the scope of a written contract; Of Counsel for “Professional Services” performed within their scope of employment; ◦ Subject to underwriting, we can include commonly owned title agencies as Named Insureds under the policy.

Innocent Insured coverage for those “Insureds” that did not personally commit, participate or acquiesce in the acts or omissions of other “Insureds” that triggered the exclusion.

Defense for criminal, fraudulent or dishonest acts otherwise covered under the policy until final adjudication.

Defense for claims alleging willful or intentional failure to comply with escrow instructions or binding authority until final adjudication.

Consent to Settle: Written consent from the Named Insured required prior to settlement.

CFPB Coverage (RECENTLY ADDED) - $150,000 sub-limit of coverage for reasonable attorneys’ fees, costs and expenses for a CFPB Matter (subpoena, civil investigation, hearing, or civil action conducted or received by the CFPB).

Fraudulent Email Wire Transfer Coverage (RECENTLY ADDED) - THIRD PARTY COVERAGE: We will pay on behalf of an insured those sums insured become legally obligated to pay up to $1m for a covered loss resulting from an employee transferring escrow funds from an account of the insured in reliance upon fraudulent email instructions received from a criminal purporting to be a legitimate party to the transaction.

Professional Services are broadly defined as those services performed by any insured for a fee in any of the following capacities:● Title Insurance Agent ● Escrow Agent ● Title Abstractor ● Closing Agent● Title Searcher ● Notary Public

Prior Acts Coverage – All claims caused by wrongful acts subsequent to the retroactive date and before the end of the policy period are covered.

Claims caused by independent contractors are covered

Claims related to a defect or deficiency not record in the public records is covered.

CFPB Coverage (RECENTLY ADDED) - $150,000 sub-limit of coverage for reasonable attorneys’ fees, costs and expenses for a CFPB Matter (subpoena, civil investigation, hearing, or civil action conducted or received by the CFPB).

Fraudulent Email Wire Transfer Coverage (RECENTLY ADDED) - THIRD PARTY COVERAGE: We will pay on behalf of an insured those sums insured become legally obligated to pay up to $1m for a covered loss resulting from an employee transferring escrow funds from an account of the insured in reliance upon fraudulent email instructions received from a criminal purporting to be a legitimate party to the transaction.

CFPB Coverage

$150,000 sub-limit of coverage for reasonable attorneys’ fees, costs and expenses for a CFPB Matter (subpoena, civil investigation, hearing, or civil action conducted or received by the CFPB).

Cyber LiabilitySecurity and Privacy LiabilityPrivacy Regulatory Defense & PenaltiesData Recovery & Loss of Business IncomeCustomer Notification and Credit Monitoring CostsData Extortion Multimedia Liability

The Escrow Security Bond (“ESB”) with computer crime rider offers protection for losses that Agents and Attorneys may incur as a result of fraudulent or dishonest acts by employees (including partners and shareholders). Dishonest acts which cause financial losses include many forms of embezzlement such as cash skimming, purchasing/payable fraud, kickbacks, gifts and gratuities, fictitious accounts receivables, personal expense reimbursement schemes etc. The ESB also offers first-party insurance for certain other losses that may be incurred as a result of computer crime, vandalism or theft, which may not be covered under other kinds of commercial first-party insurance policies or third-party liability insurance.

Computer Crime: This coverage fills a potential coverage gap by providing insurance for losses resulting directly from computer hacking or fraudulent wire transfers. Coverage exists for direct financial loss caused by hackers breaching the Insured’s computer systems and diverting Property/money from the Insured’s escrow, operating or IOLTA account at their bank to a fraudulent account controlled by the hacker.Example: A hacker infiltrates the Insured’s computer system and sends e-mails to the

Insured’s bank directing the bank to send funds to an account controlled/owned by the hacker. The bank wires the funds thinking that the requests were legitimate.

Tampering & Email Related Fraud Alert!!!“Business email compromise scams (BEC) tricking companies into sending large wire transfers has become the top fraud threat facing Financial Professionals”.◦ 7,000 US Victims for the period October 2013 thru August 2015◦ $750m in actual and attempted losses◦ 270% increase in identified victims since January 2015

FBI Public Service Announcement – August 2015

“Criminals are targeting real estate transactions in an attempt to defraud lenders, real estate brokers, title companies and law firms – Hackers, email phishing and other cyber related crimes are at an all-time high”.Florida Land Title Association, August 2015

FNTG Agents have reported an alarming increase in fraudulent email wire instruction losses.Example: A criminal monitors the email traffic of the parties to a real estate transaction purporting to be an authorized party to the transaction, typically the seller or seller’s agent, changing the wire instructions misdirecting the funds to a fraudulent bank account.

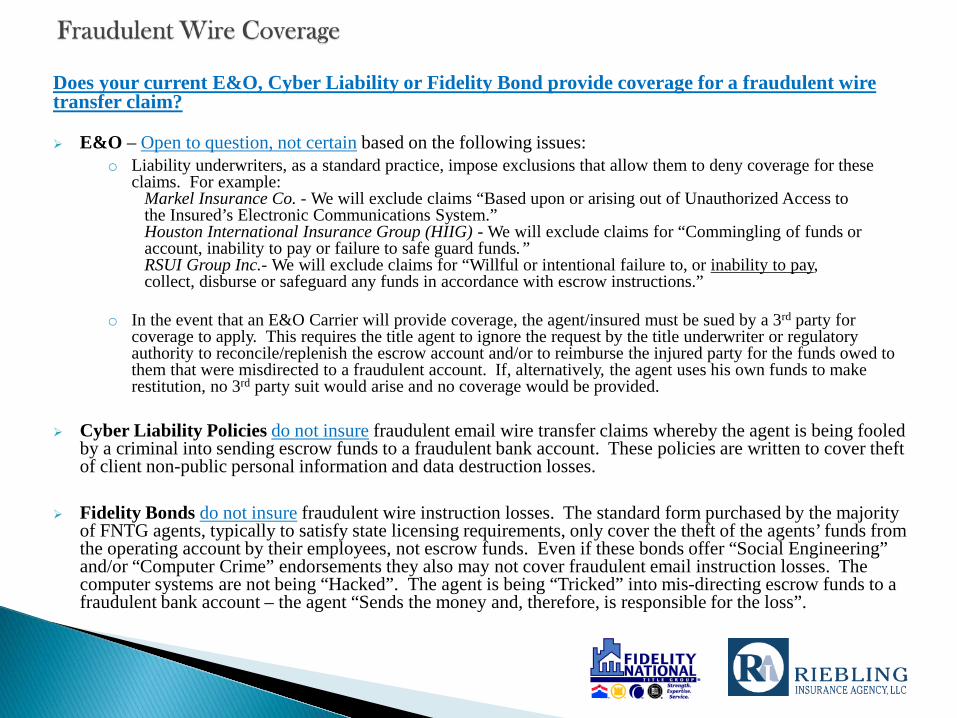

Does your current E&O, Cyber Liability or Fidelity Bond provide coverage for a fraudulent wire transfer claim?

E&O – Open to question, not certain based on the following issues:o Liability underwriters, as a standard practice, impose exclusions that allow them to deny coverage for these

claims. For example:Markel Insurance Co. - We will exclude claims “Based upon or arising out of Unauthorized Access to the Insured’s Electronic Communications System.”Houston International Insurance Group (HIIG) - We will exclude claims for “Commingling of funds or account, inability to pay or failure to safe guard funds.”RSUI Group Inc.- We will exclude claims for “Willful or intentional failure to, or inability to pay, collect, disburse or safeguard any funds in accordance with escrow instructions.”

o In the event that an E&O Carrier will provide coverage, the agent/insured must be sued by a 3rd party for coverage to apply. This requires the title agent to ignore the request by the title underwriter or regulatory authority to reconcile/replenish the escrow account and/or to reimburse the injured party for the funds owed to them that were misdirected to a fraudulent account. If, alternatively, the agent uses his own funds to make restitution, no 3rd party suit would arise and no coverage would be provided.

Cyber Liability Policies do not insure fraudulent email wire transfer claims whereby the agent is being fooled by a criminal into sending escrow funds to a fraudulent bank account. These policies are written to cover theft of client non-public personal information and data destruction losses.

Fidelity Bonds do not insure fraudulent wire instruction losses. The standard form purchased by the majority of FNTG agents, typically to satisfy state licensing requirements, only cover the theft of the agents’ funds from the operating account by their employees, not escrow funds. Even if these bonds offer “Social Engineering” and/or “Computer Crime” endorsements they also may not cover fraudulent email instruction losses. The computer systems are not being “Hacked”. The agent is being “Tricked” into mis-directing escrow funds to a fraudulent bank account – the agent “Sends the money and, therefore, is responsible for the loss”.

Important!!Fidelity-Pak is now insuring FNTG agents for fraudulent email wire instruction claims. As of January 1, 2016, Underwriters at Lloyds are providing the following enhancements to Fidelity-Pak policyholders:

E & O Fraudulent Instruction Rider - Summary o THIRD PARTY COVERAGE: We will pay on behalf of an insured those sums insured

becomes legally obligated to pay up to $1M for covered loss caused by an employee of the insured transferring funds from an account of the insured in reliance upon fraudulent instructions received from a criminal purporting to be a legitimate party to the transaction.

ESB / Computer Crime Fraudulent Instruction Rider - Summaryo FIRST PARTY COVERAGE: We will pay directly to the insured up to $250,000 for

covered loss caused by an employee of the insured transferring funds from an account of the insured in reliance upon fraudulent instructions received from a criminal purporting to be a legitimate party to the transaction.

To obtain information regarding theFidelity-Pak Program

and receive an application/quote,contact Dan Riebling at 516-280-6761

or email [email protected]