klausur für das cera modul d - aktuar.de · „brutto“- und „netto“-risikokapitalien für...

TRANSCRIPT

1

Klausur für das CERA Modul D 20.05.2017

Die Klausur hat insgesamt 180 Punkte. Zum Bestehen der Klausur sind 90 Punkte notwendig. Zur

Orientierung bei der Bearbeitungszeit: jeder Bewertungspunkt entspricht einer Bearbeitungszeit von

ungefähr einer Minute. Sie müssen nicht immer ausformulierte Antworten geben. Sie können auch

Antworten in Stichworten geben (z.B. bei Pro und Contra). Bitte beachten Sie, dass zur besseren Lesbarkeit

der Aufgaben jeweils etwas leerer Platz zwischen Aufgaben steht, so dass normalerweise jede Aufgabe auf

einer neuen Seite beginnt. Die Klausur hat 10 Seiten.

Vorbereitung für Aufgabe 1

Die dargestellte vereinfachte Bilanz der VitaLife Lebensversicherung ist Grundlage für die Aufgabe 1.

Stellen Sie sich vor, Sie sind Risikomanager in der VitaLife Lebensversicherung. Die VitaLife ist ein Versicherungsverein auf Gegenseitigkeit (VVaG). Die VitaLife vertreibt klassische Kapitallebensversicherungen mit einer Rentenoption bei garantierten Rentenfaktoren. VitaLife hat die folgende Bilanz. Gehen Sie davon aus, dass bei den Zinstiteln das Nominal dem Buchwert entspricht.

Nutzen Sie für die Umbewertung von Buchwerten zu Marktwerten das vereinfachende Verfahren des Durationsansatzes, sofern keine anderen Angaben gemacht werden.

2

Darstellung der Aktivseite

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-

developed software valued

with 5. The software is also sold

to other companies. Solvency II

principles are applied.

Immobilien

(Grundstücke, Gebäude,

etc.)

Real Estate (land,

buildings, etc.) 100 ???

Hidden Reserves: 15% of book

value

Aktien (direkt & Fonds)

Equity (direct &

Funds) 60 ???Book Value = Fair Value

Hypothekenschuldforder

ungen Mortgage Loans 110 ???Hidden Reserves of 15

Namensschuldverschreib

ungen Registered Bonds 400 ???

Average coupon of 3,2%,

modified duration of 12,

corresponding market interest

rate of 1%. Assume Book Value

= Principal Value. Calculate MV

with the very simple Duration

Approach!

Schuldscheindarlehen Debentures / Bonds 200 ???

Average coupon of 3%,

modified duration of 5,

corresponding market interest

rate of 0%. Assume Book Value

= Principal Value.

Einlagen bei

Kreditinsituten

Deposits with Credit

Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 ???

Calculate the Deferred Tax

Asset with Tax Rate 30% applied

to the positive Valuation

Difference of the Liabilities

without Own Funds and

Deferred Tax Liability

Summe Sum 910 1.122

3

Darstellung der Passivseite

Passiva Liabilities Book Value Market Value Additional Information

Eigenmittel / Own Funds

Stockholders'

Capital &

Subordinated Loan/

Own Funds 40 ???

Calculate Market Value of Own

Funds!

davon

Nachrangige

Verbindlichkeit

thereof

Subordinated

Loan 20 ???

Coupon of 3%, modified

duration of 30, corresponding

market interest rate of 2%.

Assume Book Value = Principal

Value.

Passive latente Steuern

Deferred Tax

Liability 0 ???

Calculate the Deferred Tax

Liability with Tax Rate 30%

applied to the positive

Valuation Difference of the

Assets without Deferred Tax

Assets

nicht-festgelegte RfB

non-fixed provision

for premium

refunds 35 x

Not explicitly re-evaluated!

festgelegte RfB

fixed provision for

premium refunds 15 xNot explicitly re-evaluated!

Risikomarge Risk Margin x ???

Risk Margin: 3% of Best Estimate

Liabilities (PV of guarantees

plus O&G)

O&G O&G x ???

O&G Charge: 2% of Present

Value of Guaranteed Cashflow

Deckungsrückstellung /

Eigenwert der Garantie

Technical Provisions

/ Present Value of

guaranteed

Cashflow 760 ???

Average technical interest rate

of 2,8% currently used in the

discounting of TP/PV of

guaranteed Cashflow, modified

duration of 12, corresponding

market interest rate of 1%.

Calculate BEL with the very

simple Duration Approach!

Pensionsrückstellungen Pension Provisions 20 ???

Average technical interest rate

of 4% currently used in the

discounting pension provisions,

modified duration of 20,

corresponding market interest

rate of 1,5%. Calculate best

estimate with the very simple

Duration Approach!

Sonstige Passiva Other Liabilities 40 40

Summe Sum 910 1.122

4

Aufgabe 1. Case Study – Analyse der ökonomischen Bilanz von VitaLife (50 Bewertungspunkte) Runden Sie für die nachfolgenden Teilaufgaben a) bis c) die Einzelergebnisse jeweils ohne Nachkommastellen, bevor Sie weiterrechnen.

a) Berechnen Sie die fehlenden Positionen in der Marktwertbilanz und ersetzen Sie die Fragezeichen durch die berechneten Markwerte. (16 Punkte)

b) Szenario1 ausgehend von den Ergebnissen in Teilaufgabe a): Die Duration der Namensschuldverschreibungen wurde mit 12 auf die Duration der Deckungsrückstellung abgestimmt, so dass beide gleich sind. Berechnen Sie die Veränderung der Solvency II-Eigenmittel (Own Funds) bei einer Variation des 12-Jahreszinssatzes um plus 10 Basispunkte und um minus 10 Basispunkte. Alle anderen Zinssätze bleiben gleich. Analysieren und interpretieren Sie die Ergebnisse aus Sicht eines Risikomanagers. (10 Punkte)

c) Szenario 2 ausgehend von den Ergebnissen in Teilaufgabe a): Nehmen Sie nun an, dass die Duration der Namensschuldverschreibungen nur bei 10 liegt und die der Deckungsrückstellung bei 14. Berechnen Sie die Solvency II-Eigenmittel (Own Funds) neu. Nehmen Sie dabei an, dass der 14-jährige und der 10-jährige Zinssatz mit dem 12-jährigen aus Aufgabenteil a) identisch sind. Analysieren und interpretieren Sie die Ergebnisse aus Sicht eines Risikomanagers. (10 Punkte)

d) Nehmen Sie Szenario 2 als Ausgangspunkt. Stellen Sie das Risikoprofil von VitaLife auf und diskutieren Sie die Risikosituation der VitaLife per Expertenmeinung qualitativ. Überlegen Sie sich Maßnahmen zur Verbesserung der Risikosituation. Ziehen Sie mindestens eine Absicherungsstrategie in Betracht. (14 Punkte)

5

Aufgabe 2. Case Study – Wahl eines Bewertungsmodells für VitaLife (30 Bewertungspunkte)

VitaLife nutzt die Solvency II-Standardformel zur Berechnung der Risiken mit einem einfachen

Excelmodell. In diesem Excelmodell wird auch die Solvency II-Bilanz berechnet. Bei der Aufstellung der

Bilanz werden sowohl der Wert der Optionen und Garantien als auch die Risikomarge mit einem

pauschalen prozentualen Aufschlag auf die Berechnung des Eigenwerts der Garantie (Barwerts der

garantierten Cahsflows) berücksichtigt (siehe Aufgabe 1).

Der Vorstand der VitaLife möchte die Bewertung in der Solvency II-Bilanz verbessern und hat zwei

Modelle zur Verfügung, um die Bewertung der Optionen und Garantien zu verbessern:

A. Ein deterministisches Bewertungsmodell mit einer geschlossenen Formel zur Bewertung der

Optionen und Garantien. Nach Kalibrierung mit Kapitalmarktdaten und

unternehmensinternen Daten liefert das Modell innerhalb von 5 Minuten die Solvency II-

Bilanz. Zur Bedienung des Modells sind 30% der Arbeitszeit eines Mitarbeiters notwendig.

B. Ein stochastisches Bewertungsmodell mit einem Szenariogenerator zur Bewertung der

Optionen und Garantien. Die Kalibrierung des Szenariogenerators erfordert den Aufbau von

Fachwissen und bindet 30% der Arbeitszeit eines Mitarbeiters. Die Berechnung der Solvency

II-Bilanz mit dem stochastischen Modell dauert 12 Stunden. Zur Bedienung des Modells sind

weitere 40% der Arbeitszeit eines Mitarbeiters notwendig.

Beide Modelle stellen die Solvency II-Bilanz auf, enthalten jedoch keine Risikoberechnung. Eine

Umsetzung der Risikoberechnung im Sinne der Solvency II-Standardformel muss noch gemacht werden.

Bearbeiten Sie folgende Teilaufgaben.

a) Diskutieren Sie die Vor- und Nachteile dieser Bewertungsmodelle.

(10 Punkte)

b) Schlagen Sie zusätzliche Informationen vor, die das Unternehmen anfordern oder selbst

erzeugen, auswerten und beachten sollte, bevor es sich für ein Modell entscheidet.

(10 Punkte)

c) Entscheiden Sie sich für eine Modellvariante und machen Sie einen Vorschlag, wie die

Risikoberechnung mittels der Standardformel mit dem Bewertungsmodell verknüpft werden

kann.

Diskutieren Sie die Vor- und Nachtteile ihres Vorschlags.

(10 Punkte)

6

Aufgabe 3. Risikobewertung, Risikominderung und Wertveränderung (40 Bewertungspunkte)

a) Mehrjahressicht in der Risikobewertung

(20 Bewertungspunkte)

Runden Sie Wahrscheinlichkeiten auf 1% / 0,5%-Schritte.

Gegenwärtig hat die KULANZ-Versicherung Eigenmittel von 130 und eine Solvency-II

Solvenzanforderung von 100.

Sie möchten eine zweijährige Risikoperspektive einnehmen. Dabei nehmen Sie an, dass die

Eigenmittel nach jeweils einem Jahr normalverteilt und gemeinsam multivariat normalverteilt

sind mit Erwartung gleich den aktuellen Eigenmittel sowie gleichbleibender Volatilität.

Bearbeiten Sie folgende Fragen.

i) Angenommen, Sie behalten das Sicherheitsheitsniveau von 99,5% bei, wie sind die

Kapitalanforderung und die Solvenzbedeckung? (Hier dürfen Sie annehmen, dass die

jahresweisen Änderungen unabhängig sind.)

ii) Bei welchem Sicherheitsniveau für 2-jährigen-Horizont ergibt sich dieselbe

Kapitalanforderung wie für 1-Jahres-Horizont und 99,5% Sicherheitsniveau, wenn die

jahresweisen Änderungen unabhängig sind?

iii) Bei welcher Korrelationsannahme ist die Kapitalanforderung für 2-jährigen Horizont und

Sicherheitsniveau von 95% gleich der Kapitalanforderung für 1-Jahr und 99,5%?

iv) Wie vergleicht sich die zweijährige Kapitalanforderung im Fall von ii) mit der Forderung,

nach einem Jahr noch die Solvency II-Anforderung zu erfüllen? Berechnen Sie für

letzteres die Wahrscheinlichkeit.

v) Im Kontext von Solvency II wird das 99,5%-Perzentil oft als 1-in-200-Jahres-Ereignis

bezeichnet. Was bedeuten die obigen Varianten für diese Interpretation?

vi) Ein Kollege, der gehört hat, dass das 99,5%-Perzentil in der Solvency II-Kalibrierung sehr

schwer bestimmbar ist, schlägt daher vor, dieses über iii) und das leichter bestimmbare

2-Jahres-95%-Perzentil zu berechnen. Unterziehen sie den Vorschlag einer kritischen

Würdigung.

P 75% 76% 77% 78% 79% 80% 95,0% 95,5% 96,0% 96,5% 97,0% 99,5%

Φ-1(p) 0,67 0,71 0,74 0,77 0,81 0,84 1,64 1,70 1,75 1,81 1,88 2,85

Runden Sie Wahrscheinlichkeiten auf 1% / 0,5%-Schritte.

Hinweis: Unter den getroffenen Annahmen kann die Wurzelformel für die Zerlegung des Zeitraums

genutzt werden.

7

b) Ansatz von Risikominderung und Änderung des Kapitals

(20 Bewertungspunkte)

Sie sind Risikomanager der SecuraLife Lebensversicherung.

Zum vorangegangenen Stichtag 31.12.2015 betrugen die Own Funds, der Überschuss der

Aktiva über die Verbindlichkeiten 160.

Sie haben Sensitivitätsanalysen bezüglich Zins und Spread durchgeführt und festgestellt, dass

der jeweilige Quantil-Stress die Bilanz zum 31.12.2015 wie folgt ändert:

Im Zinsstress wachsen „Brutto“ der Wert der Kapitalanlagen um +10 und der Wert

der Verbindlichkeiten um +37.

Im Spreadstress wird der „Brutto“-Wert der Kapitalanlagen um 36 reduziert.

Im kombinierten Stress addieren sich diese „Brutto“-Wirkungen.

Die antizipierte Überschussbeteiligung dämpft den Eigenmittelverlust. Sie kann in jedem der

drei Stresse jeweils um 1/3 des Stresses, maximal jedoch 12, reduziert werden, um vom

„Brutto“- auf den „Netto“-Stress zu kommen.

Beantworten Sie die folgenden Fragen.

i) Das Basis-Risikokapital wird sowohl für „Brutto“ als auch für „Netto“ mit der

Wurzelformel mit Korrelation 0 aus den beiden Einzelstressen berechnet. Das „Netto“-

Risikokapital ergibt sich aus dem Maximum aus „Netto“-Basis-Risikokapital einerseits

und „Brutto“-Basis-Risikokapital abzüglich der Überschussbeteiligung von 12. D.h.

„Netto“-RK = max(„Netto“-Basis-RK, „Brutto“-Basis-RK – 12). Berechnen Sie das „Netto“-

Risikokapital. Wie beurteilen Sie die zugrundeliegenden Annahmen?

ii) Zum 31.12.2016 ist genau der kombinierte Stress eingetreten, andere Änderungen

ergaben sich nicht und die Entwicklung ist entsprechend der Stresse. Diskutieren Sie die

Gestaltungsmöglichkeiten für die Zuordnung der Gewinne und Verluste auf die

Risikotreiber mit mindestens Zahlenbeispielen zu zwei verschiedenen Zuordnungen.

(Vernachlässigen Sie andere Einflüsse wie Roll-Forward, Neugeschäft der Berichtsperiode

etc.)

iii) Die SecuraLife ist Teil der Garantia-Gruppe mit der zweiten Tochter RiskyLife. Die Holding

hat keine eigenen Bilanz- oder Risikokapital-Beiträge. Die Gruppe benutzt ebenfalls die

obige Berechnung für „Brutto“ und „Netto“-Risikokapital. Die Gruppenbilanz im Basisfall

wie in den Stressen durch Addition der Solobilanzen bestimmt, auf Gruppenebene wird

ebenfalls die Entlastung auf die zukünftige Überschussbeteiligung der Gruppe begrenzt.

(Dies ist analog zur Standardformel in Solvency II.)

Das Risikokapital beruht wieder nur auf Zins und Spread. Beide Töchter haben identische

„Brutto“- und „Netto“-Risikokapitalien für die einzelnen Module.

Ein Kollege aus dem Rechnungswesen wundert sich, warum die Gruppe dennoch ein

niedrigeres SCR hat als die Summe der Töchter.

Geben Sie eine unter den Voraussetzungen mögliche Erklärung und ein Zahlenbeispiel.

Beurteilen Sie, in wie fern der ausgewiesene Diversifikationseffekt ökonomisch

realistisch ist.

8

Wie könnte die Berechnung modifiziert werden, um unplausible Effekte zu vermeiden?

Hinweis: Für das Zahlenbeispiel dürfen Sie andere Own Funds, Überschussbeteiligungs-

und SCR-Werte unterstellen als in Fragen 3b) i)) und 3b) ii)).

9

Aufgabe 4 Mergers & Acquisitions (M&A) (60 Bewertungspunkte)

Sie sind CRO eines Unternehmens, das bislang in der Nichtlebenserstversicherung aktiv ist und die

Schwerpunkte in der Feuer- und Elementarschadenversicherung hat. In der Kfz-Versicherung haben Sie

ein kleines, volatiles Portfolio. Ihr Unternehmen unterhält ein zertifiziertes internes Modell.

Limit und Triggersystem: der NatCat-Trigger ist im mittleren gelben Bereich.

Dem Vorstand bietet sich die Gelegenheit, ein Versicherungsunternehmen kaufen zu können, das sich

auf Kfz-Versicherung spezialisiert hat und dort sehr erfolgreich ist.

Um die Kaufentscheidung zu unterstützen, sollen Sie für den Vorstand eine Stellungnahme bezüglich der

Transaktion vorbereiten. Dazu stehen Ihnen nur öffentliche Informationen zur Verfügung.

a) Um den quantitativen Einfluss der Akquise auf Ihr internes Modell abzuschätzen, führen Sie eine

Analyse auf Basis der öffentlich verfügbaren Informationen wie Geschäftsbericht oder

Analysteninformationen durch.

Welche Informationen verwenden Sie vor allem und welche Überlegungen bezüglich der

Integration in Ihr internes Modell stellen Sie an? Gehen Sie in Ihrer Beschreibung die wichtigsten

Risikokategorien durch!

(Punkte: 15)

b) Momentan ist in Ihrem Limit- und Triggersystem der Trigger für Naturkatastrophenschäden nahe

der roten Zone. Nach der Integration des zu akquirierenden Versicherungsunternehmens gehen

Sie davon aus, dass der Trigger in die rote Zone fallen würde. Diskutieren Sie Vor- und Nachteile

zweier Möglichkeiten, die Situation zu entschärfen.

(Punkte: 8)

c) Der Vorstand möchte außer dem Einfluss auf die Solvenz auch wissen, wie sich das S&P Rating

Ihres Unternehmens voraussichtlich entwickeln wird. Welche Faktoren spielen dabei eine Rolle?

Beschreiben Sie kurz die Funktionsweise des S&P Insurance Capital Models.

(Punkte: 6)

10

Im zweiten Schritt haben Sie die Möglichkeit, von dem Management des zu akquirierenden

Unternehmens Antworten auf einige Fragen und weitergehende Materialien zu erhalten. Dabei wollen

Sie ein besseres Verständnis für einzelne Risikoklassen gewinnen.

d) Welche Emerging Risks interessieren Sie in diesem Kontext und welche Punkte möchten Sie in

Erfahrung bringen? Erörtern Sie zwei Risiken.

(Punkte: 8)

e) Welche weiteren nichtmodellierbaren Risiken könnten sich durch den Kauf ergeben? Welche

Fragen stellen Sie und wie gehen Sie mit diesen Risiken um? Diskutieren Sie auch hier zwei

Risiken.

(Punkte: 8)

Die M&A Aktion war erfolgreich und das neue Unternehmen soll durch Aufnahme fusioniert werden. Sie

sollen nun die Gesellschaft in Ihr internes Modell integrieren.

f) Führen Sie die in Aufgabenteil (a) skizzierten Überlegungen weiter und machen Sie einen

Vorschlag, wie der Diversifikationseffekt durch das neue versicherungstechnische Portfolio in der

integrierten Steuerung der beiden Portfolios verwendet werden soll. Welchen Einfluss wird das

veränderte Risikomodell auf Ihre Steuerung der Portfolios haben? Diskutieren Sie ihn am Beispiel

der Steuerungsgröße RoRaC. Wie gehen Sie damit um?

(Punkte: 15)

11

Lösungsvorschlag zu Aufgabe 1:

Teil a)

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-developed software

valued with 5. The software is also sold to

other companies. Solvency II principles are

applied.

Immobilien (Grundstücke, Gebäude,

etc.) Real Estate (land, buildings, etc.) 100 115Hidden Reserves: 15% of book value

Aktien (direkt & Fonds) Equity (direct & Funds) 60 60 Book Value = Fair Value

Hypothekenschuldforderungen Mortgage Loans 110 125 Hidden Reserves of 15

Namensschuldverschreibungen Registered Bonds 400 506

Average coupon of 3,2%, modified duration

of 12, corresponding market interest rate

of 1%. Assume Book Value = Principal

Value. Calculate MV with the very simple

Duration Approach!

Schuldscheindarlehen Debentures / Bonds 200 230

Average coupon of 3%, modified duration

of 5, corresponding market interest rate of

0%. Assume Book Value = Principal Value.

Einlagen bei Kreditinsituten Deposits with Credit Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 51

Calculate the Deferred Tax Asset with Tax

Rate 30% applied to the positive Valuation

Difference of the Liabilities without Own

Funds and Deferred Tax Liability

Summe Sum 910 1.122

Passiva Liabilities Book Value Market Value Additional Information

Eigenmittel / Own Funds

Stockholders' Capital &

Subordinated Loan/ Own Funds 40 34Calculate Market Value of Own Funds!

davon

Nachrangige Verbindlichkeit

thereof

Subordinated Loan 20 26

Coupon of 3%, modified duration of 30,

corresponding market interest rate of 2%.

Assume Book Value = Principal Value.

Passive latente Steuern Deferred Tax Liability 0 48

Calculate the Deferred Tax Liability with

Tax Rate 30% applied to the positive

Valuation Difference of the Assets without

Deferred Tax Assets

nicht-festgelegte RfB

non-fixed provision for premium

refunds 35 xNot explicitly re-evaluated!

festgelegte RfB

fixed provision for premium

refunds 15 xNot explicitly re-evaluated!

Risikomarge Risk Margin x 28

Risk Margin: 3% of Best Estimate Liabilities

(PV of guarantees plus O&G)

O&G O&G x 18

O&G Charge: 2% of Present Value of

Guaranteed Cashflow

Deckungsrückstellung / Eigenwert

der Garantie

Technical Provisions / Present

Value of guaranteed Cashflow 760 924

Average technical interest rate of 2,8%

currently used in the discounting of TP/PV

of guaranteed Cashflow, modified duration

of 12, corresponding market interest rate

of 1%. Calculate BEL with the very simple

Duration Approach!

Pensionsrückstellungen Pension Provisions 20 30

Average technical interest rate of 4%

currently used in the discounting pension

provisions, modified duration of 20,

corresponding market interest rate of 1,5%.

Calculate best estimate with the very

simple Duration Approach!

Sonstige Passiva Other Liabilities 40 40

Summe Sum 910 1.122

12

Teil b)

Fall Zinsrückgang um 10 Basispunkte:

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-developed software

valued with 5. The software is also sold to

other companies. Solvency II principles are

applied.

Immobilien (Grundstücke, Gebäude,

etc.) Real Estate (land, buildings, etc.) 100 115Hidden Reserves: 15% of book value

Aktien (direkt & Fonds) Equity (direct & Funds) 60 60 Book Value = Fair Value

Hypothekenschuldforderungen Mortgage Loans 110 125 Hidden Reserves of 15

Namensschuldverschreibungen Registered Bonds 400 510

Average coupon of 3,2%, modified duration

of 12, corresponding market interest rate

of 0,9%. Assume Book Value = Principal

Value. Calculate MV with the very simple

Duration Approach!

Schuldscheindarlehen Debentures / Bonds 200 230

Average coupon of 3%, modified duration

of 5, corresponding market interest rate of

0%. Assume Book Value = Principal Value.

Einlagen bei Kreditinsituten Deposits with Credit Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 54

Calculate the Deferred Tax Asset with Tax

Rate 30% applied to the positive Valuation

Difference of the Liabilities without Own

Funds and Deferred Tax Liability

910 1.129

Passiva Liabilities Book Value Market Value

Eigenmittel / Own Funds

Stockholders' Capital &

Subordinated Loan/ Own Funds 40 28Calculate Market Value of Own Funds!

davon

Nachrangige Verbindlichkeit

thereof

Subordinated Loan 20 26

Coupon of 3%, modified duration of 30,

corresponding market interest rate of 2%.

Assume Book Value = Principal Value.

Passive latente Steuern Deferred Tax Liability 0 50

Calculate the Deferred Tax Liability with

Tax Rate 30% applied to the positive

Valuation Difference of the Assets without

Deferred Tax Assets

nicht-festgelegte RfB

non-fixed provision for premium

refunds 35 xNot explicitly re-evaluated!

festgelegte RfB

fixed provision for premium

refunds 15 xNot explicitly re-evaluated!

Risikomarge Risk Margin x 29

Risk Margin: 3% of Best Estimate Liabilities

(PV of guarantees plus O&G)

O&G O&G x 19

O&G Charge: 2% of Present Value of

Guaranteed Cashflow

Deckungsrückstellung / Eigenwert

der Garantie

Technical Provisions / Present

Value of guaranteed Cashflow 760 933

Average technical interest rate of 2,8%

currently used in the discounting of TP/PV

of guaranteed Cashflow, modified duration

of 12, corresponding market interest rate

of 0,9%. Calculate BEL with the very simple

Duration Approach!

Pensionsrückstellungen Pension Provisions 20 30

Average technical interest rate of 4%

currently used in the discounting pension

provisions, modified duration of 20,

corresponding market interest rate of 1,5%.

Calculate best estimate with the very

simple Duration Approach!

Sonstige Passiva Other Liabilities 40 40

910 1.129

13

Veränderte Positionen im Detail:

Der Zinsrückgang bewirkt einen Rückgang in den Own Funds. Latente Steuern zeigen saldiert einen

positiven Effekt, da die aktiven latenten Steuern stärker anwachsen. Der Rückgang resultiert aus dem

stärkeren Anwachsen des Barwerts des garantierten Cashflows. Der Barwert hat zwar dieselbe Duration

wie die Namensschuldverschreibungen, bringt jedoch das doppelte Gewicht in die Berechnung mit ein.

Dies liegt daran, dass das Gewicht auf der Passivseite (Garantierter Cashflow plus Inklusive O&G und

Risikomarge) bei Zinsänderung mit Marktwert 970 (=924+18+28) nahezu doppelt so hoch ist wie die

Aktivseite (Namensschuldverschreibungen) mit Marktwert 506.

Fall Zinsanstieg um 10 Basispunkte:

Basis Szenario Delta

Registered Bonds 506 510 4

Risk Margin 28 29 1

O&G 18 19 1

Technical Provisions / Present Value of

guaranteed Cashflow 924 933 9

Deferred Tax Asset 51 54 3

Deferred Tax Liability 48 50 2

Own Funds Basis 34 28 -6

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-developed software

valued with 5. The software is also sold to

other companies. Solvency II principles are

applied.

Immobilien (Grundstücke, Gebäude,

etc.) Real Estate (land, buildings, etc.) 100 115Hidden Reserves: 15% of book value

Aktien (direkt & Fonds) Equity (direct & Funds) 60 60 Book Value = Fair Value

Hypothekenschuldforderungen Mortgage Loans 110 125 Hidden Reserves of 15

Namensschuldverschreibungen Registered Bonds 400 501

Average coupon of 3,2%, modified duration

of 12, corresponding market interest rate

of 1,1%. Assume Book Value = Principal

Value. Calculate MV with the very simple

Duration Approach!

Schuldscheindarlehen Debentures / Bonds 200 230

Average coupon of 3%, modified duration

of 5, corresponding market interest rate of

0%. Assume Book Value = Principal Value.

Einlagen bei Kreditinsituten Deposits with Credit Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 48

Calculate the Deferred Tax Asset with Tax

Rate 30% applied to the positive Valuation

Difference of the Liabilities without Own

Funds and Deferred Tax Liability

910 1.114

14

Veränderte Positionen im Detail:

Die Own Funds steigen um 2 an. Durch die Asymmetrie bei den latenten Steuern, wird der Unterschied

zwischen Assets und Liabilities, welcher einen Anstieg von 4 ergeben würde, wieder verringert. Auch hier

gilt, dass der Barwert des garantierten Cashflows stärker reagiert, da er mehr Masse hat.

Auffällig ist, dass ein Zinsrückgang um 10bp einen Rückgang der Eigenmittel um 6 verursacht, während

der Zinsanstieg im 10bp nur einen Anstieg um 2 bewirkt. Offensichtlich ist die VitaLife asymmetrisch

gegenüber Zinsänderungen positioniert.

Passiva Liabilities Book Value Market Value

Eigenmittel / Own Funds

Stockholders' Capital &

Subordinated Loan/ Own Funds 40 36Calculate Market Value of Own Funds!

davon

Nachrangige Verbindlichkeit

thereof

Subordinated Loan 20 26

Coupon of 3%, modified duration of 30,

corresponding market interest rate of 2%.

Assume Book Value = Principal Value.

Passive latente Steuern Deferred Tax Liability 0 47

Calculate the Deferred Tax Liability with

Tax Rate 30% applied to the positive

Valuation Difference of the Assets without

Deferred Tax Assets

nicht-festgelegte RfB

non-fixed provision for premium

refunds 35 xNot explicitly revaluated!

festgelegte RfB

fixed provision for premium

refunds 15 xNot explicitly revaluated!

Risikomarge Risk Margin x 28

Risk Margin: 3% of Best Estimate Liabilities

(PV of guarantees plus O&G)

O&G O&G x 18

O&G Charge: 2% of Present Value of

Guaranteed Cashflow

Deckungsrückstellung / Eigenwert

der Garantie

Technical Provisions / Present

Value of guaranteed Cashflow 760 915

Average technical interest rate of 2,8%

currently used in the discounting of TP/PV

of guaranteed Cashflow, modified duration

of 12, corresponding market interest rate

of 1,1%. Calculate BEL with the very simple

Duration Approach!

Pensionsrückstellungen Pension Provisions 20 30

Average technical interest rate of 4%

currently used in the discounting pension

provisions, modified duration of 20,

corresponding market interest rate of 1,5%.

Calculate best estimate with the very

simple Duration Approach!

Sonstige Passiva Other Liabilities 40 40

910 1.114

Basis Szenario Delta

Registered Bonds 506 501 -5

Risk Margin 28 28 0

O&G 18 18 0

Technical Provisions / Present Value of

guaranteed Cashflow 924 915 -9

Deferred Tax Asset 51 48 -3

Deferred Tax Liability 48 47 -1

Own Funds Basis 34 36 2

15

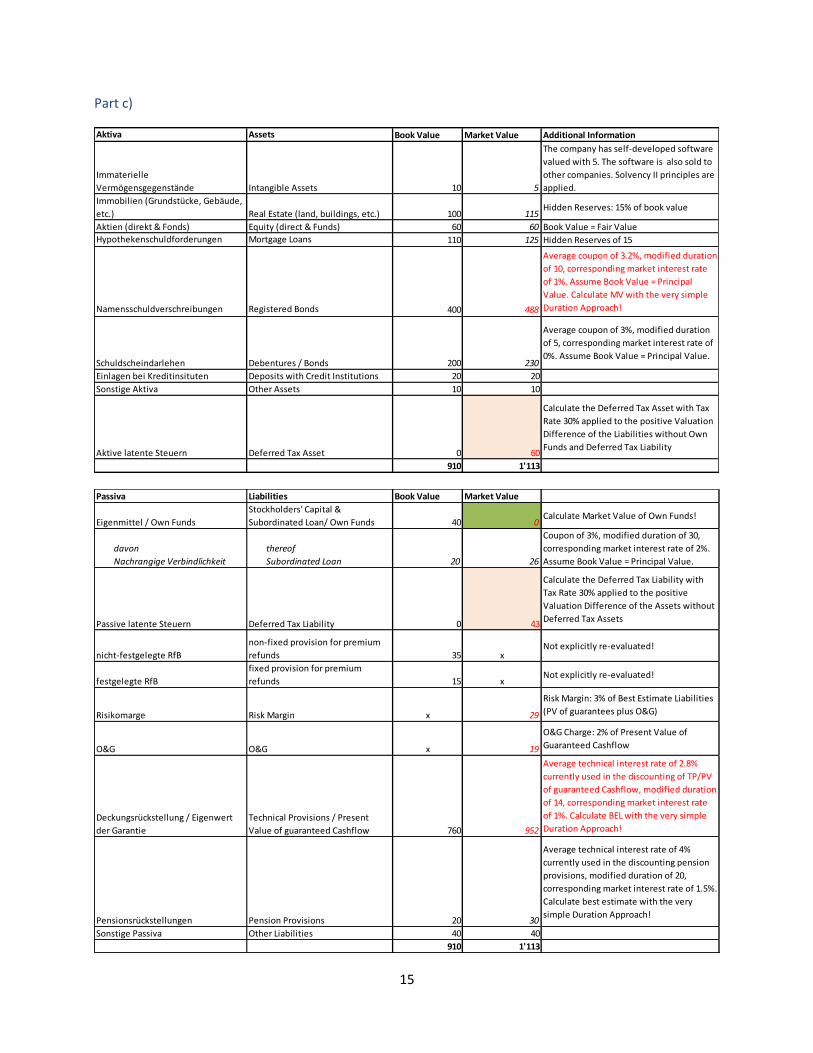

Teil c)

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-developed software

valued with 5. The software is also sold to

other companies. Solvency II principles are

applied.

Immobilien (Grundstücke, Gebäude,

etc.) Real Estate (land, buildings, etc.) 100 115Hidden Reserves: 15% of book value

Aktien (direkt & Fonds) Equity (direct & Funds) 60 60 Book Value = Fair Value

Hypothekenschuldforderungen Mortgage Loans 110 125 Hidden Reserves of 15

Namensschuldverschreibungen Registered Bonds 400 488

Average coupon of 3,2%, modified duration

of 10, corresponding market interest rate

of 1%. Assume Book Value = Principal

Value. Calculate MV with the very simple

Duration Approach!

Schuldscheindarlehen Debentures / Bonds 200 230

Average coupon of 3%, modified duration

of 5, corresponding market interest rate of

0%. Assume Book Value = Principal Value.

Einlagen bei Kreditinsituten Deposits with Credit Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 60

Calculate the Deferred Tax Asset with Tax

Rate 30% applied to the positive Valuation

Difference of the Liabilities without Own

Funds and Deferred Tax Liability

910 1.113

Passiva Liabilities Book Value Market Value

Eigenmittel / Own Funds

Stockholders' Capital &

Subordinated Loan/ Own Funds 40 0Calculate Market Value of Own Funds!

davon

Nachrangige Verbindlichkeit

thereof

Subordinated Loan 20 26

Coupon of 3%, modified duration of 30,

corresponding market interest rate of 2%.

Assume Book Value = Principal Value.

Passive latente Steuern Deferred Tax Liability 0 43

Calculate the Deferred Tax Liability with

Tax Rate 30% applied to the positive

Valuation Difference of the Assets without

Deferred Tax Assets

nicht-festgelegte RfB

non-fixed provision for premium

refunds 35 xNot explicitly re-evaluated!

festgelegte RfB

fixed provision for premium

refunds 15 xNot explicitly re-evaluated!

Risikomarge Risk Margin x 29

Risk Margin: 3% of Best Estimate Liabilities

(PV of guarantees plus O&G)

O&G O&G x 19

O&G Charge: 2% of Present Value of

Guaranteed Cashflow

Deckungsrückstellung / Eigenwert

der Garantie

Technical Provisions / Present

Value of guaranteed Cashflow 760 952

Average technical interest rate of 2,8%

currently used in the discounting of TP/PV

of guaranteed Cashflow, modified duration

of 14, corresponding market interest rate

of 1%. Calculate BEL with the very simple

Duration Approach!

Pensionsrückstellungen Pension Provisions 20 30

Average technical interest rate of 4%

currently used in the discounting pension

provisions, modified duration of 20,

corresponding market interest rate of 1,5%.

Calculate best estimate with the very

simple Duration Approach!

Sonstige Passiva Other Liabilities 40 40

910 1.113

16

Veränderte Positionen im Detail:

Die Durationslücke von 4 bewirkt in der Umbewertung von der lokalen Bilanz zur Solvency II-Bilanz, dass

die Aktiva deutlich weniger an Wert gewinnen, wie die Passiva. Neben dem Durationsunterschied trägt

das unterschiedliche Gewicht zur starken Änderung der Eigenmittel bei. Die Eigenmittel im Szenario sind

Null (!). Jede weitere negative Änderung (z.B. Zinsrückgang) bringt das Unternehmen in eine Situation

der Überschuldung nach Solvency II. Es würden negative Eigenmittel entstehen. Eigentlich kann und darf

das Unternehmen gar keine Risiken mehr eingehen.

Teil d)

VitaLife ist gegenüber folgenden Risiken exponiert

Zinsrisiko

o Garantiezinsrisiko

o Zinsänderungsrisiko

o ALM-Risiko

Spreadrisiko

o Spreadänderungsrisiko

o Bonitätsänderungsrisiko

o Ausfallrisiko

Speziell der Hypothekenbestand hat ein Ausfallrisiko, welches sehr stark von der allgemeinen

konjunkturellen Lage und der privaten Verschuldung der Hausbesitzer abhängt.

Aktienrisiko: Verlust durch Einbruch an den Aktienmärkten

Immobilienrisiko

Gegebenenfalls Fremdwährungsrisiko (nicht ersichtlich aus den Angaben)

Sterblichkeitsrisiko: vor allem in der Anwartschaftsphase der Versicherungen

Langlebigkeitsrisiko: getrieben durch die Rentenphase bei den Versicherungen

Stornorisiko: bei erhöhtem Storno verliert das Unternehmen die zukünftigen Gewinne. In der

aktuellen Situation, in der die Marktzinsen unter der Garantieverzinsung liegt, ist allerdings ein

niedrigeres Storno risikoreich, da durch das Storno das Wiederanlagerisiko im Moment

verringert wird.

Basis Szenario Delta

Registered Bonds 506 488 -18

Risk Margin 28 29 1

O&G 18 19 1

Technical Provisions / Present Value of

guaranteed Cashflow 924 952 28

Deferred Tax Asset 51 60 9

Deferred Tax Liability 48 43 -5

Own Funds Basis 34 0 -34

17

Operationelle Risiken

o Liquiditätsrisiko

o IT-Risiken

o Prozessrisiken

o Rechtsrisiken

Diese werden im Standardmodell und auch in eigenen Modellen oft nicht explizit, sondern nur

pauschal gemessen. Im Bereich der operationellen existieren Risiken, welche sehr selten sind,

jedoch eine große Schadenwirkung haben. Beispiele sind aus der IT bekannt. Z.B. Ausfall des

Bestandsführungssystems, Datenverlust von Kundendaten, und ähnliches. Auch der Bereich BCM

spielt bei den operationellen Risiken eine Rolle.

Im Szenario 2 hat die Gesellschaft keine Eigenmittel in der ökonomischen Bilanz. Daher kann VitaLife

seine Risiken nicht bedecken. Es bieten sich mehrere Strategien zur Verbesserung der Situation an:

Reduzierung der Risiken

o Abbau von Aktien, Immobilien, Spreadprodukten (Unternehmensanleihen etc.) oder

Hedging der Risiken, so dass im Risikomodell das Risiko verringert wird.

o Aufbau der Duration bei den Zinstiteln, um die Passivseite bezüglich Zinsänderungsrisiko

zu hedgen.

o Allerdings muss parallel darauf geachtet werden, dass der Kapitalanlageertrag ausreicht,

um die garantierte Verzinsung der Passivseite zu verdienen.

o Änderung des Überschussbeteiligungssystems, so dass die garantierten Rückstellungen

nicht anwachsen (z.B. mehr Schlussgewinne, laufende Gewinne nicht garantieren bzw.

mit Garantie von 0% Zins, etc.)

o Einkauf von Rückversicherung (z.B. Sterblichkeit oder Langlebigkeit)

o Entwicklung neuer Produkte, welche weniger Garantien erfordern.

o Anpassung der Modellierung von Immobilien als zinssensitiv, so dass diese im Sinne

eines ALM auch als Gegengewicht zum Cashflow der Passivseite im Zinsänderungsrisiko

dienen.

o Allgemeine Verbesserungen der Risiko-Modellierung, wo konservative Ansätze / Modelle

zum Einsatz kommen.

Aufbau von Eigenmittel durch

o Thesaurierung der Gewinne

o Nachschüsse der Mitglieder, falls dies die Satzung vorsieht

o Demutualisierung (Auflösung des Versicherungsvereins) und Verkauf der Gesellschaft an

einen Eigner, welcher Kapital einschießt

o Beantragung von Übergangsmaßnahmen bei der Aufsichtsbehörde

o Entwicklung neuer Produkte, welche weniger Garantien erfordern, so dass in der

Bewertung der Zeitwert der Optionen und Garantien kleiner wird.

o Allgemeine Verbesserungen der Bewertungs-Modellierung, wo konservative Ansätze /

Modelle zum Einsatz kommen.

18

Insgesamt ist die Situation der VitaLife äußerst kritisch, da ohne Maßnahmen die Gesellschaft keine

Risikotragfähigkeit ausweist. Größtes aus den bisherigen Daten zu erkennende Risiko ist das

Zinsänderungsrisiko.

Lösungsvorschlag zu Aufgabe 2:

Neben den hier genannten Lösungen sind auch andere Lösungen möglich.

Teil a)

Vor- und Nachteile Modell A

Pro: Wenig Aufwand. Schnelle Rechenzeit. Es sind viele Szenario-Rechnungen und Sensitivitätsanalysen

möglich. Anwendung kann unmittelbar erfolgen. Wenig Wissensaufbau notwendig. Einfache

Dokumentationsmöglichkeit.

Contra: Bewertung der O&G mit geschlossener Formel ist nur für wenige Optionen möglich. Ergebnisse

sind nicht genau genug. Nachweis der Marktkonsistenz der Bewertung ist schwierig. Abstimmung mit

den Wirtschaftsprüfer könnte schwierig werden.

Vor- und Nachteile Modell B

Pro: Exakte Bewertung der O&G möglich. Marktkonsistenz wird über die stochastischen Szenarien

sichergestellt. Es sind alle Optionen bewertbar. Abstimmung mit dem Wirtschaftsprüfer sollte einfacher

sein als bei Modell A.

Contra: Lange Rechenzeit. Höherer Aufwand als bei Modell A. Die lange Rechenzeit behindert das

Durchführen vieler Sensitivitätsanalysen. Wissensaufbau auch zu Szenariogenerator notwendig.

Teil b)

Zusätzliche Informationen können folgende sein:

Kosten der Software: Lizenzmodelle, Kauf, Pflege

Vertragsbedingungen: Rechtsstandort etc.

Kreditwürdigkeit des Anbieters

Testphase möglich

Möglichkeiten für Sensitivitätsanalysen

Einbindung in die unternehmensinterne Systemlandschaft

Programmiersprache der Software

Können unternehmensspezifische Anpassungen vorgenommen werden

Sind Anpassungen durch das Unternehmen möglich

Ist die Risikoberechnung umsetzbar

Software bereits im Einsatz: Referenzkunden

19

Einführungsprojekt: mögliche Struktur, Aufwand

Ist die Ausgabe bereits im meldefähigen Solvency II-Format

Bei Modell B: Möglichkeiten zur Beschleunigung der Rechenzeit

Auswertung der eigenen Bilanz und Überprüfung der Angemessenheit der Bewertung mit den

Modellen

Nutzung einer Testphase und Bewertung der Verpflichtungen in verschiedenen Sensitivitäten

und Analyse der Auswirkungen

Prüfung der Modellstabilität in Bezug auf die Parameter.

Teil c)

Risiko-Anbindung an Modell A mit Vor- und Nachteilen

Anbindung über Sensitivitätsanalysen: die Stressszenarien werden über die entsprechende Variation der

Eingabeparameter erzeugt. Programmierung über einen Prozess, welcher die Ergebnisse in das EIOPA-

Excel einspielt. Die die Berechnung der einzelnen Bilanz 5 Minuten dauert, ist bei 12 Stressen eine

Stunde Rechenzeit notwendig. Vorteile sind die schnelle Rechenzeit und die Einfachheit der Lösung.

Nachteil ist, dass die Genauigkeit der Risikoberechnung durch die Genauigkeit des Bewertungsmodells

beschränkt wird. Die Bewertung der O&G in den Stressfällen erfordert eine gesonderte Kalibrierung der

Inputparameter. Hier wird es in diesem einfachen Ansatz zu weiteren Näherungen kommen, welche die

Qualität der Ergebnisse negativ beeinflussen kann.

Risiko-Anbindung an Modell B mit Vor- und Nachteilen

Eine Anbindung über Sensitivitätsanalysen ist wegen der langen Rechenzeit schwierig. Mit diesem Ansatz

wäre eine parallelisierte Berechnung der Stressszenarien notwendig, da bei linearer Berechnung die

Rechenzeit jeweils um 12 Stunden ansteigt. Bei 12 Stressen wäre das Ergebnis erst nach 6 Tagen

verfügbar. Dies ist in den meisten Fällen inakzeptabel. Daher ist der Ansatz über ein mehrfaches

Berechnen mit Modell B unpraktisch. Es kann überlegt werden, die Stressberechnung direkt in Modell B

zu implementiert, so dass der Basisfall und die Stressszenarien parallel berechnet werden. Hierfür ist es

notwendig, dass die Software offen ist und selbst betreut werden kann. Ein anderer Ansatz wäre z.B. ein

replizierendes Portfolios, welches mittels des Bewertungsmodells kalibriert wird. Hierfür ist weiteres

Wissen aufzubauen.

Lösungsvorschlag zu Aufgabe 3:

Teil a)

i. Var(99,5, 2-Jahre, Korrel=0) = Var(99,5, 1-Jahr) * sqrt(2) = 100*sqrt(2) ≈ 141

ii. 2,85/sqrt(2) ≈ 1,82 bei ca. Φ(1,82) ≈ 96,5%

iii. Volatilität für ein Jahr: σ1 = 100/2,85

Volatilität für 2 Jahre bei Korrelation ρ: σ2= sqrt(2* σ1^2 + 2*ρ*σ1^2)

Var(2 Jahre 95, Korrel=ρ) = σ1* Φ-1(95%) *sqrt(2+2 ρ)

Gleichsetzen: σ1Φ-1(99,5%) = σ1* Φ-1(95%) *sqrt(2+2 ρ)

20

Korrelation ρ = ((Φ-1(99,5%) Φ-1(95%))2)/2-1 ≈ 22,6% mit obigen Rundungen ≈

23,7%

iv. Die Forderung, nach einem Jahr solvent zu sein, ist strenger, da die „Aufholung“ (Jahr 1 Quote

<100%, dann Besserung) nicht „zugelassen“ wird in dem Sinne, dass für sie die Anforderung

verletzt wird.

Die Wahrscheinlichkeit, dass die Solvenzanforderung von 100% nach einem Jahr erreicht

wird, Φ((130-100)/ σ1) ≈ Φ(0,77) ≈ 78%, σ1=100/Φ-1(99,5%)

v. Wenn man die Solvency II-Anforderung als Eigenmittel werden 0 für 1-in-200 Jahre interpretiert,

wäre die 2-Jahres-Anforderung „ungefähr“ 99,5% ein 400-Jahres-Ereignis (wenn man davon

absieht, dass entsprechend Frage iv es eine Erleichterung ist, nicht die „ungeraden“ Jahre zu

betrachten), es ist also naheliegend, das Sicherheitsniveau zu reduzieren.

Auf zwei Jahres-Sicht ist die Anforderung b) nur noch ein 2/(1-96,5%)-Jahres-Ereignis

also ca. 1-in-57 Jahre, bei c) wird die Frequenz 2/(1-95%) = 40 Jahre.

Die Festlegung des 1-Jahres-Horizonts beeinflusst also das Sicherheitsniveau in dieser

Anschauung erheblich. Die Festlegung beruht auf der Sicht, dass Geschäftsjahre eine

natürliche Einheit sind und die mutmaßliche Zeit für das wirksame Eingreifen der

Aufsicht ungefähr ein Jahr ist.

vi. Wie ii und iii zeigen, spielt die Korrelation eine erhebliche Rolle. Korrelationen sind notorisch

schwierig zu schätzen. Insofern ist der Vorteil der leichteren Schätzbarkeit fraglich.

Teil b)

Zins: „Brutto“-Änderung OF: 10-37 = -27, Überschussbeteiligung: 1/3*27=9 „Netto“-Änderung

OF: 10-37+9 = -18

Spread: „Brutto“-Änderung OF -36, Überschussbeteiligung: 1/3*36=12 „Netto“-Änderung OF:

-24

Kombiniert: „Brutto“-Änderung: OF 10-40-36 = -63, Überschussbeteiligung: min(1/3*63,12) = 12,

„Netto“-Änderung OF: -63+12= -51

Basis-Risikokapital „Brutto“: (27²+36²)^(1/2)=45, Basis-Risikokapital „Netto“ (also vor Kappung)

(18²+24²)^(1/2)=30 Risikominderung wird gekappt auf 12: „Netto“-Risikokapital: max(30; 45-12)

= 33.

Die Wurzelformel macht zwei entscheidende Annahmen: Die Risiken sind mit der angegebenen

Kovarianz z.B. normal- bzw. elliptisch verteilt. Diese Annahme ist eine gängige Vereinfachung,

auch wenn sie natürlich in der Realität im Allgemeinen nicht erwartet werden kann. Die zweite

wichtige Annahme ist, dass die Own-Funds-Änderung linear in den Risikofaktoren ist. Das ist

durch die beobachtete Nichtlinearität widerlegt.

21

i. Die Reihenfolge ist wichtig für die Größe der Einzeleffekte:

Mögliche Reihenfolgen sind

OF 2015: 160

Spread: -24

Zins: -27

OF 2016: 109

und

OF 2015: 160

Zins: -33

Spread: -18

OF 2016: 109

Durch anderes Aufteilen der Entlastung durch Reduktion der Überschussbeteiligung kann auch

jeder Zwischenwert erzeugt werden.

Die Reihenfolge der Schritte kann also die Gewichtung der Effekte massiv beeinflussen. Je nach

Interessenlage kann eine Darstellung attraktiver erscheinen als die andere (z.B. wenn Ereignisse

unterschiedlich als „hausgemacht“ angesehen werden).

ii. Beide Unternehmen haben Risikokapital 20 „Brutto“, 10 „Netto“ vor Kappung. SecuraLife hat 15

zukünftige Überschussbeteiligung, RiskyLife nur 5. Daher ergeben sich Risikokapitalien von 10 für

SecuraLife und 15 für RiskyLife.

Die Gruppe hat dann Risikokapital „Brutto“ 40, 20 „Netto“ vor Kappung, aber die

Gruppenentlastung wird gesamthaft auf 20 begrenzt, also nicht gekappt.

Die implizit unterstellte Fungibilität der risikomindernden Wirkung der Überschussbeteiligung ist

fraglich, solange keine Anhaltspunkte dafür bestehen, dass die Gesellschaften Verluste

gegenseitig ausgleichen.

Eine mögliche Lösung wäre, die gekappte Entlastung auf Unternehmensebene auf die

Einzelmodule zu allokieren und dann modulweise zur Gruppenentlastung zu aggregieren.

Lösungsvorschlag zu Aufgabe 4:

Teil a)

Skizze Musterlösung – abweichende Lösungen sind möglich:

Sie sollten sich zumindest die Kategorien Versicherungstechnische Risiken, Markt- und Kreditrisiken,

operationale Risiken betrachten. Pro Risikokategorie definieren Sie eine Segmentierung, die zu Ihrem

internen Modell kompatibel ist. Zu jedem Segment benutzen Sie beispielsweise ein Volumenmaß (VT z.B.

Prämien und Reserven, Markt- und Kredit z.B. Anlagevolumina, Forderungen an Rückversicherer und für

operationale Risiken z.B. Mitarbeiterzahl) und einen Faktor, den Sie aus Ihrem eigenen Modell oder der

Standardformel ableiten. Für Naturkatastrophenschäden können Sie auch historische Schäden aus dem

Geschäftsbericht verwenden. Für die Integration in das interne Modell werden Sie

Wahrscheinlichkeitsverteilungen pro Kategorie brauchen. Diese können Sie aus Ihrem internen Modell

22

übernehmen oder mit einfacheren Annahmen arbeiten. Bei der Integration sollten Sie sich außerdem

über Diversifikationseffekte bzw. Abhängigkeiten Gedanken machen. Dieser Punkt ist gerade bei Ihrem

Kfz-Portfolio relevant, wo Sie unter Umständen erwarten, dass der Ausgleich im Kollektiv die Risiken

kalkulierbarer macht. Bezüglich Marktrisiken- und Kreditrisiken ist außer der Anlagestruktur auch die

Frage relevant, wie mit eventuellen Rückversicherungsverträgen nach der Akquise verfahren werden soll.

Teil b)

Skizze Musterlösung – abweichende Lösungen sind möglich:

z.B. Rückversicherung. Pro – flexible Struktur, kurzfristig möglich und änderbar. Contra – eventuell

kostspielig.

z.B. Transfer auf den Kapitalmarkt, z.B. durch index-linked Produkte. Pro – wahrscheinlich günstig, Contra

– Basisrisiko verbleibt. Spezielles Knowhow zur Anpassung des Index an Portfolio notwendig)

Teil c)

cf Folien „Nebenbedingungen zur Ökonomischen Sicht: Restriktionen aufgrund von

Ratinganforderungen“

Teil d)

Skizze Musterlösung – abweichende Lösungen sind möglich:

z.B. Autonomes Fahren – wie sieht das Engagement des Unternehmens in diesem Segment aus? Welche

zukünftigen Entwicklungen werden erwartet? Welche Player sind momentan auf dem Markt aktiv?

z.B. Datendiebstahl – Sammelt das Unternehmen sensible Daten im Zusammenhang mit der Kfz-

Versicherung? Welche werden verwendet und welche Quellen werden dafür genutzt? Wie sieht das IT

System zur Verwaltung aus? Gab es Angriffe in der Vergangenheit?

Teil e)

Skizze Musterlösung – abweichende Lösungen sind möglich:

z.B. Reputationsrisiken – Im Zusammenhang mit der Datensammlung in der Kfz-Versicherung könnte das

Unternehmen in die Schlagzeilen geraten, wenn es sich unzulässiger Quellen bedient oder die Daten

unzulässig verwendet. Hier sollte Transparenz geschaffen werden über die verwendeten Daten und

Quellen, sowie rechtliche Fragestellungen geklärt werden.

z.B. Key person risk – Falls das zu akquirierende Unternehmen in sehr speziellen Geschäftssegmenten

aktiv ist, könnte es sein, dass der Erfolg an dem Knowhow einiger weniger Mitarbeiter liegt. Um diese zu

halten, können beispielsweise speziell für diese Mitarbeiter Entwicklungspläne für nach der Fusion

erstellt werden.

Teil f)

Skizze Musterlösung – abweichende Lösungen sind möglich:

Der Diversifikationseffekt aus der Versicherungstechnik soll dem neuen wie auch dem alten Portfolio zu

Gute kommen. Dies kann beispielsweise durch Verwendung des Kovarianzprinzips bei der

Kapitalallokation geschehen. Dies führt dazu, dass beispielsweise das dem Feuersegment zugeordnete

23

Risikokapital im Vergleich zu der Berechnung ohne das neue Portfolio sinkt. Der RoRaC für dieses

Segment erhöht sich dadurch. Dieser Effekt sollte transparent kommuniziert werden und auch

beispielsweise in der Zielerreichungsmessung und Zielsetzung berücksichtigt werden. Denkbar ist auch

ein langsameres Umsetzen in die Steuerung, um weniger abrupte Brüche zu erhalten und genauer die

Strategie ausrichten zu können. Die Kommunikation sollte frühzeitig erfolgen, damit die Strategie

vorausschauend angepasst werden kann.

1

Examination for CERA Module D 20.05.2017

The examination has a total of 180 marks. 90 marks are required to pass the examination.

For your guidance on how much time to spend on each question: for each mark you should spend

approximately one minute. You do not always need to formulate your answers in complete sentences. You

may write your answers in the form of keywords. Please note that, to make the questions easier to read,

some empty space has been left between questions. Each question begins on a new page. The examination

has 10 pages.

Preparation for Question 1

The simplified balance sheet of VitaLife life insurance company is to be used as the basis for Question 1.

Imagine that you are a risk manager at VitaLife life insurance company. VitaLife is a mutual insurance company. VitaLife sells classic endowment insurance policies with an annuity option with guaranteed annuity factors. VitaLife's balance sheet is below. Assume that, for the interest-bearing securities, the nominal is the same as the book value.

When revaluing book values to fair values use the duration approach for reasons of simplification unless other information is provided.

2

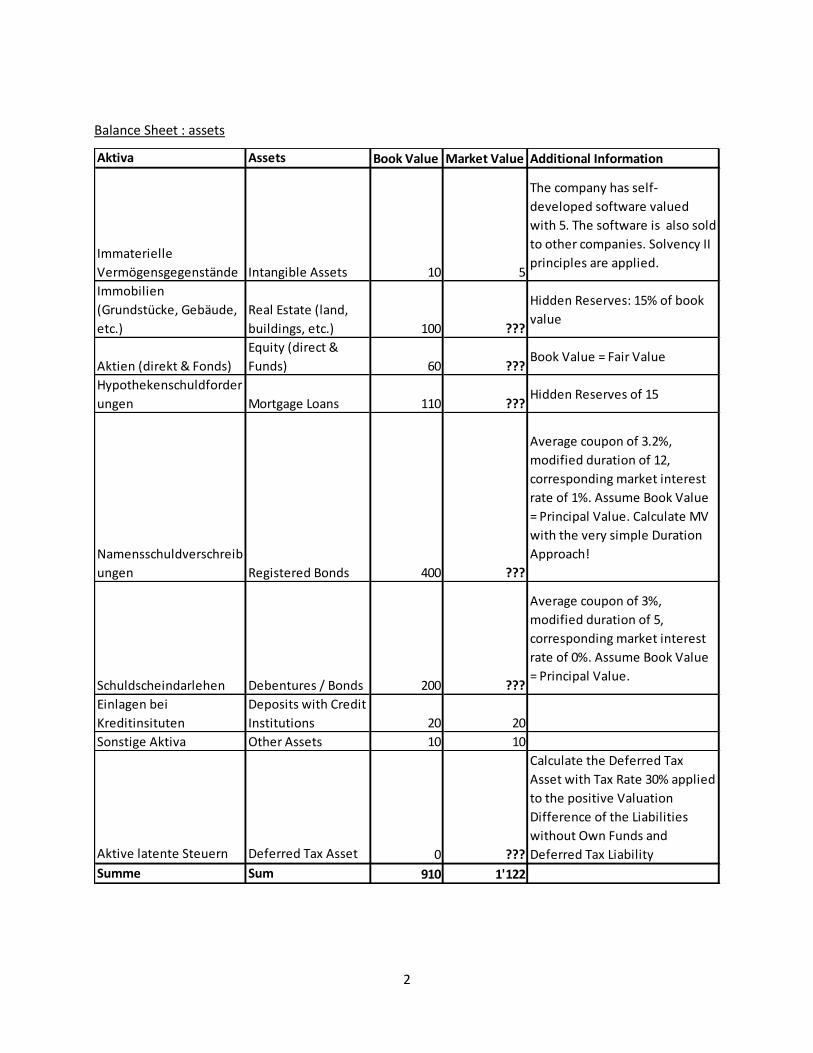

Balance Sheet : assets

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-

developed software valued

with 5. The software is also sold

to other companies. Solvency II

principles are applied.

Immobilien

(Grundstücke, Gebäude,

etc.)

Real Estate (land,

buildings, etc.) 100 ???

Hidden Reserves: 15% of book

value

Aktien (direkt & Fonds)

Equity (direct &

Funds) 60 ???Book Value = Fair Value

Hypothekenschuldforder

ungen Mortgage Loans 110 ???Hidden Reserves of 15

Namensschuldverschreib

ungen Registered Bonds 400 ???

Average coupon of 3.2%,

modified duration of 12,

corresponding market interest

rate of 1%. Assume Book Value

= Principal Value. Calculate MV

with the very simple Duration

Approach!

Schuldscheindarlehen Debentures / Bonds 200 ???

Average coupon of 3%,

modified duration of 5,

corresponding market interest

rate of 0%. Assume Book Value

= Principal Value.

Einlagen bei

Kreditinsituten

Deposits with Credit

Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 ???

Calculate the Deferred Tax

Asset with Tax Rate 30% applied

to the positive Valuation

Difference of the Liabilities

without Own Funds and

Deferred Tax Liability

Summe Sum 910 1'122

3

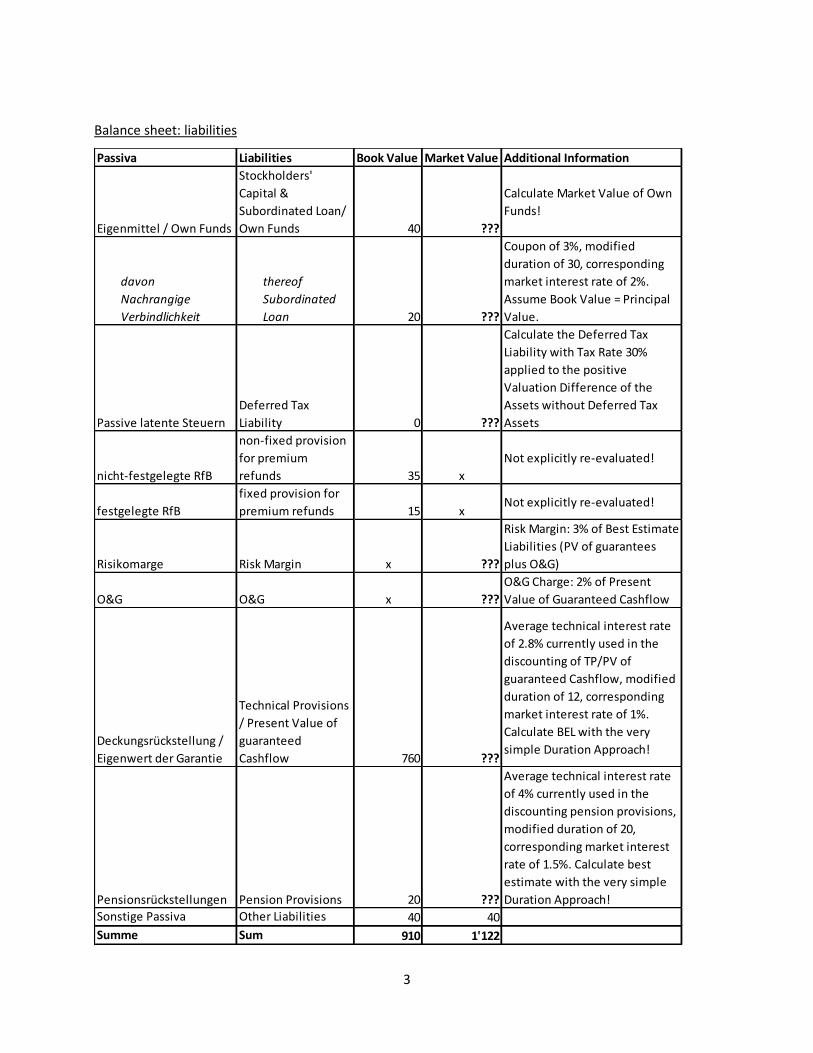

Balance sheet: liabilities

Passiva Liabilities Book Value Market Value Additional Information

Eigenmittel / Own Funds

Stockholders'

Capital &

Subordinated Loan/

Own Funds 40 ???

Calculate Market Value of Own

Funds!

davon

Nachrangige

Verbindlichkeit

thereof

Subordinated

Loan 20 ???

Coupon of 3%, modified

duration of 30, corresponding

market interest rate of 2%.

Assume Book Value = Principal

Value.

Passive latente Steuern

Deferred Tax

Liability 0 ???

Calculate the Deferred Tax

Liability with Tax Rate 30%

applied to the positive

Valuation Difference of the

Assets without Deferred Tax

Assets

nicht-festgelegte RfB

non-fixed provision

for premium

refunds 35 x

Not explicitly re-evaluated!

festgelegte RfB

fixed provision for

premium refunds 15 xNot explicitly re-evaluated!

Risikomarge Risk Margin x ???

Risk Margin: 3% of Best Estimate

Liabilities (PV of guarantees

plus O&G)

O&G O&G x ???

O&G Charge: 2% of Present

Value of Guaranteed Cashflow

Deckungsrückstellung /

Eigenwert der Garantie

Technical Provisions

/ Present Value of

guaranteed

Cashflow 760 ???

Average technical interest rate

of 2.8% currently used in the

discounting of TP/PV of

guaranteed Cashflow, modified

duration of 12, corresponding

market interest rate of 1%.

Calculate BEL with the very

simple Duration Approach!

Pensionsrückstellungen Pension Provisions 20 ???

Average technical interest rate

of 4% currently used in the

discounting pension provisions,

modified duration of 20,

corresponding market interest

rate of 1.5%. Calculate best

estimate with the very simple

Duration Approach!

Sonstige Passiva Other Liabilities 40 40

Summe Sum 910 1'122

4

Question 1. Case Study – Analysis of VitaLife's economic balance sheet (50 marks) For sections a) to c) below, please round up your individual results, with no decimal places, before you make further calculations.

a) Calculate the missing positions in the fair value balance sheet and replace the question marks (= ???) with the fair values you have calculated. (16 marks)

b) Scenario 1 based on the results from question 1 a) above: The duration of the registered bonds has been reconciled -- at 12 -- with the duration of the technical provision so that both are identical. Calculate the change in the Solvency II Own Funds if the 12-year annual interest rate varies by plus 10 basis points and by minus 10 basis. All other interest rates remain the same. Analyse and interpret the results from the perspective of a risk manager. (10 marks)

c) Scenario 2 based on the results from question 1 a) above: Assume that the duration of the registered bonds is only 10 and that the duration of the technical provision is 14. Recalculate the Solvency II Own Funds. Assume that the 14-year and the 10-year interest rate are identical to the 12-year rate from Question 1 a). Analyse and interpret the results from the perspective of a risk manager. (10 marks)

d) Take scenario 2 as a basis for your assumptions. Draw up VitaLife's risk profile and discuss VitaLife's risk situation in the form of a qualitative expert opinion. Propose measures to improve VitaLife's risk situation. Consider at least one hedging strategy. (14 marks)

5

Question 2. Case Study – Selection of a valuation model for VitaLife (30 marks)

VitaLife uses the Solvency II Standard Formula to calculate risks with a simple Excel model. The Solvency

II balance sheet is also calculated using this Excel model. When producing the economic balance sheet

both the value of the options and guarantees and of the risk margin are taken into account with a flat-

rate loading, expressed as a percentage, added to the calculation of the intrinsic value of the guarantee

(present value of guaranteed cash-flows) (See Question 1).

VitaLife's Management Board wishes to improve the valuation in the Solvency II balance sheet and has

two models available with which it could improve the valuation of the options and guarantees:

A. A deterministic valuation model with a closed formula for valuing the options and

guarantees. After calibration with capital market data and own company data the model

produces the Solvency II balance sheet within 5 minutes. Use of the model requires 30% of

the working time of one employee.

B. A stochastic valuation model with a scenario generator for valuing the options and

guarantees. Calibration of the scenario generator requires specialist know how and will tie

up 30% of the working time of one employee. Calculating the Solvency II balance sheet using

the stochastic model takes 12 hours. Use of the model requires an additional 40% of the

working time of one employee.

Both models can produce the Solvency II balance sheet but do not include a risk calculation. Performing

the risk calculation, in the sense of the Solvency II Standard Formula, must still be done.

Answer the following questions.

a) Discuss the advantages and disadvantages of these two valuation models.

(10 marks)

b) Suggest additional information that the company should obtain or produce itself, evaluate and

consider before deciding which model to select.

(10 marks)

c) Decide which model should be selected and make a proposal as to how the risk calculation by

means of the Standard Formula can be linked to the valuation model.

Discuss the advantages and disadvantages of your proposal.

(10 marks)

6

Question 3. Risk assessment, Risk mitigation and Changes in value (40 marks)

a) Multi-year view in risk assessment

(20 marks)

Round up probabilities to 1% / 0.5% percent points.

At present KULANZ Insurance has own funds of 130 and a solvency capital requirement under

Solvency II of 100.

You wish to adopt a two-year risk perspective. In so doing you assume that the own funds are

normally distributed and together multi-variate normally distributed after each year. The

Expectation remains the same as the present own funds with volatility also remaining the same.

Answer the following questions.

i) Assuming that you retain the security level of 99.5% how high would the solvency capital

requirement and solvency ratio be? (Assume that the yearly changes are independent.)

ii) At which safety level for a 2-year horizon does the same capital requirement arise as for

a 1-year horizon and a 99.5% safety level if the respective annual changes are

independent?

iii) At which correlation assumption is the capital requirement for a 2-year horizon and a

safety level of 95% the same capital requirement as for 1 year and 99.5%?

iv) How does the two-year capital requirement in the case of ii) above compare with the

requirement to still meet the Solvency II requirement after one year? Calculate the

probability for the latter, please.

v) In the context of Solvency II, the 99.5% percentile is often described as a 1 in 200 years

event. What do the above variants mean for this interpretation?

vi) A colleague has heard that the 99.5% percentile in Solvency II calibration is very hard to

determine. Therefore he proposes calculating this using iii) and the more easily

qunatifiable 2-year 95% percentile. Give a critical appraisal of the proposal.

p 75% 76% 77% 78% 79% 80% 95,0% 95,5% 96,0% 96,5% 97,0% 99,5%

Φ-1(p) 0,67 0,71 0,74 0,77 0,81 0,84 1,64 1,70 1,75 1,81 1,88 2,85

Round up probabilities to 1% / 0.5% percent point.

Note: Based on the assumptions made, the square root formula may be used for the decomposition the

period.

7

b) Risk mitigation and change in capital

(20 marks)

You are the Risk Manager at SecuraLife life insurance.

On the previous reporting date of 31.12.2015 own funds, the surplus of assets over liabilities

were 160.

You have performed sensitivity analyses concerning interest and spread and calculated that

the respective quantile stress changes the balance sheet as at 31.12.2015 as follows:

In the interest rate stress the value of assets increases "gross" by +10 and the value

of the liabilities by +37.

In the spread stress the value of the assets is reduced by 36 "gross".

In the combined stress these gross effects add up.

The anticipated with-profits surplus participation dampens the loss of own funds . In each of

the three stresses, this loss can be reduced by 1/3 of the stress, though only to a maximum

of 12, in order to get from the "gross" to the "net" stress.

Answer the following questions.

i. The “gross” as well as the “net” basic risk capital (BSCR) is calculated from the two

individual stresses with the square root formula with correlation 0. The “net” risk capital

is obtained as the maximum of the “net”-BSCR and the “gross”-BSCR minus the maximal

risk mitigation effect of with-profit surplus participation of 12, i.e. “net”-RK = max(“Net”-

BSCR, “gross”-BSCR – 12). Calculate the “net” risk capital. How do you assess the

underlying assumptions?

ii. On 31.12.2016, precisely that combined stress occurred, though there were no other

changes and the development is in line with the stresses. Argue scopes for design of

assigning the profits and losses to the risk drivers with at least figures for two different

assignments. (Ignore other influences such as roll-forward, new business during the

reporting period etc.)

iii. SecuraLife is part of the Garantia Group together with the second subsidiary, RiskyLife.

The holding company has no separate balance sheet or risk capital contributions. The

Group also uses the above calculation for "gross" and "net" risk capital. The Group

balance sheet, for the baseline case and for the stresses, is determined by adding the

individual (solo) balance sheets. At Group level any relief is limited to the Group's future

with-profits surplus participation. (This is analogous to the Standard Formula in Solvency

II.)

Once again the risk capital is only based on interest rate and spread. Both subsidiaries

have identical "gross" and "net" risk capitals for the individual modules.

A colleague from the Accounting Department wonders why the Group has a lower SCR

than the sum of the two subsidiaries.

Give a possible explanation and a numerical example, given the circumstances. Assess to

what extent the diversification effect stated is economically realistic.

8

How could the calculation be modified so as to avoid implausible effects?

Note: For the numerical example you may assume different values for own funds, with-

profits surplus participation and SCR than in Questions 3b) i) and 3b) ii).

9

Question 4. Mergers & Acquisitions (M&A) (60 marks)

You are the CRO of a company that has, until now, written primary non-life insurance and has focussed

on fire and natural disaster cover. You have a small, volatile motor insurance portfolio. Your company

uses a certified internal model.

As for limits and trigger systems the Nat Cat trigger is in the middle amber (yellow) category.

The Management Board has the opportunity to acquire an insurer that specialises in motor insurance

and is very successful in this line of business.

In order to back up its decision to acquire this insurer the Management Board asks you to prepare an

expert opinion on the transaction. You only have publicly available information at your disposal.

a) In order to assess the quantitative influence of the acquisition on your internal model you carry

out an analysis based on publicly available information such as the annual report or analysts'

research information.

Which information would you primarily use and what would you consider when it comes to

integration into your company's internal model ? In your description, please list the most

important risk categories!

(15 marks)

b) At present, in your limit and trigger system the trigger for natural catastrophes is almost at red.

Following the integration of the insurer that is to be acquired you assume that the trigger would

enter the red area. Discuss the pros and cons of two possible options to mitigate the situation.

(8 marks)

c) Apart from the impact on the company's solvency the Management Board also wishes to know

how the company's S&P rating is likely to develop. What factors are important here? Briefly

describe how the S&P Insurance Capital Model works.

(6 marks)

10

At the second stage you have the possibility to get answers to certain questions from the Management

of the insurer that is to be acquired as well as further, more detailed information. You want more

information about specific individual risk classes.

d) Which emerging risks interest you in this context and what would you like to find out? Explain

two risks.

(8 marks)

e) Which other non-modellable risk factors could arise as a result of the acquisition? What

questions would you ask and how would you deal with these risks? Discuss two risks.

(8 marks)

The M&A deal was a success and the new company is now to be merged. You have to integrate the

company into your internal model.

f) Expand on the deliberations you outlined in Question 4a) and make a proposal as to how the

diversification effect caused by the new underwriting should be used in the internal steering of

both portfolios. What impact will the changed risk model have on your steering and

management of the portfolios? Discuss this using the example of RoRaC. How would you deal

with this?

(15 marks)

11

Model Answer for Question 1:

Part a)

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-developed software

valued with 5. The software is also sold to

other companies. Solvency II principles are

applied.

Immobilien (Grundstücke, Gebäude,

etc.) Real Estate (land, buildings, etc.) 100 115Hidden Reserves: 15% of book value

Aktien (direkt & Fonds) Equity (direct & Funds) 60 60 Book Value = Fair Value

Hypothekenschuldforderungen Mortgage Loans 110 125 Hidden Reserves of 15

Namensschuldverschreibungen Registered Bonds 400 506

Average coupon of 3.2%, modified duration

of 12, corresponding market interest rate

of 1%. Assume Book Value = Principal

Value. Calculate MV with the very simple

Duration Approach!

Schuldscheindarlehen Debentures / Bonds 200 230

Average coupon of 3%, modified duration

of 5, corresponding market interest rate of

0%. Assume Book Value = Principal Value.

Einlagen bei Kreditinsituten Deposits with Credit Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 51

Calculate the Deferred Tax Asset with Tax

Rate 30% applied to the positive Valuation

Difference of the Liabilities without Own

Funds and Deferred Tax Liability

Summe Sum 910 1'122

Passiva Liabilities Book Value Market Value Additional Information

Eigenmittel / Own Funds

Stockholders' Capital &

Subordinated Loan/ Own Funds 40 34Calculate Market Value of Own Funds!

davon

Nachrangige Verbindlichkeit

thereof

Subordinated Loan 20 26

Coupon of 3%, modified duration of 30,

corresponding market interest rate of 2%.

Assume Book Value = Principal Value.

Passive latente Steuern Deferred Tax Liability 0 48

Calculate the Deferred Tax Liability with

Tax Rate 30% applied to the positive

Valuation Difference of the Assets without

Deferred Tax Assets

nicht-festgelegte RfB

non-fixed provision for premium

refunds 35 xNot explicitly re-evaluated!

festgelegte RfB

fixed provision for premium

refunds 15 xNot explicitly re-evaluated!

Risikomarge Risk Margin x 28

Risk Margin: 3% of Best Estimate Liabilities

(PV of guarantees plus O&G)

O&G O&G x 18

O&G Charge: 2% of Present Value of

Guaranteed Cashflow

Deckungsrückstellung / Eigenwert

der Garantie

Technical Provisions / Present

Value of guaranteed Cashflow 760 924

Average technical interest rate of 2.8%

currently used in the discounting of TP/PV

of guaranteed Cashflow, modified duration

of 12, corresponding market interest rate

of 1%. Calculate BEL with the very simple

Duration Approach!

Pensionsrückstellungen Pension Provisions 20 30

Average technical interest rate of 4%

currently used in the discounting pension

provisions, modified duration of 20,

corresponding market interest rate of 1.5%.

Calculate best estimate with the very

simple Duration Approach!

Sonstige Passiva Other Liabilities 40 40

Summe Sum 910 1'122

12

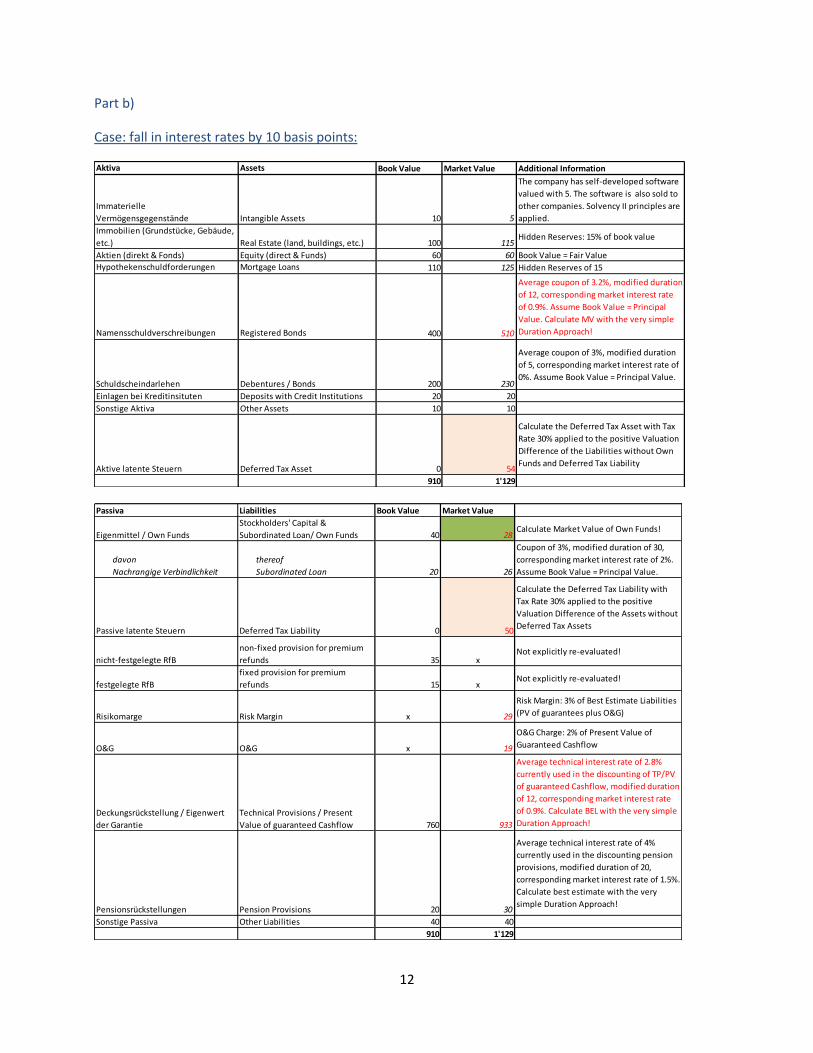

Part b)

Case: fall in interest rates by 10 basis points:

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-developed software

valued with 5. The software is also sold to

other companies. Solvency II principles are

applied.

Immobilien (Grundstücke, Gebäude,

etc.) Real Estate (land, buildings, etc.) 100 115Hidden Reserves: 15% of book value

Aktien (direkt & Fonds) Equity (direct & Funds) 60 60 Book Value = Fair Value

Hypothekenschuldforderungen Mortgage Loans 110 125 Hidden Reserves of 15

Namensschuldverschreibungen Registered Bonds 400 510

Average coupon of 3.2%, modified duration

of 12, corresponding market interest rate

of 0.9%. Assume Book Value = Principal

Value. Calculate MV with the very simple

Duration Approach!

Schuldscheindarlehen Debentures / Bonds 200 230

Average coupon of 3%, modified duration

of 5, corresponding market interest rate of

0%. Assume Book Value = Principal Value.

Einlagen bei Kreditinsituten Deposits with Credit Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 54

Calculate the Deferred Tax Asset with Tax

Rate 30% applied to the positive Valuation

Difference of the Liabilities without Own

Funds and Deferred Tax Liability

910 1'129

Passiva Liabilities Book Value Market Value

Eigenmittel / Own Funds

Stockholders' Capital &

Subordinated Loan/ Own Funds 40 28Calculate Market Value of Own Funds!

davon

Nachrangige Verbindlichkeit

thereof

Subordinated Loan 20 26

Coupon of 3%, modified duration of 30,

corresponding market interest rate of 2%.

Assume Book Value = Principal Value.

Passive latente Steuern Deferred Tax Liability 0 50

Calculate the Deferred Tax Liability with

Tax Rate 30% applied to the positive

Valuation Difference of the Assets without

Deferred Tax Assets

nicht-festgelegte RfB

non-fixed provision for premium

refunds 35 xNot explicitly re-evaluated!

festgelegte RfB

fixed provision for premium

refunds 15 xNot explicitly re-evaluated!

Risikomarge Risk Margin x 29

Risk Margin: 3% of Best Estimate Liabilities

(PV of guarantees plus O&G)

O&G O&G x 19

O&G Charge: 2% of Present Value of

Guaranteed Cashflow

Deckungsrückstellung / Eigenwert

der Garantie

Technical Provisions / Present

Value of guaranteed Cashflow 760 933

Average technical interest rate of 2.8%

currently used in the discounting of TP/PV

of guaranteed Cashflow, modified duration

of 12, corresponding market interest rate

of 0.9%. Calculate BEL with the very simple

Duration Approach!

Pensionsrückstellungen Pension Provisions 20 30

Average technical interest rate of 4%

currently used in the discounting pension

provisions, modified duration of 20,

corresponding market interest rate of 1.5%.

Calculate best estimate with the very

simple Duration Approach!

Sonstige Passiva Other Liabilities 40 40

910 1'129

13

Changed positions in detail:

The fall in interest rates causes a decrease in the Own Funds. Netted, the deferred tax liabilities show a

positive effect since the deferred tax assets increase more strongly. The decrease results from the

stronger increase in the present value of the guaranteed cash flow. The present value may have the

same duration as the registered bonds but brings twice the weighting into the calculation. This is

because the weighting in the liabilities (guaranteed cash flow plus inclusive O&G and risk margin) in the

event of a change in interest rates with a fair value of 970 (=924+18+28) is almost twice as high as the

assets (registered bonds) with a fair value of 506.

Case: increase in interest rates by 10 basis points:

Basis Szenario Delta

Registered Bonds 506 510 4

Risk Margin 28 29 1

O&G 18 19 1

Technical Provisions / Present Value of

guaranteed Cashflow 924 933 9

Deferred Tax Asset 51 54 3

Deferred Tax Liability 48 50 2

Own Funds Basis 34 28 -6

Aktiva Assets Book Value Market Value Additional Information

Immaterielle

Vermögensgegenstände Intangible Assets 10 5

The company has self-developed software

valued with 5. The software is also sold to

other companies. Solvency II principles are

applied.

Immobilien (Grundstücke, Gebäude,

etc.) Real Estate (land, buildings, etc.) 100 115Hidden Reserves: 15% of book value

Aktien (direkt & Fonds) Equity (direct & Funds) 60 60 Book Value = Fair Value

Hypothekenschuldforderungen Mortgage Loans 110 125 Hidden Reserves of 15

Namensschuldverschreibungen Registered Bonds 400 501

Average coupon of 3.2%, modified duration

of 12, corresponding market interest rate

of 1.1%. Assume Book Value = Principal

Value. Calculate MV with the very simple

Duration Approach!

Schuldscheindarlehen Debentures / Bonds 200 230

Average coupon of 3%, modified duration

of 5, corresponding market interest rate of

0%. Assume Book Value = Principal Value.

Einlagen bei Kreditinsituten Deposits with Credit Institutions 20 20

Sonstige Aktiva Other Assets 10 10

Aktive latente Steuern Deferred Tax Asset 0 48

Calculate the Deferred Tax Asset with Tax

Rate 30% applied to the positive Valuation

Difference of the Liabilities without Own

Funds and Deferred Tax Liability

910 1'114

14

Changed positions in detail:

The Own Funds increase by 2. The asymmetry in the deferred taxes reduces the difference between

assets and liabilities, which would result in an increase of 4, again. Here, too, the present value of the

guaranteed cash flow reacts more strongly because it has more mass.

It is striking that a fall in interest rates of 10bp causes Own Funds to decrease by 6, whilst the increase in

interest rates by 10bp only causes an increase of 2. Obviously, VitaLife has an asymmetrical exposure to

changes in interest rates.

Passiva Liabilities Book Value Market Value

Eigenmittel / Own Funds

Stockholders' Capital &

Subordinated Loan/ Own Funds 40 36Calculate Market Value of Own Funds!

davon

Nachrangige Verbindlichkeit

thereof

Subordinated Loan 20 26

Coupon of 3%, modified duration of 30,

corresponding market interest rate of 2%.

Assume Book Value = Principal Value.

Passive latente Steuern Deferred Tax Liability 0 47

Calculate the Deferred Tax Liability with

Tax Rate 30% applied to the positive

Valuation Difference of the Assets without

Deferred Tax Assets

nicht-festgelegte RfB

non-fixed provision for premium

refunds 35 xNot explicitly re-evaluated!

festgelegte RfB

fixed provision for premium

refunds 15 xNot explicitly re-evaluated!

Risikomarge Risk Margin x 28

Risk Margin: 3% of Best Estimate Liabilities

(PV of guarantees plus O&G)

O&G O&G x 18

O&G Charge: 2% of Present Value of

Guaranteed Cashflow

Deckungsrückstellung / Eigenwert

der Garantie

Technical Provisions / Present

Value of guaranteed Cashflow 760 915

Average technical interest rate of 2.8%

currently used in the discounting of TP/PV

of guaranteed Cashflow, modified duration

of 12, corresponding market interest rate

of 1.1%. Calculate BEL with the very simple

Duration Approach!