l6: dealing with capital flows: the role of ... · albania • armenia • azerbaijan • belarus...

TRANSCRIPT

ALBANIA • ARMENIA • AZERBAIJAN • BELARUS • BOSNIA AND HERZEGOVINA • BULGARIA • CROATIA • CZECH REPUBLIC • ESTONIA • GEORGIA HUNGARY • KAZAKHSTAN • KOSOVO • KYRGYZREPUBLIC • LATVIA • LITHUANIA • FYR MACEDONIA • MOLDOVA • MONTENEGRO • POLAND ROMANIA • RUSSIAN FEDERATION • SERBIA • SLOVAK REPUBLIC • SLOVENIA • TAJIKISTAN • TURKEY •TURKMENISTAN • UKRAINE • UZBEKISTAN

Asel Isakova, Economist, JVI

L6: DEALING WITH CAPITAL FLOWS: THE ROLE OF MACROPRUDENTIAL POLICYJVI COURSE ON MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY MARCH 21-25, 2016

The views expressed in this presentation are those of the author and do not necessarily represent those of theJoint Vienna Institute (JVI) or JVI policy. This presentation is the property of the JVI. Any reuse requires thepermission of the JVI.

Outline

Macroprudential Policy: Introduction

Tools of Macroprudential Policy

Use of Macroprudential Policy: Cross-Country Evidence

www.jvi.org [email protected] 2

Crisis has changed the consensus calling for a dedicated policy • Despite good macroeconomic management and results this

policy framework was unable to prevent the build-up of systemic financial risk

• The crisis has shown that a dedicated policy rather than a policy mix is necessary to contain systemic risks

• Thus, macroprudential policy was assigned a role of overseeing the whole system

www.jvi.org [email protected] 4

Poll No 1. What is a systemic risk?1. A risk associated with a failure of a large financial institution2. A risk associated with a failure of any individual entity, group or

component of a system3. A risk of a collapse of the whole financial system or entire market

www.jvi.org [email protected] 6

Motivation for macroprudential policy• Linkages between macroeconomic and financial market

developments create a number of externalities

• Certain externalities give rise to procyclicality and systemic risk:Externalities related to strategic complementarities: build-up of

vulnerabilities during the expansionary phase of financial cycleExternalities related to fire sales and credit crunches: drying up of finances,

deterioration of balance sheets, especially during contractionExternalities related to interconnectedness: propagation of shocks and

contagion

www.jvi.org [email protected] 7

Macrofinancial linkages and externalities

www.jvi.org [email protected] 8

Households

HouseholdsFirms

Firms

Banks

Rest of the world

Government

Build up of vulnerabilities (systemic risk) during boom: • highly leveraged banks• highly indebted

households and corporates

• growing indebtedness in foreign exchange

Macrofinancial linkages and externalities

www.jvi.org [email protected] 9

Households

HouseholdsFirms

Firms

Banks

Rest of the world

GovernmentCredit crunch, balance sheet problems in banks:• Low liquidity coverage• Rising NPLs• Capital losses

Macrofinancial linkages and externalities

www.jvi.org [email protected] 10

Households

HouseholdsFirms

Firms

Banks

Rest of the world

GovernmentInterconnectedness:• Realized systemic risk• Defaults• Economic recession

Thus, macroprudential policy should address

• Objectives and tasks of macroprudential policy are:(i) to increase resilience of financial system to shocks(ii) to contain build-up of systemic vulnerabilities over time (time dimension)(iii) to control build-up of risks linked to interlinkages (structural/cross-sectoral

dimension, strategically important financial institutions)

• Macroprudential policy uses primarily prudential tools to limit systemic risk

www.jvi.org [email protected] 11

Capital inflows and buildup of systemic risk

• Procyclicality in domestic financial sector can interact with capital flows When local funds are exhausted, banks turn to international sources Presence of foreign banks further increases financial cycle (70% of market in

EMs)

• Capital flows (through banks) lead to financial sector vulnerabilities: Balance sheet vulnerabilities – currency mismatch, maturity mismatch Credit risk due to lending in FX to unhedged borrowers Bank leverage and loan-to-deposit ratios rise Deterioration of lending standards

www.jvi.org [email protected] 12

Capital Inflow Surge

Financial Stability RisksMacroeconomic Concerns

Macro policies:• Exchange rate;• Reserves;• Monetary-Fiscal

policy mix

Prudential policies:

• Strengthen/Introduce prudential measures

Impose/Intensify Capital Controls

www.jvi.org [email protected]

Policy options to manage capital inflows

• Real exchange rate appreciation;

• Overheating of the economy and inflation

• Credit boom;

• Price bubbles;

• Unhedged FX currency exposure of banks and borrowers;

• FX lending to unhedged borrowers, etc.

Source: Ostry et al., 2010, Capital Inflows: The Role of Controls, IMF Staff Position Note, 10/04.

Macro- vs microprudential policy: time dimension

Phases of the credit cycle

www.jvi.org [email protected] 14

Upswing: both policies encourage build-up of buffers

Boom and peak: microprudpolicy does not intervene, macroprud encourages buildup of buffers Recovery: both policies

agree on build-up of buffers again but opinions may differ in timing and intensity

Downturn: tensions arise – microprud policy to ensure stability of individual firms; macroprud to stabilise the whole system

Macroprudential and monetary policy

• New paradigm: both are used in countercyclical management (one for price stability, another for financial stability)

• Potential “side effects”: policy rate can enhance risk taking incentives of economic agents (cost of borrowing, loose credit conditions, exchange rates and FX borrowing)

• Overcoming “side effects”: e.g. accommodative monetary policy can be counterbalanced by tighter macroprudential measures

www.jvi.org [email protected] 15

Macroprudential measures and capital flows

• In the times of capital inflow surges, macroprudential tools are usually not sufficient to slow down the inflows macroeconomic adjustment might be needed or other capital flow

management measures

• The aim of macroprudential tools is to create buffers in the financial system against shocks caused by possible capital flow reversals

www.jvi.org [email protected] 16

Capital flow management (CFM) and macroprudential measures (MPM)• CFMs and MPMs are similar but their primary objectives do not

necessarily overlap

• CFM and MPM tools may overlap: capital flows are the source of systemic financial sector risk and tools used to address those risks can be seen as both CFMs and MPMs

• An important distinction is between MPMs and CFMs: CFM aims at limiting capital flows Macroprudential measures seek to limit systemic risks (that may

be related to capital inflows)

www.jvi.org [email protected] 17

Outline

Macroprudential Policy: Introduction

Tools of Macroprudential Policy

Use of Macroprudential Policy: Cross-Country Evidence

www.jvi.org [email protected] 18

Operationalizing macroprudential policy is challenging

5 steps to Operationalize Macroprudential Policy

Source: IMF policy paper (2013)www.jvi.org [email protected] 19

Assessing systemic risk requires effective monitoring

Monitoring systemic risk needs to consider:

• Growth in total credit and macroeconomic drivers of imbalances

• Financial linkages b/w financial and real sector and the rest of the world

• Structure of financial system and linkages within and across key classes of intermediaries and market infrastructures

www.jvi.org [email protected] 20

Strong increase in credit can be a signal of a systemic risk

• Empirical evidence on best indicators of a crisis over 1-3 years: growth in credit to private sector “credit gap”

• Not all credit booms end in bust if justified by fundamentals can contribute to healthy financial deepening

• Important to consider macro environment that gives rise to credit

www.jvi.org [email protected] 21

Illustration: Financial cycle and macroeconomic development

The Financial and Business Cycles in the U.S.

Financial cycle (credit and property prices)

Business cycle (GDP)

www.jvi.org [email protected] 22

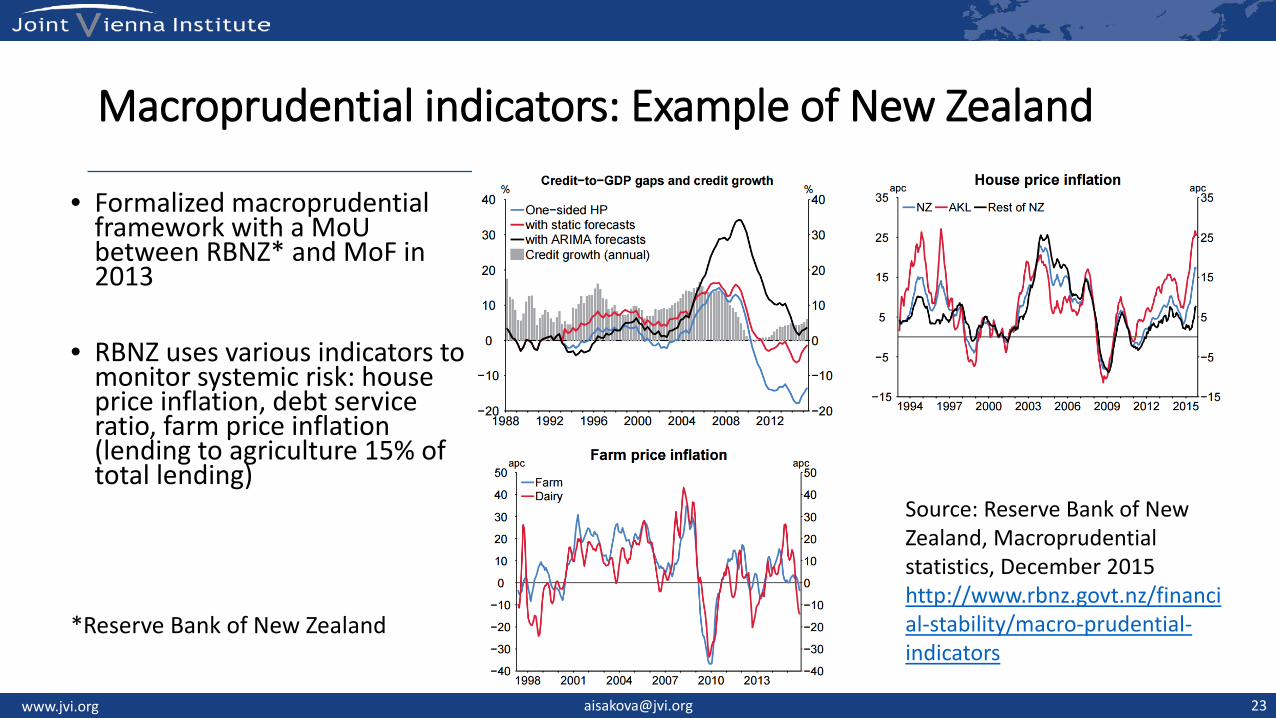

Macroprudential indicators: Example of New Zealand

• Formalized macroprudential framework with a MoUbetween RBNZ* and MoF in 2013

• RBNZ uses various indicators to monitor systemic risk: house price inflation, debt service ratio, farm price inflation (lending to agriculture 15% of total lending)

*Reserve Bank of New Zealand

www.jvi.org [email protected] 23

Source: Reserve Bank of New Zealand, Macroprudential statistics, December 2015http://www.rbnz.govt.nz/financial-stability/macro-prudential-indicators

Macroprudential toolkit: types by objectives

In the time dimension

Countercyclical capital buffers and provisions

Sectoral tools Liquidity tools

Increase resilience to

shocks

Contain risks in particular sectors

Contain funding risks

www.jvi.org [email protected] 24

In the cross-section dimension

Tools aimed at SIFI

Capital surcharges

Countercyclical capital buffer (CCB)• Proposed by the Basel committee within Basel III accord that was developed in

response the recent financial crisis: time-varying capital buffer on top of minimum capital requirements (max 2.5%)

• Aims to make banks more resilient against imbalances in credit market

• May help to reduce procyclicality of bank lending: build-up of additional capital in a boom may diminish banks’ willingness to lend excessively

• Should be released promptly in times of crises and should be complimented with other macroprudential tools

www.jvi.org [email protected] 25

CCB: an illustration

• A bank should comply with certain regulatory requirements and hold capital:

CAR = 𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝑅𝑅𝐶𝐶𝑅𝑅𝑅𝑅 𝑊𝑊𝑊𝑊𝐶𝐶𝑊𝑊𝑊𝐶𝐶𝑊𝑊𝑊𝑊 𝐴𝐴𝑅𝑅𝑅𝑅𝑊𝑊𝐶𝐶𝑅𝑅

• Then CCB is an additional requirement between 0 and 2.5 %

www.jvi.org [email protected] 26

Hypothetical path of the CCB for Spain Figure: Simulated Countercyclical Capital Buffer

(In % of risk weighted assets)

www.jvi.org [email protected] 27

Only domestic exposure

Internationalexposure

Reciprocity principle in determining CCB

• Each jurisdiction determines the CCB for credit exposures to counterparties in its country

• Internationally active banks CCB is calculated on a consolidated basis according to geographic location of its exposures

• Home supervisor is not allowed to impose a buffer requirement for credit exposure to a foreign country that is below the requirement of the host supervisor

www.jvi.org [email protected] 28

Reciprocity principle: an illustration

Country A:CCB = 2%

Bank 1 A = 100% domesticBank 2 A = 60% domestic

Country B:CCB = 1%

Bank 1 B = 20% domesticBank 2 B = 50% domestic

B

A

www.jvi.org [email protected] 29

Poll No 2. Exercise: calculate CCB for Bank 1A and Bank 2A

Option 1 2% for both

Option 2 2% and 1.6%

Option 32% and 3%

www.jvi.org [email protected] 30

Reciprocity principle: an illustration

Country A:CCB = 2%

Bank 1 A = 100% domesticBank 2 A = 60% domestic

Country B:CCB = 1%

Bank 1 B = 20% domesticBank 2 B = 50% domestic

B

ACCB calculation:

Bank 1 A = 2% * 100 % = 2%Bank 2 A = 2% * 60% + 1% * 40% = 1.6%

Bank 1 B = 1% * 20% + 2% * 80% = 1.8%Bank 2 B = 1% * 50% + 2% * 50% = 1.5%

www.jvi.org [email protected] 31

Limiting sectoral imbalances and risks

• If risks are building up in a particular sector (e.g. consumer loans, corporate exposures, etc.), then sectoral instruments are appropriate tools

• Sectoral tools can affect credit demand (limits on mortgage loans) or credit supply (sectoral capital requirements)

• Various tools can be used: Loan-to-Value limits (LTV), Debt-to-Income limits (DTI), sectoral capital requirements (e.g. housing loans, FX lending to unhedged borrowers)

www.jvi.org [email protected] 32

Limits on LTV and DTI: demand-side considerations

• Lowering limits on LTV ratio can tighten constraints of targeted borrowers and thus limit housing demand in targeted segments of the real estate market

• Limits on LTV and DTI ratios can enhance financial institutions’ resilience to house price shocks

• These measures have been found successful in containing mortgage loan growth, speculative real estate transactions and house price acceleration

www.jvi.org [email protected] 33

Loan-to-Value Ratio: Case of Hong-Kong

• Banking system assets 750% of GDP

• Residential mortgage lending – a source of largest risk for Hong-Kong banks: 20% of total lending in 1991, 37% in

2002

• Property prices in Hong-Kong exhibited strong cyclical patterns

www.jvi.org [email protected] 34Source: IMF Working paper 15/123

Loan-to-Value Ratio: Case of Hong-Kong (cont.)

• Hong-Kong Monetary Authority (HKMA) does not conduct independent monetary policy In 1991 introduced LTV of 70% to strengthen banks’ resilience to asset price

volatilities Since 1997 LTV of 60% for luxury properties (HK$ 12 million) After Asian crisis, 70% LTV is kept, however introduced mortgage insurance

program (MIP) to promote wider home ownership – allowed 90% LTV for certain buyers

After 2009, sharp increase in property prices, strong capital inflows, LTV was gradually decreased to 50-60% depending on value of property

In November 2010 introduced Special Stamp Duty (SSD) of up to 15% on residential properties resold within 24 months of purchase

www.jvi.org [email protected] 35

Liquidity tools to deal with funding shocks

• Excessive credit expansion is often funded by short-term wholesale funding as stable deposits tend to grow slower

• Banks in small open economies depend on short-term (often FX) wholesale funding building a maturity and currency mismatches

• Basel III includes measures such as Liquidity Coverage ratio (LCR) and Net Stable Funding Ratio (NSFR)

www.jvi.org [email protected] 36

Liquidity measures: Case of Korea• From 2005 banks rapidly increased short term non-core FX borrowing

creating FX mismatches: the crisis stopped the surge as wholesale funding market froze

• Macroprudential Stability Levy (MSL) was adopted in August 2011 as a proportion to each bank’s marginal contribution to systemic risk, i.e. daily average balance of non-deposit FX liabilities of maturity up to a year

• Korea also introduced caps on the loan-to-deposit ratio (2012) and ceilings on banks’ FX derivative positions

www.jvi.org [email protected] 37

Liquidity measures: Case of Korea (cont.)

• MSL was effective; banks reliance on short-term FX funding decreased

• Banks’ short term FX liability dropped by 9.3 per cent (US$ 14.4 billion) in 2012 q3

www.jvi.org [email protected] 38

Figure: Measures in Korea had a desirable effect on short-term FX funding (In % and US$ bn)

www.jvi.org [email protected] 39

Source: National statistics

Foreign Currency Lending

FX loans (In per cent of total)

FX lending to households

www.jvi.org [email protected] 40

Source: National statistics

FX loans to households (In per cent of total FX)

• The risk to financial stability is high in countries with a large share of FX loans to unhedged borrowers: households and small firms

FX lending: case of countries in Central and Easter Europe

www.jvi.org [email protected] 41

• LTV and DTI for FX loans: Hungary (2010), Poland (2010, 2012), Romania (2008)

• Higher risk weights or capital requirements (Latvia (2009), Hungary (2008), Poland (2008 and 2012), Romania(2010))

• Higher provisioning for unhedged borrowers (Romania(2008))

• Limits to open FX positions or capital requirements for open foreign currency positions (Lithuania(2007), Romania(2001))

Cross-section tools: capital surcharge • Systemically important financial institutions: failure might trigger a

financial crisis

• After crisis: Basel III new regulations target SIFIs: Introduced capital surcharges for SIBs

• Factors to classify SIFIs: size, complexity, interconnectedness, lack of substitutes, global activity

www.jvi.org [email protected] 42

Capital surcharge: case of Denmark

• In Denmark, SIFIs are identified at group level once a year

• An institution is identified as a SIFI if at least one of the following quantitative criteria is met for two consecutive years: Balance sheet as a percentage of GDP > 6.5 per cent. Lending as a percentage of total sector lending > 5 per cent. Deposits as a percentage of total sector deposits > 5 per cent.

• SIFIs are subject to a SIFI capital buffer requirement of 1-3 per cent of their risk-weighted assets depending on their systemic importance

www.jvi.org [email protected] 43

Poll No 3: Which measures can help reduce/slow down increasing capital inflows?

1 Limiting loan-to-value ratio

2Countercyclical capital buffer

3Higher liquidity requirements

www.jvi.org [email protected] 44

Calibrating macroprudential tools and monitoring

• Relative strength of different tools and their benefits are subject to uncertainty

• Discretionary variation of macroprudential tools can be politically undesirable while static calibration may be inefficiently tight – a need for “guided calibration”

• A need to monitor migration of activity outside of reach of macroprudential tools

• Statistical and supervisory data needs more granularity, frequency, homogeneity and comparability

www.jvi.org [email protected] 45

Outline

Macroprudential Policy: Introduction

Tools of Macroprudential Policy

Use of Macroprudential Policy: Cross-Country Evidence

www.jvi.org [email protected] 46

Developing macroprudential framework

• In many countries, the macroprudential framework is currently being built European Systemic Risk Board (EU body to discuss and coordinate

macroprudential policy at an EU level) recommendation on macroprudential mandate

operational framework still being debated (rules versus discretion, conditioning variables, legal underpinning, EU constraints – single rulebook)

• With some exceptions, most of the experience with the tools based on their ad-hoc activationEmerging Europe coping with pre-crisis excessive credit growth (Croatia, Poland, Bulgaria

etc.)

www.jvi.org [email protected] 47

There is a need to assign macroprudential mandate: 3 models

Model 1: Central Bank: decisions

made by the Board

Model 2: Dedicated committee within a central bank structure

Model 3: Committee outside a central bank with participation of central bank

Czech RepublicBoard

UK Australia, France, USA

www.jvi.org [email protected] 48

Home-host issues in macroprudential regulation

• The cross-border operations of financial institutions complicate assessment of systemic risk

• Affiliates in multiple jurisdictions may lead to conflicts between home and host authorities

• A need for coordination: multilateral (Basel), regional and bilateral

• Reciprocity principle for the countercyclical buffer is an important step forward

www.jvi.org [email protected] 49

Overall use of macroprudential instruments

www.jvi.org [email protected] 50

Note: LTV – loan to value, DTI –debt-to-income, CG – limits on credit growth, FL – limit on foreign lending, RR – reserve requirements, DP – dynamic provisioning, CTC – counter-cyclical capital requirements

Source: Claessens (2014)

Empirical evidence on experiences

• Reducing procyclicaty: LTV and DTI, ceiling on credit growth, reserve requirements, dynamic provisioning

• Curbing credit booms and real estate booms: LTV, credit and interest controls, limits on open foreign exchange positions

• Limiting systemic liquidity risks: the case of Korea

www.jvi.org [email protected] 51

Concluding remarks• Crisis has revealed a large gap in policy making to foresee and prevent systemic

risks

• Macroprudential policy is emerging as a new consensus to deal with the system-wide vulnerabilities

• Macroprudential tools may directly or indirectly affect capital inflows and can compliment capital management measures and macroeconomic adjustment

• Successful implementation of macroprudential measures requires multilateral coordination

www.jvi.org [email protected] 52

References and suggested reading

Claessens, S., 2014, “An Overview of Macroprudential Policy Tools,” IMF Working Paper No. 14/214 (Washington: International Monetary Fund).http://www.imf.org/external/pubs/ft/wp/2014/wp14214.pdf

IMF Policy Paper “Key Aspects of Macroprudential Policy”: http://www.imf.org/external/np/pp/eng/2013/061013b.pdf

IMF Policy Paper “Key Aspects of Macroprudential Policy- Background Paper”: http://www.imf.org/external/np/pp/eng/2013/061013C.pdf

Ostry J. et al., 2011, “Managing Capital Inflows: What Tools to Use?” IMF Staff Discussion Note No. 11/06 (Washington: International Monetary Fund). http://www.imf.org/external/pubs/ft/sdn/2011/sdn1106.pdf

www.jvi.org [email protected] 53