kirloskar oil engines | koel...

TRANSCRIPT

JM Financial Institutional Securities Limited

India’s home-grown engineering powerhouse

Kirloskar Oil Engines (KOEL) is one of India’s oldest engineering houses and

largest diesel genset suppliers in India (30%/23% volume/value mkt share).

Following a change in the top management team in FY13, including the MD,

CFO and SBU Heads, KOEL has led several initiatives such as swifter product

launches, stricter cost controls with higher R&D, geographical expansion

and numerous techno-commercial tie-ups. With forecasted net profit CAGR of

24% over FY16–19E, the company has a strong financial profile, including

FCF yield of 6–7%, RoICs of 25%+ and robust cash position (16% of market

cap.). We initiate with BUY, valuing the stock at `400, 20x Sep’18E EPS.

Management change driving new initiatives, product launches: Five out of

the top-13 members of the senior management have been part of KOEL for

less than five years, including MD, CFO and SBU Heads. The new team led

several developments such as: a) swifter product launches, b) improved NWC

days (negative in FY15), c) market share gains (+300bps since FY10), d)

higher R&D spends (2.7% of sales vs. 1.3%), f) cost controls (we expect

+300bps margin jump), and g) various techno-commercial partnerships.

Product launches to strengthen growth profile: KOEL launched a host of

products in the past three years, including high kVA gensets, power tillers,

portable gensets, fire-fighting pumps and compact gensets for defence, which

are expected to generate 15% additional sales by FY18. Furthermore, the

company has identified portfolio gaps in its existing portfolio and will be

launching products to fill the gaps with an addressable market size of `55–60bn.

Strong FCF generation and RoIC at 25%+: RoEs appear low at 11%, though

business returns are not low. RoIC stands high at 29% for KOEL (in FY17E),

similar to Cummins India, despite a much lower margin profile. Also, free

cash flow generation yield stands strong at 6–7% during FY17–19, while cash

balance will increase to `93/share by the end of FY19 (16% of mkt cap).

Initiate with BUY and TP of `400: We forecast the adjusted net profit to increase

at a CAGR of 24% during FY16–19E, led by a sales CAGR of 13% and improving

margins (+300bps by FY19E). Our TP of `400 implies 20x Sep’18E EPS, 20%

premium to its LT median multiple. Compared to its peer MNC company, our

target multiple is at 15% discount, while PEG ratio is much lower at 0.8x vs 2.2x.

Key risks are technology disruption, management attrition and prolonged

stagnation in the real estate industry. E 1.Vicky

Sandeep Tulsiyan

Tel: (+91 22) 66303085

Key data

Market cap (bn) ` 51.1 / US$ 0.8

Shares in issue (mn) 144.6

Diluted share (mn) 144.6

3-mon avg daily val (mn) ` 9.5/US$ 0.1

52-week range ` 361.9/199.2

Sensex/Nifty 28,221/8,744

`/US$ 66.5

Daily performance

-20%-10%0%10%20%30%40%50%60%70%80%

0

50

100

150

200

250

300

350

400

Sep-13 Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16

Kirloskar Oil Engines

Kirloskar Oil Engines Relative to Sensex (RHS)

% 1M 3M 12M

Absolute 23.8 31.3 27.6

Relative 24.9 27.4 22.3

* To the BSE Sensex

Shareholding pattern (%)

Mar-16 Mar-15

Promoters 59.3 72.7

FII 12.3 10.7

DII 8.8 6.2

Public / Others 19.6 10.4

Kirloskar Oil Engines | KOEL IN

6 October 2016

India | Industrials | Initiating Coverage

Price: `353

BUY

12M Target: `400

Exhibit 1. Financial summary (` mn)

Y/E March FY15A FY16A FY17E FY18E FY19E

Net sales 25,071 24,547 27,949 31,604 34,987

Sales growth (%) 8.1 -2.1 13.9 13.1 10.7

EBITDA 2,486 2,397 3,361 3,952 4,560

EBITDA (%) 9.9 9.8 12.0 12.5 13.0

Adjusted net profit 1,431 1,615 2,213 2,692 3,079

EPS (`) 9.9 11.2 15.3 18.6 21.3

EPS growth (%) -19.8 12.8 37.0 21.7 14.4

ROIC (%) 11.3 11.9 16.7 21.5 24.7

ROE (%) 11.0 11.6 14.8 16.8 17.7

PE (x) 35.7 31.7 23.1 19.0 16.6

Price/Book value (x) 3.8 3.6 3.3 3.1 2.8

EV/EBITDA (x) 16.9 17.9 12.0 9.9 8.2

Source: Company data, JM Financial. Note: Valuations as of 06/10/2016

JM Financial Research is also available

on: Bloomberg - JMFR <GO>,

Thomson Publisher & Reuters,

S&P Capital IQ and FactSet

Please see Appendix I at the end of this

report for Important Disclosures and

Disclaimers and Research Analyst

Certification.

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 2

Executive summary

KOEL, established in 1944, manufactures diesel engines, used in generator sets,

industrial machinery and agricultural pumps. It is one of the largest diesel

generator manufacturers in India with a 30%/23% market share in volume/value

terms. It offers diesel generators up to the 1,000kVA and is the leader in the

<250kVA category. The company has four manufacturing facilities located at

Pune, Kagal, Nashik and Rajkot.

Exhibit 2. Company snapshot

Kirloskar Oil Engines

Power Generation

(40%)

Gensets

Alternators, batteries and control panel

Agriculture (17%)

Crop irrigation

Farm mechanisation

Industrial (14%)

Off-highway engines

Tractor engines

Customer Support (14%)

Large Engines (5%)

Stationary power plants

Marine, defence and

railways

Exports (10%)

Source: Company, JM Financial

Exhibit 3. Revenue share and growth drivers

Revenue

Sales CAGR (%) Sales CAGR (%)

Segment Share (%) Constituents FY13-16 FY16-19E Growth drivers

Power Generation 40% Power gensets 4.4 12.5

Commercial and residential real estate

Alternators, batteries and control panel

Infra investments like airports, metros

Agriculture 17% Crop Irrigation -0.1 15.9 Farm income

Farm Mechanisation Agriculture subsidies

Industrial

14% Off-highway engines -1.8 14.5

Road construction

Tractor engines

Customer Support 14% Maintenance and repair -1.8 11.3 Segment 1 and 3

Spare Parts

Large Engines 5% Stationary power plants -12.6 8.3 Nuclear power and marine

Marine, defence and railways

Exports 10% 11.2 5.6 Investments in MENA region

Total

100%

1.4 12.5

Source: Company, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 3

Investment thesis

Management change to drive new initiatives, product

launches

While KOEL has a rich history of bringing in new products to the market,

developed largely using in-house technology, we have observed improved

execution following the assumption of office by the new management in FY13. We

saw several changes, including swifter product launches, improved financials,

geographical expansion and signing of several new technology tie-ups. We take a

look at various changes brought in by the new management in the past four

years:

Swifter product launches under new management: KOEL launched a host of

new products in the past three years, including low kVA portable gensets (in

petrol and diesel variants), petrol/kerosene pumpsets, high discharge pumps,

high kVA gensets, power tillers under farm mechanisation umbrella brand

called KMW, fire-fighting pumps, and traded products such as alternators,

batteries and control panel. The products have been able to make up for 30%

of lost sales in the past three years. We expect these products to generate

`3.5–4bn of additional sales over FY17–18, forming around 15% of FY16

sales. Furthermore, the company has entered 2–3 new countries every year

through various product streams such as power generation, industrial and

agriculture. This has led to consistent increase in exports at a CAGR of 10.3%

over FY11–16 and increased its share from 6% to 10% of net sales.

Exhibit 4. New product launches and geographies entered between FY13–16

Year Products launched/markets entered

FY13 5kVA Chhota Chilli gensets

New markets: Mozambique and Tanzania

FY14 Petrol kerosene pumpsets

High discharge pumps

New markets: Togo, Benin, Burkina Faso, Philippines and Algeria

FY15 CPCB-2 compliant gensets under KOEL Green brand

Alternators for gensets and pumpsets

<5kVA petrol and diesel Chhota Chilli gensets

15-hp power tiller launched under KMW brand

Engines for new applications in industrial segment

750kVA genset launched

New markets: Israel, Australia, France

FY16 3 new variants of tiller launched

Higher hp fire-fighting pumpset

New Markets: Nicargua, Peru, Russia, UK

Source: Company, JM Financial

Net working capital declined materially: KOEL operates with an efficient net

working capital cycle of 15–20 days (during FY07–13) compared to Cummins

India, which operates at an average working capital of 70–90 days. The

difference is due to higher exposure to agriculture (25% of sales), low/mid

kVA gensets (25% of sales) and lower contribution of high kVA gensets (5% of

sales), which are linked to long gestation projects. However, the efficiency

was further enhanced as net working capital cycle turned negative during

FY15, leading to a jump in cash flows. The improvement was a function of a

dip in debtor days, which declined from 45 days in FY13 to 8/15 days in

FY15/16. We also highlight that though NWC appears to have reverted back

to 19 days in FY16; the same is owing to non-provision of dividend in FY16

and should settle in 5–10 days range as dividend provisioning normalises in

FY18/19.

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 4

Exhibit 5. NWC came off sharply after the management change

1.7

5.3

6.3

9.9

4.0

5.4

2.3

-2.6

5.1

1.9 1.9 1.9

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Net Working Capital (`mn) NWC/Sales (%)

Source: Company, JM Financial

Cost controls in place to enable margin recovery: Operating margins

dipped during FY15–16 due to: a) adverse sales mix (dip on construction OEM

sales and increased traded goods), b) higher consultancy charges and R&D

expenses, and c) lower capacity utilisation. However, we expect margins to

revive by 200–300bps over FY17–19E on absence of consultancy charges,

lower R&D expense, operating leverage benefits on higher capacity utilisation

and continued tax subsidies at the Kagal plant. We note that margins have

substantially recovered from bottom levels (of 8.0–8.5%), as average

operating margins in the past two quarters stood at 12%, nearly 200bps

higher compared to FY15/16 levels.

Exhibit 6. Cost controls in place, margins on upward trajectory

24

,17

0

23

,26

0

23

,57

0

23

,20

0

25

,07

1

24

,54

7

27

,94

9

31

,60

4

34

,98

7

14.0%

13.1%

14.7%13.1%

9.9%

9.8%

12.0%

12.5%

13.0%

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Sales (`mn) EBITDA Margin (%)

Source: Company, JM Financial

R&D expenses increased at a CAGR of 23% during FY12–16: There was no

substantial capex involved towards the launch of new products as the average

capex ranged between `500mn and `1bn per annum, following the

completion of the Kagal factory in FY09. R&D expense increased from the

average of 1.3% of sales during FY12–14 to 2.7% in FY15–16. However, we

expect R&D expense to normalise, as new engines have been launched

commercially.

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 5

Exhibit 7. R&D expense increased at a CAGR of 23% during FY12–16

0.9%

2.0%

1.3%1.2%

1.3%

2.5%

2.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0

100

200

300

400

500

600

700

800

FY10 FY11 FY12 FY13 FY14 FY15 FY16

R&D expense (`mn) % of net sales

Source: Company, JM Financial

Product integration to avoid quality hiccups: Kirloskar started sales of

auxiliary genset products such as alternators, batteries and control panel

from 4QFY14 onwards. Integrating procurement of these products by KOEL

helped achieve various objectives such as: a) integration of product

manufacturing, b) reduction in product quality issues and c) creation of new

revenue stream. Sale of traded goods increase three-fold during FY11 to

FY16, and now constitute 17% of net sales, while average gross margins on

these products stand at 24% compared to 39% on manufactured products.

Exhibit 8. Products integrated to improve sales quality

Sales (`mn) FY11 FY12 FY13 FY14 FY15 FY16

Engines and Gensets 19 5 212 244 329 65

K-Oil 1,273 1,436 1,687 1,669 1,951 1,840

Alternators, Batteries, Panel and Switchgear 0 0 0 557 2,272 2,343

1,291 1,442 1,899 2,471 4,552 4,247

Gross Margin (%) FY11 FY12 FY13 FY14 FY15 FY16

Engines and Gensets 19% 10% 41% 25% 33% 17%

K-Oil 30% 27% 29% 31% 30% 38%

Alternators, Batteries, Panel and Switchgear 5% 10% 14%

Total 30% 27% 30% 25% 20% 24%

Source: Company, JM Financial

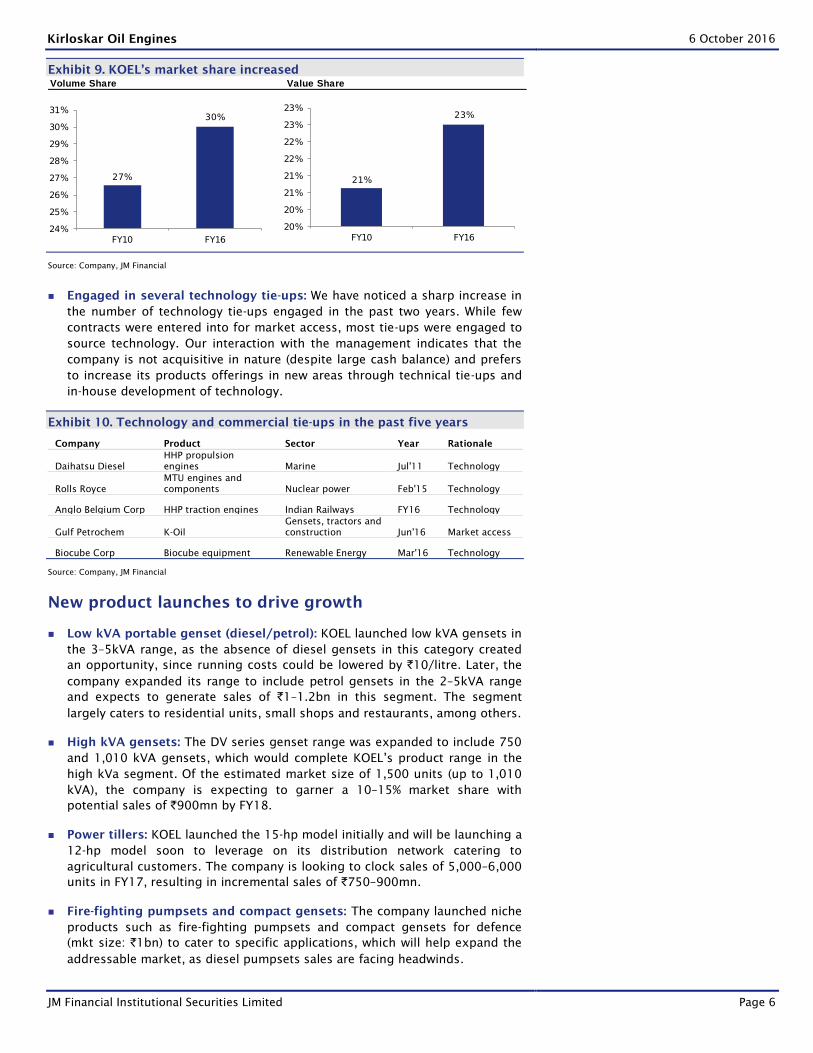

KOEL is among the few brands that increased market share: The diesel

power generator market contracted from `66bn in FY10 to `56bn in FY16,

due to a slump in the telecom tower market and decline in base load/prime

power market on improved power supply position. However, average

realisations increased during the period due to implementation of CPCB-2

norms in FY15, which bumped up realisations by 5–10%. Over the same

period, KOEL increased its value market share from 21% to 23%, and volume

share from 27% to 30%; this was achieved through extending its product

offerings and expanding its dealership network. We would like to highlight

that these gains are entirely organic in nature and there have been no

acquisitions in the past.

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 6

Exhibit 9. KOEL’s market share increased

Volume Share Value Share

27%

30%

24%

25%

26%

27%

28%

29%

30%

31%

FY10 FY16

21%

23%

20%

20%

21%

21%

22%

22%

23%

23%

FY10 FY16

Source: Company, JM Financial

Engaged in several technology tie-ups: We have noticed a sharp increase in

the number of technology tie-ups engaged in the past two years. While few

contracts were entered into for market access, most tie-ups were engaged to

source technology. Our interaction with the management indicates that the

company is not acquisitive in nature (despite large cash balance) and prefers

to increase its products offerings in new areas through technical tie-ups and

in-house development of technology.

Exhibit 10. Technology and commercial tie-ups in the past five years

Company Product Sector Year Rationale

Daihatsu Diesel

HHP propulsion

engines Marine Jul'11 Technology

Rolls Royce

MTU engines and

components Nuclear power Feb'15 Technology

Anglo Belgium Corp HHP traction engines Indian Railways FY16 Technology

Gulf Petrochem K-Oil

Gensets, tractors and

construction Jun'16 Market access

Biocube Corp Biocube equipment Renewable Energy Mar'16 Technology

Source: Company, JM Financial

New product launches to drive growth

Low kVA portable genset (diesel/petrol): KOEL launched low kVA gensets in

the 3–5kVA range, as the absence of diesel gensets in this category created

an opportunity, since running costs could be lowered by `10/litre. Later, the

company expanded its range to include petrol gensets in the 2–5kVA range

and expects to generate sales of `1–1.2bn in this segment. The segment

largely caters to residential units, small shops and restaurants, among others.

High kVA gensets: The DV series genset range was expanded to include 750

and 1,010 kVA gensets, which would complete KOEL’s product range in the

high kVa segment. Of the estimated market size of 1,500 units (up to 1,010

kVA), the company is expecting to garner a 10–15% market share with

potential sales of `900mn by FY18.

Power tillers: KOEL launched the 15-hp model initially and will be launching a

12-hp model soon to leverage on its distribution network catering to

agricultural customers. The company is looking to clock sales of 5,000–6,000

units in FY17, resulting in incremental sales of `750–900mn.

Fire-fighting pumpsets and compact gensets: The company launched niche

products such as fire-fighting pumpsets and compact gensets for defence

(mkt size: `1bn) to cater to specific applications, which will help expand the

addressable market, as diesel pumpsets sales are facing headwinds.

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 7

Exhibit 11. Revenue potential of new products

New products Incremental sales (`mn)

Portable gensets in 2–5kVA range 400-500

750/1,010 kVA gensets 800-1,000

Power tillers 1,000-1,500

Compact gensets and fire-fighting pumps 300-500

Exports 500-700

Total 3,000-4,200

Source: Company, JM Financial

Identified portfolio gaps, which will fuel future growth

Following successful launches of several new products across power generation,

agriculture and industrial segments, the management has identified its portfolio

gaps and probable launch pipeline over the next 3–4 years. To enable a launch

platform, it has developed several umbrella brands under each division such as

Kirloskar Mechanisation Works (KMW) for farm equipment, Kirloskar Shakti (for

alternators), Varsha (for agri. pumpsets), KOEL Green (for power generators), and

OEMCARE (for customer support). KOEL leverages its expansive dealer network

as it helps in: a) gauging customer feedback before launch, which helps in

introducing design/features accordingly (for e.g., power tillers), and b)

augmenting ROI of existing dealers and trade partners through expansion of

product range. New products identified in each sub segment are as follows:

Power generation: Genset nodes above 1,000 kVA range, namely 1,250 kVA,

1,500kVA and 2,000kVA.

Agriculture: Exploring trading opportunities in farm implements such as

rotavator, thresher and harvester.

Industrial: Engines for mining and railway applications.

Exhibit 12. Product portfolio gaps identified for future launches

Product Market size (`mn) Tentative launch period

Gensets above 1,010 kVA 3,500-4,000 2 to 2.5 years

Engines for mining applications 2,000-2,500 1 to 1.5 years

Engines for railways 7,500-8,000 1 to 1.5 years

Trading opportunities in farm mechanisation 40,000-45,000 4-5 years

Source: Company, JM Financial

12-17% of FY16 sales

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 8

Diversified customer base seeing cyclical recovery

New revenue streams made up for lost sales: Kirloskar Oil lost nearly 30%

of its sales in the past five years due to the hiving off bearings business,

slump in telecom tower market and loss of its largest construction OEM JCB

India. While the absence of NPCIL orders also caused a decline in sales in

FY16, the segment sales are not lost permanently; being lumpy in nature, it

may revert back in the future. However, it built portfolios in diversified

segments such as alternators (and auxiliaries), power tillers, high kVA

gensets and exports, thus resulting in flat sales from FY11to FY16. However,

since these businesses bear relatively lower margins, the EBITDA declined

30% during the same period.

Exhibit 13. What shut shop and what was introduced

Source: Company, JM Financial

Entry in new geographies led to ramp up in exports: KOEL’s exports have

grown at a healthy CAGR of 10.3% over FY11–16 (now 10% of sales vs. 6% in

FY11) vs. flat sales in the domestic segment during the same period, led by

penetration in new geographies in the Middle East and Africa for power

gensets and Europe & Russia in the industrial segment. The company entered

at least two new markets each year since FY13, thus expanding

geographically. Also, it recently incorporated a subsidiary in the US, the

largest DG set market in world and has commenced process to obtain EPA

approval for specific products.

Exhibit 14. Exports increasing consistently

Share of exports increased consistently New markets entered in past 4 years

94%93% 93%

91% 92%90%

6%7% 7%

9% 8%10%

84%

86%

88%

90%

92%

94%

96%

98%

100%

FY11 FY12 FY13 FY14 FY15 FY16

Domestic Exports

Year Markets entered

FY13 Mozambique

Tanzania

FY14 Togo

Benin

Burkina Faso

Philippines

Algeria

FY15 Israel

Australia

France

FY16 Nicargua

Russia

UK

Source: Company, JM Financial

Division Year Contribution

Bearings From 2QFY12 6% of sales in

FY11

Telecom

towers

From FY14 10% of sales in

FY10

JCB India From 2HFY11 6-7% of sales

in FY12

NPCIL From FY16 10% of sales in

FY14

Division Year Contribution

Alternators FY14 10% of sales

in FY16

Power tillers FY15 4% of sales in

1QFY17

Portable

gensets

FY13/15 3% of sales in

FY16

High kVA

gensets

625kVA:FY11

750/1000:FY16

5% of sales in

FY16

Exports 10% of sales

in FY16

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 9

Strong RoIC and free cash flow generation profile

Strong balance sheet: Despite stagnant sales and 30% lower EBITDA in the

past five years, Kirloskar Oil’s strong balance sheet stands strong, led by

minimal capex (`50–100mn per annum), improved working capital efficiency

and repayment of loans. With an estimated profit CAGR of 24% during FY16–

19E and a conservative approach towards acquisitions by the management,

we expect the company’s balance sheet strength to improve further.

Robust cash flow generation, leading to improved cash balance: KOEL

generates operating cash flows amounting to `3.8–4.2bn per annum, while

capex requirement are minimal given the current capacity utilisation rates are

hovering between 50% and 60%. This has led to a burgeoning cash balance,

which stands at `8.3bn or `57/share at the end of FY16 and is expected to

increase to `13.5bn by the end of FY19 or `93/share (including liquid

investments).

Exhibit 15. FCF generation profile aiding cash per share to increase consistently

42

3

3,6

27

1,3

38

2,8

32

3,1

04

-33

1

3,5

98

2,7

71

3,2

12

39.035.3

42.5

47.4

60.8 61.9 54.2 54.2 54.2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Free Cash Flow (`mn) Dividend payout (%)

327 327 327 327 327 327 327 327 327 327

18.1 22.0 38.1 30.6 45.6 62.3 57.1 73.7 82.8 93.5

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

CMP (`/share) Cash on books (`/share)

Source: Company, JM Financial

Strong RoIC profile, comparable to market leader: RoEs appear low at 11%,

though business returns are very healthy. RoIC is expected to increase to 29%

in FY17, which is similar to Cummins India, despite a much lower margin

profile of 12–13% vs. 16-17% for Cummins India. However, we note that core

RoICs may exceed Cummins India by a huge margin as margins expand on

operating leverage benefits due to higher capacity utilisation.

Exhibit 16. RoIC profile similar to Cummins

10%

20%

30%

40%

50%

60%

70%

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

KOEL Cummins India

Source: Company, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 10

Company Overview

KOEL, established in 1944, manufactures diesel engines, used in generator sets,

industrial machinery and agricultural pumps. It is one of the largest diesel

generator manufacturers in India with a 30%/23% market share in volume/value

terms. It offers diesel generators up to the 1,000kVA and is the leader in the

<250kVA category. The company has four manufacturing facilities located at

Pune, Kagal, Nashik and Rajkot.

Exhibit 17. Company snapshot

Kirloskar Oil Engines

Power Generation

(40%)

Gensets

Alternators, batteries and control panel

Agriculture (17%)

Crop irrigation

Farm mechanisation

Industrial (14%)

Off-highway engines

Tractor engines

Customer Support (14%)

Large Engines (5%)

Stationary power plants

Marine, defence and

railways

Exports (10%)

Source: Company, JM Financial

Exhibit 18. Manufacturing locations

Location Unit Products manufactured

Pune I Engines

Kagal I Engines, gensets and pumpsets

II Engines

III Power Tillers

Spare Parts Spares, packing and distributing

Nashik I Engines

Rajkot I Engines, gensets and pumpsets

Spare Parts

Bhare I Gensets and Pumpsets

Source: Company

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 11

Power generation (40% of sales)

Exhibit 19. Power generation: Segment overview

Power Generation (40% of sales)

DV Series

From 325-750kVA

Alternators, batteries, panel, switchgear

Low/mid kVA gensets

Source: Company

Genset industry contracted from its peak in FY10…: The Indian power

genset industry has been on a steady downward trend contracting from

`65.5bn in FY10 to just over `5.5bn in FY16. This can be attributed to two

major factors: a) the overall pick up in power generation, which has resulted

in peak/base deficit slumping from 16.6/9.8% in FY08 to a mere 2.0/0.7% in

YTDFY17, and b) muted demand from the telecom tower market, which

witnessed a drastic slowdown in the annual tower addition from 60,000

during FY08–12 to just 6,000 in FY16. Moreover, forecasts indicate that India

might have a base power surplus of 1.1% in FY17, which would pose more

challenges to the growth of the genset industry.

Exhibit 20. Anathema of diesel genset market

Power deficit nearly eliminated Telecom tower additions fell

9.9 9.8

11.010.1

8.5 8.5 8.7

4.2

3.62.1

0.7

13.5

16.6

12.0

13.3

10.311.1

9.0

4.5 4.7

0.42.0

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 YTDFY17

Base Deficit (%) Peak Deficit (%)

14

,28

3

27

,41

8

46

,00

0

61

,31

7

64

,90

0

76

,80

8

52

,97

5

15

,00

0

4,0

00

1,0

00

6,0

00

7,0

00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Telecom Tower additions (units)

Source: JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 12

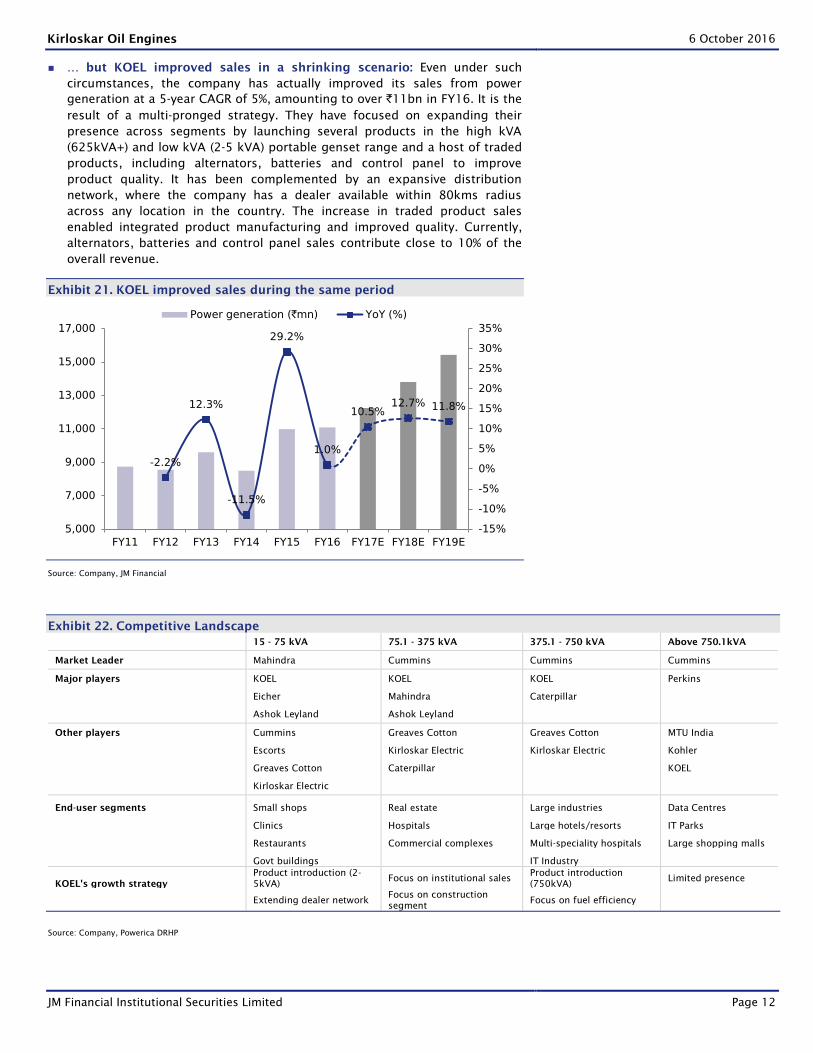

… but KOEL improved sales in a shrinking scenario: Even under such

circumstances, the company has actually improved its sales from power

generation at a 5-year CAGR of 5%, amounting to over `11bn in FY16. It is the

result of a multi-pronged strategy. They have focused on expanding their

presence across segments by launching several products in the high kVA

(625kVA+) and low kVA (2-5 kVA) portable genset range and a host of traded

products, including alternators, batteries and control panel to improve

product quality. It has been complemented by an expansive distribution

network, where the company has a dealer available within 80kms radius

across any location in the country. The increase in traded product sales

enabled integrated product manufacturing and improved quality. Currently,

alternators, batteries and control panel sales contribute close to 10% of the

overall revenue.

Exhibit 21. KOEL improved sales during the same period

-2.2%

12.3%

-11.5%

29.2%

1.0%

10.5%12.7% 11.8%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

5,000

7,000

9,000

11,000

13,000

15,000

17,000

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Power generation (`mn) YoY (%)

Source: Company, JM Financial

Exhibit 22. Competitive Landscape

15 - 75 kVA 75.1 - 375 kVA 375.1 - 750 kVA Above 750.1kVA

Market Leader Mahindra Cummins Cummins Cummins

Major players KOEL KOEL KOEL Perkins

Eicher Mahindra Caterpillar

Ashok Leyland Ashok Leyland

Other players Cummins Greaves Cotton Greaves Cotton MTU India

Escorts Kirloskar Electric Kirloskar Electric Kohler

Greaves Cotton Caterpillar KOEL

Kirloskar Electric

End-user segments Small shops Real estate Large industries Data Centres

Clinics Hospitals Large hotels/resorts IT Parks

Restaurants Commercial complexes Multi-speciality hospitals Large shopping malls

Govt buildings IT Industry

KOEL's growth strategy

Product introduction (2-

5kVA) Focus on institutional sales

Product introduction

(750kVA) Limited presence

Extending dealer network Focus on construction

segment Focus on fuel efficiency

Source: Company, Powerica DRHP

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 13

A compelling value proposition: A comparison of the 750kVA genset from

the major players in this category provides several insights. KOEL offers

better fuel efficiency overall than Cummins and Perkins, at higher load. Due

to higher indigenisation, pricing is at par with Cummins, but cheaper than

Perkins and MTU. It is also the most compact genset in this category, which

appeals to real estate developers facing space constraints. Overall, the

company has managed to build a compelling value proposition to compete

with more established players in this segment.

Exhibit 23. 750kVA genset comparison

KOEL Cummins Perkins MTU

Displacement 24-litre 38-litre 23-litre 27-litre

No of cylinders 12, Vee 12, Vee 6, in-line 12, Vee

Compression ratio 15.5 16.7 13.6 17.5

Fuel consumption at 75% load (LPH) 126.4 130.4 119.7 116.6

Fuel consumption at 100% load (LPH) 154 165.0 164.4 152.2

Dimensions in mm (LxWxH) 6,800x2,300x2,713 8,000x2,600x3,000 7,200x2,300x3,560 4,440x1,910x2,190*

Weight (kg) 8,300 11,900 9,397 6,260*

Fuel tank (litres) 990 990 990 990

Source: Company, JM Financial, *MTU dimensions and weight are not comparable as it excludes enclosure

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 14

Agriculture (17% of sales)

Exhibit 24. Agriculture: Segment Overview

Agriculture (17% of sales)

Crop Irrigation

Pumpsets

Farm mechanisation

Power tillers

Tractor spares

Source: Company

KOEL has product offerings that cater to the crop irrigation and farm

mechanisation segments.

Weak monsoons played havoc for crop irrigation sales: Portfolio includes a

range of products such as engines in the 3–130hp range, largely catering to

diesel, petrol and kerosene pumpsets in the agriculture segment. In addition,

it sells small quantities of engines to concrete mixers, hoists, harvesters,

threshers, in/out-board motors. India has had to endure below normal

monsoons for the past two years, resulting in low farm incomes. Also,

improved rural electrification and energisation of pumpsets has led to

migration of diesel pumps customers to electric/solar power-based pumpsets

in smaller ranges (3–5hp). Consequently, the crop irrigation segment has

expanded at a 5-year CAGR of just 1.4%.

Exhibit 25. Monsoons trend over the past decade

-0.5 -0.6

5.3

-1.9

-22.5

2.61.0

-7.9

5.2

-12.6

-14.5

-3.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Monsoon surplus/(deficit) ((%)

Source: IMD. +/-6% is considered normal

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 15

KOEL sailed through by introducing new products and market share

gains: However, KOEL was able to outperform weak industry sales through: a)

launch of traded products (alternators and oil), b) expansion of dealer

network and service outlets, c) extension of product offerings

(petrol/kerosene pumpsets), and d) increase in market share from 15% to

20%. It has also consolidated all engines under the Varsha brand to improve

brand recall/recognition. With better monsoons in 2016, pumpset sales are

expected to improve. In 1QFY17, the company had added 900 retailers

enabling network strength of 18,000+ in this segment.

Exhibit 26. Crop irrigation sales trend

-3%

24%

-12% -18%

11%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY11 FY12 FY13 FY14 FY15 FY16

Crop irrigation sales (`mn) YoY (%)

Source: Company, JM Financial

Farm mechanisation levels set to rise: This sub-segment has emerged as a

real growth driver in recent years aided by a number of structural factors.

Current farm mechanisation levels in India stand at a lowly 40%. Agriculture

studies indicate using a tractor in paddy fields is difficult due to swamp soil

conditions, while paddy constitutes 16% of arable land in India and 15% of

total agricultural output. With MSP for paddy increasing at 4-5% per annum in

the past 4 years, thereby improving yields, paddy cultivation is expected to

substantially go up. KOEL has a major presence in all the top 7 states, which

constitute nearly 65% of total paddy output. Low farm income makes

investment in farm mechanisation equipment unviable. Thus, the government

provides subsidy of 30–50% for different equipment. Current subsidy rates for

power tillers vary between 40% and 50%, thus bringing down the initial

investment to `30,000-40,000 (assuming LTV of 70%).

Exhibit 27. Paddy share highest among food grains

State Paddy share (%)

West Bengal 14%

Uttar Pradesh 14%

Andhra Pradesh 12%

Punjab 11%

Odisha 7%

Chhattisgarh 6%

Tamil Nadu 5%

Rest of India 31%

Source: Ministry of agriculture

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 16

Exhibit 28. Paddy prices on continuous uptick

` /quintal FY13 FY14 FY15 FY16 FY17

Common 1,250 1,310 1,360 1,410 1,470

YoY (%) 16% 5% 4% 4% 4%

Grade A 1,280 1,345 1,400 1,450 1,510

YoY (%) 15% 5% 4% 4% 4%

Source: Agri. census

Exhibit 29. Subsidy structure of power tiller

Name of the

Farm

Equipment

For SC, ST, Small & Marginal

Farmers, Women and NE States’

Beneficiaries

For Other Beneficiaries

Maximum Permissible

subsidy per

Equipment

Assistance

Maximum

Permissible

subsidy per

Equipment

Assistance

Power Tiller

(below 8 BHP) `50,000 50% `40,000 40%

Power Tiller (8

BHP & above) `75,000 50% `60,000 40%

Source: RKVY

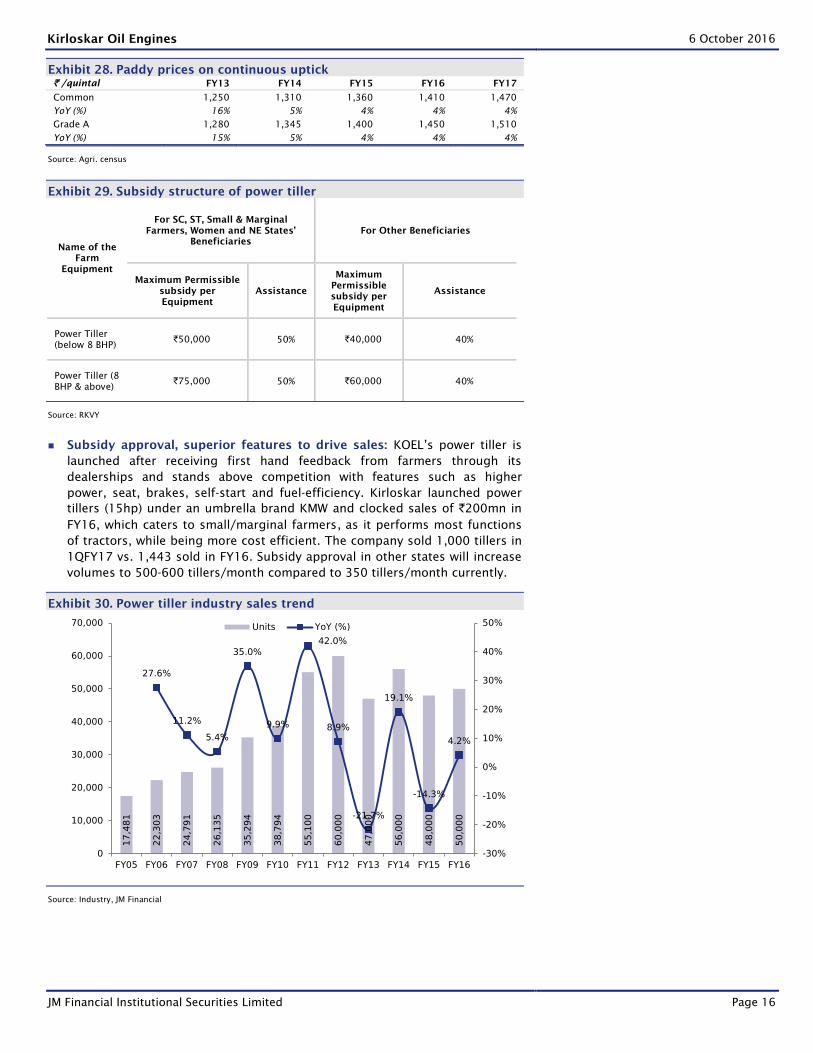

Subsidy approval, superior features to drive sales: KOEL’s power tiller is

launched after receiving first hand feedback from farmers through its

dealerships and stands above competition with features such as higher

power, seat, brakes, self-start and fuel-efficiency. Kirloskar launched power

tillers (15hp) under an umbrella brand KMW and clocked sales of `200mn in

FY16, which caters to small/marginal farmers, as it performs most functions

of tractors, while being more cost efficient. The company sold 1,000 tillers in

1QFY17 vs. 1,443 sold in FY16. Subsidy approval in other states will increase

volumes to 500-600 tillers/month compared to 350 tillers/month currently.

Exhibit 30. Power tiller industry sales trend

17

,48

1

22

,30

3

24

,79

1

26

,13

5

35

,29

4

38

,79

4

55

,10

0

60

,00

0

47

,00

0

56

,00

0

48

,00

0

50

,00

0

27.6%

11.2%

5.4%

35.0%

9.9%

42.0%

8.9%

-21.7%

19.1%

-14.3%

4.2%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Units YoY (%)

Source: Industry, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 17

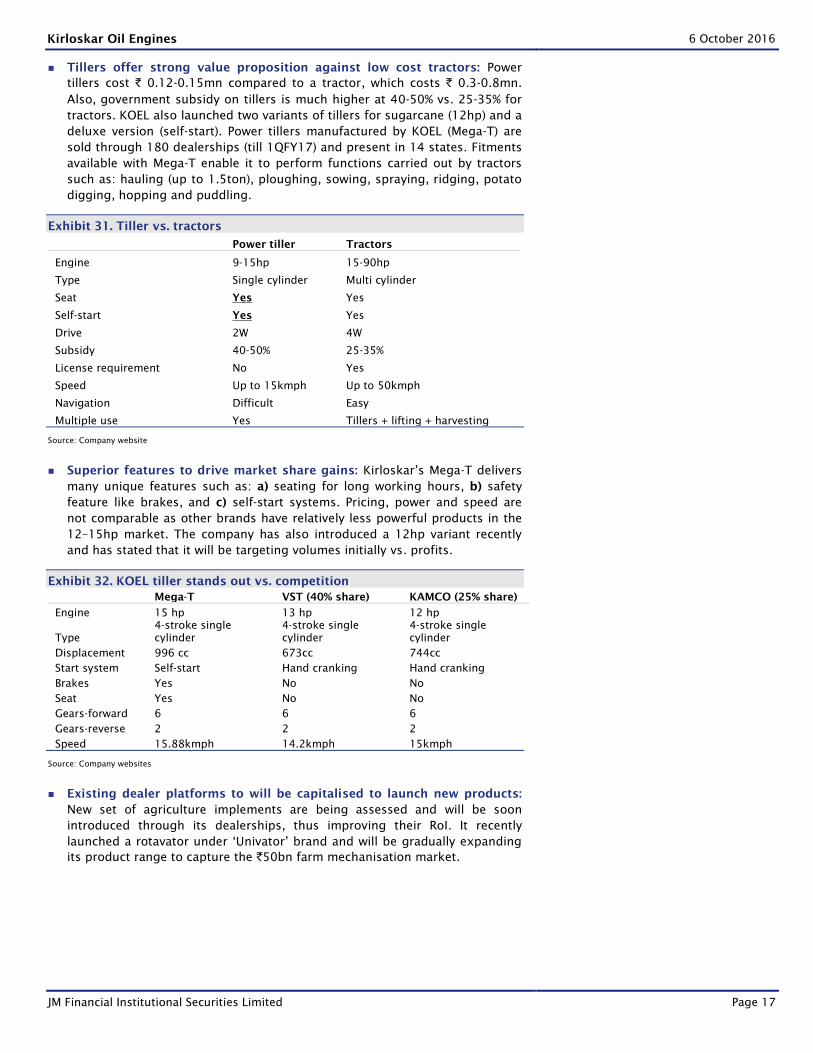

Tillers offer strong value proposition against low cost tractors: Power

tillers cost ` 0.12-0.15mn compared to a tractor, which costs ` 0.3-0.8mn.

Also, government subsidy on tillers is much higher at 40-50% vs. 25-35% for

tractors. KOEL also launched two variants of tillers for sugarcane (12hp) and a

deluxe version (self-start). Power tillers manufactured by KOEL (Mega-T) are

sold through 180 dealerships (till 1QFY17) and present in 14 states. Fitments

available with Mega-T enable it to perform functions carried out by tractors

such as: hauling (up to 1.5ton), ploughing, sowing, spraying, ridging, potato

digging, hopping and puddling.

Exhibit 31. Tiller vs. tractors

Power tiller Tractors

Engine 9-15hp 15-90hp

Type Single cylinder Multi cylinder

Seat Yes Yes

Self-start Yes Yes

Drive 2W 4W

Subsidy 40-50% 25-35%

License requirement No Yes

Speed Up to 15kmph Up to 50kmph

Navigation Difficult Easy

Multiple use Yes Tillers + lifting + harvesting

Source: Company website

Superior features to drive market share gains: Kirloskar’s Mega-T delivers

many unique features such as: a) seating for long working hours, b) safety

feature like brakes, and c) self-start systems. Pricing, power and speed are

not comparable as other brands have relatively less powerful products in the

12–15hp market. The company has also introduced a 12hp variant recently

and has stated that it will be targeting volumes initially vs. profits.

Exhibit 32. KOEL tiller stands out vs. competition

Mega-T VST (40% share) KAMCO (25% share)

Engine 15 hp 13 hp 12 hp

Type

4-stroke single

cylinder

4-stroke single

cylinder

4-stroke single

cylinder

Displacement 996 cc 673cc 744cc

Start system Self-start Hand cranking Hand cranking

Brakes Yes No No

Seat Yes No No

Gears-forward 6 6 6

Gears-reverse 2 2 2

Speed 15.88kmph 14.2kmph 15kmph

Source: Company websites

Existing dealer platforms to will be capitalised to launch new products:

New set of agriculture implements are being assessed and will be soon

introduced through its dealerships, thus improving their RoI. It recently

launched a rotavator under ‘Univator’ brand and will be gradually expanding

its product range to capture the `50bn farm mechanisation market.

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 18

Industrials (14% of sales)

Exhibit 33. Industrials: Segment Overview

Industrial (14% of sales)

Off-highway Tractors

Source: JM Financial

Improved road project awards raise high double-digit growth

expectation: KOEL sells engines in the 20-800hp range catering to various

applications such as earthmoving, construction, mining, mat handling and

fluid handling. The construction equipment market (10% of sales) stabilised

after four consecutive years of decline. The company holds a market share of

30%, down from 55% as supplies to JCB India stopped after the latter

integrated backwards. However, sales have improved in FY16 on: a) OEM

additions and b) launch of new products (excavators, motor graders and fire-

fighting). We expect this segment to grow in high double-digits on improved

road project awards (1QFY17: +40% YoY).

Exhibit 34. Construction engine industry sales slumped during FY11-16

70

,00

0

80

,00

0

64

,00

0

55

,00

0

46

,00

0

47

,00

0

14%

-20%

-14%-16%

2%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-1,00,000

-80,000

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

1,00,000

FY11 FY12 FY13 FY14 FY15 FY16

No of units YoY (%)

Source: Company, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 19

Exhibit 35. Road project awards picking up

1,734

1,234

643

3,351

5,059

6,491

1,1161,436

3,068

4,171

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

km

s

Source: NHAI

Exhibit 36. KOEL: Off-highway engine sales

-15%

-30%

-16%

-3%

12%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

-16,000

-11,000

-6,000

-1,000

4,000

9,000

FY11 FY12 FY13 FY14 FY15 FY16

Off highway sales (`/mn) YoY (%)

Source: Company, JM Financial

Firming up strong foothold in tractor market: KOEL sells tractor engines to

Swaraj, ACE and other small players, of which 90% of supplies are to Swaraj.

The supplies to Swaraj are to its model 855, which is a 55-hp model powered

with Kirloskar Oil’s three-cylinder engine. Over the past 5 years, Swaraj

Tractors doubled its market share from 8% to 15%, which led to improved

tractor sales. We believe the segment is poised for healthy growth on new

product launches by Swaraj, market share gains and improved farm income

on healthy rainfall (1QFY17: +6% YoY).

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 20

Exhibit 37. Tractor sales are expected to witness cyclical uptick

Tractor sales slumped in FY15-16, now reviving Swaraj engines gaining market share consistently

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Industry Volumes - YoY Swaraj Engines - YoY

9.0%

11.6%11.9%

12.4% 12.6%13.1%

13.7% 13.8%

15.3%

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Source: Company, JM Financial

Exhibit 38. KOEL’s tractor engine sales

42%

-23%

50%

-6% -5%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

0

200

400

600

800

1,000

1,200

1,400

FY11 FY12 FY13 FY14 FY15 FY16

Tractor sales (`/mn) YoY (%)

Source: Company, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 21

Product support (14% of sales)

Leveraging network to maintain stable sales growth: The customer

support segment offers stable growth as sales are linked to opex (not capex).

However, the segment is facing demand headwinds such as: a) customer

migration from subject matter expertise (SME) to integrated maintenance

expertise (IME), b) lower running of DG sets, and c) decline in construction

equipment fleet. However, growth is likely to revert on: a) addition of service

outlets (an outlet within 80kms radius now), b) lag effect of growth in power

gen and industrial segment growth (1QFY17: +11%), and c) focus on

institutional tie-ups for AMC contracts. KOEL has more than 450 service

outlets in the country and manages a fleet of more than 600,000 machines.

Exhibit 39. Number of service outlets

342359 362

437452

0

50

100

150

200

250

300

350

400

450

500

FY12 FY13 FY14 FY15 FY16

No of service outlets

Source: Company, JM Financial

Exhibit 40. KOEL’s customer support segment sales

11%

-6% -7%

1% 1%

12% 12%

10%

-12%

-7%

-2%

3%

8%

13%

18%

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Customer support sales (`/mn) YoY (%)

Source: Company, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 22

Large Engines (5% of sales)

Lumpy nature of NPCIL order keeps growth topsy-turvy in this segment:

KOEL supplies diesel engines in 2,400hp to 11,000hp catering to DG sets

from 1.7MW to 7.1MW for stationary power plants. Sales in this segment are

lumpy due to the investment nature of NPCIL, which procures gensets for

critical standby purpose. Following the completion of the large order from

NPCIL in 1HFY15, we saw a sharp drop in sales in the large engines business

segment. Currently, KOEL is under negotiation for a large order from NPCIL,

but we have not factored the same in our estimates due to uncertain nature

of order.

Technology tie-ups and new products to drive growth: KOEL engaged in

several technology tie-ups with Rolls Royce for high capacity MTU engines,

Bio Cube Corp, Canada, and Anglo Belgium Corp for HHP rail engines to

increase its product offerings in the large engine segment. The company is

targeting to improve growth in LEBG through: a) new products in defence:

compact genset for Indian army (mkt size: `1bn) and energy systems for

radar applications at high altitudes, b) new products for the Indian Railways,

working with RDSO, and c) initiated export of marine engines through first

order from Bangladesh.

Exhibit 41. Large engine business overview

Large engines business split Customer profile

Large Engines (5% of sales)

Stationary power plantsPropusion and auxiliary

engines

Stationary power plants Propulsion auxiliary sets and spares

Nuclear Power Corp India Indian Navy

Bharat Heavy Electricals Ltd Ship builders

Engineers India Ship owners

MECON Ship operators

Bechtel

Source: Company, JM Financial

Exhibit 42. Large engine segment’s sales trend

1,150 1,154 1,107 1,363 1,120

260 526 1,903

1,057

0

500

1,000

1,500

2,000

2,500

3,000

3,500

FY12 FY13 FY14 FY15 FY16

`m

n

Propulsion auxiliary sets and spares Stationary power plants

Source: Company, JM Financial

NPCIL order

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 23

Exports (10% of sales)

Witnessing consistent growth in sales since FY11: Exports constitute 10%

of net sales and have expanded consistently at a CAGR of 10.3% over FY11–

16 compared to domestic sales, which remained flat during the same period.

The growth was largely driven by the expansion of the existing product

franchise to new markets. While the company exports to over 40 countries,

nearly 90% of its exports are concentrated in the Middle East (58%) and Africa

(30%).

Exhibit 43. Exports: Sales grown consistently

11%

4%

18%

4%

13%

0%

8%9%

-5%

0%

5%

10%

15%

20%

0

500

1,000

1,500

2,000

2,500

3,000

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Exports (Rsmn) YoY (%)

Source: Company, JM Financial

Entry in new markets to drive future growth: KOEL has a vision to expand

footprint across the globe by 2025, by consistently entering 2–3 new

countries each year. While penetration in the Middle East and Africa is

through power gensets, entry in Europe and Russia is for industrial engines.

KOEL also recently incorporated a subsidiary in the US, the largest DG set

market in world and has identified products to get EPA approval.

Exhibit 44. Exports split: Geography and segment wise

The Middle East and Africa constitute 90% of exports Export sales split between different segments

Middle East58%

Africa30%

South Asia5%

Americas4%

Others3%

Power gen57%

Agriculture15%

Industrial20%

Customer support

8%

Large engines0%

Source: Company, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 24

Financials

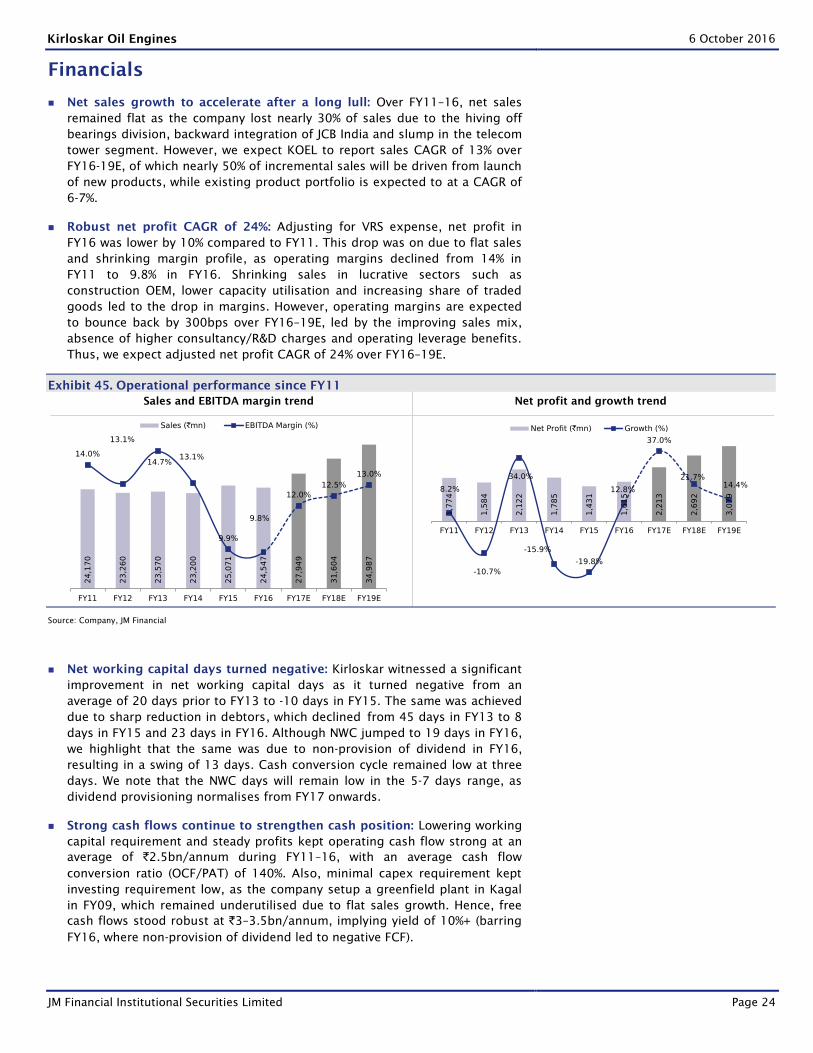

Net sales growth to accelerate after a long lull: Over FY11–16, net sales

remained flat as the company lost nearly 30% of sales due to the hiving off

bearings division, backward integration of JCB India and slump in the telecom

tower segment. However, we expect KOEL to report sales CAGR of 13% over

FY16-19E, of which nearly 50% of incremental sales will be driven from launch

of new products, while existing product portfolio is expected to at a CAGR of

6-7%.

Robust net profit CAGR of 24%: Adjusting for VRS expense, net profit in

FY16 was lower by 10% compared to FY11. This drop was on due to flat sales

and shrinking margin profile, as operating margins declined from 14% in

FY11 to 9.8% in FY16. Shrinking sales in lucrative sectors such as

construction OEM, lower capacity utilisation and increasing share of traded

goods led to the drop in margins. However, operating margins are expected

to bounce back by 300bps over FY16–19E, led by the improving sales mix,

absence of higher consultancy/R&D charges and operating leverage benefits.

Thus, we expect adjusted net profit CAGR of 24% over FY16–19E.

Exhibit 45. Operational performance since FY11

Sales and EBITDA margin trend Net profit and growth trend

24

,17

0

23

,26

0

23

,57

0

23

,20

0

25

,07

1

24

,54

7

27

,94

9

31

,60

4

34

,98

7

14.0%

13.1%

14.7%13.1%

9.9%

9.8%

12.0%

12.5%

13.0%

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Sales (`mn) EBITDA Margin (%)

1,7

74

1,5

84

2,1

22

1,7

85

1,4

31

1,6

15

2,2

13

2,6

92

3,0

79

8.2%

-10.7%

34.0%

-15.9%

-19.8%

12.8%

37.0%

21.7%14.4%

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Net Profit (`mn) Growth (%)

Source: Company, JM Financial

Net working capital days turned negative: Kirloskar witnessed a significant

improvement in net working capital days as it turned negative from an

average of 20 days prior to FY13 to -10 days in FY15. The same was achieved

due to sharp reduction in debtors, which declined from 45 days in FY13 to 8

days in FY15 and 23 days in FY16. Although NWC jumped to 19 days in FY16,

we highlight that the same was due to non-provision of dividend in FY16,

resulting in a swing of 13 days. Cash conversion cycle remained low at three

days. We note that the NWC days will remain low in the 5-7 days range, as

dividend provisioning normalises from FY17 onwards.

Strong cash flows continue to strengthen cash position: Lowering working

capital requirement and steady profits kept operating cash flow strong at an

average of `2.5bn/annum during FY11–16, with an average cash flow

conversion ratio (OCF/PAT) of 140%. Also, minimal capex requirement kept

investing requirement low, as the company setup a greenfield plant in Kagal

in FY09, which remained underutilised due to flat sales growth. Hence, free

cash flows stood robust at `3–3.5bn/annum, implying yield of 10%+ (barring

FY16, where non-provision of dividend led to negative FCF).

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 25

Exhibit 46. Lower NWC and capex requirement to keep free cash flows robust

NWC requirement to dip from FY17 onwards Strong cash flows will keep strengthening cash position

1.7

5.3

6.3

9.9

4.0

5.4

2.3

-2.6

5.1

1.9 1.9 1.9

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Net Working Capital (`mn) NWC/Sales (%)

42

3

3,6

27

1,3

38

2,8

32

3,1

04

-33

1

3,5

98

2,7

71

3,2

12

22.0

38.1

30.6

45.6

62.357.1

73.7

82.8

93.5

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Free Cash Flow (`mn) Cash on books (`/share)

Source: Company, JM Financial

Inherent business returns are strong, but increasing cash balance is

detrimental to RoEs: RoEs stood low at 11% during FY15/16 due to declining

margins, fall in asset turns on lower capacity utilisations and lower return on

increasing cash balance (5–7% vs. 20-30% in core business). We assume some

recovery in RoE to the 15-18% range on margin recovery and improved

capacity utilisation levels. Since RoEs appear low, we evaluate the RoIC profile

to analyse return on invested capital (RoIC). RoIC is expected to increase to

29% in FY17, which is similar to Cummins India, despite much lower margin

profile of 12-13% vs. 16-17% for Cummins India. We believe increasing cash

balance will keep return ratios suppressed and the management should

increase dividend payout or explore profitable ways to deploy excess cash.

Exhibit 47. Return ratios to improve materially

21.7%

15.9%18.8%

14.4%

10.7% 11.4%

14.7%16.6% 17.6%

23.2%

19.0%

26.0%

21.8%

18.5% 19.1%

28.9%

41.9%

49.9%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

RoE (%) RoIC (%)

Source: JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 26

Valuation

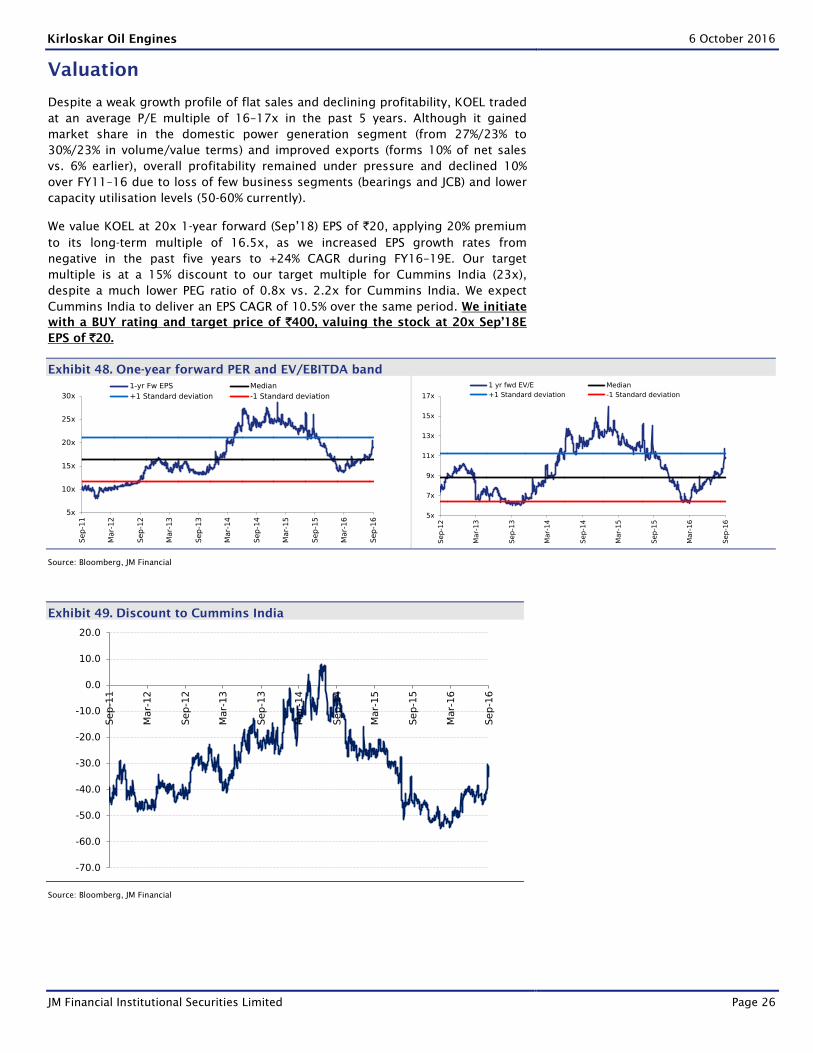

Despite a weak growth profile of flat sales and declining profitability, KOEL traded

at an average P/E multiple of 16–17x in the past 5 years. Although it gained

market share in the domestic power generation segment (from 27%/23% to

30%/23% in volume/value terms) and improved exports (forms 10% of net sales

vs. 6% earlier), overall profitability remained under pressure and declined 10%

over FY11–16 due to loss of few business segments (bearings and JCB) and lower

capacity utilisation levels (50-60% currently).

We value KOEL at 20x 1-year forward (Sep’18) EPS of `20, applying 20% premium

to its long-term multiple of 16.5x, as we increased EPS growth rates from

negative in the past five years to +24% CAGR during FY16–19E. Our target

multiple is at a 15% discount to our target multiple for Cummins India (23x),

despite a much lower PEG ratio of 0.8x vs. 2.2x for Cummins India. We expect

Cummins India to deliver an EPS CAGR of 10.5% over the same period. We initiate

with a BUY rating and target price of `400, valuing the stock at 20x Sep’18E

EPS of `20.

Exhibit 48. One-year forward PER and EV/EBITDA band

5x

10x

15x

20x

25x

30x

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

1-yr Fw EPS Median

+1 Standard deviation -1 Standard deviation

5x

7x

9x

11x

13x

15x

17x

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

1 yr fwd EV/E Median

+1 Standard deviation -1 Standard deviation

Source: Bloomberg, JM Financial

Exhibit 49. Discount to Cummins India

-70.0

-60.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Sep

-16

Source: Bloomberg, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 27

Peer valuation

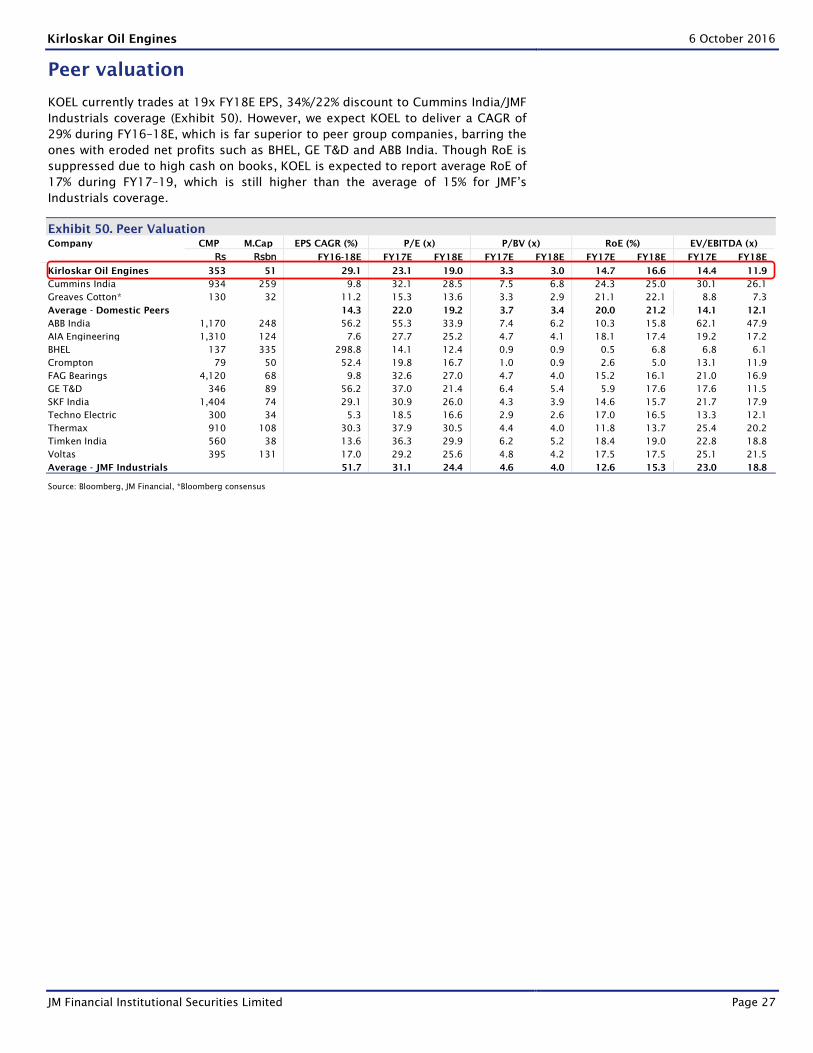

KOEL currently trades at 19x FY18E EPS, 34%/22% discount to Cummins India/JMF

Industrials coverage (Exhibit 50). However, we expect KOEL to deliver a CAGR of

29% during FY16–18E, which is far superior to peer group companies, barring the

ones with eroded net profits such as BHEL, GE T&D and ABB India. Though RoE is

suppressed due to high cash on books, KOEL is expected to report average RoE of

17% during FY17–19, which is still higher than the average of 15% for JMF’s

Industrials coverage.

Exhibit 50. Peer Valuation

Company CMP M.Cap EPS CAGR (%) P/E (x) P/BV (x) RoE (%) EV/EBITDA (x)

Rs Rsbn FY16-18E FY17E FY18E FY17E FY18E FY17E FY18E FY17E FY18E

Kirloskar Oil Engines 353 51 29.1 23.1 19.0 3.3 3.0 14.7 16.6 14.4 11.9

Cummins India 934 259 9.8 32.1 28.5 7.5 6.8 24.3 25.0 30.1 26.1

Greaves Cotton* 130 32 11.2 15.3 13.6 3.3 2.9 21.1 22.1 8.8 7.3

Average - Domestic Peers

14.3 22.0 19.2 3.7 3.4 20.0 21.2 14.1 12.1

ABB India 1,170 248 56.2 55.3 33.9 7.4 6.2 10.3 15.8 62.1 47.9

AIA Engineering 1,310 124 7.6 27.7 25.2 4.7 4.1 18.1 17.4 19.2 17.2

BHEL 137 335 298.8 14.1 12.4 0.9 0.9 0.5 6.8 6.8 6.1

Crompton 79 50 52.4 19.8 16.7 1.0 0.9 2.6 5.0 13.1 11.9

FAG Bearings 4,120 68 9.8 32.6 27.0 4.7 4.0 15.2 16.1 21.0 16.9

GE T&D 346 89 56.2 37.0 21.4 6.4 5.4 5.9 17.6 17.6 11.5

SKF India 1,404 74 29.1 30.9 26.0 4.3 3.9 14.6 15.7 21.7 17.9

Techno Electric 300 34 5.3 18.5 16.6 2.9 2.6 17.0 16.5 13.3 12.1

Thermax 910 108 30.3 37.9 30.5 4.4 4.0 11.8 13.7 25.4 20.2

Timken India 560 38 13.6 36.3 29.9 6.2 5.2 18.4 19.0 22.8 18.8

Voltas 395 131 17.0 29.2 25.6 4.8 4.2 17.5 17.5 25.1 21.5

Average - JMF Industrials

51.7 31.1 24.4 4.6 4.0 12.6 15.3 23.0 18.8

Source: Bloomberg, JM Financial, *Bloomberg consensus

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 28

Key risks

Technology disruption: Low kVA diesel generators face obsolescence risk

from high capacity solar-based inverters. However, the overlap is limited to

small-sized generators in areas with strict pollution norms. While solar

inverter systems are cheaper on the operational cost front, the initial outgo is

much higher, while the surface area required to install solar systems is large

and currently not feasible in most segments.

Management attrition: Of the five new team members in the top

management, one member has recently left. While the company has

conducted significant changes after assumption of office by the new

management team, we see limited risk of attrition as the composition of the

board of directors is likely to remain intact. However, we believe introduction

of an ESOP scheme will help retain senior positions in the company.

Higher power availability: Power deficit has declined from a peak of 16.6%

in FY08 to 2% in FY16, which has led to a decline in base load/prime power

categories of gensets. However, standby generators will remain unaffected

due to lack of alternatives. We note that share of backup gensets has

increased from 60% in FY08 to nearly 95% in FY16.

Rise in diesel prices: Diesel prices have exhibited a negative correlation with

demand for power gensets in the past. However, a decline in share of base

load/prime power gensets has reduced this impact as demand for standby

generators is not elastic due to lack of alternatives.

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 29

Management profile

Exhibit 51. Key management personnel

Name Position Profile

Atul Kirloskar Executive Chairman

Started as trainee in 1978 in Kirloskar Group and has over 38 years of experience in

the industry. He also serves as a member of World Economic Forum and was

Chairman of CII National Committee of Defence during 1998-2008

Gautam Kulkarni Executive Vice Chairman

Started as trainee in 1978 in Kirloskar Group and has over 38 years of experience in

the industry and has held various positions in Kirloskar Group companies

Nihal Kulkarni Managing Director

Joined in Jan'12. He is AB in Economics from Brown University, USA. Over 6 years’

experience in finance and investments and has worked with Toyota Motors, GG

Dandekar Machines and DSP Merrill Lynch

RR Deshpande Jt Managing Director

Joined in Jul'77 as mechanical engineer. Worked in several departments of KOEL. He

is responsible for fast growth of medium engines SBU during his tenure as SBU

Head

Rahul Kirloskar Non-Executive Director

Started his career in Kirloskar Group as BS (Mechanical Engineer) 25 years back and

has served at senior levels in different capacities. He is also Executive Chairman of

Kirloskar Pneumatic Ltd

PG Pawar Independent Non-Executive Director An Engineer from BITS, Pilani, he is Chairman of Sakal Papers and ASK Chemicals

R Srinivasan Independent Non-Executive Director

A Mechanical Engineer from University of Madras he has worked in Buckau Wolf,

Grevenbroich, M/s Krupp Widia and is currently on board of several companies like

Sundaram Fasteners, TTK Prestige, TTK Healthcare, Yuken India

M Lakshminarayan Independent Non-Executive Director

He is Masters from IIT, Mumbai and has worked with Tata Motors and Bosch. He is

presently MD of Harman International and a Director in KOEL, Carborundum

Universal, Rane Ltd ach Chairman of Wabco India

T Vinodkumar Chief Financial Officer

Jopined in Dec'12, he is a Chartered Accountant and has worked with a gamut of

companies like Voltas, Britannia, HUL and Tata Chemicals.

Sanjeev Nimkar SBU Head: Power gen and Industrial

Joined in Apr'12, he is an MBA from IIM-Calcutta and has worked with Lafarge and

Philips India earlier in various capacities

Antony Cherukara SBU Head: Agri and allied business

Joined in Apr'12, he is a Chartered Financial Analyst and Mechanical Engineer. He

has worked with New Holland and Mahindra & Mahindra in various capacities

Sheetal Kothari SBU Head: Large Engines

Working with Kirloskar Group since several years and currently heading the Large

Engines Business Group

Source: Company website

Exhibit 52. Kirloskar group family tree and ownership structure in group companies

Self and kin 0.50% Self and kin 39.35% Self and kin 0.51% Self and kin 0.11% KBL Self and kin 0.56%

Invst firms 5.78% Invst firms 0.35% Invst firms 5.74% Invst firms 0.03% Invst firms 5.90%

KOEL Self and kin 17.65% KOEL Self and kin 0.04% KOEL Self and kin 17.59% KOEL Self and kin 0.17% KOEL Self and kin 18.07%

Invst firms 1.37% Invst firms 0.00% Invst firms 1.36% Invst firms 0.01% Invst firms 1.43%

KPCL Self and kin 1.20% KPCL Self and kin 0.00% KPCL Self and kin 1.73% KPCL Self and kin 0.00% KPCL Self and kin 1.25%

Invst firms 15.28% Invst firms 0.01% Invst firms 15.28% Invst firms 0.07% Invst firms 15.54%

KFIL Self and kin 2.13% KFIL Self and kin 0.00% KFIL Self and kin 2.20% KFIL Self and kin 0.00% KFIL Self and kin 2.26%

Invst firms 12.44% Invst firms 0.01% Invst firms 12.37% Invst firms 0.06% Invst firms 12.84%

S. L. Kirloskar

Chandrakant Kirloskar Shreekant Kirloskar

Atul Kirloskar Sanjay Kirloskar Rahul Kirloskar Vikram Kirloskar

KBL

Holdings

(%)

KBL

Nihal Kulkarni

Gautam Kulkarni

KBL KBL

Source: BSE. Note: KBL: Kirloskar Brothers Ltd, KOEL: Kirloskar Oil Engines Ltd, KPCL: Kirloskar Pneumatic Ltd, KFIL: Kirloskar Ferrous Industries Ltd

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 30

Financial Tables (Standalone)

Profit & Loss Statement (` mn)

Y/E March FY15A FY16A FY17E FY18E FY19E

Net sales (Net of excise) 25,071 24,547 27,949 31,604 34,987

Growth (%) 8.1 -2.1 13.9 13.1 10.7

Other operational income 0 0 0 0 0

Raw material (or COGS) 16,257 15,431 17,888 20,226 22,392

Personnel cost 1,884 1,856 1,949 2,211 2,437

Other expenses (or SG&A) 4,444 4,864 4,751 5,215 5,598

EBITDA 2,486 2,397 3,361 3,952 4,560

EBITDA (%) 9.9 9.8 12.0 12.5 13.0

Growth (%) -18.3 -3.6 40.2 17.6 15.4

Other non-op. income 589 740 814 895 985

Depreciation and amort. 1,019 1,115 1,134 1,150 1,199

EBIT 2,056 2,022 3,041 3,698 4,346

Add: Net interest income -2 -1 -10 -10 -10

Pre tax profit 2,054 2,021 3,031 3,688 4,336

Taxes 623 361 818 996 1,257

Add: Extraordinary items 0 -255 0 0 0

Less: Minority interest 0 0 0 0 0

Reported net profit 1,431 1,405 2,213 2,692 3,079

Adjusted net profit 1,431 1,615 2,213 2,692 3,079

Margin (%) 5.7 6.6 7.9 8.5 8.8

Diluted share cap. (mn) 145 145 145 145 145

Diluted EPS (`) 9.9 11.2 15.3 18.6 21.3

Growth (%) -19.8 12.8 37.0 21.7 14.4

Total Dividend + Tax 870 870 1,198 1,458 1,667 Source: Company, JM Financial

Balance Sheet (` mn)

Y/E March FY15A FY16A FY17E FY18E FY19E

Share capital 289 289 289 289 289

Other capital 0 0 0 0 0

Reserves and surplus 13,125 14,108 15,123 16,357 17,768

Networth 13,414 14,397 15,412 16,646 18,057

Total loans 0 0 0 0 0

Minority interest 0 0 0 0 0

Sources of funds 13,414 14,397 15,412 16,646 18,057

Intangible assets 0 0 0 0 0

Fixed assets 12,492 13,120 13,870 14,870 15,870

Less: Depn. and amort. 7,356 8,346 9,480 10,630 11,828

Net block 5,136 4,773 4,390 4,240 4,041

Capital WIP 213 289 0 0 0

Investments 8,763 7,867 7,867 7,867 7,867

Def tax assets/- liability -289 -177 -177 -177 -177

Current assets 5,212 6,655 9,840 12,075 14,473

Inventories 1,716 2,029 2,297 2,598 2,876

Sundry debtors 526 1,522 1,914 2,165 2,396

Cash & bank balances 253 395 2,795 4,109 5,654

Other current assets 631 495 536 606 671

Loans & advances 2,086 2,215 2,297 2,598 2,876

Current liabilities & prov. 5,621 5,011 6,509 7,360 8,148

Current liabilities 4,204 4,448 4,977 5,628 6,231

Provisions and others 1,417 563 1,531 1,732 1,917

Net current assets -409 1,645 3,331 4,715 6,325

Others (net) 0 0 0 0 0

Application of funds 13,414 14,397 15,412 16,646 18,057 Source: Company, JM Financial

Cash flow statement (` mn)

Y/E March FY15A FY16A FY17E FY18E FY19E

Reported net profit 1,431 1,405 2,213 2,692 3,079

Depreciation and amort. 995 990 1,134 1,150 1,199

-Inc/dec in working cap. 1,451 -1,369 -148 -50 -46

Others 0 0 0 0 0

Cash from operations (a) 3,877 1,027 3,198 3,791 4,231

-Inc/dec in investments -2,686 896 0 0 0

Capex -494 -703 -461 -1,000 -1,000

Others -266 -542 861 -20 -19

Cash flow from inv. (b) -3,446 -350 400 -1,020 -1,019

Inc/-dec in capital 181 448 0 0 0

Dividend+Tax thereon -870 -870 -1,198 -1,458 -1,667

Inc/-dec in loans 0 0 0 0 0

Others -14 -112 0 0 0

Financial cash flow ( c ) -703 -534 -1,198 -1,458 -1,667

Inc/-dec in cash (a+b+c) -272 143 2,400 1,313 1,545

Opening cash balance 524 253 395 2,795 4,109

Closing cash balance 253 395 2,795 4,109 5,654 Source: Company, JM Financial

Key Ratios

Y/E March FY15A FY16A FY17E FY18E FY19E

BV/Share (`) 92.8 99.6 106.6 115.1 124.9

ROIC (%) 11.3 11.9 16.7 21.5 24.7

ROE (%) 11.0 11.6 14.8 16.8 17.7

Net Debt/equity ratio (x) -0.7 -0.6 -0.7 -0.7 -0.7

Valuation ratios (x)

PER 35.7 31.7 23.1 19.0 16.6

PBV 3.8 3.6 3.3 3.1 2.8

EV/EBITDA 16.9 17.9 12.0 9.9 8.2

EV/Sales 1.7 1.7 1.4 1.2 1.1

Turnover ratios (no.)

Debtor days 8 23 25 25 25

Inventory days 25 30 30 30 30

Creditor days 76 78 78 78 78

Source: Company, JM Financial

Kirloskar Oil Engines 6 October 2016

JM Financial Institutional Securities Limited Page 31

APPENDIX I

JM Financial Institutional Securities Limited

Corporate Identity Number: U65192MH1995PLC092522

Member of BSE Ltd. and National Stock Exchange of India Ltd. and Metropolitan Stock Exchange of India Ltd.

SEBI Registration Nos.: BSE - INZ010012532, NSE - INZ230012536 and MSEI - INZ260012539, Research Analyst – INH000000610

Registered Office: 7th Floor, Cnergy, Appasaheb Marathe Marg, Prabhadevi, Mumbai 400 025, India.

Board: +9122 6630 3030 | Fax: +91 22 6630 3488 | Email: [email protected] | www.jmfl.com

Compliance Officer: Mr. Sunny Shah | Tel: +91 22 6630 3383 | Email: [email protected]

Definition of ratings

Rating Meaning

Buy Total expected returns of more than 15%. Total expected return includes dividend yields.

Hold Price expected to move in the range of 10% downside to 15% upside from the current market price.

Sell Price expected to move downwards by more than 10%

Research Analyst(s) Certification

The Research Analyst(s), with respect to each issuer and its securities covered by them in this research report, certify that:

All of the views expressed in this research report accurately reflect his or her or their personal views about all of the issuers and their

securities; and

No part of his or her or their compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed

in this research report.

Important Disclosures

This research report has been prepared by JM Financial Institutional Securities Limited (JM Financial Institutional Securities) to provide

information about the company(ies) and sector(s), if any, covered in the report and may be distributed by it and/or its associates solely for the

purpose of information of the select recipient of this report. This report and/or any part thereof, may not be duplicated in any form and/or

reproduced or redistributed without the prior written consent of JM Financial Institutional Securities. This report has been prepared

independent of the companies covered herein.

JM Financial Institutional Securities is registered with the Securities and Exchange Board of India (SEBI) as a Research Analyst, Merchant Banker

and a Stock Broker having trading memberships of the BSE Ltd. (BSE), National Stock Exchange of India Ltd. (NSE) and Metropolitan Stock

Exchange of India Ltd. (MSEI). No material disciplinary action has been taken by SEBI against JM Financial Institutional Securities in the past

two financial years which may impact the investment decision making of the investor.

JM Financial Institutional Securities provides a wide range of investment banking services to a diversified client base of corporates in the

domestic and international markets. It also renders stock broking services primarily to institutional investors and provides the research

services to its institutional clients/investors. JM Financial Institutional Securities and its associates are part of a multi-service, integrated

investment banking, investment management, brokerage and financing group. JM Financial Institutional Securities and/or its associates might

have provided or may provide services in respect of managing offerings of securities, corporate finance, investment banking, mergers &

acquisitions, broking, financing or any other advisory services to the company(ies) covered herein. JM Financial Institutional Securities and/or

its associates might have received during the past twelve months or may receive compensation from the company(ies) mentioned in this

report for rendering any of the above services.

JM Financial Institutional Securities and/or its associates, their directors and employees may; (a) from time to time, have a long or short

position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such

securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) covered under

this report or (c) act as an advisor or lender/borrower to, or may have any financial interest in, such company(ies) or (d) considering the

nature of business/activities that JM Financial Institutional Securities is engaged in, it may have potential conflict of interest at the time of

publication of this report on the subject company(ies).

Neither JM Financial Institutional Securities nor its associates or the Research Analyst(s) named in this report or his/her relatives individually

own one per cent or more securities of the company(ies) covered under this report, at the relevant date as specified in the SEBI (Research

Analysts) Regulations, 2014.

The Research Analyst(s) principally responsible for the preparation of this research report and members of their household are prohibited

from buying or selling debt or equity securities, including but not limited to any option, right, warrant, future, long or short position issued by