last time course logistics course goals what is transportation logistics and why is it important?...

Post on 20-Dec-2015

220 views

TRANSCRIPT

Last Time

• Course logistics

• Course goals

• What is Transportation Logistics and why is it important?

• Different approaches to Transportation Logistics

Supply Chain of an Individual Firm

VendorsPlantsports

warehouse Factory DestinationCustomers

Transportation (rail, marine, road)

Transportation(e.g. long haul truck)

Transportation(e.g. local delivery truck)

warehouse

Transportation(e.g. LTL truck)

Information flow(security, internal management, and control)

Supply Distribution

Conflict between consumer oriented and inventory managementOperators, owners, managersSpatial distribution

Supply chains

• In a pull chain finished products are manufactured when requested.

• In a push chain production and distribution are based on forecasts.

• This has integrated inventory management into business planning

Transportation Goals

• Reduce cost (5-10% of sales)

• Meet reliability goals

• Meet service quality goals

• Simplify operations

Integration of Logistics into Business Operations

• Operational, or daily decisions are made by comparing transportation and inventory costs

• Strategic, or long term decisions are made by comparing logistics costs (transportation and inventory) to manufacturing and production costs

• Lengthening of supply chains as transportation cost decreased and new opportunities to reduce manufacturing cost were found

Logistics Costs

Initial gains from deregulation (restructuring of networks) dropping off$1000 reduction to each household annually

How does REI get goods to market?

Asian Factories

West CoastPort

Distribution Center

Destination Store

Container on marine vessel

Drayage truck

Short orLong-haul

truck

Due to infrastructure government infrastructure investments and decreases in Transportation cost, transportation cost is typically much less significant than theReductions in manufacturing. Inventory management has been the area of attention.

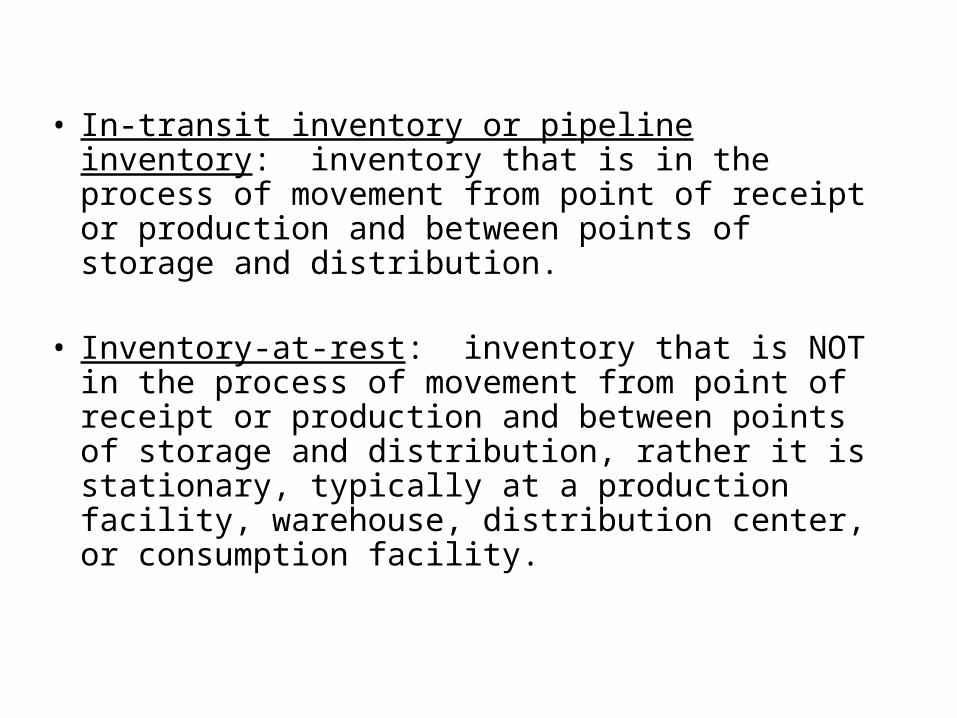

• In-transit inventory or pipeline inventory: inventory that is in the process of movement from point of receipt or production and between points of storage and distribution.

• Inventory-at-rest: inventory that is NOT in the process of movement from point of receipt or production and between points of storage and distribution, rather it is stationary, typically at a production facility, warehouse, distribution center, or consumption facility.

How does REI get goods to market?

Asian Factories

West CoastPort

Distribution Center

Destination Store

Container on marine vessel

Drayage truck

Short orLong-haul

truck

In transit inventory

• Cycle Inventory: the average amount of inventory used to satisfy demand between receipt of supplier shipments. The size of the cycle inventory is a result of the production or purchase of material in large lots. Companies produce or purchase in large lots to exploit economies of scale in the production, transportation, or purchasing process. With the increase in lot size, however, also comes an increase in carrying costs. The basic trade-off supply managers face is the cost of holding larger lots of inventory (when cycle inventory is high) versus the cost of ordering product frequently (when cycle inventory is low). Some of this inventory may be in-transit, while some may be inventory-at-rest.

• Safety inventory: inventory held in case demand exceeds expectation; it is held to counter uncertainty. If they have too much safety inventory, goods go unsold and may have to be discounted. If the company has ordered too little safety inventory, however, the company will lose sales and the margin those sales would have brought. Therefore, choosing safety inventory involves making a trade-off between the costs of having too much inventory and the costs of losing sales due to not having enough inventory. Generally this inventory is inventory-at-rest, so that it is immediately available.

Infrastructure Consequences

• Global Flows

• North American Flows

• Regional Flows

• Local Flows

January trade balance (millions of dollars)

January exports (millions of dollars)

January imports (millions of dollars)

APEC -43,703.2 58,735.7 102,438.8Pacific Rim Countries -29,649.3 23,801.6 53,450.8OECD -23,997.1 65,351.1 89,348.2OPEC -15,530.6 4,575.2 20,105.8North America -11,006.6 32,287.4 43,293.9LAFTA -9,248.0 17,982.5 27,230.5NATO Allies -9,122.3 41,147.5 50,269.7Twenty Latin American Republics -8,305.3 20,366.5 28,671.7Africa -7,904.2 1,954.8 9,859.1European Union -6,053.4 21,278.5 27,331.9Asia Near East -4,283.5 4,315.0 8,598.5ASEAN -4,133.0 5,404.2 9,537.2South/Central America -3,211.6 9,871.8 13,083.4Asia - SOUTH -1,722.4 1,350.4 3,072.8NICS -716.6 8,711.2 9,427.8Central American Common Market 315.2 1,439.8 1,124.6

Global Trade Regions

US Trading PartnersMillions of dollars Trade

Balance Rank Exports Rank Imports Rank

TOTAL -67,111.8 (X) 99,355.5 (X) 166,467.3 (X)

China -20,312.8 1 5,854.9 3 26,167.7 2

Japan -6,592.0 2 5,161.3 4 11,753.3 4

Canada -5,865.3 3 20,409.0 1 26,274.4 1

Mexico -5,141.2 4 11,878.3 2 17,019.6 3

Venezuela -3,419.5 5 767.7 25 4,187.2 8

Nigeria -3,413.0 6 235.3 47 3,648.2 10

Saudi Arabia -3,390.6 7 828.5 24 4,219.1 7

Federal Republic of Germany -2,903.9 8 4,061.7 6 6,965.6 5

Italy -1,714.8 9 1,212.1 18 2,926.9 13

Malaysia -1,700.8 10 1,060.4 21 2,761.2 14

Algeria -1,687.6 11 75.5 74 1,763.1 20

Angola -1,413.5 12 93.8 68 1,507.3 23

Ireland -1,381.3 13 739.5 28 2,120.8 17

India -1,228.3 14 1,078.4 20 2,306.7 15

Korea, South -1,184.8 15 2,740.2 8 3,924.9 9

France -1,180.4 16 2,145.2 13 3,325.7 11

Russia -1,148.4 17 557.6 31 1,706.0 21

Iraq -1,124.7 18 243.5 46 1,368.2 25

Thailand -1,094.7 19 738.6 29 1,833.3 19

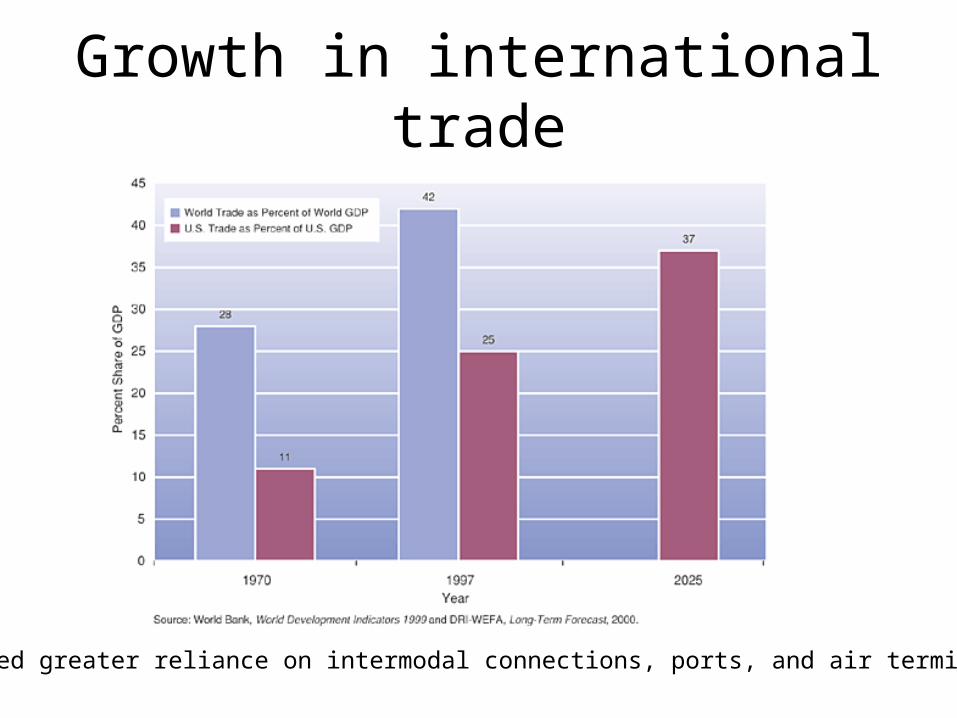

Growth in international trade

Caused greater reliance on intermodal connections, ports, and air terminals

Growth not from neighbors

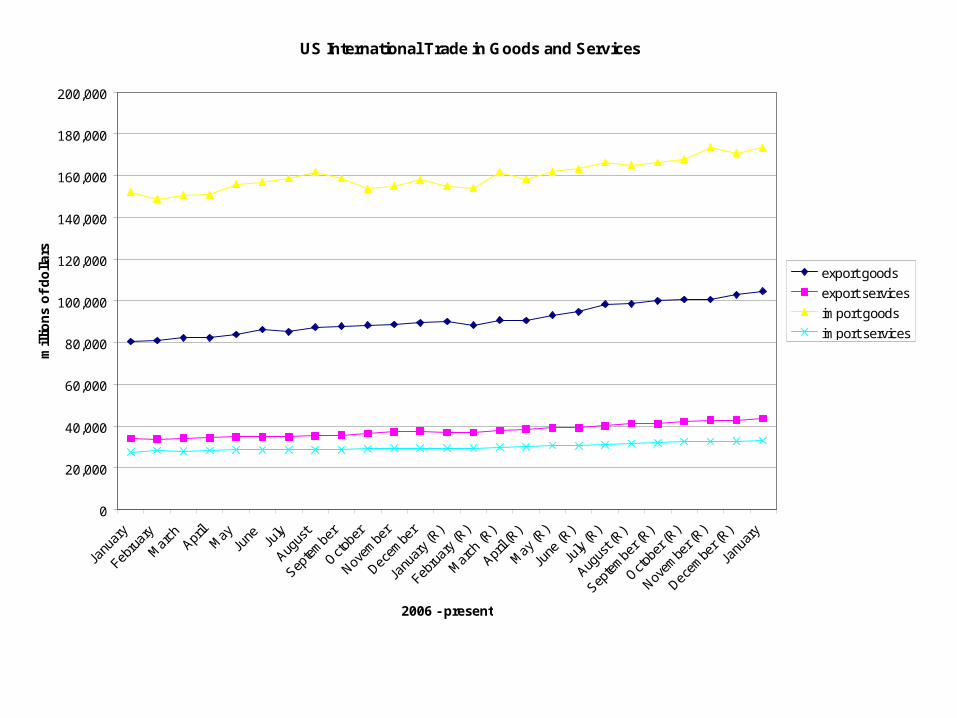

US International Trade in Goods and Services

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Janu

ary

Febru

ary

Mar

chApr

ilM

ayJu

ne July

Augus

t

Septe

mbe

r

Octobe

r

Novem

ber

Decem

ber

Janu

ary (

R)

Febru

ary (

R)

Mar

ch (R

)

April (

R)

May

(R)

June

(R)

July

(R)

Augus

t (R)

Septe

mbe

r (R)

Octobe

r (R)

Novem

ber (

R)

Decem

ber (

R)

Janu

ary

2006 - present

mil

lio

ns

of

do

lla

rs

export goods

export services

import goods

import services

The West Coast?

• Trade Statistics (see additional pdf)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Long Beach

Los Angeles

Oakland

Seattle

Tacoma

Portland(OR)

Charleston

New York/New Jersey

Houston

Vancouver (BC)

US Port Throughput (TEU)

Major Gateways

Importance of east-west corridors

West Coast Terminal Area has increased

Terminal growth over the period 1985-2005

0.0

5000.0

10000.0

15000.0

20000.0

25000.0

30000.0

35000.0

1985

1988

1989

1994

1996

1997

1998

2000

2001

2002

2003

2004

2005

Years

Ter

min

al a

rea(

acre

s)

Terminal area

Berth Length

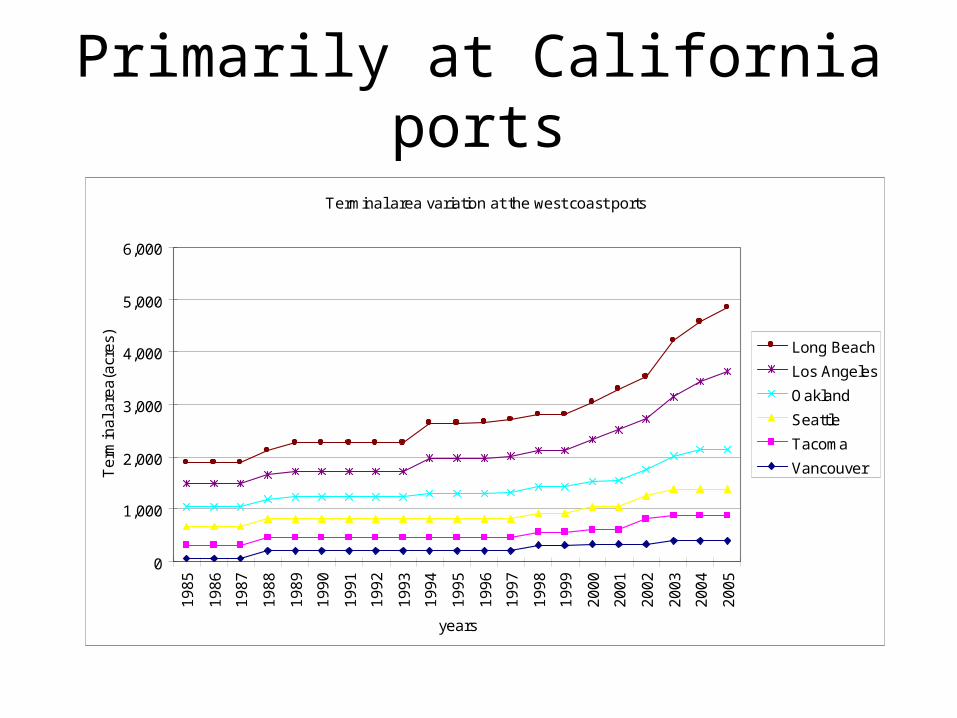

Primarily at California ports

Terminal area variation at the west coast ports

0

1,000

2,000

3,000

4,000

5,000

6,000

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

years

Ter

min

al a

rea(

acre

s) Long Beach

Los Angeles

Oakland

Seattle

Tacoma

Vancouver

Throughput density (TEUs/acre) variation across west coast ports

Throughput densi ty var i at i on across west coast ports dur i ng 1985- 2005

0

1000

2000

3000

4000

5000

6000

7000

Year

Thro

ughp

ut d

ensi

ty(T

EUs/

acre

) Long BeachLos Angel esOakl andSeat t l eTacomaVancouver (BC)

Similarly with berth lengthBerth length variation at the west coast ports

0

20,000

40,000

60,000

80,000

100,000

120,000

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

Years

Ber

th le

ngth

(feet

)

Long Beach

Los Angeles

Oakland

Seattle

Tacoma

Vancouver

Berth length (TEUs/ft) utilization at west coast ports

Berth l ength ut i l i sat i on across west coast ports dur i ng 1985- 2005

0

50

100

150

200

250

300

350

Year

Bert

h le

ngth

uti

lisa

tion

(TEU

s/ft

)

Long BeachLos Angel esOakl andSeat t l eTacomaVancouver (BC)

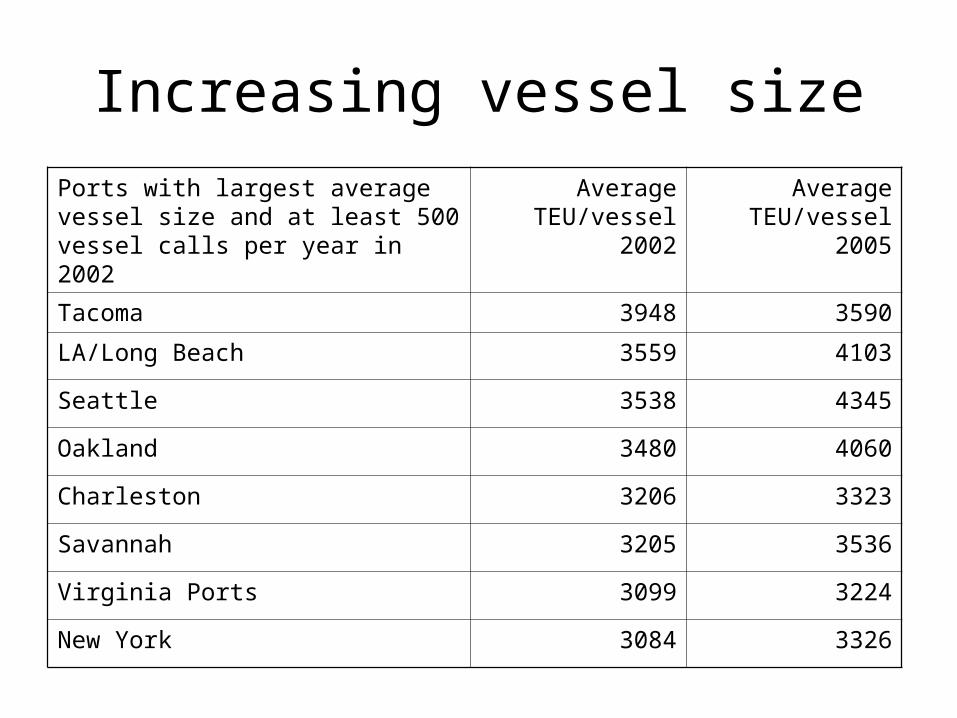

Increasing vessel size

Ports with largest average vessel size and at least 500 vessel calls per year in 2002

Average TEU/vessel 2002

Average TEU/vessel 2005

Tacoma 3948 3590

LA/Long Beach 3559 4103

Seattle 3538 4345

Oakland 3480 4060

Charleston 3206 3323

Savannah 3205 3536

Virginia Ports 3099 3224

New York 3084 3326

Shifting warehousing patterns

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

0 2 4 6 8 10 12 14 16 18

King Employment

King Avg Wage

Pierce Employment

Pierce Avg Wage