key market themes and implications for defined benefit ... slides.pdf · defined benefit pension...

TRANSCRIPT

FOR PROFESSIONAL CLIENTS ONLY, NOT TO BE DISTRIBUTED TO RETAIL CLIENTS

THIS DOCUMENT SHOULD NOT BE REPRODUCED IN ANY FORM WITHOUT PRIOR WRITTEN APPROVAL

Key market themes and implications for defined benefit pension liability risk management

27 September 2016

Interest rate market update

David JamiesonSenior Market Strategist, Financial Solutions Group

P8809

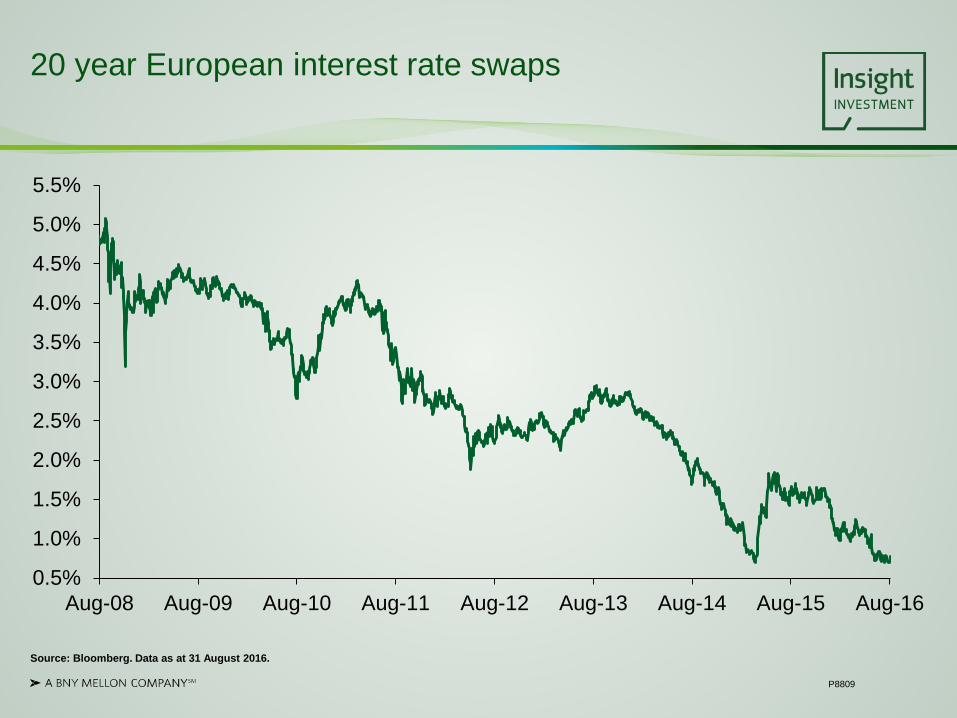

20 year European interest rate swaps

Source: Bloomberg. Data as at 31 August 2016.

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

P8809

20 year global rates

Source: Bloomberg. Data as at 31 August 2016.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Mar-12 Feb-13 Dec-13 Nov-14 Oct-15 Aug-16

%

USUK

Europe

Japan

P8809

US total debt

Debt saturation

Source: Datastream and Insight. Data as at December 2015.

-

5

10

15

20

25

30

35

40

45

50

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

US

D (t

r.)

GDP ($tr.)

Total debt ex financials ($tr.)

P8809

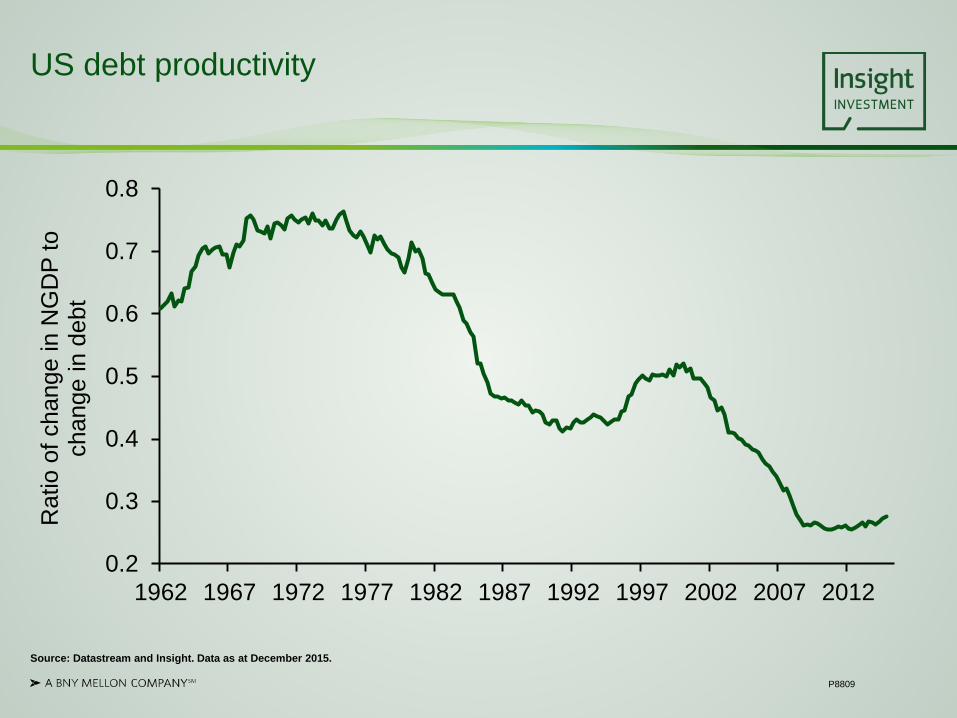

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012

Rat

io o

f cha

nge

in N

GD

P to

ch

ange

in d

ebt

US debt productivity

Source: Datastream and Insight. Data as at December 2015.

P8809

100%

120%

140%

160%

180%

200%

220%

240%

260%

280%

300%

0%

5%

10%

15%

20%

25%

1975 1980 1985 1990 1995 2000 2005 2010 2015

US debt and short-term rates

Source: Datastream and Insight. Data as at December 2015.

3 month Treasury bill rate (LHS)

Total debt ex financials/GDP (RHS)

P8809

Interest rate levels

Source: Reuters. Data as at 31 August 2016.

Country 3 months 2 years 5 years 10 years 20 yearsGermany -0.82 -0.63 -0.50 -0.07 0.27

France -0.58 -0.59 -0.39 0.18 0.79

Netherlands -0.63 -0.61 -0.43 0.04 0.35

Denmark -0.69 -0.57 -0.35 0.02 0.50

Italy -0.36 -0.09 0.25 1.14 1.80

Sweden -0.75 -0.65 -0.36 0.10 0.90

Switzerland -1.05 -0.95 -0.81 -0.50 -0.19

Japan -0.25 -0.20 -0.18 -0.07 0.34

UK 0.23 0.14 0.21 0.64 1.14

US 0.33 0.81 1.20 1.58 1.93

P8809

2016 European net bond supply

Source: BAML. Data as at 16 September 2016.

-140

-120

-100

-80

-60

-40

-20

0

20

40

Jan Feb Mar Apr May Jun Jul Aug Sep(est.)

Oct(est.)

Nov(est.)

Dec(est.)

EU

R b

n

P8809

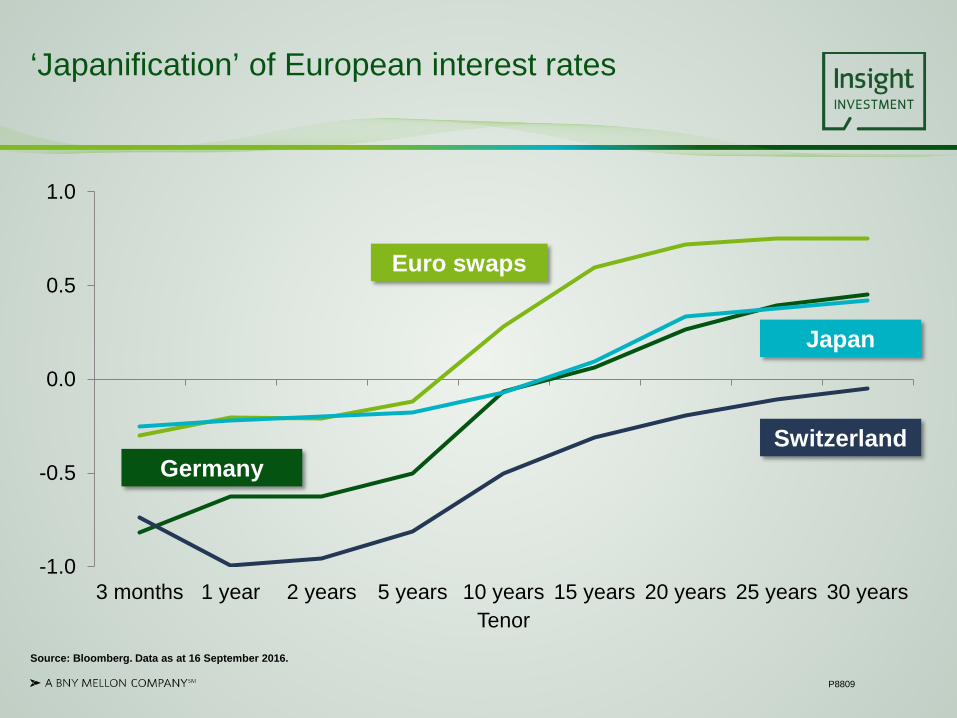

-1.0

-0.5

0.0

0.5

1.0

3 months 1 year 2 years 5 years 10 years 15 years 20 years 25 years 30 yearsTenor

‘Japanification’ of European interest rates

Source: Bloomberg. Data as at 16 September 2016.

Euro swaps

Germany

Japan

Switzerland

P8809

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

0%

2%

4%

6%

8%

10%

12%

14%

0 5 10 15 20 25 30 35 40 45 50Tenor (years)

Persistently low rates are bad too

Source: Bloomberg. Data as at 31 August 2016. 1 year carry is PV weighted.

1 year carry = 0.75%

Liabilities

1 year carry %PV (RHS)

P8809

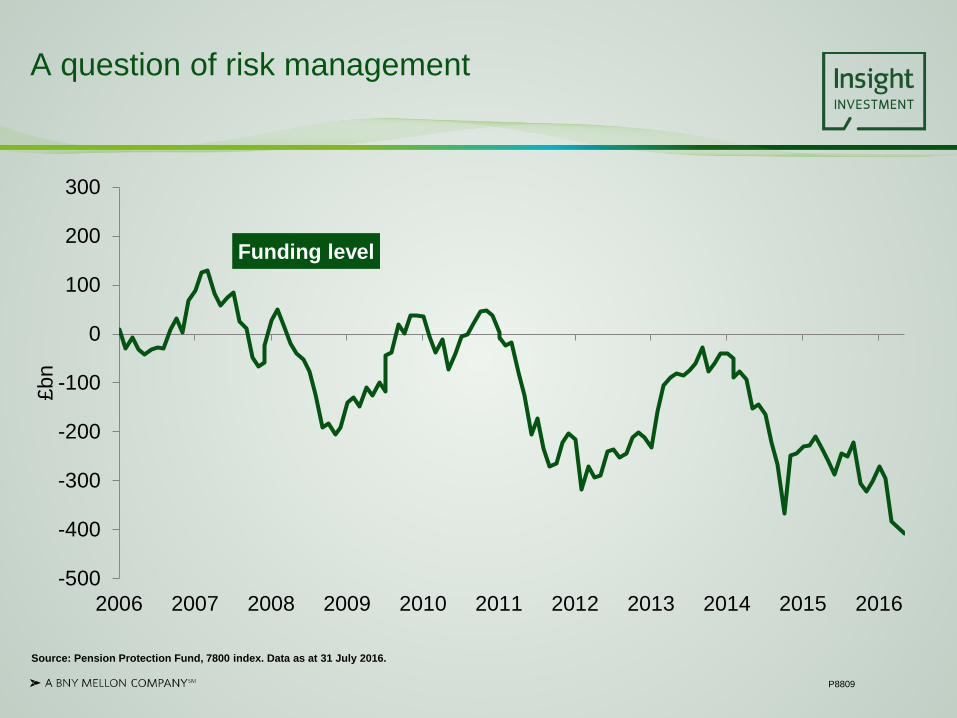

A question of risk management

Source: Pension Protection Fund, 7800 index. Data as at 31 July 2016.

-500

-400

-300

-200

-100

0

100

200

300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

£bn

Funding level

Implications for defined benefit (DB) pension liability risk management

Serkan BektasHead of Client Solutions Group

P8809

DB pension risk management demand remains high and growing

• Interest rate and inflation risk management

• Equity risk management

• Currency risk management

• Synthetic exposures

• Longevity risk management

Affordability of liability hedging is a key consideration, especially for pension schemes that are yet to commence liability hedging programmes

• Trigger programmes to manage the pace of implementation

• Instrument and maturity selection as a way to enhance affordability

• Replacing passive physical investments with synthetic alternatives to provide flexibility and enhance return

• Use of options to cheapen liability hedges and/or provide downside partial protection

Key pension risk management trends

P8809

Ensure hedge size is consistent with downside risk appetite and the overall funding plan

Treatment of hedges under MFS can be a potential consideration

• Hedging of pensioner liabilities as a potential starting point

• Deferred and active liability hedging subject to consideration of long term implications versus MFS

Triggers may be used to guide the pace of implementation

• Market level or funding level triggers to implement or vary pace of hedging

• Alternatively or in addition, time-based triggers, to ensure some minimum hedging is implemented over time

Use of overlays to ensure hedge profile matches liabilities

Size and timing of liability hedge implementation

P8809

Yield difference between government bonds and swaps

Instrument selection: government bond versus swap hedges

Source: Bloomberg. Data as at 2 September 2016.

-100

-50

0

50

100

150

200

2015 2025 2035 2045 2055 2065

Bon

d yi

elds

ver

sus

Eur

ibor

(z-s

prea

d, b

p)

Maturity

Spain

Italy

Germany

Belgium

Netherlands

France

Ireland

Austria

Finland

= Conventional= Index-linked

P8809

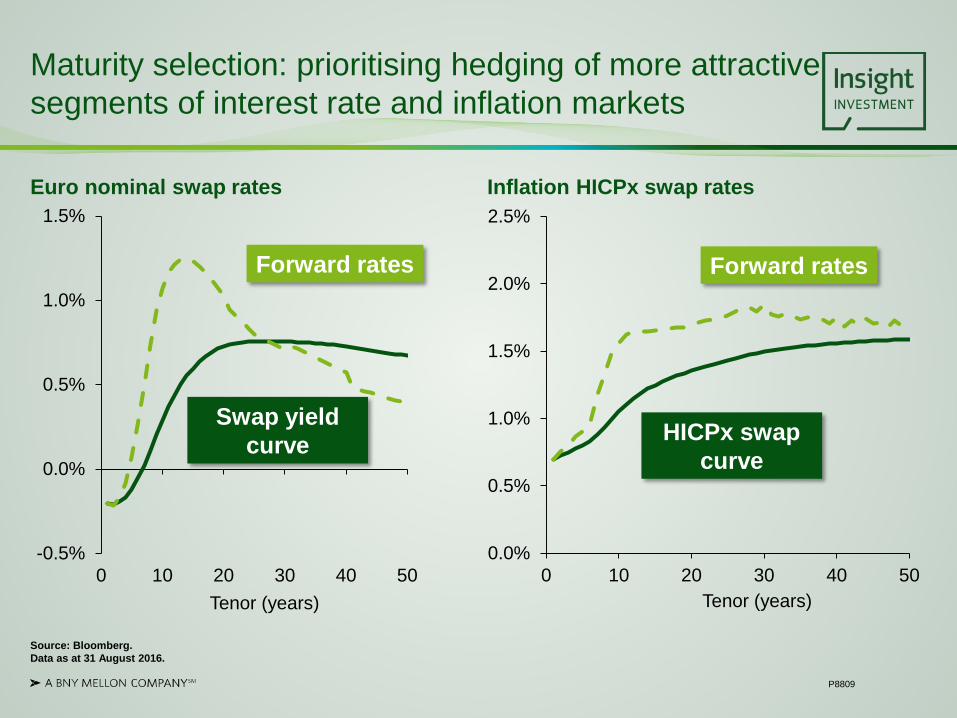

Maturity selection: prioritising hedging of more attractive segments of interest rate and inflation markets

Euro nominal swap rates Inflation HICPx swap rates

Source: Bloomberg.Data as at 31 August 2016.

-0.5%

0.0%

0.5%

1.0%

1.5%

0 10 20 30 40 50Tenor (years)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0 10 20 30 40 50Tenor (years)

Forward rates

Swap yield curve

Forward rates

HICPx swap curve

P8809

Establishment of a risk management programme, derivative documentation and collateral agreements enables access to synthetic exposures

If desired, physical investments in passive equities and credit may be efficiently replaced with derivative exposures to market indices, with the cash released enabling greater flexibility across the portfolio

Synthetic exposures to replace passive physical portfolios

Receive equity markettotal return

Pay Libor +/- rate

BankPension plan

P8809

• Options, when used with care, can enable efficient strategy implementation

• Use of options for downside risk management of return portfolios is a tried and tested approach

• In addition, options may be used in liability risk management context. For example,

– if a decision is made to hedge liabilities when rates increase, sell an option to enter into the liability hedge at a pre-agreed (higher) interest rate

– the reverse can also be implemented (reduce the size of a liability hedge if rates decline below a certain level) but, in practice, this is rare

Illustrative option strategies

P8809

• All strategies described in this presentation are illustrative and for discussion purposes only

• All risk management solutions should be coherent with your funding plan and strategic objectives

• There is lots of relevant detail: legal documents, collateral, counterparty risks being examples of some

• Effective engagement with your investment, actuarial and legal advisers is key to the design of your risk management solution

Concluding remarks

Important disclosures

This is a marketing document intended for professional clients only and should not be made available to or relied upon by retail clients. Unless otherwise stated, the source of information is Insight Investment. Any forecasts or opinions are Insight Investment’s own at the date of this document (or as otherwise specified) and may change. Material in this publication is for general information only and is not advice, proper advice (in accordance with the UK Pensions Act 1995), investment advice or recommendation of any purchase or sale of any security. It should not be regarded as a guarantee of future performance. The value of investments and any income from them will fluctuate and is not guaranteed (this may partly be due to exchange rate changes) and investors may not get back the amount invested. Past performance is not a guide to future performance. This document must not be used for the purpose of an offer or solicitation in any jurisdiction or in any circumstances in which such offer or solicitation is unlawful or otherwise not permitted. This document should not be amended or forwarded to a third party without consent from Insight Investment.

Telephone calls may be recorded.

For clients and prospects of Insight Investment Management (Global) Limited:Issued by Insight Investment Management (Global) Limited. Registered in England and Wales. Registered office 160 Queen Victoria Street, London EC4V 4LA; registered number 00827982.

For clients and prospects of Insight Investment Funds Management Limited:Issued by Insight Investment Funds Management Limited. Registered in England and Wales. Registered office 160 Queen Victoria Street, London EC4V 4LA; registered number 01835691.

For clients and prospects of Pareto Investment Management Limited:Issued by Pareto Investment Management Limited. Registered in England and Wales. Registered office 160 Queen Victoria Street, London EC4V 4LA; registered number 03169281.

Insight Investment Management (Global) Limited, Insight Investment Funds Management Limited and Pareto Investment Management Limited are authorised and regulated by the Financial Conduct Authority in the UK. Insight Investment Management (Global) Limited and Pareto Investment Management Limited are authorised to operate across Europe in accordance with the provisions of the European passport under Directive 2004/39 on markets in financial instruments.

For clients and prospects based in Singapore:This material is for Institutional Investors only. This documentation has not been registered as a prospectus with the Monetary Authority of Singapore. Accordingly, it and any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of Shares may not be circulated or distributed, nor may Shares be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons in Singapore other than (i) to an institutional investor pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “SFA”) or (ii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA.

For clients and prospects based in Australia: This material is for wholesale clients only and is not intended for distribution to, nor should it be relied upon by, retail clients.Insight Investment Management (Global) Limited is exempt from the requirement to hold an Australian financial services license under the Australian Securities and Investments Commission Corporations Act 2001 in respect of the financial services it provides. Insight Investment Management (Global) Limited is authorised and regulated by the Financial Conduct Authority under UK laws, which differ from Australian laws.

© 2016 Insight Investment. All rights reserved.