kroger shadow anchored strip center -...

TRANSCRIPT

Kroger Shadow Anchored Strip Center4153 SR 128, Cleves, OH 45002

OFFERING MEMORANDUM

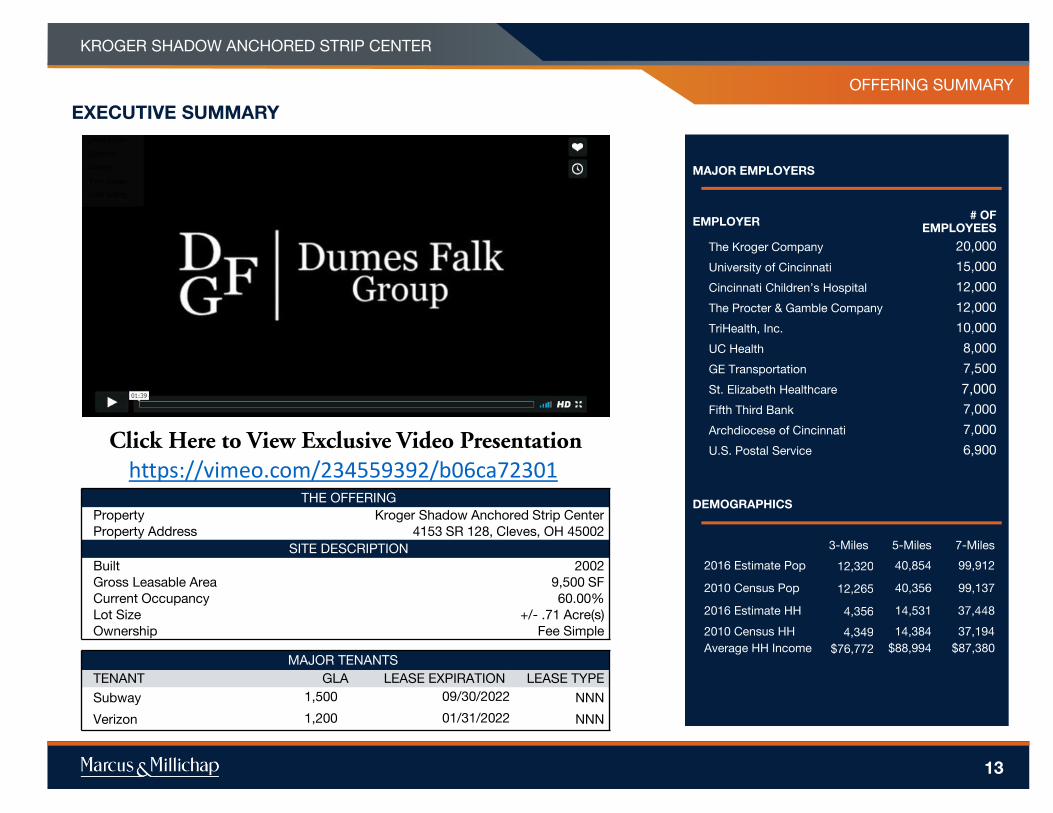

Click the Icon or Visithttps://vimeo.com/234559392/b06ca72301to View Exclusive Video Presentation

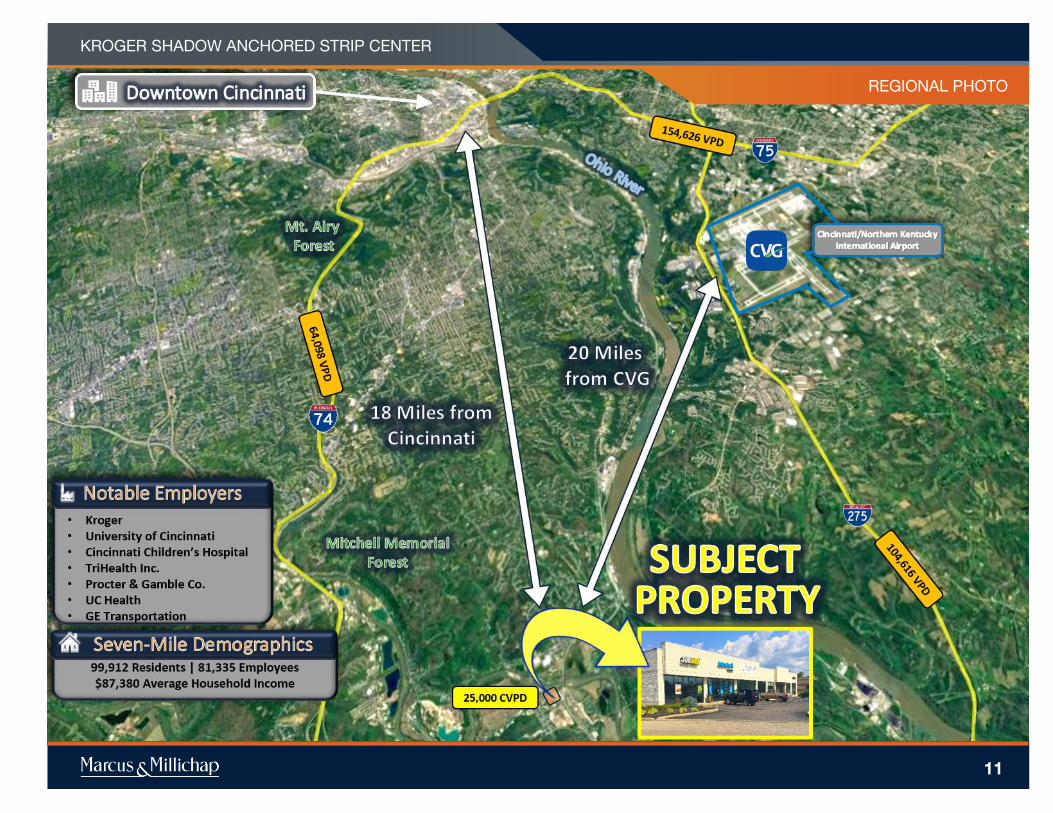

Downtown Cincinnati 18 MilesCVG International Airport 20 Miles

CLEVES KROGER ANCHORED

SHOPPING CENTER

Cleves, OH

ACT ID Y0360226

N O N - E N D O R S E M E N T A N D D I S C L A I M E R N O T I C E

Non-EndorsementsMarcus & Millichap is not affiliated with, sponsored by, or endorsed by any commercial tenant or lessee identified in

this marketing package. The presence of any corporation's logo or name is not intended to indicate or imply affiliation

with, or sponsorship or endorsement by, said corporation of Marcus & Millichap, its affiliates or subsidiaries, or any

agent, product, service, or commercial listing of Marcus & Millichap, and is solely included for the purpose of

providing tenant lessee information about this listing to prospective customers.

ALL PROPERTY SHOWINGS ARE BY APPOINTMENT ONLY.

PLEASE CONSULT YOUR MARCUS & MILLICHAP AGENT FOR MORE DETAILS.

DisclaimerTHIS IS A BROKER PRICE OPINION OR COMPARATIVE MARKET ANALYSIS OF VALUE AND SHOULD NOT BE

CONSIDERED AN APPRAISAL. This information has been secured from sources we believe to be reliable, but we

make no representations or warranties, express or implied, as to the accuracy of the information. References to

square footage or age are approximate. Buyer must verify the information and bears all risk for any inaccuracies.

Marcus & Millichap is a service mark of Marcus & Millichap Real Estate Investment Services, Inc. © 2017 Marcus &

Millichap. All rights reserved.

2

P R E S E N T E D B Y

Joel Dumes

Senior Vice President Investments

Senior Director - National Retail Group

Cincinnati Office

Tel: (513) 878-7720

Fax: (513) 878-7710

Licenses: OH SAL.2003013045, KY

63818

Stan Falk

First Vice President Investments

Director - National Retail Group

Cincinnati Office

Tel: (513) 878-7721

Fax: (513) 878-7710

License: OH SAL.2012001364

TABLE OF CONTENTS

INVESTMENT OVERVIEWSection 1

•

FINANCIAL ANALYSISSection 2

•

MARKET OVERVIEWSection 3

•

KROGER SHADOW ANCHORED STRIP CENTER

5

INVESTMENT

OVERVIEW

KROGER SHADOW ANCHORED STRIP CENTER

#

OFFERING SUMMARY

▪ Kroger Shadow Anchored Strip Center | Cincinnati, OH MSA

▪ 78 Percent of Income from National and Regional Tenants

▪ 3,800-Square Feet or 40 Percent of Realizable Vacancy Upside

▪ Positioned at Signalized Intersection | 25,000 Combined Vehicles Per Day

▪ Over 23 Percent Population Growth with Average Incomes of $89,000 in Five-Miles

▪ 18-Miles from Downtown Cincinnati | 20-Miles from the Cincinnati Airport (CVG)

INVESTMENT HIGHLIGHTS

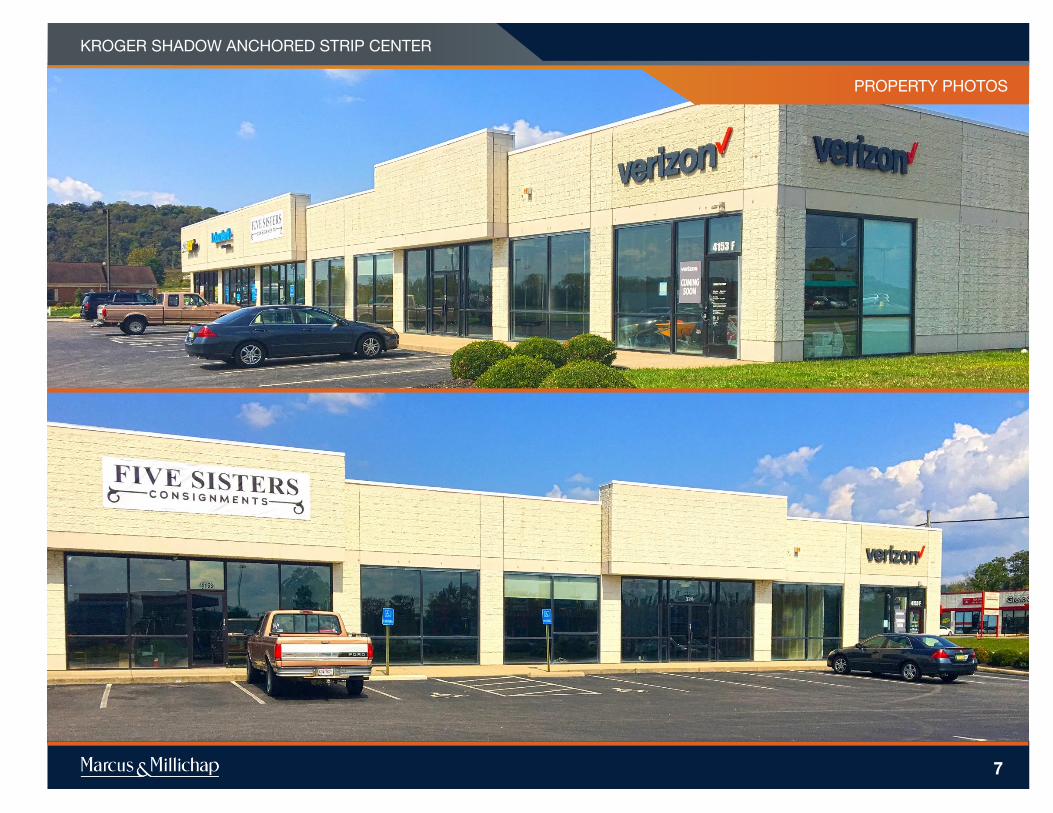

The Dumes Falk Group of Marcus & Millichap is please to bring to market a Kroger shadow anchored strip center comprised of 9,500-square feet

on approximately .71 acres in Cleves, OH – located 18-miles from downtown Cincinnati. The subject property is situated at a signalized

intersection with great signage, visibility and independent turn lanes into the center along OH-128, that combined with US-50, sees nearly 25,000

vehicles per day.

This Kroger shadow anchored strip center is currently 60 percent leased to four tenants with one remaining unit totaling 40 percent or 3,800-

square feet of vacancy upside. Leasing up the last remaining unit at market rates could nearly double the current NOI adding up to $45,000 to the

bottom line. Subway has occupied the center since the building was built in 2002 and occupies nearly 1,500-square feet or 16 percent of the GLA.

Jackson Hewitt joined the center in 2006 and occupies 1,500-square feet alongside Verizon Wireless and Five Sisters Consignments, who both

have recently signed their leases in 2017. This strip center contains a strong mix of nationally and regionally recognized tenants, all of which that

are under triple-net leases. The Kroger supermarket was originally constructed in 2001 and later developed the fuel station in 2004.

The village of Cleves is located on the westside of Cincinnati along the Great Miami River on US-50, less than 18-miles from downtown. Situated

less than two-miles away is Interstate-275, the Cincinnati loop that sees over 100,000 vehicles per day. The population has seen rapid growth of

more than twenty-three percent since 2000 with more than 40,000 residents and average household incomes of $89,000 in five-miles. The seven-

mile radius has seen growth of more than fifteen percent since 2000 with 100,000 residents and average household incomes of $87,300. There

are more than 81,000 employees in the same proximity which makes up the daytime population. Located on the other side of the river

approximately half a mile away from the center is Taylor High School, Taylor Middle School and Three Rivers Elementary School with a combined

enrollment of more than 2,500 students. The center is located less than 20-miles from the Cincinnati/Northern Kentucky International Airport, also

known as CVG.

This offering provides an incoming investor the ability to acquire a value-add Kroger shadow anchored center within a growing Cincinnati

submarket. This center should remain an integral part of the community and will continue to serve as a valued shopping destination for many of

the local residents.

INVESTMENT OVERVIEW

6

KROGER SHADOW ANCHORED STRIP CENTER

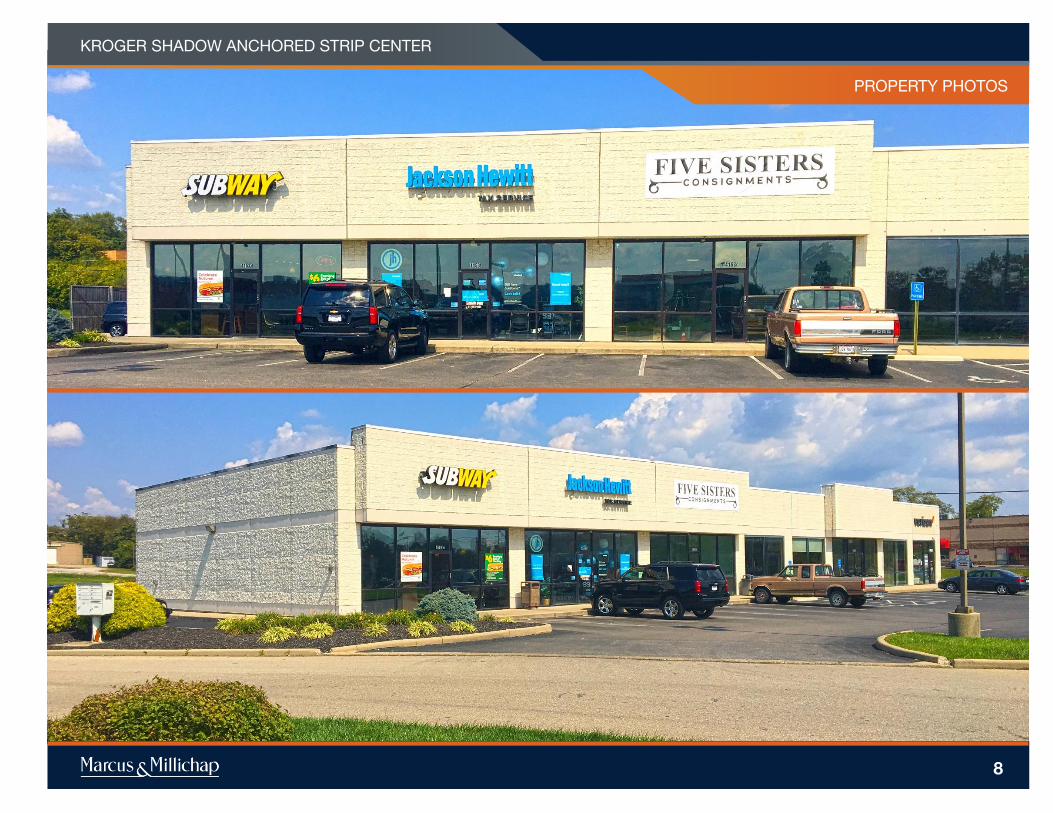

PROPERTY PHOTOS

7

KROGER SHADOW ANCHORED STRIP CENTER

PROPERTY PHOTOS

8

KROGER SHADOW ANCHORED STRIP CENTER

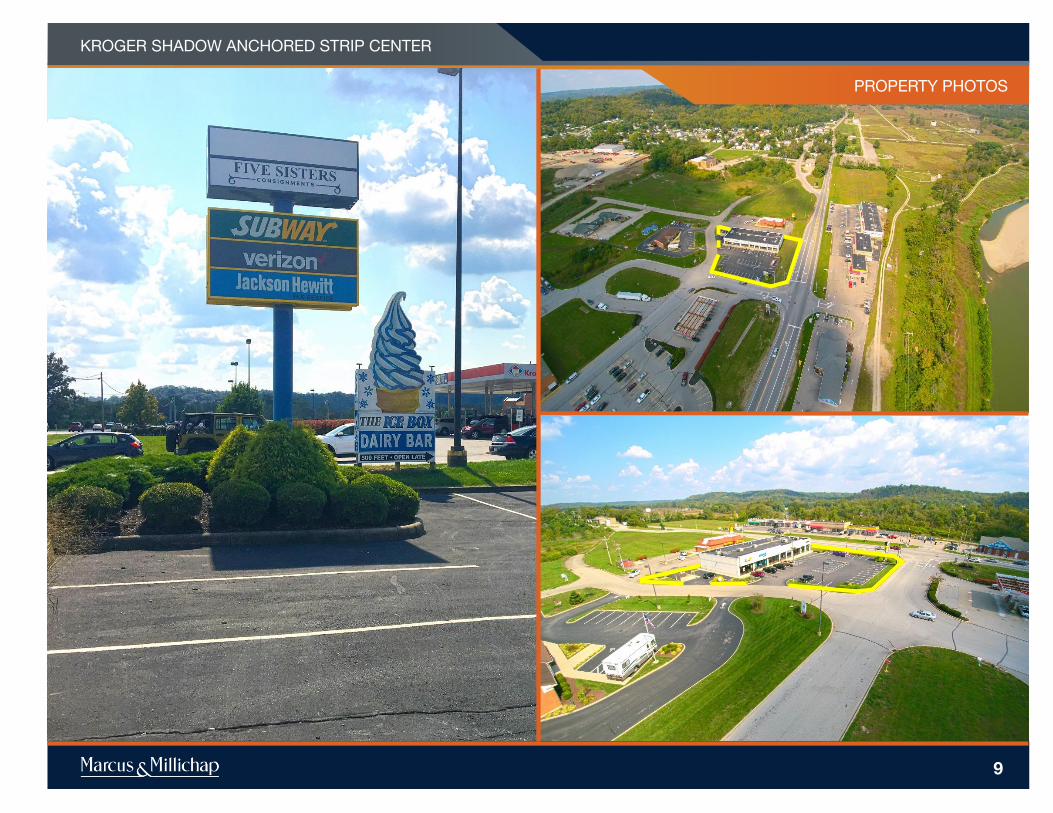

PROPERTY PHOTOS

9

KROGER SHADOW ANCHORED STRIP CENTER

Five

Sis

ters

C

on

sign

men

ts

VA

CA

NT

SITE PLAN

10

Dumpster Vacant Unit (3,800 SF) Pylon Sign

KROGER SHADOW ANCHORED STRIP CENTER

Opening Soon!

REGIONAL PHOTO

11

KROGER SHADOW ANCHORED STRIP CENTER

12

FINANCIAL

ANALYSIS

KROGER SHADOW ANCHORED STRIP CENTER

#

EXECUTIVE SUMMARY

OFFERING SUMMARY

13

THE OFFERING

Property Kroger Shadow Anchored Strip Center

Property Address 4153 SR 128, Cleves, OH 45002

SITE DESCRIPTION

Built 2002

Gross Leasable Area 9,500 SF

Current Occupancy 60.00%

Lot Size +/- .71 Acre(s)

Ownership Fee Simple

MAJOR TENANTS

TENANT GLA LEASE EXPIRATION LEASE TYPE

Subway 1,500 09/30/2022 NNN

Verizon 1,200 01/31/2022 NNN

MAJOR EMPLOYERS

EMPLOYER# OF

EMPLOYEES

The Kroger Company 20,000

University of Cincinnati 15,000

Cincinnati Children’s Hospital 12,000

The Procter & Gamble Company 12,000

TriHealth, Inc. 10,000

UC Health 8,000

GE Transportation 7,500

St. Elizabeth Healthcare 7,000

Fifth Third Bank 7,000

Archdiocese of Cincinnati 7,000

U.S. Postal Service 6,900

DEMOGRAPHICS

3-Miles 5-Miles 7-Miles

2016 Estimate Pop 12,320 40,854 99,912

2010 Census Pop 12,265 40,356 99,137

2016 Estimate HH 4,356 14,531 37,448

2010 Census HH 4,349 14,384 37,194

Average HH Income $76,772 $88,994 $87,380

https://vimeo.com/234559392/b06ca72301Click Here to View Exclusive Video Presentation

KROGER SHADOW ANCHORED STRIP CENTER

FINANCIAL ANALYSIS

14

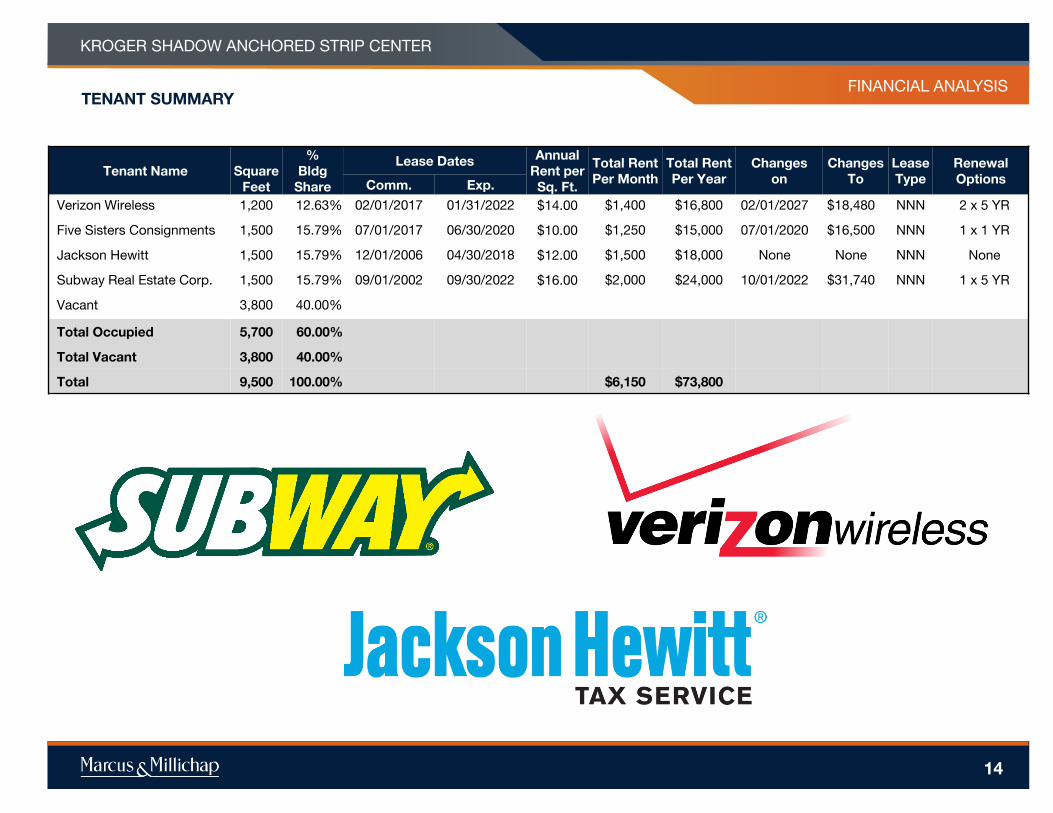

TENANT SUMMARY

Tenant Name Square

Feet

%

Bldg

Share

Lease DatesAnnual

Rent per

Sq. Ft.

Total Rent

Per Month

Total Rent

Per Year

Changes

on

Changes

To

Lease

Type

Renewal

OptionsComm. Exp.

Verizon Wireless 1,200 12.63% 02/01/2017 01/31/2022 $14.00 $1,400 $16,800 02/01/2027 $18,480 NNN 2 x 5 YR

Five Sisters Consignments 1,500 15.79% 07/01/2017 06/30/2020 $10.00 $1,250 $15,000 07/01/2020 $16,500 NNN 1 x 1 YR

Jackson Hewitt 1,500 15.79% 12/01/2006 04/30/2018 $12.00 $1,500 $18,000 None None NNN None

Subway Real Estate Corp. 1,500 15.79% 09/01/2002 09/30/2022 $16.00 $2,000 $24,000 10/01/2022 $31,740 NNN 1 x 5 YR

Vacant 3,800 40.00%

Total Occupied 5,700 60.00%

Total Vacant 3,800 40.00%

Total 9,500 100.00% $6,150 $73,800

KROGER SHADOW ANCHORED STRIP CENTER

TENANT SUMMARY

#

Subway

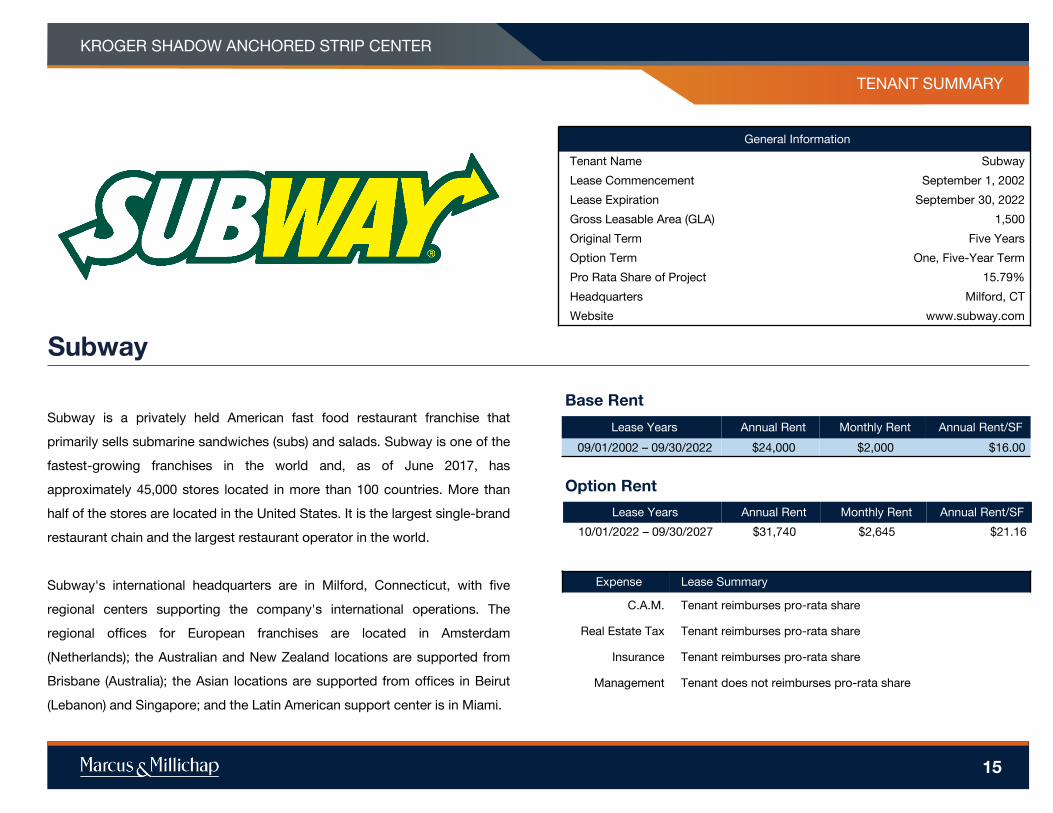

Subway is a privately held American fast food restaurant franchise that

primarily sells submarine sandwiches (subs) and salads. Subway is one of the

fastest-growing franchises in the world and, as of June 2017, has

approximately 45,000 stores located in more than 100 countries. More than

half of the stores are located in the United States. It is the largest single-brand

restaurant chain and the largest restaurant operator in the world.

Subway's international headquarters are in Milford, Connecticut, with five

regional centers supporting the company's international operations. The

regional offices for European franchises are located in Amsterdam

(Netherlands); the Australian and New Zealand locations are supported from

Brisbane (Australia); the Asian locations are supported from offices in Beirut

(Lebanon) and Singapore; and the Latin American support center is in Miami.

PRICING AND VALUATION MATRIX

PROPERTY NAMEOAKLEY STATION BUILDING

PRICING AND VALUATION MATRIX

PROPERTY NAME

15

TENANT SUMMARY

General Information

Tenant Name Subway

Lease Commencement September 1, 2002

Lease Expiration September 30, 2022

Gross Leasable Area (GLA) 1,500

Original Term Five Years

Option Term One, Five-Year Term

Pro Rata Share of Project 15.79%

Headquarters Milford, CT

Website www.subway.com

Lease Years Annual Rent Monthly Rent Annual Rent/SF

09/01/2002 – 09/30/2022 $24,000 $2,000 $16.00

Lease Years Annual Rent Monthly Rent Annual Rent/SF

10/01/2022 – 09/30/2027 $31,740 $2,645 $21.16

Base Rent

Option Rent

Expense Lease Summary

C.A.M. Tenant reimburses pro-rata share

Real Estate Tax Tenant reimburses pro-rata share

Insurance Tenant reimburses pro-rata share

Management Tenant does not reimburses pro-rata share

KROGER SHADOW ANCHORED STRIP CENTER

TENANT SUMMARY

#

Verizon Wireless

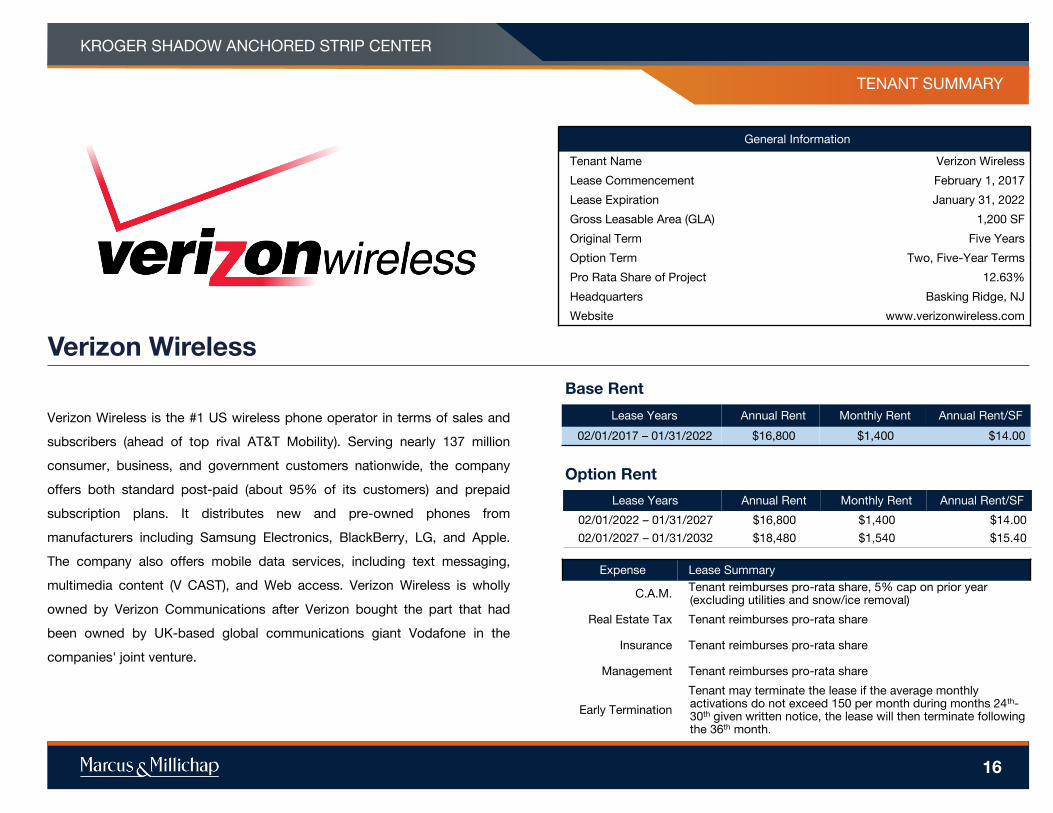

Verizon Wireless is the #1 US wireless phone operator in terms of sales and

subscribers (ahead of top rival AT&T Mobility). Serving nearly 137 million

consumer, business, and government customers nationwide, the company

offers both standard post-paid (about 95% of its customers) and prepaid

subscription plans. It distributes new and pre-owned phones from

manufacturers including Samsung Electronics, BlackBerry, LG, and Apple.

The company also offers mobile data services, including text messaging,

multimedia content (V CAST), and Web access. Verizon Wireless is wholly

owned by Verizon Communications after Verizon bought the part that had

been owned by UK-based global communications giant Vodafone in the

companies' joint venture.

PRICING AND VALUATION MATRIX

PROPERTY NAMEOAKLEY STATION BUILDING

PRICING AND VALUATION MATRIX

PROPERTY NAME

16

TENANT SUMMARY

General Information

Tenant Name Verizon Wireless

Lease Commencement February 1, 2017

Lease Expiration January 31, 2022

Gross Leasable Area (GLA) 1,200 SF

Original Term Five Years

Option Term Two, Five-Year Terms

Pro Rata Share of Project 12.63%

Headquarters Basking Ridge, NJ

Website www.verizonwireless.com

Lease Years Annual Rent Monthly Rent Annual Rent/SF

02/01/2017 – 01/31/2022 $16,800 $1,400 $14.00

Lease Years Annual Rent Monthly Rent Annual Rent/SF

02/01/2022 – 01/31/2027 $16,800 $1,400 $14.00

02/01/2027 – 01/31/2032 $18,480 $1,540 $15.40

Base Rent

Option Rent

Expense Lease Summary

C.A.M.Tenant reimburses pro-rata share, 5% cap on prior year

ff(excluding utilities and snow/ice removal)

Real Estate Tax Tenant reimburses pro-rata share

Insurance Tenant reimburses pro-rata share

Management Tenant reimburses pro-rata share

Early Termination

Tenant may terminate the lease if the average monthly ffactivations do not exceed 150 per month during months 24th-ff30th given written notice, the lease will then terminate following ffthe 36th month.

KROGER SHADOW ANCHORED STRIP CENTER

FINANCIAL ANALYSIS

17

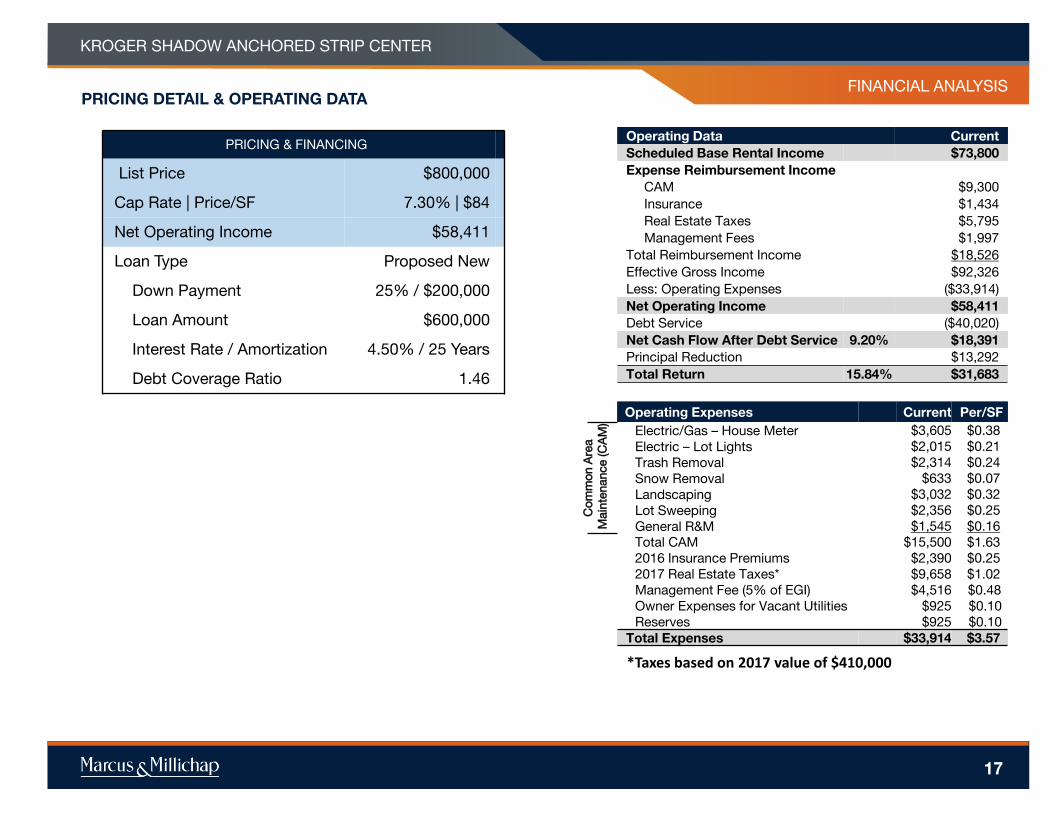

PRICING DETAIL & OPERATING DATA

Operating Data Current

Scheduled Base Rental Income $73,800

Expense Reimbursement Income

CAM $9,300

Insurance $1,434

Real Estate Taxes $5,795

Management Fees $1,997

Total Reimbursement Income $18,526

Effective Gross Income $92,326

Less: Operating Expenses ($33,914)

Net Operating Income $58,411

Debt Service ($40,020)

Net Cash Flow After Debt Service 9.20% $18,391

Principal Reduction $13,292

Total Return 15.84% $31,683

Operating Expenses Current Per/SF

Co

mm

on

Are

a

Main

tenance (C

AM

)

Electric/Gas – House Meter $3,605 $0.38

Electric – Lot Lights $2,015 $0.21

Trash Removal $2,314 $0.24

Snow Removal $633 $0.07

Landscaping $3,032 $0.32

Lot Sweeping $2,356 $0.25

General R&M $1,545 $0.16

Total CAM $15,500 $1.63

2016 Insurance Premiums $2,390 $0.25

2017 Real Estate Taxes* $9,658 $1.02

Management Fee (5% of EGI) $4,516 $0.48

Owner Expenses for Vacant Utilities $925 $0.10

Reserves $925 $0.10

Total Expenses $33,914 $3.57

PRICING & FINANCING

List Price $800,000

Cap Rate | Price/SF 7.30% | $84

Net Operating Income $58,411

Loan Type Proposed New

Down Payment 25% / $200,000

Loan Amount $600,000

Interest Rate / Amortization 4.50% / 25 Years

Debt Coverage Ratio 1.46

KROGER SHADOW ANCHORED STRIP CENTER

*Taxes based on 2017 value of $410,000

18

MARKET

OVERVIEW

KROGER SHADOW ANCHORED STRIP CENTER

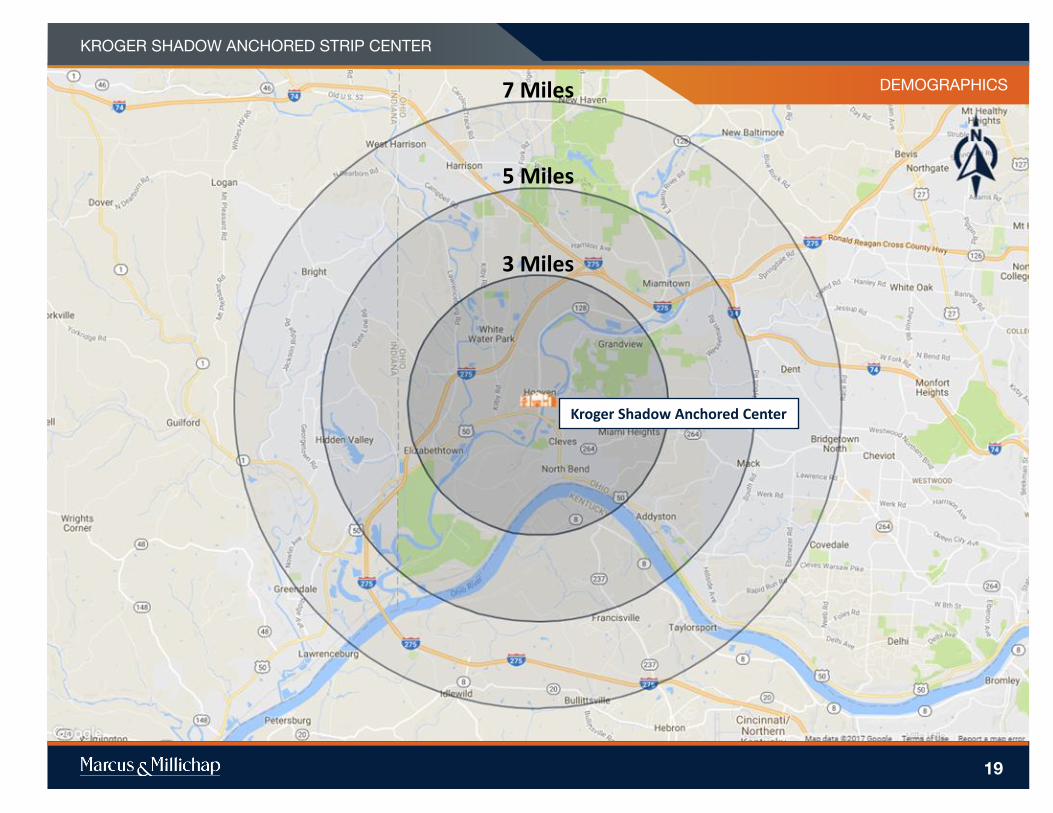

8 DEMOGRAPHICS

19

Kroger Shadow Anchored Center

3 Miles

5 Miles

7 Miles

KROGER SHADOW ANCHORED STRIP CENTER

PROPERTY NAME

MARKETING TEAMDEMOGRAPHICS

Source: © 2016 Experian

Created on September 2017

POPULATION 3 Miles 5 Miles 7 Miles

▪ 2021 Projection

Total Population 13,208 44,008 106,142

▪ 2016 Estimate

Total Population 12,320 40,854 99,912

▪ 2010 Census

Total Population 12,265 40,356 99,137

▪ 2000 Census

Total Population 10,312 33,154 86,312

▪ Current Daytime Population

2016 Estimate 10,268 29,583 81,335

HOUSEHOLDS 3 Miles 5 Miles 7 Miles

▪ 2021 Projection

Total Households 4,705 15,722 39,909

▪ 2016 Estimate

Total Households 4,356 14,531 37,448

Average (Mean) Household Size 2.80 2.77 2.67

▪ 2010 Census

Total Households 4,349 14,384 37,194

▪ 2000 Census

Total Households 3,583 11,496 31,404

▪ Occupied Units

2021 Projection 4,705 15,722 39,909

2016 Estimate 4,732 15,571 39,827

HOUSEHOLDS BY INCOME 3 Miles 5 Miles 7 Miles

▪ 2016 Estimate

$150,000 or More 6.62% 8.92% 8.71%

$100,000 - $149,000 16.57% 20.49% 18.96%

$75,000 - $99,999 11.79% 14.84% 15.15%

$50,000 - $74,999 21.44% 19.52% 19.45%

$35,000 - $49,999 13.39% 12.44% 12.40%

Under $35,000 28.54% 21.69% 23.30%

Average Household Income $76,772 $88,994 $87,380

Median Household Income $59,331 $69,937 $67,874

Per Capita Income $27,316 $31,730 $32,790

HOUSEHOLDS BY EXPENDITURE 3 Miles 5 Miles 7 Miles

Total Average Household Retail Expenditure

$67,004 $69,793 $68,765

▪ Consumer Expenditure Top 10 Categories

Housing $16,384 $16,993 $16,796

Transportation $11,668 $12,417 $12,229

Shelter $8,728 $9,013 $8,928

Food $7,952 $8,324 $8,173

Personal Insurance and Pensions $5,864 $6,535 $6,323

Health Care $4,886 $5,128 $5,151

Utilities $4,019 $4,148 $4,095

Entertainment $3,037 $3,204 $3,141

Apparel $2,826 $2,886 $2,748

Cash Contributions $1,838 $2,031 $2,100

POPULATION PROFILE 3 Miles 5 Miles 7 Miles

▪ Population By Age

2016 Estimate Total Population 12,320 40,854 99,912

Under 20 29.07% 28.06% 26.92%

20 to 34 Years 15.28% 15.46% 16.30%

35 to 39 Years 6.18% 6.09% 5.78%

40 to 49 Years 14.37% 14.18% 13.67%

50 to 64 Years 20.65% 22.19% 22.33%

Age 65+ 14.45% 14.02% 15.01%

Median Age 39.60 40.29 40.82

▪ Population 25+ by Education Level

2016 Estimate Population Age 25+ 8,121 27,308 67,637

Elementary (0-8) 3.57% 2.47% 2.17%

Some High School (9-11) 9.18% 7.14% 6.26%

High School Graduate (12) 42.44% 34.17% 33.65%

Some College (13-15) 15.31% 19.37% 20.51%

Associate Degree Only 6.59% 8.33% 8.53%

Bachelors Degree Only 15.72% 19.46% 19.93%

Graduate Degree 6.56% 8.70% 8.58%

20

KROGER SHADOW ANCHORED STRIP CENTER

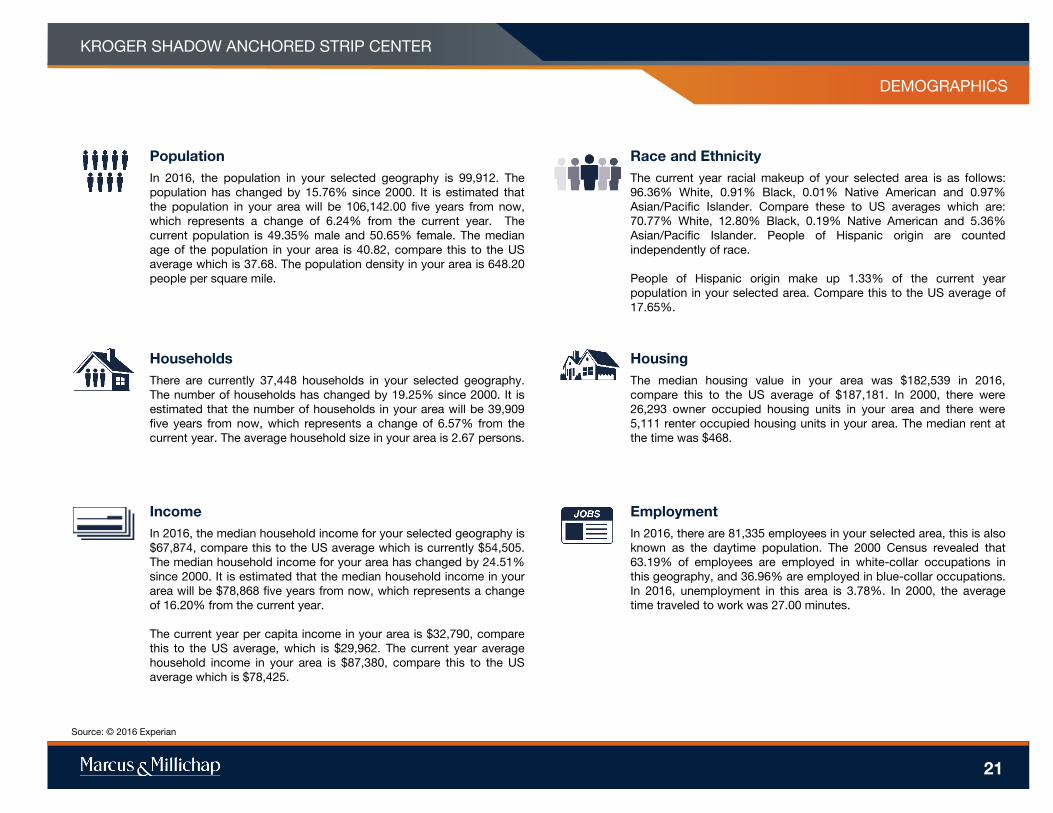

Income

In 2016, the median household income for your selected geography is

$67,874, compare this to the US average which is currently $54,505.

The median household income for your area has changed by 24.51%

since 2000. It is estimated that the median household income in your

area will be $78,868 five years from now, which represents a change

of 16.20% from the current year.

The current year per capita income in your area is $32,790, compare

this to the US average, which is $29,962. The current year average

household income in your area is $87,380, compare this to the US

average which is $78,425.

Population

In 2016, the population in your selected geography is 99,912. The

population has changed by 15.76% since 2000. It is estimated that

the population in your area will be 106,142.00 five years from now,

which represents a change of 6.24% from the current year. The

current population is 49.35% male and 50.65% female. The median

age of the population in your area is 40.82, compare this to the US

average which is 37.68. The population density in your area is 648.20

people per square mile.

Households

There are currently 37,448 households in your selected geography.

The number of households has changed by 19.25% since 2000. It is

estimated that the number of households in your area will be 39,909

five years from now, which represents a change of 6.57% from the

current year. The average household size in your area is 2.67 persons.

Employment

In 2016, there are 81,335 employees in your selected area, this is also

known as the daytime population. The 2000 Census revealed that

63.19% of employees are employed in white-collar occupations in

this geography, and 36.96% are employed in blue-collar occupations.

In 2016, unemployment in this area is 3.78%. In 2000, the average

time traveled to work was 27.00 minutes.

Race and Ethnicity

The current year racial makeup of your selected area is as follows:

96.36% White, 0.91% Black, 0.01% Native American and 0.97%

Asian/Pacific Islander. Compare these to US averages which are:

70.77% White, 12.80% Black, 0.19% Native American and 5.36%

Asian/Pacific Islander. People of Hispanic origin are counted

independently of race.

People of Hispanic origin make up 1.33% of the current year

population in your selected area. Compare this to the US average of

17.65%.

PROPERTY NAME

MARKETING TEAM

Housing

The median housing value in your area was $182,539 in 2016,

compare this to the US average of $187,181. In 2000, there were

26,293 owner occupied housing units in your area and there were

5,111 renter occupied housing units in your area. The median rent at

the time was $468.

Source: © 2016 Experian

DEMOGRAPHICS

21

KROGER SHADOW ANCHORED STRIP CENTER

MARKET OVERVIEW

CINCINNATIOVERVIEW

The Cincinnati metro is 15-county region located within portions of

Ohio, Kentucky and Indiana that maintains a population of 2.2 million.

The Ohio counties are Hamilton, Brown, Warren, Butler and Clermont.

The counties in Indiana are Dearborn, Ohio and Franklin, while

Kentucky counties are Campbell, Grant, Boone, Gallatin, Pendleton,

Bracken and Kenton. The Ohio River runs through the area,

establishing the border between Ohio and Kentucky. Nine Fortune 500

companies are located in the metro and provide thousands of jobs,

including Kroger, Cincinnati Financial, Proctor & Gamble, Macy’s, Fifth

Third Bancorp, AK Steel Holding, American Financial Group, Ashland,

and Western & Southern Financial Group

MARKET OVERVIEW

METRO HIGHLIGHTS

DIVERSIFYING ECONOMY

Growth in service-oriented industries has lessened

the metro’s dependence on the manufacturing and

transportation sectors.

ATTRACTIVE BUSINESS ENVIRONMENT

Companies are drawn to the region’s low cost of

doing business, while employees can enjoy a

relatively affordable place to live.

CENTRAL DISTRUBTION POINT

Half of the U.S. population and 30 major markets

are within a one-day drive.

22

KROGER SHADOW ANCHORED STRIP CENTER

MARKET OVERVIEW

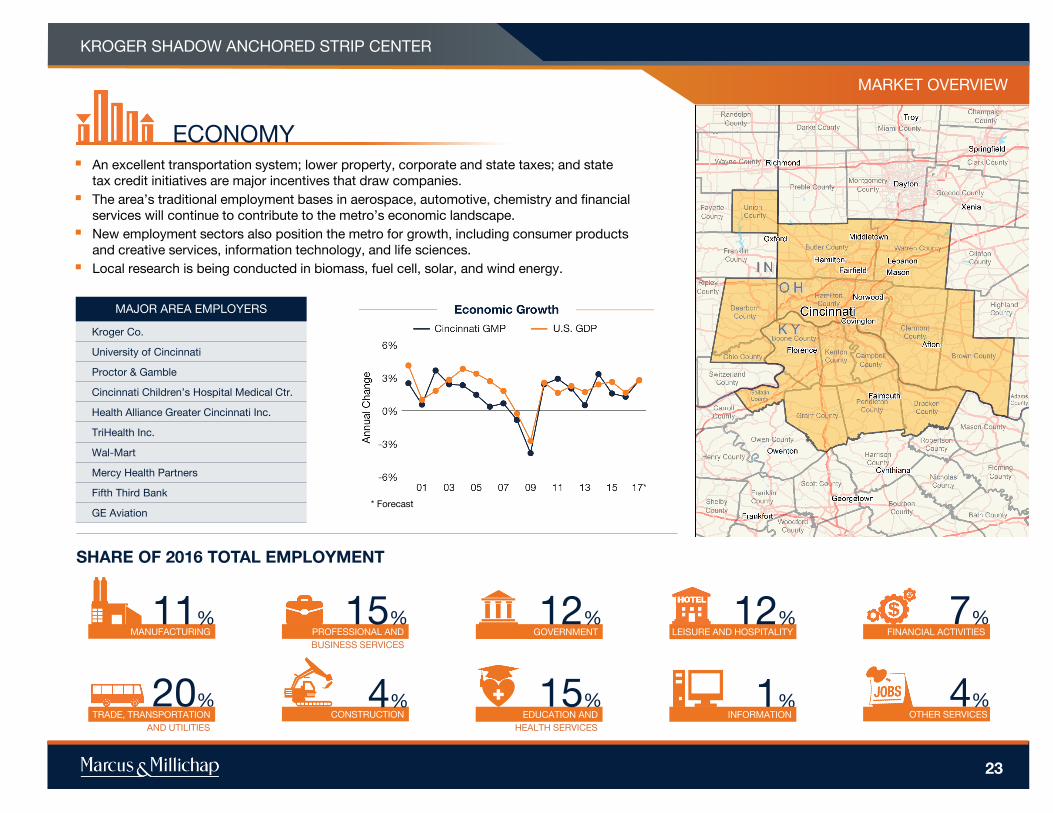

ECONOMY▪ An excellent transportation system; lower property, corporate and state taxes; and state

tax credit initiatives are major incentives that draw companies.

▪ The area’s traditional employment bases in aerospace, automotive, chemistry and financial

services will continue to contribute to the metro’s economic landscape.

▪ New employment sectors also position the metro for growth, including consumer products

and creative services, information technology, and life sciences.

▪ Local research is being conducted in biomass, fuel cell, solar, and wind energy.

SHARE OF 2016 TOTAL EMPLOYMENT

MAJOR AREA EMPLOYERS

Kroger Co.

University of Cincinnati

Proctor & Gamble

Cincinnati Children’s Hospital Medical Ctr.

Health Alliance Greater Cincinnati Inc.

TriHealth Inc.

Wal-Mart

Mercy Health Partners

Fifth Third Bank

GE Aviation* Forecast

MANUFACTURING

11%GOVERNMENT

HEALTH SERVICES

EDUCATION AND

+OTHER SERVICES

4%

LEISURE AND HOSPITALITY FINANCIAL ACTIVITIES

20%

AND UTILITIES

TRADE, TRANSPORTATION CONSTRUCTION

PROFESSIONAL AND

BUSINESS SERVICES

1%INFORMATION

15%

4%

12% 12% 7%

15%

23

KROGER SHADOW ANCHORED STRIP CENTER

MARKET OVERVIEW

DEMOGRAPHICS

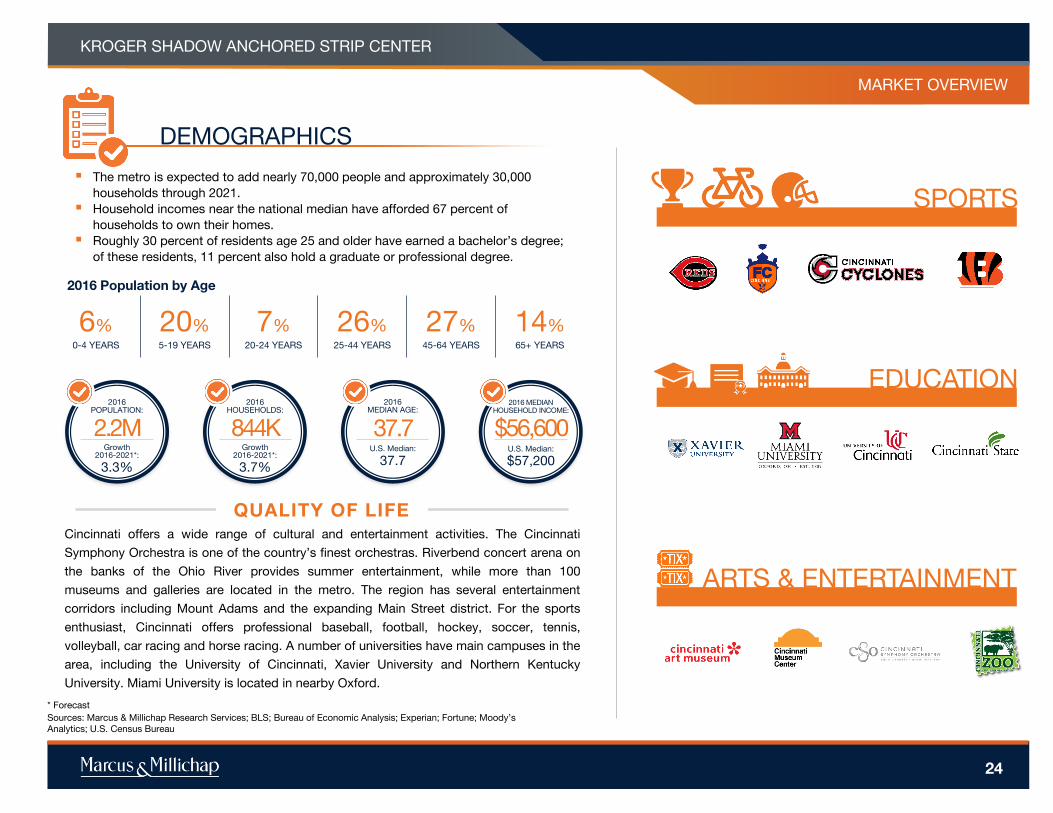

▪ The metro is expected to add nearly 70,000 people and approximately 30,000

households through 2021.

▪ Household incomes near the national median have afforded 67 percent of

households to own their homes.

▪ Roughly 30 percent of residents age 25 and older have earned a bachelor’s degree;

of these residents, 11 percent also hold a graduate or professional degree.

Cincinnati offers a wide range of cultural and entertainment activities. The Cincinnati

Symphony Orchestra is one of the country’s finest orchestras. Riverbend concert arena on

the banks of the Ohio River provides summer entertainment, while more than 100

museums and galleries are located in the metro. The region has several entertainment

corridors including Mount Adams and the expanding Main Street district. For the sports

enthusiast, Cincinnati offers professional baseball, football, hockey, soccer, tennis,

volleyball, car racing and horse racing. A number of universities have main campuses in the

area, including the University of Cincinnati, Xavier University and Northern Kentucky

University. Miami University is located in nearby Oxford.

37.7

2016MEDIAN AGE:

U.S. Median:

37.7

$56,600

2016 MEDIAN HOUSEHOLD INCOME:

U.S. Median:

$57,200

2.2M

2016POPULATION:

Growth2016-2021*:

3.3%

844K

2016HOUSEHOLDS:

3.7%

Growth2016-2021*:

QUALITY OF LIFE

2016 Population by Age

0-4 YEARS

6%5-19 YEARS

20%20-24 YEARS

7%25-44 YEARS

26%45-64 YEARS

27%65+ YEARS

14%

* Forecast

Sources: Marcus & Millichap Research Services; BLS; Bureau of Economic Analysis; Experian; Fortune; Moody’s

Analytics; U.S. Census Bureau

SPORTS

EDUCATION

ARTS & ENTERTAINMENT

24

KROGER SHADOW ANCHORED STRIP CENTER

MARKET OVERVIEW

25

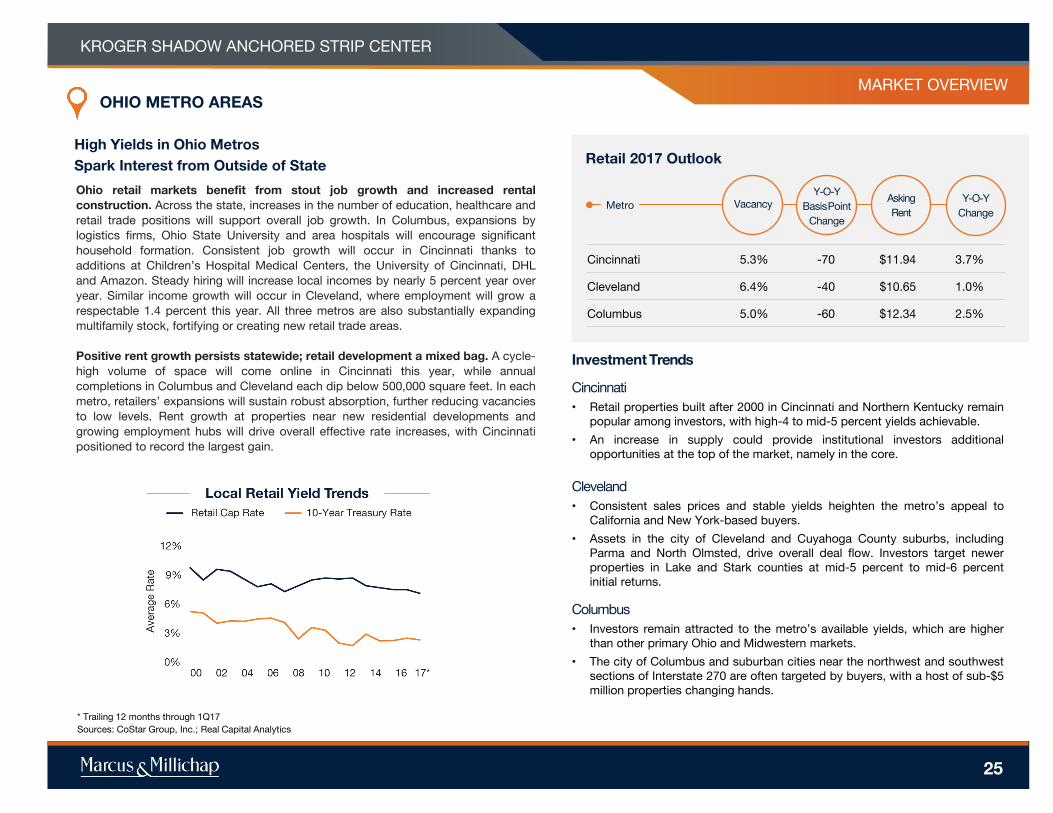

Ohio retail markets benefit from stout job growth and increased rental

construction. Across the state, increases in the number of education, healthcare and

retail trade positions will support overall job growth. In Columbus, expansions by

logistics firms, Ohio State University and area hospitals will encourage significant

household formation. Consistent job growth will occur in Cincinnati thanks to

additions at Children’s Hospital Medical Centers, the University of Cincinnati, DHL

and Amazon. Steady hiring will increase local incomes by nearly 5 percent year over

year. Similar income growth will occur in Cleveland, where employment will grow a

respectable 1.4 percent this year. All three metros are also substantially expanding

multifamily stock, fortifying or creating new retail trade areas.

Positive rent growth persists statewide; retail development a mixed bag. A cycle-

high volume of space will come online in Cincinnati this year, while annual

completions in Columbus and Cleveland each dip below 500,000 square feet. In each

metro, retailers’ expansions will sustain robust absorption, further reducing vacancies

to low levels. Rent growth at properties near new residential developments and

growing employment hubs will drive overall effective rate increases, with Cincinnati

positioned to record the largest gain.

Retail 2017 OutlookHigh Yields in Ohio Metros

Spark Interest from Outside of State

Vacancy

Y-O-Y

BasisPoint

Change

MetroAsking

Rent

Y-O-Y

Change

Cincinnati 5.3% -70 $11.94 3.7%

Cleveland 6.4% -40 $10.65 1.0%

Columbus 5.0% -60 $12.34 2.5%

OHIO METRO AREAS

* Trailing 12 months through 1Q17

Sources: CoStar Group, Inc.; Real Capital Analytics

Investment Trends

Cincinnati

• Retail properties built after 2000 in Cincinnati and Northern Kentucky remain

popular among investors, with high-4 to mid-5 percent yields achievable.

• An increase in supply could provide institutional investors additional

opportunities at the top of the market, namely in the core.

Cleveland

• Consistent sales prices and stable yields heighten the metro’s appeal to

California and New York-based buyers.

• Assets in the city of Cleveland and Cuyahoga County suburbs, including

Parma and North Olmsted, drive overall deal flow. Investors target newer

properties in Lake and Stark counties at mid-5 percent to mid-6 percent

initial returns.

Columbus

• Investors remain attracted to the metro’s available yields, which are higher

than other primary Ohio and Midwestern markets.

• The city of Columbus and suburban cities near the northwest and southwest

sections of Interstate 270 are often targeted by buyers, with a host of sub-$5

million properties changing hands.

KROGER SHADOW ANCHORED STRIP CENTER

MARKET OVERVIEW

26

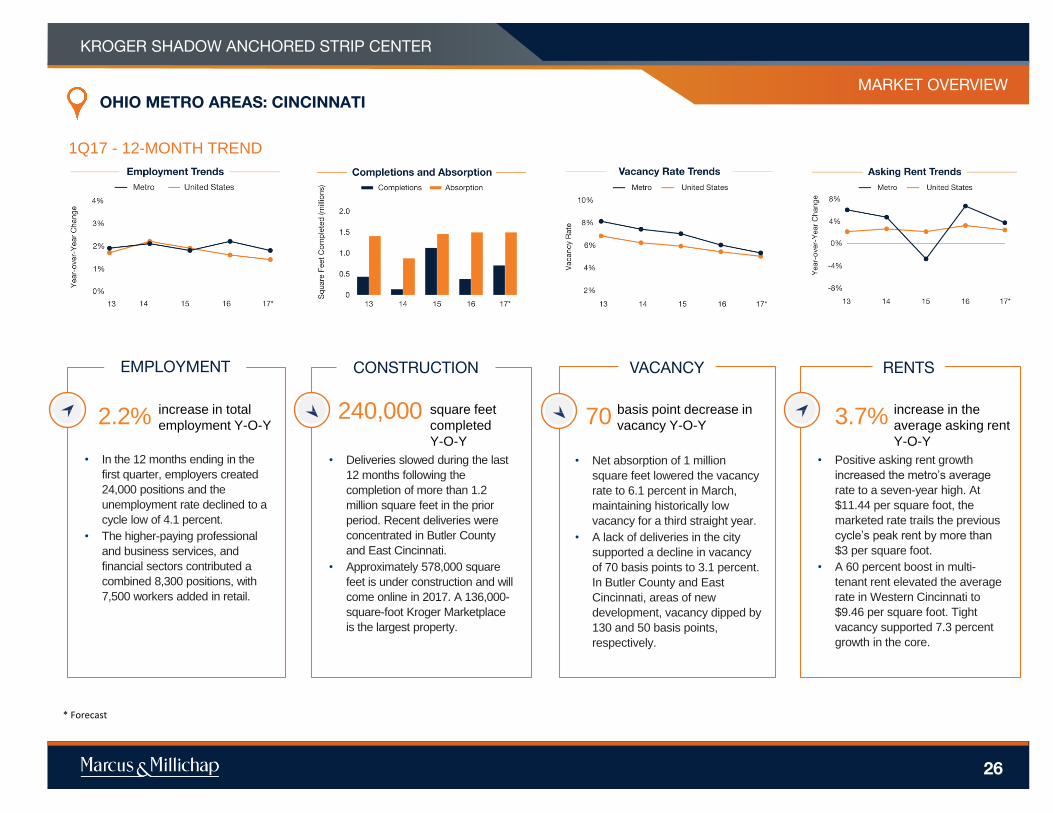

• In the 12 months ending in the

first quarter, employers created

24,000 positions and the

unemployment rate declined to a

cycle low of 4.1 percent.

• The higher-paying professional

and business services, and

financial sectors contributed a

combined 8,300 positions, with

7,500 workers added in retail.

EMPLOYMENT

• Deliveries slowed during the last

12 months following the

completion of more than 1.2

million square feet in the prior

period. Recent deliveries were

concentrated in Butler County

and East Cincinnati.

• Approximately 578,000 square

feet is under construction and will

come online in 2017. A 136,000-

square-foot Kroger Marketplace

is the largest property.

CONSTRUCTION

• Net absorption of 1 million

square feet lowered the vacancy

rate to 6.1 percent in March,

maintaining historically low

vacancy for a third straight year.

• A lack of deliveries in the city

supported a decline in vacancy

of 70 basis points to 3.1 percent.

In Butler County and East

Cincinnati, areas of new

development, vacancy dipped by

130 and 50 basis points,

respectively.

VACANCY

• Positive asking rent growth

increased the metro’s average

rate to a seven-year high. At

$11.44 per square foot, the

marketed rate trails the previous

cycle’s peak rent by more than

$3 per square foot.

• A 60 percent boost in multi-

tenant rent elevated the average

rate in Western Cincinnati to

$9.46 per square foot. Tight

vacancy supported 7.3 percent

growth in the core.

RENTS

OHIO METRO AREAS: CINCINNATI

increase in the

average asking rent

Y-O-Y

3.7%basis point decrease in

vacancy Y-O-Y70square feet

completed

Y-O-Y

240,000increase in total

employment Y-O-Y2.2%

* Forecast

1Q17 - 12-MONTH TREND

KROGER SHADOW ANCHORED STRIP CENTER

MARKET OVERVIEW

27

Demographic Highlights

2017 JOB

GROWTH

FIVE-YEAR

POPULATION

GROWTH*

48,300

FIVE-YEAR

HOUSEHOLD

GROWTH*

34,000

1Q17 MEDIAN

HOUSEHOLD

INCOME

RETAIL SALES

FORECAST*

Metro 13.9%U.S. 21.1%

$4,217 Per Household

$1,670 Per Person

1Q17 RETAIL SALES PER MONTH

Buyer Interest Intensifies; Newer Properties Targeted

Outlook: Buyers from California remain

enticed by yields that are at least 150

basis points more than those that can be

captured in their home markets.

Vacancy

Rate

Y-O-Y

BasisPoint

Change

SubmarketAsking

Rent

Y-O-Y %

Change

Cincinnati (city) 3.1% -70 $13.38 7.3%

Dearborn County 4.1% -500 $7.46 3.9%

Northern Kentucky 4.2% -70 $12.84 4.1%

Eastern Cincinnati 5.4% -50 $13.20 1.2%

Butler County 6.2% -130 $9.86 0.9%

Northern Cincinnati 6.2% 60 $12.82 -0.6%

Outlying Warren County 6.8% -60 $9.12 -12.4%

Brown County 7.5% -60 $6.21 12.5%

Western Cincinnati 9.9% 80 $9.46 12.6%

Overall Metro 6.1% -70 $11.44 3.7%

Cincinnati (city) 3.1% -70 $13.38 7.3%

Submarket Trends

Lowest Vacancy Rates 1Q17

Sales Trends

OHIO METRO AREAS: CINCINNATI

• Multi-Tenant: Throughout the metro, investors pushed the average price up 11 percent

to $181 per square foot over the year ending in the first quarter. Cap rates remain in

the low- to mid- 7 percent area.

• Single-Tenant: In the past 12 months, fast-food restaurants garnered the most interest

from investors. In sales of all single-tenant assets, the average price increased 6

percent to $287 per square foot, with the average cap rate hovering near 7 percent.

** Trailing 12 months through 1Q17

Pricing trend sources: CoStar Group, Inc.; Real Capital Analytics

*2017-2022

Metro 1.8%U.S. Average 1.4%

Metro $60,386U.S. Average $58,218

U.S. $3,785

U.S. $1,454

KROGER SHADOW ANCHORED STRIP CENTER

MARKET OVERVIEW

28

• Monetary policy in transition. The yield on the 10-year U.S. Treasury bond remained in the

low- to mid-2 percent range throughout the first quarter of 2017. Despite the Fed raising its

benchmark short-term rate twice in recent months and signaling another rise in June, long-

term rates have remained stable. The Federal Reserve wants to normalize its monetary policy

and, in addition to rate hikes, could start paring its balance sheet. While short- and long-term

rates do not always move in tandem, both actions by the Fed have the potential to lift long-

term rates.

• Sound economy a balancing act for Fed. Tight labor market conditions are finally producing

upward pressure on wages and inflation. Unemployment just hit the lowest level since 2007

and consumer confidence sits close to its all-time high. Consumers have the means and the

confidence to expand consumption and retail properties stand to gain significantly from

increased spending. The Fed must now balance growth and job creation against wage growth

and inflationary pressures. economic

• Lenders exercise disciplined approach. Overall, leverage on acquisition loans has

continued to reflect disciplined underwriting, with LTVs typically ranging from 60 percent to 70

percent for most retail properties. The combination of higher rates and conservative lender

underwriting encouraged some investor caution that slowed deal flow in late 2016, a trend that

will likely extend into 2017. A potential easing of regulations on financial institutions, though,

could liberate additional lending capacity and higher interest rates may also encourage

additional lenders to participate.

* Forecast

Sources: CoStar Group, Inc.; Real Capital Analytics

NORTH CAROLINA METRO AREAS

Capital Markets

KROGER SHADOW ANCHORED STRIP CENTER

www.MarcusMillichap.com

Joel Dumes

Senior Vice President Investments

Senior Director - National Retail Group

Cincinnati Office

Tel: (513) 878-7720

Fax: (513) 878-7710

Licenses: OH SAL.2003013045, KY 63818

Stan Falk

First Vice President Investments

Director - National Retail Group

Cincinnati Office

Tel: (513) 878-7721

Fax: (513) 878-7710

License: OH SAL.2012001364

P R E S E N T E D B Y