korea / automobiles & components hanon systems 018880 · pdf filehanon systems 018880 ks...

TRANSCRIPT

Hanon Systems 018880 KS BNP PARIBAS H James Yoon

11 DECEMBER 2015 KOREA / AUTOMOBILES & COMPONENTS

HANON SYSTEMS 018880 KS

HOW WE DIFFER FROM CONSENSUS MARKET RECS

TARGET PRICE (%) 29.0 POSITIVE 6

EPS 2015 (%) 5.3 NEUTRAL 5

EPS 2016 (%) 4.6 NEGATIVE 1

Heating up KEY STOCK DATA

Sources: FactSet estimates; BNP Paribas estimates

Initiate coverage at BUY; 22% potential upside to KRW60,000 TP We initiate coverage on Hanon with a BUY rating and KRW60,000 TP, which equates to a 2016E P/B of 3.2x (more than 2SD above the nine-year historical mean). Our TP is based on the average of ROIC and ROE-derived fair values and reflects exposure to NEVs, its industry-leading dividend payout and potential upside for inorganic growth.

Capitalising on tighter fuel economies and emissions standards Hanon is leveraging traditional climate control technology to provide non-conventional thermal management and emissions solutions, which can increase fuel economies by reducing energy consumption and improve emissions standards in both traditional and new energy powertrains to meet tightening global regulations.

Execution of revenue and EPS growth strategy key to success New management targets a five-year sales revenue CAGR of 6% to KRW7.3t by 2020. We forecast a 120bp y-y jump in OPM to 7.2% in 2016, stemming from initial efforts to raise operational efficiencies, and to 8% through expansion of non-conventional parts supply and customer diversification by 2020.

Positive commitment to shareholder-friendly initiatives New management’s commitment to shareholder-friendly initiatives is clear, based on its action plan to increase liquidity with a 1:5 share split, maintain steady dividends with an industry-leading payout of c45%, and implement a stock option plan for senior management.

Historical P/BV

Sources: Bloomberg; BNP Paribas

H James Yoon [email protected] +822 2125 0533

Our research is available on Thomson One, Bloomberg, TheMarkets.com, FactSet and on http://eqresearch.bnpparibas.com/index. Please contact your salesperson for authorisation. Please see the important notice on the back page.

PREPARED AND PUBLISHED BY NON-US BROKER-DEALER(S): BNP PARIBAS SECURITIES KOREA CO LTD. THIS MATERIAL HAS BEEN APPROVED FOR U.S DISTRIBUTION. ANALYST

CERTIFICATION AND IMPORTANT DISCLOSURES CAN BE FOUND AT APPENDIX ON PAGE 22

BUY TARGET PRICE KRW60,000

UP/DOWNSIDE +22.2%

CLOSE KRW49,100

2014A 2015E 2016E 2017E

Revenue 5,455 5,537 5,814 6,153

Rec. net profit 278 251 314 347

Recurring EPS (KRW) 2,601 2,352 2,943 3,253

EPS growth (%) (6.9) (9.6) 25.1 10.6

Recurring P/E (x) 18.9 20.9 16.7 15.1

Dividend yield (%) 2.0 2.0 2.4 3.1

EV/EBITDA (x) 9.9 10.1 8.5 7.8

Price/book (x) 3.2 2.9 2.6 2.3

Net debt/Equity (%) 1.2 (0.6) (6.8) (7.9)

ROE (%) 17.8 14.6 16.4 16.2

Share price performance 1 Month 3 Month 12 Month

Absolute (%) 2.9 38.3 6.7

Relative to country (%) 5.5 31.9 9.1

Next Results

Mkt cap (USD m) 4,436

3m avg daily turnover (USD m) 6.4

Free float (%) 30

Major shareholder Hahn&Co. Auto Holdings LLC (51%)

12m high/low (KRW) 50,700/33,000

3m historic vol. (%) 51.2

ADR ticker -

ADR closing price (USD) -

Issued shares (m) 107

YE Dec (KRW b)

February 2016

(35)(30)(25)(20)(15)(10)(5)051015

32,00034,00036,00038,00040,00042,00044,00046,00048,00050,00052,000

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Hanon Systems Rel to MSCI Korea(KRW) (%)

0.00.51.01.52.02.53.03.5

2007 2008 2009 2010 2011 2012 2013 2014 2015

(x)

+2 SD

+1 SDAvg

-1 SD-2 SD

Hanon Systems 018880 KS H James Yoon

Investment thesis We believe Hanon is a beneficiary of tightening global fuel efficiency and emissions regulations as it leverages traditional climate control technology to provide non-conventional thermal and emissions solutions, which can increase fuel economies by reducing energy consumption and improve emissions standards in both traditional and new energy powertrains.

New management plans to diversify the global customer base focused on new growth and technology-focused customers, while maintaining its current dominance with Hyundai Motor Group (HMG) and Ford, while at the same time implementing internal cost reduction efforts to raise operational profitability.

Exposure to expected expansion of NEVs (new energy vehicles) and shareholder-friendly initiatives warrant a valuation premium against global peers, in our view. BUY.

Catalyst We see the main event catalyst as the opportunity for further inorganic growth through acquisition of overseas suppliers with specific non-conventional technology and/or access to new customers. The potential earnings catalyst is OPM expansion in the immediate term through implementation of various operational efficiency enhancements in 2016.

Risk to our call Key downside risks to our view are: 1) lower than expected orders from new customers, which would hinder future growth expectations; and 2) inability to improve operational efficiencies of its global production network, which would limit expected profit margin expansion.

Company background Key assumptions

Revenues 2014 2015E 2016E 2017E

HMG (KRW b) 2,392 2,337 2,408 2,461

Ford (KRW b) 1,142 1,179 1,167 1,169

Others (KRW b) 1,920 2,021 2,238 2,523

HMG – as of total (%) 44 42 41 40

Ford– as of total (%) 21 21 20 19

Others – as of total (%) 35 37 39 41

Sources: Hanon Systems; BNP Paribas estimates

Principal activities (revenue, 2014) Earnings sensitivity

Bear-2 Bear-1 Base Bull-1 Bull-2

Change in USD/KRW -5% -1% - 1% 5%

USD/KRW (avg) 1,154 1,203 1,215 1,227 1,276

2016E OP (KRW b) 384 413 421 428 457

Change (%) (8.7) (1.7) 1.7 8.7

Source: Hanon Systems Sources: Hanon Systems; BNP Paribas estimates

Key executives

Age Joined Title

Yeo-Eul Yoon 59 2015 Chairman

In-Young Lee 58 2015 President/CEO/Rep Director

Moon-Ho Choi 48 2013 Senior Managing Director

Beom-Jun Kim 50 2015 CFO/Executive Director

Kwang-Taek Hong 49 2013 CTO/Vice President

www.hanonsystems.com

We estimate non-HMG revenue will account for 59% of the total in 2016.

A 1% change in the USD/KRW rate would result in a 1.7% change in operating profit, keeping all other factors constant.

A 5% change in the USD/KRW rate would result in a 8.7% change in operating profit, keeping all other factors constant.

Hanon Systems manufactures a variety of automotive climate control and thermal management equipment and systems. The Company's products include air conditioners, heaters, cooling modules, compressors, radiators, fans, evaporators, and condensers.

Air conditioner - 69.5%

Compressor - 21.1%

Radiator - 7.1%

Module - 2.3%

2 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

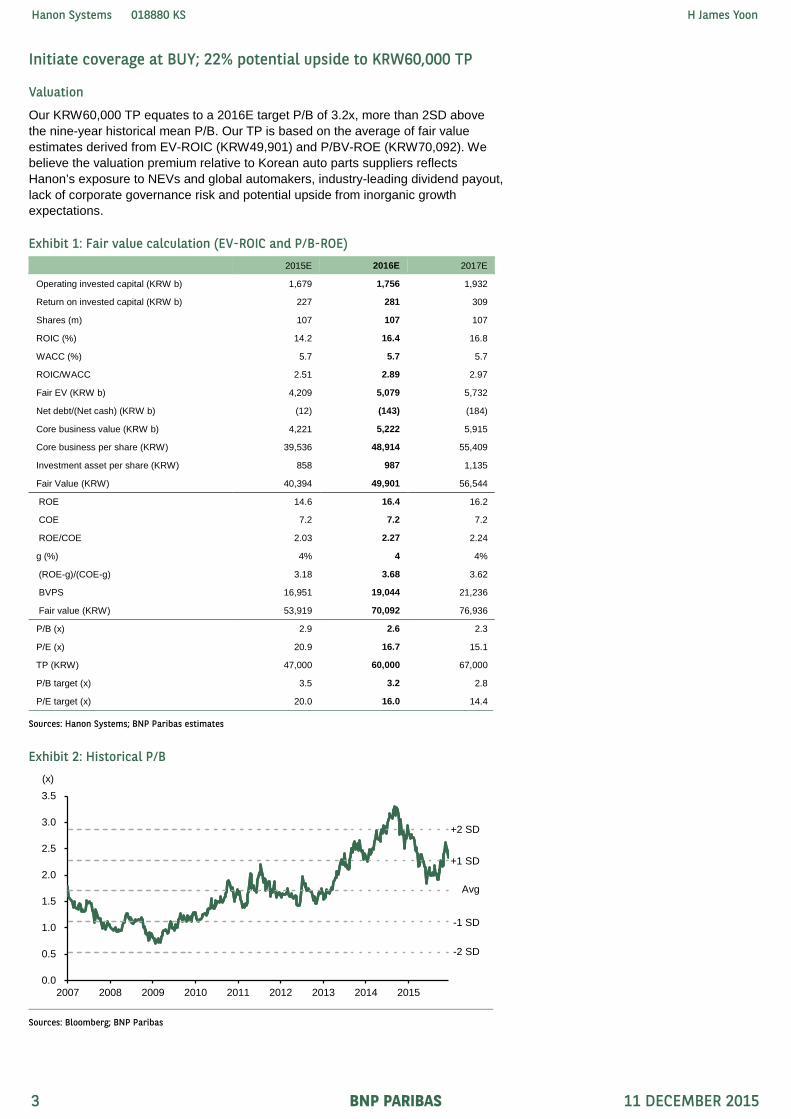

Initiate coverage at BUY; 22% potential upside to KRW60,000 TP

Valuation

Our KRW60,000 TP equates to a 2016E target P/B of 3.2x, more than 2SD above the nine-year historical mean P/B. Our TP is based on the average of fair value estimates derived from EV-ROIC (KRW49,901) and P/BV-ROE (KRW70,092). We believe the valuation premium relative to Korean auto parts suppliers reflects Hanon’s exposure to NEVs and global automakers, industry-leading dividend payout, lack of corporate governance risk and potential upside from inorganic growth expectations.

Exhibit 1: Fair value calculation (EV-ROIC and P/B-ROE) 2015E 2016E 2017E

Operating invested capital (KRW b) 1,679 1,756 1,932

Return on invested capital (KRW b) 227 281 309

Shares (m) 107 107 107

ROIC (%) 14.2 16.4 16.8

WACC (%) 5.7 5.7 5.7

ROIC/WACC 2.51 2.89 2.97

Fair EV (KRW b) 4,209 5,079 5,732

Net debt/(Net cash) (KRW b) (12) (143) (184)

Core business value (KRW b) 4,221 5,222 5,915

Core business per share (KRW) 39,536 48,914 55,409

Investment asset per share (KRW) 858 987 1,135

Fair Value (KRW) 40,394 49,901 56,544

ROE 14.6 16.4 16.2

COE 7.2 7.2 7.2

ROE/COE 2.03 2.27 2.24

g (%) 4% 4 4%

(ROE-g)/(COE-g) 3.18 3.68 3.62

BVPS 16,951 19,044 21,236

Fair value (KRW) 53,919 70,092 76,936

P/B (x) 2.9 2.6 2.3

P/E (x) 20.9 16.7 15.1

TP (KRW) 47,000 60,000 67,000

P/B target (x) 3.5 3.2 2.8

P/E target (x) 20.0 16.0 14.4

Sources: Hanon Systems; BNP Paribas estimates

Exhibit 2: Historical P/B

Sources: Bloomberg; BNP Paribas

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2007 2008 2009 2010 2011 2012 2013 2014 2015

(x)

+2 SD

+1 SD

Avg

-1 SD

-2 SD

3 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Standing out from the crowd

Hanon’s valuations seem to be more in line with those in the Korean EV supply chain, and are also well within the range of top global auto parts peers. We believe this is due to the market’s view of Hanon as a leading global auto parts supplier with strong potential to benefit from the evolution of NEVs.

While the company does not provide any breakdown of operating profitability between conventional and non-conventional parts, the c10% portion of sales revenue from non-conventional parts and our expectation that this will expand to 20% by 2020 suggests a strong contribution, in our view. We believe Hanon enjoys an early mover advantage in non-conventional parts, which are based on quoted market prices with attractive margins, not simple cost-plus prices with volume discounts built in. While Hanon may offer cost-competitive conventional products to its existing customer base, as well as to new mass brands, the company is offering high value-added non-conventional parts and systems to its technology-driven and existing customers, which warrant better profitability.

A key distinction between Hanon and its domestic peers is the lack of Korean “chaebol” risk as it is not part of a large conglomerate. In many cases, affiliates of large groups can be more susceptible to corporate governance risk. The new top management team of Hanon is a select group of auto industry and marketing professionals with many years of experience at various global automakers and parts suppliers, including Hanon itself. Hanon has one of the strongest growth profiles among covered peers with a three-year EPS CAGR of 15% through 2018E, following our expectation of 25% y-y EPS growth in 2016. This is based on expected structural improvements both within the company’s operating base and externally through growth of its non-conventional product lines.

In terms of shareholder returns, our forecast for Hanon’s 2016 dividend payout of 41% is the highest among both auto parts makers and the EV supply chain, based on Bloomberg consensus estimates for peers. ROE is near the high-end of auto parts suppliers as well. We expect the dividend payout to rise to 50% by 2018. Regarding the small free float of 30%, the stock split scheduled for 1Q16 should help to increase liquidity. While no new M&A has been confirmed at this time, new management has stated its willingness to grow inorganically, as well as to acquire smaller competitors in order to gain new technologies (such as the 2014 acquisition of the thermal and emissions business of Cooper-Standard), or widen its customer footprint. We believe any M&A news may act as a positive catalyst for the shares.

Key risks

Key downside risks to our view and target price are the following:

1 Inability to match our revenue and earnings projections due to lower than expected new customer contract wins. Although c60% of new contract wins during 2013-15 have come from new customers (ie non-Ford and Hyundai Motor Group), penetration into new OEMs and their products takes time. Management’s confidence in growth targets will need to be backed up with new business wins. In particular, the China penetration strategy may be a gauge of Hanon’s progress.

2 Inability to achieve operating margin expansion due to lower than expected cost reductions and improvement in operational efficiencies for its global production network. Hanon operates four technical centers globally (Korea, Germany, Czech Republic and US) and 29 manufacturing facilities. Given the vast footprint, management’s objectives to improve procurement supply-chain management, optimise labour and overhead costs, implement design cost innovations and instil best practises at inefficient production centers is a major task with significant upside potential to profitability, but also considerable execution risk.

4 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Exhibit 3: Global Auto Parts – valuation comparison

Local CCY (FY16E, F3/17E) BBG code Rec Price Target price Upside/ downside P/E P/BV EV/EBITDA Pay-out ratio Div. yield ROE

(LC) (LC) (%) (x) (x) (x) (%) (%) (%)

Korea Hanon Systems 018880 KS BUY 49,100 60,000 22.2 16.7 2.6 8.6 40.8 2.4 16.4

Hyundai Mobis 012330 KS BUY 234,500 270,000 15.1 6.0 0.8 5.6 12.8 2.1 13.3

Hyundai Wia 011210 KS BUY 112,500 170,000 51.1 5.8 0.8 5.1 4.9 0.8 14.9

Mando 204320 KS BUY 175,000 176,000 0.6 8.3 1.2 5.5 25.0 3.0 15.4

Average 9.2 1.3 6.2 20.9 2.1 15.0

US Johnson Controls JCI US n/a 41.0 n/a n/a 10.9 2.3 7.9 30.3 2.8 20.6

Delphi DLPH US n/a 84.4 n/a n/a 13.5 7.2 9.4 17.7 1.3 n/a

Magna MGA US n/a 42.9 n/a n/a 8.2 1.6 5.3 18.7 2.3 23.8

Borg Warner BWA US n/a 41.1 n/a n/a 12.2 2.4 7.2 16.2 1.3 20.0

Autoliv ALV US n/a 125.6 n/a n/a 17.2 2.9 8.7 33.8 2.0 17.3

Average 12.4 3.3 7.7 23.3 1.9 20.4

Europe Continental CON GY n/a 218 n/a n/a 13.9 2.9 6.9 28.5 2.0 22.0

Valeo FR FP n/a 135 n/a n/a 13.4 2.7 5.7 30.4 2.3 21.5

Average 13.7 2.8 6.3 29.5 2.2 21.7

Japan Denso Corp 6902 JP HOLD 5,792 5,500 (5.0) 16.4 1.3 6.7 33.9 2.1 16.4

Aisin Seiki 7259 JP REDUCE 5,180 3,600 (30.5) 15.8 1.2 3.6 32.0 2.0 16.4

Mitsubishi Electric 6503 JP n/a 1,320 n/a n/a 12.2 1.3 5.5 27.8 2.3 11.4

Sumitomo Electric 5802 JP n/a 1,673 n/a n/a 11.6 0.9 5.3 28.0 2.4 7.8

Toyota Boshoku 3116 JP n/a 2,533 n/a n/a 14.2 1.8 5.3 19.5 1.4 12.8

Average 14.0 1.3 5.3 28.3 2.0 13.0

ROW Motherson Sumi MSS IN n/a 270 n/a n/a 19.6 6.5 5.3 33.9 1.7 36.8

Average 19.6 6.5 5.3 33.9 1.7 36.8

Global Average 12.7 2.4 6.3 25.5 2.0 17.9

Priced at close of business 11 Dec 2015 Sources: Bloomberg; BNP Paribas estimates for covered stocks

Exhibit 4: Korea EV Supply Chain– valuation comparison (KRW) BBG code Rec Price Target price Upside/ downside P/E P/BV EV/EBITDA Pay-out ratio Div. yield ROE

(LC) (LC) (%) (x) (x) (x) (%) (%) (%)

Battery Samsung SDI 006400 KS BUY 128,500 142,000 10.5 22.9 0.7 10.8 17.8 0.8 3.1

LG Chem 051910 KS BUY 326,500 350,000 7.2 15.6 1.7 6.1 19.1 1.3 11.2

SK Innovation 096770 KS BUY 127,500 160,000 25.5 8.4 0.7 6.6 25.0 3.1 8.3

Average

15.6 1.0 7.8 20.6 1.7 7.6

IT-Auto Parts

LG Innotek 011070 KS HOLD 97,900 83,000 (15.2) 16.9 1.2 4.5 4.3 0.3 7.3

LG Electronics 066570 KS HOLD 49,300 48,000 (2.6) 17.0 0.6 3.9 14.0 0.8 3.7

Average 17.0 0.9 4.2 9.2 0.5 5.5

Battery Material

POSCO Chemtech 003670 KS n/a 13,150 n/a n/a 9.8 1.3 5.3 13.0 1.3 14.2

Soulbrain 036830 KS n/a 36,550 n/a n/a 7.3 1.1 3.6 10.4 1.4 15.5

Ecopro 086520 KS n/a 13,150 n/a n/a 25.7 3.0 n/a n/a n/a 10.6

Average

14.3 1.8 4.5 11.7 1.4 13.5

EV Average

15.5 1.3 5.8 14.8 1.3 9.2

Priced at close of business 11 Dec 2015 Sources: Bloomberg; BNP Paribas estimates for covered stocks

5 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Capitalising on tighter fuel economies and emissions standards

Hanon Systems is leveraging traditional climate control technology to provide thermal management and emissions solutions, which can increase fuel economies by reducing energy consumption and improve emissions in both traditional and new energy powertrains to meet tightening global regulations. Powertrain management, weight reduction, aerodynamics and other equipment improvements can all help to raise vehicle efficiencies, but these come at an added cost to OEMs, which in turn reflects revenue opportunities for auto parts suppliers like Hanon.

Management forecasts the traditional climate control market to grow at a five-year CAGR of 4% through 2020 to reach KRW47.3t (KRW39.7t in 2015) in sales. As such, this should remain the bread and butter of the company’s sales revenue mix. Conventional parts currently account for c90% of total revenues. Maintaining market shares with core customers is crucial to the growth of Hanon’s climate control business, as is expanding the foot print to mass-brand growth customers and introduction of next generation climate control products.

Meanwhile, the burgeoning thermal management and emissions parts and systems market is expected by management to see a five-year CAGR of 16% through 2020 to reach KRW13.9t (KRW6.5t in 2015) in sales as the auto industry as a whole takes various strategies to improve fuel economies and reduce emissions. Management targets the sales revenue contribution of non-conventional parts to expand to 20% by 2020, from the current c10%. Hanon’s technology customers are already leading the industry as early adopters of thermal and emissions solutions in cutting edge EVs such as the BMW i8 and i3 and the Tesla Model S and Model X.

Despite the recent market focus on zero emission BEVs (battery electric vehicles) as the end game in meeting toughening global fuel emission standards, there are various intermediate technologies that can provide a means to reaching the same end. So-called micro/mild hybrids, which utilise such technologies as ISG (idle stop-and-go) technology, HEVs (hybrid electric vehicles) and PHEVs (plug-in hybrid electric vehicles) are all viable examples of new energy powertrains through which automakers can improve emissions and fuel economies. Down-sized traditional gasoline engines equipped with turbochargers, and even recently tainted clean diesel technology, represent efforts to optimise traditional ICEs (internal combustion engines). GDI (gasoline direct injection) has also been used to increase fuel efficiencies in recent years.

BNP Paribas estimates the number of NEVs (new energy vehicles) on the road will rise from 2.6% of global passenger vehicles last year, to 12.6% in 2020, and 27.8% in 2025. HEVs are likely to remain the dominant form, at two-thirds of NEVs in 2020 and one-half in 2025. FCEVs (fuel-cell electric vehicle) are likely to account for 4-5%

Exhibit 5: Strict regulations lead to changes in the technology landscape

Source: Hanon Systems

Traditional Climate Products

Strict Fuel Flexibilitiy and Emissions Regulation

Thermal & Emission Systems

Charge Air Cooler

Electronic Coolant Pump and Valve

Electronic Throttle Body

Exhaust Gas Recirculation (EGR)

Electronic Watergate Actuator

6 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

of all NEVs and 1.3% of the entire market in 2025. Note, however, that even 10 years from now we assume traditional ICEs should still account for 72% of total auto sales. We attribute this to considerable room to improve the emissions performance of ICEs and slower adoption rates of costly electrified solutions in EM, which account for more than half of the global market.

Hanon provides new technology parts and systems solutions for all types of vehicle powertrains. For example, powertrain cooling is used to preventing overheating of the ICE by circulating coolant to remove heat from the engine and expelling it to outside or to the cabin to provide heating for the passengers. Another example is the cold storage evaporator, which is an HVAC (heating, ventilating, air conditioning) heat exchanger targeted for micro hybrid (ISG) and mild hybrid electric vehicle applications. Hanon’s cold storage evaporate enables the climate control system to maintain passenger comfort while the vehicle's engine is turned off by adding a phase change material (PCM) inside the evaporator core.

A third example is the electric wastegate actuator used in turbochargers, which help to reduce fuel consumption but enable more torque with smaller engines. This was gained from the acquisition of the thermal and emissions business of Coopers-Standard. A fourth example is the heat pump system, which can help extend the driving range of EVs as it uses minimal energy to control the temperature of the car. This is a thermal management solution for heating BEV, HEV and ICEs through a heat pump, PTC (positive temperature coefficient) heater and electric heater where there is insufficient waste heat for cabin heating or when there is a need to reduce electrical load. Redirection of refrigerant via valves enables cooling of the vehicle using common system components.

Exhibit 6: Global CO2 targets, grams/km Exhibit 7: Diesel engine NOx emission standards

Sources: ICCT; EU; ACEA; JAMA; EPA estimates Sources: JAMA; ICCT; ACEA estimates

Exhibit 8: NEVs as % of light-vehicle sales

Sources: industry associations; IEA; LMC; BNP Paribas estimates

90

110

130

150

170

190

210

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

(grams/km) EU JapanUS (cars) China

0

50

100

150

200

250

300

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

(mg/km) EU US Japan

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

(%) HEVs PHEVs BEVs FCEVs All NEVs

7 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

In a recent BNP Paribas report [Trying to win a negative sum game, 13 October 2015], Japan Autos analyst Clive Wiggins estimated that compliance with tighter regulations, such as the step up from Euro 5 to Euro 6 standards for NOx emissions, has added EUR600/unit to the cost of diesel-powered cars over the past five years. EGR (Exhaust Gas Recirculation) is an example of a key component with which most diesels are equipped. EGR recirculates cooled exhaust gas to the combustion chamber to reduce oxygen supply and hence the peak combustion temperature. This lowers the amount of NOx produced, but raises CO2 emissions. While industry expectations for the “death of diesel” have become commonplace, ironically the market demand for equipment such as EGRs should increase as diesel regulations become stricter as EGRs, which can lead to fuel savings of c3-5%.

The exhibit below shows Hanon’s portfolio of products and modules used to reduce CO2 and NOx emissions. Two main systems are the exhaust heat recovery system and the EGR module, which both recirculate gas and heat from exhaust within the powertrain to improve powertrain efficiencies and reduce emissions.

The exhibit below shows Hanon’s direct and indirect refrigerant cooling systems, which can be used in HEVs, PHEVs and BEVs to regulate the temperature of the battery module. As electric motors become hot, magnets within the motor lose effectiveness and strength. Likewise, as lithium ion batteries overheat, the conductivity of the electrolyte decreases and hinders the movement of ions, which charge and discharge the battery. Thus thermal management systems are needed.

Exhibit 9: Regulations drive thermal innovation

Source: Hanon Systems

Exhibit 10: Refrigerant direct cooling and refrigerant indirect cooling

Source: Hanon Systems

EPA Off-Cycle Credit

CO₂ (2015 - 2025) Average

EGR (Exhaust Gas Recirculation)

NOx (2015 - 2025) Average

EU : 48%

2015: 130g/km2025: 68g/km

US : 37%

2016: 140g/km2025: 89g/km

EU : 50%

2015: 0.08g/km2025: 0.04g/km

US : 70%

2015: 0.08g/km2025: 0.02g/mi

Active Air Flap

Self-Controlled Auto Transmission Fluid Warmer

Exhaust Heat Recovery System

Wavy Fin Type EGR Cooler

EGR Module

Plastic Housing EGR Cooler

EGR / EHRS / Oil Cooler

Condenser

Evaporator

ThermalExpansion Valve

Compressor

Battery Contact Cooler

Battery Module

Refrigerant Direct Cooling

Condenser

Evaporator

ThermalExpansion Valve

Compressor

Battery Module

Refrigerant Indirect Cooling

Chiller

InductionHeater Pump

8 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

New management to execute revenue and earnings growth strategy

New management targets a sales revenue CAGR of 6% to KRW7.3t by 2020. Hanon plans to diversify the customer base toward what it terms “technology” and “growth” customer groups, while maintaining dominance in its “core” customers – Hyundai Motor Group (HMG) and Ford. Core customers are anchor customers with strong relationships, affordable technology and cost competitiveness. Hanon forecasts a 10-year sales revenue CAGR of 3% for its core customer base to KRW5.2t in 2025, from KRW3.8t in 2015, but a lower revenue contribution of 50%, from 71%. Growth should be fuelled by new model launches and expansion of customer product line-up to include more NEVs. For example, HMG plans to expand its NEV line-up to 22 models from the current 11 models by 2020.

Technology customers such as BMW and Tesla are early adopters of technology requiring advanced co-developed projects and differentiated products, which then cascade down to core customers. Hanon targets a 10-year sales revenue CAGR for technology customers of 16% to KRW1.2t in 2025, from KRW0.3t in 2015, to raise their contribution to 12% from 5%. Growth should stem from increasing supply to high-end hybrid and BEV models. Finally, ‘growth’ customers are large-scale mass brands such as GM and VW, requiring cost competitiveness and significant volumes to justify lower margins. Hanon targets a 10-year sales revenue CAGR of 11% for this segment to KRW3.9t in 2025, from KRW1.3t in 2015, to raise its contribution to 38% from 24%. Supply of both conventional and non-conventional parts and systems in order to improve efficiencies of traditional ICE powertrain models should remain the focus of this large category of customers.

Exhibit 11: Revenue breakdown by customer Exhibit 12: Sales % from non-HMG – Korea Auto Parts

Sources: Company data; BNP Paribas estimates Sources: Company data; BNP Paribas estimates

Exhibit 13: Strategic customer portfolio – Hanon Systems Exhibit 14: Customer diversification target – Hanon Systems

Source: Company data Source: Hanon Systems

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2013 2014 2015E 2016E 2017E

(KRW b) Hyundai Motor Hyundai Mobis Ford Others

0

10

20

30

40

50

60

70

Hanon Systems Mando Wia Mobis

(%) 2013 2016E

Core: Anchor customers with strong relationship, affordable technology, cost competitiveness

Technology: Early adopters requiring advanced co-developed projects and differentiated products, which cascade down to Core customers

Growth: Large-scale mass brands requiring cost competitiveness and huge volumes to justify lower margins

Core50%

Technology12%

Growth38%

2025E

Core71%

Technology5%

Growth24%

2015E

9 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

We forecast a 120bp y-y jump in OPM to 7.2% in 2016, stemming from initial efforts to raise operational efficiencies, and then to 8% by 2020E, through expansion of non-conventional parts supply to c20% of total sales revenue and customer diversification to increase operational leverage. We believe the market will judge new management by the success of its initial execution of cost reduction and efficiency improvement initiatives, which should be reflected in the raising of profit margins within the next few quarters.

While our 2016 forecast calls for a KRW70b increase in operating profit, we believe achievable cost reductions may actually be greater, as management will likely pass on some of the benefits to obtain business wins from new customers. We believe the streamlining of the company’s procurement supply-chain management offers the best opportunity for cost savings, followed by rationalisation of labour and overhead costs.

Since the acquisition of Visteon assets in 2013, there has not been much in the way of visible operational synergies, as the previous regional-based management structure hindered operational synergies post-acquisition. The 2015 results have been down YTD, with a 170bp drop in gross margin to 14.9% as of 9M15 due to the aging product mix of HMG, which translates to lower margins for Hanon, sluggish European business due to underperforming regional plants and EUR currency weakness, and forex hedging losses due to KRW depreciation against USD.

The focus of management in the immediate term is to increase efficiencies by optimising the cost structure, consolidating procurement and implementing standard best practises for manufacturing processes. Such cost reduction efforts are to be accomplished through reorganisation along global functional lines from the previous inefficient local country-based focus, set up of a consolidated IT management system, emphasis on design-cost innovation, raising productivity of underperforming assets, etc.

Management plans to actively expand China sales revenue, which currently stands at cKRW1t, or c19% of total revenues, with 11 plants across the country. Major Chinese OEMs need to partner with qualified global suppliers in order to improve quality, raise fuel economies and reduce emissions. In particular, the race toward lengthening the product line-up of NEVs requires access to various products and technologies, such as heat pump systems, battery coolers, electronic coolant pumps and valves, induction heaters and high voltage electric compressors and air heaters.

Hanon’s China business with local OEMs accounts for only c10% of the company’s China revenues at this time. Some of this legacy business stems from the acquisition of Visteon assets. Hanon says it is engaged in discussions with three of the top five local OEMs and plans to capture business with the remaining two brands. In addition to its wholly-owned China facilities, which house proprietary technology, the company plans to set up new joint ventures with various brands in order to increase

Exhibit 15: OPM trend Exhibit 16: OPM trend by region

Sources: Hanon Systems; BNP Paribas estimates Sources: Hanon Systems; BNP Paribas estimates

0

1

2

3

4

5

6

7

8

4,600

4,800

5,000

5,200

5,400

5,600

5,800

6,000

6,200

6,400

2013 2014 2015E 2016E 2017E

(%)(KRW b) Sales (LHS) OPM (RHS)

0

2

4

6

8

10

12

14

2013 2014 2015E 2016E 2017E

(%) Korea Europe ChinaN America Others

10 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

penetration. As management is aware of the likelihood of some technology leakage through joint venture structures, control of the production process and proprietary technology will remain a key focus.

We believe inorganic growth will continue to enhance enterprise value through acquisition of new technologies, increased penetration into existing customers, while also facilitating diversification of the customer base and widening the product portfolio. The acquisition of Visteon assets for around KRW422b in 2013 is a prime example of Hanon growing the customer base and gaining scale economies. The acquisition of the thermal and emissions business of Coopers-Standard for around KRW47b in 2014 reflects the access to new products and technology, which complement the company’s existing strengths in traditional climate control and system-based solutions. This acquisition should help to drive the contribution of non-conventional parts sales toward management’s target of 20% by 2020.

Hanon maintains a healthy balance sheet in 2015, with not much change from 2014 net gearing of close to 0% and EBITDA/debt of 1.3x. Free cash flow to equity has averaged KRW104b during the past four-year period, along with sustained average annual capex of KRW185b over the same period. R&D expenses of 3.3% of sales in 2014 have risen to 4% in 2015 YTD. However, we expect Hanon’s net cash position to grow to KRW270b by 2018, to enable funding for potential acquisitions.

Exhibit 17: Revenue expansion through M&A

Sources: Hanon Systems; BNP Paribas estimates

Exhibit 18: Free cash flow breakdown Exhibit 19: Net cash trend

Sources: Hanon Systems; BNP Paribas estimates Sources: Hanon Systems; BNP Paribas estimates

0

5

10

15

20

25

30

35

40

45

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2011 2012 2013 2014 2015E 2016E

(y-y %)(KRW b) Hanon Systems (LHS) Visteon (LHS)Cooper Standard (LHS) Revenue growth (RHS)

0

50

100

150

200

250

(600)

(400)

(200)

0

200

400

600

800

2014 2015E 2016E 2017E 2018E

(KRW b)(KRW b)

Depreciation Pre-tax profitCAPEX Net working capital changeOther Free Cash Flow (RHS)

(50)

0

50

100

150

200

250

300

2014 2015E 2016E 2017E 2018E

(KRW b)

11 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Positive commitment to shareholder-friendly initiatives

New management set forth three shareholder-friendly initiatives to be set in motion in 2016. The first is to increase liquidity of the existing 30% free float through a 1:5 stock split in 1Q16. This will increase the number of outstanding shares to 533.8m from the current 106.8m. The second is the implementation of a stock-option plan for senior management in order to align its objectives directly in line with those of minority shareholders. The third initiative is to pay quarterly dividends in order to regulate returns to investors throughout the year.

The CFO guides for a steady dividend per share in 2015, similar in amount to the KRW970/share paid to shareholders in 2014, regardless of the company’s earnings this year. During the past four-year period, Hanon’s dividend payout ratio has averaged 33%. While no formal dividend policy based on cash flow or payout of profits has been established by the new management, the CFO guides the stability of absolute dividends to be the main focus for the time being. Based on our 2015 earnings forecast, we estimate dividend per share of KRW970 to equate to a payout ratio of 40%. Subsequently, we expect the dividend payout to rise by 25% per annum during our forecast period, to lead to a payout ratio of 50% in 2018E.

The past dividend history of Hanon places it at the top among global and domestic peers in terms of payout ratio to shareholders. For the most part, the global auto industry offers a dividend payout in the broad range of 20-30%, with higher levels only in rare instances. As such, we believe shareholder returns are one reason why Hanon shares should trade at a premium to peers. We believe expectations for a further increase in payout are justified as this would reflect alignment of a common objective for management, owners, as well as minority shareholders.

Exhibit 20: Timeline for Hanon Systems’ stock split

From To

Board of Directors' resolution 11/5/2015

Shareholders’ meeting 12/22/2015

Tendering of existing shares 12/23/2015 1/25/2016

Suspension of trading 1/22/2016 2/15/2016

Listing of new shares 2/16/2016

Source: FSS

Exhibit 21: Dividend pay-out ratio – Korea Auto Parts Exhibit 22: Dividend and yield trend – Hanon Systems

Sources: Hanon Systems; BNP Paribas estimates Sources: Hanon Systems; BNP Paribas estimates

0

10

20

30

40

50

Hanon Systems Mando Wia Mobis

(%) 2013 2014 2015E 2016E

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

400

800

1,200

1,600

2,000

2014 2015E 2016E 2017E 2018E

(%)(KRW) DPS (LHS) Dividend yield (RHS)

12 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Key charts

Product line-up

Exhibit 23: Hanon System’s main products

Climate Control ICE Thermal Management System EV Thermal Management System

HVAC Compressor Cooling Module TF Coolant heater Heat Pump System

Fluid Transport Controller Charge Air Cooler EGR System HV BLDC Cooling Fan Motor

Battery Thermal Management

Ionizer Cooling Module Cold Storage Evaporator Transmission Thermal Management Turbo Blower COD Heater

Source: Hanon Systems

Exhibit 24: Hanon System’s main products (continued)

Source: Hanon Systems

Exhaust Heat Recovery

Battery Thermal Management

Heat PumpSystem

Thin Film HeaterExhaust GasRecirculation

Air ChargeAir Cooler

Water ChargeAir Cooler

Coolant Heater

Centrifugal AirCompressor

High voltage Positive Temperature Coefficient Heater

13 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Exhibit 25: Hanon Systems – new technology product

Name Description

Efficient

Water Cooled Condenser

Hanon Systems’ water-cooled condenser is a new concept in vehicle air conditioning and can be included in a heat pump system. It transfers heat from the refrigerant circulating in the system to coolant as an intermediate medium

VS Compressor

A variable swashplate compressor is a pump that can vary its duty cycle and change the amount of refrigerant displaced, which improves power consumption compared to a fixed displacement compressor

RS Compressor

A rotary suction compressor is a pump with a fixed displacement swashplate that draws refrigerant through the centre shaft to deliver better fuel economy by creating less suction loss compared to a traditional suction valve

Cold Storage Evaporator

A cold storage evaporator is an HVAC heat exchanger targeted for micro hybrid (stop-start) and mild hybrid electric vehicle applications. Hanon Systems’ cold storage evaporate enables an A/C system to maintain passenger comfort while the vehicle's engine is turned off by adding a phase change material (PCM) inside the evaporator core

Comfort

High Efficiency Blower

A high efficiency blower scroll re-conceptualized HVAC wheel and scroll geometry to improve power consumption. Hanon Systems has leveraged its expertise in fluid and thermal dynamics to create new shapes and flow patterns to optimize HVAC efficiency

UV LED and Photo catalyst Module

An ultraviolet (UV) light emitting diode (LED) and photocatalyst are electronic devices that generate radicals that attach to and eliminate odour causing substances. Hanon Systems has added this UV LED and Photocatalyst technology to an HVAC module to remove odour causing gases and microorganisms that can grow on an evaporator

CO₂ Sensor

A CO₂ sensor monitors the levels of carbon dioxide in a vehicle cabin. When Hanon Systems’ CO₂ sensor detects level that exceed the threshold, the sensor signals the HVAC to introduce fresh air

Fragrance Module

A fragrance dispenser diffuses a pleasant aroma in the cabin when running the ventilation system. Hanon Systems’ fragrance module offers vehicle occupants a choice of two scents with a toggle witch to turn the system on and off

Eco-Friendly

Fuel Cell Brushless DC Motor

A fuel cell stack, which provides electric power to operate a fuel cell vehicle, generates more heat and needs more cooling power than an internal combustion engine. A cooling module with high power BLDC motors is needed to reduce the temperature of a fuel cell stack, allowing operation in optimal thermal conditions

Fuel Cell Centrifugal Air Compressor

A centrifugal air compressor is a turbine that forces high pressure oxygen into a fuel cell stack to power a fuel cell electric vehicle (FCEV). Hanon Systems’ innovative centrifugal air compressor provides a clean air supply and significantly improves durability and NVH performance compared to a traditional dual lobe screw compressor

Fuel Cell Glycol Heater

A fuel cell glycol heater heats the fuel cell stack for optimal operation during cold start conditions and eliminates oxygen build up around a fuel cell cathode in the event of a vehicle impact.

Heat Pump

A heat pump is a thermal management solution for heating electric, hybrid and internal-combustion engine vehicles where there is insufficient waste heat for cabin heating or when there is a need to reduce electrical load. Redirection of refrigerant via valves enables cooling of the vehicle using common system components.

Source: Hanon Systems

Exhibit 26: Hanon’s hybrid/EV product line-up

Source: Hanon Systems

MicroHybrid

(Idle stop)

Mildhybrid(48V)

FullHybrid

Plug-inHybrid

Fuel CellEV

ElectricVehicle

Kia K5 Hybrid

Kia K5 Hybrid

LF Sonata

2014 Kia PS EV

BMW i3

Hyundai LMFC

Cold Storage Evaporator

48V eCompressor

48V Cooling Fan Motor

48V eSupercharger

High voltageeCompressor

High voltageeCompressor

Exhaust HeatRecovery System

HV iCool Centrifuged Air Compressor

Cathode Oxygen Depletion Heater

HV iCond

Induction HeaterHigh Voltage

Cooling Module

14 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Exhibit 27: Product portfolio by market trend

Efficient Light, Compact Turbo Diesel Stop-Start e-Mobility

HV Modular Family Variable Compressor Sliding Door HVAC Charge Air Cooler (CAC) Exhaust Gas

Recirculation (EGR) Cold Storage Evaporator FCEV Centrifugal Air Compressor

Blower Scroll Rotary Suction Compressor (0.4kg lighter than Previous) Water-Cooled CAC Positive Temp

Coefficient Heater 48V e-Compressor Heat Pump

Standardised High Performance-to-weight Evaporator and Heater

Split Condenser (0.24 Drag Coefficient) Low Temp Radiator Exhaust Heat Recovery

Systems (EHRS) Electronic Coolant Pump Battery Thermal Management

Water-Air Cooled Condenser Charge Air Pre-Conditioner Electronic Coolant Valve HV iCool

Source: Hanon Systems

15 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Operations

Hanon controls 52% of the Korean climate control market by sales revenue, as the first-tier supplier to HMG, with Doowon (unlisted) as the second-tier supplier with 27% market share. Korea Delphi (unlisted) controls 13% of the marker as the main supplier to GM-Daewoo (unlisted). In the global market, Hanon is the second-largest climate control supplier with 13% market share after Denso which is the main supplier to Toyota. Valeo is the largest European supplier with a global revenue market share of 13%.

As of 2014, air conditioners are the main product of Hanon, accounting for 70% of the total product mix. This is followed by compressors with 21% contribution. In terms of geographies, Korea and Europe are the main markets with respective 28% and 31% contributions to total sales revenue, mainly due to Hanon’s core customers HMG and Ford. This is followed by China and North America, both with roughly 15% of total sales revenue, again mainly due to the company’s core customer base.

Exhibit 28: Domestic climate control market share (2014) Exhibit 29: Global climate control market share (2013)

Source: Company date Sources: Company data; BNP Paribas estimates

Exhibit 30: Revenue breakdown by product Exhibit 31: Revenue breakdown by region

Sources: Hanon Systems; BNP Paribas estimates Sources: Hanon Systems; BNP Paribas estimates

Hanon Systems

52%

Doowon Climate Control

27%

Korea Delphi13%

Others8%

Denso24%

Hanon Systems

13%

Valeo13%Behr

8%

Calsonic5%

Sanden5%

Others32%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2013 2014 2015E 2016E 2017E

(KRW b) Air conditioner Compressor FEM Radiator

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2013 2014 2015E 2016E 2017E

(KRW b) Korea Europe China N America Others

16 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Historical valuations

Hanon’s shares have been trading above their nine-year average P/E and P/B levels since the acquisition of Visteon assets in 2013, due to the surge in top-line revenues, expectations for continued M&A-fuelled growth and ownership issues with the 70% ownership stake of Visteon up for sale. We believe expectations for further customer diversification, inorganic growth opportunities and structural recovery of profit margins justifies the potential 22% upside to our KRW60,000 target price.

Exhibit 32: Historical P/E Exhibit 33: Historical P/BV

Sources: Hanon Systems; BNP Paribas estimates Sources: Hanon Systems; BNP Paribas estimates

Exhibit 34: Historical EV/EBTIDA

Sources: Hanon Systems; BNP Paribas estimates

Exhibit 35: DuPont analysis

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E FY18E

Net margin (%) 4.6 6.8 6.4 5.7 5.1 4.5 5.4 5.6 5.8

Asset turnover (%) 155.5 161.7 163.4 175.7 168.4 162.7 161.2 160.2 160.2

Equity multiplier (x) 1.8 1.7 1.7 2.0 2.1 2.0 1.9 1.8 1.7

ROE (%) 12.7 18.9 17.6 20.6 17.8 14.6 16.4 16.2 15.9

Sources: Hanon Systems; BNP Paribas estimates

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Jun-

06Ja

n-07

Aug-

07M

ar-0

8O

ct-0

8M

ay-0

9D

ec-0

9Ju

l-10

Feb-

11Se

p-11

Apr-1

2N

ov-1

2Ju

n-13

Jan-

14Au

g-14

Mar

-15

Oct

-15

(KRW)

4.4x

8.9x

13.4x

17.9x

22.3x

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Jan-

06Au

g-06

Mar

-07

Oct

-07

May

-08

Dec

-08

Jul-0

9Fe

b-10

Sep-

10Ap

r-11

Nov

-11

Jun-

12Ja

n-13

Aug-

13M

ar-1

4O

ct-1

4M

ay-1

5

(KRW)

3.3x

2.7x

2.0x

1.4x

0.7x

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Jun-

06Ja

n-07

Aug-

07M

ar-0

8O

ct-0

8M

ay-0

9D

ec-0

9Ju

l-10

Feb-

11Se

p-11

Apr-1

2N

ov-1

2Ju

n-13

Jan-

14Au

g-14

Mar

-15

Oct

-15

(KRW b)

11.2x

9.1x

7.0x

4.8x

2.7x

17 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Appendix

Exhibit 36: Shareholding structure – Hanon Systems

Source: Hanon Systems

Exhibit 37: Hanon Systems History

Date Event

1986 Established as Joint Venture between Ford motor Co. and Mando Machinery Corp

1996 Listed on Korea stock Exchange

1999 Visteon became the majority shareholder

2006 Ownership increase in Canada, Portugal, and Thailand (from Visteon)

2007 Ownership increase in India, Beijing and Alabama (from Visteon)

2008 Acquired ownership in Slovakia (from Visteon)

2009 Obtained 100% controlling interests in HVCC Alabama

Sep 2012 Transaction outlined to acquire Visteon Climate business (18 entities and intellectual property)

Jan 2013 Acquired Visteon's climate business

Mar 2013 Changed company name from Halla Climate Control Corp to Halla Visteon Climate Control Corp

Jul 2014 Acquired Cooper-Standard Automotive's thermal and emission business

Sep 2014 Acquisition of majority stake in JCS Nanjing, China

Dec 2014 Hahn & Co. and Hankook Tire acquired Visteon's stake to become majority shareholders

Source: Hanon Systems

Exhibit 38: Major events vs share price v

Source: Hanon Systems

Hahn&Co50.5%

Hankook Tire19.5%

Other30.0%

0

10,000

20,000

30,000

40,000

50,000

60,000

Jan-06 Oct-06 Jul-07 Apr-08 Jan-09 Oct-09 Jul-10 Apr-11 Jan-12 Oct-12 Jul-13 Apr-14 Jan-15 Oct-15

(KRW)

Air-conditioner order of KRW 170b from VW

Application for bankruptcy protection by Visteon

Air-conditioner compressore order of $ 30m from Chrysler

Master service agreement with Visteon

Visteon launches tender offer for Halla Climate Control

Air-conditioner order of KRW 56b from Tesla

Korea's National Pension Service rejects Visteon Tender offer

Acquired Visteon's climate business

Acquires Cooper-Standard automotive/s thermal and emissions business

Visteon decided to sell its stake (70%) to Hahn&Co and Hankook Tire

18 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Corporate governance

Board structure

Number of Independent Directors (ID) 5

Percentage of IDs in the board 55.6%(5/9)

ID participation/attendance at board meetings 95%

ID participation in audit/remuneration committees 100%

ID terms (years of service, re-election/replacement procedures) 3 years or less; Nominating Committee will make recommendations to the Board on all appointments, while appointments are finalised at the general meeting

Sources: Hanon Systems; BNP Paribas

Audit Practices

Auditor EY Han Young

Length of service 2 years

Reporting incidents NIL

Fee track record 380m KRW (FY2014)

Policy on change of Audit firm Reviewed annually at the AGM

Sources: Hanon Systems; BNP Paribas

Compensation and remuneration

Directors' remuneration vs. earnings/ROE/share performance KRW492m (FY14)

Changes/stability in senior management As Visteon sold its ownership to Hahn & Co. and Hankook Tire in December, 2014, c50% of senior management was newly appointed in FY15

Incidents of termination of senior management NIL

Track record on Insider sales NIL

Sources: Hanon Systems; BNP Paribas

Shareholders' rights

Communication - shareholder participation in AGMs/EGMs Periodic and timely communication with shareholders for AGM/EGM

Related party transactions In FY14, the company had KRW155.6b in related party transactions for sales, purchase of raw materials, services, fixed asset purchase and disposal, etc.

Voting issues - policies, incidents of rejected proposals NIL

Sources: Hanon Systems; BNP Paribas

19 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Financial statements Hanon Systems

Sources: Hanon Systems; BNP Paribas estimates

Profit and Loss (KRW b) Year Ending Dec 2013A 2014A 2015E 2016E 2017E

Revenue 5,189 5,455 5,537 5,814 6,153

Cost of sales ex depreciation (4,164) (4,381) (4,526) (4,681) (4,936)

Gross profit ex depreciation 1,025 1,074 1,011 1,134 1,216Other operating income 0 0 0 0 0

Operating costs (500) (538) (502) (538) (575)

Operating EBITDA 525 536 508 596 641Depreciation (160) (163) (170) (171) (173)

Goodwill amortisation (2) (2) (4) (4) (4)

Operating EBIT 364 370 335 421 464Net financing costs 0 (12) (21) (20) (18)

Associates 8 13 14 15 15

Recurring non operating income 33 13 30 31 31

Non recurring items 0 0 0 0 0

Profit before tax 397 371 344 431 478Tax (85) (80) (83) (104) (116)

Profit after tax 312 290 261 327 362Minority interests (16) (15) (14) (17) (19)

Preferred dividends 0 0 0 0 0

Other items 0 0 0 0 0

Reported net profit 296 275 247 310 343Non recurring items & goodwill (net) 2 2 4 4 4

Recurring net profit 298 278 251 314 347

Per share (KRW)

Recurring EPS * 2,793 2,601 2,352 2,943 3,253

Reported EPS 2,776 2,579 2,314 2,904 3,214

DPS 970 970 970 1,200 1,500

Growth

Revenue (%) 42.1 5.1 1.5 5.0 5.8

Operating EBITDA (%) 24.5 1.9 (5.1) 17.2 7.6

Operating EBIT (%) 17.4 1.9 (9.6) 25.7 10.3

Recurring EPS (%) 27.9 (6.9) (9.6) 25.1 10.6

Reported EPS (%) 28.0 (7.1) (10.3) 25.5 10.7

Operating performance

Gross margin inc depreciation (%) 16.7 16.7 15.2 16.6 17.0

Operating EBITDA margin (%) 10.1 9.8 9.2 10.3 10.4

Operating EBIT margin (%) 7.0 6.8 6.0 7.2 7.5

Net margin (%) 5.7 5.1 4.5 5.4 5.6

Effective tax rate (%) 21.3 21.7 24.2 24.2 24.2

Dividend payout on recurring profit (%) 34.7 37.3 41.2 40.8 46.1

Interest cover (x) n/a 31.4 17.4 22.9 28.1

Inventory days 24.7 30.0 31.2 31.1 31.1

Debtor days 52.0 58.7 60.9 58.0 56.9

Creditor days 49.5 56.6 53.6 50.0 49.5

Operating ROIC (%) 24.5 20.2 16.0 18.7 19.2

ROIC (%) 22.2 17.2 14.3 16.5 16.9

ROE (%) 20.6 17.8 14.6 16.4 16.2

ROA (%) 12.1 9.8 8.5 9.9 10.2*Pre exceptional pre-goodwill and fully diluted

Revenue By Division (KRW b) 2013A 2014A 2015E 2016E 2017E

Air conditioner 3,482 3,791 4,043 4,249 4,505

Compressor 1,193 1,152 1,046 1,095 1,151

Radiator 400 386 320 335 352

Module 113 126 128 136 145

20 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Financial statements Hanon Systems

Sources: Hanon Systems; BNP Paribas estimates

Cash Flow (KRW b) Year Ending Dec 2013A 2014A 2015E 2016E 2017E

Recurring net profit 298 278 251 314 347

Depreciation 160 163 170 171 173

Associates & minorities (24) (28) (27) (32) (34)

Other non-cash items (5) 5 14 14 14

Recurring cash flow 431 420 411 472 504Change in working capital (75) (79) (82) 22 (79)

Capex - maintenance (193) (269) (270) (270) (270)

Capex - new investment 0 0 0 0 0

Free cash flow to equity 164 71 59 224 155Net acquisitions & disposals (422) (47) 0 0 0

Dividends paid (76) (104) (104) (104) (128)

Non recurring cash flows 53 22 76 11 14

Net cash flow (281) (57) 32 131 41Equity finance 0 0 0 0 0

Debt finance 226 92 3 (40) (37)

Movement in cash (54) 34 34 91 4

Per share (KRW)

Recurring cash flow per share 4,040 3,933 3,853 4,422 4,725

FCF to equity per share 1,536 668 556 2,096 1,454

Balance Sheet (KRW b) Year Ending Dec 2013A 2014A 2015E 2016E 2017E

Working capital assets 1,358 1,475 1,501 1,496 1,608

Working capital liabilities (962) (999) (943) (960) (993)

Net working capital 396 476 557 536 615Tangible fixed assets 970 1,053 1,122 1,220 1,317

Operating invested capital 1,366 1,528 1,679 1,756 1,932Goodwill 0 0 0 0 0

Other intangible assets 156 172 198 199 200

Investments 86 87 92 105 121

Other assets 37 72 76 79 83

Invested capital 1,645 1,859 2,044 2,140 2,337Cash & equivalents (347) (381) (416) (507) (511)

Short term debt 72 124 338 197 161

Long term debt * 237 277 66 167 167

Net debt (37) 20 (12) (143) (184)Deferred tax 0 0 0 0 0

Other liabilities 63 72 75 75 75

Total equity 1,494 1,619 1,810 2,033 2,267

Minority interests 47 51 63 63 63

Invested capital 1,645 1,859 2,044 2,140 2,337

Per share (KRW)

Book value per share 13,995 15,160 16,951 19,044 21,236

Tangible book value per share 12,534 13,551 15,100 17,181 19,359

Financial strength

Net debt/equity (%) (2.4) 1.2 (0.6) (6.8) (7.9)

Net debt/total assets (%) (1.3) 0.6 (0.3) (4.0) (4.8)

Current ratio (x) 1.6 1.7 1.5 1.7 1.8

CF interest cover (x) n/a 6.8 3.8 12.2 9.7

* includes convertables and preferred stock which is being treated as debt

Valuation 2013A 2014A 2015E 2016E 2017E

Recurring P/E (x) * 17.6 18.9 20.9 16.7 15.1

Recurring P/E @ target price (x) * 21.5 23.1 25.5 20.4 18.4

Reported P/E (x) 17.7 19.0 21.2 16.9 15.3

Dividend yield (%) 2.0 2.0 2.0 2.4 3.1

P/CF (x) 12.2 12.5 12.7 11.1 10.4

P/FCF (x) 32.0 73.5 88.3 23.4 33.8

Price/book (x) 3.5 3.2 2.9 2.6 2.3

Price/tangible book (x) 3.9 3.6 3.3 2.9 2.5

EV/EBITDA (x) ** 9.3 9.9 10.1 8.5 7.8

EV/EBITDA @ target price (x) ** 11.6 12.0 12.2 10.5 9.7

EV/invested capital (x) 3.2 2.9 2.6 2.4 2.2* Pre exceptional & pre-goodwill and fully diluted ** EBITDA includes associate income and recurring non operating income

21 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Disclaimers and Disclosures

APPENDIX

DISCLAIMERS AND DISCLOSURES APPLICABLE TO NON-US BROKER-DEALER(S): BNP PARIBAS SECURITIES KOREA CO LTD

ANALYST(S) CERTIFICATION

H James Yoon, BNP Paribas Securities Korea Co Ltd , +822 2125 0533, [email protected] The BNP Paribas Securities Korea Co Ltd Analysts mentioned in this disclaimer are employed by a non-US affiliate of BNP Paribas Securities Corp., and are not registered/ qualified pursuant to NYSE and/or FINRA regulations

The individual(s) identified above certify(ies) that (i) all views expressed in this report accurately reflect the personal view of the analyst(s) with regard to any and all of the subject securities, companies or issuers mentioned in this report; and (ii) no part of the compensation of the analyst(s) was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed herein.

IMPORTANT DISCLOSURES REQUIRED IN THE UNITED STATES BY FINRA RULES AND OTHER JURISDICTIONS "BNP Paribas” is the marketing name for the global banking and markets business of BNP Paribas Group. No portion of this report was prepared by BNP Paribas Securities Corp (US) personnel, and it is considered Third-Party Affiliate research under NASD Rule 2711. The following disclosures relate to relationships between companies covered in this research report and the BNP entity identified on the cover of this report, BNP Securities Corp., and other entities within the BNP Paribas Group (collectively, "BNP Paribas"). The disclosure column in the following table lists the important disclosures applicable to each company that has been rated and/or recommended in this report:

BNP Paribas represents that: 1. Within the past year, it has managed or co-managed a public offering for this company, for which it received fees. 2. It had an investment banking relationship with this company in the last 12 months. 3. It received compensation for investment banking services from this company in the last 12 months. 4. It expects to receive or intends to seek compensation for investment banking services from the subject company/ies in the next 3 months. 5. It beneficially owns 1% or more of any class of common equity securities of the subject company. 6. It makes a market in securities in respect of this company. 7. The analyst(s) or an individual who assisted in the preparation of this report (or a member of his/her household) has a financial interest position in

securities issued by this company. The financial interest is in the common stock of the subject company, unless otherwise noted. 8. The analyst (or a member of his/her household) is an officer, director, or advisory board member of this company or has received compensation from the

company.

IMPORTANT DISCLOSURES REQUIRED IN KOREA The disclosure column in the following table lists the important disclosures applicable to each Korea listed company that has been rated and/or recommended in this report:

1. The performance of obligations of the Company is directly or indirectly guaranteed by BNP Paribas Securities Korea Co. Ltd (“BNPPSK”) by means of payment guarantees, endorsements, and provision of collaterals and/or taking over the obligations.

2. BNPPSK owns 1/100 or more of the total outstanding shares issued by the Company. 3. The Company is an affiliate of BNPPSK as prescribed by Item 3, Article 2 of the Monopoly Regulation and Fair Trade Act. 4. BNPPSK is the financial advisory agent of the Company for the Merger and Acquisition transaction or of the Target Company whereby the size of the

transaction does not exceed 5/100 of the total asset of the Company or the total number of outstanding shares. 5. BNPPSK has taken financial advisory service regarding listing to the Company within the past 1 year. 6. With regards to the tender offer initiated by the Company based on Item 2, Article 133 of the Financial Investment Services and Capital Market Act,

BNPPSK acts in the capacity of the agent for the tender offer designated either by the Company or by the target company, provided that this provision shall apply only where tender offer has not expired.

7. The listed company which issued the stocks in question in case where 40 days has not passed since the new shares were listed from the date of entering into arrangement for public offering or underwriting-related agreement for issuance of stocks

8. The Company that has signed a nominated advisor contract with BNPPSK as defined in Item 2 of Article 8 of the KONEX Market Listing Regulation. 9. The Company is recognized as having considerable interests with BNPPSK in relation to No.1 to No. 8. 10. The analyst or his/her spouse owns (including delivery claims of marketable securities based on legal regulations and trading and misc. contracts) the

following securities or rights (hereinafter referred to as “Securities, etc.” in this Article) regardless of whose name is used in the trading. 1) Stocks, bond with stock certificate, and certificate of pre-emptive rights issued by the Company whose securities dealings are being solicited. 2) Stock options of the Company whose securities dealings are being solicited. 3) Individual stock future, stock option, and warrants that use the stocks specified in Item 1) as underlying.

GENERAL DISCLAIMER

This report was produced by BNP Paribas Securities Korea Co Ltd , member company(ies) of the BNP Paribas Group.

This report is for the use of intended recipients only and may not be reproduced (in whole or in part) or delivered or transmitted to any other person without our prior written consent. By accepting this report, the recipient agrees to be bound by the terms and limitations set forth herein. This report does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Customers are advised to use the information contained herein as just one of many inputs and considerations prior to engaging in any

Company Ticker Disclosure (as applicable)

N/A N/A N/A

Company Ticker Price (as of 09-Dec-2015 closing price) InterestHanon Systems 018880 KS KRW44,250 N/A

22 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

trading activity. This report does not constitute a prospectus or other offering document or an offer or solicitation to buy or sell any securities or other investments. This report is not intended to provide the sole basis of any evaluation of the subject securities and companies mentioned in this report. Information and opinions contained in this report are published for reference of the recipients and are not to be relied upon as authoritative or without the recipient’s own independent verification, or taken in substitution for the exercise of judgment by the recipient. Additionally, the products mentioned in this report may not be available for sale in certain jurisdictions. As an investment bank with a wide range of activities, BNP Paribas may face conflicts of interest, which are resolved under applicable legal provisions and internal guidelines. You should be aware, however, that BNP Paribas may engage in transactions in a manner inconsistent with the views expressed in this document, either for its own account or for the account of its clients. Australia: This report is being distributed in Australia by BNP Paribas Sydney Branch, registered in Australia as ABN 23 000 000 117 at 60 Castlereagh Street Sydney NSW 2000. BNP Paribas Sydney Branch is licensed under the Banking Act 1959 and the holder of Australian Financial Services Licence no. 238043 and therefore subject to regulation by the Australian Securities & Investments Commission in relation to delivery of financial services. By accepting this document you agree to be bound by the foregoing limitations, and acknowledge that information and opinions in this document relate to financial products or financial services which are delivered solely to wholesale clients (in terms of the Corporations Act 2001, sections 761G and 761GA; Corporations Regulations 2001, division 2, reg. 7.1.18 & 7.1.19) and/or professional investors (as defined in section 9 of the Corporations Act 2001). Canada: The information contained herein is not, and under no circumstances is to be construed as, a prospectus, an advertisement, a public offering, an offer to sell securities described herein, or solicitation of an offer to buy securities described herein, in Canada or any province or territory thereof. Any offer or sale of the securities described herein in Canada will be made only under an exemption from the requirements to file a prospectus with the relevant Canadian securities regulators and only by a dealer properly registered under applicable securities laws or, alternatively, pursuant to an exemption from the dealer registration requirement in the relevant province or territory of Canada in which such offer or sale is made. The information contained herein is under no circumstances to be construed as investment advice in any province or territory of Canada and is not tailored to the needs of the recipient. To the extent that the information contained herein references securities of an issuer incorporated, formed or created under the laws of Canada or a province or territory of Canada, any trades in such securities must be conducted through a dealer registered in Canada. No securities commission or similar regulatory authority in Canada has reviewed or in any way passed judgment upon these materials, the information contained herein or the merits of the securities described herein, and any representation to the contrary is an offence. Hong Kong: This report is prepared for professional investors and is being distributed in Hong Kong by BNP Paribas Securities (Asia) Limited to persons whose business involves the acquisition, disposal or holding of securities, whether as principal or agent. BNP Paribas Securities (Asia) Limited, a subsidiary of BNP Paribas, is regulated by the Securities and Futures Commission for the conduct of dealing in securities, advising on securities, providing automated trading services, dealing in futures contacts and advising on corporate finance. For professional investors in Hong Kong, please contact BNP Paribas Securities (Asia) Limited for all matters and queries relating to this report. India: In India, this document is being distributed by BNP Paribas Securities India Pvt. Ltd. ("BNPPSIPL"), having its registered office at 5th floor, BNP Paribas House, 1 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra (East), Mumbai 400 051, INDIA (Tel. no. +91 22 3370 4000 / 6196 4000, Fax no. +91 22 6196 4363). BNPPSIPL is registered with the Securities and Exchange Board of India (“SEBI”) as a research analyst (Regn. No. INH000000792) and as a stockbroker in the Equities and the Futures & Options segments of National Stock Exchange of India Ltd. and BSE Ltd. (SEBI Regn. Nos.: INB/INF/NSF231474835, INB/INF011474831; CIN: U74920MH2008FTC182807; Website: www.bnpparibas.co.in). No material disciplinary action has been taken against BNPPSIPL by any regulatory or government authority. Indonesia: This report is being distributed by PT BNP Paribas Securities Indonesia and is delivered by its licensed employee(s), including marketing/sales person, to its client. PT BNP Paribas Securities Indonesia, having its registered office at Menara BCA, 35th floor, Grand Indonesia, JL. M.H. Thamrin No.1, Jakarta 10310, Indonesia, is a subsidiary company of BNP Paribas SA and licensed under Capital Market Law no. 8 year 1995, a holder of broker-dealer and underwriter licenses issued by the Capital Market and Financial Institution Supervisory Agency (now Otoritas Jasa Keuangan/OJK). PT BNP Paribas Securities Indonesia is also a member of Indonesia Stock Exchange and supervised by Otoritas Jasa Keuangan (OJK). Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens except in compliance with applicable Indonesian capital market laws and regulations. This report is not an offer of securities in Indonesia and may not be distributed within the territory of the Republic of Indonesia or to Indonesian citizens in circumstance which constitutes an offering within the meaning of Indonesian capital market laws and regulations. Japan: This report is being distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited or by a subsidiary or affiliate of BNP Paribas not registered as a financial instruments firm in Japan, to certain financial institutions defined by article 17-3, item 1 of the Financial Instruments and Exchange Law Enforcement Order. BNP Paribas Securities (Japan) Limited is a financial instruments firm registered according to the Financial Instruments and Exchange Law of Japan and a member of the Japan Securities Dealers Association, the Financial Futures Association of Japan and the Type II Financial Instruments Firms Association. BNP Paribas Securities (Japan) Limited accepts responsibility for the content of a report prepared by another non-Japan affiliate only when distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited. Some of the foreign securities stated on this report are not disclosed according to the Financial Instruments and Exchange Law of Japan. Malaysia: This report is issued and distributed by BNP Paribas Capital (Malaysia) Sdn Bhd. The views and opinions in this research report are our own as of the date hereof and are subject to change. BNP Paribas Capital (Malaysia) Sdn Bhd has no obligation to update its opinion or the information in this research report. This publication is strictly confidential and is for private circulation only to clients of BNP Paribas Capital (Malaysia) Sdn Bhd. This publication is being provided to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of BNP Paribas Capital (Malaysia) Sdn Bhd. Philippines: This report is being distributed in the Philippines by BNP Paribas Manila Branch, an Offshore Banking Unit (OBU) of BNP Paribas whose head office is in Paris, France. BNP Paribas Manila OBU is registered as an offshore banking unit under Presidential Decree No. 1034 (PD 1034), and regulated by the Bangko Sentral ng Pilipinas. This report is being distributed in the Philippines to qualified clients of OBUs as allowed under PD 1034, and is qualified in its entirety to the products and services allowed under PD 1034. Singapore: This report is distributed in Singapore by BNP Paribas Securities (Singapore) Pte Ltd ("BNPPSSL") and may be distributed in Singapore only to an Accredited or Institutional Investor, each as defined under the Financial Advisers Regulations ("FAR") and the Securities and Futures Act (Chapter 289) of Singapore, as amended from time to time. In relation to the distribution to such categories of investors, BNPPSSL and its representatives are exempted under Regulation 35 of the FAR from the requirements in Section 36 of the Financial Advisers Act of Singapore, regarding the disclosure of certain interests in, or certain interests in the acquisition or disposal of, securities referred to in this report. For Institutional and Accredited Investors in Singapore, please contact BNP Paribas Securities (Singapore) Ptd Ltd (company registration number: 199801966C; address: 10 Collyer Quay, 34/F Ocean Financial Centre, Singapore 049315; tel: (65) 6210 1288; fax: (65) 6210 1980) for all matters and queries relating to this report. South Africa: In South Africa, BNP Paribas Securities South Africa (Pty) Ltd is a licensed member of the Johannesburg Stock Exchange and an authorised Financial Services Providers and subject to regulation by the Financial Services Board. BNP Paribas Securities South Africa (Pty) Ltd does not expressly or by implication represent, recommend or propose that the financial products referred to in this report are appropriate to the particular investment objectives, financial situation or particular needs of the recipient. This document does not constitute advice as contemplated in the Financial Advisory and Intermediary Services Act, 2002. South Korea: BNP Paribas Securities Korea is registered as a Licensed Financial Investment Business Entity under the FINANCIAL INVESTMENT SERVICES AND CAPITAL MARKETS ACT and regulated by the Financial Supervisory Service and Financial Services Commission. This document does not constitute an offer to sell to or the solicitation of an offer to buy from any person any financial products where it is unlawful to make the offer or solicitation in South Korea. Switzerland: This report is intended solely for customers who are “Qualified Investors” as defined in article 10 paragraphs 3 and 4 of the Swiss Federal Act on Collective Investment Schemes of 23 June 2006 (CISA) and the relevant provisions of the Swiss Federal Ordinance on Collective Investment Schemes of 22 November 2006 (CISO). “Qualified Investors” includes, among others, regulated financial intermediaries such as banks, securities dealers, fund management companies and asset managers of collective investment schemes, regulated insurance companies as well as pension funds and companies with professional treasury operations. This document may not be suitable for customers who are not Qualified Investors and should only be used and passed on to Qualified Investors. For specification purposes, a “Swiss Corporate Customer” is a Client which is a corporate entity, incorporated and existing under the laws of

23 BNP PARIBAS 11 DECEMBER 2015

Hanon Systems 018880 KS H James Yoon

Switzerland and which qualifies as “Qualified Investor” as defined above." BNP Paribas (Suisse) SA is authorised as bank and as securities dealer by the Swiss Federal Market Supervisory Authority FINMA. BNP Paribas (Suisse) SA is registered at the Geneva commercial register under No. CH-270-3000542-1. BNP Paribas (Suisse) SA is incorporated in Switzerland with limited liability. Registered Office: 2 place de Hollande, CH-1204 Geneva. Taiwan: Information on securities that trade in Taiwan is distributed by BNP Paribas Securities (Taiwan) Co., Ltd. Such information is for your reference only. The reader should independently evaluate the investment risks and is solely responsible for their investment decision. Information on securities that do not trade in Taiwan is for informational purposes only and is not to be construed as a recommendation or a solicitation to trade in such securities. BNP Paribas Securities (Taiwan) Co., Ltd. may not execute transactions for clients in these securities. This publication may not be distributed to the public media or quoted or used by the public media without the express written consent of BNP Paribas.